Table of Contents

AS FILED WITH THE SECURITIES AND EXCHANGE COMMISSION ON NOVEMBER 15, 2004

SECURITIES ACT FILE NO. 333-

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-14

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933 x

PRE-EFFECTIVE AMENDMENT NO. ¨

POST-EFFECTIVE AMENDMENT NO. ¨

SCUDDER TOTAL RETURN FUND

(Exact Name of Registrant as Specified in Charter)

222 South Riverside Plaza Chicago, IL 60606

(Address of Principal Executive Offices) (Zip Code)

617-295-2572

(Registrant’s Area Code and Telephone Number)

John Millette, Secretary

Scudder Total Return Fund

Two International Place Boston, MA 02110

(NAME AND ADDRESS OF AGENT FOR SERVICE)

WITH COPIES TO:

Cathy G. O’Kelly, Esq. | John W. Gerstmayr, Esq. | |

David A. Sturms, Esq. | Ropes & Gray LLP | |

Vedder, Price, Kaufman & Kammholz, P.C. | One International Place | |

222 North LaSalle Street | Boston, Massachusetts 02110-2624 | |

Chicago, Illinois 60601 |

APPROXIMATE DATE OF PROPOSED PUBLIC OFFERING: As soon as practicable after the effective date of this Registration Statement.

No filing fee is required because an indefinite number of shares have previously been registered pursuant to Rule 24f-2 under the Investment Company Act of 1940.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment that specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

Questions & Answers

Scudder Portfolio Trust

Scudder Balanced Fund

Q&A

Q What is happening?

A Deutsche Asset Management (“DeAM”), the investment manager for the Scudder funds, has initiated a program to reorganize and combine selected funds within the Scudder fund family.

Q What issue am I being asked to vote on?

A You are being asked to vote on a proposal to merge Scudder Balanced Fund into Scudder Total Return Fund. Both funds are managed by substantially the same portfolio management team and seek to achieve similar investment objectives through similar types of investments.

After carefully reviewing the proposal, your fund’s Board has determined that this action is in the best interest of the fund. The Board unanimously recommends that you vote for this proposal.

Q Why has this proposal been made for my fund?

A The combined fund will pay a lower management fee than Scudder Balanced Fund. In addition, combining the two funds means that the costs of operating the fund are anticipated to be spread across a larger asset base. Finally, DeAM has agreed to cap the expenses of the combined fund at levels lower than the expenses currently paid by Scudder Balanced Fund for approximately three years following the merger. Consequently, the combined fund will have lower total operating expenses than Scudder Balanced Fund.

Table of Contents

Q&A continued

Q Will I have to pay taxes as a result of the merger?

A The merger is expected to be a tax-free transaction, and will not take place unless special tax counsel provides an opinion to that effect. As a result of the merger, however, your fund may lose the benefit of certain tax losses that could have been used to offset or defer future gains. If you choose to redeem or exchange your shares before or after the merger, the redemption or exchange will generate taxable gain or loss; therefore, you may wish to consult a tax advisor before doing so. Of course, you may also be subject to capital gains as a result of the normal operations of your fund whether or not the transaction occurs.

Q Upon merger, will I own the same number of shares?

A The aggregate value of your shares will not change as a result of the merger. It is likely, however, that the number of shares you own will change as a result of the merger because your shares will be exchanged at the net asset value per share of Scudder Total Return Fund, which will probably be different from the net asset value per share of Scudder Balanced Fund.

Q Will any fund pay for the proxy solicitation and legal costs associated with this solicitation?

A No. DeAM will bear these costs.

Q When would the merger take place?

A If approved, the merger would occur on or about [March 14], 2005 or as soon as reasonably practicable after shareholder approval is obtained. Shortly after completion of the merger, shareholders whose accounts are affected by the merger will receive a confirmation statement reflecting their new account number and number of shares owned.

Table of Contents

Q&A continued

Q How can I vote?

A You can vote in any one of four ways:

| • | Through the Internet by going to the website listed on your proxy card; |

| • | By telephone, with a toll-free call to the number listed on your proxy card; |

| • | By mail, by sending the enclosed proxy card, signed and dated, to us in the enclosed envelope; or |

| • | In person, by attending the special meeting. |

We encourage you to vote over the Internet or by telephone, following the instructions that appear on your proxy card. Whichever method you choose, please take the time to read the full text of the proxy statement before you vote.

Q If I send my proxy in now as requested, can I change my vote later?

A You may revoke your proxy at any time before it is voted by: (1) sending a written revocation to the Secretary of the fund as explained in the proxy statement; or (2) forwarding a later-dated proxy that is received by the fund at or prior to the special meeting; or (3) attending the special meeting and voting in person. Even if you plan to attend the special meeting, we ask that you return the enclosed proxy. This will help us ensure that an adequate number of shares are present for the special meeting to be held.

Q Will I be able to continue to track my fund’s performance in the newspaper, on the Internet or through the voice response system (Easy-Access Line or SAIL, as applicable)?

A Yes. You will be able to continue to track your fund’s performance through all these means.

Q Whom should I call for additional information about this proxy statement?

A Please call Georgeson Shareholder, your fund’s proxy solicitor, at 1-888-288-5518.

Table of Contents

SCUDDER BALANCED FUND

A Message from the Fund’s Chief Executive Officer

[December ], 2004

Dear Shareholder:

I am writing to you to ask for your vote on an important matter that affects your investment in Scudder Balanced Fund (“Balanced Fund”). While you are, of course, welcome to join us at the Balanced Fund shareholders’ meeting, most shareholders cast their vote by filling out and signing the enclosed proxy card, or by voting by telephone or through the Internet.

We are asking for your vote on the following matter:

| Proposal: | Approval of a proposed merger of Balanced Fund into Scudder Total Return Fund (“Total Return Fund”). In this merger, your shares of Balanced Fund would, in effect, be exchanged, on a tax-free basis, for shares of Total Return Fund with an equal aggregate net asset value. |

The proposed merger is part of a program initiated by Deutsche Asset Management (“DeAM”), the investment manager of the Scudder funds. This program is intended to provide a more streamlined selection of investment options that is consistent with the changing needs of investors. If approved by fund boards and fund shareholders, this program will enable DeAM to:

| • | Eliminate redundancies within the Scudder fund family by reorganizing and combining certain funds; and |

| • | Focus its investment resources on a core set of mutual funds that best meet investor needs. |

The Trustees of Balanced Fund recommend approval of the merger because they believe it offers fund shareholders the following benefits, among others:

| • | A similar investment opportunity in a larger fund with a lower management fee; and |

| • | A lower expense ratio. |

The investment objective and policies of Balanced Fund are similar to those of Total Return Fund. If the merger is approved, the Board expects that the proposed changes will take effect during the first calendar quarter of 2005.

Included in this booklet is information about the upcoming shareholders’ meeting:

| • | A Notice of a Special Meeting of Shareholders, which summarizes the issue for which you are being asked to provide voting instructions; and |

| • | A Prospectus/Proxy Statement, which provides detailed information on Total Return Fund, the specific proposal being considered at the shareholders’ meeting, and why the proposal is being made. |

Table of Contents

Although we would like very much to have each shareholder attend the meeting, we realize this may not be possible. Whether or not you plan to be present, we need your vote. We urge you to review the enclosed materials thoroughly. Once you’ve determined how you would like your interests to be represented, please promptly complete, sign, date and return the enclosed proxy card, vote by telephone or record your voting instructions on the Internet. A postage-paid envelope is enclosed for mailing, and telephone and Internet voting instructions are listed at the top of your proxy card. You may receive more than one proxy card. If so, please vote each one.

I’m sure that you, like most people, lead a busy life and are tempted to put this proxy aside for another day. Please don’t. Your prompt return of the enclosed proxy card (or your voting by telephone or through the Internet) may save the necessity and expense of further solicitations.

Your vote is important to us. We appreciate the time and consideration I am sure you will give to this important matter. If you have questions about the proposal, please call Georgeson Shareholder, Balanced Fund’s proxy solicitor, at 1-888-288-5518 or contact your financial advisor. Thank you for your continued support of Scudder Investments.

Sincerely yours,

Julian F. Sluyters

Chief Executive Officer

Scudder Balanced Fund

Table of Contents

SCUDDER BALANCED FUND

NOTICE OF A SPECIAL MEETING OF SHAREHOLDERS

This is the formal agenda for your Fund’s shareholder meeting. It tells you what matter will be voted on and the time and place of the meeting, in the event you choose to attend in person.

