Exhibit 99.2

TIMKEN

Stronger. By Design.

Timken Investor Day

June 19, 2014

FORWARD-LOOKING STATEMENTS

Certain statements in this presentation (including statements regarding the company’s forecasts, estimates and expectations) that are not historical in nature are “forward-looking” statements within the meaning of the Private Securities Litigation Reform Act of 1995. In particular, the statements related to expectations regarding each company’s future financial performance, plans for executing the spinoff, the taxable nature of the spinoff, future prospects of the companies as independent companies, revenue and market growth and similar statements are forward-looking. The company cautions that actual results may differ materially from those projected or implied in forward-looking statements due to a variety of important factors, including: each company’s ability to respond to the changes in its end markets that could affect demand for the company’s products; unanticipated changes in business relationships with customers or their purchases from each company; changes in the financial health of each company’s customers, which may have an impact on each company’s revenues, earnings and impairment charges; fluctuations in raw material and energy costs and their impact on the operation of each company’s surcharge mechanisms; the impact of each company’s last-in, first-out accounting; weakness in global or regional economic conditions and financial markets; changes in the expected costs associated with product warranty claims; the ability to achieve satisfactory operating results in the integration of acquired companies; the impact on operations of general economic conditions; higher or lower raw material and energy costs; fluctuations in customer demand; the impact on each company’s pension obligations due to changes in interest rates or investment performance; each company’s ability to achieve the benefits of announced programs, initiatives, and capital investments; each company’s ability to fund its pension plans; the timing and amount of any additional repurchases of the company’s common shares; the timing and amount of dividends on the company’s common shares; uncertainties that may delay or negatively impact the spinoff or cause the spinoff to not occur; changes to the actual amount of one-time spinoff costs compared to the company’s estimate; the inability to establish or maintain certain strategic relationships between both companies; and disruptions to operations as a result of effecting the spinoff. Additional factors are discussed in the company’s filings with the Securities and Exchange Commission, including the company’s Annual Report on Form 10-K for the year ended Dec. 31, 2013, quarterly reports on Form

10-Q and current reports on Form 8-K. Except as required by the federal securities laws, the company undertakes no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise.

This presentation includes certain non-GAAP financial measures as defined by the rules and regulations of the Securities and Exchange Commission. A reconciliation of those measures to the most directly comparable GAAP equivalent is provided in the Appendix to this presentation.

2

Stronger.By Design. TIMKEN

AGENDA

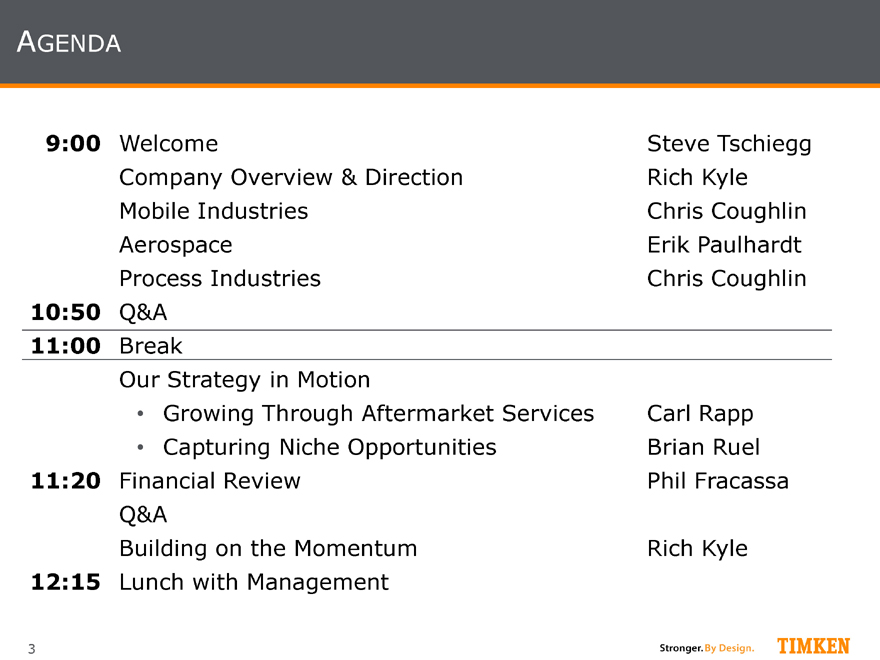

9:00 Welcome Steve Tschiegg

Company Overview & Direction Rich Kyle

Mobile Industries Chris Coughlin

Aerospace Erik Paulhardt

Process Industries Chris Coughlin

10:50 Q&A

11:00 Break

Our Strategy in Motion

Growing Through Aftermarket Services Carl Rapp

Capturing Niche Opportunities Brian Ruel

11:20 Financial Review Phil Fracassa

Q&A

Building on the Momentum Rich Kyle

12:15 Lunch with Management

3

Stronger.By Design. TIMKEN

TIMKEN

Stronger.By Design.

Company Overview and Direction Rich Kyle, President and CEO

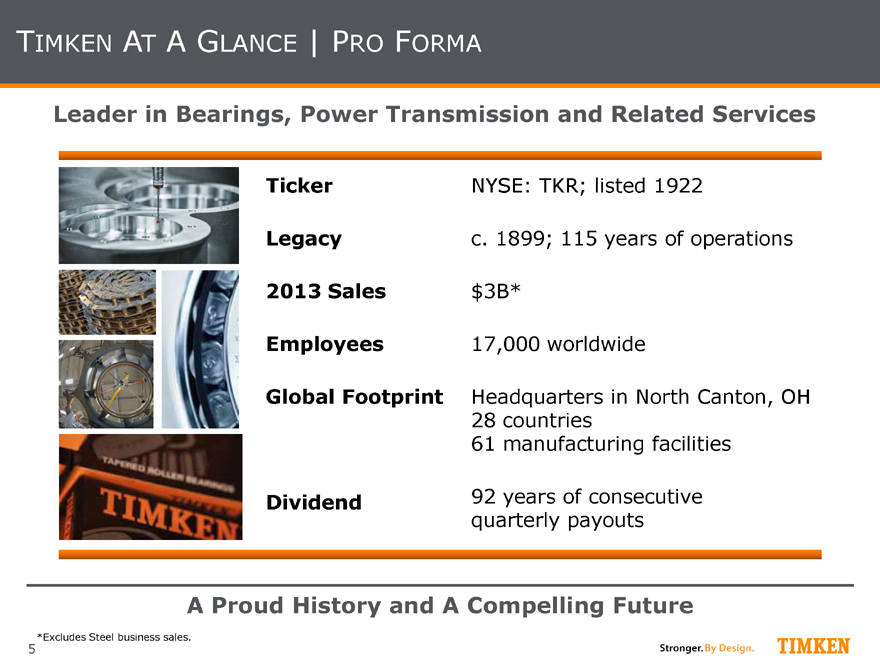

TIMKEN AT A GLANCE | PRO FORMA

Leader in Bearings, Power Transmission and Related Services

Ticker NYSE: TKR; listed 1922

Legacy c. 1899; 115 years of operations

2013 Sales $3B*

Employees 17,000 worldwide

Global Footprint Headquarters in North Canton, OH

28 countries

61 manufacturing facilities

Dividend 92 years of consecutive

quarterly payouts

A Proud History and A Compelling Future

*Excludes Steel business sales.

5

Stronger.By Design. TIMKEN

WHAT YOU’LL HEAR TODAY

Exciting time for Timken

Accountable, results-oriented

management team

Differentiated business model

Clear strategy to achieve compelling

long-term targets

Multiple growth opportunities

Innovation, product expansion

Aftermarket and services

Emerging markets

Disciplined and strategic M&A

Focus on operational excellence

Improved FCF generation leads

to increased return of capital

and funding of growth

THREE STRONG SEGMENTS

Mobile

Realigned and now well-

positioned to grow with

the market

Process

Growth to be fueled by

new products, Asia and

M&A

Aerospace

Attractive market

opportunities; focused on

margin expansion

6

Stronger.By Design. TIMKEN

EXPERIENCED BUSINESS LEADERS

Rich Kyle

President and CEO

Joined Timken in 2006;

Previously Cooper Industries &

Hubbell

Phil Fracassa

Chief Financial Officer

Joined Timken in 2005;

Previously Visteon, GM & PwC

Chris Coughlin

Group President

30 years with Timken

Erik Paulhardt

Vice President, Aerospace

28 years with Timken

Brian Ruel

Vice President, Mobile Industries

30 years with Timken

Carl Rapp

Vice President, Power Systems

Joined Timken in 2011;

