UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

☑ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended March 31, 2024

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the period from _____ to _____

333-4028-LA

(Commission file No.)

MINISTRY PARTNERS INVESTMENT COMPANY, LLC

(Exact name of registrant as specified in its charter)

CALIFORNIA |

| 26-3959348 |

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

915 West Imperial Highway, Brea, Suite 120, California, 92821

(Address of principal executive offices)

(714) 671-5720

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ◻.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No ◻

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company filer, or an emerging growth company. See the definitions of “accelerated filer,” “large accelerated filer,” “smaller reporting company,” and “emerging growth company.” in Rule 12b-2 of the Exchange Act. (check one):

| | |

Large accelerated filer ◻ | Accelerated filer ☐ | Non-accelerated filer ◻ |

Smaller reporting company filer ☑ | Emerging growth company ☐ | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ◻

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No þ.

At March 31, 2024, registrant had issued and outstanding 146,522 units of its Class A common units. The information contained in this Form 10-Q should be read in conjunction with the registrant’s Annual Report on Form 10-K for the year ended December 31, 2023.

MINISTRY PARTNERS INVESTMENT COMPANY, LLC

FORM 10-Q

TABLE OF CONTENTS

| | |

| | |

F - 1 | ||

| F - 2 | |

| F - 3 | |

| F - 4 | |

| F - 5 | |

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 3 | |

17 | ||

17 | ||

| | |

| | |

| | |

18 | ||

18 | ||

18 | ||

18 | ||

18 | ||

18 | ||

19 | ||

| | |

| 20 | |

| | |

Exhibit 31.1: | Certification of Chief Executive Officer pursuant to Rule 13a-14(a) or Rule 15(d)-14(a) | |

Exhibit 31.2: | Certification of Principal Accounting Officer pursuant to Rule 13a-14(a) or Rule 15(d)-14(a) | |

Exhibit 32.1: | Certification pursuant to 18 U.S.C. §1350 as adopted pursuant to section 906 of the Sarbanes-Oxley Act of 2002 | |

Exhibit 32.2: | Certification pursuant to 18 U.S.C. §1350 as adopted pursuant to section 906 of the Sarbanes-Oxley Act of 2002 | |

2

Ministry Partners Investment Company, LLC and Subsidiaries

Consolidated Balance Sheets

March 31, 2024 and December 31, 2023

(dollars in thousands except unit data)

| | | | | | |

| | March 31, | | December 31, | ||

|

| 2024 |

| 2023 | ||

| | (Unaudited) | | (Audited) | ||

Assets: | | | | | | |

Cash and cash equivalents | | $ | 11,193 | | $ | 10,854 |

Restricted cash | | | 1,760 | | | 1,757 |

Certificates of deposit | | | 1,251 | | | 1,279 |

Loans receivable, net of allowance for expected credit losses of $1,449 and $1,501 as of March 31, 2024 and December 31, 2023, respectively | | | 99,901 | | | 98,573 |

Accrued interest receivable | | | 464 | | | 432 |

Investment in joint venture | | | 870 | | | 871 |

Other investments | | | 1,053 | | | 1,052 |

Property and equipment, net | | | 95 | | | 56 |

Foreclosed assets, net | | | 301 | | | 301 |

Servicing assets | | | 88 | | | 98 |

Other assets | | | 971 | | | 1,374 |

Total assets | | $ | 117,947 | | $ | 116,647 |

Liabilities and members’ equity | | | | | | |

Liabilities: | | | | | | |

Lines of credit | | $ | 7,500 | | $ | 4,500 |

Other secured borrowings | | | 7 | | | 7 |

Debt certificates payable, net of debt issuance costs of $130 and $52 as of March 31, 2024 and December 31, 2023, respectively | | | 95,590 | | | 96,979 |

Accrued interest payable | | | 361 | | | 383 |

Other liabilities | | | 1,896 | | | 1,683 |

Total liabilities | | | 105,354 | | | 103,552 |

Members' Equity: | | | | | | |

Series A preferred units, 1,000,000 units authorized, 117,100 units issued and outstanding at March 31, 2024 and December 31, 2023 (liquidation preference of $100 per unit); See Note 13 | | | 11,715 | | | 11,715 |

Class A common units, 1,000,000 units authorized, 146,522 units issued and outstanding at March 31, 2024 and December 31, 2023; See Note 13 | | | 1,509 | | | 1,509 |

Net assets of Ministry Partners for Christ, with donor restrictions | | | 1,700 | | | — |

Accumulated deficit | | | (2,331) | | | (129) |

Total members' equity | | | 12,593 | | | 13,095 |

Total liabilities and members' equity | | $ | 117,947 | | $ | 116,647 |

The accompanying notes are an integral part of these consolidated financial statements.

F-2

Ministry Partners Investment Company, LLC and Subsidiaries

Consolidated Statements of Operations (Unaudited)

For the three months ended March 31, 2024 and 2023

(dollars in thousands)

| | | | | | |

| | Three months ended | ||||

| | March 31, | ||||

|

| 2024 |

| 2023 | ||

Interest income: | | | | | | |

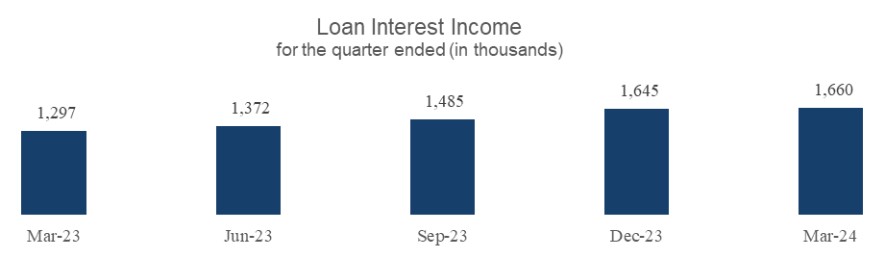

Interest on loans | | $ | 1,660 | | $ | 1,297 |

Interest on interest-bearing accounts | | | 151 | | | 88 |

Total interest income | | | 1,811 | | | 1,385 |

Interest expense: | | | | | | |

Debt certificates | | | 1,182 | | | 860 |

Other debt | | | 83 | | | 58 |

Total interest expense | | | 1,265 | | | 918 |

Net interest income | | | 546 | | | 467 |

Credit for expected credit losses | | | (52) | | | (162) |

Net interest income after credit for expected credit losses | | | 598 | | | 629 |

Non-interest income: | | | | | | |

Broker-dealer commissions and fees | | | 175 | | | 215 |

Other income | | | 36 | | | 63 |

Charitable contributions, with donor restrictions | | | — | | | 400 |

Total non-interest income | | | 211 | | | 678 |

Non-interest expenses: | | | | | | |

Salaries and benefits | | | 527 | | | 762 |

Marketing and promotion | | | 21 | | | 27 |

Office occupancy | | | 47 | | | 47 |

Office operations and other expenses | | | 393 | | | 412 |

Foreclosed assets, net | | | 10 | | | 4 |

Legal and accounting | | | 155 | | | 118 |

Total non-interest expenses | | | 1,153 | | | 1,370 |

Loss before provision for income taxes | | | (344) | | | (63) |

Provision for income taxes and state LLC fees | | | 5 | | | 5 |

Net loss | | $ | (349) | | $ | (68) |

The accompanying notes are an integral part of these consolidated financial statements.

