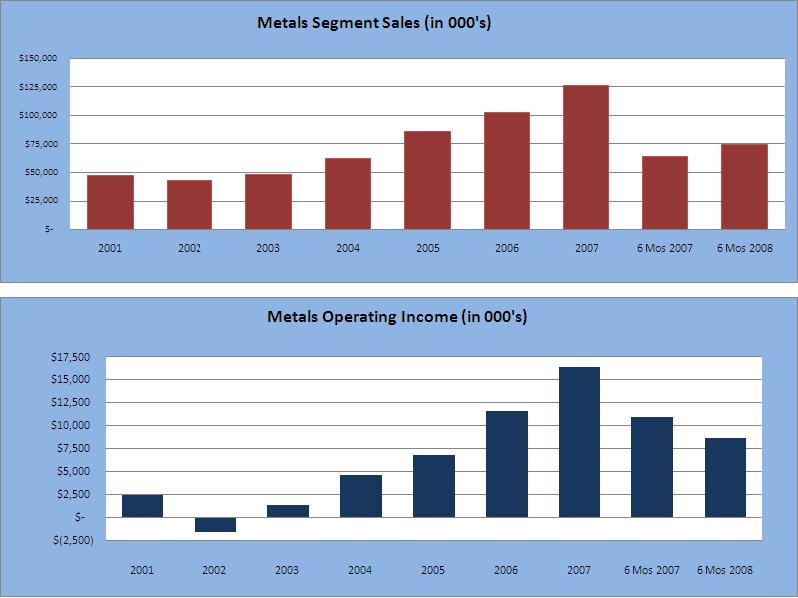

METALS SEGMENT – BRISTOL METALS

LARGEST DOMESTIC PRODUCER OF STAINLESS STEEL PIPE

PROVIDER OF TOTAL PIPING SOLUTIONS FOR GLOBAL INFRASTRUCTURE

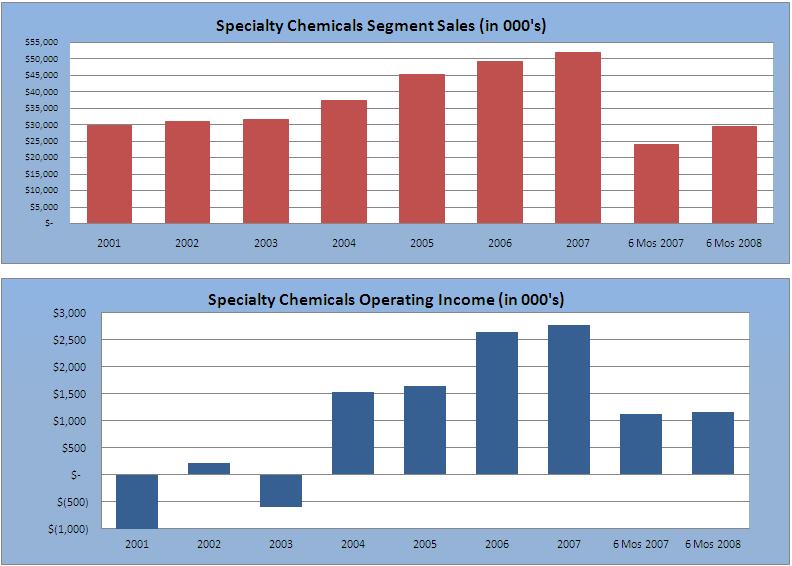

SPECIALTY CHEMICALS SEGMENT

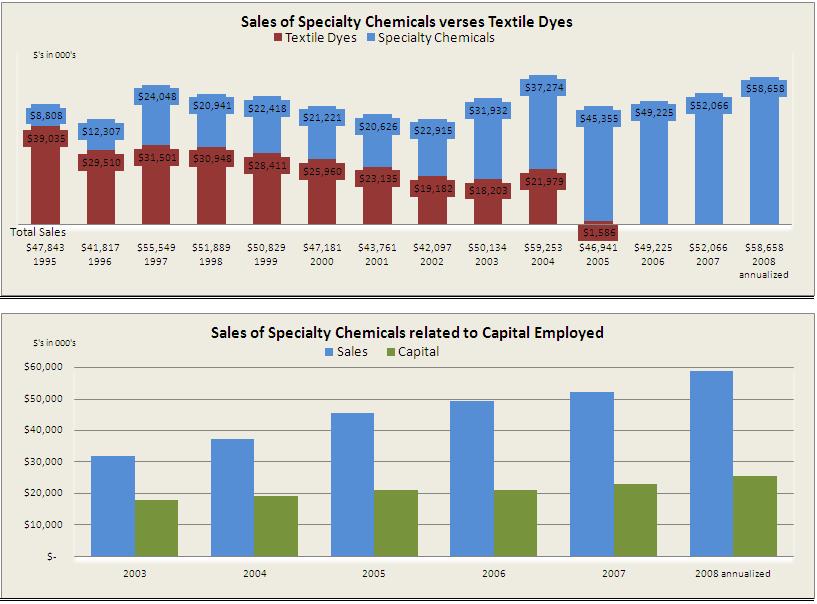

TRANSITIONED FROM TEXTILE DYES INTO A HIGH QUALITY PROVIDER OF SPECIALTY CHEMICALS TO DOMESTIC AND OVERSEAS CUSTOMERS

BRISTOL METALS

UNIQUE CHARACTERISTICS OF BRISTOL METALS:

Largest domestic manufacturer of welded stainless steel pipe

Producer of all size ranges from ½ inch to 120 inches in diameter, up to 16 inches utilizing continuous mills, in wall thicknesses of up to 1 ½ inch and in lengths up to 60 feet

Producer of all types of austenitic stainless steel and high-nickel alloys with capabilities that include real time x-ray and hydro-testing