Previously Philadelphia Gear and Carborundum Abrasives

Mike Connors

Vice President, Aftermarket

31 years with Timken

Focused on Creating Shareholder Value

7

Stronger.By Design. TIMKEN

THE TIMKEN TRANSFORMATION 2007 - 2014

2007 • Exited business that did not meet value proposition

criteria

$1B exited and business restructured

Completed in December 2013

Built capabilities to win in the marketplace

Global ERP system

Global footprint expansion

Product expansion

Service capabilities

Company-wide operational excellence initiative

Pension plans fully funded; commenced de-risking

2014 • TimkenSteel spinoff to create shareholder value

8

Stronger.By Design. TIMKEN

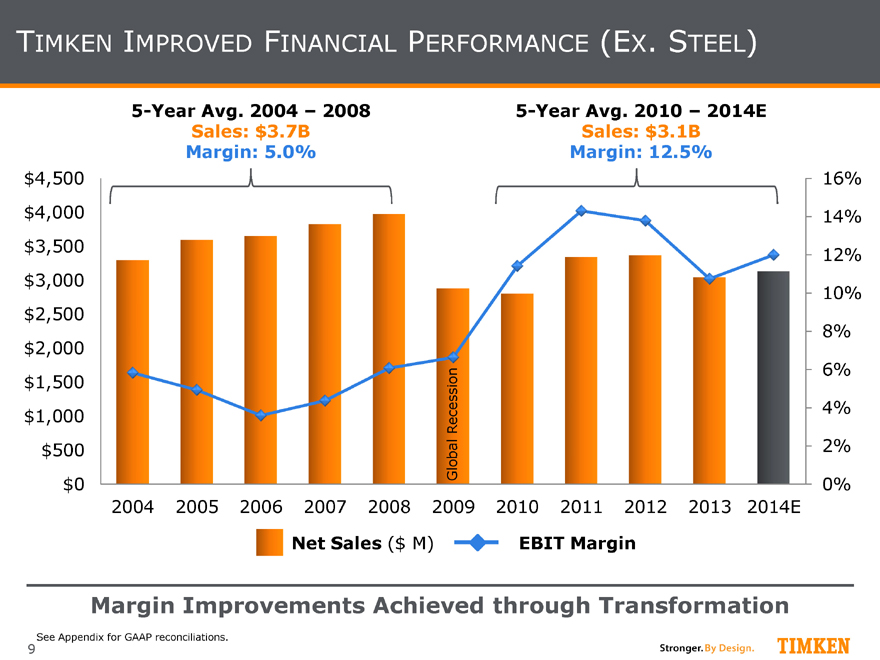

TIMKEN IMPROVED FINANCIAL PERFORMANCE (EX. STEEL)

5-Year Avg. 2004 – 2008 5-Year Avg. 2010 – 2014E

Sales: $3.7B Sales: $3.1B

Margin: 5.0% Margin: 12.5%

$4,500 16%

$4,000 14%

$3,500 12%

$3,000

10%

$2,500 8%

$2,000

6%

$1,500

$1,000 Recession 4%

$500 Global 2%

$0 0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014E

Net Sales ($ M) EBIT Margin

Margin Improvements Achieved through Transformation

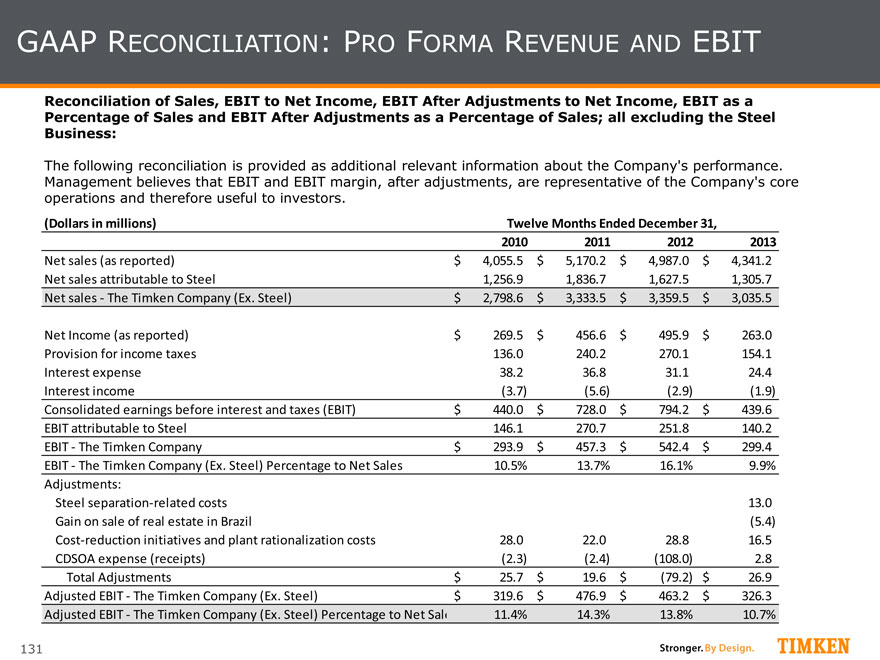

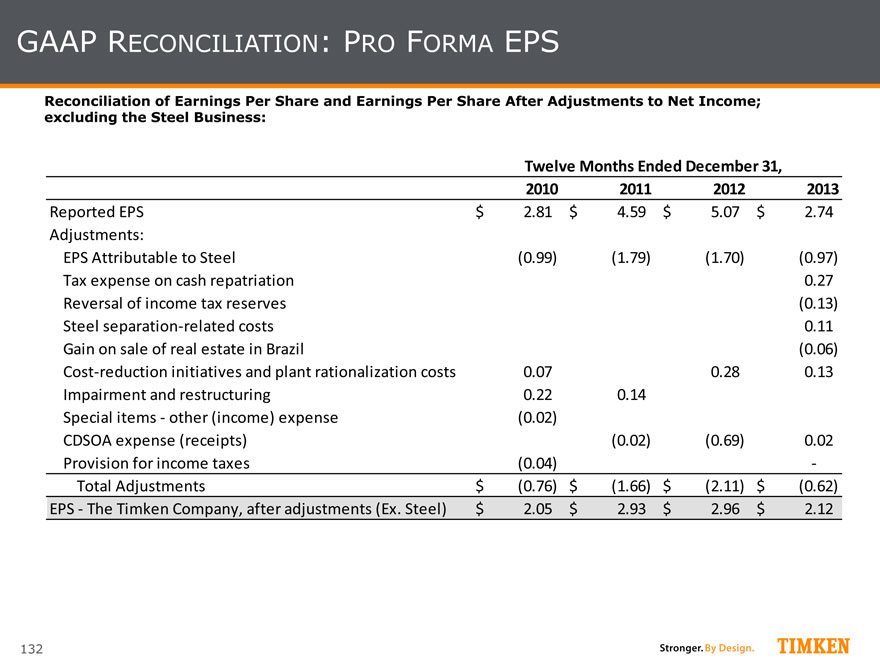

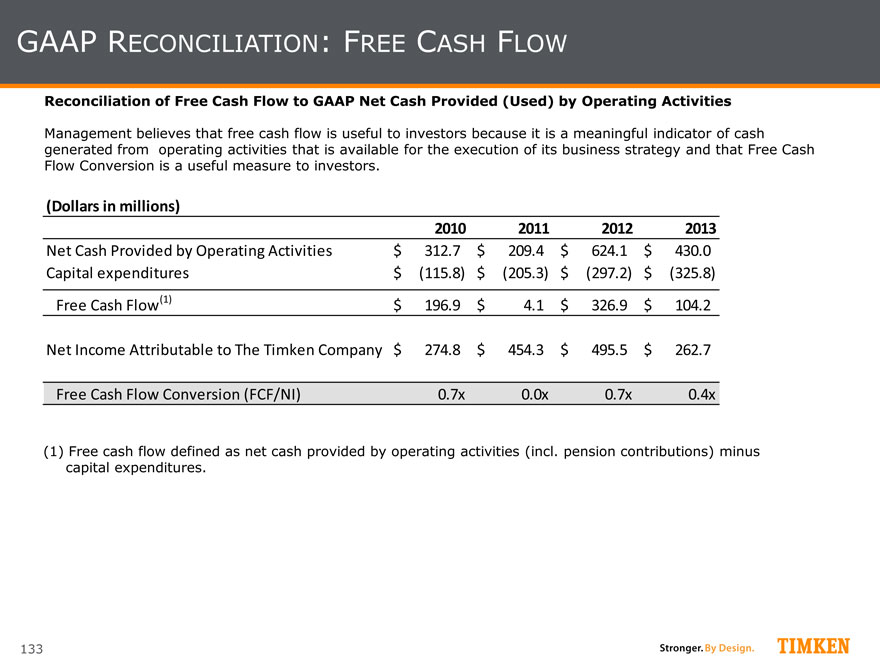

See Appendix for GAAP reconciliations.

