UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER

THE SECURITIES EXCHANGE ACT OF 1934

For the month of July, 2019

Commission File Number: 001-13742

ISRAEL CHEMICALS LTD.

(Exact name of registrant as specified in its charter)

Israel Chemicals Ltd.

Millennium Tower

23 Aranha Street

P.O. Box 20245

Tel Aviv, 61202 Israel

(972-3) 684-4400

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

| Form 20-F | X | Form 40-F |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

| Yes | No | X |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

| Yes | No | X |

ISRAEL CHEMICALS LTD.

| 1. | S&P Reaffirms ICL’s BBB- Rating with a Stable Outlook |

Item 1

S&P Reaffirms ICL’s BBB- Rating with a Stable Outlook

The Company hereby reports that S&P has reaffirmed the Company’s Long-Term Issuer Default Rating at BBB- with a Stable Outlook.

The S&P report is attached.

Israel Chemicals Ltd. Primary Credit Analyst: Paulina Grabowiec, London (44) 20 - 7176 - 7051; paulina.grabo wiec@spglobal.com Secondary Contact: Hila Perelmuter, RAMAT - GAN (972) 3 - 753 - 9727; hila.perelm uter@spglobal.com Table Of Contents Credit Highlights Outlook Our Base - Case Scenario Company Description Business Risk Financial Risk Liquidity Covenant Analysis Environmental, Social, And Governance Group Influence Issue Ratings - Subordination Risk Analysis Reconciliation Ratings Score Snapshot JULY 4, 2019 1 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT

Table Of Contents (cont.) Related Criteria JULY 4, 2019 2 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT

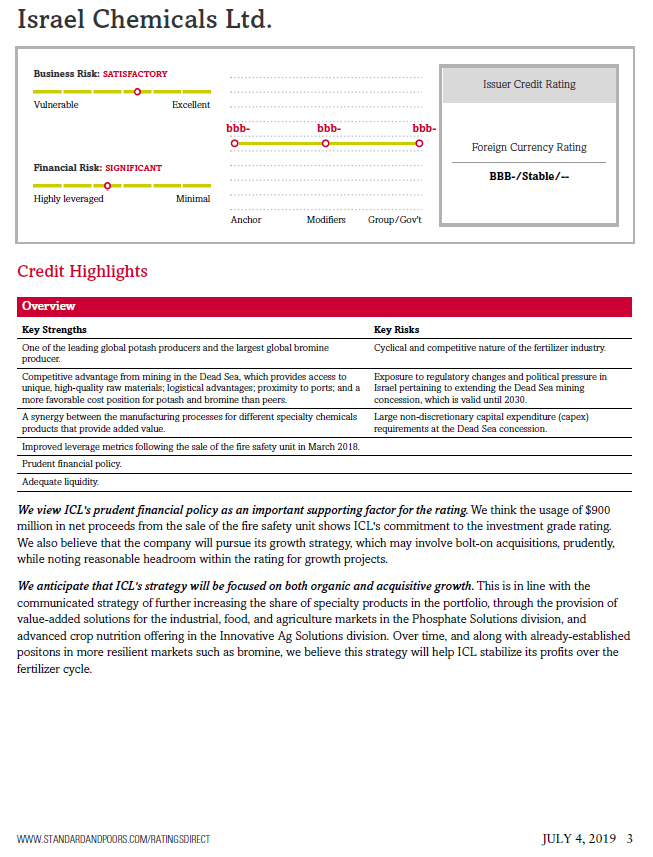

Israel Chemicals Ltd. V ulner a ble Excellent Financial Risk: SIGNIFICANT Highly leveraged Minimal bbb - bbb - bbb - Anchor Modifie r s G r oup/G o v't Business Risk: SATISFACTORY Issuer Credit Rating Foreign Currency Rating BBB - /Sta b le/ -- Credit Highlights Overview Key Strengths Key Risks One of the leading global potash producers and the largest global bromine Cyclical and competitive nature of the fertilizer industry. producer. Competitive advantage from mining in the Dead Sea, which provides access to unique, high - quality raw materials; logistical advantages; proximity to ports; and a more favorable cost position for potash and bromine than peers. Exposure to regulatory changes and political pressure in Israel pertaining to extending the Dead Sea mining concession, which is valid until 2030. A synergy between the manufacturing processes for different specialty chemicals products that provide added value. Large non - discretionary capital expenditure (capex) requirements at the Dead Sea concession. Improved leverage metrics following the sale of the fire safety unit in March 2018. Prudent financial policy. Adequate liquidity. We view ICL's prudent financial policy as an important supporting factor for the rating . We think the usage of $ 900 million in net proceeds from the sale of the fire safety unit shows ICL's commitment to the investment grade rating . We also believe that the company will pursue its growth strategy, which may involve bolt - on acquisitions, prudently, while noting reasonable headroom within the rating for growth projects . We anticipate that ICL's strategy will be focused on both organic and acquisitive growth. This is in line with the communicated strategy of further increasing the share of specialty products in the portfolio, through the provision of value - added solutions for the industrial, food, and agriculture markets in the Phosphate Solutions division, and advanced crop nutrition offering in the Innovative Ag Solutions division. Over time, and along with already - established positons in more resilient markets such as bromine, we believe this strategy will help ICL stabilize its profits over the fertilizer cycle. JULY 4, 2019 3 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT

Outlook: Stable The stable outlook on Israel Chemicals Ltd. (ICL) reflects our expectation that ICL will maintain S&P Global Ratings - adjusted debt to EBITDA of 2.5x - 3.5x in the gradually recovering fertilizer pricing environment. Our expectation is based on the company's plan to undertake midsize acquisitions in the coming years and maintain its current dividend policy. We anticipate that ICL will generate adjusted EBITDA of about $1.1 billion - $1.3 billion in 2019 and 2020, benefiting from a strong position in the fertilizer markets and low production costs in Israel. We consider an adjusted debt - to - EBITDA ratio of 3.0x at the top of the business cycle and 4.0x at the bottom of the cycle to be commensurate with the current rating. Upside scenario We would consider a positive rating action if ICL strengthened its financial risk profile such that its adjusted debt to EBITDA remained below 2.5x on a sustainable basis. We believe, at current leverage, ICL has some headroom for bolt - on acquisitions. We understand it may be pursuing these to enhance its product portfolio and geographic reach. Rating upside is further constrained by the lack of sufficient clarity on the growth strategy of Israel Corp, ICL's 46% parent and main shareholder. Downside scenario We would consider a negative rating action if the company's debt to EBITDA was close to 4.0x without near - term prospects of recovery, and its operating performance deteriorated. In our view, this could arise if ICL implemented aggressive business or financial policies, either by deviating from its publicly stated dividend policy or through sizable leveraged acquisitions. Further deterioration in market conditions that may hurt operating results could also lead to a downgrade. In the medium term, the rating could come under pressure if uncertainty regarding the renewal of the Dead Sea concession continues. In this scenario, we expect pressure on the company's business risk, which currently benefits from its inherent advantages in the Dead Sea. JULY 4, 2019 4 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT Our Base - Case Scenario Israel Chemicals Ltd.

