|

MANAGEMENT’S DISCUSSION AND ANALYSIS |

TABLE OF CONTENTS

| | |

| 12 | | Forward-looking statements |

| 13 | | Non-GAAP measures |

| 14 | | Financial highlights |

| | |

| ¢ Overview |

| |

| 15 | | Financial results |

| 15 | | Economic outlook |

| 16 | | Shareholder returns |

| 17 | | Impact of foreign currency translation |

| | |

| ¢ Group Financial Performance |

| |

| 18 | | Net income |

| 18 | | Net interest income |

| 20 | | Non-interest income |

| 21 | | Provision for credit losses |

| 24 | | Non-interest expenses |

| 24 | | Income taxes |

| 25 | | Financial results review: 2015 vs 2014 |

| 27 | | Fourth quarter review |

| 29 | | Trending analysis |

| | |

| ¢ Group Financial Condition |

| |

| 30 | | Statement of financial position |

| 31 | | Capital management |

| 42 | | Off-balance sheet arrangements |

| 45 | | Financial instruments |

| 46 | | Selected credit instruments – publically known risk items |

| | |

| | |

| | |

| ¢ Business Lines |

| |

| 47 | | Overview |

| 49 | | Canadian Banking |

| 52 | | International Banking |

| 55 | | Global Banking and Markets |

| 58 | | Other |

| | |

| ¢ Risk Management |

| |

| 70 | | Credit risk |

| 80 | | Market Risk |

| 87 | | Liquidity risk |

| 96 | | Other risks |

| 96 | | Operational risk |

| 97 | | Reputational risk |

| 97 | | Environmental risk |

| 98 | | Insurance risk |

| 98 | | Strategic risk |

| | |

| ¢ Controls and Accounting Policies |

| |

| 99 | | Controls and procedures |

| 99 | | Critical accounting estimates |

| 103 | | Future accounting developments |

| 106 | | Regulatory developments |

| 107 | | Related party transactions |

| | |

| ¢ Supplementary Data |

| |

| 109 | | Geographic information |

| 112 | | Credit risk |

| 117 | | Revenues and expenses |

| 119 | | Selected quarterly information |

| 120 | | Eleven-year statistical review |

2 0 1 6 S C O T I A B A N K A N N U A L R E P O R T | 11

MANAGEMENT’S DISCUSSION AND ANALYSIS

FORWARD LOOKING STATEMENTS

Our public communications often include oral or written forward-looking statements. Statements of this type are included in this document, and may be included in other filings with Canadian securities regulators or the U.S. Securities and Exchange Commission, or in other communications. All such statements are made pursuant to the “safe harbor” provisions of the U.S. Private Securities Litigation Reform Act of 1995 and any applicable Canadian securities legislation. Forward-looking statements may include, but are not limited to, statements made in this document, the Management’s Discussion and Analysis in the Bank’s 2016 Annual Report under the headings “Overview-Outlook,” for Group Financial Performance “Outlook,” for each business segment “Outlook” and in other statements regarding the Bank’s objectives, strategies to achieve those objectives, the regulatory environment in which the Bank operates, anticipated financial results (including those in the area of risk management), and the outlook for the Bank’s businesses and for the Canadian, U.S. and global economies. Such statements are typically identified by words or phrases such as “believe,” “expect,” “anticipate,” “intent,” “estimate,” “plan,” “may increase,” “may fluctuate,” and similar expressions of future or conditional verbs, such as “will,” “may,” “should,” “would” and “could.”

By their very nature, forward-looking statements involve numerous assumptions, inherent risks and uncertainties, both general and specific, and the risk that predictions and other forward-looking statements will not prove to be accurate. Do not unduly rely on forward-looking statements, as a number of important factors, many of which are beyond the Bank’s control and the effects of which can be difficult to predict, could cause actual results to differ materially from the estimates and intentions expressed in such forward-looking statements. These factors include, but are not limited to: the economic and financial conditions in Canada and globally; fluctuations in interest rates and currency values; liquidity and funding; significant market volatility and interruptions; the failure of third parties to comply with their obligations to the Bank and its affiliates; changes in monetary policy; legislative and regulatory developments in Canada and elsewhere, including changes to, and interpretations of tax laws and risk-based capital guidelines and reporting instructions and liquidity regulatory guidance; changes to the Bank’s credit ratings; operational (including technology) and infrastructure risks; reputational risks; the risk that the Bank’s risk management models may not take into account all relevant factors; the accuracy and completeness of information the Bank receives on customers and counterparties; the timely development and introduction of new products and services in receptive markets; the Bank’s ability to expand existing distribution channels and to develop and realize revenues from new distribution channels; the Bank’s ability to complete and integrate acquisitions and its other growth strategies; critical accounting estimates and the effects of changes in accounting policies and methods used by the Bank as described in the Bank’s annual financial statements (See “Controls and Accounting Policies – Critical accounting estimates” in the Bank’s 2016 Annual Report) and updated by this document; global capital markets activity; the Bank’s ability to attract and retain key executives; reliance on third parties to provide components of the Bank’s business infrastructure; unexpected changes in consumer spending and saving habits; technological developments; fraud or other criminal behavior by internal or external parties, including the use of new technologies in unprecedented ways to defraud the Bank or its customers; increasing cyber security risks which may include theft of assets, unauthorized access to sensitive information or operational disruption; anti-money laundering; consolidation in the financial services sector in Canada and globally; competition, both from new entrants and established competitors including through internet and mobile banking; judicial and regulatory proceedings; natural disasters, including, but not limited to, earthquakes and hurricanes, and disruptions to public infrastructure, such as transportation, communication, power or water supply; the possible impact of international conflicts and other developments, including terrorist activities and war; the effects of disease or illness on local, national or international economies; and the Bank’s anticipation of and success in managing the risks implied by the foregoing. A substantial amount of the Bank’s business involves making loans or otherwise committing resources to specific companies, industries or countries. Unforeseen events affecting such borrowers, industries or countries could have a material adverse effect on the Bank’s financial results, businesses, financial condition or liquidity. These and other factors may cause the Bank’s actual performance to differ materially from that contemplated by forward-looking statements. For more information, see the “Risk Management” section Bank’s 2016 Annual Report.

Material economic assumptions underlying the forward-looking statements contained in this document are set out in the 2016 Annual Report under the heading “Overview-Outlook,” as updated by this document; and for each business segment “Outlook”. The “Outlook” sections are based on the Bank’s views and the actual outcome is uncertain. Readers should consider the above-noted factors when reviewing these sections. The preceding list of factors is not exhaustive of all possible risk factors and other factors could also adversely affect the Bank’s results. When relying on forward-looking statements to make decisions with respect to the Bank and its securities, investors and others should carefully consider the preceding factors, other uncertainties and potential events. The Bank does not undertake to update any forward-looking statements, whether written or oral, that may be made from time to time by or on its behalf.

Additional information relating to the Bank, including the Bank’s Annual Information Form, can be located on the SEDAR website at www.sedar.com and on the EDGAR section of the SEC’s website at www.sec.gov.

November 29, 2016

12 | 2 0 1 6 S C O T I A B A N K A N N U A L R E P O R T

MANAGEMENT’S DISCUSSION AND ANALYSIS | OVERVIEW

MANAGEMENT’S DISCUSSION & ANALYSIS

The Management’s Discussion and Analysis (MD&A) is provided to enable readers to assess the Bank’s financial condition and results of operations as at and for the year ended October 31, 2016. The MD&A should be read in conjunction with the Bank’s 2016 Consolidated Financial Statements and Notes. This MD&A is dated November 29, 2016.

Additional information relating to the Bank, including the Bank’s 2016 Annual Report, are available on the Bank’s website at www.scotiabank.com. As well, the Bank’s 2016 Annual Report and Annual Information Form are available on SEDAR at www.sedar.com and on the EDGAR section of the SEC’s website at www.sec.gov.

Non-GAAP Measures

The Bank uses a number of financial measures to assess its performance. Some of these measures are not calculated in accordance with Generally Accepted Accounting Principles (GAAP), which are based on International Financial Reporting Standards (IFRS), are not defined by GAAP and do not have standardized meanings that would ensure consistency and comparability among companies using these measures. The Bank believes that certain non-GAAP measures are useful in assessing underlying ongoing business performance and provide readers with a better understanding of how management assesses performance. These non-GAAP measures are used throughout this report and defined below.

T1 Impact of the 2016 restructuring charge

The table below reflects the impact of the 2016 restructuring charge of $378 million pre-tax ($278 million after tax)(1).

| | | | | | | | | | | | |

| | | |

For the year ended October 31, 2016 ($ millions) | | Reported | | | Impact of the

restructuring charge | | | Adjusting for the

restructuring charge | |

Net income ($ millions) | | $ | 7,368 | | | $ | 278 | | | $ | 7,646 | |

Diluted earnings per share | | $ | 5.77 | | | $ | 0.23 | | | $ | 6.00 | |

Return on equity | | | 13.8 | % | | | 0.5 | % | | | 14.3 | % |

Productivity ratio | | | 55.2 | % | | | (1.5 | )% | | | 53.7 | % |

Operating leverage | | | (1.9 | )% | | | 2.9 | % | | | 1.0 | % |

| | | | | | | | | | | | | |

| (1) | Calculated using the statutory tax rates of the various jurisdictions. |

T2 Adjusted diluted earnings per share

The adjusted diluted earnings per share (EPS) is calculated as follows:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | |

| | | 2016 | | | 2015 | | | 2014 | |

| For the year ended October 31 ($ millions) | | Diluted EPS(1) | | | Diluted EPS(1) | | | Diluted EPS(1) | |

Net income attributable to common shareholders (diluted) (refer to Note 33) | | $ | 7,070 | | | $ | 5.77 | | | $ | 6,983 | | | $ | 5.67 | | | $ | 6,924 | | | $ | 5.66 | |

Restructuring charge | | | 278 | | | | 0.23 | | | | – | | | | – | | | | 110 | | | | 0.09 | |

Net income attributable to common shareholders (diluted) adjusting for restructuring charge | | | 7,348 | | | | 6.00 | | | | 6,983 | | | | 5.67 | | | | 7,034 | | | | 5.75 | |

Other 2014 notable items(2) | | | – | | | | – | | | | – | | | | – | | | | (400 | ) | | | (0.32 | ) |

Net income attributable to common shareholders (diluted) adjusting for restructuring charge and other notable items | | | 7,348 | | | | 6.00 | | | | 6,983 | | | | 5.67 | | | | 6,634 | | | | 5.43 | |

Amortization of intangible assets, excluding software | | | 76 | | | | 0.05 | | | | 65 | | | | 0.05 | | | | 62 | | | | 0.06 | |

Adjusted net income attributable to common shareholders (diluted) | | $ | 7,424 | | | $ | 6.05 | | | $ | 7,048 | | | $ | 5.72 | | | $ | 6,696 | | | $ | 5.49 | |

Weighted average number of diluted common shares outstanding (millions) | | | 1,226 | | | | | | | | 1,232 | | | | | | | | 1,222 | | | | | |

| (1) | Adjusted diluted earnings per share calculations are based on full dollar and share amounts. |

| (2) | Refer to T15 Notable items. |

Core banking assets

Core banking assets are average earning assets excluding bankers’ acceptances and average trading assets within Global Banking and Markets.

