UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

[ü] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2009 |

| OR | |

[ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from __________ to __________. |

Commission File Number 001-16191

TENNANT COMPANY

(Exact name of registrant as specified in its charter)

| Minnesota | | 41-0572550 |

| State or other jurisdiction of | | (I.R.S. Employer |

| incorporation or organization | | Identification No.) |

701 North Lilac Drive, P.O. Box 1452 Minneapolis, Minnesota 55440 |

| (Address of principal executive offices) (Zip Code) |

Registrant’s telephone number, including area code 763-540-1200

Securities registered pursuant to Section 12(b) of the Act:

| | Name of exchange on which registered |

| Common Stock, par value $0.375 per share | | New York Stock Exchange |

| Preferred Share Purchase Rights | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None |

| | | | | |

| Indicate by check mark if the registrant is a well-known seasoned issuer, as defined by Rule 405 of the Securities Act. | | Yes | ü | No |

| Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. | | Yes | ü | No |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months |

(or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | ü | Yes | | No |

| Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and |

| posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit | |

| and post such files). | | Yes | | No |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ü ] |

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one): |

| Large accelerated filer | | | Accelerated filer | ü | |

| Non-accelerated filer | | (Do not check if a smaller reporting company) | Smaller reporting company | | |

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). | | Yes | ü | No |

| The aggregate market value of the voting and non-voting common equity held by non-affiliates as of June 30, 2009, was approximately $339,083,805. |

| As of February 24, 2010, there were 18,800,981 shares of Common Stock outstanding. |

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement for its 2010 annual meeting of shareholders (the “2010 Proxy Statement”) are incorporated by reference in Part III.

Tennant Company

Form 10–K

| PART I | | | | | Page |

| | Item 1 | | | | |

| | Item 1A | | |

| | Item 1B | | |

| | Item 2 | | | | |

| | Item 3 | | |

| | Item 4 | | |

| | | | | | | |

| PART II | | | | | |

| | Item 5 | | |

| | Item 6 | | |

| | Item 7 | | |

| | Item 7A | | |

| | Item 8 | | |

| | | | | |

| | | | | |

| | | | | |

| | | | 1 | | | |

| | | | 2 | | | |

| | | | 3 | | | |

| | | | 4 | | | |

| | | | 5 | | | |

| | | | 6 | | | |

| | | | 7 | | | |

| | | | 8 | | | |

| | | | 9 | | | |

| | | | 10 | | | |

| | | | 11 | | | |

| | | | 12 | | | |

| | | | 13 | | | |

| | | | 14 | | | |

| | | | 15 | | | |

| | | | 16 | | | |

| | | | 17 | | | |

| | | | 18 | | | |

| | | | 19 | | | |

| | | | 20 | | | |

| | Item 9 | | |

| | Item 9A | | |

| | Item 9B | | |

| | | | | | | |

| PART III | | | | | |

| | Item 10 | | |

| | Item 11 | | |

| | Item 12 | | |

| | Item 13 | | |

| | Item 14 | | |

| PART IV | | | | | |

| | Item 15 | | |

| | | | | | | |

TENNANT COMPANY

2009

ANNUAL REPORT

Form 10–K

(Pursuant to Securities Exchange Act of 1934)

PART I

General Development of Business

Tennant Company, a Minnesota corporation incorporated in 1909, is a world leader in designing, manufacturing and marketing solutions that help create a cleaner, safer world. The Company’s floor maintenance and outdoor cleaning equipment, chemical-free cleaning technologies, specialty surface coatings and related products are used to clean and coat surfaces in factories, office buildings, parking lots and streets, airports, hospitals, schools, warehouses, shopping centers and more. Customers include building service contract cleaners to whom organizations outsource facilities maintenance, as well as end-user businesses, healthcare facilities, schools and local, state and federal governments who handle facilities maintenance themselves. We reach these customers through the industry’s largest direct sales and service organization and through a strong and well-supported network of authorized distributors worldwide.

Industry Segments, Foreign and Domestic Operations and Export Sales

The Company has one reportable business segment. The Company sells its products domestically and internationally. Financial information on the Company’s geographic areas is provided in Note 18, Segment Reporting. Nearly all of the Company’s foreign investments in assets reside within The Netherlands, Australia, the United Kingdom, France, Germany, Canada, Austria, Japan, Spain, Brazil and China.

Principal Products, Markets and Distribution

The Company offers products and solutions mainly consisting of motorized cleaning equipment targeted at commercial and industrial markets; parts, consumables and service maintenance and repair; business solutions such as pay-for-use offerings, rental and leasing programs; and technologies such as chemical-free cleaning technologies that enhance the performance of Tennant cleaning equipment. Adjacent products include specialty surface coatings and floor preservation products. In 2009, the Company launched its S20, a compact sweeper, and extended the availability of its proprietary electrically converted water technology (“ec-water”), which cleans without chemicals, to five rider scrubber machines. In addition, the Company licensed this technology for use in a hand-held spray bottle for commercial and consumer cleaning applications. The Company’s products are sold through direct and distribution channels in various regions around the world. In North America, products are sold through a direct sales organization and independent distributors; in Australia, Japan and many countries principally in Western Europe, products are sold primarily through direct sales organizations; and in more than 80 other countries, Tennant relies on a broad network of independent distributors.

Raw Materials and Purchased Components

The Company has not experienced any significant or unusual problems in the availability of raw materials or other product components. The Company has sole-source vendors for certain components. A disruption in supply from such vendors may disrupt the Company’s operations. However, the Company believes that it can find alternate sources in the event there is a disruption in supply from such vendors.

Patents and Trademarks

The Company applies for and is granted United States and foreign patents and trademarks in the ordinary course of business, none of which is of material importance in relation to the business as a whole.

Seasonality

Although the Company’s business is not seasonal in the traditional sense, historically revenues and earnings have been more concentrated in the fourth quarter of each year reflecting the tendency of customers to increase capital spending during such quarter and the Company’s efforts to close orders and reduce order backlogs. In addition, the Company offers annual distributor rebates and sales commissions which tend to drive sales in the fourth quarter. Typical seasonality did not occur in the 2008 fourth quarter due to the deterioration of the worldwide economy and global credit crisis. Typical seasonality also did not occur during 2009. The Company’s focus and accomplishment during 2009 was to increase sales sequentially each quarter beginning with the increase from the 2009 first quarter to the 2009 second quarter.

Working Capital

The Company funds operations through a combination of cash and cash equivalents and cash flows from operations. Wherever possible, cash management is centralized and intercompany financing is used to provide working capital to subsidiaries as needed. In addition, credit facilities are available for additional working capital needs or investment opportunities.

Major Customers

The Company sells its products to a wide variety of customers, none of which is of material importance in relation to the business as a whole. The customer base includes several governmental entities; however, these customers generally have terms similar to other customers.

Backlog

The Company processes orders within two weeks on average. Therefore, no significant backlogs existed at December 31, 2009 or December 31, 2008.

Competition

While there is no industry association or industry data, the Company believes, through its own market research, that it is a world-leading manufacturer of floor maintenance and cleaning equipment. Significant competitors exist in all key geographic regions. However, the key competitors vary by region. The Company competes primarily on the basis of offering a broad line of high-quality; innovative products supported by an extensive sales and service network in major markets.

Product Research and Development

The Company strives to be an industry leader in innovation and is committed to investing in research and development. The Company’s Global Innovation Center is dedicated to various activities including development of new products and technologies, improvements of existing product design or manufacturing processes and new product applications. In 2009, 2008 and 2007, the Company spent $23.0 million, $24.3 million and $23.9 million on research and development, respectively.

Environmental Protection

Compliance with federal, state and local provisions regulating the discharge of materials into the environment, or otherwise relating to the protection of the environment, has not had, and the Company does not expect it to have, a material effect upon the Company’s capital expenditures, earnings or competitive position.

Employment

The Company employed 2,786 people in worldwide operations as of December 31, 2009.

Access to Information on the Company’s Website

The Company makes available free of charge, through the Company’s website at www.tennantco.com, its Annual Reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or Section 15(d) of the Exchange Act simultaneously when such reports are filed electronically with, or furnished to, the Securities and Exchange Commission (“SEC”).

The following are significant factors known to us that could materially adversely affect our business, financial condition, or operating results.

We may encounter additional financial difficulties if the United States or other global economies continue to experience a significant long-term economic downturn, decreasing the demand for our products.