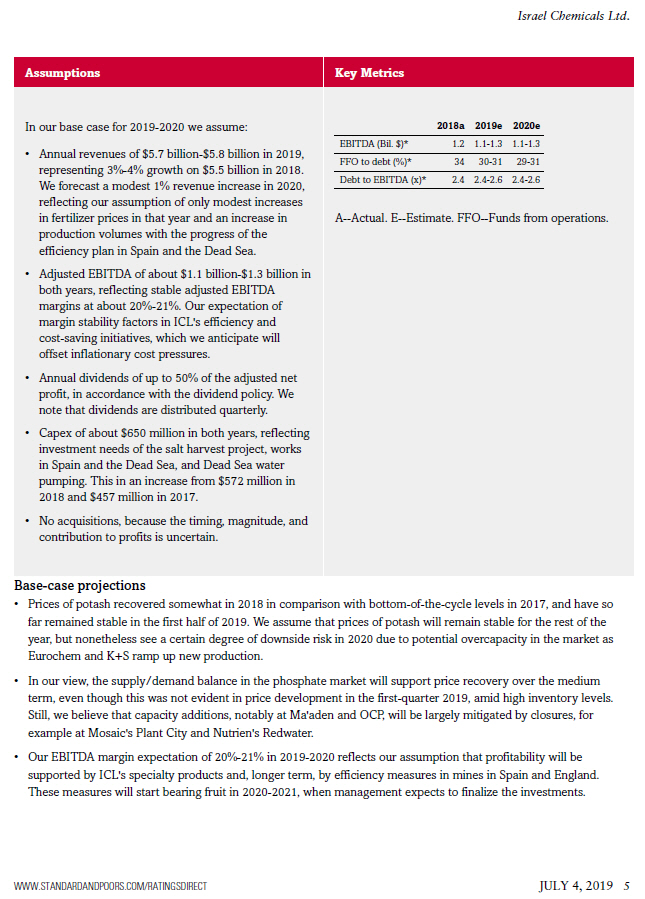

Assumptions Key Metrics In our base case for 2019 - 2020 we assume: 2018a 2019e 2020e • Annual revenues of $ 5 . 7 billion - $ 5 . 8 billion in 2019 , representing 3 % - 4 % growth on $ 5 . 5 billion in 2018 . We forecast a modest 1 % revenue increase in 2020 , EBITDA (Bil. $)* 1.2 1.1 - 1.3 1.1 - 1.3 FFO to debt (%)* 34 30 - 31 29 - 31 Debt to EBITDA (x)* 2.4 2.4 - 2.6 2.4 - 2.6 reflecting our assumption of only modest increases in fertilizer prices in that year and an increase in A -- Actual. E -- Estimate. FFO -- Funds from operations. production volumes with the progress of the efficiency plan in Spain and the Dead Sea. • Adjusted EBITDA of about $1.1 billion - $1.3 billion in both years, reflecting stable adjusted EBITDA margins at about 20% - 21%. Our expectation of margin stability factors in ICL's efficiency and cost - saving initiatives, which we anticipate will offset inflationary cost pressures. • Annual dividends of up to 50% of the adjusted net profit, in accordance with the dividend policy. We note that dividends are distributed quarterly. • Capex of about $650 million in both years, reflecting investment needs of the salt harvest project, works in Spain and the Dead Sea, and Dead Sea water pumping. This in an increase from $572 million in 2018 and $457 million in 2017. • No acquisitions, because the timing, magnitude, and contribution to profits is uncertain. JULY 4, 2019 5 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT Base - case projections • Prices of potash recovered somewhat in 2018 in comparison with bottom - of - the - cycle levels in 2017, and have so far remained stable in the first half of 2019. We assume that prices of potash will remain stable for the rest of the year, but nonetheless see a certain degree of downside risk in 2020 due to potential overcapacity in the market as Eurochem and K+S ramp up new production. • In our view, the supply/demand balance in the phosphate market will support price recovery over the medium term, even though this was not evident in price development in the first - quarter 2019, amid high inventory levels. Still, we believe that capacity additions, notably at Ma'aden and OCP, will be largely mitigated by closures, for example at Mosaic's Plant City and Nutrien's Redwater. • Our EBITDA margin expectation of 20% - 21% in 2019 - 2020 reflects our assumption that profitability will be supported by ICL's specialty products and, longer term, by efficiency measures in mines in Spain and England. These measures will start bearing fruit in 2020 - 2021, when management expects to finalize the investments. Israel Chemicals Ltd.

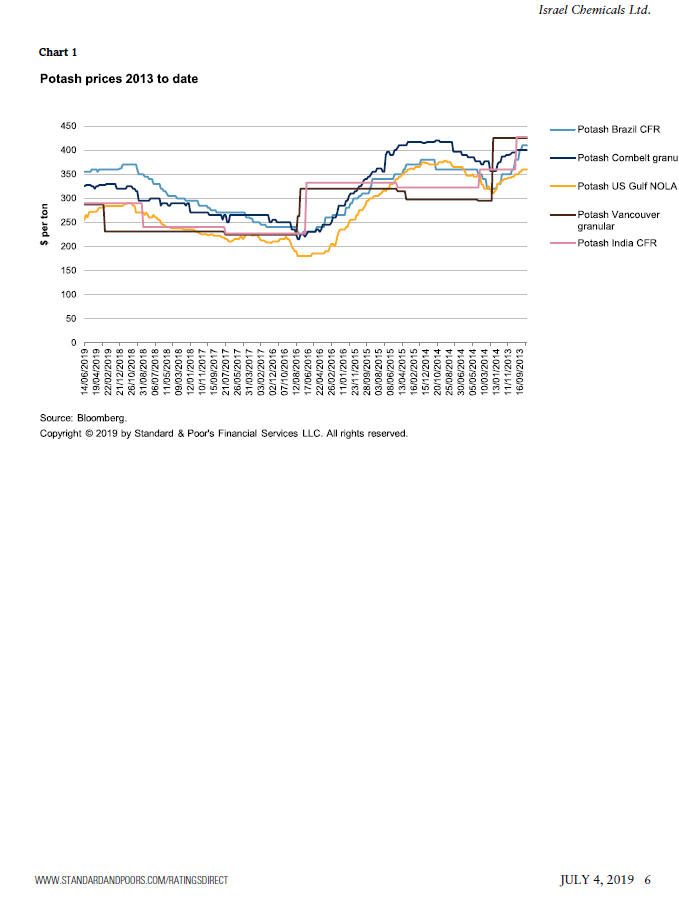

Israel Chemicals Ltd. Chart 1 JULY 4, 2019 6 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT

