UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2020

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to Commission file number: 1-07183

TEJON RANCH CO.

(Exact name of registrant as specified in its charter)

Delaware 77-0196136

(State or other jurisdiction of incorporation or organization.) (I.R.S. Employer Identification No.)

P.O. Box 1000, Tejon Ranch, California 93243

(Address of principal executive offices) (Zip Code)

(661) 248-3000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | | | | | | | |

| Title of each class | | Trading symbol(s) | | Name of each exchange on which registered | |

| Common Stock, $0.50 par value | | TRC | | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

| | | | | | | | | | | | | | | | | | | | | | |

| Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | | |

| Yes | ☐ | No | ☒ | | | | |

| Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. | | |

| Yes | ☐ | No | ☒ | | | | |

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | | |

| Yes | ☒ | No | ☐ | | | | |

| Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T ((§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). | | |

| Yes | ☒ | No | ☐ | | | | |

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer” “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act.: | | |

| Large accelerated filer | ☐ | Accelerated filer | ☐ | | | |

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ | | | |

| | | Emerging growth company | ☐ | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨ | | |

| Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒ |

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). | | |

| Yes | ☐ | No | ☒ | | | | |

The aggregate market value of registrant’s Common Stock, par value $.50 per share, held by persons other than those who may be deemed to be affiliates of registrant on June 30, 2020 was $377,594,813 based on the last reported sale price on the New York Stock Exchange as of the close of business on that date. | | |

The number of the Company’s outstanding shares of Common Stock on February 28, 2021 was 26,285,692.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the Annual Meeting of Stockholders relating to the directors and executive officers of the Company are incorporated by reference into Part III.

TABLE OF CONTENTS

PART I

Forward-Looking Statements

This annual report on Form 10-K contains forward-looking statements, including without limitation, statements regarding strategic alliances, the almond, pistachio and grape industries, the future plantings of permanent crops, future yields, prices, and water availability for our crops and real estate operations, future prices, production and demand for oil and other minerals, future development of our property, future revenue and income of our jointly-owned travel plaza and other joint venture operations, potential losses to the Company as a result of pending environmental proceedings, the adequacy of future cash flows to fund our operations, and of current assets and contracts to meet our water and other commitments, market value risks associated with investment and risk management activities and with respect to inventory, accounts receivable and our own outstanding indebtedness, ongoing negotiations, the uncertainties regarding the expected impact of COVID-19 on the Company, its customers, suppliers, global economic conditions, and other future events and conditions. In some cases, these statements are identifiable through the use of words such as “anticipate,” “believe,” “estimate,” “expect,” “intend,” “plan,” “project,” “target,” “can,” “could,” “may,” “will,” “should,” “would,” “likely,” and similar expressions such as “in the process,” “designed to,” or “envisioned to” In addition, any statements that refer to projections of our future financial performance, our anticipated growth, and trends in our business and other characterizations of future events or circumstances are forward-looking statements. We caution you not to place undue reliance on these forward-looking statements. These forward-looking statements are not a guarantee of future performance and are subject to assumptions and involve known and unknown risks, uncertainties and other important factors that could cause the actual results, performance or achievements of the Company, or industry results, to differ materially from any future results, performance, or achievement implied by such forward-looking statements. These risks, uncertainties and important factors include, but are not limited to, the impact of COVID-19 and the actions taken by governments, businesses, and individuals in response to it, weather, market and economic forces, availability of financing for land development activities, and competition and success in obtaining various governmental approvals and entitlements for land development activities. No assurance can be given that the actual future results will not differ materially from the forward-looking statements that we make for a number of reasons including those described above and in Part I, Item 1A, “Risk Factors” of this report.

As used in this annual report on Form 10-K, references to the “Company,” “Tejon,” “TRC,” “we,” “us,” and “our” refer to Tejon Ranch Co. and its consolidated subsidiaries. The following discussion should be read in conjunction with the consolidated financial statements and the accompanying notes appearing elsewhere in this annual report on Form 10-K.

ITEM 1. BUSINESS

Company Overview

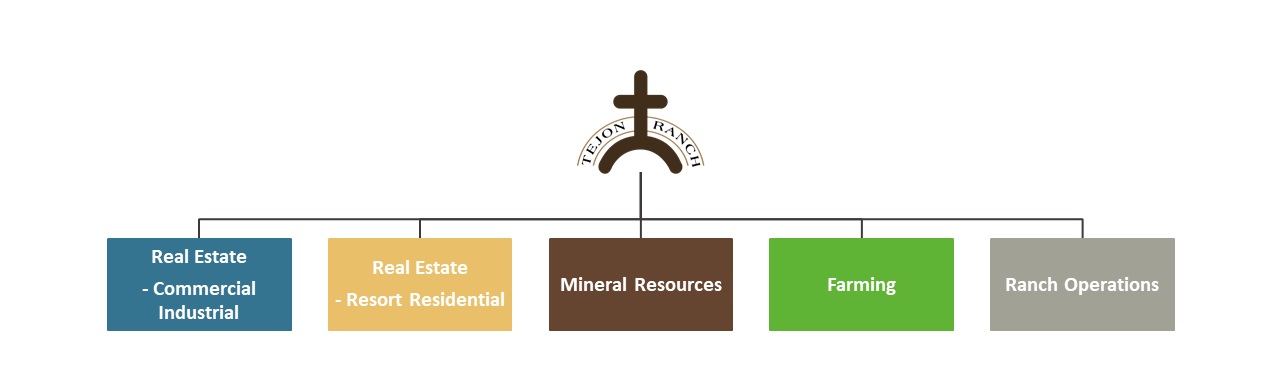

We are a diversified real estate development and agribusiness company committed to responsibly using our land and resources to meet the housing, employment, and lifestyle needs of Californians and create value for our shareholders. Current operations consist of land planning and entitlement, land development, commercial land sales and leasing, leasing of land for mineral royalties, water asset management and sales, grazing leases, farming, and ranch operations.

These activities are performed through our five reporting segments:

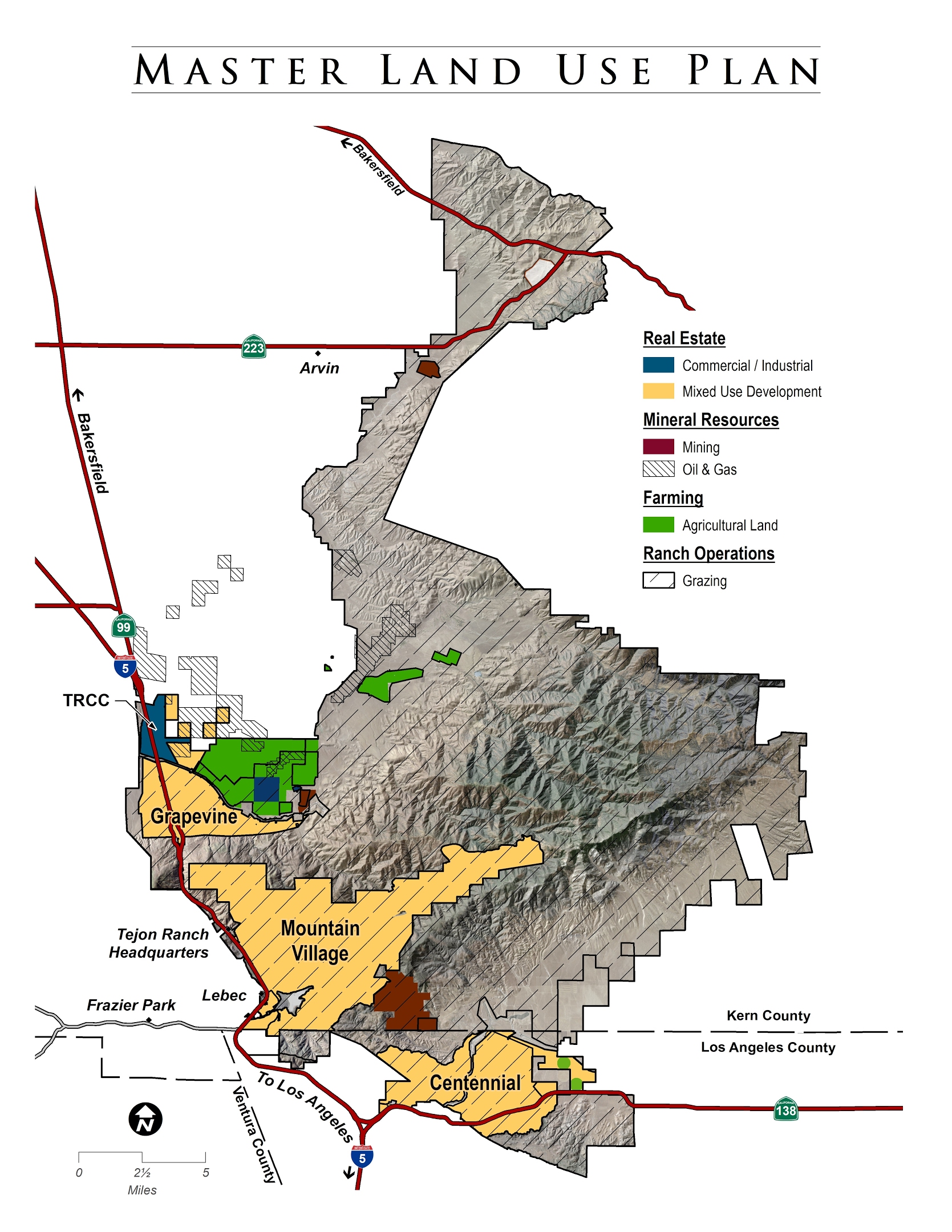

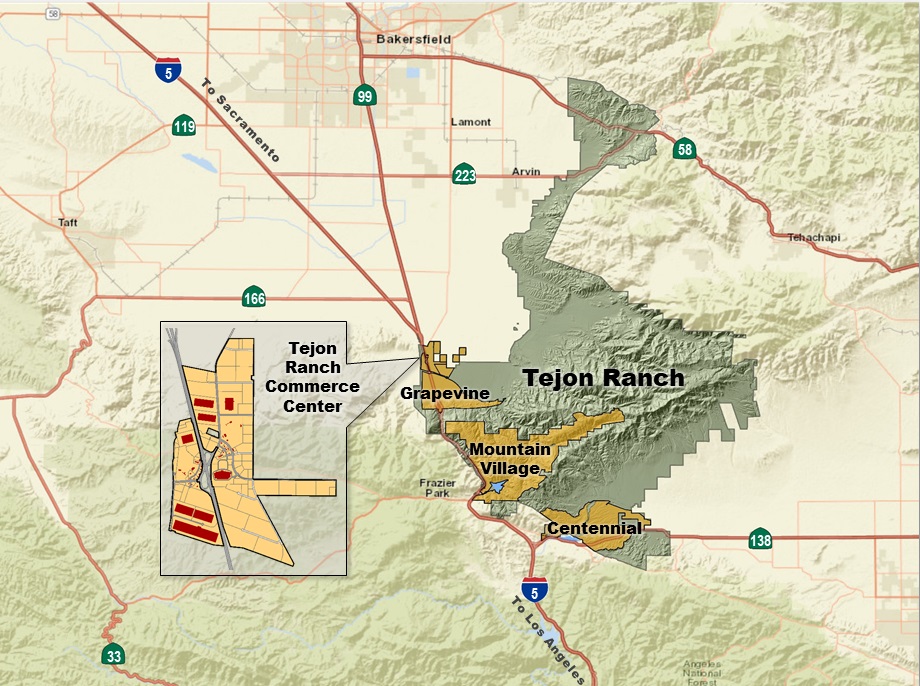

Our prime asset is approximately 270,000 acres of contiguous, largely undeveloped land that, at its most southerly border, is 60 miles north of downtown Los Angeles and, at its most northerly border, is 15 miles east of Bakersfield. We create value by securing entitlements for our land, facilitating infrastructure development, strategic land planning, monetization of land through development and/or sales, and conservation in order to maximize the highest and best use for our land. We are involved in seven joint ventures that either own, develop, and/or operate real estate properties. We enter into joint ventures as a means to facilitate the development of portions of our land.

