SCHEDULE 14A INFORMATION

PROXY STATEMENT PURSUANT TO SECTION 14(A) OF THE SECURITIES EXCHANGE ACT OF 1934

Filed by the Registrant ☒

Filed by a party other than the Registrant o

Check the appropriate box:

o | Preliminary Proxy Statement |

o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

☒ | Definitive Proxy Statement |

o | Definitive Additional Materials |

o | Soliciting Material Under Rule 14a-12 |

Tidewater Inc. |

(Name of Registrant as Specified In Its Charter) |

(Name(s) of Person(s) Filing Proxy Statement, if other than the Registrant) |

Payment of Filing Fee (Check the appropriate box):

☒ | No fee required | ||

o | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | ||

1) | Title of each class of securities to which transaction applies: | ||

2) | Aggregate number of securities to which transaction applies: | ||

3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | ||

4) | Proposed maximum aggregate value of transaction: | ||

5) | Total fee paid: | ||

o | Fee paid previously with preliminary materials. | ||

o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | ||

1) | Amount Previously Paid: | ||

2) | Form, Schedule or Registration Statement No.: | ||

3) | Filing Party: | ||

4) | Date Filed: | ||

![]()

TIDEWATER INC.

6002 Rogerdale Road, Suite 600

Houston, Texas 77072

March 18, 2019

To Our Stockholders:

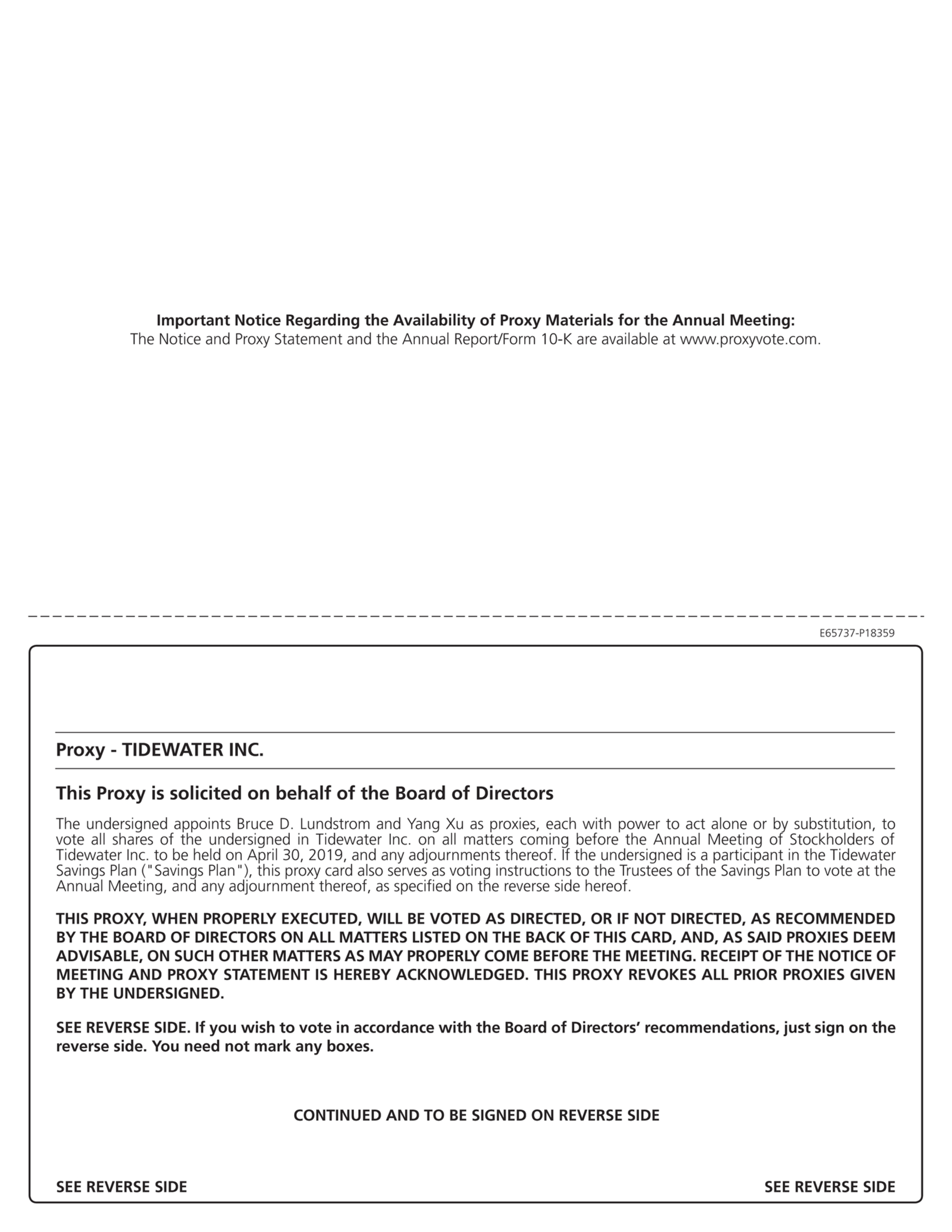

You are cordially invited to attend the 2019 Annual Meeting of Stockholders of Tidewater Inc. to be held at SpringHill Suites by Marriott Houston Westchase, 5851 Rogerdale Road, Houston, Texas, on April 30, 2019 at 10:00 a.m., Central Time.

The attached Notice of Annual Meeting and Proxy Statement describe the formal business to be conducted at the meeting. Our directors and officers will be present at the meeting to respond to your questions.

This year, we are once again giving certain stockholders the option of receiving their proxy materials electronically. The Securities and Exchange Commission’s proxy rules allow companies to furnish proxy materials to stockholders by allowing them to access material on the internet instead of mailing a printed set to each stockholder, unless the stockholder requests delivery by traditional mail or electronically by email. In accordance with these rules, beginning on or about March 18, 2019, we began mailing a Notice of Internet Availability of Proxy Materials to certain stockholders and made our proxy materials available online. As discussed in greater detail below, the Notice of Internet Availability of Proxy Materials contains instructions on how to access our proxy materials online as well as how to vote by telephone, online or in person at the annual meeting. Most stockholders will not receive printed copies of the proxy materials unless requested.

You are requested to vote by proxy as promptly as possible. You may vote by telephone or online, or, if you have received a paper copy of our proxy materials, you may vote by signing, dating, and returning the enclosed proxy card in the envelope provided. If you attend the meeting, which we hope that you will, you may vote in person even if you previously voted by proxy.

Sincerely, | |

| |

THOMAS R. BATES, JR. Chairman of the Board |

TIDEWATER INC.

6002 Rogerdale Road, Suite 600

Houston, Texas 77072

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

The 2018 Annual Meeting of Stockholders of Tidewater Inc. (the “company”) will be held at SpringHill Suites by Marriott Houston Westchase, 5851 Rogerdale Road, Houston, Texas, on April 30, 2019 at 10:00 a.m., Central Time, for the following purposes:

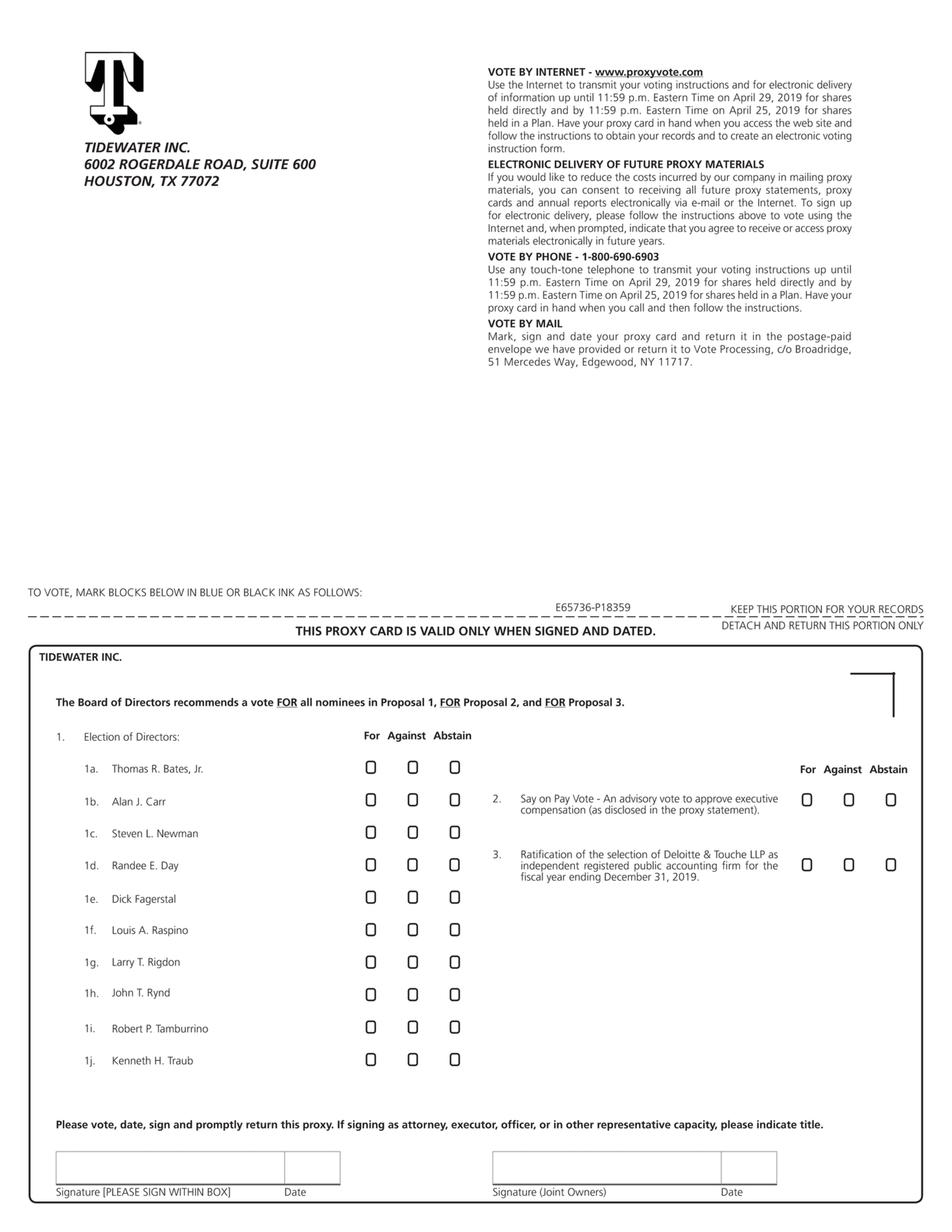

| • | to elect ten (10) directors, each for a one-year term; |

| • | to approve, on an advisory basis, our executive compensation as disclosed in this proxy statement (the “say-on-pay” vote); |

| • | to ratify the selection of Deloitte & Touche LLP as the company’s independent registered public accounting firm for the fiscal year ending December 31, 2019; and |

| • | to transact such other business as may properly come before the meeting or any adjournment thereof. |

Only stockholders of record at the close of business on March 6, 2019 are entitled to notice of, and to vote at, the 2019 annual meeting. Our board of directors unanimously recommends that you vote FOR each of the ten (10) director nominees, FOR approval of our executive compensation, and FOR ratification of our selection of Deloitte & Touche LLP as our auditors.

Your vote is important. If you are unable to attend the meeting in person and wish to have your shares voted, you may vote by telephone or online, or, if you have received a paper copy of our proxy materials, by completing, dating, and signing the enclosed proxy card and returning it in the accompanying envelope as promptly as possible. You may revoke your proxy by giving a revocation notice to our Secretary at any time before the 2019 annual meeting, by timely delivering a proxy bearing a later date, or by voting in person at the meeting.

By Order of the Board of Directors | |

| |

BRUCE D. LUNDSTROM Executive Vice President, General Counsel and Secretary | |

Houston, Texas | |

March 18, 2019 |

IMPORTANT NOTICE REGARDING THE AVAILABILITY OF

OUR PROXY MATERIALS FOR THE

ANNUAL MEETING OF STOCKHOLDERS ON APRIL 30, 2019.

This proxy statement and our 2018 annual report on Form 10-K are available at

www.proxyvote.com

REQUIREMENTS FOR ATTENDING THE ANNUAL MEETING IN PERSON

If you plan to attend the annual meeting in person, please bring the following:

| 1. | proper personal identification (preferably a current driver’s license); and |

| 2. | acceptable proof of ownership if your shares are held for you by a broker, bank, or other nominee (in “street name”). |

If your shares are held in street name, we will accept, as proof of your ownership of those shares, either an account statement or a letter from your broker, bank, or other nominee confirming that you were the beneficial owner of our stock on the record date.

We reserve the right to deny admission to the meeting to any person other than a stockholder of record on the record date (or a duly-designated proxy) or a beneficial owner of shares held in street name on the record date who has produced acceptable proof of ownership.

If you need directions to the annual meeting, please contact us at (713) 470-5300.

TIDEWATER INC.

6002 Rogerdale Road, Suite 600

Houston, Texas 77072

PROXY STATEMENT

This summary highlights selected information contained elsewhere in this proxy statement, but does not contain all of the information that you should consider before voting your shares. We recommend that you read the entire proxy statement carefully before voting. For complete information regarding the 2019 annual meeting of stockholders, the proposals to be voted on at the annual meeting, and our company’s performance during the 2018 fiscal year, please review the entire proxy statement and our Annual Report on Form 10-K for the period ended December 31, 2018. These materials are being made available to stockholders on or about March 18, 2019.

2019 Annual Meeting of Stockholders

Time and Date: 10:00 a.m., Central Time, Tuesday, April 30, 2019

Place: SpringHill Suites by Marriott Houston Westchase, 5851 Rogerdale Road, Houston, Texas 77072

Record Date: March 6, 2019

Voting: Only stockholders as of the record date are entitled to vote. Each share of common stock is entitled to one vote for each director nominee and one vote for each of the other proposals.

2018 Performance Highlights (page 27)

| • | Successful Completion of the Business Combination. On November 15, 2018, we successfully completed our business combination (the “business combination”) with GulfMark Offshore, Inc. (“GulfMark”) in an all-stock transaction, creating a global OSV leader that is both positioned to capitalize on superior growth opportunities as the OSV sector recovery gains traction and achieve significant cost synergies. The combined company now has the industry’s largest fleet and one of the broadest global operating footprints in the OSV sector, with an unmatched ability to support customers across geo-markets and water depths. In particular, the combination expanded Tidewater’s position in the recovering North Sea region and enhanced Tidewater’s fleet quality. The all-equity transaction helped preserve the strong balance sheet and liquidity position of both parties, with the combined company having the highest market capitalization and the lowest leverage in the OSV sector. Further, the combination is expected to position the combined company to realize at least $30 million in annualized cost synergies by the fourth quarter of 2019. |

| • | Substantial Progress Implementing the Business Combination Integration. Since the closing, our combined team has made, and continues to make, substantial progress implementing our merger integration plan. As a result of the business combination, we have reduced our combined on-shore operational footprint, with the consolidation and closing of five facilities, including the consolidation of all corporate operations to the existing Tidewater headquarters in Houston. In addition, the optimization of the combined vessel fleet continues to progress well, with several GulfMark vessels finding new employment in the broader geographical footprint serviced by Tidewater. |

| • | Cash Flow Positive from Operations and Cash Flow Positive from Investing Activities for the Full Year 2018. Although we continue to face a challenging operating environment in the global OSV industry, throughout the full year 2018 and into 2019, we continue to focus on maximizing revenue, cost control and capital discipline, each of which improves our cash flow position. As a result, we were cash flow positive from both an operations and investing activities standpoints for the full year 2018. We remain prepared to respond to changes in industry conditions so that our key objectives of cash flow positive operations and maintaining capital discipline can be achieved. |

| • | Capital Discipline Focus, including Sales of Stacked Fleet, Continue to Improve Cash Flow From Operations. Our capital discipline focus, including fleet rationalization, working capital management, and disciplined investments in vessels, contributed significantly to our positive cash flow in fiscal 2018. We continue to implement a variety of cost-control initiatives, including: reductions to vessel operating costs, |

1

reductions in world-wide staffing levels, targeted reductions in compensation and salaries company-wide, consolidation of offices globally, changes to our insurance program, improved management of vessel repair and maintenance, and other cost control measures. Furthermore, we once again led our sector in selling stacked vessels into peripheral markets and recycling yards in 2018, and we currently expect to continue this commitment in 2019 and beyond.

| • | We Remain an Industry Leader in Safety Performance. Our safety performance history continues to be among the best in our industry, with a Total Recordable Incident Rate (“TRIR”) of 0.12 per 200,000 hours worked in 2018. Our safety performance positively impacted our financial results, contributing to significant reductions in our insurance and loss reserves in 2018. We also believe that our strong safety record gives us a competitive advantage, both in retaining existing business and competing for new contracts. |

Executive Compensation Highlights (page 28)

What We Do | What We Don’t Do | ||

✔ | Performance-Based Short-Term Incentives. We typically award short-term incentive (“STI”) compensation tied to key financial, safety and individual performance metrics. | ✘ | Prohibition on Hedging and Derivative Transactions. We prohibit directors and officers from engaging in hedging or derivative transactions involving company securities. |

✔ | Clawback Policy. We have adopted a “clawback” policy that permits the company to recoup cash and equity incentive compensation in certain situations if the financial statements covering the reporting period to which such compensation relates must be restated. | ✘ | No Income or Excise Tax Gross-Ups. The company renegotiated the change in control agreements with executive officers to eliminate all excise tax gross-up provisions effective January 1, 2018. We also do not pay tax gross-ups on any perquisites. |

✔ | Robust Stock Ownership Guidelines. We require our directors and executive officers to hold stock and full-value equity interests at substantial levels. Each executive or director has a five-year period from the later of his or her appointment or July 31, 2017 to come into compliance with these guidelines. | ✘ | Effective January 1, 2018, Salaries for Executives and Annual Cash Retainers for Directors Reduced by 15%. In support of our continuing cost-cutting efforts, we approved a reduction in salary of at least 15% for our named executive officers and a 15% reduction in the annual cash retainers paid to our non-employee directors, effective January 1, 2018. |