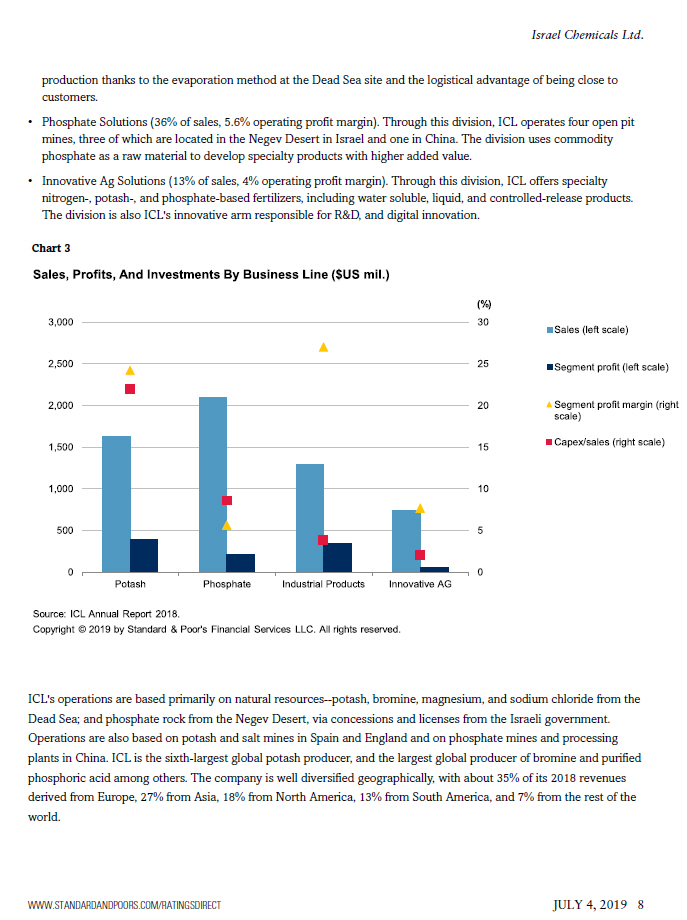

Company Description ICL is a multinational company that operates in the manufacturing and marketing of basic and specialty fertilizers based on potash, phosphate, and bromine. The company is organised into four main divisions: • Industrial Products (23% of 2018 sales, 23% operating profit margin). Through this key division, ICL manufactures elemental bromine for a wide range of applications in flame retardants, magnesia and salt products, and energy storage. ICL's Dead Sea operations offer the world's largest reserves with the highest bromine concentration. Together with its two main competitors, Albemarle and Lanxess, ICL accounted for the majority of global bromine production in 2018. Barriers to entry in this market are high, due to access to economically viable reserves of bromine, and stringent requirements for the logistics system (special containers are required for transporting the bromine). ICL uses about 75% of its elemental bromine production (that is about 130,000 tonnes) internally for the production of higher margin bromine compounds. • Potash (28% of sales, 20% operating profit margin). In this segment, ICL produces and markets potash fertilizers and salt extracted from the Dead Sea through a cost - efficient evaporation process, and from a conventional underground mine in Spain. It also transitioned its U.K. - based Boulby mine to the production of advanced polyhalite - based fertilizer (marketed by ICL as Polysulphate) from the production of potash. Even though ICL's potash operations are smaller than key competitors Nutrien, Uralkali, or Mosaic, ICL benefits from low cost of JULY 4, 2019 7 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT Israel Chemicals Ltd. Chart 2

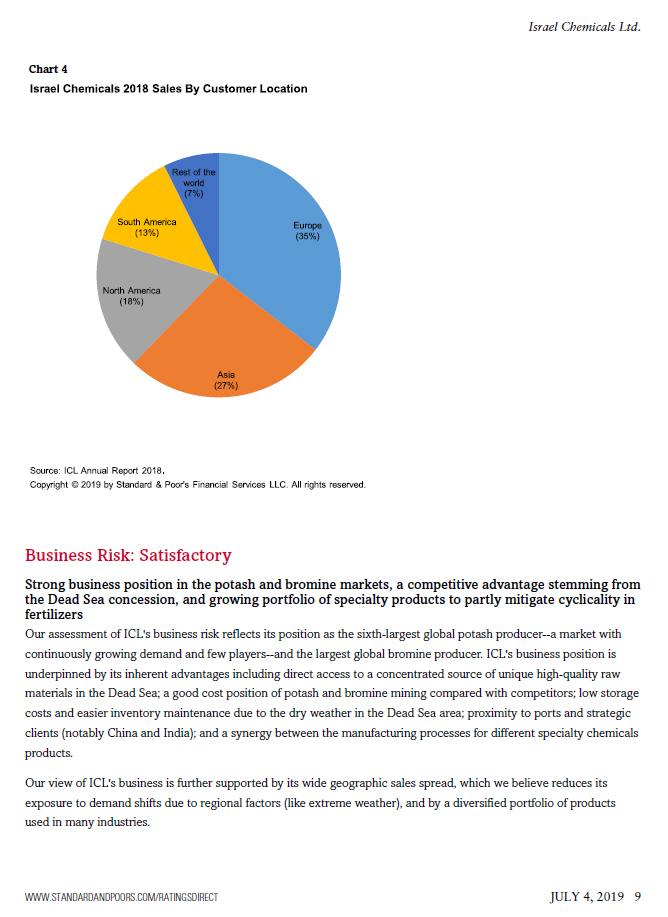

ICL's operations are based primarily on natural resources -- potash, bromine, magnesium, and sodium chloride from the Dead Sea; and phosphate rock from the Negev Desert, via concessions and licenses from the Israeli government. Operations are also based on potash and salt mines in Spain and England and on phosphate mines and processing plants in China. ICL is the sixth - largest global potash producer, and the largest global producer of bromine and purified phosphoric acid among others. The company is well diversified geographically, with about 35% of its 2018 revenues derived from Europe, 27% from Asia, 18% from North America, 13% from South America, and 7% from the rest of the world. JULY 4, 2019 8 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT Israel Chemicals Ltd. production thanks to the evaporation method at the Dead Sea site and the logistical advantage of being close to customers. • Phosphate Solutions (36% of sales, 5.6% operating profit margin). Through this division, ICL operates four open pit mines, three of which are located in the Negev Desert in Israel and one in China. The division uses commodity phosphate as a raw material to develop specialty products with higher added value. • Innovative Ag Solutions (13% of sales, 4% operating profit margin). Through this division, ICL offers specialty nitrogen - , potash - , and phosphate - based fertilizers, including water soluble, liquid, and controlled - release products. The division is also ICL's innovative arm responsible for R&D, and digital innovation. Chart 3

