Investor Supplement

First Quarter Update - 2011

2

Forward-Looking Statements

Certain statements made by Meadowbrook Insurance Group, Inc. in this presentation may

constitute forward-looking statements including, but not limited to, those statements that include

the words "believes," "expects," "anticipates," "estimates," or similar expressions. Please refer

to the Company's most recent 10-K, 10-Q, and other Securities and Exchange Commission

filings for more information on risk factors. Actual results could differ materially. These forward-

looking statements involve risks and uncertainties including, but not limited to the following: the

frequency and severity of claims; uncertainties inherent in reserve estimates; catastrophic

events; a change in the demand for, pricing of, availability or collectability of reinsurance;

increased rate pressure on premiums; obtainment of certain rate increases in current market

conditions; investment rate of return; changes in and adherence to insurance regulation;

actions taken by regulators, rating agencies or lenders; obtainment of certain processing

efficiencies; changing rates of inflation; and general economic conditions. Meadowbrook is not

under any obligation to (and expressly disclaims any such obligation to) update or alter its

forward-looking statements whether as a result of new information, future events or otherwise.

constitute forward-looking statements including, but not limited to, those statements that include

the words "believes," "expects," "anticipates," "estimates," or similar expressions. Please refer

to the Company's most recent 10-K, 10-Q, and other Securities and Exchange Commission

filings for more information on risk factors. Actual results could differ materially. These forward-

looking statements involve risks and uncertainties including, but not limited to the following: the

frequency and severity of claims; uncertainties inherent in reserve estimates; catastrophic

events; a change in the demand for, pricing of, availability or collectability of reinsurance;

increased rate pressure on premiums; obtainment of certain rate increases in current market

conditions; investment rate of return; changes in and adherence to insurance regulation;

actions taken by regulators, rating agencies or lenders; obtainment of certain processing

efficiencies; changing rates of inflation; and general economic conditions. Meadowbrook is not

under any obligation to (and expressly disclaims any such obligation to) update or alter its

forward-looking statements whether as a result of new information, future events or otherwise.

3

(in thousands, except ratios)

Underwriting and Investing

Activities

Activities

Top line earned premium growth

driven primarily by new initiatives that

were launched in the second half of

2009

driven primarily by new initiatives that

were launched in the second half of

2009

Growth in net investment income

reflects 11.6% growth in average

invested assets, off-set by a

prolonged lower yields. See the

following slide for combined ratio

analysis

reflects 11.6% growth in average

invested assets, off-set by a

prolonged lower yields. See the

following slide for combined ratio

analysis

Net Commissions & Fees

Decline in fee and commission

revenue is driven by conversion of

USSU to our paper

revenue is driven by conversion of

USSU to our paper

Excluding the conversion, net

commissions and fees were up

slightly in 2011

commissions and fees were up

slightly in 2011

The increase in GS&A relates

primarily to investments in sales

initiatives to stimulate revenue growth

in net commissions and fees

primarily to investments in sales

initiatives to stimulate revenue growth

in net commissions and fees

Other Expenses

Reduction in other expenses driven

by a reduction in the variable

compensation expense accrual in the

current quarter, interest rate and

reduction of scheduled amortization

by a reduction in the variable

compensation expense accrual in the

current quarter, interest rate and

reduction of scheduled amortization

4

Loss and LAE Ratio

The 2011 loss ratio includes 1.9 points of favorable

development compared to 6.4 points of favorable

development in 2010.

development compared to 6.4 points of favorable

development in 2010.

The accident year loss ratio improved to 63.6%

from 64.2%, driven primarily by:

from 64.2%, driven primarily by:

Lower level of losses in 2011 as

compared to 2010 on certain short-tail

lines of business

compared to 2010 on certain short-tail

lines of business

Anticipated benefit of rate and

underwriting actions effectuated in 2010

underwriting actions effectuated in 2010

Expense Ratio

The 2011 expense ratio decreased 0.6 points in

comparison to the same 2010 period. The

decrease was primarily driven by:

comparison to the same 2010 period. The

decrease was primarily driven by:

Decrease in insurance related

assessments

assessments

Continued leveraging of fixed costs over

a larger premium base

a larger premium base

(in thousands, except ratios)

