UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07255

Oppenheimer International Bond Fund

(Exact name of registrant as specified in charter)

6803 South Tucson Way, Centennial, Colorado 80112-3924

(Address of principal executive offices) (Zip code)

Arthur S. Gabinet

OFI Global Asset Management, Inc.

Two World Financial Center, New York, New York 10281-1008

(Name and address of agent for service)

Registrant’s telephone number, including area code: (303) 768-3200

Date of fiscal year end: September 30

Date of reporting period: 9/30/2013

Item 1. Reports to Stockholders.

ANNUAL REPORT 9.30.2013 OPPENEIMER INTERNATIOL BOND FUND OPPENHEIMER FUND THE RIGHT WAY TO INVEST

Table of Contents

Class A Shares

AVERAGE ANNUAL TOTAL RETURNS AT 9/30/13

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Class A Shares of the

Fund | | | | | | | | | | | | | |

| | | | | | | | | | | | JPMorgan | | | | | | | |

| | | | | | | | | Citigroup | | | Government | | | JPMorgan | | | | |

| | | Without | | | With | | | Non-U.S. | | | Bond Index- | | | Emerging | | | | |

| | | Sales | | | Sales | | | Dollar World | | | Emerging | | | Markets Bond | | | Reference | |

| | | Charge | | | Charge | | | Government | | | Markets | | | Index Global | | | Index | |

| | | | | | | | | Bond Index | | | Global | | | Diversified | | | | |

| | | | | | | | | | | | Diversified | | | | | | | |

| 1-Year | | | -2.77 % | | | | -7.39 % | | | | -5.65 % | | | | -3.74 % | | | | -4.06 % | | | | -4.67 % | |

| 5-Year | | | 5.68 | | | | 4.66 | | | | 4.27 | | | | 7.28 | | | | 9.75 | | | | 6.01 | |

| 10-Year | | | 7.28 | | | | 6.76 | | | | 4.91 | | | | 10.05 | | | | 8.46 | | | | 6.62 | |

Performance data quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Fund returns include changes in share price, reinvested distributions, and a 4.75% maximum applicable sales charge except where “without sales charge” is indicated. Current performance may be lower or higher than the performance quoted. Returns do not consider capital gains or income taxes on an individual’s investment. For performance data current to the most recent month-end, visit oppenheimerfunds.com or call 1.800.CALL OPP (225.5677).

2 OPPENHEIMER INTERNATIONAL BOND FUND

Fund Performance Discussion

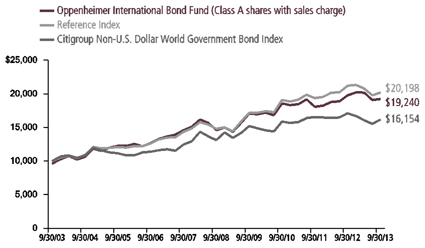

The Fund’s Class A shares (without sales charge) produced a total return of -2.77% during the 12-month reporting period. On a relative basis, the Fund outperformed its Reference Index, a customized weighted index currently comprised of 50% of the Citigroup Non-U.S. Dollar World Government Bond Index, 30% of the JPMorgan Government Bond Index - Emerging Markets Global Diversified, and 20% of the JPMorgan Emerging Markets Bond Index Global Diversified, which returned -4.67%.

MARKET OVERVIEW

Global economic sentiment was undermined early in the reporting period by a number of concerns, most notably lingering, yet diminished, debt concerns in Europe, economic slowdowns in China and other emerging markets, and high unemployment and muted housing recovery in the United States. However, investor optimism was boosted when central banks throughout the globe announced new accommodative policy measures intended to stimulate greater economic growth. The Federal Reserve (the “Fed”) continued open-ended quantitative

easing involving monthly purchases of mortgage-backed securities issued by U.S. government agencies, and the European Central Bank (the “ECB”) signaled its intention to purchase massive amounts of debt from troubled members of the European Union. In China, a new government was widely expected to adopt less restrictive monetary and fiscal policies. Even in Japan, which had been mired in economic weakness for years, new government leadership adopted economic policies and the central bank announced massive quantitative easing.

COMPARISON OF CHANGE IN VALUE OF $10,000 HYPOTHETICAL INVESTMENTS IN:

3 OPPENHEIMER INTERNATIONAL BOND FUND

In this environment, emerging market bonds performed well over the first half of the reporting period as economic concerns about a China slowdown abated, and as quantitative easing globally pushed investors into products that can potentially provide more yield. For U.S. residents, U.S. dollar-denominated securities outperformed their local currency-denominated counterparts as governments in Japan and Europe took steps to reduce the value of the yen and euro, respectively, relative to the U.S. dollar.

At the end of May, market volatility picked up measurably as comments from Fed Chairman Ben Bernanke at a Congressional hearing surprised the market when he indicated a possible slowdown of the central bank’s asset purchase program if the economy continued to show improvement. Fears about a possible slowdown in the word’s emerging economies were exacerbated by the prospect of quantitative easing, which has been a steady source of liquidity, coming to an end. As a result, risk assets sold off across the board, with Japanese stocks and emerging market debt absorbing the brunt of the selling, although investment grade credit was certainly not immune. Simultaneously, the intermediate and long-end of the U.S. Treasury curve steepened quite dramatically as investors began to price in the likelihood of higher interest rates in the future.

The final quarter of the reporting period marked a transition from expectations of tapering “very soon” to “tapering sometime later”, and this presented varying outcomes

for fixed-rate, duration-sensitive debt markets. U.S ten-year Treasury yields, which had risen to about 3.00%, rallied back closer to 2.60% as the prospects for Fed tapering abated when the Federal Open Market Committee (FOMC) decided to maintain its quantitative easing measures. A combination of Fed jaw-boning and the ascent of dovish Janet Yellen as a likely successor to Ben Bernanke were among the factors leading to lower U.S. yields. Not all debt markets recovered as strongly, however. Emerging market debt and high yield bonds did improve from their second quarter 2013 tail-spin, but neither has recovered fully yet.

FUND REVIEW

The Fund’s outperformance this reporting period was driven by its developed market debt strategies. In particular, we maintained a near zero allocation to the Japanese yen and favored the U.S. dollar. Our underweight position in the yen benefited the Fund as the introduction of quantitative easing in Japan pushed the yen lower along with yields on the longer term debt of that nation. A very low euro exposure benefited the Fund over the first half of the period amid ongoing turmoil in the Eurozone, though it hindered performance later in the period. While these underweight positions benefited performance, we also increased our developed market allocation to roughly 51%. This helped performance later in the period when developed markets generally outperformed emerging markets. Much of our re-allocation from emerging markets (particularly emerging market high yield

4 OPPENHEIMER INTERNATIONAL BOND FUND

sovereigns and local currency bonds) to developed markets was redeployed in European corporate debt and securitized assets. We have added banks and financials, transportation, energy, and BBB- and BB-rated industrials, primarily – but not exclusively – from core Europe. Among the names added were Deutsche Bank, Lloyds TSB Bank, Koninklijke KPN (a Dutch telecom company), and Portugal Telecom International Finance.

The performance of the emerging market sleeve presented varied results during a volatile period. Emerging market debt had a rough time after the initial rate rise in U. S. Treasuries. While emerging market countries linked to a modestly improving European economy fared better, those in Latin America and Asia that harbor high current account deficits, slackening economies, or that face political unrest, continued to swoon but at a more gradual rate than previously. Many of the nations that appeared to benefit from the Fed’s extraordinarily accommodative stance performed poorly when tapering fears peaked, and then rebounded somewhat in terms of the prices of their debt and currencies as tapering talk abated. Nevertheless, valuations in many cases now seem cheap, broadly speaking.

For the Fund, emerging market debt denominated in local currency was the most significant detractor from relative performance during the one-year reporting period, whereas U.S-dollar denominated emerging market debt outperformed. The

greatest detractor from performance was Turkey, where civil unrest broke out during the period. Venezuela and Ukraine U.S.- dollar denominated debt also hurt performance this period. Our limited exposure to Indonesia helped performance relative to the Reference Index. As mentioned earlier, we decreased our allocation to emerging markets debt during the reporting period, and increased our exposure to developed markets.

STRATEGY & OUTLOOK

Spikes in market volatility may be difficult to stomach although such potential “value creation events” do seem to be more common since 2008. The second quarter sell-off of international bonds was acute, and its repercussions did not fully dissipate as the third quarter progressed. While we continue to believe that the U.S. dollar is likely to remain relatively strong in the near term, the outsized spike in emerging market debt yields is not fully justified, in our view. To the extent that fast money has pushed the less liquid emerging market debt and domestic high yield bonds around in this “duration aversion shock”, we expect fundamentals to reassert themselves as 2013 comes to a close. The abrupt change in market sentiment did lay bare some fundamental challenges to countries with high current account deficits – challenges that a prolonged period of easy money in the U.S. may have masked to some degree. Washington’s debt ceiling imbroglio and posturing over the Affordable Care Act (often referred to as Obamacare) does not provide for calmer markets as we enter the fourth quarter.

5 OPPENHEIMER INTERNATIONAL BOND FUND

During periods of underperformance it is good to ask what has changed and what has not changed. Clearly, the Fed is closer but not quite ready to reduce its stimulative measures as the domestic economy expands; yet, the amount of liquidity injected by Japan into global capital markets would be expected to replenish much of what the Fed may remove. We expect Japan to be a source of meaningful liquidity for some time, and we note that both the Bank of England’s and the ECB’s forward guidance, if you will, will remain dovish. Australia is in easing mode, and only Brazil, and a few emerging market countries are in true tightening mode. China’s clamp-down on credit expansion is warranted, in our view, and unlikely to lead to an unreasonable contraction. While most emerging market economies are below trend growth, GDP is positive and likely to improve with the recovery in the U.S. and Europe. Moreover, we are witnessing signs that the recession in Europe has ended as the troubled continental economy may continue its moderate expansion. The outcome of the recession in Europe has ended as the troubled

1. Hemant Baijal became Portfolio Manager on January 28, 2013.

continental economy may continue its moderate expansion. The outcome of the upcoming U.S. debt ceiling debate could potentially cause a disruption in world economic growth should there be a prolonged period of time before a resolution.

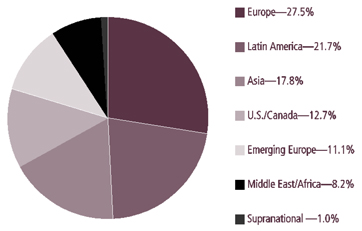

At period end, the Fund had a roughly 51.2% allocation to developed markets, 24.5% to emerging markets denominated in U.S. dollars and 19.9% to emerging markets denominated in local currencies. After hedging, the Fund had a roughly 55% allocation to U.S. dollar exposure. We added high-grade emerging market sovereign debt at the expense of high-yield sovereign debt, and we look to add to European credit and securitized assets up to about 5%. The Fund’s overall duration remained shorter than its Reference Index. Our aversion to the yen is intact, but at period end we now have a roughly 1.2% exposure, and we remain underweight the euro with an approximate 13.3% allocation. Overall, the Fund is focused on diversified sources of risk-adjusted carry, or additional yield, by maintaining positions that boost income above that of the Reference Index – a strategy that will reap rewards in a low or moderate volatility environment in our view.

6 OPPENHEIMER INTERNATIONAL BOND FUND

Top Holdings and Allocations

TOP TEN GEOGRAPHICAL HOLDINGS

| | | | | | |

United States | | | 11 .8 | % | | |

Japan | | | 9 .3 | | | |

Mexico | | | 8 .7 | | | |

Russia | | | 7 .2 | | | |

Brazil | | | 7 .1 | | | |

United Kingdom | | | 6 .1 | | | |

Italy | | | 4 .9 | | | |

Germany | | | 4 .8 | | | |

France | | | 4 .4 | | | |

Australia | | | 3 .8 | | | |

| |

| Portfolio holdings and allocation are subject to change. Percentages are as of September 30, 2013, and are based on total market value of investments. | | | |

REGIONAL ALLOCATION

Portfolio holdings and allocations are subject to change. Percentages are as of September 30, 2013, and are based on the total market value of investments. Portfolio holdings and allocations are subject to change. Percentages are as of September 30, 2013, and are based on the total market value of investments.