F-3

Ministry Partners Investment Company, LLC and Subsidiaries

Consolidated Statements of Cash Flows (Unaudited)

For the three months ended March 31, 2024 and 2023

| | | | | | |

| | Three months ended | ||||

| | March 31, | ||||

|

| 2024 |

| 2023 | ||

CASH FLOWS FROM OPERATING ACTIVITIES: | | | | | | |

Net loss | | $ | (349) | | $ | (68) |

Adjustments to reconcile net loss to net cash provided (used) by operating activities: | | | | | | |

Depreciation | | | 17 | | | 11 |

Amortization of deferred loan fees | | | (23) | | | (14) |

Amortization of debt issuance costs | | | 17 | | | 20 |

Credit for expected credit losses | | | (52) | | | (162) |

Accretion of loan discount | | | (3) | | | (3) |

Gain on sale of loans | | | — | | | (7) |

Loss on retirement of fixed assets | | | 2 | | | — |

Gain on other investments | | | (1) | | | (1) |

Adoption of new accounting standard | | | — | | | (112) |

Changes in: | | | | | | |

Accrued interest receivable | | | (32) | | | 93 |

Other assets | | | 415 | | | (119) |

Accrued interest payable | | | (21) | | | 33 |

Other liabilities | | | 207 | | | (331) |

Net cash provided (used) by operating activities | | | 177 | | | (660) |

CASH FLOWS FROM INVESTING ACTIVITIES: | | | | | | |

Loan purchases | | | (10) | | | (2,545) |

Loan originations | | | (3,126) | | | (25) |

Loan sales | | | — | | | 7 |

Loan principal collections | | | 1,886 | | | 2,014 |

Purchase of certificates of deposit | | | 27 | | | — |

Purchase of property and equipment | | | (58) | | | — |

Net cash (used) by investing activities | | | (1,281) | | | (549) |

CASH FLOWS FROM FINANCING ACTIVITIES: | | | | | | |

Borrowings, net of repayments on lines of credit | | | 3,000 | | | — |

Net change in debt certificates payable | | | (1,311) | | | 8,966 |

Debt issuance costs | | | (95) | | | (24) |

Dividends paid on preferred units | | | (148) | | | (182) |

Net cash provided by financing activities | | | 1,446 | | | 8,760 |

Net increase in cash and restricted cash | | | 342 | | | 7,551 |

Cash, cash equivalents, and restricted cash at beginning of period | | | 12,611 | | | 9,564 |

Cash, cash equivalents, and restricted cash at end of period | | $ | 12,953 | | $ | 17,115 |

Supplemental disclosures of cash flow information | | | | | | |

Interest paid | | $ | 1,286 | | $ | 885 |

Income taxes paid | | | 12 | | | — |

Supplemental disclosures of non-cash transactions | | | | | | |

Servicing assets recorded | | | — | | | 9 |

Leased assets obtained in exchange of new operating lease liabilities | | | 387 | | | — |

Lease liabilities recorded | | | 387 | | | — |

Dividends declared to preferred unit holders | | | 153 | | | 160 |

The accompanying notes are an integral part of these consolidated financial statements.

F-4

MINISTRY PARTNERS INVESTMENT COMPANY, LLC

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

The accounting and financial reporting policies of MINISTRY PARTNERS INVESTMENT COMPANY, LLC and its wholly owned subsidiaries, Ministry Partners Funding, LLC, MP Realty Services, Inc., Ministry Partners Securities, LLC, and Ministry Partners for Christ, Inc. conform to accounting principles generally accepted in the United States and general financial industry practices. The accompanying interim consolidated financial statements have not been audited. The Company’s 2023 annual report filed on Form 10-K provides a more detailed description of its accounting policies. In the opinion of management, all adjustments (which include only normal recurring adjustments) necessary to present fairly the financial position, results of operations, and cash flows as of March 31, 2024, and for the three months ended March 31, 2024 and 2023, have been made.

Certain information and note disclosures normally included in financial statements prepared in accordance with generally accepted accounting principles have been condensed or omitted. The results of operations for the periods ended March 31, 2024 and 2023 are not necessarily indicative of the results for the full year.

Note 1: Nature of Business and Summary of Significant Accounting Policies

Nature of Business

Throughout these notes to consolidated financial statements, we refer to Ministry Partners Investment Company, LLC and its subsidiaries as “the Company.” Formed in California in 1991, the Company is a financial services organization specializing in both financing ministries through funding commercial real property secured loans and providing investment services to the Christian community. The Company funds its investments in ministry loans primarily through the sale of debt certificates.

The Company’s wholly-owned subsidiaries are:

| ● | Ministry Partners Funding, LLC, a Delaware limited liability company (“MPF”); |

| ● | MP Realty Services, Inc., a California corporation (“MP Realty”); |

| ● | Ministry Partners Securities, LLC, a Delaware limited liability company (“MP Securities”); and |

F-5

| ● | Ministry Partners for Christ, Inc., a not-for-profit Delaware corporation (“MPC”). |

The Company formed MPF in 2007 and then deactivated the subsidiary on November 30, 2009. In December 2014, the Company reactivated MPF to enable it to serve as collateral agent for loans held as collateral for its Secured Investment Certificates.

The Company formed MP Realty in November 2009, and obtained a license to operate as a corporate real estate broker through the California Department of Real Estate on February 23, 2010. MP Realty has conducted limited operations to date.

The Company formed MP Securities on April 26, 2010, to provide investment and financial planning solutions for individuals, churches, charitable institutions, and faith-based organizations. MP Securities acts as the selling agent for the Company’s public and private placement notes.

The Company formed MPC on December 28, 2018, to be used exclusively for religious and charitable purposes within the meaning of Section 501(c)(3) of the U.S. Internal Revenue Code of 1986 (“IRC”). MPC is a not-for-profit corporation formed and organized under Delaware law. MPC makes charitable grants to Christian educational organizations, and provides accounting, consulting, and financial expertise to aid Christian ministries. On August 23, 2019, the Internal Revenue Service granted MPC tax-exempt status as a private foundation under Section 501(c)(3) of the IRC. The MPC Board of Directors approved its first charitable grants during the year ended December 31, 2020.

Principles of Consolidation

The consolidated financial statements include the accounts of Ministry Partners Investment Company, LLC and its wholly-owned subsidiaries. Management eliminates all significant inter-company balances and transactions in consolidation.

Conversion to LLC

Effective December 31, 2008, the Company converted from a corporation organized under California law to a California limited liability company. After this conversation, the separate existence of Ministry Partners Investment Corporation ceased and the entity continued by operation of law under the name Ministry Partners Investment Company, LLC. As an LLC, a group of managers provides oversight of the Company’s affairs. The managers have full, exclusive, and complete discretion, power, and authority to oversee the management of Company affairs. An Operating Agreement governs the Company’s management structure and governance procedures.

F-6

Risks and Uncertainties

COVID-19, a global pandemic, adversely impacted the broad economy, affecting most industries, including businesses, schools, hospitality-, and travel-based employers, and disrupted the supply and distribution networks that deliver products to the consuming public. While the pandemic has ended, we cannot know at this time if there will be any negative long-term effects to in-person attendance and giving trends at faith-based organizations and churches. Negative attendance and giving trends impacting the organizations that the Company serves could have a material financial impact on the Company.

In addition, Russia’s invasion of Ukraine, increasing current levels of inflation, the disruption of global supply chains, rising interest rates, and recent bank failures are putting strain on the U.S. economy and the U.S. consumer. While it is not possible to know the full extent of the long-term impact of these current events, the Company is disclosing potentially material factors that could impact our business of which it is aware.

Cash, and Cash Equivalents

Cash equivalents include time deposits, and all highly liquid debt instruments with original maturities of three months or less. The Company had demand deposits and money market deposit accounts as of March 31, 2024 and December 31, 2023.

The National Credit Union Share Insurance Fund insures a portion of the Company’s cash held at credit unions, and the Federal Deposit Insurance Corporation insures a portion of cash held by the Company at other financial institutions. The Company holds cash deposits that may exceed insured limits. Management does not expect to incur losses in these cash accounts.

