Filed Pursuant to Rule 424(b)(2) Registration No. 333-228614 |

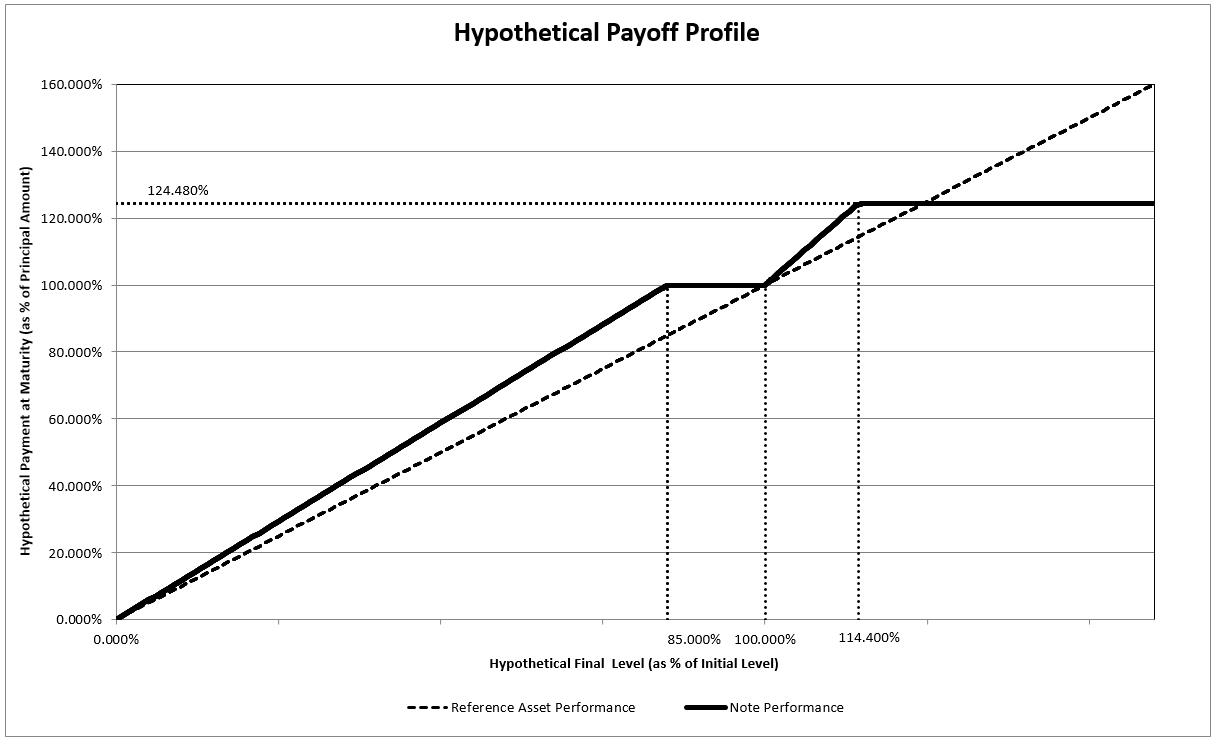

| ● | if the final level is greater than the initial level (the percentage change is positive), you will receive an amount in cash equal to the sum of (i) $1,000 plus (ii) the product of (a) $1,000 times (b) the percentage change times (c) 170%, subject to the maximum payment amount; |

| ● | if the final level is equal to the initial level or less than the initial level, but not by more than 15.00% (the percentage change is zero or negative but equal to or greater than -15.00%), you will receive an amount in cash equal to $1,000; or |

| ● | if the final level is less than the initial level by more than 15.00% (the percentage change is negative and is less than -15.00%), you will receive an amount in cash equal to the sum of (i) $1,000 plus (ii) the product of (a) $1,000 times (b) the buffer rate of approximately 117.65% times (c) the sum of the percentage change plus 15.00%. |

| Per Note | Total | |

| Original Issue Price | 100.00% | $6,789,000.00 |

| Underwriting commissions | 0.00% | $0.00 |

| Proceeds to The Bank of Nova Scotia | 100.00% | $6,789,000.00 |

Scotia Capital (USA) Inc. |

Issuer: | The Bank of Nova Scotia (the “Bank”) | |

Issue: | Senior Note Program, Series A | |

CUSIP/ISIN: | CUSIP: 064159QM1 / ISIN: US064159QM19 | |

Type of Notes: | Capped Buffered Enhanced Participation Notes | |

Reference Asset: | The S&P 500® Index (Bloomberg Ticker: SPX) | |

Minimum Investment and Denominations: | $1,000 and integral multiples of $1,000 in excess thereof | |