Core banking margin

This ratio represents net interest income divided by average core banking assets.

2 0 1 6 S C O T I A B A N K A N N U A L R E P O R T | 13

MANAGEMENT’S DISCUSSION AND ANALYSIS

T3 Financial highlights

| | | | | | | | | | | | |

| | | |

| As at and for the years ended October 31 | | 2016 | | | 2015 | | | 2014 | |

Operating results($ millions) | | | | | | | | | | | | |

Net interest income | | | 14,292 | | | | 13,092 | | | | 12,305 | |

Non-interest income | | | 12,058 | | | | 10,957 | | | | 11,299 | |

Total revenue | | | 26,350 | | | | 24,049 | | | | 23,604 | |

Provision for credit losses | | | 2,412 | | | | 1,942 | | | | 1,703 | |

Non-interest expenses | | | 14,540 | | | | 13,041 | | | | 12,601 | |

Income tax expense | | | 2,030 | | | | 1,853 | | | | 2,002 | |

Net income | | | 7,368 | | | | 7,213 | | | | 7,298 | |

Net income attributable to common shareholders | | | 6,987 | | | | 6,897 | | | | 6,916 | |

Operating performance | | | | | | | | | | | | |

Basic earnings per share ($) | | | 5.80 | | | | 5.70 | | | | 5.69 | |

Diluted earnings per share ($) | | | 5.77 | | | | 5.67 | | | | 5.66 | |

Adjusted diluted earnings per share ($)(1)(2) | | | 6.05 | | | | 5.72 | | | | 5.49 | |

Return on equity (%) | | | 13.8 | | | | 14.6 | | | | 16.1 | |

Productivity ratio (%)(3) | | | 55.2 | | | | 54.2 | | | | 53.4 | |

Operating leverage (%)(3) | | | (1.9 | ) | | | (1.6 | ) | | | 2.8 | |

Core banking margin (%)(1)(3) | | | 2.38 | | | | 2.39 | | | | 2.39 | |

Financial position information($ millions) | | | | | | | | | | | | |

Cash and deposits with financial institutions | | | 46,344 | | | | 73,927 | | | | 56,730 | |

Trading assets | | | 108,561 | | | | 99,140 | | | | 113,248 | |

Loans | | | 480,164 | | | | 458,628 | | | | 424,309 | |

Total assets | | | 896,266 | | | | 856,497 | | | | 805,666 | |

Deposits | | | 611,877 | | | | 600,919 | | | | 554,017 | |

Common equity | | | 52,657 | | | | 49,085 | | | | 44,965 | |

Preferred shares | | | 3,594 | | | | 2,934 | | | | 2,934 | |

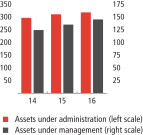

Assets under administration | | | 472,817 | | | | 453,926 | | | | 427,547 | |

Assets under management | | | 192,702 | | | | 179,007 | | | | 164,820 | |

Capital and liquidity measures | | | | | | | | | | | | |

Common Equity Tier 1 (CET1) capital ratio (%) | | | 11.0 | | | | 10.3 | | | | 10.8 | |

Tier 1 capital ratio (%) | | | 12.4 | | | | 11.5 | | | | 12.2 | |

Total capital ratio (%) | | | 14.6 | | | | 13.4 | | | | 13.9 | |

Leverage ratio (%) | | | 4.5 | | | | 4.2 | | | | N/A | |

CET1 risk-weighted assets ($ millions)(4) | | | 364,048 | | | | 357,995 | | | | 312,473 | |

Liquidity coverage ratio (LCR) (%) | | | 127 | | | | 124 | | | | N/A | |

Credit quality | | | | | | | | | | | | |

Net impaired loans ($ millions)(5) | | | 2,446 | | | | 2,085 | | | | 2,002 | |

Allowance for credit losses ($ millions) | | | 4,626 | | | | 4,197 | | | | 3,641 | |

Net impaired loans as a % of loans and acceptances(5) | | | 0.49 | | | | 0.44 | | | | 0.46 | |

Provision for credit losses as a % of average net loans and acceptances | | | 0.50 | | | | 0.43 | | | | 0.40 | |

Common share information | | | | | | | | | | | | |

Closing share price ($)(TSX) | | | 72.08 | | | | 61.49 | | | | 69.02 | |

Shares outstanding (millions) | | | | | | | | | | | | |

Average – Basic | | | 1,204 | | | | 1,210 | | | | 1,214 | |

Average – Diluted | | | 1,226 | | | | 1,232 | | | | 1,222 | |

End of period | | | 1,208 | | | | 1,203 | | | | 1,217 | |

Dividends per share ($) | | | 2.88 | | | | 2.72 | | | | 2.56 | |

Dividend yield (%)(6) | | | 4.7 | | | | 4.4 | | | | 3.8 | |

Market capitalization ($ millions)(TSX) | | | 87,065 | | | | 73,969 | | | | 83,969 | |

Book value per common share ($) | | | 43.59 | | | | 40.80 | | | | 36.96 | |

Market value to book value multiple | | | 1.7 | | | | 1.5 | | | | 1.9 | |

Price to earnings multiple (trailing 4 quarters) | | | 12.4 | | | | 10.8 | | | | 12.1 | |

Other information | | | | | | | | | | | | |

Employees | | | 88,901 | | | | 89,214 | | | | 86,932 | |

Branches and offices | | | 3,113 | | | | 3,177 | | | | 3,288 | |

| | | | | | | | | | | | | |

| (1) | Refer to page 13 for a discussion of Non-GAAP measures. |

| (2) | Refer to T2 Adjusted diluted earnings per share. |

| (3) | Effective 2016, the taxable equivalent adjustment is no longer included in the calculation. Prior period amounts have been restated. |

| (4) | As at October 31, 2016, credit valuation adjustment (CVA) risk-weighted assets were calculated using scalars of 0.64, 0.71 and 0.77 to compute CET1, Tier 1 and Total Capital ratios, respectively. |

| (5) | Excludes loans acquired under the Federal Deposit Insurance Corporation (FDIC) guarantee related to the acquisition of R-G Premier Bank of Puerto Rico. |

| (6) | Based on the average of the high and low common share price for the year. |

14 | 2 0 1 6 S C O T I A B A N K A N N U A L R E P O R T

MANAGEMENT’S DISCUSSION AND ANALYSIS | OVERVIEW

Overview

Financial Results

The Bank’s net income for the year was $7,368 million, up 2% from $7,213 million last year and diluted earnings per share (EPS) were $5.77 compared to $5.67 last year. Return on equity was 13.8% in 2016 compared to 14.6% last year.

The Bank recorded a restructuring charge of $378 million pre-tax, or $278 million after tax, in 2016 (refer T1). Adjusting for the restructuring charge, net income was $7,646 million, up 6% and diluted earnings per share rose 6% to $6.00 compared to last year. Return on equity was 14.3% compared to 14.6% last year.

Current year net income was positively impacted by increases in net interest income and non-interest income, as well as acquisitions and the favourable impact of foreign currency translation. Partially offsetting were higher provision for credit losses, non-interest expenses and income taxes.

Net interest income increased $1,200 million or 9% to $14,292 million, driven by growth in core banking assets across all business lines and acquisitions. The core banking margin was 2.38%, down one basis point from last year.

Non-interest income increased $1,101 million or 10% to $12,058 million from the prior year. Strong growth in banking and trading revenues, acquisitions and the favourable impact of foreign currency translation contributed to the increase. Also contributing to the increase was a gain on sale of a non-core lease financing business in Canada, while gains on sale of real estate this year were largely offset by lower net gains on investment securities.

The total provision for credit losses was $2,412 million, up $470 million from last year. Contributing to this increase were higher provisions related to energy exposures in Global Banking and Markets, higher commercial provisions in International Banking, and higher retail provisions in Canadian Banking, primarily in credit cards and automotive loans, generally in line with volume growth. Partially offsetting were higher acquisition-related benefits this year.

Non-interest expenses were $14,540 million this year, an increase of $1,499 million or 11% over last year. Adjusting for the restructuring charge (refer T1), expenses increased 9%. The increase reflects the impact of acquisitions, higher performance-based compensation, as well as higher business initiative and volume-driven costs including technology and professional fees, software amortization, and deposit insurance. As well, last year benefited from lower pension benefit costs of $204 million related to modifications made to the Bank’s main pension plan partly offset by the costs relating to the reorganization of Canadian shared services of $61 million. Operating leverage was negative 1.9% on a reported basis, or positive 1.0% adjusting for the restructuring charge (refer T1).