Business Risk: Satisfactory Strong business position in the potash and bromine markets, a competitive advantage stemming from the Dead Sea concession, and growing portfolio of specialty products to partly mitigate cyclicality in fertilizers Our assessment of ICL's business risk reflects its position as the sixth - largest global potash producer -- a market with continuously growing demand and few players -- and the largest global bromine producer. ICL's business position is underpinned by its inherent advantages including direct access to a concentrated source of unique high - quality raw materials in the Dead Sea; a good cost position of potash and bromine mining compared with competitors; low storage costs and easier inventory maintenance due to the dry weather in the Dead Sea area; proximity to ports and strategic clients (notably China and India); and a synergy between the manufacturing processes for different specialty chemicals products. Our view of ICL's business is further supported by its wide geographic sales spread, which we believe reduces its exposure to demand shifts due to regional factors (like extreme weather), and by a diversified portfolio of products used in many industries. JULY 4, 2019 9 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT Israel Chemicals Ltd. Chart 4

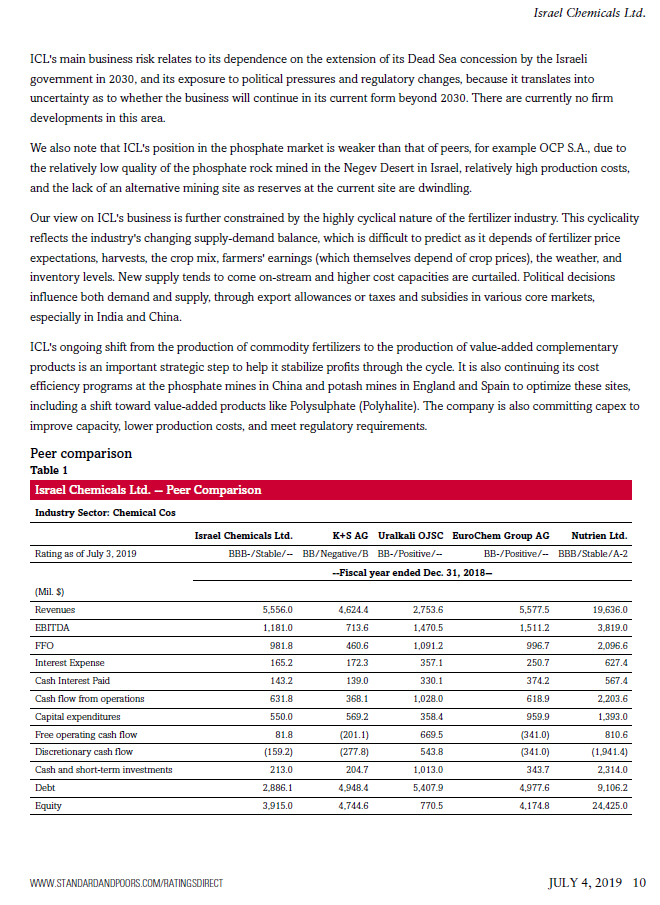

Israel Chemicals Ltd. -- Peer Comparison Industry Sector: Chemical Cos Israel Chemicals Ltd. K+S AG Uralkali OJSC EuroChem Group AG Nutrien Ltd. Rating as of July 3, 2019 BBB - /Stable/ -- BB/Negative/B BB - /Positive/ -- BB - /Positive/ -- BBB/Stable/A - 2 -- Fiscal year ended Dec. 31, 2018 -- JULY 4, 2019 10 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT (Mil. $) Revenues 5,556.0 4,624.4 2,753.6 5,577.5 19,636.0 EBITDA 1,181.0 713.6 1,470.5 1,511.2 3,819.0 FFO 981.8 460.6 1,091.2 996.7 2,096.6 Interest Expense 165.2 172.3 357.1 250.7 627.4 Cash Interest Paid 143.2 139.0 330.1 374.2 567.4 Cash flow from operations 631.8 368.1 1,028.0 618.9 2,203.6 Capital expenditures 550.0 569.2 358.4 959.9 1,393.0 Free operating cash flow 81.8 (201.1) 669.5 (341.0) 810.6 Discretionary cash flow (159.2) (277.8) 543.8 (341.0) (1,941.4) Cash and short - term investments 213.0 204.7 1,013.0 343.7 2,314.0 Debt 2,886.1 4,948.4 5,407.9 4,977.6 9,106.2 Equity 3,915.0 4,744.6 770.5 4,174.8 24,425.0 Israel Chemicals Ltd. ICL's main business risk relates to its dependence on the extension of its Dead Sea concession by the Israeli government in 2030, and its exposure to political pressures and regulatory changes, because it translates into uncertainty as to whether the business will continue in its current form beyond 2030. There are currently no firm developments in this area. We also note that ICL's position in the phosphate market is weaker than that of peers, for example OCP S . A . , due to the relatively low quality of the phosphate rock mined in the Negev Desert in Israel, relatively high production costs, and the lack of an alternative mining site as reserves at the current site are dwindling . Our view on ICL's business is further constrained by the highly cyclical nature of the fertilizer industry. This cyclicality reflects the industry's changing supply - demand balance, which is difficult to predict as it depends of fertilizer price expectations, harvests, the crop mix, farmers' earnings (which themselves depend of crop prices), the weather, and inventory levels. New supply tends to come on - stream and higher cost capacities are curtailed. Political decisions influence both demand and supply, through export allowances or taxes and subsidies in various core markets, especially in India and China. ICL's ongoing shift from the production of commodity fertilizers to the production of value - added complementary products is an important strategic step to help it stabilize profits through the cycle. It is also continuing its cost efficiency programs at the phosphate mines in China and potash mines in England and Spain to optimize these sites, including a shift toward value - added products like Polysulphate (Polyhalite). The company is also committing capex to improve capacity, lower production costs, and meet regulatory requirements. Peer comparison Table 1

