EXHIBIT 99.1

Continuing the Journey JP Morgan Healthcare Conference January 13, 2015 Flemming Ornskov, MD, MPH Chief Executive Officer [GRAPHIC OMITTED] |  |

"SAFE HARBOR" statement under the Private Securities Litigation Reform Act of 1995 and tender offer materials Statements included in this communication that are not historical facts are forward -looking statements. Such forward -looking statements involve a number of risks and uncertainties and are subject to change at any time. In the event such risks or uncertainties materialize, Shire's results could be materially adversely affected. The risks and uncertainties include, but are not limited to, that: [] Shire's products may not be a commercial success; [] revenues from ADDERALL XR and INTUNIV are subject to generic erosion; [] the failure to obtain and maintain reimbursement, or an adequate level of reimbursement, by third-party payors in a timely manner for Shire's products may impact future revenues, financial condition and results of operations; [] Shire conducts its own manufacturing operations for certain of its products and is reliant on third party contract manufacturers to manufacture other products and to provide goods and services. Some of Shire's products or ingredients are only available from a single approved source for manufacture. Any disruption to the supply chain for any of Shire's products may result in Shire being unable to continue marketing or developing a product or may result in Shire being unable to do so on a commercially viable basis for some period of time; [] the development, approval and manufacturing of Shire's products is subject to extensive oversight by various regulatory agencies. Submission of an application for regulatory approval of any of our product candidates, such as our planned submission of a New Drug Application to the FDA for Lifitegrast, may be delayed for any number of reasons and, once submitted, may be subjected to lengthy review and ultimately rejected. Moreover, regulatory approvals or interventions associated with changes to manufacturing sites, ingredients or manufacturing processes could lead to significant delays, increase in operating costs, lost product sales, an interruption of research activities or the delay of new product launches; [] the actions of certain customers could affect Shire 's ability to sell or market products profitably. Fluctuations in buying or distribution patterns by such customers can adversely impact Shire's revenues, financial condition or results of operations; [] investigations or enforcement action by regulatory authorities or law enforcement agencies relating to Shire's activities in the highly regulated markets in which it operates may result in significant legal costs and the payment of substantial compensation or fines; [] adverse outcomes in legal matters and other disputes, including Shire's ability to enforce and defend patents and other intellectual property rights required for its business, could have a material adverse effect on Shire's revenues, financial condition or results of operations; [] Shire faces intense competition for highly qualified personnel from other companies, academic institutions, government entities and other organizations. Shire is undergoing a corporate reorganization and the consequent uncertainty could adversely impact Shire's ability to attract and/or retain the highly skilled personnel needed for Shire to meet its strategic objectives; [GRAPHIC OMITTED] 2 |  |

"SAFE HARBOR" statement under the Private Securities Litigation Reform Act of 1995 and tender offer materials [] failure to achieve Shire's strategic objectives with respect to the acquisition of ViroPharma Incorporated may adversely affect Shire's financial condition and results of operations; [] Shire's proposed acquisition of NPS Pharma may not be consummated due to the occurrence of an event, change or other circumstances that gives rise to the termination of the merger agreement; [] a governmental or regulatory approval required for the proposed acquisition of NPS Pharma may not obtained, or may be obtained subject to conditions that are not anticipated, or another condition to the closing of the proposed acquisition may not be satisfied; [] NPS Pharma may be unable to retain and hire key personnel and/or maintain its relationships with customers, suppliers and other business partners pending the consummation of the proposed acquisition by Shire, or NPS Pharma's business may be disrupted by the proposed acquisition, including increased costs and diversion of management time and resources; [] difficulties in integrating NPS Pharma into Shire may lead to the combined company not being able to realize the expected operating efficiencies, cost savings, revenue enhancements, synergies or other benefits at the time anticipated or at all; [] and other risks and uncertainties detailed from time to time in Shire's or NPS Pharma's filings with the U.S. Securities and Exchange Commission, including their respective most recent Annual Reports on Form 10-K. THIS COMMUNICATION IS FOR INFORMATIONAL PURPOSES ONLY AND DOES NOT CONSTITUTE AN OFFER TO PURCHASE OR A SOLICITATION OF AN OFFER TO SELL NPS PHARMA COMMON STOCK. THE OFFER TO BUY NPS PHARMA COMMON STOCK WILL ONLY BE MADE PURSUANT TO A TENDER OFFER STATEMENT (INCLUDING THE OFFER TO PURCHASE, LETTER OF TRANSMITTAL AND OTHER RELATED TENDER OFFER MATERIALS) . INVESTORS AND SECURITY HOLDERS ARE URGED TO READ BOTH THE TENDER OFFER STATEMENT (WHICH WILL BE FILED BY SHIRE AND A SUBSIDIARY OF SHIRE WITH THE SECURITIES AND EXCHANGE COMMISSION (SEC)) AND THE SOLICITATION/RECOMMENDATION STATEMENT ON SCHEDULE 14D-9 WITH RESPECT TO THE TENDER OFFER (WHICH WILL BE FILED BY NPS PHARMA WITH THE SEC) WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION, INCLUDING THE TERMS AND CONDITIONS OF THE OFFER. INVESTORS AND SECURITY HOLDERS MAY OBTAIN A FREE COPY OF THESE MATERIALS (WHEN AVAILABLE) AND OTHER DOCUMENTS FILED BY Shire AND NPS PHARMA WITH THE SEC AT THE WEBSITE MAINTAINED BY THE SEC AT WWW. SEC.GOV. THE TENDER OFFER STATEMENT AND RELATED MATERIALS, AND THE SOLICITATION/RECOMMENDATION STATEMENT, MAY ALSO BE OBTAINED (WHEN AVAILABLE) FOR FREE BY CONTACTING SHIRE INVESTOR RELATIONS AT +1 484 595 2220 IN THE US AND +44 1256 894157 IN THE UK. COPIES OF THESE MATERIALS AND ANY DOCUMENTATION RELATING TO THE TENDER OFFER ARE NOT BEING, AND MUST NOT BE, DIRECTLY OR INDIRECTLY, MAILED OR OTHERWISE FORWARDED, DISTRIBUTED OR SENT IN, INTO OR FROM ANY JURISDICTION WHERE TO DO SO WOULD BE UNLAWFUL. [GRAPHIC OMITTED] 3 |  |

