Creating a Retail Powerhouse Investor Presentation Filed by SUPERVALU INC. Pursuant to Rule 425 under the Securities Act of 1933 Subject Company: SUPERVALU INC., File #1-5418 Exhibit 99.2 |

2 Forward-Looking Statement CAUTIONARY STATEMENTS RELEVANT TO FORWARD-LOOKING INFORMATION FOR THE PURPOSE OF “SAFE HARBOR” PROVISIONS OF THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995 Except for the historical and factual information contained herein, the matters set forth in this filing, including statements as to the expected benefits of the acquisition such as efficiencies, cost savings, market profile and financial strength, and the competitive ability and position of the combined company, and other statements identified by words such as “estimates,” “expects,” “projects,” “plans,” and similar expressions are forward-looking statements within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are subject to risks and uncertainties that may cause actual results to differ materially, including required approvals by Supervalu and Albertsons shareholders and regulatory agencies, the possibility that the anticipated benefits from the acquisition cannot be fully realized or may take longer to realize than expected, the possibility that costs or difficulties related to the integration of Albertsons operations into Supervalu will be greater than expected, the impact of competition and other risk factors relating to our industry as detailed from time to time in each of Supervalu’s and Albertsons reports filed with the SEC. You should not place undue reliance on these forward-looking statements, which speak only as of the date of this press release. Unless legally required, Supervalu undertakes no obligation to update publicly any forward-looking statements, whether as a result of new information, future events or otherwise. ADDITIONAL INFORMATION Supervalu and Albertsons will file a joint proxy statement/prospectus with the Securities and Exchange Commission (SEC). INVESTORS ARE URGED TO READ THE JOINT PROXY STATEMENT/PROSPECTUS WHEN IT BECOMES AVAILABLE BECAUSE IT WILL CONTAIN IMPORTANT INFORMATION. You will be able to obtain the joint proxy statement/prospectus, as well as other filings containing information about Supervalu and Albertsons, free of charge, at the website maintained by the SEC at www.sec.gov. Copies of the joint proxy statement/prospectus and the filings with the SEC that will be incorporated by reference in the joint proxy statement/prospectus can also be obtained, free of charge, by directing a request to Supervalu, Inc., 11840 Valley View Road, Eden Prairie, Minnesota, 55344, Attention: Corporate Secretary, or to Albertsons, Inc., 250 East Parkcenter Boulevard, Boise, Idaho, 83706-3940, Attention: Corporate Secretary. The respective directors and executive officers of Supervalu and Albertsons and other persons may be deemed to be participants in the solicitation of proxies in respect of the proposed transaction. Information regarding Supervalu’s directors and executive officers is available in its proxy statement filed with the SEC by Supervalu on May 12, 2005, and information regarding Albertsons directors and executive officers is available in its proxy statement filed with the SEC by Albertsons on May 6, 2005. Other information regarding the participants in the proxy solicitation and a description of their direct and indirect interests, by security holdings or otherwise, will be contained the joint proxy statement/prospectus and other relevant materials to be filed with the SEC when they become available. Investors should read the joint proxy statement/prospectus carefully when it becomes available before making any voting or investment decisions. |

3 Transaction Overview • SUPERVALU, CVS and Cerberus-led investment group to acquire Albertsons for $17.4 billion in cash, stock and assumption of debt. – SUPERVALU to acquire Acme Markets, Bristol Farms, Jewel-Osco, Shaw’s Supermarkets, Star Markets, and 569 Albertsons stores, as well as in-store pharmacies under the Osco Drug and Sav-on names. The Albertsons stores are located in Idaho, Southern California, Nevada, Utah and the northwestern United States. – CVS to acquire stand-alone pharmacy operations. – Cerberus and its partners, Kimco Realty and Schottenstein Realty, to acquire remaining retail properties. • SUPERVALU’s consideration equals approximately $12.4B. – $3.8B in cash – $2.5B in stock – $6.1B assumption of debt |

