The PMI Group, Inc. May 2008 Exhibit 99.1 |

2 The PMI Group, Inc. Forward-Looking Statement FORWARD-LOOKING STATEMENTS: Statements in this presentation and oral statements made at this conference that are not historical facts or that relate to future plans, events or performance are "forward- looking" statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements include our expectations with respect to: future economic and mortgage market conditions in the United States and other areas of the world in which we conduct business; and our current and future strategy. Many factors could cause actual results and developments to differ materially from those expressed or implied by forward-looking statements, including, among others, conditions affecting the mortgage insurance and financial guaranty industries, general economic conditions, and regulatory and legislative developments in the US, Europe and Australia, including the continued implementation of-Basel II bank capital directives. In particular, changes in housing values, unemployment rates, interest rates, refinancing activity and the use of alternatives to mortgage insurance could affect the demand for mortgage insurance and/or cause claims on policies issued to increase. Our future strategy and various new ventures may be subject to a number of risks, including: the need for regulatory, rating agency and other third party approvals; challenges in attracting and retaining key employees; unexpected changes in foreign regulations and laws; and the need to successfully develop and market products appropriate to the new market. Accordingly, there can be no assurance that new ventures and further geographic diversification will be achieved or that such ventures will achieve profitability. Other risks and uncertainties are discussed in our SEC filings, including our Form 10-K for the year ended December 31, 2007 and our Quarterly Report on Form 10-Q for the quarter ended March 31, 2008. We undertake no obligation to update forward-looking statements, except as required by law. |

3 The PMI Group, Inc. The PMI Group, Inc. For over 35 years PMI has combined its risk management expertise and financial strength to serve the evolving needs of the financial markets. PMI provides insurance, guarantees and reinsurance for residential mortgages and securities, public finance obligations and asset-backed securities around the world. |

4 The PMI Group, Inc. PMI’s Five Point Plan for Progress Implemented significant changes to underwriting guidelines principally related to 100% LTVs, Alt-As and distressed markets Resulting business will be better credit quality Book High Quality New Business Mitigate losses through claim verification, foreclosure prevention, early borrower contact and an emphasis on workouts Significant benefit from our captive reinsurance programs Mitigate Losses Intense focus on expenses Invest in our business and commit resources where they are needed Manage Expenses Focus on core MI business will position us for growth Continue to work to stabilize the value of our financial guaranty investments Focus on Core Mortgage Insurance Business Evaluating our current and projected need for capital to support business now and into the future We are exploring a wide range of options, including capital markets transactions, reinsurance and certain asset sales Maintain Financial Strength |

