QuickLinks -- Click here to rapidly navigate through this document[PHOTO]

Tesma International Inc.

Annual Report 2003

TESMA Measuring Our Success

Tesma At A Glance

| | 2003 Operating Highlights

| | Major Customers

|

|---|

Tesma

Engine

Technologies |

|

• Expanded customer base to include Hyundai, Fiat and

the PSA Group

• Expanded product line to include more value-added

assemblies and modules — Hyundai V6 engine front cover

module, General Motors' (GM) 3.9L engine front cover

module

• Established two new entities in Italy on one site to produce

oil and water pump assemblies and front end accessory drive

components for European customers

• Intensified Six Sigma continuous improvement activities

• Established a plant in China to manufacture automatic belt

tensioners for Volkswagen |

|

• General Motors

(including Fiat, Saab, Isuzu)

• Ford

(including Volvo, Mazda,

Jaguar)

• DaimlerChrysler

(including Mitsubishi,

Hyundai)

• Honda

• Toyota

• Renault-Nissan-Samsung

• Hitachi |

|

Tesma Transmission Technologies |

|

• Awarded hub and housing business on new GM

6-speed rear wheel drive transmission

• Launched various new products, including continuously

variable transmission (CVT) cylinders for ZF in Europe and

aluminium clutch pistons for GM

• Expanded research and development (R&D) capabilities

to include high-speed spin burst testing and multi-channel

torque and axial load fatigue testing

• Launched transfer case shafts and hubs for a key

program for Magna Steyr

• Launched transmission centre support housing for GM

• Realized operational efficiency and capacity utilization

improvements through Six Sigma initiatives

• Announced agreement to acquire Davis Industries, Inc.

(Davis), a U.S.-based powertrain supplier (completed

January 2, 2004) |

|

• General Motors

• Ford

(including Mazda)

• DaimlerChrysler

• Allison Transmission

• ZF

• Renault-Nissan-Samsung

• Magna Steyr |

|

Tesma Fuel Technologies |

|

• Focused R&D initiatives on the development of low

permeation capless filler systems, filler pipes and fuel tank

assemblies to meet Low Emission Vehicle (LEV II)

Legislation and Partial Zero Emission Vehicle (PZEV)

legislation

• Continued Six Sigma initiatives, LEAN/Synchronous

manufacturing efforts and VA/VE design improvements

to increase product functionality and reduce costs

• Launched several fuel filler pipe programs in Europe and

North America for Ford and DaimlerChrysler

• Launched the Volkswagen PQ34 PZEV stainless steel

fuel tank in Europe |

|

• General Motors

(including Fiat)

• Ford

(including Volvo)

• DaimlerChrysler

• Volkswagen Group

• BMW

• Audi |

Product Offerings

| | 2004 Goals and Strategy

|

|---|

• Front End Accessory Drive Systems

• Accessory and Timing Drive Tensioners

• Steel, Phenolic and Aluminium Pulleys

• Idler Assemblies

• Engine Front Cover Modules

• Engine Oil Pumps

• Water Pumps

• Cooling Management Systems

• Overrunning Alternator Decouplers

• Cam Covers

• Variable Camshaft Phasing Systems

• Engine Oil Pan Assemblies

• Engine Balance Shaft Assemblies

• Collapsible Drive Shaft Assemblies

• Rocker Covers |

|

• Capitalize on Tesma's component manufacturing

expertise/capabilities and further integrate to value-added

assemblies and modules

• Expand customer base in key markets for our engine front

cover modules, cooling and lubrication systems

• Continue to develop full-service capabilities by further

expanding our design, development, testing and validation

capabilities at both the component and systems levels

• Continue to expand benchmarking capabilities for cooling,

lubrication and engine systems products

• Successfully launch our first oil pumps and pulleys from

our operations in Italy

• Continue to develop unique and innovative products,

technologies and materials

• Successfully launch significant business at our

South Korean operations, including our first engine

front cover module for Hyundai |

|

• Automatic Transmission Clutch Housings and Shaft Assemblies

• Flow-Formed Clutch Housings

• Cam Die-Formed Transmission Shells

• Torque Converter Damper Assemblies

• Oil Pump Assemblies

• Die-Formed Oil Pan Assemblies

• Aluminium Die-Cast and Machined Case Extensions

and Clutch Housings

• Servo Piston and Accumulator Assemblies

• Roller Die-Formed Drive Hubs and Housings

• Fineblanked Products, Separator Plates and Backing Plates

• Flexplates

• Reaction and Input Shells

• CVT — Pistons, Plungers and Clutch Housings

• Friction Clutch Pack Assemblies

• Transfer Case Output Shafts and Flanges

• Torque Converter Stator Shafts |

|

• Successfully integrate the Davis operations

• Expand engineering and testing capabilities to include

complete clutch pack assemblies

• Continue to pursue and expand content in the precision

aluminium transmission die-cast components area

• Continue to pursue value-added sub-assemblies for

various transmission applications

• Expand our transmission oil pump assemblies to include

vane pump technology and unique variable flow

technology

• Expand transfer case component and sub-assembly

capability

• Expand customer base into non-traditional OEM market |

|

• Fuel Caps

• Fuel Filler Inlets and Valves

• Capless Filler Systems

• Steel Fuel Filler Pipes

• Steel Fuel Tank Assemblies

• Vent, Fill and Spud Tubes

• Fuel Sender Units |

|

• Provide leadership in the development and market

introduction of innovative fuel system solutions and

alternative material applications

• Expand our current product portfolio in Europe and

North America

• Provide customers with improved fuel system permeation

and corrosion performance and reduced waste through

improved recyclability

• Successfully launch the JR fuel tank and LX fuel filler pipe

programs for DaimlerChrysler in North America

• Continue with the successful ramp-up of Ford's global C1

fuel filler pipe program in our Austrian facility |

Profile

Tesma International Inc. (Tesma or the Company) designs, engineers, tests and manufactures technologically-advanced engine, transmission and fuel components, modules and systems for the global automotive industry. Tesma employs over 5,500 people in 28 manufacturing facilities (subsequent to the Davis Industries, Inc. acquisition) in North and South America, Europe and Asia and five focused tooling, design and R&D centres supporting our three principal product technology groups: Tesma Engine Technologies, Tesma Transmission Technologies and Tesma Fuel Technologies. Tesma ships its products to Original Equipment Manufacturers (OEMs) on six continents.

Tesma's Class A Subordinate Voting Shares trade on the Toronto Stock Exchange under the symbol TSM. A and the NASDAQ Stock Market under the symbol TSMA.

Forward-Looking Statements: This Annual Report may contain "forward-looking statements" within the meaning of applicable securities legislation. Such statements involve certain risks, assumptions, uncertainties and other factors (as described in Tesma's Annual Information Form, Form 40-F and other public filings) which may cause Tesma's actual future results or performance to differ materially from those expressed or implied herein. Tesma expressly disclaims any intention, and undertakes no obligation, to update or revise any forward-looking statements to reflect subsequent information, events, results, circumstances or otherwise.

| FOLD — OUT | | Tesma At A Glance |

| 02 | | Results |

| 03 | | Global Performance |

| 03 | | Content Per Vehicle |

| 04 | | Chairman's Message |

| 05 | | Letter to Shareholders |

| 09 | | Glossary |

| 10 | | Components, Modules and Systems |

| 13 | | Tesma Engine Technologies |

| 17 | | Tesma Transmission Technologies |

| 21 | | Tesma Fuel Technologies |

| | 22 | | Policies |

| | 22 | | Corporate Constitution |

| | 22 | | Employee's Charter |

| 23 | | Corporate Governance |

| 24 | | Review |

[PHOTO]

Customers. Employees. Shareholders.

They all have expectations.

And Tesma delivers results.

We're an industry leader in quality.

That's what our customers tell us.

They assess our performance every day.

We're a great place to work.

That's what employees tell us — in opinion surveys

and through long-term commitments to our team.

We build shareholder value.

That's what financial metrics tell us.

We're a leader among our peers.

But no one expects more of Tesma

than we do of ourselves.

That's how we measure our success.

The details are inside.