Plant expansions completed in 2006 and 2007, allow the manufacture of pipe up to 42 inches in diameter utilizing more readily available raw materials at lower costs, provide improved product handling and additional space for planned equipment additions.

Piping systems operation that processes a significant amount of our pipe production into piping systems that conform to engineered drawings furnished by customers

Low-cost producer including purchase of stainless steel

Strategically located domestically within primary markets utilizing stainless steel pipe

Management team that has demonstrated the ability to identify and penetrate new markets, such as power generation and waste water treatment, for its products transitioning from a commodity business into a specialty pipe operation

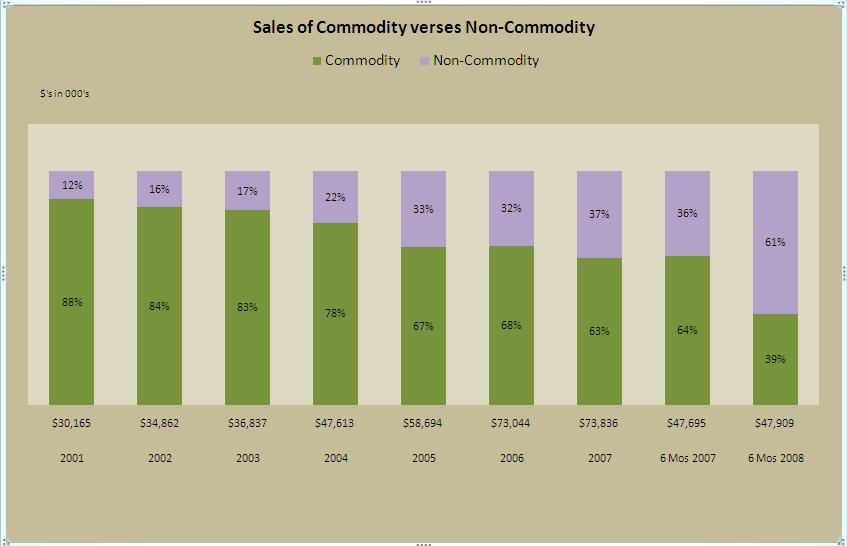

COMMODITY PIPE OPERATION

CUSTOMER BASE

Bristol Metals sells its commodity pipe primarily through distribution including all of the major PVF distributor houses:

McJunkin Redman, Southwest Stainless (HD Supply), Ferguson Enterprises, Warren Alloys, Robert James Sales, Wilson Supply, Global Stainless

COMMODITY PRICING

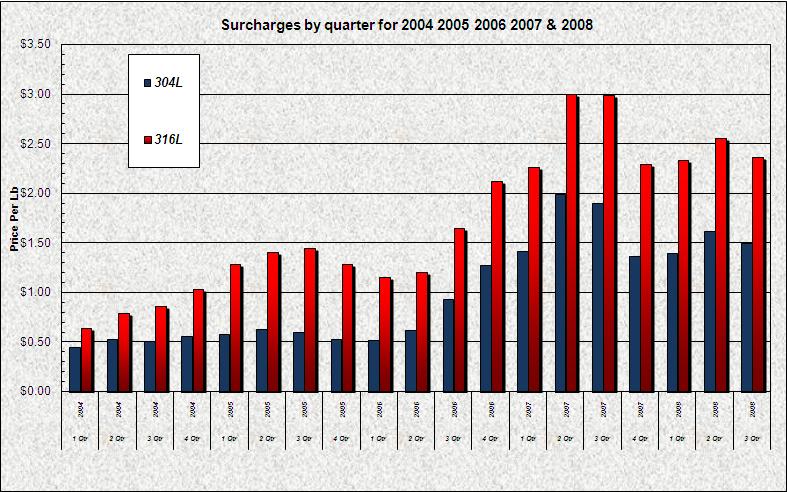

Commodity prices are significantly influenced by surcharges paid to the steel mills based primarily on nickel (304 & 316) and molybdenum (316), and to a lesser extent on chromium. These surcharges, which make up as much as ½ of the selling prices are routinely passed on to the customer (See attached graph on surcharges)

Surcharges are quoted 2 months out and are calculated based on the average of the current month’s surcharges paid by the steel mills to their suppliers. They are included as part of the raw material cost based on the date the material is received, and charged to the customer based on the date the pipe is shipped. Under FIFO inventory costing, increases in surcharges generally have a positive impact on profitability while decreases have a negative impact

COMPETITION

There are 3 primary domestic competitors – Outokumpu (Wildwood, FL), Marcegaglia (Munhall, PA) and Felker Bros (Marshfield, WI) capable of producing most size ranges, and several smaller domestic producers with limited capabilities.

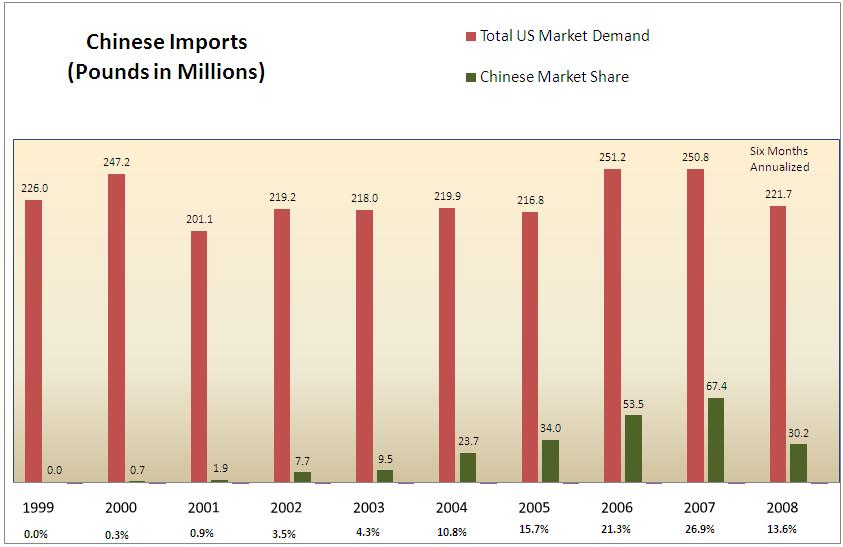

Foreign imports, primarily Chinese, are significant especially in smaller diameters up to 8 inches (See attached graph)