The COVID-19 Pandemic

Our first priority with regard to the COVID-19 pandemic is to provide for the health and safety of our employees, customers, suppliers and others with whom we partner. We are fully committed to continuing our essential business operations in this unprecedented environment, subject to appropriate risk mitigation and safety practices. Employees are required to wear masks and maintain proper social distancing. The commercial real estate operations that we and our joint ventures operate, are comprised of major national restaurant, retail and fuel brands that follow nationally accepted safety standards that help mitigate the spread of COVID-19.

The U.S. and global economies continue to be affected by the COVID-19 pandemic. There are no reliable estimates of how long the pandemic will last or how many more people will be affected by it, or its continued impact on our business. The return to normalcy is highly contingent on, among other things, the wide spread dissemination and use of an effective vaccine, which is still in its very early stages of distribution. Additionally, the efficacy of current vaccines on newer and potentially more lethal strains of COVID-19 is still being investigated by the scientific community and may also impact the return to normalcy.

We operate in the State of California and our operations were initially subject to the "shelter-in-place" order issued by the California Governor in March 2020, in addition to orders set by Los Angeles and Kern County governments. The State of California took an extremely cautious approach in reopening and even re-imposed statewide stay-at-home orders during the winter of 2020. On January 26, 2021, California lifted regional stay-at-home orders across the state, returning the state to a system of county-by-county restrictions. Kern County and Los Angeles County are rated Purple, as of the date of this report, and represents widespread COVID-19 transmission risk under California's Blueprint for a Safer Economy. Under such circumstances, our farming and mineral resources segments have operated and may continue to operate as normal, while our retail outlets can currently operate at 25% capacity and our restaurants can operate for take-out and outdoor dining only.

The actions taken by governments, other businesses, and individuals in response to the pandemic did have and will continue to have an impact our results of operations and overall financial performance. In 2020, we evaluated our operations for expense reductions and cash savings by renegotiating contracts and pricing with a significant portion of our vendors, and right sizing our labor needs. We will continue to monitor and evaluate our needs for expense reduction throughout 2021.

Please see the "Results of Operations" by Segment in Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations" for further discussion of the impact of COVID-19 on our various reporting segments.

Business Objectives and Strategies

Our primary business objective is to maximize long-term shareholder value through the monetization of our land-based assets. A key element of our strategy is to entitle and then develop large-scale mixed-use master planned residential and commercial/industrial real estate projects to serve the growing populations of Southern and Central California. Our mixed-use master planned residential developments have been approved to collectively include up to 35,278 housing units, and more than 35 million square feet of commercial space. We have obtained entitlements on Mountain Village at Tejon Ranch, or MV, and the tentative tract map for the first four phases of residential development in MV has been approved, as well as the commercial site plan for the first phase of commercial development in MV. Centennial, at Tejon Ranch, or Centennial, had entitlements approved in December 2018, and received legislative approvals in April 2019 from the Los Angeles County Board of Supervisors. The Kern County Board of Supervisors unanimously reapproved the Grapevine at Tejon Ranch project, or Grapevine in 2019. We are currently engaged in construction, commercial sales, and leasing at our fully operational commercial/industrial center Tejon Ranch Commerce Center, or TRCC. In January 2021, the Kern County Board of Supervisors approved two Conditional Use Permits, authorizing development of multi-family apartment uses within the Tejon Ranch Commerce Center, on a 27-acre site located immediately north of the Outlets at Tejon. This authorization allows the Company to develop up to a maximum of 495 multi-family residences, in thirteen apartment buildings, as well as approximately 6,500 square feet of community amenity space and 8,000 square feet of community serving retail on the ground floor of a portion of the residential buildings. All of these efforts are supported by diverse revenue streams generated from other operations including: farming, mineral resources, and our various joint ventures.

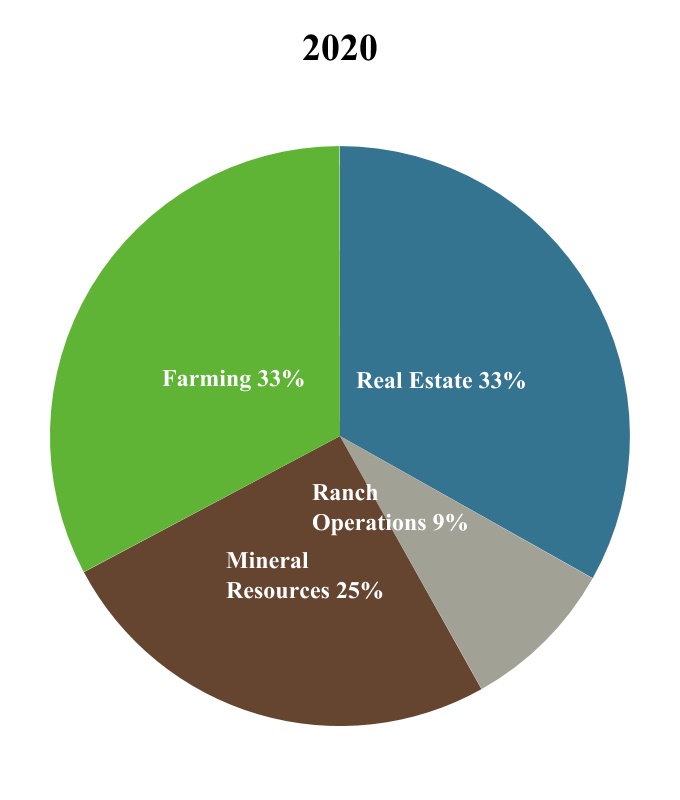

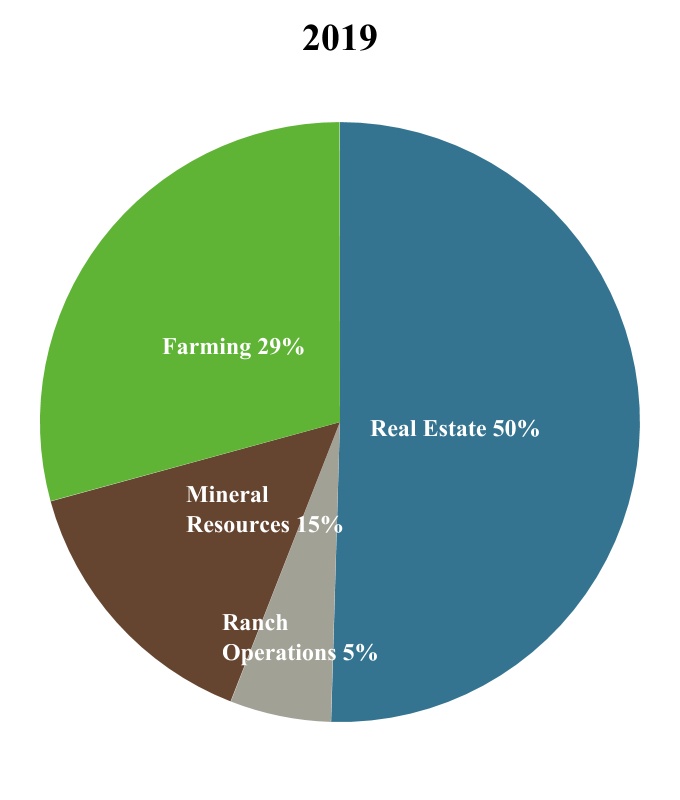

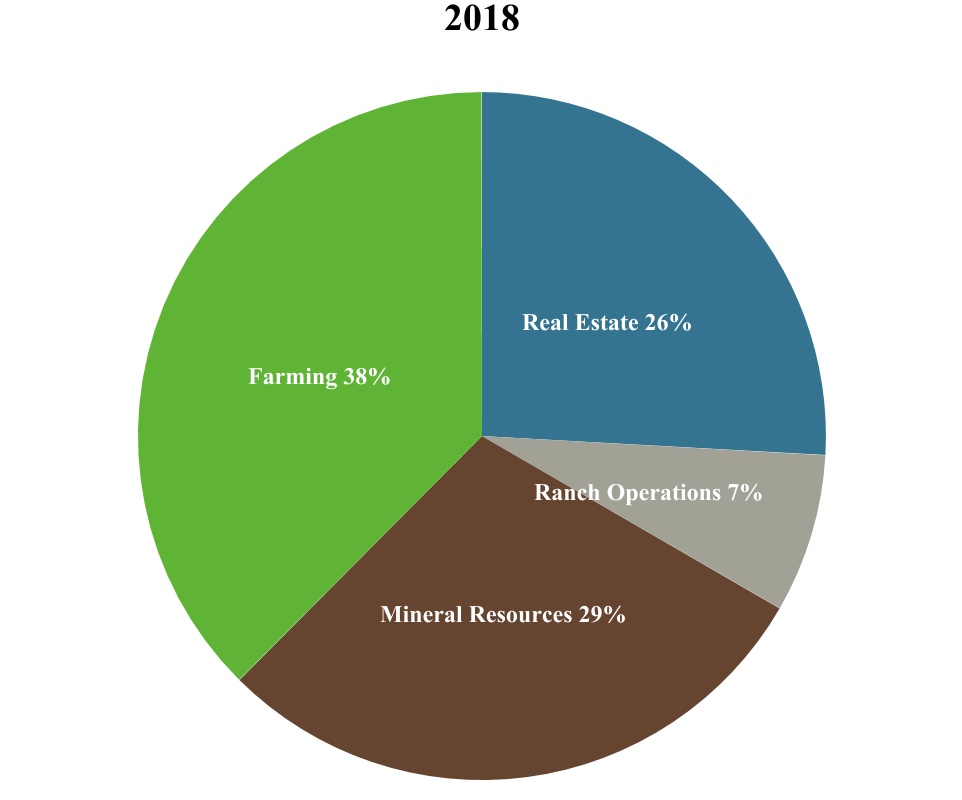

Percentage of Total Revenue1,2 by Segment:

1. Real Estate includes equity in earnings of unconsolidated joint ventures.

2. Charts presented only include the segment revenues, other income components are excluded.

Note: Our Resort Residential reporting segment did not report revenues in the periods reported herein.