TESMA 1

Results

Financial Highlights

| | December 31

| |

|

|---|

| | % change

|

|---|

| | 2003

| | 2002

|

|---|

(U.S. dollars in millions, except per share and shares amounts)

| |

| |

| |

|

|---|

| Results for the year ended | | | | | | | | |

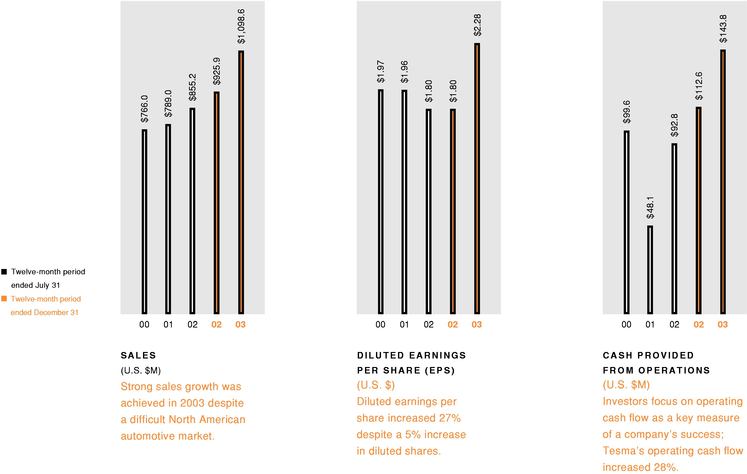

| Sales | | $ | 1,098.6 | | $ | 925.9 | | +19% |

| Income before income taxes | | $ | 110.0 | | $ | 82.9 | | +33% |

| Net income | | $ | 74.1 | | $ | 56.0 | | +32% |

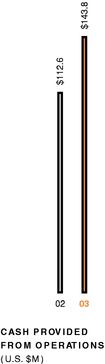

| Operating cash flow | | $ | 143.8 | | $ | 112.6 | | +28% |

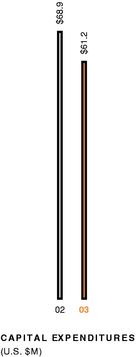

| Capital expenditures | | $ | 61.2 | | $ | 68.9 | | -11% |

Earnings per Class A Subordinate |

|

|

|

|

|

|

|

|

| | Voting Share or Class B Share | | | | | | | | |

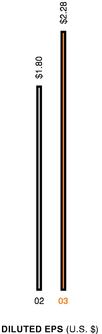

| | | Basic | | $ | 2.29 | | $ | 1.82 | | +26% |

| | | Diluted | | $ | 2.28 | | $ | 1.80 | | +27% |

| Cash dividends paid per Class A Subordinate | | | | | | | | |

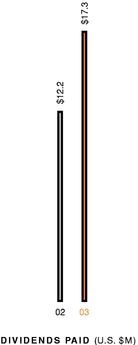

| | Voting Share or Class B Share (CDN $) | | $ | 0.75 | | $ | 0.64 | | |

| Average number of Class A Subordinate | | | | | | | | |

| | Voting Shares and Class B Shares outstanding | | | | | | | | |

| | | Basic | | | 32.3 | | | 30.7 | | +5% |

| | | Diluted | | | 32.5 | | | 31.1 | | +5% |

Year end position, as at |

|

|

|

|

|

|

|

|

| Cash (net of bank indebtedness) | | $ | 122.5 | | $ | 89.0 | | +38% |

| Total assets | | $ | 839.0 | | $ | 656.8 | | +28% |

| Long-term debt (including current portion) | | $ | 66.8 | | $ | 49.4 | | +35% |

| Shareholders' equity | | $ | 549.3 | | $ | 410.2 | | +34% |

| Book Value per Class A Subordinate | | | | | | | | |

| | Voting Share or Class B Share | | $ | 16.92 | | $ | 12.66 | | +34% |

2 TESMA

Global Performance

| | NORTH AMERICA

| | EUROPE

| | OTHER

|

|---|

| | December 31

| | December 31

| | December 31

|

|---|

Operating Segment

|

|---|

| | 2003

| | 2002

| | 2003

| | 2002

| | 2003

| | 2002

|

|---|

(U.S. dollars in millions, except facilities and employees)

| |

| |

| |

| |

| |

| |

|

|---|

| Sales | | $ | 856.0 | | $ | 725.5 | | $ | 235.6 | | $ | 180.6 | | $ | 28.8 | | $ | 33.8 |

| Income before income taxes | | $ | 97.5 | | $ | 87.5 | | $ | 18.3 | | $ | (6.1 | ) | $ | (5.8 | ) | $ | 1.5 |

| Capital assets | | $ | 206.1 | | $ | 197.8 | | $ | 65.2 | | $ | 49.1 | | $ | 32.4 | | $ | 26.2 |

| Manufacturing facilities | | | 15 | | | 15 | | | 6 | | | 5 | | | 4 | | | 3 |

| Employees | | | 3,600 | | | 3,500 | | | 1,100 | | | 1,200 | | | 300 | | | 200 |

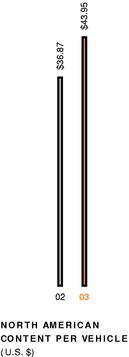

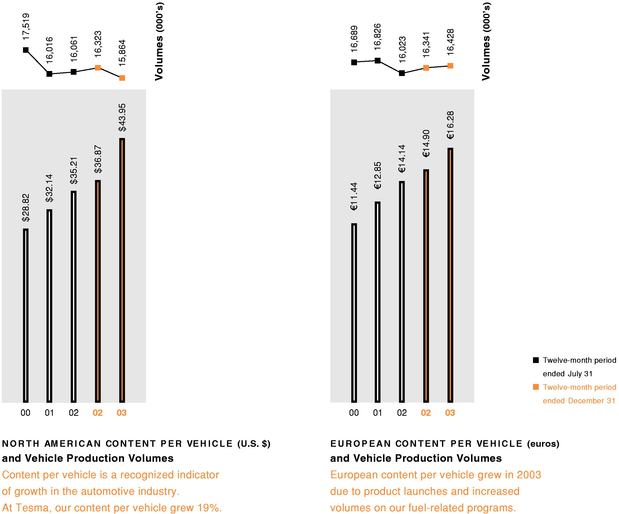

Content Per Vehicle

TESMA 3

[PHOTO]

MANFRED GINGL

Chairman & Chief Executive Officer

Chairman's Message

Tesma's success is very much a measure of our corporate culture and structure, both of which have their roots in Magna. Why have we placed such an emphasis on these two elements of how we do business? The answer is quite simple. It's not enough to have the right structure; a great company needs the right people, too.

Our greatest asset is outstanding and entrepreneurial individuals. We hold them accountable, we challenge and empower them — and we reward them through employee profit participation and share ownership programs. We provide them with training and education programs, as well as the opportunity to use what they have learned. Financial compensation is an important incentive — but so is the sense of pride and ownership that comes from working for, and contributing to, the success of Tesma. And so is "having fun along the way"!

Our manufacturing divisions operate as individual profit centres with dedicated production, finance, human resources and engineering teams. These teams can quickly respond to issues impacting operations, as well as investing in resources to develop opportunities for the future. In a centralized organization, by the time information reaches the top and filters back again, it's often too late.

While we work in a decentralized environment, we still try to capitalize on Tesma's brand identity and purchasing power, as well as its expertise in treasury, finance, information technology, tax and sales by maintaining certain centralized corporate office functions. This structure allows each general manager to focus on his division's performance in quality, delivery and profitability. To ensure consistency in our human resources initiatives and policies within all divisions, Tesma's HR department oversees the implementation and compliance of these initiatives on an ongoing basis.

I believe in our culture and our structure. It is the unique combination of these elements at Tesma that will allow us to continue to drive forward, benefit from trends in the automotive powertrain area and provide further growth and success.

/s/ MANFRED GINGL

MANFRED GINGL

CHAIRMAN & CHIEF EXECUTIVE OFFICER | | |

4 TESMA

[PHOTO]

ANTHONY E. DOBRANOWSKI

President & Chief Financial Officer

Letter to Shareholders

We had another great year. We surpassed our competitors in key performance measures such as return on funds employed, return on assets and return on equity. We increased sales 19% over 2002 and continued to grow our content per vehicle, which rose from U.S. $36.87 to U.S. $43.95 in North America and from €14.90 to €16.28 in Europe. Our North American sales grew 18% to U.S. $856 million despite lower vehicle production volumes. Overall, our bottom line increased to U.S. $74.1 million from U.S. $56.0 million a year ago.

TESMA 5

Why does Tesma remain profitable in the current tough market?

Many factors play a part. I'll point out just a few. First, we have people with the product development and manufacturing skills needed to wring savings from our processes, make continuous improvements, enhance quality and productivity and provide strong technical expertise and service to our customers.