4 SUPERVALU Transaction Highlights To be acquired by Cerberus Dallas - Ft. Worth, Florida, Northern California, Rocky Mountain and Southwest OTHER RETAIL PROPERTIES To be acquired by CVS STAND-ALONE DRUG ALBERTSONS To be acquired by SUPERVALU Acme Markets, Bristol Farms, Jewel-Osco, Shaw’s Supermarkets, Star Markets, and 569 Albertsons stores, as well as in-store pharmacies under the Osco Drug and Sav-on names. FOOD RETAILING Total Stores: 1,126 FY 2006E Revenues: $24.5B FY 2006E EBITDA: $1.77B % Margin 7.2% |

5 The Right Deal at the Right Time • Years of operational and financial staging have prepared us – Strong regional chains – Local market strategy – Strong supply chain backbone – Empowered local management teams • Proven ability to manage a variety of retail formats • Track record of successful integration of acquisitions |

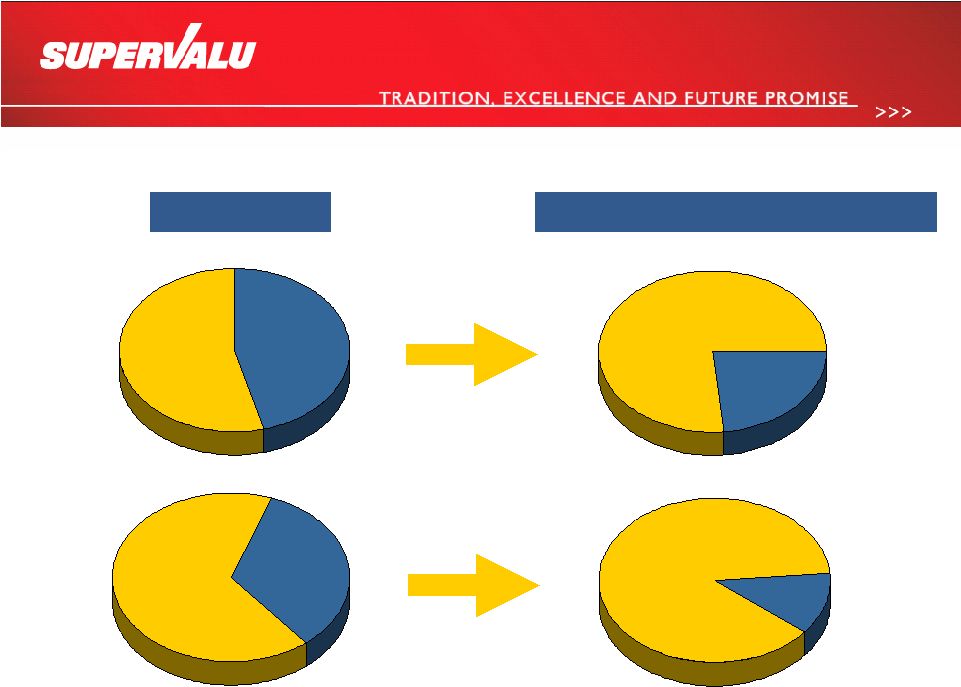

6 Strategic Overview • Transformational in scale and scope. – Doubles SUPERVALU’s revenue to $44 billion proforma (FY’ 06E). – Triples SUPERVALU’S Food Retail revenues to $35 billion proforma (FY’ 06E). Almost triples SUPERVALU’s EBITDA to $2.7 billion proforma (FY’ 06E). • Enhances industry ranking – Elevates SUPERVALU to the No. 2 spot in the grocery industry – measured by revenue. – New SUPERVALU will have the nation’s largest grocery network with 2,653 stores. • Adds leading positions in key markets across the United States. – Obtains leading positions in Boston, Chicago, Las Vegas, Los Angeles, Orange County, Philadelphia and San Diego. • Expands SUPERVALU’s supply chain footprint. • Provides synergies of approximately $150-175 million pretax to the new SUPERVALU. • Significantly changes SUPERVALU’s business model with expanded retail operations, providing enhanced growth prospects. – 89% of Company’s EBITDA will be in the higher-growth retail segment. |

7 Strengthening Our Business SUPERVALU $.3B 33% EBITDA: $.9B EBITDA: $2.7B $.3B 11% $2.4B 89% $9B 20% Revenue: $44B $35B 80% Retail Revenue: $19B $.6B 67% NEW SUPERVALU Proforma $9B 47% $10B 53% Supply Chain Retail Supply Chain Retail Supply Chain Retail Supply Chain Reflects SUPERVALU First Call and Albertsons management estimates for Fiscal 2006 |