Principal Amount: | $1,000 per note; $6,789,000 in the aggregate for all the offered notes; the aggregate principal amount of the offered notes may be increased if the Bank, at its sole option, decides to sell an additional amount of the offered notes on a date subsequent to the date of this pricing supplement. | |

Original Issue Price: | 100% of the principal amount of each note | |

Currency: | U.S. dollars | |

Trade Date: | October 25, 2019 | |

Original Issue Date: | November 1, 2019 Delivery of the notes will be made against payment therefor on the 5th business day following the date of pricing of the notes (this settlement cycle being referred to as “T+5”). Under Rule 15c6-1 of the Securities Exchange Act of 1934, as amended, trades in the secondary market generally are required to settle in two business days (“T+2”), unless the parties to any such trade expressly agree otherwise. Accordingly, purchasers who wish to trade the notes on or prior to the second business day before delivery of the notes will be required, by virtue of the fact that each note initially will settle in five business days (T+5), to specify alternative settlement arrangements to prevent a failed settlement. | |

Valuation Date: | February 22, 2022 The valuation date could be delayed by the occurrence of a market disruption event. See “General Terms of the Notes—Market Disruption Events” beginning on page PS-20 in the accompanying product prospectus supplement. Further, if the valuation date is not a trading day, the valuation date will be postponed in the same manner as if a market disruption event has occurred. | |

Maturity Date: | February 24, 2022, subject to adjustment due to a market disruption event, a non-trading day or a non-business day as described in more detail under “General Terms of the Notes—Maturity Date” on page PS-18 in the accompanying product prospectus supplement. |

Principal at Risk: | You may lose all or a substantial portion of your initial investment at maturity if there is a percentage decrease from the initial level to the final level of more than 15.00%. | |

Purchase at amount other than principal amount: | The amount we will pay you on the maturity date for your notes will not be adjusted based on the original issue price you pay for your notes, so if you acquire notes at a premium (or discount) to the principal amount and hold them to the maturity date, it could affect your investment in a number of ways. The return on your investment in such notes will be lower (or higher) than it would have been had you purchased the notes at the principal amount. Also, the stated buffer level would not offer the same measure of protection to your investment as would be the case if you had purchased the notes at the principal amount. Additionally, the maximum payment amount would be triggered at a lower (or higher) percentage return than indicated below, relative to your initial investment. See “Additional Risks—If you purchase your notes at a premium to the principal amount, the return on your investment will be lower than the return on notes purchased at the principal amount and the impact of certain key terms of the notes will be negatively affected” beginning on page P-19 of this pricing supplement. | |

Fees and Expenses: | As part of the distribution of the notes, SCUSA or one of our other affiliates has agreed to sell the notes to certain unaffiliated securities dealers at the original issue price per note specified on the cover hereof. See “Supplemental Plan of Distribution (Conflicts of Interest)” in this pricing supplement. The price at which you purchase the notes includes costs that the Bank or its affiliates expect to incur and profits that the Bank or its affiliates expect to realize in connection with hedging activities related to the notes, as set forth below under “Supplemental Plan of Distribution (Conflicts of Interest)”. These costs and profits will likely reduce the secondary market price, if any secondary market develops, for the notes. As a result, you may experience an immediate and substantial decline in the market value of your notes on the trade date. See “Additional Risks—Hedging activities by the Bank and SCUSA may negatively impact investors in the notes and cause our respective interests and those of our clients and counterparties to be contrary to those of investors in the notes” in this pricing supplement. | |

