UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT

PURSUANT TO SECTIONS 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2005

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to to

Commission file number 001-13828

MEMC Electronic Materials, Inc.

(Exact name of registrant as specified in its charter)

| | |

| Delaware | | 56-1505767 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| |

501 Pearl Drive (City of O’Fallon) St. Peters, Missouri | | 63376 |

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code:

(636) 474-5000

Securities registered pursuant to Section 12(b) of the Act:

| | |

Title of Each Class

| | Name of Each Exchange on Which Registered:

|

| $.01 Par Value Common Stock | | New York Stock Exchange |

Securities Registered Pursuant to Section 12(g) of the Act:

None

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ¨ No x

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer. See the definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the voting stock held by nonaffiliates of the registrant, based upon the closing price of such stock on June 30, 2005 of $15.77, as reported by the New York Stock Exchange, and 209,323,066 shares outstanding on such date, was approximately $2,096,304,097. The number of shares outstanding of the registrant’s Common Stock as of June 30, 2006, was 222,023,958 shares.

DOCUMENTS INCORPORATED BY REFERENCE

1. Portions of the registrant’s 2005 Annual Report to Stockholders (Part I and Part II)

PART I

Overview

We are a leading worldwide producer of wafers for the semiconductor industry. We are one of four wafer suppliers having more than a 10% share of the overall market. We operate manufacturing facilities in every major semiconductor manufacturing region throughout the world, including Europe, Japan, Malaysia, South Korea, Taiwan and the United States. Our customers include virtually all of the major semiconductor device manufacturers in the world, including the major memory, microprocessor and applications specific integrated circuit, or ASIC, manufacturers, as well as the world’s largest foundries. We provide wafers in sizes ranging from 100 millimeters (4 inch) to 300 millimeters (12 inch) and in three general categories: prime polished, epitaxial and test/monitor. A prime polished wafer is a highly refined, pure wafer with an ultra-flat and ultra-clean surface. An epitaxial wafer consists of a thin, silicon layer grown on the polished surface of the wafer. A test/monitor wafer is substantially the same as a prime polished wafer, but with some less rigorous specifications.

We were formed in 1984 as a Delaware corporation and completed our initial public stock offering in 1995. Our corporate structure includes, in addition to our wholly owned subsidiaries, an 80%-owned consolidated joint venture in South Korea (MEMC Korea Company or MKC). In February 2004, we acquired approximately 100% ownership of Taisil Electronic Materials Corporation (Taisil) in Taiwan. Prior to February 2004, Taisil was a 45%-owned unconsolidated joint venture. In addition, in August 2004, we acquired 100% ownership of MEMC Southwest Inc. in Sherman, Texas. Prior to August 2004, MEMC Southwest Inc. was an 80%-owned consolidated joint venture.

On November 13, 2001, an investor group led by Texas Pacific Group and including TPG Wafer Holdings LLC and funds managed by Leonard Green & Partners, L.P. and TCW/Crescent Mezzanine Management LLC (collectively, TPG) acquired beneficial ownership of approximately 72% of our outstanding common stock and approximately $910 million of our debt from E.ON AG. All of the debt acquired by TPG from E.ON has been restructured or repaid. As part of the restructuring, TPG received shares of our Series A Cumulative Convertible Preferred Stock. On July 10, 2002, TPG converted all of the outstanding shares of Series A Cumulative Convertible Preferred Stock and the related accumulated but unpaid dividends into 125,010,556 shares of MEMC common stock. TPG sold approximately 15 million, 34 million, 66 million and 18 million shares of our common stock in public offerings in May 2003, February 2004, February 2005 and August 2005, respectively. TPG currently beneficially owns approximately 25% of our outstanding common stock.

In 2005, we were engaged in one reportable industry segment—the design, manufacture and sale of silicon wafers. Financial information regarding this industry segment is contained in our 2005 Annual Report, which information is incorporated herein by reference.

Industry Background

Almost all semiconductors are manufactured from wafers, and thus the performance of the wafer industry is highly correlated to the unit shipments of the semiconductor device industry. The worldwide semiconductor device industry grew at a compound annual growth rate of 10% from 73 billion units in 1985 to 456 billion units in 2005, according to SIA & WSTS. In 2005, semiconductor device units increased 5% from 2004, according to SIA & WSTS.

The silicon wafer industry grew at a compound annual growth rate of 9% from 1,118 million square inches in 1985 to 6,645 million square inches in 2005, according to SIA/SEMI. In 2005, silicon wafer volumes grew 6.1%, according to SEMI.

The fabrication of semiconductor devices requires a large number of complex and repetitive processing steps to layer different materials and imprint various features on a single wafer. Wafers are becoming

1

increasingly differentiated by specific physical and electrical characteristics such as flatness, silicon purity and uniform crystal structures. As markets for semiconductor devices continue to evolve and become more specialized, we believe device manufacturers recognize the enhanced role that wafers and other materials play in improving device performance and reducing their production costs.

Semiconductor device manufacturers continue to move towards devices with shrinking device geometries (i.e., the distance between the electrical contacts on the device) and more stringent technical specifications. The wafers required to produce these next-generation devices are being developed in larger diameters. Thus, semiconductor device manufacturers continue to move to larger diameter wafers, with the 200 millimeter wafer being the primary wafer used today.

Over the past decade, we believe the wafer industry has consolidated, with only four suppliers now having more than a 10% share of the overall market. We believe this change in the competitive landscape is causing segmentation between larger and smaller producers with larger manufacturers gaining an increasing share of the overall wafer market. Semiconductor device manufacturers seek suppliers with whom they can better align wafer technology development with their own product development efforts. We believe these manufacturers will continue to select wafer suppliers that offer advanced technological capabilities, a broad product portfolio and superior service to satisfy their exacting device requirements.

Products

We offer wafers with a wide variety of features satisfying numerous product specifications to meet our customers’ exacting requirements. Our wafers vary in diameter, surface features, composition, purity levels, crystal properties and electrical properties. We provide our customers with a reliable supply of high quality wafers with consistent characteristics. These wafers range from 100 millimeter to 300 millimeter in diameter. Our wafers are used as a starting material for the manufacture of various types of semiconductor devices, including microprocessor, memory, logic and power devices. In turn, these semiconductor devices are used in computers, cellular phones and other mobile electronic devices, automobiles and other consumer and industrial products.

We continue to advance our products’ capabilities. In addition to other new product offerings, we offer wafers with the Magic Denuded Zone®, or MDZ®, product feature. As compared to traditional techniques, this patented product feature can increase our customers’ yields in both prime polished and epitaxial wafers by drawing impurities away from the surface of the wafer in a manner that is efficient and reliable, with results that are reproducible.

Our products include three general categories of wafers:

Prime Polished Wafers

Our prime polished wafer is a highly refined, pure wafer with an ultraflat and ultraclean surface. Our prime polished wafers are manufactured with a sophisticated chemical-mechanical polishing process that removes defects and leaves an extremely smooth surface. As devices become more complex, wafer flatness and cleanliness requirements, along with crystal perfection, become increasingly important because these properties have a significant impact on our customers’ processes and yields.

Our OPTIA™ wafer is a 100% defect-free crystalline structure based on our patented technologies and processes, including MDZ®. We believe the OPTIA™ wafer is the most technically advanced polished wafer available today.