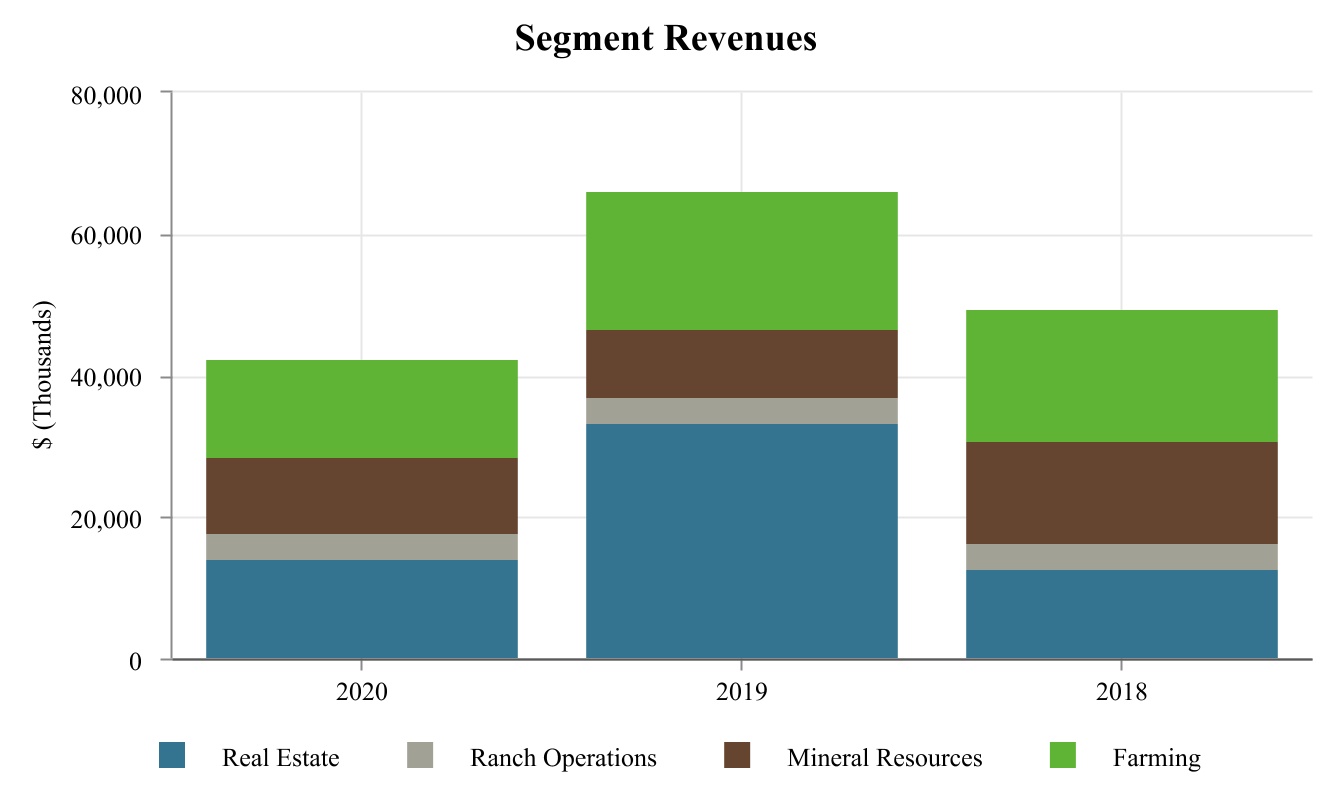

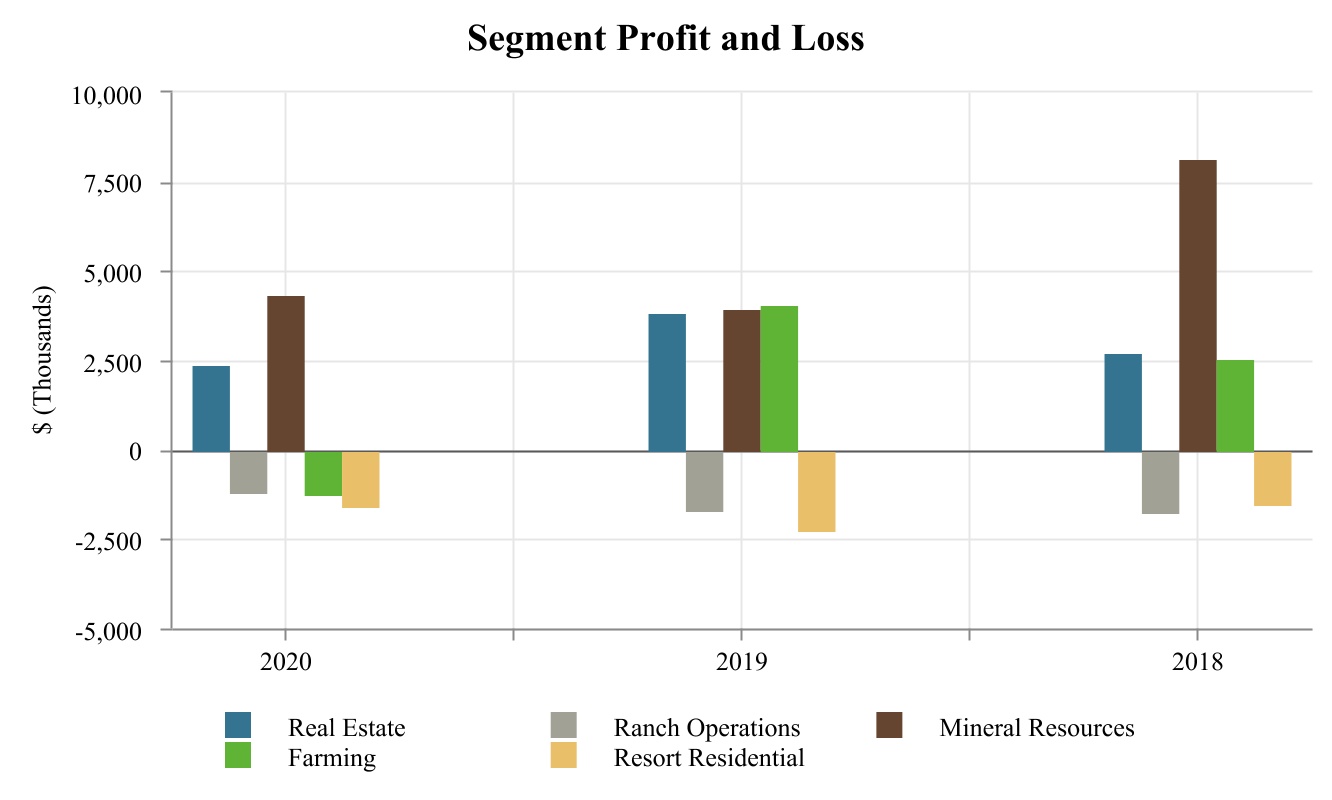

The following table shows the revenues from continuing operations, segment profits and identifiable assets of each of our continuing segments for the last three years:

FINANCIAL INFORMATION ABOUT SEGMENTS

(Amounts in thousands of dollars)

| | | | | | | | | | | | | | | | | | | | |

| | Year Ended December 31, |

| | 2020 | | 2019 | | 2018 |

| Revenues and Other Income | | | | | | |

| Real Estate—Commercial/Industrial | | $ | 9,536 | | | $ | 16,792 | | | $ | 8,970 | |

| Mineral Resources | | 10,736 | | | 9,791 | | | 14,395 | |

| Farming | | 13,866 | | | 19,331 | | | 18,563 | |

| Ranch operations | | 3,692 | | | 3,609 | | | 3,691 | |

| Segment revenues | | 37,830 | | | 49,523 | | | 45,619 | |

| | | | | | |

| Investment income | | 884 | | | 1,239 | | | 1,344 | |

| Revenues and other income | | 38,714 | | | 50,762 | | | 46,963 | |

| Equity in earnings of unconsolidated joint ventures | | 4,504 | | | 16,575 | | | 3,834 | |

Total revenues and other income (1) | | $ | 43,218 | | | $ | 67,337 | | | $ | 50,797 | |

| Segment Profits (Losses) and Net Income | | | | | | |

| Real Estate—Commercial/Industrial | | $ | 2,414 | | | $ | 3,831 | | | $ | 2,724 | |

| Real Estate—Resort/Residential | | (1,612) | | | (2,247) | | | (1,530) | |

| Mineral Resources | | 4,322 | | | 3,973 | | | 8,172 | |

| Farming | | (1,237) | | | 4,080 | | | 2,535 | |

| Ranch operations | | (1,204) | | | (1,707) | | | (1,760) | |

Segment profits (2) | | 2,683 | | | 7,930 | | | 10,141 | |

| Gain on sale of real estate | | 1,331 | | | — | | | — | |

| Investment income | | 884 | | | 1,239 | | | 1,344 | |

| Other income (loss) | | 110 | | | (1,824) | | | (59) | |

| Corporate expenses | | (9,430) | | | (9,361) | | | (9,705) | |

| (Loss) income from operations before equity in earnings of unconsolidated joint ventures | | (4,422) | | | (2,016) | | | 1,721 | |

| Equity in earnings of unconsolidated joint ventures | | 4,504 | | | 16,575 | | | 3,834 | |

| Income before income taxes | | 82 | | | 14,559 | | | 5,555 | |

| Income tax expense | | 829 | | | 3,980 | | | 1,320 | |

| Net (loss) income | | (747) | | | 10,579 | | | 4,235 | |

| Net loss attributable to non-controlling interest | | (7) | | | (1) | | | (20) | |

| Net (loss) income attributable to common stockholders | | $ | (740) | | | $ | 10,580 | | | $ | 4,255 | |

Identifiable Assets by Segment (3) | | | | | | |

| Real estate—commercial/industrial | | $ | 73,317 | | | $ | 76,814 | | | $ | 65,929 | |

| Real estate—resort/residential | | 297,052 | | | 286,801 | | | 273,620 | |

| Mineral Resources | | 57,797 | | | 55,049 | | | 54,144 | |

| Farming | | 38,090 | | | 41,258 | | | 40,835 | |

| Ranch operations | | 2,442 | | | 2,624 | | | 2,973 | |

| Corporate | | 67,651 | | | 76,876 | | | 91,547 | |

| Total assets | | $ | 536,349 | | | $ | 539,422 | | | $ | 529,048 | |

(1) Refer to Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations for additional detail on segment revenues.

(2) Segment profits are revenues less operating expenses, excluding investment income and expense, corporate expenses, equity in earnings of unconsolidated joint ventures, and income taxes.

(3) Total Assets by Segment include both assets directly identified with those operations and an allocable share of jointly used assets. Corporate assets consist of cash and cash equivalents, refundable and deferred income taxes, land, buildings, and improvements.

Real Estate Development Overview

Our real estate operations consist of the following activities: real estate development, commercial land sales and leasing, land planning and entitlement, and conservation.

Interstate 5, one of the nation’s most heavily traveled freeways, brings in excess of 88,000 vehicles per day through our land, which includes 16 miles of Interstate 5 frontage on each side of the freeway and the commercial land surrounding three interchanges. The strategic plan for real estate focuses on development opportunities along the Interstate 5 and Highway 138 corridors, which includes TRCC in Kern County, Centennial, a mixed-use master planned community on our land in Los Angeles County, MV, a resort and residential community in Kern County, and Grapevine, a mixed-use master planned community on our land in Kern County. TRCC includes developments east and west of Interstate 5 at TRCC-East and TRCC-West, respectively.