To the Shareholders of Scudder Balanced Fund:

A Special Meeting of Shareholders of Scudder Balanced Fund (“Balanced Fund”) will be held [February 24], 2005 at [9:00 a.m.] Eastern time, at the offices of Deutsche Investment Management Americas Inc., 345 Park Avenue, 27th Floor, New York, New York 10154 (the “Meeting”), to consider the following (the “Proposal”):

| Proposal: | Approving an Agreement and Plan of Reorganization and the transactions it contemplates, including the transfer of all of the assets of Balanced Fund to Scudder Total Return Fund (“Total Return Fund”), in exchange for shares of Total Return Fund and the assumption by Total Return Fund of all liabilities of Balanced Fund, and the distribution of such shares, on a tax-free basis, to the shareholders of Balanced Fund in complete liquidation of Balanced Fund. |

The persons named as proxies will vote in their discretion on any other business that may properly come before the Meeting or any adjournments or postponements thereof.

Holders of record of shares of Balanced Fund at the close of business on [December 2], 2004 are entitled to vote at the Meeting and at any adjournments or postponements thereof.

In the event that the necessary quorum to transact business or the vote required to approve the merger is not obtained at the Meeting, the persons named as proxies may propose one or more adjournments of the Meeting in accordance with applicable law to permit such further solicitation of proxies as may be deemed necessary or advisable. Any adjournment will require the affirmative vote of a majority of the votes cast on the question in person or by proxy at the session of the Meeting to be adjourned. The persons named as proxies will vote FOR any such adjournment those proxies that they are entitled to vote in favor of the Proposal and will vote AGAINST any such adjournment those proxies to be voted against the Proposal.

By order of the Trustees

Dawn-Marie Driscoll (Chair)

Henry P. Becton, Jr.

Keith R. Fox

Louis E. Levy

Jean Gleason Stromberg

Jean C. Tempel

Carl W. Vogt

[December ], 2004

WE URGE YOU TO MARK, SIGN, DATE AND MAIL THE ENCLOSED PROXY IN THE POSTAGE-PAID ENVELOPE PROVIDED OR RECORD YOUR VOTING INSTRUCTIONS BY TELEPHONE OR THROUGH THE INTERNET SO THAT YOU WILL BE REPRESENTED AT THE MEETING.

Table of Contents

INSTRUCTIONS FOR SIGNING PROXY CARDS

The following general rules for signing proxy cards may be of assistance to you and avoid the time and expense involved in validating your vote if you fail to sign your proxy card properly.

1. Individual Accounts: Sign your name exactly as it appears in the registration on the proxy card.

2. Joint Accounts: Either party may sign, but the name of the party signing should conform exactly to the name shown in the registration on the proxy card.

3. All Other Accounts: The capacity of the individual signing the proxy card should be indicated unless it is reflected in the form of registration. For example:

Registration | Valid Signature | |

Corporate Accounts: | ||

(1) ABC Corp. | ABC Corp. John Doe, Treasurer | |

(2) ABC Corp. | John Doe, Treasurer | |

(3) ABC Corp. c/o John Doe, Treasurer | John Doe | |

(4) ABC Corp. Profit Sharing Plan | John Doe, Trustee | |

Partnership Accounts | ||

(1) The XYZ Partnership | Jane B. Smith, Partner | |

(2) Smith and Jones, Limited Partnership | Jane B. Smith, General Partner | |

Trust Accounts | ||

(1) ABC Trust Account | Jane B. Doe, Trustee | |

(2) Jane B. Doe, Trustee u/t/d 12/28/78 | Jane B. Doe | |

Custodial or Estate Accounts | ||

(1) John B. Smith, Cust. f/b/o John B. Smith Jr. | John B. Smith | |

(2) Estate of John B. Smith | John B. Smith, Jr., Executor | |

Table of Contents

IMPORTANT INFORMATION

FOR SHAREHOLDERS OF

SCUDDER BALANCED FUND

This document contains a combined prospectus/proxy statement and a proxy card. A proxy card is, in essence, a ballot. When you vote your proxy, it tells us how to vote on your behalf on an important issue relating to your Fund. If you complete and sign the proxy (or tell us how you want to vote by voting by telephone or through the Internet), we’ll vote it exactly as you tell us. If you simply sign the proxy, we’ll vote it in accordance with the Trustees’ recommendation on page [ ].

We urge you to review the prospectus/proxy statement carefully, and either fill out your proxy card and return it to us by mail, vote by telephone or record your voting instructions through the Internet. You may receive more than one proxy card since several shareholder meetings are being held as part of the broader restructuring program of the Scudder fund family. If so, please vote each one. Your prompt return of the enclosed proxy card (or your voting by telephone or through the Internet) may save the necessity and expense of further solicitations.

We want to know how you would like to vote and welcome your comments. Please take a few minutes to read these materials and return your proxy to us.

If you have any questions, please call Georgeson Shareholder, Balanced Fund’s proxy solicitor, at the special toll-free number we have set up for you (1-888-288-5518) or contact your financial advisor.

Table of Contents

PROSPECTUS/PROXY STATEMENT

, 2004

Acquisition of the assets of: | By and in exchange for shares of: | |

Scudder Balanced Fund a series of Scudder Portfolio Trust | Scudder Total Return Fund a series of Scudder Total Return Fund | |

Two International Place Boston, MA 02110 (617) 295-2572 | 222 S. Riverside Plaza Chicago, IL 60606 (617) 295-2572 | |

This Prospectus/Proxy Statement is being furnished in connection with the proposed merger of Scudder Balanced Fund (“Balanced Fund”) into Scudder Total Return Fund (“Total Return Fund”). Total Return Fund and Balanced Fund are referred to herein collectively as the “Funds,” and each is referred to herein individually as a “Fund.” As a result of the proposed merger, each shareholder of Balanced Fund will receive a number of full and fractional shares of the corresponding class of Total Return Fund equal in value as of the date of the exchange to the total value of such shareholder’s Balanced Fund shares.

This Prospectus/Proxy Statement is being mailed on or about [December ], 2004. It explains concisely what you should know before voting on the matter described herein or investing in Total Return Fund, a diversified series of an open-end management investment company. Please read it carefully and keep it for future reference.

The securities offered by this Prospectus/Proxy Statement have not been approved or disapproved by the Securities and Exchange Commission (the “SEC”), nor has the SEC passed upon the accuracy or adequacy of this Prospectus/Proxy Statement. Any representation to the contrary is a criminal offense.

The following documents have been filed with SEC and are incorporated into this Prospectus/Proxy Statement by reference:

| (i) | the prospectus of Total Return Fund dated , 2004, as supplemented from time to time, for Class S and Class AARP shares (the “Total Return Fund Prospectus”), a copy of which is included with this Prospectus/Proxy Statement; |

| (ii) | the prospectus of Balanced Fund dated May 1, 2004, as supplemented from time to time, for Class S and Class AARP shares (the “Balanced Fund Prospectus” and, together with the Total Return Fund Prospectus, the “Prospectuses”); |

| (iii) | the statement of additional information of Balanced Fund dated May 1, 2004, as supplemented from time to time, for Class S and Class AARP shares (the “Balanced Fund SAI”); |

| (iv) | the statement of additional information relating to the proposed merger, dated , 2004 (the “Merger SAI” and, together with the Balanced Fund SAI, the “SAIs”); and |

1

Table of Contents

| (v) | the audited financial statements and related independent accountant’s report for Balanced Fund contained in the Annual Report for the fiscal year ended December 31, 2003, and the unaudited financial statements contained in the Semi-annual Report for the six-month period ended June 30, 2004. |

No other parts of the Prospectuses, SAIs, Annual Report or Semi-annual Report are incorporated by reference herein.

The updated financial highlights for Total Return Fund contained in the Semi-annual Report for the six-month period ended April 30, 2004 are attached to this Prospectus/Proxy Statement. See Exhibit B.

Shareholders may get free copies of the Annual Report, Semi-annual Report, prospectus and/or statement of additional information for a Fund, request other information about a Fund, or make shareholder inquiries, by contacting their financial advisor or by calling the corresponding Fund at 1-800-253-2277 for Class AARP shares and 1-800-SCUDDER for Class S shares.