✔ | Risk Mitigation. Our compensation plans are designed to mitigate risk exposure through caps on the maximum level of short-term incentives, clawback provisions, multiple performance metrics and board of directors and management processes to identify and address risk. | ✘ | Decrease in Maximum Possible Payouts under STI Plan for 2018. As part of our continuing efforts to contain costs, the compensation committee reduced the overall maximum payout under the STI plan for 2018 from 150% of target to 118.75% of target. |

✔ | Independent Consultant. The compensation committee has its own independent executive compensation consultant, Meridian Compensation Partners, LLC. The consultant reports directly to the committee and does not provide any services to management. | ✘ | Company Matching Contributions and SERP Accruals Suspended Effective January 1, 2018. In support of our continuing cost-cutting efforts, we suspended any additional benefit accruals under our Supplemental Executive Retirement Plan (the “SERP”) and any company matching contributions to the 401(k) Savings Plan and Supplemental Savings Plan effective January 1, 2018. |

✔ | Director Independence. As of the record date, eight of our ten directors are independent and our compensation committee is made up entirely of independent directors. | ✘ | Limited Executive Perquisites. We offer our executives very few perquisites that are not generally available to all employees. |

2

Agenda and Voting Recommendations

Proposal | Description | Board Vote Recommendation | Page |

1 | Election of directors | FOR each nominee | |

2 | Advisory vote on executive compensation | FOR | |

3 | Ratification of selection of independent registered public accounting firm | FOR |

Director Highlights (page 11)

Name | Age | Director Since | Principal Occupation | Independent | Board Committees |

Thomas R. Bates, Jr. | 69 | 2017 | Director and Chairman of the board of each of Tidewater Inc. and Independence Contract Drilling, Inc. | Yes | Compensation Nominating and Corporate Governance |

Alan J. Carr | 48 | 2017 | Chief Executive Officer of Drivetrain, LLC | Yes | Compensation Nominating and Corporate Governance (chair) |

Randee E. Day | 70 | 2017 | Chief Executive Officer of Goldin Maritime, LLC | Yes | Audit Nominating and Corporate Governance |

Dick Fagerstal | 58 | 2017 | Chairman and Chief Executive Officer of Global Marine Holdings LLC and Executive Chairman of Global Marine Systems Ltd. | Yes | Audit (chair) |

Steven L. Newman | 54 | 2017 | Former Chief Executive Officer and director of Transocean Ltd. and director of Dril-Quip, Inc. and SNC-Lavalin Group Inc. | Yes | Compensation (chair) |

Louis A. Raspino | 66 | 2018 | Former Chairman of Clarion Offshsore Partners | Yes | Audit |

Larry T. Rigdon | 71 | 2017 | Director of Professional Rental Tools, LLC | Yes* | Audit |

John T. Rynd | 61 | 2018 | President and Chief Executive Officer of Tidewater Inc. | No | |

Robert P. Tamburrino | 62 | 2018 | Former Operating Partner for affiliates of Q Investments, L.P. and former Chief Restructuring Officer and member of the Office of Chief Executive at Vantage Drilling | No | |

Kenneth H. Traub | 57 | 2018 | Former Managing Partner of Raging Capital Management, LLC | Yes | Nominating and Corporate Governance |

| * | Mr. Rigdon was not independent during his five-month service as our interim president and chief executive officer and did not serve on any committees during that period (which ended on March 5, 2018). The board has determined that Mr. Rigdon is currently independent and appointed him to serve on the Audit Committee effective November 15, 2018. |

3

QUESTIONS AND ANSWERS ABOUT THE ANNUAL MEETING AND VOTING

| Q: | Why am I receiving these proxy materials? |

| A: | Our board of directors (our “board”) is soliciting your proxy to vote at our 2019 annual meeting because you owned shares of our common stock at the close of business on March 6, 2019, the record date for the meeting, and are entitled to vote those shares at the meeting. This proxy statement, along with a proxy card or a voting instruction form, is being mailed to certain stockholders and will be available online at www.proxyvote.com beginning March 18, 2019. This proxy statement summarizes information relevant to your vote on the matters that will be considered at the annual meeting. You do not need to attend the annual meeting in person to vote your shares. |

| Q: | Why did I receive a one-page “Notice of Internet Availability of Proxy Materials” instead of a full set of proxy materials? |

| A: | Under rules adopted by the Securities and Exchange Commission (the “SEC”), we are electing to furnish proxy materials to certain stockholders online rather than mailing printed copies of those materials. If you received a Notice of Internet Availability of Proxy Materials (“Notice”) by mail, you will not receive a printed copy of our proxy materials unless you request one. Instead, the Notice will instruct you as to how you may access and review the proxy materials online. If you received a Notice by mail and would like to receive a printed copy of our proxy materials, please follow the instructions included in the Notice. |

| Q: | How do I get electronic access to the proxy materials? |

| A: | Our proxy statement and Annual Report on Form 10-K for the year ended December 31, 2018 are available at www.proxyvote.com and also on our website at www.tdw.com under “SEC Filings” in the “Investor Relations” section. |

| Q: | On what matters will I be asked to vote? |

| A: | At the annual meeting, our stockholders will be asked: |

| • | to elect ten (10) directors for a one-year term; |

| • | to approve, on an advisory basis, our executive compensation as disclosed in this proxy statement (the “say-on-pay” vote); |

| • | to ratify the selection of Deloitte & Touche LLP (“Deloitte & Touche”) as our independent registered public accounting firm for fiscal year 2019; and |

| • | to consider any other matter that properly comes before the meeting. |

| Q: | Where and when will the meeting be held? |

| A: | The meeting will be held at SpringHill Suites by Marriott Houston Westchase, 5851 Rogerdale Road, Houston, Texas, on April 30, 2019 at 10:00 a.m., Central Time. |

| Q: | Who is soliciting my proxy? |

| A: | Our board, on behalf of the company, is soliciting your proxy to vote your shares on all matters that you are entitled to vote at our 2019 annual meeting of stockholders. By completing and returning the proxy card or voting instruction form, or by casting your vote by phone or online, you are authorizing the proxy holder designated by the board to vote your shares of common stock at our annual meeting in accordance with your instructions. |

| Q: | How many votes may I cast? |

| A: | With respect to any matter properly presented for a stockholder vote other than the election of directors, you may cast one vote for every share of our common stock that you owned on the record date. With respect to the election of directors, for every share of common stock that you held on the record date, you may cast one vote for each director nominee. |

| Q: | What is the total number of votes that can be cast by all stockholders? |

| A: | On the record date, we had 37,289,713 shares of common stock outstanding, each of which was entitled to one vote per share. |

4

| Q: | I hold warrants to purchase shares of common stock. Am I allowed to vote my warrants? |

| A: | No. A holder of warrants to purchase shares of our common stock does not have any rights as a stockholder, including voting rights, unless and until those warrants are exercised and exchanged for shares of our common stock. |

| Q: | How many shares must be present to hold the meeting? |

| A: | Our bylaws provide that the presence at the meeting, whether in person or by proxy, of a majority of the outstanding shares of our common stock entitled to vote constitutes a “quorum,” which is required to hold the meeting. On the record date, 18,644,857 shares constituted a majority of our outstanding stock entitled to vote at the meeting. |

| Q: | What is the difference between holding shares as a stockholder of record and as a beneficial owner? |

| A: | If your shares are registered in your name with our transfer agent, Computershare, you are the “stockholder of record” with respect to those shares and we have sent the Notice and/or proxy materials directly to you. |

If your shares are held on your behalf in a stock brokerage account or by a bank or other nominee, you are the “beneficial owner” of shares held in “street name” and the Notice and/or proxy materials have been forwarded to you by your broker, bank, or nominee who is considered, with respect to those shares, the stockholder of record. As the beneficial owner, you have the right to instruct your broker, bank, or nominee as to how to vote your shares by using the voting instruction form included in the mailing or by following their instructions for voting by telephone or the internet.

| Q: | How do I vote? |

| A: | You may vote using any of the following methods: |

| • | Proxy card or voting instruction form: If your shares are registered in your name and you receive a printed copy of our proxy materials, you may vote your shares by completing, signing, and dating the proxy card and then returning it in the enclosed prepaid envelope. If your shares are held in street name by a broker, bank, or other nominee, that entity should have provided you with a voting instruction form that will set forth the procedures you should follow to cast your vote. |

| • | By telephone or online: If your shares are registered in your name, you may also vote by telephone by calling 1-800-690-6903 or online at www.proxyvote.com by following the instructions at that site. The availability of telephone and online voting for beneficial owners whose shares are held in street name will depend on the voting procedures adopted by your broker, bank, or nominee. Therefore, we recommend that you follow the instructions in the materials they have provided to you. |

| • | In person at the annual meeting: You may also vote in person at the annual meeting, either by attending the meeting yourself or authorizing a representative to attend the meeting on your behalf. You may also execute a proper proxy designating that person to act as your representative at the meeting. If you are a beneficial owner of shares, you must obtain a proxy from your broker, bank, or nominee naming you as the proxy holder and present it to the inspector of election with your ballot when you vote at the annual meeting. |

| Q: | Once I deliver my proxy, can I revoke or change my vote? |

| A: | Yes. You may revoke or change your proxy at any time before it is voted at the meeting by delivering a written revocation notice to our Secretary or by delivering an executed replacement proxy by the voting deadline. In addition, if you vote in person at the meeting, you will revoke any prior proxy. Your attendance alone at the annual meeting will not be enough to revoke your proxy. |

| Q: | Can my shares be voted if I do not return the proxy card and do not attend the meeting in person? |

| A: | If you hold shares in street name and you do not provide voting instructions to your broker, bank, or nominee, your shares will not be voted on any proposal that your broker does not have discretionary authority to vote (a “broker non-vote”). Brokers, banks, and other nominees generally only have discretionary authority to vote without instructions from beneficial owners on the ratification of the appointment of an independent registered public accounting firm; they do not have authority to vote in the absence of instructions from beneficial owners on any other matter proposed in this proxy statement. |

5

Shares represented by proxies that include broker non-votes on a given proposal will be considered present at the meeting for purposes of determining a quorum, but those shares will not be considered to be represented at the meeting for purposes of calculating the vote with respect to that proposal.