To the extent that the U.S. and other global economies experience a continued significant long-term economic downturn, our revenues could decline to the point that we may have to take additional cost saving measures to reduce our fixed costs to a level that is in line with a lower level of sales in order to stay in business long-term in a depressed economic environment. Our product sales are sensitive to declines in capital spending by our customers. Decreased demand for our products could result in decreased revenues, profitability and cash flows and may impair our ability to maintain our operations and fund our obligations to others.

We may not be able to effectively manage organizational changes which could negatively impact our operating results or financial condition.

We are continuing to integrate acquired companies into our business and adjust to reduced staffing levels as a result of our workforce reduction. This consolidation and reallocation of resources is part of our ongoing efforts to optimize our cost structure in the current economy. Our operating results may be negatively impacted if we are unable to manage these organizational changes either by failing to incorporate new employees from acquired businesses or failing to assimilate the work of the positions that are eliminated as part of our actions to reduce headcount. In addition, if we do not effectively manage the transition of our reduced headcount, we may not fully realize the anticipated savings of these actions or they may negatively impact our ability to serve our customers or meet our strategic objectives.

We may not be able to effectively optimize the allocation of Company resources to our strategic objectives, which could adversely affect our operating results.

The decline in the global economy has constrained resources that are available to allocate among strategic business objectives. If we are not able to appropriately prioritize our objectives, we risk allocating our resources to projects that do not accomplish our strategic objectives most effectively, which could result in increased costs and could adversely impact our operating results.

We are subject to competitive risks associated with developing innovative products and technologies, which generally cost more than our competitors’ products.

Our products are sold in competitive markets throughout the world. Competition is based on product features and design, brand recognition, reliability, durability, technology, breadth of product offerings, price, customer relationships, and after-sale service. Although we believe that the performance and price characteristics of our products will provide competitive solutions for our customers’ needs, because of our dedication to innovation and continued investments in research and development, our products generally cost more than our competitor’s products. We believe that customers will pay for the innovation and quality in our products; however, in the current economic environment, it may be difficult for us to compete with lower cost products offered by our competitors and there can be no assurance that our customers will continue to choose our products over products offered by our competitors. If our products, markets and services are not competitive, we may experience a decline in sales, pricing, and market share, which adversely impacts revenues, margin, and the success of our operations.

We may not be able to adequately acquire, retain and protect our proprietary intellectual property rights which could put us at a competitive disadvantage.

We rely on trade secret, copyright, trademark and patent laws and contractual protections to protect our proprietary technology and other proprietary rights. Our competitors may attempt to copy our products or gain access to our trade secrets. Our efforts to secure patent protection on our inventions may be unsuccessful. Notwithstanding the precautions we take to protect our intellectual property rights, it is possible that third parties may illegally copy or otherwise obtain and use our proprietary technology without our consent. Any litigation concerning infringement could result in substantial cost to us and diversions of our resources, either of which could adversely affect our business. In some cases, there may be no effective legal recourse against duplication of products or services by competitors. Intellectual property rights in foreign jurisdictions may be limited or unavailable. Patents of third parties also have an important bearing on our ability to offer some of our products and services. Our competitors may obtain patents related to the types of products and services we offer or plan to offer. Any infringement by us on intellectual property rights of others could result in litigation and adversely affect our ability to continue to provide, or could increase the cost of providing, our products and services.

We may encounter difficulties as we invest in changes to our processes and computer systems that are foundational to our ability to maintain and manage our systems data.

We rely on our computer systems to effectively manage our business, serve our customers and report financial data. Our current systems are adequate for our current business operations; however, we are in the process of standardizing our processes and the way we utilize our computer systems with the objective that we will improve our ability to effectively maintain and manage our systems data so that as our business grows, our processes will be able to more efficiently handle this growth. There are inherent risks in changing processes and systems data and if we are not successful in our attempts to improve our data and system processes, we may experience higher costs or an interruption in our business which could adversely impact our ability to serve our customers and our operating results.

We may be unable to conduct business if we experience a significant business interruption in our computer systems, manufacturing plants or distribution facilities for a significant period of time.

We rely on our computer systems, manufacturing plants and distribution facilities to efficiently operate our business. If we experience an interruption in the functionality in any of these items for a significant period of time, we may not have adequate business continuity planning contingencies in place to allow us to continue our normal business operations on a long-term basis. Significant long-term interruption in our business could cause a decline in sales, an increase in expenses and could adversely impact our operating results.

We are subject to product liability claims and product quality issues that could adversely affect our operating results or financial condition.

Our business exposes us to potential product liability risks that are inherent in the design, manufacturing and distribution of our products. If products are used incorrectly by our customers, injury may result leading to product liability claims against us. Some of our products or product improvements may have defects or risks that we have not yet identified that may give rise to product quality issues, liability and warranty claims. If product liability claims are brought against us for damages that are in excess of our insurance coverage or for uninsured liabilities and it is determined we are liable, our business could be adversely impacted. Any losses we suffer from any liability claims, and the effect that any product liability litigation may have upon the reputation and marketability of our products, may have a negative impact on our business and operating results. We could experience a material design or manufacturing failure in our products, a quality system failure, other safety issues, or heightened regulatory scrutiny that could warrant a recall of some of our products. Any unforeseen product quality problems could result in loss of market share, reduced sales, and higher warranty expense.

We may encounter difficulties obtaining raw materials or component parts needed to manufacture our products and the prices of these materials are subject to fluctuation.

Raw materials and commodity-based components. As a manufacturer, our sales and profitability are dependent upon availability and cost of raw materials, which are subject to price fluctuations, and the ability to control or pass on an increase in costs of raw materials to our customers. We purchase raw materials, such as steel, rubber, lead and petroleum-based resins and components containing these commodities for use in our manufacturing operations. The availability of these raw materials is subject to market forces beyond our control. Under normal circumstances, these materials are generally available on the open market from a variety of sources. From time to time, however, the prices and availability of these raw materials and components fluctuate due to global market demands, which could impair our ability to procure necessary materials, or increase the cost of such materials. Inflationary and other increases in the costs of these raw materials and components have occurred in the past and may recur from time to time, and our financial performance depends in part on our ability to incorporate changes in costs into the selling prices for our products.

Freight costs associated with shipping and receiving product and sales and service vehicle fuel costs are impacted by fluctuations in the cost of oil and gas. We do not use derivative commodity instruments to manage our exposure to changes in commodity prices such as steel, oil, gas and lead. Any fluctuations in the supply or prices for any of these commodities could have a material adverse affect on our profit margins and financial condition.

Single-source supply. We depend on many suppliers for the necessary parts to manufacture our products. However, there are some components that are purchased from a single supplier due to price, quality, technology or other business constraints. These components cannot be quickly or inexpensively re-sourced to another supplier. If we are unable to purchase on acceptable terms or experience significant delays or quality issues in the delivery of these necessary parts or components from a particular vendor and we need to locate a new supplier for these parts and components, shipments for products impacted could be delayed, which could have a material adverse affect on our business, financial condition and results of operations.

We are subject to a number of regulatory and legal risks associated with doing business in the United States and international markets.

Our business and our products are subject to a wide range of international, federal, state and local laws, rules and regulations, including, but not limited to, data privacy laws, anti-trust regulations, employment laws, product labeling and regulatory requirements, and the Foreign Corrupt Practices Act and similar anti-bribery regulations. Many of these requirements are challenging to comply with as there are frequent changes and many inconsistencies across the various jurisdictions. Any violation of these laws or regulations could lead to significant fines and/or penalties could limit our ability to conduct business in those jurisdictions and could cause us to incur additional operating and compliance costs.

We are subject to risks associated with changes in foreign currency exchange rates.

We are exposed to market risks from changes in foreign currency exchange rates. As a result of our increasing international presence, we have experienced an increase in transactions and balances denominated in currencies other than the U.S. dollar. There is a direct financial impact of foreign currency exchange when translating profits from local currencies to U.S. dollars. Our primary exposure is to transactions denominated in the Euro, British pound, Australian and Canadian dollar, Japanese yen, Chinese yuan and Brazilian real. Any significant change in the value of the currencies of the countries in which we do business against the U.S. dollar could affect our ability to sell products competitively and control our cost structure. Because a substantial portion of our products are manufactured in the United States, a stronger U.S. dollar generally has a negative impact on results from operations outside the United States while a weaker dollar generally has a positive effect. Unfavorable changes in exchange rates between the U.S. dollar and these currencies impact the cost of our products sold internationally and could significantly reduce our reported sales and earnings. We periodically enter into contracts, principally forward exchange contracts, to protect the value of certain of our foreign currency-denominated assets and liabilities. The gains and losses on these contracts generally approximate changes in the value of the related assets and liabilities. However, all foreign currency exposures cannot be fully hedged, and there can be no assurances that our future results of operations will not be adversely affected by currency fluctuation.