We also have great discipline in the quoting process. We won't quote on jobs just to fill floor space and increase sales. And we are intensifying our focus on initiatives like better supplier management and offshore purchasing.

Geographic diversification allows us to increase our opportunities while mitigating our risks. From a product standpoint, we have expertise on a part of the vehicle that offers relatively great scope for proprietary products and technical proficiency, which we have developed through innovative solutions.

How are your customer relationships evolving?

We have solid and stable relationships with the majority of the world's major vehicle manufacturers. Our operations are efficient and world-class, with the right people and processes in place to help our customers. We are always looking for ways to exceed their expectations. Our industry faces price and margin pressures from OEMs, which means Tesma must make products better, faster and at lower cost than our competitors — and we do.

Our three technology groups have grown by taking single products and building on them. Tesma Engine Technologies, which began by manufacturing pulleys and front end accessory drive components, now makes entire front cover modules and is expanding down the engine. Tesma Transmission Technologies started with a few components and today offers a variety of transmission modules and assemblies. Tesma Fuel Technologies originally manufactured only caps, but has evolved to sell complete filler pipes and tanks as well. That's our organic growth curve.

Our customers are buying more and more systems and modules, rather than individual products — and they are relying on suppliers for engineering and development. In 2003, we derived approximately 80% of our sales from complete, value-added modules and assemblies, up from 75% last year. These types of products also represented about 80% of the business awarded to us during the year.

Our plan is to increase our North American market presence beyond the "Big Three" and to derive 15% of our sales from New Domestic manufacturers by 2006. The acquisition of Davis in early January 2004 moves us closer to this goal. Davis, a U.S.-based automotive parts manufacturer and supplier with annual sales of U.S. $129 million in their recently completed fiscal year, focuses on stamped powertrain components and assemblies that complement our existing product offerings.

Davis gives us, for the first time, a presence close to the assembly facilities of the OEMs in the southern U.S. Just as importantly, the acquisition broadens our customer relationships with non-traditional customers, as a high percentage of Davis' sales are to New Domestics. We expect Davis to be immediately accretive and to add more than U.S. $0.10 per share annually to our earnings in 2004.

80%

In 2003, we derived approximately 80% of our sales from complete, value-added modules and assemblies, up from 75% last year.

6 TESMA

What are you doing to diversify geographically and why?

From a very sound base in North America, we have set our sights on obtaining significant business in Europe and Asia. Our approach is to start small and develop the critical mass required to meet our customers' needs, while achieving good returns and strategic leverage for Tesma.

Global presence is important for the simple reason that our customers are demanding global capability from their suppliers. They expect us to offer global manufacturing, testing and product development, and technical and sales representation. With this in mind, we made a number of moves in 2003.

From a manufacturing perspective, we opened our first Italian operations. We'll use these operations to migrate to Europe some pulley business that is currently exported from Canada and will supply Fiat with oil and water pumps for the European market. We expanded our South Korean facilities and established our first plant in China. It will manufacture automatic belt tensioners for Volkswagen to supply the Chinese market. We are building an infrastructure and a team with potential to broaden our manufacturing capabilities and capitalize on future business opportunities in China.

In terms of testing and product development, we added resources in Korea and began building our capabilities in China. We also improved our ability to conduct testing and product development in Europe. And we increased our technical and sales representation in Japan.

Are more acquisitions likely?

There are three key elements that influence our interest in acquisitions: products, processes and geographic presence. We are reviewing our products to determine whether we should make any changes in our focus due to the emergence of new technologies or for other reasons. We already use more than 50 processes, but there are others, such as those used to manufacture powdered metal and magnesium components, which could strengthen our portfolio. Our decisions with respect to geographic location are a balance between what customers want us to do, what our real needs are and whether we have a viable business model. For example, we are looking to create critical mass in Europe and continue to review acquisition opportunities on that continent.

In evaluating acquisition targets, we try to strike a balance between the price we are willing to pay for a "strategic" versus a "good fit" acquisition; our ability to support the purchase price and future growth requirements; the implementation and integration risks that are inherent in all transactions; and the impact on our shareholders. Other factors include "cultural" and employee fit and reliance on particular customers.

We continue to look for attractive targets, but we will only make deals that make sense for Tesma. Acquisitions are not the only way to expand our business. We are launching new products and generating solid internal growth. For instance, in 2003 we booked new business that will represent over U.S. $270 million in annual sales by the time these programs reach full production volumes in 2007. Our strong balance sheet and cash reserves give us the flexibility to make the best choices for Tesma.

U.S. $270M

In 2003, we booked new business that will represent over U.S. $270 million in annual sales at full production volumes.

TESMA 7

What is the market potential — and how competitive is Tesma?

While outsourcing is an accelerating trend among OEMs, the powertrain sector is one of the least exploited segments and offers the best potential. In spite of Tesma's excellent growth record, we currently represent just 2.3% of the estimated U.S. $46 billion annual global powertrain market for Tesma's product portfolio.

Certainly foreign exchange is a competitive challenge for any Canadian exporter, as the Canadian dollar appreciated by 12% in 2003 against the U.S. dollar. Our Canadian counterparts are in the same boat as Tesma, but we also have competitors in the United States. Up to now, we have managed the impact of foreign exchange; if the dollar appreciates beyond a certain point we'll feel the pain of converting Canadian costs into U.S. dollars for quoting purposes. Still, it's not the end of the world for us.

We do have the flexibility to set up manufacturing facilities locally if appropriate. The Davis acquisition expands our presence in the southern U.S. and improves this flexibility.

Also, one needs to consider where sales are generated. It's not just a question of the differential between the Canadian and U.S. dollars. Our sales are denominated in yen, in euros and in various other currencies. We may lose on one transaction, but benefit on another.

Other aspects of competitiveness include the immediate pressures for customer givebacks. This means we must review and adjust the resources within our facilities to make the most of our manufacturing processes. We're doing an effective job of that.

The question of competitiveness underscores why it's important to diversify our customer base and geographic presence. We don't want to be overly reliant on any single source of business.

How will Tesma measure up in 2004 and beyond?

From 2003 to 2006, vehicle production volumes are expected to grow from 15.9 million units to 16.5 million units in North America and from 16.5 million units to 17.3 million units in Europe. Like the economy and currency fluctuations, industry volumes are among the uncontrollable factors that affect our business. We are determined to optimize Tesma's performance, whatever the conditions.

We anticipate that Tesma's annual sales will increase 12 to 13%, on average, over the next three years. We will enhance our performance metrics through sales growth and rigorous focus on costs and production efficiencies. During nearly a decade as a public company, Tesma has focused on the "Big Three" OEMs. In 2004 and beyond, we will continue to grow this business while highlighting opportunities with other OEMs in North America, Europe and Asia, including the New Domestic OEMs.

I am confident that Tesma will measure up well over the long term, due largely to our strong relationships with customers, employees and shareholders. I'd like to express my personal thanks for their support in 2003.

Tesma's ultimate vision is to be the world's leading Tier 1 supplier of advanced powertrain modules and systems. By designing, testing and building highly-engineered and proprietary products for global markets and a growing customer base, we are well positioned to reach our goal.

/s/ ANTHONY E. DOBRANOWSKI

ANTHONY E. DOBRANOWSKI

PRESIDENT & CHIEF FINANCIAL OFFICER | | |

2.3%

We currently represent just 2.3% of the estimated U.S. $46 billion annual global powertrain market for Tesma's product portfolio.

8 TESMA

Glossary

"Big 3" or Traditional OEMs

Refers to the North American operations of General Motors, Ford Motor Company and DaimlerChrysler

Content Per Vehicle (North America or Europe)

The average dollar (or euro) value of parts produced by Tesma included in each vehicle assembled in North America (or Europe) respectively. It is calculated as Tesma's total product sales to customers in North America or Europe divided by the number of vehicles assembled in each of these markets.

Continuously Variable Transmission (CVT)

A transmission that continuously varies the gear ratios between the engine input and torque output. A CVT allows optimum revolutions per minute (RPM), for maximized fuel economy, engine efficiency, low emissions and improved performance. A manual or automatic transmission has a predefined set of gear ratios, which does not allow for optimal performance.