Like shares of Balanced Fund, shares of Total Return Fund are not deposits or obligations of, or guaranteed or endorsed by, any financial institution, are not insured by the Federal Deposit Insurance Corporation, the Federal Reserve Board or any other agency, and involve risk, including the possible loss of the principal amount invested.

This document is designed to give you the information you need to vote on the proposal. Much of the information is required disclosure under rules of the SEC; some of it is technical. If there is anything you don’t understand, please contact Georgeson Shareholder, Balanced Fund’s proxy solicitor, at 1-888-288-5518, or contact your financial advisor.

Total Return Fund is subject to the informational requirements of the Securities Exchange Act of 1934, as amended, and in accordance therewith files reports and other information with the SEC. You may review and copy information about the Funds, including the SAIs, at the SEC’s public reference room at 450 Fifth Street, NW, Washington, D.C. You may call the SEC at 1-202-942-8090 for information about the operation of the public reference room. You may obtain copies of this information, with payment of a duplication fee, by electronic request at the following e-mail address: publicinfo@sec.gov, or by writing the Public Reference Branch, Office of Consumer Affairs and Information Services, Securities and Exchange Commission, Washington, D.C. 20549-0102. You may also access reports and other information about the Funds on the EDGAR database on the SEC’s Internet site at http://www.sec.gov.

2

Table of Contents

The responses to the questions that follow provide an overview of key points typically of concern to shareholders considering a proposed merger between mutual funds. These responses are qualified in their entirety by the remainder of this Prospectus/Proxy Statement, which you should read carefully because it contains additional information and further details regarding the proposed merger.

1. What is being proposed?

The Trustees of Scudder Portfolio Trust (the “Trust”), of which Balanced Fund is a series, are recommending that shareholders approve the transactions contemplated by the Agreement and Plan of Reorganization (as described below in Part IV and the form of which is attached hereto as Exhibit A), which we refer to as a merger of Balanced Fund into Total Return Fund. If approved by shareholders, all of the assets of Balanced Fund will be transferred to Total Return Fund solely in exchange for the issuance and delivery to Balanced Fund of shares of Total Return Fund (“Merger Shares”) with a value equal to the value of Balanced Fund’s assets net of liabilities and for the assumption by Total Return Fund of all liabilities of Balanced Fund. Immediately following the transfer, the appropriate class of Merger Shares received by Balanced Fund will be distributed pro rata, on a tax-free basis, to its shareholders of record.

2. What will happen to my shares of Balanced Fund as a result of the merger?

Your shares of Balanced Fund will, in effect, be exchanged on a tax-free basis for shares of the same class of Total Return Fund with an equal aggregate net asset value on the date of the merger.

3. Why have the Trustees of the Trust recommended that I approve the merger?

The Trustees believe that the merger may provide shareholders of Balanced Fund with the following benefits:

| • | Lower Expense Ratio. If the merger is approved, Balanced Fund shareholders are expected to benefit from a lower total fund operating expense ratio. |

| • | Compatible Investment Opportunity. The merger offers shareholders of Balanced Fund the opportunity to invest in a substantially larger combined fund with similar investment policies. Deutsche Investment Management Americas Inc. (“DeIM” or the “Advisor”), the investment advisor for the Funds, has advised the Trustees that Balanced Fund and Total Return Fund have compatible investment objectives and policies. In addition, the Advisor has advised the Trustees that both Funds have substantially the same portfolio management team and follow substantially similar investment processes. |

The Trustees of the Trust have concluded that: (1) the merger is in the best interests of Balanced Fund and (2) the interests of the existing shareholders of Balanced Fund will not be diluted as a result of the merger. Accordingly, the Trustees of the Trust unanimously recommend that shareholders approve the Agreement and Plan of Reorganization (as defined below) effecting the merger.

3

Table of Contents

4. How do the investment goals, policies and restrictions of the two Funds compare?

Total Return Fund seeks the highest total return, a combination of income and capital appreciation, consistent with reasonable risk. Balanced Fund seeks a balance of growth and income from a diversified portfolio of equity and fixed-income securities. Total Return Fund can buy many types of securities, among them common stocks, convertible securities, corporate bonds, U.S. government bonds and mortgage- and asset-backed securities. Balanced Fund normally invests approximately 60% of its net assets in common stocks and other equity securities and approximately 40% of its net assets in investment-grade bonds and other fixed income securities. Balanced Fund may, however, invest up to 75% of its net assets in equity securities and up to 50% in fixed income securities, based on the portfolio managers’ evaluation of the relative attractiveness of equity securities as compared to fixed income securities. At all times, Balanced Fund invests at least 25% of net assets in fixed income senior securities.

Both Funds’ bond investments consist mainly of investment-grade bonds (those in the top four grades of credit quality). However, Total Return Fund could invest up to 35% of total assets in junk bonds, while Balanced Fund could invest up to 10% of total assets, though no more than 20% of its bond assets, in junk bonds. Both Funds may also invest in foreign securities (in the case of Total Return Fund, up to 25% of total assets). Although not one of either Fund’s principal investment strategies, each Fund is permitted, but not required, to use various types of derivatives (contracts whose value is based on, for example, indices, currencies or securities). Each Fund may use derivatives in circumstances where the managers believe they offer an economical means of gaining exposure to a particular asset class or to keep cash on hand to meet shareholder redemptions or other needs while maintaining exposure to the market. Please also see Part II—Investment Strategies and Risk Factors—below for a more detailed comparison of the Funds’ investment policies and restrictions.

The following table sets forth a summary of the composition of the investment portfolio of each Fund as of April 30, 2004, and of Total Return Fund on a pro forma combined basis, giving effect to the proposed merger.

Portfolio Composition (as a % of Fund)

| Balanced Fund | Total Return Fund | Pro Forma (Combined)(1) | |||||||

Common and Preferred Stocks | 58 | % | 63 | % | 62 | % | |||

Fixed Income Holdings | 40 | % | 36 | % | 37 | % | |||

Cash and Cash Equivalents | 2 | % | 1 | % | 1 | % | |||

| 100 | % | 100 | % | 100 | % |

| (1) | Reflects the blended characteristics of Balanced Fund and Total Return Fund as of April 30, 2004. The portfolio composition and characteristics of the merged Fund will change consistent with its stated investment objective and policies. |

4

Table of Contents

5. How do the management fees and expense ratios of the two Funds compare, and what are they estimated to be following the merger?

The following tables summarize the fees and expenses you may pay when investing in the Funds, the expenses that each of the Funds incurred for the year ended April 30, 2004 and the pro forma estimated expense ratios of Total Return Fund assuming consummation of the merger, which reflects the lower management fee schedule to be adopted by Total Return Fund as of that date.

Shareholder Fees (fees paid directly from your investment)

| Class S1 | Class AARP1 | |||

Maximum Sales Charge (Load) | ||||

Balanced Fund | None | None | ||

Total Return Fund | None | None | ||

Maximum Contingent Deferred Sales Charge (Load) | ||||

Balanced Fund | None | None | ||

Total Return Fund | None | None | ||

Redemption/Exchange Fee | ||||

Balanced Fund2 | None | None | ||

Total Return Fund2 | None | None |

| (1) | Class S and Class AARP for Total Return Fund have not yet commenced operations as of the date of this Prospectus/Proxy Statement. |

| (2) | Effective February 1, 2005, each Fund will impose a redemption fee of 2% of the total redemption amount on all Fund shares redeemed or exchanged within 15 days of buying them (either by purchase or exchange). |

The table below compares the annual management fee schedules of the Funds, expressed as a percentage of net assets. The management fee schedule for Total Return Fund reflects reductions that will be effective upon the consummation of the merger. As of April 30, 2004, Total Return Fund and Balanced Fund had net assets of $1,974,345,900 and $725,903,647, respectively.

Balanced Fund | Total Return Fund | |||||

Average Daily Net Assets | Management Fee | Average Daily Net Assets | Management Fee | |||

$0 - $1.5 billion | .470% | $0 - $1.5 billion | .470% | |||

$1.5 billion - $2 billion | .445% | $1.5 billion - $2 billion | .445% | |||

$2 billion - $6.25 billion | .410% | $2 billion - $3.5 billion | .410% | |||

$6.25 billion - $8.5 billion | .400% | $3.5 billion - $5.5 billion | .400% | |||

$8.5 billion - $12.5 billion | .385% | $5.5 billion - $7.5 billion | .390% | |||

Over $12.5 billion | .375% | $7.5 billion - $10.0 billion | .380% | |||

| $10.0 billion - $12.5 billion | .370% | |||||

| Over $12.5 billion | .360% | |||||

5

Table of Contents

As shown below, the merger is expected to result in a lower management fee ratio and total expense ratio for shareholders of Balanced Fund. However, there can be no assurance that the merger will result in expense savings.