The Company maintains cash accounts with Royal Bank of Canada Dain Rauscher (“RBC Dain”) as part of its clearing agreement for its securities-related activities, and with the Central Registration Depository (“CRD”) for regulatory purposes in connections with its investment advisory and securities-related business. The Company also maintains cash in an account with America’s Christian Credit Union (“ACCU”) as collateral for its secured borrowings. The Company classifies these accounts as restricted cash on its balance sheet.

Certificates of Deposit

Certificates of deposit include investments in certificates of deposit held at financial institutions that carry original maturities of greater than three months. The Company had

F-7

$1.3 million in certificates with terms of greater than three months as of March 31, 2024, and December 31, 2023.

Use of Estimates

The Company’s creation of consolidated financial statements that conform to United States Generally Accepted Accounting Principles ("GAAP") requires management to make estimates and assumptions. These estimates and assumptions affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. These estimates govern areas such as the allowance for credit losses and the fair value of financial instruments and foreclosed assets. Actual results could differ from these estimates.

Investments in Joint Venture

In 2016, the Company entered into a joint venture agreement to develop and sell property we acquired as part of a Deed in Lieu of Foreclosure agreement reached with one of our borrowers. The joint venture owns a property located in Santa Clarita, California.

The Company accounts for its investment in the joint venture using the equity method of accounting. Under this method, the Company records its proportionate share of the joint venture’s net income or loss in the statement of operations.

On a periodic basis, or whenever events or circumstances arise that would necessitate analysis, management analyzes the Company’s investment in the joint venture for impairment. In this analysis, management compares the carrying value of the investment to the estimated value of the underlying real property. The Company records any impairment charges as a valuation allowance against the value of the asset. Management records these valuation changes as realized gains or losses on investment on the Company’s consolidated statements of operations. Management determined that investment in the joint venture was not impaired as of March 31, 2024.

Other Investments

In June 2022, MP Securities purchased two ten-year fixed annuities from insurance companies. These annuities each carry unique features, including guaranteed fixed income components, variable income components, premium bonuses, and potential withdrawal charges. The Company carries these investments at cost and adjusts for guaranteed income when such income is realized. The principal balances of these annuities are guaranteed but are not insured; however, management determined that the annuities were not impaired as of March 31, 2024, and December 31, 2023, and does not anticipate losses.

F-8

Loans Receivable

The Company reports loans that management has the intent and ability to hold for the foreseeable future at their outstanding unpaid principal balance adjusted for an allowance for expected credit losses, deferred loan fees and costs, and loan discounts.

Interest Accrual on Loans Receivable

The Company accrues loan interest income daily. Management defers loan origination fees and costs generated in making a loan. The Company amortizes these fees and costs as an adjustment to the related loan yield using the interest method.

Loan discounts can arise from interest accrued and unpaid which the Company adds to loan principal balances when it modifies the loan. The Company does not accrete discounts to income on impaired loans. However, when management determines that a previously impaired loan is no longer impaired, the Company begins accreting loan discounts to interest income over the term of the modified loan. For loans purchased from third parties, loan discounts include differences between the purchase price and the recorded principal balance of the loan. The Company accretes these discounts to interest income over the term of the loan using the interest method.

Management considers a loan impaired if it concludes that the collection of principal or interest according to the terms of the loan agreement is doubtful. The Company stops the accrual of interest when management determines the loan is impaired.

For loans that the Company places on non-accrual status, management reverses all uncollected accrued interest against interest income. Management accounts for the interest on these loans on the cash basis or cost-recovery method until the loan qualifies for return to accrual status. It is not until all the principal and interest amounts contractually due are brought current and future payments are reasonably assured that the Company returns a loan to accrual status.

Allowance for Expected Credit Losses

The Company sets aside an allowance for expected credit losses by charging the provision for expected credit losses account on the Company’s consolidated statements of operations. This charge decreases the Company’s earnings. Management charges off the part of loan balances it believes it will not collect against the allowance. The Company credits subsequent recoveries, if any, to the allowance.

F-9

Loan Portfolio Segments and Classes

Management separates the loan portfolio into portfolio segments for purposes of evaluating the allowance for expected credit losses. A portfolio segment is defined as the level at which the Company develops and documents a systematic method for determining its allowance for expected credit losses. The Company segments the loan portfolio based on loan types and the underlying risk factors present in each loan type. Management periodically reviews and revises such risk factors, as it considers appropriate. The Company’s loan portfolio comprises two segments: ministry-related non-profit loans and commercial loans. The risk characteristics of the Company’s portfolio segments are as follows:

Non-profit Commercial Loans: The Company underwrites its non-profit loans based on the cash flows and other key financial performance indicators of the borrower, as well as the value of the collateral securing the loan. Unlike for-profit commercial borrowers, the cash flows generated by these borrowers often depend on contributions rather than cash flows generated by the operation of a business. In addition, collateral values can fluctuate as many church properties have limited commercial use outside of the ministry sector.

For-profit Commercial Loans: The Company underwrites for-profit loans commercial based on the cash flows and other key financial performance indicators of the borrower, as well as the value of the collateral securing the loan. Repayment of these loans is generally dependent on the success of the business operated on the property being used to secure the loan.

The Company has also segregated its portfolio into the following classes, which are a subsets of segments:

F-10

Management has segregated the loan portfolio into the following portfolio classes: | | |

Loan Class |

| Class Description |

Wholly Owned First Collateral Position, Amortizing | | Wholly owned loans and the retained portion of loans originated by the Company and sold for which the Company possesses a senior lien on the collateral underlying the loan. This class contains only those loans that amortize based on an agreed upon contractual principal and interest payments. |

Wholly Owned Other Collateral Position, Amortizing | | Wholly owned loans and the retained portion of loans originated by the Company and sold for which the Company possesses a lien on the underlying collateral that is superseded by another lien on the same collateral or that is secured by collateral other than real property. This class contains only those loans that amortize based on an agreed upon contractual principal and interest payments. These loans present higher credit risk than loans for which the Company possesses a senior lien due to the increased risk of loss should the loan default. |

Wholly Owned Unsecured, Amortizing | | Wholly owned loans and the retained portion of loans originated by the Company and sold for which the Company does not possess an interest in collateral securing the loan. This class contains only those loans that amortize based on an agreed upon contractual principal and interest payments. These loans present higher credit risk than loans for which the Company possesses a lien due to the increased risk of loss should the loan default. |

Wholly Owned Other Collateral Position, Lines of Credit | | Wholly owned loans and the retained portion of loans originated by the Company and sold for which the Company possesses a lien on the underlying collateral that is superseded by another lien on the same collateral or that is secured by collateral other than real property. This class contains only line of credit agreements. |

Wholly Owned Unsecured, Lines of Credit | | Wholly owned loans and the retained portion of loans originated by the Company and sold for which the Company does not possess an interest in collateral securing the loan. This class contains only line of credit agreements. |

Wholly Owned, Construction | | Wholly owned loans and the retained portion of loans originated by the Company and sold which have been made for the purpose of constructing real property to be used for the borrower’s ministry. These loans present different risks due to the nature of construction projects and the underlying collateral. |

Participations First Collateral Position | | Participated loans purchased from another financial entity for which the Company possesses a senior lien on the collateral underlying the loan. Loan participations purchased may present higher credit risk than wholly owned loans because disposition and direction of actions regarding the management and collection of the loans must be coordinated and negotiated with the other participants, whose best interests regarding the loan may not align with those of the Company. |

Participations Construction | | Loan participations purchased in loans made for the purpose of constructing commercial real property and where the collateral securing the property comprises the construction project. These loans present different risks due to the nature of construction projects and the underlying collateral. |

Finally, the Company segregates each class by risk rating, as loans determined to have lower credit quality present different and greater risk than those of higher credit quality.

F-11

The Company’s credit quality grading system is described in detail below in the section titled “Credit Quality Indicators.”