9

Stronger.By Design. TIMKEN

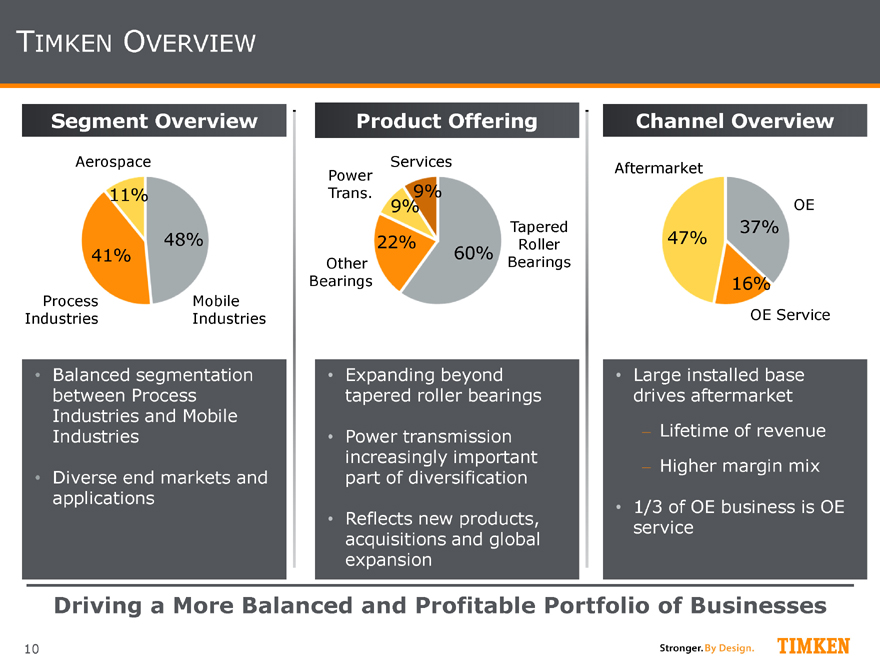

TIMKEN OVERVIEW

Segment Overview Product Offering Channel Overview

Aerospace Services Aftermarket

Power 9%

11% Trans.

9% OE

Tapered 37% 48% 22% Roller 47%

41% 60%

Other Bearings

Bearings 16% Process Mobile

Industries Industries OE Service

Balanced segmentation

between Process

Industries and Mobile

Industries

Diverse end markets and

applications

Expanding beyond

tapered roller bearings

Power transmission

increasingly important

part of diversification

Reflects new products,

acquisitions and global

expansion

Large installed base

drives aftermarket

Lifetime of revenue

Higher margin mix

1/3 of OE business is OE

service

Driving a More Balanced and Profitable Portfolio of Businesses

10

Stronger.By Design. TIMKEN

OPERATING IN 28 COUNTRIES ACROSS THE GLOBE

EMEA

18% Russia

Canada U.K. Germany

Poland Czech Republic

NA 59%

France Japan

ItalyRomania

U.S. Spain China

Turkey South Korea

LatAm 8%

India

Mexico U.A.E. Thailand Taiwan APAC 15%

Vietnam

Singapore

Brazil Indonesia

Australia

Plants/Service Centers | 61

South Africa

Distribution/Shipping | 23 Argentina

Technology Center |5

24% of 2013 Revenue Derived from Developing Markets

Note: Based on 2013 sales of $3.0B, ex. Steel business sales.

11

Stronger.By Design. TIMKEN

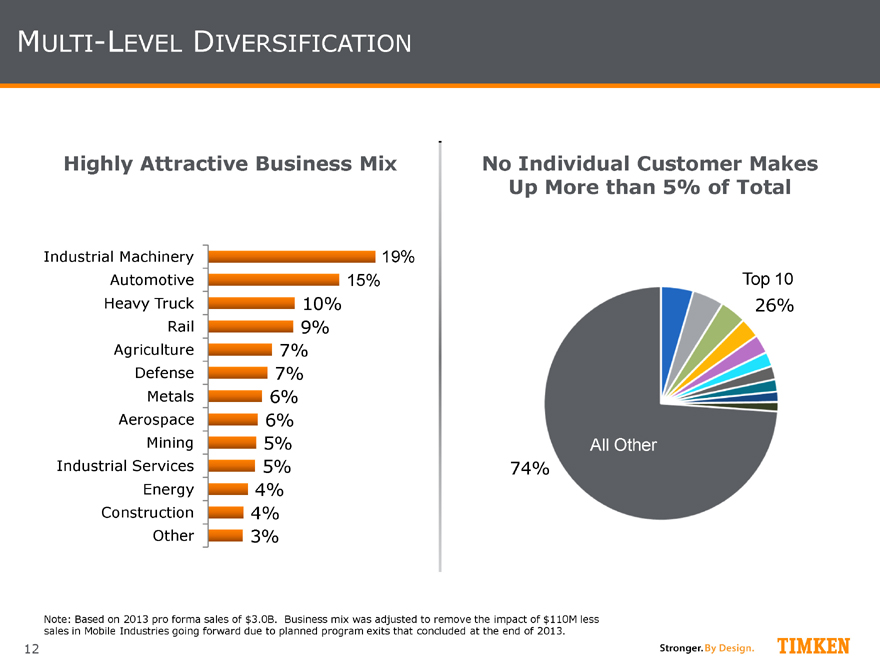

MULTI-LEVEL DIVERSIFICATION

Highly Attractive Business Mix

Industrial Machinery 19%

Automotive 15%

Heavy Truck 10%

Rail 9%

Agriculture 7%

Defense 7%

Metals 6%

Aerospace 6%

Mining 5%

Industrial Services 5%

Energy 4%

Construction 4%

Other 3%

No Individual Customer Makes

Up More than 5% of Total

Top 10

26%

All Other

74%

Note: Based on 2013 pro forma sales of $3.0B. Business mix was adjusted to remove the impact of $110M less

sales in Mobile Industries going forward due to planned program exits that concluded at the end of 2013.

12

Stronger.By Design. TIMKEN

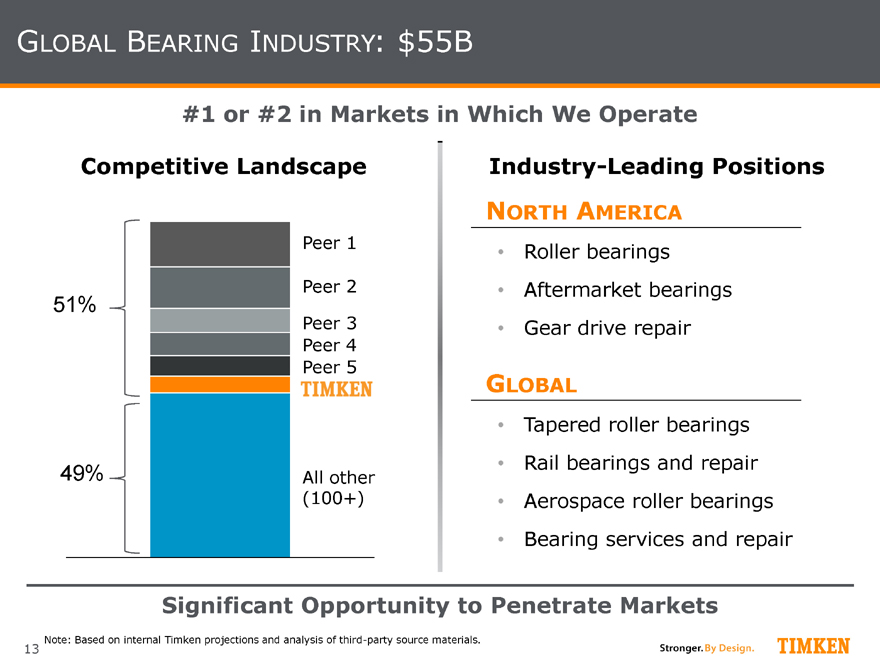

GLOBAL BEARING INDUSTRY: $55B

#1 or #2 in Markets in Which We Operate

Competitive Landscape Industry-Leading Positions

NORTH AMERICA

Peer 1

51% Peer 2

Peer 3

Peer 4

Peer 5 TIMKEN

49% All other

(100+)

Roller bearings

Aftermarket bearings

Gear drive repair

GLOBAL

Tapered roller bearings

Rail bearings and repair

Aerospace roller bearings

Bearing services and repair

Significant Opportunity to Penetrate Markets

Note: Based on internal Timken projections and analysis of third-party source materials.