Annual Fund Operating Expenses (expenses that are deducted from Fund assets)

| Management Fees | Distribution/ Service Fee | Other Expenses | Total Annual Fund Operating Expenses | Less Expense Waiver/ Reimbursements | Net Annual Fund Operating Expenses | ||||||||||||

Balanced Fund | |||||||||||||||||

Class S | 0.47 | % | None | 0.29 | %2 | 0.76 | % | —3 | 0.76 | % | |||||||

Class AARP | 0.47 | % | None | 0.32 | %2 | 0.79 | % | —3 | 0.79 | % | |||||||

Total Return Fund | |||||||||||||||||

Class S4 | 0.54 | % | None | 0.28 | % | 0.82 | % | — | 0.82 | % | |||||||

Class AARP4 | 0.54 | % | None | 0.31 | % | 0.85 | % | — | 0.85 | % | |||||||

Total Return Fund (Pro forma combined) | |||||||||||||||||

Class S4 | 0.45 | %1 | None | 0.28 | %6 | 0.73 | % | —5 | 0.73 | % | |||||||

Class AARP4 | 0.45 | %1 | None | 0.31 | %6 | 0.76 | % | 0.01 | %5 | 0.75 | % | ||||||

| (1) | Restated to reflect the management fee schedule for Total Return Fund that is effective upon consummation of the merger and estimated other expenses expected upon consummation of the merger. |

| (2) | Restated to reflect estimated costs due to the termination of the fixed rate administrative fee for Balanced Fund. |

| (3) | Through September 30, 2005, the Advisor has contractually agreed to waive all or a portion of its management fee and/or reimburse or pay operating expenses of the Fund to the extent necessary to maintain Balanced Fund’s total annual operating expenses at 0.915% for Class S and Class AARP shares, excluding certain expenses such as extraordinary expenses, taxes, brokerage, interest, Rule 12b-1 distribution and/or service fees, trustee and trustee counsel fees and organizational and offering expenses. |

| (4) | Estimated since no Class S or Class AARP shares were issued as of April 30, 2004. |

| (5) | Through [February 28], 2008, DeIM has contractually agreed to waive all or a portion of its management fee and/or reimburse or pay operating expenses of the combined fund to the extent necessary to maintain the combined fund’s total operating expenses at 0.73% and 0.75% for Class S and Class AARP shares, respectively, excluding certain expenses such as extraordinary expenses, taxes, brokerage, interest, Rule 12b-1 and/or service fees, trustee and trustee counsel fees, and organizational and offering expenses. |

| (6) | Other expenses are estimated, accounting for the effect of the merger. |

The tables are provided to help you understand the expenses of investing in the Funds and your share of the operating expenses that each Fund incurs and that Deutsche Asset Management (“DeAM”), the investment manager for the Scudder funds, expects the combined Fund to incur in the first year following the merger.

6

Table of Contents

Examples

These examples translate the expenses shown in the preceding table into dollar amounts. By doing this, you can more easily compare the costs of investing in the Funds. The examples make certain assumptions. They assume that you invest $10,000 in a Fund for the time periods shown and reinvest all dividends and distributions. They also assume a 5% return on your investment each year and that a Fund’s operating expenses remain the same. The examples are hypothetical; your actual costs and returns may be higher or lower.

| 1 Year | 3 Years | 5 Years | 10 Years | |||||||||

Balanced Fund | ||||||||||||

Class S | $ | 78 | $ | 243 | $ | 422 | $ | 942 | ||||

Class AARP | $ | 81 | $ | 252 | $ | 439 | $ | 978 | ||||

Total Return Fund | ||||||||||||

Class S | $ | 84 | $ | 262 | $ | 455 | $ | 1,014 | ||||

Class AARP | $ | 87 | $ | 271 | $ | 471 | $ | 1,049 | ||||

Total Return Fund (Pro forma combined) | ||||||||||||

Class S | $ | 75 | $ | 233 | $ | 406 | $ | 906 | ||||

Class AARP1 | $ | 77 | $ | 240 | $ | 419 | $ | 939 | ||||

| (1) | Includes three years of capped expenses in each period. |

6. What are the federal income tax consequences of the proposed merger?

For federal income tax purposes, no gain or loss is expected to be recognized by Balanced Fund or its shareholders as a direct result of the merger. For a discussion of taxes that you may incur indirectly as a result of the merger (e.g., due to differences in the Funds’ portfolio turnover rates and net investment income), please see “Information about the Proposed Merger—Federal Income Tax Consequences,” below.

7. Will my dividends be affected by the merger?

The merger will not result in a change in dividend policy.

8. Do the procedures for purchasing, redeeming and exchanging shares of the two Funds differ?

No. The procedures for purchasing and redeeming shares of a particular class for each Fund, and for exchanging shares of each Fund for shares of other Scudder funds, are identical.

Orders for the purchase or redemption of Class S and Class AARP shares of the Funds may be made either directly with the Funds or through a “third party provider”—for example, a workplace retirement plan, financial supermarket or financial advisor—which may have its own policies or instructions.

Each Fund reserves the right to honor any request for redemption or repurchase by “redeeming in kind,” that is, by making payment in readily marketable securities (which typically involve brokerage costs when liquidating the securities to cash).

7

Table of Contents

Orders received by the Funds are effected only on days when the New York Stock Exchange (“NYSE”) is open for trading. Purchases and redemptions of shares of each Fund are made at the Fund’s net asset value (“NAV”) per share calculated as of the close of the NYSE (normally, 4:00 p.m. Eastern time). You can place an order to buy or sell shares at any time. The NAV per each class of each Fund is calculated by dividing the value of total assets of the class, minus all liabilities, by the total number of the class outstanding shares.

9. How will I be notified of the outcome of the merger?

If the proposed merger is approved by shareholders, you will receive confirmation after the reorganization is completed, indicating your new account number and the number of Merger Shares you are receiving. Otherwise, you will be notified in the next annual report of Balanced Fund.

10. Will the number of shares I own change?

Yes, the number of shares you own will most likely change, but the total value of the shares of Total Return Fund you receive will equal the total value of the shares of Balanced Fund that you hold at the time of the merger. Even though the net asset value per share of each Fund is likely to be different, the total value of each shareholder’s holdings will not change as a result of the merger.

11. What percentage of shareholders’ votes is required to approve the merger?

Approval of the merger will require the “yes” vote of the holders of a majority of the shares of Balanced Fund.

The Trustees of Balanced Fund believe that the proposed merger is in the best interests of Balanced Fund. Accordingly, the Trustees unanimously recommend that shareholders vote FOR approval of the proposed merger.

II. Investment Strategies and Risk Factors

What are the main investment strategies and related risks of Total Return Fund, and how do they compare with those of Balanced Fund?

Investment Objectives and Strategies. As noted above, Total Return Fund and Balanced Fund have similar investment objectives. Total Return Fund’s investment objective is to seek the highest total return, a combination of income and capital appreciation, consistent with reasonable risk. Balanced Fund’s investment objective is to seek a balance of growth and income from a diversified portfolio of equity and fixed-income securities. The portfolio managers for the two Funds are substantially the same.

Total Return Fund. Total Return Fund follows a flexible investment program, investing in a mix of growth stocks and bonds.

8

Table of Contents

Total Return Fund can buy many types of securities, among them common stocks, convertible securities, corporate bonds, U.S. government bonds and mortgage- and asset-backed securities. In deciding which type of securities to buy, the managers consider the relative attractiveness of growth stocks and bonds and determine allocations for each. Their decisions are generally based on a number of factors, including interest rates and general market conditions. Generally, most securities are from U.S. issuers, but the fund may invest up to 25% of total assets in foreign securities.

Normally, Total Return Fund’s bond component consists mainly of investment-grade bonds (those in the top four grades of credit quality). However, Total Return Fund could invest up to 35% of total assets in junk bonds (i.e., grade BB and below). Compared to investment-grade bonds, junk bonds may pay higher yields and have higher volatility and risk of default on payments.

