Table of Contents

Table of Contents

WASHINGTON FEDERAL, INC.

ANNUAL REPORT 2010

425 Pike Street, Seattle, WA 98101

| 1 | ||||

| 2 | ||||

Management’s Discussion and Analysis of Financial | 5 | |||

| 14 | ||||

| 15 | ||||

| 20 | ||||

Management’s Report on | 44 | |||

| 44 | ||||

| 46 | ||||

| 47 | ||||

| 48 |

A SHORT HISTORY

Washington Federal, Inc. (Company or Washington Federal) is a unitary thrift holding company headquartered in Seattle, Washington. Its principal subsidiary is Washington Federal Savings, which operates 160 offices in eight western states.

The Company had its origin on April 24, 1917, as Ballard Savings and Loan Association. In 1935, the state-chartered Company converted to a federal charter, became a member of the Federal Home Loan Bank (FHLB) system and obtained federal deposit insurance. In 1958, Ballard Federal Savings and Loan Association merged with Washington Federal Savings and Loan Association of Bothell, and the latter name was retained for wider geographical acceptance. In 1971, Seattle Federal Savings and Loan Association, with three offices, merged into the Company, and at the end of 1978, was joined by the 10 offices of First Federal Savings and Loan Association of Mount Vernon.

On November 9, 1982, the Company converted from a federal mutual to a federal stock association. In 1987 and 1988, acquisitions of United First Federal, Provident Federal Savings and Loan, and Northwest Federal Savings and Loan, all headquartered in Boise, Idaho, added 28 Idaho offices to the Company. In 1988, the acquisition of Freedom Federal Savings and Loan Association in Corvallis, Oregon, added 13 Oregon offices, followed in 1990 by the eight Oregon offices of Family Federal Savings.

In 1991, the Company added three branches with the acquisition of First Federal Savings and Loan Association of Idaho Falls, Idaho, and acquired the deposits of First Western Savings Association of Las Vegas, Nevada, in Portland and Eugene, Oregon, where they were doing business as Metropolitan Savings Association. In 1993, 10 branches were added with the acquisition of First Federal Savings Bank of Salt Lake City, Utah. In 1994, the Company expanded into Arizona.

In 1995, the stockholders approved a reorganization whereby Washington Federal Savings became a wholly owned subsidiary of a newly formed holding company, Washington Federal, Inc. That same year, the Company purchased West Coast Mutual Savings Bank with its one branch in Centralia, Washington, and opened six additional branches. In 1996, the Company acquired Metropolitan Bancorp of Seattle, adding eight offices in Washington in addition to opening four branches in existing markets. Between 1997 and 1999, Washington Federal Savings continued to develop its branch network, opening a total of seven branches and consolidating three offices into existing locations.

In 2000, the Company expanded into Las Vegas, opening its first branch in Nevada along with two branches in Arizona. In 2001, the Company opened two additional branches in Arizona and its first branch in Texas with an office in the Park Cities area of Dallas. In 2002, Washington Federal Savings opened five full-service branches in existing markets. In 2003, the Company purchased United Savings and Loan Bank with its four branches in the Seattle metropolitan area, added one new branch in Puyallup, Washington, and consolidated one branch in Nampa, Idaho. In 2005, the Company consolidated two branches in Mount Vernon, Washington, into one and opened branches in Plano, Texas, and West Bend, Oregon. In 2006, the Company opened locations in Klamath Falls, Oregon, Richardson, Texas and another in Las Vegas, Nevada. During 2006, a branch in Medford, Oregon, was opened.

The Company acquired First Federal Banc of the Southwest, Inc., the holding company for First Federal Bank located in Roswell, New Mexico, on February 13, 2007. First Federal Bank had 13 branch locations, 11 in New Mexico and two in El Paso, Texas. The Company acquired First Mutual Bancshares, Inc. (“First Mutual”), the holding company for First Mutual Bank, on February 1, 2008. First Mutual had 12 branches primarily located in the eastside of Seattle. The Company also opened a location in Redmond, Oregon in 2008. During 2009, the Company opened two new locations, one in Las Vegas, Nevada and the other in Prescott Valley, Arizona.

On January 8, 2010, the Company acquired certain assets and liabilities, including most of the loans and deposits, of Horizon Bank, headquartered in Bellingham, Washington (“Horizon”) from the Federal Deposit Insurance Corporation (“FDIC”), as receiver for Horizon. Horizon operated eighteen full-service offices, four commercial loan centers and four real estate loan centers in Washington. Through consolidation with existing Washington Federal branches, there was a net increase of 10 branches as a result of the Horizon acquisition.

The Company obtains its funds primarily through deposits from the general public, from repayments of loans, borrowings and retained earnings. These funds are used largely to make loans to individuals and business for the purchase of new and existing homes, construction and land loans, commercial real estate, commercial and industrial loans, and for investments.

Table of Contents

| September 30, | 2010 | 2009 | % Change | |||||||||

| (In thousands, except per share data) |

| ||||||||||

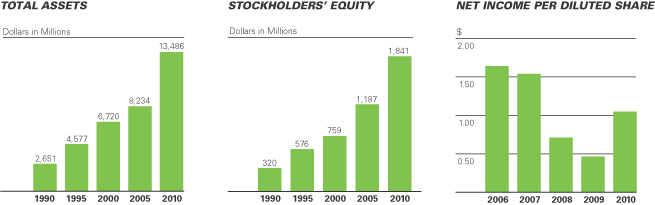

Assets | $ | 13,486,379 | $ | 12,582,475 | 7 | % | ||||||

Cash and cash equivalents | 888,622 | 498,388 | 78 | |||||||||

Investment securities | 358,061 | 21,259 | 1,584 | |||||||||

Loans receivable, net | 8,423,703 | 8,983,430 | -6 | |||||||||

Covered loans, net | 534,474 | 0 | — | |||||||||

Mortgage-backed securities | 2,203,139 | 2,282,865 | -3 | |||||||||

Customer accounts | 8,852,540 | 7,842,310 | 13 | |||||||||

FHLB advances and other borrowings | 2,665,548 | 2,879,530 | -7 | |||||||||

Stockholders’ equity | 1,841,147 | 1,745,485 | 5 | |||||||||

Net income available to common shareholders | 118,653 | 40,684 | 192 | |||||||||

Diluted earnings per share | 1.05 | 0.46 | 128 | |||||||||

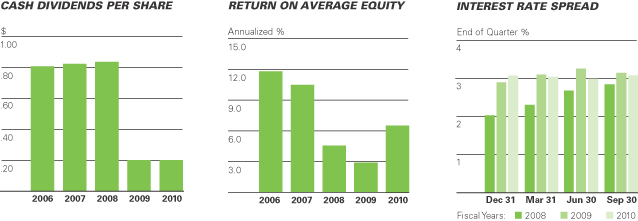

Dividends per share | 0.20 | 0.20 | — | |||||||||

Stockholders’ equity per share | 16.37 | 15.55 | 5 | |||||||||

Shares outstanding | 112,484 | 112,248 | NM | |||||||||

Return on average stockholders’ equity | 6.55 | % | 2.87 | % | NM | |||||||

Return on average assets | 0.89 | 0.33 | NM | |||||||||

Efficiency ratio (1) | 26.26 | 27.30 | NM | |||||||||

| (1) | Calculated as total operating costs divided by net interest income, plus other income (excluding Investment gains and FHLB prepayment fee) |

NM – not meaningful

| 1 |

Table of Contents

Fellow Stockholder:

It is my privilege to advise you that last fiscal year was a successful one. Net income for our company amounted to $118,653,000, an increase of 192% over the $40,684,000 recorded in the prior year. Two extraordinary items, a $54.8 million after tax gain on the acquisition of certain assets and liabilities of the former Horizon Bank, and the recapture of $39 million related to a contingent federal tax liability, delivered a welcome boost to earnings from normal operations that were weakened by the high cost of resolving problem loans. In a year that saw the highest number of bank failures in nearly 20 years, we are delighted and somewhat relieved to close the books on fiscal 2010 and report such positive results.

For generations the management of Washington Federal has worked to develop a reputation as a business built upon integrity, with a fortress financial condition and a culture of treating clients fairly. This substantial effort brought real rewards during the year as business gravitated to us because we were viewed as a safe harbor and a good place to do business. Our strong financial position also enabled the company to gain market share at a very reasonable price through the FDIC-assisted acquisition of the aforementioned Horizon Bank, a $1.1 billion institution with 18 branches that was headquartered in Bellingham, Washington. The integration of a failed institution is not without trauma for their employees and clients and we lost a few good ones in each category along the way. For those who remained loyal and worked with us through a challenging time, we cannot thank you enough. We are intensely committed to proving that you made a good decision.

