Annual Meeting of Shareholders 18 May 2011 Exhibit 99.1 |

Building from Strength Joseph L. Hooley Chairman, President and Chief Executive Officer |

3 Reminder This presentation contains “forward-looking statements” within the meaning of U.S. securities laws, including statements about industry trends, management’s expectations about our financial performance, market growth, acquisitions and divestitures, new technologies, services and opportunities and earnings, management’s confidence in our strategies and other matters that do not relate strictly to historical facts. Forward-looking statements are often identified by such forward-looking terminology as “expect,” “look,” “believe,” “anticipate,” “estimate,” “seek,” “may,” “will,” “trend,” “target” and “goal,” or similar statements or variations of such terms. Forward-looking statements are subject to various risks and uncertainties, which change over time, are based on management’s expectations and assumptions at the time the statements are made, and are not guarantees of future results. Management’s expectations and assumptions, and the continued validity of the forward-looking statements, are subject to change due to a broad range of factors affecting the national and global economies, the equity, debt, currency and other financial markets, as well as factors specific to State Street and its subsidiaries, including State Street Bank. Therefore, actual outcomes and results may differ materially from what is expressed in those statements, and those statements should not be relied upon as representing our expectations or beliefs as of any date subsequent to May 18, 2011. Important factors that could cause changes in the expectations or assumptions on which forward-looking statements are based include, but are not limited to: the manner in which the Federal Reserve and other regulators implement the Dodd-Frank Act and other regulatory initiatives in the U.S. and internationally, including any increases in the minimum regulatory capital ratios applicable to us and regulatory developments that result in changes to our operating model, or other changes to the provision of our services in order to comply with or respond to such regulations; required regulatory capital ratios under Basel II and Basel III, in each case as fully implemented by State Street and State Street Bank (and in the case of Basel III, when finally adopted by the Federal Reserve), which may result in the need for substantial additional capital or increased levels of liquidity in the future; changes in law or regulation that may adversely affect our, our clients’ or our counterparties’ business activities and the products or services that we sell, including additional or increased taxes or assessments thereon, capital adequacy requirements and changes that expose us to risks related to compliance; financial market disruptions and the economic recession, whether in the U.S. or internationally; the liquidity of the U.S. and international securities markets, particularly the markets for fixed-income securities, and the liquidity requirements of our clients; increases in the volatility of, or declines in the levels of, our net interest revenue, changes in the composition of the assets on our consolidated statement of condition and the possibility that we may be required to change the manner in which we fund those assets; the financial strength and continuing viability of the counterparties with which we or our clients do business and to which we have investment, credit or financial exposure; the credit quality, credit agency ratings, and fair values of the securities in our investment securities portfolio, a deterioration or downgrade of which could lead to other-than-temporary impairment of the respective securities and the recognition of an impairment loss in our consolidated statement of income; delays or difficulties in the execution of our previously announced global multi-year program designed to enhance our operating model, which could lead to changes in our estimates of the charges, expenses or savings associated with the planned program, resulting in increased volatility of our earnings; the maintenance of credit agency ratings for our debt and depository obligations as well as the level of credibility of credit agency ratings; the risks that acquired businesses will not be integrated successfully, or that the integration will take longer than anticipated, that expected synergies will not be achieved or unexpected disynergies will be experienced, that client and deposit retention goals will not be met, that other regulatory or operational challenges will be experienced and that disruptions from the transaction will harm relationships with clients, employees or regulators; the ability to complete acquisitions, divestitures and joint ventures, including the ability to obtain regulatory approvals, the ability to arrange financing as required and the ability to satisfy closing conditions; the performance of and demand for the products and services we offer, including the level and timing of redemptions and withdrawals from our collateral pools and other collective investment products; the possibility that our clients will incur substantial losses in investment pools where we act as agent, and the possibility of significant reductions in the valuation of assets; our ability to attract deposits and other low-cost, short-term funding; potential changes to the competitive environment, including changes due to the effects of consolidation, and perceptions of State Street as a suitable service provider or counterparty; the level and volatility of interest rates and the performance and volatility of securities, credit, currency and other markets in the U.S. and internationally; our ability to measure the fair value of the investment securities on our consolidated statement of condition; the results of litigation, government investigations and similar disputes or proceedings; our ability to control operating risks, information technology systems risks and outsourcing risks, and our ability to protect our intellectual property rights, the possibility of errors in the quantitative models we use to manage our business and the possibility that our controls will prove insufficient, fail or be circumvented; adverse publicity or other reputational harm; our ability to grow revenue, attract and/or retain and compensate highly skilled people, control expenses and attract the capital necessary to achieve our business goals and comply with regulatory requirements; the potential for new products and services to impose additional costs on us and expose us to increased operational risk; changes in accounting standards and practices; and changes in tax legislation and in the interpretation of existing tax laws by U.S. and non-U.S. tax authorities that affect the amount of taxes due. Other important factors that could cause actual results to differ materially from those indicated by any forward-looking statements are set forth in our 2010 Annual Report on Form 10-K and our subsequent SEC filings. We encourage investors to read these filings, particularly the sections on risk factors, for additional information with respect to any forward- looking statements and prior to making any investment decision. The forward-looking statements contained in this presentation speak only as of the date hereof, May 18, 2011, and we do not undertake efforts to revise those forward-looking statements to reflect events after that date. |