13

Stronger.By Design. TIMKEN

THE GROWTH PLAN: WHAT YOU CAN EXPECT

Capture Share

and

Market Growth

Win Globally

Leverage

Technology and

Know-How to

Grow Organically

Pursue Strategic,

Bolt-on

Acquisitions

Execute Timken Business Model

Grow International Sales and

Focus on Emerging Markets

Accelerate Product Development Rate

Focus on

Bearings | International | Adjacencies | Services

14

Stronger.By Design. TIMKEN

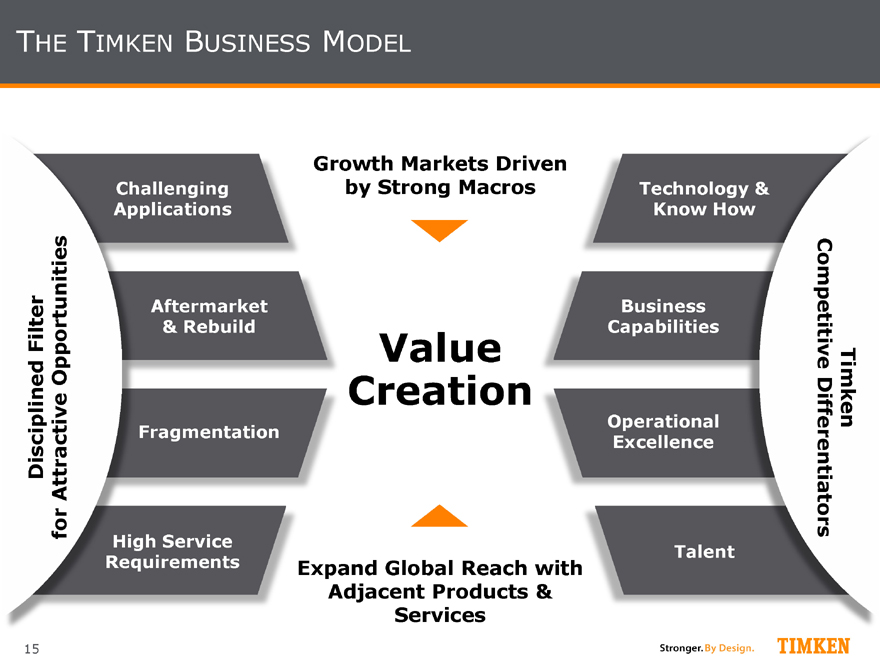

THE TIMKEN BUSINESS MODEL

15 Disciplined Filter for Attractive Opportunities

Challenging

Applications

Aftermarket

& Rebuild

Fragmentation

High Service

Requirements

Growth Markets Driven

by Strong Macros

Value

Creation

Expand Global Reach with

Adjacent Products &

Services

Technology & Know How

Business Capabilities

Operational Excellence

Talent

Timken

Competitive Differentiators

Stronger.By Design. TIMKEN

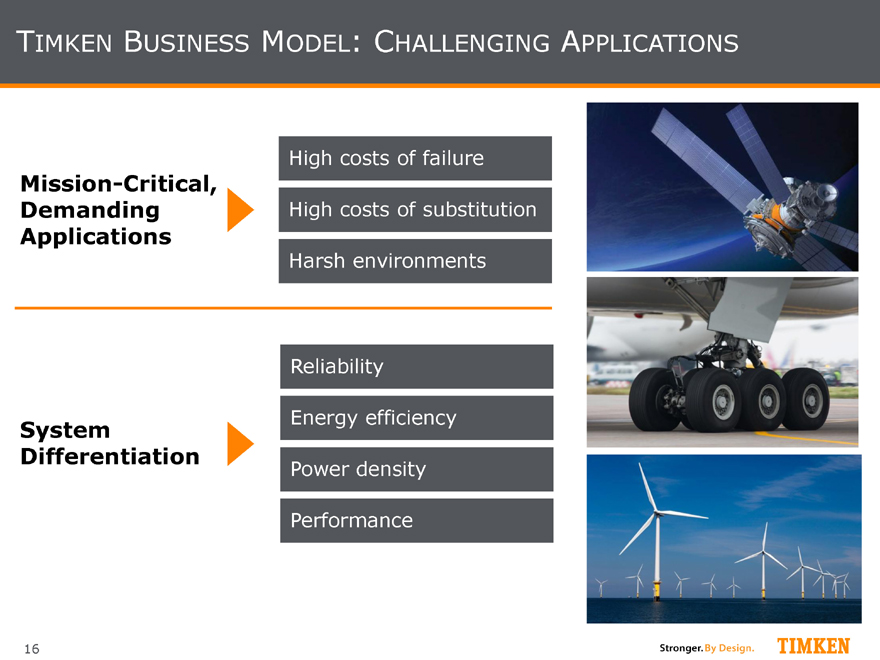

TIMKEN BUSINESS MODEL: CHALLENGING APPLICATIONS

Mission-Critical,

Demanding Applications

System

Differentiation

High costs of failure

High costs of substitution

Harsh environments

Reliability

Energy efficiency

Power density

Performance

16

Stronger.By Design. TIMKEN

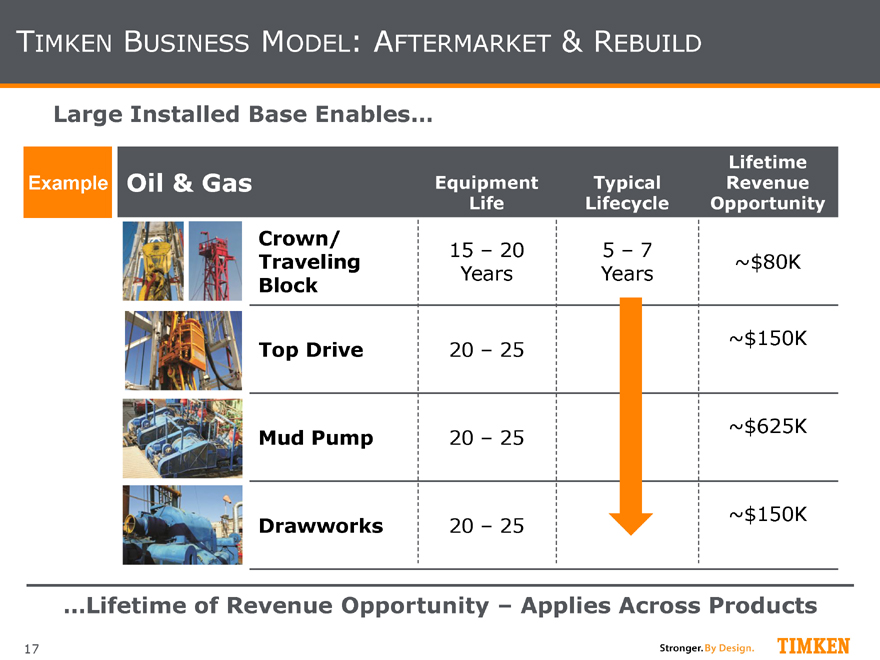

TIMKEN BUSINESS MODEL: AFTERMARKET & REBUILD

Large Installed Base Enables…

Lifetime Example Oil & Gas Equipment Typical Revenue Life Lifecycle Opportunity

Crown/

15 – 20 5 – 7

Traveling ~$80K

Years Years

Block

~$150K

Top Drive 20 – 25

~$625K

Mud Pump 20 – 25

~$150K

Drawworks 20 – 25

…Lifetime of Revenue Opportunity – Applies Across Products

17

Stronger.By Design. TIMKEN

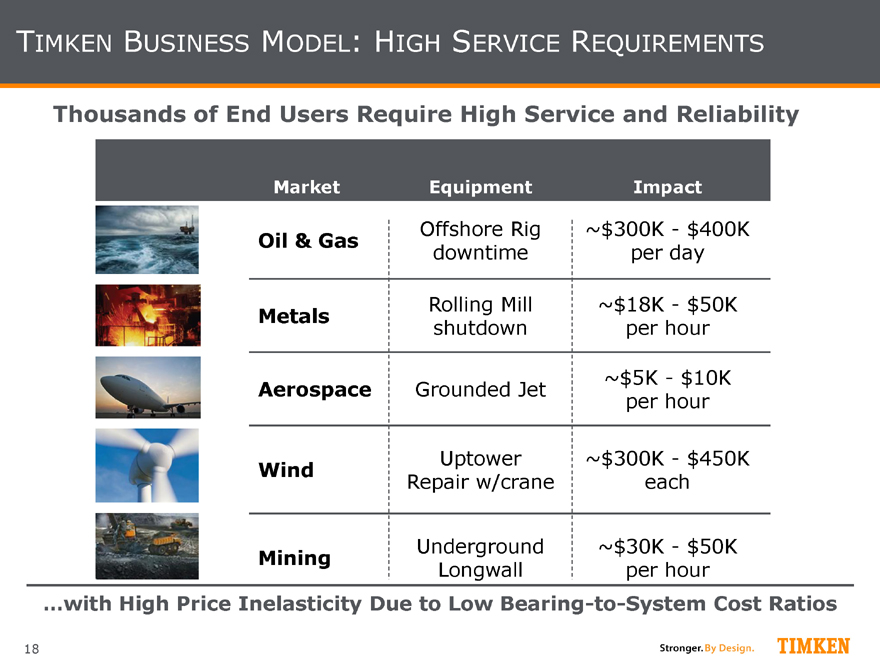

TIMKEN BUSINESS MODEL: HIGH SERVICE REQUIREMENTS

Thousands of End Users Require High Service and Reliability

Market Equipment Impact

Offshore Rig ~$300K - $400K

Oil & Gas downtime per day

Rolling Mill ~$18K - $50K

Metals shutdown per hour

~$5K - $10K

Aerospace Grounded Jet per hour

Uptower ~$300K - $450K

Wind

Repair w/crane each

Underground ~$30K - $50K

Mining

Longwall per hour

…with High Price Inelasticity Due to Low Bearing-to-System Cost Ratios

18

Stronger.By Design. TIMKEN

FOCUS ON MARKETS WITH STRONG MACRO FUNDAMENTALS

Infrastructure

Urbanization Development Sustainability

Strong demand in end markets driven by population growth, industrialization of developing countries

