FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

Corporate Offices

PO Box 990

Minneapolis, MN 55440

(952) 828-4000

December 17, 2008

VIA EDGAR CORRESPONDENCE

Mr. Andrew Mew

Accounting Branch Chief

Office of Consumer Products

Division of Corporation Finance

Securities and Exchange Commission

100 F Street, N.E.

Washington, D.C. 20549

| Re: | SUPERVALU INC. Form 10-K for the Fiscal Year Ended February 23, 2008 Form 10-Q for the Fiscal Quarter Ended June 14, 2008 and September 6, 2008 File No. 1-5418 |

Dear Mr. Mew:

SUPERVALU INC. (the “Company”), respectfully submits this response to the comments of the Staff of the Division of Corporation Finance (the “Staff”) of the Securities and Exchange Commission (the “Commission”), received by facsimile on November 10, 2008, to the above-referenced filings. For your convenience, we have set forth each of the Staff’s comments immediately preceding each of our responses.

Form 10-K for the Fiscal Year Ended February 23, 2008

Consolidated Financial Statements

Notes to Consolidated Financial Statements

Note 17—Segment Information, page F-43

| 1. | We note the supplemental information and response to our prior comments two, three and four. Based on what you have provided, your chief operating decision maker (“CODM”) receives financial information in several formats to evaluate performance and allocate resources, and uses anticipated levels of sales, expected return on investment, EBIT as a percent of sales as well as other factors. You also |

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

state you manage your retail food business by region and have identified five operating segments which are being aggregated into one reportable segment — Retail Food. In this regard, the reports you currently provide on a regular basis to the CODM and the Board, based on the sample provided to us, do not show information for the operating segments you have identified in your response. Instead, there appears to be three operating segments within your Retail Food reportable segments that qualify as operating segments as defined by paragraph 10 based on the reports provided to your CODM which present discrete financial information by store brand grouped by the retail food stores of Albertson’s, Inc., (“Acquired Operations”), Core Retail and Save-A-Lot (“Extreme Value food stores”), aggregated into the Retail Food reportable segment. |

| Further, it appears each of the Acquired Operations, Core Retail and Extreme Value stores as grouped in your reports have sufficient dissimilar economic characteristics when compared to each other to disqualify them from aggregation under paragraph 17 of SFAS 131. Using historical data you provided, the retail food operations as grouped in reports provided to the CODM, do not appear to have the ability to converge over the long-term to attain similar EBIT or gross margin operating trends indicating there are dissimilar economic characteristics supporting separate reportable operating segments. Please revise your segment reporting and related disclosures to present three or more reportable retail food segments to comply with the reporting requirements of SFAS 131. Please advise or show us what your revised disclosures will look like. |

Response:

Executive Summary

The Company’s prior response did not provide the Staff with a sufficiently comprehensive view of the facts and circumstances with respect to the Company’s segment reporting and related disclosure and the thought process and analysis that the Company undertook in arriving at its conclusion on reportable segments. In particular, the Company’s response did not fully describe the two possible and reasonable views that have been considered regarding the application of Statement of Financial Accounting Standards No. 131, “Disclosures about Segments of an Enterprise and Related Information” (“SFAS 131”) and the overall conclusion that the Company has two reportable segments: Retail Food and Supply Chain Services. Our CODM allocates resources and assesses the Company’s performance based on these two reportable segments. When making decisions with respect to budgeting, forecasting and allocating all of the resources of the Company, the CODM receives information from various sources, but makes decisions at the Retail Food and Supply Chain Services segments on a national basis.

We believe the Company’s retail food business may be viewed in either of two ways (or somewhat of a combination of both) based on the guidance provided in SFAS 131:

| (i) | as five retail operating segments with regional managers reporting to the CODM; or |

-2-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

| (ii) | as one Retail Food operating segment with the CODM also acting as the segment manager for Retail Food. |

We do not believe that the Company’s facts and circumstances clearly suggest that one approach is more correct than the other. Rather, they suggest that the combined analysis produces a reasonable and appropriate result that is consistent with the objectives of SFAS 131. Under either scenario, whether we are viewed as having five retail operating segments during this period or one retail food operating segment with the CODM as the segment manager, we respectfully submit that the result is the same: the Company correctly disclosed one Retail Food reportable segment.

Prior to our transformational acquisition of New Albertson’s, Inc. (“NABS”) on June 2, 2006 (the “Acquisition”), the Company operated with one Retail Food segment and did not have geographic regional managers. Immediately after the Acquisition, regional manager positions were established for each of these regional groupings to provide more direct oversight of the large number of newly acquired stores and to manage their integration into the Retail Food segment.1 Consequently, the CODM looked to the regional managers as a way of having closer oversight of the stores on a national basis. Because the Company facilitates the managing of the day-to-day operations of its retail operations by virtue of the regional groupings, they might be viewed under SFAS 131 as operating segments and thus the Company incorporated this view into its prior segment analysis. However, other than with respect to same store sales data, a breakdown of the operating performance of Retail Food by geographic region has never been provided in the reports furnished to the CODM during this period, suggesting that these geographic regions may not qualify as operating segments.2 Throughout this transitional period, the CODM allocated resources and made decisions based on only two reportable segments.