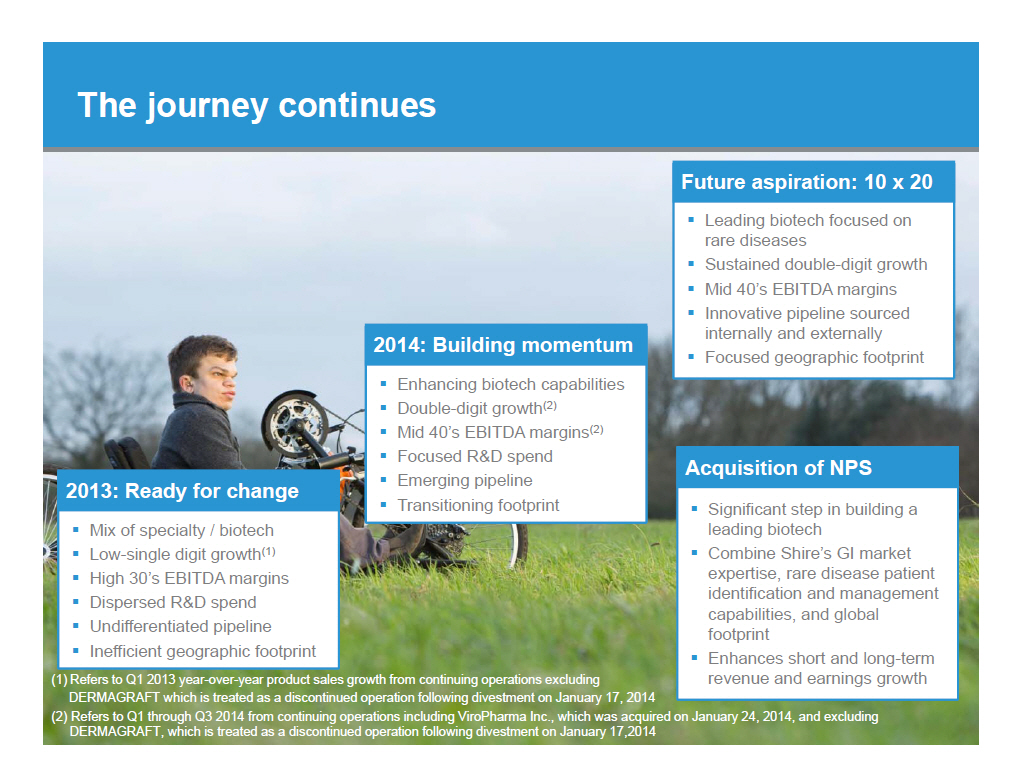

Journey to become a leading biotech 2013: Ready for change * Mix of specialty / biotech * Low-single digit growth(1) * High 30's EBITDA margins * Dispersed RandD spend * Undifferentiated pipeline * Inefficient geographic footprint (1) Refers to Q1 2013 year-over-year product sales growth from continuing operations excluding DERMAGRAFT which is treated as a discontinued operation following divestment on January 17, 2014 |  |

Journey to become a leading biotech 2014: Building momentum * Enhancing biotech capabilities * Double -digit growth(2) * Mid 40's EBITDA margins (2) * Focused RandD spend * Emerging pipeline * Transitioning footprint 2013: Ready for change * Mix of specialty / biotech * Low-single digit growth(1) * High 30's EBITDA margins * Dispersed RandD spend * Undifferentiated pipeline * Inefficient geographic footprint (1) Refers to Q1 2013 year-over-year product sales growth from continuing operations excluding DERMAGRAFT which is treated as a discontinued operation following divestment on January 17, 2014 (2) Refers to Q1 through Q3 2014 from continuing operations including ViroPharma Inc., which was acquired on January 24, 2014, and excluding DERMAGRAFT, which is treated as a discontinued operation following divestment on January 17,2014 |  |

Journey to become a leading biotech Future aspiration: 10 x 20 * Leading biotech focused on rare diseases * Sustained double-digit growth * Mid 40's EBITDA margins * Innovative pipeline sourced internally and externally * Focused geographic footprint 2014: Building momentum * Enhancing biotech capabilities * Double -digit growth(2) * Mid 40's EBITDA margins (2) * Focused RandD spend * Emerging pipeline * Transitioning footprint 2013: Ready for change * Mix of specialty / biotech * Low-single digit growth(1) * High 30's EBITDA margins * Dispersed RandD spend * Undifferentiated pipeline * Inefficient geographic footprint (1) Refers to Q1 2013 year-over-year product sales growth from continuing operations excluding DERMAGRAFT which is treated as a discontinued operation following divestment on January 17, 2014 (2) Refers to Q1 through Q3 2014 from continuing operations including ViroPharma Inc., which was acquired on January 24, 2014, and excluding DERMAGRAFT, which is treated as a discontinued operation following divestment on January 17,2014 |  |

Journey to become a leading biotech Future aspiration: 10 x 20 * Leading biotech focused on rare diseases * Sustained double-digit growth * Mid 40's EBITDA margins * Innovative pipeline sourced internally and externally * Focused geographic footprint 2014: Building momentum * Enhancing biotech capabilities * Double -digit growth(2) * Mid 40's EBITDA margins (2) * Focused RandD spend * Emerging pipeline * Transitioning footprint 2013: Ready for change * Mix of specialty / biotech * Low-single digit growth(1) * High 30's EBITDA margins * Dispersed RandD spend * Undifferentiated pipeline * Inefficient geographic footprint Acquisition of NPS * Significant step in building a leading biotech * Combine Shire's GI market expertise, rare disease patient identification and management capabilities, and global footprint * Enhances short and long-term revenue and earnings growth (1) Refers to Q1 2013 year-over-year product sales growth from continuing operations excluding DERMAGRAFT which is treated as a discontinued operation following divestment on January 17, 2014 (2) Refers to Q1 through Q3 2014 from continuing operations including ViroPharma Inc., which was acquired on January 24, 2014, and excluding DERMAGRAFT, which is treated as a discontinued operation following divestment on January 17,2014 |  |

