UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended January 29, 2011

Commission File No.0-25464

DOLLAR TREE, INC.

(Exact name of registrant as specified in its charter)

| Virginia | 26-2018846 |

| (State or other jurisdiction of | (I.R.S. Employer |

| incorporation or organization) | Identification No.) |

500 Volvo Parkway, Chesapeake, VA 23320

(Address of principal executive offices)

Registrant’s telephone number, including area code: (757) 321-5000

| Securities Registered Pursuant to Section 12(b) of the Act: |

| Title of Each Class | Name of Each Exchange on Which Registered |

| None | None |

Securities Registered Pursuant to Section 12(g) of the Act:

Common Stock (par value $.01 per share)

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act.

Indicate by check mark whether Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ( )

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer (X) | Accelerated filer ( ) |

| Non-accelerated filer ( ) | Smaller reporting company ( ) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

The aggregate market value of Common Stock held by non-affiliates of the Registrant on July 30, 2010, was $5,369,024,223, based on a $43.57 average of the high and low sales prices for the Common Stock on such date. For purposes of this computation, all executive officers and directors have been deemed to be affiliates. Such determination should not be deemed to be an admission that such executive officers and directors are, in fact, affiliates of the Registrant.

On March 9, 2011, there were 122,041,216 shares of the Registrant’s Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The information regarding securities authorized for issuance under equity compensation plans called for in Item 5 of Part II and the information called for in Items 10, 11, 12, 13 and 14 of Part III are incorporated by reference to the definitive Proxy Statement for the Annual Meeting of Stockholders of the Company to be held June 16, 2011, which will be filed with the Securities and Exchange Commission not later than May 27, 2011.

DOLLAR TREE, INC.

TABLE OF CONTENTS

| | | Page |

| | PART I | |

| | | |

| Item 1. | BUSINESS | 6 |

| | | |

| Item 1A. | RISK FACTORS | 10 |

| | | |

| Item 1B. | UNRESOLVED STAFF COMMENTS | 13 |

| | | |

| Item 2. | PROPERTIES | 13 |

| | | |

| Item 3. | LEGAL PROCEEDINGS | 14 |

| | | |

| Item 4. | RESERVED | 15 |

| | | |

| | PART II | |

| | | |

| Item 5. | MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED | |

| | STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | 15 |

| | | |

| Item 6. | SELECTED FINANCIAL DATA | 17 |

| | | |

| Item 7. | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL | |

| | CONDITION AND RESULTS OF OPERATIONS | 19 |

| | | |

| Item 7A. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 28 |

| | | |

| Item 8. | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | 29 |

| | | |

| Item 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON | |

| | ACCOUNTING AND FINANCIAL DISCLOSURE | 52 |

| | | |

| Item 9A. | CONTROLS AND PROCEDURES | 52 |

| | | |

| Item 9B. | OTHER INFORMATION | 53 |

| | | |

| | PART III | |

| | | |

| Item 10. | DIRECTORS, EXECUTIVE OFFICERS, AND CORPORATE GOVERNANCE | 53 |

| | | |

| Item 11. | EXECUTIVE COMPENSATION | 53 |

| | | |

| Item 12. | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS | |

| | AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | 54 |

| | | |

| Item 13. | CERTAIN RELATIONSHIPS, RELATED TRANSACTIONS AND DIRECTOR INDEPENDENCE | 54 |

| | | |

| Item 14. | PRINCIPAL ACCOUNTING FEES AND SERVICES | 54 |

| | | |

| | PART IV | |

| | | |

| Item 15. | EXHIBITS, FINANCIAL STATEMENT SCHEDULES, AND REPORTS ON FORM 8-K | 54 |

| | | |

| | SIGNATURES | 59 |

A WARNING ABOUT FORWARD-LOOKING STATEMENTS: This document contains "forward-looking statements" as that term is used in the Private Securities Litigation Reform Act of 1995. Forward-looking statements address future events, developments and results. They include statements preceded by, followed by or including words such as "believe," "anticipate," "expect," "intend," "plan," "view," “target” or "estimate." For example, our forward-looking statements include statements regarding:

· | our anticipated sales, including comparable store net sales, net sales growth and earnings growth; |

· | costs of pending and possible future legal claims; |

· | our growth plans, including our plans to add, expand or relocate stores, our anticipated square footage increase, and our ability to renew leases at existing store locations; |

· | the average size of our stores to be added in 2011 and beyond; |

· | the effect of a slight shift in merchandise mix to consumables and the increase in the number of our stores with freezers and coolers on gross profit margin and sales; |

· | the net sales per square foot, net sales and operating income of our stores and store-level cash payback metrics; |

· | the possible effect of the current economic downturn, inflation and other economic changes on our costs and profitability, including the possible effect of future changes in minimum wage rates, shipping rates, domestic and import freight costs, fuel costs and wage and benefit costs; |

· | our gross profit margin, earnings, inventory levels and ability to leverage selling, general and administrative and other fixed costs; |

· | our seasonal sales patterns including those relating to the length of the holiday selling seasons and the effect of a later Easter in 2011; |

· | the effect that expanding tender types accepted by our stores will have on sales; |

· | the capabilities of our inventory supply chain technology and other new systems; |

· | the future reliability of, and cost associated with, our sources of supply, particularly imported goods such as those sourced from China; |

· | the capacity, performance and cost of our distribution centers; |

· | our cash needs, including our ability to fund our future capital expenditures and working capital requirements; |

· | our expectations regarding competition and growth in our retail sector; and |

· | management's estimates associated with our critical accounting policies, including inventory valuation, accrued expenses, and income taxes. |

For a discussion of the risks, uncertainties and assumptions that could affect our future events, developments or results, you should carefully review the risk factors described in Item 1A “Risk Factors” beginning on page 10, as well as Item 7 "Management’s Discussion and Analysis of Financial Condition and Results of Operations" beginning on page 19 of this Form 10-K.

Our forward-looking statements could be wrong in light of these risks, uncertainties and assumptions. The future events, developments or results described in this report could turn out to be materially different. We have no obligation to publicly update or revise our forward-looking statements after the date of this annual report and you should not expect us to do so.

Investors should also be aware that while we do, from time to time, communicate with securities analysts and others, we do not, by policy, selectively disclose to them any material, nonpublic information or other confidential commercial information. Accordingly, shareholders should not assume that we agree with any statement or report issued by any securities analyst regardless of the content of the statement or report. We do not issue detailed financial forecasts or projections and we do not, by policy, confirm those issued by others. Thus, to the extent that reports issued by securities analysts contain any projections, forecasts or opinions, such reports are not our responsibility.

INTRODUCTORY NOTE: Unless otherwise stated, references to "we," "our" and "Dollar Tree" generally refer to Dollar Tree, Inc. and its direct and indirect subsidiaries on a consolidated basis. Unless specifically indicated otherwise, any references to “2011” or “fiscal 2011”, “2010” or “fiscal 2010”, “2009” or “fiscal 2009”, and “2008” or “fiscal 2008”, relate to as of or for the years ended January 28, 2012, January 29, 2011, January 30, 2010 and January 31, 2009, respectively.

AVAILABLE INFORMATION

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act are available free of charge on our website at www.dollartree.com as soon as reasonably practicable after electronic filing of such reports with the SEC.

PART I

Item 1. BUSINESS

Overview

We are the leading operator of discount variety stores offering merchandise at the fixed price of $1.00. We believe the variety and quality of products we sell for $1.00 sets us apart from our competitors. At January 29, 2011, we operated 4,101 discount variety retail stores. Our stores operate under the names of Dollar Tree, Deal$, Dollar Tree Deal$, Dollar Giant and Dollar Bills. Approximately 3,935 of these stores sell substantially all items for $1.00 or less in the United States and $1.25 or less in Canada. Substantially all of the remaining stores, operating as Deal$, sell items for $1.00 or less but also sell items for more than $1.