The provision for income taxes was $2,030 million, an increase of $177 million from last year. The Bank’s overall effective tax rate for the year was 21.6% compared to 20.4% in 2015. The increase in the effective tax rate was due primarily to lower tax-exempt income and higher taxes in foreign jurisdictions this year.

The all-in Basel III Common Equity Tier 1 ratio was 11.0% as at October 31, 2016, compared to 10.3% last year, and remained well above the regulatory minimum.

Economic Outlook

The United States will be the reference point for economic developments in the year ahead owing to the potentially large shifts brought about by the results of the November 2016 elections. After an initial period of uncertainty as the priorities of the new American administration are clarified, we expect U.S. economic activity to continue picking up as additional fiscal stimulus, delivered through tax cuts and infrastructure spending, accelerates the recovery in U.S. domestic demand that has already been buoyed by reasonably strong gains in employment, consumer spending, and residential construction.

Canadian output growth is rebounding owing to the rebuilding of Fort McMurray after the devastating wildfires in early May, a resumption of crude oil shipments from Alberta post-fire, and a modest pick-up in non-energy exports. Although uncertainty about the new U.S. government’s approach to trade policy may temporarily dampen investment growth in early 2017, capital spending should pick up again as Canada’s federal stimulus package and U.S. demand growth both take hold later in the year. Consumer demand should be reasonably well supported in the year ahead by recent employment gains and the anticipated impact of the Canada Child Benefit. A number of downside risks to Canada’s economy remain, including stretched valuations in the Vancouver and Toronto housing markets and high household indebtedness, but these appear well-managed.

The outlook for the Pacific Alliance countries remains closely tied to the U.S. economy. Some country-specific risks will remain salient in the year ahead, but the medium-term outlook for the region remains strong. We are positive about Mexico’s underlying strengths, and we also anticipate further economic rebound in Brazil.

Across the Atlantic, most economic indicators in the U.K. point to much stronger than expected growth in the aftermath of the ‘Brexit’ vote as currency movements provide a cushion for real activity. Despite this unanticipated resilience, we continue to expect the U.K. economy to slow as the British government moves towards negotiations on withdrawal from the E.U. The knock-on effects in Europe, alongside financial sector challenges and local political uncertainty, are likely to provide a drag on growth across the Continent. Japan’s recovery will probably remain muted as the authorities strive to make new monetary and fiscal measures effective. The pace of growth throughout the rest of the Pacific Rim will be favourable, with indicators pointing to a pick-up in China’s industrial activity.

2 0 1 6 S C O T I A B A N K A N N U A L R E P O R T | 15

MANAGEMENT’S DISCUSSION AND ANALYSIS

Shareholder Returns

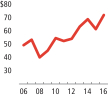

In fiscal 2016, the total shareholder return on the Bank’s shares was 22.5%, which outperformed the 12.6% total return of the S&P/TSX Composite Index.

The total compound annual shareholder return on the Bank’s shares over the past five years was 11.1%, and 8.2% over the past 10 years. This exceeded the total return of the S&P/TSX Composite Index, which was 7.0% over the past five years and 4.8% over the last ten years, as shown in chart C2.

Quarterly dividends were raised twice during the year – a two cent increase effective the second quarter and a further two cent increase effective in the fourth quarter. As a result, dividends per share totaled $2.88 for the year, up 6% from 2015. The Bank was within its target payout range of40-50%, with a payout ratio of 49.6% for the year.

T4 Shareholder returns

| | | | | | | | | | | | |

| | | |

| For the years ended October 31 | | 2016 | | | 2015 | | | 2014 | |

Closing market price per common share ($) | | | 72.08 | | | | 61.49 | | | | 69.02 | |

Dividends paid ($ per share) | | | 2.88 | | | | 2.72 | | | | 2.56 | |

Dividend yield (%)(1) | | | 4.7 | | | | 4.4 | | | | 3.8 | |

Increase (decrease) in share price (%) | | | 17.2 | | | | (10.9 | ) | | | 8.9 | |

Total annual shareholder return (%)(2) | | | 22.5 | | | | (7.0 | ) | | | 13.2 | |

| (1) | Dividend yield is calculated as the dividend paid divided by the average of the high and low common share price for the year. |

| (2) | Total annual shareholder return assumes reinvestment of quarterly dividends, and therefore may not equal the sum of dividend and share price returns in the table. |

16 | 2 0 1 6 S C O T I A B A N K A N N U A L R E P O R T

| C1 | Closing common share price |

as at October 31

| C2 | Return to common shareholders |

Share price appreciation plus dividends reinvested, 2006=100

MANAGEMENT’S DISCUSSION AND ANALYSIS | OVERVIEW

Impact of Foreign Currency Translation

The impact of foreign currency translation on net income is shown in T5.

T5 Impact of foreign currency translation

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | |

| | | 2016 | | | 2015 | | | 2014 | |

| For the fiscal years | | Average

exchange rate | | | % Change | | | Average

exchange rate | | | % Change | | | Average

exchange rate | | | % Change | |

U.S. dollar/Canadian dollar | | | 0.754 | | | | (6.4 | )% | | | 0.806 | | | | (12.2 | )% | | | 0.918 | | | | (6.5 | )% |

Mexican Peso/Canadian dollar | | | 13.666 | | | | 10.3 | % | | | 12.386 | | | | 2.8 | % | | | 12.049 | | | | (3.7 | )% |

Peruvian Sol/Canadian dollar | | | 2.539 | | | | 1.3 | % | | | 2.505 | | | | (3.0 | )% | | | 2.582 | | | | (1.3 | )% |

Colombian Peso/Canadian dollar | | | 2,307 | | | | 10.8 | % | | | 2,082 | | | | 16.4 | % | | | 1,789 | | | | (1.4 | )% |

Chilean Peso/Canadian dollar | | | 514.549 | | | | 0.5 | % | | | 512.203 | | | | 0.2 | % | | | 511.261 | | | | 6.8 | % |

| | | | | | | | | | | | |

| | | |

| Impact on net income(1) ($ millions except EPS) | | 2016 vs. 2015 | | | 2015 vs. 2014 | | | 2014 vs. 2013 | |

Net interest income | | $ | (51 | ) | | $ | 232 | | | $ | 191 | |

Non-interest income(2) | | | 182 | | | | 243 | | | | 195 | |

Non-interest expenses | | | 86 | | | | (151 | ) | | | (134 | ) |

Other items (net of tax) | | | (34 | ) | | | (62 | ) | | | (70 | ) |

Net income | | $ | 183 | | | $ | 262 | | | $ | 182 | |

Earnings per share (diluted) | | $ | 0.15 | | | $ | 0.21 | | | $ | 0.15 | |

Impact by business line ($ millions) | | | | | | | | | | | | |

Canadian Banking | | $ | 14 | | | $ | 20 | | | $ | 8 | |

International Banking(2) | | | 44 | | | | 84 | | | | 80 | |

Global Banking and Markets | | | 65 | | | | 110 | | | | 85 | |

Other(2) | | | 60 | | | | 48 | | | | 9 | |

| | | $ | 183 | | | $ | 262 | | | $ | 182 | |

| (1) | Includes impact of all currencies |

| (2) | Includes the impact of foreign currency hedges. |

2 0 1 6 S C O T I A B A N K A N N U A L R E P O R T | 17

MANAGEMENT’S DISCUSSION AND ANALYSIS

GROUP FINANCIAL PERFORMANCE

Net Income

Net income was $7,368, up 2% compared to $7,213 last year. Included in this year’s results is a restructuring charge of $378 million pre-tax, or $278 million after tax (refer T1). Adjusting for the restructuring charge, net income increased $433 million or 6%.

Net Interest Income

Net interest income was $14,292 million, an increase of $1,200 million or 9% from the prior year. This increase was driven by a 9% growth in core earning assets, including acquisitions, as the core banking margin was in line with last year.

Canadian Banking’s net interest income was up $608 million or 9% driven by strong asset and deposit growth, expansion in margin, and the impact of an acquisition. Net interest income increased $652 million or 11% in International Banking primarily due to strong asset growth and the impact of acquisitions. Global Banking and Markets net interest income increased $222 million or 21% driven by an increase in both average earning assets and margin. Partially offsetting these increases were lower contribution from asset/liability management activities reflected in the Other segment.

Core banking assets increased $50 billion to $598 billion. The increase was driven by strong growth in both retail and commercial loans in International Banking, corporate loans in Global Banking and Markets, automotive and credit card loans in Canadian Banking and higher volume of assets held for liquidity purposes in the Other segment. Also contributing to the asset increase was the positive impact of foreign currency translation.

The core banking margin of 2.38% was in line with the previous year. The margin increase in Canadian Banking was offset by lower contribution from asset/liability management activities reflected in the Other segment.

Outlook

Net interest income is expected to increase in 2017 mainly due to growth in core banking assets across all business lines. The total margin is expected to be in line with 2016, as improvements from business mix, both on the asset and deposit side, are generally offset by continued deposit margin compression in an expected low interest rate environment.