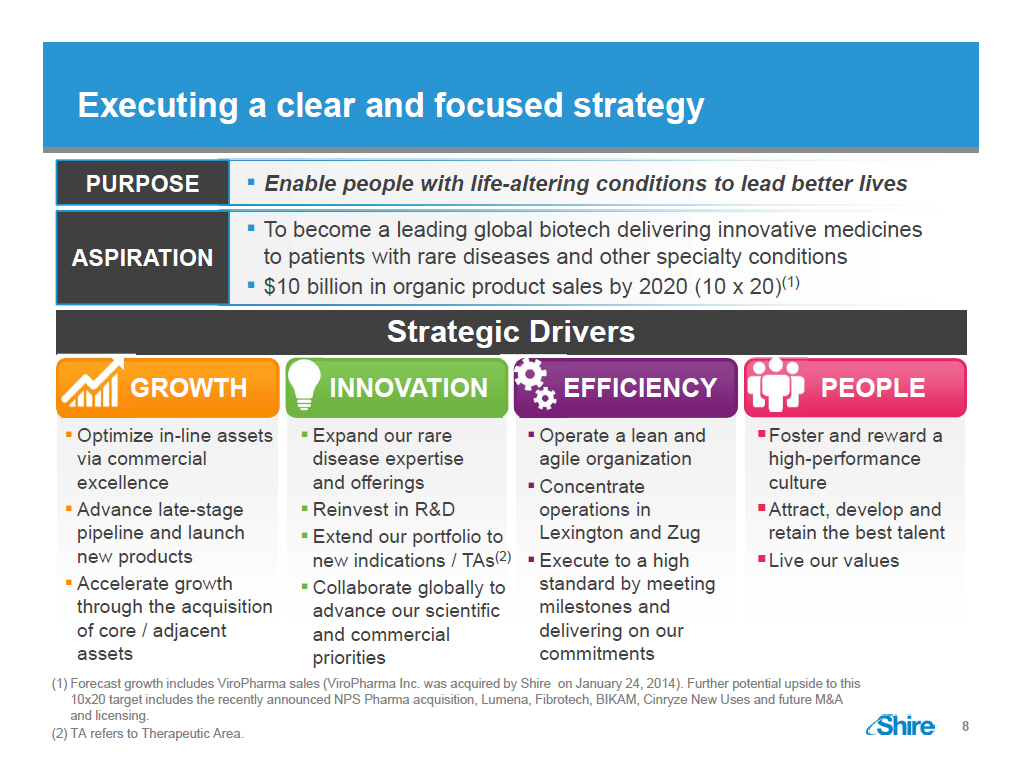

Executing a clear and focused strategy PURPOSE ASPIRATION [] Enable people with life-altering conditions to lead better lives [] To become a leading global biotech delivering innovative medicines to patients with rare diseases and other specialty conditions [] $10 billion in organic product sales by 2020 (10 x 20)(1) Strategic Drivers [GRAPHIC OMITTED] [] Optimize in-line assets via commercial excellence [] Advance late-stage pipeline and launch new products [] Accelerate growth through the acquisition of core / adjacent assets [] Expand our rare disease expertise and offerings [] Reinvest in RandD [] Extend our portfolio to new indications / TAs(2) [] Collaborate globally to advance our scientific and commercial priorities [] Operate a lean and agile organization [] Concentrate operations in Lexington and Zug [] Execute to a high standard by meeting milestones and delivering on our commitments *Foster and reward a high-performance culture *Attract, develop and retain the best talent *Live our values (1) Forecast growth includes ViroPharma sales (ViroPharma Inc. was acquired by Shire on January 24, 2014). Further potential upside to this 10x20 target includes the recently announced NPS Pharma acquisition, Lumena, Fibrotech, BIKAM, Cinryze New Uses and future MandA and licensing. (2) TA refers to Therapeutic Area. [GRAPHIC OMITTED] 8 |  |

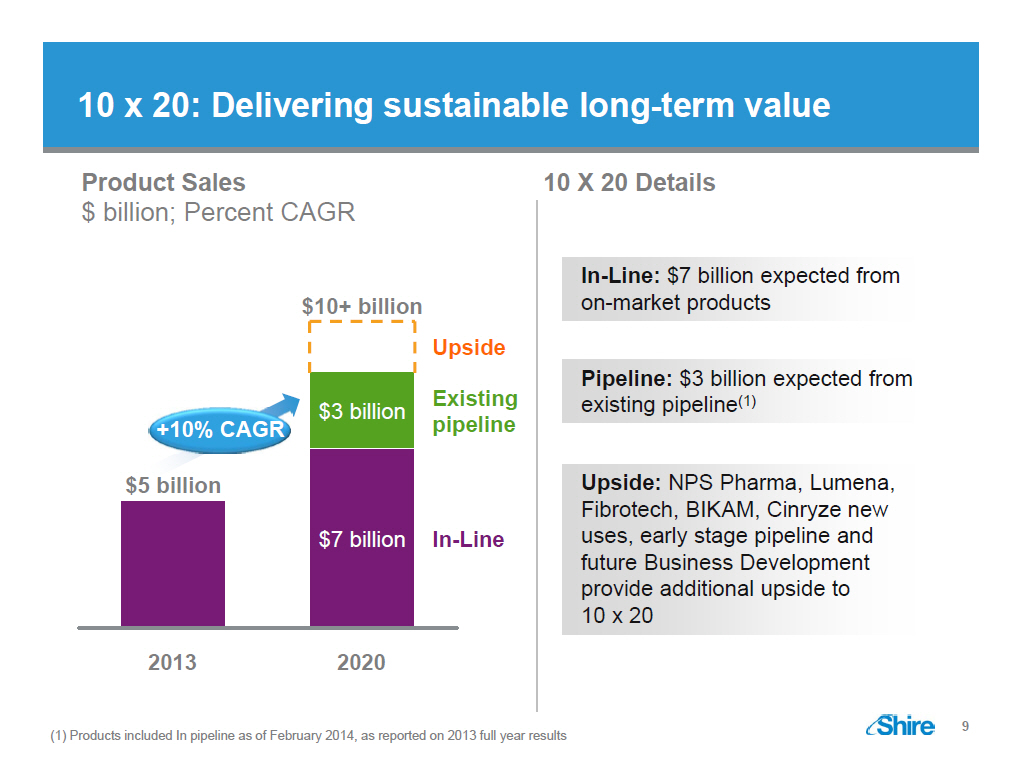

10 x 20: Delivering sustainable long-term value

Product Sales

$ billion; Percent CAGR

$10+ billion Upside

Existing $3 billion

+10% CAGR pipeline $5 billion $7 billion In-Line

2013 2020

10 X 20 Details

In-Line: $7 billion expected from

on-market products

Pipeline: $3 billion expected from

existing pipeline (1)