Although not one of its principal investment strategies, Total Return Fund is permitted, but not required, to use various types of derivatives (contracts whose value is based on, for example, indices, currencies or securities). In particular, Total Return Fund may use futures, currency options and forward currency transactions. Total Return Fund may use derivatives in circumstances where the managers believe they offer an economical means of gaining exposure to a particular asset class or to keep cash on hand to meet shareholder redemptions or other needs while maintaining exposure to the market.

In choosing stocks, the portfolio managers for Total Return Fund favor large companies with a history of above-average growth, attractive prices relative to potential growth, sound financial strength and effective management, among other factors.

The portfolio managers for Total Return Fund may shift the proportion of Total Return Fund’s holdings, at different times favoring stocks or bonds (and within those asset classes, different types of securities), while still maintaining variety in terms of the securities, issuers and economic sectors represented.

Total Return Fund will normally sell a stock when the managers believe its price is unlikely to go much higher, its fundamental qualities have deteriorated or other investments offer better opportunities.

In deciding what types of bonds to buy and sell, the managers of Total Return Fund consider their relative potential for stability and attractive income, and other factors such as credit quality and market conditions. Total Return Fund may invest in bonds of any duration.

Balanced Fund. Balanced Fund normally invests approximately 60% of its net assets in common stocks and other equity securities and approximately 40% of its net assets in investment-grade bonds and other fixed income securities. Balanced Fund may, however, invest up to 75% of its net assets in equity securities and up to 50% in fixed income securities, based on the portfolio managers’ evaluation of the relative attractiveness of equity securities as compared to fixed income securities. At all times, Balanced Fund invests at least 25% of net assets in fixed-income senior securities.

Balanced Fund’s bond investments are normally in the top four grades of credit quality. Balanced Fund could put up to 10% of total assets—though no more than 20%

9

Table of Contents

of its bond assets—in junk bonds (i.e., grade BB/Ba and below). Compared to investment-grade bonds, junk bonds may pay higher yields but have higher volatility and risk of default. Balanced Fund may also invest in foreign securities.

Although not one of its principal investment strategies, Balanced Fund is permitted, but not required, to use various types of derivatives (contracts whose value is based on, for example, indices, currencies or securities). Balanced Fund may use derivatives in circumstances where the managers believe they offer an economical means of gaining exposure to a particular asset class or to keep cash on hand to meet shareholder redemptions or other needs while maintaining exposure to the market.

In choosing stocks, the managers of Balanced Fund primarily invest in U.S. companies that they believe offer the potential for sustainable growth of revenue or earnings and whose market values appear reasonable in light of their business prospects. The managers of Balanced Fund focus on high-quality growth companies that are leaders or potential leaders in their respective industries. The managers of Balanced Fund conduct in-depth company research, examining, among other factors, relative growth rates, innovation, regional and global exposure and management.

In choosing individual bonds, the managers review each bond’s fundamentals, consider how it is structured and use independent analysis of an issuer’s creditworthiness. Balanced Fund can buy many types of bonds of any maturity, including mortgage- and asset-backed securities, corporate bonds and government securities.

The managers of Balanced Fund will normally sell a security when they believe its fundamental factors have changed, other investments offer better opportunities, or in the course of adjusting their emphasis on or within a given industry.

The managers of Balanced Fund may favor different types of securities at different times.

Balanced Fund may lend its fixed income investment securities up to 33 1/3% of its total assets to approved institutional borrowers who need to borrow securities in order to complete certain transactions.

In addition, for temporary defensive purposes, each Fund may invest, without limit, in cash and cash equivalents, U.S. government securities, money market instruments and high quality debt securities without equity features. In such a case, each Fund would not be pursuing, and may not achieve, its investment objective.

General. The Funds have identical fundamental investment policies, which may not be changed without a shareholder vote.

DeAM believes that Total Return Fund should provide a comparable investment opportunity for shareholders of Balanced Fund.

For a more detailed description of the investment techniques used by Total Return Fund and Balanced Fund, please see the applicable Fund’s Prospectus and SAI.

10

Table of Contents

Primary Risks. As with any stock fund, you may lose money by investing in Total Return Fund. Certain risks associated with an investment in Total Return Fund are summarized below. Subject to limited exceptions, the risks of an investment in Total Return Fund are substantially similar to the risks of an investment in Balanced Fund. More detailed descriptions of the risks associated with an investment in Total Return Fund can be found in the Total Return Fund Prospectus and Total Return Fund SAI.

The value of your investment in Total Return Fund will change with changes in the values of the investments held by Total Return Fund. A wide array of factors can affect those values. In this summary we describe the principal risks that may affect Total Return Fund’s investments as a whole. Total Return Fund could be subject to additional principal risks because the types of investments it makes can change over time.

Stock Market Risk. As with most stock funds, an important factor with Total Return Fund is how stock markets perform—in this case, the large company portion of the U.S. stock market. When large company stock prices fall, you should expect the value of your investment to fall as well. At times, large company stocks may not perform as well as stocks of smaller or mid-sized companies. Because a stock represents ownership in its issuer, stock prices can be hurt by poor management, shrinking product demand and other business risks. These may affect single companies as well as groups of companies. In addition, movements in financial markets may adversely affect a stock’s price, regardless of how well the company performs. The market as a whole may not favor the types of investments each Fund makes and each Fund may not be able to get attractive prices for them. An investment in Balanced Fund is also subject to this risk.

Industry Risk. While Total Return Fund does not concentrate in any industry, to the extent that Total Return Fund has exposure to a given industry or sector, any factors affecting that industry or sector could affect the value of portfolio securities. For example, manufacturers of consumer goods could be hurt by a rise in unemployment, or technology companies could be hurt by such factors as market saturation, price competition and rapid obsolescence. An investment in Balanced Fund is also subject to this risk.

Securities Lending Risk. Any loss in the market price of securities loaned by Total Return Fund that occurs during the term of the loan would be borne by Total Return Fund and would adversely affect Total Return Fund’s performance. Also, there may be delays in recovery of securities loaned or even a loss of rights in the collateral should the borrower of the securities fail financially while the loan is outstanding. However, loans will be made only to borrowers selected by Total Return Fund’s delegate after a review of relevant facts and circumstances, including the creditworthiness of the borrower. An investment in Balanced Fund is also subject to this risk.

Credit Risk. A fund purchasing bonds faces the risk that the creditworthiness of the issuer may decline, causing the value of its bonds to decline. In addition, an issuer may not be able to make timely payments on the interest and principal on the bonds it has issued. Because the issuers of junk bonds (rated below the fourth highest category) may be in uncertain financial health, the prices of their bonds can be more vulnerable to bad economic news or even the expectation of bad news, than investment-grade bonds. In some cases, bonds may decline in credit quality or go into default. Because Total Return Fund may invest in securities not paying current interest or in securities already in default, these risks may be more pronounced. An investment in Balanced Fund is also subject to this risk.

11

Table of Contents

Interest Rate Risk. Generally, fixed income securities will decrease in value when interest rates rise, and increase in value when interest rates decline. The longer the effective maturity of Total Return Fund’s securities, the more sensitive it will be to interest rate changes. (As a general rule, a 1% rise in interest rates means a 1% fall in value for every year of duration.) As interest rates decline, the issuers of securities held by Total Return Fund may prepay principal earlier than scheduled, forcing Total Return Fund to reinvest in lower yielding securities. This prepayment may reduce Total Return Fund’s income. As interest rates increase, slower than expected principal payments may extend the average life of fixed income securities. This will have the effect of locking in a below-market interest rate, increasing Total Return Fund’s duration and reducing the value of such a security. Because Total Return Fund may invest in mortgage-related securities, it is more vulnerable to both of these risks. An investment in Balanced Fund is also subject to this risk.

Other factors that could affect performance include:

| • | the managers could be incorrect in their analysis of industries, companies, economic trends, the relative attractiveness of different sizes of stocks or other matters; |

| • | at times, market conditions might make it hard to value some investments. As a result, if Total Return Fund has valued its securities too highly, you may end up paying too much for Total Return Fund shares when you buy into Total Return Fund. If Total Return Fund underestimates the price of its securities, you may not receive the full market value for your Total Return Fund shares when you sell; |

| • | foreign securities tend to be more volatile than their U.S. counterparts, for reasons such as currency fluctuations and political and economic uncertainty; |

| • | the Advisor measures credit quality at the time it buys securities, using independent rating agencies or, for unrated securities, judged by the Advisor to be of equivalent quality. In addition, the Advisor applies its own credit quality standards to evaluate securities. If a security’s credit quality declines, the Advisor will decide what to do with the security, based on the circumstances and its assessment of what would benefit shareholders most; and |

| • | derivatives could produce disproportionate losses due to a variety of factors, including the unwillingness or inability of the counterparty to meet its obligations or unexpected price or interest rate movements (see “Secondary Risks” in each Fund’s Prospectus for more information). |

An investment in Balanced Fund is also subject to these other risk factors.