We believe our optimal store is between 8,000 and 10,000 selling square feet. This store size provides the appropriate amount of space for our broad merchandise offerings while allowing us to provide great service to our customers. As we have been expanding our merchandise offerings, we have added freezers and coolers to approximately 1,840 stores to increase sales and shopping frequency. At February 3, 2007, we operated 3,219 stores in 48 states. At January 29, 2011, we operated 4,015 stores in 48 states and the District of Columbia, as well as 86 stores in Canada. Our selling square footage increased from approximately 26.3 million square feet in February 2007 to 35.1 million square feet in January 2011. Our store growth has resulted primarily from opening new stores with additional growth from mergers and acquisitions, such as Deal$ and Dollar Giant.

Business Strategy

Value Merchandise Offering. We strive to exceed our customers' expectations of the variety and quality of products that they can purchase for $1.00 by offering items that we believe typically sell for higher prices elsewhere. We buy approximately 55% to 60% of our merchandise domestically and import the remaining 40% to 45%. Our domestic purchases include closeouts and promotional merchandise. We believe our mix of imported and domestic merchandise affords our buyers flexibility that allows them to consistently exceed the customer's expectations. In addition, direct relationships with manufacturers permit us to select from a broad range of products and customize packaging, product sizes and package quantities that meet our customers' needs.

Mix of Basic Variety and Seasonal Merchandise. We maintain a balanced selection of products within traditional variety store categories. We offer a wide selection of everyday basic products and we supplement these basic, everyday items with seasonal, closeout and promotional merchandise. We attempt to keep certain basic consumable merchandise in our stores continuously to establish our stores as a destination and we have slightly increased the mix of consumable merchandise in order to increase the traffic in our stores. Closeout and promotional merchandise is purchased opportunistically and represents less than 10% of our purchases.

Our merchandise mix consists of:

| | |

· | consumable merchandise, which includes candy and food, health and beauty care, and household consumables such as paper, plastics and household chemicals and in select stores, frozen and refrigerated food; |

| | |

· | variety merchandise, which includes toys, durable housewares, gifts, party goods, greeting cards, softlines, and other items; and |

| | |

· | seasonal goods, which include Easter, Halloween and Christmas merchandise. |

We have added freezers and coolers to certain stores and increased the amount of consumable merchandise carried by those stores. We believe this initiative helps drive additional transactions and allows us to appeal to a broader demographic mix. We have added freezers and coolers to approximately 420 additional stores in 2010. Therefore, as of January 29, 2011, we have freezers and coolers in approximately 1,840 of our stores. We plan to add them to approximately 225 more stores in 2011. As a result of the installation of freezers and coolers in select stores, consumable merchandise has grown as a percentage of purchases and sales and we expect this trend to continue. The following table shows the percentage of sales of each major product group for the years ended January 29, 2011 and January 30, 2010:

| | | January 29, | | | January 30, | |

| Merchandise Type | | 2011 | | | 2010 | |

| | | | | | | |

| Consumable | | | 49.5 | % | | | 48.0 | % |

| Variety categories | | | 45.8 | % | | | 46.8 | % |

| Seasonal | | | 4.7 | % | | | 5.2 | % |

At any point in time, we carry approximately 6,100 items in our stores and as of the end of 2010 approximately 2,700 of our basic, everyday items are automatically replenished. The remaining items are primarily ordered by our store managers on a weekly basis. Through automatic replenishment and our store managers’ ability to order product, each store manager is able to satisfy the demands of their particular customer base.

Customer Payment Methods. All of our stores accept cash, checks, debit cards, VISA credit cards, Discover and American Express and approximately 950 stores accept MasterCard credit cards. Along with the shift to more consumables and the rollout of freezers and coolers, we have increased the number of stores accepting Electronic Benefits Transfer(EBT) cards and food stamps (under the Supplemental Nutrition Assistance Program (“SNAP”)) to approximately 3,500 stores as of January 29, 2011.

Convenient Locations and Store Size. We primarily focus on opening new stores in strip shopping centers anchored by mass merchandisers or grocers, whose target customers we believe to be similar to ours. Our stores have proven successful in metropolitan areas, mid-sized cities and small towns. The range of our store sizes allows us to target a particular location with a store that best suits that market and takes advantage of available real estate opportunities. Our stores are attractively designed and create an inviting atmosphere for shoppers by using bright lighting, vibrant colors and decorative signs. We enhance the store design with attractive merchandise displays. We believe this design attracts new and repeat customers and enhances our image as both a destination and impulse purchase store.

For more information on retail locations and retail store leases, see Item 2 "Properties” beginning on page 13 of this Form 10-K.

Profitable Stores with Strong Cash Flow. We maintain a disciplined, cost-sensitive approach to store site selection in order to minimize the initial capital investment required and maximize our potential to generate high operating margins and strong cash flows. We believe that our stores have a relatively small shopping radius, which allows us to profitably concentrate multiple stores within a single market. Our ability to open new stores is dependent upon, among other factors, locating suitable sites and negotiating favorable lease terms.

The strong cash flows generated by our stores allow us to self-fund infrastructure investment and new stores. Over the past five years, cash flows from operating activities have exceeded capital expenditures.

For more information on our results of operations, see Item 7 "Management's Discussion and Analysis of Financial Condition and Results of Operations” beginning on page 19 of this Form 10-K.

Cost Control. We believe that our substantial buying power at the $1.00 price point and our flexibility in making sourcing decisions contributes to our successful purchasing strategy, which includes disciplined, targeted merchandise margin goals by category. We also believe our ability to select quality merchandise helps to minimize markdowns. We buy products on an order-by-order basis and have no material long-term purchase contracts or other assurances of continued product supply or guaranteed product cost. No vendor accounted for more than 10% of total merchandise purchased in any of the past five years.

Our supply chain systems continue to provide us with valuable sales information to assist our buyers and improve merchandise allocation to our stores. Controlling our inventory levels has resulted in more efficient distribution and store operations.

Information Systems. We believe that investments in technology help us to increase sales and control costs. Our inventory management system has allowed us to improve the efficiency of our supply chain, improve merchandise flow, increase inventory turnover and control distribution and store operating costs. Our automatic replenishment system automatically reorders key items, based on actual store level sales and inventory. At the end of 2010, we had approximately 2,700 basic, everyday items on automatic replenishment.

Point-of-sale data allows us to track sales and inventory by merchandise category at the store level and assists us in planning for future purchases of inventory. We believe that this information allows us to ship the appropriate product to stores at the quantities commensurate with selling patterns. Using this point-of-sale data to plan purchases of inventory has helped us increase our inventory turns in each of the last five years. Our inventory turns increased to approximately 4.2 in 2010.

Corporate Culture and Values. We believe that honesty and integrity, doing the right things for the right reasons, and treating people fairly and with respect are core values within our corporate culture. We believe that running a business, and certainly a public company, carries with it a responsibility to be above reproach when making operational and financial decisions. Our executive management team visits and shops our stores like every customer, and ideas and individual creativity on the part of our associates are encouraged, particularly from our store managers who know their stores and their customers. We have standards for store displays, merchandise presentation, and store operations. We maintain an open door policy for all associates. Our distribution centers are operated based on objective measures of performance and virtually everyone in our store support center is available to assist associates in the stores and distribution centers.

Our disclosure committee meets at least quarterly and monitors our internal controls over financial reporting to ensure that our public filings contain discussions about the risks our business faces. We believe that we have the controls in place to be able to certify our financial statements. Additionally, we have complied with the listing requirements for the Nasdaq Stock Market.

Growth Strategy

Store Openings and Square Footage Growth. The primary factors contributing to our net sales growth have been new store openings, an active store expansion and remodel program, and selective mergers and acquisitions. In the last five years, net sales increased at a compound annual growth rate of 10.3%. We expect that the majority of our future sales growth will come primarily from new store openings and from our store expansion and relocation program.