4 Building from Strength 2010: A Year of Transition Strategic Direction Investing in Communities and Corporate Social Responsibility 2011: Progress Agenda |

5 2010: A Year of Transition |

6 Building from Strength 2010: A Year of Transition INCREASED CAPITAL FLEXIBILITY • Repositioned investment portfolio to lay the foundation to restore the dividend and prepare for Basel III ahead of implementation dates • 90% of investment portfolio assets rated AAA / AA* ADDRESSED ISSUES FROM FINANCIAL CRISIS • Reached settlement with SEC on fixed-income issues • Implemented solution to provide clients in securities lending program with improved access to liquidity • Strengthened risk infrastructure DEEPENED CLIENT RELATIONSHIPS • Added $1.4T in assets to be serviced • Added $160B in gross new asset management business • Launched new products and services EXPANDED MARKET SHARE • Strategic acquisitions advanced State Street’s market share in Europe and key client segments INITIATED OPS AND IT TRANSFORMATION PROGRAM • Multi-year strategic transformational plan in place • Broad-based organizational focus * As of March 31, 2011. |

7 Building from Strength State Street Corporation “Well Capitalized” 1 3/31/11 12/31/10 12/31/09 Tier 1 Leverage 5.0% 2 8.7% 8.2% 8.5% Tier 1 Capital 6.0% 19.6% 20.5% 17.7% Tier 1 Common Ratio 3 ---- 17.5% 18.1% 15.6% Total Capital 10.0% 21.6% 22.0% 19.1% Tangible Common Equity 4 ---- 7.4% 7.6% 6.6% CAPITAL RATIOS 2010: A Year of Transition – Increased Capital Flexibility Capital Ratios Exceed Regulatory “Well Capitalized” Requirements 1 Except as noted in note 4 below, minimum “Well Capitalized” as defined by Federal regulators under Basel I. 2 Minimum “Well Capitalized,” as defined by Federal regulators, applies to State Street Bank and Trust only and therefore stated only as a reference point. 3 The tier 1 common ratio is not required by GAAP or on a recurring basis by bank regulations. See State Street’s website (www.statestreet.com) for a description of this ratio and related reconciliations. 4 As defined by State Street. The TCE ratio is not required by GAAP or by bank regulations. See State Street’s website (www.statestreet.com) for a description of this ratio and related reconciliations. |

8 Building from Strength 2010: A Year of Transition – Deepened Client Relationships Growing Momentum in Core Businesses 2000 2010 Top 100 clients 11.4 products 13.2 products Top 1,000 clients 7.1 products 7.9 products Expanded Relationships New Clients INVESTMENT SERVICING • Babson Capital Management • Charles Schwab • Legg Mason Global Asset Management • Martin Currie • Norges Bank • Guotai Nasdaq-100 Index Fund • Marshall Wace • National Employment Savings Trust (NEST) • PineBridge Investments • REST Industry Super INVESTMENT MANAGEMENT • AT&T • Stichting Pensionefonds Ahold • Mass PRIM • AP7 • NY State Teachers • Lincoln Financial Group • Previambiante • Pegaso Pension Fund • Qsuper • Alliance Bernstein • Illinois State Teachers • UAW |