Increased focus on equipment redesigns to improve fuel efficiency, reliability and emissions

Mega trends expected to drive demand for Timken products and services bearings are central

19

Stronger.By Design. TIMKEN

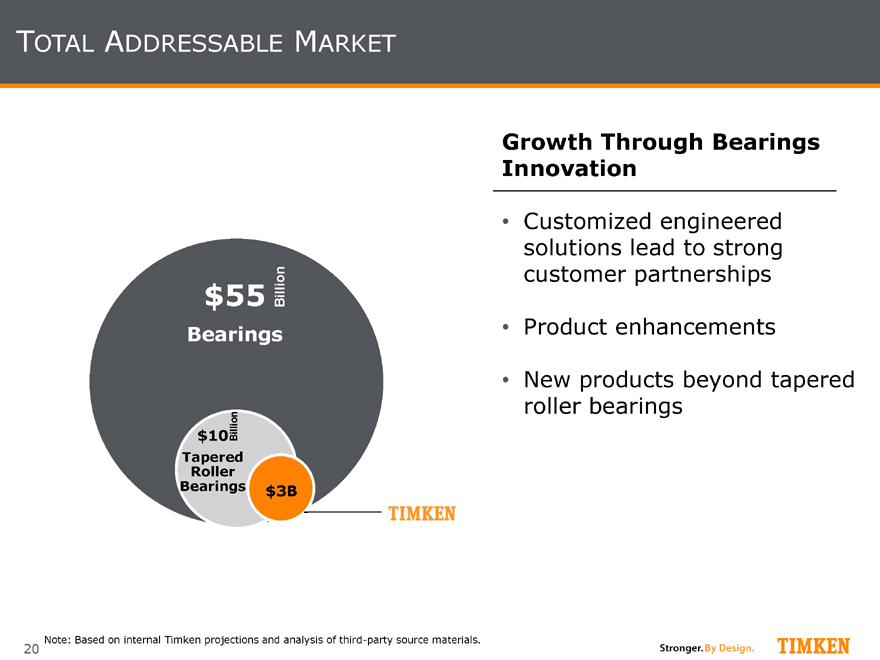

TOTAL ADDRESSABLE MARKET

Growth Through Bearings Innovation

Customized engineered solutions lead to strong customer partnerships

Product enhancements

New products beyond tapered roller bearings

$55 Billion

Bearings

$10 Billion

Tapered

Roller

Bearings $3B TIMKEN

Note: Based on internal Timken projections and analysis of third-party source materials.

20

Stronger.By Design. TIMKEN

|

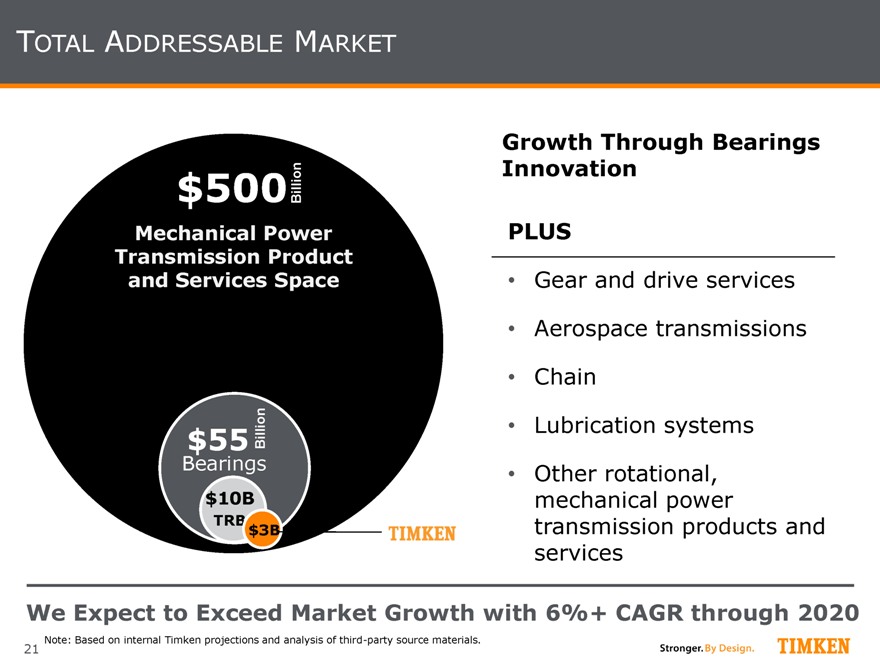

TOTAL ADDRESSABLE MARKET

$500Billion

Mechanical Power Transmission Product and Services Space

Billion

Bearings $55 $10B

TRB $3B

We Expect to Exceed Market Growth with 6%+ CAGR through 2020

Note: Based on internal Timken projections and analysis of third-party source materials.

Growth Through Bearings Innovation

PLUS

Gear and drive services

Aerospace transmissions

Chain

Lubrication systems

Other rotational, mechanical power transmission products and services

21

|

EXPANDING THE PRODUCT REACH

22

|

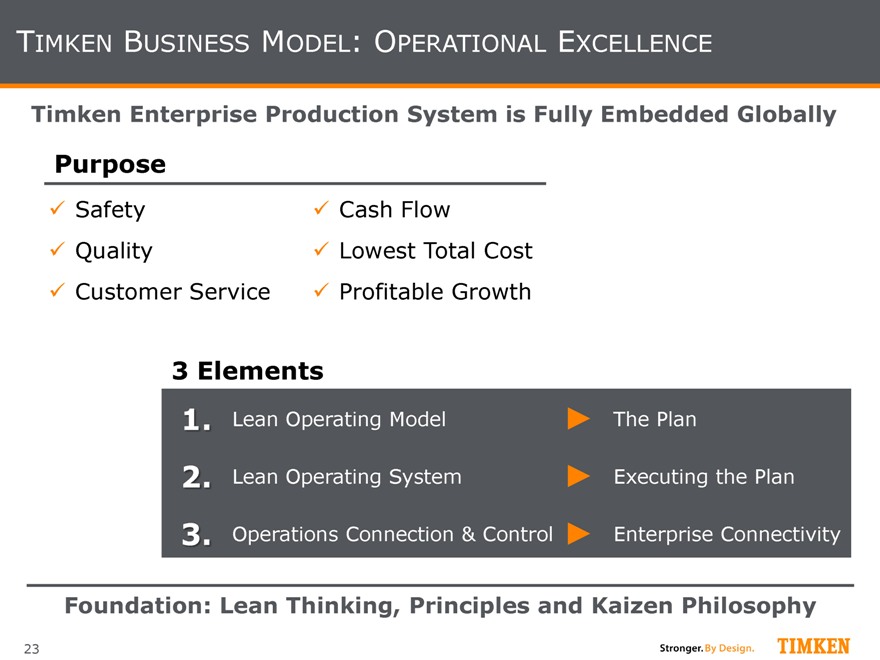

TIMKEN BUSINESS MODEL: OPERATIONAL EXCELLENCE

Timken Enterprise Production System is Fully Embedded Globally

Purpose

Safety Cash Flow

Quality Lowest Total Cost Customer Service Profitable Growth

3 Elements

1. Lean Operating Model The Plan

2. Lean Operating System Executing the Plan

3. Operations Connection & Control Enterprise Connectivity

Foundation: Lean Thinking, Principles and Kaizen Philosophy

23

|

TIMKEN BUSINESS MODEL: OPERATIONAL EXCELLENCE

Lean Operating Model for Each Plant Documents Critical Strategies; Links to KPIs for 9 Key Elements of the Production Process

Customer Demand Profile

Customer Requirements Demand Profile

Customer Demand Signal Alignment

Lead Times Ship Frequency Firm Order Windows

Network Strategy

Network Design Safety Stock, Replenishment Triggers

Finished Goods Strategy

Service Levels Safety Stock

Scheduling Strategy

Make to Order Make to Schedule

Manufacturing Operation Strategy

Capacity Labor Loading Lot Size & Set-up Times

Promising Strategy

Promising Rules Capacity Control Measures

Raw Material Strategy

Ordering Strategy Lot Size, Supermarkets Visual Signals

Sourcing Strategy

Supplier Capacity Supplier Quality Supplier Lead Times

Links Internal Capabilities with External Requirements

24

|

TIMKEN BUSINESS MODEL: HIGH SERVICE LEVELS

Operational Excellence Driving Significant Benefits through Improved Customer Service and Asset Efficiency

Fixed Asset Turnover

4.2x

3.3x

2008 – 2009 2012—2013 Avg. Avg.