Our annealed wafer is a prime polished wafer with near surface crystalline defects dissolved during a high-temperature thermal treatment.

2

Epitaxial Wafers

Our epitaxial, or EPI, wafers consist of a thin silicon layer grown on the polished surface of the wafer. Typically, the epitaxial layer has different electrical properties from the underlying wafer. This provides our customers with better isolation between circuit elements than a polished wafer, and the ability to tailor the wafer to the specific demands of the device. Without sufficient isolation of the various circuit elements, the elements could communicate electrically with each other, which could render the device useless. Epitaxial wafers provide improved isolation, thereby allowing for increased reliability of the finished semiconductor device and greater efficiencies during the semiconductor manufacturing process, which ultimately allows for more complex semiconductor devices.

Our AEGIS™ product is designed for certain specialized applications requiring high resistivity epitaxial wafers and our MDZ® product feature. The AEGIS™ wafer includes a thin epitaxial layer grown on a standard starting wafer. The AEGIS™ wafer’s thin epitaxial layer eliminates harmful defects on the surface of the wafer, thereby allowing device manufacturers to increase yields and improve process reliability.

Test/Monitor Wafers

We supply test/monitor wafers to our customers for their use in testing semiconductor fabrication lines and processes. Although test/monitor wafers are substantially the same as prime polished wafers with respect to cleanliness, and in some cases flatness, other specifications are generally less rigorous. This allows us to produce some of the test/monitor wafers from the portion of the silicon ingot that does not meet customer specifications for wafers to be used in the manufacture of semiconductors.

Sales, Marketing and Customers

We market our products primarily through a global direct sales force. We have customer service and support centers globally, including in China, France, Germany, Italy, Japan, Malaysia, South Korea, Taiwan and the United States. A key element of our marketing strategy is establishing and maintaining close relationships with our customers. We accomplish this through multi-functional teams of technical, sales and marketing, and manufacturing personnel. These teams work closely with our customers to continually optimize our products for their production processes in their current and future facilities. We monitor changing customer needs and target our research and development and manufacturing to produce wafers adapted to each customer’s process and requirements. We complete sales principally through agreements of one year or less (such agreements often are of three months or six months duration), which agreements specify price and typically indicate only expected volumes or market share.

We sell our products to virtually all major semiconductor device manufacturers, including the major memory, microprocessor and ASIC manufacturers, as well as the world’s largest foundries. Samsung accounted for more than 10% of our sales in 2005. No other customer represented 10% or more of our 2005 sales.

We sell our products to certain customers under consignment arrangements. Generally, these consignment arrangements require us to maintain a certain quantity of product in inventory at the customer’s facility or at a storage facility designated by the customer. Under these arrangements, we ship the wafers to the storage facility, but do not charge the customer or recognize revenue for those wafers until title passes to the customer. Title passes when the customer pulls the product from the assigned MEMC storage facility or storage area or, if the customer does not pull the product within a stated period of time (generally 60–90 days), at the end of that period, or when the customer otherwise agrees to take title to the product. Until that time, the wafers are considered part of MEMC’s inventory and are reflected on MEMC’s books and records as inventory. As such, these consignment arrangements are essentially inventory transfer arrangements. At December 31, 2005, we had approximately $18 million of inventory held on consignment.

Manufacturing

To meet our customers’ needs worldwide, we have established a global manufacturing network consisting of nine manufacturing facilities.

3

Our wafer manufacturing process begins with high purity semiconductor grade polysilicon. The polysilicon is melted in a quartz crucible along with minute amounts of electrically active elements such as arsenic, boron, phosphorous or antimony. We then lower a silicon seed crystal into the melt and slowly extract it from the melt. The resultant body of silicon is called an ingot. The temperature of the melt, speed of extraction and rotation of the crucible govern the diameter of the ingot, while the concentration of the electrically active element in the melt governs the electrical properties of the wafers to be made from the ingot. This is a complex, proprietary process requiring many control features on the crystal-growing equipment.

We then grind the ingots to the specified diameter and slice the ingots into thin wafers. Next, we prepare the wafers for surface polishing with a multi-step process using precision wafer planarization machines, edge contour machines and chemical etchers. Final polishing and cleaning processes give the wafers the clean and ultraflat mirror polished surfaces required for the fabrication of semiconductor devices. We further process some of our products into epitaxial wafers by utilizing a chemical vapor deposition process to deposit a single crystal silicon layer on the polished surface.

In certain of our manufacturing facilities we have fully integrated manufacturing capabilities that encompass the full range of wafer manufacturing process steps, including ingot growth, wafer slicing, wafer polishing and epitaxial deposition. We conduct certain of our processes in state-of-the-art cleanroom environments.

Raw Materials

We obtain our requirements for several raw materials, equipment, parts and supplies from sole suppliers. The main raw material in our production process is polysilicon. We use two types of polysilicon: granular polysilicon and chunk polysilicon. We produce all of our requirements for granular polysilicon at our facility in Pasadena, Texas. We do not believe there are other sources of semiconductor grade granular polysilicon. We produce chunk polysilicon in our Merano, Italy facility. Chunk polysilicon can be substituted for granular polysilicon, although our manufacturing throughput and yields could be adversely affected. We believe our ability to meet the majority of our polysilicon requirements through our in-house capabilities provides us with a key cost advantage to compete more effectively in the wafer industry. We have previously announced our plans to expand our polysilicon production capacity over the next few years. We sell some polysilicon to third parties and we also buy some polysilicon on the open market.

Research and Development

The wafer market is characterized by continuous technological development and product innovation. We believe that continued and timely development of new products and enhancements to existing products are necessary to maintain our competitive position. Our goal in research and development is to maintain a close working relationship with our customers to continually develop new products and refine existing products to meet the needs of the marketplace. Our research and development model combines engineering innovation with specific commercialization strategies. Our model closely aligns our technology efforts with our customers’ requirements. We accomplish this through a better understanding of our customers’ technology requirements and through targeted research and development projects aimed at developing products to meet those technology requirements. Some of these projects involve formal and informal joint development efforts with our customers.

In addition, in order to strengthen our customer relationships and interaction and to better target our research and development efforts, we assign research and development engineers to key customers worldwide. We do this through our Applications Engineering Group, in our laboratories located in the United States, Italy, Japan and South Korea, as well as field and resident engineers located at strategic locations throughout the world. The primary purpose of the Applications Engineering Group is to establish a close, technical working relationship with our customers to obtain a better knowledge of our customers’ material requirements.

We devote a portion of our research and development resources to enhance our position in the crystal technology area. We have dedicated engineers and scientists, located in our St. Peters, Missouri, Merano, Italy

4

and Chonan, South Korea facilities, to further our understanding of defect control, cost reduction and the use of granular polysilicon. In conjunction with these efforts, we are developing wafering technologies to meet advanced flatness and particle requirements of our customers. In addition, we continue to focus on the development of our advanced epitaxial wafer technology with a dedicated staff of scientists located primarily in our St. Peters, Missouri, Novara, Italy and Utsunomiya, Japan facilities, who focus on the development of new epitaxial wafer products and cost reduction processes.

In addition to our focus on advancements in wafer material properties, we also continue to invest in research and development associated with larger wafer diameters. We produced our first 300 millimeter diameter wafer in 1991 and continue to enhance our 300 millimeter technology program using our staff of research and development scientists, engineers and technicians located primarily in our St. Peters, Missouri and Utsunomiya, Japan facilities. In addition, we continue to focus on process design advancements to drive cost reductions and productivity improvements.