ITEM 1B – Unresolved Staff Comments

None.

The Company’s corporate offices are owned by the Company and are located in the Minneapolis, Minnesota, metropolitan area. Manufacturing facilities are located in the states of Minnesota, Michigan, Kentucky and in Uden, The Netherlands; the United Kingdom; São Paulo, Brazil; and Shanghai, China. Sales offices, warehouse and storage facilities are leased in various locations in North America, Europe, Japan, China, Asia, Australia and Latin America. The Company’s facilities are in good operating condition, suitable for their respective uses and adequate for current needs. Further information regarding the Company’s property and lease commitments is included in the Contractual Obligations section of Item 7 and in Note 13, Commitments and Contingencies.

There are no material pending legal proceedings other than ordinary routine litigation incidental to the Company’s business.

ITEM 4 – Submission of Matters to a Vote of Security Holders

No matters were submitted to a vote of security holders during the fourth quarter of 2009.

PART II

ITEM 5 – Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities

STOCK MARKET INFORMATION – Tennant common stock is traded on the New York Stock Exchange, under the ticker symbol TNC. As of January 29, 2010, there were approximately 500 shareholders of record and 4,400 beneficial shareholders. The common stock price was $23.93 per share on January 29, 2010.

STOCK SPLIT – On April 26, 2006, the Board of Directors declared a two-for-one common stock split effective July 26, 2006. As a result of the stock split, shareholders of record received one additional common share for every share held at the close of business on July 12, 2006. All share and per share data has been retroactively adjusted to reflect the stock split.

QUARTERLY PRICE RANGE – The accompanying chart shows the quarterly price range of the Company’s shares over the past two years:

| | First | | Second | | Third | | Fourth |

| 2009 | $7.76-16.41 | | $9.89-21.26 | | $15.79-30.79 | | $26.16-31.92 |

| 2008 | $31.88-45.41 | | $30.07-41.00 | | $24.90-40.48 | | $15.33-33.26 |

DIVIDEND INFORMATION – Cash dividends on Tennant’s common stock have been paid for 65 consecutive years. Tennant’s annual cash dividend payout increased for the 38th consecutive year to $0.53 per share in 2009, an increase of $0.01 per share over 2008. Dividends generally are declared each quarter. The Company announced a quarterly cash dividend of $0.14 per share payable March 15, 2010, to shareholders of record on February 26, 2010. Following are the anticipated remaining record dates for 2010: June 15, 2010, September 15, 2010 and December 15, 2010.

DIVIDEND REINVESTMENT OR DIRECT DEPOSIT OPTIONS – Shareholders have the option of reinvesting quarterly dividends in additional shares of Company stock or having dividends deposited directly to a bank account. The Transfer Agent should be contacted for additional information.

TRANSFER AGENT AND REGISTRAR – Shareholders with a change of address or questions about their account may contact:

Wells Fargo Bank, N.A.

Shareowner Services

P.O. Box 64854

South St. Paul, MN 55164-0854

(800) 468-9716

SHARE REPURCHASES – On May 3, 2007, the Board of Directors authorized the repurchase of 1,000,000 shares of our common stock. Share repurchases are made from time to time in the open market or through privately negotiated transactions, primarily to offset the dilutive effect of shares issued through our stock-based compensation programs. In order to preserve cash, we had temporarily suspended these repurchases effective September 2008. Our March 4, 2009 amendment to our Credit Agreement prohibited us from conducting share repurchases during the 2009 fiscal year and limits the payment of dividends and repurchases of stock in fiscal years after 2009 to an amount ranging from $12.0 million to $40.0 million based on our leverage ratio after giving effect to such payments.

For the Quarter Ended December 31, 2009 | Total Number of Shares Purchased (1) | Average Price Paid Per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs |

| October 1–31, 2009 | | 33 | | $ 29.03 | | - | | | 288,874 |

| November 1–30, 2009 | - | | - | | - | | | 288,874 |

| December 1–31, 2009 | 988 | | 26.82 | | - | | | 288,874 |

| Total | | 1,021 | | $ 26.89 | | - | | | 288,874 |

(1) Includes 1,021 shares delivered or attested to in satisfaction of the exercise price and/or tax withholding obligations by employees who exercised stock options or restricted stock under employee stock compensation plans.

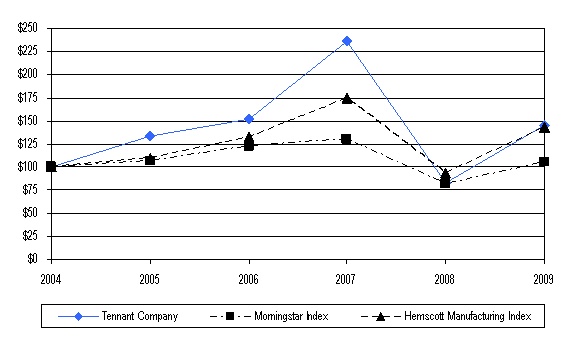

COMPARATIVE STOCK PERFORMANCE – The following graph compares the cumulative total shareholder return on the common stock of the Company for the last five fiscal years with the cumulative total return over the same period on the Overall Stock Market Performance Index (Morningstar Index) and the Industry Index (Hemscott Group Index 62 – Industrial Goods, Manufacturing).

This assumes an investment of $100 in the Company’s common stock, the Morningstar Index and the Hemscott Group Index on December 31, 2004, with reinvestment of all dividends.

COMPARISON OF 5-YEAR CUMULATIVE TOTAL RETURN

AMONG TENNANT COMPANY

MORNINGSTAR INDEX AND HEMSCOTT GROUP INDEX

| | | 2004 | | | 2005 | | | 2006 | | | 2007 | | | 2008 | | | 2009 | |

| Tennant Company | | | 100.00 | | | | 134.05 | | | | 152.19 | | | | 235.51 | | | | 83.28 | | | | 146.00 | |

| Morningstar Index | | | 100.00 | | | | 106.52 | | | | 123.24 | | | | 130.53 | | | | 82.19 | | | | 105.58 | |

| Hemscott Manufacturing Index | | | 100.00 | | | | 110.13 | | | | 132.56 | | | | 174.13 | | | | 94.15 | | | | 143.81 | |

ITEM 6 – Selected Financial Data (In thousands, except shares and per share data)

| Years Ended December 31 | | 2009 | | | 2008 | | | 2007 | | | 2006 | | | 2005 | |

| Year End Financial Results | | | | | | | | | | | | | | | |

| Net Sales | | $ | 595,875 | | | | 701,405 | | | | 664,218 | | | | 598,981 | | | | 552,908 | |

| Cost of Sales | | $ | 349,767 | | | | 415,155 | | | | 385,234 | | | | 347,402 | | | | 318,044 | |

| Gross Margin – % | | | 41.3 | | | | 40.8 | | | | 42.0 | | | | 42.0 | | | | 42.5 | |

| Research and Development Expense | | $ | 22,978 | | | | 24,296 | | | | 23,869 | | | | 21,939 | | | | 19,351 | |

| % of Net Sales | | | 3.9 | | | | 3.5 | | | | 3.6 | | | | 3.7 | | | | 3.5 | |

| Selling and Administrative Expense | | $ | 245,623 | (1) | | | 243,385 | (2) | | | 200,270 | (3) | | | 189,676 | | | | 180,676 | |

| % of Net Sales | | | 41.2 | | | | 34.7 | | | | 30.2 | | | | 31.7 | | | | 32.7 | |

| (Loss) Profit from Operations | | $ | (22,493 | ) (1) | | | 18,569 | (2) | | | 54,845 | (3) | | | 39,964 | | | | 34,837 | |

| % of Net Sales | | | (3.8 | ) | | | 2.6 | | | | 8.3 | | | | 6.7 | | | | 6.3 | |

| Total Other (Expense) Income, Net | | $ | (1,827 | ) | | | (994 | ) | | | 2,867 | (3) | | | 3,338 | | | | 157 | |

| Income Tax Expense | | $ | 1,921 | (1) | | | 6,951 | (2) | | | 17,845 | (3) | | | 13,493 | | | | 12,058 | |

| % of (Loss) Profit Before Income Taxes | | | 7.9 | | | | 39.6 | | | | 30.9 | | | | 31.2 | | | | 34.5 | |

| Net (Loss) Earnings | | $ | (26,241 | ) (1) | | | 10,624 | (2) | | | 39,867 | (3) | | | 29,809 | | | | 22,936 | |

| % of Net Sales | | | (4.4 | ) | | | 1.5 | | | | 6.0 | | | | 5.0 | | | | 4.2 | |