7 OPPENHEIMER INTERNATIONAL BOND FUND

Share Class Performance

AVERAGE ANNUAL TOTAL RETURNS WITHOUT SALES CHARGE AS OF 9/30/13

| | | | | | | | | | |

| | | Inception Date | | 1-Year | | 5-Year | | | | 10-Year |

| Class A (OIBAX) | | 6/15/95 | | -2.77% | | 5.68% | | | | 7.28% |

| Class B (OIBBX) | | 6/15/95 | | -3.46% | | 4.78% | | | | 6.76% |

| Class C (OIBCX) | | 6/15/95 | | -3.30% | | 4.95% | | | | 6.53% |

| Class I (OIBIX) | | 1/27/12 | | -2.31% | | 1.93% | | * | | N/A |

| Class N (OIBNX) | | 3/1/01 | | -3.16% | | 5.24% | | | | 6.85% |

| Class Y (OIBYX) | | 9/27/04 | | -2.36% | | 5.99% | | | | 7.28% * |

|

AVERAGE ANNUAL TOTAL RETURNS WITH SALES CHARGE AS OF 9/30/13 |

| | | Inception Date | | 1-Year | | 5-Year | | | | 10-Year |

| Class A (OIBAX) | | 6/15/95 | | -7.39% | | 4.66% | | | | 6.76% |

| Class B (OIBBX) | | 6/15/95 | | -8.12% | | 4.45% | | | | 6.76% |

| Class C (OIBCX) | | 6/15/95 | | -4.23% | | 4.95% | | | | 6.53% |

| Class I (OIBIX) | | 1/27/12 | | -2.31% | | 1.93% | | * | | N/A |

| Class N (OIBNX) | | 3/1/01 | | -4.09% | | 5.24% | | | | 6.85% |

| Class Y (OIBYX) | | 9/27/04 | | -2.36% | | 5.99% | | | | 7.28% * |

* Shows performance since inception. | | | | | | | | |

STANDARDIZED YIELDS

| | | | | | |

| |

| For the 30 Days Ended 9/30/13 | | | |

| Class A | | | 3 .47 | % | | |

| Class B | | | 2 .81 | % | | |

| Class C | | | 2 .98 | % | | |

| Class I | | | 4 .11 | % | | |

| Class N | | | 3 .79 | % | | |

| Class Y | | | 3 .90 | % | | |

Performance data quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. Returns do not consider capital gains or income taxes on an individual’s investment. For performance data current to the most recent month-end, visit oppenheimerfunds.com or call 1.800.CALL OPP (225.5677). Fund returns include changes in share price, reinvested distributions, and the applicable sales charge (unless otherwise indicated): for Class A shares, the current maximum initial sales charge of 4.75%; for Class B shares, the contingent deferred sales charge of 5% (1-year) and 2% (5-year); and for Class C and N shares, the contingent deferred sales charge of 1% for the 1-year period. There is no sales charge for Class I and Class Y shares. Because Class B shares convert to Class A shares

8 OPPENHEIMER INTERNATIONAL BOND FUND

72 months after purchase, the 10-year return for Class B shares uses Class A performance for the period after conversion. Returns for periods of less than one year are cumulative and not annualized.

Standardized yield is based on net investment income for the 30-day period ended 9/30/13 and the maximum offering price at the end of the period for Class A shares and the net asset value for Class B, Class C, Class I, Class N and Class Y shares. Each result is compounded semiannually and then annualized. Falling share prices will tend to artificially raise yields.

The Fund’s performance is compared to the Citigroup Non-U.S. Dollar World Government Bond Index, JPMorgan Government Bond Index - Emerging Markets Global Diversified, the JPMorgan Emerging Markets Bond Index Global Diversified, and the Fund’s Reference Index. The Citigroup Non-U.S. Dollar World Government Bond Index is an index of fixed rate government bonds with maturities of one year or longer. The JPMorgan Government Bond Index - Emerging Markets Global Diversified is a comprehensive, global local Emerging Markets Index, and consists of regularly traded, liquid fixed-rate, domestic currency government bonds to which international investors can gain exposure. The JPMorgan Emerging Markets Bond Index Global Diversified tracks total returns for U.S. dollar-denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities: Brady bonds, loans, Eurobonds. The Fund’s Reference Index is a customized weighted index currently comprised of 50% of the Citigroup Non-U.S. Dollar World Government Bond Index, 30% of the JPMorgan Government Bond Index - Emerging Markets Global Diversified, and 20% of the JPMorgan Emerging Markets Bond Index Global Diversified. The indices are unmanaged and cannot be purchased directly by investors. Index performance includes reinvestment of income, but does not reflect transaction costs, fees, expenses or taxes. Index performance is shown for illustrative purposes only as a benchmark for the Fund’s performance, and does not predict or depict performance of the Fund. The Fund’s performance reflects the effects of the Fund’s business and operating expenses.

The Fund’s investment strategy and focus can change over time. The mention of specific fund holdings does not constitute a recommendation by OppenheimerFunds, Inc. or its affiliates.

Before investing in any of the Oppenheimer funds, investors should carefully consider a fund’s investment objectives, risks, charges and expenses. Fund prospectuses and summary prospectuses contain this and other information about the funds, and may be obtained by asking your financial advisor, visiting oppenheimerfunds.com, or calling 1.800.CALL OPP (225.5677). Read prospectuses and summary prospectuses carefully before investing.

Shares of Oppenheimer funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency, and involve investment risks, including the possible loss of the principal amount invested.

9 OPPENHEIMER INTERNATIONAL BOND FUND

Fund Expenses

Fund Expenses. As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments, contingent deferred sales charges on redemptions; and (2) ongoing costs, including management fees; distribution and service fees; and other Fund expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000.00 invested at the beginning of the period and held for the entire 6-month period ended September 30, 2013.

Actual Expenses. The first section of the table provides information about actual account values and actual expenses. You may use the information in this section for the class of shares you hold, together with the amount you invested, to estimate the expense that you paid over the period. Simply divide your account value by $1,000.00 (for example, an $8,600.00 account value divided by $1,000.00 = 8.60), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second section of the table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio for each class of shares, and an assumed rate of return of 5% per year for each class before expenses, which is not the actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example for the class of shares you hold with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front-end or contingent deferred sales charges (loads), or a $12.00 fee imposed annually on accounts valued at less than $500.00 (subject to exceptions described in the Statement of Additional Information). Therefore, the “hypothetical” section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

10 OPPENHEIMER INTERNATIONAL BOND FUND

| | | | | | | | | | | | | | | | | | | | | |

| Actual | | Beginning

Account Value

April 1, 2013 | | Ending Account Value September 30, 2013 | | Expenses Paid During 6 Months Ended

September 30, 2013 |

Class A | | $ | | | | 1,000.00 | | | $ 952.90 | | | $ 4.96 | |

Class B | | | | | | 1,000.00 | | | | | | | 950.10 | | | | | | | 9.14 | |

Class C | | | | | | 1,000.00 | | | | | | | 950.90 | | | | | | | 8.35 | |

Class I | | | | | | 1,000.00 | | | | | | | 954.90 | | | | | | | 2.80 | |

Class N | | | | | | 1,000.00 | | | | | | | 951.20 | | | | | | | 6.87 | |

Class Y | | | | | | 1,000.00 | | | | | | | 955.60 | | | | | | | 3.63 | |

| | | | | | |

Hypothetical | | | | | | | | | | | | | | | | | | | | | |

| (5% return before expenses) | | | | | | | | | | | | | | | | | | | | | |

Class A | | | | | | 1,000.00 | | | | | | | 1,020.00 | | | | | | | 5.13 | |

Class B | | | | | | 1,000.00 | | | | | | | 1,015.74 | | | | | | | 9.44 | |

Class C | | | | | | 1,000.00 | | | | | | | 1,016.55 | | | | | | | 8.63 | |

Class I | | | | | | 1,000.00 | | | | | | | 1,022.21 | | | | | | | 2.89 | |

Class N | | | | | | 1,000.00 | | | | | | | 1,018.05 | | | | | | | 7.11 | |

Class Y | | | | | | 1,000.00 | | | | | | | 1,021.36 | | | | | | | 3.76 | |

Expenses are equal to the Fund’s annualized expense ratio for that class, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). Those annualized expense ratios, excluding indirect expenses from affiliated funds, based on the 6-month period ended September 30, 2013 are as follows:

| | | | | | | |

| Class | | Expense Ratios | | |

Class A | | | | 1.01 | % | | |

Class B | | | | 1.86 | | | |

Class C | | | | 1.70 | | | |

Class I | | | | 0.57 | | | |

Class N | | | | 1.40 | | | |

Class Y | | | | 0.74 | | | |

The expense ratios reflect voluntary waivers and/or reimbursements of expenses by the Fund’s Manager and Transfer Agent. Some of these undertakings may be modified or terminated at any time, as indicated in the Fund’s prospectus. The “Financial Highlights” tables in the Fund’s financial statements, included in this report, also show the gross expense ratios, without such waivers or reimbursements and reduction to custodian expenses, if applicable.

11 OPPENHEIMER INTERNATIONAL BOND FUND

| | | | |

| | |

| | STATEMENTOF INVESTMENTS September 30, 2013 | | |

| | | | | | | | | | |

| | | |

| Principal

Amount |

| | | Valu | e |

| Asset-Backed Securities—0.2% | | | | | | | | | | |

| Axius Europe CLO SA, Series 2007-1X, Cl. E, 4.803%, 11/15/231 | | | | $ | 6,972,613 | | | $ | 8,716,340 | |

| Halcyon Structured Asset Management European CLO BV, Series 2006-IIX, Cl. E, 4.19%, 1/25/231 | | | | | 6,470,000 | | | | 7,561,665 | |

| Stichting Halcyon Structured Asset Management European, Series 2007-IX, Cl. E, 4.134%, 7/24/231 | | | | | 1,654,222 | | | | 1,987,570 | |

| Theseus European CLO SA, Series 2006-1X, Cl. E, 4.343%, 8/27/221 | | | | | 3,505,000 | | | | 4,446,634 | |

| Total Asset-Backed Securities (Cost $21,260,339) | | | | | | | | | 22,712,209 | |

| U.S. Government Obligations—7.2% | | | | | | | | | | |

| U.S. Treasury Bills: | | | | | | | | | | |

| 0.003%, 12/12/133 | | | | | 246,070,000 | | | | 246,053,229 | |

| 0.029%, 11/14/133 | | | | | 175,000,000 | | | | 174,995,275 | |

| 0.029%, 11/7/13 | | | | | 148,890,000 | | | | 148,886,724 | |

| 0.053%, 10/31/133,4 | | | | | 133,810,000 | | | | 133,806,655 | |

| U.S. Treasury Nts., 0.625%, 8/15/16 | | | | | 85,000,000 | | | | 85,076,330 | |

| Total U.S. Government Obligations (Cost $788,637,907) | | | | | | | | | 788,818,213 | |

| Foreign Government Obligations—60.7% | | | | | | | | | | |

| Angola—0.2% | | | | | | | | | | |

| Republic of Angola Via Northern Lights III BV Sr. Unsec. Nts., 7%, 8/16/19 | | USD | | | 24,225,000 | | | | 26,072,156 | |

| Australia—2.8% | | | | | | | | | | |

| New South Wales Treasury Corp. Sr. Unsec. Nts., 6%, Series 19, 4/1/19 | | AUD | | | 15,520,000 | | | | 16,139,419 | |

| Queensland Treasury Corp. Sr. Unsec. Nts.: | | | | | | | | | | |

| Series 19, 6.25%, 6/14/19 | | AUD | | | 19,590,000 | | | | 20,606,332 | |

| Series 21, 6.00%, 6/14/21 | | AUD | | | 134,010,000 | | | | 140,246,482 | |

| Series 22, 6.00%, 7/21/22 | | AUD | | | 6,565,000 | | | | 6,742,982 | |

Victoria Treasury Corp. Sr. Unsec. Nts.: 5.50%, 11/17/26 | | AUD | | | 85,540,000 | | | | 85,194,201 | |

| Series 1224, 5.50%, 12/17/24 | | AUD | | | 18,415,000 | | | | 18,502,403 | |

| Western Australia Treasury Corp. Unsec. Nts., 7%, Series 19, 10/15/19 | | AUD | | | 7,500,000 | | | | 8,111,752 | |

| | | | | | | | | | 295,543,571 | |

| Belgium—1.5% | | | | | | | | | | |

| Kingdom of Belgium Unsec. Bonds, 4.25%, Series 60, 3/28/415 | | EUR | | | 5,055,000 | | | | 7,665,655 | |

| Kingdom of Belgium Bonds, 3.75%, Series 58, 9/28/20 | | EUR | | | 100,000,000 | | | | 151,636,896 | |

| | | | | | | | | | 159,302,551 | |

| Bolivia—0.0% | | | | | | | | | | |

| Plurinational State of Bolivia Sr. Unsec. Nts., 4.875%, 10/29/225 | | USD | | | 2,445,000 | | | | 2,221,894 | |

| Brazil—4.2% | | | | | | | | | | |

| Brazil Minas SPE via State of Minas Gerais Sec. Bonds, 5.333%, 2/15/285 | | USD | | | 12,675,000 | | | | 12,263,062 | |

| Federative Republic of Brazil Letra Tesouro Nacional Sr. Unsec. Nts., 9.029%, 1/1/142 | | BRL | | | 243,910,000 | | | | 107,542,487 | |

| Federative Republic of Brazil Letra Tesouro Nacional Unsec. Nts., 8.897%, 7/1/142 | | BRL | | | 122,850,000 | | | | 51,698,160 | |