Upside: NPS Pharma, Lumena,

Fibrotech, BIKAM, Cinryze new

uses, early stage pipeline and

future Business Development

provide additional upside to

10 x 20

(1) Products included In pipeline as of February 2014, as

reported on 2013 full year results

[GRAPHIC OMITTED]

9

|  |

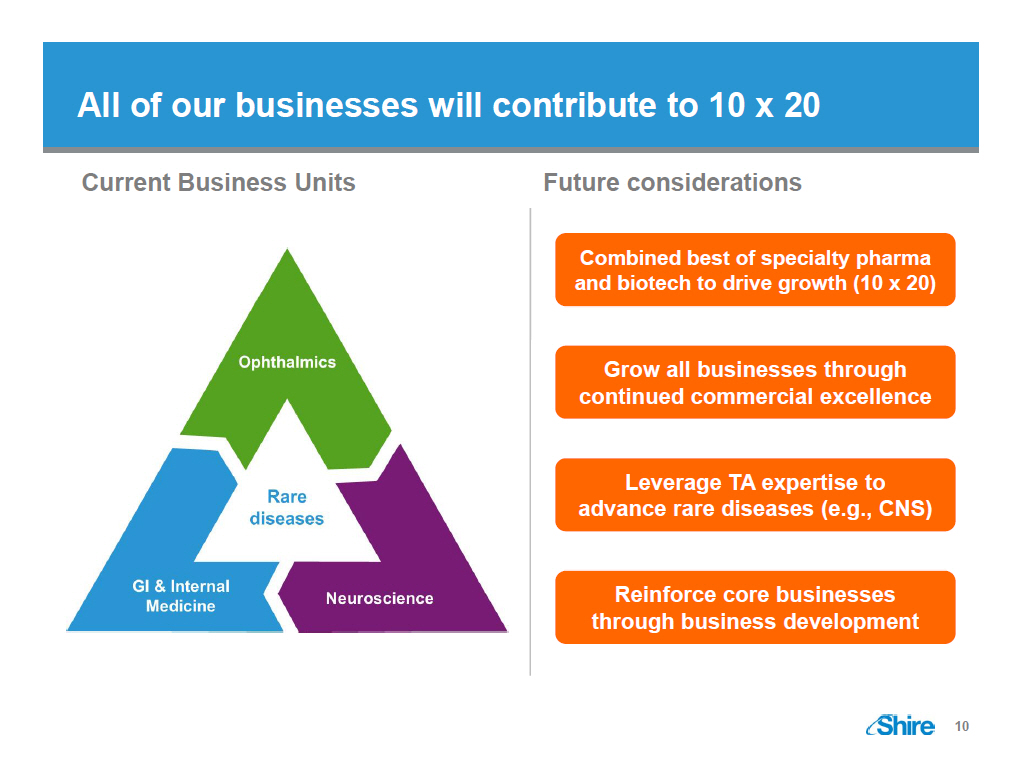

All of our businesses will contribute to 10 x 20 Current Business Units [GRAPHIC OMITTED] Future considerations Combined best of specialty pharma and biotech to drive growth (10 x 20) Grow all businesses through continued commercial excellence Leverage TA expertise to advance rare diseases (e.g., CNS) Reinforce core businesses through business development [GRAPHIC OMITTED] 10 |  |

Shire and NPS Pharma -- Leadership in rare diseases Shire is acquiring NPS Pharma, a significant step on our journey to become a leading biotechnology company Building on NPS Pharma's success, we will use our GI market expertise, rare disease patient identification and management capabilities, and global footprint to deliver NPS Pharma's products to patients worldwide The transaction will enhance Shire's growth profile and is expected to be accretive to Non GAAP EPS from 2016 onward [GRAPHIC OMITTED] 11 |  |

NPS Pharma is a biopharmaceutical company focused on rare diseases [GRAPHIC OMITTED] History * Founded in 1986, with an early focus on osteoporosis and thyroid disorders * Acquired Allelix Pharmaceuticals in 1999 to specialize in rare disease with first-in or best-in-class disease therapies Key Products * GATTEX ([R])/REVESTIVE ([R]) (teduglutide) for the treatment of short bowel syndrome (SBS), a rare GI condition, launched in the U.S. (Q1 2013), and Europe (Q3 2014) * NATPARA ([R])/NATPAR ([R]) (recombinant parathyroid hormone) for the treatment of hypoparathyroidism (HPT), a rare endocrine disease, in registration phase in the U.S. and EU General Facts * NASDAQ listed (NASDAQ: NPSP) * Headquarters: Bedminster, NJ, U.S. * Operations in the U.S., Canada, Europe, Latin America, and Japan * More than 350 employees Note: Gattex[R] / Revestive[R] and Natpara[R] / Natpar[R] are copyrights of NPS Pharma [GRAPHIC OMITTED] 12 |  |