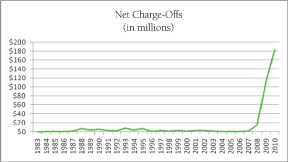

On the financial management front, the company’s capital and liquidity positions were already world-class, so the focus last year was on the disposition of problem assets and positioning the balance sheet for changing interest rates. Regarding problem assets, we center attention on what are known in the industry as Non-Performing Assets (“NPA’s”), comprised of loans on which interest is no longer being accrued plus assets acquired through foreclosure. Such assets peaked in June 2009 at $606 million and have declined each quarter since, ending September 2010 at $435 million, representing a decline of 28%. This is good news and we expect the trend to continue. The adjacent chart, though, shows in a dramatic way that much of the reduction in NPA’s came as a result of write-offs, which have skyrocketed since the begin ning of the so-called Great Recession, brought on by the bursting of the housing bubble. The combination of a concentration in residential real estate, declining home values and high unemployment, meant that there was simply no way for the company to avoid losses. Yet the overall performance of the company under such dire circumstances is a real testament to the strength of the institution and should give investors confidence that it can survive just about any economic calamity. As with NPA’s, management believes that the worst is behind us and that we have experienced the peak in asset writedowns for this credit cycle. Fiscal 2011 should see considerable improvement in that area.

Interest rate risk, defined as the impact on earnings of a change in interest rates, is an area where management is less confident in its ability to forecast events. In fact, there may never have been a time at which it’s been so easy to make the convincing case for both inflationary and deflationary scenarios. In the end though, because the company is heavily invested in 30 year fixed rate mortgages, the deeper concern is with rising interest rates brought on by inflationary expectations, so it is against that greater risk that we are fortifying the company. We do so primarily by shortening the maturities of assets – allowing mortgage loans to refinance elsewhere, for example, increasing investment in short-term or floating rate assets, increasing cash which can be invested at higher rates in the future, and maintaining high levels of capital that can be leveraged in the future to offset any decline in margin. Management has also locked in long-term financing to the maximum extent that it deems prudent, given that there remains a strong case for low rates to continue for a considerable period of time. The result of these moves collectively has been to reduce the interest rate risk posture of the company. Earnings in the near-term will be lower as a result, because we make money by taking risk and we are consciously avoiding interest rate risk today. We view this as an investment in the future, similar to the premiums paid on an insurance policy. As always, we’re willing to leave a little on the table today to make certain that we prosper in the future.

| 2 | . |

Table of Contents

The Company completed its rebranding during the year, and for the first time in years, the same sign now hangs over all of our offices. The name was shortened to that which we are known by anyway and to reflect the slightly broader product line. The “invested here” tagline bubbled up from within the soul of the company and conveys the notion that we are absolutely committed to the long-term best interests of our clients, owners, employees and the neighborhoods and businesses we serve. Although we still believe that this is a business built upon relationships developed one at a time, we spent a bit of money on advertising during the year to reinforce the new brand and increase name recognition; hopefully, you noticed. |  | |

| (Back row - from left to right) Thomas E. Kasanders, Executive Vice President, Linda S. Brower, Executive Vice President, Mark A. Schoonover, Executive Vice President and Chief Credit Officer, Angela D. Veksler, Senior Vice President and Chief Information Officer (Front row - from left to right) Jack B. Jacobson, Executive Vice President, Roy M. Whitehead, Chairman, President and Chief Executive Officer, Edwin C. Hedlund, Executive Vice President and Secretary, Brent J. Beardall, Executive Vice President and Chief Financial Officer. |

Each passing year brings more dependence on information technology. In recognition of that reality, we advised you two years ago that the company had embarked upon a major upgrade to its systems. At this writing, I am pleased to report that Project Tritan, the rewrite of our in-house core operating system, is complete and that after converting three acquired companies to the system in the past seven months, the entire company is once again operating on a single system. Hardware throughout the company has also been upgraded to a single standard, while IT governance practices, information security and business continuity plans have also been enhanced. In August, we added the Chief Information Officer position to the executive management team in recognition of the growing importance of this part of the business.

Other than loan-related losses, the most consequential setback during the year was a management failure to meet the expectations of the company’s primary regulator regarding certain business processes. What management regarded as elegantly simple and pragmatic, the regulators regarded as uncommonly sparse. We bowed to their requirements and the resulting memorandum of understanding was detailed in a voluntary public disclosure at the time it was signed. Over the past ninety days the company has, or shortly will have, completed all agreed upon tasks. Higher costs and increased operational complexity will be traded off for the benefit of more detailed management of certain risks. The company will also be easier to examine in the future because its processes will align more closely with regulator expectations and be more fully documented.

Looking to the new fiscal year, we are optimistic that better times lie ahead, yet continue to advise investors to be realistic in their expectations. This is not due to concerns about our own company, but to fundamental changes in the business environment which affect our cost structure, profit margins, and attitude toward risk that will take some time to correct. Chief concerns include an economy that is likely to be slow-growth at best with ongoing high unemployment, the enormously imbalanced financial condition of government at all levels, ultralow interest rates that reduce earnings on capital and limit our appetite for investing, continued softness in the housing market, the increase in regulatory burden and change in primary regulators required by the populist Dodd-Frank bill, and continued overcapacity in financial services despite the ongoing industry shakeout. We also continue to be concerned about changing social attitudes toward personal responsibility for credit; namely, the so-called “strategic defaults” that see those able to pay simply decide not to. It’s always surprising to hear financial planners, economists or government officials speak of it so casually as being rational or to be expected, because like insurance fraud or shoplifting, in our view it is unethical and irresponsible behavior that in the end will raise costs for everyone and devalue us as a society. At the same time, investors and the public should know that Washington Federal has voluntarily modified 1,274 mortgage loans, or 3% of our total mortgage loans, for families

| 3 |

Table of Contents

TO OUR STOCKHOLDERS(CONTINUED)

that have fallen on hard times and simply need a temporary hand-up. Each of those borrowers remains in good standing with us and we’re very pleased to be able to help because it’s the right thing to do and because it’s good business.

The economic dark clouds overhead don’t fully obscure the sun though, and we see many opportunities. Washington Federal is currently the largest financial institution headquartered in the Pacific Northwest. With one of the strongest capital positions in the industry, solid earnings prospects, an updated operating structure and a solid reputation, we are well positioned to take advantage of opportunities that come our way. In 2011, management intends to refocus the company on external opportunities. While we prefer to grow the company one good client at a time, the company is also postured to acquire if that opportunity presents. As always, you can help by referring your friends, neighbors and business acquaintances to Washington Federal for their banking needs.

In closing, I’d like to thank the Board of Directors, the Executive Management Committee and all of our hard-working and loyal employees for their contributions during the year. The IT staff and those involved in the disposition of problem assets deserve special recognition. Most importantly, I’d like to end this letter by advising you as a stockholder that we never forget that we work for you and by thanking you for entrusting us with your investment.

I look forward to seeing you at the Annual Meeting of Stockholders to be held at 2:00 pm, on January 19, 2011 at Benaroya Hall in downtown Seattle.

Sincerely,

Roy M. Whitehead

Chairman, President and Chief Executive Officer

| 4 | . |

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

This Annual Report on Form 10-K and the documents into which it may be incorporated by reference may contain, and from time to time our management may make, certain statements that constitute forward-looking statements. Words such as “expects,” “anticipates,” “believes,” “estimates” and other similar expressions or future or conditional verbs such as “will,” “should,” “would” and “could” are intended to identify such forward-looking statements. These statements are not historical facts, but instead represent the current expectations, plans or forecasts of the Company and are based on the beliefs and assumptions of the management of the Company and the information available to management at the time that these disclosures were prepared. The Company intends for all such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 and the provisions of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These statements are not guarantees of future results or performance and involve certain risks, uncertainties and assumptions that are difficult to predict and often are beyond the Company’s control. Actual outcomes and results may differ materially from those expressed in, or implied by, the Company’s forward-looking statements.

You should not place undue reliance on any forward-looking statement and should consider the following uncertainties and risks, as well as the risks and uncertainties discussed elsewhere in this report, including under Item 1A. “Risk Factors,” and in any of the Company’s other subsequent Securities and Exchange Commission filings:

| • | the Bank’s ability to comply with the terms of its memorandum of understanding with the OTS |

| • | negative economic conditions, including sharp declines in the real estate market, home sale volumes and financial stress on borrowers as a result of the uncertain economic environment, that adversely affect our borrowers and their customers, and may adversely affect our financial condition and results of operations; |

| • | the severe effects of the continued economic downturn, including high unemployment rates and severe declines in housing prices and property values, in our primary market areas; |

| • | fluctuations in interest rate risk and changes in market interest rates, which may negatively affect the Company’s results of operations and financial conditions; |

| • | the Company’s ability to make accurate assumptions and judgments about the collectability of its loan portfolio, including the creditworthiness of its borrowers and the value of the assets securing these loans; |

| • | legislative and regulatory limitations, including those arising under the Dodd-Frank Wall Street Reform Act and potential limitations in the manner in which we conduct our business and undertake new investments and activities; |

| • | changes in other economic, competitive, governmental, regulatory, and technological factors affecting the Company’s markets, operations, pricing, products, services and fees; and |

| • | the timing and occurrence or non-occurrence of events that may be subject to circumstances beyond the Company’s control. |

All forward-looking statements speak only as of the date on which such statements are made, and Washington Federal undertakes no obligation to update or revise any forward-looking statements to reflect changed assumptions, the occurrence of unanticipated events, changes to future operating results over time, or the impact of circumstances that arise after the date the forward-looking statement was made.

