Proliance International, Inc. <br/>(AMEX: PLI)<br/><br/>Annual Stockholders Meeting

May 3, 2007

Presented by:

Charley Johnson – President and CEO

FORWARD-LOOKING STATEMENTS

Agenda

2006 Review

Market

Actions

Results

2007 Outlook

Performance Factors

Goals

Outlook

2006: Market Conditions

Soft market for heat exchange and A/C products, due to weather conditions and high fuel costs, which impacted miles driven and consumer buying?

Soft market for heat exchange and A/C products, due to weather conditions and high fuel costs, which impacted miles driven and consumer buying?

Resulted in higher inventories than desirable at the end of the selling season and caused us to cut back our plants

Did achieve goal of lower inventory at end of 2007 compared to end of 2006, even with $10 million in embedded higher material costs

Record-high raw material costs, which were not recoverable with price actions, impacted automotive and light truck radiators

Strong local competition at the branch level, driven by new competitive market entries, impacted the radiator and A/C markets

Shift in radiator sales unit mix from branches toward wholesale customers caused lower average margins

Changes in customer acceptance of lower quality or different radiator product designs also drove new competitive challenge

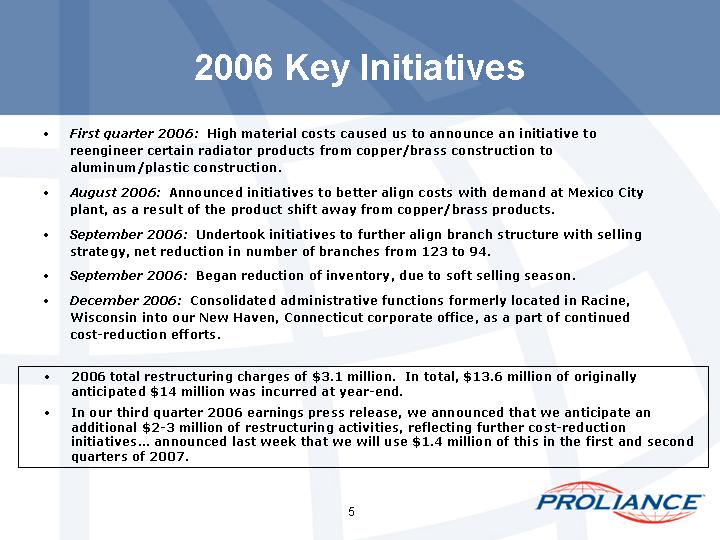

2006 Key Initiatives

First quarter 2006: High material costs caused us to announce an initiative to reengineer certain radiator products from copper/brass construction to aluminum/plastic construction.

First quarter 2006: High material costs caused us to announce an initiative to reengineer certain radiator products from copper/brass construction to aluminum/plastic construction.

August 2006: Announced initiatives to better align costs with demand at Mexico City plant, as a result of the product shift away from copper/brass products.

September 2006: Undertook initiatives to further align branch structure with selling strategy, net reduction in number of branches from 123 to 94.

September 2006: Began reduction of inventory, due to soft selling season.

December 2006: Consolidated administrative functions formerly located in Racine, Wisconsin into our New Haven, Connecticut corporate office, as a part of continued cost-reduction efforts.

2006 total restructuring charges of $3.1 million. In total, $13.6 million of originally anticipated $14 million was incurred at year-end.

2006 total restructuring charges of $3.1 million. In total, $13.6 million of originally anticipated $14 million was incurred at year-end.