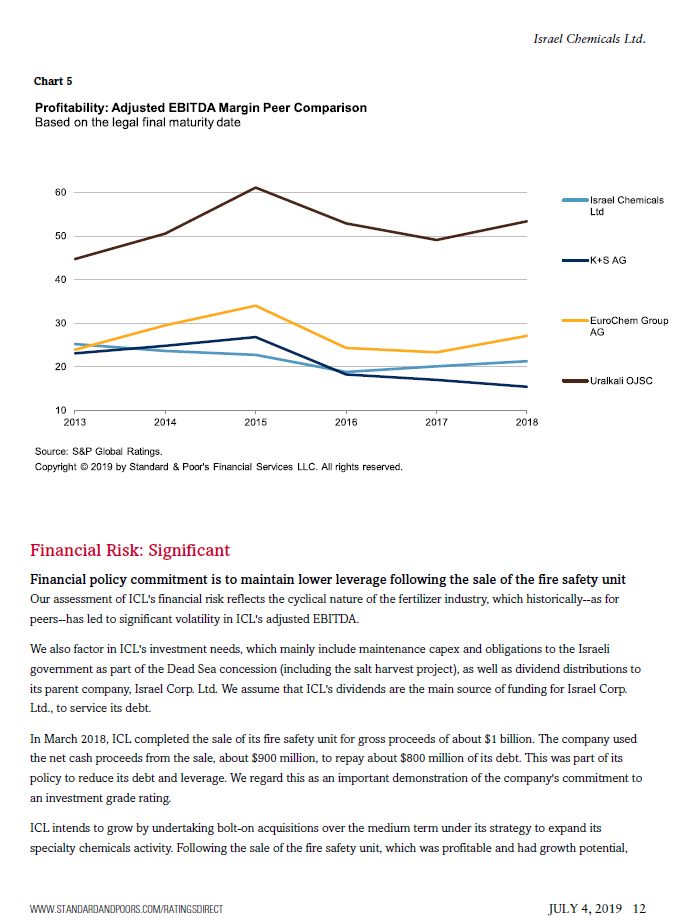

JULY 4, 2019 11 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT Israel Chemicals Ltd. -- Peer Comparison (cont.) Industry Sector: Chemical Cos Israel Chemicals Ltd. K+S AG Uralkali OJSC EuroChem Group AG Nutrien Ltd. Adjusted ratios EBITDA margin (%) 21.3 15.4 53.4 27.1 19.4 Return on capital (%) 11.2 2.7 19.2 13.5 5.4 EBITDA interest coverage (x) 7.1 4.1 4.1 6.0 6.1 FFO cash interest coverage (x) 7.9 4.3 4.3 3.7 4.7 Debt/EBITDA (x) 2.4 6.9 3.7 3.3 2.4 FFO/debt (%) 34.0 9.3 20.2 20.0 23.0 Cash flow from operations/debt (%) 21.9 7.4 19.0 12.4 24.2 Free operating cash flow/debt (%) 2.8 (4.1) 12.4 (6.9) 8.9 Discretionary cash flow/debt (%) (5.5) (5.6) 10.1 (6.9) (21.3) We compare ICL with business peers operating in the potash and phosphate fertilizer industry, such as K+S AG, Uralkali OJSC, EuroChem Group AG, and Nutrien Ltd. ICL's adjusted EBITDA margins have historically lagged those of Eurochem, which benefits from a first - quartile position on the phosphate cost curve thanks to access to lower gas prices for Russian producers and a high degree of vertical integration. In comparison with K+S, ICL displays higher margins, reflecting its highly advantageous cost position in potash given its access to high quality raw materials in the Dead Sea. By comparison, K+S' profitability has been declining in recent years due to production challenges and the high cost position of its German mines. Overall, the EBITDA margins of ICL, K+S, and Eurochem contrast with Uralkali's superior margins. The latter has large and very - low - cost reserves, which position it as leader on the global cost curve. Israel Chemicals Ltd. Table 1

Financial Risk: Significant Financial policy commitment is to maintain lower leverage following the sale of the fire safety unit Our assessment of ICL's financial risk reflects the cyclical nature of the fertilizer industry, which historically -- as for peers -- has led to significant volatility in ICL's adjusted EBITDA. We also factor in ICL's investment needs, which mainly include maintenance capex and obligations to the Israeli government as part of the Dead Sea concession (including the salt harvest project), as well as dividend distributions to its parent company, Israel Corp. Ltd. We assume that ICL's dividends are the main source of funding for Israel Corp. Ltd., to service its debt. In March 2018, ICL completed the sale of its fire safety unit for gross proceeds of about $1 billion. The company used the net cash proceeds from the sale, about $900 million, to repay about $800 million of its debt. This was part of its policy to reduce its debt and leverage. We regard this as an important demonstration of the company's commitment to an investment grade rating. ICL intends to grow by undertaking bolt - on acquisitions over the medium term under its strategy to expand its specialty chemicals activity. Following the sale of the fire safety unit, which was profitable and had growth potential, JULY 4, 2019 12 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT Israel Chemicals Ltd. Chart 5

Israel Chemicals Ltd. -- Yearly Data Industry Sector: Chemical Cos -- Fiscal year ended Dec. 31 -- JULY 4, 2019 13 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT 2018 2017 2016 2015 2014 Rating history BBB - /St a ble/ -- BBB - /St a ble/ -- BBB - /St a ble/ -- BBB/Negat i ve/ - - BBB/St a ble/ -- (Mil. $) Revenues 5,556.0 5,418.0 5,363.0 5,405.0 6,110.7 EBITDA 1,181.0 1,087.0 1,006.5 1,224.9 1,443.7 FFO 981.8 810.7 776.0 1,086.8 1,212.5 Interest Expense 165.2 175.3 187.5 132.1 131.7 Cash Interest Paid 143.2 149.3 146.5 118.1 72.5 Cash flow from operations 631.8 859.7 987.0 595.8 916.4 Capital expenditures 550.0 434.0 610.0 598.0 819.2 Free operating cash flow 81.8 425.7 377.0 (2.2) 97.1 Discretionary cash flow (159.2) 188.7 215.0 (350.2) (748.8) Cash and short - term investments 213.0 173.0 116.0 248.0 247.3 Gross available cash 183.0 146.0 96.0 248.0 247.3 Debt 2,886.1 3,812.5 3,923.0 3,786.1 3,234.9 Equity 3,915.0 2,930.0 2,659.0 3,188.0 3,000.2 Israel Chemicals Ltd. ICL's EBITDA decreased by about $80 million. We understand that ICL's board of directors has approved the current dividend distribution policy for 2019, unchanged since 2016, despite the deleveraging following the fire safety unit sale. In 2019 - 2020, ICL intends to invest further in its mines in Spain and England to increase the efficiency of its potash production and comply with regulatory requirements in these countries. We also anticipate that due to a maintenance period in the Dead Sea, production at this site will decline temporarily in the fourth quarter of 2019. In our base - case scenario, therefore, we assume an increase in capex in 2019 - 2020 due to high investment needs in England, Spain, the Negev Desert, and the Dead Sea (including the salt harvest project). We understand that these projects will be finalized in 2020 - 2021, leading to an improvement in production efficiency when the sites get back to full capacity. Under our base case, we forecast that adjusted debt to EBITDA will be around 2.4x - 2.6x and adjusted funds from operations (FFO) to debt will be around 29% - 31% in 2019 - 2020, depending on the pace of the efficiency plan, compared with 2.4x and 34% in 2018. We do not factor in any acquisitions because the timing, magnitude, and contribution to profits is uncertain, but we note that the company has reasonable headroom to pursue growth projects. The fertilizer industry's cyclicality is a structural constraint to its financial risk because it translates into certain volatility in profits outside of the company's control, as well as large seasonal working capital swings. ICL's track record of navigating the business through the cycle, in combination with prudent financial policy, are important mitigating factors. Financial summary Table 2