The following table shows the average selling square footage of our stores and the selling square footage per new store opened over the last five years. Our growth and productivity statistics are reported based on selling square footage because our management believes the use of selling square footage yields a more accurate measure of store productivity.

| Year | Number of Stores | Average Selling Square Footage Per Store | Average Selling Square Footage Per New Store Opened |

| 2006 | 3,219 | 8,160 | 8,780 |

| 2007 | 3,411 | 8,330 | 8,480 |

| 2008 | 3,591 | 8,440 | 8,100 |

| 2009 | 3,806 | 8,480 | 7,950 |

| 2010 | 4,101 | 8,570 | 8,400 |

We expect to increase our selling square footage in the future by opening new stores in underserved markets and strategically increasing our presence in our existing markets via new store openings and store expansions (expansions include store relocations). In fiscal 2011 and beyond, we plan to predominantly open stores that are approximately 8,000 - 10,000 selling square feet and we believe this size allows us to achieve our objectives in the markets in which we plan to expand. At January 29, 2011, 2,160 of our stores, totaling 64.8% of our selling square footage, were 8,000 selling square feet or larger.

In addition to new store openings, we plan to continue our store expansion program to increase our net sales per store and take advantage of market opportunities. We target stores for expansion based on the current sales per selling square foot and changes in market opportunities. Stores targeted for expansion are generally less than 6,000 selling square feet in size. Store expansions generally increase the existing store size by approximately 3,900 selling square feet.

Since 1995, we have added a total of 695 stores through several mergers and acquisitions. Our acquisition strategy has been to target companies that have a similar single-price point concept that have shown success in operations or companies that provide a strategic advantage. We evaluate potential acquisition opportunities in our retail sector as they become available.

In November 2010, we completed our acquisition of 86 Dollar Giant stores based in Vancouver, British Columbia. These stores offer a wide assortment of quality general merchandise, contemporary seasonal goods and everyday consumables, all priced at $1.25 (CAD) or less. The stores operate in the Canadian provinces of British Columbia, Ontario, Alberta and Saskatchewan. This is the first expansion of our retail operations outside of the United States and provides us with a proven management team and distribution network as well as additional potential store growth in a new market.

In 2006, we completed our acquisition of 138 Deal$ stores, which included stores that offered an expanded assortment of merchandise including items that sell for more than $1. These stores provide us an opportunity to leverage our Dollar Tree infrastructure in the testing of new merchandise concepts, including higher price points, without disrupting the single-price point model in our Dollar Tree stores. Since the acquisition, we have opened new Deal$ stores, including some in new markets, and operate 164 Deal$ stores as of January 29, 2011.

From time to time, we also acquire the rights to store leases through bankruptcy proceedings of certain retailers. We will take advantage of these opportunities as they arise in the future and fit within our selling square footage size parameters.

Merchandising and Distribution. Expanding our customer base is important to our growth plans. We plan to continue to stock our new stores with the ever-changing merchandise that our current customers have come to appreciate. Consumable merchandise typically leads to more frequent return trips to our stores resulting in increased sales. The presentation and display of merchandise in our stores are critical to communicating value to our customers and creating a more exciting shopping experience. We believe our approach to visual merchandising results in higher store traffic, higher sales volume and an environment that encourages impulse purchases.

A strong and efficient distribution network is critical to our ability to grow and to maintain a low-cost operating structure. In 2009, we purchased a new distribution center in San Bernardino, California which began shipping merchandise in April 2010. This distribution center replaced the Salt Lake City distribution center which closed when its lease expired in April 2010. We believe our distribution center network is currently capable of supporting approximately $7.5 billion in annual sales in the United States. New distribution sites, like this one in San Bernardino, California, are strategically located to reduce stem miles, maintain flexibility and improve efficiency in our store service areas. We also are a party to an agreement which provides distribution services in two facilities in Canada.

Our stores receive approximately 90% of their inventory from our distribution centers via contract carriers. The remaining store inventory, primarily perishable consumable items and other vendor-maintained display items, are delivered directly to our stores from vendors. For more information on our distribution center network, see Item 2 “Properties” beginning on page 13 of this Form 10-K.

Competition

The retail industry is highly competitive and we expect competition to increase in the future. The principal methods of competition include closeout merchandise, convenience and the quality of merchandise offered to the customer. We operate in the discount retail merchandise business, which is currently and is expected to continue to be highly competitive with respect to price, store location, merchandise quality, assortment and presentation, and customer service. Our competitors include single-price dollar stores, multi-price dollar stores, mass merchandisers, discount retailers and variety retailers. In addition, several mass merchandisers and grocery store chains carry "dollar store" or “dollar zone” concepts in their stores, which increase competition. We believe we differentiate ourselves from other retailers by providing high value, high quality, low cost merchandise in attractively designed stores that are conveniently located. Our sales and profits could be reduced by increases in competition, especially because there are no significant economic barriers for others to enter our retail sector.

Trademarks

We are the owners of several federal service mark registrations including "Dollar Tree," the "Dollar Tree" logo, the Dollar Tree logo with a “1”, and "One Price...One Dollar." In addition, we own a concurrent use registration for "Dollar Bill$" and the related logo. We also acquired the rights to use trade names previously owned by Everything's A Dollar, a former competitor in the $1.00 price point industry. Several trade names were included in the purchase, including the marks "Everything's $1.00 We Mean Everything!," and "Everything's $1.00." With the acquisition of Deal$, we became the owners of the trademark “Deal$”. With the acquisition of Dollar Giant, we became the owners of the trademark “Dollar Giant” and others in Canada. We have federal trademark registrations for a variety of private labels that we use to market some of our product lines.

Employees

We employed approximately 13,060 full-time and 50,800 part-time associates on January 29, 2011. Part-time associates work an average of less than 35 hours per week. The number of part-time associates fluctuates depending on seasonal needs. We consider our relationship with our associates to be good, and we have not experienced significant interruptions of operations due to labor disagreements.

Item 1A. RISK FACTORS

An investment in our common stock involves a high degree of risk. Any failure to meet market expectations, including our comparable store sales growth rate, earnings and earnings per share or new store openings, could cause the market price of our stock to decline. You should carefully consider the specific risk factors listed below together with all other information included or incorporated in this report. Any of the following risks may materialize, and additional risks not known to us, or that we now deem immaterial, may arise. In such event, our business, financial condition, results of operations or prospects could be materially adversely affected.

Our profitability is vulnerable to cost increases.

Future increase in costs such as the cost of merchandise, wage levels, shipping rates, freight costs, fuel costs and store occupancy costs may reduce our profitability. We will not raise the sales price of our merchandise to offset cost increases because we are committed to selling at the $1.00 price point to continue to provide value to the customer. We are dependent on our ability to adjust our product assortment, to operate more efficiently or effectively or to increase our comparable store net sales in order to offset inflation. We can give no assurance that we will be able to operate more efficiently or increase our comparable store net sales in the future. Please see Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations," beginning on page 19 of this Form 10-K for further discussion of the effect of Inflation and Other Economic Factors on our operations.

Litigation may adversely affect our business, financial condition and results of

operations.

Our business is subject to the risk of litigation by employees, consumers, suppliers, competitors, shareholders, government agencies, or others through private actions, class actions, administrative proceedings, regulatory actions or other litigation. We are currently defendants in several employment-related class action cases and changes in Federal law could cause these types of claims to rise even more. The outcome of litigation, particularly class action lawsuits, regulatory actions and intellectual property claims, is difficult to assess or quantify. Plaintiffs in these types of lawsuits may seek recovery of very large or indeterminate amounts, and the magnitude of the potential loss relating to these lawsuits may remain unknown for substantial periods of time. In addition, certain of these lawsuits, if decided adversely to us or settled by us, may result in liability material to our financial statements as a whole or may negatively affect our operating results if changes to our business operation are required. The cost to defend current and future litigation may be significant. There also may be adverse publicity associated with litigation, including litigation related to product safety and customer information, which could negatively affect customer perception of our business, regardless of whether the allegations are valid or whether we are ultimately found liable.

For a discussion of current legal matters, please see Item 3. “Legal Proceedings” beginning on page 14 of this Form 10-K. Resolution of certain matters described in that item, if decided against the Company, could have a material adverse effect on our results of operations, accrued liabilities or cash flows.