In support of the view that the Company only had one Retail Food reportable segment, we note that during this period the CODM allocated the resources of the Company at a national level and did not make decisions regarding budgeting or forecasting based on the regional groupings described above, a fact that would be supportive of the view that the CODM was the segment manager of Retail Food and that Retail Food could be viewed as the Company’s sole retail operating segment.

The Company’s presentation of two reportable segments of Retail Food and Supply Chain Services is identical to the presentation in our periodic reports, complies with SFAS 131, and provides users of our financial statements with meaningful information about our Retail Food and Supply Chain Services businesses that enables investors to understand the Company’s performance, assess the Company’s prospects for future net cash flows and make informed judgments about the Company. As a result, while we acknowledge the Staff’s request that we revise our segment reporting and related disclosures, we respectfully submit that our segment reporting and related disclosures have been accurately reflected in our financial statements as two reportable segments and that no revision is required.

1 | The Acquisition represented an approximately 214% increase in the number of owned stores in our portfolio. |

2 | Inclusion of financial information in a report furnished to the CODM is normally a key indicator that operating results are regularly reviewed by the CODM, as contemplated by paragraph 10(b) of SFAS 131. |

-3-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

Operating Structure

We acknowledge that certain of the supplemental information provided in response to the Staff’s prior comments presented data grouped by Acquired Operations, Core Retail and Save-A-Lot. As a result of the transformational nature of the Acquisition and the time necessary to accurately integrate the accounting systems, the CODM reports provided to the Staff were transitory and are not reflective of the way the CODM viewed or managed the business after the Acquisition.3 The presentation of newly acquired stores separate from legacy stores was always intended as a temporary arrangement as a result of:

(i) | the dual accounting systems that required careful and methodical integration in accordance with the Company’s obligations under Section 404 of the Sarbanes-Oxley Act of 2002 (“SOX”);4 |

| (ii) | the CODM’s focus on how the newly acquired stores were performing; and |

| (iii) | the post-acquisition obligation of NABS to file periodic reports with the Commission (as described below). |

The CODM uses the regional managers at each of Retail West, Retail Midwest, Retail East, Save-A-Lot and Bristol Farms, who manage the day to day operations of the retail operations, to facilitate his understanding of the performance of the Company. Although the CODM uses the regional managers for data gathering with respect to the stores in different regions, the CODM at all times allocates resources and assesses the ultimate performance of the Company based on two segments: Retail Food and Supply Chain Services.

At the time of the Acquisition, the Company disclosed that it anticipated that the integration of NABS into the Company would take approximately three years from the date of the Acquisition.5 In the third quarter of fiscal year 2009, we substantially completed the integration of the general ledgers of the two companies. We expect substantially all of the financial systems to be fully integrated by the end of fiscal year 2010 in accordance with the timetable set out at the time of the Acquisition.

3 | The Acquisition transformed the Company. Our book value increased to $5.2 billion as a result of the Acquisition, as compared to $2.6 billion before the Acquisition. Further, the balance between Retail Food and Supply Chain Services shifted dramatically with a much greater percentage of the Company’s EBIT being derived from Retail Food. We had 521 owned stores prior to the Acquisition and 1,637 owned stores immediately after the Acquisition. |

4 | The NABS accounting system ran on an Oracle platform and the Core Retail accounting systems ran on a custom platform. |

5 | For example, immediately after the Acquisition, we announced on June 28, 2006 in connection with the annual meeting of stockholders of SUPERVALU that we anticipated “a three year timeframe to fully realize [the] synergies” of the merger (Form 8-K, filed June 28, 2006). We reaffirmed this in our annual report for the fiscal year ended February 23, 2008 (Form 10-K, filed April 23, 2008) stating that the Company was “implementing its integration plan that commenced on the Acquisition Date” and that the Company expected the integration plan to be “substantially complete within a three-year time frame.” We also disclosed in January 2008 that certain merchandising systems would take longer to fully integrate than originally anticipated (third quarter earnings conference call, January 8, 2008). |

-4-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

The need to integrate the two distinct accounting systems was one of the reasons our CODM reports presented separate financial data for Acquired Operations and Core Retail. The integration of two different systems is a challenging task that has required a substantial number of hours of planning, testing, business process alignment, and implementation to ensure a seamless transition to one general ledger. This transition has been performed with a view to the Company’s compliance with Section 404 of SOX and throughout the integration process we have maintained effective internal control over financial reporting. During the transition, while we appropriately focused on complying with our obligations under SOX, the CODM reports reflected information from both the legacy accounting system and the inherited accounting systems.6

A second reason for this presentation of separate financial data for Acquired Operations and Core Retail during this transition period was to provide the CODM with more information about the newly acquired operations and allow him to compare the results and assess the integration of those newly acquired stores as well as assess the comparable performance of the legacy stores.