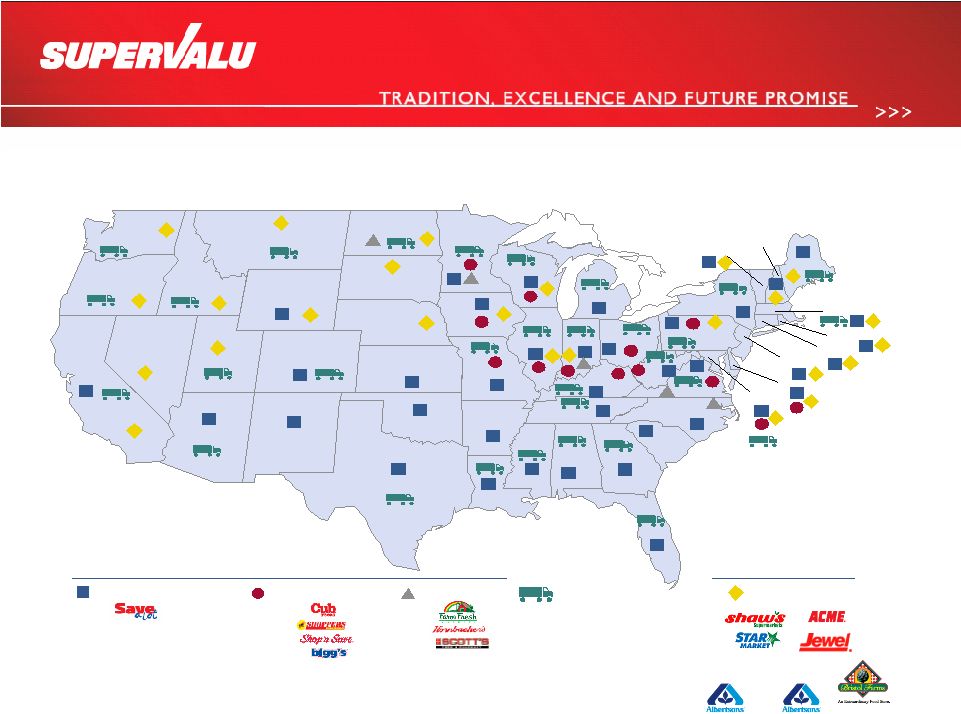

8 SUPERVALU’s Current Footprint • SUPERVALU has a retail or distribution presence in 42 states, and is predominately focused in the East, Southeast and Midwest (1) Includes 27 TLC owned or managed facilities Supermarkets Extreme Value Stores Price Superstores Supply Chain Services/ Distribution Centers (1) Texas New Mexico Colorado Wyoming Montana Idaho California Arizona Nevada Utah Washington Oregon North Dakota South Dakota Nebraska Kansas Oklahoma Arkansas Missouri Iowa Minnesota Michigan Wisconsin Illinois Indiana Ohio Pennsylvania New York Kentucky Tennessee Louisiana Mississippi Alabama Georgia Florida Maine South Carolina North Carolina Virginia West Virginia Massachusetts New Hampshire Vermont Connecticut New Jersey Delaware Maryland Rhode Island 18 23 15 5 6 1 89 31 64 20 48 1 18 7 3 7 117 1 18 20 39 12 92 62 1 22 53 22 9 43 4 105 16 18 55 13 3 9 103 1 19 22 40 39 17 7 3 2 1 3 3 1 2 2 5 6 3 2 1 1 4 3 1 4 2 1 8 2 2 9 7 2 14 1 2 37 1 17 1 3 1 1 1 |

9 Current Footprint of To-Be Acquired Retail Stores Banners Combination / Conventional Stores 85 55 Oregon Washington Montana Idaho Utah Arizona New Mexico Colorado Wyoming North Dakota South Dakota Nebraska Kansas Missouri Oklahoma Texas Arkansas Louisiana Iowa Minnesota Wisconsin Illinois Indiana Ohio Michigan Kentucky Tennessee Mississippi Alabama Georgia South Carolina North Carolina Virginia West Virginia Pennsylvania New York Vermont Maine New Hampshire Massachusetts Rhode Island Connecticut New Jersey Delaware Maryland Florida 43 34 49 1 1 2 1 15 180 6 53 18 23 35 94 17 25 61 12 8 32 85 279 California Nevada Northwestern / Intermountain Southern California |