We have also entered into a license agreement for certain layer-transfer wafer technology and we are in the process of establishing production capability for 200 millimeter and 300 millimeter silicon-on-insulator (SOI) wafers using a dedicated group of engineers and scientists located in our St. Peters, Missouri facility.

Competition

The market for wafers is highly competitive. We compete in all the major semiconductor-producing regions of the world and face intense competition from established manufacturers. We estimate there are six major competitors in our industry; however, our major competitors are Shin-Etsu Handotai, SUMCO and Siltronic. Some of our competitors have substantial financial, technical, engineering and manufacturing resources. Our wafers compete with wafers manufactured by others on the basis of product quality, consistency, price, technical innovation, customer service and product availability. We believe we are competitive on the basis of these factors.

Proprietary Information and Intellectual Property

We believe that the success of our business depends in part on our proprietary technology, information, processes and know how. We try to protect our intellectual property rights based on patents and trade secrets as part of our ongoing research, development and manufacturing activities. As of December 31, 2005, we owned of record or beneficially approximately 232 U.S. patents, of which approximately 19 will expire by 2010, approximately 44 will expire between 2011 and 2015 and approximately 169 will expire after 2015. As of December 31, 2005, we owned of record or beneficially approximately 365 foreign patents, of which approximately 53 will expire by 2010, approximately 33 will expire between 2011 and 2015 and approximately 279 will expire after 2015. These foreign patents are generally counterparts of our U.S. patents. As of December 31, 2005, we had approximately 50 pending U.S. patent applications and approximately 317 pending foreign patent applications. The patents we beneficially own relate to polysilicon technology. We exclusively licensed these patents from Albemarle Corporation in connection with our purchase of Albemarle’s granular polysilicon business. We may request that these patents be assigned to us at any time in exchange for a nominal purchase price.

We have agreed to indemnify some of our customers against claims of infringement of the intellectual property rights of others in our sales contracts with these customers. Historically, we have not paid any claims under these indemnification obligations and we do not have any pending indemnification claims.

Employees

At December 31, 2005, we had approximately 5,000 full time employees and 500 temporary workers worldwide. We have approximately 1,500 unionized employees in our St. Peters, Missouri, Pasadena, Texas,

5

South Korea and Italy facilities. We have not experienced any material work stoppages at any of our facilities due to labor union activities during the last several years.

Geographic Information

Information regarding our foreign and domestic operations is contained in Note 20, “Geographic Segments”, of Notes to Consolidated Financial Statements included in our 2005 Annual Report, which information is incorporated herein by reference.

Available Information

We make available free of charge through our website (http://www.memc.com) reports we file with the SEC, including our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as soon as reasonably practical after we electronically file such material with, or furnish it to, the SEC.

This Annual Report on Form 10-K contains “forward-looking” statements within the meaning of the Private Securities Litigation Reform Act of 1995, including those set forth under “Item 1. Business” and “Item 3. Legal Proceedings” and those incorporated herein by reference from our 2005 Annual Report. In addition to the business risks and uncertainties discussed elsewhere in this Form 10-K, the following are important risk factors which could cause actual results and events to differ materially from those contained in any forward-looking statement made by us.

Our business depends on the semiconductor device industry and if that industry experiences future downturns, our sales could decrease and we could be forced to reduce our prices while maintaining fixed costs, all of which could have significant negative effects on our operating results and financial condition.

Our business depends in large part upon the market demand for our customers’ semiconductors and products utilizing semiconductors. The semiconductor device industry experiences:

| | • | | rapid technological change; |

| | • | | changes in product mix; |

| | • | | fluctuations in product supply and demand |

From time to time, the semiconductor device industry has experienced significant downturns. These downturns often occur in connection with declines in general economic conditions. Some of these downturns have lasted for more than a year and have resulted in a substantial decrease in demand for our products. For example, in 2001, the semiconductor industry experienced a significant downturn as a result of weakened demand and a broad-based inventory correction. The 2001 downturn continued into early 2003. In the second half of 2004, much of the semiconductor industry experienced a downturn related to product oversupply and a resulting inventory correction. These industry conditions continued into 2005, before improving in the second half of 2005. If the semiconductor device industry experiences future downturns, we will face pressure to reduce prices and we may need to further rationalize capacity and reduce fixed costs. At the same time, our ability to reduce expenditures for capital, research and development and global infrastructure during an industry downturn is limited because of the need to maintain our competitive position. If we are unable to reduce our expenses sufficiently to offset reductions in price and volume, our operating results and financial condition could be materially adversely affected.

6

Our dependence on single and limited source suppliers could require us to obtain new qualifications from customers and adversely affect our manufacturing throughput and yield.

We obtain several raw materials, equipment, parts and supplies from sole suppliers. Likewise, we obtain all of our requirements for granular polysilicon from our facility in Pasadena, Texas. In the case of granular polysilicon, we believe that we could substitute chunk polysilicon for granular polysilicon. In either case, however, it may take us several months to transition to a new supplier and we may be required to obtain new qualifications from our customers in order to change or substitute materials or sources of supply. We cannot predict whether we would be successful or how long the qualification process would take. In addition, our manufacturing process could be interrupted and our manufacturing throughput and yields could be adversely affected. A failure to obtain a new qualification or a decrease in our manufacturing throughput or yields could have a material adverse effect on our operating results.

From time to time we have experienced limited supplies of certain raw materials, equipment, parts and supplies, particularly polysilicon. Because of the cyclical nature of our industry, we may experience shortages of our key raw materials, equipment, parts and supplies in the future. A prolonged inability to obtain raw materials, equipment, parts or supplies, or increases in prices resulting from these shortages could have a material adverse effect on our operating results.

The success of our currently planned expansion of polysilicon capacity and penetration of the solar market presents business risks which could materially adversely affect our results of operations.

We are investing significantly in expanding our polysilicon production capacity. We are also making progress in our plan to make and sell wafers to the solar market. Historically, our expertise has been in the production and sale of wafers to semiconductor customers. In order to succeed at our planned expansion activities, we will need to devote capital expenditures as well as the investment of management time and related resources to penetrate this additional market. This could disrupt our existing business, affect our operating results and distract our management team. Expansion of our polysilicon production capacity is subject to risks such as availability of capital equipment; delays in construction of new production capacity; and availability of additional precursor raw materials. Our plan to sell wafers into the solar market is subject to similar risks and, because it involves sales into a new application, it is also subject to additional risks, including refining and adapting our manufacturing technologies for solar applications; creating and developing demand for and market acceptance of our technologies in the solar wafer market; marketing, promoting and distributing wafers to solar customers; competing with other, better established, wafer manufacturers; and establishing and maintaining sufficient internal research and development, marketing, sales, production and customer service infrastructures to support these efforts. There can be no assurance that we will be able to successfully penetrate the solar market. Use of resources that otherwise would have been made available to our semiconductor wafer customers could have material adverse consequences on our results of operations if we fail to penetrate the solar market successfully.

Our expansion of our 300 millimeter production capacity in Taiwan presents business risks which could materially adversely affect our results of operations if we fail to manage this expansion successfully.