9 Building from Strength No. 2 Manager of Worldwide Institutional Assets Pensions & Investments 2010 Money Managers Survey HF Administrator of the Year and PE Fund Administrator of the Year International Custody and Fund Administration 2010 Americas Service Provider Awards Transition Manager of the Year 2010 Global Pensions Awards No. 1 Custodian for Institutional Investors Global Custodian 2010 Global Custody Survey No. 1 Among Custodians* Global Investor / isf 2010 Beneficial Owners Survey No. 1 Global Custodian in Asia Pacific Global Investor / isf 2010 Global Custody Survey Equity Lender of the Year Global Investor / isf 2010 Equity Lending Survey Best Multi-Asset Class Trading Platform (FX Connect) Profit & Loss 2010 Digital Markets Awards Most Recognized ETF Brand, Americas exchangetradedfunds.com 2010 Global ETF Awards 2010: A Year of Transition – Deepened Client Relationships MARKET RECOGNITION * Weighted by lendable assets. |

10 INTESA SANPAOLO’S SECURITIES SERVICES • State Street is now: – Leading asset servicer in Italy – No. 2 asset servicer of offshore funds in Luxembourg and Ireland 1 • Goal to retain 90% of revenue of ~€293M • Additional cross-sell opportunities MOURANT INTERNATIONAL FINANCE ADMINISTRATION • State Street is now No. 1 in Alternative Asset Servicing globally 2 : – Hedge funds – Private equity – Real estate assets • Annualized revenue of about $100 million • Additional cross-sell opportunities BANK OF IRELAND ASSET MANAGEMENT • Expected to deepen SSgA’s capabilities across key investment strategies Building from Strength 1 Fitzrovia 12/10. 2 ICFA Annual Fund Administration Survey, 2010; HFN Biannual Fund Administration Survey 6/10. 2010: A Year of Transition – Expanded Market Share |

11 Building from Strength SUPPORTING GROWTH • Market expansion • Mergers and acquisitions • Geographic expansion ENABLING PRODUCTIVITY • Business process excellence • Flexible global workforce • Global shared services ACCELERATING INNOVATION • New product development • Technology leadership • Global solutions BENEFITING THE CLIENT • Service excellence • Time to market • New products and services 2010: A Year of Transition – Initiated Ops and IT Transformation Program Expect to Save Between $575M and $625M by the End of 2014 |

12 Building from Strength 2010: A Year of Transition $ in millions 12/31/10 1 12/31/09 1 % Change Operating-basis revenue $8,714 $8,138 +7.1% Operating-basis expenses $6,176 $5,667 + 9.0% Operating-basis EPS $3.40 $3.32 +2.4% Operating-basis ROE 10.4% 12.6% -220 bps FOR THE TWELVE MONTHS ENDED • Responded effectively to the global financial crisis • Strengthened capital position • Deepened client relationships • Expanded market share • Launched Ops and IT Transformational Program 1 Financial data presented on an operating or non-GAAP basis (which is adjusted to exclude, among other things, discount accretion). For a description of GAAP to operating-basis results, and related reconciliations, please see the Appendix on State Street’s website (www.statestreet.com) or State Street‘s current Report on Form 8-K filed with the SEC on the date hereof. |

13 Strategic Direction |

14 Building from Strength Strategic Direction – Secular Trends Support Growth GLOBALIZATION • Asset managers increasingly invest beyond their borders • Asset management industry globalizing product and distribution strategies RETIREMENT SAVINGS • Driven by demographics, especially in Europe and Asia • Evolution of retirement / savings schemes OUTSOURCING • Growing global trend driven by complexity, cost and risk management • Expanding into middle and front office CONSOLIDATION • Non-core activity for universal banks • Increasing requirement for global capabilities |

15 Year ended 12/31/00 2 Year ended 12/31/10 % Change Operating-basis revenue $3.45B $8.71B +152% Operating-basis non-US revenue $0.94B $3.18B +238% Employees 3 17,281 28,670 +66% Non-US employees 3 3,463 12,518 +261% Building from Strength 1 Financial data presented on an operating-basis (which is adjusted to exclude, among other things, discount accretion). For a description of operating-basis revenue and related reconciliations, see State Street’s website (www.statestreet.com) or State Street’s current report on Form 8-K filed with the SEC on the date hereof. 2 Data exclude the revenue and employees associated with the Corporate Trust and Private Asset Management businesses divested in 2002 and 2003, respectively. 3 At period end. Strategic Direction – Globalization1 |