| Return on beginning Shareholders’ Equity – % | | | (12.5 | ) | | | 4.2 | | | | 17.4 | | | | 15.4 | | | | 13.2 | |

| Per Share Data | | | | | | | | | | | | | | | | | | | | |

| Basic (Loss) Earnings | | $ | (1.42 | ) (1) | | | 0.58 | (2) | | | 2.14 | (3) | | | 1.61 | | | | 1.27 | |

| Diluted (Loss) Earnings | | $ | (1.42 | ) (1) | | | 0.57 | (2) | | | 2.08 | (3) | | | 1.57 | | | | 1.26 | |

| Cash Dividends | | $ | 0.53 | | | | 0.52 | | | | 0.48 | | | | 0.46 | | | | 0.44 | |

| Shareholders’ Equity (ending) | | $ | 9.83 | | | | 11.48 | | | | 13.65 | | | | 12.25 | | | | 10.50 | |

| Year-End Financial Position | | | | | | | | | | | | | | | | | | | | |

| Cash and Cash Equivalents | | $ | 18,062 | | | | 29,285 | | | | 33,092 | | | | 31,021 | | | | 41,287 | |

| Total Current Assets | | $ | 215,912 | | | | 250,419 | | | | 240,724 | | | | 235,404 | | | | 211,601 | |

| Property, Plant and Equipment, Net | | $ | 97,217 | | | | 103,730 | | | | 96,551 | | | | 82,835 | | | | 72,588 | |

| Total Assets | | $ | 377,726 | | | | 456,604 | | | | 382,070 | | | | 354,250 | | | | 311,472 | |

| Total Current Liabilities | | $ | 116,152 | | | | 107,159 | | | | 96,673 | | | | 94,804 | | | | 88,965 | |

| Total Long-Term Liabilities | | $ | 77,295 | | | | 139,541 | | | | 32,966 | | | | 29,782 | | | | 29,405 | |

| Shareholders’ Equity | | $ | 184,279 | | | | 209,904 | | | | 252,431 | | | | 229,664 | | | | 193,102 | |

| Current Ratio | | | 1.9 | | | | 2.3 | | | | 2.5 | | | | 2.5 | | | | 2.4 | |

| Debt: | | | | | | | | | | | | | | | | | | | | |

| Current | | $ | 4,019 | | | | 3,946 | | | | 2,127 | | | | 1,812 | | | | 2,232 | |

| Long-Term | | $ | 30,192 | | | | 91,393 | | | | 2,470 | | | | 1,907 | | | | 1,608 | |

| Debt-to-Capital ratio | | | 15.7 | | | | 31.2 | | | | 1.8 | | | | 1.6 | | | | 1.9 | |

| Cash Flows | | | | | | | | | | | | | | | | | | | | |

| Net Cash Provided by Operating Activities | | $ | 75,185 | | | | 37,394 | | | | 39,640 | | | | 40,319 | | | | 44,237 | |

| Net Cash Used for Investing Activities | | $ | (13,334 | ) | | | (101,827 | ) | | | (10,357 | ) | | | (45,959 | ) | | | (11,781 | ) |

| Net Cash (Used for) Provided by Financing Activities | | $ | (74,068 | ) | | | 62,075 | | | | (26,679 | ) | | | (4,876 | ) | | | (8,111 | ) |

| Other Data | | | | | | | | | | | | | | | | | | | | |

| Interest Income | | $ | 393 | | | | 1,042 | | | | 1,854 | | | | 2,698 | | | | 1,691 | |

| Interest Expense | | $ | 2,830 | | | | 3,944 | | | | 898 | | | | 737 | | | | 564 | |

| Depreciation and Amortization | | $ | 22,803 | | | | 22,959 | | | | 18,054 | | | | 14,321 | | | | 13,039 | |

| Purchases of Property, Plant and Equipment | | $ | 11,483 | | | | 20,790 | | | | 28,720 | | | | 23,872 | | | | 20,880 | |

| Proceeds from disposals of Property, Plant and Equipment | | $ | 311 | | | | 808 | | | | 7,254 | | | | 632 | | | | 3,049 | |

| Number of employees at year-end | | | 2,786 | | | | 3,002 | | | | 2,774 | | | | 2,653 | | | | 2,496 | |

| Diluted Weighted Average Shares Outstanding | | | 18,507,772 | | | | 18,581,840 | | | | 19,146,025 | | | | 18,989,248 | | | | 18,209,888 | |

| Closing share price at year-end | | $ | 26.19 | | | | 15.40 | | | | 44.29 | | | | 29.00 | | | | 26.00 | |

| Common stock price range during year | | $ | 7.76-31.92 | | | | 15.33-45.41 | | | | 27.84-49.32 | | | | 21.71–29.88 | | | | 17.39-26.23 | |

| Closing Price/Earnings ratio | | | (18.4 | ) | | | 27.0 | | | | 21.3 | | | | 18.5 | | | | 20.6 | |

The results of operations from our 2009 and 2008 acquisitions have been included in the Consolidated Financial Statements, as well as the Selected Financial Data presented above, since each of their respective dates of acquisition. Refer to additional information in Note 4, Acquisitions and Divestitures.

(1) 2009 includes a goodwill impairment charge of $43,363 pretax ($42,289 aftertax or $2.29 per diluted share), a benefit from a revision during the first quarter of 2009 to the 2008 workforce reduction charge of $1,328 pretax ($1,249 aftertax or $0.07 per diluted share) and a net tax benefit, primarily from a United Kingdom business reorganization of $1,864 aftertax (or $0.10 per diluted share). (2) 2008 includes a workforce reduction charge and associated expenses of $14,551 pretax ($12,003 aftertax or $0.65 per diluted share), increase in Allowance for Doubtful Accounts of $3,361 pretax ($3,038 aftertax or $0.16 per diluted share), write-off of technology investments of $1,842 pretax ($1,246 aftertax or $0.07 per diluted share), and a gain on sale of Centurion assets of $229 pretax ($143 aftertax or $0.01 per diluted share). (3) 2007 includes a restructuring charge and associated expenses of $2,507 pretax ($1,656 aftertax or $0.09 per diluted share), a one-time tax benefit relating to a reduction in valuation reserves, net of the impact of tax rate changes in foreign jurisdictions on deferred taxes of $3,644 aftertax (or $0.19 per diluted share) and a gain on the sale of the Maple Grove, Minnesota facility of $5,972 pretax ($3,720 aftertax or $0.19 per diluted share).

ITEM 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations

Overview

Tennant Company is a world leader in designing, manufacturing and marketing solutions that help create a cleaner, safer world. We provide floor maintenance and outdoor cleaning equipment, chemical-free cleaning technologies, specialty surface coatings and related products that are used to clean and coat surfaces in factories, office buildings, parking lots and streets, airports, hospitals, schools, warehouses, shopping centers and more. We sell our products through our direct sales and service organization and a network of authorized distributors worldwide. Geographically, our customers are primarily located in North America, Europe, the Middle East, Africa, Asia-Pacific and Latin America. We strive to be an innovator in our industry through our commitment to understanding our customers’ needs and using our expertise to create innovative products and solutions.

Net Loss for 2009 was $26.2 million, or $1.42 loss per diluted share, compared to Net Earnings of $10.6 million, or $0.57 per diluted share for 2008. Net Loss was impacted by a non-cash pretax goodwill impairment charge of $43.4 million, or $2.29 loss per diluted share, taken during the first quarter of 2009 as well as a significant year over year decline in Net Sales due to ongoing unfavorable global economic conditions. Net Sales totaled $595.9 million, down 15.0% from 2008 driven primarily by a decline in equipment unit sales volume. Gross Margins increased 50 basis points to 41.3%. Benefits from commodity price deflation, cost reductions, flexible production management and workforce reductions more than offset the impact of lower sales and the unfavorable impact of lower production volume through our manufacturing facilities. Selling and Administrative Expense (“S&A Expense”) decreased 80 basis points as a percentage of Net Sales to 33.9% compared to 34.7% in 2008 due to benefits from our workforce reduction program, reductions in volume-related expenses, and delays in discretionary spending to align expenses with the lower level of sales.

Tennant continues to invest in innovative product development, with 3.9% of Net Sales spent on Research and Development in 2009. We launched one new product in 2009 in addition to the continued global rollout of our electrically converted water technology (“ec-water”) on five of our rider scrubbers. Sales of new products introduced in the past three years generated approximately 41% of our equipment sales during 2009, exceeding our long-term goal of 30%.