In July 2005, we embarked upon a significant expansion of our 300 millimeter production capacity by establishing such production capacity at our Taisil facility in Taiwan, in addition to continuing our improvements to our Japan 300 millimeter operation. The establishment of this capacity at a new facility involves significant risks, including availability and timing of capital equipment installation, distraction of worldwide and local management; costs and spending in excess of budgeted amounts; timing of production ramp; and qualification of a new facility at new and existing customers. We believe that establishment of 300 millimeter capacity in Taiwan is important for strategic reasons, including market share and profitability. There can be no assurance that we will be able to successfully reach our production, timing and cost goals for this expansion or maintain them for our Japan facility as customer specifications evolve. Use of capital and management resources that otherwise would have been made available to expand other parts of our business could have material adverse consequences on our results of operations if we fail to manage this expansion successfully or do not improve our Japan 300 millimeter operations to keep pace with market requirements.

7

We experience intense competition in the wafer industry which could force us to reduce our prices to retain market share or face losing market share and revenues.

We face intense competition in the wafer industry from established manufacturers throughout the world. If we cannot compete effectively with other wafer manufacturers, our operating results could be materially adversely affected. Some of our competitors have substantial financial, technical, engineering and manufacturing resources to develop products that currently, and may in the future, compete favorably against our products.

We compete on the basis of product quality, consistency, price, technical innovation, customer service and product availability. We expect that our competitors will continue to improve the design and performance of their products and to introduce new products with competitive price and performance characteristics. We may need to reduce our prices to retain market share, which could have a material adverse effect on our operating results.

If we fail to meet changing customer demands, we may lose customers and our sales could suffer.

The wafer industry changes rapidly. Changes in our customers’ requirements result in new and more demanding technology, product specifications and diameters, and manufacturing processes. Our ability to remain competitive will depend upon our ability to develop technologically advanced products and processes. We must continue to meet the increasingly demanding requirements of our customers on a cost-effective basis. As a result, we expect to continue to make significant investments in research and development and equipment. We cannot be certain that we will be able to successfully introduce, market and cost effectively manufacture any new products, or that we will be able to develop new or enhanced products and processes that satisfy customer needs or achieve market acceptance.

Because we cannot easily transfer production of specific products from one of our manufacturing facilities to another, manufacturing delays at a single facility could result in a loss of product volume.

It typically takes three to six months for our customers to qualify a manufacturing facility to produce a specific product, but it can take longer depending upon a customer’s requirements and market conditions. Interruption of operations at any of our primary wafer manufacturing facilities could result in delays or cancellations of shipments of wafers and a loss of product volume. Likewise, interruption of operations at our granular polysilicon manufacturing facility could adversely affect our wafer manufacturing throughput and yields and could result in our inability to produce certain qualified wafer products, delays or cancellations of shipments of wafers and a loss of product volume. A number of factors could cause interruptions, including labor disputes, equipment failures, or shortages of raw materials or supplies. Unions represent some of the employees at our wafer facilities in St. Peters, Missouri, Italy and South Korea and our granular polysilicon facility in Pasadena, Texas. A strike at any of these facilities could cause interruptions in manufacturing. We cannot be certain that alternate qualified capacity would be available on a timely basis or at all.

If we do not continue to reduce our manufacturing costs and operating expenses, we may not be able to compete effectively in our industry.

The success of our business depends, in part, on our continuous reduction of manufacturing costs and operating expenses. The wafer industry has historically experienced price erosion and will likely continue to experience such price erosion. If we are not able to reduce our manufacturing costs and operating expenses sufficiently to offset future price erosion, our operating results will be adversely affected. During the past few years, we have engaged in various cost-cutting and other initiatives intended to reduce costs and increase productivity. These activities have included reduction of headcount, refinement of our processes and efforts to increase yields and reduce cycle time. We cannot assure you that we will be able to continue to reduce our manufacturing costs and operating expenses. Moreover, any future closure of facilities or reduction of headcount may adversely affect our ability to manufacture wafers in required volumes to meet customer demand and may result in other production disruptions.

8

We are subject to periodic fluctuations in foreign currency exchange rates which can cause reported financial results to vary significantly from period to period.

Approximately 69% of our sales in 2005 were made outside North America. We expect that international sales will continue to represent a significant percentage of our total sales. In addition, a significant portion of our manufacturing operations is located outside of the United States. Sales outside of the United States expose us to currency exchange rate fluctuations. Our risk exposure from these sales is primarily related to Euro, Japanese Yen and Korean Won. Our risk exposure from expenses at international manufacturing facilities is concentrated in Euro, Japanese Yen, Korean Won, Malaysian Ringgit and New Taiwanese Dollar. To the extent that our sales in foreign currencies occur at foreign sites which incur expenses in those currencies, our net exposure is reduced. We generally hedge receivables denominated in foreign currencies at the time of sale.

Our foreign subsidiaries have debt denominated in Euro, Japanese Yen, New Taiwanese Dollars and U.S. Dollars. We generally do not hedge these net foreign currency exposures.

We recognized net currency losses totaling approximately $1 million in 2005, net current losses totaling approximately $2 million in 2004 and net currency gains totaling approximately $14 million in 2003. We cannot predict whether these foreign currency exchange risks inherent in doing business in foreign countries will have a material adverse effect on our operations and financial results in the future.

We may acquire other businesses, products or technologies; if we do, we may be unable to integrate them with our business effectively or at all, which may impair our financial performance.

If we find appropriate opportunities, we may acquire businesses, products or technologies that we believe are strategic. If we acquire a business, product or technology, the process of integration may produce unforeseen operating difficulties and expenditures and may absorb significant attention of our management that would otherwise be available for the ongoing development of our business. If we make future acquisitions, we may issue shares of stock that dilute other stockholders, expend cash, incur debt, assume contingent liabilities or create additional expenses related to amortizing other intangible assets with estimated useful lives, any of which might harm our business, financial condition or results of operations.

Our business may be harmed if we fail to properly protect our intellectual property.

We believe that the success of our business depends in part on our proprietary technology, information, processes and know how. We try to protect our intellectual property rights based on trade secrets and patents as part of our ongoing research, development and manufacturing activities. We cannot be certain, however, that we have adequately protected or will be able to adequately protect our technology, that our competitors will not be able to utilize our existing technology or develop similar technology independently, that the claims allowed with respect to any patents held by us will be broad enough to protect our technology or that foreign intellectual property laws will adequately protect our intellectual property rights. Moreover, we cannot be certain that our patents do or will provide us with a competitive advantage.

The protection of our intellectual property rights and the defense of claims of infringement against us by third parties may subject us to costly patent litigation.

Any litigation in the future to enforce patents issued to us, to protect trade secrets or know how possessed by us or to defend us or indemnify others against claimed infringement of the rights of others could have a material adverse effect on our financial condition and operating results. From time to time, we receive notices from other companies that we may be infringing certain of their patents or other rights. If we are unable to resolve these matters satisfactorily, or to obtain licenses on acceptable terms, we may face litigation, which could have a material adverse effect on us. In fact, we are presently involved in multiple cases involving allegations of patent infringement. Regardless of the validity or successful outcome of any such intellectual property claims, we may need to expend significant time and expense to protect our intellectual property rights or to defend against claims

9

of infringement by third parties, which could have a material adverse effect on us. If we lose any such litigation, we may be required to:

| | • | | pay substantial damages; |

| | • | | seek licenses from others; or |

| | • | | change, or stop manufacturing or selling, some of our products. |

Any of these outcomes could have a material adverse effect on our business, results of operations or financial condition.