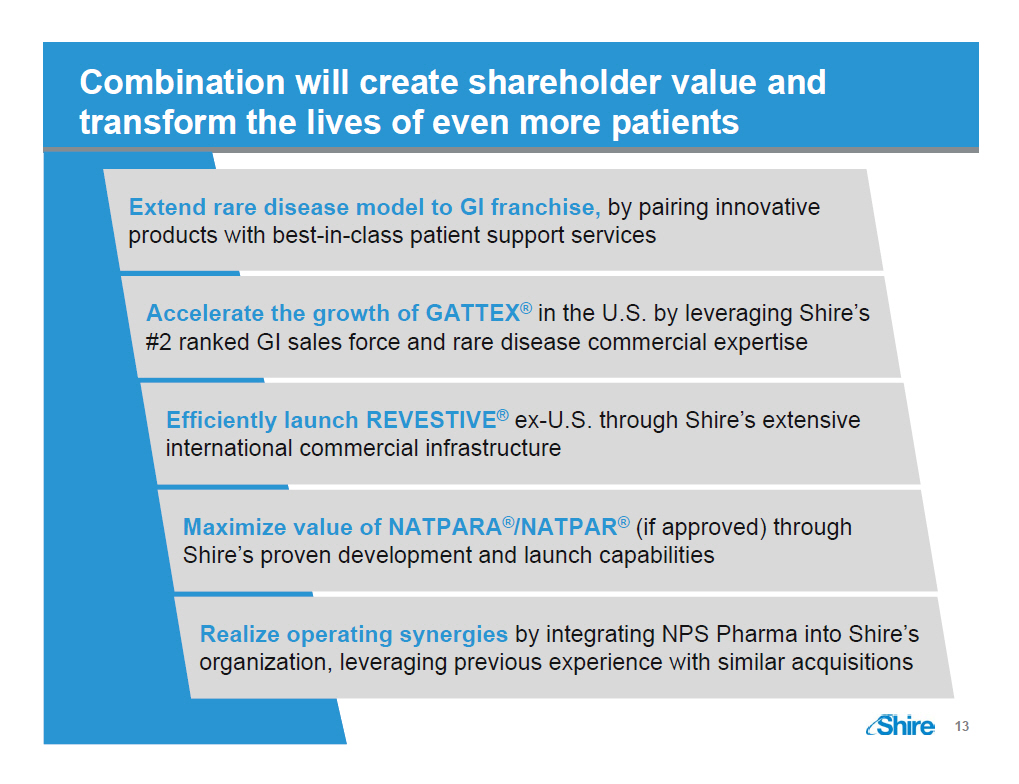

Combination will create shareholder value and transform the lives of even more patients Extend rare disease model to GI franchise, by pairing innovative products with best-in-class patient support services Accelerate the growth of GATTEX ([R]) in the U.S. by leveraging Shire's #2 ranked GI sales force and rare disease commercial expertise Efficiently launch REVESTIVE ([R]) ex-U.S. through Shire's extensive international commercial infrastructure Maximize value of NATPARA ([R])/NATPAR ([R]) (if approved) through Shire's proven development and launch capabilities Realize operating synergies by integrating NPS Pharma into Shire's organization, leveraging previous experience with similar acquisitions [GRAPHIC OMITTED] 13 |  |

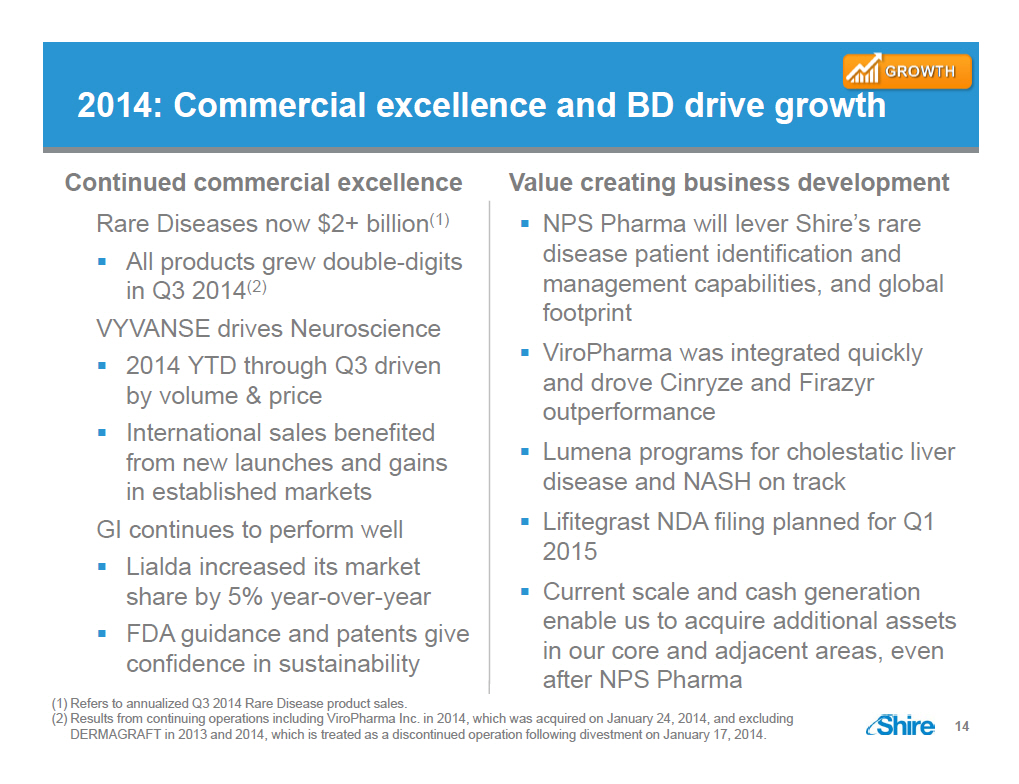

2014: Commercial excellence and BD drive growth Continued commercial excellence Rare Diseases now $2+ billion(1) * All products grew double-digits in Q3 2014(2) VYVANSE drives Neuroscience * 2014 YTD through Q3 driven by volume and price * International sales benefited from new launches and gains in established markets GI continues to perform well * Lialda increased its market share by 5% year-over-year * FDA guidance and patents give confidence in sustainability Value creating business development * NPS Pharma will lever Shire's rare disease patient identification and management capabilities, and global footprint * ViroPharma was integrated quickly and drove Cinryze and Firazyr outperformance * Lumena programs for cholestatic liver disease and NASH on track * Lifitegrast NDA filing planned for Q1 2015 * Current scale and cash generation enable us to acquire additional assets in our core and adjacent areas, even after NPS Pharma (1) Refers to annualized Q3 2014 Rare Disease product sales. (2) Results from continuing operations including ViroPharma Inc. in 2014, which was acquired on January 24, 2014, and excluding DERMAGRAFT in 2013 and 2014, which is treated as a discontinued operation following divestment on January 17, 2014. [GRAPHIC OMITTED] 14 |  |