Israel Chemicals Ltd. -- Yearly Data (cont.) Industry Sector: Chemical Cos -- Fiscal year ended Dec. 31 -- JULY 4, 2019 14 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT 2018 2017 2016 2015 2014 Adjusted ratios EBITDA margin (%) 21.3 20.1 18.8 22.7 23.6 Return on capital (%) 11.2 9.3 8.3 12.1 16.2 EBITDA interest coverage (x) 7.1 6.2 5.4 9.3 11.0 FFO cash interest coverage (x) 7.9 6.4 6.3 10.2 17.7 Debt/EBITDA (x) 2.4 3.5 3.9 3.1 2.2 FFO/debt (%) 34.0 21.3 19.8 28.7 37.5 Cash flow from operations/debt (%) 21.9 22.6 25.2 15.7 28.3 Free operating cash flow/debt (%) 2.8 11.2 9.6 (0.1) 3.0 Discretionary cash flow/debt (%) (5.5) 5.0 5.5 (9.3) (23.1) FFO -- Funds from operations. Liquidity: Adequate ICL's liquidity is adequate. Our assessment of ICL's liquidity reflects our expectation that the ratio of sources and uses will be around 1.3x in the 12 months from March 31, 2019. Our assessment is underpinned by the company's prudent liquidity management, sufficient unutilized committed credit lines, and good access to the banking system and the Israeli capital markets. Principal Liquidity Sources Principal Liquidity Uses • Available cash and cash equivalents of about $183 million on March 31, 2019. • Availability under long - term committed credit facilities maturing beyond one year of about $1 billion; and • Our forecast of unadjusted cash FFO of about $900 million. • Short - term debt maturities of about $638 million; • Capex of about $650 million; • Working capital outflows (including intra - year) of about $150 million - $200 million; and • Dividend distribution of about $200 million - $250 million. Covenant Analysis We forecast comfortable headroom under the covenants incorporated in ICL's debt agreements. These include: • Total shareholders' equity greater than $2 billion; • EBITDA net interest cover ratio equal to, or greater than 3.5x; Israel Chemicals Ltd. Table 2

Environmental, Social, And Governance As with peers, ICL can be subject to regulatory and environmental requirements that relate to its use of natural resources under its concession agreement with the Israeli government. Two major projects are the harvest project and the pumping station, both at the Dead Sea. The minerals from the Dead Sea are produced by means of solar evaporation, in which salt sinks to the bottom of one of the pools. This creates a layer on the bottom of the pool, which increases the water level. Raising the water above a certain level may cause damage to the foundations and hotel buildings located near the shoreline and to other infrastructure on the beach. The company, together with the Israeli government, is working on both the establishment of coastal defenses and the permanent solution of the harvest of salt from the bottom of the sea. As part of the production process, ICL draws water from the northern basin of the Dead Sea through a dedicated pumping station and transfers them to the pools of salt and carnallite at the southern part of the sea. As a result, there was a decrease in the water level of the northern basin of the Dead Sea along the years. This may create pressure on ICL to reduce the use of minerals from the Dead Sea, which can have an adverse effect on its business in the long term. In addition, ICL is exposed to lawsuits in connection with malfunctions at its plants with ecological environmental impact. For example, in 2017, a pool used to store water gypsum formed in production processes in the Negev collapsed. This event led to a severe environmental pollution and ICL immediately began rehabilitation procedures, to the extent possible. However, class action suits were filed against ICL in which the company was required to bear long - term costs relating to rehabilitation programs. Such costs are hard to predict but could influence the financials and credit metrics of the company once incurred. JULY 4, 2019 15 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT Group Influence ICL is controlled by Israel Corp. Ltd., an Israel - based company, traded on the Tel Aviv stock exchange. Israel Corp's asset portfolio is dominated by its controlling stake in ICL (about 80% of Israel Corp's portfolio value). It is also the major shareholder of Oil Refineries Ltd. (ORL), an Israel - based energy company (about 20% of its portfolio value). Israel Corp.'s main source of cash for its debt service are the dividends from ICL, bearing in mind that ORL's dividends are relatively limited. As such, we view ICL as a core subsidiary of Israel Corp. Notwithstanding this status, we view ICL's credit quality as insulated from the estimated credit quality of Israel Corp due to relatively strong Israeli legislative and regulatory protection frameworks, where both companies are incorporated. Still, we understand that Israel Corp's new stated strategy is to expand its holding portfolio to new industries, through Israel Chemicals Ltd. • Net financial debt to EBITDA less than 4.0x; and • Ratio of certain subsidiaries loans to total consolidated assets of less than 10%.