We have a limited number of principal customers and a loss of one or several of those customers would hurt our business.

Our operating results could materially suffer if we experience a significant reduction in, or loss of, purchases by one or more of our top customers. We made approximately 57% of our sales to our ten biggest customers in 2005. Only Samsung accounted for more than 10% of our sales in 2005.

We are subject to periodic foreign economic downturns and political instability, which may adversely affect our sales and cost of doing business in those regions of the world.

Economic downturns in the Asia Pacific region and Japan have affected our operating results in the past, and economic downturns in those and other regions in which we operate could affect our operating results in the future. Additionally, other factors may have a material adverse effect on our operations in the future, including:

| • | the imposition of governmental controls or changes in government regulation; |

| • | export license requirements; |

| • | restrictions on the export of technology; |

| • | geo-political instability; and |

| • | trade restrictions and changes in tariffs. |

We cannot predict whether these economic risks inherent in doing business in foreign countries will have a material adverse effect on our operations and financial results in the future.

We are required to evaluate our internal control under Section 404 of the Sarbanes-Oxley Act of 2002 and any adverse results from such evaluation could result in a loss of investor confidence in our financial reports and could have an adverse effect on our stock price.

Pursuant to Section 404 of the Sarbanes-Oxley Act of 2002, we are required to furnish a report by our management on our internal control over financial reporting. Such report contains, among other matters, an assessment of the effectiveness of our internal control over financial reporting as of the end of our fiscal year, including a statement as to whether or not our internal control over financial reporting is effective. This assessment must include disclosure of any material weaknesses in our internal control over financial reporting identified by management. Such report must also contain a statement that our auditors have issued an attestation report on management’s assessment of such internal controls. Public Company Oversight Board Auditing Standard No. 2 provides the professional standards and related performance guidance for auditors to attest to, and report on, management’s assessment of the effectiveness of internal control over financial reporting under Section 404.

Each year we must perform the system and process documentation and evaluation needed to comply with Section 404. During this process, if our management identifies one or more material weaknesses in our internal control over financial reporting, we will be unable to assert such internal control is effective. For both fiscal 2004 and fiscal 2005, we reported at least one material weakness in our internal control over financial reporting. Although we have taken actions to address these material weaknesses, there can be no assurance that these

10

actions will fully address such material weaknesses, or that we will not have one or more material weaknesses in the future. If we are unable to assert that our internal control over financial reporting is effective presently or in the future (or if our auditors are unable to attest that our management’s report is fairly stated or if they are unable to express an opinion on the effectiveness of our internal controls), we could lose investor confidence in the accuracy and completeness of our financial reports, which could have an adverse effect on our stock price.

We are subject to numerous environmental laws and regulations, which could require us to discharge environmental liabilities, increase our manufacturing and related compliance costs or otherwise adversely affect our business.

We are subject to a variety of foreign, federal, state and local laws and regulations governing the protection of the environment. These environmental laws and regulations include those relating to the use, storage, handling, discharge, emission, disposal and reporting of toxic, volatile or otherwise hazardous materials used in our manufacturing processes. These materials may have been or could be released to the environment at properties currently or previously owned or operated by us, at other locations during the transport of the materials, or at properties to which we send substances for treatment or disposal. If we were to violate or become liable under environmental laws and regulations or become non-compliant with permits required at some of our facilities, we could be held financially responsible and incur substantial costs, including cleanup costs, fines and civil or criminal sanctions, third-party property damage or personal injury claims. Groundwater and/or soil contamination has been detected at four of our facilities. We believe we are taking all necessary remedial steps at these facilities. We do not expect these known conditions to have a material impact on our business. However, environmental issues relating to presently known or unknown matters could require additional investigation, assessment or expenditures. In addition, new laws and regulations or stricter enforcement of existing laws and regulations could give rise to additional compliance costs and liabilities.

The market price of our common stock has fluctuated significantly and may continue to do so.

The market price of our common stock may be affected by various factors, including:

| | • | | quarterly fluctuations in our operating results resulting from factors such as timing of orders from and shipments to major customers, product mix and competitive pricing pressures; |

| | • | | announcements of technological innovations, new products or upgrades to existing products by us or our competitors; |

| | • | | market conditions in the semiconductor device and wafer industries; |

| | • | | developments in patent or other proprietary rights by us or by our competitors; |

| | • | | changes in our relationships with our customers; |

| | • | | interruption of operations at our manufacturing facilities; |

| | • | | actual or perceived changes in our relationship with our largest stockholder, TPG; |

| | • | | the size of the public float of our common stock; |

| | • | | announcements of operating results that are not aligned with the expectations of investors; and |

| | • | | general stock market trends. |

Technology company stocks in general have experienced extreme price and trading volume fluctuations that often have been unrelated to the operating performance of these companies. This market volatility may adversely affect the market price of our common stock.

If we fail to comply with covenants under our credit facility, the lenders could cause outstanding amounts to become immediately due and payable, and we might not have sufficient funds and assets to pay such loans.

We are party to a $200 million revolving credit facility with National City Bank of the Midwest, US Bank National Association and other lenders named therein. This facility contains certain restrictive covenants,

11

including covenants to maintain minimum consolidated EBITDA and interest coverage ratio, as those terms are defined in such agreement. A continuing violation of any of these covenants, which in our industry could occur in a sudden or sustained downturn, would be deemed an event of default under the facility. In such event, upon election of the lenders, the loan commitments under the credit facility would terminate and the loans and accrued interest then outstanding would be due and payable immediately. We may not have sufficient funds and assets to cover any such required payments and may not be able to obtain replacement financing on a timely basis or at all. In addition, because all of the capital stock of most of our domestic subsidiaries and 65% of the capital stock of certain of our foreign subsidiaries is pledged as collateral under the facility, the lenders could foreclose on that stock upon an event of default. These events would have a material adverse effect on us. As of December 31, 2005, we had no outstanding borrowings under this facility, although we had approximately $8 million of outstanding third party letters of credit backed by this facility at such date.

Future sales of shares of our common stock may depress the price of our common stock.

If we or our stockholders sell a substantial number of shares of our common stock in the public market, or investors become concerned that substantial sales might occur, the market price of our common stock could decrease. We have granted TPG registration rights with respect to all of the shares of our common stock and warrants to purchase common stock owned by TPG. Future sales of our common stock or warrants to purchase our common stock by TPG in the public market, or the perception that such sales might occur, could cause such a decrease in the price of our common stock.

TPG has significant voting power to influence our direction and policies, which could prevent a favorable acquisition of us and create other conflicts of interest between us and TPG.

TPG, through its approximate 25% beneficial ownership interest of our common stock, has significant voting power to influence our direction and policies, including any merger, consolidation or sale of all or substantially all of our assets. For example, under our restructuring agreement with TPG, we must either obtain the consent of TPG or give TPG a right of first refusal over any issuances of our equity securities to any person or group to the extent that the equity securities would have 10% or more of the voting power of all of our then outstanding voting securities. As a practical matter, as a result of its share ownership, TPG has the ability to influence the election and composition of our Board of Directors. Two of the seven members of our current Board of Directors are partners of certain TPG entities.