DaimlerChrysler Group

Includes the automotive companies Chrysler, Mercedes-Benz, Hyundai, MCC (Smart) and Mitsubishi

European Vehicle Production

Vehicles assembled in Western Europe, which includes Austria, Belgium, Finland, France, Germany, Italy, the Netherlands, Norway, Portugal, Spain, Sweden and the United Kingdom

Ford Motor Company

Includes the automotive companies Ford, Volvo, Jaguar, Aston Martin, Mazda and Land Rover

General Motors Group

Includes the automotive companies General Motors, Hummer, Saab, Saturn, Fiat, Isuzu, Subaru (Fuji Heavy Industries), Holden, Opel, Vauxhall and Daewoo

Global Six

The six largest automotive OEMs: General Motors, Ford Motor Company, DaimlerChrysler, Toyota, Volkswagen Group and Renault-Nissan-Samsung

Low Emission Vehicle (Level 2) LEV II

LEV I was the original Low Emission Vehicle specification for conventional gas fueled vehicles and LEV II was established with more stringent specifications for emissions. It was initiated by the California Air Resources Board (CARB).

Modules and Systems

A series of components or sub-assemblies that are integrated into a package.

North American New Domestic OEMs

OEMs that assemble vehicles, engines or transmissions in North America other than the "Big 3" — examples are: Toyota, Honda, Renault-Nissan Samsung and BMW

North American Non-traditional OEMs

OEMs that sell vehicles in North America other than the "Big 3" — examples are: Toyota, Honda and KIA

North American Vehicle Production

The number of light vehicles assembled in the United States, Canada and Mexico

OEM Outsourcing

The procuring of components, modules and systems used in the manufacture of motor vehicles to outside suppliers or manufacturers in order to cut costs.

Original Equipment Manufacturers (OEMs)

Assemblers of complete vehicles, including their engine and transmission operations. OEMs provide the original product design and are directly responsible for manufacturing and modifying the products, making them commercially available and providing warranty coverage.

Partial Zero Emission Vehicle (PZEV)

A lower emission vehicle (a more stringent regulation than LEV II) which does not meet full-zero emission specifications for gas fueled vehicles as set out by CARB regulations.

Powertrain

An engine and transmission combined; can also include the driveshaft and drive axle

Production Part Approval Process (PPAP)

An OEM process where quality and specification monitoring is done prior to the part entering the commercial manufacturing stage.

Six Sigma

A disciplined and data driven approach to eliminate waste and reduce variation in any process using the Breakthrough Methodology which is define, measure, analyze, improve and control.

Tier 1 Supplier

A company that sells their products directly to the Original Equipment Manufacturer (OEM).

Volkswagen Group

Includes the automotive companies Volkswagen, Audi, Seat, Skoda and Auto-Europa

TESMA 9

Components, Modules and Systems

Tesma manufactures thousands of individual components. These products are assembled in a variety of modules and systems for the world's leading vehicle manufacturers. To us, the quality of each component, each module and each system is the foundation of our success.

| [PHOTO] | | Tesma Engine Technologies | | |

| [PHOTO] | | Engine Front Cover Module | | |

| [PHOTO] | | Balance Shaft Assembly | | |

| [PHOTO] | | Water Pump | | |

| [PHOTO] | | Engine Oil Pump | | |

| [PHOTO] | | Water Management (Thermostat) Assembly | | |

| [PHOTO] | | Accessory and Timing Drive Tensioner | | [PHOTO] |

| [PHOTO] | | Water Pump Pulley | | |

| [PHOTO] | | Engine Oil Pan Assembly | | |

| [PHOTO] | | Rocker Cover | | |

| [PHOTO] | | Water Pump Module | | |

| [PHOTO] | | Camshaft Phasing System | | Products shown are representative parts only, illustrating Tesma's capabilities.

Actual parts used in this vehicle may be different. |

10 TESMA

| Tesma Fuel Technologies | | Fuel Tank | | [PHOTO] |

| | | Fuel Filler Pipe | | [PHOTO] |

| | | Fuel Cap | | [PHOTO] |

| | | Universal Sender Unit | | [PHOTO] |

| Tesma Transmission Technologies | | Die-Cast Transmission Case Extension | | [PHOTO] |

| | | Flexplate | | [PHOTO] |

| | | Rotating Clutch Housing | | [PHOTO] |

| [PHOTO] | | Torque Converter Damper Assembly | | [PHOTO] |

| | | Centre Support | | [PHOTO] |

| | | Transmission Oil Pan | | [PHOTO] |

| | | Servo Piston Assembly | | [PHOTO] |

| | | Transmission Oil Pump Assembly | | [PHOTO] |

| | | Clutch Pack Assembly | | [PHOTO] |

| | | Torque Converter Cover | | [PHOTO] |

| | | | |

TESMA 11

[PHOTO]

Quality is not simply about the ability to use gauges or instruments to measure a part's performance. Quality is about process capability. It's about having equipment in place that can accurately perform a particular function — and people in place who can use it most effectively. Tesma stands out in quality. That's how we measure success.

12 TESMA

| [PHOTO] | | [PHOTO] | | [PHOTO] | | |

JON ENOAE |

|

PETER VERT |

|

RANDY SCOTT |

|

|

Group Vice President

Engine Technologies |

|

Director of

Group Engineering &

Product Development

Engine Technologies |

|

Group Controller

Engine Technologies |

|

"Tesma's philosophy is that we don't want to compete at the bottom end of the market — what we refer to in the engineering world as 'quote to print'. Companies that do this wind up competing on price alone. We differentiate ourselves, first of all, by excelling in complex design, engineering, testing, quality and delivery. Secondly, we are establishing ourselves as a leading supplier of modules. In value-added markets, few suppliers can compete with us." |

|

|

|

|

|

|

GM 3.9L V6 ENGINE

FRONT COVER MODULE |

|

|

|

|

|

|

[PHOTO] |

Tesma Engine Technologies

Quality Standout

Tesma is a pioneer and leader in front end accessory drive systems, tensioners and idler assemblies. Our strategy is to combine components at the front of the engine and ship them to our customers as modules. We have unique manufacturing and engineering experience in every facet of the front of the engine, including water and oil pumps, castings to make covers, pulleys, and accessory drive systems.

Tesma Engine Technologies' sales increased 17% to U.S. $745 million in 2003 from U.S. $639 million in 2002. Our success shows that our strategy is working.

Key awards in 2003 included the front cover module and oil pan assembly for GM's 3.9L V6 engine for its higher volume mid-size car platforms. We also won the front cover module and flexplates for Hyundai's largest V6 engine program — Tesma's first major award from this South Korean manufacturer. Front covers are our primary strategic focus. Tesma is one of the few companies that can design, develop and manufacture most of the components that make up the front cover module. Over the next couple of years, the percentage of sales from front cover modules in the Tesma Engine Technologies group will more than double.

Just half a dozen years ago, Tesma made no water pumps. In 2003, we were the largest water pump manufacturer in North America, with annual sales of about 4.5 million units. This equates to more than 30% of all engines assembled during the year in North America. Moreover, through our Litens Automotive Partnership, we are the largest supplier of accessory drive tensioners in the world.

17%

Sales increase in 2003.

TESMA 13

| [PHOTO] | [PHOTO] | [PHOTO] |

|

Our skilled and experienced people — from press operators and tool makers to facility general managers — embrace our focus on operational efficiencies. We look to them to share their ideas for manufacturing process improvements and cost-effective solutions. |

During 2003, Ford China ordered accessory drive tensioners for its 1.3L L4 engine –opening up a new geographic market for our product. We also won the oil and water pump business for PSA's 2.2L diesel engine. While this award represents just U.S. $7 million in sales by 2007, it is a significant order from one of Europe's most successful vehicle manufacturers. In addition, we increased our oil and water pump sales to Ford of Europe by launching these products for the Lion V6 diesel engine.

Highlights for the year included major product launches. Among these were GM's HFV6 engine front cover module, DaimlerChrysler's 5.7L LX engine water pump, GM's GEN IV engine cam cover and balance shaft assemblies for GM's Line 4 and Line 5 engine programs. We also began making oil pumps for the Jaguar V8 and Lincoln LS V8 engines — shipping these pumps to plants in England and the United States. Our launch of the water pump for Honda's Accord was the first time a non-Japanese supplier has provided water pumps to this customer.