Finally, we had to maintain the separate NABS legacy accounting system so that we could file certain reports for NABS under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). In accordance with Rule 12h-3 under the Exchange Act, a company that files a registration statement is not eligible to suspend its reporting requirements in the fiscal year in which the registration statement became effective. The NABS Registration Statement on Form S-4 became effective in April 2006. Therefore, we were required to continue the separate existence of NABS for the purposes of filing Forms 10-Q for the quarter ended August 31, 2006, filed on October 10, 2006, and the quarter ended November 30, 2006, filed January 9, 2007, and the Form 10-K for the fiscal year ended February 22, 2007, filed April 26, 2007. Since the separate reporting was required to comply with Section 13(a) of the Exchange Act, the CODM believed he should have received data on that basis since he was signing the certifications pursuant to Sections 302 and 906 of SOX.

After the Acquisition, the number of grocery stores increased from 521 to 1,637 or by approximately 214%.7 The regional management structure that we describe above was designed to provide greater executive touch points and to facilitate the integration of the large number of new stores. Our management structure has never been aligned on the basis of Acquired Operations, Core Retail and Save-A-Lot and therefore these categories should not be viewed as our retail operating segments. There has not been any personnel structuring based on that distinction nor has the CODM ever allocated resources or assessed the Company’s performance based on that distinction. If the CODM wanted to discuss the results for Acquired Operations or

6 | Even during this transition, certain reports presented to the CODM reflected the geographic segments with respect to same store sales data. See Financial Report, Period 3, Fiscal 2008, May 19, 2007, SUPERVALU Retail 3 Year Trend Identical Store Sales (marked as documents SVU-105 and SVU-106 in our June 9, 2008 supplemental submission to the Staff) and SUPERVALU Identical Store Sales-Fiscal 2008 and -Quarter to Date, (marked as documents SVU-107 and SVU-108 in our June 9, 2008 supplemental submission to the Staff). |

7 | Store numbers and the percent increase in the number of stores exclude 870 independent Save-A-Lot licensee stores. |

-5-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

Core Operations, he would have had discussions with several regional managers. However, the CODM does not view or manage the Company on such a basis. We believe that the guidance provided in paragraphs 13 and 14 of SFAS 131 supports one view that we had five retail operating segments comprised of Retail West, Retail Midwest, Retail East, Save-A-Lot and Bristol Farms.

Each regional manager reports directly to the CODM and provides him with information about the Retail Food business. The regional managers are accountable to and in regular direct contact with the CODM regarding operating activities and regularly discuss operating activities, financial results and proposed plans for their respective regions directly with the CODM. The banner presidents below each of the segment managers report to the segment managers (none of such persons report directly to the CODM). Each regional manager oversees operations of substantially similar size, each of which consists of multiple store formats.8 Our CODM presents the results of operations for Retail Food as a whole directly to our Board of Directors and may direct the regional managers to present information about their respective regions. The Board never receives a presentation from an Acquired Operations or Core Retail manager as neither exists.

The structure chart below reflects the regional managers and illustrates how the regional managers report directly to the CODM.

[CONFIDENTIAL TREATMENT REQUESTED PURSUANT TO RULE 83 (17 CFR 200.83)]

Aggregation of Operating Segments into Retail Food Reportable Operating Segment

If we are viewed as having five retail operating segments, we believe that aggregating the retail operating segments into one reportable operating segment, Retail Food, is consistent with the objective and basic principles set forth in paragraph 3 of SFAS 131.9 Each of the retail operating segments is comprised of the same “types of business activities,” specifically, the

8 | With the exception of Bristol Farms, which consists of only 17 stores, and is not material to the Company’s results of operations, and Save-A-Lot, which is only comprised of one store format. |

9 | SFAS 131 paragraph 3 provides the objective and basic principles of SFAS 131: “The objective of requiring disclosures about segments of an enterprise and related information is to provide information about the different types of business activities in which an enterprise engages and the different economic environments in which it operates to help users of financial statements: a. better understand the enterprise’s performance; b. better assess its prospects for future net cash flows; c. make more informed judgments about the enterprise as a whole.” |

-6-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

business of selling grocery items directly to consumers of groceries, and “economic environments,” specifically, all sales are made within the United States, which is generally subject to the same economic conditions and factors. A user of our financial statements is not focused on our retail food business by geographic region, but is instead looking at the retail food business as a whole in order to understand the Company’s performance, assess its prospects for future net cash flows and make informed judgments about the enterprise as a whole. Additionally, analyst reports also generally focus and report results on the Retail Food segment as a whole, rather than geographic regions. Most importantly, the CODM manages the Retail Food segment on a national basis, not by geographic region, and it is important that the presentation of our financial data accurately reflect such fact.

The Operating Segments Have Similar Economic Characteristics

As indicated above, the Company’s structure could lead one to conclude we have five operating segments. If the Company is viewed as having five operating segments, then we consider whether these operating segments meet the aggregation criteria in SFAS 142. In determining whether the retail operating segments have “similar economic characteristics,” we look to both quantitative and qualitative factors.10 We believe that both the quantitative and qualitative economic characteristics of the Retail West, Retail Midwest, Retail East, Save-A-Lot and Bristol Farms operating segments support aggregation of such retail operating segments into one Retail Food reportable operating segment.