Allowance for Expected Credit Loss Evaluation

The Company adopted FASB Accounting Standards Update (ASU) No. 2016-13, Financial Instruments - Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments ("CECL") on January 1, 2023. CECL replaces the previous methodology for measuring credit losses, which involved estimated allowances for current known and inherent losses within the portfolio. The CECL methodology requires the Company to implement an expected loss model for measuring credit losses, which encompasses allowances for losses expected to be incurred over the life of the borrowings in its portfolio. The allowance for expected credit loss model used under CECL requires the measurement of all expected credit losses for financial assets at amortized cost, as well as certain off-balance sheet credit exposures based on historical experiences, current conditions, and reasonable and supportable forecasts.

In accordance with FASB Accounting Standards Update (ASU) No. 2019-04, Codification Improvements to Topic 326, Financial Instruments-Credit Losses, Topic 815, Derivatives and Hedging, and Topic 825, Financial Instruments, the Company has made the accounting policy election not to measure an allowance for credit losses on accrued interest receivable amounts. This is allowable if the Company writes off uncollectible accrued interest receivable when a loan is 90 days past due or interest is otherwise considered uncollectible, which is its current policy and practice. The Company has also elected to continue to present accrued interest on its loans receivable separately on its consolidated balance sheet.

CECL Model

The CECL methodology does not prescribe any specific model for determining expected losses. Management has determined that, due to the nature of the borrowings in its portfolio and the nature of the collateral securing a significant portion of its borrowings, it would use a “probability of default” calculation as the basis for estimating expected losses. This methodology uses information about the borrower, the loan, and the collateral securing the loan to determine a borrower’s ability to meet the contractual requirements of the loan agreement. It then applies a calculated probability that the borrower will default to the estimated amount of loss the Company would incur in a default scenario. To perform this calculation, the methodology requires management to collect and analyze certain data for the loans in its portfolio including:

F-12

| ● | the value of collateral securing the loan, as supported by third-party appraisals or other valuations; |

| ● | adjustments to the collateral value related to geographical and economic trends, and estimated costs to sell; and |

| ● | the borrower’s ability to meet its contractual obligations as determined by financial information collected regularly from borrowers. |

All loans that the Company does not individually review use the probability of default calculation described above. In addition, management has determined that there are qualitative factors affecting expected credit losses for which the probability of default model cannot account. These qualitative factors represent significant issues that management considers likely to cause estimated credit losses associated with the Company’s existing portfolio to differ from the probability of default calculation. These factors are applied in varying degrees depending on a loan’s segment, class, and credit quality. Management adjusts these factors on an on-going basis, some of which include:

| ● | changes in national, regional, and local economic and industry conditions that affect the collectability of the portfolio; |

| ● | changes in the volume and severity of past due loans, the volume of non-accrual loans, and the volume and severity of adversely classified loans; |

| ● | changes in the value of collateral, including the limitations of using commercial price indices to adjust collateral value; |

| ● | the inherent risk in borrowings with high loan-to-value figures; and |

| ● | broad trends in the Christian church industry in which the Company primarily lends. |

Loans that management has classified as non-performing and impaired receive a specific reserve. For such loans, an allowance is established when the carrying value of that loan is higher than the amount management expects to collect. Management uses multiple approaches to determine the amount the Company expects to collect. These include the discounted cash flow method, using the loan’s underlying collateral value reduced by expected selling costs, or using the observable market price of the impaired loan.

F-13

Individually Reviewed

The Company reviews its loan portfolio monthly by examining several data points. This process includes reviewing delinquency reports, any new information related to the financial condition of its borrowers, and any new appraisal or other collateral valuation. Throughout this process, the Company identifies potential impaired loans. Management generally deems a loan is impaired when current facts and circumstances indicate that it is probable a borrower will be unable to make payments according to the loan agreement. If management has not already deemed a loan impaired, it will classify the loan as non-accrual when it becomes 90 days or more past due. All loans in the loan portfolio are subject to impairment analysis. The Company monitors impaired loans on an ongoing basis as part of management’s loan review and work out process.

Any loans that management has determined are non-performing and impaired are individually analyzed for potential losses. These loans include non-accrual loans, loans 90 days or more past due and still accruing, non-performing modified loans, and loans where the borrowers have defaulted on contractual terms of their loan agreement.

| ● | Non-accrual loans are loans on which management has discontinued interest accruals. |

| ● | Modified loans are loans in which the Company has granted the borrower a concession due to financial distress. Concessions are usually a reduction of the interest rate or a change in the original repayment terms. |

| ● | Loans that have defaulted on other contractual terms could include loans where the borrower has failed to provide required financial information, has violated a covenant, or has otherwise failed to comply with the terms of the loan agreement. |

Management considers several factors when determining impairment status. These factors include the loan’s payment status, the value of any secured collateral, and the probability of collecting scheduled payments when due. Management generally does not classify loans that experience minor payment delays or shortfalls as impaired. Management determines the significance of payment delays or shortfalls on a case-by-case basis, taking into consideration all the circumstances surrounding the loan and the borrower. These circumstances include the length and reasons for the delay, the borrower’s payment history, and the amount of the shortfall in relation to the principal and interest owed.

Management measures impairment on a loan-by-loan basis using one of three methods:

F-14

| ● | the present value of expected future cash flows discounted at the loan’s effective interest rate; |

| ● | the obtainable market price; or |

| ● | the fair value of the collateral if the loan is collateral-dependent. |

Loan Modifications

A loan modification is a loan for which the Company, for reasons related to a borrower’s financial difficulties, grants a concession to a borrower that the Company would not otherwise consider. A modification of a loan usually involves an interest rate reduction, extension of the maturity date, payment reduction, or reduction of accrued interest owed on the loan on a contingent or absolute basis.

Management considers loans that it renews at below-market terms to be loan modifications if the below-market terms represent a concession due to the borrower’s troubled financial condition. The Company classifies loan modifications as impaired loans. For the loans that are not considered to be collateral-dependent, management measures loan modifications at the present value of estimated future cash flows using the loan’s effective rate prior to the loan’s initial modification. The Company reports the change in the present value of cash flows related to the passage of time as interest income. If management considers the loan to be collateral-dependent, impairment is measured based on the fair value of the collateral.

In accordance with industry standards, the Company classifies a loan as impaired if management has modified it as part of a loan modification. However, loan modifications, upon meeting certain performance conditions, are eligible to receive non-classified loan ratings (pass or watch) and to be moved out of non-accrual status. These loans continue to be classified as impaired loans but not necessarily as non-accrual or collateral-dependent loans. Modified loans can be included in the collectively reviewed pool of loans if they return to performing status.

Loan Charge-offs

Management charges off loans or portions thereof when it determines the loans or portions of the loans are uncollectible. The Company evaluates collectability periodically on all loans classified as “Loans of Lesser Quality.” Key factors management uses in assessing a loan’s collectability are the financial condition of the borrower, the value of any secured collateral, and the terms of any workout agreement between the Company and the borrower. In workout situations, the Company charges off the amount deemed

F-15

uncollectible due to the terms of the workout, the inability of the borrower to make agreed upon payments, and the value of the collateral securing the loan.

Credit Quality Indicators

The Company has established a loan grading system to assist its management in analyzing and monitoring the loan portfolio. The Company classifies loans it considers lesser quality (“classified loans”) as watch, special mention, substandard, doubtful, or loss assets. The loan grading system is as follows:

Pass:

The borrower has sufficient cash to fund debt services. The borrower may be able to obtain similar financing from other lenders with comparable terms. The risk of default is considered low.

Watch:

These loans exhibit potential or developing weaknesses that deserve extra attention from credit management personnel. If the developing weakness is not corrected or mitigated, there may be deterioration in the ability of the borrower to repay the debt in the future. Management must report loans graded Watch to executive management and the Board of Managers (“Board”). The potential for loss under adverse circumstances is elevated, but not foreseeable. Watch loans are considered pass loans.