T6 Net interest income and core banking margin(1)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | |

| | | 2016 | | | 2015 | | | 2014 | |

($ billions, except percentage amounts) | | Average balance | | | Interest | | | Average rate | | | Average balance | | | Interest | | | Average rate | | | Average balance | | | Interest | | | Average rate | |

Total average assets and net interest income | | $ | 913.8 | | | $ | 14.3 | | | | | | | $ | 860.6 | | | $ | 13.1 | | | | | | | $ | 795.6 | | | $ | 12.3 | | | | | |

Less: total assets in Capital Markets(1) | | | 259.4 | | | | – | | | | | | | | 258.1 | | | | – | | | | | | | | 232.5 | | | | – | | | | | |

Banking margin on average total assets | | $ | 654.4 | | | $ | 14.3 | | | | 2.18 | % | | $ | 602.5 | | | $ | 13.1 | | | | 2.18 | % | | $ | 563.1 | | | $ | 12.3 | | | | 2.19 | % |

Less: non-earning assets and customers’ liability under acceptances | | | 56.6 | | | | | | | | | | | | 54.4 | | | | | | | | | | | | 48.0 | | | | | | | | | |

Core banking assets and margin | | $ | 597.8 | | | $ | 14.3 | | | | 2.38 | % | | $ | 548.1 | | | $ | 13.1 | | | | 2.39 | % | | $ | 515.1 | | | $ | 12.3 | | | | 2.39 | % |

| (1) | Net interest income from Capital Markets trading assets is recorded in trading revenues in non-interest income. |

18 | 2 0 1 6 S C O T I A B A N K A N N U A L R E P O R T

MANAGEMENT’S DISCUSSION AND ANALYSIS | GROUP FINANCIAL PERFORMANCE

T7 Average balance sheet(1) and net interest income

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | |

| | | 2016 | | | 2015 | | | 2014 | |

| | | | | | | | | |

| For the fiscal years ($ billions) | | Average

balance | | | Interest | | | Average

rate | | | Average

balance | | | Interest | | | Average

rate | | | Average

balance | | | Interest | | | Average

rate | |

Assets | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

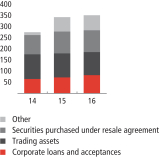

Deposits with financial institutions | | $ | 67.8 | | | $ | 0.4 | | | | 0.58 | % | | $ | 71.1 | | | $ | 0.3 | | | | 0.41 | % | | $ | 60.1 | | | $ | 0.3 | | | | 0.44 | % |

Trading assets | | | 107.2 | | | | 0.2 | | | | 0.16 | % | | | 111.2 | | | | 0.2 | | | | 0.17 | % | | | 113.3 | | | | 0.1 | | | | 0.12 | % |

Securities purchased under resale agreements and securities borrowed | | | 99.8 | | | | 0.1 | | | | 0.16 | % | | | 99.9 | | | | 0.2 | | | | 0.16 | % | | | 91.1 | | | | 0.2 | | | | 0.20 | % |

Investment securities | | | 67.8 | | | | 1.1 | | | | 1.57 | % | | | 43.7 | | | | 0.7 | | | | 1.69 | % | | | 41.2 | | | | 0.8 | | | | 1.91 | % |

Loans: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Residential mortgages | | | 218.6 | | | | 7.4 | | | | 3.37 | % | | | 214.4 | | | | 7.5 | | | | 3.51 | % | | | 210.9 | | | | 7.6 | | | | 3.60 | % |

Personal and credit cards | | | 96.8 | | | | 7.3 | | | | 7.57 | % | | | 87.5 | | | | 6.6 | | | | 7.52 | % | | | 79.6 | | | | 6.1 | | | | 7.61 | % |

Business and government | | | 161.4 | | | | 5.5 | | | | 3.41 | % | | | 142.2 | | | | 4.6 | | | | 3.25 | % | | | 128.5 | | | | 4.3 | | | | 3.39 | % |

Allowance for credit losses | | | (4.6 | ) | | | | | | | | | | | (4.0 | ) | | | | | | | | | | | (3.6 | ) | | | | | | | | |

Total loans | | $ | 472.2 | | | $ | 20.2 | | | | 4.28 | % | | $ | 440.1 | | | $ | 18.7 | | | | 4.26 | % | | $ | 415.4 | | | $ | 18.0 | | | | 4.34 | % |

Total earning assets | | $ | 814.8 | | | $ | 22.0 | | | | 2.70 | % | | $ | 766.0 | | | $ | 20.1 | | | | 2.63 | % | | $ | 721.1 | | | $ | 19.4 | | | | 2.69 | % |

Customers’ liability under acceptances | | | 11.4 | | | | | | | | | | | | 11.4 | | | | | | | | | | | | 10.4 | | | | | | | | | |

Other assets | | | 87.6 | | | | | | | | | | | | 83.2 | | | | | | | | | | | | 64.1 | | | | | | | | | |

Total assets | | $ | 913.8 | | | $ | 22.0 | | | | 2.41 | % | | $ | 860.6 | | | $ | 20.1 | | | | 2.34 | % | | $ | 795.6 | | | $ | 19.4 | | | | 2.43 | % |

Liabilities and equity | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Deposits: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Personal | | $ | 195.1 | | | $ | 2.4 | | | | 1.22 | % | | $ | 181.4 | | | $ | 2.3 | | | | 1.27 | % | | $ | 172.6 | | | $ | 2.4 | | | | 1.42 | % |

Business and government | | | 384.7 | | | | 3.9 | | | | 1.01 | % | | | 368.1 | | | | 3.4 | | | | 0.91 | % | | | 339.7 | | | | 3.5 | | | | 1.02 | % |

Financial institutions | | | 42.8 | | | | 0.4 | | | | 1.03 | % | | | 37.3 | | | | 0.3 | | | | 0.85 | % | | | 38.4 | | | | 0.3 | | | | 0.77 | % |

Total deposits | | $ | 622.6 | | | $ | 6.7 | | | | 1.08 | % | | $ | 586.8 | | | $ | 6.0 | | | | 1.02 | % | | $ | 550.7 | | | $ | 6.2 | | | | 1.13 | % |

Obligations related to securities sold under repurchase agreements and securities lent | | | 99.1 | | | | 0.2 | | | | 0.19 | % | | | 90.7 | | | | 0.2 | | | | 0.26 | % | | | 87.3 | | | | 0.3 | | | | 0.32 | % |

Subordinated debentures | | | 7.5 | | | | 0.2 | | | | 3.10 | % | | | 5.6 | | | | 0.2 | | | | 3.33 | % | | | 5.3 | | | | 0.2 | | | | 3.84 | % |

Other interest-bearing liabilities | | | 54.9 | | | | 0.6 | | | | 1.04 | % | | | 50.1 | | | | 0.6 | | | | 1.20 | % | | | 50.2 | | | | 0.4 | | | | 0.72 | % |

Total interest-bearing liabilities | | $ | 784.1 | | | $ | 7.7 | | | | 0.98 | % | | $ | 733.2 | | | $ | 7.0 | | | | 0.96 | % | | $ | 693.5 | | | $ | 7.1 | | | | 1.02 | % |

Other liabilities including acceptances | | | 74.4 | | | | | | | | | | | | 75.9 | | | | | | | | | | | | 54.4 | | | | | | | | | |

Equity(2) | | | 55.3 | | | | | | | | | | | | 51.5 | | | | | | | | | | | | 47.7 | | | | | | | | | |

Total liabilities and equity | | $ | 913.8 | | | $ | 7.7 | | | | 0.84 | % | | $ | 860.6 | | | $ | 7.0 | | | | 0.81 | % | | $ | 795.6 | | | $ | 7.1 | | | | 0.89 | % |

Net interest income | | | | | | $ | 14.3 | | | | | | | | | | | $ | 13.1 | | | | | | | | | | | $ | 12.3 | | | | | |

| (1) | Average of daily balances. |

| (2) | Includes non-controlling interests of $1.5 in 2016, $1.3 in 2015 and $1.2 in 2014. |

2 0 1 6 S C O T I A B A N K A N N U A L R E P O R T | 19

MANAGEMENT’S DISCUSSION AND ANALYSIS

T8 Non-interest income

| | | | | | | | | | | | | | | | |

| | | | |

For the fiscal years ($ millions) | | 2016 | | | 2015 | | | 2014 | | | 2016 versus 2015 | |

Banking | | | | | | | | | | | | | | | | |

Card revenues | | $ | 1,359 | | | $ | 1,089 | | | $ | 933 | | | | 25 | % |

Deposit and payment services | | | | | | | | | | | | | | | | |

Deposit services | | | 949 | | | | 928 | | | | 901 | | | | 2 | |

Other payment services | | | 330 | | | | 307 | | | | 282 | | | | 7 | |

| | $ | 1,279 | | | $ | 1,235 | | | $ | 1,183 | | | | 4 | % |

Credit fees | | | | | | | | | | | | | | | | |

Commitment and other credit fees | | | 870 | | | | 787 | | | | 778 | | | | 11 | |

Acceptance fees | | | 284 | | | | 266 | | | | 236 | | | | 7 | |

| | $ | 1,154 | | | $ | 1,053 | | | $ | 1,014 | | | | 10 | % |

Other | | | 436 | | | | 406 | | | | 379 | | | | 7 | |

Banking fee related expenses | | | 559 | | | | 423 | | | | 339 | | | | 32 | |

Total banking revenues | | $ | 3,669 | | | $ | 3,360 | | | $ | 3,170 | | | | 9 | % |

Wealth management | | | | | | | | | | | | | | | | |

Mutual funds | | $ | 1,624 | | | $ | 1,619 | | | $ | 1,468 | | | | – | % |

Brokerage fees | | | 1,010 | | | | 1,006 | | | | 942 | | | | – | |

Investment management and trust | | | | | | | | | | | | | | | | |

Investment management and custody | | | 443 | | | | 440 | | | | 419 | | | | 1 | |

Personal and corporate trust | | | 205 | | | | 204 | | | | 194 | | | | – | |

| | | 648 | | | | 644 | | | | 613 | | | | 1 | |

Total wealth management revenues | | $ | 3,282 | | | $ | 3,269 | | | $ | 3,023 | | | | – | % |

Underwriting and other advisory | | $ | 594 | | | $ | 525 | | | $ | 712 | | | | 13 | % |

Non-trading foreign exchange | | | 540 | | | | 492 | | | | 420 | | | | 10 | |

Trading revenues | | | 1,403 | | | | 1,185 | | | | 1,114 | | | | 18 | |

Net gain on investment securities | | | 534 | | | | 639 | | | | 741 | | | | (16 | ) |

Net income from investments in associated corporations | | | 414 | | | | 405 | | | | 428 | | | | 2 | |

Insurance underwriting income, net of claims | | | 603 | | | | 556 | | | | 474 | | | | 8 | |

Other | | | 1,019 | | | | 526 | | | | 1,217 | | | | 94 | |

Total non-interest income | | $ | 12,058 | | | $ | 10,957 | | | $ | 11,299 | | | | 10 | % |

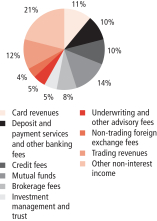

| C3 | Sources of non-interest income |

Non-Interest Income

Non-interest income was $12,058 million, up $1,101 million or 10%, primarily from growth in banking and trading revenues and higher underwriting and advisory fees. The positive impact of acquisitions, foreign currency translation and hedging activities, and gain from the sale of a non-core lease finance business also contributed to the increase. Gains on sales of real estate were generally offset by lower net gains on investment securities.