GENERAL | Washington Federal, Inc. (Company or Washington Federal) is a unitary thrift holding company. The Company’s primary operating subsidiary is Washington Federal Savings (Bank), a federally-chartered savings and loan association. |

The Company’s fiscal year end is September 30th. All references to 2010, 2009 and 2008 represent balances as of September 30, 2010, September 30, 2009, and September 30, 2008, or activity for the fiscal years then ended.

CRITICAL ACCOUNTING POLICIES | Preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires the use of estimates and assumptions that affect reported amounts of certain assets, liabilities, revenues and expenses in the Company’s consolidated financial statements. Accordingly, estimated amounts may fluctuate from one reporting period to another due to changes in assumptions underlying estimated values. |

| 5 |

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS(CONTINUED)

The Company has determined that the only accounting policy deemed critical to an understanding of the consolidated financial statements of Washington Federal relates to the methodology for determining the valuation of the allowance for loan losses, as described below.

The Company maintains an allowance for loan losses to absorb losses inherent in the loan portfolio. The allowance is based on ongoing, quarterly assessments of the probable and estimable losses inherent in the loan portfolio. The Company’s methodology for assessing the appropriateness of the allowance consists of several key elements, which include the general allowance and specific allowances.

The general loan loss allowance is established by applying a loss percentage factor to the different loan types. The allowance is provided based on Management’s continuing evaluation of the pertinent factors underlying the quality of the loan portfolio, including changes in the size and composition of the loan portfolio, actual loan loss experience, current economic conditions, collateral values, geographic concentrations, seasoning of the loan portfolio, specific industry conditions and the duration of the current business cycle. The recovery of the carrying value of loans is susceptible to future market conditions beyond the Company’s control, which may result in losses or recoveries differing from those provided.

Specific allowances are established for loans which are individually evaluated, in cases where Management has identified significant conditions or circumstances related to a loan that Management believes indicate the probability that a loss has been incurred.

INTEREST RATE RISK | The primary source of income for the Company is net interest income, which is the difference between the interest income generated by our interest-earning assets and the interest expense generated by our interest-bearing liabilities. The level of net interest income is a function of the average balances of our interest-earnings assets and liabilities, and the spread between the yield on such assets and the cost of such liabilities. These factors are influenced by both the pricing and mix of our interest-earning assets and our interest-bearing liabilities. If the interest rates on our interest-bearing liabilities increase at a faster pace than the interest rates on our interest-earning assets, the result could be a reduction in net interest income and with it, a reduction in our earnings. |

The Company accepts a higher level of interest rate volatility as a result of its significant holdings of fixed-rate single-family home loans that are longer-term than the short-term characteristics of its primary liabilities of customer accounts. As a result, assets do not respond as quickly to changes in interest rates as liabilities. As a result, Net interest income typically would decline when interest rates rise and would expand when interest rates fall as compared to a portfolio of matched maturities of assets and liabilities.

The Company manages its interest rate risk in part by originating more fixed-rate loans when yields are higher and adding loans and investments with shorter term characteristics, such as construction or commercial loans, when loan rates are lower. This balance sheet strategy, in conjunction with a strong capital position and low operating costs have allowed the Company to manage interest rate risk, within guidelines established by the Board of Directors, through all interest rate cycles. Although a significant increase in market interest rates could adversely affect net interest income of the Company, the Company’s interest rate risk approach has never resulted in the recording of a monthly operating loss.

The following table shows the estimated repricing periods for earning assets and paying liabilities.

| Repricing Period | ||||||||||||||||

| Within One Year | After 1 year - before 6 Years | Thereafter | Total | |||||||||||||

| (In thousands) | ||||||||||||||||

As of September 30, 2010 | ||||||||||||||||

Earning Assets * | $ | 3,270,289 | $ | 4,424,269 | $ | 4,865,189 | $ | 12,559,747 | ||||||||

Paying Liabilities | (7,075,460 | ) | (4,441,030 | ) | (1,597 | ) | (11,518,087 | ) | ||||||||

Excess (Liabilities) Assets | $ | (3,805,171 | ) | $ | (16,761 | ) | $ | 4,863,592 | ||||||||

Excess as % of Total Assets | -28.2 | % | ||||||||||||||

Policy limit for one year excess | -60.0 | % | ||||||||||||||

| * | Asset repricing period includes estimated prepayments based on historical activity |

At September 30, 2010, the Company had approximately $3.8 billion more liabilities subject to repricing in the next year than assets, which amounted to a negative maturity gap of 28% of total assets. As of September 30, 2009, the amount of excess liabilities subject to repricing within one year was approximately $4.1 billion, or 33%, of total assets. The decrease of approximately $333 million of liabilities in excess of assets repricing within one year was due to the increasing cash balances and deposit accounts moving into maturities beyond one year. By having an excess of liabilities repricing within one year over assets, the Company is subject to decreasing net interest income should interest rates rise. However, if the size and or mix of the balance sheet changes, rising rates may not cause a decrease in net interest income.

| 6 | . |

Table of Contents

The Company’s net interest spread decreased from 3.17% at September 30, 2009 to 3.09% at September 30, 2010. Net interest spread represents the difference between the contractual rates of earning assets and the contractual rates of paying liabilities as of a specific date. The spread decreased due to a higher proportion of lower yielding investment balances compared to total earning assets as deposit growth has exceeded loan growth. In addition, loan yields are lower as a result of refinancing of fixed-rate mortgages into historically low long-term interest rates. Rates on customer accounts decreased by 45 basis points over the prior year while rates on earning assets decreased by 54 basis points (see Period End Spread table below).

As of September 30, 2010, the Company had grown total assets by $903,904,000, or 7.2%, from $12,582,475,000 at September 30, 2009, including $1,133,589,000 in assets acquired on January 8, 2010 from the Horizon transaction described in Note A. For the year ended September 30, 2010, compared to September 30, 2009, loans (both non-covered and covered) decreased $25,253,000, or 0.3%, and investment securities increased $257,075,000, or 11.2%. Cash and cash equivalents of $888,622,000 and stockholders’ equity of $1,841,147,000 provides management with flexibility in managing interest rate risk going forward.

ASSET QUALITY & ALLOWANCE FOR LOAN LOSSES | The Company maintains an allowance to absorb losses inherent in the loan portfolio. The allowance is based on ongoing, quarterly assessments of the probable and estimable losses inherent in the loan portfolio. The Company’s methodology for assessing the appropriateness of the allowance consists of several key elements, which include the general allowance and specific allowances. |

The general portion of the loan loss allowance is established by applying a loss percentage factor to the different loan types. Management believes loan types are the most relevant factor to group loans for the allowance calculation as the risk characteristics in these groups are similar. The allowances are provided based on Management’s continuing evaluation of the pertinent factors underlying the quality of the loan portfolio, including changes in the size and composition of the loan portfolio, actual loan loss experience, current economic conditions, geographic concentrations, seasoning of the loan portfolio, specific industry conditions, and the duration of the current business cycle. The recovery of the carrying value of loans is susceptible to future market conditions beyond the Company’s control, which may result in losses or recoveries differing from those provided.

During 2009, the Company enhanced its general reserve allowance calculation to be reflective of the current economic environment. Changes included shortening the look-back period for determining historical loss factors “HLF” and modifying the methodology to give more weighting to risks by asset type rather than geographic exposure. In addition to utilizing the HLF to calculate the general reserve, we utilize a qualitative risk factor “QRF” which is determined by loan type and allows management to augment reserve levels to reflect the current environment and portfolio performance trends including recent charge off trends.

By shortening the look-back period the Company has taken into account the current housing environment where home values have declined substantially from the housing peak of 2007. We monitor delinquency trends as well as regional economic conditions including employment and housing values when determining the QRF. Washington Federal did not originate many of the “high risk” loan types, such as Option ARM or interest only long term loans, which have caused significant losses throughout the industry.

Specific allowances are established for loans which are individually evaluated; in cases where Management has identified significant conditions or circumstances related to a loan that Management believes indicate the probability that a loss has been incurred.

Loans for commercial purposes, including multi-family loans, builder construction loans and commercial loans are reviewed on an individual basis to assess the ability of the borrowers to continue to service all of their principal and interest obligations. If a loan shows signs of weakness, it is downgraded and, if warranted, placed on non-accrual status. Updated valuations are generally obtained from external sources on collateral dependent commercial loans when a loan exhibits weakness or is modified. The Company has an asset quality review function that reports the results of its internal reviews to the Board of Directors on a quarterly basis.

Restructured single-family residential loans are reserved for under the Company’s general reserve methodology. If any individual loan is significant in balance, the Company may establish a specific reserve as warranted.