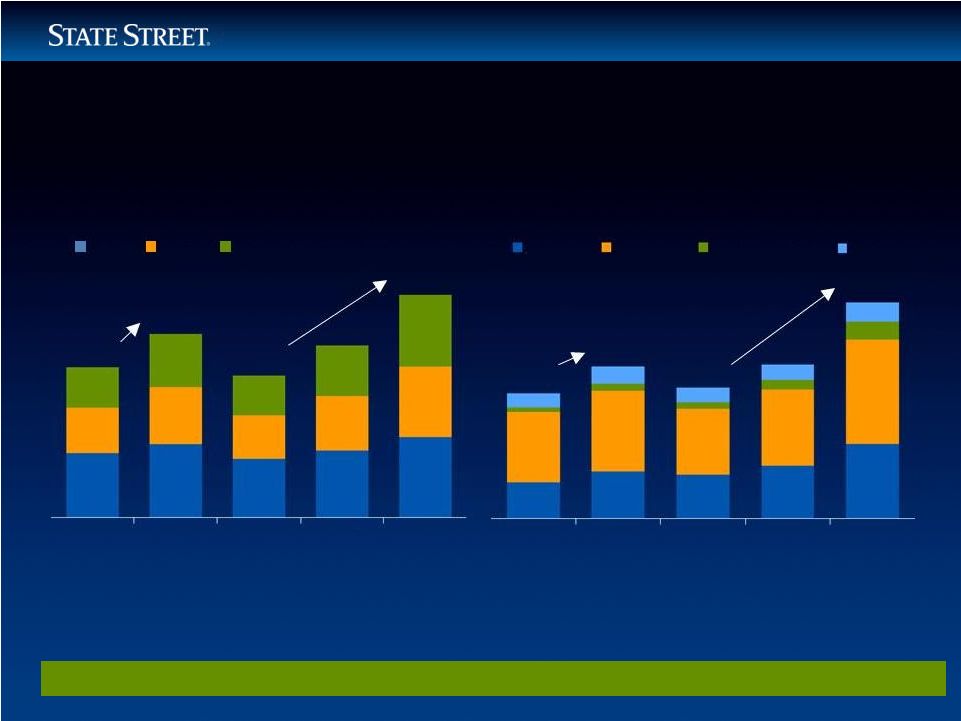

16 Building from Strength Non-US Retirement Growth US Retirement Growth $13.6T $16.6T $12.8T $15.6T $20.1T 10.5% CAGR 7.8% CAGR $6.6T $8.1T $7.0T $8.1T $11.3T 10.8% CAGR 8.3% CAGR Almost 50% of expected retirement asset growth (2008 – 2014) will come from Europe Strategic Direction – Retirement Savings Global Retirement Assets are Expected to Grow 32% ($7.7 Trillion) from 2010 through 2014 Source: Cerulli Associates “Global Markets 2010” statistics DC and IRA assets will lead US retirement growth, with 8.6% and 10.1% expected CAGRs (2008 – 2014) DB DC IRA 2005 2007 2008 2010E 2014F 2005 2007 2008 2010E 2014F APAC Europe Latin America Other |

17 Building from Strength INVESTMENT MANAGER OPERATIONS OUTSOURCING • Leading provider with more than $7 trillion of AUA • Market sized at approximately $53 trillion 1 HEDGE FUND SERVICING • Second largest servicer in the world 2 with about $470 billion 3 of AUA in hedge fund assets • Market sized at $1.7 trillion 4 and growing at an estimated 19% CAGR through 2013 5 INVESTMENT MANAGEMENT SOLUTIONS • Customized strategic and tactical asset allocation solutions through flexible and efficient portfolio implementation across and within global asset classes Strategic Direction – Outsourcing 1 Pension & Investment,/Watson Wyatt World 500, 12/28/09. 2 ICFA Annual Fund Administration Survey, 2010. 3 As of March 31, 2011. 4 Hedge Fund Research, 3/31/10. 5 McKinsey, 7/09. |