Special mention:

These credit facilities exhibit potential or actual weaknesses that present a higher potential for loss under adverse circumstances and deserve management’s close attention. If uncorrected, these weaknesses may result in deterioration of the repayment prospects for the loan at some future date.

Substandard:

Management considers loans and other credit extensions bearing this grade to be inadequately protected by the current net worth and debt service capacity of the borrower or of any pledged collateral. These obligations, even if apparently protected by collateral value, have well-defined weaknesses related to adverse financial, managerial, economic, ministry, or environmental conditions which have clearly jeopardized repayment of principal and interest as originally intended. Furthermore, there is the possibility that some future loss will be sustained if such weaknesses are not corrected.

F-16

Doubtful:

This classification consists of loans that display the properties of substandard loans with the added characteristic that the severity of the weaknesses makes collection or liquidation in full highly questionable or improbable based upon currently existing facts, conditions, and values. The probability of some loss is very high, but because of certain important and reasonably specific factors, the amount of loss cannot be exactly determined. Such pending factors could include a merger or liquidation, additional capital injection, refinancing plans, or perfection of liens on additional collateral.

Loss:

Loans in this classification are considered uncollectible and cannot be justified as a viable asset. This classification does not mean the loan has absolutely no recovery value, but that it is neither practical nor desirable to defer writing off this loan even though partial recovery may be obtained in the future.

Revenue Recognition

The Company recognizes two primary types of revenue: interest income and non-interest income.

Interest Income

The Company’s principal source of revenue is interest income from loans, which is not within the scope of ASU 2014-09, Revenue from Contracts with Customers and all subsequent amendments to the ASU (collectively, "ASC 606"). Refer to the discussion in “Loans Receivable” above to understand the Company’s recognition of interest income.

Non-interest Income

Non-interest income includes revenue from various types of transactions and services provided to customers. Contracts with customers can include multiple services, which are accounted for as separate “performance obligations” if they are determined to be distinct. Our performance obligations to our customers are generally satisfied when we transfer the promised good or service to our customer, either at a point in time or over time. Revenue from a performance obligation transferred at a point in time is recognized at the time that the customer obtains control over the promised good or service. Revenue from our performance obligations satisfied over time are recognized in a manner that depicts our performance in transferring control of the good or service, which is generally measured based on time elapsed, as our customers simultaneously receive and consume the benefit of our services as they are provided.

F-17

Payment for the majority of our services is variable consideration, as the amount of revenues we expect to receive is subject to factors outside of our control, including market conditions. Variable consideration is only included in revenue when amounts are not subject to significant reversal, which is generally when uncertainty around the amount of revenue to be received is resolved.

Wealth advisory fees

Generally, management recognizes wealth advisory fees over time as the Company renders services to its clients. The Company receives these fees either based on a percentage of the market value of the assets under management, or as a fixed fee based on the services the Company provides to the client. The Company’s delivery of these services represents its related performance obligations. The Company typically collects the wealth advisory fees at the beginning of each quarter from the client’s account. Management recognizes these fees ratably over the related billing period as the Company fulfills its performance obligation. In addition, management recognizes any commissions or referral fees paid related to this revenue ratably over the related billing period as the Company fulfills its performance obligation.

Investment brokerage fees

Investment brokerage fees arise from the selling, distribution, and trade execution services. The Company’s execution of these services fulfills its related performance obligations.

The Company also offers sales and distribution services and earns commissions through the sale of annuity and mutual fund products. The Company acts as an agent in these transactions and recognizes revenue at a point in time when the customer executes a contract with a product carrier. The Company may also receive trailing commissions and 12b-1 fees related to mutual fund and annuity products. Management recognizes this revenue in the period when it is earned, estimating the revenue, if necessary, based on the balance of the investment and the commission rate on the product.

The Company earns and recognizes trade execution commissions on the trade date, which is when the Company fulfills its performance obligation. Payment for the trade execution is due on the settlement date.

Lending Fees

Lending fees represent charges earned for services we provide as part of the lending process, such as late charges, servicing fees, and documentation fees. The Company

F-18

recognizes late charges as earned when they are paid. The Company recognizes revenue on other lending fees in the period in which the Company has performed the service.

Gains on sales of loans receivable

From time to time, the Company sells participation interests in loans receivable that it services. Upon completion of the loan sale, the Company recognizes a gain based on certain factors including the maturity date of the loan, the percentage of the loan sold and retained, and the servicing rate charged to the participant on the sold portion.

Charitable contributions

Charitable contributions include amounts that were donated by a not-for-profit charitable ministry to the Company’s not-for-profit subsidiary, MPC. This revenue comprises donations analyzed by management and determined to be unconditional, non-exchange transactions. Contributions are measured at their fair value at the date of contribution. All contributions are considered to be available for unrestricted use unless specifically restricted by the donor. Amounts received that are designated for future periods or restricted by the donor for specific purposes are reported as carrying donor restrictions. The $1.7 million in charitable contributions recognized during 2023, were permanently restricted by the donor as part of a designated fund agreement that allows for limited annual distributions. These funds are included in the restricted net assets of MPC and are presented on the balance sheet as part of retained earnings.

Gains/losses on sales of foreclosed assets

The Company records a gain or loss from the sale of foreclosed assets when control of the property transfers to the buyer, which generally occurs at the time of an executed deed. When the Company finances the sale of a foreclosed asset to the buyer, the Company assesses whether the buyer is committed to perform their obligation under the contract and whether collectability of the transaction price is probable, among other factors. Once these criteria are met, the foreclosed asset is derecognized and the gain or loss on sale is recorded upon the transfer of control of the property to the buyer. In determining the gain or loss on the sale, the Company adjusts the transaction price and related gain (loss) on sale if a significant financing component is present.

Other non-interest income

Other non-interest income includes fees earned based on service contracts the Company has entered into with credit unions. The Company recognizes the revenue monthly based on the terms of the contracts, which require monthly payments for services the Company

F-19

performs. Other non-interest income also includes realized income and gains on other investments.

Foreclosed Assets

Management records assets acquired through foreclosure or other proceedings at fair market value less estimated costs of disposal. Management determines the fair value at the date of foreclosure, which establishes a new cost for the asset. After foreclosure, the Company carries the asset at the lower of cost or fair value, less estimated costs of disposal. Management evaluates these real estate assets regularly to ensure that the asset’s fair value supports the recorded amount. If necessary, management also ensures that valuation allowances reduce the carrying amount to fair value less estimated costs of disposal. Revenue and expense from the operation of the Company’s foreclosed assets and changes in the valuation allowance are included in net expenses from foreclosed assets. When the Company sells the foreclosed property, it recognizes a gain or loss on the sale equal to the difference between the net sales proceeds received and the carrying amount of the property.

Transfers of Financial Assets

Management accounts for transfers of financial assets as sales when the Company has surrendered control over the asset. Management deems the Company has surrendered control over transferred assets when:

| ● | the assets have been isolated from the Company; |

| ● | the transferee obtains the right (free of conditions that constrain it from taking advantage of that right) to pledge or exchange the transferred asset; and |

| ● | the Company does not maintain effective control over the transferred asset through an agreement to repurchase it before its maturity. |

The Company, from time to time, sells participation interests in mortgage loans it has originated or acquired. To recognize the transfer of a portion of a financial asset as a sale, the transferred portion, and any portion that the transferor continues to hold must represent a participating interest. In addition, the transfer of the participating interest must meet the conditions for surrender of control. To qualify as a participating interest:

| ● | each portion of a financial asset must represent a proportionate ownership interest in an entire financial asset; |

F-20

| ● | from the date of transfer, all cash flows received from the entire financial asset must be divided proportionately among the participating interest holders in an amount equal to their respective share of ownership; |

| ● | the transfer must be made on a non-recourse basis (other than standard representations and warranties made under the loan participation sale agreement); |

| ● | the transfer may not be subordinate to any other participating interest holder; and |

| ● | no party has the right to pledge or exchange the entire financial asset. |

If the transaction does not meet either the participating interest or surrender of control criteria, management accounts for it as a secured borrowing arrangement.