Payment at Maturity: | The payment at maturity, for each $1,000 principal amount of notes, will be based on the performance of the reference asset and will be calculated as follows: | |

• If the final level is greater than the initial level, then the payment at maturity will equal: o The lesser of (a) principal amount + [principal amount x percentage change x participation rate] and (b) maximum payment amount | ||

• If the final level is greater than or equal to the buffer level, but less than or equal to the initial level, then the payment at maturity will equal the principal amount • If the final level is less than the buffer level, then the payment at maturity will equal: o principal amount + [principal amount x buffer rate x (percentage change + buffer percentage)] In this case you will suffer a percentage loss on your initial investment equal to the buffer rate multiplied by the negative percentage change in excess of the buffer percentage. Accordingly, you could lose up to 100% of your initial investment. | ||

Closing Level: | As used herein, the “closing level” of the reference asset on any date will be determined based upon the closing level published on the Bloomberg Professional® service |

(“Bloomberg”) page “SPX <Index>” or any successor page on Bloomberg or any successor service, as applicable, on such date. | ||

Initial Level: | 3,022.55, which was the closing level of the reference asset on the trade date. | |

Final Level: | The closing level of the reference asset on the valuation date. In certain special circumstances, the final level will be determined by the calculation agent, in its discretion. See “General Terms of the Notes—Unavailability of the Level of the Reference Asset on a Valuation Date” beginning on page PS-19 and “General Terms of the Notes—Market Disruption Events” beginning on page PS-20 in the accompanying product prospectus supplement. | |

Percentage Change: | The percentage change, expressed as a percentage, with respect to the payment at maturity, is calculated as follows: final level – initial level initial level For the avoidance of doubt, the percentage change may be a negative value. | |

Participation Rate: | 170.00% | |

Buffer Level: | 85.00% of the initial level | |

Buffer Percentage: | 15.00% | |

Buffer Rate: | The quotient of the initial level divided by the buffer level, which equals approximately 117.65% | |

Maximum Payment Amount: | $1,244.80 for each $1,000 principal amount of your notes, which equals the principal amount x 124.480%. The maximum payment amount sets a cap on appreciation of the reference asset of 14.40%. | |

Form of Notes: | Book-entry | |

Calculation Agent: | Scotia Capital Inc., an affiliate of the Bank | |

Status: | The notes will constitute direct, unsubordinated and unsecured obligations of the Bank ranking pari passu with all other direct, unsecured and unsubordinated indebtedness of the Bank from time to time outstanding (except as otherwise prescribed by law). Holders will not have the benefit of any insurance under the provisions of the CDIC Act, the U.S. Federal Deposit Insurance Act or under any other deposit insurance regime of any jurisdiction. | |

Tax Redemption: | The Bank (or its successor) may redeem the notes, in whole but not in part, at a redemption price determined by the calculation agent in a manner reasonably calculated to preserve your and our relative economic position, if it is determined that changes in tax laws or their interpretation will result in the Bank (or its successor) becoming obligated to pay additional amounts with respect to the notes. See “Tax Redemption” in the accompanying product prospectus supplement. | |

Listing: | The notes will not be listed on any securities exchange or quotation system. |

Use of Proceeds: | General corporate purposes | |

Clearance and Settlement: | Depository Trust Company | |

Trading Day: | A day on which the respective principal securities markets for all of the stocks comprising the reference asset (the “reference asset constituent stocks”) are open for trading, the sponsor of the reference asset (the “sponsor”) is open for business and the reference asset is calculated and published by the sponsor. | |

Business Day: | New York and Toronto | |

Terms Incorporated: | All of the terms appearing above the item under the caption “General Terms of the Notes” beginning on page PS-15 in the accompanying product prospectus supplement, as modified by this pricing supplement. | |