In addition, Net Loss was also impacted by a benefit from net favorable discrete tax items, which contributed $0.03 per diluted share, and a tax benefit from a United Kingdom business reorganization which contributed $0.10 per diluted share.

We ended 2009 with a Debt-to-Capital ratio of 15.7%, $18.1 million in Cash and Cash Equivalents and Shareholders’ Equity of $184.3 million. During 2009 we generated operating cash flows of $75.2 million. Total debt was $34.2 million as of December 31, 2009, a significant decrease from $95.3 million at the same time last year.

Historical Results

The following table compares the historical results of operations for the years ended December 31, 2009, 2008 and 2007 in dollars and as a percentage of Net Sales (in thousands, except per share amounts):

| | | 2009 | | | % | | | 2008 | | | % | | | 2007 | | | % | |

| Net Sales | | $ | 595,875 | | | | 100.0 | | | $ | 701,405 | | | | 100.0 | | | $ | 664,218 | | | | 100.0 | |

| Cost of Sales | | | 349,767 | | | | 58.7 | | | | 415,155 | | | | 59.2 | | | | 385,234 | | | | 58.0 | |

| Gross Profit | | | 246,108 | | | | 41.3 | | | | 286,250 | | | | 40.8 | | | | 278,984 | | | | 42.0 | |

| Operating Expense: | | | | | | | | | | | | | | | | | | | | | | | | |

Research and Development Expense | | | 22,978 | | | | 3.9 | | | | 24,296 | | | | 3.5 | | | | 23,869 | | | | 3.6 | |

Selling and Administrative Expense | | | 202,260 | | | | 33.9 | | | | 243,614 | | | | 34.7 | | | | 206,242 | | | | 31.1 | |

| Goodwill Impairment Charge | | | 43,363 | | | | 7.3 | | | | - | | | | - | | | | - | | | | - | |

| Gain on Divestiture of Assets | | | - | | | | - | | | | (229 | ) | | | - | | | | - | | | | - | |

| Gain on Sale of Facility | | | - | | | | - | | | | - | | | | - | | | | (5,972 | ) | | | (0.9 | ) |

| Total Operating Expenses | | | 268,601 | | | | 45.1 | | | | 267,681 | | | | 38.2 | | | | 224,139 | | | | 33.7 | |

| (Loss) Profit from Operations | | | (22,493 | ) | | | (3.8 | ) | | | 18,569 | | | | 2.6 | | | | 54,845 | | | | 8.3 | |

| Other Income (Expense): | | | | | | | | | | | | | | | | | | | | | | | | |

| Interest Income | | | 393 | | | | 0.1 | | | | 1,042 | | | | 0.1 | | | | 1,854 | | | | 0.3 | |

| Interest Expense | | | (2,830 | ) | | | (0.5 | ) | | | (3,944 | ) | | | (0.6 | ) | | | (898 | ) | | | (0.1 | ) |

Net Foreign Currency Transaction (Losses) Gains | | | (412 | ) | | | (0.1 | ) | | | 1,368 | | | | 0.2 | | | | 39 | | | | - | |

| ESOP Income | | | 990 | | | | 0.2 | | | | 2,219 | | | | 0.3 | | | | 2,568 | | | | 0.4 | |

| Other Income (Expense), Net | | | 32 | | | | - | | | | (1,679 | ) | | | (0.2 | ) | | | (696 | ) | | | (0.1 | ) |

Total Other (Expense) Income, Net | | | (1,827 | ) | | | (0.3 | ) | | | (994 | ) | | | (0.1 | ) | | | 2,867 | | | | 0.4 | |

| (Loss) Profit Before Income Taxes | | | (24,320 | ) | | | (4.1 | ) | | | 17,575 | | | | 2.5 | | | | 57,712 | | | | 8.7 | |

| Income Tax Expense | | | 1,921 | | | | 0.3 | | | | 6,951 | | | | 1.0 | | | | 17,845 | | | | 2.7 | |

| Net (Loss) Earnings | | $ | (26,241 | ) | | | (4.4 | ) | | $ | 10,624 | | | | 1.5 | | | $ | 39,867 | | | | 6.0 | |

| Net (Loss) Earnings per Share | | $ | (1.42 | ) | | | | | | $ | 0.57 | | | | | | | $ | 2.08 | | | | | |

Consolidated Financial Results

Net Loss for 2009 was $26.2 million, or $1.42 loss per diluted share, compared to Net Earnings of $10.6 million, or $0.57 per diluted share for 2008. Net Loss was impacted by:

| § | A decline in Net Sales of 15.0%, primarily due to a decrease in equipment unit sales volume experienced during 2009. |

| § | A 50 basis point increase in Gross Margins to 41.3% due to benefits from commodity price deflation, cost reductions, flexible production management and workforce reductions which more than offset the decline in equipment unit sales volume. |

| § | A decrease in S&A Expense as a percentage of Net Sales of 80 basis points due to benefits from our workforce reduction program, reductions in volume-related expenses and delays in discretionary spending. |

| § | Non-cash pretax goodwill impairment charge of $43.4 million during the first quarter of 2009. |

| § | A benefit from net favorable discrete tax items contributed $0.03 per diluted share and a tax benefit from a United Kingdom business reorganization contributed $0.10 per diluted share. |

In 2008, Net Earnings declined 73.4% to $10.6 million or $0.57 per diluted share as compared to 2007. Net Earnings were impacted by:

| § | Growth in Net Sales of 5.6% to $701.4 million, driven by 2008 acquisitions and increases in Other International. |

| § | A 120 basis point decline in Gross Margins to 40.8% as fixed manufacturing costs within our plants were not fully leveraged due to a significant equipment unit volume decline of $22.9 million experienced in the fourth quarter of 2008. |

| § | An increase in S&A Expense as a percentage of Net Sales of 360 basis points due to the inclusion of $19.8 million of expenses associated with the fourth quarter workforce reduction charge and other charges as well as expenses incurred earlier in the year to expand international market coverage and support new product launches. |

| § | The inclusion of a $2.7 million net foreign currency gain from settlement of forward contracts related to a British pound denominated loan. |

| § | A net benefit from discrete tax items, primarily related to U.S. federal tax settlements, added $0.07 per diluted share. |

| § | A dilutive impact to Net Earnings related to our 2008 acquisitions of $2.8 million. |

For 2009, we used operating profit and cash flows from operations as key indicators of financial performance and the primary metrics for performance-based incentives. Other key drivers we focus on to measure how effectively we utilize net assets in the business include “Accounts Receivable Days Sales Outstanding” (DSO), “Days Inventory on Hand” (DIOH) and capital expenditures. These key drivers are discussed in greater depth throughout Management’s Discussion and Analysis.

Net Sales

In 2009, consolidated Net Sales were $595.9 million, a decrease of 15.0% as compared to 2008. Consolidated Net Sales were $701.4 million in 2008, an increase of 5.6% over 2007.

The components of the consolidated Net Sales change for 2009 as compared to 2008 and 2008 compared to 2007 were as follows:

| | | % Change | | % Change |

| Growth Elements | from 2008 | | from 2007 |

| Organic (Decline) Growth: | | | |

| | Volume | (14%) | | (5%) |

| | Price | 1% | | 4% |

| | Organic Decline | (13%) | | (1%) |

| Foreign Currency | (3%) | | 2% |

| Acquisitions | 1% | | 5% |

| | Total | (15%) | | 6% |

The 15.0% decrease in consolidated Net Sales for 2009 from 2008 was primarily driven by:

| § | An organic decline of 13%, which includes a decline in base business equipment sales volume experienced in almost all geographic regions, slightly offset by the net benefit from higher year-over-year selling prices. |

| § | An unfavorable direct foreign currency exchange impact of 3%. |

The 5.6% increase in consolidated Net Sales for 2008 from 2007 was primarily driven by:

| § | An increase of 5% in sales volume due to our March 28, 2008 acquisition of Sociedade Alfa Ltda. (“Alfa”), our February 29, 2008 acquisition of Applied Sweepers, Ltd. (“Applied Sweepers”) and our February 1, 2007 acquisition of Floorep Limited (“Floorep”). |

| § | A favorable direct foreign currency exchange impact of 2%. |

| § | An organic decline of 1%, which includes a decline in base business volume, primarily within North America, partially offset by the net benefit from price increases implemented during the year. |

The following table sets forth annual Net Sales by geography and the related percent change from the prior year (in thousands, except percentages):

| | | 2009 | | | % | | | 2008 | | | % | | | 2007 | | | % | |

| North America | | $ | 345,766 | | | | (14.0 | ) | | $ | 402,174 | | | | (3.7 | ) | | $ | 417,757 | | | | 6.8 | |

| Europe, Middle East and Africa | | | 177,829 | | | | (18.3 | ) | | | 217,594 | | | | 18.8 | | | | 183,188 | | | | 17.6 | |

Other International | | | 72,280 | | | | (11.5 | ) | | | 81,637 | | | | 29.0 | | | | 63,273 | | | | 21.8 | |

| Total | | $ | 595,875 | | | | (15.0 | ) | | $ | 701,405 | | | | 5.6 | | | | 664,218 | | | | 10.9 | |

North America – In 2009, North America Net Sales declined 14.0% to $345.8 million compared with $402.2 million in 2008. The primary driver of the decrease in Net Sales is attributable to a decline in equipment unit volume, during the first three quarters of 2009, somewhat offset by benefits from slightly higher selling prices. There was no impact from foreign currency translation during 2009.