Most restructured loans are accruing and performing loans where the borrower has proactively approached the Company about modifications due to temporary financial difficulties. Each request is individually evaluated for merit and likelihood of success. Single-family residential loans comprised 75.9% of restructured loans as of September 30, 2010. The concession for these loans is typically a payment reduction through a rate reduction of from 100 to 200 bps for a specific term, usually six to twelve months. Interest-only payments may also be approved during the modification period. The subsequent default rate on restructured single- family mortgage loans has been approximately 15% since inception of the program in November 2008. Concessions for construction (3.6%), land A&D (12.3%) and multi-family loans (4.7%) are typically an extension of maturity combined with a rate reduction of normally 100 bps. The subsequent default rate on restructured commercial loans has been less than 10% since December 2009.

| 7 |

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS(CONTINUED)

For commercial loans, six consecutive payments on newly restructured loan terms are required prior to returning the loan to accrual status. In some instances after the required six consecutive payments are made, a management assessment will conclude that collection of the entire principal balance is still in doubt. In those instances, the loan will remain on non-accrual. Homogeneous loans may or may not be on accrual status at the time of restructuring, but all are placed on accrual status upon the restructuring of the loan. Homogenous loans are restructured only if the borrower can demonstrate the ability to meet the restructured payment terms; otherwise, collection is pursued and the loan remains on non-accrual status until liquidated. If the homogenous restructured loan does not perform it will be placed in non-accrual status when it is 90 days delinquent.

A loan that defaults and is subsequently modified would impact the Company’s delinquency trend, which is part of the QRF component of the general reserve calculation. Any modified loan that re-defaults and is charged-off would impact the HLF component of our general reserve calculation.

Non-performing assets were $434,530,000, or 3.22%, of total assets, at September 30, 2010, compared to $557,120,000, or 4.43%, of total assets, at September 30, 2009. This elevated level of non-performing assets is a result of the significant decline in housing values in the western United States and the national recession over the last three years. Total delinquencies over 30 days were $304,665,000, or 3.53%, of net loans at September 30, 2010, compared to $456,318,000, or 5.08%, of net loans at September 30, 2009.

The loans and foreclosed real estate purchased in the Horizon transaction (see Note A) are covered by two loss share agreements between the FDIC and the Bank (one for single family loans and the other for all other loans and foreclosed real estate), which affords the Bank significant loss protection. Under the loss share agreements, the FDIC will cover 80% of covered loan and foreclosed real estate losses up to $536 million and 95% of losses in excess of that amount. The term for loss sharing on residential real estate loans is ten years, while the term for loss sharing on non-residential real estate loans is five years with respect to losses and eight years with respect to loss recoveries. The losses reimbursable by the FDIC are based on the book value of the relevant loan as determined by the FDIC at the date of the transaction. New loans made after that date are not covered by the loss share agreements. As a result of the loss sharing agreements with the FDIC, the Bank recorded a receivable of $228 million at the time of acquisition. To account for the transaction, the balance sheet now has three new line items, as follows:

“Covered loans” represent the loans acquired from Horizon recorded at their estimated fair market value;

“Covered real estate held for sale” represents the estimated fair market value of the repossessed real estate acquired in the transaction. The covered loans and covered real estate held for sale are collectively referred to as “covered assets”;

“FDIC indemnification asset” represents the estimated fair value of the guarantee provided by the FDIC on the covered assets.

Loans that were classified as non-performing loans by Horizon are no longer classified as non-performing because, at acquisition, the carrying value of these loans was adjusted to reflect fair value and are covered under the FDIC loss sharing agreements. Management believes that the new book value reflects an amount that will ultimately be collected.

The following table details non-performing asset by type, comparing 2010 and 2009.

| September 30, | ||||||||||||||||

| Non-Performing Assets | 2010 | 2009 | $ Change | % Change | ||||||||||||

| (In thousands) | ||||||||||||||||

Non-accrual loans: | ||||||||||||||||

Single-family residential | $ | 123,624 | $ | 116,268 | $ | 7,356 | 6 | % | ||||||||

Construction – speculative | 39,915 | 50,348 | (10,433 | ) | -21 | % | ||||||||||

Construction – custom | — | — | — | — | ||||||||||||

Land – acquisition & development | 64,883 | 187,061 | (122,178 | ) | -65 | % | ||||||||||

Land – consumer lot loans | — | — | — | — | ||||||||||||

Multi-Family | 4,931 | 4,368 | 563 | 13 | % | |||||||||||

Commercial real estate | 10,831 | 2,733 | 8,098 | 296 | % | |||||||||||

Commercial & industrial | 371 | 18,823 | (18,452 | ) | NM | |||||||||||

HELOC | — | — | — | — | ||||||||||||

Consumer | 977 | 656 | 321 | 49 | % | |||||||||||

Total non-accrual loans | 245,532 | 380,257 | (134,725 | ) | -35 | % | ||||||||||

Total REO & REHI | 188,998 | 176,863 | 12,135 | 7 | % | |||||||||||

Total non-performing assets | $ | 434,530 | $ | 557,120 | $ | (122,590 | ) | -22 | % | |||||||

| 8 | . |

Table of Contents

A disproportionate share of the Company’s non-performing assets (“NPAs”) and charge-offs come from the land A&D and speculative construction portfolios. These assets have seen the largest declines in value in the loan portfolio. The continued elevated level of non-performing assets is attributable to lower home values, high unemployment and weak economic conditions in the Company’s eight state market territory.

In response to the improving overall credit quality of our loan portfolio, the allowance for loan loss decreased by $3,742,000, or 2.2%, over 2009. $98,092,000 of the allowance is calculated under the formulas (general reserve) contained in our methodology and the remaining $65,002,000 is made up of specific reserves on loans that were deemed to be impaired at September 30, 2010. The general reserve increased by $38,631,000, or 61.6%, to $98,092,000, while the specific reserve decreased by $42,373,000, or 39.5%. The shift in the allowance, increasing the general reserve and decreasing the specific reserve is due to 1) the continued economic uncertainty driven primarily by high unemployment rates which had the effect of increasing the general reserve and 2) the declining balances of land acquisition and development and speculative construction loans, and related specific reserves.

Recently, legal issues involving documentation flaws in the mortgage foreclosure process used by large servicing organizations have gained a very high profile in the national media. For example, attention has been brought to so-called “Robo-signers”, which is a description given to a servicing employee involved in signing hundreds of documents, allegedly without a complete review of their contents. Questions have also been raised by borrowers regarding the legality of the Mortgage Electronic Registration System (“MERS”), which was created to transfer ownership of mortgage loans electronically and improve the efficiency of the secondary markets, to affect foreclosure. The Company has proactively reviewed its practices in this area and believes that its foreclosure activities are not affected. Washington Federal is a portfolio lender and does not sell loans in the secondary market and therefore is not a participant in MERS. Likewise, the Company is not a large servicing organization and thus is able to handle all foreclosures using a limited number of staff members and attorneys. The review discovered no systemic issues involving foreclosure documentation of the types being alleged by borrowers and it is believed that any documentation weaknesses that would prevent foreclosure will be isolated and not material to the overall financial results. The absence of secondary market sales by the Company also eliminates the risk of “putbacks”, or repurchase requests from loan purchasers, which is a significant potential source of litigation and economic loss for large mortgage originators and servicers in the currently distressed market.

LIQUIDITY AND CAPITAL RESOURCES | The principal sources of funds for the Company’s activities are retained earnings, loan repayments (including prepayments), net deposit inflows, repayments and sales of investments and borrowings. Washington Federal’s principal sources of revenue are interest on loans and interest and dividends on investments. |

The Company’s net worth at September 30, 2010, was $1,841,147,000, or 13.7%, of total assets. This is an increase of $95,662,000 from September 30, 2009, when net worth was $1,745,485,000, or 13.9%, of total assets. The Company’s net worth increased due in part to net income of $118,653,000, less cash dividends paid of $22,450,000 on common stock. The Company paid out 19% of its 2010 earnings in cash dividends to common shareholders, compared with 43% last year. Over the long term, the Company would prefer its dividend payout ratio to be less than 50%.

Washington Federal Saving’s percentage of net worth to total assets is over three times the minimum required under Office of Thrift Supervision (OTS) regulations (see Note M). Management believes this strong net worth position will help the Company manage its interest rate risk and will enable it to compete more effectively.