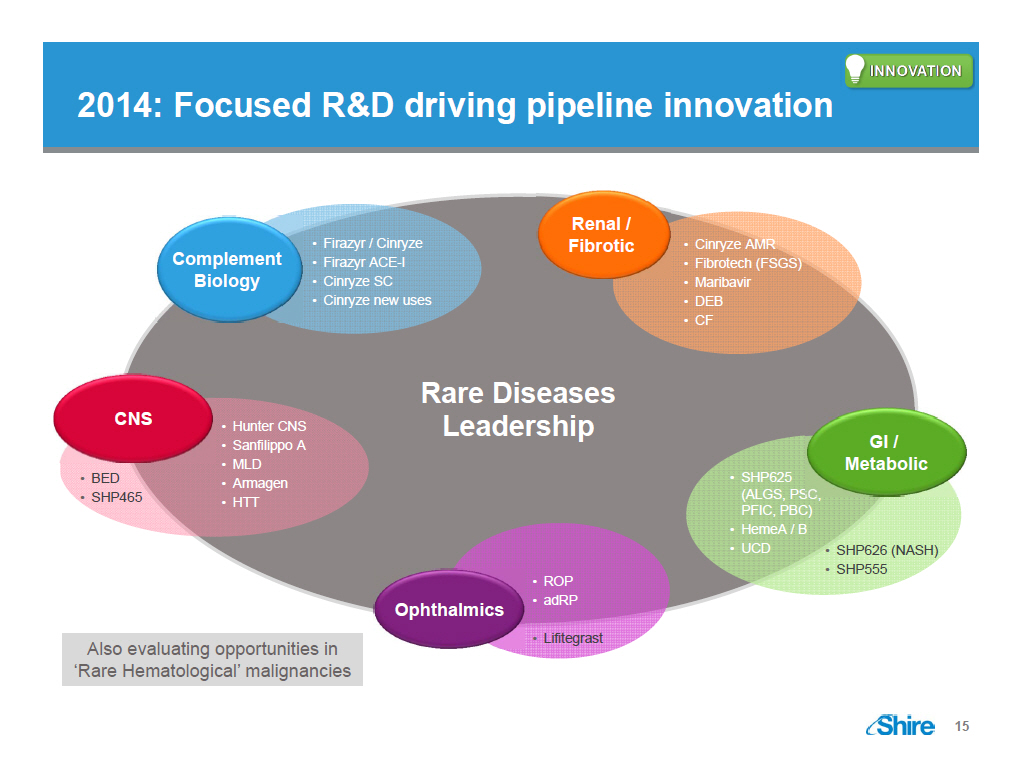

2014: Focused RandD driving pipeline innovation [GRAPHIC OMITTED] [GRAPHIC OMITTED] [GRAPHIC OMITTED] 15 |  |

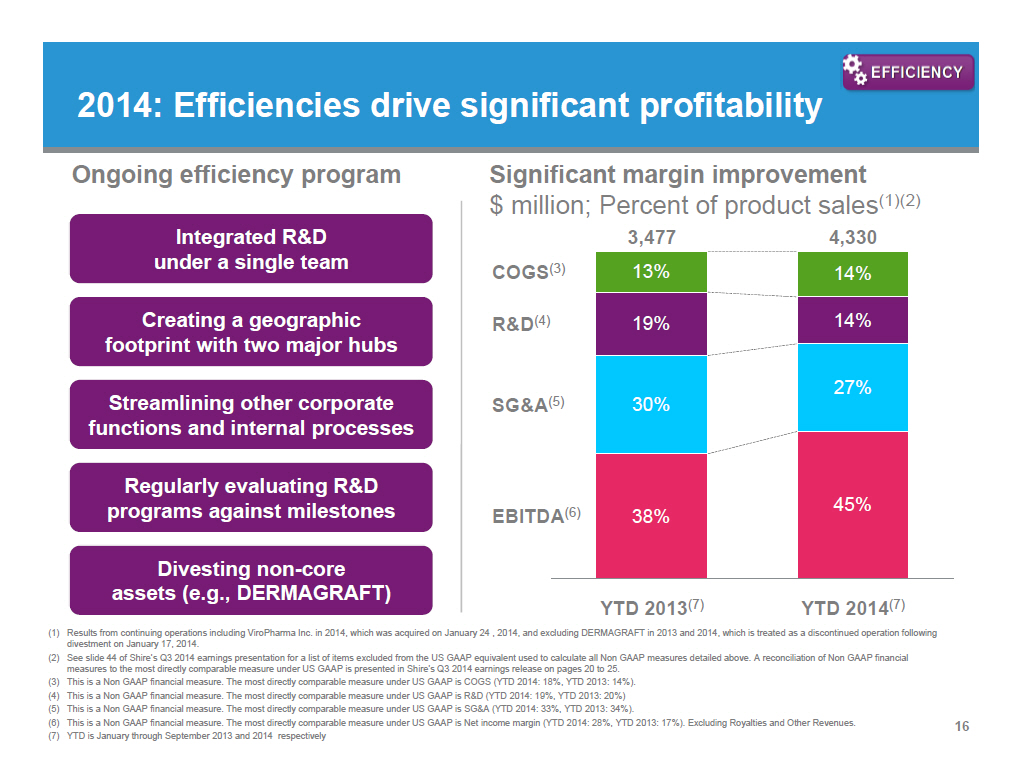

2014: Efficiencies drive significant profitability [GRAPHIC OMITTED] Ongoing efficiency program Integrated RandD under a single team Creating a geographic footprint with two major hubs Streamlining other corporate functions and internal processes Regularly evaluating RandD programs against milestones Divesting non-core assets (e.g., DERMAGRAFT) Significant margin improvement $ million; Percent of product sales(1)(2) [GRAPHIC OMITTED] (1) Results from continuing operations including ViroPharma Inc. in 2014, which was acquired on January 24 , 2014, and excluding DERMAGRAFT in 2013 and 2014, which is treated as a discontinued operation following divestment on January 17, 2014. (2) See slide 44 of Shire's Q3 2014 earnings presentation for a list of items excluded from the US GAAP equivalent used to calculate all Non GAAP measures detailed above. A reconciliation of Non GAAP financial measures to the most directly comparable measure under US GAAP is presented in Shire's Q3 2014 earnings release on pages 20 to 25. (3) This is a Non GAAP financial measure. The most directly comparable measure under US GAAP is COGS (YTD 2014: 18%, YTD 2013: 14%). (4) This is a Non GAAP financial measure. The most directly comparable measure under US GAAP is RandD (YTD 2014: 19%, YTD 2013: 20%) (5) This is a Non GAAP financial measure. The most directly comparable measure under US GAAP is SGandA (YTD 2014: 33%, YTD 2013: 34%). (6) This is a Non GAAP financial measure. The most directly comparable measure under US GAAP is Net income margin (YTD 2014: 28%, YTD 2013: 17%). Excluding Royalties and Other Revenues. (7) YTD is January through September 2013 and 2014 respectively 16 |  |