Under some circumstances, when the Company sells a participation in a wholly owned loan receivable that it services, it retains loan-servicing rights, and records a servicing asset that is initially measured at fair value. As quoted market prices are generally not available for these assets, the Company estimates fair value based on the present value of future expected cash flows associated with the loan receivable. The Company amortizes servicing assets over the life of the associated receivable using the interest method. Any gain or loss recognized on the sale of a loan receivable depends in part on both the previous carrying amount of the financial asset involved in the sale, allocated between the asset sold and the interest that continues to be held by the Company based on its relative fair value at the date of transfer, and the proceeds received.

Property and Equipment

The Company states its furniture, fixtures, equipment, and leasehold improvements at cost, less accumulated depreciation and amortization. Management computes depreciation on a straight-line basis over the estimated useful lives of the assets. The useful lives of the Company’s assets range from three to seven years.

Debt Issuance Costs

The Company’s debt consists of borrowings from financial institutions and obligations to investors incurred through the sale of debt certificates. Management presents debt net of debt issuance costs and amortizes debt issuance costs into interest expense over the contractual terms of the debt using the straight-line method.

F-21

Employee Benefit Plans

The Company records contributions to the qualified employee retirement plan as compensation cost in the period incurred. The Company has also entered into a Supplemental Executive Retirement Plan (the “SERP”) with its former President and Chief Executive Officer, Joseph W. Turner, Jr. As the benefits of the plan have fully vested as of December 31, 2023, the Company has already recorded all expenses related to the SERP and no future expenses will be recorded.

Leases

We recognize right-of-use (“ROU”) assets and lease liabilities on the balance sheet for leases with lease terms longer than 12 months. The recognition, measurement and presentation of lease expenses and cash flows depend on the lease classification as a finance or operating lease.

The Company has operating leases for real estate and a vehicle. Its leases have remaining lease terms of one to three years. Our real estate lease agreements may include renewal or termination options for varying periods that are generally at our discretion. In our lease term, we only include those periods related to renewal options we are reasonably certain to exercise. However, we generally do not include these renewal options as we are not reasonably certain to renew at the lease commencement date. This determination is based on our consideration of certain economic, strategic, and other factors that we evaluate at lease commencement date and reevaluate throughout the lease term. Some leases also include options to terminate the leases and we only include those periods beyond the termination date if we are reasonably certain not to exercise the termination option.

Some leasing arrangements require variable payments that are dependent on usage or may vary for other reasons, such as payments for insurance and tax payments. The Company does not include the variable part of lease payments its ROU assets or lease liabilities. Rather, variable payments, other than those dependent upon an index or rate, are expensed when the obligation for those payments is incurred and are included in lease expenses recorded in selling and administrative expenses on the Consolidated Statements of Operations.

If any of the lease agreements have both lease and non-lease components, we treat those as a single lease component for all underlying asset classes. Accordingly, we account for all expenses associated with a lease contract as lease expenses.

F-22

Leases with a term of 12 months or less are not recognized on the balance sheet, but rather expensed on a straight-line basis over the lease term.

Income Taxes

The Company has elected to be treated as a partnership for income tax purposes. Therefore, the Company passes through its income and expenses to its members for tax reporting purposes.

Tesoro Hills, LLC, is a joint venture in which the Company has an investment. Tesoro Hills, according to its operating agreement, has elected to be treated as a partnership for income tax purposes.

The Company and MP Securities are subject to a California LLC fee.

The Company uses a recognition threshold and a measurement attribute for the consolidated financial statement recognition and measurement of a tax position taken in a tax return. The Company recognizes benefits from tax positions in the consolidated financial statements only when it is more likely than not that the tax position will be sustained upon examination by the appropriate taxing authority that would have full knowledge of all relevant information. A tax position that meets the more-likely-than-not recognition threshold is measured at the largest amount of benefit that is greater than 50 percent likely of being realized upon ultimate settlement. Tax positions that previously failed to meet the more-likely-than-not recognition threshold are recognized in the first subsequent financial reporting period in which that threshold is met. Management derecognizes previously recognized tax positions that no longer meet the more-likely-than-not recognition threshold in the first subsequent financial reporting period in which that threshold is no longer met.

Note 2: Pledged Cash and Restricted Cash

Under the terms of its debt agreements, the Company can pledge cash as collateral for its borrowings. On March 31, 2024 and December 31, 2023, the Company had cash of $7 thousand pledged as collateral for its secured borrowings. See “Note 3: Related Party Transactions” for additional details. This is included in restricted cash in the table below.

The following table provides a reconciliation of cash, cash equivalents, and restricted cash reported within the statement of financial position to the amounts reported in the statements of cash flows (dollars in thousands):

F-23

| | | | | | | | | |

| | March 31, | | December 31, | |||||

|

| 2024 |

| 2023 |

| 2023 | |||

Cash and cash equivalents | | $ | 11,193 | | $ | 17,057 | | $ | 10,854 |

Restricted cash | | | 1,760 | | | 58 | | | 1,757 |

Total cash, cash equivalents, and restricted cash shown in the statement of cash flows | | $ | 12,953 | | $ | 17,115 | | $ | 12,611 |

Restricted cash includes $1.7 million donated to MPC as permanently restricted funds under a designated fund agreement. The agreement allows for limited annual distributions of the funds. Other amounts included in restricted cash represent those required to be set aside in the CRD account with Financial Industry Regulation Authority (“FINRA”), funds the Company has deposited with RBC Dain as clearing deposits, and cash maintained in an account with ACCU as collateral for the Company’s secured borrowings. The Company may only use the CRD funds for certain fees charged by FINRA. These fees are to maintain the membership status of the Company or are related to the licensing of registered and associated persons of the Company.

Note 3: Related Party Transactions

Transactions with Equity Owners

Transactions with AdelFi Credit Union, a California state chartered credit union (“AdelFi”)

The tables below summarize transactions the Company conducts with AdelFi, (formerly Evangelical Christian Credit Union), the Company’s largest equity owner.

Related party balances pertaining to the assets of the Company (dollars in thousands):

| | | | | | |

| | March 31, | | December 31, | ||

|

| 2024 |

| 2023 | ||

Total funds held on deposit at AdelFi | | $ | 3,135 | | $ | 3,457 |

Loan participations purchased from and serviced by AdelFi | | | 1,284 | | | 1,298 |

F-24

Related party transactions of the Company (dollars in thousands):

| | | | | | |

| | Three months ended | ||||

| | March 31, | ||||

|

| 2024 |

| 2023 | ||

Interest earned on funds held with AdelFi | | $ | 39 | | $ | — |

Interest income earned on loans purchased from AdelFi | | | 21 | | | 1 |

Fees paid to AdelFi from MP Securities Networking Agreement | | | 3 | | | 2 |

Loan participation interests purchased:

The tables above show the number of loans purchased from Adelfi and the balance of loans serviced by Adelfi. For these loans, management negotiated the pass-through interest rates on a loan-by-loan basis and believes these negotiated terms were equivalent to those that would prevail in an arm’s length transaction.

MP Securities Networking Agreement with AdelFi:

MP Securities has entered into a Networking Agreement with AdelFi pursuant to which MP Securities agreed to offer investment and insurance products and services to AdelFi’s members that:

| (1) | AdelFi or its Board of Directors has approved; |

| (2) | comply with applicable investor suitability standards required by federal and state securities laws and regulations; |

| (3) | are offered in accordance with National Credit Union Administration (“NCUA”) rules and regulations; and |

| (4) | comply with its membership agreement with FINRA. |

The agreement provides that MP Securities will pay AdelFi a percentage of total revenue received by MP Securities from transactions conducted for or on behalf of AdelFi members. Either AdelFi or MP Securities may terminate the Networking Agreement without cause upon thirty days prior written notice.