Performance Information. The following information provides some indication of the risks of investing in each Fund. The bar charts show year-to-year changes in the performance of Total Return Fund’s Class A shares and Balanced Fund’s Class S shares.

The table following the charts compares the Funds’ performance to each other’s and to that of broad measures of market performance (which, unlike a Fund, do not have any fees or expenses). Of course, a Fund’s past performance is not an indication of future performance.

12

Table of Contents

Because Class S and Class AARP shares of Total Return Fund have not yet begun operations as of the date of this Prospectus/Proxy Statement, no performance information for these classes is available.

For Balanced Fund, the inception date for Class AARP shares was August 28, 2000. In the bar chart, the performance figures for Class S are shown, since this was the Fund’s original share class. In the table, the performance figures for Class AARP prior to its inception are based on the historical performance of Class S.

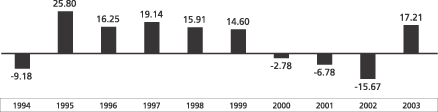

Calendar Year Total Returns (%)

Total Return Fund—Class A Shares

For the periods included in the bar chart:

Best Quarter: 13.07%, Q2 1997 Worst Quarter: -10.01%, Q2 2002

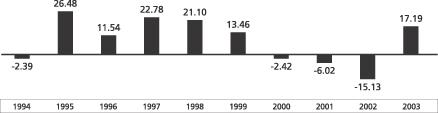

Balanced Fund—Class S Shares*

For the periods included in the bar chart:

Best Quarter: 14.71%, Q4 1998 Worst Quarter: -9.72%, Q2 2002

| * | In the bar chart, total returns for 1995 through 1998 would have been lower if operating expenses had not been reduced. |

Performance figures for the bar chart for Class A shares of Total Return Fund do not reflect the impact of sales charges. If they did, performance for Class A shares of Total Return Fund would be lower than as shown. Year-to-date performance through September 30, 2004 was 0.81% for Total Return Fund and 1.14% for Balanced Fund. During the periods shown in the bar chart, the highest returns for a quarter were 13.07% (quarter ended 6/30/97) for Total Return Fund and 14.71% (quarter ended 12/31/98) for Balanced Fund, and the lowest returns for a quarter were -10.01% (quarter ended 6/30/02) for Total Return Fund and -9.72% (quarter ended 6/30/02) for Balanced Fund.

13

Table of Contents

Average Annual Total Returns (for periods ended December 31, 2003)

| Past 1 year | Past 5 years | Past 10 years | |||||||

Total Return Fund | |||||||||

Class A (Return before Taxes)(5) | 10.47 | % | -0.66 | % | 5.90 | % | |||

(Return after Taxes on distributions) | 10.01 | % | -2.00 | % | 3.52 | % | |||

(Return after Taxes on distributions and Sale of Fund Shares) | 6.94 | % | -1.15 | % | 3.87 | % | |||

S&P 500 Index1 (Reflects no deductions for fees, expenses or taxes) | 28.68 | % | -0.57 | % | 11.07 | % | |||

Lehman Brothers Government/Corporate Bond Index2 (Reflects no deductions for fees, expenses or taxes) | 4.67 | % | 6.66 | % | 6.98 | % | |||

Russell 1000 Growth Index3 (Reflects no deductions for fees, expenses or taxes) | 29.75 | % | -5.11 | % | 9.21 | % | |||

Lehman Brothers Aggregate Bond Index4 (Reflects no deductions for fees, expenses or taxes) | 4.10 | % | 6.62 | % | 6.95 | % | |||

Balanced Fund* | |||||||||

Class S (Return before Taxes) | 17.19 | % | 0.69 | % | 7.80 | % | |||

(Return after Taxes on distributions) | 15.37 | % | -2.46 | % | 3.19 | % | |||

(Return after Taxes on distributions and Sale of Fund Shares) | 9.99 | % | -2.07 | % | 2.76 | % | |||

Class AARP (Return before Taxes) | 17.26 | % | 0.70 | % | 7.80 | % | |||

S&P 500 Index1 (Reflects no deductions for fees, expenses or taxes) | 28.68 | % | -0.57 | % | 11.07 | % | |||

Russell 1000 Growth Index3 (Reflects no deductions for fees, expenses or taxes) | 29.75 | % | -5.11 | % | 9.21 | % | |||

Lehman Brothers Aggregate Bond Index4 (Reflects no deductions for fees, expenses or taxes) | 4.10 | % | 6.62 | % | 6.95 | % | |||

| (1) | The Standard & Poor’s 500 Composite Index is a capitalization-weighted index of 500 stocks. The index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. |

| (2) | The Lehman Brothers Government/Corporate Bond Index is an unmanaged index comprising intermediate and long-term government and investment-grade corporate debt securities. |

| (3) | The Russell 1000 Growth is an unmanaged capitalization-weighted index containing those securities in the Russell 1000 Index with higher book-to-price ratios and higher forecasted growth values. |

| (4) | The Lehman Brothers Aggregate Bond Index is an unmanaged, market value-weighted measure of treasury issues, corporate bond issues and mortgage securities. The Lehman Brothers Aggregate Bond Index will replace the Lehman Brothers Government/Corporate Bond Index as one of Total Return Fund’s primary benchmarks, as the Lehman Brothers Aggregate Bond Index is believed to be more reflective of the investment strategy pursued by Total Return Fund’s Advisor. |

14

Table of Contents

| (5) | Class S and Class AARP shares of Total Return Fund would have substantially similar annual returns as Class A shares, as the shares are invested in the same portfolio of securities, and would differ only to the extent that Class S and Class AARP shares do not have the same expenses as Class A shares. |

| * | In the table, total returns for 1995 through 1998 would have been lower if operating expenses had not been reduced. |

Current performance may be higher or lower than the performance data quoted above. For more recent performance information for Class S shares, call 1-800-SCUDDER or visit the website at www.myScudder.com or for Class AARP shares, call 1-800-253-2277 or visit the website at www.aarp.scudder.com.

Unlike the bar charts, the performance information for Class A shares of Total Return Fund in the table reflects the impact of maximum sales charges (5.75%). After-tax returns are estimates based on the historical highest individual federal income tax rates and do not reflect state and local taxes. Actual after-tax returns will depend on an investor’s tax situation and are likely to differ from those shown. After-tax returns for Total Return Fund are shown for Class A shares only and will vary for Class S and Class AARP. After-tax returns for Balanced Fund are shown for Class S shares only and will vary for Class AARP. After-tax returns are not relevant to those investing through 401(k) plans, IRAs or other tax-deferred arrangements.

III. Other Comparisons Between the Funds

Advisor and Portfolio Managers. Deutsche Investment Management Americas Inc. (“DeIM” or the “Advisor”) is the investment advisor for each Fund. Under the supervision of the Board of Trustees of each Fund, DeIM, with headquarters at 345 Park Avenue, New York, New York 10154, makes each Fund’s investment decisions, buys and sells securities for each Fund and conducts research that leads to these purchase and sale decisions. The Advisor is also responsible for selecting brokers and dealers and for negotiating brokerage commissions and dealer charges. DeIM is part of DeAM and an indirect wholly-owned subsidiary of Deutsche Bank AG. Deutsche Bank AG is a major global banking institution that is engaged in a wide range of financial services, including investment management, mutual fund, retail, private and commercial banking, investment banking and insurance.

Equity Team

Julie M. Van Cleave, CFA, is the Managing Director of DeAM and Lead Manager of the equity portion of each Fund. Ms. Van Cleave joined DeAM and each Fund in 2002 and is the Head of Large Cap Growth Portfolio Selection Team. Ms. Van Cleave’s previous experience includes 18 years’ investment industry experience at Mason Street Advisors, most recently serving as Managing Director and team leader for the large cap investment team. Ms. Van Cleave holds an MBA from the University of Wisconsin—Madison.