[GRAPHIC OMITTED] 2014: Enhanced our committed and focused team Managed uncertainty of 2014 Turnover consistent with historical levels Hired ~1,000 employees Issued retention to key employees to ensure business stability Organization continued to deliver Hiring for the future [GRAPHIC OMITTED] [GRAPHIC OMITTED] [GRAPHIC OMITTED] 17 |  |

2014: On track to meet product sales and earnings guidance Continued execution Delivering results On track to meet 2014 product sales and earnings guidance [GRAPHIC OMITTED] 18 |  |

2015: Mix of top-line opportunities and challenges [GRAPHIC OMITTED] Opportunities Launching VYVANSE for BED (pending regulatory approval GATTEX product sales, NATPARA launch (if approved), and other NPS Pharma royalty streams Future BD opportunities in our core / adjacent TAs Challenges ViroPharma YOY comparables INTUNIV generic (Dec-14) Foreign exchange headwinds [GRAPHIC OMITTED] 19 |  |

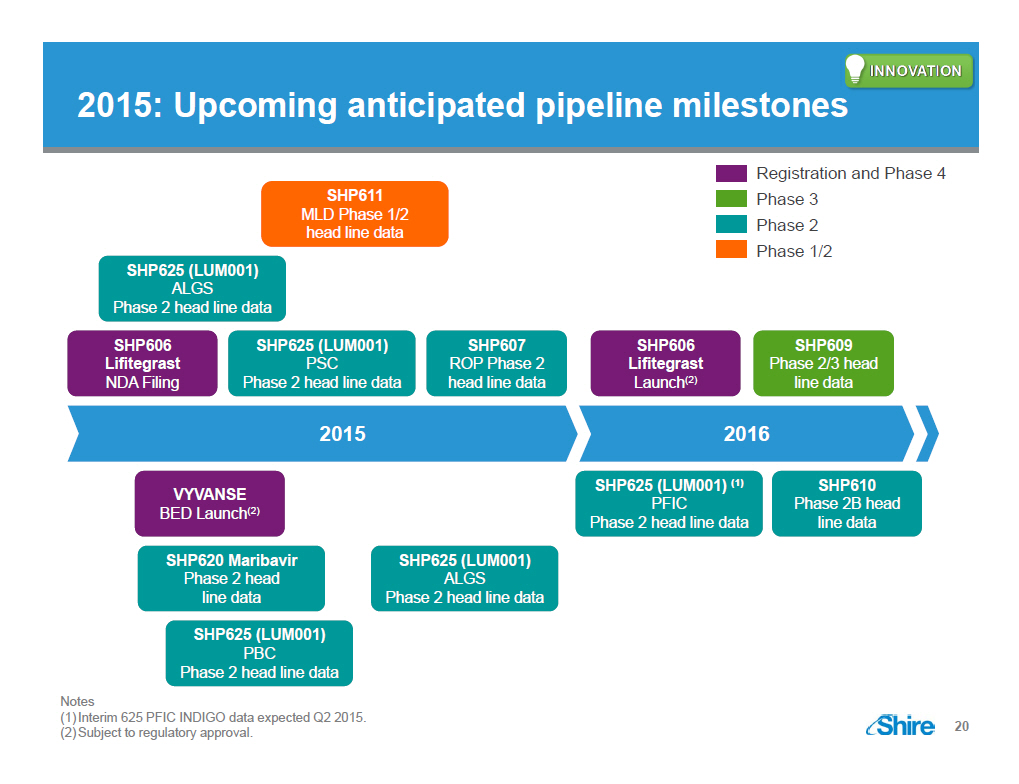

[GRAPHIC OMITTED] 2015: Upcoming anticipated pipeline milestones Registration and Phase 4 Phase 3 Phase 2 Phase 1/2 SHP611 MLD Phase 1/2 head line data SHP625 (LUM001) ALGS Phase 2 head line data SHP606 Lifitegrast NDA Filing SHP625 (LUM001) PSC Phase 2 head line data SHP607 ROP Phase 2 head line data SHP606 Lifitegrast Launch (2) SHP609 Phase 2/3 head line data 2015 VYVANSE BED Launch (2) SHP620 Maribavir Phase 2 head line data SHP625 (LUM001) PBC Phase 2 head line data SHP625 (LUM001) ALGS Phase 2 head line data 2016 SHP625 (LUM001) (1) PFIC Phase 2 head line data SHP610 Phase 2B head line data Notes (1)Interim 625 PFIC INDIGO data expected Q2 2015. (2)Subject to regulatory approval. [GRAPHIC OMITTED] 20 |  |