12 OPPENHEIMER INTERNATIONAL BOND FUND

| | | | | | | | | | |

| | | | |

| Principal

Amount |

| | | Valu | e |

| Brazil Continued | | | | | | | | | | |

| Federative Republic of Brazil Nota Do Tesouro Nacional Sr. Unsec. Nts., 9.762%, 1/1/17 | | BRL | | | 121,585,000 | | | $ | 53,041,358 | |

| Federative Republic of Brazil Nota Do Tesouro Nacional Unsec. Nts.: | | | | | | | | | | |

| 9.762%, 1/1/14 | | BRL | | | 128,625,000 | | | | 58,048,135 | |

| 9.762%, 1/1/18 | | BRL | | | 76,680,000 | | | | 33,046,438 | |

| 9.762%, 1/1/21 | | BRL | | | 203,440,000 | | | | 85,223,415 | |

| 13.288%, 8/15/506 | | BRL | | | 19,290,000 | | | | 20,322,403 | |

| 13.505%, 5/15/456 | | BRL | | | 21,060,000 | | | | 22,309,716 | |

| Federative Republic of Brazil Sr. Unsec. Nts., 4.875%, 1/22/21 | | USD | | | 12,573,000 | | | | 13,563,124 | |

| | | | | | | | | | 457,058,298 | |

| Canada—1.0% | | | | | | | | | | |

| Canada Treasury Bills, 1.037%, 12/5/132 | | CAD | | | 32,835,000 | | | | 31,821,627 | |

| Canada Unsec. Bonds, 3.75%, 6/1/19 | | CAD | | | 73,380,000 | | | | 77,863,799 | |

| | | | | | | | | | 109,685,426 | |

| Colombia—0.4% | | | | | | | | | | |

| Republic of Colombia Sr. Unsec. Bonds, 6.125%, 1/18/41 | | USD | | | 3,135,000 | | | | 3,440,662 | |

| Republic of Colombia Sr. Unsec. Nts.: | | | | | | | | | | |

| 4.00%, 2/26/24 | | USD | | | 11,010,000 | | | | 10,817,325 | |

| 7.375%, 1/27/17 | | USD | | | 4,470,000 | | | | 5,225,430 | |

| 7.375%, 3/18/19 | | USD | | | 19,585,000 | | | | 23,815,360 | |

| 8.125%, 5/21/24 | | USD | | | 6,980,000 | | | | 9,047,825 | |

| Series B, 10.00%, 7/24/24 | | COP | | | 5,474,000,000 | | | | 3,573,927 | |

| | | | | | | | | | 55,920,529 | |

| Costa Rica—0.0% | | | | | | | | | | |

| Republic of Costa Rica Sr. Unsec. Bonds, 4.375%, 4/30/255 | | USD | | | 1,760,000 | | | | 1,544,400 | |

| Croatia—0.3% | | | | | | | | | | |

| Republic of Croatia Sr. Unsec. Nts.: | | | | | | | | | | |

| 5.50%, 4/4/235 | | USD | | | 18,975,000 | | | | 18,263,437 | |

| 6.25%, 4/27/175 | | USD | | | 9,450,000 | | | | 9,953,874 | |

| 6.375%, 3/24/215 | | USD | | | 4,635,000 | | | | 4,809,971 | |

| 6.75%, 11/5/195 | | USD | | | 4,535,000 | | | | 4,858,119 | |

| | | | | | | | | | 37,885,401 | |

| Denmark—0.4% | | | | | | | | | | |

| Kingdom of Denmark Unsec. Nts., 4%, 11/15/19 | | DKK | | | 220,720,000 | | | | 46,764,767 | |

| Dominican Republic—0.2% | | | | | | | | | | |

| Banco de Reservas de la Republica Dominicana Sub. Nts., 7%, 2/1/235 | | USD | | | 7,305,000 | | | | 6,976,275 | |

| Dominican Republic Sr. Unsec. Bonds, 5.875%, 4/18/245 | | USD | | | 8,080,000 | | | | 7,534,600 | |

| | | | | | | | | | 14,510,875 | |

| Finland—0.6% | | | | | | | | | | |

| Republic of Finland Sr. Unsec. Nts.: | | | | | | | | | | |

| 1.50%, 4/15/235 | | EUR | | | 29,645,000 | | | | 38,371,849 | |

| 1.625%, 9/15/225 | | EUR | | | 20,300,000 | | | | 26,854,360 | |

| | | | | | | | | | 65,226,209 | |

| France—2.7% | | | | | | | | | | |

| Government of France Unsec. Bonds: | | | | | | | | | | |

| 2.75%, 10/25/27 | | EUR | | | 25,245,000 | | | | 33,571,624 | |

13 OPPENHEIMER INTERNATIONAL BOND FUND

| | | | |

| | |

| | STATEMENTOF INVESTMENTS Continued | | |

| | | | | | | | | | |

| | | | |

| Principal

Amount |

| | | Valu | e |

| France Continued | | | | | | | | | | |

| Government of France Unsec. Bonds: Continued | | | | | | | | | | |

| 4.50%, 4/25/41 | | EUR | | | 58,950,000 | | | $ | 95,708,025 | |

| Government of France Unsec. Nts.: | | | | | | | | | | |

| 2.25%, 10/25/22 | | EUR | | | 64,835,000 | | | | 88,052,527 | |

| 3.75%, 10/25/19 | | EUR | | | 46,690,000 | �� | | | 71,741,935 | |

| | | | | | | | | | 289,074,111 | |

| Germany—4.4% | | | | | | | | | | |

| Federal Republic of Germany Unsec. Bonds, 2.50%, 7/4/44 | | EUR | | | 36,120,000 | | | | 47,880,313 | |

| Federal Republic of Germany Unsec. Nts.: | | | | | | | | | | |

| 0.25%, 4/13/18 | | EUR | | | 97,970,000 | | | | 130,041,816 | |

| 1.50%, 5/15/23 | | EUR | | | 120,045,000 | | | | 159,040,325 | |

| 4.00%, 10/11/13 | | EUR | | | 104,110,000 | | | | 140,947,465 | |

| | | | | | | | | | 477,909,919 | |

| Guatemala—0.1% | | | | | | | | | | |

| Republic of Guatemala Sr. Unsec. Bonds, 4.875%, 2/13/285 | | USD | | | 7,935,000 | | | | 7,300,200 | |

| Hungary—1.5% | | | | | | | | | | |

| Hungary Sr. Unsec. Bonds, 7.625%, 3/29/41 | | USD | | | 925,000 | | | | 994,375 | |

| Hungary Sr. Unsec. Nts.: | | | | | | | | | | |

| 5.375%, 2/21/23 | | USD | | | 15,750,000 | | | | 15,395,625 | |

| 5.75%, 6/11/18 | | EUR | | | 2,220,000 | | | | 3,153,493 | |

| 6.375%, 3/29/21 | | USD | | | 21,340,000 | | | | 22,807,125 | |

| Hungary Unsec. Bonds: | | | | | | | | | | |

| Series 17/A, 6.75%, 11/24/17 | | HUF | | | 3,634,000,000 | | | | 17,681,151 | |

| Series 19/A, 6.50%, 6/24/19 | | HUF | | | 3,733,000,000 | | | | 18,052,970 | |

| Series 20/A, 7.50%, 11/12/20 | | HUF | | | 2,065,000,000 | | | | 10,539,982 | |

| Series 23/A, 6.00%, 11/24/23 | | HUF | | | 4,296,900,000 | | | | 19,842,356 | |

| Hungary Unsec. Nts.: | | | | | | | | | | |

| Series 16/D, 5.50%, 12/22/16 | | HUF | | | 3,416,000,000 | | | | 16,046,574 | |

| Series 18/A, 5.50%, 12/20/18 | | HUF | | | 9,208,000,000 | | | | 42,679,937 | |

| | | | | | | | | | 167,193,588 | |

| Indonesia—0.5% | | | | | | | | | | |

| Perusahaan Penerbit SBSN Indonesia Sr. Unsec. Bonds, 4%, 11/21/185 | | USD | | | 15,790,000 | | | | 15,355,775 | |

| Perusahaan Penerbit SBSN Indonesia Unsec. Nts., 6.125%, 3/15/195 | | USD | | | 9,685,000 | | | | 10,145,037 | |

| Republic of Indonesia Sr. Unsec. Nts.: | | | | | | | | | | |

| 4.875%, 5/5/215 | | USD | | | 14,755,000 | | | | 14,681,225 | |

| 5.375%, 10/17/235 | | USD | | | 16,640,000 | | | | 16,640,000 | |

| 11.625%, 3/4/195 | | USD | | | 3,265,000 | | | | 4,371,019 | |

| | | | | | | | | | 61,193,056 | |

| Italy—4.7% | | | | | | | | | | |

| Republic of Italy Buoni Ordinari del Tesoro BOT, 0.427%, 10/31/132 | | EUR | | | 15,545,000 | | | | 21,022,712 | |

| Republic of Italy Buoni Poliennali del Tesoro Unsec. Bonds: | | | | | | | | | | |

| 3.50%, 11/1/17 | | EUR | | | 21,770,000 | | | | 29,945,270 | |

| 4.00%, 9/1/20 | | EUR | | | 54,165,000 | | | | 74,478,864 | |

| 4.50%, 3/1/19 | | EUR | | | 126,305,000 | | | | 179,483,652 | |

| 4.75%, 9/1/445 | | EUR | | | 20,230,000 | | | | 25,823,360 | |

| 5.00%, 3/1/22 | | EUR | | | 10,125,000 | | | | 14,503,025 | |

| 5.00%, 9/1/40 | | EUR | | | 40,540,000 | | | | 54,361,906 | |

14 OPPENHEIMER INTERNATIONAL BOND FUND

| | | | | | | | | | |

| | | | |

| Principal

Amount |

| | | Valu | e |

| Italy Continued | | | | | | | | | | |

| Republic of Italy Buoni Poliennali del Tesoro Unsec. Nts., 4.75%, 5/1/17 | | EUR | | | 27,240,000 | | | $ | 39,154,124 | |

| Republic of Italy Certificati di Credito del Tesoro Unsec. Nts., 1.129%, 10/15/171 | | EUR | | | 22,685,000 | | | | 29,081,952 | |

| Republic of Italy International Sr. Unsec. Bonds, 4.50%, 6/8/15 | | JPY | | | 4,391,000,000 | | | | 46,729,943 | |

| | | | | | | | | | 514,584,808 | |

| Ivory Coast—0.3% | | | | | | | | | | |

| Republic of Cote d’Ivoire Sr. Unsec. Bonds, 5.75%, 12/31/321 | | USD | | | 37,205,000 | | | | 33,019,438 | |