Qualitative Economic Characteristics

The following qualitative economic characteristics support the conclusion that the retail operating segments have similar economic characteristics that apply to grocery stores on a national level, which support aggregation:

| (1) | Sales of each of the operating segments and the stores within those segments are similarly affected by general economic conditions that impact consumer spending habits, such as inflation, unemployment or declining consumer confidence. |

10 | Although not formally issued by the FASB, with regards to interpreting the similarity of economic characteristics of operating segments, the proposed FASB Staff Position FAS 131-a states, in part: |

“4. Q1—Should both quantitative and qualitative factors be considered for purposes of determining whether the economic characteristics of two or more operating segments are similar?

5. A1—The FASB staff believes both quantitative and qualitative factors should be considered for purposes of determining whether the economic characteristics of two or more operating segments are similar. Even if the qualitative factors (including those listed in paragraph 17 of Statement 131) are virtually identical, the FASB staff believes it is still necessary to evaluate the quantitative factors to determine whether the segments have similar economic characteristics. Quantitative factors could include performance measures such as gross margins, trends in sales growth, returns on assets employed, and operating cash flows. Qualitative factors could include nonperformance measures such as competitive and operating risks, currency risks, and economic and political conditions associated with each segment.”

-7-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

| (2) | Costs of sales for each of the operating segments are similarly affected by the same general economic factors, such as inflation, supplier pricing and fuel/transportation costs. |

| (3) | Competitive risks across operating segments are similar, including the risk of new entrants into a market and the risk of local price competition. Our competition is largely national and regional grocery retailers and discount retailers with grocery components. While these competitors can have short-term effects on our results, we do not anticipate changes on a long-term basis from competitor activity in relation to our market share. |

| (4) | Each of the operating segments conducts the same type of business in the retail food industry (i.e., all segments are comprised of grocery stores selling directly to consumers), which, industry wide, is generally a low-margin business consistent throughout the operating segments. |

| (5) | The manner in which the operating segments operate and generate sales is similar. |

| (6) | Our Retail Food operations are largely centralized, with national procurement, purchasing and marketing. |

| (7) | Our Retail Food operations are supported by shared administrative, information technology, finance, human resources and legal staffs and share significant assets such as common distribution facilities, truck fleets and administrative offices. |

Quantitative Economic Characteristics

As discussed in our October 15, 2008 response, we believe that the overall profitability of the retail operating segments, measured by EBIT as a percentage of sales, is the appropriate quantitative measure for assessing whether the Retail West, Retail Midwest, Retail East, Save-A-Lot and Bristol Farms operating segments satisfy the aggregation criteria under SFAS 131 paragraph 17. We believe that EBIT as a percentage of sales is the key measure of overall profitability as it takes into account both gross margin and the costs related to operating the business that produces that margin. The CODM focuses on EBIT as a percentage of sales, rather than gross margin in assessing the performance and allocating the resources of the Retail Food business on a national level. For example, the CODM reports contain data on EBIT as a percentage of sales for the Retail Food reportable operating segment, which is ultimately where the CODM looks to assess performance of the Retail Food segment. Additionally, in the retail grocery business, gross margin is not as good an indicator as EBIT margin of the economic similarity of the operating segments because many of the significant costs to produce revenue in a retail grocery business are below the gross margin line. Gross margin takes into account many factors that vary on a store-by-store basis, but are not indicative of overall profitability, including real estate costs, labor costs, worker’s compensation and pension benefits and nearby competition and utilities costs.

[CONFIDENTIAL TREATMENT REQUESTED PURSUANT TO RULE 83 (17 CFR 200.83)]

-8-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

[CONFIDENTIAL TREATMENT REQUESTED PURSUANT TO RULE 83 (17 CFR 200.83)]

-9-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

[CONFIDENTIAL TREATMENT REQUESTED PURSUANT TO RULE 83 (17 CFR 200.83)]

While sales is also an important quantitative measure for assessing our performance, sales varies based on what is happening at a store-by-store level and therefore a geographic region may experience an increase or decrease in sales in any given year that leads to fluctuations between the geographic regions, but is driven by the individual stores, not the region. We acknowledge that sales are variable over time, although, as the chart below illustrates, they generally migrate to a common range over a longer period of time.

[CONFIDENTIAL TREATMENT REQUESTED PURSUANT TO RULE 83 (17 CFR 200.83)]

-10-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

Qualitative Factors

In addition to the qualitative and quantitative factors discussed above with respect to similar economic characteristics, as described in our June 9, 2008 response, the Retail West, Retail Midwest, Retail East, Save-A-Lot and Bristol Farms operating segments also meet the qualitative factors specifically outlined in SFAS 131 paragraph 17:

SFAS 131 paragraph 17 Qualitative Factor | Application to the Company’s Retail Operating Segments | |

Nature of products and services | The nature of the products sold in the grocery stores within each retail operating segment is substantially the same across all retail operating segments focusing on food and related products. | |

Nature of production processes | Substantially all of the products sold in the grocery stores within each geographic segment are initially purchased from vendors for resale through centralized procurement. | |

Type of class of customer for products or services | The customer or potential customer for each of the retail operating segments is any consumer of food or related products in the United States. | |

Methods used to distribute products or provide services | Each of the retail operating segments use the same distribution method for its products (i.e., grocery store). | |

If applicable, nature of regulatory environment | All the Company’s retail operating segments are subject to federal laws and regulations. | |

We believe that the five retail operating segments meets the aggregation criteria under SFAS 131 paragraph 17, which results in one reportable segment, Retail Food. This is consistent with the presentation in our financial statements in our periodic reports. We believe that this presentation is consistent with the objective and principles of SFAS 131 paragraph 3 and provides users of our financial statements with all of the information about our retail food grocery business helpful in their understanding of the Company’s performance, assessing the Company’s prospects for future net cash flows and making more informed judgments about the Company as a whole.