In 2008, North America Net Sales declined 3.7% to $402.2 million compared with $417.8 million in 2007. The primary driver of the decrease in Net Sales is attributable to a decline in equipment unit volume, with the most significant declines occurring in the fourth quarter as a result of the credit crisis and its impact on an already sluggish U.S. economy. Partially offsetting these declines were benefits from pricing actions taken during the year and a net favorable impact from foreign currency translation. Our acquisition of Applied Sweepers contributed approximately 1% to North America’s 2008 Net Sales.

Europe, Middle East and Africa – Europe, Middle East and Africa (“EMEA”) Net Sales in 2009 decreased 18.3% to $177.8 million compared to 2008 Net Sales of $217.6 million. Unfavorable direct foreign currency exchange effects decreased EMEA Net Sales by approximately 7% in 2009. Our Applied Sweepers acquisition contributed approximately 1% to EMEA Net Sales in 2009. EMEA’s organic sales decline of approximately 12% was primarily due to lower equipment unit volume in most regions due to weak economic conditions somewhat offset by higher equipment unit volume in the UK and Italy and slightly higher selling prices.

EMEA Net Sales in 2008 increased 18.8% to $217.6 million compared to 2007 Net Sales of $183.2 million. Favorable direct foreign currency exchange effects increased EMEA Net Sales by approximately 6% in 2008. Our Applied Sweepers acquisition contributed approximately 14% to EMEA’s 2008 Net Sales. EMEA’s organic sales were essentially flat in 2008 when compared to 2007. Pricing increases and volume growth in emerging markets were offset by lower sales of equipment in the mature markets within Europe. The majority of the equipment unit volume decline occurred in the fourth quarter following the global credit crisis and a significant slowdown in these economies.

Other International – Our Other International markets are comprised of the following key geographic regions: China and other Asia Pacific markets, Japan, Australia and Latin America. Other International Net Sales in 2009 decreased 11.5% to $72.3 million over 2008 Net Sales of $81.6 million. Our Alfa acquisition contributed approximately 2% to Other International Net Sales in 2009, while unfavorable direct foreign currency exchange effects decreased Net Sales by approximately 1% in 2009. Other International’s organic sales decline of approximately 12% was primarily due to lower equipment unit volume in Latin America due to weak economic conditions somewhat offset by higher equipment unit volume in Australia and China.

Other International Net Sales in 2008 increased 29.0% to $81.6 million over 2007 Net Sales of $63.3 million. Growth in Net Sales was driven in part by organic growth, resulting from expanded market coverage in Brazil and China as well as a net benefit from pricing actions taken during the year. Our acquisitions contributed approximately 12% to Other International’s 2008 Net Sales. Price increases also contributed to the 2008 growth in Net Sales. Favorable direct foreign currency exchange effects increased Net Sales in Other International markets by approximately 3% in 2008.

Gross Profit

Gross Margin was 41.3% in 2009, an increase of 50 basis points as compared to 2008. Gross Margin was unfavorably impacted by the decline in equipment unit volume as compared to the prior year; however, this was more than offset by commodity price deflation, cost reductions, flexible production management and savings from workforce reductions.

Gross Margin was 40.8% in 2008, down 120 basis points as compared to 2007. Although benefits from pricing actions and cost reduction initiatives were able to essentially offset higher raw material and purchased component costs during 2008, the inability to leverage the fixed manufacturing costs in our plants, due to the significant decline in unit volume experienced in the fourth quarter, drove a decline in margins year over year. Gross Margin was also impacted by an unfavorable sales mix and by the inclusion of $1.2 million in expense from the flow-through of fair market value inventory step-up from our acquisitions of Applied Sweepers and Alfa.

Operating Expenses

Research and Development Expense – Research and Development Expense (“R&D Expense”) decreased $1.3 million, or 5.4%, in 2009 compared to 2008 and increased 40 basis points to 3.9% as a percentage of Net Sales. Despite lower sales levels in 2009 investments continued to be made in key research and development projects and technologies.

R&D Expense increased $0.4 million, or 1.8%, in 2008 compared to 2007 and decreased 10 basis points to 3.5% as a percentage of Net Sales.

Selling and Administrative Expense – S&A Expense decreased by $41.4 million, or 17.0%, in 2009 compared to 2008. As a percentage of Net Sales, 2009 S&A Expense decreased 80 basis points to 33.9%. S&A Expense benefited from decreased headcount in 2009 due to the fourth quarter 2008 workforce reduction, decreased selling costs associated with a lower level of sales and delays in discretionary spending, partially offset by higher incentives as compared to the prior period due to strong operating profit results and cash flows from operations. Favorable foreign currency exchange was approximately $3.4 million in 2009.

S&A Expense increased by $37.4 million, or 18.1%, in 2008 compared to 2007. The inclusion of expense from our 2008 acquisitions of Applied Sweepers, Alfa and Shanghai ShenTan Mechanical and Electrical Equipment Co. Ltd. (“Shanghai ShenTan”) added $10.7 million to S&A Expense during 2008. S&A Expense included a $14.6 million workforce reduction charge as discussed in Note 3 to the Consolidated Financial Statements. S&A Expense was also impacted by a significant increase in bad debt expense of $3.4 million resulting from increased Accounts Receivable reserves due to the global credit crisis and a write-off of $1.8 million related to technology investments that will be replaced by new solutions. Unfavorable foreign currency exchange was approximately $4.5 million in 2008.

Goodwill Impairment Charge – During the first quarter of 2009, we recorded a non-cash pretax goodwill impairment charge of $43.4 million related to our EMEA reporting unit. All but $3.8 million of this charge is not tax deductible.

Gain on Divestiture of Assets – We sold assets related to our Centurion line of sweepers during the second quarter of 2008 for a pretax gain of $0.2 million.

Gain on Sale of Facility – We completed the sale of our Maple Grove, Minnesota facility during the fourth quarter of 2007 for a net pretax gain of $6.0 million.

Total Other Income (Expense), Net

Interest Income – Interest Income was $0.4 million in 2009, a decrease of $0.6 million from 2008. The decrease reflects the impact of a lower level of cash on hand during 2009 as compared to 2008 as well as a slightly lower interest rate.

Interest Income was $1.0 million in 2008, a decrease of $0.8 million from 2007. The decrease between 2008 and 2007 reflects the impact of a decline in interest rates between periods on lower average cash levels.

Interest Expense – Interest Expense was $2.8 million in 2009 as compared to $3.9 million in 2008. This decline is primarily due to significant repayments of debt during 2009 as compared to 2008.

Interest Expense was $3.9 million in 2008 as we became a net debtor during the first quarter of 2008 borrowing against our revolving credit facility, primarily to fund the two acquisitions that closed during the first quarter of 2008.

Net Foreign Currency Transaction Gains (Losses) – Net Foreign Currency Transaction Gains decreased $1.8 million between 2009 and 2008 from a $1.4 million net gain in 2008 to a $0.4 million net loss during 2009. Included in the 2008 net gain of $1.4 million was a $2.7 million net foreign currency gain from the settlement of forward contracts related to a British pound denominated loan, partially offset by a $0.9 million unfavorable movement in the foreign currency exchange rates related to a deal contingent non-speculative forward contract. There were no individually significant transactions in the 2009 activity, resulting in a net unfavorable impact from other foreign currency fluctuations between years.

Net Foreign Currency Transaction Gains increased $1.3 million between 2008 and 2007. A $2.7 million net foreign currency gain from the settlement of forward contracts related to a British pound denominated loan was the most significant contributor to the change between years. This gain was partially offset by the $0.9 million unfavorable movement in the foreign currency exchange rates related to a deal contingent non-speculative forward contract that we entered into that fixed the cash outlay in U.S. dollars for the Alfa acquisition in the first quarter of 2008. The remaining change was due to a net favorable impact from other foreign currency fluctuations between years.