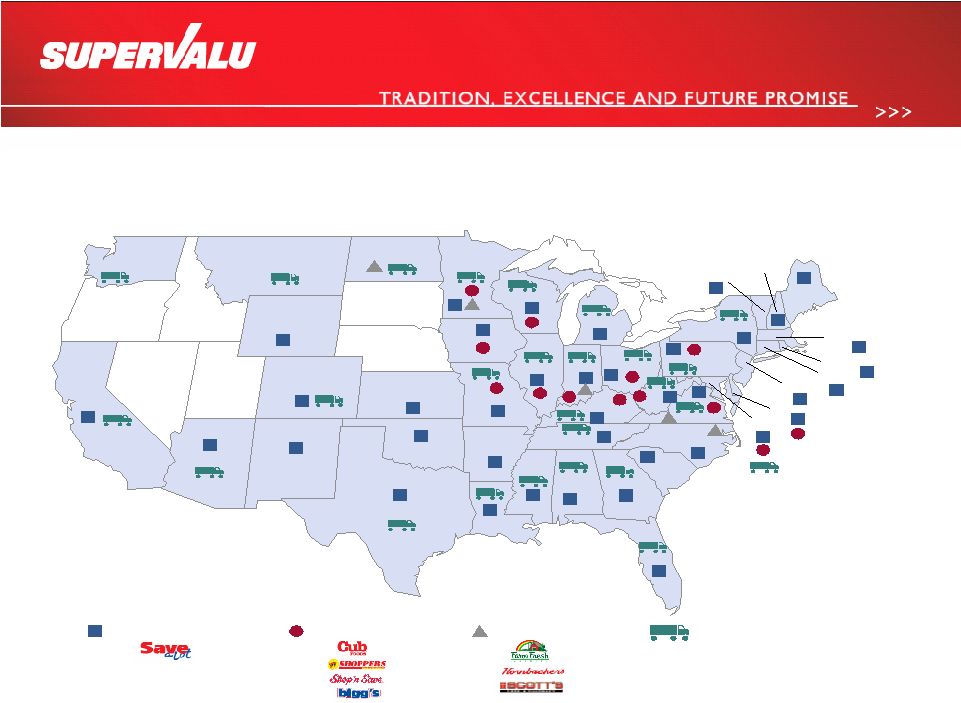

10 Proforma Operations Footprint of new SUPERVALU Will have a retail presence in 48 states and the District of Columbia Supermarkets Supply Chain Services/ Distribution Centers (1) Supermarkets Price Superstores Extreme Value Stores SUPERVALU New Banners Texas New Mexico Colorado Wyoming Montana Idaho California Arizona Nevada Utah Washington Oregon North Dakota South Dakota Nebraska Kansas Oklahoma Arkansas Missouri Iowa Minnesota Michigan Wisconsin Illinois Indiana Ohio Pennsylvania New York Kentucky Tennessee Louisiana Mississippi Alabama Georgia Florida Maine South Carolina North Carolina Virginia West Virginia Massachusetts New Hampshire Vermont Connecticut New Jersey Delaware Maryland Rhode Island 18 23 15 5 6 1 89 31 64 20 48 1 18 7 3 7 117 1 18 20 39 12 92 62 1 22 53 22 9 43 4 105 16 18 55 13 3 9 103 1 19 22 40 39 17 7 3 2 1 3 3 1 2 2 5 8 3 2 1 1 5 3 1 6 1 2 1 8 2 2 9 7 2 14 1 2 37 1 17 1 279 55 85 34 43 47 32 2 180 15 6 1 2 61 53 94 16 25 35 18 12 8 22 1 1 3 1 1 1 1 1 1 1 (1) Includes 27 TLC owned or managed facilities Northwestern / Intermountain Southern California |