Jack A. Zehner is Director of DeAM and Portfolio Manager of each Fund. Mr. Zehner joined DeAM and each Fund in 2002. Mr. Zehner’s previous experience includes nine years’ investment industry experience at Mason Street Advisors where he served most recently as Director—Common Stock. Mr. Zehner holds an MBA from Marquette University.

15

Table of Contents

Thomas J. Schmid, CFA, is Director of DeAM and Portfolio Manager of each Fund. Mr. Schmid joined DeAM and each Fund in 2002. Mr. Schmid’s previous experience includes 15 years’ investment industry experience, most recently serving as Director—Common Stock at Mason Street Advisors. Mr. Schmid holds an MBA from the University of Chicago.

Fixed Income Team

J. Christopher Gagnier is Managing Director of DeAM and Portfolio Manager of each Fund. Mr. Gagnier joined DeAM in 1997 and each Fund in 2002. Prior to that, Mr. Gagnier was portfolio manager at Paine Webber from 1984 to 1997. An analyst specializing in asset-backed securities and government investments, Mr. Gagnier has over 25 years of investment industry experience and holds an MBA from the University of Chicago.

Gary W. Bartlett, CFA, is Managing Director of DeAM and Portfolio Manager of each Fund. Mr. Bartlett joined DeAM in 1992 and each Fund in 2002. An analyst specializing in taxable municipal and government investments, Mr. Bartlett has over 23 years of investment industry experience and holds an MBA from Drexel University.

Warren S. Davis is Managing Director of DeAM and Portfolio Manager of each Fund. Mr. Davis joined DeAM in 1995 and each Fund in 2002. An analyst specializing in mortgage- and asset-backed securities, Mr. Davis has over 19 years of investment industry experience and holds an MBA from Drexel University.

Daniel R. Taylor, CFA, is Managing Director of DeAM and Portfolio Manager of each Fund. Mr. Taylor joined DeAM in 1998 and each Fund in 2002. Prior to that, Mr. Taylor was fixed income portfolio manager, asset-backed securities analyst and senior credit analyst with CoreStates Investment Advisors from 1992 to 1998. An analyst specializing in asset-backed securities and government securities, Mr. Taylor has over 12 years of investment industry experience.

Thomas J. Flaherty is Managing Director of DeAM and Portfolio Manager of each Fund. Mr. Flaherty joined DeAM in 1995 and each Fund in 2002. An analyst specializing in corporate bonds and mortgages, Mr. Flaherty has over 19 years of investment industry experience.

Andrew P. Cestone is Managing Director of DeAM and Portfolio Manager of each Fund. Mr. Cestone joined DeAM in 1998 and each Fund in 2002. Prior to that, Mr. Cestone was an investment analyst with Phoenix Investment Partners from 1997 to 1998, and credit officer, asset based lending group with Fleet Bank from 1995 to 1997.

William T. Lissenden is Director of DeAM and Portfolio Manager of each Fund. Mr. Lissenden joined DeAM in 2002 and each Fund in 2003. Prior to that, Mr. Lissenden had 31 years of experience as a fixed income strategist and director of research at Conseco Capital Management, director of fixed income research and product management at Prudential Securities, national sales manager for fixed income securities at Prudential Securities and institutional sales professional at several firms including Prudential, Goldman Sachs and Merrill Lynch. Mr. Lissenden holds an MBA from Baruch College.

16

Table of Contents

Timothy C. Vile, CFA, is Managing Director of DeAM and Portfolio Manager of each Fund. Mr. Vile joined DeAM in 1991 and each Fund in 2003. Prior to that, Mr. Vile was a portfolio manager for fixed income portfolios at Equitable Capital Management. Mr. Vile has over 20 years of investment industry experience.

Brett Diment is Managing Director of DeAM and Consultant to Total Return Fund. Mr. Diment joined DeAM in 1991 and Total Return Fund in 2002. Mr. Diment is the Head of Emerging Market Debt for London Fixed Income and is responsible for coordinating research into Continental European markets and managing global fixed income, balanced and cash based portfolios: London. Mr. Diment began his investment career in 1991.

Asset Allocation Team

Janet Campagna is Managing Director of DeAM and Portfolio Manager of each Fund. Ms. Campagna joined DeAM in 1999 and each Fund in 2002. The head of global and tactical asset allocation, Ms. Campagna was an investment strategist and manager of the asset allocation strategies group for Barclays Global Investors from 1994 to 1999. Ms. Campagna has over 16 years of investment industry experience. She holds a Master’s degree in Social Science from California Institute of Technology and has a Ph.D. in Political Science from University of California at Irvine.

Distribution and Service Fees. Pursuant to separate Underwriting and Distribution Services Agreements, Scudder Distributors, Inc. (“SDI”), 222 South Riverside Plaza, Chicago, Illinois 60606, an affiliate of DeIM, is the principal underwriter, distributor and administrator for the Class A, Class B, Class C, Class R, Institutional Class, Class S and Class AARP shares of Total Return Fund, and acts as agent of each Fund in the continuing offer of such shares. Pursuant to an underwriting agreement, SDI is the principal underwriter for the Class S and Class AARP shares of Balanced Fund. Rule 12b-1 distribution plans have not been adopted for Class S shares or Class AARP shares of either Fund.

Trustees and Officers. The Trustees of Scudder Portfolio Trust (of which Balanced Fund is a series) are different from those of Scudder Total Return Fund. The following individuals comprise the Board of Trustees of the Trust: Dawn-Marie Driscoll (Chair), Henry P. Becton, Jr., Keith R. Fox, Louis E. Levy, Jean Gleason Stromberg, Jean C. Tempel and Carl W. Vogt. The following individuals comprise the Board of Trustees of Scudder Total Return Fund: John W. Ballantine, Lewis A. Burnham, Donald L. Dunaway, James R. Edgar, Paul K. Freeman, Robert B. Hoffman, Shirley D. Peterson (Chair), Fred B. Renwick (who will retire at the end of the year), William N. Shiebler and John G. Weithers. The officers of the Trust are the same as those of Scudder Total Return Fund, except that Philip J. Collora, Vice President and Assistant Secretary of Scudder Total Return Fund, is not an officer of Scudder Portfolio Trust, and John Millette, Secretary of Scudder Total Return Fund, is Vice President and Secretary of Scudder Portfolio Trust.

Independent Registered Public Accounting Firms (“Auditors”). Total Return Fund’s Auditors are Ernst & Young LLP. Balanced Fund’s Auditors are PricewaterhouseCoopers LLP.

17

Table of Contents

Charter Documents.

Scudder Portfolio Trust

General. The Trust is an open-end management investment company, which was established as a Massachusetts business trust pursuant to an Agreement and Declaration of Trust dated September 20, 1984, as amended (“Declaration of Trust”). Scudder Balanced Fund is a diversified series of the Trust. The Trust is also governed by its bylaws and applicable state law.

Shares. The Trust is authorized to issue an unlimited number of shares of beneficial interest, of par value $0.01 per share, from an unlimited number of series of shares. All shares are fully paid and non-assessable, transferable, have no pre-emptive or conversion rights and are redeemable as described in the Balanced Fund Prospectus and the Balanced Fund SAI.

Voting Rights. The shareholders shall have power to vote only (i) for the election or removal of Trustees; (ii) with respect to any investment advisory or management contract entered into; (iii) with respect to termination of the Trust; (iv) with respect to any amendment of the Declaration of Trust; (v) with respect to any merger, consolidation or sale of assets; (vi) with respect to incorporation of the Trust, or any series; (vii) to the same extent as the stockholders of Massachusetts business corporation as to whether or not a court action, proceeding or claim should or should not be brought or maintained derivatively or as a class action on behalf of the Trust or the Shareholders; (viii) with respect to any plan adopted pursuant to Rule 12b-1 (or any successor rule) under the 1940 Act; and (ix) with respect to such additional matters relating to the Trust as may be required by the Declaration of Trust, the By-laws or any registration of the Trust as an investment company under the 1940 Act with the SEC (or any successor agency) or as the Trustees may consider necessary or desirable. Each whole share shall be entitled to one vote as to any matter on which it is entitled to vote and each fractional share shall be entitled to a proportionate fractional vote, except that the Trustees may, in conjunction with the establishment of any series of shares, establish or reserve the right to establish conditions under which the several series shall have separate voting rights or, if a series would not, in the sole judgment of the Trustees, be materially affected by a proposal, no voting rights. There shall be no cumulative voting in the election of Trustees.