During the year, we completed the purchase of 55% of an Italian company with a manufacturing facility near Naples, Italy. This provides a domestic beachhead for our pulley business in Europe and is located close to the Fiat plants it will initially supply. Our first water pumps for Fiat from our wholly-owned subsidiary on the same site have been through the Production Parts Approval Process (PPAP) and will launch in 2004. Three new oil pumps are scheduled for launch in the next couple of years from this facility. We expect our Italian manufacturing capabilities will enhance our penetration of the European market.

In 2003, we set up our first plant in China and it will begin manufacturing automatic belt tensioners for Volkswagen in the first quarter of 2004. China represents great business potential for us. We expect that our plant will become the focal point for expanding our manufacturing and sales in the country. We also increased our presence in Asia last year by adding significant manufacturing space and increasing our testing and product development capabilities in our existing facilities in South Korea.

Important product development initiatives include electric water pumps, variable flow oil pumps, linear and rotary proportional valves and balance shaft driven oil pumps. These products have the potential to represent important new business for us going forward, based on attractive near-term market opportunities and good long-term growth potential.

Tesma's test engineering staff are instrumental in designing and specifying some of the most sophisticated test rigs, customized to the needs of each OEM and product application.

[GRAPHIC]

Tesma's new facilities located in Italy and China

14 TESMA

[PHOTO]

TESMA 15

[PHOTO]

Tesma leads the competition in its ability to select the materials and processes best suited to making a product from among a wide range of in-house choices. Our diversity of materials and manufacturing processes allows us to provide the greatest benefits in terms of cost versus function for each product application. That's how we measure success.

16 TESMA

| [PHOTO] | | [PHOTO] | | [PHOTO] | | |

SAM BOZZO |

|

DAVE PASCOE |

|

BRIAN HOYLE |

|

|

Group Vice President

Transmission Technologies |

|

Director of

Group Engineering &

Product Development

Transmission Technologies |

|

Group Controller

Transmission Technologies |

|

"Many of the people who work in product development have a manufacturing background, because Tesma is built on grassroots manufacturing. So when our people are designing products they are already thinking about the most economical way to manufacture them. At the end of the day, it's about taking cost out of the equation, not about eroding margin — while making a technically better product that can be sold at a lower price." |

|

|

|

|

|

|

CLUTCH HOUSING

FOR MAGNA STEYR |

|

|

|

|

|

|

[PHOTO] |

Tesma Transmission Technologies

Greatest Benefits

In less than a decade, Tesma Transmission Technologies has progressed from a stamper of single components to a successful supplier of value-added assemblies and modules. When Tesma became a public company in 1995, our products represented less than 1% of the North American outsourced transmission module market. Today we have 4% of the total transmission pump business in North America and 1% of the world market.

Tesma Transmission Technologies' sales increased 15% to U.S. $250 million in 2003 from U.S. $218 million in 2002.

A key to our success in 2003 was the continued ramp-up of the Ford 5R110 oil pump; essentially, an oil pump and transmission hydraulic control unit combined. With 66 components and required tolerances to within a few microns, this is the most complex assembly ever launched by Tesma. In 2004, we are ramping up from 1,200 to 2,000 assemblies daily. Nearly 80,000 individual components move along the single assembly line for this product each day.

We are gearing up our facilities by installing equipment, refining designs and conducting tests in order to fill a number of major product launches in 2004. For instance, we have installed large and complex presses to facilitate production of high tolerance components in clutch pack assemblies for ZF, a Tier 1 European-based transmission design and manufacturing company.

We were recently awarded business to supply die-cast and machined components and assemblies to GM. These parts will be used in various transmission applications for certain of their mid-size vehicles, full-size Cadillac models and heavier duty full-size pick-up trucks.

15%

Sales increase in 2003.

TESMA 17

| [PHOTO] | [PHOTO] | [PHOTO] |

|

Our technologies and facilities are second to none. We continually invest in state-of-the-art equipment to enhance our design, development, engineering, testing, program management and manufacturing capabilities. |

We are also preparing to supply flow-formed clutch housings to Magna Steyr Powertrain as part of a large multi-year contract awarded in 2003. This is significant in terms of both volume and strategy. In the past, we have focused primarily on automotive transmissions, but the Magna Steyr business enables us to apply our product capabilities to the transfer case market as well.

During 2003, we enhanced our flow-forming capability. Flow-forming is a process where precision internal splines are produced in various types of material using chipless rotational forming techniques. This manufacturing method enables us to make clutch housings as a single component.

Also, we were awarded business from GM based in part on our decision to add grobing to our broad portfolio of technologies and processes. Grobing involves the incremental forming of splines onto a stamped steel clutch housing by means of rollers forming splines onto a mandrel. This is the first use of grobing by any Tesma division on this type of product and it should create new opportunities for us to win clutch housing and other business where this process is the best application.

The acquisition of Davis in January 2004 adds three manufacturing facilities to this technology group. Davis' main product focus is stamped powertrain components and assemblies, which complements and broadens our current product offerings.

Our priorities in 2004 include expanding our clutch module business for automatic transmissions to enhance our market position. Going forward, our product development program will focus on lightweight differentials, new methods of power transmission from shaft-to-shaft and planetary carriers in each case utilizing various methods of manufacturing to best serve our customers' requirements. We are also continuing to evolve our modules and systems product line, particularly in the oil pump and transfer case areas.

Innovative, highly-engineered, complex — the Ford 5R110 transmission oil pump represents one of the most advanced products in the Tesma modular product portfolio.

Ford 5R55N transmission oil pan manufactured at Davis.

18 TESMA

[PHOTO]

TESMA 19

[PHOTO]

We offer our customers much more than design and manufacturing expertise; as important as these are. In some instances, we have test rigs with capabilities our customers can't duplicate. They come to us for testing because we can simulate a variety of unique operating conditions. Customers can then rewrite performance specifications for their products using the support we provide. That's how we measure success.

20 TESMA

| | | | | [PHOTO] | | |

|

|

|

|

PAUL MANNERS |

|

|

| | | | | Group Vice President

Fuel Technologies | | "The key message is innovation. There is no doubt that success in our business requires us to come up with better-functioning solutions that involve less cost to the customer and to Tesma. At the same time, we recognize that people drive innovation. Attracting, developing, maintaining and stimulating talent is essential to our success. Tesma hires people who can fuel the innovation process that sets us apart from the competition." |

|

|

|

|

|

|

DAIMLERCHRYSLER JR

FUEL TANK |

|

|

|

|

|

|

[PHOTO] |

Tesma Fuel Technologies

We Offer More

In just a few years, Tesma Fuel Technologies has moved rapidly up the value chain from a small parts manufacturer to a full-service fuel systems supplier. We began by producing fuel caps for the European market and now supply caps, fuel filler pipes and entire fuel tank assemblies to OEM customers in North America and Europe.

A key to this evolution was our early introduction of metal filler pipes and tanks, which reduce permeation and improve recyclability. Various U.S. states, beginning with California, have mandated lower fuel permeation rates and increased corrosion resistance on all vehicles. These standards take effect beginning in 2005. Tesma Fuel Technologies continues to work with all of our customers to develop the best technical and commercial solutions to meet these new requirements.

We launched a variety of fuel filler pipe and metal fuel tank programs in late 2002 and 2003. Key programs include fuel filler pipes for Ford, fuel filler tubes and a fuel tank for DaimlerChrysler and fuel tanks for Volkswagen and Volvo. Business awarded in 2003 included fuel filler pipes for General Motors Daewoo of South Korea — expanding our global reach into the Asian market.

Tesma Fuel Technologies' sales increased 51% to U.S. $104 million in 2003 from U.S. $64 million in 2002.

As we look to the future, we aim to continue diversifying our existing product portfolio by developing improved tank ventilation systems, capless refueling systems and universal sender unit modules.

51%

Sales increase in 2003.

TESMA 21

Policies

Corporate Constitution

Tesma's Corporate Constitution includes the following principles:

Employee Equity and Profit Participation

Ten percent of Tesma's profit before tax will be allocated to employees. These funds will be used for the purchase of Tesma shares in trust for employees and for cash distributions to employees, recognizing length of service.

Shareholder Profit Participation

Tesma will distribute, on average, not less than 20 percent of its annual net profit after tax to shareholders.

Management Profit Participation

To obtain long-term contractual commitment from senior management, Tesma provides a compensation arrangement which, in addition to a base salary below industry standards, allows for the distribution of up to six percent of its profit before tax.

Research and Development

Tesma will allocate a minimum of 7 percent of its profit before tax for research and development to ensure its long-term viability.