ESOP Income – ESOP Income decreased $1.2 million between 2009 and 2008 due to a lower average stock price. We benefit from ESOP Income when the shares held by Tennant’s ESOP Plan are utilized and the basis of those shares is lower than the current average stock price. This benefit is offset in periods when the number of shares needed exceeds the number of shares available from the ESOP as the shortfall must be issued at the current market rate, which is generally higher than the basis of the ESOP shares. We issued additional shares throughout 2009 as we experienced a lower average stock price during 2009 as compared to 2008. On December 31, 2009, the ESOP loan matured and was repaid to us, completing the twenty year term for this plan.

ESOP Income decreased $0.3 million between 2008 and 2007 due to a lower average stock price. We benefit from ESOP Income when the shares held by Tennant’s ESOP Plan are utilized and the basis of those shares is lower than the current average stock price. This benefit is offset in periods when the number of shares needed exceeds the number of shares available from the ESOP as the shortfall must be issued at the current market rate, which is generally higher than the basis of the ESOP shares. During the year ended 2008 compared to 2007, we experienced a lower average stock price and issued additional shares during the fourth quarter of 2008.

Other Income (Expense), Net – The $1.7 million decrease in Other Expense, Net between 2009 and 2008 was primarily due to a decrease in discretionary contributions to Tennant’s charitable foundation.

Other Expense, Net increased $1.0 million between 2008 and 2007. The increase in Other Expense, Net was primarily due to an increase in discretionary contributions to Tennant’s charitable foundation.

Income Taxes

Our effective income tax rate was 7.9%, 39.6% and 30.9% in 2009, 2008 and 2007, respectively. The 2009 tax expense includes only a $1.1 million tax benefit associated with the $43.4 million impairment of Goodwill recorded in the first quarter, materially impacting the overall rate. Excluding the $1.1 million tax benefit associated with the first quarter goodwill impairment, the 2009 effective tax rate would have been 15.7%. The 2009 tax expense also includes a $2.3

million tax benefit associated with a United Kingdom business reorganization in the fourth quarter, also materially impacting the overall rate. Excluding the tax benefit associated with the first quarter goodwill impairment and the fourth quarter United Kingdom business reorganization, the 2009 effective tax rate would have been 27.8%. The decrease in the 2009 effective tax rate excluding these items was substantially related to changes in our operating profit by taxing jurisdiction.

During 2008, we had a negative impact due to a correction of an immaterial error related to reserves for uncertain tax positions covering tax years 2004 to 2006. The change in the 2008 rate as compared to 2007 was also negatively impacted due to the 2007 favorable one-time discrete item related to the reversal of a German valuation allowance, as noted below.

During 2007, a favorable one-time discrete item of $3.6 million related to the reversal of a German valuation allowance, net of the impact of tax rate changes in foreign jurisdictions on deferred taxes, was recognized in the third quarter. It was determined that it was now more likely than not that a tax loss carryforward in Germany will be utilized in the future and accordingly the valuation allowance on the related deferred tax asset was reduced to zero.

Liquidity and Capital Resources

Liquidity – Cash and Cash Equivalents totaled $18.1 million at December 31, 2009, as compared to $29.3 million of Cash and Cash Equivalents as of December 31, 2008. Cash and Cash Equivalents held by our foreign subsidiaries totaled $10.1 million as of December 31, 2009 as compared to $14.6 million of Cash and Cash Equivalents held by our foreign subsidiaries as of December 31, 2008. Wherever possible, cash management is centralized and intercompany financing is used to provide working capital to subsidiaries as needed. Our current ratio was 1.9 and 2.3 as of December 31, 2009 and 2008, based on working capital of $99.8 million and $143.3 million, respectively.

Our Debt-to-Capital ratio was 15.7% as of December 31, 2009, compared with 31.2% as of December 31, 2008. Our capital structure was comprised of $34.2 million of Long-Term Debt and $184.3 million of Shareholders’ Equity as of December 31, 2009.

On July 29, 2009, we filed a shelf registration statement with the SEC to facilitate any future issuances of debt securities, preferred stock, depository shares and common stock up to $175.0 million. This shelf registration statement was declared effective by the SEC on December 15, 2009.

On July 29, 2009, we entered into a Private Shelf Agreement (the “Shelf Agreement”) with Prudential Investment Management, Inc. (“Prudential”) and Prudential affiliates from time to time party thereto. The Shelf Agreement provides us and our subsidiaries access to uncommitted, senior secured, debt capital with a maximum aggregate principal amount of $80.0 million. There was no balance outstanding under this credit facility as of December 31, 2009.

Cash Flow Summary – Cash provided by (used in) our operating, investing and financing activities is summarized as follows (in thousands):

| | | 2009 | | | 2008 | | | 2007 | |

| Operating Activities | | $ | 75,185 | | | $ | 37,394 | | | $ | 39,640 | |

| Investing Activities: | | | | | | | | | | | | |

Purchases of Property, Plant and Equipment, Net of Disposals | | | (11,172 | ) | | | (19,982 | ) | | | (21,466 | ) |

| Acquisitions of Businesses, Net of Cash Acquired | | | (2,162 | ) | | | (81,845 | ) | | | (3,141 | ) |

| Change in Short-Term Investments | | | - | | | | - | | | | 14,250 | |

| Financing Activities | | | (74,068 | ) | | | 62,075 | | | | (26,679 | ) |

| Effect of Exchange Rate Changes on Cash and Cash Equivalents | | | 994 | | | | (1,449 | ) | | | (533 | ) |

| Net Increase (Decrease) in Cash and Cash Equivalents | | $ | (11,223 | ) | | $ | (3,807 | ) | | $ | 2,071 | |

Operating Activities – Cash provided by operating activities was $75.2 million in 2009, $37.4 million in 2008 and $39.6 million in 2007. In 2009, cash provided by operating activities was driven by strong working capital management, offset somewhat by a decrease in Employee Compensation and Benefits and Other Accrued Expenses due in part to the cash payments in 2009 for the workforce reduction, which were accrued in 2008. Cash flow provided by operating activities was $37.8 million higher in 2009 compared to 2008. This increase was primarily driven by a reduction in Inventories and an increase in Income Taxes Payable and Accounts Payable, offset by a decrease in Employee Compensation and Benefits and Other Accrued Expenses.

In 2008, cash provided by operating activities was driven by Net Earnings, as well as increases in Employee Compensation and Benefits and Other Accrued Expenses and Accounts Receivable, partially offset by a decrease in Income Taxes Payable/Prepaid.

As discussed previously, two metrics used by management to evaluate how effectively we utilize our net assets are “Accounts Receivable Days Sales Outstanding” (DSO) and “Days Inventory on Hand” (DIOH), on a FIFO basis. The metrics are calculated on a rolling three month basis in order to more readily reflect changing trends in the business. These metrics for the quarters ended December 31 were as follows (in days):

| | | 2009 | | 2008 | | 2007 |

| DSO | | 67 | | 77 | | 61 |

| DIOH | | 87 | | 101 | | 83 |

DSO decreased 10 days in 2009 compared to 2008 primarily due to our proactive management of risk in this area by increasing focus on credit reviews and credit limits and more aggressively pursuing collection of past due balance in light of the more difficult economic environment.

DIOH decreased 14 days in 2009 compared to 2008 primarily due to lower levels of inventory as a result of inventory reduction initiatives.

Investing Activities – Net cash used for investing activities was $13.3 million in 2009, $101.8 million in 2008 and $10.4 million in 2007. The primary use of cash in investing activities during 2009 was net capital expenditures, which totaled $11.2 million.

Net capital expenditures were $11.2 million during 2009 compared to $20.0 million in 2008. Net capital expenditures were $21.5 million in 2007. Capital expenditures in 2009 included technology upgrades, tooling related to new product development and investments in our Minnesota facilities to complete the Global Innovation Center to support new product innovation efforts. Net capital expenditures in 2008 included upgrades to our information technology systems and related infrastructures and investments in tooling in support of new products, as well as investment in our corporate facilities to create a Global Innovation Center for research and development. Net capital expenditures in 2007 included continued investments in our footprint consolidation initiative, new product tooling and capital spending related to our global expansion initiatives.