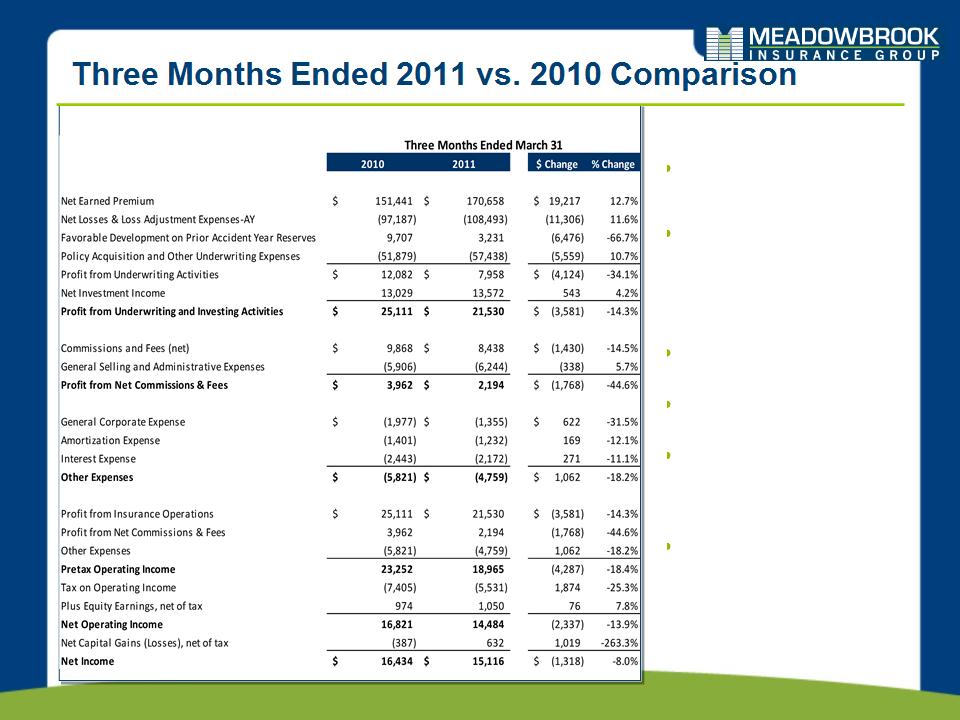

Calendar Year Ratios | 3 months ended 2010 | 3 months ended 2011 | |

Net Earned Premium | $ 151,441 | $ 170,658 | |

Net Loss and Loss Adjustment Expense | (87,480) | (105,262) | |

GAAP Net Loss and LAE Ratio | 57.8% | 61.7% | |

Policy Acquisition and Other Underwriting Expenses | (51,879) | (57,438) | |

GAAP Expense Ratio | 34.3% | 33.7% | |

GAAP Combined Ratio | 92.1% | 95.4% | |

Accident Year Ratios | |||

Calendar Year GAAP Net Loss and LAE Ratio | 57.8% | 61.7% | |

Favorable Prior Year Development | $9,707 | $3,231 | |

Impact of Favorable Prior Year Development | 6.4% | 1.9% | |

Accident Year Loss Ratio | 64.2% | 63.6% | |

GAAP Expense Ratio | 34.3% | 33.7% | |

Accident Year Combined Ratio | 98.5% | 97.3% | |

5

ROE Components

We have generated predictable earnings over the past two years, meeting our target

ROAE range of 10% - 17%.

ROAE range of 10% - 17%.

*2011 figures are annualized for comparative purposes

6

ROAE & Combined Ratio Illustration

2010 - ROAE of 11.4%, Combined Ratio of 95.0% and Investment Yield of 4.2%

2011 - Annualized ROAE of 10.9%, QTD Combined Ratio of 95.4% and Investment

Yield of 4.2% as of 3/31

Yield of 4.2% as of 3/31

2010 A

We strive to deliver predictable earnings across the market cycle with a return on average

equity target of 10% - 17%.

equity target of 10% - 17%.

