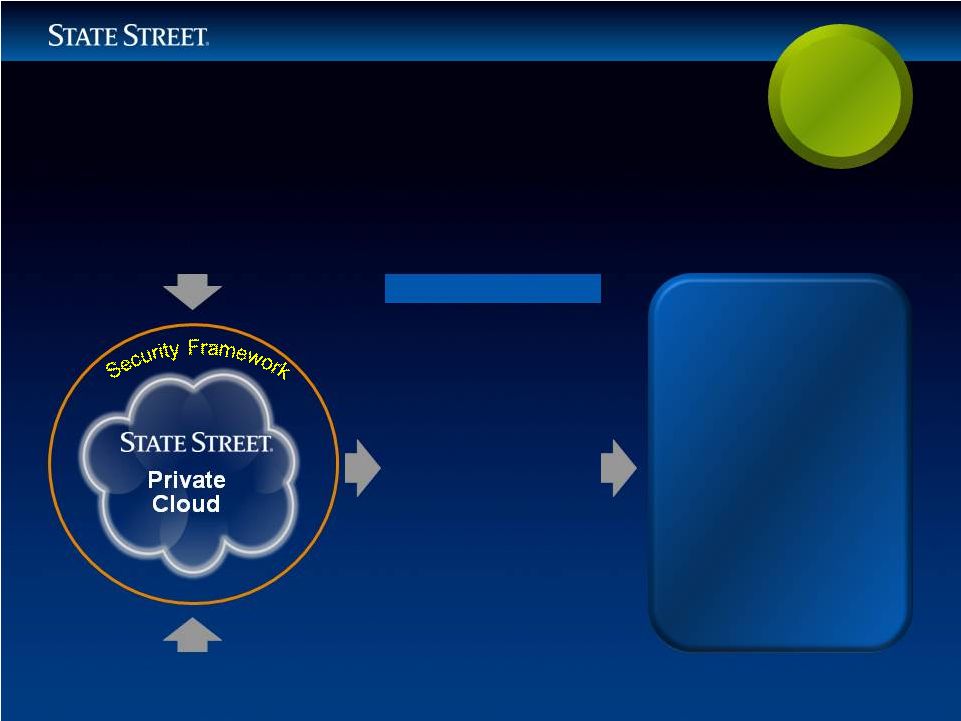

3 Forward-looking Statements This presentation contains forward-looking statements as defined by United States securities laws, including statements relating to our financial, operational, strategic, commercial, technological and other goals and expectations regarding our Business Operations and Information Technology Transformation program, as well as regarding other goals and expectations for our business, financial and capital condition, results of operations, operating margins, strategies and the business environment. Forward-looking statements are often, but not always, identified by such forward-looking terminology as "plan," "expect," "look," "believe," "anticipate," "estimate," "seek," "may," "will," "trend," "target,” and "goal," or similar statements or variations of such terms. These statements are not guarantees of future performance, are inherently uncertain, are based on current assumptions that are difficult to predict and involve a number of risks and uncertainties. Therefore, actual outcomes and results may differ materially from what is expressed in those statements, and those statements should not be relied upon as representing our expectations or beliefs as of any date subsequent to December 7, 2011. Important factors that may affect future results and outcomes include, but are not limited to: delays or difficulties in the execution of our previously announced business operations and information technology transformation program, which could lead to changes in our estimates of the charges, expenses or savings associated with the planned program, resulting in increased volatility of our earnings; our ability to control operating risks, data security breach risks, information technology systems risks and outsourcing risks, and our ability to protect our intellectual property rights, the possibility of errors in the quantitative models we use to manage our business and the possibility that our controls will prove insufficient, fail or be circumvented; the potential for new products and services to impose additional costs on us and expose us to increased operational risk; the manner in which the Federal Reserve and other regulators implement the Dodd- Frank Act and other regulatory initiatives in the U.S. and internationally, including any increases in the minimum regulatory capital ratios applicable to us and regulatory developments that result in changes to our operating model or other changes to the provision of our services in order to comply with or respond to such regulations; required regulatory capital ratios under Basel II and Basel III, in each case as fully implemented by State Street and State Street Bank (and in the case of Basel III, when finally adopted by the Federal Reserve), which may result in the need for substantial additional capital or increased levels of liquidity in the future; changes in law or regulation that may adversely affect our, our clients’ or our counterparties’ business activities and the products or services that we sell, including additional or increased taxes or assessments thereon, capital adequacy requirements and changes that expose us to risks related to compliance; financial market disruptions and the economic recession, whether in the U.S. or internationally; the liquidity of the U.S. and international securities markets, particularly the markets for fixed- income securities, and the liquidity requirements of our clients; increases in the volatility of, or declines in the levels of, our net interest revenue, changes in the composition of the assets on our consolidated balance sheet and the possibility that we may be required to change the manner in which we fund those assets; the financial strength and continuing viability of the counterparties with which we or our clients do business and to which we have investment, credit or financial exposure; the credit quality, credit agency ratings, and fair values of the securities in our investment securities portfolio, a deterioration or downgrade of which could lead to other-than-temporary impairment of the respective securities and the recognition of an impairment loss in our consolidated statement of income; the maintenance of credit agency ratings for our debt and depository obligations as well as the level of credibility of credit agency ratings; the results of, and costs associated with, government investigations, litigation and similar claims, disputes, or proceedings; the risks that acquired businesses will not be integrated successfully, or that the integration will take longer than anticipated, that expected synergies will not be achieved or unexpected disynergies will be experienced, that client and deposit retention goals will not be met, that other regulatory or operational challenges will be experienced and that disruptions from the transaction will harm relationships with clients, employees or regulators; the ability to complete acquisitions, divestitures and joint ventures, including the ability to obtain regulatory approvals, the ability to arrange financing as required and the ability to satisfy closing conditions; the performance of and demand for the products and services we offer, including the level and timing of redemptions and withdrawals from our collateral pools and other collective investment products; the possibility that our clients will incur substantial losses in investment pools where we act as agent, and the possibility of significant reductions in the valuation of assets; our ability to attract deposits and other low-cost, short-term funding; potential changes to the competitive environment, including changes due to the effects of consolidation, and perceptions of State Street as a suitable service provider or counterparty; the level and volatility of interest rates and the performance and volatility of securities, credit, currency and other markets in the U.S. and internationally; our ability to measure the fair value of the investment securities on our consolidated balance sheet; adverse publicity or other reputational harm; our ability to grow revenue, attract and/or retain and compensate highly skilled people, control expenses and attract the capital necessary to achieve our business goals and comply with regulatory requirements; changes in accounting standards and practices; and changes in tax legislation and in the interpretation of existing tax laws by U.S. and non-U.S. tax authorities that affect the amount of taxes due. Other important factors that could cause actual results to differ materially from those indicated by any forward-looking statements are set forth in our 2010 Annual Report on Form 10-K and our subsequent SEC filings. We encourage investors to read these filings, particularly the sections on risk factors, for additional information with respect to any forward-looking statements and prior to making any investment decision. The forward-looking statements contained in this presentation speaks only as of the date hereof, December 7, 2011, and we do not undertake efforts to revise those forward-looking statements to reflect events after that date. Among the initiatives incorporated within Business Operations and Information Technology Transformation program, we are standardizing several core business and information technology processes, primarily through the execution of Lean efficiency principles and increased automation. We are also creating a new technology platform, including moving many core software applications to a private cloud. In addition, we are planning additional servicing and processing centers of excellence in globally distributed low-cost locations to improve the work allocation and responsiveness of service demands and have also expanded our relationships with strategic information technology service providers to enhance efficiencies. |