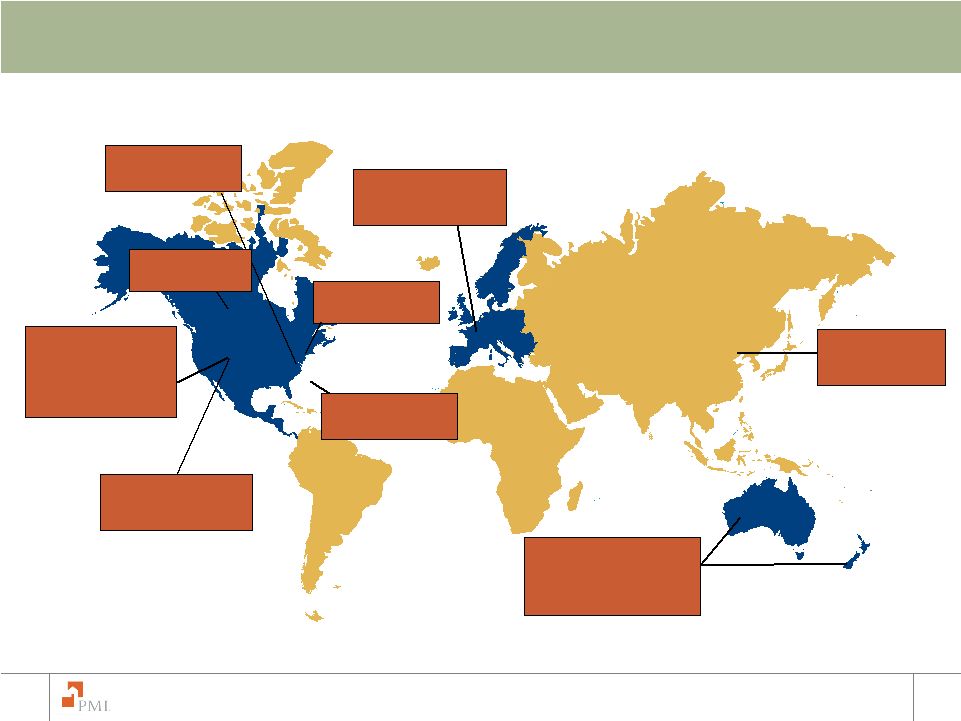

5 The PMI Group, Inc. PMI’s Global Footprint U.S. Mortgage Insurance Primary IIF $1 24 B Pool RIF $ 3 B Australia + New Zealand $183 billion IIF Europe $63 billion IIF RAM Re 24% ownership Asia $3 billion IIF FGIC 42% ownership CMG $20 billion IIF PMI Canada As of March 31, 2008 PMI Guaranty |

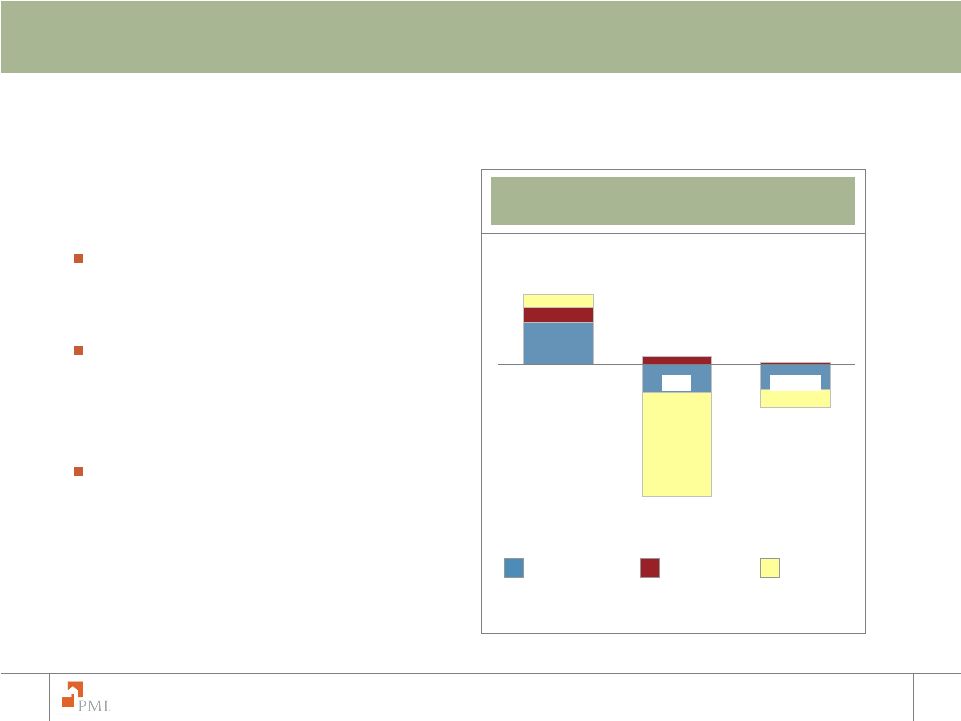

6 The PMI Group, Inc. Segment Net Income The PMI Group’s three business segments: U.S. Mortgage Insurance Operations is a core business with opportunities for growth. International Mortgage Insurance Operations remains a positive contributor to consolidated net income. Financial Guaranty is no longer a core strategic segment. Net Income by Business Segment* (dollars in millions) U.S. Mortgage Insurance Operations International Mortgage Insurance Operations Financial Guaranty • Totals represent consolidated net income, Corporate and Other business segment not displayed in columns $420 $(915) $(274) 2006 2007 Q1 2008 |