Banking revenues, excluding related expenses, grew $445 million or 12% to $4,228 million reflecting strong growth in card revenues of 25% due to higher fee income and the impact from acquisitions in Canadian Banking and International Banking. Credit fees were up $101 million or 10% mainly from growth in Global Banking and Markets, as well as contributions from Canadian Banking and International Banking. Banking fee related expenses rose $136 million or 32%, primarily due to card expenses in Canadian Banking and International Banking, reflecting higher transaction volumes as well as acquisitions.

Underwriting and other advisory fees were up $69 million or 13%, mainly due to higher new issue activity and investment advisory fees in Global Banking and Markets.

Non-trading foreign exchange revenues rose $48 million or 10% to $540 million, primarily in Latin America and the Caribbean.

Trading revenues of $1,403 million were higher by $218 million or 18% (refer to T9) from the prior year mainly related to fixed income. Higher commodities and foreign exchange trading revenues were offset by lower equity trading revenues.

Insurance underwriting income was up $47 million or 8%, mostly from strong premium growth in Canada and the Caribbean.

Other income increased significantly by $493 million to $1,019 million primarily due to the gain on sale of a non-core lease financing business, the impact of acquisitions, and gains on sale of real estate.

Outlook

Non-interest income is expected to reflect continued growth in 2017 benefiting from higher card revenues, mutual fund management fees and brokerage revenues. Gains on investment securities, primarily recorded in the Other segment, are expected to be lower than 2016.

20 | 2 0 1 6 S C O T I A B A N K A N N U A L R E P O R T

MANAGEMENT’S DISCUSSION AND ANALYSIS | GROUP FINANCIAL PERFORMANCE

T9 Trading revenues

| | | | | | | | | | | | |

| | | |

| For the fiscal years ($ millions) | | 2016 | | | 2015 | | | 2014 | |

By trading products: | | | | | | | | | | | | |

Interest rate and credit | | $ | 613 | | | $ | 400 | | | $ | 415 | |

Equities | | | 101 | | | | 177 | | | | 92 | |

Commodities | | | 376 | | | | 345 | | | | 359 | |

Foreign exchange | | | 262 | | | | 201 | | | | 208 | |

Other | | | 51 | | | | 62 | | | | 40 | |

Total trading revenues | | | 1,403 | | | | 1,185 | | | | 1,114 | |

% of total revenues | | | 5.3 | % | | | 4.9 | % | | | 4.7 | % |

Provision for Credit Losses

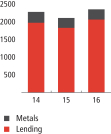

The total provision for credit losses was $2,412 million, up $470 million from last year net of acquisition-related benefits of $152 million. The provision for credit losses ratio was 50 basis points compared to 43 basis points in the prior year.

In Canadian Banking, the provision for credit losses was $832 million, an increase of $145 million. The provision for credit losses was higher due to growth in retail portfolios, primarily in credit cards and auto loans, with additional increases from commercial provisions. The provision for credit losses ratio was 28 basis points, up five basis points from the prior year.

The provision for credit losses in International Banking increased $153 million to $1,281 million. Retail provisions were flat compared to 2015. Increases from acquisitions and higher provisions for credit losses in Latin America from strong retail loan growth were offset by favourable foreign currency translation. In the commercial portfolio, provisions were higher in Colombia, primarily the energy sector, and in Puerto Rico. Overall, the provision for credit losses ratio was 126 basis points, up two basis points from last year.

The provision for credit losses in Global Banking and Markets was $249 million, an increase of $182 million from last year due to higher provisions in the United States and Europe, primarily in the energy sector, and also in Asia. The provision for credit losses ratio was up 20 basis points to 30 basis points.

Outlook

The quality of the Bank’s credit portfolio is expected to remain strong given its broad global diversification. The total provision for credit losses ratio is expected to reduce in 2017. In Canadian Banking, the retail provision for credit losses ratio is expected to increase from changes in the business mix while the commercial ratio is expected to normalize in relation to historical experience. In International Banking, the retail provision for credit losses ratio is expected to be in line with last year after accounting for the integration of prior acquisitions while the commercial ratio should improve. In Global Banking and Markets, the provision for credit losses ratio is expected to decline driven by lower energy related issues. Overall, provision levels in 2017 will be within the Bank’s risk appetite and aligned with strategy.

T10 Provisions against impaired loans by business line

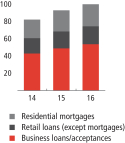

| | | | | | | | | | | | |

| | | |

| For the fiscal years ($ millions) | | 2016 | | | 2015 | | | 2014 | |

Canadian Banking | | | | | | | | | | | | |

Retail | | $ | 770 | | | $ | 642 | | | $ | 607 | |

Commercial | | | 62 | | | | 45 | | | | 56 | |

| | $ | 832 | | | $ | 687 | | | $ | 663 | |

International Banking | | | | | | | | | | | | |

Caribbean and Central America | | $ | 250 | | | $ | 184 | | | $ | 248 | |

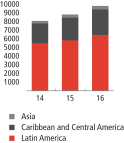

Latin America | | | | | | | | | | | | |

Mexico | | | 224 | | | | 260 | | | | 240 | |

Peru | | | 317 | | | | 265 | | | | 267 | |

Chile | | | 112 | | | | 108 | | | | 74 | |

Colombia | | | 320 | | | | 247 | | | | 146 | |

Other Latin America | | | 58 | | | | 64 | | | | 49 | |

Total Latin America | | | 1,031 | | | | 944 | | | | 776 | |

| | $ | 1,281 | | | $ | 1,128 | | | $ | 1,024 | |

Global Banking and Markets | | | | | | | | | | | | |

Canada | | $ | 43 | | | $ | 42 | | | $ | 3 | |

U.S. | | | 113 | | | | 4 | | | | 2 | |

Asia and Europe | | | 93 | | | | 21 | | | | 11 | |

| | $ | 249 | | | $ | 67 | | | $ | 16 | |

Total | | $ | 2,362 | | | $ | 1,882 | | | $ | 1,703 | |

2 0 1 6 S C O T I A B A N K A N N U A L R E P O R T | 21

MANAGEMENT’S DISCUSSION AND ANALYSIS

T11 Provision for credit losses as a percentage of average net loans and acceptances

| | | | | | | | | | | | |

| | | |

| For the fiscal years (%) | | 2016 | | | 2015 | | | 2014 | |

Canadian Banking | | | | | | | | | | | | |

Retail | | | 0.29 | % | | | 0.25 | % | | | 0.24 | % |

Commercial | | | 0.15 | | | | 0.12 | | | | 0.17 | |

| | | 0.28 | | | | 0.23 | | | | 0.23 | |

International Banking | | | | | | | | | | | | |

Retail | | | 2.08 | | | | 2.33 | | | | 2.13 | |

Commercial | | | 0.52 | | | | 0.26 | | | | 0.51 | |

| | | 1.26 | | | | 1.24 | | | | 1.27 | |

Global Banking and Markets | | | 0.30 | | | | 0.10 | | | | 0.03 | |

Provisions against impaired loans | | | 0.49 | | | | 0.42 | | | | 0.40 | |

Provisions against performing loans | | | 0.01 | | | | 0.01 | | | | 0.00 | |

Total | | | 0.50 | % | | | 0.43 | % | | | 0.40 | % |

T12 Net charge-offs(1) as a percentage of average loans and acceptances

| | | | | | | | | | | | |

| | | |

| For the fiscal years (%) | | 2016 | | | 2015 | | | 2014 | |

Canadian Banking | | | | | | | | | | | | |

Retail | | | 0.26 | % | | | 0.26 | % | | | 0.21 | % |

Commercial | | | 0.16 | | | | 0.20 | | | | 0.24 | |

| | | 0.24 | | | | 0.25 | | | | 0.21 | |

International Banking | | | | | | | | | | | | |

Retail | | | 1.90 | | | | 1.99 | | | | 1.66 | |

Commercial | | | 0.31 | | | | 0.30 | | | | 0.14 | |

| | | 1.06 | | | | 1.10 | | | | 0.70 | |

Global Banking and Markets | | | 0.21 | | | | 0.01 | | | | 0.11 | |

Total | | | 0.41 | % | | | 0.39 | % | | | 0.33 | % |

| (1) | Write-offs net of recoveries. |

22 | 2 0 1 6 S C O T I A B A N K A N N U A L R E P O R T

MANAGEMENT’S DISCUSSION AND ANALYSIS | GROUP FINANCIAL PERFORMANCE

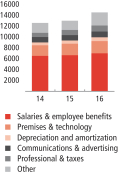

T13 Non-interest expenses and productivity

| | | | | | | | | | | | | | | | |

| | | | |

For the fiscal years ($ millions) | | 2016 | | | 2015 | | | 2014 | | | 2016 versus 2015 | |

Salaries and employee benefits | | | | | | | | | | | | | | | | |

Salaries | | $ | 4,071 | | | $ | 4,019 | | | $ | 3,680 | | | | 1 | % |

Performance-based compensation | | | 1,538 | | | | 1,438 | | | | 1,473 | | | | 7 | |