Canadian Bail-in: | The notes are not bail-inable debt securities under the CDIC Act. |

| ● | You fully understand the risks inherent in an investment in the notes, including the risk of losing all or a substantial portion of your initial investment. |

| ● | You can tolerate a loss of up to 100% of your initial investment. |

| ● | You are willing to make an investment that, if the final level is less than the buffer level, has an accelerated downside risk greater than the downside market risk of an investment in the reference asset or in the reference asset constituent stocks. |

| ● | You believe that the level of the reference asset will appreciate over the term of the notes and that the appreciation is unlikely to exceed the cap on appreciation within the maximum payment amount. |

| ● | You are willing to hold the notes to maturity, a term of approximately 28 months, and accept that there may be little or no secondary market for the notes. |

| ● | You understand and accept that your potential payment at maturity is limited to the maximum payment amount and you are willing to invest in the notes based on the maximum payment amount indicated on the cover hereof. |

| ● | You can tolerate fluctuations in the price of the notes prior to maturity that may be similar to or exceed the downside fluctuations in the level of the reference asset or in the price of the reference asset constituent stocks. |

| ● | You do not seek current income from your investment. |

| ● | You are willing to assume the credit risk of the Bank for all payments under the notes, and understand that if the Bank defaults on its obligations you may not receive any amounts due to you including any repayment of principal. |

| ● | You do not fully understand the risks inherent in an investment in the notes, including the risk of losing all or a substantial portion of your initial investment. |

| ● | You require an investment designed to guarantee a full return of principal at maturity. |

| ● | You cannot tolerate a loss of all or a substantial portion of your initial investment. |

| ● | You are not willing to make an investment that, if the final level is less than the buffer level, has an accelerated downside risk greater than the downside market risk of an investment in the reference asset or in the reference asset constituent stocks. |

| ● | You believe that the level of the reference asset will decline during the term of the notes and the final level will likely be less than the buffer level, or you believe the level of the reference asset will appreciate over the term of the notes and that the appreciation is likely to equal or exceed the cap on appreciation within the maximum payment amount. |

| ● | You seek an investment that has unlimited return potential without a cap on appreciation or you are unwilling to invest in the notes based on the maximum payment amount indicated on the cover hereof. |

| ● | You cannot tolerate fluctuations in the price of the notes prior to maturity that may be similar to or exceed the downside fluctuations in the level of the reference asset or in the price of the reference asset constituent stocks. |

| ● | You seek current income from your investment or prefer to receive dividends paid on the reference asset constituent stocks. |

| ● | You are unable or unwilling to hold the notes to maturity, a term of approximately 28 months, or you seek an investment for which there will be a secondary market. |

| ● | You are not willing to assume the credit risk of the Bank for all payments under the notes. |

| Key Terms and Assumptions | |

Principal amount | $1,000 |

Participation rate | 170.00% |

Maximum payment amount | $1,244.80 for each $1,000 principal amount of your notes |

Buffer level | 85.00% of the initial level |

Buffer percentage | 15.00% |

Buffer rate | Approximately 117.65% |

Neither a market disruption event nor a non-trading day occurs on the originally scheduled valuation date | |

No change in or affecting any of the reference asset constituent stocks or the method by which the sponsor calculates the reference asset | |

Notes purchased on the original issue date at the principal amount and held to the maturity date | |

Hypothetical Final Level (as Percentage of Initial Level) | Hypothetical Payment at Maturity (as Percentage of Principal Amount) |

| 150.000% | 124.480% |

| 140.000% | 124.480% |

| 130.000% | 124.480% |

| 120.000% | 124.480% |

| 114.400% | 124.480% |

| 110.000% | 117.000% |

| 105.000% | 108.500% |

| 100.000% | 100.000% |

| 95.000% | 100.000% |

| 90.000% | 100.000% |

| 85.000% | 100.000% |

| 80.000% | 94.118% |

| 70.000% | 82.353% |

| 60.000% | 70.588% |

| 50.000% | 58.824% |

| 25.000% | 29.412% |

| 0.000% | 0.000% |

Example 1— | Calculation of the payment at maturity where the percentage change is positive. | |

| Percentage Change: | 5.00% | |

| Payment at Maturity: | $1,000.00 + ($1,000.00 x 170.00% x 5.00%) = $1,000.00 + $85.00 = $1,085.00 | |

| On a $1,000.00 investment, a 5.00% percentage change results in a payment at maturity of $1,085.00. | ||