7 The PMI Group, Inc. Core business is experiencing challenges: We have taken steps to successfully navigate this cycle. Expect challenges to continue this year and, as a result, we will have losses on a consolidated basis in 2008. Demand trends and underwriting quality have increased significantly. U.S. Mortgage Insurance (Dollar’s in millions) 2006 2007 Q1 2008 U.S. Mortgage Insurance Net Income $290.3 $(190.8) $(172.5) U.S. Mortgage Insurance Total Revenues $916.0 $797.6 $277.3 2006 Q1 2008 2007 |

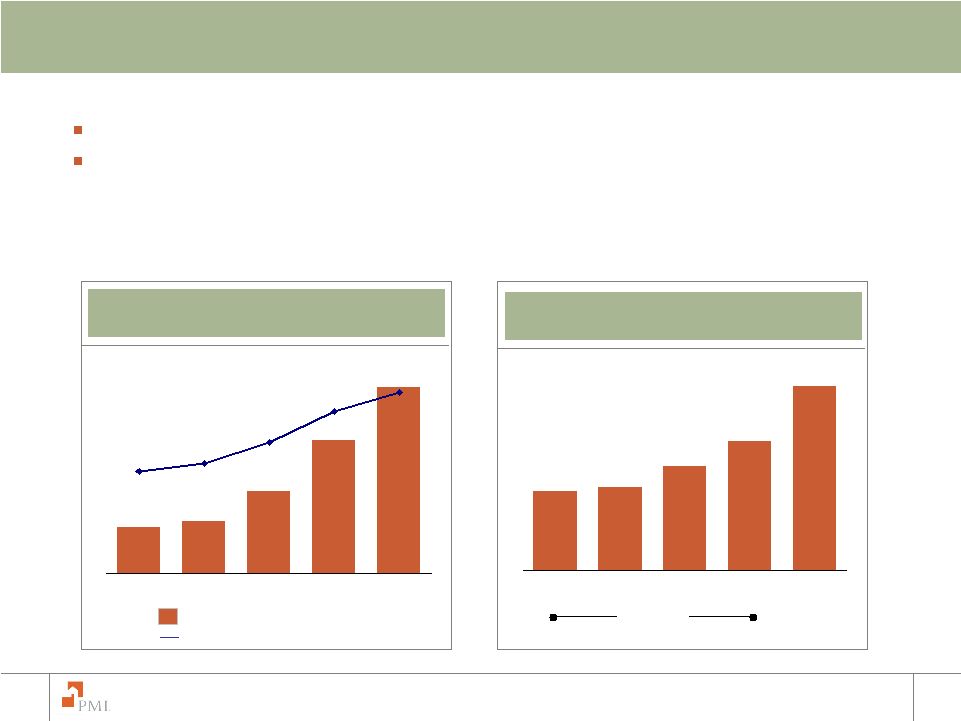

8 The PMI Group, Inc. 2006 2007 Q1 2008 $102.6 $123.6 $124.3 Primary Insurance in Force (dollars in billions) Premiums Earned (dollars in millions) 2006 2007 Q1 2008 $688.0 $801.0 $207.8 2006 2007 Q1 2008 23.2% 22.5% *13.0% U.S. Mortgage Insurance Operations Expense Ratio Primary Persistency Rate 77.6% 56.2% 44.6% 60.9% 61.9% 69.6% 75.5% 2002 2003 2004 2005 2006 2007 Q1 2008 U.S. Mortgage Insurance •The Q1 2008 expense ratio was affected by a $34 million impairment of deferred policy acquisitions costs associated with PMI’s 2007 book year in the fourth quarter of 2007. |

9 The PMI Group, Inc. Credit Environment Economy National economy trending toward modest recession Modest rise in unemployment Interest rates continue to move downward Geographic Diversification Portfolio is well diversified throughout the U.S. Florida accounts for 10.8% of risk in force California accounts for 8.4% of risk in force Product Diversification High quality book of insured loans Primarily first time home buyers with modest loan size Low percentage of interest only and payment option ARMs Credit Performance Primary default rate at March 31, 2008 was 8.78% Slowing HPA has affected ability to mitigate losses Larger loans sizes from recent vintages are resulting in larger claim sizes Increase in length of time loans stay delinquent has grown as servicers face a backlog of defaults |

