5

Diverse Revenue

Sources

Earned premium from insurance operations

Fee revenue from risk management services

Flexibility to utilize multiple distribution channels

Positioned to Manage

Insurance Cycles

Conservative

Investment

Philosophy

Ability to Attract and

Retain Talented

Professionals

Our model allows us to deliver more predictable results

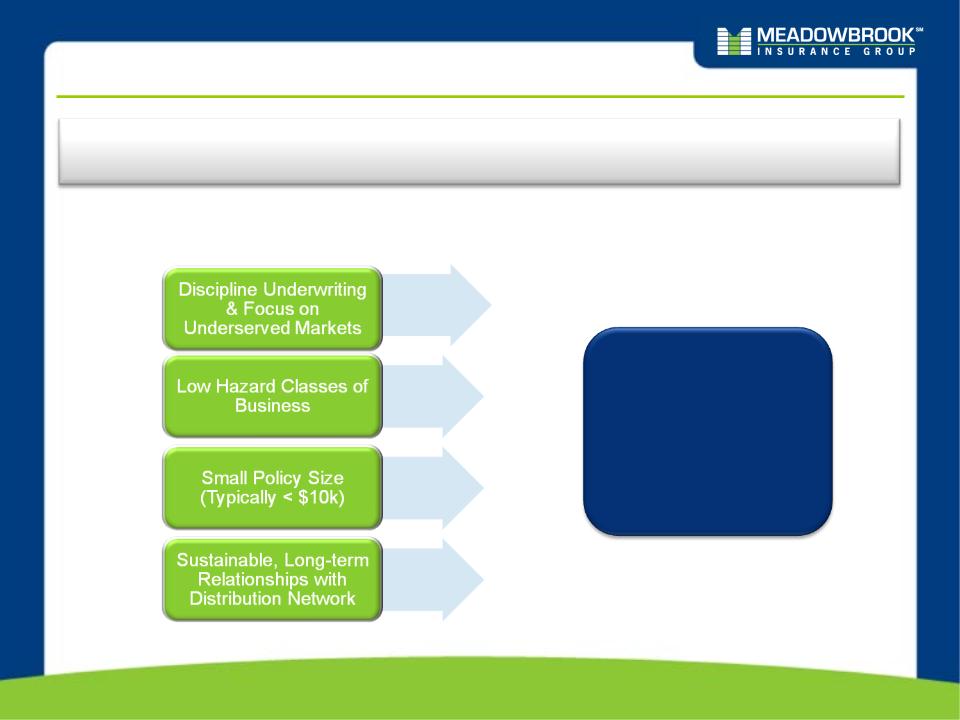

Product, program and geographic diversification

Admitted market capabilities contribute to stability and higher renewal retention

Non-admitted capabilities enable opportunistic response in volatile pricing environment

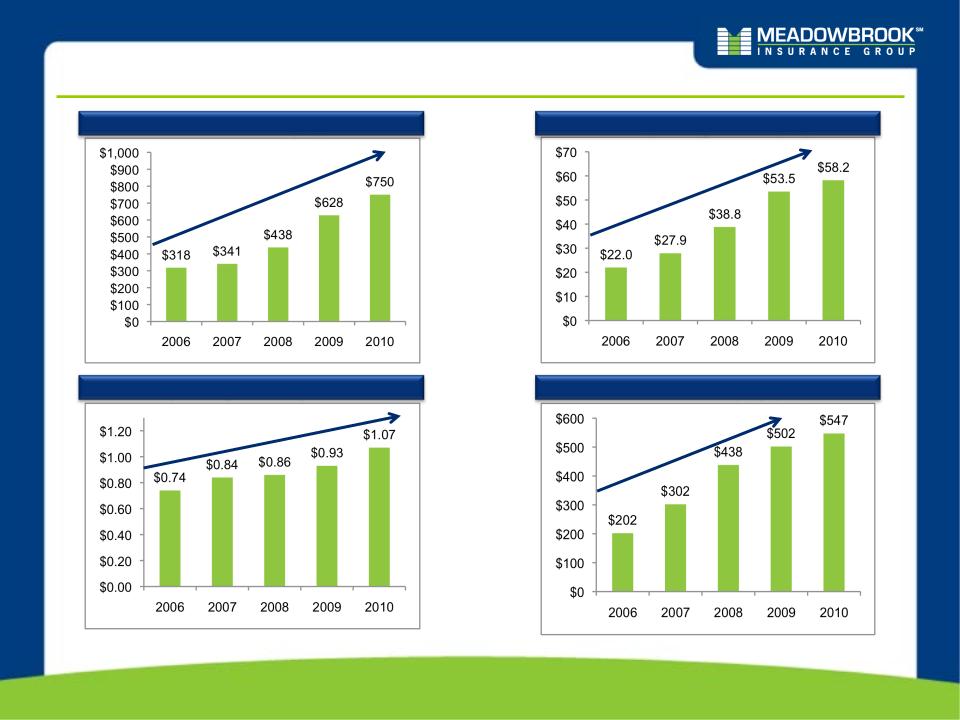

High-quality fixed income approach to our $1.3 billion portfolio

Investment approach reinforces our focus on underwriting profitability

Insurance subsidiaries rated A- (Excellent) by A.M. Best

Insurance subsidiary surplus levels can support meaningful premium growth

Insurance subsidiaries have additional borrowing capacity through FHLB membership

Generate cash flows from both regulated and non-regulated sources, which provides

flexibility

Manageable debt levels, with access to $35 million line of credit

(no outstanding balance)

Strong Capital and

Liquidity Position

Team of talented insurance professionals with a wide range of expertise across all

functions and lines of business

Regional structure enables associates to deliver strong and responsive local service

to clients

What Makes Us Different:

We are Flexible and are Able to Adapt to Changing Market Conditions