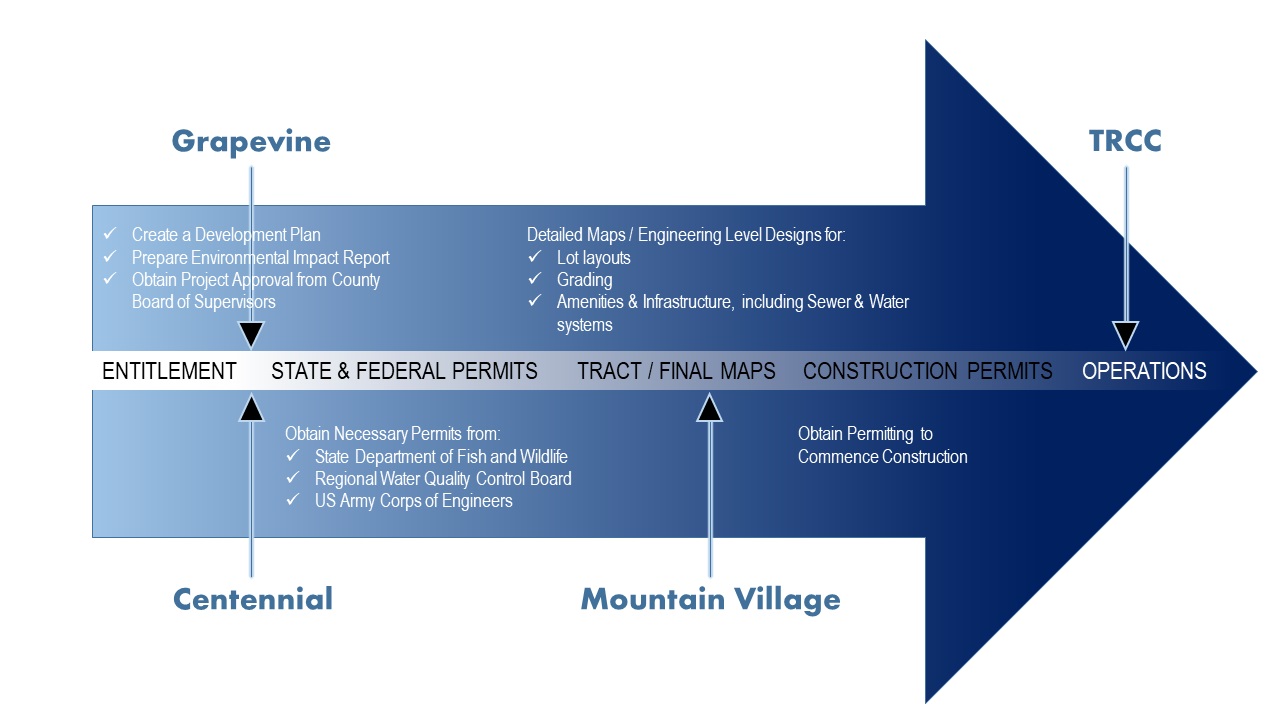

The chart below is a continuum of the real estate development process highlighting each project's current status and key milestones to be met in moving through the real estate development process in California. During this process, we may experience delays arising from factors beyond our control. Such factors include litigation and a changing regulatory environment.

Operating Segments

Real Estate - Commercial/Industrial

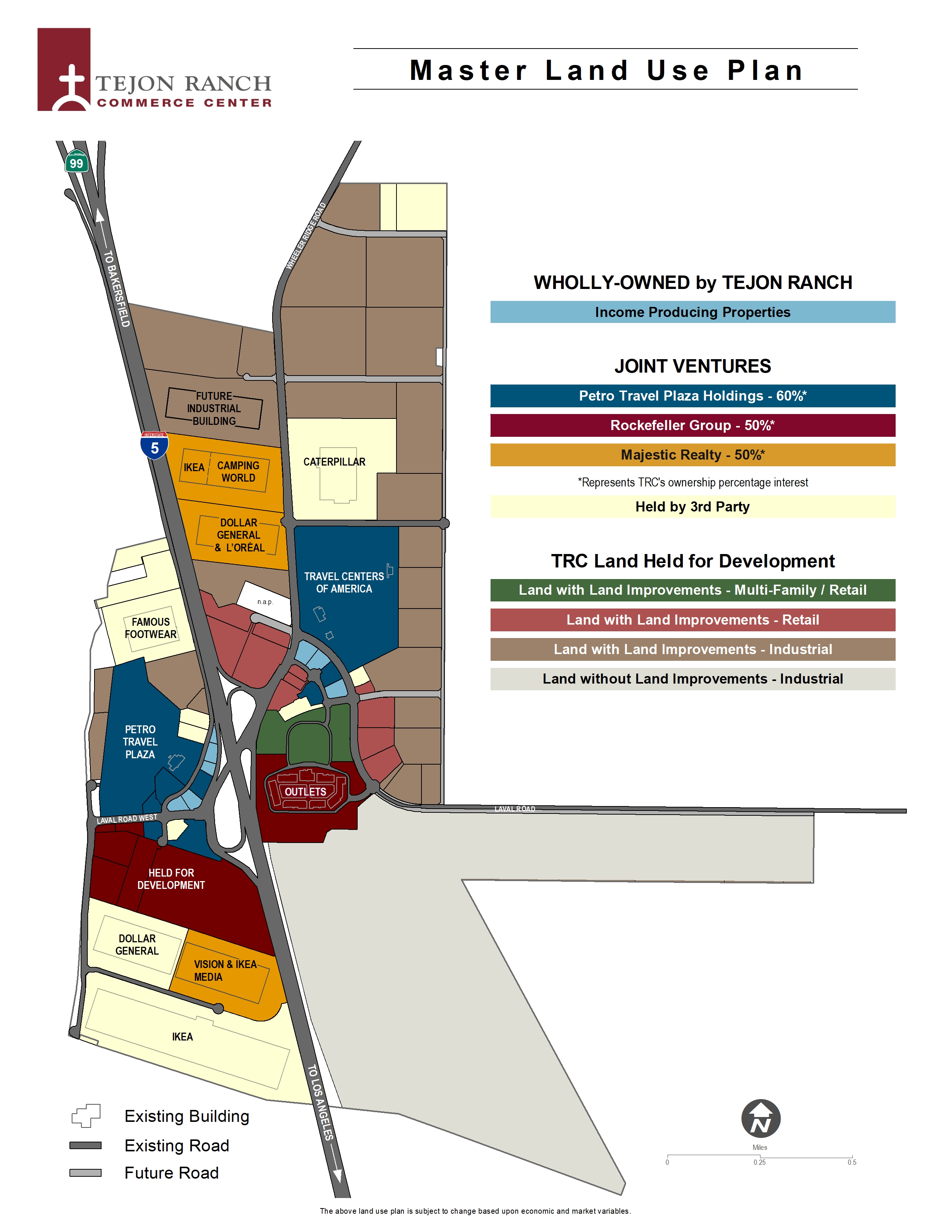

Our real estate commercial/industrial segment includes: planning, and permitting of land for development; construction of infrastructure; the construction of pre-leased buildings; the construction of buildings to be leased or sold; and the sale of land to third parties for their own development. The commercial/industrial segment also includes activities related to communications leases and landscape maintenance fees. At the heart of our real estate commercial/industrial segment is TRCC, a 20 million square foot commercial/industrial development on Interstate 5 just north of the Los Angeles basin. Nearly six million square feet of industrial, commercial and retail space has already been developed, including distribution centers for IKEA, Caterpillar, Famous Footwear, L'Oreal, Camping World and Dollar General. TRCC sits on both sides of Interstate 5, giving distributors immediate access to the west coast’s principal north-south goods movement corridor.

The U.S. Department of Commerce expanded the Foreign Trade Zone (FTZ) it previously granted, covering all the industrial sites within TRCC, an area totaling 1,094 acres. The FTZ designation allows the user within the FTZ to secure the many benefits and cost reductions associated with streamlined movement of goods in and out of the zone. This FTZ designation is further supplemented by the Economic Development Incentive Policy, or EDIP, adopted by the Kern County Board of Supervisors. EDIP is aimed to expand and enhance the County's competitiveness by taking affirmative steps to attract new businesses and to encourage the growth and resilience of existing businesses. The EDIP provides incentives such as assistance in obtaining state tax incentives, building supporting infrastructure, and workforce development.

TRCC Residential:

On January 6, 2021, the Kern County Board of Supervisors approved two Conditional Use Permits (CUP) which will authorize development of multi-family apartment uses within the Tejon Ranch Commerce Center. The approved CUP's authorize the Company to develop up to a maximum of 495 multi-family residences, in thirteen apartment buildings, as well as approximately 6,500 square feet of community amenity space and 8,000 square feet of community retail on the ground floor of a portion of the residential buildings. The development would be located on a 27-acre site located immediately north of the Outlets at Tejon. The Company will allocate resources to this project during 2021 to advance this new project at TRCC, providing the much needed housing for the thousands of employees currently working at the various distribution centers, retailers and fast-food restaurants at TRCC.

Construction:

We formed TRC-MRC 3, a joint venture with Majestic Realty Co., or Majestic, a Los Angeles-based commercial/industrial developer, to pursue the development, construction, leasing, and management of a 579,040 square foot industrial building at TRCC-East in 2018. The construction of the industrial building was completed in the fourth quarter of 2019, and the Company has leased 100% of the rentable space to two tenants.

Also in 2019, we completed construction of a 4,900 square foot multi-tenant retail building at TRCC-East. We contributed this multi-tenant building and underlying land to our joint venture with TravelCenters of America Inc. In return for this land contribution, the Company received a priority distribution right of $2.8 million from the joint venture. The joint venture opened this location for operations in 2020, operating several national brands including Dunkin' Donuts, Jamba Juice, Charleys Philly Steaks, and Baskin Robbins.

The following is a summary of the Company's commercial, retail and industrial real estate developments as of December 31, 2020:

| | | | | | | | | | | | | | |

| ($ in thousands) | | | | |

| Project | Cost to Date | Estimated Cost to Complete | Total Estimated Cost at Completion | Estimated Completion Date |

| Tejon Ranch Commerce Center | $ | 90,294 | | $ | 70,083 | | $ | 160,377 | | TBD |

Less: Reimbursements from TRPFFA1 | 76,891 | | 50,537 | | 127,428 | | TBD |

| TRCC Development Costs, net | $ | 13,403 | | $ | 19,546 | | $ | 32,949 | | |

| | | | |

1The Tejon Ranch Public Facilities Financing Authority, or TRPFFA, is a joint powers authority formed by Kern County and Tejon-Castac Water District, or TCWD, to finance public infrastructure within the Company’s Kern County developments. TRPFFA, through bond sales, will reimburse the Company for qualifying infrastructure costs at TRCC. |

The following table summarizes total entitlements for TRCC as of December 31, 2020:

| | | | | | | | |

| (in square feet) | Industrial | Commercial Retail |

| Total entitlements received | 19,300,941 | 956,309 |

| Total entitlements used | 5,296,669 | 637,695 |

| Entitlements available | 14,004,272 | 318,614 |

|

|

|

Commercial/industrial real estate sales:

The logistics operators currently located within TRCC have demonstrated success in serving all of California and the western region of the United States, and we are building from their success in our marketing efforts. We will continue to focus our marketing strategy for TRCC on the significant labor and logistical benefits of our site, the pro-business approach of Kern County, and the success of the current tenants and owners within our development. Our strategy fits within the logistics model that many companies are using, which favors large, centralized distribution facilities which have been strategically located to maximize the balance of inbound and outbound efficiencies, rather than a number of decentralized smaller distribution centers. Operators located within TRCC have demonstrated success through utilization of this model. With access to markets of over 40 million people for next-day delivery service, they are also demonstrating success with e-commerce fulfillment.