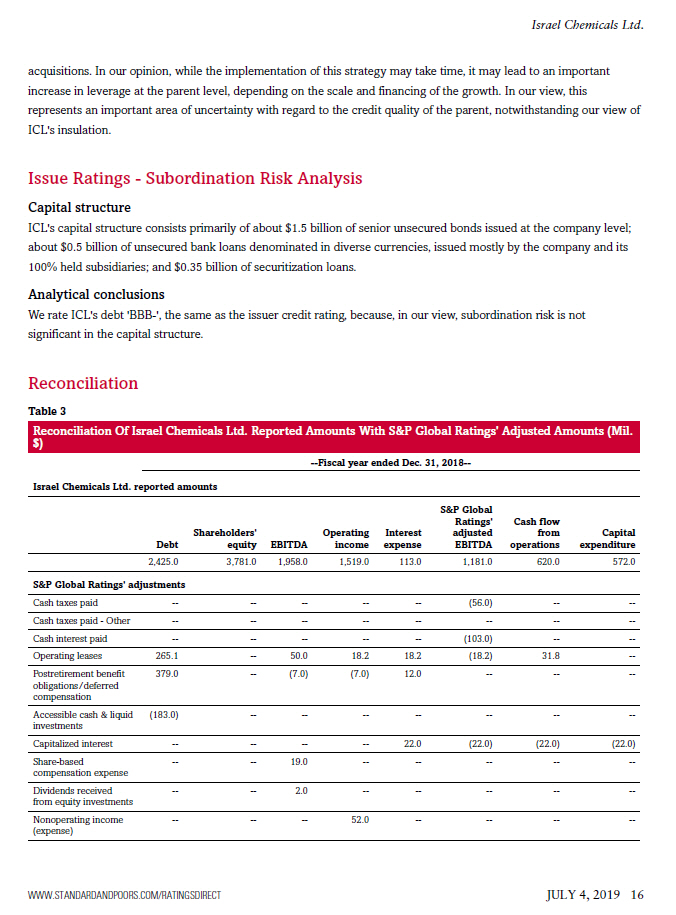

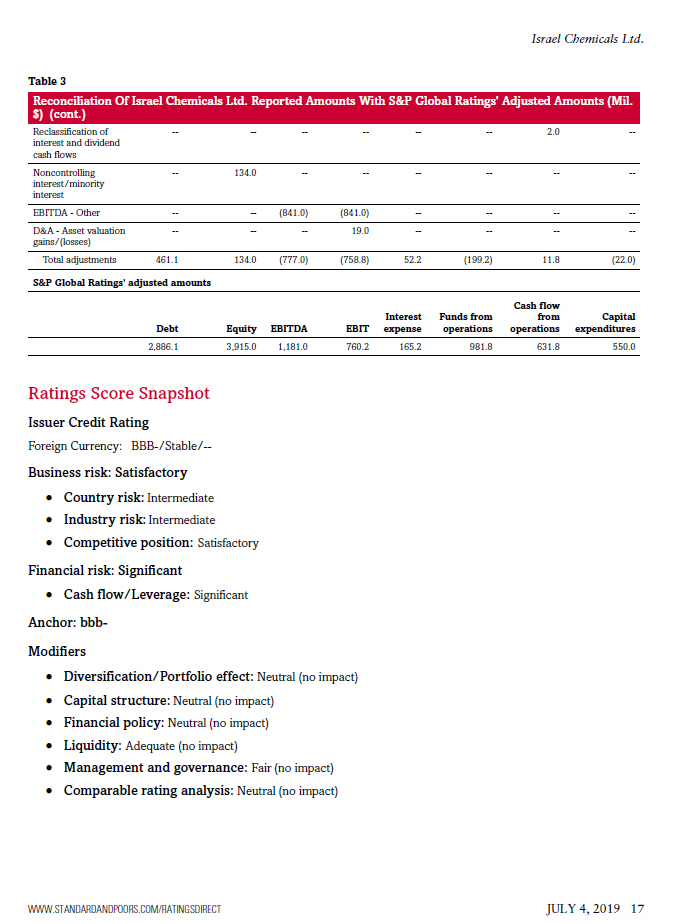

Reconciliation Of Israel Chemicals Ltd. Reported Amounts With S&P Global Ratings' Adjusted Amounts (Mil. $) -- Fiscal year ended Dec. 31, 2018 -- Israel Chemicals Ltd. reported amounts JULY 4, 2019 16 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT Debt Shareholders' equity EBIT D A Ope r atin g incom e Inte r es t expens e S&P Global Ratings' adjuste d EBITDA Cash flow f r o m ope r ation s Capita l expenditu r e 2,425.0 3,781.0 1,958.0 1,519.0 113.0 1,181.0 620.0 572.0 S&P Global Ratings' adjustments Cash taxes paid -- -- -- -- -- (56.0) -- -- Cash taxes paid - Other -- -- -- -- -- -- -- -- Cash interest paid -- -- -- -- -- (103.0) -- -- Operating leases 265.1 -- 50.0 18.2 18.2 (18.2) 31.8 -- Postretirement benefit obligations/deferred compensation 379.0 -- (7.0) (7.0) 12.0 -- -- -- Accessible cash & liquid investments (183.0) -- -- -- -- -- -- -- Capitalized interest -- -- -- -- 22.0 (22.0) (22.0) (22.0) Share - based compensation expense -- -- 19.0 -- -- -- -- -- Dividends received from equity investments -- -- 2.0 -- -- -- -- -- Nonoperating income (expense) -- -- -- 52.0 -- -- -- -- Israel Chemicals Ltd. acquisitions. In our opinion, while the implementation of this strategy may take time, it may lead to an important increase in leverage at the parent level, depending on the scale and financing of the growth. In our view, this represents an important area of uncertainty with regard to the credit quality of the parent, notwithstanding our view of ICL's insulation. Issue Ratings - Subordination Risk Analysis Capital structure ICL's capital structure consists primarily of about $ 1 . 5 billion of senior unsecured bonds issued at the company level ; about $ 0 . 5 billion of unsecured bank loans denominated in diverse currencies, issued mostly by the company and its 100 % held subsidiaries ; and $ 0 . 35 billion of securitization loans . Analytical conclusions We rate ICL's debt 'BBB - ', the same as the issuer credit rating, because, in our view, subordination risk is not significant in the capital structure. Reconciliation Table 3

JULY 4, 2019 17 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT Reconciliation Of Israel Chemicals Ltd. Reported Amounts With S&P Global Ratings' Adjusted Amounts (Mil. $) (cont.) Reclassification of -- interest and dividend cash flows -- -- -- -- -- 2.0 -- Noncontrolling -- interest/minor ity interest 134.0 -- -- -- -- -- -- EBIT D A - Other -- -- (841.0) (841.0) -- -- -- -- D&A - Asset v aluation - - gains/(losses) -- -- 19.0 -- -- -- -- Total adjustments 461.1 134.0 (777.0) (758.8) 52.2 (199.2) 11.8 (22.0) S&P Global Ratings' adjusted amounts Inte r est Funds from Cash flow from Capital Debt Equity EBIT D A EBIT expense ope r ations ope r ations expenditu r es 2,886.1 3,915.0 1,181.0 760.2 165.2 981.8 631.8 550.0 Ratings Score Snapshot Issuer Credit Rating Foreign Currency: BBB - /Stable/ -- Business risk: Satisfactory Country risk: Intermediate Industry risk: Intermediate Competitive position: Satisfactory Financial risk: Significant Cash flow/Leverage: Significant Anchor: bbb - Modifiers Diversification/Portfolio effect: Neutral (no impact) Capital structure: Neutral (no impact) Financial policy: Neutral (no impact) Liquidity: Adequate (no impact) Management and governance: Fair (no impact) Comparable rating analysis: Neutral (no impact) Israel Chemicals Ltd. Table 3