Share-based payments | | | 243 | | | | 220 | | | | 270 | | | | 10 | |

Other employee benefits | | | 1,173 | | | | 1,004 | | | | 1,124 | | | | 17 | |

| | $ | 7,025 | | | $ | 6,681 | | | $ | 6,547 | | | | 5 | % |

Premises and technology | | | | | | | | | | | | | | | | |

Premises | | | | | | | | | | | | | | | | |

Net rent | | | 428 | | | | 433 | | | | 392 | | | | (1 | ) |

Property taxes | | | 89 | | | | 89 | | | | 82 | | | | – | |

Other premises costs | | | 431 | | | | 421 | | | | 415 | | | | 2 | |

| | $ | 948 | | | $ | 943 | | | $ | 889 | | | | 1 | % |

| | | | | | | | | | | | | | | | |

Technology | | $ | 1,290 | | | $ | 1,143 | | | $ | 1,047 | | | | 13 | % |

| | $ | 2,238 | | | $ | 2,086 | | | $ | 1,936 | | | | 7 | % |

| | | | |

Depreciation and amortization | | | | | | | | | | | | | | | | |

Depreciation | | | 325 | | | | 303 | | | | 297 | | | | 7 | |

Amortization of intangible assets | | | 359 | | | | 281 | | | | 229 | | | | 28 | |

| | $ | 684 | | | $ | 584 | | | $ | 526 | | | | 17 | % |

| | | | | | | | | | | | | | | | |

Communications | | $ | 442 | | | $ | 434 | | | $ | 417 | | | | 2 | % |

| | | | | | | | | | | | | | | | |

Advertising and business development | | $ | 617 | | | $ | 592 | | | $ | 571 | | | | 4 | % |

| | | | | | | | | | | | | | | | |

Professional | | $ | 693 | | | $ | 548 | | | $ | 471 | | | | 27 | % |

| | | | | | | | | | | | | | | | |

Business and capital taxes | | | | | | | | | | | | | | | | |

Business taxes | | | 356 | | | | 319 | | | | 276 | | | | 12 | |

Capital taxes | | | 47 | | | | 42 | | | | 38 | | | | 12 | |

| | $ | 403 | | | $ | 361 | | | $ | 314 | | | | 12 | % |

| | | | | | | | | | | | | | | | |

Other | | $ | 2,438 | | | $ | 1,755 | | | $ | 1,819 | | | | 39 | % |

| | | | | | | | | | | | | | | | |

Total non-interest expenses | | $ | 14,540 | | | $ | 13,041 | | | $ | 12,601 | | | | 11 | % |

Productivity ratio | | | 55.2 | % | | | 54.2 | % | | | 53.4 | % | | | | |

$ millions

| C5 | Direct and indirect taxes |

$ millions

2 0 1 6 S C O T I A B A N K A N N U A L R E P O R T | 23

MANAGEMENT’S DISCUSSION AND ANALYSIS

Non-Interest Expenses

Non-interest expenses were $14,540 million, an increase of $1,499 million or 11% from the prior year.

The Bank took a restructuring charge this year of $378 million (refer T1). The restructuring will enable the Bank to enhance its customer experience, drive a digital transformation and improve its productivity. The restructuring charge, recorded in the Other segment, arises from a structural cost reduction program that relates primarily to changes in Canadian Banking and organization-wide structural changes. These strategic efforts will better position the Bank for long-term growth.

Adjusting for the restructuring charge, the increase was $1,121 million or 9%. The increase was driven by acquisitions, higher performance-based compensation, as well as initiative and volume-driven growth in technology, software amortization, professional fees, and deposit insurance. There were also higher employee pension and benefit expenses as last year benefited from lower pension benefit costs related to modifications made to the Bank’s main pension plan. These were partly offset by net savings of $55 million realized from structural cost reduction initiatives related to this year’s restructuring charge, as well as the reorganization cost incurred in 2015.

The productivity ratio was 55.2%, or 53.7% on an adjusted basis (refer T1), compared to 54.2% in 2015.

Operating leverage was negative 1.9%. Adjusting for the restructuring charge, it was positive 1.0% (refer T1).

Outlook

Non-interest expenses are expected to rise in 2017, after adjusting for the 2016 restructuring charge. This is driven by business growth, ongoing strategic and technology investments as well as higher pension and benefit expenses. The growth will be partly offset by savings from structural cost reduction initiatives.

Income Taxes

The provision for income taxes was $2,030 million, an increase from $1,853 million last year. The Bank’s overall effective tax rate for the year was 21.6% compared to 20.4% for 2015. The increase in the effective tax rate was due primarily to lower tax-exempt income and higher taxes in foreign jurisdictions this year.

Outlook

The Bank’s consolidated effective tax rate is expected to be in the range of 22% to 25% in 2017.

24 | 2 0 1 6 S C O T I A B A N K A N N U A L R E P O R T

MANAGEMENT’S DISCUSSION AND ANALYSIS | GROUP FINANCIAL PERFORMANCE

Financial Results Review: 2015 vs. 2014

In order to identify key business trends between 2015 and 2014, commentary and the related financial results are below.

Net income

The Bank had net income of $7,213 million in 2015, compared to $7,298 million in 2014 and diluted earnings per share (EPS) of $5.67 compared to $5.66 in 2014. Return on equity was 14.6% compared to 16.1% in 2014.

The 2015 net income was positively impacted by an increase in net interest income, the favourable impact of foreign currency translation and lower income taxes. Mostly offsetting these positive impacts were higher provision for credit losses and higher non-interest expenses. The 2015 net income included the following, largely offsetting items, comprised of a reduction in the pension benefit accrual related to modifications made to the Bank’s main pension plan of $204 million pre-tax ($151 million after tax; approximately 3% of the pension liability), an increase to the collective allowance against performing loans of $60 million pre-tax ($44 million after tax) to support the growing loan portfolio, and reorganization costs related to the consolidation of Canadian shared services operations of $61 million pre-tax ($45 million after tax). These items were recorded in the Other segment. The 2014 net income was impacted by several notable items (refer T15) totaling a net benefit of $301 million pre-tax or $290 million after tax, or approximately 23 cents per share.

Net interest income

Net interest income increased $787 million or 6% to $13,092 million in 2015, primarily from growth in core banking assets and the favourable impact of foreign currency translation. The core banking margin was stable at 2.39%.

Non-interest income

Non-interest income was $10,957 million, a decrease of $342 million from $11,299 million. The 2014 non-interest income was positively impacted by notable items of $566 million (refer T15). In 2015, increases in wealth management and banking revenues and the positive impact of foreign currency translation were partly offset by lower underwriting and advisory fees and lower net gains on investment securities.

Provision for credit losses

The total provision for credit losses was $1,942 million in 2015, up $239 million from 2014. This was primarily from increased provisions in the Canadian and International retail portfolios, as well as higher Global Banking and Markets corporate loan provisions in Canada and Europe. These higher provisions were partially offset by lower commercial provisions in Canadian Banking. The 2015 provision also included a $60 million increase in the collective allowance against performing loans. The 2014 provision included a notable item of $62 million related to a change in write-off policy on unsecured bankrupt retail accounts in Canada.

Non-interest expenses

Non-interest expenses were $13,041 million in 2015, an increase of $440 million or 3% over 2014. The increase reflects higher technology, business development and reorganization costs and the negative impact of foreign currency translation. These were partly offset by lower pension benefit costs. The 2014 non-interest expenses included notable items of $203 million (refer T15). Operating leverage was negative 1.5% on a reported basis, or negative 0.7% after adjusting for the 2014 notable items.

Provision for income taxes

The provision for income taxes was $1,853 million, a decrease of $149 million from 2014. The Bank’s overall effective tax rate for 2015 was 20.4% compared to 21.5% in 2014. The decrease in the effective tax rate was due primarily to higher tax-exempt income and lower earnings in higher tax jurisdictions, partially offset by a lower tax rate on the notable gain in the prior year.

T14 Financial Results Review

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

| For the year ended October 31, 2015 ($ millions)(1) | | Canadian

Banking | | | International

Banking | | | Global Banking

and Markets | | | Other(2) | | | Total | |

Net interest income | | $ | 6,415 | | | $ | 5,706 | | | $ | 1,071 | | | $ | (100 | ) | | $ | 13,092 | |

Non-interest income | | | 4,832 | | | | 3,137 | | | | 2,953 | | | | 35 | | | | 10,957 | |

Total revenue | | $ | 11,247 | | | $ | 8,843 | | | $ | 4,024 | | | $ | (65 | ) | | $ | 24,049 | |

Provision for credit losses | | | 687 | | | | 1,128 | | | | 67 | | | | 60 | | | | 1,942 | |

Non-interest expenses | | | 6,014 | | | | 5,095 | | | | 1,846 | | | | 86 | | | | 13,041 | |

Income tax expense | | | 1,202 | | | | 568 | | | | 558 | | | | (475 | ) | | | 1,853 | |

Net income | | $ | 3,344 | | | $ | 2,052 | | | $ | 1,553 | | | $ | 264 | | | $ | 7,213 | |

Net income attributable to non-controlling interests | | | – | | | | 199 | | | | – | | | | – | | | | 199 | |

Net income attributable to equity holders of the Bank | | $ | 3,344 | | | $ | 1,853 | | | $ | 1,553 | | | $ | 264 | | | $ | 7,014 | |

| | (1) | Taxable equivalent basis. Refer to Glossary. |

| | (2) | Includes all other smaller operating segments, including Group Treasury, and corporate adjustments, such as the elimination of the tax-exempt income gross-up reported in net interest income, non-interest income and provision for income taxes for the year ended October 31, 2015 – $390 to arrive at the amounts reported in Consolidated Statement of income, and differences in the actual amount of costs incurred and charged to the operating segments. |