Transactions with America’s Christian Credit Union, a California state chartered credit union (“ACCU”)

The Company has several related party agreements with ACCU, one of the Company’s equity owners. The following describes the nature and dollar amounts of the material related party transactions with ACCU.

F-25

Related party balances pertaining to the assets of the Company (dollars in thousands):

| | | | | | |

| | March 31, | | December 31, | ||

|

| 2024 |

| 2023 | ||

Total funds held on deposit at ACCU | | $ | 82 | | $ | 164 |

Dollar amount of outstanding loan participations sold to ACCU and serviced by the Company | | | 935 | | | 941 |

Amount owed on ACCU secured borrowings | | | 7 | | | 7 |

Amount owed on ACCU line of credit | | | 3,000 | | | 4,500 |

Loans pledged on ACCU line of credit | | | 7,121 | | | 7,167 |

Related party transactions of the Company (dollars in thousands):

| | | | | | |

| | Three months ended | ||||

| | March 31, | ||||

|

| 2024 |

| 2023 | ||

Interest earned on funds held with ACCU | | $ | — | | $ | 1 |

Dollar amount of net draws (payments) made on ACCU line of credit | | | (1,500) | | | — |

Interest expense on ACCU borrowings | | | 70 | | | 20 |

Income from broker services provided to ACCU by MPS | | | 8 | | | 9 |

Fees paid based on MP Securities Networking Agreement with ACCU | | | 24 | | | 36 |

Loan participation interests sold:

From time to time, the Company sells loan participation interests in loans it originates and services to ACCU. The Company negotiates pass-through interest rates on loan participation interests sold to ACCU on a loan-by-loan basis. Management believes these terms are equivalent to those that prevail in arm’s length transactions.

Effective August 9, 2021, the Company entered into a Master Loan Participation Purchase and Sale Agreement (“the Master LP Agreement”) with ACCU. The Master LP Agreement is intended to facilitate the sale to ACCU of small participation interests in the Company’s originated loans. As a part of any transaction conducted under the Master LP Agreement, the borrower of the loan being sold would become a member of ACCU, thereby meeting the requirements of NCUA regulations that govern loan participation purchases by credit unions. This allows the Company to sell additional participations in the loan to other credit unions.

Sales made under the Master LP Agreement are done on a recourse basis, requiring the Company to repurchase the participation interest in the event of default by the borrower. Under a separate Deposit Control Agreement reached in conjunction with the Master LP Agreement, the Company deposited cash on a one-to-one basis as collateral to secure the participation interest sold to ACCU. This cash is considered restricted cash. The Company

F-26

retains the ability to sell loan participation interests to ACCU outside of the Master LP Agreement.

As of March 31, 2024 and December 31, 2023, $7 thousand in participation interests had been sold and were outstanding under this agreement. These have been classified as secured borrowings on our balance sheet. The Company has deposited equal amounts of cash in an account at ACCU as collateral for these borrowings. These funds are considered restricted cash.

MP Securities Networking Agreement with ACCU:

MP Securities has entered into a Networking Agreement with ACCU pursuant to which MP Securities has agreed to offer investment and insurance products and services to ACCU’s members that:

| (1) | ACCU or its Board of Directors has approved; |

| (2) | comply with applicable investor suitability standards required by federal and state securities laws and regulations; |

| (3) | are offered in accordance with NCUA rules and regulations; and |

| (4) | comply with its membership agreement with FINRA. |

The agreement provides that MP Securities will pay ACCU a percentage of total revenue received by MP Securities from transactions conducted for or on behalf of ACCU members. Either ACCU or MP Securities may terminate the Networking Agreement without cause upon thirty days prior written notice.

Line of Credit:

On September 23, 2021, the Company entered into a Loan and Security Agreement with ACCU. The ACCU line of credit (“ACCU LOC”) is a $5.0 million short-term demand facility with a maturity date of September 23, 2024. See “Note 10: Credit Facilities and Other Debt” for additional terms and conditions of the ACCU LOC. Management believes these terms are equivalent to those that prevail in arm’s length transactions.

Transactions with Kane County Teachers Credit Union (“KCT”)

Our Board Chairperson, R. Michael Lee, serves as the Chief Executive Officer and President of KCT, an Illinois state chartered financial institution.

F-27

Related party balances pertaining to the assets of the Company (dollars in thousands):

| | | | | | |

| | March 31, | | December 31, | ||

|

| 2024 |

| 2023 | ||

Total funds held on deposit at KCT | | $ | 3,251 | | $ | 1,308 |

Amount owed on KCT line of credit | | | 4,500 | | | — |

Loans pledged on KCT lines of credit | | | 11,932 | | | 10,962 |

Certificates of deposit pledged on KCT Warehouse LOC | | | 1,250 | | | 1,250 |

Outstanding loan participations sold to KCT and serviced by the Company | | | 3,365 | | | 3,455 |

Related party transactions of the Company (dollars in thousands):

| | | | | | |

| | Three months ended | ||||

| | March 31, | ||||

|

| 2024 |

| 2023 | ||

Interest earned on funds held with KCT | | $ | 8 | | $ | 10 |

Dollar amount of draws on KCT line of credit | | | 4,500 | | | — |

Interest expense on KCT line of credit | | | 13 | | | — |

Fees paid based on MP Securities Networking Agreement with KCT | | | 5 | | | 8 |

Funds on deposit with KCT:

On March 15, 2024, the Company purchased a $1.3 million certificate of deposit from KCT. The certificate matures on March 15, 2025, and carries an interest rate of 2.25%. This certificate is pledged as a compensating balance deposit on one of the lines of credit the Company holds with KCT. The Company also holds a savings account with KCT.

Lines of credit:

On June 6, 2022, the Company terminated the existing $7.0 million Loan and Security Agreement with KCT. It replaced this agreement with two short-term demand credit facilities, a $5.0 million warehouse line of credit (“KCT Warehouse LOC”) and a $5.0 million operating line of credit (“KCT Operating LOC”). See “Note 10: Credit Facilities and Other Debt” for additional terms and conditions of these credit facilities. Management believes these terms are equivalent to those that prevail in arm’s length transactions.

MP Securities Networking Agreement

MP Securities, the Company’s wholly owned subsidiary, has entered into a Networking Agreement with KCT pursuant to which MP Securities agreed to offer investment and insurance products and services to KCT’s members that:

| (1) | KCT or its Board of Directors has approved; |

F-28

| (2) | comply with applicable investor suitability standards required by federal and state securities laws and regulations; |

| (3) | are offered in accordance with NCUA rules and regulations; and |

| (4) | comply with its membership agreement with FINRA. |

The agreement provides that MP Securities pay KCT a percentage of total revenue received by MP Securities from transactions conducted for or on behalf of KCT members. Either KCT or MP Securities may terminate the Networking Agreement without cause upon thirty days prior written notice.

Loan Participation Interests Sold

Occasionally the Company sells loan participation interests to KCT in the normal course of business. The Company retains the right to service these participation loans sold to KCT, and charges KCT a customary fee for servicing the loan. As of March 31, 2024 and December 31, 2023, respectively, the Company serviced $3.4 million and $3.5 million in loan participations that it has sold to KCT.

Transactions with Other Equity Owners

From time to time the Company will engage in transactions with other owners or related parties.