If you do not vote shares registered in your name, your shares will not be voted. However, the proxy agent may vote your shares if you execute and return a blank or incomplete proxy card (see “What happens if I return a proxy card without voting instructions?” below regarding record holders).

| Q: | What happens if I return a proxy card without voting instructions? |

| A: | If you properly execute and return a proxy or voting instruction form, your stock will be voted as you specify. |

If you are a stockholder of record and you execute and return a blank or incomplete proxy card without voting instructions, the proxy agent will vote your shares (i) FOR each of the ten director nominees, (ii) FOR the say-on-pay vote, and (iii) FOR the ratification of the selection of Deloitte & Touche as our independent registered public accounting firm for fiscal 2019.

If you are a beneficial owner of shares and do not give voting instructions to your broker, bank, or nominee, your broker, bank, or nominee will be entitled to vote your shares only with respect to the ratification of the appointment of Deloitte & Touche as our independent registered public accounting firm.

| Q: | How does Tidewater recommend I vote on each proposal? What vote is required to approve each proposal? What effect do abstentions and broker non-votes have on each proposal? |

| A: | The following chart explains what your voting options are with regard to each matter proposed for a vote at the annual meeting, how we recommend that you vote, what vote is required for that proposal to be approved, and how abstentions and broker non-votes affect the outcome of that vote. |

Proposal | Your Voting Options | Voting Recommendation of the Board | Vote Required for Approval | Effect of Abstentions | Effect of Broker Non- Votes |

Election of directors | You may vote “FOR” or “AGAINST” each nominee or choose to “ABSTAIN” from voting. | The board recommends you vote FOR each of the ten nominees. | each nominee is elected by a majority of votes cast | no effect | no effect |

Say-on-pay vote (advisory) | You may vote “FOR” or “AGAINST” this proposal or choose to “ABSTAIN” from voting. | The board recommends you vote FOR approval of our executive compensation as disclosed in this proxy statement. | affirmative vote of a majority of the shares present in person or represented by proxy and entitled to vote on the matter | will count as a vote AGAINST this proposal | no effect |

Ratification of our selection of Deloitte & Touche as our auditors | You may vote “FOR” or “AGAINST” this proposal or choose to “ABSTAIN” from voting. | The board recommends you vote FOR ratification of our selection of auditors. | affirmative vote of a majority of the shares present in person or represented by proxy and entitled to vote on the matter | will count as a vote AGAINST this proposal | not applicable (this is a routine matter for which brokers have discretionary voting authority) |

Majority Voting in Director Elections. Our directors are elected by majority vote except in the event of a contested election, in which case a plurality standard will apply. If in an uncontested election, an existing director receives a greater number of “AGAINST” votes than “FOR” votes, he or she is required to tender his or her resignation to the board. The board’s nominating and corporate governance committee will make a recommendation to the board on whether to accept or reject the resignation, or whether other action should be taken. The board will act on the committee’s recommendation and disclose its decision and rationale within 90 days from the certification of the election results. You may find more information about our majority voting policy in this proxy statement under the heading “Proposal 1: Election of Directors – Majority Voting.”

6

Any Other Matters. Any other matter that properly comes before the annual meeting will be decided by the vote of the holders of a majority of the shares of common stock present in person or represented by proxy, except where a different vote is required by statute, our certificate of incorporation, or our bylaws.

| Q: | Who pays for soliciting proxies? |

| A: | We pay all costs of soliciting proxies. In addition to solicitations by mail, we have retained Alliance Advisors to aid in the solicitation of proxies for our 2019 annual meeting at an estimated fee of $18,000. Our directors, officers, and employees, in the course of their employment and for no additional compensation, may request the return of proxies by mail, telephone, internet, personal interview, or other means. We are also requesting that banks, brokerage houses, and other nominees or fiduciaries forward the soliciting materials to their principals and that they obtain authorization for the execution of proxies. We will reimburse them for their reasonable expenses. |

| Q: | What is “householding”? |

| A: | Under the rules adopted by the SEC, we may deliver a single set of proxy materials to one address shared by two or more of our stockholders. This delivery method is referred to as “householding” and can result in significant cost savings. To take advantage of this opportunity, we have delivered only one set of proxy materials to multiple stockholders who share the same address, unless we received contrary instructions from the impacted stockholders prior to the mailing date. We agree to deliver promptly, upon written or oral request, a separate copy of the proxy materials, as requested, to any stockholder at the shared address to which a single copy of these documents was delivered. If you prefer to receive separate copies of the proxy statement or annual report, contact Broadridge Financial Solutions, Inc. by calling 1-866-540-7095 or in writing at 51 Mercedes Way, Edgewood, New York 11717, Attention: Householding Department. |

In addition, if you currently are a stockholder who shares an address with another stockholder and would like to receive only one copy of future notices and proxy materials for your household, you may notify your broker if your shares are held in a brokerage account or, if you are a stockholder of record, you may notify us through Broadridge at the above-listed phone number or address.

| Q: | Could other matters be considered and voted upon at the meeting? |

| A: | Our board does not expect to bring any other matter before the annual meeting and it is not aware of any other matter that may be considered at the meeting. In addition, under our bylaws, the time has expired for any stockholder to properly bring a matter before the meeting. However, in the unexpected event that any other matter does properly come before the meeting, subject to applicable SEC rules, the proxy holder will vote the proxies in his discretion. |

| Q: | What happens if the meeting is postponed or adjourned? |

| A: | Your proxy will still be valid and may be voted at the postponed or adjourned meeting. You will still have the right to change or revoke your proxy until it is voted. |

| Q: | When will the voting results be announced? |

| A: | We will announce preliminary voting results at the annual meeting. We will also disclose the voting results on a Form 8-K filed with the SEC within four business days after the annual meeting, which will also be available on our website. |

7

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS

The table below shows the name, address and stock ownership of each person known by us to beneficially own more than 5% of our common stock as of March 6, 2019.

Name and Address of Beneficial Owner | Amount and Nature of Beneficial Ownership | Percent of Class(1) | ||||

Raging Capital Management, LLC | 2,585,057 | (2) | 6.90 | % | ||

William C. Martin Ten Princeton Avenue Post Office Box 228 Rocky Hill, New Jersey 08553 | ||||||

Third Avenue Management LLC 622 Third Avenue, 32nd Floor New York, New York 10017 | 2,408,549 | (3) | 6.46 | % | ||

American International Group, Inc. 175 Water Street New York, New York 10038 | 2,369,809 | (4) | 6.36 | % | ||

T. Rowe Price Associates 100 East Pratt Street Baltimore, Maryland 21202 | 2,345,945 | (5) | 6.29 | % | ||

Captain Q, LLC | 2,116,109 | (6) | 5.65 | % | ||

Q Global Capital Management, L.P. | ||||||

Renegade Swish, LLC 301 Commerce Street, Suite 3200 Fort Worth, Texas 76102 | ||||||

BlackRock, Inc. 55 East 52nd Street New York, New York 10055 | 2,057,623 | (7) | 5.52 | % | ||