On February 27, 2009, we acquired certain assets of Applied Cleansing Solutions Pty Ltd ("Applied Cleansing"), a long-term importer and distributor for Green Machines™ products in Australia and New Zealand, in a business combination for an initial purchase price of $0.4 million in cash. This acquisition provides us with the opportunity to accelerate our growth in the city cleaning business within the Asia Pacific region. The purchase agreement also provides for additional contingent consideration to be paid for each of the four quarters following the acquisition date if certain future revenue targets are met. We recorded additional contingent consideration of approximately $0.2 million, which represented our best estimate of these probable quarterly payments. As of December 31, 2009, we have paid additional consideration of $0.2 million for the first three quarters following the date of acquisition. The acquisition of Applied Cleansing is accounted for as a business combination and the results of operations have been included in the Consolidated Financial Statements since the date of acquisition. The purchase price allocation is preliminary and will be

adjusted retroactively based upon the final determination of fair value of assets acquired and liabilities assumed.

On December 1, 2008, we entered into an asset purchase agreement with Hewlett Equipment (“Hewlett”) for a purchase price of $0.6 million in cash. The purchase of Hewlett’s existing rental fleet of industrial equipment will accelerate Tennant’s strategy to grow its direct sales and service business in the Brisbane, Australia area. Hewlett will continue as a distributor and service agent of Tennant’s commercial equipment.

On August 15, 2008, we acquired Shanghai ShenTan Mechanical and Electrical Equipment Co. Ltd. (“Shanghai ShenTan”) for a purchase price including transaction costs of $0.6 million in cash. The purchase agreement provides for additional contingent consideration to be paid in each of the three one-year periods following the acquisition date if certain future revenue targets are met and if other future events occur. Amounts paid under this earn-out will be considered additional purchase price. The potential earn-out is denominated in foreign currency which approximates $0.6 million in the aggregate and is calculated based on 1) growth in revenues and 2) visits to specified customer locations during each of the three one-year periods following the acquisition date. During 2009, we recorded $0.1 million for the earn-out related to the first one-year period following the acquisition.

On March 28, 2008, we acquired Alfa for an initial purchase price including transaction costs of $12.3 million in cash and $1.4 million in debt assumed. Alfa manufactures the Alfa brand of commercial cleaning machines, is based in São Paulo, Brazil, and is recognized as the market leader in the Brazilian cleaning equipment industry. The purchase agreement with Alfa also provides for additional contingent consideration up to approximately $6.8 million to be paid if certain revenue targets are met based on growth in revenues during the 2009 calendar year. Amounts paid under this earn-out will be considered additional purchase price. During the first quarter of 2009, we paid the maximum earn-out amount of $1.2 million related to the interim period calculation based on growth in 2008 revenues. As of December 31, 2009, we do not anticipate that there will be any additional earn-out payments.

On February 29, 2008, we acquired Applied Sweepers, a privately-held company based in Falkirk, Scotland, for a purchase price of $68.9 million in cash. Applied Sweepers is the manufacturer of Green Machines™ and is recognized as the leading manufacturer of sub-compact outdoor sweeping machines in the United Kingdom. Applied Sweepers also has locations in the United States, France and Germany and sells through a broad distribution network around the world.

In February 2007, we acquired Floorep, a distributor of cleaning equipment based in Scotland, for a purchase price of $3.6 million in cash. The results of Floorep’s operations have been included in the Consolidated Financial Statements since February 2, 2007, the date of acquisition.

Financing Activities – Net cash used for financing activities was $74.1 million in 2009. Net cash provided by financing activities was $62.1 million in 2008. Net cash used for financing activities was $26.7 million in 2007. In 2009, payments of Long-Term Debt used $67.2 million and dividend payments used $9.9 million. In 2008, issuance of Long-Term Debt for our 2008 acquisitions provided $87.5 million and significant uses of cash included $14.3 million in repurchases of Common Stock related to our share repurchase program and $9.6 million of dividends paid. Our annual cash dividend payout increased for the 38th consecutive year to $0.53 per share in 2009, an increase of $0.01 per share over 2008.

Proceeds from the issuance of Common Stock generated $0.9 million in 2009, $1.9 million in 2008 and $8.7 million in 2007. Proceeds are due to employees’ stock option exercises which have declined over the past two years as our average stock price has declined.

On May 3, 2007, the Board of Directors authorized the repurchase of 1,000,000 shares of our Common Stock. At December 31, 2009, there remained approximately 288,874 shares authorized for repurchase.

There were no shares repurchased during 2009 and 450,100 and 735,900 shares were repurchased during the years ended 2008 and 2007, respectively, at average repurchase prices of $31.62 and $39.34, respectively. Beginning in September 2008, repurchases were temporarily suspended in order to conserve cash and on March 4, 2009, our amendment to our Credit Agreement prohibited us from conducting share repurchases during 2009 and also limited the payment of dividends and repurchases of stock in future years to amounts ranging from $12.0 million to $40.0 million based on our leverage ratio after giving effect to such payments.

Indebtedness – As of December 31, 2009, we had committed lines of credit totaling approximately $134.3 million and uncommitted lines of credit totaling $80.0 million. There was $25.0 million in outstanding borrowings under our JPMorgan facility and no borrowings under any other facilities as of December 31, 2009. In addition, we had stand alone letters of credit of approximately $2.1 million outstanding and bank guarantees in the amount of approximately $1.0 million. Commitment fees on unused lines of credit for the year ended December 31, 2009 were $0.5 million.

Our most restrictive covenants are part of our Credit Agreement with JPMorgan, which are the same covenants in the Shelf Agreement with Prudential, and require us to maintain an indebtedness to EBITDA ratio of not greater than 3.50 to 1 and to maintain an EBITDA to interest expense ratio of no less than 3.50 to 1 as of the end of each quarter. As of December 31, 2009, our indebtedness to EBITDA ratio was 0.88 to 1 and our EBITDA to interest expense ratio was 14.94 to 1.

JPMorgan Chase Bank, National Association

On June 19, 2007, we entered into a Credit Agreement (the “Credit Agreement”) with JPMorgan Chase Bank, National Association (“JPMorgan”), as administrative agent, Bank of America, N.A., as syndication agent, BMO Capital Markets Financing, Inc. and U.S. Bank National Association, as Co-Documentation Agents and the Lenders from time to time party thereto. The Credit Agreement provides us and certain of our foreign subsidiaries access to a $125.0 million revolving credit facility until June 19, 2012. Borrowings may be denominated in U.S. dollars or certain other currencies. The facility is available for general corporate purposes, working capital needs, share repurchases and acquisitions. The Credit Agreement contains customary representations, warranties and covenants, including but not limited to covenants restricting our ability to incur indebtedness and liens and to merge or consolidate with another entity. Further, the Credit Agreement initially contains a covenant requiring us to maintain an indebtedness to EBITDA ratio as of the end of each quarter of not greater than 3.50 to 1 and to maintain an EBITDA to interest expense ratio of no less than 3.50 to 1.

On February 21, 2008, we amended the Credit Agreement to increase the sublimit on foreign currency borrowings from $75.0 million to $125.0 million and to increase the sublimit on borrowings by the foreign subsidiaries from $50.0 million to $100.0 million.

On March 4, 2009, we entered into a second amendment to the Credit Agreement. This amendment principally provided: (i) an exclusion from our EBITDA calculation for all non-cash losses and charges, up to $15.0 million cash restructuring charges during the 2008 fiscal year and up to $3.0 million cash restructuring charges during the 2009 fiscal year, (ii) an amendment of the indebtedness to EBITDA financial ratio required for the second and third quarters of 2009 to not greater than 4.00 to 1 and 5.50 to 1, respectively, (iii) an amendment to the EBITDA to interest expense financial ratio for the third quarter of 2009 to not less than 3.25 to 1, and (iv) the ability for us to incur up to an additional $80.0 million of indebtedness pari passu with the lenders under the Credit Agreement. The revolving credit facility available under the Credit Agreement remains at $125.0 million, but the amendment reduced the expansion feature under the Credit Agreement from $100.0 million to $50.0 million. The amendment put a cap on permitted new acquisitions of $2.0 million for the 2009 fiscal year and the amount of permitted new acquisitions in fiscal years after 2009 will be limited according to our then current leverage ratio. The amendment prohibited us from conducting share repurchases during the 2009

fiscal year and limits the payment of dividends and repurchases of stock in fiscal years after 2009 to an amount ranging from $12.0 million to $40.0 million based on our leverage ratio after giving effect to such payments. Finally, if we obtain additional indebtedness as permitted under the amendment, to the extent that any revolving loans under the credit agreement are then outstanding we are required to prepay the revolving loans in an amount equal to 100% of the proceeds from the additional indebtedness. Additionally, proceeds over $25.0 million and under $35.0 million will reduce the revolver commitment on a 50% dollar for dollar basis and proceeds over $35.0 million will reduce the revolver commitment on a 100% dollar for dollar basis.