| O L S H A N | PARK AVENUE TOWER ● 65 EAST 55TH STREET ● NEW YORK, NEW YORK 10022 TELEPHONE: 212.451.2300 ● FACSIMILE: 212.451.2222 |

EMAIL: MNEIDELL@OLSHANLAW.COM

DIRECT DIAL: 212.451.2230

November 9, 2012

VIA EDGAR AND ELECTRONIC MAIL

David L. Orlic, Esq.

Special Counsel

United States Securities and Exchange Commission

Office of Mergers and Acquisitions

Mail Stop 3628

100 F Street, N.E.

Washington, D.C. 20549

| Re: | Cracker Barrel Old Country Store, Inc. |

| Definitive Additional Proxy Soliciting Materials |

| Filed on October 25, 2012 by Biglari Holdings Inc. (“Biglari”) |

| File No. 001-25225 |

Dear Mr. Orlic:

We acknowledge receipt of the letter of comment dated October 26, 2012 from the Staff (the “Comment Letter”) with regard to the above-referenced matter. We are providing the following response on behalf of Biglari. Our responses are numbered to correspond to your comments.

General

| 1. | Please provide support for the assertion that your nominees will bring to the board of directors “experience in engineering an operational turnaround” and “a history of generating shareholder value at Biglari Holdings.” |

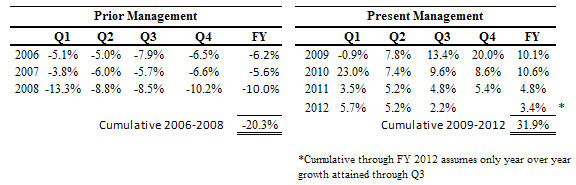

Since Mr. Biglari assumed the position of Chief Executive Officer of Biglari in August 2008, he has led a major turnaround of the Steak n Shake restaurant chain, a wholly-owned subsidiary of Biglari. Prior to that time, Steak n Shake had struggled through 13 consecutive quarters of declines in same-store traffic. The following tables show the turnaround in customer traffic after Mr. Biglari assumed the CEO position in August 2008:

| O L S H A N F R O M E W O L O S K Y L L P | WWW.OLSHANLAW.COM |

November 9, 2012

Page 2

Same-Store Traffic

The complete transformation of Steak n Shake’s business, which required drastic changes in strategy, operations and culture, is well-recognized in the industry. In 2010, Steak n Shake received from Nations Restaurant News the coveted Golden Chain Award in 2010, an accolade annually given to only a few top chains.

In addition, when Mr. Biglari assumed the CEO position on August 5, 2008, Biglari’s stock was $144.00 (split adjusted) and the S&P 500 Index stood at 1,285. As of October 31, 2012, Biglari’s stock price was $353.61 versus 1,412 for the S&P 500, representing an increase of 145.6% for Biglari’s stock price since Mr. Biglari assumed the CEO position, compared to an increase of only 9.9% for the S&P 500 in the same period.

| 2. | We note your response to the first bullet point of prior comment 1. We also note your statements on page 10 that Biglari Holdings is a “diversified holding company” and that Cracker Barrel falls into the “pile of a partially-owned business.” We continue to request support for these assertions, noting, as in our prior comment, that 99.5% of your net revenues for fiscal 2011 appear to have come from just two operations, both in the restaurant industry and both wholly owned by you. |

Biglari believes that focusing solely on its current sources of revenue to characterize Biglari as being in the business of acquiring restaurant companies, as Cracker Barrel incorrectly maintains, presents an inaccurate characterization of Biglari’s business. The essence of Cracker Barrel’s claim that Biglari is “a restaurant acquisition vehicle” is forward-looking in nature, i.e., that “Sardar Biglari’s true intentions may be to take control of Cracker Barrel.” In Biglari’s view, these claims represent unfounded statements of Biglari’s intention to focus reinvestment and acquisition activity on the restaurant industry. While its restaurant business is currently its core business, Biglari’s public disclosures consistently refute this erroneous notion, such as the following statement from Mr. Biglari’s 2011 Chairman’s letter:

“We focus on cash generating companies, and we seek redeployment of cash to add to a varied collection of businesses. It is apparent where the source of the cash is currently coming from — restaurant operations and investment management — but it is unclear where the funds will be going for reinvestment. We feel certain that our redeployment of capital to other industries over time will dwarf our current exposure to the restaurant business.” (Emphasis added)

November 9, 2012

Page 3

Biglari is neither required nor inclined to reinvest the funds generated by its operating businesses in other restaurant companies. Cracker Barrel’s implications that Biglari is seeking to reinvest such funds in the restaurant industry are therefore false and misleading.

Furthermore, as reported in the Form 13F filed by Biglari on August 14, 2012, as of June 30, 2012, Biglari holds substantial non-controlling interests (i.e., “partially-owned businesses”) in the common stock of a number of companies, including Berkshire Hathaway Inc., a holding company owning subsidiaries engaged in a number of diverse business activities, CCA Industries Inc., a manufacturer and distributer of health and beauty aid products, and Goldman Sachs Group Inc., a global investment banking, securities and investment management firm. Unrealized gains/losses on investments held by Biglari are not included in net revenues.

* * *

November 9, 2012

Page 4

The Staff is invited to contact the undersigned with any comments or questions it may have.

| Sincerely, |

| /s/ Michael R. Neidell |

| Michael R. Neidell |