| Japan—8.8% | | | | | | | | | | |

| Japan Bank for International Cooperation Sr. Unsec. Nts., 2.30%, 3/19/18 | | CAD | | | 13,205,000 | | | | 12,726,182 | |

| Japan Sr. Unsec. Bonds: | | | | | | | | | | |

| Series 112, 2.10%, 6/20/29 | | JPY | | | 14,243,000,000 | | | | 162,893,146 | |

| Series 134, 1.80%, 3/20/32 | | JPY | | | 9,053,000,000 | | | | 96,632,935 | |

| Series 143, 1.60%, 3/20/33 | | JPY | | | 13,914,000,000 | | | | 142,656,755 | |

| Series 314, 1.10%, 3/20/21 | | JPY | | | 16,614,000,000 | | | | 176,746,964 | |

| Series 328, 0.60%, 3/20/23 | | JPY | | | 10,115,000,000 | | | | 102,415,726 | |

| Series 329, 0.80%, 6/20/23 | | JPY | | | 3,029,000,000 | | | | 31,194,401 | |

| Series 36, 2.00%, 3/20/42 | | JPY | | | 17,678,000,000 | | | | 192,121,796 | |

| Series 38, 1.80%, 3/20/43 | | JPY | | | 3,031,000,000 | | | | 31,485,798 | |

| Series 39, 1.90%, 6/20/43 | | JPY | | | 1,010,000,000 | | | | 10,724,382 | |

| | | | | | | | | | 959,598,085 | |

| Kazakhstan—0.1% | | | | | | | | | | |

| Development Bank of Kazakhstan JSC Sr. Unsec. Bonds, 4.125%, 12/10/225 | | USD | | | 5,645,000 | | | | 5,235,737 | |

| Latvia—0.1% | | | | | | | | | | |

| Republic of Latvia Sr. Unsec. Nts., 5.25%, 6/16/215 | | USD | | | 6,855,000 | | | | 7,446,244 | |

| Lithuania—0.3% | | | | | | | | | | |

| Republic of Lithuania Sr. Unsec. Bonds: | | | | | | | | | | |

| 6.125%, 3/9/215 | | USD | | | 14,430,000 | | | | 16,540,387 | |

| 6.625%, 2/1/225 | | USD | | | 13,255,000 | | | | 15,591,194 | |

| | | | | | | | | | 32,131,581 | |

| Malaysia—0.9% | | | | | | | | | | |

| Bank Negara Malaysia Treasury Bills: | | | | | | | | | | |

| Series 0213, 2.975%, 1/9/142 | | MYR | | | 64,245,000 | | | | 19,548,042 | |

| Series 0413, 2.974%, 1/16/142 | | MYR | | | 128,495,000 | | | | 39,074,937 | |

| Series 2513, 2.953%, 12/5/132 | | MYR | | | 32,125,000 | | | | 9,804,576 | |

| Federation of Malaysia Sr. Unsec. Bonds, 4.262%, 9/15/16 | | MYR | | | 83,350,000 | | | | 26,171,235 | |

| | | | | | | | | | 94,598,790 | |

| Mexico—5.7% | | | | | | | | | | |

| United Mexican States Sr. Unsec. Bonds: | | | | | | | | | | |

| 6.75%, 9/27/34 | | USD | | | 6,275,000 | | | | 7,467,250 | |

| 7.50%, 4/8/33 | | USD | | | 2,375,000 | | | | 3,028,125 | |

| United Mexican States Treasury Bills: | | | | | | | | | | |

| 3.692%, 3/6/14 | | MXN | | | 355,340,000 | | | | 26,722,643 | |

| 3.761%, 10/31/13 | | MXN | | | 362,070,000 | | | | 27,575,630 | |

| 3.796%, 11/14/132 | | MXN | | | 751,065,000 | | | | 57,122,138 | |

| 3.807%, 10/3/13 | | MXN | | | 388,000,000 | | | | 29,633,187 | |

| 3.945%, 12/11/13 | | MXN | | | 318,600,000 | | | | 24,168,522 | |

15 OPPENHEIMER INTERNATIONAL BOND FUND

| | | | |

| | |

| | STATEMENTOF INVESTMENTS Continued | | |

| | | | | | | | | | |

| | | | |

| Principal

Amount |

| | | Valu | e |

| Mexico Continued | | | | | | | | | | |

| United Mexican States Treasury Bills: Continued | | | | | | | | | | |

| 3.982%, 11/7/13 | | MXN | | | 513,700,000 | | | $ | 39,057,604 | |

| 3.99%, 2/6/14 | | MXN | | | 318,600,000 | | | | 24,030,027 | |

| 3.993%, 1/23/14 | | MXN | | | 253,500,000 | | | | 19,147,631 | |

| United Mexican States Unsec. Bonds: | | | | | | | | | | |

| Series M, 5.00%, 6/15/17 | | MXN | | | 284,215,000 | | | | 22,146,601 | |

| Series M, 6.50%, 6/9/22 | | MXN | | | 607,450,000 | | | | 48,165,478 | |

| Series M, 7.00%, 6/19/14 | | MXN | | | 258,550,000 | | | | 20,302,343 | |

| Series M, 8.00%, 12/19/13 | | MXN | | | 1,969,200,000 | | | | 152,000,968 | |

| Series M10, 7.75%, 12/14/17 | | MXN | | | 751,940,000 | | | | 64,272,243 | |

| Series M20, 7.50%, 6/3/27 | | MXN | | | 376,370,000 | | | | 31,536,065 | |

| Series M20, 8.50%, 5/31/29 | | MXN | | | 297,480,000 | | | | 26,587,705 | |

| | | | | | | | | | 622,964,160 | |

| Morocco—0.1% | | | | | | | | | | |

| Kingdom of Morocco Sr. Unsec. Nts., 4.25%, 12/11/225 | | USD | | | 10,365,000 | | | | 9,486,048 | |

| Netherlands—0.7% | | | | | | | | | | |

| Kingdom of the Netherlands Unsec. Bonds: | | | | | | | | | | |

| 4.00%, 7/15/195 | | EUR | | | 37,870,000 | | | | 58,943,012 | |

| 4.00%, 1/15/375 | | EUR | | | 13,535,000 | | | | 22,214,582 | |

| | | | | | | | | | 81,157,594 | |

| Nigeria—0.5% | | | | | | | | | | |

| Federal Republic of Nigeria Treasury Bills: | | | | | | | | | | |

| 11.235%, 1/23/142 | | NGN | | | 1,426,000,000 | | | | 8,537,909 | |

| 11.835%, 10/24/132 | | NGN | | | 354,000,000 | | | | 2,179,508 | |

| 11.851%, 10/10/132 | | NGN | | | 269,000,000 | | | | 1,663,329 | |

| Federal Republic of Nigeria Unsec. Bonds: | | | | | | | | | | |

| 7.00%, 10/23/19 | | NGN | | | 1,658,000,000 | | | | 7,707,348 | |

| 16.00%, 6/29/19 | | NGN | | | 1,690,000,000 | | | | 11,629,589 | |

| 16.39%, 1/27/22 | | NGN | | | 1,786,000,000 | | | | 12,816,232 | |

| Republic of Nigeria Sr. Unsec. Bonds, 5.125%, 7/12/185 | | USD | | | 5,755,000 | | | | 5,855,712 | |

| | | | | | | | | | 50,389,627 | |

| Panama—0.1% | | | | | | | | | | |

| Republic of Panama Sr. Unsec. Bonds: | | | | | | | | | | |

| 6.70%, 1/26/36 | | USD | | | 8,115,000 | | | | 9,311,962 | |

| 8.875%, 9/30/27 | | USD | | | 3,530,000 | | | | 4,880,225 | |

| 9.375%, 4/1/29 | | USD | | | 3,515,000 | | | | 5,035,237 | |

| | | | | | | | | | 19,227,424 | |

| Paraguay—0.0% | | | | | | | | | | |

| Republic of Paraguay Sr. Unsec. Bonds, 4.625%, 1/25/235 | | USD | | | 2,560,000 | | | | 2,348,800 | |

| Peru—0.5% | | | | | | | | | | |

| El Fondo MIVIVIENDA SA Unsec. Nts., 3.50%, 1/31/235 | | USD | | | 8,095,000 | | | | 7,062,888 | |

| Republic of Peru Sr. Unsec. Bonds: | | | | | | | | | | |

| 6.55%, 3/14/37 | | USD | | | 6,435,000 | | | | 7,641,562 | |

| 7.84%, 8/12/205 | | PEN | | | 46,865,000 | | | | 19,521,586 | |

| 8.20%, 8/12/265 | | PEN | | | 50,410,000 | | | | 22,067,091 | |

| | | | | | | | | 56,293,127 | |

16 OPPENHEIMER INTERNATIONAL BOND FUND

| | | | | | | | | | | | |

| | | | |

| Principal

Amount |

| | | | | Value | |

| Philippines—0.2% | | | | | | | | | | | | |

| Republic of the Philippines Sr. Unsec. Bonds: | | | | | | | | | | | | |

| 6.375%, 1/15/32 | | USD | | | $ 11,750,000 | | | $ | | | 13,806,250 | |

| 6.375%, 10/23/34 | | USD | | | 11,680,000 | | | 13,797,000 | |

| | | | | | | | | | | | 27,603,250 | |

| Poland—1.0% | | | | | | | | | | | | |

| Republic of Poland Sr. Unsec. Bonds: | | | | | | | | | | | | |

| 3.00%, 3/17/23 | | USD | | | 8,160,000 | | | | | | 7,494,960 | |

| 5.00%, 3/23/22 | | USD | | | 7,970,000 | | | | | | 8,591,660 | |

| 5.125%, 4/21/21 | | USD | | | 13,800,000 | | | | | | 15,042,000 | |

| Republic of Poland Unsec. Bonds: | | | | | | | | | | | | |

| 5.25%, 10/25/17 | | PLN | | | 103,545,000 | | | | | | 35,080,496 | |

| 5.50%, 4/25/15 | | PLN | | | 74,715,000 | | | | | | 24,819,802 | |

| 5.75%, 4/25/29 | | PLN | | | 69,995,000 | | | | | | 24,896,375 | |

| | | | | | | | | | | | 115,925,293 | |

| Portugal—1.2% | | | | | | | | | | | | |

| Republic of Portugal Obrigacoes do Tesouro OT: | | | | | | | | | | | | |

| 4.10%, 4/15/37 | | EUR | | | 23,735,000 | | | | | | 22,195,643 | |

| 4.35%, 10/16/175 | | EUR | | | 78,070,000 | | | | | | 100,072,634 | |

| 4.75%, 6/14/19 | | EUR | | | 4,390,000 | | | | | | 5,493,407 | |

| | | | | | | | | | | | 127,761,684 | |

| Romania—0.2% | | | | | | | | | | | | |

| Romania Sr. Unsec. Bonds, 6.75%, 2/7/225 | | USD | | | 14,425,000 | | | | | | 16,501,479 | |

| Russia—3.0% | | | | | | | | | | | | |

| AHML Via AHML Finance Ltd. Unsec. Nts., 7.75%, 2/13/185 | | RUB | | | 346,100,000 | | | | | | 10,445,541 | |

| Russian Federation Sr. Unsec. Bonds: | | | | | | | | | | | | |

| 4.875%, 9/16/235 | | USD | | | 9,765,000 | | | | | | 10,009,125 | |

| 5.875%, 9/16/435 | | USD | | | 6,655,000 | | | | | | 6,904,562 | |

| Series 6211, 7.00%, 1/25/23 | | RUB | | | 2,365,300,000 | | | | | | 72,269,710 | |

| Russian Federation Unsec. Bonds: | | | | | | | | | | | | |

| Series 6204, 7.50%, 3/15/18 | | RUB | | | 1,022,600,000 | | | | | | 32,656,987 | |

| Series 6205, 7.60%, 4/14/21 | | RUB | | | 1,467,700,000 | | | | | | 46,837,393 | |

| Series 6208, 7.50%, 2/27/19 | | RUB | | | 1,349,700,000 | | | | | | 43,019,696 | |