Example 2— | Calculation of the payment at maturity where the percentage change is positive and the payment at maturity is subject to the maximum payment amount. | |

| Percentage Change: | 50.00% | |

| Payment at Maturity: | $1,000.00 + ($1,000.00 x 170.00% x 50.00%) = $1,000.00 + $850.00 = $1,850.00. However, the maximum payment amount is $1,244.80 and the payment at maturity would be $1,244.80. | |

| On a $1,000.00 investment, a 50.00% percentage change results in a payment at maturity of $1,244.80. | ||

Example 3— | Calculation of the payment at maturity where the percentage change is negative but is equal to or greater than -15.00%. | |

| Percentage Change: | -8.00% | |

| Payment at Maturity: | $1,000.00 (at maturity, if the percentage change is negative BUT the decrease is not more than the buffer percentage, then the payment at maturity will equal the principal amount). | |

| On a $1,000.00 investment, a -8.00% percentage change results in a payment at maturity of $1,000.00. | ||

Example 4— | Calculation of the payment at maturity where the percentage change is negative and is less than -15.00%. | |

| Percentage Change: | -50.00% | |

| Payment at Maturity: | $1,000.00 + [$1,000.00 x 117.65% x (-50.00% + 15.00%)] = $1,000.00 - $411.76 = $588.24 | |

On a $1,000.00 investment, a -50.00% percentage change results in a payment at maturity of $588.24. Accordingly, if the percentage change is less than -15.00%, the Bank will pay you less than the full principal amount, resulting in a percentage loss on your investment that is equal to the buffer rate multiplied by the negative percentage change in excess of the buffer percentage. You may lose up to 100% of your principal amount. | ||

We cannot predict the actual final level or what the market value of your notes will be on any particular trading day, nor can we predict the relationship between the level of the reference asset and the market value of your notes at any time prior to the maturity date. The actual amount that you will receive, if any, at maturity and the rate of return on the offered notes will depend on the actual final level, which will be determined by the calculation agent as described above. Moreover, the assumptions on which the hypothetical returns are based may turn out to be inaccurate. Consequently, the amount of cash to be paid in respect of your notes, if any, on the maturity date may be very different from the information reflected in the examples above. |

broker or lender. In those and other capacities, we, SCUSA and/or our other affiliates purchase, sell or hold a broad array of investments, actively trade securities (including the notes or other securities that we have issued), the reference asset constituent stocks, derivatives, loans, credit default swaps, indices, baskets and other financial instruments and products for our own accounts or for the accounts of our customers, and we will have other direct or indirect interests, in those securities and in other markets that may not be consistent with your interests and may adversely affect the level of the reference asset and/or the value of the notes. You should assume that we or they will, at present or in the future, provide such services or otherwise engage in transactions with, among others, us and the issuers of the reference asset constituent stocks, or transact in securities or instruments or with parties that are directly or indirectly related to these entities. These services could include making loans to or equity investments in those companies, providing financial advisory or other investment banking services, or issuing research reports. Any of these financial market activities may, individually or in the aggregate, have an adverse effect on the level of the reference asset and the market for your notes, and you should expect that our interests and those of SCUSA and/or our other affiliates, clients or counterparties, will at times be adverse to those of investors in the notes.

Corporate Action |

| Share Count Revision Required? |

| Divisor Adjustment Required? |

Stock split |

| Yes – share count is revised to reflect new count. |

| No – share count and price changes are off-setting |

Change in shares outstanding (secondary issuance, share repurchase and/or share buy-back) |

| Yes – share count is revised to reflect new count. |

| Yes |

Special dividends |

| No |

| Yes – calculation assumes that share price drops by the amount of the dividend; divisor adjustment reflects this change in index market value |

Change in IWF |

| No |

| Yes – divisor change reflects the change in market value caused by the change to an IWF |

Company added to or deleted from the S&P 500® Index |

| No |

| Yes – divisor is adjusted by the net change in market value, calculated as the shares issued multiplied by the price paid |

Rights Offering |

| No |

| Yes – divisor adjustment reflects increase in market capitalization (calculation assumes that offering is fully subscribed) |