-11-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

Functional Analysis

Our view that we could have one Retail Food operating segment that continued through this transitional period was based on the fact that the CODM was responsible for reviewing the operating activities, financial results, forecasts and plans for such operating segment and therefore could be viewed as the segment manager of the Retail Food segment. Paragraph 14 of SFAS 131 emphasizes that the proper inquiry focuses on the manager’s functional role, rather than title:

“The term segment manager identifies afunction, not necessarily a manager with a specific title. The chief operating decision maker also may be the segment manager for more than one operating segment.” (emphasis added)13

[CONFIDENTIAL TREATMENT REQUESTED PURSUANT TO RULE 83 (17 CFR 200.83)]

13 | Similarly, the federal securities laws typically require a functional approach for comparable determinations regarding a registrant’s officers or managerial personnel. See, e.g., Sections 302(a) and 906 of the Sarbanes-Oxley Act of 2002 (requiring certifications by “persons performing similarfunctions” to the registrant’s CEO and CFO); Rule 3b-7 (defining “executive officer” by reference to performance of “a policy makingfunction”); Rule 3b-2 (defining “officer” by reference to specified titles and “any person routinely performing correspondingfunctions”); Rule 16a-1 (defining “officer” by reference to performance of “a policy-makingfunction”); Item 401(c) of Regulation S-K (requiring certain disclosures with respect to persons “who are not executive officers but who make or are expected to make significant contributions to the business of the registrant”) (emphasis added). |

-12-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

[CONFIDENTIAL TREATMENT REQUESTED PURSUANT TO RULE 83 (17 CFR 200.83)]

While we believe that one view of our operating segments is six operating segments comprised of Retail West, Retail Midwest, Retail East, Save-A-Lot, Bristol Farms and Supply Chain Services, we believe that one can also view the Company as having had two operating segments of Retail Food and Supply Chain Services because the CODM consistently allocated the resources of the Company at a national level rather than by geographic region or store banner. However, whether we had five retail operating segments during this transitional period with four different regional managers or one retail operating segment with the CODM as the segment manager, we respectfully submit the result is the same, and that this result reflects how the CODM views and manages the business: the Company had one Retail Food reportable segment.

The presentation of two reportable segments of Retail Food and Supply Chain Services is identical to the presentation in our periodic reports. Such presentation is consistent with the objective and basic principles of SFAS 131 in that it provides users of our financial statements with meaningful information about our Retail Food and Supply Chain Services businesses to enable investors to understand the Company’s performance, assess the Company’s prospects for future net cash flows and make informed judgments about the Company as a whole.

| 2. | Our review of your Financial Report for each period end noted under the segment tab a profit and loss summary for retail food which included a line item titled Distribution Retail Profit that has no sales data but does present gross profit, selling, general and administrative expenses and operating earnings. Please explain what distribution operations are included the line item Distribution Retail Profit and how it generates operating earnings from your retail food store operations. Explain to us if these operations also meet the qualifications of an operating segment as defined by paragraph 10 of SFAS 131. |

Response:

We note the Staff’s comment that the historical CODM reports provided to the Staff include a line item on the profit and loss summary for Retail Food titled Distribution Retail Profit. In response to the Staff’s comment regarding the Distribution Retail Profit line item and how this item generates operating revenues from Retail Food, this line item reflects inter-company profit related to product received at certain Company owned retail food stores from the Company owned distribution operations that also supply third party stores (Supply Chain Services). Note that for each item added to the income of the Retail Food segment there is a corresponding deduction from the Supply Chain Services segment. Therefore, since this item is

-13-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

only inter-company related, it does not apply to paragraph 10 of SFAS 131 nor does the CODM look at this data when managing the business.

Our current CODM reports do not contain this line item nor will any future reports contain this line item as the current integrated general ledger posts these items directly to the general ledger, which incorporates all of the Company’s operations.

Form 10-Q for the Fiscal Quarter Ended September 6, 2008

Financial Statements

Notes to Consolidated Financial Statements (Unaudited)

Note 3—Goodwill and Intangible Assets, page 10

| 3. | We note the supplemental information you provided and your response to our prior comment five regarding an impairment review of goodwill under SFAS 142. Even though we understand the quoted price of your common stock should not be the sole measurement basis of your fair value, we believe market capitalization can be used as an overall evaluation in the review process. In this regard, using your closing share price of $24 as of September 6, 2008 your market capitalization value was approximately $5.1 billion, compared to recorded goodwill of $7 billion, yielding a material negative variance of $1.9 billion, or 27%. Further, using your closing stock price of $28 as of February 23, 2008, your market capitalization value was approximately $5.8 billion, compared to recorded goodwill of $7 billion, yielding a large negative variance of $1.2 billion, or 17%. We believe the existence of such material negative variances raises serious questions about whether any impairment of goodwill has occurred. In light of the further deterioration of an unfavorable business climate, the continuing decline in consumer spending and negative same store stales performance, please provide us with a copy of the recent sensitivity analysis you prepared supporting your conclusion as of September 6, 2008 that there was no indication of impairment of goodwill since the last annual test. Please also provide us with a comprehensive discussion of the basis for each of the major assumptions relating to revenue growth, operating ratios, and annual gross margin and EBIT percent used for each reporting unit by forecast year. We may have further comments upon review of your response. |