We believe that our ability to provide fully-entitled, shovel-ready land parcels to support buildings of any size, can provide us with a potential marketing advantage in the future. We continue our marketing efforts targeting industrial users in the Santa Clarita Valley of northern Los Angeles County, and the northern part of the San Fernando Valley for whom we may be an attractive provider due to the limited availability of new product and high real estate costs in these locations. Tenants in these geographic areas are typically users of smaller facilities, but often are looking to expand operations and cannot find larger size buildings in these markets.

The commercial/industrial real estate sales market is highly competitive, with competition throughout California. The principal factors of competition in this industry are price, availability of labor, proximity to the port complexes of Los Angeles and Long Beach and customer base. A potential disadvantage to our development strategy is our distance from the ports of Los Angeles and Long Beach in comparison to the warehouses and distribution centers located in the West Inland Empire.

Our most direct regional competitors are in the Inland Empire, a large industrial area located 60 miles east of Los Angeles, which continues its expansion eastward beyond Riverside and San Bernardino into the Perris, Moreno Valley, and Beaumont regions of Southern California. We also face competition within Northern Los Angeles, which is comprised of the San Fernando Valley and Santa Clarita Valley along with areas north of us in the San Joaquin Valley of California. Strong demand for large distribution facilities is driving development farther east in search for large entitled parcels. As development in the Inland Empire continues to move east and farther away from the ports, our distance from the ports is becoming less of a disadvantage.

During 2020, vacancy rates in the Inland Empire dropped to a historic low of 2.6% compared to 3.5% in 2019, with 2020 net absorption totaling 23,805,058 square feet. Asking rents continued to rise by 5.6% year-over-year. The Inland Empire industrial market has not been negatively impacted by the ongoing COVID-19 pandemic. As lease rates increase in the Inland Empire, we often times have greater pricing advantages due to our lower land basis.

During 2020, vacancy rates in the northern Los Angeles industrial market, which includes the San Fernando Valley and Santa Clarita Valley, increased to 2.3%, compared to 1.4% in 2019. Rents have been increasing for the past seven years, and is forecasted to stabilize at the current level at $0.86 PSF NNN. Industrial vacancy rates are expected to continue to drop, and industrial users seeking larger spaces are having to go further north into neighboring Kern County and particularly, TRCC which has attracted increased attention as market conditions continue to tighten. In 2020, the Los Angeles and Long Beach Port container traffic remained high at 14.69 million Twenty-Foot Equivalent Units, or TEU's compared to 14.57 million TEU in 2019. TEU is a measure of a ship's cargo carrying capacity. The dimensions of one TEU are equal to that of a standard shipping container measuring 20 feet long by 8 feet tall.

Joint Ventures:

Our joint venture with TA/Petro owns and operates two travel and truck stop facilities, restaurants, and five separate gas stations with convenience stores within TRCC-West and TRCC-East.

We are involved in three joint ventures with Majestic to develop, lease, manage, and/or acquire industrial buildings within TRCC. The three joint ventures currently own and operate three industrial buildings occupying over 1.7 million rentable square feet.

At December 31, 2020, we were involved in two joint ventures with Rockefeller Development Group (RDG). The two joint ventures are: (1) 18-19 West LLC, which owns 61.5 acres of land for future development within TRCC-West; and (2) TRCC/Rock Outlet Center LLC, which operates the Outlets at Tejon. Our Five West Parcel, LLC joint venture with RDG was dissolved in the fourth quarter of 2020. In 2019, Five West Parcel, LLC sold the building and land within the joint venture to a third party at a sales price of $29,088,000, recognizing a gain of $17,537,000. Our 18-19 West LLC joint venture entered into a land purchase option agreement with the third-party that purchased the Five West building and land, to purchase lots 18 and 19

at a price of $13.8 million through the option period ending May 21, 2021. If the option is extended to November 21, 2021, the price increases to $15.2 million. The land option expires in the fourth quarter of 2021.

In conjunction with providing relief to certain tenants as a result of the COVID-19 pandemic, the TRCC/Rock Outlet Center has agreed to defer rent for certain tenants due to the closure of the outlet center from March 20, 2020 through May 27, 2020. The following table sets forth information regarding the minimum rents billed and deferred to-date at the TRCC/Rock Outlet Center property level for the year-ended December 31, 2020. TRCC/Rock Outlet Center is continuing to work with tenants on temporary rent payment relief through rent deferrals. We continue to assess the probability of collecting outstanding receivables related to the two tenants with whom we are currently in on-going negotiations. Management will continue to monitor each negotiation diligently, and when determined collectability is not probable, will reserve accordingly.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| ($ in thousands, except number of tenants) | Tenants2 | | Rent Billing1 | | Rent Relief due to COVID-19 | | Deferred Rent Contractually Due in 2020 | | Deferred Rent Contractually Due in 2021 |

| Rent Deferral Agreements | 8 | | | $ | 977 | | | $ | 217 | | | $ | 24 | | | $ | 193 | |

| Rent Abatement Agreements | 17 | | | $ | 1,413 | | | $ | 575 | | | N/A3 | | N/A3 |

| On-Going Deferral Negotiations | 2 | | | $ | 269 | | | $ | — | | | $ | — | | | $ | — | |

| 27 | | 2,659 | | | 792 | | | 24 | | | 193 | |

| | | | | | | | | |

| Percentage of Rent Deferred or Abated | | 30 | % | | | | |

| | | | | | | | | |

1Amounts shown represent rent billing for tenants that had or are undergoing lease renegotiations as of the year-ended December 31, 2020. Of the total contractual rent billings of $2.7 million, $0.8 million was subject to COVID-19 rent relief, while $1.9 million was contractually due as of December 31, 2020. |

2 Excludes percentage rent tenants. |

3 Not applicable for rent abatement. | | | | | | | | | |

Leasing:

Within our commercial/industrial segment, we lease land to various types of tenants. We currently lease land to two auto service stations with convenience stores, 13 fast-food operations, a full-service restaurants, a motel, an antique shop, and a post office.

In addition, the Company leases several microwave repeater locations, radio and cellular transmitter sites, fiber optic cable routes, and 32 acres of land to Pastoria Energy Facility, L.L.C., or PEF, for an electric power plant.

In response to the COVID-19 pandemic, tenants began requesting various forms of rent relief beginning in March 2020 and although the requests range in scope, the most common request is for a full or partial rent deferment for three months. During the twelve months ended December 31, 2020, the Company has agreed to defer rent for certain tenants at TRCC, with the requirement that a significant amount of the deferred rent will be fully repaid in 2021. The following table sets forth information regarding the minimum rents billed and deferred for the twelve months ended December 31, 2020.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| ($ in thousands, except for impacted tenants) | Tenants | | Rent Billing1 | | Deferred Rent due to COVID-19 | | Deferred Rent Contractually Due in 2020 | | Deferred Rent Contractually Due in 2021 |

| TRCC Leasing | 5 | | | $ | 1,362 | | | $ | 104 | | | $ | 18 | | | $ | 86 | |

| Other Commercial Leases | 3 | | | 522 | | | $ | 70 | | | 13 | | | 57 | |

| 8 | | | $ | 1,884 | | | $ | 174 | | | $ | 31 | | | $ | 143 | |

| | | | | | | | | |

| Percentage of Rent Deferred | | 9 | % | | | | |

| | | | | | | | | |

1Amounts shown represent rent billing for tenants that had or are undergoing lease renegotiation for the twelve months ended December 31, 2020. Of the total contractual rent billings of $1.9 million, $0.2 million was subject to COVID-19 rent relief, while $1.7 million was contractually due as of December 31, 2020. |

The following table summarizes information with respect to lease expirations for our consolidated entities as of December 31, 2020.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Year of Lease Expiration | | Number of Expiring Leases | | RSF of Expiring Leases | | Annualized Base Rent1 | | Percentage of Annual Minimum Rent |

| 2021 | | 6 | | 60,722 | | $239 | | 3.97% |

| 2022 | | 6 | | 47,614 | | $383 | | 6.36% |

| 2023 | | 5 | | 4,640 | | $394 | | 6.54% |

| 2024 | | — | | — | | $— | | —% |

| 2025 | | 5 | | 60,208 | | $536 | | 8.90% |

| 2026 | | 3 | | 4,645 | | $259 | | 4.30% |

| 2027 | | 1 | | 1,801 | | $62 | | 1.03% |

20282 | | 1 | | — | | $14 | | 0.23% |

20293 | | 1 | | 1,394,000 | | $3,794 | | 63.00% |

| 2030 | | — | | — | | $— | | —% |

| 2031 | | — | | — | | $— | | —% |

| Thereafter | | 4 | | 193,207 | | $341 | | 5.66% |

| 1 - Annualized base rent is calculated as monthly base rent (cash basis) per the lease, as of the reporting period, multiplied by 12. Annualized base rent shown in thousands. |

| 2 - This lease pertains to a communication lease that does not have defined rentable square feet. |

| 3 - This amount includes 32 acres of the PEF ground lease. |

For the year ended December 31, 2020, we had two lease renewals and three lease expirations. These expirations represented less than 5% of annualized base rent.

Please refer to Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for information regarding our 2020 commercial/industrial operating results.

Real Estate - Resort/Residential

Our resort/residential segment activities include land entitlement, land planning and pre-construction engineering, and land stewardship and conservation activities. We have three major resort/residential communities within this segment:

•Mountain Village at Tejon Ranch

•Centennial at Tejon Ranch

•Grapevine at Tejon Ranch

The entitlement process precedes the regulatory approvals necessary for land development and routinely takes several years to complete. The Conservation Agreement we entered into with five major environmental organizations in 2008 is designed to minimize opposition from environmental groups to these projects and eliminate or reduce the time spent in litigation once governmental approvals are received. Litigation by environmental and other special interest groups have been a primary cause of delays and increased costs for real estate development projects in California. For discussion on legal matters pertaining to our developments, see Note 14 (Commitments and Contingencies) of the Notes to Consolidated Financial Statements.

As we embark on our mixed-use master planned communities, we understand that it can take up to 25 years, or longer, to complete from commencement of construction. The entitlement process for development of property in California is complex, lengthy (spanning multiple years) and costly, involving numerous federal, state, and county regulatory approvals. We are unable to determine anticipated completion dates for our real estate development projects with certainty because the time for completion is heavily dependent on the regulatory approvals necessary for land development. Also, as a real estate developer, we are cognizant of the micro- and macro-economic factors that have a significant influence on the real estate sector. As a developer, one would be at an economic disadvantage to bring product to market with no willing or able buyers. This ebb and flow of the economy also plays into the timing of our completion date. Costs will also fluctuate over the life of these projects as a result of the cost of labor and raw materials and the timing of approvals and other activity. The uncertainty of estimated costs to completion is compounded by the potential impact of inflation, which will fluctuate with the equally uncertain completion dates for our projects.