Inventory Turns

5.1x

4.3x

2008 – 2009 2012—2013 Avg. Avg.

Industry-leading stock-in rates, lead times and on-time delivery

Recognized by:

With Even More Headroom Going Forward

25

|

TIMKEN: BUILDING ON THE MOMENTUM

Recognized industry leader for technology, quality and people

Foundation

26

|

TIMKEN: BUILDING ON THE MOMENTUM

Recognized industry leader for technology, quality and people Most attractive market and channel mix in the industry

Global reach

2007—2014 Strong cash flow Funded, frozen and

Transformation commenced

de-risking pensions

Recognized service leader

Increasingly diverse product and service mix

27

|

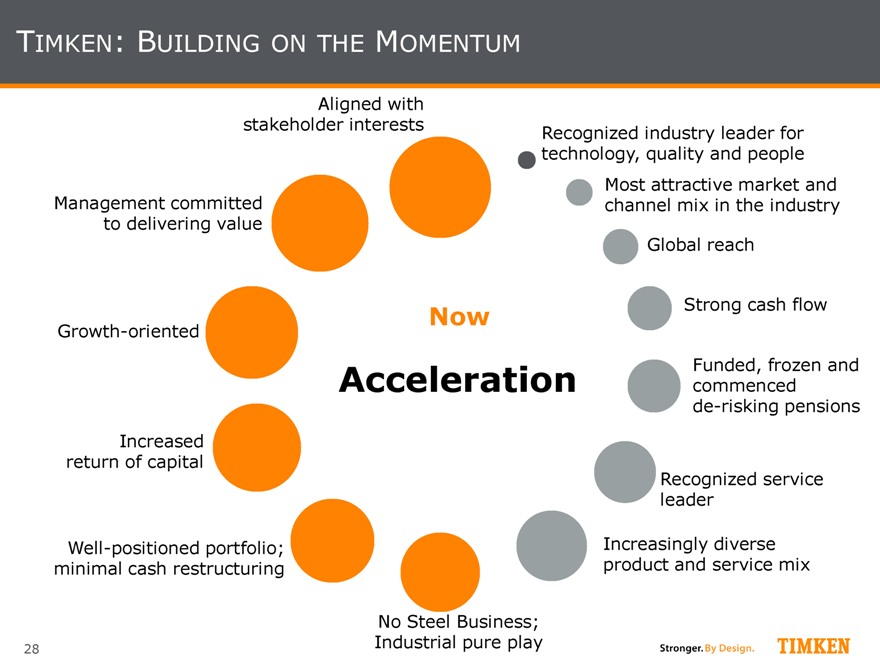

TIMKEN: BUILDING ON THE MOMENTUM

Aligned with

stakeholder interests Recognized industry leader for

technology, quality and people

Most attractive market and

Management committed channel mix in the industry

to delivering value

Global reach

Now Strong cash flow

Growth-oriented

frozen and

Acceleration commenced Funded,

de-risking pensions

Increased

return of capital

Recognized service

leader

Well-positioned portfolio; Increasingly diverse

minimal cash restructuring product and service mix

No Steel Business;

Industrial pure play

28

|

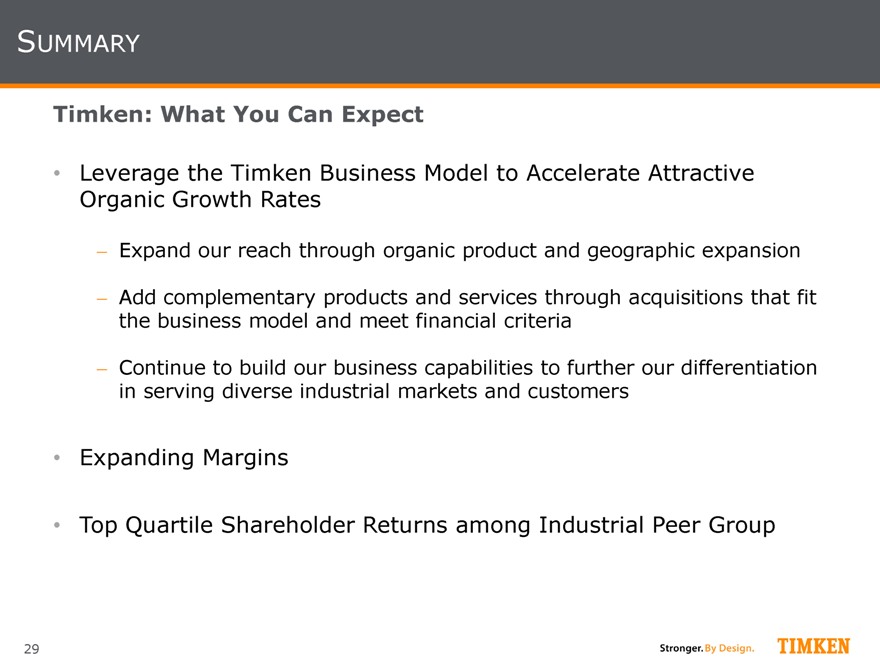

SUMMARY

Timken: What You Can Expect

Leverage the Timken Business Model to Accelerate Attractive Organic Growth Rates

Expand our reach through organic product and geographic expansion

Add complementary products and services through acquisitions that fit the business model and meet financial criteria

Continue to build our business capabilities to further our differentiation in serving diverse industrial markets and customers

Expanding Margins

Top Quartile Shareholder Returns among Industrial Peer Group

29

|

Mobile Industries

Chris Coughlin, Group President

|

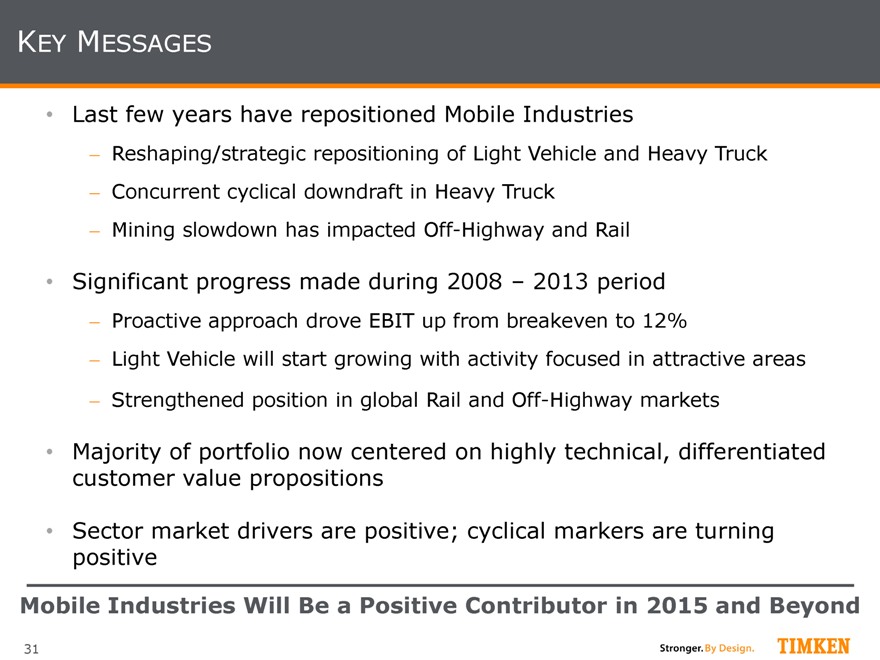

KEY MESSAGES

Last few years have repositioned Mobile Industries

Reshaping/strategic repositioning of Light Vehicle and Heavy Truck

Concurrent cyclical downdraft in Heavy Truck

Mining slowdown has impacted Off-Highway and Rail

Significant progress made during 2008 – 2013 period

Proactive approach drove EBIT up from breakeven to 12%

Light Vehicle will start growing with activity focused in attractive areas

Strengthened position in global Rail and Off-Highway markets

Majority of portfolio now centered on highly technical, differentiated customer value propositions