Certain provisions of our Restated Certificate of Incorporation and Restated By-Laws could delay or make more difficult a change of control or change in management that would benefit our stockholders.

Certain provisions of our Restated Certificate of Incorporation and Restated By-Laws may delay, defer or make more difficult:

| | • | | a merger, tender offer or proxy contest; |

| | • | | the assumption of control by a holder of a large block of our securities; and |

| | • | | the replacement or removal of current management by our stockholders. |

For example, our Restated Certificate of Incorporation divides the Board of Directors into three classes, with members of each class to be elected for staggered three-year terms. This provision may make it more difficult for stockholders to change the majority of directors and may frustrate accumulations of large blocks of common stock by limiting the voting power of such blocks. This may further discourage a change of control or change in current management.

These provisions may limit participation by our stockholders in any merger or other change of control transaction, whether or not the transaction is favored by current management or would be favorable to our stockholders. These provisions may also make removal of current management by our stockholders more difficult, even if such removal would be beneficial to the stockholders generally.

12

In addition, our Board of Directors is authorized to issue up to 50,000,000 shares of preferred stock without the vote of our holders of common stock, subject to certain restrictions on the issuance of preferred stock contained in our restructuring agreement with TPG. The issuance of preferred stock could adversely affect the voting power or other rights of the holders of our common stock and could have the effect of delaying, deferring or impeding a change in control of us.

Cautionary Statement Regarding Forward-Looking Statements

The following statements are or may constitute forward-looking statements:

| | • | | statements set forth in this Form 10-K or statements incorporated by reference from documents we have filed with the Securities and Exchange Commission, including possible or assumed future results of our operations, including but not limited to any statements contained herein or therein concerning: |

| | • | | Our belief that we have the financial resources needed to meet business requirements for the next 12 months, including capital expenditures and working capital requirements; |

| | • | | Our belief that our tax reserves reflect the probable outcome of known contingencies; |

| | • | | Our expectation that the adoption of SFAS 123R will have an estimated negative $0.03 to $0.04 impact on diluted earnings per share for the year ended December 31, 2006; |

| | • | | Our belief that as markets for semiconductor devices continue to evolve and become more specialized, device manufacturers will recognize the enhanced role that wafers and other materials play in improving device performance and reducing their production costs; |

| | • | | Our belief that wafer industry consolidation is causing segmentation between larger and smaller wafer producers, with larger manufacturers gaining an increasing share of the overall wafer market; |

| | • | | Our belief that semiconductor device manufacturers seek suppliers with whom they can better align wafer technology development with their own product development efforts, and the belief that these manufacturers will continue to select wafer suppliers that offer advanced technology capabilities, a broad product portfolio and superior service to satisfy their exacting device requirements; |

| | • | | Our belief that the OPTIA™ wafer is the most technically advanced polished wafer available today; |

| | • | | Our belief that there are not other sources of semiconductor grade granular polysilicon; |

| | • | | Our belief that our ability to meet the majority of our polysilicon requirements through our in-house capabilities provides us with a key cost advantage; |

| | • | | Our belief that continued and timely development of new products and enhancements to existing products is necessary to maintain our competitive position; |

| | • | | Our expectation that our competitors will continue to improve the design and performance of their products to introduce new products with competitive price and performance characteristics; |

| | • | | Our belief that our wafers are competitive with competitors’ on the basis of product quality, consistency, price, technical innovation, customer service and product availability; |

| | • | | Our belief that the success of our business depends in part on our proprietary technology, information, processes and know how; |

| | • | | Our expectation that international sales will continue to represent a significant percentage of our total sales; |

| | • | | Our belief that that we could substitute chunk polysilicon for granular polysilicon; |

| | • | | Our belief that establishment of 300 millimeter capacity in Taiwan is important for strategic reasons, including market share and profitability; |

13

| | • | | Our expectation that we will continue to make significant investments in research and development and equipment; |

| | • | | Our belief that the success of our business depends in part on our proprietary technology, information, processes and know how; |

| | • | | Our belief that we are taking all necessary environmental remediation steps at our facilities, and our expectation that these known conditions will not have a material impact on our business; |

| | • | | Our belief that our existing facilities and equipment are well maintained, in good operating condition and are adequate to meet our current requirements; |

| | • | | The impact of pending litigation on us; |

| | • | | Our expectation that contributions to our pension plans will be approximately $16 million in 2006; |

| | • | | Our determination that the adoption of SFAS 154 will not have a material impact on our consolidated results of operations and financial condition; |

| | • | | Other statements contained or incorporated by reference in this Form 10-K regarding matters that are not historical facts; and |

| | • | | Any statements preceded by, followed by or that include the words “believes,” “expects,” “predicts,” “anticipates,” “intends,” “estimates,” “should,” “may” or similar expressions. |

Because such statements are subject to risks and uncertainties, actual results may differ materially from those expressed or implied by such forward-looking statements. You should not place undue reliance on such statements, which speak only as of the date that they were made. Factors that could cause actual results to differ materially are set forth under this “Item 1A. Risk Factors.”

These cautionary statements should be considered in connection with any written or oral forward-looking statements that we may issue in the future. We do not undertake any obligation to release publicly any revisions to such forward-looking statements to reflect later events or circumstances or to reflect the occurrence of unanticipated events.

| Item 1B. | Unresolved Staff Comments |

None.

Our principal executive offices are located at 501 Pearl Drive (City of O’Fallon), St. Peters, Missouri 63376, and our telephone number at that address is (636) 474-5000. Our principal manufacturing and administrative facilities comprised approximately 3.9 million square feet as of December 31, 2005 and were situated in the following locations:

| | |

Location

| | Square Footage

|

St. Peters, MO, USA | | 744,000 |

Sherman, TX, USA | | 693,000 |

Pasadena, TX, USA | | 436,000 |

Hsinchu, Taiwan | | 522,000 |

Chonan, South Korea | | 453,000 |

Utsunomiya, Japan | | 327,000 |

Merano, Italy | | 327,000 |

Novara, Italy | | 322,000 |

Kuala Lumpur, Malaysia | | 86,000 |

14

In December 2005, we purchased from the City of O’Fallon, Missouri the portion of our St. Peters facility that had been leased from the City of O’Fallon in connection with an industrial revenue bond financing. We lease the land on which our Pasadena, Texas facility is located. The term of the Pasadena lease expires in 2030 and is extendable for four (4) additional renewal terms of five (5) years each. We lease the land on which our Hsinchu, Taiwan facility is located. This lease expires in 2014. We also lease our facility in Kuala Lumpur, Malaysia. This lease expires in March 2009.

We believe that our existing facilities and equipment are well maintained, in good operating condition and are adequate to meet our current requirements. The extent of utilization of these facilities varies from plant to plant and from time to time during the year.

Albemarle Corporation et al. vs. MEMC Electronic Materials, Inc., et al.

In a case entitled Damewood vs. Ethyl Corporation, et al. (Cause No. 96-38521), filed on August 1, 1996, three employees of the former operator of MEMC Pasadena’s plant, Albemarle Corporation, filed suit against us and others in the 189th Judicial District Court, Harris County, Texas. The employees alleged that they sustained injuries during an explosion at that plant on January 27, 1996. We settled this matter with the plaintiffs and were dismissed as a party. One of the other defendants, Ethyl Corporation, was the only defendant in this case at the time of trial in October 1998. A jury awarded a verdict in favor of the plaintiffs that resulted in a judgment against Ethyl Corporation in the amount of $6.8 million. Ethyl Corporation appealed this judgment. Ethyl Corporation and the plaintiffs subsequently settled this matter for $5.2 million.