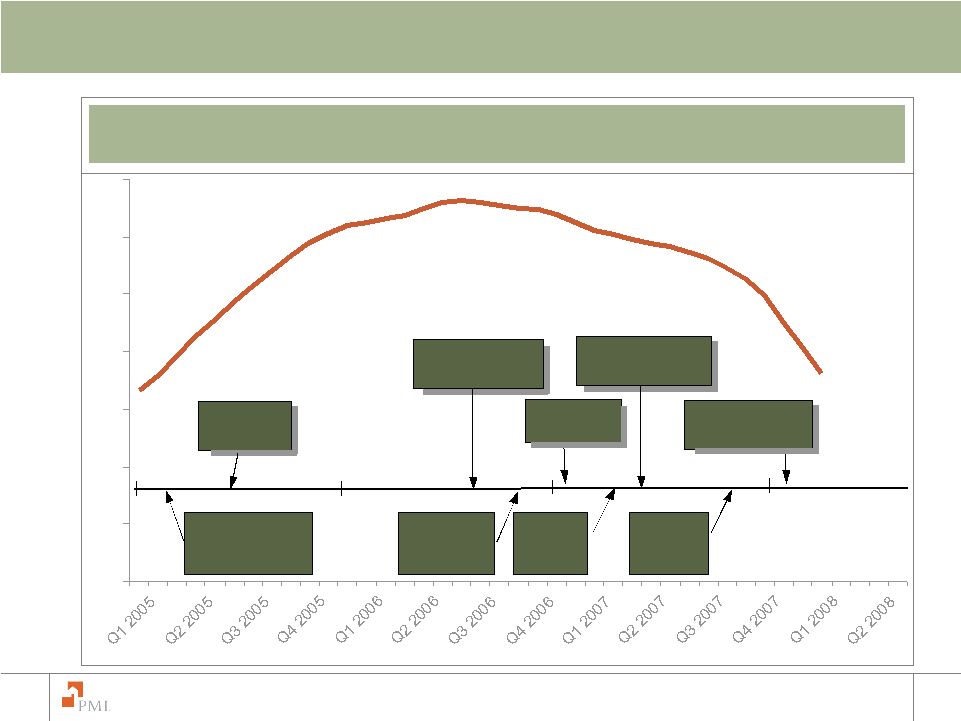

10 The PMI Group, Inc. 160 170 180 190 200 210 220 230 PMI Field UW Investigations Unit formed Managing Risk Ahead of the Market Action Time Line Standard & Poor’s Case Shiller Composite Index PMI makes first of many bulk guideline & pricing changes PMI leads industry on 100 LTV guideline & pricing changes Additional Bulk guideline changes PMI implements MSA level distressed markets policy PMI’s Risk Index provides early warning of housing market downturns Origination fraud detection tools implemented LPMI guideline changes PMI leads on Alt-A guideline changes |