Social Responsibility

Tesma will allocate a maximum of 2 percent of its profit before tax for charitable, cultural, educational and political purposes to support the basic fabric of society.

Minimum Profit Performance

Management has an obligation to produce a profit. If Tesma does not generate a minimum after-tax return of 4 percent on share capital for two consecutive years, Tesma's Class A shareholders, voting as a class, will have the right to elect additional directors.

Unrelated Investments

Tesma Class A and Class B shareholders, with each class voting separately, will have the right to approve any investment in an unrelated business in the event such investment, together with all other investments in unrelated businesses, exceeds 20 percent of Tesma's equity.

Board of Directors

Tesma believes that outside directors provide independent counsel and discipline. A majority of the members of Tesma's Board of Directors will be outsiders.

Constitutional Amendments

Any change to the Corporate Constitution will require the approval of Tesma's Class A and Class B shareholders, with each class voting separately.

Employee's Charter

Tesma is committed to an operating philosophy which is based on fairness and concern for people. This philosophy is part of Tesma's Fair Enterprise culture in which employees and management share in the responsibility to ensure the success of the Company.

It includes these principles:

Job Security

Being competitive by making a better product for a better price is the best way to enhance job security. Tesma is committed to working together with its employees to help protect their job security.

To assist employees, Tesma will provide:

- •

- Job Counselling

- •

- Training

- •

- Employee Assistance Programs

A Safe and Healthful Workplace

Tesma strives to provide employees with a working environment which is safe and healthful.

Fair Treatment

Tesma offers equal opportunities based on an individual's qualifications and performance, free from discrimination or favouritism.

22 TESMA

Competitive Wages and Benefits

Tesma will provide employees with information which will enable them to compare their total compensation, including total wages and total benefits, with those earned by employees of competitors, as well as with other plants in the community. If total compensation is found not to be competitive, then wages will be adjusted.

Employee Equity and Profit Participation

Tesma believes that every employee should share in the financial success of the Company.

Communication and Information

Through regular monthly meetings between management and employees and through publications, Tesma will provide employees with information so they will know what is going on in the Company and within the industry.

The Hotline

Should an employee have a problem, or feel the above principles are not being met, Tesma encourages such employees to contact the Hotline to register their complaints. Employees do not have to give their name, but if they do, it will be held in strict confidence. Hotline Investigators will answer the call. The Hotline is committed to investigate and resolve all employee concerns or complaints and must report the outcome to Magna's Global Human Resources Department.

Employee Relations Advisory Board

The Employee Relations Advisory Board is a group of people who have proven recognition and credibility relating to humanitarian and social issues. This Board will monitor, advise and ensure that Tesma operates within the spirit of this Employee's Charter and the principles of Tesma's Corporate Constitution.

Corporate Governance

Tesma believes that effective corporate governance structures and practices help to protect the well-being of the Corporation as a whole and its stakeholders. Accordingly, Tesma has adopted a number of structures and procedures to assist in the implementation of effective corporate governance practices and permit the Board of Directors to functions independently of management. These include:

- •

- Tesma's Corporate Constitution, which attempts to strike a balance among Tesma's stakeholders — its employees, managers and investors — by specifically defining their respective rights to participate in the Corporation's profits, while at the same time imposing certain responsibilities and disciplines on management;

- •

- Tesma's Board Charter, which requires that a majority of the Board of Directors be comprised of independent directors, formalizes the Board's overall responsibility for the stewardship of Tesma and assists in defining the limits of management's responsibility;

- •

- Tesma's Audit Committee Charter, which formalizes the Audit Committee's responsibility for ensuring the integrity of Tesma's financial statements and the financial reporting process;

- •

- Tesma's Corporate Governance and Compensation Committee Charter, which invests this Committee with broad authority for the development of Tesma's system of, and overall approach to, corporate governance generally; and

- •

- Tesma's Code of Conduct, applicable equally to our directors, officers and employees, which defines the types of conduct which Tesma encourages and those which it prohibits, and establishes a system of enforcement to ensure effective implementation of the Code.

Each of the above, together with the other elements of Tesma's corporate governance structures and practices, are available for review on Tesma's website (www.tesma.com) under the heading Corporate.

TESMA 23

Review

[PHOTO]

| 25 | | Management's Discussion and Analysis |

| 44 | | Financial Results |

| | | 44 | | Management's Responsibility for Financial Reporting |

| | | 44 | | Auditors' Report |

| | | 45 | | Consolidated Financial Statements |

| | | 52 | | Notes to Consolidated Financial Statements |

| | | 80 | | Quarterly Results of Operations |

| | | 81 | | Historical Financial Summary |

| 82 | | Shareholder Information |

| 84 | | Board of Directors |

| 85 | | Officers |

| 86 | | Corporate Information |

24 TESMA

Management's Discussion and Analysis of Results of Operations and Financial Position

For the year ended December 31, 2003

Tesma International Inc. (Tesma or the Company) designs, engineers, tests and manufactures technologically-advanced powertrain (engine, transmission and fuel) components, modules and systems for the global automotive industry. Subsequent to our acquisition of Davis Industries, Inc. (Davis), we employ approximately 5,500 skilled and motivated people in 28 manufacturing facilities in North and South America, Europe and Asia, and five focused tooling, design and research and development (R&D) centres supporting our three principal product technology groups: Tesma Engine Technologies, Tesma Transmission Technologies and Tesma Fuel Technologies.

Effective December 31, 2002, we changed our fiscal year end from July to December. This change was made, in part, to enable our financial performance to be compared more readily to that of our peer group in the automotive industry. The statements of income and cash flows presented for the immediately preceding period for comparative purposes in our consolidated financial statements are for the five-month period ended December 31, 2002. However, to provide for more informative and appropriate discussion and analysis, the following management's discussion and analysis of our results of operations and financial position (MD&A) will focus on the audited results for the year ended December 31, 2003 compared to results for the unaudited year ended December 31, 2002 (as presented on page 28 of this annual report). This MD&A should be read in conjunction with the accompanying audited consolidated financial statements and notes for the year ended December 31, 2003 found on pages 44 through 79 of this annual report. All amounts reported in this MD&A are in millions of U.S. dollars unless otherwise noted.

OVERVIEW

Our strategic objective is to be the world's leading Tier 1 supplier of advanced powertrain modules and systems. Our ability to develop and manufacture individual components and to assemble them as highly-engineered modules and systems places us at the forefront of industry trends towards modularization and outsourcing. Our reputation for product quality and reliability, our strong customer relationships and our world-class development, manufacturing and testing capabilities help position us to achieve this objective.

We posted strong 2003 results, despite continued vehicle production declines and decreasing market share at our traditional North American customers. Our content per vehicle for the year increased in both of our major markets, reflecting the launch of more complex and value-added modules and systems over the latter part of the year. These launches included our first fully-integrated engine front cover module for General Motors' (GM) High Feature V6 engine, the fuel filler pipe assembly for Ford's high-volume C170 Focus program in Europe and initial ramp-up volumes of several new production programs launched in South Korea.

We completed the acquisition of Davis in early January 2004. This acquisition increases our presence in the United States, including the south, providing us with a closer presence to some of our non-traditional customers. It also improves the balance of our North American operations between Canada and the United States which, given the recent strength of the Canadian dollar, improves our overall competitiveness. The majority of Davis' current product base complements our existing transmission product offerings and other stamped components. Given Davis' existing strong relationships with Ford, Honda and Nissan, we see the opportunity to expand and strengthen our relationships with these customers and offer our broader and more technologically-advanced transmission and engine modules and systems to them.

We also made additional strategic investments in foreign markets during 2003. First, we completed a transaction to acquire a 55% interest in an Italian company which will produce pulleys and other engine components for European customers. We intend to capitalize on this additional presence in Europe with the launch of new production business in the near term (including water pump assemblies) and, over the longer term, as we pursue our objective of increasing the penetration of our more complex modules and systems across the European market. Additionally, we have entered the Chinese market with a moderate investment in a new plant to establish limited production capability. We view China as a market with strong growth potential; however, our initial focus will be to support the operations of some of our current customers that have set up production facilities in China. Through this initial step, we intend to gain valuable insight and experience in operating in China and ultimately reduce risk as we plan for additional investments in this developing automotive market. Our newly established presence will put us in a better position to capitalize on future opportunities that are likely to evolve.

Our content per vehicle increased in both of our major markets as we launched more complex, value-added modules and systems.

We made strategic investments beyond our domestic market through acquisitions and plant start-ups in the United States, Italy and China.