On September 29, 1998, Albemarle Corporation made a demand against us for defense and indemnity in this case on behalf of Ethyl Corporation. Albemarle Corporation assumed the obligation to defend and indemnify Ethyl Corporation under an agreement in which Ethyl Corporation transferred ownership of the plant where the injury took place to Albemarle Corporation. In November 1998, we made a demand for indemnity in this case against Albemarle Corporation. Demands for indemnity made by Albemarle Corporation on behalf of Ethyl Corporation and by us are both based on contractual indemnity language contained in the contract for the sale of the MEMC Pasadena plant from Albemarle Corporation to us.

In a case entitled Albemarle Corporation et al. vs. MEMC Electronic Materials, Inc., et al. (Cause No. 2002-59930), filed on November 20, 2002 in the 55th Judicial District Court, Harris County, Texas, Albemarle and its insurers filed suit against us and MEMC Pasadena seeking indemnification and costs of defense in the above matter. On February 14, 2003, we filed an answer denying the allegations by Albemarle Corporation and its insurers. On March 17, 2003, we filed a counterclaim against Albemarle Corporation seeking indemnification, costs of defense and payment of certain funds recovered by Albemarle Corporation’s workers’ compensation carrier in connection with the above matter. On October 22, 2004, the court entered an order granting Albemarle’s motion for summary judgment and denying our motion for summary judgment. The court did not consider the issue of damages. We appealed the summary judgment decision on April 15, 2005. Both parties have briefed the issue with the appellate court and are awaiting a decision.

We do not believe that this matter will have a material adverse effect on us. Due to uncertainty regarding the litigation process, however, the scope and interpretation of contractual indemnity provisions and the status of any insurance coverage, the outcome of this matter could be unfavorable, in which event we might be required to pay damages and other expenses.

Lemelson Medical, Education and Research Foundation, Limited Partnership vs. ESCO Electronics Corporation, et al.

In a case entitled Lemelson Medical, Education and Research Partnership vs. ESCO Electronics Corporation, et al. (Civil Action No. 00-0660-PHX-ROS) filed on April 14, 2000, the Lemelson Medical,

15

Education and Research Foundation, Limited Partnership filed suit against us and approximately 90 other companies in the United States District Court for the District of Arizona. The Lemelson Foundation alleges that we infringe on certain patents owned by the Lemelson Foundation related to bar coding and machine vision reading systems. The Lemelson Foundation seeks damages against us in an unstated amount, attorneys’ fees and an order enjoining us from further infringement of the unexpired patents. On March 29, 2001, the court issued an order to stay this litigation pending the entry of a final non-appealable judgment in earlier-filed actions involving the same patents. In January 2004, the court in these earlier-filed actions ruled that the patents at issue were invalid, unenforceable and not infringed by bar code scanners and machine vision reading systems very similar to the bar code scanners and machine vision reading systems used by us. On February 1, 2006, the U.S. District Court for the District of Arizona granted plaintiff Lemelson Medical, Education and Research Foundation, Limited Partnership’ motion, and dismissed with prejudice all claims against us and the other defendants and accordingly, this litigation against us has been terminated.

Sumitomo Mitsubishi Silicon Corporation et al. vs. MEMC Electronic Materials, Inc.

On December 14, 2001, MEMC filed a lawsuit against Sumitomo Mitsubishi Silicon Corporation (“SUMCO”) and several of its affiliates in the Northern District of California (the “First SUMCO Case”) alleging infringement of one of MEMC’s U.S. patents. On March 16, 2004, the court entered summary judgment against MEMC. MEMC appealed this decision to the U.S. Federal Circuit Court of Appeals, and on August 22, 2005, the U.S. Federal Circuit Court of Appeals reversed the grant of summary judgment with respect to inducement of infringement by SUMCO, and the case was remanded to the U.S. District Court for further proceedings. On February 24, 2006, the U.S District Court granted certain summary judgment motions of each of SUMCO and MEMC. In light of the summary judgment rulings in favor of SUMCO, on February 27, 2006 the U.S District Court issued a final judgment against MEMC in the First SUMCO Case. On February 28, 2006, MEMC filed its Notice of Appeal of the grant of certain of the summary judgment rulings in favor of SUMCO in the First SUMCO Case with the U.S. Federal Circuit Court of Appeals.

On July 13, 2004, SUMCO and certain of its affiliates filed a lawsuit against MEMC in the U.S. District Court for the District of Delaware (the “Second SUMCO Case”) in a case captionedSumitomo Mitsubishi Silicon Corporation, aka SUMCO, a corporation of Japan and SUMCO USA Corporation, a Delaware corporation, v. MEMC Electronic Materials, Inc., a Delaware corporation, Civil Action No. 04-852-SLR. In May 2005, MEMC successfully had this case removed to the Northern District of California, although the Second SUMCO Case and the First SUMCO Case will not be consolidated. In the Second SUMCO Case, plaintiffs allege that MEMC violated the antitrust laws by attempting to control sales of low defect silicon wafers in the United States, including through its patent policies and enforcement of its patents related to low defect silicon wafers. Plaintiffs also seek a declaratory judgment that plaintiffs’ wafers do not infringe the claims of two MEMC patents and that these two MEMC patents are invalid and unenforceable. Finally, plaintiffs allege that these two MEMC patents are void and unenforceable because of MEMC’s alleged patent misuse. Plaintiffs seek treble damages in an unspecified amount, and attorneys’ fees and costs incurred by plaintiffs in the Second SUMCO Case and in the First SUMCO Case. MEMC had asserted defenses against these claims, including a counterclaim for infringement of one of the two patents. In June 2006, in light of the pending appeal with the U.S. Federal Circuit Court of Appeals on certain matters from the First SUMCO Case, certain of the counts related to the two MEMC patents were dismissed from the Second SUMCO Case without prejudice. MEMC believes that SUMCO’s position in the Second SUMCO Case has no merit and is asserting a vigorous defense.

S.O.I.TEC Silicon on Insulator Technologies S.A. and Soitec USA, Inc. vs. MEMC Electronic Materials, Inc.

On November 21, 2005, S.O.I.TEC Silicon on Insulator Technologies S.A. and Soitec USA, Inc. (“Soitec”) filed a Complaint for Declaratory Judgment against MEMC in the U.S. District Court for the District of Delaware (Civil Action No. 05-806) alleging invalidity and/or non-infringement of seven MEMC U.S. patents. In January 2006, MEMC filed a motion to dismiss with respect to six of the seven patents in the case, and also brought a counterclaim against Soitec for infringement in the United States by Soitec of the remaining U.S. patent. The

16

parties subsequently agreed to the dismissal of six of the seven patents from the case. Soitec filed an amended complaint in April 2006, and MEMC filed its amended answer and counterclaim in May 2006. Although the case is in the early stages, we believe that Soitec’s declaratory judgment action against us has no merit, and we are asserting a vigorous defense against that claim, as well as pursuing our counterclaim for infringement. Also, on December 28, 2005, MEMC filed suit against Soitec in France for infringement by Soitec of three of MEMC’s foreign patents. This case remains in the early stages. We do not believe that either Soitec case, should they be decided against MEMC, in whole or in part, will have a material adverse effect on us. Due to uncertainty regarding the litigation process, however, the outcome of both matters are unpredictable and the result of either case could be unfavorable for MEMC.