Wells Fargo & Company 420 Montgomery Street San Francisco, California 94163 | 2,000,439 | (8) | 5.36 | % | ||

| (1) | Based on 37,289,713 shares of common stock outstanding on March 6, 2019. |

| (2) | Based on a Schedule 13D/A jointly filed with the SEC on February 25, 2019 by Raging Capital Management, LLC (“Raging Capital”) and William C. Martin. Mr. Martin is Chairman, Chief Investment Officer, and Managing Member of Raging Capital. Mr. Martin and Raging Capital share voting and dispositive power over (a) 2,413,379 shares held by a limited partnership for which Raging Capital serves as general partner and (b) 170,975 shares held by two investment funds for which Raging Capital serves as investment manager (164,889 of which are shares issuable upon exercise of Legacy GLF Equity Warrants). Mr. Martin holds sole voting and dispositive power over the remaining 703 shares reported in the table above (644 of which are shares issuable upon exercise of Legacy GLF Equity Warrants). |

| (3) | Based on a Schedule 13G/A filed with the SEC on February 13, 2019 by Third Avenue Management LLC, as investment adviser to several investment companies, reports sole voting and dispositive power over all reported shares. |

| (4) | Based on a Schedule 13G/A filed with the SEC on February 13, 2019 by American International Group, Inc., which has sole voting and dispositive power over 2,341,223 shares and shares voting and dispositive power over the remaining 28,586 shares with its wholly-owned subsidiary, SunAmerica Asset Management, LLC, as investment adviser to an investment company. |

| (5) | Based on a Schedule 13G/A filed with the SEC on February 14, 2019 by T. Rowe Price Associates, a registered investment advisor, which has sole voting power over 660,533 shares and sole dispositive power over all reported shares. |

| (6) | Based on a Schedule 13G jointly filed with the SEC on February 14, 2019 by Captain Q, LLC (“Captain Q”), Q Global Capital Management, L.P. (“QGCM”), and Renegade Swish, LLC (“RS”). Captain Q has sole voting and dispositive power over 360,946 shares, consisting of 221,739 shares held by an entity for which it serves as sole general partner and 139,207 shares issuable upon exercise of TDW Equity Warrants. QGCM has sole voting and dispositive power over another 1,748,701 shares that are held by an entity for which QGCM serves as sole investment manager. RS, as sole manager of both Captain Q and QGCM and as the direct holder of the remaining 6,462 shares, may be deemed to have sole voting and dispositive power over all reported shares. |

| (7) | Based on a Schedule 13G filed with the SEC on February 8, 2019, by BlackRock, Inc., which has sole voting power over 1,990,023 shares and sole dispositive power over all reported shares. |

| (8) | Based on a Schedule 13G/A filed with the SEC on January 22, 2019, by Wells Fargo & Company (reporting ownership on a consolidated basis), which has sole voting and dispositive power over 1,790,718 shares and shared voting and dispositive power over the remaining 209,721 shares. |

8

SECURITY OWNERSHIP OF MANAGEMENT

The following table sets forth the beneficial ownership of our common stock as of March 6, 2019 by each director, by each executive officer named in the 2018 Summary Compensation Table (our “named executives” or “NEOs”), and by all directors and executive officers as a group. Unless otherwise indicated, each person has sole voting and investment power with respect to all shares of our common stock beneficially owned by him or her.

Name of Beneficial Owner | Amount and Nature of Beneficial Ownership | Percent of Class of Common Stock(1) | Restricted Stock Units(2) | ||||||

Directors | |||||||||

Thomas R. Bates, Jr. | 5,870 | * | 3,771 | ||||||

Alan J. Carr | 5,870 | * | 3,771 | ||||||

Randee E. Day | 5,870 | * | 3,771 | ||||||

Dick Fagerstal | 5,870 | * | 3,771 | ||||||

Steven L. Newman | 5,870 | * | 3,771 | ||||||

Louis A. Raspino | 7,540 | * | 3,126 | ||||||

Larry T. Rigdon(3) | 15,745 | * | 3,771 | ||||||

John T. Rynd(3) | — | * | 106,741 | ||||||

Robert P. Tamburrino | — | * | 3,126 | ||||||

Kenneth H. Traub | 6,462 | * | 3,126 | ||||||

Named Executives(4) | |||||||||

Quintin V. Kneen | 24,888 | (5) | * | 86,768 | |||||

Quinn P. Fanning(6) | 157,341 | (7) | * | — | |||||

Jeffrey A. Gorski | 45,135 | (7) | * | 129,577 | |||||

Bruce D. Lundstrom | 45,827 | (7) | * | 129,577 | |||||

All directors and executive officers as a group (13 persons) | 174,947 | (8) | * | 497,261 | |||||

| * | Less than 1.0%. |

| (1) | Based on 37,289,713 shares of common stock outstanding on March 6, 2019, and includes for each person and group the number of shares that person or group has the right to acquire within 60 days of such date. |

| (2) | Reflects the number of restricted stock units held by each director or executive officer that will not vest within 60 days of March 6, 2019 and thus are not included in his or her beneficial ownership calculation. |

| (3) | Each of Messrs. Rynd and Rigdon was a named executive for fiscal 2018. Mr. Rynd was appointed as president, chief executive officer, and a director of Tidewater effective March 5, 2018. Mr. Rigdon, a sitting director, served as Tidewater’s president and chief executive officer on an interim basis for a five-month period from October 15, 2017 until Mr. Rynd’s appointment. |

| (4) | Information regarding shares beneficially owned by Messrs. Rigdon and Rynd, each of whom was a named executive for fiscal 2018 in addition to Messrs. Kneen, Fanning, Gorski, and Lundstrom, appears immediately above under the caption “Directors.” |

| (5) | Includes 8,025 shares acquirable within 60 days upon exercise of Legacy GLF Equity Warrants and 16,121 time-based RSUs that will vest on April 13, 2019. |

| (6) | Mr. Fanning, who served as our Executive Vice President and Chief Financial Officer, stepped down as Chief Financial Officer effective November 15, 2018 and from all other positions with the company effective February 28, 2019. |

| (7) | The total number of shares shown as beneficially owned by each of these named executives includes the following: |

Named Executive | Shares Held in 401(k) Savings Plan Account | Shares Acquirable within 60 days upon Exercise of Series A Warrants | Shares Acquirable within 60 days upon Exercise of Series B Warrants | ||||||

Mr. Fanning | 52 | 1,869 | 2,020 | ||||||

Mr. Gorski | 19 | 2,158 | 2,333 | ||||||

Mr. Lundstrom | 57 | 2,401 | 2,595 | ||||||

| (8) | Includes (a) 17,512 shares of Tidewater common stock that executive officers have the right to acquire within 60 days through the exercise of warrants, (b) 16,121 shares that are acquirable within 60 days of the record date through the vesting of RSUs, and (c) 76 shares attributable to such persons’ accounts in Tidewater’s 401(k) Savings Plan. |

9

PROPOSAL 1: ELECTION OF DIRECTORS

As provided by our bylaws, our directors are elected annually. We currently have ten directors, six of whom joined our board immediately following our July 31, 2017 restructuring (the “restructuring”), Mr. Rynd, our president and CEO, who joined us in March of 2018, and three of whom joined our board immediately following the business combination with GulfMark (the “GulfMark designated directors”). Our bylaws require that, subject to applicable law and the directors’ fiduciary duties, each of the three GulfMark designated directors (or a replacement candidate as provided in the bylaws) will be included in the slate of nominees recommended by our board to stockholders for election at the 2019 annual meeting.

Upon the recommendation of our nominating and corporate governance committee, our board has re-nominated each of our ten current board members to serve another term as director. Each director elected at the 2019 annual meeting will serve a one-year term beginning at the annual meeting and ending when his or her successor, if any, is elected or appointed. Assuming stockholders elect all of these director nominees at the annual meeting, our board will continue to have ten directors.

We intend to vote the proxies received in response to this solicitation “FOR” the election of each of the nominees. If, contrary to our present expectations, any nominee cannot or will not serve, we intend to vote the proxies “FOR” the election of the other nominees and proxies may be voted for any substitute nominee of our board. Each nominee has consented to being named as a nominee in this proxy statement and to serve as a director if elected. Our board has no information or reason to believe that any nominee will not be a candidate at the time of the annual meeting or, if elected, will be unable or unwilling to serve as a director. In no event will the proxies be voted for more than ten nominees.

Majority Voting. Our directors are elected by majority vote. Any director who stands for re-election in an uncontested election and who receives a greater number of “AGAINST” votes than “FOR” votes must tender his or her resignation to the board. Our board’s nominating and corporate governance committee is required to promptly consider and recommend to our board whether to accept the tendered resignation. Our board will then act on the committee’s recommendation and disclose its decision and rationale within 90 days from the certification of the election results. We would then promptly and publicly disclose the board’s findings and final decision in a current report on Form 8-K filed with the SEC. A copy of our Corporate Governance Policy, which includes our majority voting policy, may be obtained as described under “Corporate Governance – Availability of Corporate Governance Materials.” Abstentions and broker non-votes will have no effect on this proposal.

Our board of directors recommends that you vote “FOR” each of the following ten nominees: Thomas R. Bates, Jr., Alan J. Carr, Randee E. Day, Dick Fagerstal, Steven L. Newman, Louis A. Raspino, Larry T. Rigdon, John T. Rynd, Robert P. Tamburrino, and Kenneth H. Traub.

10

A biography of each director nominee is set forth below. Each director nominee’s biography contains information regarding that person’s service as a director, business experience, other public company directorships held currently or at any time during the last five years, and the nominee’s experiences, qualifications, attributes, or skills that led the nominating and corporate governance committee and our board to determine that he or she should serve as a director for our company. The information in each biography is presented as of March 6, 2019.