Mountain Village at Tejon Ranch:

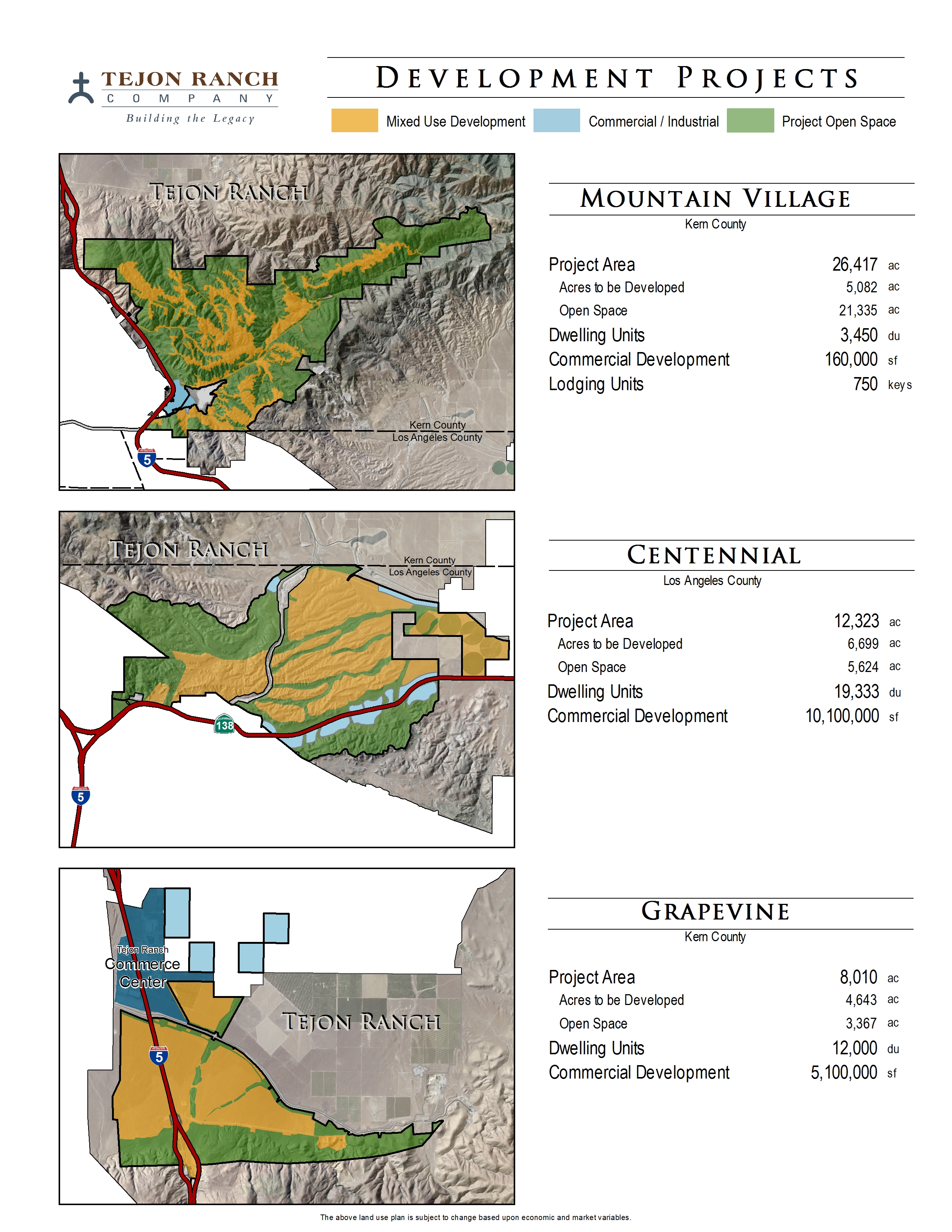

MV is planned to be an exclusive, low-density, resort-based community that will provide its owners and guests with a wide variety of recreational opportunities, lodging and spa facilities, putting greens, a range of housing options, and other exclusive services and amenities that are designed to distinguish MV as the resort community of choice for the Southern California market. MV encompasses 26,417 acres, including 5,082 acres for a mixed-use master planned community to include housing, retail, and commercial components. MV is entitled for 3,450 homes, 160,000 square feet of commercial development, 750 hotel keys, and 21,335 acres of open space. The first tentative tract map for the project, which includes 752 residential lots, was approved by Kern County in December 2017.

We are working toward delivering the first phase of the 160,000 square foot commercial center that we call Farm Village. Farm Village will serve as the commercial center and community gathering place for MV residents and visitors, as well as the gateway to MV. Farm Village will include fresh culinary offerings, artisan markets, boutique lodging, and an array of trails, gardens, and agriculture that will be intertwined to create the most unique, relaxing and edutaining experience while fulfilling the needs of residents of MV. In April 2018, we obtained commercial site plan approval from Kern County for the first phase of the Farm Village consisting of 53,180 square feet.

MV is fully entitled and all necessary permits have been issued to begin development once the mapping process is complete. Timing of MV development in the coming years will be dependent on the strength of both the economy and the residential real estate market. For 2021, we will focus on the completion of the final map for the first phases of MV, consumer and market research studies and fine tuning of development business plans as well as defining the capital funding sources for this development. As we complete the final map, we expect to begin exploring funding opportunities for the development of MV. Such funding opportunities could come from a variety of sources, such as joint ventures with financial partners, debt financing, or the Company’s issuance of common stock.

Centennial at Tejon Ranch:

The Centennial development is a mixed-use master planned community development encompassing 12,323 acres of our land within Los Angeles County. Centennial is entitled for 19,333 homes and 10.1 million square feet of commercial development. Centennial will incorporate business districts, schools, retail and entertainment centers, medical facilities and other commercial office and light industrial businesses that, when complete, will create a substantial number of jobs. The project is being developed by Centennial Founders, LLC, a consolidated joint venture in which we have a 92.85% ownership interest as of December 31, 2020. Centennial is envisioned to be an ecologically friendly community that will achieve a jobs-housing balance.

In December 2018, the Los Angeles County Board of Supervisors took action to approve the Specific Plan and 30 year Development Agreement for Centennial by a vote of 4-1. In April 2019, the Los Angeles County Board of Supervisors' affirmed their final approval of Centennial project. The Company is working with the County of Los Angeles to address litigation filed in the Los Angeles Superior Court and is currently waiting for the Court's decision.

In 2016, Lewis Investment Company withdrew from the joint venture. The surviving members (TRC, TRI Pointe Homes and CalAtlantic) absorbed the equity of Lewis Investment Company based on their respective proportionate interest in the joint venture at the time of the withdrawal. In 2018, CalAtlantic also withdrew from the joint venture. The surviving members (TRC and TRI Pointe Homes, Inc.) absorbed the equity of CalAtlantic based on their respective proportionate interest in the joint venture at the time of the withdrawal. Both withdrawals were deemed an equity transaction between members and had no earnings impact on the Company.

Grapevine at Tejon Ranch:

Grapevine is a mixed-use master planned community encompassing 8,010 acres of our lands within Kern County located on the San Joaquin Valley floor, adjacent to TRCC. Grapevine is entitled for 12,000 homes, 5.1 million square feet for commercial development, and more than 3,367 acres of open space and parks. The 4,643 acres designated for mixed-use development will include housing, retail, commercial, and industrial components. On December 6, 2016, the Kern County Board of Supervisors unanimously approved the Specific Plan and the Environmental Impact Report, or EIR, for the development of the Grapevine community, which included approval for land use designation, zoning and a development agreement. On December 11, 2018, the Kern County Superior Court ruled that portions of the EIR required corrections and ordered that the County rescind the Grapevine project approvals until a supplemental environmental analysis addressing the corrections was completed. On December 10, 2019, the Kern County Board of Supervisors adopted the supplemental re-circulated EIR prepared in response to the court ruling, and reapproved the development of Grapevine unanimously. On January 10, 2020, an action was filed in Kern County Superior Court pursuant to CEQA against Kern County, concerning Kern County’s approval of the December 2019 re-entitlement, including certification of the final EIR. On January 22, 2021 the court ruled in favor of the Company and Kern

County on all issues, and directed Kern County and the Company to prepare a final judgment reflecting its ruling in favor of the Company. See Note 14 (Commitments and Contingencies) of the Notes to Consolidated Financial Statement for further discussion.

The greatest competition for the Centennial and Grapevine communities will come from California developments in the Santa Clarita Valley, Lancaster, Palmdale, and Bakersfield. The developments in these areas will be providing similar housing product as our developments. The principal factors of competition in this industry are product segmentation, pricing of product, amenities offered, and location. We will attempt to differentiate our developments through our unique setting, land planning and different product offerings. MV will compete generally for discretionary dollars that consumers will allocate to recreational and residential homes.

The following is a summary of the Company's residential real estate developments as of December 31, 2020:

| | | | | | | | | | | | | | |

| Community: | Mountain Village | Grapevine | Centennial | Resort |

| Location: | Kern County | Kern County | Los Angeles County | Residential |

Project Status1: | Entitled | Entitled | Entitled | Total |

| Entitlement Area (acres): | 26,417 | 8,010 | 12,323 | 46,750 |

| Housing Units: | 3,450 | 12,000 | 19,333 | 34,783 |

Commercial Development (sqft)2: | 160,000 | 5,100,000 | 10,100,000 | 15,360,000 |

| Open Areas (acres): | 21,335 | 3,367 | 5,624 | 30,326 |

Costs to Date3: | $146,662 | $36,815 | $108,600 | $292,077 |

(1) Estimated completion anticipated to be 25 years, or longer, from commencement of construction. To-date construction has not begun.

(2) MV also has approval for up to 750 lodging units and 350,000 square feet of facilities in support of two 18-hole golf courses.

(3) Total estimated project costs are difficult to accurately forecast with any certainty at this time due to finalization of entitlement and mapping processes, as well as final engineering for the developments, and capital funding structure selected. Dollars presented in thousands.

Mineral Resources

Mineral resources consist of oil and gas royalties, rock and aggregate royalties, royalties from a cement operation leased to National Cement Company of California, Inc., or National, and the management of water assets and water infrastructure. We continue to look for opportunities to grow our mineral resource revenues through expansion of leasing and encouraging new exploration. The management of our water assets consists of the evaluation of near-term highest and best uses, which can include the sale of water on a temporary basis, the use of water for internal purposes, and the storage of water for future use in our development projects. At the same time we are also evaluating opportunities as they arise for the purchase of additional water assets as we have done in the past.

We receive our royalty interest in cash. Royalty rates are contractually defined and based on a percentage of production and are received in cash. Our royalty revenues fluctuate based on changes in the market prices for oil, natural gas, and rock and aggregate product, the inevitable decline in production of existing wells and quarries, and other factors affecting the third-party oil and natural gas exploration and production companies that operate on our lands including the cost of development and production.

Estimates of oil and gas reserves on our properties are unknown to us. We do not make such estimates, and our lessees do not make information concerning reserves available to us.

We lease certain portions of our land to oil companies for the exploration and production of oil and gas. We however do not engage in any oil exploration or extraction activities. As of December 31, 2020, 10,332 acres were committed to producing oil and gas leases from which the operators produced and sold approximately 114,567 barrels of oil and 207,000 MCF (each MCF being 1,000 cubic feet) of dry gas during 2020. Our share of production, based upon average royalty rates during the last three years, has been 37, 78, and 89 barrels of oil per day for 2020, 2019, and 2018, respectively. There are 313 active oil wells located on the leased land as of December 31, 2020. Royalty rates on our leases averaged approximately 12% of oil production in 2020.

In 2020, social distancing and California's stay-at-home orders reduced the demand for oil and gasoline within California. The average price per barrel of oil, at one point, decreased 25% from their December 31, 2019 levels. Oil pricing decreased as a result of a surplus of oil in the first half of 2020 impacting the production levels of our lessees. The Company believes that pricing will slowly and gradually improve once consumers feel safe and the global economy reopens, fully. However, it is very

difficult to predict when this will occur. Thus far in 2021, the price per barrel of oil is 22% higher than its December 31, 2020 level.