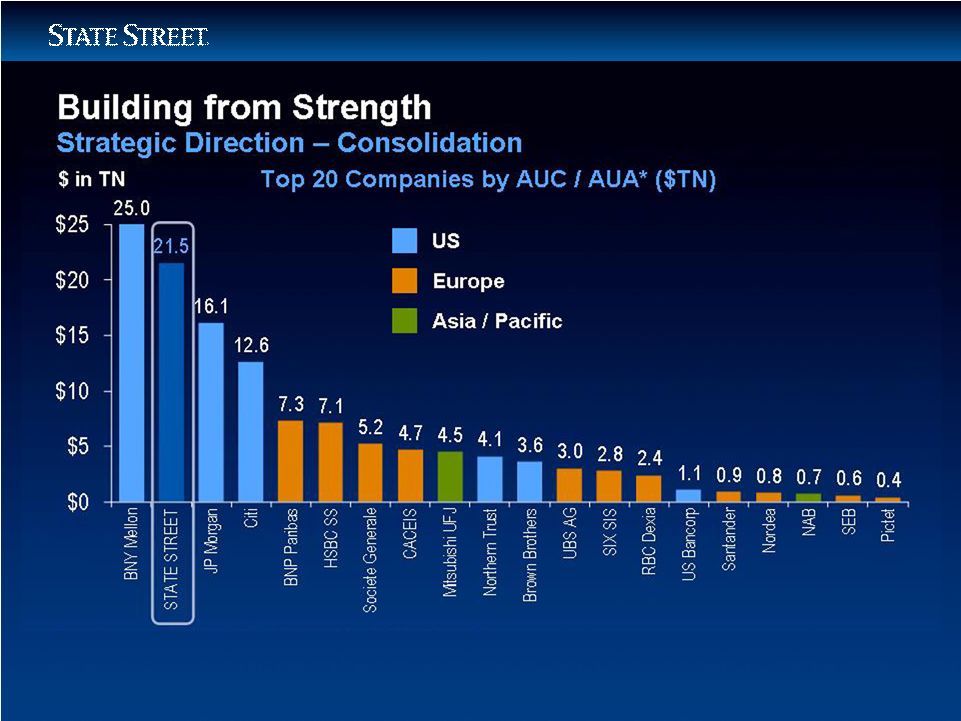

18 Source: Company reports, Global Custody.net, Institutional Investor Global Custodian Survey. * Data for BNY, State Street, & CACEIS reflect AUA as of 12/31/2010; as of 9/30/10 for, BNP Paribas, Societe Generale, & Brown Brothers; as of 6/30/10 for RBC Dexia & HSBC ; all others reflect AUC data: JP Morgan, Citi, & Northern Trust as of 12/31/10; Nordea, NAB, & SEB as of 9/30/10; Pictet as of 6/30/10; Mitsubishi, UBS, SIX SIS, & Santander: as of 3/31/10. |