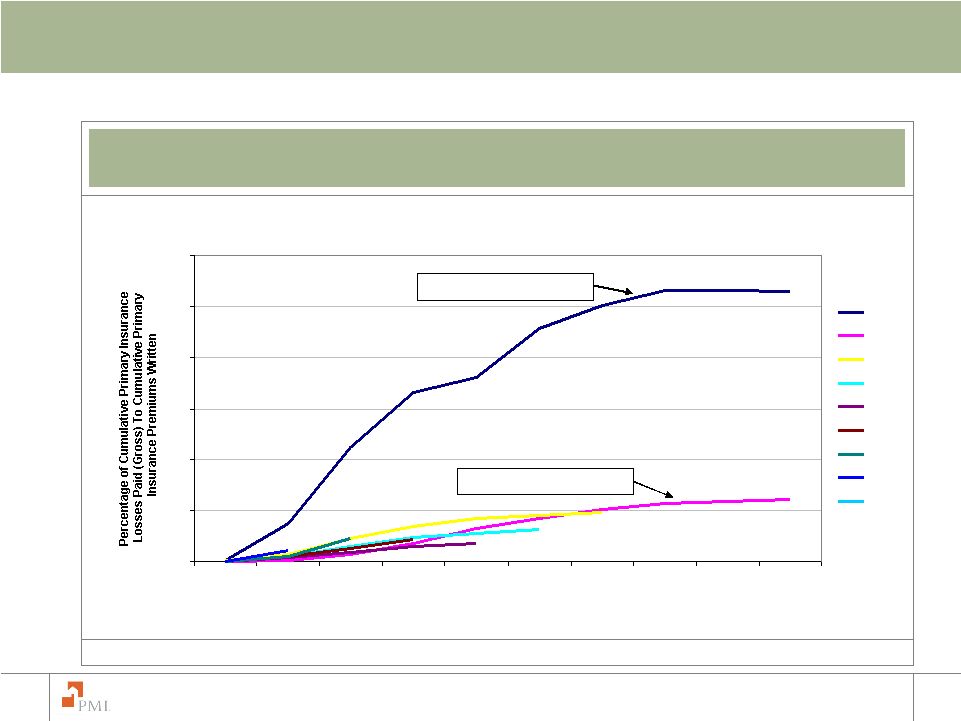

11 The PMI Group, Inc. U.S. Portfolio – Policy Year Loan Performance *Gross premiums written include ceded and refunded premiums. Percentage of Cumulative Primary Insurance Losses Paid (Gross) To Cumulative Primary Insurance Premiums Written (Gross)* 1982 “Oil Patch” experience 1990 “California” experience 0 50 100 150 200 250 300 1 2 3 4 5 6 7 8 9 10 Years Since Policy Issue 1982 1990 2001 2002 2003 2004 2005 2006 2007 |

12 The PMI Group, Inc. $72.8 $75.7 $95.9 $117.9 Q1 2007 Q2 2007 Q3 2007 Q4 2007 Q1 2008 Significant strengthened reserves for losses and loss adjustment expenses (LAE). Intense focus on foreclosure prevention through payment plans, loan modifications, presales, deeds in lieu. • Partially as a result, in the first quarter of 2008 approximately 600 foreclosures were avoided and 1,000 borrowers were able to retain their homes. U.S. Portfolio – Credit (Dollar’s in millions) Reserves for Losses and LAE and Notices of Default Total Claims Paid Including LAE $168.8 FY 2007 $362.3 Reserves for Losses and LAE Notices of Default $386,000 $444,600 $698,200 $1,133,080 $1,589,253 103,254 92,340 74,531 62,587 57,706 Q1 2007 Q2 2007 Q3 2007 Q4 2007 Q1 2008 |