During the last quarter, the Basel Committee on Banking Supervision, a consortium of international financial regulators, published proposed capital standards to be implemented in the future. The following table shows the proposed standards and the Company’s current capital position.

| Washington Federal as of 9/30/10 | Proposed Basel Requirements (2019) | Excess | ||||||||||

Tier 1 common to risk weighted assets: | 22.17 | % | 7.00 | % | 15.17 | % | ||||||

Tier 1 capital to risk weighted assets: | 22.17 | % | 8.50 | % | 13.67 | % | ||||||

Leverage ratio: | 11.67 | % | 3.00 | % | 8.67 | % | ||||||

Customer accounts increased $1,010,230,000, or 12.9%, from one year ago. As described in Note A, the Company acquired $819,528,000 of deposits from the Horizon transaction. As of September 30, 2010, the balance of these accounts had decreased by $294,059,000, or 35.9%, to $525,469,000, which was included in the $8,852,540,000 period end balance. The decrease in Horizon balances, which was anticipated by the Company, is due to the nature of the transaction and the repricing of deposits to current market rates. Excluding the $525,469,000 of Horizon accounts at September 30, 2010, balances at legacy branches increased by $484,761,000, or 6.2%, which reflects the opportunity created in the marketplace by the failure and/or merger of several large institutions throughout the Company’s footprint.

| 9 |

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS(CONTINUED)

The Company has a credit line with the FHLB Seattle equal to 50% of total assets, providing a substantial source of liquidity if needed. FHLB advances are collateralized as provided for in the Advances, Pledge and Security Agreement by all FHLB stock owned by the Company, deposits with the FHLB and certain mortgages or deeds of trust securing such properties as provided in the agreements with the FHLB.

The Company’s cash and cash equivalents amounted to $888,622,000 at September 30, 2010, a 78.3% increase from the cash and cash equivalents balance of $498,388,000 one year ago. This increase is primarily the result of diminished loan demand and strong deposit growth. Additionally, see “Interest Rate Risk” above and the “Statement of Cash Flows” included in the financial statements.

CHANGES IN FINANCIAL POSITION | Available-for-sale and held-to-maturity securities. The Company purchased $1,774,343,000 of securities during 2010, all of which have been classified as available-for-sale. |

The Company sold $496,024,000 of available-for-sale securities in the current year. As of September 30, 2010, the Company had net unrealized gains in its available-for-sale portfolio of $78,548,000, as compared to net unrealized gains of $86,057,000 as of September 30, 2009. The decrease in net unrealized gains was primarily a result of the repayment and sale of securities that were in gain positions during the year.

Loans receivable. Loans receivable decreased $559,727,000, or 6.2%, to $8,423,703,000 at September 30, 2010, from $8,983,430,000 one year earlier. The decrease resulted primarily from loan repayments (including prepayments) of $1,855,560,000 , which exceeded originations of $1,481,124,000 by $374,436,000. The Company’s current decision not to originate and hold in its loan portfolio 30 year fixed-rate loans at rates below 4.50%, due to the duration risk associated with such low mortgage rates, contributed to the net run off of the loan portfolio. Additionally, during the year, $222,057,000 of loans were transferred to REO. The following table shows the change in the geographic distribution by state of the gross loan portfolio from 2009 to 2010.

| 2010 | 2009 | Change | ||||||||||

Washington | 43.8 | % | 43.9 | % | -0.1 | % | ||||||

Oregon | 17.6 | 17.0 | 0.6 | % | ||||||||

Idaho | 7.0 | 7.3 | -0.3 | % | ||||||||

Arizona | 8.8 | 8.5 | 0.3 | % | ||||||||

Utah | 7.6 | 7.8 | -0.2 | % | ||||||||

New Mexico | 3.9 | 4.1 | -0.2 | % | ||||||||

Texas | 2.2 | 1.7 | 0.5 | % | ||||||||

Nevada | 1.9 | 1.7 | 0.2 | % | ||||||||

Other | 7.2 | 8.0 | -0.8 | % | ||||||||

| 100.0 | % | 100.0 | % | |||||||||

Real estate held for sale. The balance of real estate held for sale at September 30, 2010 was $188,998,000, an increase of $12,135,000 from one year ago. This increase is a result of the foreclosure of non-performing loans as discussed in the “Asset Quality” section above. The migration of problem assets from loans, to REO is to be expected and we believe is a positive sign that the Company is dealing with problem loans. At year end, the Company owned 635 properties in its REO. During 2010, the company sold 518 properties for net proceeds of $113,600,000.

Intangible assets. The Company’s intangible assets are made up of $251,653,000 of goodwill, servicing rights intangible of $1,775,000, as well as the unamortized balances of the core deposit intangible of $4,290,000 at September 30, 2010.

Customer accounts. Customer accounts at September 30, 2010 totaled $8,852,540,000 compared with $7,842,310,000 at September 30, 2009, a 12.9% increase. See “Liquidity and Capital Resources” above.

FHLB advances and other borrowings. Total borrowings decreased $213,982,000, or 7.4%, to $2,665,548,000 at September 30, 2010 as the Company chose to prepay $200 million of FHLB advances that were maturing in August 2011, that had a rate of 4.80%. This prepayment resulted in a prepayment fee of $8,150,000 and will enhance net interest income over the next three quarters. The Company chose to fund asset growth with a mix of customer accounts and stockholders’ equity. See “Interest Rate Risk” above.

| 10 | . |

Table of Contents

Contractual obligations. The following table presents, as of September 30, 2010, the Company’s significant fixed and determinable contractual obligations, within the categories described below, by payment date or contractual maturity.

| Contractual Obligations | Total | Less than 1 Year | 1 to 5 Years | Over 5 Years | ||||||||||||

| (In thousands) | ||||||||||||||||

Debt obligations (1) | $ | 2,665,548 | $ | — | $ | 1,015,548 | $ | 1,650,000 | ||||||||

Operating lease obligations | 8,397 | 2,573 | 4,938 | 886 | ||||||||||||

| $ | 2,673,945 | $ | 2,573 | $ | 1,020,486 | $ | 1,650,886 | |||||||||

| (1) | Represents final maturities of debt obligations. |

These contractual obligations, except for the operating leases, are included in the Consolidated Statements of Financial Condition. The payment amounts represent those amounts contractually due.

RESULTS OF OPERATIONS | GENERAL |

See Note P, “Selected Quarterly Financial Data (Unaudited),” which highlights the quarter-by-quarter results for the years ended September 30, 2010 and 2009.

Net income mentioned below refers to net income available to common shareholders’, which consists of net income less dividends accrued on the preferred stock that was repaid in full in May 2009.

COMPARISON OF 2010 RESULTS WITH 2009

In 2010 net income increased $77,969,000, or 191.6%, from 2009, primarily as a result of the $54,789,000 after tax gain on the acquisition of Horizon and a $38,865,000 tax benefit related to the settlement of a contingent tax liability. In addition, during the twelve months ended September 30, 2010, the Company recognized a gain on sale of available-for-sale securities of $22,409,000. Losses recognized on real estate acquired through foreclosure was $80,475,000 for the twelve months ended September 30, 2010 as compared to $16,354,000 for the fiscal year ended September 30, 2009.

Interest income on loans, covered loans and mortgage-backed securities decreased $35,886,000, or 5.2%, in 2010 due to a 1.7% decrease in the average outstanding balance, as well as a 21 basis point decrease in the weighted average yield during the year from 6.04% in 2009 to 5.83% in 2010.

Interest and dividend income on investment securities and cash equivalents increased $7,672,000, or 252.0%, in 2010 from 2009. This increase was primarily due to an increase in the average outstanding balance of investment securities, cash equivalents and FHLB stock, which increased 251.0% to $1,252,991,000.

Interest expense on customer accounts decreased 23.5% to $146,360,000 for 2010 from $191,435,000 for 2009. The decrease primarily related to a 87 basis point decrease in the average cost of customer accounts to 1.69% during the year compared to 2.56% one year ago, offset by a 15.4% increase in the average balance of customer accounts over the prior year. Interest expense on FHLB advances and other borrowings decreased to $122,741,000 in 2010 from $127,192,000 in 2009 due to a decrease in the average balance of borrowings to $2,880,322,000 during 2010 from $3,235,231,000 during 2009. Partially offsetting the decrease in the average balance of borrowings was the increase in the average cost of borrowings for the year ended September 30, 2010 to 4.26% from 3.93% for the same period one year ago

The Company recorded a $179,909,000 provision for loan losses in 2010 compared to $193,000,000 in 2009. Non-performing assets decreased by $122,590,000 over 2009. The Company had net charge-offs of $183,651,000 for the twelve months ended September 30, 2010 compared with $111,222,000 of net charge-offs for the same period one year ago. The decrease in the provision for loan losses is in response to four primary factors: first, the improvement in the amount of NPAs year-over-year; second, non-accrual loans as a percentage of total loans decreased from 4.23% at September 30, 2009, to 2.91% at September 30, 2010; third, the percentage of loans 30 days or more delinquent decreased from 4.86% at September 30, 2009, to 3.53% at September 30, 2010; and finally, the Company’s exposure in the land A&D and speculative construction portfolios, where the majority of losses have come from during this period of the cycle, has decreased from a combined 8.4% of the gross loan portfolio at September 30, 2009, to 5.4% at September 30, 2010. Management expects the provision to remain at elevated levels until NPAs and charge-offs improve measurably. Management believes the allowance for loan losses, totaling $163,094,000, is sufficient to absorb estimated losses inherent in the portfolio.

Total other income increased $101,421,000, or 533.5%, in 2010 from 2009. The year ended September 30, 2010, included an $85,608,000 gain on the acquisition of Horizon (see Note A).