Changes in federal, state or local law, or our failure to comply with such laws, could increase our expenses and expose us to legal risks

Our business is subject to a wide array of laws and regulations. Significant legislative changes, such as the healthcare legislation, that impact our relationship with our workforce could increase our expenses and adversely affect our operations. Changes in other regulatory areas, such as consumer credit, privacy and information security, product safety or environmental protection, among others, could cause our expenses to increase. In addition, if we fail to comply with applicable laws and regulations, particularly wage and hour laws, we could be subject to legal risk, including government enforcement action and class action civil litigation, which could adversely affect our results of operations. Changes in tax laws, the interpretation of existing laws, or our failure to sustain our reporting positions on examination could adversely affect our effective tax rate.

We could encounter disruptions or additional costs in obtaining and distributing merchandise.

Our success depends on the ability of our vendors to supply merchandise and our ability to transport merchandise to our distribution centers and then ship it to our stores in a timely and cost-effective manner. We may not anticipate, respond to or control all of the challenges of operating our receiving and distribution systems. Additionally, if a vendor fails to deliver on its commitments, we could experience merchandise shortages that could lead to lost sales. Some of the factors that could have an adverse effect on our supply chain systems or costs are:

§ Economic conditions. Suppliers may encounter financial or other difficulties. |

§ Shipping. Our oceanic shipping schedules may be disrupted or delayed from time to time. We have experienced volatility in shipping rates over the past few years and the outlook for shipping rates in 2011 is uncertain. |

§ Diesel fuel costs. We have experienced significant volatility in diesel fuel costs over the past few years. Diesel prices have increased in the first part of 2011 and the outlook for 2011 remains uncertain. |

§ Vulnerability to natural or man-made disasters. A fire, explosion or natural disaster at ports or any of our distribution facilities could result in a loss of merchandise and impair our ability to adequately stock our stores. Some facilities are especially vulnerable to earthquakes, hurricanes or tornadoes. |

§ Labor disagreement. Labor disagreements or disruptions may result in delays in the delivery of merchandise to our stores and increase costs. |

§ War, terrorism and other events. War and acts of terrorism in the United States, or in China or other parts of Asia, where we buy a significant amount of our imported merchandise, could disrupt our supply chain. |

We may be unable to expand our square footage as profitably as planned.

We plan to expand our selling square footage by approximately 6.9% in 2011 to increase our sales and profits. Expanding our square footage profitably depends on a number of uncertainties, including our ability to locate, lease, build out and open or expand stores in suitable locations on a timely basis under favorable economic terms. In addition, our expansion is dependent upon third-party developers’ abilities to acquire land, obtain financing, and secure necessary permits and approvals. Turmoil in the financial markets has made it difficult for third party developers to obtain financing for new projects. We must also open or expand stores within our established geographic markets, where new or expanded stores may draw sales away from our existing stores. We may not manage our expansion effectively, and our failure to achieve our expansion plans could materially and adversely affect our business, financial condition and results of operations.

Sales below our expectations during peak seasons may cause our operating results to suffer materially.

Our highest sales periods are the Christmas and Easter seasons. We generally realize a disproportionate amount of our net sales and our operating and net income during the fourth quarter. In anticipation, we stock extra inventory and hire many temporary employees to prepare our stores. A reduction in sales during these periods could adversely affect our operating results, particularly operating and net income, to a greater extent than if a reduction occurred at other times of the year. Untimely merchandise delays due to receiving or distribution problems could have a similar effect. Sales during the Easter selling season are materially affected by the timing of the Easter holiday. Easter in fiscal 2011 is on April 24th, while in fiscal 2010 it was on April 4th.

Our sales and profits rely on imported merchandise, which may increase in cost or become unavailable.

Merchandise imported directly accounts for approximately 40% to 45% of our total retail value purchases. In addition, we believe that a portion of our goods purchased from domestic vendors is imported. China is the source of a substantial majority of our imports. Imported goods are generally less expensive than domestic goods and increase our profit margins. A disruption in the flow of our imported merchandise or an increase in the cost of those goods may significantly decrease our profits. Risks associated with our reliance on imported goods include:

§ disruptions in the flow of imported goods because of factors such as: |

o raw material shortages, work stoppages, strikes and political unrest; |

o problems with oceanic shipping, including shipping container shortages; and |

o economic crises and international disputes. |

| |

§ increases in the cost of purchasing or shipping imported merchandise, resulting from: |

o increases in shipping rates imposed by the trans-Pacific ocean carriers; |

o import duties, import quotas and other trade sanctions; |

o changes in currency exchange rates or policies and local economic conditions, including inflation in the country of origin; and |

o failure of the United States to maintain normal trade relations with China. |

A downturn in economic conditions could impact our sales.

Deterioration in economic conditions, such as those caused by a recession, inflation, higher unemployment, consumer debt levels, lack of available credit, cost increases, as well as adverse weather conditions or terrorism, could reduce consumer spending or cause customers to shift their spending to products we either do not sell or do not sell as profitably. Adverse economic conditions could disrupt consumer spending and significantly reduce our sales, decrease our inventory turnover, cause greater markdowns or reduce our profitability due to lower margins.

Our profitability is affected by the mix of products we sell.

Our gross profit margin could decrease if we increase the proportion of higher cost goods we sell in the future. In recent years, the percentage of our sales from higher cost consumable products has increased and is likely to increase slightly in 2011. As a result, our gross profit could decrease unless we are able to maintain our current merchandise cost sufficiently to offset any decrease in our product margin percentage. We can give no assurance that we will be able to do so.

Pressure from competitors may reduce our sales and profits.

The retail industry is highly competitive. The marketplace is highly fragmented as many different retailers compete for market share by utilizing a variety of store formats and merchandising strategies. We expect competition to increase in the future because there are no significant economic barriers for others to enter our retail sector. Many of our current or potential competitors have greater financial resources than we do. We cannot guarantee that we will continue to be able to compete successfully against existing or future competitors. Please see Item 1, “Business,” beginning on page 6 of this Form 10-K for further discussion of the effect of competition on our operations.

Certain provisions in our Articles of Incorporation and Bylaws could delay or discourage a takeover attempt that may be in a shareholder's best interest.

Our Articles of Incorporation and Bylaws currently contain provisions that may delay or discourage a takeover attempt that a shareholder might consider in his best interest. These provisions, among other things:

· provide that only the Board of Directors, chairman or president may call special meetings of the shareholders; |

· establish certain advance notice procedures for nominations of candidates for election as directors and for shareholder proposals to be considered at shareholders' meetings; |

· permit the Board of Directors, without further action of the shareholders, to issue and fix the terms of preferred stock, which may have rights senior to those of the common stock. |

However, we believe that these provisions allow our Board of Directors to negotiate a higher price in the event of a takeover attempt which would be in the best interest of our shareholders.

In 2010, the shareholders approved an amendment to our Articles of Incorporation which will result in the declassification of our Board of Directors by 2012.

Item 1B. UNRESOLVED STAFF COMMENTS

None.

Item 2. PROPERTIES

Stores

As of January 29, 2011, we operated 4,101 stores in 48 states and the District of Columbia, as well as the Canadian provinces of British Columbia, Ontario, Alberta and Saskatchewan as detailed below:

| Alabama | 88 | | Maine | 21 | | Oklahoma | 52 |

| Arizona | 76 | | Maryland | 91 | | Oregon | 77 |

| Arkansas | 45 | | Massachusetts | 73 | | Pennsylvania | 216 |

| California | 323 | | Michigan | 150 | | Rhode Island | 17 |

| Colorado | 66 | | Minnesota | 68 | | South Carolina | 80 |

| Connecticut | 43 | | Mississippi | 53 | | South Dakota | 9 |

| Delaware | 23 | | Missouri | 85 | | Tennessee | 101 |

| District of Columbia | 1 | | Montana | 9 | | Texas | 250 |

| Florida | 276 | | Nebraska | 16 | | Utah | 39 |

| Georgia | 146 | | Nevada | 32 | | Vermont | 5 |

| Idaho | 23 | | New Hampshire | 26 | | Virginia | 140 |

| Illinois | 168 | | New Jersey | 89 | | Washington | 79 |

| Indiana | 98 | | New Mexico | 30 | | West Virginia | 33 |

| Iowa | 33 | | New York | 178 | | Wisconsin | 76 |

| Kansas | 30 | | North Carolina | 162 | | Wyoming | 11 |

| Kentucky | 70 | | North Dakota | 6 | | | |

| Louisiana | 65 | | Ohio | 167 | | | |

| | | | | | | | |

| Alberta | 16 | | Ontario | 31 | | | |

| British Columbia | 36 | | Saskatchewan | 3 | | | |

We currently lease our stores and expect to lease the majority of our new stores as we expand. Our leases typically provide for a short initial lease term, generally five years, with options to extend, however in some cases we have initial lease terms of seven to ten years. We believe this leasing strategy enhances our flexibility to pursue various expansion opportunities resulting from changing market conditions. As current leases expire, we believe that we will be able to obtain lease renewals, if desired, for present store locations, or to obtain leases for equivalent or better locations in the same general area.