Name, Age and Position | Business and Leadership Experience, Skills, and Qualifications | Tidewater Director since |

Thomas R. Bates, Jr., 69 Chair of the Board Member of the Compensation Committee and Nominating and Corporate Governance Committee | Business and Leadership Experience: Mr. Bates has been an Adjunct Professor at the Neeley School of Business at Texas Christian University since January 2011 and currently serves on the Advisory Board for the Energy MBA Program. Mr. Bates began his career with Shell Oil Company where he was responsible for aspects of drilling research and operations. He served as President of the Anadrill division of Schlumberger Limited from 1992 to 1997, Chief Executive Officer of Weatherford Enterra, Inc. from 1997 to 1998, Senior Vice President and Discovery Group President of Baker Hughes Incorporated from 1998 to 2000, and Managing Director and Senior Advisor of Lime Rock Partners from 2002 to 2012. Mr. Bates holds B.S.E., M.S.E., and Ph.D. degrees in Mechanical Engineering from the University of Michigan. Mr. Bates currently serves as Chairman and Director of Independence Contract Drilling, Inc. He also serves as Chairman and Director of Vantage Drilling International, which trades on the OTC. Mr. Bates also serves on the boards of Alacer Gold Corporation, and TETRA Technologies, Inc. He previously served on the boards of FTS International Inc., T-3 Energy Services, Inc., Hercules Offshore, Inc. and NATCO Group, Inc. Skills and Qualifications: With 40 years of executive and board-level leadership in the oil and gas industry, Mr. Bates brings valuable insight to our board. His extensive knowledge of the industry and decades of board service to publicly-traded, multinational companies make Mr. Bates well-qualified to lead our board. | 2017 |

Alan J. Carr, 48 Chair of the Nominating and Corporate Governance Committee Member of the Compensation Committee | Business and Leadership Experience: Mr. Carr has served as the Chief Executive Officer and Managing Member of Drivetrain, LLC, a fiduciary services firm which supports the investment community, since 2013. Mr. Carr practiced as a corporate restructuring attorney at Ravin, Sarasohn, Baumgarten, Fisch & Rosen from 1995 to 1997 and at Skadden, Arps, Slate, Meagher & Flom LLP from 1997 to 2003. From 2003 to 2013, he served as the Managing Director at Strategic Value Partners LLC, an investment manager for hedge funds and private equity funds. Mr. Carr holds a B.A. in Economics from Brandeis University and a J.D. from Tulane Law School. Mr. Carr currently serves on the boards of TEAC Corporation, Verso Corporation, and Midstates Petroleum Company. He also serves on the board of Sears Holdings Corp., which trades on the OTC. However, Mr. Carr will not stand for reelection as a director of TEAC Corporation at its 2019 annual meeting or as a director of Sears Holdings Corp. at its next annual meeting. Skills and Qualifications: Mr. Carr brings to our board significant experience with corporate restructurings. In addition, our board benefits from the significant financial and investment knowledge he has acquired through his experience with private equity investment. Mr. Carr’s corporate governance expertise and legal background contribute to our board’s ability to evaluate the risks and corporate opportunities in our industry. | 2017 |

11

Name, Age and Position | Business and Leadership Experience, Skills, and Qualifications | Tidewater Director since |

Randee E. Day, 70 Member of the Audit Committee and Nominating and Corporate Governance Committee | Business and Leadership Experience: Ms. Day has served as the Chief Executive Officer of Goldin Maritime, LLC, since 2016. She previously led the boutique restructuring and advisory firm Day & Partners, LLC from 2011 to 2016; and in 2011, she served as the interim Chief Executive Officer of DHT Maritime, Inc. Ms. Day served as a Managing Director at the Seabury Group, a transportation advisory firm from 2004 to 2010, where she led the maritime practice and was the Division Head of JP Morgan’s shipping group in New York from 1978 to 1985. Ms. Day currently serves as a director on the boards of Eagle Bulk Shipping Inc. and International Seaways, Inc. She has previously served on the boards of numerous public companies, including TBS International Ltd., Ocean Rig ASA, DHT Maritime Inc. and Excel Maritime. Ms. Day is a graduate of the School of International Relations at the University of Southern California and undertook graduate business studies at The George Washington University. In December 2014, she graduated from the Senior Executives in National and International Security Program at the Kennedy School at Harvard University. Skills and Qualifications: Ms. Day has considerable executive management, business development, and corporate restructuring experience. Her expertise in many aspects of the maritime transportation industry adds significant value to our board’s knowledge base. | 2017 |

Dick Fagerstal, 58 Chair of the Audit Committee | Business and Leadership Experience: Mr. Fagerstal serves as Chairman and Chief Executive Officer of Global Marine Holdings LLC and Executive Chairman of Global Marine Systems Ltd., positions he has held since 2014. He served as an independent director of Frontier Oil Corporation, Manila, Philippines from 2014 to 2017. Mr. Fagerstal previously held the positions of Senior Vice President, Finance & Corporate Development from 2003 to 2014 and Vice President Finance & Treasurer from 1997 to 2003 at SEACOR Holdings, Inc. Mr. Fagerstal held the positions of Executive Vice President, Chief Financial Officer and director of Era Group Inc. from 2011 to 2012 and was the Senior Vice President and Chief Financial Officer and director of Chiles Offshore Inc. from 1997 to 2002. Prior to that time, he served as a senior banker at DNB ASA in New York from 1986 to 1997. Prior to his business career, Mr. Fagerstal served as an officer in the Special Air Service unit of the Swedish Defense Forces from 1979 to 1983. Mr. Fagerstal received a B.S. in Economics from the University of Gothenburg in 1984 and an M.B.A. in Finance, as a Fulbright Scholar, from New York University in 1986. Skills and Qualifications: Mr. Fagerstal brings a strong finance and accounting background to our board. Given the nature and scope of our operations, his extensive international experience and considerable knowledge of the energy industry contributes to our board’s collective ability to monitor the risks and challenges facing our company. | 2017 |

12

Name, Age and Position | Business and Leadership Experience, Skills, and Qualifications | Tidewater Director since |

Steven L. Newman, 54 Chair of the Compensation Committee | Business and Leadership Experience: Mr. Newman served as Chief Executive Officer at Transocean Ltd. from March 2010 to February 2015 and as President from May 2008 to February 2015. He served as the Chief Operating Officer of Transocean Ltd. from May 2008 to November 2009 and held various other positions with Transocean beginning in 1994. Prior to working with Transocean, he served as a Financial Analyst at Chevron from 1992 to 1994, and was a Reservoir Engineer with Mobil E&P, US from 1989 to 1990. Mr. Newman currently serves as a director of Dril-Quip, Inc. and of SNC-Lavalin Group Inc. He previously served as a director of Transocean Ltd. and of Bumi Armada Berhad. Mr. Newman received a B.S. in Petroleum Engineering from the Colorado School of Mines and an MBA from the Harvard University Graduate School of Business. Skills and Qualifications: Mr. Newman has considerable operational and executive leadership experience in the energy sector. He brings extensive management and business experience to our board as well as a deep understanding of complex issues facing publicly-traded companies in the offshore oilfield services industry. | 2017 |

Louis A. Raspino, 66 Member of the Audit Committee | Business and Leadership Experience: Mr. Raspino’s career has spanned almost 40 years in the energy industry, most recently as Chairman of Clarion Offshore Partners, a partnership with Blackstone that served as its platform for pursuing worldwide investments in the offshore oil & gas services sector, from October 2015 until October 2017. Mr. Raspino served as President, Chief Executive Officer and a director of Pride International, Inc. from June 2005 until the company merged with Ensco plc in May 2011 and as its Executive Vice President and Chief Financial Officer from December 2003 until June 2005. From July 2001 until December 2003, he served as Senior Vice President, Finance and Chief Financial Officer of Grant Prideco, Inc. and from February 1999 until March 2001, he served as Vice President of Finance at Halliburton. Prior to joining Haliburton, Mr. Raspino served as Senior Vice President at Burlington Resources, Inc. from October 1997 until July 1998. From 1978 until its merger with Burlington Resources, Inc. in 1997, he held a variety of positions at Louisiana Land and Exploration Company, most recently as Senior Vice President, Finance and Administration and Chief Financial Officer. Mr. Raspino previously served as a director of Chesapeake Energy Corporation and chairman of its audit committee from March 2013 until March 2016, and as a director of Dresser-Rand Group, Inc., where he served as chairman of the compensation committee and member of the audit committee, from December 2005 until its merger into Siemens in June 2015. He has served as a director of Forum Energy Technologies, an NYSE-listed global oilfield products company, since January 2012 and currently serves as the chairman of its compensation committee. Mr. Raspino also currently serves on the board of The American Bureau of Shipping, where he is a member of the audit and compensation committees. Mr. Raspino served as Chairman of the GulfMark board from November 2017 until consummation of the business combination. Skills and Qualifications: Having served in executive leadership roles at several energy companies, including both the chief executive officer and chief financial officer positions, Mr. Raspino brings in-depth operational and financial expertise to our board. In addition, his service on a variety of oil and gas industry boards provides our board with key and timely insights into industry conditions and trends. | 2018 |