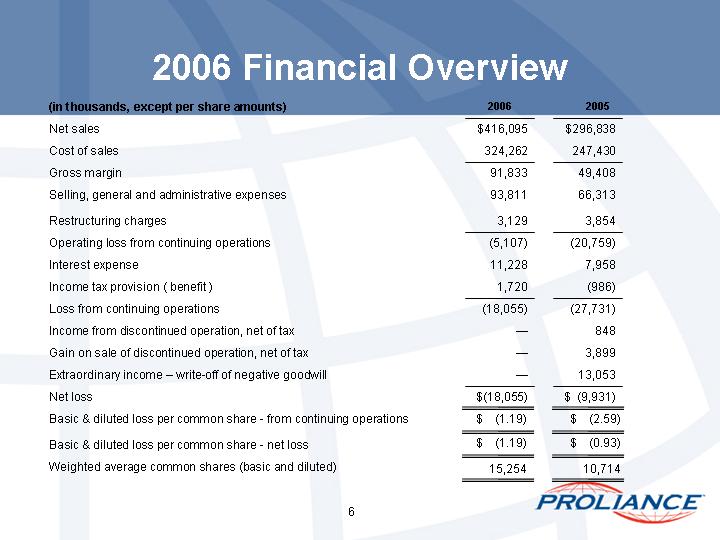

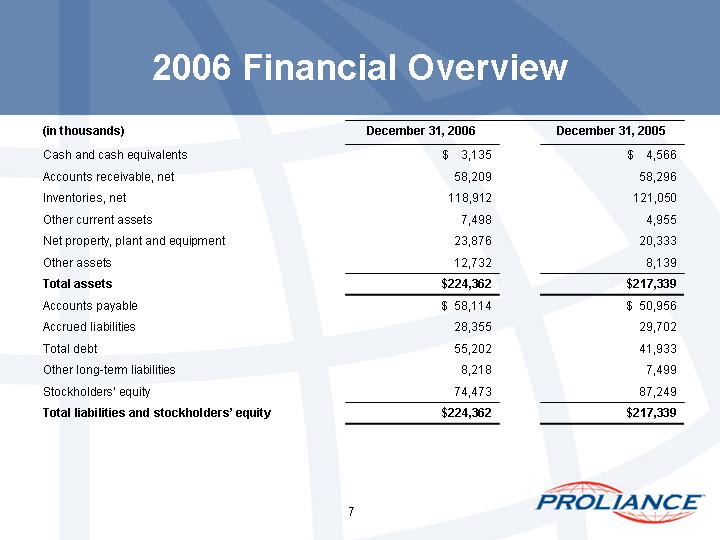

2006 Financial Overview

2006 Financial Overview

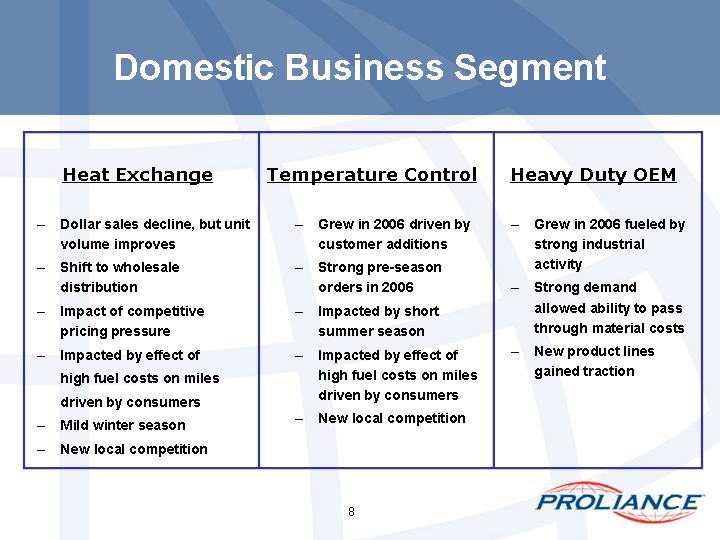

Domestic Business Segment

Heat Exchange

Heat Exchange

Dollar sales decline, but unit volume improves

Shift to wholesale distribution

Impact of competitive pricing pressure

Impacted by effect of

high fuel costs on miles

driven by consumers

Mild winter season

New local competition

Temperature Control

Temperature Control

Grew in 2006 driven by customer additions

Strong pre-season orders in 2006

Impacted by short summer season

Impacted by effect of high fuel costs on miles driven by consumers

New local competition

Heavy Duty OEM

Heavy Duty OEM

Grew in 2006 fueled by strong industrial activity

Strong demand allowed ability to pass through material costs

New product lines gained traction

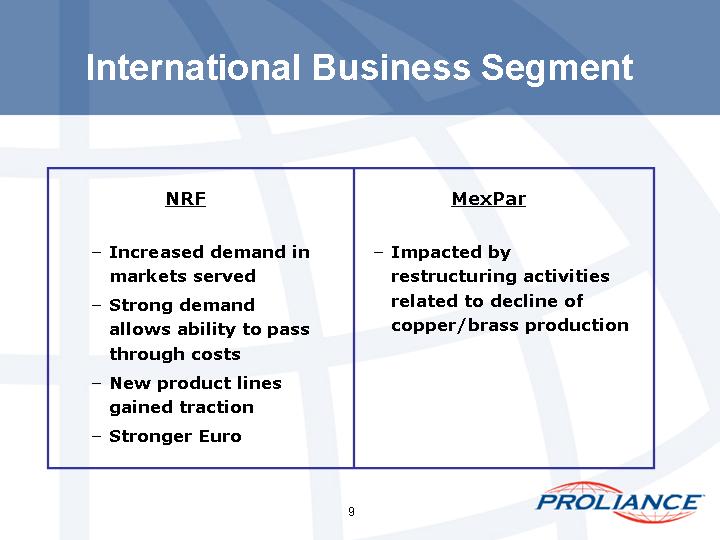

International Business Segment

MexPar

MexPar

Impacted by restructuring activities related to decline of copper/brass production

NRF

NRF

Increased demand in markets served

Strong demand allows ability to pass through costs

New product lines gained traction

Stronger Euro

2006 Objectives

We Exit 2006 Better Positioned?

Product competitiveness? radiators and A/C cost improvements? results not yet seen? will improve margins as we go through the year

Product competitiveness? radiators and A/C cost improvements? results not yet seen? will improve margins as we go through the year

Reduced SG&A overhead costs

Improved supply flexibility to reduce inventory and excess inventory risk

Outstanding product cataloging and breadth of product offering

2007: Factors Impacting Outlook

Continued price-down pressure in heat exchange products driven by global availability? our product engineering capabilities are a strength

Continued price-down pressure in heat exchange products driven by global availability? our product engineering capabilities are a strength

Continued high and “variable” raw material costs will continue to challenge margins

High fuel costs will challenge consumers? we have improved our supply flexibility and speed in order to limit excess inventory risk

Retail and wholesale customers continue to grow their share of the market, however, we also have a better postured branch system to serve specific local customer groups more effectively

2007 Goals

Serve customers well

Serve customers well

Improve inventory turns

Continue to sharpen our branch distribution model

Implement additional product cost improvement actions that will improve margins, even in the face of a competitive marketplace, and continue to reduce overhead

Achieve profitability for the full year 2007

2007 Outlook

First quarter loss a bit greater than 2006, as higher-cost inventory works its way through to market and other cost-reduction initiatives begin to take hold? first quarter 2006 benefited from higher preseason A/C orders

First quarter loss a bit greater than 2006, as higher-cost inventory works its way through to market and other cost-reduction initiatives begin to take hold? first quarter 2006 benefited from higher preseason A/C orders

Margin and expense improvement expected in second and third quarters, as seasonal sales kick in with higher margins and lower overhead levels. Second quarter results will be impacted by previously announced restructuring costs.

Strong improvement in fourth quarter results

Proliance International, Inc. <br/>(AMEX: PLI)