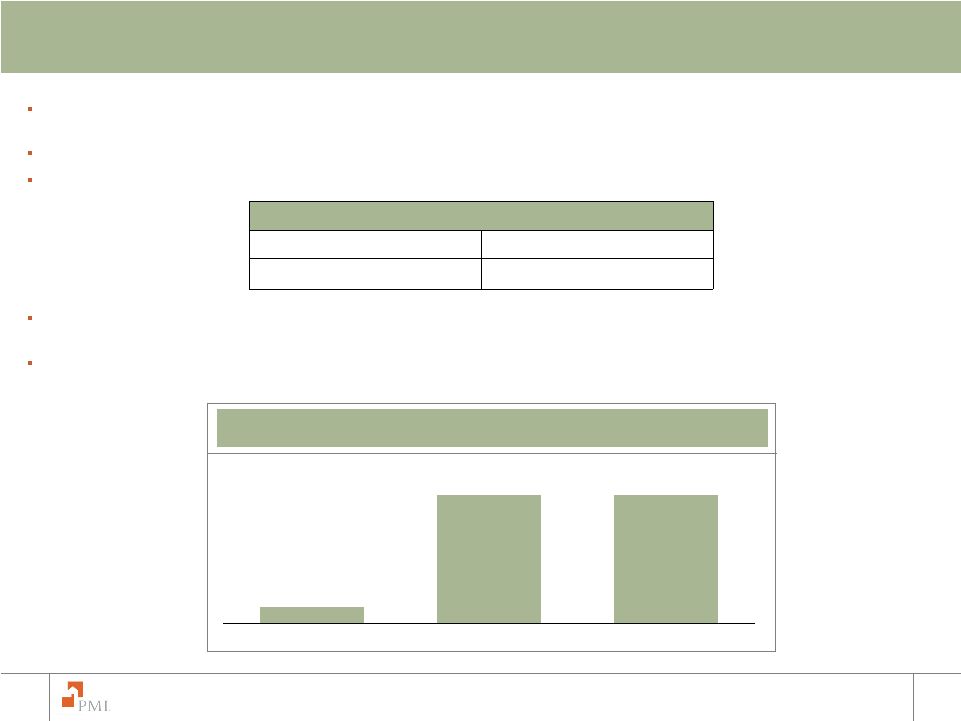

13 The PMI Group, Inc. $275 $275 $34 2007 2008 2009 Captive reinsurers are wholly-owned, bankruptcy remote subsidiaries of originators that provide mezzanine level reinsurance for loans for which PMI has provided primary mortgage insurance coverage. PMI is the named beneficiary on captive trust balances totaling approximately $747 million as of March 31, 2008. At December 31, 2007, approximately 62% of flow risk in force was covered by captive reinsurance agreements, including: Captive trust balances will continue to grow with new insurance written in the flow channel. Future ceded premiums can be used to meet capital adequacy for existing book years. Based on current expectations of defaults, PMI forecasts approximately the following reductions to total incurred losses as a result of captive reinsurance agreements in 2008 and 2009: Expected Benefit from Captive Reinsurance Agreements PMI’s Captive Reinsurance Agreements (Dollars in Millions) Flow Risk in Force Covered by Captives ~ 55% of LTVs >97%* ~ 65% of less-than-A quality ~ 48% of Alt-A ~ 65% of prime * Captive coverage for LTVs greater than 97% may overlap with other listed categories |

14 The PMI Group, Inc. 2006 2007 Q1 2008 International Mortgage Insurance International MI Operations Net Income (dollars in millions) $103.5 International MI operations have consistently been a positive net income contributor. PMI Europe has posted net losses in recent quarters as a result of increased losses and mark-to-market on CDS related to European prime mortgage. $55.0 $17.8 |