Response:

Executive Summary

The Company concluded that as of September 6, 2008, the last day of the second quarter of fiscal year 2009, there was no indication of impairment of our goodwill. The Company considered the economic conditions at the end of the quarter and concluded that based on industry- and company-specific factors, the decline in our stock price below book value per share was temporary and was expected to recover above book value per share in the near term. Additionally, we considered the operating performance of each of our reporting units in the

-14-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

second quarter to assess whether there was a change in the business climate that warranted further analysis and based on such review, concluded that it was appropriate to conduct a sensitivity analysis for certain reporting units in order to determine whether there was an indication of the need to perform step one testing for impairment under SFAS 142. The results of such sensitivity analysis were that no indication of impairment had occurred as of the end of the second quarter of fiscal year 2009.

In the third quarter of fiscal year 2009, however, our stock price has declined over 50%, the credit markets have frozen as the full impact of financial events, such as Lehman Brothers filing for bankruptcy on September 15, 2008 and Washington Mutual being seized and sold on September 26, 2008, are absorbed by the market. Further, the economy has officially been declared in recession, investors have fled the equity markets for more secure investments such as Treasury bonds and investors have battered the stocks of companies with non-investment grade debt.

[CONFIDENTIAL TREATMENT REQUESTED PURSUANT TO RULE 83 (17 CFR 200.83)]

Second Quarter Fiscal Year 2009 Test of Goodwill

Following the second quarter ended September 6, 2008, management considered current economic conditions and the decline in retail operating earnings compared to the prior year and concluded that it was appropriate to conduct a review and sensitivity analysis for certain reporting units in order to determine whether there was an indication of impairment under SFAS 142.15 Based on that review and sensitivity analysis, we concluded at that time that no indication of impairment had occurred and a step one analysis was not required.

We first considered economic factors with respect to our industry and our company that may have indicated a need for an impairment test. We considered a decline in our market capitalization below book value and analyzed external market events on the sector versus the general volatility of the market.16 While we agree that a negative variance between market capitalization and goodwill is a factor to consider in determining whether an impairment of

15 | Pursuant to SFAS 142 paragraph 28, “Goodwill of a reporting unit shall be tested for impairment between annual tests if an event occurs or circumstances change that would more likely than not reduce the fair value of a reporting unit below its carrying amount. Examples of such events or circumstances include “[a] significant adverse change in legal factors or in the business climate . . . .” |

16 | cf. Steven Jacobs, Remarks before the 2008 AICPA National Conference on Current SEC and PCAOB Developments (Dec. 9, 2008). |

-15-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

goodwill has occurred, market capitalization is not the sole basis for a measurement of fair value as there are no bright-line rules with respect to when an impairment has occurred and, accordingly, no one factor is determinative of the actual fair value of a reporting unit’s goodwill.17 In conjunction with our second quarter analysis, we did not believe our market capitalization was an accurate indicator of the fair value of our reporting units for two primary reasons. First, much of the weakness spanned the entire equity market due to concerns about the weakening economy. However, the retail foods industry is generally more immune to economic downturns than other retail industries. Food is a non-discretionary item in family budgets and spending on groceries is relatively stable, yet the market capitalization of retail foods companies has declined along with other retail businesses, despite the more stable cash flows of traditional grocery stores. Second, despite our strong cash flows and back-up credit capacity, our stock price has been negatively impacted as a result of the debt incurred in connection with the Acquisition. As of the end of the second quarter, we viewed the decline in our stock price below book value per share as temporary.

Retail Foods Industry Factors

The retail foods industry and, in particular, traditional grocery stores, are different than other retailers and industries and are better positioned to endure the current macro-economic crisis without material impact to sales or cash flows. This conclusion is based upon factors that indicate that grocery store sales and cash flows industry-wide are less impacted than other retail industries and the market in general. As a result, the recent general decline in stock prices of traditional retail food grocers is more a product of general market environment than an assessment of the future prospects and value of the companies within the retail foods industry. Accordingly, assessing fair value only by a review of market capitalization may result in an inaccurate fair value assessment of the Company’s reporting units.

First, non-discretionary product offerings account for a majority of sales in traditional grocery stores. We believe that sales of non-discretionary products are generally less directly affected than sales of discretionary products in a down economy in which consumers have less disposable income and are increasingly price conscious. Additionally, we believe that consumers increasingly opt to purchase groceries in lieu of eating meals at restaurants, a trend which further limits the impact of a poor economy on sales of traditional grocery stores.