Sector market drivers are positive; cyclical markers are turning positive

Mobile Industries Will Be a Positive Contributor in 2015 and Beyond

31

|

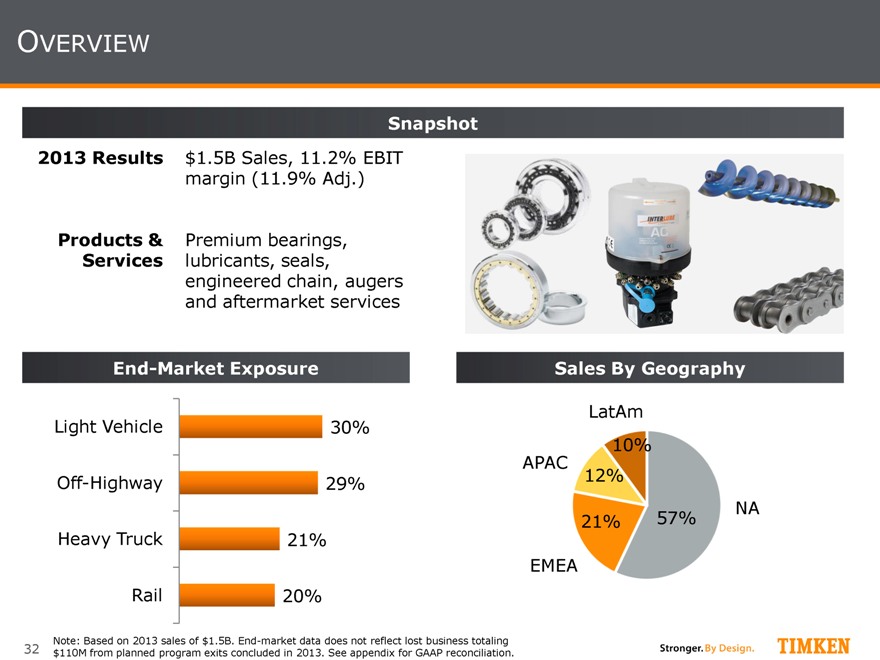

OVERVIEW

Snapshot

2013 Results $1.5B Sales, 11.2% EBIT

margin (11.9% Adj.)

Products & Premium bearings,

Services lubricants, seals,

engineered chain, augers

and aftermarket services

End-Market Exposure

Light Vehicle 30% Off-Highway 29% Heavy Truck 21% Rail 20%

Sales By Geography

LatAm APAC 10% 12%

NA 21% 57%

EMEA

Note: Based on 2013 sales of $1.5B. End-market data does not reflect lost business totaling $110M from planned program exits concluded in 2013. See appendix for GAAP reconciliation.

32

|

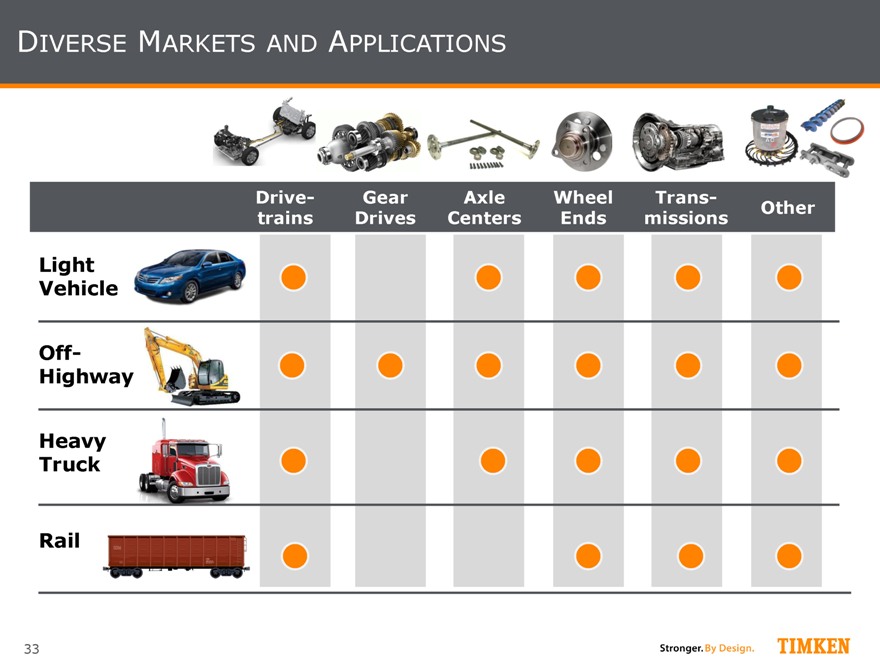

DIVERSE MARKETS AND APPLICATIONS

Drive- Gear Axle Wheel Trans-

Other trains Drives Centers Ends missions

Light Vehicle

Off-Highway

Heavy Truck

Rail

33

|

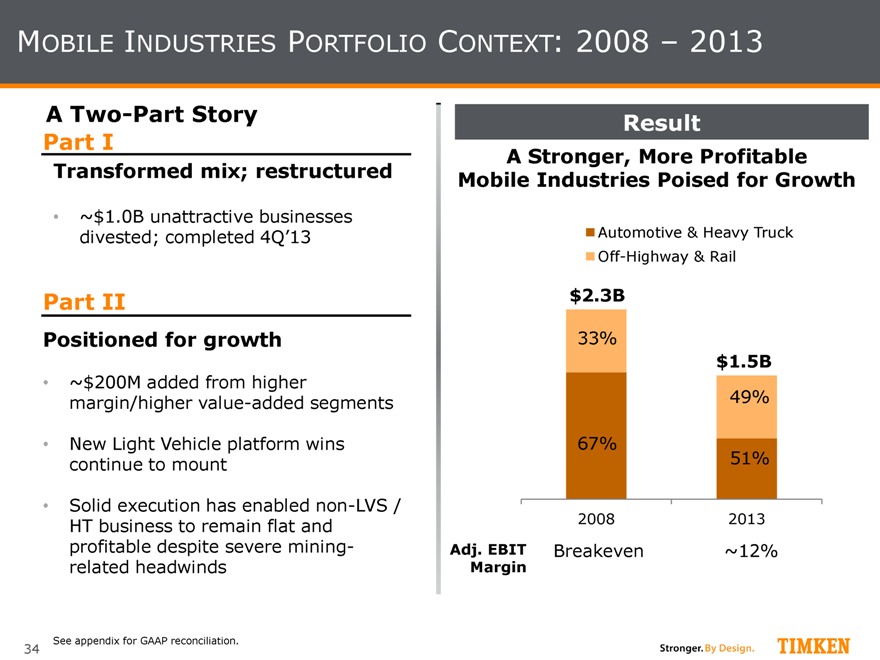

MOBILE INDUSTRIES PORTFOLIO CONTEXT: 2008 – 2013

A Two-Part Story Part I

Transformed mix; restructured

~$1.0B unattractive businesses divested; completed 4Q’13

Part II

Positioned for growth

~$200M added from higher margin/higher value-added segments

New Light Vehicle platform wins continue to mount

Solid execution has enabled non-LVS / HT business to remain flat and profitable despite severe mining-related headwinds

Result

A Stronger, More Profitable Mobile Industries Poised for Growth

Automotive & Heavy Truck Off-Highway & Rail

$2.3B

33% $1.5B

49%

67%

51%

2008 2013

Adj. EBIT Breakeven ~12%

Margin

See appendix for GAAP reconciliation.

34

|

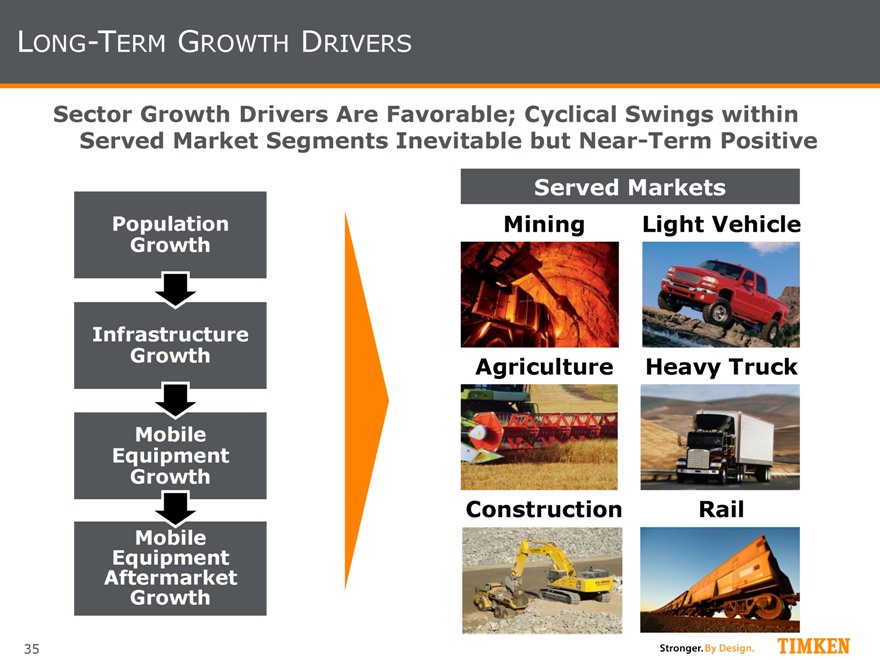

LONG-TERM GROWTH DRIVERS

Sector Growth Drivers Are Favorable; Cyclical Swings within Served Market Segments Inevitable but Near-Term Positive