Related party balances pertaining to the assets of the Company (dollars in thousands):

| | | | | | |

| | March 31, | | December 31, | ||

|

| 2024 |

| 2023 | ||

Outstanding loan participations sold to NFCU and serviced by the Company | | $ | 4,712 | | $ | 4,745 |

Outstanding notes payable to officers and managers | | | 2,781 | | | 2,871 |

Loan Participation Interests

The Company has entered into a Loan Participation Agreement with Navy Federal Credit Union (“NFCU”), an owner of both the Company’s Class A Common Units and Series A Preferred Units. Under this agreement, the Company sold NFCU a $5.0 million loan participation interest in one of its construction loans on March 20, 2020. As part of this agreement, the Company retained the right to service the loan, and it charges NFCU a fee for servicing the loan. Management believes the terms of the agreement are equivalent to those that prevail in arm’s length transactions for similar agreements entered into by other credit unions.

F-29

From time to time, the Company may purchase a loan participation interest from a related party. The Company and its related party will negotiate in good faith the terms and conditions of such a purchase and in accordance with the Company’s related party procedures and governance practices. Each party must approve such a purchase after full disclosure of the related party transaction and must include terms and conditions that would normally be included in arm’s length transactions conducted by independent parties.

Debt Certificates Sold

From time to time, the Company’s Board and members of its executive management team have purchased debt certificates from the Company or have purchased investment products through MP Securities. Debt certificates payable owned by related parties totaled $2.8 million and $2.9 million as of March 31, 2024 and December 31, 2023, respectively.

Transactions with Subsidiaries

The Company has entered into several agreements with its subsidiary, MP Securities. The Company eliminates the income and expense related to these agreements in the consolidated financial statements. MP Securities serves as the managing broker for the Company’s public and private placement note offerings. MP Securities receives compensation related to these broker dealer services ranging from 0.25% to 5.50% over the life of a note. The amount of the compensation depends on the length of the note and the terms of the offering under which MP Securities sold the note.

The Company has also entered into an Administrative Services Agreement with MP Securities. The Administrative Services Agreement provides services such as the use of office space, use of equipment, including computers and phones, and payroll and personnel services. The agreement stipulates that MP Securities will provide ministerial, compliance, marketing, operational, and investor relations-related services in relation to the Company’s debt certificates program. As stated above, the Company eliminates all intercompany transactions related to this agreement in its consolidated financial statements.

Related Party Transaction Policy

The Board has adopted a Related Party Transaction Policy to assist in evaluating transactions the Company may enter into with a related party. Under this policy, a majority of the members of the Company’s Board and majority of its independent Board members must approve a material transaction that it enters into with a related party. As a result, all transactions that the Company undertakes with an affiliate, or a related party are entered into on terms believed by management to be no less favorable than are available from

F-30

unaffiliated third parties. In addition, a majority of the Company’s independent Board members must approve these transactions.

Note 4: Loans Receivable and Allowance for Expected Credit Losses

The Company’s loan portfolio comprises two segments, Non-profit commercial loans to Christian churches and ministries, and for-profit commercial loans. See “Note 1 – Loan Portfolio Segments and Classes” to Part I “Financial Information” of this Report. The loans fall into eight classes:

| ● | wholly owned amortizing loans for which the Company possesses the first collateral position; |

| ● | wholly owned amortizing loans for which the Company possesses security other than a first collateral position on real property; |

| ● | wholly owned amortizing loans that are unsecured; |

| ● | wholly owned lines of credit for which the Company possesses security other than a first collateral position on real property; |

| ● | wholly owned lines of credit that are unsecured; |

| ● | wholly owned construction loans |

| ● | participated amortizing loans purchased for which the Company possesses the first collateral position; and |

| ● | participated construction loans purchased. |

Prior to January 1, 2023, the Company’s loan portfolio comprised one segment – commercial loans – and four classes. Prior period data has been reclassified in the following tables to conform to current period presentation.

The Company primarily originates or purchases participations in loans that are made to Christian non-profit organizations and churches. The purpose of these loans is to purchase, construct, or improve facilities. Occasionally the Company purchases for-profit commercial loans to meet the Company’s revenue and yield goals, as well as to diversify the Company’s loan portfolio. Maturities on the loan portfolio extend through 2038. The loan portfolio had a weighted average interest rate of 6.68% and 6.42% as of March 31, 2024 and December 31, 2023, respectively.

F-31

The table below is a summary of the Company’s mortgage loans owned (dollars in thousands):

| | | | | | |

| | March 31, | | December 31, | ||

|

| 2024 |

| 2023 | ||

Non-profit commercial loans: | | | | | | |

Real estate secured | | $ | 88,799 | | $ | 87,524 |

Unsecured | | | 68 | | | 74 |

Total non-profit commercial loans: | | | 88,867 | | | 87,598 |

For-profit commercial loans: | | | | | | |

Real estate secured | | | 12,787 | | | 12,783 |

Total loans | | | 101,654 | | | 100,381 |

Deferred loan fees, net | | | (139) | | | (139) |

Loan discount | | | (165) | | | (168) |

Allowance for expected credit losses | | | (1,449) | | | (1,501) |

Loans, net | | $ | 99,901 | | $ | 98,573 |

Allowance for expected credit losses

Management believes it has properly calculated the allowance for expected credit losses using CECL methodology as of March 31, 2024 and December 31, 2023. The following table shows the changes in the allowance for expected credit losses for the three months ended March 31, 2024 and the year ended December 31, 2023 (dollars in thousands):

| | | | | | | | | |

| | Three months ended | |||||||

|

| March 31, 2024 | |||||||

Segment: | | Non-profit Commercial | | For-profit Commercial | | Total | |||

Balance, beginning of period | | $ | 1,471 | | $ | 30 | | $ | 1,501 |

Provision (credit) for expected credit loss | | | (53) | | | 1 | | | (52) |

Charge-offs | | | — | | | — | | | — |

Recoveries | | | — | | | — | | | — |

Balance, end of period | | $ | 1,418 | | $ | 31 | | $ | 1,449 |

| | | | | | | | | |

| | Year ended | |||||||

| | December 31, 2023 | |||||||

Segment: | | Non-profit Commercial | | For-profit Commercial | | Total | |||

Balance, beginning of period | | $ | 1,530 | | $ | 21 | | $ | 1,551 |

Adjustment related to implementation of CECL model | | | 129 | | | (16) | | | 113 |

Provision (credit) for expected credit loss | | | (167) | | | 25 | | | (142) |

Charge-offs | | | (21) | | | — | | | (21) |

Recoveries | | | — | | | — | | | — |

Balance, end of period | | $ | 1,471 | | $ | 30 | | $ | 1,501 |

F-32

In the course of its lending operations, the Company has made loans that include commitments to fund additional amounts over the remaining term of the loan. These include construction loans and lines of credit, both revolving and non-revolving. The Company has established an allowance for losses on these unfunded commitments. See "Note 12: Commitments and Contingencies" for details on its allowance for credit losses on off-balance sheet commitments.

The table below presents loans by portfolio segment and the related allowance for expected credit losses. In addition, the table segregates loans and the allowance for expected credit losses by impairment methodology (dollars in thousands).

| | | | | | |

| | Loans and Allowance for | ||||

| | As of | ||||

|

| March 31, 2024 |

| December 31, 2023 | ||

Non-profit Commercial Loans: | | | | | | |

Individually evaluated for impairment | | $ | 16,767 | | $ | 16,792 |

Collectively evaluated for impairment | | | 72,100 | | | 70,806 |

Total Non-profit Commercial Loans | | | 88,867 | | | 87,598 |

For-profit Commercial Loans: | | | | | | |

Individually evaluated for impairment | | | — | | | — |

Collectively evaluated for impairment | | | 12,787 | | | 12,783 |

Total For-profit Commercial Loans | | | 12,787 | | | 12,783 |

Balance | | $ | 101,654 | | $ | 100,381 |

| | | | | | |

Allowance for expected credit losses: | | | | | | |

Non-profit Commercial Loans: | | | | | | |

Individually evaluated for impairment | | $ | 675 | | $ | 669 |

Collectively evaluated for impairment | | | 743 | | | 802 |

Total Non-profit Commercial Loan Allowance | | | 1,418 | | | 1,471 |