Shareholder Meetings. The Trust is generally not required to hold meetings of its shareholders. Meetings of shareholders may be called at any time by the President, and shall be called by the President and Secretary at the request in writing or by resolution of a majority of Trustees, or at the written request of the holder or holders of ten percent or more of the total number of shares then issued and outstanding of the Trust entitled to vote at such meeting.

Election and Term of Trustees. The Trustees shall be elected by the shareholders owning of record a plurality of the shares voting at a meeting of shareholders. Except in the event of resignation or removal pursuant to the Declaration of Trust, or death, bankruptcy, adjudicated incompetence or other incapacity, each Trustee shall hold office until such time as less than a majority of the Trustees holding office have been elected by shareholders. In such event, the Trustees then in office will call a shareholders’ meeting for the election of Trustees.

18

Table of Contents

Shareholder Liability. Under Massachusetts law, shareholders of a series could, under certain circumstances, be held liable for the obligations of their series. However, the Trust’s Declaration of Trust disclaims shareholder liability for acts or obligations of the Trust and permits notice of such disclaimer to be given in each agreement, obligation, or instrument entered into or executed by a Fund or the Trust’s Trustees. Moreover, the Declaration of Trust of the Trust provides indemnification for all losses and expenses of any shareholder held liable for the obligations of their series. The indemnification and reimbursement required by the preceding sentence shall be made only out of the assets of the one or more series of which the shareholder who is entitled to indemnification or reimbursement was a shareholder at the time the act or event occurred which gave rise to the claim or liability, and the Fund may be covered by insurance. Thus the risk of a shareholder liability is considered by DeAM to be remote and not material, since it is limited to circumstances in which a disclaimer is inoperative and such Fund itself is unable to meet its obligations.

Trustee Liability. The Trustees of the Trust generally are not liable for any obligation of the Trust. The Trust will indemnify its Trustees against all liabilities and expenses, except for those arising from the Trustee’s willful misfeasance, bad faith, gross negligence or reckless disregard of such Trustee’s duties.

Scudder Total Return Fund

General. Scudder Total Return Fund (for purposes of this section only, the “Trust”) is an open-end management investment company, which was established as a Massachusetts business trust pursuant to a Declaration of Trust dated October 24, 1985, and effective January 31, 1986. Total Return Fund, pursuant to a reorganization, succeeded to the assets and liabilities of Kemper Total Return Fund, Inc., a Maryland corporation organized in 1963. Total Return Fund was known as Balanced Income Fund until 1972 and as Supervised Investors Income Fund, Inc. until 1977. Total Return Fund is classified as a diversified series of the Trust. The Trust is also governed by its bylaws and applicable state law.

Shares. The Trust is authorized to issue an unlimited number of shares of beneficial interest, without a par value, from an unlimited number of series of shares. All shares issued and outstanding are fully paid and non-assessable, transferable, have no pre-emptive or conversion rights and are redeemable as described in the Total Return Fund Prospectus and Total Return Fund SAI. Each share has equal rights with each other share of the same class of Total Return Fund as to voting, dividends, exchanges, conversion features and liquidation.

Voting Rights. On each matter submitted to a vote of shareholders of Scudder Total Return Fund, each full share is entitled to one vote, and each fractional share is entitled to a fractional vote. The Shareholders shall have power to vote only: (a) for the election or removal of Trustees; (b) with respect to any investment advisor or manager; (c) with respect to any termination or reorganization of the Trust or any series or class thereof; (d) with respect to any amendment of the Declaration of Trust; and (e) with respect to such additional matters relating to the Trust as may be required by law, the 1940 Act, the Declaration of Trust, the By-Laws or any registration of the Trust with the SEC (or any successor agency) or any state, or as the Trustees may consider necessary or desirable.

19

Table of Contents

Notwithstanding any other provision of the Declaration of Trust, on any matter submitted to a vote of shareholders all shares of the Trust then entitled to vote shall, except to the extent otherwise required or permitted by the preferences and special or relative rights or privileges of any class of shares, be voted by individual series and not in the aggregate or by class, except (a) when required by the 1940 Act, shares shall be voted in the aggregate and not by individual series; and (b) when the Trustees have more series or classes, then only shareholders of such series or class shall be entitled to vote thereon. There shall be no cumulative voting in the election of Trustees. Shares may be voted in person or by proxy. Until shares of any series or class are issued, the Trustees may exercise all rights of shareholders and may take any action required by law, the Declaration of Trust or the By-Laws to be taken by shareholders of such series or class.

Shareholder Meetings. The Trust generally is not required to hold annual meetings of shareholders unless required by the 1940 Act. Meetings of the shareholders may be called at any time by the Trustees, by the President or, if the Trustees and the President shall fail to call any meeting of shareholders for a period of 30 days after written application of one or more shareholders who hold at least 25% of all shares issued and outstanding and entitle to vote at the meeting (or 10% if the purpose of the meeting is to determine if a trustee shall be removed from office), then such shareholders may call such meeting. Each call of a meeting shall state the place, date, hour and purposes of the meeting.

Election and Term of Trustees. The Trustees shall be elected by the shareholders owning of record a plurality of the shares voting at a meeting of shareholders. Each Trustee serves until the next meeting of shareholders, if any, called for the purpose of electing Trustees and until the election and qualification of a successor or until such Trustee sooner dies, retires, resigns or is removed.

Shareholder Liability. Under Massachusetts law, shareholders of a series could, under certain circumstances, be held liable for the obligations of their series. However, the Trust’s Declaration of Trust disclaims shareholder liability for acts or obligations of the Trust and provides indemnification for all losses and expenses of any shareholder held liable for the obligations of this series. The indemnification and reimbursement required by the preceding sentence shall be made only out of the assets of the one or more series of which the shareholder who is entitled to indemnification or reimbursement was a shareholder at the time the act or event occurred which gave rise to the claim or liability.

Trustee Liability. The Trustees of the Trust generally are not liable for any obligation of the Trust. The Trust will indemnify its Trustees against all liabilities and expenses, except for those arising from the Trustee’s willful misfeasance, bad faith, gross negligence or reckless disregard of such Trustee’s duties.

The foregoing is only a summary of the charter documents of Scudder Total Return Fund and Scudder Portfolio Trust and is not a complete description of provisions contained in those sources. Shareholders should refer to the provisions of those documents and state law directly for a more thorough description.

Fund Accounting Fees. Scudder Fund Accounting Corporation (“SFAC”), Two International Place, Boston, Massachusetts 02110, a subsidiary of DeIM, is responsible

20

Table of Contents

for determining the net asset value per share of each Fund and maintaining the portfolio and general accounting records for each Fund. Balanced Fund pays a fee directly to SFAC. Total Return Fund does not pay a fee directly to SFAC, but indirectly pays for the services through its management fee.

IV. Information About the Proposed Merger

General. The shareholders of Balanced Fund are being asked to approve a merger between Balanced Fund and Total Return Fund pursuant to an Agreement and Plan of Reorganization between the Funds (the “Agreement”), the form of which is attached to this Prospectus/Proxy Statement as Exhibit A.

The merger is structured as a transfer of all of the assets of Balanced Fund to Total Return Fund in exchange for the assumption by Total Return Fund of all liabilities of Balanced Fund and for the issuance and delivery to Balanced Fund of Merger Shares of Total Return Fund equal in aggregate value to the net value of the assets transferred to Total Return Fund.

After receipt of the Merger Shares, Balanced Fund will distribute the Merger Shares to its shareholders, in proportion to their existing shareholdings, in complete liquidation of Balanced Fund, and the legal existence of Balanced Fund as a series of Scudder Portfolio Trust will be terminated. Each shareholder of Balanced Fund will receive a number of full and fractional Merger Shares of the same class(es) as, and equal in value at the date of the exchange to, the aggregate value of the shareholder’s Balanced Fund shares.

Prior to the date of the merger, Balanced Fund will sell all investments that are not consistent with the current investment objective, policies and restrictions of Total Return Fund, if any, and declare a taxable distribution which, together with all previous distributions, will have the effect of distributing to shareholders all of its net investment income and net realized capital gains, if any, through the date of the merger. The sale of such investments may increase the taxable distribution to shareholders of Balanced Fund occurring prior to the merger above that which they would have received absent the merger. [DeIM has represented that, as of , 2004, Balanced Fund did not have any investments that were not consistent with the current investment objective, policies and restrictions of Total Return Fund.]