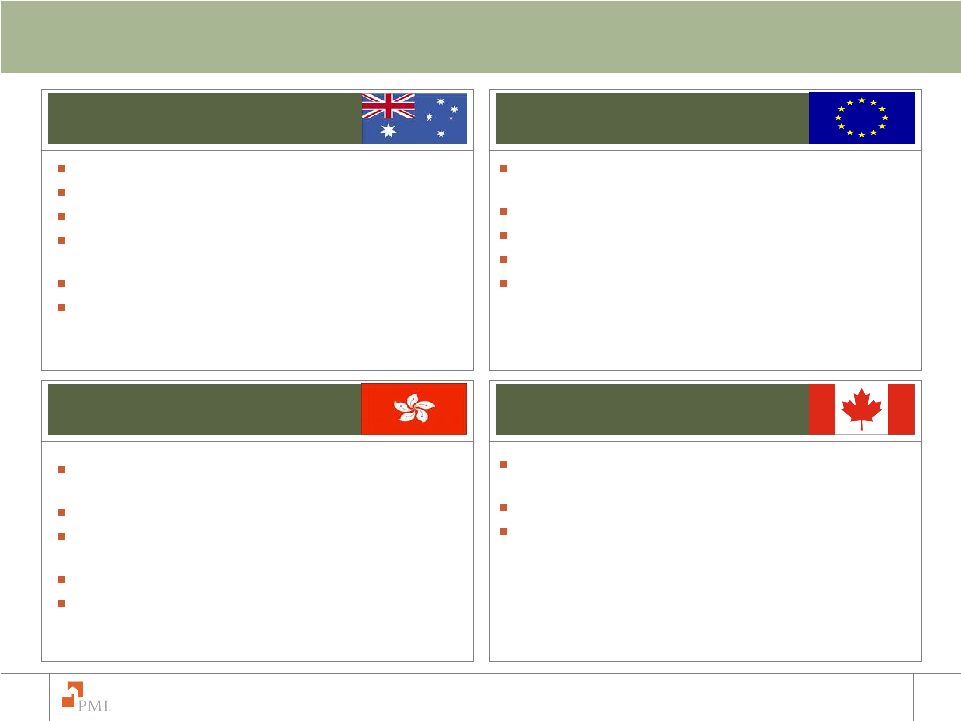

15 The PMI Group, Inc. International Mortgage Insurance Australia Strong growth in written premiums and net income Losses are trending towards more normal levels Continued strong economic growth and employment Position business to lead in flow and structured segments Stronger relationships with Top 4 lenders Development of products to fit new regulatory and capital regimes Europe Current challenges with higher losses and negative mark-to-market losses Developing Italian flow channel Office opened in Spain in 2007 Product development for new regulatory regimes Significant opportunities in structured, super senior and first loss transactions Asia PMI is one of the few providers of reinsurance to the Hong Kong Mortgage Corporation History of strong results in Hong Kong Develop market leading programs to expand home ownership Poised for capital markets opportunities Strong platform to enter other Asian markets Canada Second largest mortgage insurance market behind the U.S. Strong leadership team and board assembled Innovative products and services |

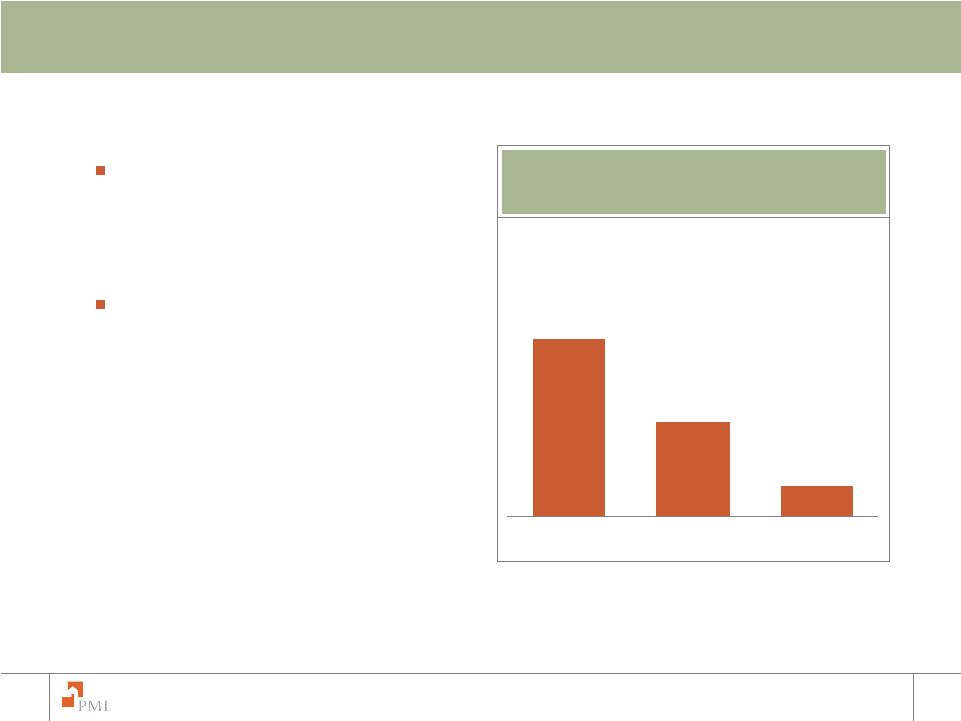

16 The PMI Group, Inc. Financial Guaranty Financial Guaranty segment is no longer strategic to our operations. FGIC carrying value was reduced to zero at March 31, 2008, therefore, the Company will not recognize in future periods its proportionate share of FGIC losses, if any. No additional capital will be invested in FGIC or RAM Re. PMI’s management team continues to work with the both FGIC and RAM Re in stabilizing their respective businesses and our equity investments. FGIC RAM Re Financial Guaranty Investments Carrying Value* $0.0 $26.0 Financial Guaranty Segment Net Income $(731.7) $97.3 $(124.2) *At March 31, 2008 2006 Q1 2008 2007 |

17 The PMI Group, Inc. Summary We are executing our plan to return to profitability and are making substantial progress. Continue to see strong fundamentals in the mortgage insurance business. We continue to believe that our core mortgage insurance operations will be an attractive long-term business. PMI’s entire management team, and each and every PMI employee, is committed to executing our plan, as well as fostering sustainable home ownership, which we believe will bring long term value to our shareholders. |

|