| Series 6209, 7.60%, 7/20/22 | | RUB | | | 1,040,300,000 | | | | | | 33,021,575 | |

| Vnesheconombank Sr. Unsec. Bonds, Series 18, 8.55%, 9/17/321 | | RUB | | | 279,000,000 | | | | | | 8,800,148 | |

| Vnesheconombank Sr. Unsec. Bonds, Series 9, 7.90%, 3/18/211 | | RUB | | | 256,800,000 | | | | | | 7,969,150 | |

| Vnesheconombank Via VEB Finance plc Sr. Unsec. Bonds: | | | | | | | | | | | | |

| 5.375%, 2/13/175 | | USD | | | 9,910,000 | | | | | | 10,514,510 | |

| 5.45%, 11/22/175 | | USD | | | 11,295,000 | | | | | | 12,041,600 | |

| 6.902%, 7/9/205 | | USD | | | 21,205,000 | | | | | | 23,326,560 | |

| | | | | | | | | | | | 317,816,557 | |

| Rwanda—0.1% | | | | | | | | | | | | |

| Republic of Rwanda Sr. Unsec. Bonds, 6.625%, 5/2/235 | | USD | | | 10,815,000 | | | | | | 9,544,237 | |

| Serbia—0.2% | | | | | | | | | | | | |

| Republic of Serbia Sr. Unsec. Bonds, 5.25%, 11/21/175 | | USD | | | 7,160,000 | | | | | | 7,142,100 | |

| Republic of Serbia Treasury Bills: | | | | | | | | | | | | |

| 9.824%, 1/30/142 | | RSD | | | 317,000,000 | | | | | | 3,641,612 | |

| 10.004%, 6/12/142 | | RSD | | | 1,287,000,000 | | | | | | 14,220,495 | |

| | | | | | | | | | | 25,004,207 | |

17 OPPENHEIMER INTERNATIONAL BOND FUND

| | | | |

| | |

| | STATEMENTOF INVESTMENTS Continued | | |

| | | | | | | | | | | | |

| | | | |

| Principal

Amount |

| | | | | Value | |

| Singapore—0.2% | | | | | | | | | | | | |

| Republic of Singapore Sr. Unsec. Bonds, 2.375%, 4/1/17 | | SGD | | | 25,130,000 | | | $ | | | 21,246,133 | |

| South Africa—2.0% | | | | | | | | | | | | |

| Republic of South Africa Sr. Unsec. Bonds: | | | | | | | | | | | | |

| 5.875%, 5/30/22 | | USD | | | 2,200,000 | | | | | | 2,387,000 | |

| 5.875%, 9/16/25 | | USD | | | 9,810,000 | | | | | | 10,342,192 | |

| Series R207, 7.25%, 1/15/20 | | ZAR | | | 678,740,000 | | | | | | 67,582,636 | |

| Series R208, 6.75%, 3/31/21 | | ZAR | | | 995,785,000 | | | | | | 95,631,660 | |

| Republic of South Africa Unsec. Bonds: | | | | | | | | | | | | |

| Series 2023, 7.75%, 2/28/23 | | ZAR | | | 176,270,000 | | | | | | 17,683,444 | |

| Series R213, 7.00%, 2/28/31 | | ZAR | | | 227,086,000 | | | | | | 19,470,534 | |

| | | | | | | | | | | | 213,097,466 | |

| South Korea—0.2% | | | | | | | | | | | | |

| Korea Housing Finance Corp. Sec. Nts., 1.625%, 9/15/185 | | USD | | | 26,200,000 | | | | | | 24,753,026 | |

| Spain—0.9% | | | | | | | | | | | | |

| Autonomous Community of Madrid Spain Sr. Unsec. Bonds, 4.30%, 9/15/26 | | EUR | | | 49,775,000 | | | | | | 59,965,124 | |

| Instituto de Credito Oficial Sr. Unsec. Nts., 5%, 5/15/15 | | NOK | | | 75,000,000 | | | | | | 12,563,580 | |

| Kingdom of Spain Sr. Unsec. Bonds, 4.50%, 1/31/18 | | EUR | | | 18,675,000 | | | | | | 26,959,821 | |

| | | | | | | | | | | | 99,488,525 | |

| Sri Lanka—0.3% | | | | | | | | | | | | |

| Democratic Socialist Republic of Sri Lanka Sr. Unsec. Bonds: | | | | | | | | | | | | |

| 5.875%, 7/25/225 | | USD | | | 5,970,000 | | | | | | 5,522,250 | |

| 6.25%, 10/4/205 | | USD | | | 6,570,000 | | | | | | 6,430,388 | |

| 6.25%, 7/27/215 | | USD | | | 12,385,000 | | | | | | 11,920,563 | |

| | | | | | | | | | | | 23,873,201 | |

| Tanzania—0.1% | | | | | | | | | | | | |

| United Republic of Tanzania Sr. Unsec. Nts., 6.392%, 3/9/201 | | USD | | | 9,950,000 | | | | | | 10,323,125 | |

| Thailand—0.8% | | | | | | | | | | | | |

| Kingdom of Thailand Sr. Unsec. Bonds: | | | | | | | | | | | | |

| 3.58%, 12/17/27 | | THB | | | 1,085,000,000 | | | | | | 32,729,573 | |

| 3.625%, 6/16/23 | | THB | | | 1,062,300,000 | | | | | | 33,298,350 | |

| 3.65%, 12/17/21 | | THB | | | 684,300,000 | | | | | | 21,691,938 | |

| | | | | | | | | | | | 87,719,861 | |

| Turkey—2.2% | | | | | | | | | | | | |

| Republic of Turkey Sr. Unsec. Bonds: | | | | | | | | | | | | |

| 5.625%, 3/30/21 | | USD | | | 8,165,000 | | | | | | 8,524,260 | |

| 6.25%, 9/26/22 | | USD | | | 12,810,000 | | | | | | 13,805,978 | |

| 6.875%, 3/17/36 | | USD | | | 4,565,000 | | | | | | 4,868,573 | |

| Republic of Turkey Unsec. Bonds: | | | | | | | | | | | | |

| 5.00%, 5/13/15 | | TRY | | | 115,520,000 | | | | | | 54,184,401 | |

| 5.828%, 2/11/156 | | TRY | | | 20,680,000 | | | | | | 13,868,247 | |

| 6.30%, 2/14/18 | | TRY | | | 32,695,000 | | | | | | 14,752,849 | |

| 7.10%, 3/8/23 | | TRY | | | 42,330,000 | | | | | | 18,492,723 | |

| 9.00%, 3/5/14 | | TRY | | | 139,610,000 | | | | | | 69,665,048 | |

| 9.00%, 3/8/17 | | TRY | | | 105,795,000 | | | | | | 53,027,122 | |

| | | | | | | | | | | 251,189,201 | |

18 OPPENHEIMER INTERNATIONAL BOND FUND

| | | | | | | | | | |

| | | | |

| Principal

Amount |

| | | Valu | e |

| United Arab Emirates—0.1% | | | | | | | | | | |

| Emirate of Dubai Government Sr. Unsec. International Bonds, 5.591%, 6/22/21 | | USD | | $ | 13,320,000 | | | $ | 14,418,900 | |

| United Kingdom—3.4% | | | | | | | | | | |

| United Kingdom Unsec. Treasury Bonds: | | | | | | | | | | |

| 3.75%, 9/7/21 | | GBP | | | 104,275,000 | | | | 186,938,205 | |

| 4.00%, 9/7/16 | | GBP | | | 41,200,000 | | | | 72,922,533 | |

| 4.25%, 12/7/55 | | GBP | | | 15,155,000 | | | | 28,744,856 | |

| 4.75%, 12/7/38 | | GBP | | | 37,875,000 | | | | 75,239,743 | |

| | | | | | | | | 363,845,337 | |

| Uruguay—0.2% | | | | | | | | | | |

| Oriental Republic of Uruguay Sr. Unsec. Bonds, 4.50%, 8/14/24 | | USD | | | 18,330,000 | | | | 18,650,775 | |

| Venezuela—0.8% | | | | | | | | | | |

| Bolivarian Republic of Venezuela Sr. Unsec. Bonds: | | | | | | | | | | |

| 7.00%, 3/31/38 | | USD | | | 13,855,000 | | | | 9,109,663 | |

| 7.65%, 4/21/25 | | USD | | | 18,795,000 | | | | 13,626,375 | |

| 8.25%, 10/13/24 | | USD | | | 19,375,000 | | | | 14,676,563 | |

| 9.00%, 5/7/23 | | USD | | | 26,520,000 | | | | 21,653,580 | |

| 12.75%, 8/23/22 | | USD | | | 8,895,000 | | | | 8,903,895 | |

| 13.625%, 8/15/185 | | USD | | | 23,620,000 | | | | 24,801,000 | |

| | | | | | | | | 92,771,076 | |

Total Foreign Government Obligations (Cost $6,814,614,004) | | | | | | | | | 6,624,421,747 | |

| Corporate Loan—0.1% | | | | | | | | | | |

Hallertau SPC, Sr. Sec. Credit Facilities Term Loan, 7.94%, 8/15/1410 (Cost $5,543,125) | | | | | 15,837,500 | | | | 7,411,950 | |

| Corporate Bonds and Notes—26.7% | | | | | | | | | | |

| Consumer Discretionary—0.2% | | | | | | | | | | |

| Auto Components—0.0% | | | | | | | | | | |

| GKN Holdings plc, 6.75% Sr. Unsec. Nts., 10/28/19 | | GBP | | | 2,635,000 | | | | 4,853,309 | |

| Servus Luxembourg Holding SCA, 7.75% Sr. Sec. Nts., 6/15/185 | | EUR | | | 3,110,000 | | | | 4,292,352 | |

| | | | | | | | | 9,145,661 | |

| Automobiles—0.1% | | | | | | | | | | |

Jaguar Land Rover Automotive plc, 8.25% Sr. Unsec. Nts., 3/15/205 | | GBP | | | 8,855,000 | | | | 16,005,429 | |

| Household Durables—0.0% | | | | | | | | | | |

Arcelik AS, 5% Sr. Unsec. Nts., 4/3/235 | | | | | 4,795,000 | | | | 4,141,681 | |

| Media—0.1% | | | | | | | | | | |

| Globo Comunicacao e Participacoes SA, 5.307% Sr. Unsec. Nts., 5/11/221,5 | | | | | 3,710,000 | | | | 3,747,100 | |

| Myriad International Holdings BV, 6% Sr. Unsec. Nts., 7/18/205 | | | | | 5,225,000 | | | | 5,512,375 | |

| | | | | | | | | 9,259,475 | |

| Textiles, Apparel & Luxury Goods—0.0% | | | | | | | | | | |

| Levi Strauss & Co., 7.75% Sr. Unsec. Nts., 5/15/18 | | EUR | | | 350,000 | | | | 506,169 | |

| Consumer Staples—0.2% | | | | | | | | | | |

| Beverages—0.1% | | | | | | | | | | |

| Coca-Cola Icecek AS, 4.75% Sr. Unsec. Nts., 10/1/185,8 | | | | | 6,245,000 | | | | 6,313,558 | |