13

Name, Age and Position | Business and Leadership Experience, Skills, and Qualifications | Tidewater Director since |

Larry T. Rigdon, 71 Member of the Audit Committee (since November 2018) Former Interim President and CEO (October 2017-March 2018) | Business and Leadership Experience: Mr. Rigdon, who was initially appointed to serve as an independent director in connection with our restructuring, served as Tidewater’s interim President and Chief Executive Officer between October 16, 2017 and March 5, 2018. He has nearly 40 years of experience in the offshore oil and gas industry. Mr. Rigdon worked as a consultant for FTI Consulting from 2015 to 2016 and for Duff and Phelps, LLC from 2010 to 2011. He served as the Chairman and Chief Executive Officer of Rigdon Marine from 2002 to 2008. Previously at Tidewater, Mr. Rigdon served as an Executive Vice President from 2000 to 2002, a Senior Vice President from 1997 to 2000, and a Vice President from 1992 to 1997. Before working at Tidewater, he served as Vice President at Zapata Gulf Marine from 1985 to 1992, and in various capacities, including Vice President of Domestic Divisions from 1983 to 1985, at Gulf Fleet Marine from 1977 to 1985. Mr. Rigdon currently serves as a director of Professional Rental Tools, LLC. He formerly served as a director of Jackson Offshore Holdings, Terresolve Technologies, GulfMark Offshore, and Rigdon Marine. Skills and Qualifications: Mr. Rigdon has considerable leadership experience in the maritime transportation industry and brings to our board a thorough understanding of the strategic and operational challenges facing our company specifically and our industry overall. His experience founding new businesses provides an entrepreneurial viewpoint and his successful completion of mergers and acquisitions contributes to the board’s ability to evaluate those opportunities. | 2017 |

John T. Rynd, 61 | Business and Leadership Experience: Mr. Rynd was appointed to serve as Tidewater’s president, chief executive officer, and a director effective March 5, 2018. He served as an outside director of Hornbeck Offshore, Inc. from 2011 to February 2018. From 2008 through 2016, Mr. Rynd served as President, Chief Executive Officer, and a director of Hercules Offshore, Inc., a publicly traded global provider of offshore contract drilling and liftboat services (“Hercules”). On August 13, 2015, Hercules and certain of its subsidiaries filed voluntary petitions for relief under the provisions of Chapter 11 of the United States Bankruptcy Code in the United States Bankruptcy Court for the District of Delaware. On November 6, 2015, Hercules emerged from bankruptcy. On June 5, 2016, Hercules again filed voluntary petitions for relief under Chapter 11 of the United States Bankruptcy Code in the United States Bankruptcy Court for the District of Delaware. On December 2, 2016, Hercules’ assets were transferred to the HERO Liquidating Trust, and the common stock was canceled pursuant to its Chapter 11 plan. Prior to his time with Hercules, Mr. Rynd spent 11 years with Noble Drilling Services, Inc., where he served in a variety of management roles. Earlier in his career, he served in various roles of increasing levels of responsibility with Chiles Offshore and Rowan Companies. Mr. Rynd served as Chairman of the National Ocean Industries Association (NOIA) from 2014-15 and currently holds an Ex-Officio position on the Executive Committee. Skills and Qualifications: Mr. Rynd’s many years of executive and board level leadership make him an ideal person to serve on our board. Given the variety of leadership roles he has held over his career, Mr. Rynd brings to the board a deep understanding of the operations of a publicly-traded company in the offshore oilfield services industry. In addition, in his position as our president and chief executive officer, Mr. Rynd serves as a valuable liaison between our board and management team. | 2018 |

14

Name, Age and Position | Business and Leadership Experience, Skills, and Qualifications | Tidewater Director since |

Robert P. Tamburrino, 62 | Business and Leadership Experience: Mr. Tamburrino served as an Operating Partner for affiliates of Q Investments, L.P. from September 2006 through June 2016. Mr. Tamburrino served as the Chief Restructuring Officer and member of the Office of Chief Executive at Vantage Drilling International from March 21, 2016 to June 23, 2016. He served as the president and manager of Key 3 Casting, LLC from November 2009 through December 2013, following his roles as the Chief Executive Officer, President and Chief Operating Officer of INTERMET Corporation, and Chief Executive Officer and Chairman of the Board of Environmental Systems Products, an auto emissions testing business. He served as the Chief Financial Officer of Milgard Manufacturing, a Masco company from September 2004 through August 2006. He served in the Chief Financial Officer, Treasurer and Vice President, and Chief Operating Officer roles of Old Ladder Co. (DE), Inc. (also known as Werner Holding Co. (DE), Inc.) during December 1998 to April 2002. Prior to joining Werner Holding, he served in financial roles for Usinor subsidiaries from 1991 through 1998 including Chief Financial Officer for the steel service center group of Usinor, Senior Vice President and Chief Financial Officer of Francosteel Corporation, and Executive Vice President and Chief Financial Officer of Edgcomb Metals Company. He held financial and Chief Executive Officer positions with Rome Cable Corp., a manufacturer and distributor of copper electrical wire and cable from 1984 to 1990 and was employed by KPMG Peat Marwick from 1978 to 1984. Mr. Tamburrino is a certified public account. Since 2016, Mr. Tamburrino has also served in advisory and consulting roles in the energy sector. He recently served on the boards of directors of SVP Worldwide (also known as Singer Company) and Alloy Die Casting. He currently serves as a director and chair of the finance committee for the Board of Directors of Basset Health Care Network, a non-profit. He graduated from Clarkson University, and has a Master of Business Administration from Columbia University. Skills and Qualifications: Mr. Tamburrino has considerable depth of experience in the areas of restructuring and integration. He brings to the board a perspective that will be invaluable during the critical post-business combination integration period as well as going forward to evaluate future acquisition opportunities. | 2018 |

15

Name, Age and Position | Business and Leadership Experience, Skills, and Qualifications | Tidewater Director since |

Kenneth H. Traub, 57 Member of the Nominating and Corporate Governance Committee | Business and Leadership Experience: Mr. Traub served as a Managing Partner of Raging Capital Management, LLC, a diversified investment firm, from December 2015 to January 2019. Prior to joining Raging Capital Management, LLC, he served as President and Chief Executive Officer of Ethos Management, LLC from 2009 through 2015. From 1999 until its acquisition by JDS Uniphase Corp. (“JDSU”) in 2008, Mr. Traub served as President and Chief Executive Officer of American Bank Note Holographics, Inc. (“ABNH”), a leading global supplier of optical security devices for the protection of documents and products against counterfeiting. Following the sale of ABNH, he served as Vice President of JDSU, a global leader in optical technologies and telecommunications. Mr. Traub currently serves on the boards of directors of the following public companies: (i) DSP Group, Inc., (NASDAQ-DSPG), a leading supplier of wireless chipset solutions for converged communications, since 2012, and where Mr. Traub has served as Chairman since 2017, (ii) Intermolecular, Inc., (NASDAQ-IMI), an innovator in materials sciences, since 2016 and where Mr. Traub has served as Chairman since 2018 and (iii) Immersion Corporation (NASDAQ: IMMR), a leading provider of haptics technology, since 2018. Mr. Traub has previously served on the boards of numerous companies including MIPS Technologies, Inc., a provider of industry standard processor architectures and cores, from 2011 until the company was sold in 2013, Xyratex Limited, a leading supplier of data storage technologies, from 2013 until the company was sold in 2014, Vitesse Semiconductor Corporation, a supplier of integrated circuit solutions for next-generation carrier and enterprise networks, from 2013 until the company was sold in 2015, Athersys, Inc., a biotechnology company engaged in the discovery and development of therapeutic product candidates, from 2012 to 2016, A. M. Castle & Co., a specialty metals distribution company from, 2014 to 2016, IDW Media Holdings, Inc., a diversified media company, from 2016 to 2018, and as Chairman of MRV Communications, Inc., a supplier of communication networking equipment, from 2011 until the company was sold in 2017. Mr. Traub served as a member of the GulfMark board from November 2017 until consummation of the business combination. Mr. Traub earned a B.A. degree from Emory University and an M.B.A. from Harvard Business School. Skills and Qualifications: Mr. Traub’s extensive management background and experience serving on a wide variety of corporate boards enable Mr. Traub to provide valuable financial and transactional expertise and insight to our board. | 2018 |

16

THE BOARD OF DIRECTORS UNANIMOUSLY RECOMMENDS THAT STOCKHOLDERS VOTE “FOR” EACH OF THE TEN NOMINEES FOR DIRECTOR LISTED ABOVE.

Director Nominating Process and Considerations.The nominating and corporate governance committee is responsible for reviewing and evaluating with our board the appropriate skills, experience, and background desired of board members in the context of our business and the then-current composition of our board.

Director Independence. Under our Corporate Governance Policy and the rules of the New York Stock Exchange (“NYSE”), a majority of our directors must be independent. Our board has determined that, as of the record date, each of our director nominees meets the NYSE’s definition of “independence” (discussed in greater detail below under “Board of Directors – Director Independence”), except for Messrs. Rynd and Tamburrino. Mr. Rynd is our president and chief executive officer and, prior to joining our board, Mr. Tamburrino provided consulting services to the company. For more information on director independence, please see the section entitled, “Board of Directors – Director Independence.”

