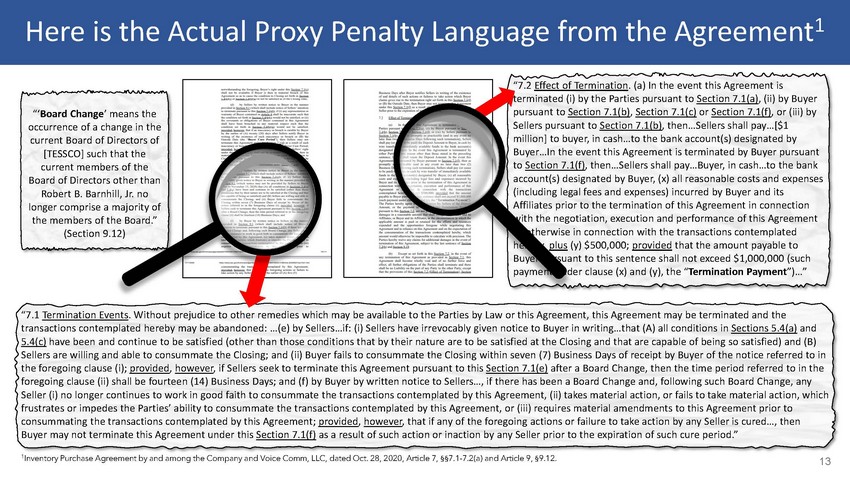

| Disclaimer Important Additional Information Robert B. Barnhill, Jr., Kathleen McLean, Emily Kellum (Kelly) Boss, J. Timothy Bryan, John Diercksen, UA 6-9-2016 Robert B. Barnhill, Jr. Rev Trust, RBB-TRB LLC, a Maryland limited liability company (“RBB-TRB”), RBB-CRB LLC, a Maryland limited liability company (“RBB-CRB”), Robert B Barnhill Jr & Janet W Barnhill Tr FBO Durkin Slattery Barnhill Trust, Janet W Barnhill Tr UA 6 9 2016 Janet W Barnhill Rev Trust, Winston Foundation, Incorporated, a Maryland corporation, and Donald Manley (the “Participants” or “We”) are participants in the solicitation of consents from the TESSCO Technologies Incorporated (NASDAQ: TESS) ("TESSCO" or the "Company") shareholders to remove John D. Beletic, Jay G. Baitler, Paul J. Gaffney, Dennis J. Shaughnessy and Morton F. Zifferer, Jr. and elect Ms. McLean, Ms. Boss, Mr. Bryan and Mr. Diercksen to fill four of the resulting vacancies (as well as to amend the Company's Sixth Amended and Restated By-Laws (the "Bylaws") proposed in connection therewith). We have filed a definitive consent solicitation statement and a WHITE consent card with the Securities and Exchange Commission (the “SEC”) in connection with any such solicitation of proxies from the Company's shareholders. SHAREHOLDERS OF THE COMPANY ARE STRONGLY ENCOURAGED TO READ THE DEFINITIVE CONSENT SOLICITATION STATEMENT, ACCOMPANYING WHITE CONSENT CARD AND ALL OTHER DOCUMENTS FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY AS THEY CONTAIN IMPORTANT INFORMATION. UPDATED INFORMATION REGARDING THE IDENTITY OF POTENTIAL PARTICIPANTS AND THEIR DIRECT OR INDIRECT INTERESTS, BY SECURITY HOLDINGS OR OTHERWISE, IS SET FORTH IN THE DEFINITIVE CONSENT SOLICITATION STATEMENT AND OTHER MATERIALS FILED WITH THE SEC. Shareholders can obtain the definitive consent solicitation statement and any amendments or supplements to the definitive consent solicitation statement filed by the Participants with the SEC at no charge at the SEC’s website at www.sec.gov. Copies will also be available, without charge, on request from the Participants’ proxy solicitor, Harkins Kovler, LLC at +1 (800) 257-3995 or via email at SaveTESSCO@HarkinsKovler.com. Certain Information Regarding the Participants Mr. Barnhill is the founder, former Chairman of the Board and the largest shareholder of the Company. Mr. Barnhill beneficially owns 1,620,387 shares of common stock (approximately 18.5% of the outstanding shares) of the Company ("Common Stock"), which includes 11,503.5 shares that Mr. Barnhill owns directly and the shares owned by the following Participants: UA 6-9-2016 Robert B. Barnhill, Jr. Rev Trust owns 1,265,882 shares of Common Stock, RBB-TRB, LLC owns 109,125 shares of Common Stock, RBB-CRB, LLC owns 109,125 shares of Common Stock, Robert B Barnhill Jr & Janet W Barnhill Tr FBO Durkin Slattery Barnhill Trust, owns 30,750 shares of Common Stock, Janet W Barnhill Tr UA 6 9 2016 Janet W Barnhill Rev Trust owns 67,500 shares of Common Stock, and the Winston Foundation, Incorporated owns 26,500 shares of Common Stock. Mr. Barnhill is the sole manager of RBB-TRB and RBB-CRB, a trustee of the UA 6-9-2016 Robert B. Barnhill, Jr. Rev Trust and the Robert B Barnhill Jr & Janet W Barnhill Tr FBO Durkin Slattery Barnhill Trust and a director of the Winston Foundation, Incorporated. Mr. Barnhill’s spouse is a trustee of the Janet W Barnhill Tr UA 6 9 2016 Janet W Barnhill Rev Trust. The percentage of Mr. Barnhill’s stock ownership is based on the 8,760,562 shares of Common Stock outstanding as of October 13, 2020, as reported in the TESSCO's Consent Revocation Statement on Schedule 14A, filed with the SEC on October 15, 2020. Christopher Barnhill may be considered a Participant in the solicitation but is no longer providing any assistance with respect to the solicitation and does not currently beneficially, directly or indirectly own any securities of the Company. None of the Participants (other than Mr. Barnhill) currently beneficially, directly or indirectly own any securities of the Company. 16 |