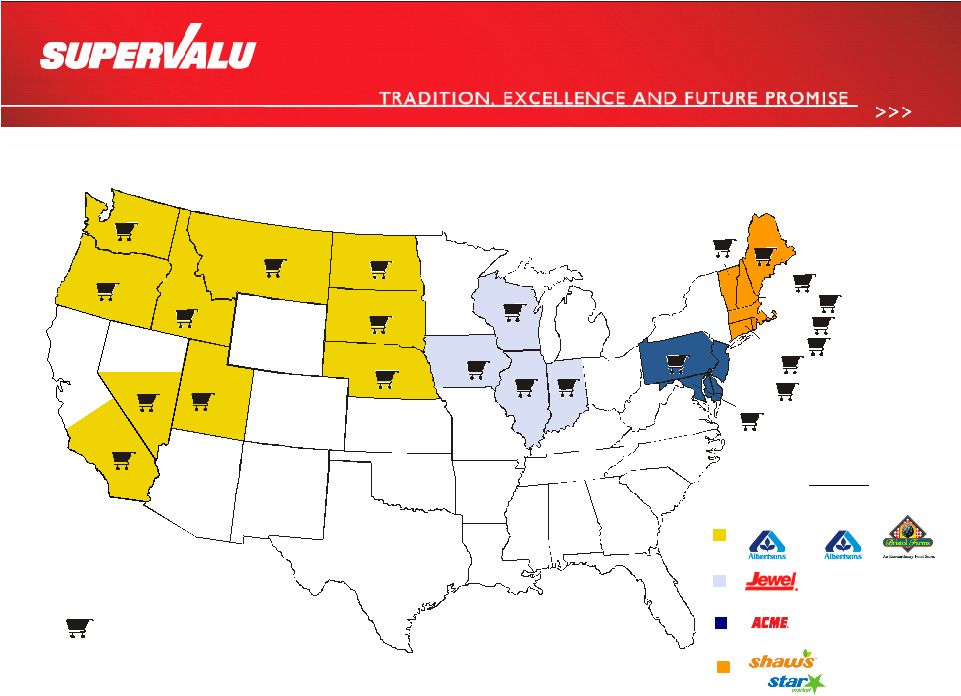

11 Second-largest grocery retailer in the United States, operating numerous well-known national and regional banners. Food Retailing Operations to be Acquired by SUPERVALU BANNERS DESCRIPTION STORES KEY MARKETS 134 Delaware, Maryland, Pennsylvania and New Jersey; largely concentrated in the Philadelphia metropolitan area For more than a century, Acme has built a reputation for quality products, low prices and friendly service. Acme holds the No. 1 market share in Philadelphia. Stores include conventional supermarkets and combination food and drug stores under the Acme Sav-on banner. 11 Southern California This upscale southern California gourmet and specialty food retailer is known for its innovative approach to grocery retailing. A unique atmosphere, specialty items and friendly service have won it numerous awards. Northwestern / Intermountain 258 Idaho, Montana, Nevada, Utah, Oregon and Washington; largely concentrated in Boise, Portland, Salt Lake City and Seattle metropolitan areas With No. 1 market share in Boise and Salt Lake City, Albertsons is the leading grocery chain in much of this region with conventional supermarkets and combinations food and drug stores. These combination stores offer a convenient one-stop shopping experience. Southern California 311 California and Nevada; largely concentrated in the metropolitan areas of Las Vegas, Los Angeles, Orange County and San Diego With the leading share in fast-growing metropolitan areas like Las Vegas, Orange County and San Diego, these Albertsons banner stores include conventional supermarkets and combination stores under the Albertsons/Sav-on banner. 210 Shaw’s and Star Market are both well-established in the New England market. With roots reaching back to the Civil War, Shaw’s ranks No. 2 in the Boston Market. Stores include conventional supermarkets and Shaw’s Osco combination food and drug stores. Six New England states; largely concentrated in Boston, Hartford and Providence metropolitan areas 200 Illinois, Indiana and Wisconsin; largely concentrated in the Chicago and Milwaukee metropolitan areas Prime locations, one-stop shopping services and a loyal customer base have helped give Jewel-Osco the No. 1 market share in the Chicago area. Stores include conventional Jewel supermarkets and combination food and drug stores under the Jewel-Osco banner. |

12 For more than a century, Acme has built a reputation for quality products, low prices and friendly service. Stores include conventional supermarkets and combination food and drug stores under the Acme Sav-On banner. Number of Stores Key Markets 134 Delaware, Maryland, Pennsylvania and New Jersey; largely concentrated in the Philadelphia metropolitan area No. 1 in Philadelphia |