19 OPPENHEIMER INTERNATIONAL BOND FUND

| | | | |

| | |

| | STATEMENTOF INVESTMENTS Continued | | |

| | | | | | | | | | |

| | | | |

| Principal

Amount |

| | | Valu | e |

| Food Products—0.1% | | | | | | | | | | |

| BFF International Ltd., 7.25% Sr. Unsec. Nts., 1/28/205 | | | | $ | 1,120,000 | | | $ | 1,243,200 | |

| BRF SA, 5.875% Sr. Unsec. Nts., 6/6/225 | | | | | 2,775,000 | | | | 2,768,062 | |

| MHP SA, 8.25% Sr. Unsec. Nts., 4/2/205 | | | | | 12,885,000 | | | | 10,310,577 | |

| | | | | | | | | 14,321,839 | |

| Energy—4.8% | | | | | | | | | | |

| Energy Equipment & Services—0.3% | | | | | | | | | | |

| Drill Rigs Holdings, Inc., 6.50% Sr. Sec. Nts., 10/1/175 | | | | | 4,580,000 | | | | 4,751,750 | |

| Odebrecht Offshore Drilling Finance Ltd., 6.75% Sr. Sec. Nts., 10/1/225 | | | | | 13,270,000 | | | | 13,634,925 | |

| QGOG Constellation SA, 6.25% Sr. Unsec. Nts., 11/9/195 | | | | | 10,455,000 | | | | 9,958,388 | |

| Seadrill Ltd., 5.625% Sr. Unsec. Nts., 9/15/175 | | | | | 5,045,000 | | | | 5,120,675 | |

| | | | | | | | | 33,465,738 | |

| Oil, Gas & Consumable Fuels—4.5% | | | | | | | | | | |

| Alliance Oil Co. Ltd., 9.875% Sr. Unsec. Nts., 3/11/155 | | | | | 17,565,000 | | | | 18,838,462 | |

| CNOOC Curtis Funding No 1 Pty Ltd., 4.50% Sr. Unsec. Nts., 10/3/237,8 | | | | | 9,430,000 | | | | 9,516,002 | |

| Ecopetrol SA, 7.625% Sr. Unsec. Nts., 7/23/19 | | | | | 2,255,000 | | | | 2,677,813 | |

| Empresa Nacional del Petroleo, 4.75% Sr. Unsec. Nts., 12/6/215 | | | | | 8,575,000 | | | | 8,479,526 | |

| Gazprom OAO Via Gaz Capital SA: | | | | | | | | | | |

| 4.95% Sr. Unsec. Nts., 7/19/225 | | | | | 35,355,000 | | | | 34,250,156 | |

| 5.999% Sr. Unsec. Nts., 1/23/215 | | | | | 4,165,000 | | | | 4,378,456 | |

| 8.146% Sr. Unsec. Nts., 4/11/185 | | | | | 21,855,000 | | | | 25,434,849 | |

| 8.625% Sr. Unsec. Nts., 4/28/345 | | | | | 16,825,000 | | | | 20,190,000 | |

| 9.25% Sr. Unsec. Nts., 4/23/195 | | | | | 33,200,000 | | | | 41,008,640 | |

| KazMunayGas National Co. JSC, 9.125% Sr. Unsec. Nts., 7/2/185 | | | | | 6,655,000 | | | | 8,177,331 | |

| Lukoil International Finance BV: | | | | | | | | | | |

| 4.563% Sr. Unsec. Unsub. Nts., 4/24/235 | | | | | 4,325,000 | | | | 4,034,144 | |

| 7.25% Sr. Unsec. Nts., 11/5/195 | | | | | 9,535,000 | | | | 10,882,296 | |

| MEG Energy Corp.: | | | | | | | | | | |

| 6.50% Sr. Unsec. Nts., 3/15/215 | | | | | 4,115,000 | | | | 4,166,438 | |

| 7.00% Sr. Unsec. Nts., 3/31/245 | | | | | 2,550,000 | | | | 2,569,125 | |

| Novatek OAO via Novatek Finance Ltd.: | | | | | | | | | | |

| 4.422% Sr. Unsec. Nts., 12/13/225 | | | | | 24,040,000 | | | | 22,116,800 | |

| 7.75% Sr. Unsec. Nts., 2/21/175 | | RUB | | | 156,720,000 | | | | 4,823,415 | |

| Odebrecht Drilling Norbe VIII/IX Ltd., 6.35% Sr. Sec. Nts., 6/30/215 | | | | | 1,726,050 | | | | 1,764,886 | |

| Pacific Rubiales Energy Corp., 5.125% Sr. Unsec. Nts., 3/28/235 | | | | | 9,795,000 | | | | 8,827,744 | |

| Pemex Project Funding Master Trust: | | | | | | | | | | |

| 5.75% Sr. Unsec. Nts., 3/1/18 | | | | | 5,590,000 | | | | 6,218,875 | |

| 6.625% Sr. Unsec. Nts., 6/15/35 | | | | | 24,335,000 | | | | 25,819,678 | |

| Pertamina Persero PT, 4.875% Sr. Unsec. Nts., 5/3/225 | | | | | 7,835,000 | | | | 7,110,263 | |

| Petroleos de Venezuela SA: | | | | | | | | | | |

| 5.125% Sr. Unsec. Nts., 10/28/16 | | | | | 6,630,000 | | | | 5,353,725 | |

| 8.50% Sr. Unsec. Nts., 11/2/175 | | | | | 27,690,000 | | | | 25,156,365 | |

| 12.75% Sr. Unsec. Nts., 2/17/225 | | | | | 15,405,000 | | | | 15,096,900 | |

| Petroleos Mexicanos: | | | | | | | | | | |

| 3.50% Sr. Unsec. Nts., 1/30/23 | | | | | 21,265,000 | | | | 19,382,452 | |

| 4.875% Sr. Unsec. Nts., 1/18/24 | | | | | 28,860,000 | | | | 28,932,150 | |

20 OPPENHEIMER INTERNATIONAL BOND FUND

| | | | | | | | | | | | |

| | | | | | |

| Principal

Amount |

| | | Value | |

| Oil, Gas & Consumable Fuels Continued | | | | | | | | | | | | |

| Petroleos Mexicanos: Continued | | | | | | | | | | | | |

| 5.50% Sr. Unsec. Nts., 6/27/44 | | | | | | $ | 6,020,000 | | | $ | 5,494,544 | |

| 6.00% Sr. Unsec. Nts., 3/5/20 | | | | | | | 26,750,000 | | | | 29,826,250 | |

| 6.50% Sr. Unsec. Nts., 6/2/41 | | | | | | | 10,855,000 | | | | 11,302,736 | |

| 8.00% Sr. Unsec. Nts., 5/3/19 | | | | | | | 15,635,000 | | | | 18,957,438 | |

| Petroleum Co. of Trinidad & Tobago Ltd.: | | | | | | | | | | | | |

| 6.00% Sr. Unsec. Nts., 5/8/225 | | | | | | | 1,410,000 | | | | 1,512,225 | |

| 9.75% Sr. Unsec. Nts., 8/14/195 | | | | | | | 3,760,000 | | | | 4,850,400 | |

| Petronas Capital Ltd., 7.875%, 5/22/225 | | | | | | | 7,595,000 | | | | 9,679,774 | |

| Reliance Industries Ltd., 5.875% Sr. Unsec. Perpetual Bonds5,9 | | | | | | | 21,245,000 | | | | 17,420,900 | |

| Schahin II Finance Co. SPV Ltd., 5.875% Sr. Sec. Nts., 9/25/225 | | | | | | | 16,673,990 | | | | 15,965,345 | |

| Sibur Securities Ltd., 3.914% Sr. Unsec. Nts., 1/31/185 | | | | | | | 11,075,000 | | | | 10,576,625 | |

| Tengizchevroil Finance Co. Sarl, 6.124% Sr. Sec. Nts., 11/15/145 | | | | | | | 2,997,100 | | | | 3,072,028 | |

| | | | | | | | | | | | 493,864,756 | |

| Financials—12.1% | | | | | | | | | | | | |

| Capital Markets—0.8% | | | | | | | | | | | | |

| Deutsche Bank AG, 4.296% Jr. Sub. Nts., 5/24/281 | | | | | | | 21,980,000 | | | | 19,897,901 | |

| Deutsche Bank Capital Trust V, 4.901% Jr. Sub. Perpetual Bonds1,5,9 | | | | | | | 20,330,000 | | | | 18,042,875 | |

| UBS AG (Jersey Branch): | | | | | | | | | | | | |

| 4.28% Jr. Sub. Perpetual Bonds1,9 | | EUR | | | | | 6,195,000 | | | | 8,474,604 | |

| 7.152% Jr. Sub. Perpetual Bonds1,9 | | EUR | | | | | 4,420,000 | | | | 6,614,929 | |

| 7.25% Sub. Nts., 2/22/221 | | | | | | | 19,375,000 | | | | 20,857,672 | |

| | | | | | | | | | | 73,887,981 | |

| Commercial Banks—8.4% | | | | | | | | | | | | |

| Akbank TAS, 7.50% Sr. Unsec. Nts., 2/5/185 | | TRY | | | | | 33,370,000 | | | | 15,102,029 | |

| Alfa Bank OJSC Via Alfa Bond Issuance plc, 7.875% Sr. Unsec. Nts., 9/25/175 | | | | | | | 13,165,000 | | | | 14,556,804 | |

| Banco ABC Brasil SA, 8.50% Sr. Unsec. Nts., 3/28/167 | | BRL | | | | | 8,360,000 | | | | 3,385,417 | |

| Banco Bilbao Vizcaya Argentaria SA, 9% Jr. Sub. Perpetual Bonds1,9 | | | | | | | 1,785,000 | | | | 1,770,988 | |

| Banco BMG SA: | | | | | | | | | | | | |

| 8.875% Sub. Nts., 8/5/205 | | | | | | | 3,945,000 | | | | 3,728,025 | |

| 9.15% Sr. Unsec. Nts., 1/15/165 | | | | | | | 6,915,000 | | | | 7,191,600 | |

| 9.95% Sub. Nts., 11/5/195 | | | | | | | 9,060,000 | | | | 8,969,400 | |

| Banco de Costa Rica, 5.25% Sr. Unsec. Nts., 8/12/185 | | | | | | | 8,105,000 | | | | 8,230,627 | |

| Banco del Estado de Chile: | | | | | | | | | | | | |

| 3.875% Sr. Unsec. Nts., 2/8/225 | | | | | | | 5,150,000 | | | | 5,008,699 | |

| 4.125% Sr. Unsec. Nts., 10/7/205 | | | | | | | 8,765,000 | | | | 8,922,419 | |

| Banco do Brasil SA (Cayman), 9.25% Jr. Sub. Perpetual Bonds1,5,9 | | | | | | | 35,685,000 | | | | 38,004,525 | |

| Banco do Estado do Rio Grande do Sul SA, 7.375% Sub. Nts., 2/2/225 | | | | | | | 32,780,000 | | | | 32,575,125 | |

| Banco Santander Brasil SA (Cayman Islands), 8% Sr. Unsec. Unsub. Nts., 3/18/165 | | BRL | | | | | 14,290,000 | | | | 5,996,345 | |

| Banco Santander Mexico SA, 4.125% Sr. Unsec. Nts., 11/9/225 | | | | | | | 19,400,000 | | | | 17,848,000 | |

| Bancolombia SA, 5.125% Unsec. Sub. Nts., 9/11/22 | | | | | | | 20,280,000 | | | | 18,606,900 | |

| Bank of Scotland plc, 4.875% Sr. Sec. Nts., 12/20/24 | | GBP | | | | | 7,625,000 | | | | 13,971,683 | |

| Bank of Scotland plc, 4.875% Sr. Sec. Unsub. Nts., 11/8/16 | | GBP | | | | | 4,535,000 | | | | 8,113,854 | |