Second, traditional grocery store retailers, such as the Company, with convenient store locations, a well-known reputation and private or exclusive label brands, are especially well positioned to capitalize on these trends and, as a result, sales are less likely to decline materially, compared to prior periods under adverse economic conditions. Additionally, we further believe that comparing sales and the quoted stock price of grocery store companies at any one given time

17 | See Robert G. Fox III, Professional Accounting Fellow, Office of the Chief Accountant, Remarks before the 2008 AICPA National Conference on Current SEC and PCAOB Developments (Dec. 8, 2008) (“Contrary to some rumors I have heard, the staff does not have ‘bright line’ tests that we use in determining the reasonableness of a control premium. Instead, we believe that a registrant needs to carefully analyze the facts and circumstances of their particular situation in determining an appropriate control premium and that there is normally a range of reasonable judgments a registrant might reach.”) |

-16-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

without due consideration to the positioning and composition of the stores within a particular company could prove an inaccurate assessment of the company’s fair value.

In the second quarter, we believe that the stock market did not appropriately distinguish between the stocks of traditional grocery stores and other retailers and industries, but rather was being driven by overall volatility in the stock market. Given that same store sales and cash flows have remained relatively stable for retail food companies compared to other retail companies during this period, it is clear that the broad decline in the market capitalization of these companies is more closely correlated to the broader market decline and weakening of investor confidence, as the economy began to weaken.

Company-Specific Factors

Although same store sales performance was slightly negative in the second quarter, there were additional Company-specific considerations that outweighed that factor in assessing the Company’s fair value, quoted stock price and our conclusion at the end of the second quarter that there was no indicator of impairment of goodwill at any of the Company’s reporting units as of the end of the second quarter of fiscal year 2009.

As a result of the acquisition of NABS in June 2006, we are more highly leveraged than our competitors and are the only major grocery retailer with non-investment grade debt. As a result of being a more leveraged company, in the second quarter, our stock price traded at a lower price to earnings ratio than our major competitors. However, our stock price is not reflective of our cash flows or our ability to service our indebtedness, but reflective of overall market trends.[CONFIDENTIAL TREATMENT REQUESTED PURSUANT TO RULE 83 (17 CFR 200.83)]

As a result of the performance of the Company and the declines in the macro-economy in the second quarter, the Company’s earnings per share targets for fiscal year 2009 were reduced from a range of $3.00 to $3.16 to a range of $2.86 to $2.96, and fiscal year 2009 same store sales guidance was reduced from 0.5% to flat to (0.5)%. Additionally, while second quarter fiscal year 2009 results were below expectations, as of the end of the second quarter, the Company was forecasting that fiscal year 2009 earnings per share would increase over the prior year (although at a more modest rate than in prior years) and at the end of the second quarter noted that the revised fiscal year 2009 same store sales guidance anticipated flat to positive 0.5% same store sales for the balance of fiscal year 2009. Given the minimal variance between the Company’s actual and projected results as of the end of the second quarter and our historical results, we believe that the decline in the Company’s quoted stock price as of the end of the second quarter was overly impacted by general market conditions as opposed to the Company’s results of operations and expectations for future performance, which had not significantly declined.

As mentioned previously, at the time of our second quarter impairment review, we looked at the strength of the Company’s fundamentals in our reporting units and our belief that we are well-positioned to remain stable or grow during the macro-economic downturn. We had publicly announced that strong cash flows would allow for over $1 billion of capital reinvestment as well as a reduction of $400 million of the Company’s outstanding debt. We

-17-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

looked at the fact that the Company is well positioned in the industry and had maintained its market share positions. Additionally, we continued to pay dividends while maintaining our corporate credit rating.18

At the end of the second quarter, our stock price was approximately $24 and had traded at an average of $27.94 during the quarter.

[CONFIDENTIAL TREATMENT REQUESTED PURSUANT TO RULE 83 (17 CFR 200.83)]

18 | In the third quarter of fiscal year 2009, on October 15, 2008, S&P affirmed its “BB-” non-investment grade corporate credit rating on the Company, but lowered its rating outlook from “Positive” to “Stable.” |

-18-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

[CONFIDENTIAL TREATMENT REQUESTED PURSUANT TO RULE 83 (17 CFR 200.83)]

As described in our October 15, 2008 response letter, we did update our risk factor disclosure in our second quarter 10-Q to include disclosure regarding potential impairment of goodwill or other intangible assets.

Third Quarter Fiscal Year 2009 Test of Goodwill

The third fiscal quarter of 2009 saw seismic events in the financial world. The Lehman Brothers bankruptcy on September 15, 2008 and the seizure and sale of Washington Mutual on September 26, 2008 were two of the major events that led to a wide scale flight from equity securities and freezing of the credit markets. While at the end of the second quarter we believed that there would be a near term recovery in our stock price above book value per share, the ramifications and effects of these events in the third quarter made a near term recovery unlikely as of the end of the third quarter of fiscal year 2009.