ASi Industries GmbH vs. MEMC Electronic Materials, Inc. and MEMC Pasadena, Inc.

On June 19, 2006, ASi Industries GmbH (“ASi”) filed a Complaint for Breach of Contract and Declaratory Judgment against MEMC in the U.S. District Court for the Eastern District of Missouri (Civil Action No. 4:06-CV-00951-CDP) alleging breach of contract by MEMC, unjust enrichment, tortious interference with ASi’s contracts, antitrust violations and seeking a declaratory judgment of non-infringement, all related to a purchase order agreement related to polysilicon. MEMC has not yet filed its answer and any related counterclaims. Although the case is in the very early stages, we believe our actions under the purchase order at issue were permitted, and are asserting a vigorous defense, as well as intending to pursue our counterclaims for infringement related to certain intellectual property related to polysilicon technology.

We do not believe that the ASi case, should it be decided against MEMC, in whole or in part, will have a material adverse effect on us. Due to uncertainty regarding the litigation process, however, the outcome of this matter is unpredictable and the result of the case could be unfavorable for MEMC.

| Item 4. | Submission of Matters to a Vote of Security Holders |

No matters were submitted to a vote of security holders during the fourth quarter of the fiscal year covered by this report.

17

PART II

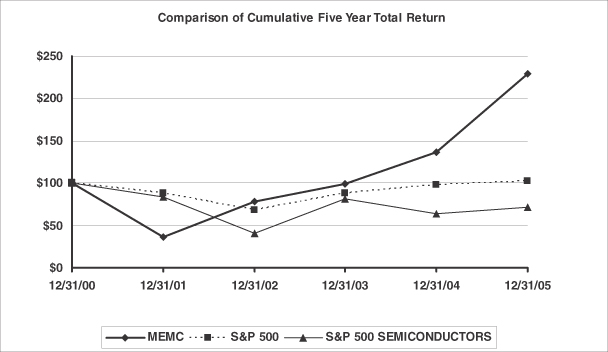

| Item 5. | Market for Registrant’s Common Equity and Related Stockholder Matters |

The narrative and tabular information regarding the market for our common equity and related stockholder matters required by this item is set forth under Note 21, “Unaudited Quarterly Financial Information”, of Notes to Consolidated Financial Statements, included in our 2005 Annual Report and under “Stockholders’ Information” in our 2005 Annual Report, which information is incorporated herein by reference. We have not paid any dividends on our common stock for the last three fiscal years. Under the terms of our $200 million National City Bank revolving credit facility, we are prohibited from paying cash dividends on our common stock. Likewise, under the restructuring agreement between us and TPG, we cannot pay cash dividends on our common stock without the consent of TPG.

The information required under this Item concerning equity compensation plan information is set out below under Item 12 and is incorporated herein by this reference.

| Item 6. | Selected Financial Data |

The tabular information (including the footnotes thereto) required by this item is set forth under “Five Year Selected Financial Highlights” in our 2005 Annual Report, which information is incorporated herein by reference.

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

The information required by this item is set forth under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our 2005 Annual Report, which information is incorporated herein by reference.

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk |

The information required by this item is set forth under “Market Risk” included in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our 2005 Annual Report, which information is incorporated herein by reference.

| Item 8. | Financial Statements and Supplementary Data |

The information required by this item is set forth under “Consolidated Statements of Operations”, “Consolidated Balance Sheets”, “Consolidated Statements of Cash Flows”, “Consolidated Statements of Stockholders’ Equity (Deficiency)”, “Notes to Consolidated Financial Statements” and “Reports of the Independent Registered Public Accounting Firm” in our 2005 Annual Report, all of which are incorporated herein by reference.

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

None.

| Item 9A. | Controls and Procedures |

| (a) | Evaluation of Disclosure Controls and Procedures |

We carried out an evaluation as of December 31, 2005, under the supervision and with the participation of our management, including our Chief Executive Officer and Chief Financial Officer, of the effectiveness of the design and operation of our disclosure controls and procedures, as defined in Rules 13-15(e) and 15d-15(e) under

18

the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Based upon that evaluation, our Chief Executive Officer and Chief Financial Officer concluded that our disclosure controls and procedures were not effective as of December 31, 2005, based on the material weaknesses discussed in Management’s Report on Internal Control Over Financial Reporting set out below.

| (b) | Management’s Report on Internal Control Over Financial Reporting |

Our management is responsible for establishing and maintaining adequate internal control over financial reporting as defined in Rules 13a-15(f) and 15d-15(f) under the Securities Exchange Act of 1934. Our internal control over financial reporting is designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with U.S. generally accepted accounting principles.

As of December 31, 2005, management conducted an assessment of the effectiveness of the Company’s internal control over financial reporting based upon the framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO) inInternal Control—Integrated Framework. Based upon this assessment, management concluded that, as of December 31, 2005, the Company did not maintain effective internal control over financial reporting. Management has identified the following material weaknesses:

| | 1. | Ineffective Company-Level Controls.We did not maintain effective company-level controls as defined in theInternal Control—Integrated Framework, published by the Committee of Sponsoring Organizations of the Treadway Commission (COSO). These deficiencies related to four of the five components of internal control as defined by COSO (control environment, risk assessment, information and communication, and monitoring). Specifically, |

| | a. | Our control environment did not sufficiently promote an appropriate level of control awareness throughout the organization, and this material weakness was a contributing factor in the development of other material weaknesses described below; |

| | b. | We did not maintain a sufficient number of adequately trained personnel necessary to anticipate and identify risks critical to financial reporting; |

| | c. | There was inadequate emphasis to employees regarding the importance of controls and employees’ duties and control responsibilities; and |

| | d. | We had inadequate monitoring controls to ensure that appropriate personnel regularly obtain evidence that controls are functioning effectively and that identified control deficiencies are remediated timely. |

These deficiencies resulted in more than a remote likelihood that a material misstatement of our interim or annual consolidated financial statements would not be prevented or detected.

| | 2. | Inadequate Expertise in U.S. Generally Accepted Accounting Principles. We lacked adequately trained finance and accounting personnel with appropriate U.S. generally accepted accounting principles (US GAAP) expertise. As a result, an effective internal secondary review of technical accounting matters could not be performed in certain circumstances. Specifically, this material weakness encompasses specific deficiencies in, and resulted in errors in accounting for certain transactions related to, the following areas: |

| | a. | Accounting for income taxes. Our finance and accounting personnel did not have adequate expertise in accounting for income taxes to ensure the timely identification of discrete events that should not have been included in the annual effective tax rate calculation used to record income taxes in our interim consolidated financial statements. This deficiency also resulted in the failure to ensure the proper identification and recording of deferred tax assets and liabilities. This deficiency resulted in a restatement of our consolidated financial statements for the first and second quarters of 2005 and resulted in material errors in our consolidated financial statements for |

19

| | the third quarter of 2005 and as of and for the year ended December 31, 2005, that were corrected prior to issuance. |