Distribution Centers

The following table includes information about the distribution centers that we own and operate in the United States. In 2009, we purchased a new distribution center in San Bernardino, California which began shipping merchandise in April 2010. This facility replaced the Salt Lake City distribution center which closed when its lease expired in April 2010. We believe our distribution center network is currently capable of supporting approximately $7.5 billion in annual sales in the United States.

Location | Size in Square Feet |

| | |

| Chesapeake, Virginia | 400,000 |

| Olive Branch, Mississippi | 425,000 |

| Joliet, Illinois | 1,200,000 |

| Stockton, California | 525,000 |

| Briar Creek, Pennsylvania | 1,003,000 |

| Savannah, Georgia | 603,000 |

| Marietta, Oklahoma | 603,000 |

| San Bernardino, California | 448,000 |

| Ridgefield, Washington | 665,000 |

Each of our distribution centers contains advanced materials handling technologies, including radio-frequency inventory tracking equipment and specialized information systems. With the exception of our Ridgefield facility, each of our distribution centers also contains automated conveyor and sorting systems.

We are also a party to a contract which provides distribution services in British Columbia and Ontario. In fiscal 2011, this contract terminated and we entered into a new agreement for similar services.

For more information on financing of our distribution centers, see Item 7 "Management's Discussion and Analysis of Financial Condition and Results of Operations- Funding Requirements" beginning on page 24 of this Form 10-K.

Item 3. LEGAL PROCEEDINGS

From time to time, we are defendants in ordinary, routine litigation or proceedings incidental to our business, including allegations regarding:

| | |

· | employment related matters; |

| | |

· | infringement of intellectual property rights; |

| | |

· | product safety matters, which may include product recalls in cooperation with the Consumer Products Safety Commission or other jurisdictions; |

| | |

· | personal injury/wrongful death claims; and |

| | |

· | real estate matters related to store leases. |

In 2006, a former store manager filed a collective action against us in Alabama federal court. She claims that she and other store managers should have been classified as non-exempt employees under the Fair Labor Standards Act and received overtime compensation. The Court preliminarily allowed nationwide (except California) notice to be sent to all store managers employed for the three years immediately preceding the filing of the suit. Approximately 265 individuals are included in the collective action. The Court on its own motion continued the case from its previously scheduled July 2010 trial date. Our motion to decertify the collective action has been dismissed without prejudice to refile at a later date. Additional discovery, pursuant to the Court’s direction, is presently ongoing. There is no scheduled trial date. We will continue to vigorously defend ourselves in this matter.

In 2007, two store managers filed a class action against us in California federal court, claiming they and other California store managers should have been classified as non-exempt employees under California and federal law. The Court has allowed notice to be sent to all California store managers employed since December 12, 2004, and a class of approximately 184 individuals remains. We filed a motion to decertify the class which was both granted and denied in part. The current class was redefined by the Court in its ruling which resulted in a significant reduction in the number of class members. The Court on its own continued a previously scheduled March 2011 trial date. A pretrial conference has been set for June 2011 at which time a new trial date will be established. It is anticipated the case will go to trial in calendar year 2011. We are vigorously defending ourselves in this matter.

In 2008, we were sued under the Equal Pay Act in Alabama federal court by two female store managers alleging that they and other female store managers were paid less than male store managers. Among other things, they seek monetary damages and back pay. The Court ordered that notice be sent to potential plaintiffs and there are now approximately 363 opt-in plaintiffs. We expect that the Court will rule upon our motion to decertify the collective action later in 2011. We are vigorously defending ourselves in this matter. In 2009, 34 plaintiffs, most of whom are opt-in plaintiffs in the Alabama action, filed a new class action in a federal court in Virginia, alleging gender pay and promotion discrimination under Title VII. On March 11, 2010, the case was dismissed with prejudice. Plaintiff then filed a motion requesting the Court to alter, amend and vacate its dismissal Order which the trial Court denied. Plaintiffs have filed an appeal to the U.S. Court of Appeals for the Fourth Circuit. It is anticipated the Court will hand down a decision in 2011.

In 2010, two former assistant store managers filed a collective action against us in a Florida federal court. Their amended claim is that they were required to work off the clock without compensation in violation of the Fair Labor Standards Act. An additional 22 party plaintiffs have joined the suit. Our motion to transfer venue to the U.S. District Court for the Eastern District of Virginia was recently overruled without prejudice pending future case developments. There is no trial date. We will continue to vigorously defend ourselves in this matter.

We do not believe that any of these matters will, individually or in the aggregate, have a material adverse effect on our business or financial condition. We cannot give assurance, however, that one or more of these lawsuits will not have a material adverse effect on our results of operations for the period in which they are resolved.

Item 4. REMOVED AND RESERVED

PART II

Item 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock has been traded on The Nasdaq Global Select Market® under the symbol "DLTR" since our initial public offering on March 6, 1995. The following table gives the high and low sales prices of our common stock as reported by Nasdaq for the periods indicated, restated to reflect a 3-for-2 stock split effected as a stock dividend in June 2010.

| | | High | | | Low | |

| Fiscal year ended January 30, 2010: | | | | | | |

| | | | | | | |

| First Quarter | | $ | 30.22 | | | $ | 21.96 | |

| Second Quarter | | | 31.52 | | | | 27.05 | |

| Third Quarter | | | 34.48 | | | | 29.33 | |

| Fourth Quarter | | | 34.80 | | | | 30.51 | |

| | | | | | | | | |

| Fiscal year ended January 29, 2011: | | | | | | | | |

| | | | | | | | | |

| First Quarter | | $ | 41.79 | | | $ | 31.33 | |

| Second Quarter | | | 45.12 | | | | 38.40 | |

| Third Quarter | | | 52.62 | | | | 40.60 | |

| Fourth Quarter | | | 57.99 | | | | 50.09 | |

On March 9, 2011, the last reported sale price for our common stock, as quoted by Nasdaq, was $51.96 per share. As of March 9, 2011, we had approximately 435 shareholders of record.

The following table presents our share repurchase activity for the 13 weeks ended January 29, 2011:

| | | | | | | | | | | | Approximate | |

| | | | | | | | | Total number | | | dollar value of | |

| | | | | | | | | of shares | | | shares that may | |

| | | | | | | | | purchased as | | | yet be purchased | |

| | | Total number | | | Average | | | part of publicly | | under the plans | |

| | | of shares | | | price paid | | | announced plans | | | or programs | |

| Period | | purchased | | | per share | | | or programs | | | (in millions) | |

| October 31, 2010 to November 27, 2010 | | | 456,038 | | | $ | 52.30 | | | | 456,038 | | | $ | 445.9 | |

| November 28, 2010 to January 1, 2011 | | | 370,852 | | | | 56.32 | | | | 370,852 | | | | 425.0 | |

| January 2, 2011 to January 29, 2011 | | | 1,504,650 | | | | 52.58 | | | | 1,504,650 | | | | 345.9 | |

| Total | | | 2,331,540 | | | $ | 53.12 | | | | 2,331,540 | | | $ | 345.9 | |

We repurchased approximately 9.3 million shares for approximately $414.7 million in fiscal 2010. At January 29, 2011, we have approximately $345.9 million remaining under Board authorization.