Compensation expense increased $12,782,000, or 22.4%, in 2010 primarily due to the addition of Horizon employees and incentive compensation paid related to the increase in net income. Personnel, including part-time employees considered on a full-time equivalent basis, increased to 1,223 at September 30, 2010 compared to 1,105 one year ago.

| 11 |

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS(CONTINUED)

Occupancy expense increased $884,000, or 6.77%, during the year primarily due to the additional branches acquired in the Horizon transaction. The branch network increased to 160 offices at September 30, 2010 versus 150 offices one year ago.

FDIC insurance expense increased to $18,626,000 for 2010 from $10,688,000 in 2009 as a result of the significant increase in bank failures during the year which has depleted the FDIC fund. The FDIC has undertaken to replenish the FDIC fund through special assessments and higher insurance premiums for all insured depository institutions. Other expenses increased $3,725,000 during the year primarily related to the operating costs added from the Horizon acquisition and increased information technology spending. Operating expense for 2010 and 2009 equaled 0.98% and .87% of average assets, respectively. Despite the increase in operating expenses, the Company continues to operate as one of the most efficient financial institutions in the country.

The loss on real estate acquired through foreclosure increased from $16,354,000 in 2009 to $80,475,000 in 2010 due to the growth in balances of real estate acquired through foreclosure, combined with the resulting net loss on sale and any additional valuation adjustments of properties stemming from continued declines in real estate values.

Income tax expense decreased $23,198,000 or 84.1%, in 2010 as a result of a $38,865,000 tax benefit related to the settlement of a contingent tax liability (see Note A). The effective tax rate was 3.55% for 2010 versus 36.40% for 2009. The Company expects an effective tax rate of 36.00% going forward.

COMPARISON OF 2009 RESULTS WITH 2008

In 2009 net income decreased $21,648,000, or 34.7%, from 2008, primarily as a result of an $193,000,000 provision for loan losses which resulted from the significant decline in asset quality and higher net charge offs. In addition, the other expenses increased $19,840,000 in 2009 over the prior year, due primarily to increased FDIC insurance costs of $9,896,000, which resulted from the significant increase in bank failures during the year that necessitated replenishment of the deposit insurance fund.

In comparing operating results of 2009 versus 2008 it is important to understand that 2009 had 12 months of operating results, both income and expense, from the First Mutual acquisition; 2008 had only 8 months of operating results from the First Mutual acquisition.

Interest income on loans and mortgage-backed securities increased only $427,000, or 0.1%, in 2009 due to a 7.7% increase in the average outstanding balance of loans and mortgage-backed securities, offset by a 46 basis point decrease in the weighted average yield during the year from 6.51% in 2008 to 6.04% in 2009.

Interest and dividend income on investment securities and cash equivalents decreased $10,081,000, or 76.8%, in 2009 from 2008. This decrease was primarily due to a decrease in the weighted average rate earned on investment securities, cash equivalents and FHLB stock, which decreased 284 basis points to 0.85%. The Company’s required investment in FHLB stock, which amounted to $144,495,000 as of 2009, produced a yield of only 0.28% during the year.

Interest expense on customer accounts decreased 26.3% to $191,435,000 for 2009 from $259,769,000 for 2008. The decrease primarily related to a 131 basis point decrease in the average cost of customer accounts to 2.56% during the year compared to 3.87% one year ago, offset by a 11.5% increase in the average balance of customer accounts over the prior year. Interest expense on FHLB advances and other borrowings decreased to $127,192,000 in 2009 from $137,872,000 in 2008 due to a decrease in the average cost of borrowings for the year ended September 30, 2009 to 3.93% from 4.41% for the same period one year ago. Partially offsetting the decrease in average cost of borrowings was an increase in the average balance of borrowings to $3,235,231,000 during 2009 from $3,122,950,000 during 2008.

The Company recorded a $193,000,000 provision for loan losses in 2009 compared to $60,516,000 in 2008. The current year provision is due to the significant increase in the Company’s non-performing asset balances. Non-performing assets increased by $392,929,000 over 2008. Non-accrual loans as a percentage of total loans increased from 1.34% in 2008 to 4.23% in 2009. Economic conditions deteriorated in the primary markets served by the Company, as evidenced by an increase in unemployment, a reduction in the number of home sales and weak consumer confidence. Total delinquencies over 30 days were $456,318,000, or 4.97% of net loans at September 30, 2009 compared to $236,848,000, or 2.49% of net loans at September 30, 2008. Actual net charge-offs during 2009 were $111,222,000. Management believes the allowance for loan losses, totaling $166,836,000, is sufficient to absorb estimated losses inherent in the portfolio.

Total other income increased $78,200,000, or 132.1%, in 2009 from 2008. The increase in 2009 was driven primarily by the other than temporary impairment (“OTTI”) charge of $87,747,000 in the prior year. Additionally in 2008, the Company reported $13,123,000 of gain on the sale of real estate.

Compensation expense increased $4,265,000, or 8.1%, in 2009 primarily due to full year of operations combined with First Mutual. Personnel, including part-time employees considered on a full-time equivalent basis, increased to 1,105 at September 30, 2009 compared to 1,095 one year ago.

| 12 | . |

Table of Contents

Occupancy expense increased $1,836,000, or 16.4%, during the year primarily due to the 12 additional branches acquired in the First Mutual transaction. The branch network increased to 150 offices at September 30, 2009 versus 148 offices one year ago.

FDIC insurance expense increased to $9,896,000 for 2009 from $792,000 in 2008 as a result of the significant increase in bank failures during the year which has depleted the FDIC fund. The FDIC has undertaken to replenish the FDIC fund through special assessments and higher insurance premiums for all insured depository institutions. Other expenses increased $2,160,000 during the year primarily related to the operating costs added from First Mutual and increased information technology spending. Operating expense for 2009 and 2008 equaled .87% and .77% of average assets, respectively. Despite the increase in operating expenses, the Company continues to operate as one of the most efficient financial institutions in the country.

The loss on real estate acquired through foreclosure increased from $1,021,000 in 2008 to $16,354,000 in 2009 due to the growth in balances of real estate acquired through foreclosure and the resulting loss on sale of some of those properties stemming from continued declines in real estate values in the western United States.

Income tax expense decreased $5,937,000 or 17.7%, in 2009 due to a lower taxable income base. Additionally, 2009 included $1,500,000 of additional tax related to a tax liability arising from the First Mutual acquisition (see Note A). The effective tax rate was 36.40% for 2009 versus 34.96% for 2008.

PERIOD END SPREAD – AS OF THE DATE SHOWN

| Dec 31 2008 | Mar 31 2009 | Jun 30 2009 | Sep 30 2009 | Dec 31 2009 | Mar 31 2010 | Jun 30 2010 | Sep 30 2010 | |||||||||||||||||||||||||

Interest rate on loans and mortgage-backed securities | 6.22 | % | 6.17 | % | 6.12 | % | 6.04 | % | 6.00 | % | 5.97 | % | 5.89 | % | 5.75 | % | ||||||||||||||||

Interest rate on investment securities | 1.22 | 1.68 | 0.69 | 0.45 | 0.56 | 1.21 | 1.21 | 1.26 | ||||||||||||||||||||||||

Combined | 6.11 | 6.09 | 5.99 | 5.75 | 5.49 | 5.37 | 5.21 | 5.21 | ||||||||||||||||||||||||

Interest rate on customer accounts | 2.99 | 2.54 | 2.14 | 1.96 | 1.75 | 1.70 | 1.63 | 1.51 | ||||||||||||||||||||||||

Interest rate on borrowings | 3.64 | 4.08 | 4.25 | 4.25 | 4.25 | 4.19 | 4.19 | 4.14 | ||||||||||||||||||||||||

Combined | 3.20 | 2.98 | 2.72 | 2.58 | 2.41 | 2.30 | 2.25 | 2.12 | ||||||||||||||||||||||||

Interest rate spread | 2.91 | % | 3.11 | % | 3.27 | % | 3.17 | % | 3.08 | % | 3.07 | % | 2.96 | % | 3.09 | % | ||||||||||||||||

The interest rate spread decreased during 2010 from 3.17% at September 30, 2009 to 3.09% at September 30, 2010. See “Interest Rate Risk” section above.

| 13 |

Table of Contents

| Year ended September 30, | 2010 | 2009 | 2008 | 2007 | 2006 | |||||||||||||||

| (In thousands, except per share data) | ||||||||||||||||||||

Interest income | $ | 663,560 | $ | 691,774 | $ | 701,428 | $ | 618,682 | $ | 529,883 | ||||||||||

Interest expense | 269,101 | 318,627 | 397,641 | 358,501 | 273,361 | |||||||||||||||

Net interest income | 394,459 | 373,147 | 303,787 | 260,181 | 256,522 | |||||||||||||||

Provision for loan losses | 179,909 | 193,000 | 60,516 | 1,550 | 535 | |||||||||||||||