2 0 1 6 S C O T I A B A N K A N N U A L R E P O R T | 25

MANAGEMENT’S DISCUSSION AND ANALYSIS

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

| For the year ended October 31, 2014 ($ millions)(1) | | Canadian

Banking | | | International

Banking | | | Global Banking

and Markets | | | Other(2) | | | Total | |

Net interest income | | $ | 5,996 | | | $ | 5,155 | | | $ | 1,064 | | | $ | 90 | | | $ | 12,305 | |

Non-interest income | | | 5,263 | | | | 2,945 | | | | 3,167 | | | | (76 | ) | | | 11,299 | |

Total revenue | | $ | 11,259 | | | $ | 8,100 | | | $ | 4,231 | | | $ | 14 | | | $ | 23,604 | |

Provision for credit losses | | | 663 | | | | 1,024 | | | | 16 | | | | – | | | | 1,703 | |

Non-interest expenses | | | 5,799 | | | | 4,690 | | | | 1,880 | | | | 232 | | | | 12,601 | |

Income tax expense | | | 1,113 | | | | 544 | | | | 665 | | | | (320 | ) | | | 2,002 | |

Net income | | $ | 3,684 | | | $ | 1,842 | | | $ | 1,670 | | | $ | 102 | | | $ | 7,298 | |

Net income attributable to non-controlling interests | | | 1 | | | | 226 | | | | – | | | | – | | | | 227 | |

Net income attributable to equity holders of the Bank | | $ | 3,683 | | | $ | 1,616 | | | $ | 1,670 | | | $ | 102 | | | $ | 7,071 | |

| | (1) | Taxable equivalent basis. Refer to Glossary. | |

| | (2) | Includes all other smaller operating segments, including Group Treasury and corporate adjustments, such as the elimination of the tax-exempt income gross-up reported in net interest income, non-interest income and provision for income taxes for the year ended October 31, 2014 – $354 million to arrive at the amounts reported in Consolidated Statement of Income, and differences in the actual amount of costs incurred and charged to the operating segments. |

2014 Notable Items

There were several notable items in 2014 totaling a net benefit of $290 million ($301 million pre-tax), or approximately 23 cents per share as outlined in the table below.

T15 2014 Notable items

| | | | | | | | | | | | | | | | |

| | |

| | | | | | 2014 | |

| | | | |

For the year ended October 31 ($ millions, except EPS) | | Notes | | | Pre-tax | | | After-tax | | | EPS

Impact | |

Gain on sale | | | | | | | | | | | | | | | | |

Sale of holdings in CI Financial Corp. | | | 1 | | | $ | 643 | | | $ | 555 | | | $ | 0.45 | |

Provision for credit losses | | | | | | | | | | | | | | | | |

Unsecured bankrupt retail accounts in Canada | | | 2 | | | | (62 | ) | | | (46 | ) | | | (0.04 | ) |

Valuation adjustments | | | | | | | | | | | | | | | | |

Funding valuation adjustment | | | 3 | | | | (30 | ) | | | (22 | ) | | | (0.02 | ) |

Revaluation of monetary assets in Venezuela | | | 4 | | | | (47 | ) | | | (47 | ) | | | (0.04 | ) |

Legal provisions | | | 5 | | | | (55 | ) | | | (40 | ) | | | (0.03 | ) |

Sub-total | | | | | | | 449 | | | | 400 | | | | 0.32 | |

Restructuring charges | | | 6 | | | | (148 | ) | | | (110 | ) | | | (0.09 | ) |

Total | | | | | | $ | 301 | | | $ | 290 | | | $ | 0.23 | |

By Business line | | | | | | | | | | | | | | | | |

Canadian Banking | | | | | | $ | 506 | | | $ | 453 | | | | | |

International Banking | | | | | | | (81 | ) | | | (74 | ) | | | | |

Global Banking and Markets | | | | | | | (38 | ) | | | (27 | ) | | | | |

Other | | | | | | | (86 | ) | | | (62 | ) | | | | |

Total | | | | | | $ | 301 | | | $ | 290 | | | $ | 0.23 | |

By Consolidated Statement of Income line | | | | | | | | | | | | | | | | |

Trading revenues | | | | | | $ | (30 | ) | | $ | (22 | ) | | | | |

Other income | | | | | | | 596 | | | | 508 | | | | | |

Non-interest income | | | | | | | 566 | | | | 486 | | | | | |

Provision for credit losses | | | | | | | (62 | ) | | | (46 | ) | | | | |

Non-interest expenses | | | | | | | (203 | ) | | | (150 | ) | | | | |

Total | | | | | | $ | 301 | | | $ | 290 | | | $ | 0.23 | |

Notes

Q3 2014 items

(1) Sale of majority of Bank’s holding in CI Financial Corp.

The Bank sold a majority of its holding in CI Financial Corp. resulting in a $643 million pre-tax gain ($555 million after tax), or 45 cents per share. This included an unrealized gain of $174 million pre-tax, or $152 million after tax, on the reclassification of the Bank’s remaining investment to available-for-sale securities.

Q4 2014 items

(2) Provision for credit losses

The Bank changed its write-off policy on unsecured bankrupt retail accounts in Canada in order to accelerate write-offs upon notification of a bankruptcy filing. As a result, a charge of $62 million ($46 million after tax) was recorded.

(3) Funding valuation adjustment

The Bank enhanced the fair value methodology and recognized a funding valuation adjustment (FVA) charge of $30 million ($22 million after tax), to reflect the implied funding cost on uncollateralized derivative instruments.

(4) Venezuela

Venezuela was designated as hyper-inflationary and measures of exchange controls have been imposed by the Venezuelan government. These restrictions have limited the Bank’s ability to repatriate cash and dividends out of Venezuela.

The Bank’s Venezuelan Bolivar (VEF) exposures include its investment in Banco del Caribe, and unremitted dividends and other cash amounts (“monetary assets”) in Venezuela. As at October 31, 2014, the Bank remeasured its net investment and monetary assets at the SICAD II rate (1 USD to 50 VEF). As a result, the Bank recorded a charge of $47 million in the Consolidated Statement of Income representing the revaluation impact on the monetary assets and a reduction in carrying value of the net investment of $129 million has been charged to Other Comprehensive Income.

(5) Legal provision

The Bank recorded a legal provision of approximately $55 million ($40 million after tax) related to certain ongoing legal claims.

(6) Restructuring charges

The Bank recorded a restructuring charge of $148 million ($110 million after tax), the majority relating to employee severance charges. These charges will drive greater operational efficiencies. In Canada, the charges relate to recent initiatives to centralize and automate several mid-office branch functions, as well as reductions in required wealth management operational support. In International Banking, the charges are primarily for closing or downsizing approximately 120 branches, which will allow us to focus on high-growth markets, minimize branch overlap, and realize synergies resulting from recent acquisitions. The Bank also made a series of changes to simplify its leadership structure and operating model, recorded in the Other segment.

26 | 2 0 1 6 S C O T I A B A N K A N N U A L R E P O R T

MANAGEMENT’S DISCUSSION AND ANALYSIS | GROUP FINANCIAL PERFORMANCE

Fourth Quarter Review

T16 Fourth Quarter Financial Results

| | | | | | | | | | | | |

| |

| | | For the three months ended | |

| | | |

| ($ millions) | | October 31

2016 | | | July 31 2016 | | | October 31

2015 | |

Net Interest income | | $ | 3,653 | | | $ | 3,602 | | | $ | 3,371 | |

Non-interest income | | | 3,098 | | | | 3,038 | | | | 2,754 | |

Total revenue | | | 6,751 | | | | 6,640 | | | | 6,125 | |

Provision for credit losses | | | 550 | | | | 571 | | | | 551 | |

Non-interest expenses | | | 3,650 | | | | 3,505 | | | | 3,286 | |

Income tax expense | | | 540 | | | | 605 | | | | 445 | |

Net income | | $ | 2,011 | | | $ | 1,959 | | | $ | 1,843 | |

Net income attributable to non-controlling interests in subsidiaries | | $ | 72 | | | $ | 62 | | | $ | 60 | |

Net income attributable to equity holders of the Bank | | $ | 1,939 | | | $ | 1,897 | | | $ | 1,783 | |

Preferred shareholders | | | 31 | | | | 37 | | | | 29 | |

Common shareholders | | $ | 1,908 | | | $ | 1,860 | | | $ | 1,754 | |

Q4 2016 vs. Q4 2015

Net income

Net income was $2,011 million, an increase of $168 million or 9%. Strong asset growth and higher capital markets revenues were partly offset by higher non-interest expenses and income taxes.

Net interest income

Net interest income was $3,653 million, an increase of $282 million or 8%. The increase was attributable primarily to growth in retail and commercial loans in International Banking, credit cards, automotive loans and residential mortgages in Canadian Banking, and corporate loans in Global Banking and Markets.

The core banking margin was 2.40%, up five basis points driven by higher margins across all business lines, partially offset by lower contribution from asset/liability management activities in the Other segment.

Non-interest income

Non-interest income of $3,098 million was up $344 million or 12%. This was driven by higher banking fees, wealth management and trading revenues, underwriting and other advisory fees and net income from investments in associated corporations. Gains on sale of real estate were largely offset by lower net gains on investment securities.

Provision for credit losses

The provision for credit losses was $550 million, down $1 million. Last year’s increase in collective allowance against performing loans of $60 million was mostly offset by higher provisions in Canadian Banking and International Banking.

Non-interest expenses

Non-interest expenses increased by $364 million or 11% to $3,650 million. Last year benefited from lower pension benefit costs, partly offset by the reorganization costs relating to Canadian shared services. The increase was primarily due to higher performance and stock-based compensation, acquisitions and continued investments in the business, including technology and professional expenses. This was partly offset by the favourable impact of foreign currency translation and savings from structural cost reduction initiatives.

The productivity ratio was 54.1%, compared to 53.6%.