We anticipate that substantially all of our cash flow from operations in the foreseeable future will be retained for the development and expansion of our business, the repayment of indebtedness and, as authorized by our Board of Directors, the repurchase of stock. Management does not anticipate paying dividends on our common stock in the foreseeable future.

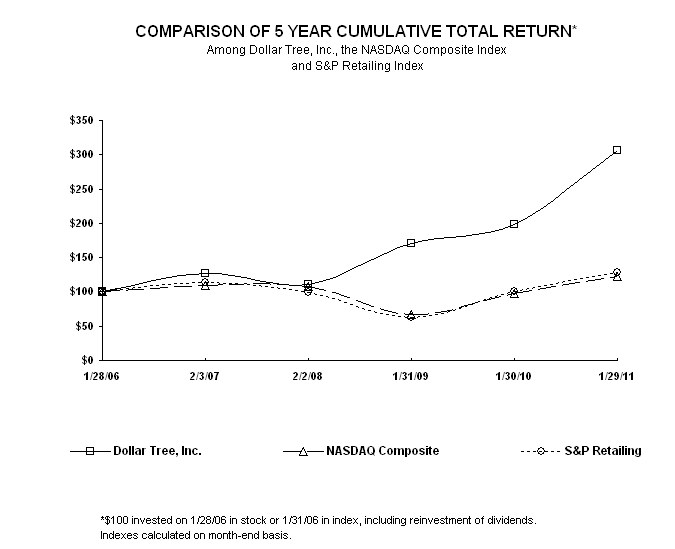

Stock Performance Graph

The following graph sets forth the yearly percentage change in the cumulative total shareholder return on our common stock during the five fiscal years ended January 29, 2011, compared with the cumulative total returns of the NASDAQ Composite Index and the S&P Retailing Index. The comparison assumes that $100 was invested in our common stock on January 28, 2006, and, in each of the foregoing indices on January 28, 2006, and that dividends were reinvested.

Item 6. SELECTED FINANCIAL DATA

The following table presents a summary of our selected financial data for the fiscal years ended January 29, 2011, January 30, 2010, January 31, 2009, February 2, 2008, and February 3, 2007. Fiscal 2006 included 53 weeks, commensurate with the retail calendar, while all other fiscal years reported in the table contain 52 weeks. The selected income statement and balance sheet data have been derived from our consolidated financial statements that have been audited by our independent registered public accounting firm. This information should be read in conjunction with the consolidated financial statements and related notes, "Management’s Discussion and Analysis of Financial Condition and Results of Operations" and our financial information found elsewhere in this report.

Comparable store net sales compare net sales for stores open throughout each of the two periods being compared, including expanded stores. Net sales per store and net sales per selling square foot are calculated for stores open throughout the period presented.

Amounts in the following tables are in millions, except per share data, number of stores data, net sales per selling square foot data and inventory turns.

| | | Years Ended | |

| | | January 29, | | | January 30, | | | January 31, | | | February 2, | | | February 3, | |

| | | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | |

| Income Statement Data: | | | | | | | | | | | | | | | |

| Net sales | | $ | 5,882.4 | | | $ | 5,231.2 | | | $ | 4,644.9 | | | $ | 4,242.6 | | | $ | 3,969.4 | |

| Gross profit | | | 2,087.6 | | | | 1,856.8 | | | | 1,592.2 | | | | 1,461.1 | | | | 1,357.2 | |

| Selling, general and administrative expenses | | | 1,457.6 | | | | 1,344.0 | | | | 1,226.4 | | | | 1,130.8 | | | | 1,046.4 | |

| Operating income | | | 630.0 | | | | 512.8 | | | | 365.8 | | | | 330.3 | | | | 310.8 | |

| Net income | | | 397.3 | | | | 320.5 | | | | 229.5 | | | | 201.3 | | | | 192.0 | |

| | | | | | | | | | | | | | | | | | | | | |

| Margin Data (as a percentage of net sales): | | | | | | | | | | | | | | | | | |

| Gross profit | | | 35.5 | % | | | 35.5 | % | | | 34.3 | % | | | 34.4 | % | | | 34.2 | % |

| Selling, general and administrative expenses | | | 24.8 | % | | | 25.7 | % | | | 26.4 | % | | | 26.6 | % | | | 26.4 | % |

| Operating income | | | 10.7 | % | | | 9.8 | % | | | 7.9 | % | | | 7.8 | % | | | 7.8 | % |

| Net income | | | 6.8 | % | | | 6.1 | % | | | 4.9 | % | | | 4.7 | % | | | 4.8 | % |

| | | | | | | | | | | | | | | | | | | | | |

| Per Share Data: | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| Diluted net income per share | | $ | 3.10 | | | $ | 2.37 | | | $ | 1.69 | | | $ | 1.39 | | | $ | 1.23 | |

| Diluted net income per share increase | | | 30.8 | % | | | 40.2 | % | | | 21.6 | % | | | 13.0 | % | | | 15.6 | % |

| | | As of | |

| | | January 29, | | | January 30, | | | January 31, | | | February 2, | | | February 3, | |

| | | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | |

| Balance Sheet Data: | | | | | | | | | | | | | | | |

| Cash and cash equivalents | | | | | | | | | | | | | | | |

| and short-term investments | | $ | 486.0 | | | $ | 599.4 | | | $ | 364.4 | | | $ | 81.1 | | | $ | 306.8 | |

| Working capital | | | 800.4 | | | | 829.7 | | | | 663.3 | | | | 382.9 | | | | 575.7 | |

| Total assets | | | 2,380.5 | | | | 2,289.7 | | | | 2,035.7 | | | | 1,787.7 | | | | 1,882.2 | |

| Total debt, including capital lease obligations | | | 267.8 | | | | 267.8 | | | | 268.2 | | | | 269.4 | | | | 269.5 | |

| Shareholders' equity | | | 1,459.0 | | | | 1,429.2 | | | | 1,253.2 | | | | 988.4 | | | | 1,167.7 | |

| | | Years Ended |

| | | January 29, | | | January 30, | | | January 31, | | | February 2, | | | February 3, | |

| | | | 2011 | | | | 2010 | | | | 2009 | | | | 2008 | | | | 2007 | |

| Selected Operating Data: | | | | | | | | | | | | | | | | | | | | |

| Number of stores open at end of period | | | 4,101 | | | | 3,806 | | | | 3,591 | | | | 3,411 | | | | 3,219 | |

| Gross square footage at end of period | | | 44.4 | | | | 41.1 | | | | 38.5 | | | | 36.1 | | | | 33.3 | |

| Selling square footage at end of period | | | 35.1 | | | | 32.3 | | | | 30.3 | | | | 28.4 | | | | 26.3 | |

| Selling square footage annual growth | | | 8.8 | % | | | 6.6 | % | | | 6.7 | % | | | 8.0 | % | | | 14.3 | % |

| Net sales annual growth | | | 12.4 | % | | | 12.6 | % | | | 9.5 | % | | | 6.9 | % | | | 16.9 | % |

| Comparable store net sales increase | | | 6.3 | % | | | 7.2 | % | | | 4.1 | % | | | 2.7 | % | | | 4.6 | % |

| Net sales per selling square foot | | $ | 174 | | | $ | 167 | | | $ | 158 | | | $ | 155 | | | $ | 161 | |

| Net sales per store | | $ | 1.5 | | | $ | 1.4 | | | $ | 1.3 | | | $ | 1.3 | | | $ | 1.3 | |

| Selected Financial Ratios: | | | | | | | | | | | | | | | | | | | | |

| Return on assets | | | 17.0 | % | | | 14.8 | % | | | 12.0 | % | | | 11.0 | % | | | 10.4 | % |

| Return on equity | | | 27.5 | % | | | 23.9 | % | | | 20.5 | % | | | 18.7 | % | | | 16.4 | % |

| Inventory turns | | | 4.2 | | | | 4.1 | | | | 3.8 | | | | 3.7 | | | | 3.5 | |

Item 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

In Management’s Discussion and Analysis, we explain the general financial condition and the results of operations for our company, including:

| | |

· | what factors affect our business; |

| | |

· | what our net sales, earnings, gross margins and costs were in 2010, 2009 and 2008; |

| | |

· | why those net sales, earnings, gross margins and costs were different from the year before; |

| | |

· | how all of this affects our overall financial condition; |

| | |

· | what our expenditures for capital projects were in 2010 and 2009 and what we expect them to be in 2011; and |

| | |

· | where funds will come from to pay for future expenditures. |

As you read Management’s Discussion and Analysis, please refer to our consolidated financial statements, included in Item 8 of this Form 10-K, which present the results of operations for the fiscal years ended January 29, 2011, January 30, 2010 and January 31, 2009. In Management’s Discussion and Analysis, we analyze and explain the annual changes in some specific line items in the consolidated financial statements for the fiscal year 2010 compared to the comparable fiscal year 2009 and the fiscal year 2009 compared to the comparable fiscal year 2008.