7

Investment Portfolio Appendix

8

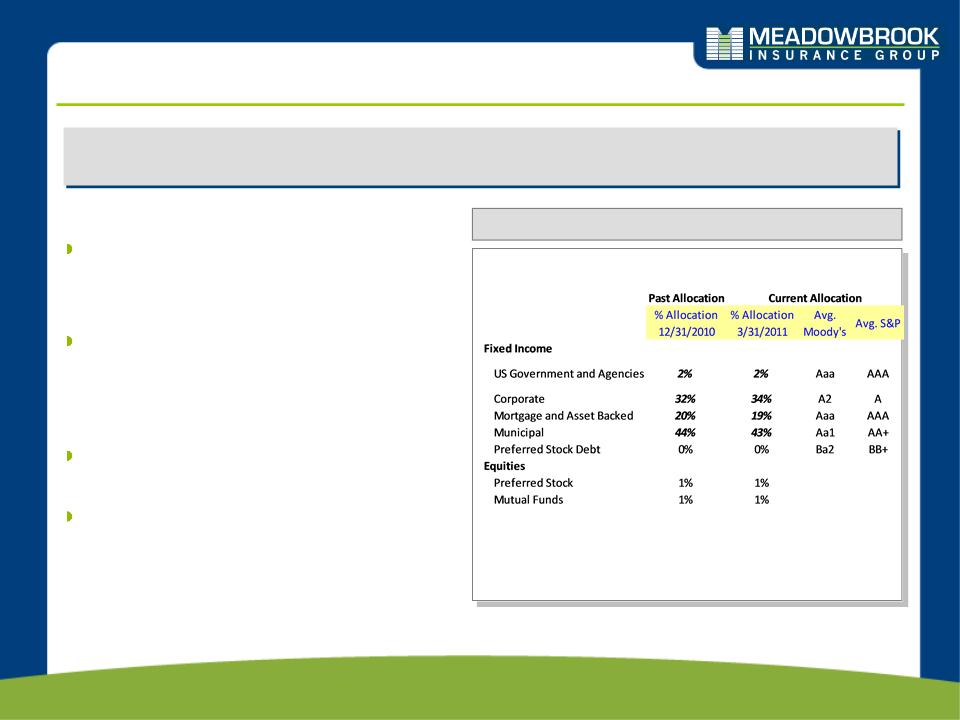

We Maintain a High Quality, Low Risk Investment Portfolio

We maintain a conservative investment portfolio

Portfolio Allocation and Quality

Allocation based on market value

Low equity risk exposure

– 98% fixed income and cash

– 2% equity

High credit quality

– 98% of bonds are investment grade

– Average S&P rating of AA / Moody’s

of Aa2

of Aa2

The effective duration of our $1.3 billion

portfolio is 5.1 years

portfolio is 5.1 years

The duration on net reserves of $802

million is approximately 3.4 years

million is approximately 3.4 years

NOTE: Data above as of March 31, 2011

9

Municipal Bonds—March 31, 2011 Profile

State Profile

Municipals v. Entire Portfolio

Quality Indicators

$545 million market value; 43% of the

investment portfolio

investment portfolio

March 31, 2011 net unrealized gain was

$19.2M

$19.2M

Tax exempt unrealized gain $18.8M

Taxable unrealized gain $ 0.4M

Average tax equivalent yield: 5.52%

FMV as a % of BV is 103.7% as of March 31,

2011

2011

Summary Profile

Credit Enhancements*

Based on market value

10

Structured Securities—March 31, 2011 Profile

$246 million market value; 19% of the managed

portfolio

portfolio

March 31, 2011 unrealized gain was $11.7M

RMBS unrealized gain $ 9.9M

CMBS unrealized gain $ 0.7M

ABS unrealized gain $ 1.1M

Average investment yield: 5.10%

Quality Indicators

Structured Profile

Summary Profile

11

Corporate Fixed Income—March 31, 2011 Profile

Quality Indicators

$433 million market value; 34% of the

investment portfolio

investment portfolio

March 31, 2011 unrealized gain was

$17.7M.

$17.7M.

Average investment yield: 4.43%

Summary Profile

Corporate’s v. Entire Portfolio

Corporate’s Profile

12

Government and Agency—March 31, 2011 Profile

$24 million market value; approximately

2% of the managed portfolio

2% of the managed portfolio

100% rated AAA

March 31, 2011 unrealized gain was $1.0

million

million

Average investment yield: 3.26%

Government and Agency v. Entire Portfolio

Summary Profile

Government v. Agency

13

Equities—March 31, 2011 Profile

Equity Mix Profile

Equities v. Entire Portfolio

Top 5 Equity Holdings

$29 million market value; 2% of the managed

portfolio

portfolio

March 31, 2011 unrealized gain was $3.5M

Preferred stock unrealized gain $2.4M

Bond mutual fund unrealized gain $1.1M

Average tax equivalent yield: 7.66%

Summary Profile