21 OPPENHEIMER INTERNATIONAL BOND FUND

| | | | |

| | |

| | STATEMENTOF INVESTMENTS Continued | | |

| | | | | | | | | | | | |

| | | | | | |

| Principal

Amount |

| | | Value | |

| Commercial Banks Continued | | | | | | | | | | | | |

| Barclays Bank plc: | | | | | | | | | | | | |

| 4.75% Jr. Sub. Perpetual Bonds1,9 | | EUR | | | | $ | 12,320,000 | | | $ | 13,266,521 | |

| 6.00% Jr. Sub. Perpetual Bonds1,9 | | GBP | | | | | 7,115,000 | | | | 10,395,422 | |

| 14.00% Jr. Sub. Perpetual Bonds1,9 | | GBP | | | | | 27,645,000 | | | | 60,189,418 | |

| BBVA Banco Continental SA, 5% Sr. Unsec. Nts., 8/26/225 | | | | | | | 8,075,000 | | | | 7,772,187 | |

| BNP Paribas SA: | | | | | | | | | | | | |

| 5.945% Jr. Sub. Perpetual Bonds1,9 | | GBP | | | | | 7,005,000 | | | | 11,199,773 | |

| 7.195% Jr. Sub. Perpetual Bonds1,5,9 | | | | | | | 13,195,000 | | | | 13,310,456 | |

| BPCE SA, 9% Jr. Sub. Perpetual Bonds1,9 | | EUR | | | | | 24,160,000 | | | | 34,773,418 | |

| Caixa Economica Federal, 4.50% Sr. Unsec. Nts., 10/3/185,8 | | | | | | | 12,505,000 | | | | 12,407,461 | |

| Commerzbank AG, 8.125% Sub. Nts., 9/19/235 | | | | | | | 3,560,000 | | | | 3,640,100 | |

| Corp. Financiera de Desarrollo SA, 4.75% Sr. Unsec. Nts., 2/8/225 | | | | | | | 8,700,000 | | | | 8,460,750 | |

| CorpGroup Banking SA, 6.75% Sr. Unsec. Nts., 3/15/235 | | | | | | | 13,035,000 | | | | 11,144,925 | |

| Credit Agricole SA, 8.375% Jr. Sub. Perpetual Bonds1,5,9 | | | | | | | 36,265,000 | | | | 39,846,169 | |

| Danske Bank, 5.684% Jr. Sub. Perpetual Bonds1,9 | | GBP | | | | | 6,405,000 | | | | 10,369,054 | |

| EUROFIMA, 6.25% Sr. Unsec. Nts., 12/28/18 | | AUD | | | | | 31,010,000 | | | | 31,382,108 | |

| European Investment Bank: | | | | | | | | | | | | |

| 6.00% Sr. Unsec. Nts., 8/6/20 | | AUD | | | | | 35,115,000 | | | | 35,220,768 | |

| 6.50% Sr. Unsec. Nts., 8/7/19 | | AUD | | | | | 17,550,000 | | | | 18,089,154 | |

| Export-Import Bank of India, 4% Sr. Unsec. Nts., 1/14/23 | | | | | | | 3,395,000 | | | | 2,909,176 | |

| Grupo Aval Ltd., 4.75% Sr. Unsec. Nts., 9/26/225 | | | | | | | 10,935,000 | | | | 9,841,500 | |

| ICICI Bank Ltd., 6.375% Jr. Sub. Nts., 4/30/221,5 | | | | | | | 7,120,000 | | | | 6,657,200 | |

| LBG Capital No.1 plc: | | | | | | | | | | | | |

| 7.869% Sub. Nts., 8/25/20 | | GBP | | | | | 8,795,000 | | | | 15,120,767 | |

| 11.04% Sub. Nts., 3/19/20 | | GBP | | | | | 39,781,000 | | | | 75,002,005 | |

| Lloyds TSB Bank plc, 6% Sec. Nts., 2/8/29 | | GBP | | | | | 13,525,000 | | | | 27,426,544 | |

| Rabobank Capital Funding Trust IV, 5.556% Jr. Sub. Perpetual Bonds1,5,9 | | GBP | | | | | 7,380,000 | | | | 11,985,702 | |

| RBS Capital Trust III, 5.512% Jr. Sub. Perpetual Bonds1,9 | | | | | | | 11,112,000 | | | | 10,306,380 | |

| Royal Bank of Scotland NV: | | | | | | | | | | | | |

| 3.37% Sub. Nts., 5/17/181 | | AUD | | | | | 8,795,000 | | | | 7,191,227 | |

| 7.577% Sub. Nts., 5/17/181 | | AUD | | | | | 10,618,000 | | | | 8,681,802 | |

| Royal Bank of Scotland plc (The): | | | | | | | | | | | | |

| 2.375% Sub. Nts., 11/2/15 | | CHF | | | | | 2,650,000 | | | | 2,931,454 | |

| 13.125% Sub. Nts., 3/19/221 | | AUD | | | | | 11,457,000 | | | | 12,772,697 | |

| Sberbank of Russia Via SB Capital SA: | | | | | | | | | | | | |

| 5.125% Sub. Nts., 10/29/225 | | | | | | | 9,790,000 | | | | 9,180,083 | |

| 5.40% Sr. Unsec. Nts., 3/24/17 | | | | | | | 5,670,000 | | | | 6,052,725 | |

| 6.125% Sr. Unsec. Nts., 2/7/225 | | | | | | | 15,050,000 | | | | 15,802,500 | |

| Scottish Widows plc, 5.125% Jr. Sub. Perpetual Bonds1,9 | | GBP | | | | | 2,175,000 | | | | 3,406,671 | |

| Societe Generale SA, 5.922% Jr. Sub. Perpetual Bonds1,5,9 | | | | | | | 10,050,000 | | | | 10,302,818 | |

| Stadshypotek AB, 6% Sec. Nts., 6/21/17 | | SEK | | | | | 169,680,000 | | | | 29,938,763 | |

| Standard Chartered plc, 5.20% Sub. Nts., 1/26/245 | | | | | | | 8,890,000 | | | | 8,953,510 | |

| Turkiye Halk Bankasi AS, 4.875% Sr. Unsec. Nts., 7/19/175 | | | | | | | 10,690,000 | | | | 10,743,450 | |

| Turkiye Is Bankasi: | | | | | | | | | | | | |

| 3.875% Sr. Unsec. Nts., 11/7/175 | | | | | | | 4,225,000 | | | | 4,071,844 | |

| 6.00% Sub. Nts., 10/24/225 | | | | | | | 12,700,000 | | | | 11,652,250 | |

| 7.293% Unsec. Nts., 10/9/132 | | TRY | | | | | 32,125,000 | | | | 15,874,764 | |

| Turkiye Sise ve Cam Fabrikalari AS, 4.25% Sr. Unsec. Nts., 5/9/205 | | | | | | | 4,575,000 | | | | 3,975,675 | |

22 OPPENHEIMER INTERNATIONAL BOND FUND

| | | | | | | | | | | | |

| | | | | | |

| Principal

Amount |

| | | Value | |

| Commercial Banks Continued | | | | | | | | | | | | |

| Turkiye Vakiflar Bankasi Tao, 3.75% Sr. Unsec. Nts., 4/15/185 | | | | | | $ | 14,535,000 | | | $ | 13,590,225 | |

| VTB Bank OJSC Via VTB Capital SA: | | | | | | | | | | | | |

| 6.00% Sr. Unsec. Nts., 4/12/175 | | | | | | | 6,440,000 | | | | 6,794,200 | |

| 6.465% Sr. Unsec. Nts., 3/4/155 | | | | | | | 4,525,000 | | | | 4,785,550 | |

| 6.875% Sr. Unsec. Nts., 5/29/185 | | | | | | | 11,360,000 | | | | 12,240,400 | |

| Yapi ve Kredi Bankasi AS: | | | | | | | | | | | | |

| 5.50% Unsec. Sub. Nts., 12/6/225 | | | | | | | 16,235,000 | | | | 13,962,100 | |

| 6.75% Sr. Unsec. Nts., 2/8/175 | | | | | | | 8,940,000 | | | | 9,389,235 | |

| | | | | | | | | | | | 914,993,341 | |

| Consumer Finance—0.0% | | | | | | | | | | | | |

Astana Finance JSC, 9.16% Sr. Unsec. Nts., 3/14/1210 | | | | | | | 14,000,000 | | | | 796,250 | |

| Diversified Financial Services—2.1% | | | | | | | | | | | | |

| AG Spring Finance Ltd., 7.50% Sr. Sec. Nts., 6/1/185 | | EUR | | | | | 665,000 | | | | 917,638 | |

| Autopistas del Nordeste Cayman Ltd., 9.39% Unsec. Nts., 4/15/245 | | | | | | | 18,302,772 | | | | 17,804,937 | |

| AyT Cedulas Cajas X Fondo de Titulizacion, 3.75% Sec. Nts., 6/30/25 | | EUR | | | | | 4,390,000 | | | | 4,815,742 | |

| Banco BTG Pactual SA (Cayman Islands): | | | | | | | | | | | | |

| 4.00% Sr. Unsec. Nts., 1/16/205 | | | | | | | 17,065,000 | | | | 15,315,837 | |

| 5.75% Sub. Nts., 9/28/225 | | | | | | | 9,105,000 | | | | 8,240,025 | |

| Banco Invex SA, 31.938% Mtg.-Backed Certificates, Series 062U, 3/13/3410 | | MXN | | | | | 27,602,566 | | | | 1,395,657 | |

| Brazil Loan Trust 1, 5.477% Sec. Nts., 7/24/235 | | | | | | | 10,265,000 | | | | 10,470,300 | |

| Cedulas TDA 6 Fondo de Titulizacion de Activos, 3.875% Sec. Nts., 5/23/25 | | EUR | | | | | 4,390,000 | | | | 4,849,654 | |

| European Investment Bank, 5% Sr. Unsec. Nts., 8/22/22 | | AUD | | | | | 21,955,000 | | | | 20,513,955 | |

| Export Credit Bank of Turkey, 5.875% Sr. Unsec. Nts., 4/24/195 | | | | | | | 23,865,000 | | | | 24,551,119 | |

| ING Verzekeringen NV, 6.375% Sub. Nts., 5/7/271 | | EUR | | | | | 7,460,000 | | | | 10,486,414 | |

| JPMorgan Hipotecaria su Casita: | | | | | | | | | | | | |

| 6.10% Sec. Nts., 9/25/35 | | MXN | | | | | 8,139,550 | | | | 992,730 | |

| 6.47% Sec. Nts., 8/26/357 | | MXN | | | | | 34,101,099 | | | | 233,074 | |

| Magyar Export-Import Bank RT, 5.50% Sr. Unsec. Nts., 2/12/185 | | | | | | | 8,250,000 | | | | 8,342,813 | |

| National Savings Bank, 8.875% Sr. Unsec. Nts., 9/18/185 | | | | | | | 6,080,000 | | | | 6,251,000 | |

| Queensland Treasury Corp. Sr. Unsec. Nts., 6.50%, Series 33, 3/14/33 | | AUD | | | | | 93,705,000 | | | | 98,431,108 | |

| | | | | | | | | | | | 233,612,003 | |

| Insurance—0.4% | | | | | | | | | | | | |

| Assicurazioni Generali SpA, 7.75% Sr. Sub. Nts., 12/12/421 | | EUR | | | | | 1,755,000 | | | | 2,573,095 | |

| Aviva plc, 6.125% Jr. Sub. Perpetual Bonds1,9 | | GBP | | | | | 6,360,000 | | | | 10,249,871 | |

| AXA SA, 6.379% Jr. Sub. Perpetual Bonds1,5,9 | | | | | | | 17,595,000 | | | | 17,001,169 | |

| Swiss Re Capital I LP, 6.854% Jr. Sub. Perpetual Bonds1,5,9 | | | | | | | 9,935,000 | | | | 10,433,677 | |

| Swiss Reinsurance Co. via ELM BV: | | | | | | | | | | | | |

| 3.96% Jr. Sub. Perpetual Bonds1,9 | | AUD | | | | | 4,405,000 | | | | 3,756,704 | |

| 7.635% Jr. Sub. Perpetual Bonds1,9 | | AUD | | | | | 1,755,000 | | | | 1,683,360 | |

| | | | | | | | | | | | 45,697,876 | |

| Real Estate Management & Development—0.4% | | | | | | | | | | | | |

| BR Malls International Finance Ltd., 8.50% Perpetual Bonds5,9 | | | | | | | 7,475,000 | | | | 7,432,953 | |