13 Bristol Farms is an upscale southern California gourmet and specialty food retailer known for its innovative approach to grocery retailing. Bristol Farms’ unique atmosphere, specialty items and friendly service have led to numerous awards. Number of Stores Key Market 11 Southern California Upscale, Gourmet |

14 Prime locations, one-stop shopping services and a loyal customer base have helped make Jewel-Osco a household name. Stores include conventional Jewel supermarkets and combination food and drug stores under the Jewel-Osco banner. Number of Stores Key Markets 200 Illinois, Indiana and Wisconsin; largely concentrated in Chicago and Milwaukee metropolitan areas No. 1 in Chicago |

15 Northwestern / Intermountain Albertsons is the leading grocery chain in much of the Northwestern and Intermountain regions. Albertsons conventional supermarkets and combination food and drug stores offer a convenient, one-stop shopping experience. Number of Stores Key Markets 258 Idaho, Montana, Nevada, Oregon, Utah and Washington; largely concentrated in Boise, Portland, Salt Lake City and Seattle metropolitan areas No. 1 in Boise, Salt Lake City |

16 With roots reaching back to the Civil War, Shaw’s Supermarkets and Star Market are both well-established in the New England market. Stores include conventional supermarkets and Shaw’s Osco combination food and drug stores. Number of Stores Key Markets 210 Six New England states; largely concentrated in Boston, Hartford and Providence metropolitan areas No. 2 in New England |

17 Southern California Albertson’s Southern California region is one of the fastest-growing divisions of Albertsons, with stores located in some of the most rapidly expanding cities in the country. Stores include conventional supermarkets and combination stores. Number of Stores Key Markets 311 California and Nevada; largely concentrated in Las Vegas, Los Angeles, Orange County and San Diego metropolitan areas No. 1 in Las Vegas, Orange County |

18 Key Financial Highlights • SUPERVALU’s consideration equals approximately $12.4B. – $3.8B in cash – $2.5B in stock – $6.1B assumption of debt • EBITDA multiple of 7.0X • Newly capitalized company will be formed, comprised of: – SVU shareholders – approximately 65% – ABS shareholders – approximately 35% • SUPERVALU will continue to pay dividends. • Expected to close by summer 2006. |

19 New SUPERVALU Provides: Broad-based Future Growth Potential and Immediate Diluted Earnings Per Share Accretion on Annualized Basis Excluding One-Time Costs • Expect transaction to be immediately double-digit accretive when excluding one-time costs of approximately $125 million. • Proforma FY’06 EBITDA margins increase 140 basis points from 4.8% to 6.2% through combination. • EBITDA margins expected to increase by additional 30 - 40 basis points to 6.5% - 6.6% after combined entity synergies of $150-175 million realized. |