Income taxes

The tax rate was 21.2% compared to 19.4%, due primarily to lower tax-exempt income.

2 0 1 6 S C O T I A B A N K A N N U A L R E P O R T | 27

MANAGEMENT’S DISCUSSION AND ANALYSIS

Q4 2016 vs. Q3 2016

Net income

Net income was $2,011 million, an increase of $52 million or 3% over the prior quarter. Higher revenues, lower provision for credit losses and lower income taxes, were partly offset by higher non-interest expenses.

Net interest income

Net interest income was $3,653 million, an increase of $51 million or 1%. The increase was attributable to asset growth primarily in residential mortgages and automotive loans in Canadian Banking, and retail loans in International Banking.

The core-banking margin was 2.40%, up two basis points, mostly from higher margins in Canadian Banking and Global Banking and Markets.

Non-interest income

Non-interest income was $3,098 million, up $60 million or 2%. Higher banking and wealth management revenues and contributions from associated corporations were partly offset by lower underwriting and advisory fees. Gains on sale of real estate were offset by lower net gains on investment securities.

Provision for credit losses

The provision for credit losses was $550 million, a decline from $571 million, due primarily to lower provisions in International Banking.

Non-interest expenses and productivity

Non-interest expenses were up $145 million or 4%. This was mainly due to continued investments in the business, including technology and professional fees, and higher seasonal marketing expenses.

The productivity ratio was 54.1% compared to 52.8%.

Income taxes

The effective tax rate was 21.2% compared to 23.6%, due primarily to higher taxes in certain foreign jurisdictions in the previous quarter.

28 | 2 0 1 6 S C O T I A B A N K A N N U A L R E P O R T

MANAGEMENT’S DISCUSSION AND ANALYSIS | GROUP FINANCIAL PERFORMANCE

Trending Analysis

T17Quarterly financial highlights

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| |

| | | For the three months ended | |

| | | | | | | | |

| ($ millions) | | October 31

2016 | | | July 31

2016 | | | April 30

2016 | | | January 31

2016 | | | October 31

2015 | | | July 31

2015 | | | April 30

2015 | | | January 31

2015 | |

Net interest income | | $ | 3,653 | | | $ | 3,602 | | | $ | 3,518 | | | $ | 3,519 | | | $ | 3,371 | | | $ | 3,354 | | | $ | 3,198 | | | $ | 3,169 | |

Non-interest income | | | 3,098 | | | | 3,038 | | | | 3,076 | | | | 2,846 | | | | 2,754 | | | | 2,770 | | | | 2,739 | | | | 2,694 | |

Total revenue | | $ | 6,751 | | | $ | 6,640 | | | $ | 6,594 | | | $ | 6,365 | | | $ | 6,125 | | | $ | 6,124 | | | $ | 5,937 | | | $ | 5,863 | |

Provision for credit losses | | | 550 | | | | 571 | | | | 752 | | | | 539 | | | | 551 | | | | 480 | | | | 448 | | | | 463 | |

Non-interest expenses | | | 3,650 | | | | 3,505 | | | | 3,817 | | | | 3,568 | | | | 3,286 | | | | 3,334 | | | | 3,224 | | | | 3,197 | |

Income tax expense | | | 540 | | | | 605 | | | | 441 | | | | 444 | | | | 445 | | | | 463 | | | | 468 | | | | 477 | |

Net income | | $ | 2,011 | | | $ | 1,959 | | | $ | 1,584 | | | $ | 1,814 | | | $ | 1,843 | | | $ | 1,847 | | | $ | 1,797 | | | $ | 1,726 | |

Basic earnings per share ($) | | | 1.58 | | | | 1.55 | | | | 1.24 | | | | 1.44 | | | | 1.46 | | | | 1.46 | | | | 1.43 | | | | 1.36 | |

Diluted earnings per share ($) | | | 1.57 | | | | 1.54 | | | | 1.23 | | | | 1.43 | | | | 1.45 | | | | 1.45 | | | | 1.42 | | | | 1.35 | |

Net income

The Bank recorded strong net income over the past eight quarters. The second quarter of 2016 was impacted by a restructuring charge of $378 million pre-tax, or $278 million after tax.

Net interest income

Net interest income rose throughout the year. Core banking assets increased steadily during 2016 from continuing growth in Latin America, and retail loan growth in Canadian Banking, corporate loan growth in Global Banking and Markets, as well as the benefit from the impact of foreign currency translation. The average balance of low-spread deposits with banks has declined since the fourth quarter of last year.

The core banking margin for the year was 2.38%, a one basis point decrease from last year. The margin was stable for the first three quarters, and increased by five basis points in the fourth quarter.

Canadian Banking’s margin improved during the year mainly from growth in higher spread products, including credit cards and consumer automotive. International Banking’s margin increased in each of the first three quarters, but declined slightly in the fourth quarter due to lower spreads in Chile, Peru and the Caribbean. The banking margin in Global Banking and Markets increased each quarter during the year mainly due to higher deposit interest and loan amortization fees, partly offset by lower spreads in the U.S. and Asia corporate loan portfolios. Lower contributions from asset/liability management activities and higher funding costs in the Other segment had a dampening effect on the margin.

Non-interest income

Non-interest revenues grew during the first two quarters, declined in the third and rebounded in the fourth quarter. Banking revenues trended upward during the year with strong growth in card fees in Canadian and International Banking. Mutual fund fees and retail brokerage fees were strong in the first quarter, but dropped back in the second before climbing steadily through the second half of the year. Trading revenues recovered in the last three quarters of the year, from the low levels experienced at the end of last year and the first quarter of the current year. The level of net gains on investment securities reflected market opportunities.

Provision for credit losses

Provision for credit losses peaked in the second quarter, primarily in the energy sector, with declines in the third and fourth quarters. Loan loss ratios in Canadian Banking increased slightly in the first three quarters, and declined by one basis point in the last quarter of the year. Overall provisions were up slightly from last year due mainly to an increased mix of consumer loan and credit card volumes. International Banking provisions peaked in the second quarter, and then declined in both the third and fourth quarters. The provision for credit losses in Global Banking and Markets was impacted by softness in the energy sector, with increases in both the first and second quarters, before returning to more normalized levels in the second half of the year.

Non-interest expenses

Non-interest expenses increased during the year. This was in part due to the impact of acquisitions, continued investment in growth initiatives, and volume-related technology expenses. The restructuring charge taken in the second quarter and timing-related expenses, such as share and performance-based compensation as well as advertising and business development costs, contributed to the quarterly fluctuations.

Income taxes

The effective tax rate ranged between 19.4% and 23.6% reflecting different levels of income earned in lower tax jurisdictions, as well as the fluctuation of tax-exempt dividend income.

2 0 1 6 S C O T I A B A N K A N N U A L R E P O R T | 29

MANAGEMENT’S DISCUSSION AND ANALYSIS

GROUP FINANCIAL CONDITION

T18Condensed statement of financial position

| | | | | | | | | | | | |

| | | |

| As at October 31 ($ billions) | | 2016 | | | 2015 | | | 2014 | |

Assets | | | | | | | | | | | | |

Cash, deposits with financial institutions and precious metals | | $ | 54.8 | | | $ | 84.5 | | | $ | 64.0 | |

Trading assets | | | 108.6 | | | | 99.1 | | | | 113.2 | |

Securities purchased under resale agreements and securities borrowed | | | 92.1 | | | | 87.3 | | | | 93.9 | |

Investment securities | | | 72.9 | | | | 43.2 | | | | 38.7 | |

Loans | | | 480.2 | | | | 458.6 | | | | 424.3 | |

Other | | | 87.7 | | | | 83.8 | | | | 71.6 | |

Total assets | | $ | 896.3 | | | $ | 856.5 | | | $ | 805.7 | |

| | | |

Liabilities | | | | | | | | | | | | |

Deposits | | $ | 611.9 | | | $ | 600.9 | | | $ | 554.0 | |

Obligations related to securities sold under repurchase agreements and securities lent | | | 97.1 | | | | 77.0 | | | | 89.0 | |

Other liabilities | | | 121.8 | | | | 118.9 | | | | 108.6 | |

Subordinated debentures | | | 7.6 | | | | 6.2 | | | | 4.9 | |

Total liabilities | | $ | 838.4 | | | $ | 803.0 | | | $ | 756.5 | |

| | | |

Equity | | | | | | | | | | | | |

Common equity | | | 52.7 | | | | 49.1 | | | | 45.0 | |

Preferred shares | | | 3.6 | | | | 2.9 | | | | 2.9 | |

Non-controlling interests in subsidiaries | | | 1.6 | | | | 1.5 | | | | 1.3 | |

Total equity | | $ | 57.9 | | | $ | 53.5 | | | $ | 49.2 | |

Total liabilities and shareholders’ equity | | $ | 896.3 | | | $ | 856.5 | | | $ | 805.7 | |

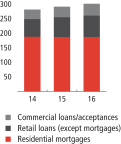

loans & acceptances, $ billions, as at October 31

$ billions, as at October 31

Statement of Financial Position

Assets

The Bank’s total assets as at October 31, 2016 were $896 billion, up $40 billion or 5% from October 31, 2015. This growth was primarily in loans and trading assets, while higher investment securities were offset by lower deposits with financial institutions.

Cash and deposits with financial institutions decreased $28 billion due primarily to lower balances with the U.S. Federal Reserve. Securities purchased under resale agreements and securities borrowed increased $5 billion.

Trading assets increased $9 billion or 10% from October 31, 2015, due primarily to an increase in trading securities from higher holdings of Canadian and U.S. government debt and common equities.

Investment securities increased $30 billion or 69% from October 31, 2015, due primarily to an increase in held-to-maturity securities. As of October 31, 2016, the unrealized gain on available-for-sale securities, after the impact of qualifying hedges, decreased $241 million to $26 million due mainly to realized gains on disposals.