Key Events and Recent Developments

Several key events have had or are expected to have a significant effect on our operations. You should keep in mind that:

| | |

· | On November 15, 2010, we completed our acquisition of 86 Dollar Giant stores, located in the Canadian provinces of British Columbia, Ontario, Alberta and Saskatchewan. These stores offer a wide assortment of quality general merchandise, contemporary seasonal goods and everyday consumables, all priced at $1.25 (CAD) or less. This is our first expansion of retail operations outside of the United States. |

| · | On May 26, 2010, the Company’s Board of Directors approved a 3-for-2 stock split in the form of a 50% common stock dividend. New shares were distributed on June 24, 2010 to shareholders of record as of the close of business on June 10, 2010. As a result, all share and per share data in this Form 10-K have been retroactively adjusted to reflect this dividend having the effect of a 3-for-2 stock split. |

| · | We assign cost to store inventories using the retail inventory method, determined on a weighted average cost basis. From our inception and through fiscal 2009, we used one inventory pool for this calculation. Because of our investments over the years in our retail technology systems, we were able to refine our estimate of inventory cost under the retail method and on January 31, 2010, the first day of fiscal 2010, we began using approximately 30 inventory pools in our retail inventory calculation. As a result of this change, we recorded a non-recurring, non-cash charge to gross profit and a corresponding reduction in inventory, at cost, of $26.3 million in the first quarter of 2010. This was a prospective change and did not have any effect on prior periods. |

· | On November 2, 2009, we purchased a new distribution center in San Bernardino, California. We have spent approximately $31.0 million in capital expenditures for this new distribution center during fiscal 2009 and an additional $5.7 million in fiscal 2010. This new distribution center replaced our Salt Lake City, Utah leased facility whose lease ended in April 2010. |

· | On February 20, 2008, we entered into a five-year $550.0 million unsecured Credit Agreement (the Agreement). The Agreement provides for a $300.0 million revolving line of credit, including up to $150.0 million in available letters of credit, and a $250.0 million term loan. The interest rate on the facility is based, at our option, on a LIBOR rate, plus a margin, or an alternate base rate, plus a margin. |

Overview

Our net sales are derived from the sale of merchandise. Two major factors tend to affect our net sales trends. First is our success at opening new stores or adding new stores through acquisitions. Second, sales vary at our existing stores from one year to the next. We refer to this change as a change in comparable store net sales, because we compare only those stores that are open throughout both of the periods being compared. We include sales from stores expanded during the year in the calculation of comparable store net sales, which has the effect of increasing our comparable store net sales. The term 'expanded' also includes stores that are relocated.

At January 29, 2011, we operated 4,101 stores in 48 states and the District of Columbia, as well as the Canadian provinces of British Columbia, Ontario, Alberta and Saskatchewan, with 35.1 million selling square feet compared to 3,806 stores with 32.3 million selling square feet at January 30, 2010. During fiscal 2010, we opened 235 stores, expanded 95 stores, acquired 86 stores and closed 26 stores, compared to 240 new stores opened, 75 stores expanded and 25 stores closed during fiscal 2009. In the current year we increased our selling square footage by 8.8%. Of the 2.8 million selling square foot increase in 2010, 0.4 million was added by expanding existing stores and 0.7 million was added with the acquisition of Dollar Giant. The average size of our stores opened in 2010 was approximately 8,400 selling square feet (or about 10,200 gross square feet). For 2011, we continue to plan to open stores that are approximately 8,000 - 10,000 selling square feet (or about 10,000 - 12,000 gross square feet). We believe that this store size is our optimal size operationally and that this size also gives our customers an ideal shopping environment that invites them to shop longer and buy more.

In fiscal 2010, comparable store net sales increased by 6.3%. The comparable store net sales increase was primarily the result of a 5.0% increase in the number of transactions and a 1.3% increase in average ticket. We believe comparable store net sales continued to be positively affected by a number of our initiatives, as debit and credit card penetration continued to increase in 2010, and we continued the roll-out of frozen and refrigerated merchandise to more of our stores. At January 29, 2011 we had frozen and refrigerated merchandise in approximately 1,840 stores compared to approximately 1,400 stores at January 30, 2010. We believe that the addition of frozen and refrigerated product enables us to increase sales and earnings by increasing the number of shopping trips made by our customers. In addition, we accept food stamps (under the Supplemental Nutrition Assistance Program (“SNAP”)) in approximately 3,500 qualified stores compared to 2,900 at the end of 2009.

With the pressures of the current economic environment, we have seen increases in the demand for basic, consumable products in 2010. As a result, we have continued to shift the mix of inventory carried in our stores to more consumer product merchandise which we believe increases the traffic in our stores and has helped to increase our sales even during the current economic downturn. While this shift in mix has impacted our merchandise costs we were able to offset that impact in the current year with decreased costs for merchandise in many of our categories.

Our point-of-sale technology provides us with valuable sales and inventory information to assist our buyers and improve our merchandise allocation to our stores. We believe that this has enabled us to better manage our inventory flow resulting in more efficient distribution and store operations and increased inventory turnover for each of the last five years. Inventory turnover improved by approximately 10 basis points in 2010.

In 2007, legislation was enacted that increased the Federal Minimum Wage. The last increase to $7.25 an hour was effective in July 2009. As a result, our wages have increased in the third quarter of 2009 through the first half of 2010; however, we offset the increase in payroll costs through increased productivity and continued efficiencies in product flow to our stores.

We must continue to control our merchandise costs, inventory levels and our general and administrative expenses as increases in these line items could negatively impact our operating results.

Results of Operations

The following table expresses items from our consolidated statements of operations, as a percentage of net sales. On January, 31, 2010, the first day of fiscal 2010, we began using approximately 30 inventory pools in our retail inventory calculation, rather than one inventory pool as we had done since our inception. As a result of this change, we recorded a non-recurring, non-cash charge to gross profit and a corresponding reduction in inventory, at cost, of $26.3 million in the first quarter of 2010.

| | | Year Ended | | | Year Ended | | | Year Ended | |

| | | January 29, | | | January 30, | | | January 31, | |

| | | 2011 | | | 2010 | | | 2009 | |

| | | | | | | | | | |

| Net sales | | | 100.0 | % | | | 100.0 | % | | | 100.0 | % |

| Cost of sales, excluding non-cash beginning inventory adjustment | | | 64.1 | % | | | 64.5 | % | | | 65.7 | % |

| Non-cash beginning inventory adjustment | | | 0.4 | % | | | 0.0 | % | | | 0.0 | % |

| Gross profit | | | 35.5 | % | | | 35.5 | % | | | 34.3 | % |

| | | | | | | | | | | | | |

| Selling, general and administrative | | | | | | | | | | | | |

| expenses | | | 24.8 | % | | | 25.7 | % | | | 26.4 | % |

| | | | | | | | | | | | | |

| Operating income | | | 10.7 | % | | | 9.8 | % | | | 7.9 | % |

| | | | | | | | | | | | | |

| Interest expense,net | | | (0.1 | %) | | | (0.1 | %) | | | (0.2 | %) |

| Other income, net | | | 0.1 | % | | | - | | | | - | |

| | | | | | | | | | | | | |

| Income before income taxes | | | 10.7 | % | | | 9.7 | % | | | 7.7 | % |

| | | | | | | | | | | | | |

| Provision for income taxes | | | (3.9 | %) | | | (3.6 | %) | | | (2.8 | %) |

| | | | | | | | | | | | | |

| Net income | | | 6.8 | % | | | 6.1 | % | | | 4.9 | % |

Fiscal year ended January 29, 2011 compared to fiscal year ended January 30, 2010

Net Sales. Net sales increased 12.4%, or $651.2 million, in 2010 compared to 2009, resulting from a 6.3% increase in comparable store net sales and sales in our new stores. Comparable store net sales are positively affected by our expanded and relocated stores, which we include in the calculation, and, to a lesser extent, are negatively affected when we open new stores or expand stores near existing ones.