In July 2020, our largest oil royalty tenant, California Resources Corporation, or CRC, filed a voluntary petition for relief under Chapter 11 of the U.S. Bankruptcy Code, intended to allow them to improve their liquidity and debt positions. While in bankruptcy CRC received permission from the courts to allow them to pay lease and oil royalty obligations without interruption. CRC successfully emerged from bankruptcy in October 2020 and is once again being traded on public markets. CRC reduced production in 2020 and we expect as prices improve that we will later in 2021 begin to see increases in production levels. CRC has approved permits and drill sites on our land and has delayed the start of drilling as it evaluates the market. A positive aspect of our lease with CRC is that the approved drill sites are in an area of the ranch where the development and production costs are moderate due to the depths being drilled. CRC is current on all payments due to us through December 31, 2020.

We have approximately 2,000 acres under lease to National, for the purpose of manufacturing Portland cement from limestone deposits found on the leased acreage. National owns and operates a cement manufacturing plant on our property with a capacity of approximately 1,000,000 tons of cement per year. The amount of payment that we receive under the lease is based upon shipments from the cement plant. In 2020, payments increased due to an increase in production caused by an increase in regional construction. The term of this lease expires in 2026, but National has options to extend the term for successive periods of 20 and 19 years. Proceedings under environmental laws relating to the cement plant are in process. The Company is indemnified by the current and former tenants, and at this time, we have no cost related to the issues at the cement plant. See Item 3, “Legal Proceedings,” for a further discussion.

We also lease 521 acres to Granite Construction and Griffith Construction for the mining of rock and aggregate product that is used in construction of roads and bridges. The royalty revenues we receive under these leases are based upon the amount of product produced at these sites.

Water sales opportunities for 2021 will depend on rain and snowfall volume along with California State Water Project, or SWP, allocations. As of December 31, 2020, the 2021 SWP allocation is at 10% of contract amounts.

In August 2015, we entered into a water sale agreement with PEF, our current lessee under a power plant lease. PEF may purchase from us up to 3,500 acre feet of water per year through July 2030, with an option to extend the term. PEF is under no obligation to purchase water from us in any year, but is required to pay us an annual option payment equal to 30% of the maximum annual payment. The price of the water under the agreement is $1,279 per acre-foot of annual water in 2020, subject to 3% annual increases for the duration of the lease agreement. The Company's commitments to sell this water can be met through current water sources.

Farming Operations

In the San Joaquin Valley, we farm permanent crops including the following acreage: wine grapes— 835; almonds—2,281 (1,548 in production and 733 not in production); and pistachios—1,053. We manage the farming of alfalfa and forage mix on 626 acres in the Antelope Valley, and we periodically lease 720 acres of land that is used for the growing of vegetables but also can be used for the development of permanent crops such as almonds.

The Company's agribusiness operations are deemed essential and have been allowed to operate under California's COVID-19 orders. The Company continues to provide its employees with face masks and safety training to promote a safe working environment. As of the December 31, 2020, COVID-19 has not had a measurable impact on the Company's farming operations.

We sell our farm commodities to several commercial buyers. As a producer of these commodities, we are in direct competition with other producers within the United States, or U.S., and throughout the world. Prices we receive for our commodities are determined by total industry production and demand levels. We attempt to improve price margins by producing high quality crops through proven cultural practices and by obtaining better prices through marketing arrangements with handlers.

Nut and grape crop markets are particularly sensitive to the size of each year’s world crop and the demand for those crops. The industry continues to see strong demand for almonds and pistachios but the continued increase in production has begun to negatively impact prices. Crop prices, especially almonds, are also adversely affected by a strong U.S. dollar which makes U.S. exports more expensive and decreases demand for the products we produce. The U.S. dollar weakened against the Chinese Yuan for most of 2020 as a result of the pandemic, making U.S. nut crops more attractive.

Sales of our grape crop typically occur in the third and fourth quarters of the calendar year. Sales of our pistachio and almond crops also typically occur in the third and fourth quarters of the calendar year, but can occur up to a year or more after each crop is harvested. In 2020, we sold 40% of our grape crop to one winery, 38% to a second winery and the remainder to two other

customers. These sales are under contracts ranging from one to eight years. In 2020, our almonds were sold to various commercial buyers, with the largest buyer accounting for 29% of our crop. We sold pistachios to three customers with the largest accounting for 62% of our crop. We do not believe that we would be adversely affected by the loss of any or all of these buyers because of the markets for these commodities, the large number of buyers that would be available to us, and the fact that the prices for these commodities do not vary based on the identity of the buyer or the size of the contract.

For 2020, the almond industry had record production in excess of 3 billion pounds. The Company’s 2020 almond yields saw a small increase over 2019 levels as a result of putting into service two additional almond crop units. The mix of demand has been changed in the near term as a result of COVID-19 as more product is moving through wholesale markets and less through high end users such as restaurants. This temporary trend, along with the strong 2020 industry production, has negatively impacted pricing. Comparatively, the average price per pound for the 2020 almond crop is $2.02 per pound compared to $2.82 per pound for the 2019 almond crop.

Although 2020 was an on production year for pistachios, unfavorable warm winter conditions adversely impacted our pistachio's blooms and yields. Overall 2020 pistachio yields decreased 45% when compared to 2019 which was a down bearing year. In terms of pricing, our 2020 crop is selling for $2.04 per pound compared to $1.98 in 2019. The impact of lower chill hours has impacted pistachio growers in the southern end of the San Joaquin Valley in similar areas as to where we farm and lower production has been seen in these areas. Overall for California, production is up due to 2020 being an on production year and chill hours being greater in growing areas to the north of our lands.

For wine grapes, yields deceased as a result of removing a 313-acre vineyard in 2020. Overall average pricing for wine grapes has increased slightly because the remaining multi-year wine grape sales contracts have an overall higher price.

Weather conditions could impact the number of tree and vine dormant hours, which are integral to tree and vine growth. We will not know the impact of current weather conditions on 2021 production until the early summer of 2021.

At this time the State Department of Water Resources has announced that the estimated water supply for 2021 will be at 10% of full entitlement. This allocation is expected to change based upon winter storms. The current 10% allocation of SWP water alone is not enough for us to farm our crops, but our additional water resources, such as groundwater and surface sources, and those of the water districts we are in, should allow us to have sufficient water for our farming needs. It is too early in the year to determine the impact of 2021 water supplies and its impact on 2021 California crop production for almonds, pistachios, and wine grapes. See discussion of water contract entitlement and long-term outlook for water supply under Item 2, “Properties.” Also see Note 6. (Long-Term Water Assets) of the Notes to Consolidated Financial Statements for additional information regarding our water assets.

Ranch Operations

Ranch operations consist of game management revenues and ancillary land uses such as grazing leases and filming. Within game management, we operate our High Desert Hunt Club, a premier upland bird hunting club. The High Desert Hunt Club offers over 6,400 acres and 35 hunting fields, each field providing different terrain and challenges. The hunting season runs from mid-October through March. We also sell individual hunting packages as well as seasonal hunting memberships.

Approximately 256,000 acres are used for two grazing leases, which account for 43% of total revenues from ranch operations at December 31, 2020.

Ranch operations also includes Hunt at Tejon, which offers a wide variety of guided big game hunts, including trophy Rocky Mountain elk, deer, turkey and wild pig. We offer guided hunts and memberships for both the Spring and Fall hunting seasons. At December 31, 2020, game management accounts for 37% of the total revenue from ranch operations.

In addition, the ranch operations segment is in charge of upkeep, maintenance, and security of all 270,000 acres of land.

General Environmental Regulation

Our operations are subject to federal, state, and local environmental laws and regulations including laws relating to water, air, solid waste, and hazardous substances. Although we believe that we are in material compliance with these requirements, there can be no assurance that we will not incur costs, penalties, and liabilities, including those relating to claims for damages to property or natural resources, resulting from our operations. Environmental liabilities may also arise from claims asserted by adjacent landowners or other third parties. We also expect continued legislation and regulatory development in the area of climate change and greenhouse gases. It is unclear as of this date how any such developments will affect our business. Enactment of new environmental laws or regulations, or changes in existing laws or regulations or the interpretation of these laws or regulations, might require expenditures in the future. We historically have not had material environmental liabilities.

Environmental Sustainability

Environmental stewardship, or sustainability, is one of Tejon Ranch Co.’s core values, along with quality and visionary innovation. This commitment to sustainability manifests itself in many ways across the Company and its operations.

Climate Change

The Company maintains policies intended to both reduce its carbon footprint and proactively sequester, or capture and store, carbon.

•Since 2008, the Company has voluntarily conserved 240,000 acres of its land covered by trees and other vegetation. A recent analysis conducted for the Company by Dudek Environmental Service s determined that this acreage effectively sequesters 3.3 million tons of carbon. That equals the volume of carbon produced in a single year by 2.5 million passenger vehicles-10% of California’s 2019 passenger vehicle fleet.

•Solar power is used significantly within TRCC. For example, in 2019 the Company installed a solar covered parking structure at the Outlets at Tejon. The structure covers 1.85 acres and is projected to offset 83% of the center’s electricity needs for shared spaces and produce 1,076,000 kWh of clean energy every year. In addition, the IKEA distribution center at TRCC features a 1.8 MW photovoltaic solar array covering 370,000 square feet of the warehouse’s rooftop. The system handles the power needs of IKEA’s distribution center and provides power into the electric grid as well.

•The Company has entered into a lease with Calpine Energy, a power generating company, for the development of a 600-acre industrial-sized solar field. Located immediately adjacent to Calpine’s PEF, a natural gas and steam powered generating plant in the San Joaquin Valley portion of the Ranch, the solar array is expected to produce approximately 100 MW of power once fully operational.

•The Company’s three master planned mixed-use residential communities are also designed to make use of renewable energy sources:

◦At Grapevine, 50% or more of its energy supply will be produced on site by renewable sources.

◦All homes in Mountain Village will feature roof-top photovoltaic solar arrays.

◦At Centennial, like Grapevine, at least 50% of the energy supply will be produced by on-site renewable sources.

Air Quality

•The Company has contracted with the San Joaquin Valley Unified Air Pollution Control District (“SJVUAPCD”) to pre-mitigate air emissions related to the Company’s current development at TRCC-East and future development at Mountain Village and Grapevine. As of 2020, the SJVUAPCD had fully offset current air emissions at TRCC-East, as well as future emissions projected to occur at full build-out of the project.

•Nearly two decades ago, the Company helped establish and has continuously supported Valley Clean Air Now (“VCAN”), a non-profit, 501(c)(3) public charity that advances quantifiable and voluntary solutions addressing air pollution in California’s San Joaquin Valley, a region with some of the worst air quality and highest poverty levels in the United States. The Company continues to support VCAN in its mission to improve public health and quality of life in disadvantaged communities located in the region.

◦VCAN’s programs deliver $850 smog repair vouchers and $9,500 in down payment incentives to low-income residents in the region so they can replace high-polluting vehicles with used plug-in or hybrid cars.

◦In the past five years, VCAN has helped more than 35,000 households improve their vehicle emissions by completing over 20,000 smog repairs and providing more than 26,000 smog repair vouchers. Additionally, VCAN’s vehicle replacement program has delivered more than 2,000 plug-in electric vehicles. Based on pre- and post-repair emission capture readings, VCAN’s vehicle repair and replacement work has generated 692 tons of oxides of nitrogen (also known as “NOx”), 71 tons of carbon monoxide, and 90 tons of hydro-carbon emission reductions.