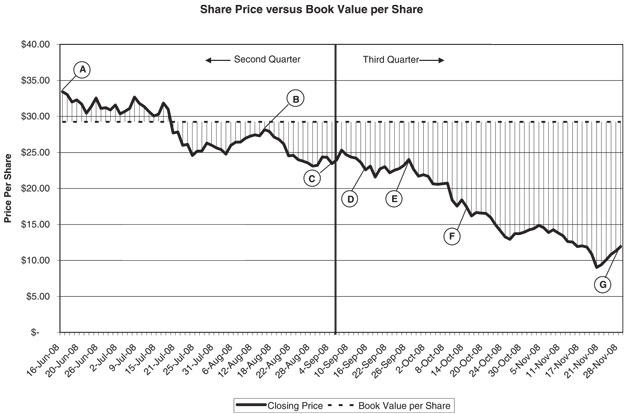

As the equity markets reacted to these events, the Company experienced a significant decline in market capitalization in the third fiscal quarter. In the second fiscal quarter, our stock price traded above our $29.25 book value per share for 40% of the trading days in the quarter and at 96% of book value per share as recently as 16 trading days prior to the end of the second quarter. In contrast, in the third quarter, our stock price never traded above our book value per share. The Company’s average stock price in the third quarter of fiscal year 2009 was $17.26 as compared to an average of $27.94 in the second quarter of fiscal year 2009, a decline of 38.2%. As evidenced in the chart below, as of the end of the third quarter, there had been a precipitous decline in our stock price:

-19-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

| Trading Date | Significance | |||

| A | June 16, 2008 | Stock price on first trading day of Q2 was $33.44 ($4.19 above book value per share). | ||

| B | August 14, 2008 | Closed at 96% of book value per share 16 trading days prior to the last trading day of Q2. | ||

| C | September 8, 2008 | Stock price on first trading day of Q3 was $25.31 ($3.94 below book value per share). | ||

| D | September 15 2008 | Lehman Brothers files for Bankruptcy protection. | ||

| E | September 26, 2008 | Washington Mutual sold to JPMorgan Chase after being seized by federal regulators. | ||

| F | October 14, 2008 | Release of second quarter fiscal year 2009 earnings. | ||

| G | November 28, 2008 | Stock price traded below book value every day of Q3 and ended Q3 at $11.91/share ($17.34 below book value per share). | ||

[CONFIDENTIAL TREATMENT REQUESTED PURSUANT TO RULE 83 (17 CFR 200.83)]

The chart below summarizes certain data points for the Company’s stock price and economic factors during the second and third quarters of fiscal year 2009. Whereas the factors in the second quarter indicated a weakening of economic indicators, we still believed our stock price would recover in the short term. Even in the declining economy our average stock price

-20-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

during the second quarter was 95.5% of book value per share. By December 1, 2008, however, a recession had been officially declared and our average stock price during the quarter was 59.0% of book value. These factors caused us to conclude that an indication of impairment had occurred as of the end of the third quarter.

Factor | Second Quarter ended Sept. 6, 2008 | Third Quarter ended Nov. 29, 2008 | ||

Economy | Declining economy | Official recession declared on December 1 | ||

Mutual Fund Net Cash Flows21 | -$51,892 million (Jun., Jul. & Aug.) | -$128,648 million (Sept. & Oct. only) | ||

Credit Markets22 | 1,085 M&A Deals 21 High Yield Deals | 792 M&A Deals 6 High Yield Deals | ||

Stock Price at Beginning of Quarter | $33.44 | $25.31 | ||

Stock Price at End of Quarter | $23.95 | $11.91 | ||

Average Stock Price | $27.94 | $17.26 | ||

Average Stock Price as Percentage of Book Value | 95.5% | 59.0% | ||

Percentage Decline in Stock Price during Quarter | 28.4% | 52.9% | ||

Last Day within 5% of Book Value | August 14 | n/a | ||

Percentage of Trading Days Above Book Value | 40% | 0% | ||

[CONFIDENTIAL TREATMENT REQUESTED PURSUANT TO RULE 83 (17 CFR 200.83)]

21 | Source: Investment Company Institute, “Trends in Mutual Fund Investing” June – October, 2008. |

22 | M&A figures are for deals announced in the quarter. Source for both M&A and high yield figures: Dealogic. |

-21-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

[CONFIDENTIAL TREATMENT REQUESTED PURSUANT TO RULE 83 (17 CFR 200.83)]

* * * * * * * *

The Company acknowledges that:

| • | the Company is responsible for the adequacy and accuracy of the disclosure in the filing; |

| • | Staff comments or changes to disclosure in response to Staff comments do not foreclose the Commission from taking any action with respect to the filing; and |

| • | the Company may not assert Staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States. |

-22-

FOIA CONFIDENTIAL TREATMENT

REQUESTED BY SUPERVALU INC PURSUANT TO RULE 83

We would be happy to discuss with you any additional questions the Staff may have regarding the Company’s financial disclosures. If you have any questions, please contact our counsel, John J. Huber of Latham & Watkins LLP, at (202) 637-2242.

| Sincerely, |

| /s/ Pamela K. Knous |

Pamela K. Knous Executive Vice President and Chief Financial Officer |

| cc: | David L. Boehnen, Executive Vice President, SUPERVALU INC. |

Burt M. Fealing, Vice President, Corporate Secretary

and Chief Securities Counsel, SUPERVALU INC.

Jacquelyn K. Daylor, KPMG LLP

David J. Middendorf, KPMG LLP

Melanie F. Dolan, KPMG LLP

Brenna J. Wist, KPMG LLP

Frank E. Casal, KPMG LLP

John J. Huber, Latham & Watkins LLP

Joel H. Trotter, Latham & Watkins LLP

enclosures

-23-