Other income | 39,955 | 2,655 | (60,212 | ) | 15,569 | 16,252 | ||||||||||||||

Other expense | 131,480 | 107,060 | 87,220 | 64,888 | 53,579 | |||||||||||||||

Income before income taxes | 123,025 | 75,742 | 95,839 | 209,312 | 218,660 | |||||||||||||||

Income taxes | 4,372 | 27,570 | 33,507 | 74,295 | 75,558 | |||||||||||||||

Net income | $ | 118,653 | $ | 48,172 | $ | 62,332 | $ | 135,017 | $ | 143,102 | ||||||||||

Preferred dividends accrued | — | 7,488 | — | — | — | |||||||||||||||

Net income available to common shareholders | $ | 118,653 | $ | 40,683 | $ | 62,332 | $ | 135,017 | $ | 143,102 | ||||||||||

Per share data | ||||||||||||||||||||

Basic earnings | $ | 1.06 | $ | 0.46 | $ | 0.71 | $ | 1.55 | $ | 1.64 | ||||||||||

Diluted earnings | 1.05 | 0.46 | 0.71 | �� | 1.54 | 1.64 | ||||||||||||||

Cash dividends | 0.20 | 0.20 | 0.84 | 0.83 | 0.81 | |||||||||||||||

| September 30, | 2010 | 2009 | 2008 | 2007 | 2006 | |||||||||||||||

Total assets | $ | 13,486,379 | $ | 12,582,475 | $ | 11,830,141 | $ | 10,285,417 | $ | 9,069,020 | ||||||||||

Loans and mortgage-backed securities | 10,626,842 | 11,266,295 | 11,053,223 | 9,601,947 | 8,457,759 | |||||||||||||||

Investment securities | 358,061 | 21,259 | 49,001 | 240,391 | 256,650 | |||||||||||||||

Cash and cash equivalents | 888,622 | 498,388 | 82,600 | 61,378 | 45,722 | |||||||||||||||

Customer accounts | 8,852,540 | 7,842,310 | 7,169,539 | 5,996,785 | 5,311,726 | |||||||||||||||

FHLB advances | 1,865,548 | 2,078,930 | 1,998,308 | 1,760,979 | 1,500,000 | |||||||||||||||

Other borrowings | 800,000 | 800,600 | 1,177,600 | 1,075,000 | 870,000 | |||||||||||||||

Stockholders’ equity | 1,841,147 | 1,745,485 | 1,332,674 | 1,318,127 | 1,262,720 | |||||||||||||||

Number of | ||||||||||||||||||||

Customer accounts | 327,430 | 305,129 | 298,926 | 281,778 | 249,533 | |||||||||||||||

Loans | 42,540 | 44,453 | 47,331 | 44,713 | 36,955 | |||||||||||||||

Offices | 160 | 150 | 148 | 135 | 123 | |||||||||||||||

| 14 | . |

Table of Contents

CONSOLIDATED STATEMENTS OF FINANCIAL CONDITION

| September 30, | 2010 | 2009 | ||||||

(In thousands, except share data) | ||||||||

ASSETS | ||||||||

Cash and cash equivalents | $ | 888,622 | $ | 498,388 | ||||

Available-for-sale securities, including encumbered securities of $933,315 and $860,655 | 2,481,093 | 2,201,083 | ||||||

Held-to-maturity securities, including encumbered securities of $60,970 and $80,717 | 80,107 | 103,042 | ||||||

Loans receivable, net | 8,423,703 | 8,983,430 | ||||||

Covered loans, net | 534,474 | — | ||||||

Interest receivable | 49,020 | 53,288 | ||||||

Premises and equipment, net | 162,721 | 133,477 | ||||||

Real estate held for sale | 188,998 | 176,863 | ||||||

Covered real estate held for sale | 44,155 | — | ||||||

FDIC indemnification asset | 131,128 | — | ||||||

FHLB stock | 151,748 | 144,495 | ||||||

Intangible assets, including goodwill of $251,653 | 257,718 | 256,797 | ||||||

Federal and state income taxes | 8,093 | — | ||||||

Other assets | 84,799 | 31,612 | ||||||

| $ | 13,486,379 | $ | 12,582,475 | |||||

LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

Liabilities | ||||||||

Customer accounts | ||||||||

Savings and demand accounts | $ | 8,825,918 | $ | 7,786,467 | ||||

Repurchase agreements with customers | 26,622 | 55,843 | ||||||

| 8,852,540 | 7,842,310 | |||||||

FHLB advances | 1,865,548 | 2,078,930 | ||||||

Other borrowings, primarily securities sold under agreements to repurchase | 800,000 | 800,600 | ||||||

Advance payments by borrowers for taxes and insurance | 39,504 | 38,376 | ||||||

Federal and state income taxes, including net deferred liabilities of $21,951 and $449 | — | 18,075 | ||||||

Accrued expenses and other liabilities | 87,640 | 58,699 | ||||||

| 11,645,232 | 10,836,990 | |||||||

Stockholders’ equity | ||||||||

Common stock, $1.00 par value, 300,000,000 shares authorized;129,555,956 and 129,320,072 shares issued;112,483,632 and 112,247,748 shares outstanding | 129,556 | 129,320 | ||||||

Paid-in capital | 1,578,527 | 1,574,555 | ||||||

Accumulated other comprehensive income (loss), net of tax | 49,682 | 54,431 | ||||||

Treasury stock, at cost;17,072,324 shares | (208,985 | ) | (208,985 | ) | ||||

Retained earnings | 292,367 | 196,164 | ||||||

| 1,841,147 | 1,745,485 | |||||||

| $ | 13,486,379 | $ | 12,582,475 | |||||

| SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS | 15 |

Table of Contents

CONSOLIDATED STATEMENTS OF OPERATIONS

| Year ended September 30, | 2010 | 2009 | 2008 | |||||||||

| (In thousands, except per share data) | ||||||||||||

INTEREST INCOME | ||||||||||||

Loans | $ | 561,069 | $ | 579,244 | $ | 599,878 | ||||||

Mortgage-backed securities | 91,775 | 109,486 | 88,425 | |||||||||

Investment securities | 10,716 | 3,044 | 13,125 | |||||||||

| 663,560 | 691,774 | 701,428 | ||||||||||

INTEREST EXPENSE | ||||||||||||

Customer accounts | 146,360 | 191,435 | 259,769 | |||||||||

FHLB advances and other borrowings | 122,741 | 127,192 | 137,872 | |||||||||

| 269,101 | 318,627 | 397,641 | ||||||||||

Net interest income | 394,459 | 373,147 | 303,787 | |||||||||

Provision for loan losses | 179,909 | 193,000 | 60,516 | |||||||||

Net interest income after provision for loan losses | 214,550 | 180,147 | 243,271 | |||||||||

OTHER INCOME (LOSS) | ||||||||||||

Other than temporary impairment charge | — | — | (87,747 | ) | ||||||||

Gain on FDIC-assisted transaction | 85,608 | — | — | |||||||||

Gain on sale of investments | 22,409 | — | — | |||||||||

Gain on sale of real estate | — | — | 13,123 | |||||||||

Prepayment penalty on FHLB advance | (8,150 | ) | — | — | ||||||||

Other | 20,563 | 19,009 | 15,433 | |||||||||

| 120,430 | 19,009 | (59,191 | ) | |||||||||

OTHER EXPENSE | ||||||||||||

Compensation and fringe benefits | 69,879 | 57,097 | 52,832 | |||||||||

Amortization of intangibles | 2,140 | 3,331 | 2,441 | |||||||||

Occupancy expense | 13,933 | 13,049 | 11,213 | |||||||||

FDIC Insurance | 18,626 | 10,688 | 792 | |||||||||

Other | 28,830 | 25,105 | 22,945 | |||||||||

Deferred loan origination costs | (1,928 | ) | (2,210 | ) | (3,003 | ) | ||||||

| 131,480 | 107,060 | 87,220 | ||||||||||

Gain (loss) on real estate acquired through foreclosure, net | (80,475 | ) | (16,354 | ) | (1,021 | ) | ||||||

Income before income taxes | 123,025 | 75,742 | 95,839 | |||||||||

Income taxes | ||||||||||||

Current | (19,890 | ) | 56,075 | 81,158 | ||||||||

Deferred | 24,262 | (28,505 | ) | (47,651 | ) | |||||||

| 4,372 | 27,570 | 33,507 | ||||||||||

NET INCOME | $ | 118,653 | $ | 48,172 | $ | 62,332 | ||||||

Preferred dividends accrued | — | 7,488 | — | |||||||||

Net income available to common shareholders | $ | 118,653 | $ | 40,684 | $ | 62,332 | ||||||

PER SHARE DATA | ||||||||||||

Basic earnings per share | $ | 1.06 | $ | 0.46 | $ | 0.71 | ||||||

Diluted earnings per share | 1.05 | 0.46 | 0.71 | |||||||||

Cash dividends | 0.20 | 0.20 | 0.84 | |||||||||

Basic weighted average number of shares outstanding | 112,438,059 | 88,689,553 | 87,675,978 | |||||||||