TESMA 25

As previously reported, our future business growth looks strong with the awards of new business during the latter part of the year from some of our traditional customers (new assemblies for DaimlerChrysler and for GM, in particular the engine front cover module, water pump and oil pan for GM's new 3.9L engine used in their higher volume midsize car platforms) and non-traditional customers (including water pumps and oil pumps for the PSA Group, other assemblies for Land Rover, as well as the selection of our South Korean facility by Hyundai Motor Company to supply front cover modules for a new V6 engine program to be produced in both Korea and North America). Our future growth was further solidified by some recent awards of significant business including cam covers for GM's Line 4, 5 and 6 engine programs (which are installed in their mid-size SUV and pick-up truck platforms) and takeover volumes to supply several die-cast and machined components and assemblies that are currently installed into GM's 4T65E, 4T80E and 4L80 transmissions (which are assembled into certain of their mid-size vehicles, full-size Cadillac models and heavier duty full-size pick-up trucks, respectively). This organic growth, combined with the acquired Davis business, provides a solid base for us to continue our track record of growth.

Although we funded a significant portion of the Davis acquisition from our existing cash balances, our financial position continues to be very strong. Our considerable cash reserves that remain will enable us to capitalize on new business opportunities and we continue to look for other potential acquisition targets that, like Davis, will add both growth and profitability, at a reasonable price, and will ultimately increase shareholder value.

As previously communicated, we undertook an evaluation of the viability of our German die-casting operations (Eralmetall) and potential initiatives that could help improve its operating performance. This evaluation was completed during the fourth quarter of 2003. Over the past eighteen months, Eralmetall's new management team has worked hard to improve production and eliminate waste, our employees have agreed to assist in achieving targeted savings and our customers have expressed a willingness to discuss alternatives to support this operation. Although still not meeting our financial expectations, the decision was made to continue operating Eralmetall as a going concern in support of our customers, as doing so is not expected to significantly affect our overall results. We will continue to closely monitor the results of this operation and evaluate its future prospects should results deteriorate.

ACQUISITION OF DAVIS INDUSTRIES, INC.

Subsequent to our year-end, on January 2, 2004, we completed the acquisition of Davis. Through this acquisition, we added over 700 employees and 3 manufacturing facilities located in Indiana (2 facilities) and Tennessee to our North American manufacturing operations. Davis' main product focus is stamped powertrain components and assemblies, including driveplate assemblies, transmission shells and oil pan assemblies and engine valve covers, but also includes some body and chassis stampings and fuel filler door assemblies. For their most recently completed fiscal year ended September 30, 2003, Davis reported sales of approximately $129 million.

The total consideration for the acquisition of all the outstanding shares of Davis amounted to approximately $75.0 million, consisting of $45.1 million paid in cash (including transaction costs), the assumption of $22.0 million of long-term debt, $4.5 million of other long-term obligations and the issuance of a $3.4 million five-year note payable bearing interest at the rate of prime plus 1% per annum (see Note 24(a) of the accompanying audited consolidated financial statements and notes thereto).

OTHER ACQUISITION

In October 2003, we completed the acquisition of a 55% interest in Agla Benevento S.r.l. of Benevento, Italy (subsequently renamed Tesma-Agla S.r.l. (Tesma-Agla)), for cash consideration, including transaction costs, of $1.2 million (net of cash acquired of $0.2 million). The transaction was accounted for under the purchase method of accounting and the initial impact on our consolidated balance sheet was an increase in non-cash working capital of $0.4 million, property, plant, equipment and other long-lived assets of $2.6 million, assumed debt of $2.0 million and net future tax assets of $0.2 million.

Our future growth will be driven by new business awards and acquisitions.

26 TESMA

Pursuant to agreements executed upon the closing of the transaction, the approval of certain strategic, operating and financing decisions of this company are subject to a majority vote by Tesma-Agla's Board of Directors. The Board of Directors consists of four members, of which we are entitled to appoint two (including the Chairman of the Board). We account for our interest in this jointly-controlled entity using the proportionate consolidation method. Tesma-Agla had no operating activities prior to October 2003, but was preparing for the launch of pulleys and other engine components for the European market.

ACCOUNTING CHANGES

Reporting Currency

Effective January 1, 2003, we implemented the previously announced change in our financial reporting currency from the Canadian dollar to the United States dollar (U.S. dollar). This change enables our financial performance to be compared more readily to that of our peer group in the global automotive industry. We implemented this change in accordance with Canadian generally accepted accounting principles (CDN GAAP) and consistent with the requirements under accounting principles generally accepted in the United States (U.S. GAAP). In accordance with these rules, comparative amounts have been restated in U.S. dollars using the current rate method, whereby all revenues, expenses and cash flows are translated at the average exchange rates that were in effect during these periods and all assets and liabilities are translated at the closing rate in effect at the end of these periods. Utilizing this method, the comparative unaudited consolidated statements of income and cash flows for the year ended December 31, 2002, as presented and discussed in this MD&A, were translated into U.S. dollars using an average rate for the year of U.S. $0.6372 per CDN $1.00. The comparative consolidated balance sheet at December 31, 2002 was translated into U.S. dollars using the prevailing rate at December 31, 2002 of U.S. $0.6376 per CDN $1.00.

Stock-Based Compensation

In September 2003, the Canadian Institute of Chartered Accountants (CICA) issued amendments to Handbook Section 3870, "Stock-Based Compensation and other Stock-Based Payments" (CICA 3870) which are effective for fiscal years beginning on or after January 1, 2004. The amended standard now requires recognition of all stock-based compensation transactions at fair value and eliminates the alternative of using the intrinsic value method of accounting with fair value disclosures provided on a pro forma basis. We have elected to adopt these amendments early and to apply them on a retroactive basis to stock-based awards granted on or after August 1, 2002, the date we were initially required to adopt CICA 3870. Upon application of the new rules, we recorded compensation expense totaling $0.5 million and $0.1 million in the years ended December 31, 2003 and 2002, respectively. Diluted earnings per share for these same periods decreased by $0.01 and $nil, respectively, as a result of the adoption of these rules.

Compensation expense to be recognized is determined by first calculating the total estimated fair value of each tranche of stock options as at the date of grant and then recording compensation expense, on an amortized basis, over the applicable vesting periods of the underlying stock options. As such, at each reporting date, cumulative compensation expense will be recognized for each tranche of stock options to the extent that they are vested as at that date. Compensation expense recognized is recorded as part of selling, general and administrative expense, with a corresponding increase to contributed surplus. As the underlying stock options issued on or after August 1, 2002 are exercised, a portion of the accumulated balance in contributed surplus is transferred systematically to the Class A Subordinate Voting Shares issued and reflected as additional proceeds received on these exercises.

REPORTING CURRENCY

The currency in which a company discloses its financial information including its financial statements. Tesma's reporting currency is the U.S. dollar. All of Tesma's divisions with functional currencies other than the U.S. dollar have their financial results converted to U.S. dollars for reporting purposes.

TESMA 27

RESULTS OF OPERATIONS

The Company's comparative consolidated operating results for the years ended December 31, 2003 and 2002 are as follows:

| | 2003

| | 2002

|

|---|

(U.S. dollars in thousands, except per share and share figures)

| | (audited)

| | (unaudited)

|

|---|

| Sales | | $ | 1,098,591 | | $ | 925,921 |

| | |

| |

|

| Cost of goods sold | | | 855,503 | | | 718,136 |

| Selling, general and administrative | | | 69,204 | | | 59,833 |

| Depreciation and amortization | | | 51,609 | | | 40,536 |

| Affiliation and social fees | | | 12,449 | | | 10,404 |

| Interest (income) expense, net | | | (204 | ) | | 1,987 |

| Impairment loss at German die-casting subsidiary | | | — | | | 12,088 |

| | |

| |

|

| Income before income taxes | | | 110,030 | | | 82,937 |

| Income taxes | | | 35,918 | | | 26,978 |

| | |

| |

|

| Net income attributable to Class A Subordinate Voting Shares and Class B Shares | | $ | 74,112 | | $ | 55,959 |

| | |

| |

|

| Earnings per Class A Subordinate Voting Share or Class B Share | | | | | | |

| | Basic | | $ | 2.29 | | $ | 1.82 |

| | Diluted | | $ | 2.28 | | $ | 1.80 |

| | |

| |

|

Average number of Class A Subordinate Voting Shares and Class B Shares

outstanding (in thousands) | | | | | | |

| | Basic | | | 32,344 | | | 30,725 |

| | Diluted | | | 32,531 | | | 31,057 |

| | |

| |

|

Impairment Loss at German Die-Casting Subsidiary

Our comparative results for the year ended December 31, 2002 were significantly affected by an impairment loss booked in 2002 at Eralmetall, our German die-casting subsidiary. Initially prompted by a history of operating losses and projected future losses following the launch of new business at Eralmetall, we initiated and completed a review for impairment on $20.6 million of machinery, equipment, land, buildings and other long-lived assets at this subsidiary. As a result of this review, an impairment loss of $12.1 million ($8.5 million after applicable taxes) was recorded as an operating expense in the year ended December 31, 2002. The impact of this loss on diluted earnings per share for the year ended December 31, 2002 was $0.27.