19 Investing in Communities and Corporate Social Responsibility |

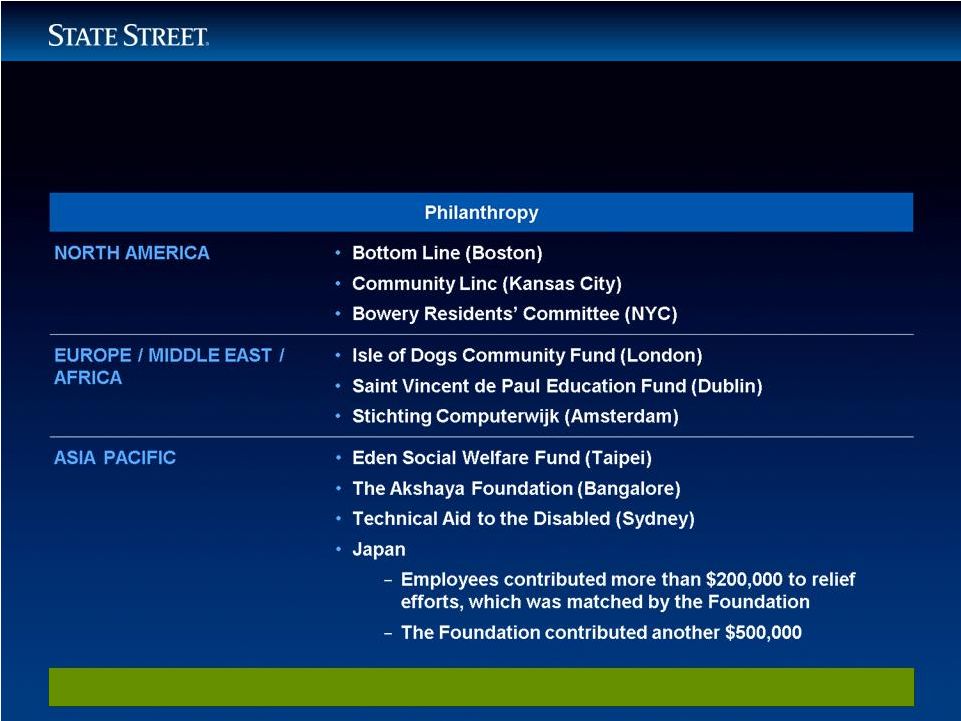

Building from Strength Investing in Communities and Corporate Social Responsibility Provided 619 Grants Worldwide 20 |

21 Building from Strength Investing in Communities and Corporate Social Responsibility Volunteerism PROJECTS INCLUDED • Environmental cleanups • Food sorting and service • Distance and web-based volunteerism • Youth Mentoring • Support Pledge-a-thons EXECUTIVES ACTIVE WITH MANY NON-PROFIT ORGANIZATIONS INCLUDING • Boys & Girls Club of Boston • Boston Partners in Education • Boston Symphony Orchestra • Earthwatch Institute • Women’s Lunch Place • Oxfam Hong Kong • Urban League of Eastern Massachusetts 78,000 Volunteer Hours Dedicated by State Street Employees and Alumni |

22 Building from Strength CORPORATE RESPONSIBILITY PRACTICES Organization Ranking Newsweek Magazine: Greenest US Companies No. 35 of Top 500 Carbon Disclosure Project First time on S&P 500 Business Leadership Index Dow Jones Sustainability World and North America Indices One of only three U.S. financial services companies listed on both indices CR Magazine’s 100 Best Corporate Citizens One of only three financial services companies listed • Established new Executive Corporate Responsibility Committee • Recent accolades include: Annual CSR Report One of the Only Independently Verified Reports Among US-based Financial Services Firms Investing in Communities and Corporate Social Responsibility |

23 2011: Progress |

24 Building from Strength 2011: Progress – Recent Update CAPITAL DEPLOYMENT DIVIDEND PAYOUT • Announced increase in quarterly dividend to $0.18 per share at a 20% payout ratio SHARE REPURCHASE PROGRAM • Board approved up to $675M in share purchase program for 2011 BUSINESS INVESTMENTS • Fund organic growth • Continue to evaluate accretive acquisition opportunities to expand our global footprint, accelerate our growth, and extend our product capabilities |

25 Building from Strength $ in millions, except per share data Q1 2011 1 Q1 2010 1 Change Operating-basis revenue $2,330 $2,116 +10.1% Operating-basis expenses $1,683 $1,566 +7.5% Operating-basis EPS $0.88 $0.75 +17.3% Operating-basis ROE 9.9% 10.0% -10 bps Positive operating leverage 2 260 bps 2011: Progress – Recent Update Q1 2011 COMPARED TO Q1 2010 1 Financial data presented on an operating basis (which is adjusted to exclude, among other things, discount accretion). For a description of GAAP to operating-basis results, and related reconciliations, please see the Appendix on State Street’s website (www.statestreet.com) or State Street‘s current Report on Form 8-K filed with the SEC on the date hereof. 2 Operating leverage represents the difference between the growth rate of total revenue and the growth rate of total expenses, each determined on an operating basis. |

26 Building from Strength STT +15% S & P Fin. +8% BK 0% NTRS -7% Strong Annual Share Performance Bank of New York Mellon Corp. Northern Trust Corp. S&P 500 / Financials State Street Corp. |

27 Building from Strength Delivering Long-Term Shareholder Value Summary Successfully Transitioned Through Crisis in 2010 Well-Positioned Against Secular Growth Trends Financial and Capital Strength Executing our Strategic Plan |

28 |

29 |