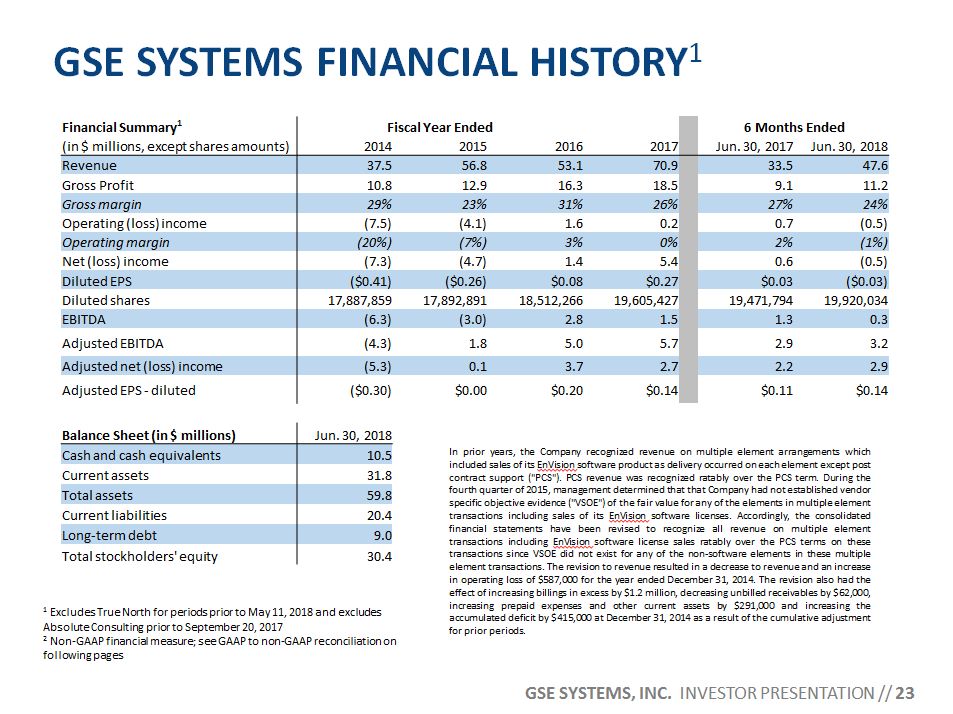

FORWARD LOOKING STATEMENTSand non-gaap financial measures This presentation, our remarks, and answers to questions contain statements that are considered forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934. These statements reflect our current expectations concerning future events and results. We use words such as "expect," "intend," "believe," "may," "will," "should," "could," "anticipate," and similar expressions to identify forward-looking statements, but their absence does not mean a statement is not forward-looking. These statements are not guarantees of our future performance and are subject to risks, uncertainties, and other important factors that could cause our actual performance or achievements to be materially different from those we project. For a full discussion of these risks, uncertainties, and factors, we encourage you to read our documents on file with the Securities and Exchange Commission, including those set forth in our periodic reports under the forward-looking statements and risk factors sections. We do not intend to update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise.This presentation, our remarks, and answers to questions include references to adjusted EBITDA, adjusted net income, and adjusted earnings per share (“adjusted EPS”), which do not adhere to generally accepted accounting principles (“GAAP”). We define EBITDA as earnings before interest, taxes, depreciation and amortization (“EBITDA”). We define Adjusted EBITDA as EBITDA plus adjustments for consulting support for finance restructuring, stock-based compensation expense, restructuring charges, gain/loss from the changes in fair value of contingent consideration, acquisition-related expense, and customer bankruptcy related expense. We define adjusted net income as net income plus adjustments for consulting support for finance restructuring, stock-based compensation expense, restructuring charges, gain/loss from the changes in fair value of contingent consideration, acquisition-related expense, customer bankruptcy-related expense, tax reform impact, and release of valuation allowance. We define adjusted EPS as adjusted net income divided by fully diluted shares of common stock issued and outstanding. EBITDA, Adjusted EBITDA, adjusted net income, and adjusted EPS are reconciled to net income, the most directly comparable GAAP measure, in the financial tables included in the Appendix to this presentation. We believe that this additional information and the reconciliation we provide may be useful to help evaluate our operations. This information supplements our results as reported in accordance with GAAP and should not be viewed in isolation from, or as a substitute for, our GAAP results.With respect to Adjusted EBITDA on a forward-looking basis and as a combined company following certain recent acquisitions, a reconciliation of the difference between this non-GAAP expectation and the corresponding GAAP measure (expected net income) is not available without unreasonable effort due to potentially high variability, complexity and low visibility as to the items that would be excluded from the GAAP measure in the relevant future period, such as unusual gains and losses, adjustments to the provision for income taxes, depreciation of fixed assets, amortization of intangibles, costs related to restructuring actions and interest expense, and certain anticipated cost synergies, the impact and timing of potential acquisitions and divestitures, and other structural changes or their probable significance. The variability of the excluded items may have a significant, and potentially unpredictable, impact on our future GAAP results.Unless otherwise indicated, all results of operations and the financial condition of the Company are as of June 30, 2018 and all market data set forth in this presentation is as of August 20, 2018. We undertake no duty to update or revise the information in light of new information, future events or otherwise, although we may do so from time to time as management believes is appropriate. Any such updating may be made through the filing of reports or documents with the Securities and Exchange Commission, through press releases or through other public disclosures. 2