Foreign Currency Exchange Rates

As substantially all of our operations have functional currencies other than the U.S. dollar, our reported results in U.S. dollars can be affected by movements in the exchange rates of the Canadian dollar, euro, Swiss franc and Korean won, all relative to the U.S. dollar. The magnitude of the impact of foreign exchange on our results in periods presented will primarily depend on, and vary directly with, the size of fluctuations, relative to the U.S. dollar, of the underlying functional currencies in our Canadian, European and South Korean-based operations.

The average exchange rates for our most significant functional currencies relative to the U.S. dollar during the years ended December 31 were as follows:

| | 2003

| | 2002

| | %

|

|---|

| Canadian dollar | | 0.7159 | | 0.6372 | | +12% |

| Euro | | 1.1320 | | 0.9456 | | +20% |

| Korean won | | 0.000840 | | 0.000804 | | +4% |

| | |

| |

| |

|

The impact of the strengthening of foreign currencies relative to the U.S. dollar, in particular strong gains by the Canadian dollar and euro, increased sales by approximately $125 million or 72% of our overall growth in 2003. Similarly, the strengthening of these functional currencies significantly affected all other line items on our income statement, the extent of which will be specifically addressed in each of the respective discussions that follow.

FUNCTIONAL CURRENCY

The currency in which each entity transacts its business. For example, a subsidiary located in Germany uses the euro as its functional currency, and pays its employees and purchases the majority of its materials in its functional currency.

FOREIGN CURRENCY TRANSLATION

When divisional functional currency results are converted to Tesma's reporting currency (U.S. dollars), the results are converted at the average foreign exchange rate for the period.

28 TESMA

The exchange rates in effect as at the end of the years ended December 31 were as follows:

| | 2003

| | 2002

| | %

|

|---|

| Canadian dollar | | 0.7752 | | 0.6376 | | +22% |

| Euro | | 1.2591 | | 1.0411 | | +21% |

| Korean won | | 0.000836 | | 0.000835 | | unch. |

| | |

| |

| |

|

Vehicle Production Volumes

| |

| |

| | Change

|

|---|

| | 2003

| | 2002

| | Units

| | %

|

|---|

(in millions of units)

| |

| |

| |

| |

|

|---|

| North America | | 15.9 | | 16.3 | | (0.4 | ) | -3% |

| Europe | | 16.4 | | 16.3 | | 0.1 | | +1% |

| | |

| |

| |

| |

|

North American vehicle production volumes, as historically reported by us, included medium and heavy trucks. To conform our reporting with most of our industry peers, effective January 1, 2003, we changed our reporting basis to include light vehicles only. All comparative North American vehicle production and content per vehicle amounts have been restated to conform with this new presentation. On this basis, North American vehicle production volumes for the year were 15.9 million units, a 3% decrease from the 16.3 million units produced in the prior year. In 2003, North America's "Big Three" (General Motors, Ford and DaimlerChrysler) Original Equipment Manufacturers (OEMs) continued to offer record levels of attractive financing rates and other consumer incentive campaigns to spur demand and maintain market share. However, the use of these incentive campaigns was unsuccessful in the aggregate as the "Big Three" experienced production declines ranging from 3% to 9% in 2003. As a result, their production share declined largely to the benefit of the New Domestic OEMs (mainly Toyota, Honda and Nissan) which experienced production volume increases ranging from 8% to 11% during the year.

In Europe, vehicle production volumes were 16.4 million, up 1% from last year. However, some of our larger customers, namely DaimlerChrysler and Fiat, experienced production declines of 3% and 16%, respectively, during the year.

Average Content per Vehicle

Average content per vehicle is a measure commonly used in the automotive supply industry to measure a company's growth, penetration and success, excluding the impact of fluctuations in vehicle production levels. Continued growth in content per vehicle indicates success in introducing products onto new programs (primarily engine and transmission) or vehicle platforms, and/or expanded sales on existing programs (i.e. if more vehicle platforms are added to a particular engine program, or if strong demand for certain vehicle platforms, such as SUVs, is driving increased engine production on which we have significant content). Industry analysts use content per vehicle to assess our performance and growth in our two major markets, North America and Europe. This measure is calculated by dividing our production sales to North American and European customers, respectively, by the industry's North American and European total light vehicle production volumes, respectively. Although this measure does indicate growth, management does not place significant emphasis on this measure to assess performance as it has certain shortcomings. The majority of our products are shipped to OEM engine and transmission facilities, not vehicle assembly plants. Many engine and transmission programs are produced in a single facility, and then shipped to many global assembly facilities. As a result, the number of engine and transmissions produced in each major region in which we operate can differ materially from the number of vehicles assembled. Unfortunately, the availability of accurate data for engine and transmission production in each of our three key markets does not currently exist on a timely basis. Therefore, we cannot use an alternative measure to present content information on a timely basis.

Our average content per vehicle for the years ended December 31 was as follows:

| | 2003

| | 2002

| | %

|

|---|

| North America | | $43.95 | | $36.87 | | +19% |

| Europe | | € 16.28 | | € 14.90 | | +9% |

| | |

| |

| |

|

TESMA 29

Sales

| | 2003

| | 2002

| | Change

|

|---|

(in millions)

| |

| |

| |

|

|---|

| North America | | $ | 856.0 | | $ | 725.5 | | +18% |

| Europe | | | 235.6 | | | 180.6 | | +30% |

| Other Automotive | | | 28.8 | | | 33.8 | | -15% |

| Intersegment | | | (21.8 | ) | | (14.0 | ) | |

| | |

| |

| |

|

| Total external sales | | $ | 1,098.6 | | $ | 925.9 | | +19% |

| | |

| |

| |

|

Consolidated sales in 2003 increased 19% from 2002 to $1.1 billion. North American sales rose 18%, while sales increased 30% in our European operations. Our strong growth in North America occurred despite the 3% decrease in North American vehicle production volumes and even larger declines experienced by our largest customers. In Europe, our growth was fueled by the launch of new business, as vehicle production levels increased only slightly over the prior year.

North American Operations

During 2003, our North American operations consisted of 15 manufacturing facilities (13 in Canada and 2 in the United States) employing 3,600 employees. These operations reported sales of $856.0 million for the year, up 18% from $725.5 million in the prior year. The stronger Canadian dollar accounted for approximately $85 million or 65% of this growth. The remaining increase of approximately $45 million represents true native currency growth of 6%, and, as discussed above, was realized despite the 3% to 9% production declines at our largest customers. Our growth was fueled by increases in our average content per vehicle, which grew 19% to $43.95 for the year from $36.87 for 2002. The true native currency growth in 2003 reflects new program launches and higher volumes on production ramp-ups of other recently launched programs.

The new launches include a complex integrated front cover module for the GM High Feature V6 engine, balance shaft assemblies for GM's Line 4 and Line 5 engine programs, water pumps, camshaft phasers and housings for GM's Premium V8 engine, and fuel filler pipe assemblies for DaimlerChrysler's JR car and HB truck programs. We were not able to realize the full benefit of these launches, however, as many of them occurred in the second half of the year at lower than expected levels.

Significant programs on which we achieved higher volumes included the following:

- •

- the complex oil pump assembly and other components supplied for Ford's 5R110 transmission used in the diesel engine application of Ford's heavier duty F-Series trucks;

- •

- front covers with an integrated oil pump, oil pan, thermostat housing and crossover tube and other components for GM's L850 4-cylinder engine program used in some of GM's high volume vehicle platforms (including the Chevrolet Cavalier and Malibu, Pontiac Sunfire and Grand Am and Saturn Ion and VUE models);

- •