Diluted weighted average number of shares outstanding, including dilutive stock options | 112,745,261 | 88,711,694 | 87,818,580 | |||||||||

| 16 | SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS . |

Table of Contents

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

| Common Stock | Preferred Stock | Paid-in Capital | Retained Earnings | Accumulated Other Comprehensive Income (loss) | Treasury Stock | Total | ||||||||||||||||||||||

| (In thousands) | ||||||||||||||||||||||||||||

Balance at September 30, 2007 | $ | 104,921 | $ | — | $ | 1,254,490 | $ | 185,683 | $ | (13,033 | ) | $ | (213,934 | ) | $ | 1,318,127 | ||||||||||||

Comprehensive income: | ||||||||||||||||||||||||||||

Net income | 62,332 | 62,332 | ||||||||||||||||||||||||||

Other comprehensive income, | ||||||||||||||||||||||||||||

Unrealized gains on securities | 72,540 | 72,540 | ||||||||||||||||||||||||||

Reclassification adjustment | (57,035 | ) | (57,035 | ) | ||||||||||||||||||||||||

Total comprehensive income | 77,837 | |||||||||||||||||||||||||||

Dividends | (73,688 | ) | (73,688 | ) | ||||||||||||||||||||||||

Compensation expense related to common stock options | 1,286 | 1,286 | ||||||||||||||||||||||||||

Proceeds from exercise of common stock options | 146 | 2,052 | 2,198 | |||||||||||||||||||||||||

Tax benefit related to exercise of stock options | 348 | 348 | ||||||||||||||||||||||||||

Restricted stock | 26 | 769 | 795 | |||||||||||||||||||||||||

Proceeds from Employee Stock Ownership Plan | 2,087 | 3,684 | 5,771 | |||||||||||||||||||||||||

Treasury stock | — | |||||||||||||||||||||||||||

Balance at September 30, 2008 | $ | 105,093 | $ | — | $ | 1,261,032 | $ | 174,327 | $ | 2,472 | $ | (210,250 | ) | $ | 1,332,674 | |||||||||||||

Comprehensive income: | ||||||||||||||||||||||||||||

Net income | 48,172 | 48,172 | ||||||||||||||||||||||||||

Other comprehensive income, net of tax of $28,598: | ||||||||||||||||||||||||||||

Unrealized gains on securities | 51,273 | 51,273 | ||||||||||||||||||||||||||

Reclassification adjustment | 686 | 686 | ||||||||||||||||||||||||||

Total comprehensive income | 100,131 | |||||||||||||||||||||||||||

Preferred stock issuance | 197,873 | 197,873 | ||||||||||||||||||||||||||

Preferred stock discount and accretion | 2,127 | (2,127 | ) | — | ||||||||||||||||||||||||

Dividends paid on common stock | (18,847 | ) | (18,847 | ) | ||||||||||||||||||||||||

Dividends paid on preferred stock | (5,361 | ) | (5,361 | ) | ||||||||||||||||||||||||

Preferred stock redemption | (200,000 | ) | (200,000 | ) | ||||||||||||||||||||||||

Compensation expense related to common stock options | 1,327 | 1,327 | ||||||||||||||||||||||||||

Proceeds from exercise of common stock options | 13 | 145 | 158 | |||||||||||||||||||||||||

Proceeds from issuance of common stock | 24,150 | 309,027 | 333,177 | |||||||||||||||||||||||||

Tax benefit related to exercise of stock options | 22 | 22 | ||||||||||||||||||||||||||

Restricted stock | 64 | 799 | 863 | |||||||||||||||||||||||||

Issuance of Warrants | 2,127 | 2,127 | ||||||||||||||||||||||||||

Proceeds from Employee Stock Ownership Plan | 76 | 1,265 | 1,341 | |||||||||||||||||||||||||

Treasury stock | — | |||||||||||||||||||||||||||

Balance at September 30, 2009 | $ | 129,320 | $ | — | $ | 1,574,555 | $ | 196,164 | $ | 54,431 | $ | (208,985 | ) | $ | 1,745,485 | |||||||||||||

Comprehensive income: | ||||||||||||||||||||||||||||

Net income | 118,653 | 118,653 | ||||||||||||||||||||||||||

Other comprehensive income, | ||||||||||||||||||||||||||||

Unrealized losses on securities | (19,203 | ) | (19,203 | ) | ||||||||||||||||||||||||

Reclassification adjustment | 14,454 | 14,454 | ||||||||||||||||||||||||||

Total comprehensive income | 113,904 | |||||||||||||||||||||||||||

Dividends paid on common stock | (22,450 | ) | (22,450 | ) | ||||||||||||||||||||||||

Compensation expense related to common stock options | 1,213 | 1,213 | ||||||||||||||||||||||||||

Proceeds from exercise of common stock options | 145 | 1,614 | 1,759 | |||||||||||||||||||||||||

Tax benefit related to exercise of stock options | 181 | 181 | ||||||||||||||||||||||||||

Restricted stock | 91 | 964 | 1,055 | |||||||||||||||||||||||||

Treasury stock | — | |||||||||||||||||||||||||||

Balance at September 30, 2010 | $ | 129,556 | $ | — | $ | 1,578,527 | $ | 292,367 | $ | 49,682 | $ | (208,985 | ) | $ | 1,841,147 | |||||||||||||

| SEE NOTES TO CONSOLIDATED FINANCIAL STATEMENTS | 17 |

Table of Contents

CONSOLIDATED STATEMENTS OF CASH FLOWS

| Year ended September 30, | 2010 | 2009 | 2008 | |||||||||

| (In thousands) | ||||||||||||

CASH FLOWS FROM OPERATING ACTIVITIES | ||||||||||||

Net income | $ | 118,653 | $ | 48,172 | $ | 62,332 | ||||||

Adjustments to reconcile net income to net cash provided by operating activities | ||||||||||||

Amortization (accretion) of fees, discounts, premiums and intangible assets, net | 21,624 | 4,813 | 2,951 | |||||||||

Decrease in FDIC indemnification asset | 92,551 | — | — | |||||||||

Depreciation | 5,766 | 5,153 | 4,281 | |||||||||

Stock option compensation expense | 1,213 | 1,327 | 1,286 | |||||||||

Provision for (reversal of) loan losses | 179,909 | 193,000 | 60,516 | |||||||||

Loss (gain) on investment securities and real estate held for sale, net | 58,066 | 15,101 | (12,655 | ) | ||||||||

Gain on FDIC-assisted transaction | (85,608 | ) | — | — | ||||||||

Other than temporary impairment | — | — | 87,747 | |||||||||

Decrease in accrued interest receivable | 7,999 | 1,077 | 185 | |||||||||

Decrease in income taxes payable | (23,408 | ) | (45,831 | ) | (48,910 | ) | ||||||

FHLB stock dividends | (6 | ) | (15 | ) | (103 | ) | ||||||

Decrease in other assets | (51,635 | ) | (16,156 | ) | (586 | ) | ||||||

Increase (decrease) in accrued expenses and other liabilities | (74,243 | ) | (22,399 | ) | 5,186 | |||||||

Net cash provided by operating activities | 250,881 | 184,242 | 162,230 | |||||||||

CASH FLOWS FROM INVESTING ACTIVITIES | ||||||||||||

Loans originations, net of principal collections | 281,826 | 71,509 | (497,939 | ) | ||||||||

FHLB stock redeemed | — | 394 | 748 | |||||||||

Available-for-sale securities purchased | (1,774,343 | ) | (1,175,321 | ) | (313,950 | ) | ||||||

Principal payments and maturities of available-for-sale securities | 1,052,545 | 513,218 | 240,368 | |||||||||

Available-for-sale securities sold | 496,024 | 18,453 | 72,030 | |||||||||

Principal payments and maturities of held-to-maturity securities | 23,128 | 21,691 | 13,983 | |||||||||

Net cash received from (paid for) acquisition | 111,684 | — | (166,859 | ) | ||||||||

Proceeds from sales of real estate held for sale | 129,447 | 98,822 | 39,193 | |||||||||

Premises and equipment purchased, net | (13,027 | ) | (5,273 | ) | (22,334 | ) | ||||||

Net cash provided (used) by investing activities | 307,284 | (456,507 | ) | (634,760 | ) | |||||||

CASH FLOWS FROM FINANCING ACTIVITIES | ||||||||||||

Net increase in customer accounts | 190,702 | 672,771 | 426,000 | |||||||||

Net increase (decrease) in short term borrowings | — | (377,000 | ) | 102,000 | ||||||||

Proceeds from long-term borrowings | 200,000 | 100,000 | 436,313 | |||||||||

Repayments of long-term borrowings | (539,034 | ) | (19,378 | ) | (408,821 | ) | ||||||

Proceeds from exercise of common stock options and related tax benefit | 1,940 | 180 | 2,546 | |||||||||

Dividends paid on common stock | (22,450 | ) | (18,847 | ) | (73,688 | ) | ||||||