A successful trade case filed in the 1st quarter of 2008 against Chinese imports appeared to curtail the import growth in 2008. On August 28, 2008, the Dept. of Commerce announced the preliminary determination of countervailing and anti-dumping duties ranging from 22% to 128% on imported stainless steel welded pipe smaller than 16 inch from China which should continue to positively impact the domestic pipe market over the next several years

SUPPLIERS

Stainless steel coils and sheet are purchased primarily from domestic mills such as Allegheny Ludlum (Allegheny Technologies, sym: ATI), North American Stainless (Acerinox Group, sym: ACX.MC), and AK Steel (sym: AK), and foreign suppliers in Europe and Asia such as Arcelor Mittal (sym: MT)

NON-COMMODITY PIPE OPERATIONS

BUSINESS DESCRIPTION

Includes sales of large diameter (18 inch and larger) 304L and 316L pipe, sales of other alloy pipe, and fabrication of piping systems

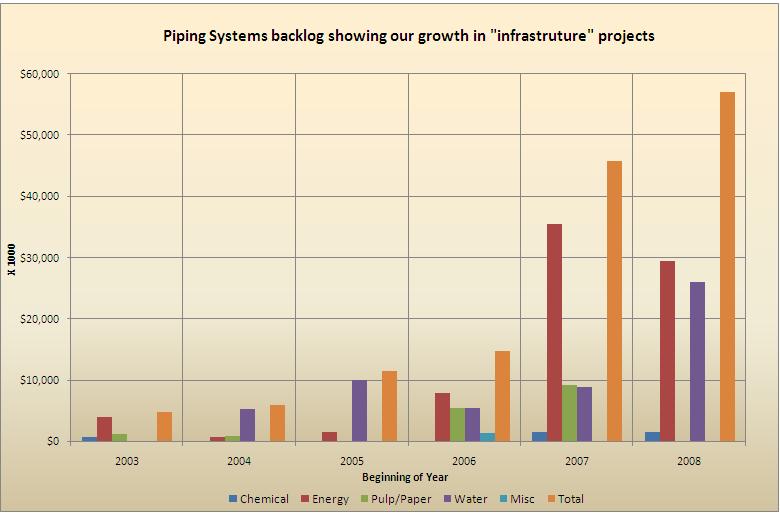

Piping Systems has transitioned from primarily the pulp and paper and chemical industries to a focus on infrastructure projects in industries such as liquid natural gas (LNG), power generation, waste water treatment and water treatment (See attached backlog graph)

Non-commodity pipe is sold to order allowing us to lock in material costs minimizing the surcharge impact

We are only 1 of 2 domestic producers that makes pipe and further processes it into piping systems

CUSTOMER BASE

Piping Systems has a strong on-going relationship with all of the major engineering, procurement and construction companies, including: BE&K, Bechtel, Chicago Bridge & Iron, Fluor, and AMEC

Our strong customer relationships allow us to participate in current project activities of our customers most of which currently have historically high backlogs

Project business gives us 2 opportunities to book business for each project – 1) to fabricate the piping systems from our pipe, and 2), if unable to obtain the award for the fabrication, to supply the loose pipe requirements of the project

COMPETITION

Domestic fabrication competitors include Shaw Group (Baton Rouge, LA), Turner IPS (Baton Rouge, LA), and Team Industries, Inc. (Appleton, WI)

Foreign competitors include Butting (Germany), Rivit Inoxtech (Italy), and EEW (Germany)