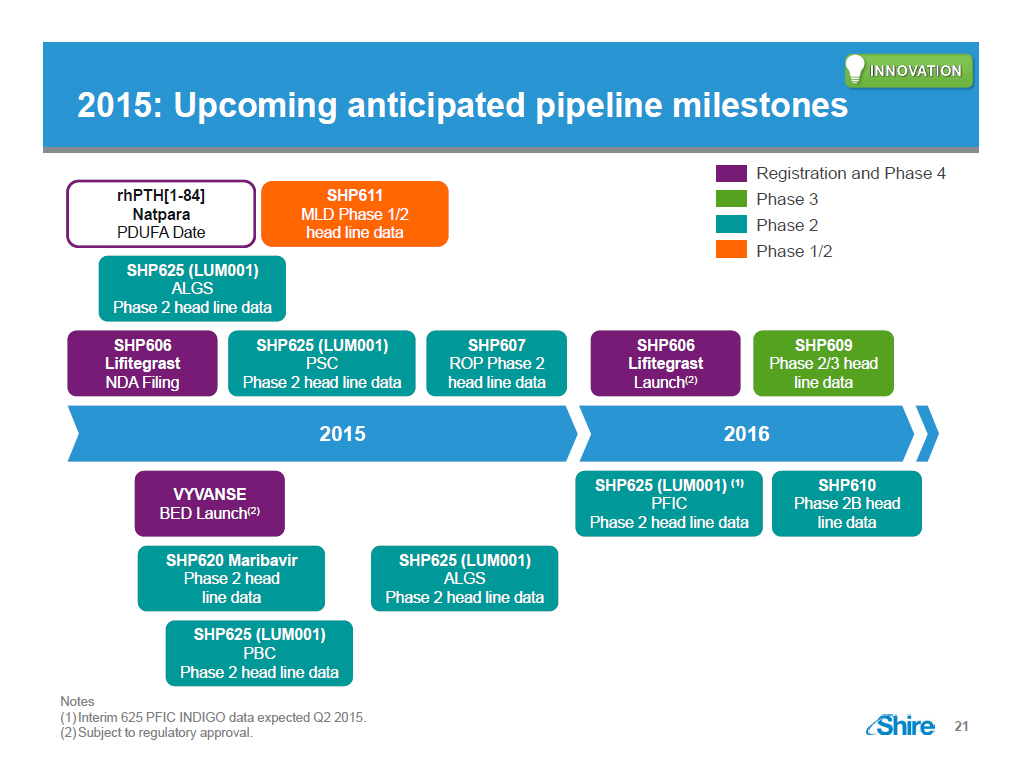

[GRAPHIC OMITTED] 2015: Upcoming anticipated pipeline milestones Registration and Phase 4 Phase 3 Phase 2 Phase 1/2 rhPTH[1 -84] Natpara PDUFA Date SHP625 (LUM001) ALGS Phase 2 head line data SHP611 MLD Phase 1/2 head line data SHP606 Lifitegrast NDA Filing SHP625 (LUM001) PSC Phase 2 head line data SHP607 ROP Phase 2 head line data SHP606 Lifitegrast Launch (2) SHP609 Phase 2/3 head line data 2015 VYVANSE BED Launch (2) SHP620 Maribavir Phase 2 head line data SHP625 (LUM001) PBC Phase 2 head line data SHP625 (LUM001) ALGS Phase 2 head line data 2016 SHP625 (LUM001) (1) PFIC Phase 2 head line data SHP610 Phase 2B head line data Notes (1)Interim 625 PFIC INDIGO data expected Q2 2015. (2)Subject to regulatory approval. [GRAPHIC OMITTED] 21 |  |

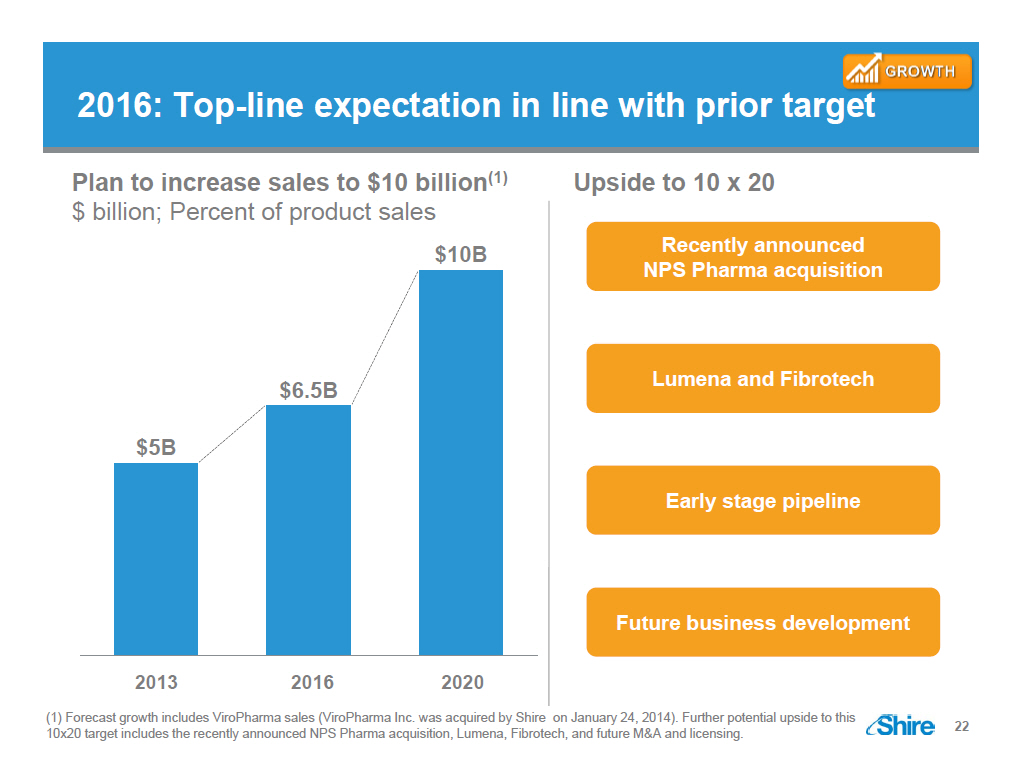

2016: Top-line expectation in line with prior target [GRAPHIC OMITTED] Plan to increase sales to $10 billion(1) $ billion; Percent of product sales [GRAPHIC OMITTED] Upside to 10 x 20 Recently announced NPS Pharma acquisition Lumena and Fibrotech Early stage pipeline Future business development (1) Forecast growth includes ViroPharma sales (ViroPharma Inc. was acquired by Shire on January 24, 2014). Further potential upside to this 10x20 target includes the recently announced NPS Pharma acquisition, Lumena, Fibrotech, and future MandA and licensing. [GRAPHIC OMITTED] 22 |  |

The journey continues 2013: Ready for change * Mix of specialty / biotech * Low-single digit growth(1) * High 30's EBITDA margins * Dispersed RandD spend * Undifferentiated pipeline * Inefficient geographic footprint 2014: Building momentum * Enhancing biotech capabilities * Double -digit growth(2) * Mid 40's EBITDA margins (2) * Focused RandD spend * Emerging pipeline * Transitioning footprint Future aspiration: 10 x 20 * Leading biotech focused on rare diseases * Sustained double-digit growth * Mid 40's EBITDA margins * Innovative pipeline sourced internally and externally * Focused geographic footprint Acquisition of NPS * Significant step in building a leading biotech * Combine Shire's GI market expertise, rare disease patient identification and management capabilities, and global footprint * Enhances short and long-term revenue and earnings growth (1) Refers to Q1 2013 year-over-year product sales growth from continuing operations excluding DERMAGRAFT which is treated as a discontinued operation following divestment on January 17, 2014 (2) Refers to Q1 through Q3 2014 from continuing operations including ViroPharma Inc., which was acquired on January 24, 2014, and excluding DERMAGRAFT, which is treated as a discontinued operation following divestment on January 17,2014 |  |

QandA breakout [GRAPHIC OMITTED] |  |