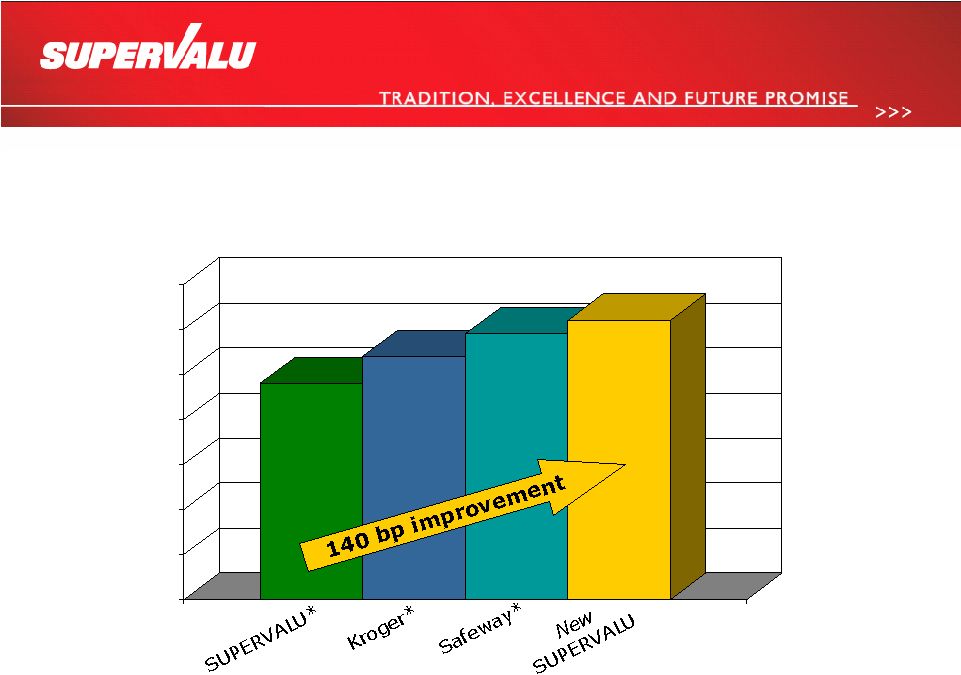

20 Looking at the Impact Another Way 0 1 2 3 4 5 6 7 EBITDA % Compared to our Peers 6.2% 5.9% 5.4% 4.8% * First Call analyst estimates for Fiscal 2006 |

21 Synergies of the New SUPERVALU Approximately $150-$175 million of pretax synergies by the end of the third full year. Supply Chain Optimization Retail Leverage and Efficiencies Corporate Synergies $25-$30 million $75-$85 million $50-$60 million Total Synergies $150-$175 million |

22 Illustrative EPS Accretion +35% +17% Accretion 224 $3.02 $677 1,110 (995) (745) 150 $2,700 Combined with Synergies $2.61 $2.24 EPS $ in million except EPS 224 78 146 Share Count Fully Diluted $585 $265 $320 Net Income 960 452 508 Pretax (995) (683) (312) Depreciation/Amortization (745) (630) (115) Net Interest Expense Synergies $2,700 $1,765* $935 EBITDA Combined w/o Synergies Combination Adjustments SUPERVALU F’06E First Call * EBITDA represents Albertsons management estimates for Fiscal 2006 |

23 Debt/EBITDA Illustrative Combined Leverage $ in million 3.6 4.6 1.8 Debt/EBITDA 2,700 1,765 935 EBITDA 9,718 8,035 1,683 Debt Combined Combination Adjustments SUPERVALU FY’06 E EBITDA represents SUPERVALU First Call and Albertsons management estimates for Fiscal 2006 |

24 Illustrative Combined Free Cash Flow (Excluding One-Time Transaction Costs) $ in million 540 371 169 Free Cash Flow (925) (550) (375) Cash Capital Expenditures (150) (62) (88) Dividends (375) (187) (188) Income Taxes (710) (595) (115) Interest (cash) 2,700 1,765* 935 EBITDA Combined Combination Adjustments SUPERVALU F’06E First Call * EBITDA represents Albertsons management estimates for Fiscal 2006 |

25 Illustrative Combined Key Metrics 224M N/A 146M Share Count Fully Diluted 65% N/A 39% Debt-to-Capital Ratio $1.1B $650M $450M Capital Spending 6. 2% 7.2% 4.8% EBITDA Margins $2.7B $1.77B $0.9B EBITDA $43.8B $24.5B $19.3B Revenue 198,000 144,000 54,000 Employees 896 722 174 In-store Pharmacies 2,656 1,124 1,532 Store Network New SUPERVALU Business to be Acquired SUPERVALU EBITDA is SUPERVALU’s First Call and Albertsons management estimates for Fiscal 2006 |

26 Next Steps • Earn regulatory approvals • Issue proxy, gain shareholder approval • Transition planning underway • Close summer 2006 • Launch transition plan post-close – In full coordination with future management team – Be paced and thoughtful – Complete in three years – Synergies fully implemented by end of the third year |

27 THE NEW • Become No. 2 grocery retailer in the nation. • Leverage size and scale of supply chain enterprise. • Expand broad portfolio of industry’s best regional nameplates. • Acquire desirable assets: Great Brands, Great Locations, Great People. • Realize synergy potential through better procurement scale, optimized supply chain and retail expertise. • Maximize growth opportunity that is exceptional and deliverable. – Significantly enhanced business model with higher EBITDA margins, EPS and cash flow generation Formidable Retail Powerhouse |

28 THE NEW Northwestern / Intermountain Southern California |