FUTURE OPPORTUNITIES FOR NON-COMMODITY PIPE IN THE “INFRASTRUCTURE” MARKET AREAS

LIQUID NATURAL GAS -

7 new US LNG Regas terminals proposed to FERC

12 new US LNG Regas terminals approved by FERC but not yet under construction

3 new Canadian Regas terminals approved but not yet under construction

1 new Mexican Regas terminal approved but not yet under construction

4-5 new Liquefaction projects will proceed in the next 1-3 years in the Middle East, Asia and Australia

2 Projects proceeding in South America

COAL FIRE PROJECTS – 4 new coal fire projects by 2011

SCRUBBER INSTALLATIONS – more than 260 scrubber units to be installed in the United States

WATER & WASTE WATER TREATMENT - We are currently tracking 13 WWTP projects with an estimated bid range of $5-$10MM each

DESALINATION - - We have participated in the domestic desalination business in the past 3 years and continue to track potential projects in North America. In addition, we see a real potential from the large scale facilities planned for the Middle East

ETHANOL - While ethanol is slowing, there are still 538 projects in the planned or approved status.

NUCLEAR – Although 7 to 10 years away, we have the necessary qualifications, such as an N-Stamp, and A&E and contractor contacts to participate in this market successfully

THE SYNALLOY CHEMICALS GROUP

BUSINESS DESCRIPTION AND STRATEGIES

The Synalloy Chemicals Group consists of 3 operations in 2 locations: Manufacturers’ Chemicals (MC) located in Cleveland, TN, and Blackman Uhler Chemicals (BU) and Organic Pigments (OP) located in Spartanburg, SC.

The Group produces specialty chemicals, pigments and dyes for the carpet, chemical, paper, metals, mining, photographic, pharmaceutical, agriculture, fiber, paint, textile, automotive, petroleum, cosmetics, mattress, furniture, janitorial, and other industries

Focus on industries and markets that have good prospects for sustainability in the U.S. in light of global trends

Rely on sales to end users through our own sales force, but also sell chemical intermediates to other chemical companies and distributors

Utilize close working relationships with a significant number of major chemical companies that outsource their production for regional manufacture and distribution to specialty chemical companies of our size to provide contract production and toll manufacturing

Capitalize on process & equipment to fully utilize capacity

Broaden end use markets & sell across company lines by:

Focusing on fast customer response opportunities

Focusing on right first time, product consistency and on-time delivery, monitoring through continuous tracking

Use renewable feed-stocks wherever possible

Utilize milling technology to produce chemical dispersions of fine particle size

Expand exports through growth of business with strategic partners aimed at paper and agriculture industries

SALES TARGETS

To End Users through Sales Force

Reaction Intermediates to other Chemical Companies

Contract or Toll Manufacturing for Large Producers & Marketing Based Companies

MARKETS

Paper & Pulp

Water Treatment The markets in this group are also served by Bristol Metals

Oil Refining

Chemical Intermediates

Mining

Agriculture

Construction Materials

Latex & Rubber Products

Textile & Carpet

Plastics

Automotive

Coatings

Cosmetics

Surgical Devices

Leather

Metal Working

Wire Coating

Mattress & Upholstery

Graphic Arts & Ink

Paint

PROCESSES AND CAPACITIES

| Manufacturers Chemicals | | Blackman Uhler | | Organic Pigments |

| | Esterification | | | Hydrogenation | | | Aqueous Pigment Dispersion |

| | Amidation | | | Epoxidation | | | Aqueous Chemical Dispersion |

| | Condensation | | | Methylation | | | Dispersions in Oils |

| | Imidazolines | | | Carboxylation | | | |

| | Phosphation | | | Nitration | | | |

| | Sulfation | | | Polymerization | | | |

| | Quaternization | | | | | | |

| | Hydrophobization | | Milling | | | |

| | Dye Blending | | | Spray Drying | | | |

| | Homogenization | | | Kosher Certification | | | |

| | Blending | | | ISO Certification | | | |

| | ISO Certification | | | (in addition to all items done at MC) |