The following table summarizes the components of the changes in our store count for fiscal years ended January 29, 2011 and January 30, 2010.

| | | January 29, 2011 | | | January 30, 2010 | |

| | | | | | | |

| New stores | | | 235 | | | | 240 | |

| Acquired stores | | | 86 | | | | - | |

| Expanded or relocated stores | | | 95 | | | | 75 | |

| Closed stores | | | (26 | ) | | | (25 | ) |

Of the 2.9 million selling square foot increase in 2010 approximately 0.4 million was added by expanding existing stores and 0.7 million was the result of the acquisition of the Dollar Giant stores.

Gross profit margin was 35.5% in 2010 and 2009. Excluding the effect of the $26.3 million non-cash beginning inventory adjustment, gross profit margin increased to 35.9%. This increase was due to the following:

· | Occupancy and distribution costs decreased 30 basis points in the current year resulting fromthe leveraging of the comparable store sales increase. |

· | Shrink costs decreased 15 basis points due to improved shrink results in the current year and a lower shrink accrual rate during fiscal 2010 compared to fiscal 2009. |

· | Merchandise costs, including freight, increased 15 basis points due primarily to higher import and domestic freight costs during fiscal 2010 compared to fiscal 2009. |

Selling, General and Administrative Expenses. Selling, general and administrative expenses, as a percentage of net sales, decreased to 24.8% for 2010 compared to 25.7% for 2009. The decrease is primarily due to the following:

· | Payroll expenses decreased 45 basis points fue to leveraging associated with the increase in comparable store net sales in the current year and lower store hourly payroll. |

· | Depreciation decreased 30 basis points primarily due to the leveraging associated with the increase in comparable store net sales in current year. |

· | Store operating costs decreased 20 basis points primarily as a result of lower utility costs as a percentage of sales, due to lower rates in the current year and the leveraging from the comparable store net sales increase in 2010. |

Operating Income. Operating income margin was 10.7% in 2010 compared to 9.8% in 2009. Excluding the $26.3 million non-cash adjustment to beginning inventory, operating income margin was 11.1% due to the reasons discussed above.

Income Taxes. Our effective tax rate was 36.9% in 2010 and 2009.

Fiscal year ended January 30, 2010 compared to fiscal year ended January 31, 2009

Net Sales. Net sales increased 12.6%, or $586.3 million, in 2009 compared to 2008, resulting from a 7.2% increase in comparable store net sales and sales in our new stores. Comparable store net sales are positively affected by our expanded and relocated stores, which we include in the calculation, and, to a lesser extent, are negatively affected when we open new stores or expand stores near existing ones.

The following table summarizes the components of the changes in our store count for fiscal years ended January 30, 2010 and January 31, 2009.

| | | January 30, 2010 | | | January 31, 2009 | |

| | | | | | | |

| New stores | | | 240 | | | | 227 | |

| Acquired leases | | | - | | | | 4 | |

| Expanded or relocated stores | | | 75 | | | | 86 | |

| Closed stores | | | (25 | ) | | | (51 | ) |

Of the 2.0 million selling square foot increase in 2009 approximately 0.3 million was added by expanding existing stores.

Gross profit margin increased to 35.5% in 2009 compared to 34.3% in 2008. The increase was due to the following:

· | Merchandise costs, including inbound freight, decreased 80 basis points due primarily to lower fuel costs and lower ocean freight rates compared to the prior year. Improved initial mark-up in many categories during the year was partially offset by an increase in the mix of higher cost consumer product merchandise during fiscal 2009 compared to fiscal 2008. |

· | Outbound freight costs decreased 20 basis points in the current year due primarily to decreased fuel costs. |

· | Occupancy and distribution costs decreased 30 basis points in the current year resulting from the leveraging of the comparable store sales increase. |

Selling, General and Administrative Expenses. Selling, general and administrative expenses, as a percentage of net sales, decreased to 25.7% for 2009 compared to 26.4% for 2008. The decrease is primarily due to the following:

· | Depreciation decreased 40 basis points primarily due to the leveraging associated with the increase in comparable store net sales in the current year. |

· | Store operating costs decreased 30 basis points primarily as a result of lower utility costs as a percentage of sales, due to lower rates in the current year and the leveraging from the comparable store net sales increase in 2009. |

Operating Income. Due to the reasons discussed above, operating income margin was 9.8% in 2009 compared to 7.9% in 2008.

Income Taxes. Our effective tax rate was 36.9% in 2009 compared to 36.1% in 2008. The higher rate in the current year was the result of the favorable settlement of several state tax audits in 2008 and a higher blended state tax rate in 2009.

Liquidity and Capital Resources

Our business requires capital to build and open new stores, expand our distribution network and operate existing stores. Our working capital requirements for existing stores are seasonal and usually reach their peak in September and October. Historically, we have satisfied our seasonal working capital requirements for existing stores and have funded our store opening and distribution network expansion programs from internally generated funds and borrowings under our credit facilities.

The following table compares cash-flow related information for the years ended January 29, 2011, January 30, 2010 and January 31, 2009:

| | | January 29, | | | January 30, | | | January 31, | |

| (in millions) | | 2011 | | | 2010 | | | 2009 | |

| Net cash provided by (used in): | | | | | | | | | |

| Operating activities | | $ | 518.7 | | | $ | 581.0 | | | $ | 403.1 | |

| Investing activities | | | (374.1 | ) | | | (212.5 | ) | | | (102.0 | ) |

| Financing activities | | | (404.3 | ) | | | (161.3 | ) | | | 22.7 | |

Net cash provided by operating activities decreased $62.3 million in 2010 compared to 2009 due to an increase in cash used to purchase merchandise inventories partially offset by increased earnings before income taxes, depreciation and amortization in the current year.

Net cash provided by operating activities increased $177.9 million in 2009 compared to 2008 due to increased earnings before income taxes, depreciation and amortization in 2009. Also providing more cash at January 30, 2010 was better inventory management resulting in lower inventory balances per store and higher accounts payable balances due to the timing of payments and increased incentive compensation accruals.

Net cash used in investing activities increased $161.6 million in the current year primarily due to short-term investment activity and the Dollar Giant acquisition. In 2010 we purchased $157.8 million of short-term investments compared to $27.8 million in 2009. This was partially offset by an increase in proceeds from the sales of short-term investments of $10.8 million in the current year.

Net cash used in investing activities increased $110.5 million in 2009 primarily due to short-term investment activity and increased capital expenditures in 2009. In 2008 we liquidated our short-term investments due to market conditions. The net proceeds from this liquidation of $40.5 million were put into cash equivalent money market accounts. In 2009 we also purchased $27.8 million of short-term investments. Capital expenditures increased $33.5 million in 2009 primarily due to the purchase of our new distribution center in San Bernardino, CA.

In 2010, net cash used in financing activities increased $243.0 million as a result of increased share repurchases in 2010 and repayments of $13.8 million for debt acquired from Dollar Giant.

In 2009, net cash used in financing activities increased $184.0 million as the result of share repurchases in 2009. There were no share repurchases in 2008.

At January 29, 2011, our long-term borrowings were $266.5 million and our capital lease commitments were $1.4 million. We also have $121.5 million and $50.0 million Letter of Credit Reimbursement and Security Agreements, under which approximately $106.9 million were committed to letters of credit issued for routine purchases of imported merchandise at January 29, 2011.