23 OPPENHEIMER INTERNATIONAL BOND FUND

| | | | |

| | |

| | STATEMENTOF INVESTMENTS Continued | | |

| | | | | | | | | | | | |

| | | | | | |

| Principal

Amount |

| | | Value | |

| Real Estate Management & Development Continued | | | | | | | | | | | | |

| Country Garden Holdings Co. Ltd., 7.50% Sr. Unsec. Unsub. Nts., 1/10/235 | | | | | | $ | 17,235,000 | | | $ | 16,674,862 | |

| Techem GmbH, 6.125% Sr. Sec. Nts., 10/1/195 | | EUR | | | | | 3,310,000 | | | | 4,836,168 | |

| | | | | | | | | | | 28,943,983 | |

| Health Care—0.0% | | | | | | | | | | | | |

| Health Care Equipment & Supplies—0.0% | | | | | | | | | | | | |

| ConvaTec Healthcare D Sarl, 10.875% Sr. Unsec. Nts., 12/15/185 | | EUR | | | | | 2,385,000 | | | $ | 3,654,065 | |

| Industrials—1.2% | | | | | | | | | | | | |

| Aerospace & Defense—0.0% | | | | | | | | | | | | |

Embraer SA, 5.15% Sr. Unsec. Nts., 6/15/22 | | | | | | | 5,160,000 | | | | 5,018,100 | |

| Airlines—0.2% | | | | | | | | | | | | |

Emirates Airline, 4.50% Sr. Unsec. Nts., 2/6/255 | | | | | | | 21,415,000 | | | | 19,273,500 | |

| Construction & Engineering—0.3% | | | | | | | | | | | | |

| Andrade Gutierrez International SA, 4% Sr. Unsec. Nts., 4/30/185 | | | | | | | 8,555,000 | | | | 8,063,087 | |

| IIRSA Norte Finance Ltd., 8.75% Sr. Sec. Nts., 5/30/247 | | | | | | | 13,535,430 | | | | 15,836,453 | |

| OAS Investments GmbH, 8.25% Sr. Nts., 10/19/195 | | | | | | | 6,285,000 | | | | 6,363,563 | |

| Odebrecht Finance Ltd., 8.25% Sr. Unsec. Nts., 4/25/185 | | BRL | | | | | 9,645,000 | | | | 3,625,524 | |

| | | | | | | | | | | | 33,888,627 | |

| Electrical Equipment—0.0% | | | | | | | | | | | | |

Orion Engineered Carbons Bondco GmbH, 10% Nts., 6/15/187 | | EUR | | | | | 3,325,500 | | | | 5,016,726 | |

| Industrial Conglomerates—0.3% | | | | | | | | | | | | |

| General Electric Capital Australia Funding Pty Ltd., 7% Sr. Unsec. Nts., 10/8/15 | | AUD | | | | | 20,805,000 | | | | 20,712,239 | |

| Hutchison Whampoa Ltd., 3.75% Perpetual Bonds1,9 | | EUR | | | | | 3,510,000 | | | | 4,517,014 | |

| KOC Holding AS, 3.50% Sr. Unsec. Nts., 4/24/205 | | | | | | | 13,425,000 | | | | 11,532,075 | |

| | | | | | | | | | | | 36,761,328 | |

| Road & Rail—0.4% | | | | | | | | | | | | |

| Kazakhstan Temir Zholy Finance BV, 6.375% Sr. Unsec. Nts., 10/6/205 | | | | | | | 6,215,000 | | | | 6,836,500 | |

| Red de Carreteras de Occidente SAPIB de CV, 9% Sr. Sec. Nts., 6/10/285 | | MXN | | | | | 200,900,000 | | | | 13,690,085 | |

| REFER-Rede Ferroviaria Nacional, 4% Sr. Unsec. Nts., 3/16/15 | | EUR | | | | | 17,945,000 | | | | 23,305,817 | |

| Transnet SOC Ltd., 4% Sr. Unsec. Nts., 7/26/225 | | | | | | | 3,940,000 | | | | 3,496,750 | |

| Ukraine Railways via Shortline plc, 9.50% Sec. Nts., 5/21/185 | | | | | | | 2,155,000 | | | | 1,734,775 | |

| | | | | | | | | | | 49,063,927 | |

| Information Technology—0.0% | | | | | | | | | | | | |

| Internet Software & Services—0.0% | | | | | | | | | | | | |

| Cerved Group SpA, 6.375% Sr. Sec. Nts., 1/15/205 | | EUR | | | | | 3,485,000 | | | | 4,832,549 | |

| Materials—2.5% | | | | | | | | | | | | |

| Chemicals—0.3% | | | | | | | | | | | | |

| Braskem Finance Ltd.: | | | | | | | | | | | | |

| 5.375% Sr. Unsec. Nts., 5/2/225 | | | | | | | 14,565,000 | | | | 13,654,687 | |

| 5.75% Sr. Unsec. Nts., 4/15/215 | | | | | | | 11,690,000 | | | | 11,514,650 | |

| Mexichem SAB de CV, 4.875% Sr. Unsec. Nts., 9/19/225 | | | | | | | 9,800,000 | | | | 9,530,500 | |

| | | | | | | | | | | 34,699,837 | |

24 OPPENHEIMER INTERNATIONAL BOND FUND

| | | | | | | | | | | | |

| | | | | | |

| Principal

Amount |

| | | Value | |

| Construction Materials—0.8% | | | | | | | | | | | | |

| Cemex Espana Luxembourg: | | | | | | | | | | | | |

| 9.25% Sr. Sec. Nts., 5/12/205 | | | | | | $ | 24,830,000 | | | $ | 26,816,400 | |

| 9.875% Sr. Sec. Nts., 4/30/195 | | | | | | | 22,730,000 | | | | 25,571,250 | |

| Cemex Finance LLC, 9.375% Sr. Sec. Nts., 10/12/225 | | | | | | | 15,115,000 | | | | 16,626,500 | |

| Cemex SAB de CV: | | | | | | | | | | | | |

| 6.50% Sec. Nts., 12/10/195 | | | | | | | 11,815,000 | | | | 11,667,312 | |

| 7.25% Sr. Sec. Nts., 1/15/215,8 | | | | | | | 12,705,000 | | | | 12,689,119 | |

| HeidelbergCement Finance BV, 8% Sr. Unsec. Nts., 1/31/17 | | EUR | | | | | 1,610,000 | | | | 2,543,136 | |

| Lafarge SA, 5.375% Sr. Unsec. Nts., 6/26/17 | | EUR | | | | | 1,775,000 | | | | 2,590,916 | |

| | | | | | | | | | | 98,504,633 | |

| Containers & Packaging—0.1% | | | | | | | | | | | | |

| Smurfit Kappa Acquisitions, 7.75% Sr. Sec. Nts., 11/15/195 | | EUR | | | | | 3,540,000 | | | | 5,217,904 | |

| Metals & Mining—1.3% | | | | | | | | | | | | |

| ALROSA Finance SA, 7.75% Nts., 11/3/205 | | | | | | | 27,135,000 | | | | 30,260,952 | |

| Consolidated Minerals Ltd., 8.875% Sr. Sec. Nts., 5/1/165 | | | | | | | 7,360,000 | | | | 7,488,800 | |

| CSN Islands XI Corp., 6.875% Sr. Unsec. Nts., 9/21/195 | | | | | | | 5,530,000 | | | | 5,751,200 | |

| Evraz Group SA, 6.50% Sr. Unsec. Nts., 4/22/205 | | | | | | | 11,455,000 | | | | 10,588,773 | |

| Ferrexpo Finance plc, 7.875% Sr. Unsec. Nts., 4/7/165 | | | | | | | 12,720,000 | | | | 11,575,200 | |

| FMG Resources August 2006 Pty Ltd., 6.875% Sr. Unsec. Nts., 2/1/185 | | | | | | | 4,685,000 | | | | 4,913,394 | |

| Gerdau Holdings, Inc., 7% Sr. Unsec. Nts., 1/20/205 | | | | | | | 2,195,000 | | | | 2,348,650 | |

| Gerdau Trade, Inc., 5.75% Sr. Unsec. Nts., 1/30/215 | | | | | | | 5,840,000 | | | | 5,752,400 | |

| Metalloinvest Finance Ltd., 5.625% Unsec. Nts., 4/17/205 | | | | | | | 8,600,000 | | | | 8,352,750 | |

| Mexico Generadora de Energia S de RL, 5.50% Sr. Sec. Nts., 12/6/325 | | | | | | | 9,120,000 | | | | 8,230,800 | |

| Samarco Mineracao SA, 4.125% Sr. Unsec. Nts., 11/1/225 | | | | | | | 6,875,000 | | | | 5,998,438 | |

| Severstal OAO Via Steel Capital SA, 4.45% Sr. Unsec. Nts., 3/19/185 | | | | | | | 5,730,000 | | | | 5,622,563 | |

| Vedanta Resources plc, 6% Sr. Nts., 1/31/195 | | | | | | | 9,640,000 | | | | 9,206,200 | |

| | | | | | | | | | | 116,090,120 | |

| Telecommunication Services—3.0% | | | | | | | | | | | | |

| Diversified Telecommunication Services—0.9% | | | | | | | | | | | | |

| Colombia Telecomunicaciones SA ESP, 5.375% Sr. Unsec. Nts., 9/27/225 | | | | | | | 4,270,000 | | | | 3,939,075 | |

| Koninklijke KPN NV, 6.125% Sr. Sub. Perpetual Bonds1,9 | | EUR | | | | | 3,960,000 | | | | 5,492,557 | |

| Oi SA: | | | | | | | | | | | | |

| 5.75% Sr. Unsec. Nts., 2/10/225 | | | | | | | 15,500,000 | | | | 13,717,500 | |

| 9.75% Sr. Unsec. Nts., 9/15/165 | | BRL | | | | | 19,740,000 | | | | 7,845,053 | |

| Portugal Telecom International Finance BV, 5.625% Sr. Unsec. Nts., 2/8/16 | | EUR | | | | | 2,425,000 | | | | 3,444,694 | |

| Telecom Italia SpA, 7.75% Sub. Nts., 3/20/731 | | EUR | | | | | 14,495,000 | | | | 19,595,246 | |

| Telefonica Chile SA, 3.875% Sr. Unsec. Nts., 10/12/225 | | | | | | | 7,735,000 | | | | 6,908,152 | |

| Telefonica Emisiones SAU, 3.987% Sr. Unsec. Nts., 1/23/23 | | EUR | | | | | 2,565,000 | | | | 3,380,866 | |

| Telemar Norte Leste SA, 5.50% Sr. Unsec. Nts., 10/23/205 | | | | | | | 30,520,000 | | | | 27,162,800 | |

| Verizon Communications, Inc., 6.55% Sr. Unsec. Nts., 9/15/43 | | | | | | | 4,440,000 | | | | 5,029,348 | |

| | | | | | | | | | | 96,515,291 | |

| Wireless Telecommunication Services—2.1% | | | | | | | | | | | | |

| America Movil SAB de CV: | | | | | | | | | | | | |

| 6.45% Sr. Unsec. Nts., 12/5/22 | | MXN | | | | | 167,530,000 | | | | 12,045,611 | |

25 OPPENHEIMER INTERNATIONAL BOND FUND

| | | | |

| | |

| | STATEMENTOF INVESTMENTS Continued | | |

| | | | | | | | | | | | |

| | | | | | | | Principal Amount | | | | Value | |

| Wireless Telecommunication Services Continued | | | | | | | | | | | | |

| America Movil SAB de CV: Continued | | | | | | | | | | | | |

| 8.46%, 12/18/36 | | MXN | | | | $ | 140,800,000 | | | $ | 10,530,166 | |

| Digicel Group Ltd., 8.25% Sr. Unsec. Nts., 9/30/205 | | | | | | | 4,610,000 | | | | 4,794,400 | |

| Digicel Ltd., 6% Sr. Unsec. Nts., 4/15/215 | | | | | | | 8,800,000 | | | | 8,294,000 | |

| Millicom International Cellular SA, 4.75% Sr. Unsec. Nts., 5/22/205 | | | | | | | 6,600,000 | | | | 6,154,500 | |

| MTS International Funding Ltd.: | | | | | | | | | | | | |

| 5.00% Sr. Unsec. Nts., 5/30/235 | | | | | | | 8,570,000 | | | | 7,905,825 | |

| 8.625% Sr. Unsec. Nts., 6/22/205 | | | | | | | 14,110,000 | | | | 16,561,613 | |

| Vimpel Communications Via VIP Finance Ireland Ltd. OJSC: | | | | | | | | | | | | |

| 7.748% Sr. Unsec. Nts., 2/2/215 | | | | | | | 16,210,000 | | | | 17,506,800 | |

| 9.125% Sr. Unsec. Nts., 4/30/185 | | | | | | | 34,205,000 | | | | 39,763,313 | |

| VimpelCom Holdings BV: | | | | | | | | | | | | |