Water Conservation

•At TRCC-East, all water used for irrigation purposes is reclaimed water from the water treatment plant. Landscaping at the Outlets at Tejon consists of drought-tolerant, native planting material.

•Each of the Company’s master planned mixed-use residential communities will feature state-of-the-art water conservation measures, reclaimed water for irrigation, stormwater capture, and drought-tolerant landscaping.

•The Company’s agricultural operations use highly efficient drip irrigation to water its orchards and vineyards.

Customers

During 2020, our PEF power plant lease accounted for 12% of total revenues. In both 2019 and 2018, the PEF power plant lease generated 9% of our total revenues. No other customer represents 5% or more of our revenues in 2020 and 2018.

Organization

Tejon Ranch Co. is a Delaware corporation incorporated in 1987 to succeed the business operated as a California corporation since 1936.

Employees

At December 31, 2020, we had 85 full-time employees. We believe that we have good relations with our employees. We have adopted a Compliance with State and Federal Statutes, Rules and Regulations Reporting Policy that applies to all of our employees. Its receipt and review by each employee is documented and verified quarterly. None of our employees are covered by a collective bargaining agreement.

Reports

We make available free of charge through our Internet website, www.tejonranch.com, our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to these reports filed or to be furnished pursuant to Section 13(a) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after we electronically file such material with or furnish it to the SEC. We also make available on our website our corporate governance guidelines, charters of our Board of Directors’ Committees (audit, compensation, nominating and corporate governance, and real estate), and our Code of Business Conduct and Ethics for Directors, Officers, and Employees. These items are also available in printed copy upon request. We intend to disclose in the future any amendments to our Code of Business Conduct and Ethics for Directors, Officers, and Employees, or waivers of such provisions granted to executive officers and directors, on the web site within four business days following the date of such amendment or waiver. Any document we file with the Securities and Exchange Commission, or SEC, may be inspected, without charge, at the SEC’s website: http://www.sec.gov.

Information about our Executive Officers

The following table shows each of our executive officers and the offices held as of March 3, 2021, the period the offices have been held, and the age of the executive officer.

| | | | | | | | | | | | | | | | | | | | |

| Name | | Office | | Held since | | Age |

| Gregory S. Bielli | | President and Chief Executive Officer, Director | | 2013 | | 60 |

| Allen E. Lyda | | Executive Vice President and Chief Operating Officer | | 2019 | | 63 |

| Hugh McMahon | | Executive Vice President, Real Estate | | 2014 | | 54 |

| Robert D. Velasquez | | Senior Vice President, Chief Financial Officer | | 2019 | | 54 |

A description of present and prior positions with us, and business experience is given below.

Mr. Bielli has been employed by the Company since September 2013. Mr. Bielli joined the Company as President and Chief Operating Officer and became President and Chief Executive Officer on December 17, 2013. Prior to joining the Company, Mr. Bielli was President of Newland Communities' Western Region, a diversified real estate company, and was responsible for overseeing management of all operational aspects of Newland's real estate projects in the region. Mr. Bielli worked with Newland Communities from 2006 through August 2013.

Mr. Lyda has been employed by us since 1990, initially serving as Vice President, Finance and Treasurer. He was elected Assistant Secretary in 1995 and Chief Financial Officer in 1999. Mr. Lyda was promoted to Senior Vice President in 2008, and Executive Vice President in 2012. Mr. Lyda's title was subsequently changed in 2013 to Executive Vice President and Chief Financial Officer to more accurately describe the responsibilities of his office. On January 1, 2019, he was appointed to the role of Chief Operating Officer and ceased serving as the Company's Chief Financial Officer.

Mr. McMahon joined the Company in November 2001 as Director of Financial Analysis. In 2008, Mr. McMahon became Vice President of Commercial/Industrial Development and in December of 2014, was promoted to Senior Vice President of Commercial/Industrial Development and elected as an officer of the Company. In 2015, he was promoted to Executive Vice President. Mr. McMahon's title was subsequently changed to Executive Vice President, Real Estate.

Mr. Velasquez joined the Company as Vice President of Finance in 2014. Mr. Velasquez's title was subsequently changed, in 2015, to Vice President of Finance and Chief Accounting Officer to more accurately describe the responsibilities of his office. Prior to joining the Company, Mr. Velasquez served as an Executive Director at Ernst & Young in their audit and assurance practice section. Mr. Velasquez worked with Ernst & Young from 1999 through 2014. Mr. Velasquez holds a B.S. in Business Administration – Option: Accounting from California State University, Los Angeles. Mr. Velasquez is a Certified Public Accountant in the state of California. On January 1, 2018 he was promoted to Senior Vice President, Finance and Chief Accounting Officer. On January 1, 2019, he was appointed Chief Financial Officer.

ITEM 1A. RISK FACTORS

The risks and uncertainties described below are not the only ones facing the Company. If any of the following risks occur, our business, financial condition, results of operations or future prospects could be materially adversely affected. Our strategy, focused on more aggressive development of our land, involves significant risk and could result in operating losses. The risks that we describe in our public filings are not the only risks that we face. Additional risks and uncertainties not presently known to us, or that we currently consider immaterial, also may materially adversely affect our business, financial condition, and results of operations. In addition, to the effects of the COVID-19 pandemic and resulting global disruptions on our business and operations discussed in Item 7 of this Form 10-K and in the risk factors below, additional or unforeseen effects from the pandemic and the global economic climate may give rise to or amplify many of these risks discussed below.

STRATEGIC RISKS

Strategic risk relates to the Company's future business plans and strategies, including the risks associated with the macro- and micro- environment in which we operate, including the demand for our products and services, the success of investments in our real estate development, technology and public policy.

Adverse changes in economic conditions in markets where we conduct our operations and where prospective purchasers of our future homes and commercial products live could reduce the demand for our products and, as a result, could adversely affect our business, results of operations, and financial condition. Adverse changes in economic conditions in markets where we conduct our operations and where prospective purchasers of our real estate products live have had and may in the future have a negative impact on our business. Adverse changes in employment levels, job growth, consumer confidence, interest rates, and population growth, or an oversupply of product for sale or lease may reduce demand and depress prices and cause buyers to cancel their purchase agreements. This, in turn, could adversely affect our results of operations and financial condition.

Higher interest rates and lack of available financing can have significant impacts on the real estate industry. Higher interest rates generally impact the real estate industry by making it harder for buyers to qualify for financing, which can lead to a decrease in the demand for residential, commercial or industrial sites. Any decrease in demand will negatively impact our proposed developments. Lack of available credit to finance real estate purchases can also negatively impact demand. Any downturn in the economy or consumer confidence can also be expected to result in reduced housing demand and slower industrial development, which would negatively impact the demand for land we are developing.

We are subject to various land use regulations and require governmental approvals and permits for our developments that could be denied. In planning and developing our land, we are subject to various local, state, and federal statutes, ordinances, rules and regulations concerning zoning, infrastructure design, subdivision of land, and construction. All of our new developments require amending existing general plan and zoning designations, so it is possible that our entitlement applications could be denied. In addition, the zoning that ultimately is approved could include density provisions that would limit the number of homes and other structures that could be built within the boundaries of a particular area, which could adversely impact the financial returns from a given project. Many states, cities and counties (including neighboring Ventura County) have in the past approved various “slow growth” or “urban limit line” measures. If that were to occur in the jurisdictions governing the Company’s land use, our future real estate development activities could be significantly adversely affected.

Third-party litigation could increase the time and cost of our development efforts. The land use approval processes we must follow to ultimately develop our projects have become increasingly complex. Moreover, the statutes, regulations and ordinances governing the approval processes provide third parties the opportunity to challenge the proposed plans and approvals. As a result, the prospect of third-party challenges to planned real estate developments provides additional uncertainties in real estate development planning and entitlements. Third-party challenges in the form of litigation could result in denial of the right to develop, or would, by their nature, adversely affect the length of time and the cost required to obtain the necessary approvals. In addition, adverse decisions arising from any litigation would increase the costs and length of time to obtain ultimate approval of a project and could adversely affect the design, scope, plans and profitability of a project.

We are subject to environmental regulations and opposition from environmental groups that could cause delays and increase the costs of our development efforts or preclude such development entirely. Environmental laws that apply to a given site can vary greatly according to the site’s location and condition, present and former uses of the site, and the presence or absence of sensitive elements like wetlands and endangered species. Federal and state environmental laws also govern the construction and operation of our projects and require compliance with various environmental regulations, including analysis of the environmental impact of our projects and evaluation of our reduction in the projects’ carbon footprint and greenhouse gas emissions. Environmental laws and conditions may result in delays, cause us to incur additional costs for compliance, mitigation and processing land use applications, or preclude development in specific areas. In addition, in California, third parties have the ability to file litigation challenging the approval of a project which they usually do by alleging inadequate disclosure and mitigation of the environmental impacts of the project. Certain groups opposed to development have made clear they intend to oppose our projects vigorously, so litigation challenging their approval is expected. Currently, the Centennial entitlement approval has been opposed through litigation against the Company and Los Angeles County. At Grapevine, the issues most commonly cited in opponents’ public comments include the poor air quality of the San Joaquin Valley air basin, potential impacts of projects on the California condor and other species of concern, the potential for our lands to function as wildlife movement corridors, potential impacts of our projects on traffic and air quality in Los Angeles County, emissions of greenhouse gases, water availability and criticism of proposed development in rural areas as being “sprawl.” In addition, California has a specific statutory and regulatory scheme intended to reduce greenhouse gas emissions in the state and efforts to enact federal legislation to address climate change concerns could require further reductions in our projects’ carbon footprint in the future.

Until final permits are received, litigation is complete, and final maps are received, we will have a limited inventory of real estate. Each of our four current and planned real estate projects, TRCC, Centennial, MV, and Grapevine involve obtaining various governmental agency permits, overcoming litigation, and receiving final maps from local jurisdictions. A delay in achieving these items could lead to additional costs related to these developments and potentially lost opportunities for the sale of lots to developers and land users.

We are in competition with several other developments for customers and residents. Within our real estate activities, we are in direct competition for customers with other industrial sites in Northern, Central, and Southern California. We are also in competition with other highway interchange locations using Interstate 5 and State Route 99 for commercial leasing opportunities. Once they receive all necessary permits and approvals, Centennial and Grapevine will ultimately compete with other residential housing options in the region, such as developments in the Santa Clarita Valley, Lancaster, Palmdale, and Bakersfield. MV will compete generally for discretionary dollars that consumers will allocate to recreation and second homes, so its competition will include a greater area and range of projects. Intense competition may decrease our sales and harm our results of operations.

Increases in taxes or government fees could increase our cost, and adverse changes in tax laws could reduce demand for homes in our future residential communities. Increases in real estate taxes and other local government fees, such as fees imposed on developers to fund schools, open space, and road improvements, could increase our costs and have an adverse effect on our operations. In addition, any changes to income tax laws that would reduce or eliminate tax deductions or incentives to homeowners, such as a change limiting the deductibility of real estate taxes or interest on home mortgages, could make housing less affordable or otherwise reduce the demand for housing, which in turn could reduce future sales.

Our developable land is concentrated entirely in California. All of our developable land is in California and our business is especially sensitive to the economic conditions within California. Any adverse change in the economic climate of California, or our regions of that state, and any adverse change in the political or regulatory climate of California, or the counties where our land is located could adversely affect our real estate development activities. Ultimately, our ability to sell or lease lots may decline as a result of weak economic conditions or restrictive regulations.