Board Diversity. Our board does not have a formal written policy with regard to the consideration of diversity in identifying director nominees. Our nominating and corporate governance committee charter, however, requires the committee to monitor the composition of the board and its committees and may develop and recommend to the board, if necessary or appropriate, specific criteria for selecting director nominees. In considering the composition of our board as a whole, the committee and the board evaluate the skills and experiences of each candidate to ensure that the specific knowledge, experience, skills, expertise, integrity, analytical ability, diversity, and other characteristics needed to maintain our board’s effectiveness are possessed by an appropriate combination of directors. The committee seeks a diverse group of prospective candidates for board service who possess the requisite characteristics, skills, and experience, taking into consideration the availability of highly qualified candidates; committee workloads and membership needs and anticipated director retirements. Our overarching goal is that the unique skills and experiences of each individual director complement and enhance the overall capabilities of the board.

Neither the committee nor our board have adopted specific criteria for selecting director nominees, preferring to maintain the flexibility to evaluate the board’s needs at any given point in time in light of our company’s business model, strategic plan, and the skillset of the then-current members of the board. However, as evidenced by the biographies of our director nominees that appear above, we believe it is important that our board have individual directors who possess skills in such broad areas as:

| • | strategic planning and business development; |

| • | mergers and acquisitions; |

| • | legal and regulatory compliance; |

| • | finance and accounting matters; |

| • | industry experience and knowledge (particularly in the energy services and maritime sectors), including hands-on operational experience; |

| • | demonstrated leadership of large, complex organizations; |

| • | public company board service; and |

| • | international business. |

Each candidate is evaluated to ensure that he or she possesses personal and professional character and integrity, and each must demonstrate exceptional ability and judgment in his or her respective endeavors. Candidates must possess sufficient time and availability to effectively carry out their duties and responsibilities as a director of our company. The committee may employ professional search firms (for which it would pay a fee) to assist it in identifying potential nominees for board service with the right mix of skills and disciplines.

This year, as in prior years, the committee reviewed the qualifications of each of our current directors as well as the contributions each has made to our board and the company during his or her tenure as a director. The committee recommended each of these ten directors be nominated for an additional one-year term. Subsequently, our board approved this slate of ten director nominees to be submitted for election by our stockholders at the annual meeting.

Consideration of Candidates Recommended by Stockholders. Our bylaws provide that a stockholder of our company entitled to vote for the election of directors may nominate candidates for election to our board at our annual

17

meeting of stockholders by complying with the required notice procedures, as described in greater detail below. The nominating and corporate governance committee’s policy is to consider director candidates recommended by stockholders on the same basis and in the same manner as it considers all director candidates.

No director candidates were recommended by stockholders in time for consideration at the 2019 annual meeting. To be timely for our 2020 annual meeting, a stockholder’s notice must be given in writing and delivered or mailed to the company’s Secretary and received at our principal executive offices no earlier than January 1, 2020 and no later than January 31, 2020.

Stockholder recommendations of nominees are required to be accompanied by, among other things, specific information as to the nominees and as to the stockholder making the nomination or proposal. We may require any proposed nominee to furnish such information as may reasonably be required to determine his or her eligibility to serve as a director of our company. A description of these requirements is set forth in the company’s bylaws, which may be obtained as described under “Corporate Governance – Availability of Corporate Governance Materials.”

18

Our board of directors has adopted corporate governance practices designed to aid the board and management in the fulfillment of their respective duties and responsibilities to our stockholders.

Corporate Governance Policy. Our board has adopted a Corporate Governance Policy, which, together with our certificate of incorporation, bylaws, and board committee charters, form the framework for the governance of our company. The nominating and corporate governance committee is charged with reviewing the Corporate Governance Policy at least annually to assess the continued appropriateness of those guidelines in light of any new regulatory requirements and evolving corporate governance practices. After this review, the committee recommends any proposed changes to the Corporate Governance Policy to the full board for approval.

Code of Business Conduct and Ethics. Our board has also adopted a Code of Business Conduct and Ethics. The Code of Business Conduct and Ethics sets forth principles of ethical and legal conduct to be followed by our directors, officers, and employees. The Code of Business Conduct and Ethics requires any employee who reasonably believes or suspects that any director, officer, or employee has violated the Code of Business Conduct and Ethics, company policy, or applicable law to report such activities to his or her supervisor or to our Chief Compliance Officer (Bruce D. Lundstrom, our General Counsel), either directly or anonymously. We do not tolerate retaliation of any kind against any person who, in good faith, reports any known or suspected improper activities pursuant to the Code of Business Conduct and Ethics or assists with any ensuing investigation.

Our Code of Business Conduct and Ethics also references disclosure controls and procedures required to be followed by all officers and employees involved with the preparation of the company’s SEC filings. These disclosure controls and procedures are designed to enhance the accuracy and completeness of the company’s SEC filings and, among other things, to ensure continued compliance with the Foreign Corrupt Practices Act.

Communicating with Directors. Stockholders and other interested parties may communicate directly with our board, the non-management directors, or any committee or individual director by writing to any one of them in care of our Secretary at 6002 Rogerdale Road, Suite 600, Houston, Texas 77072. Our company or the director contacted will forward the communication to the appropriate director. For more information regarding how to contact the members of our board, please visit our website at www.tdw.com/about-tidewater/corporate-governance/.

Complaint Procedures for Accounting, Auditing, and Financial Related Matters. The audit committee has established procedures for receiving, reviewing, and responding to complaints from any source regarding accounting, internal accounting controls, and auditing matters. The audit committee has also established procedures for the confidential and anonymous submission by employees of concerns regarding questionable accounting or auditing matters. Interested parties may communicate such complaints to the audit committee chair by following the procedures described under the heading “Communicating with Directors” above. Employees may report such complaints by following the procedures outlined in the Code of Business Conduct and Ethics and through other procedures communicated and available to them. As noted above, we do not tolerate retaliation of any kind against any person who, in good faith, submits a complaint or concern under these procedures.

Availability of Corporate Governance Materials. You may access our certificate of incorporation, our bylaws, our Corporate Governance Policy, our Code of Business Conduct and Ethics, and all committee charters under “Corporate Governance” in the “About Tidewater” section of our website at www.tdw.com. You also may request printed copies, which will be mailed to you without charge, by writing to us in care of our Secretary, 6002 Rogerdale Road, Suite 600, Houston, Texas 77072.

As of the date of this proxy statement, our board has ten members. Assuming all director nominees are elected, our board will continue to have ten members following the 2019 annual meeting.

Board Meetings and Attendance. During the 2018 fiscal year, our board held 18 meetings including telephonic meetings. Each director attended at least 75% of the meetings of the board and of the committees on which he or she served during the portion of fiscal 2018 in which he or she was a board member.

Our board does not have a policy requiring director attendance at annual meetings; however, our board’s practice is to schedule a board meeting on the same day as the annual meeting of stockholders in order to facilitate director attendance at the annual meeting.

19

Director Independence. Our board has affirmatively determined that 8 of our 10 directors –Messrs. Bates and Carr, Ms. Day, Messrs. Fagerstal, Newman, Raspino, Rigdon, and Traub – are currently independent. However, Mr. Rigdon, who was appointed as an independent director immediately following our restructuring, was not independent during his five-month tenure as our interim president and chief executive officer (October 16, 2017 – March 5, 2018). Neither Mr. Rynd, our president and chief executive officer, nor Mr. Tamburrino, who provided consulting services to the company prior to his appointment as a director, is currently independent.

The standards relied upon by the board in affirmatively determining whether a director is independent are the objective standards set forth in the corporate governance listing standards of the NYSE. In making independence determinations, our board evaluates responses to a questionnaire completed annually by each director regarding relationships and possible conflicts of interest between each director, the company, and management. In its review of director independence, our board also considers any commercial, industrial, banking, consulting, legal, accounting, charitable, and familial relationships any director may have with the company or management of which it is aware.

Board Leadership Structure. The roles of chairman and chief executive officer are currently held by two different persons – Mr. Bates serves as our chairman and Mr. Rynd serves as our president and chief executive officer.

Our board believes that, at this time, our current leadership structure best serves the interests of our company and our stockholders by clearly allocating responsibilities between the two offices. As our president and chief executive officer, Mr. Rynd’s primary responsibilities are to manage the day-to-day business and to develop and implement the company’s business strategy with the oversight of, and input from, the board. As chairman, Mr. Bates’ primary responsibility is to lead the board in its responsibilities of providing guidance to, and oversight of, management.

We have not adopted a policy requiring that these two roles be separate; rather, our board’s policy is to determine from time to time whether it is in the best interests of the company and its stockholders for the roles to be separate or combined. We believe that our board should have the flexibility to make these determinations in a way that will best provide appropriate leadership for our company based on needs of the company at that particular time. If we combine these roles in the future, or if the board determines that the chairman is otherwise not independent under NYSE standards, the board will elect a lead independent director at the same time that it elects its chairman.