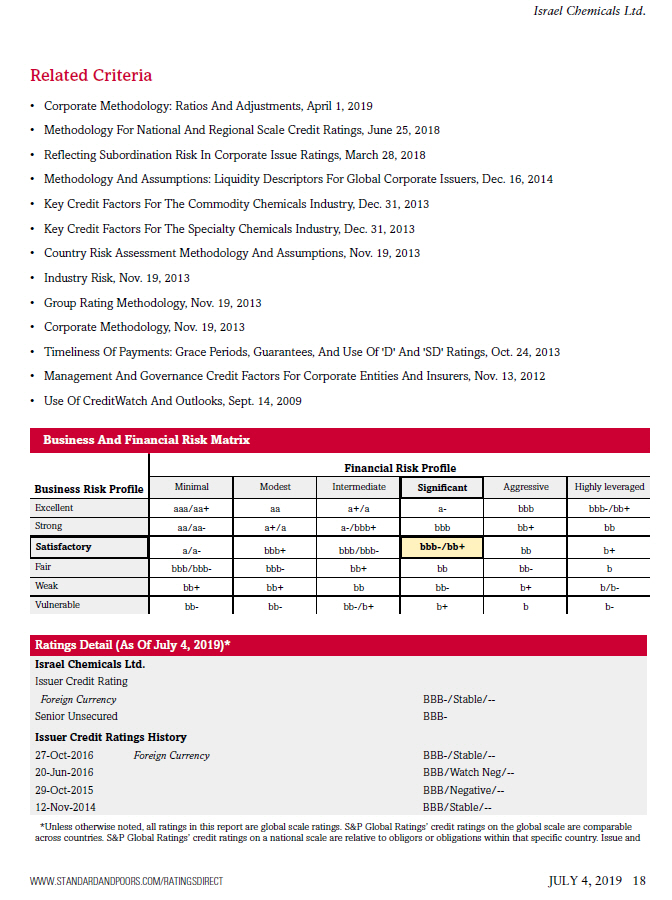

JULY 4, 2019 18 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT Related Criteria • Corporate Methodology: Ratios And Adjustments, April 1, 2019 • Methodology For National And Regional Scale Credit Ratings, June 25, 2018 • Reflecting Subordination Risk In Corporate Issue Ratings, March 28, 2018 • Methodology And Assumptions: Liquidity Descriptors For Global Corporate Issuers, Dec. 16, 2014 • Key Credit Factors For The Commodity Chemicals Industry, Dec. 31, 2013 • Key Credit Factors For The Specialty Chemicals Industry, Dec. 31, 2013 • Country Risk Assessment Methodology And Assumptions, Nov. 19, 2013 • Industry Risk, Nov. 19, 2013 • Group Rating Methodology, Nov. 19, 2013 • Corporate Methodology, Nov. 19, 2013 • Timeliness Of Payments: Grace Periods, Guarantees, And Use Of 'D' And 'SD' Ratings, Oct. 24, 2013 • Management And Governance Credit Factors For Corporate Entities And Insurers, Nov. 13, 2012 • Use Of CreditWatch And Outlooks, Sept. 14, 2009 Business And Financial Risk Matrix Business Risk Profile Financial Risk Profile Minimal Modest Intermediate Significant Aggressive Highly leveraged Excellent aaa/aa+ aa a+/a a - bbb bbb - /bb+ Strong aa/aa - a+/a a - /bbb+ bbb bb+ bb Satisfactory a/a - bbb+ bbb/bbb - bbb - /bb+ bb b+ Fair bbb/bbb - bbb - bb+ bb bb - b Weak bb+ bb+ bb bb - b+ b/b - Vulnerable bb - bb - bb - /b+ b+ b b - Ratings Detail (As Of July 4, 2019)* Israel Chemicals Ltd. Issuer Credit Rating Foreign Currency BBB - /Stable/ -- Senior Unsecured BBB - Issuer Credit Ratings History 27 - Oct - 2016 Foreign Currency BBB - /Stable/ -- 20 - Jun - 2016 BBB/Watch Neg/ -- 29 - Oct - 2015 BBB/Negative/ -- 12 - Nov - 2014 BBB/Stable/ -- *Unless otherwise noted, all ratings in this report are global scale ratings. S&P Global Ratings’ credit ratings on the global scale are comparable across countries. S&P Global Ratings’ credit ratings on a national scale are relative to obligors or obligations within that specific country. Issue and Israel Chemicals Ltd.

JULY 4, 2019 19 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT Ratings Detail (As Of July 4, 2019)*(cont.) debt ratings could include debt guaranteed by another entity, and rated debt that an entity guarantees. Additional Contact: Industrial Ratings Europe; Cor porate_Admin_London@spglobal.com Israel Chemicals Ltd.

JULY 4, 2019 20 WWW.STANDARDANDPOORS.COM/RATINGSDIRECT Copyright © 2019 by Standard & Poor’s Financial Services LLC. All rights reserved. No content (including ratings, credit - related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of Standard & Poor’s Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be used for any unlawful or unauthorized purposes. S&P and any third - party providers, as well as their directors, officers, shareholders, employees or agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content is provided on an “as is” basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT’S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised of the possibility of such damages. Credit - related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact. S&P’s opinions, analyses and rating acknowledgment decisions (described below) are not recommendations to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable, S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives. Rating - related publications may be published for a variety of reasons that are not necessarily dependent on action by rating committees, including, but not limited to, the publication of a periodic update on a credit rating and related analyses. To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain regulatory purposes, S&P reserves the right to assign, withdraw or suspend such acknowledgment at any time and in its sole discretion. S&P Parties disclaim any duty whatsoever arising out of the assignment, withdrawal or suspension of an acknowledgment as well as any liability for any damage alleged to have been suffered on account thereof. S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain non - public information received in connection with each analytical process. S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites, www.standardandpoors.com (free of charge), and www.ratingsdirect.com (subscription), and may be distributed through other means, including via S&P publications and third - party redistributors. Additional information about our ratings fees is available at www.standardandpoors.com/usratingsfees. STANDARD & POOR’S, S&P and RATINGSDIRECT are registered trademarks of Standard & Poor’s Financial Services LLC.

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| Israel Chemicals Ltd. | |||||

| By: | /s/ Kobi Altman | ||||

| Name: | Kobi Altman | ||||

| Title: | Chief Financial Officer | ||||

| Israel Chemicals Ltd. | |||||

| By: | /s/ Aya Landman | ||||

| Name: | Aya Landman | ||||

| Title: | Global Company Secretary | ||||

Date: July 5, 2019