Population Growth

Infrastructure Growth

Mobile Equipment Growth

Equipment Mobile Aftermarket Growth

Served Markets

Mining Light Vehicle Agriculture Heavy Truck Construction Rail

35

|

MOBILE INDUSTRIES OPERATING MODEL

Mobile Industries Operating Model Provides Foundation for Future Growth, Profitability

Continuously assess evolving needs of OEMs and end users in demanding mobile equipment and vehicle markets

Selectively develop highly engineered power transmission products and solutions addressing needs with a focus on:

Differentiated applications that create high value for end users

Solutions that provide long-term aftermarket opportunities

Provide industry-leading customer service and technical support

Leverage Timken capabilities

Geographical infrastructure

Timken Business Model

36

|

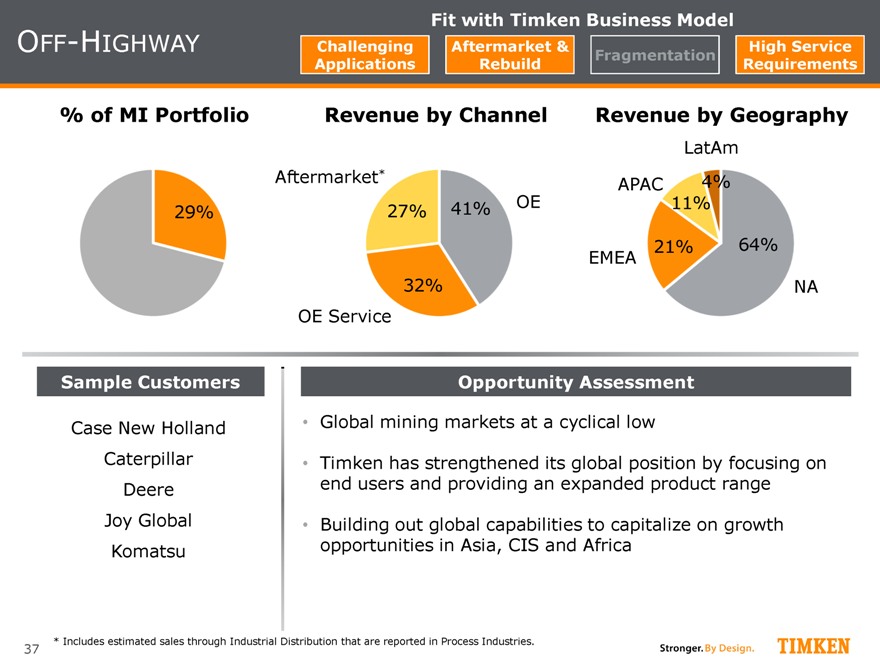

Fit with Timken Business Model

OFF-HIGHWAY Challenging Aftermarket & High Service Fragmentation Applications Rebuild Requirements

% of MI Portfolio Revenue by Channel Revenue by Geography

LatAm Aftermarket* 4% OE APAC

27% 41% 11% 29%

21% 64% EMEA

32% NA OE Service

Sample Customers

Case New Holland Caterpillar Deere Joy Global Komatsu

Opportunity Assessment

Global mining markets at a cyclical low

Timken has strengthened its global position by focusing on end users and providing an expanded product range

Building out global capabilities to capitalize on growth opportunities in Asia, CIS and Africa

* Includes estimated sales through Industrial Distribution that are reported in Process Industries.

37

|

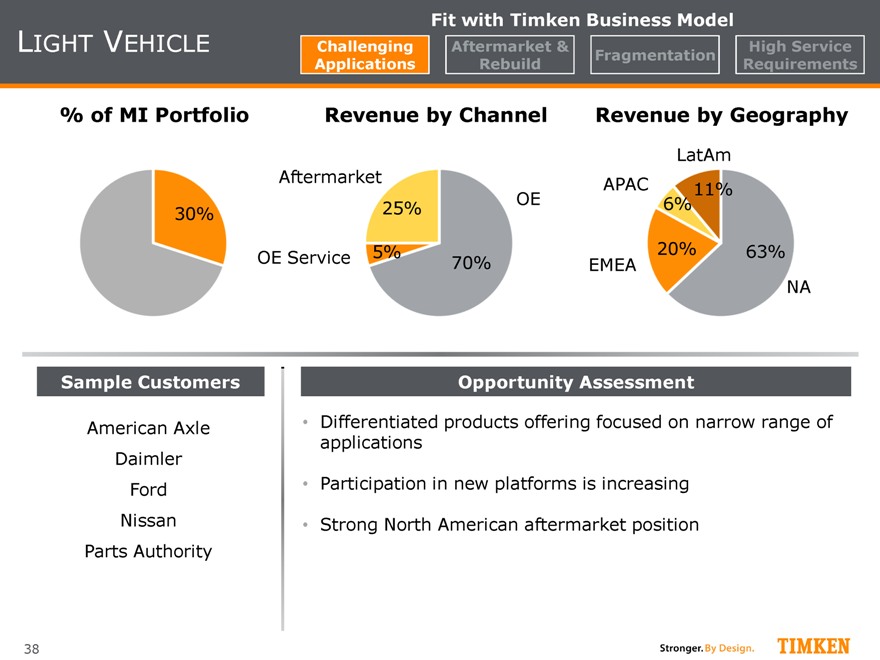

LIGHT VEHICLE

Fit with Timken Business Model

Challenging Aftermarket & High Service Fragmentation Applications Rebuild Requirements

% of MI Portfolio Revenue by Channel Revenue by Geography

LatAm Aftermarket APAC

11% OE 6% 30% 25%

5% 20% 63% OE Service 70% EMEA

NA

Sample Customers

American Axle Daimler Ford Nissan Parts Authority

Opportunity Assessment

Differentiated products offering focused on narrow range of applications

Participation in new platforms is increasing

Strong North American aftermarket position

38

|

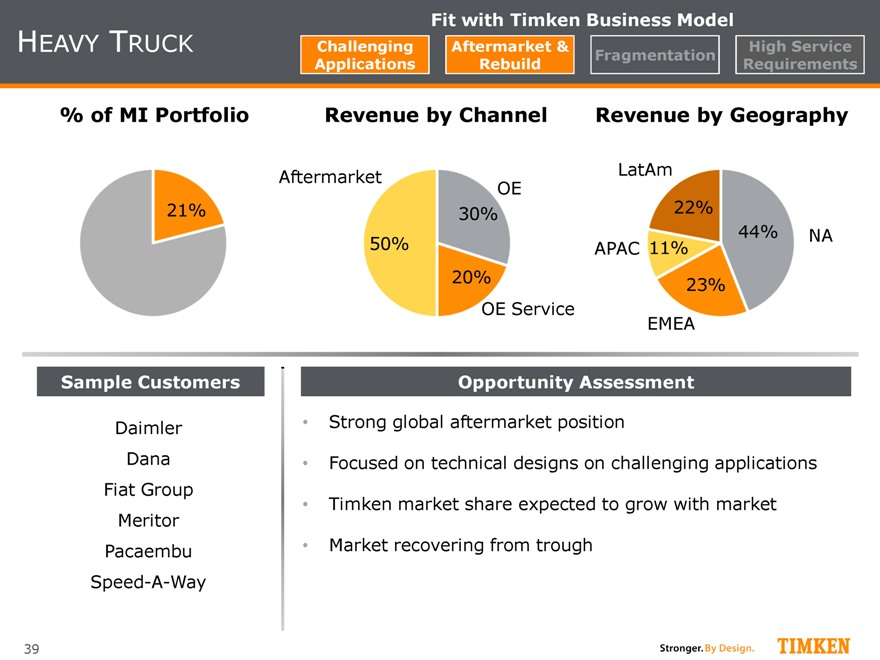

HEAVY TRUCK

Fit with Timken Business Model

Challenging Aftermarket & High Service Fragmentation Applications Rebuild Requirements

% of MI Portfolio

21%

Revenue by Channel

Aftermarket

OE 30% 50% 20% OE Service

Revenue by Geography

LatAm 22%

44% NA APAC 11% 23%

EMEA

Sample Customers

Daimler Dana Fiat Group Meritor Pacaembu Speed-A-Way

Opportunity Assessment

Strong global aftermarket position

Focused on technical designs on challenging applications

Timken market share expected to grow with market

Market recovering from trough

39

|

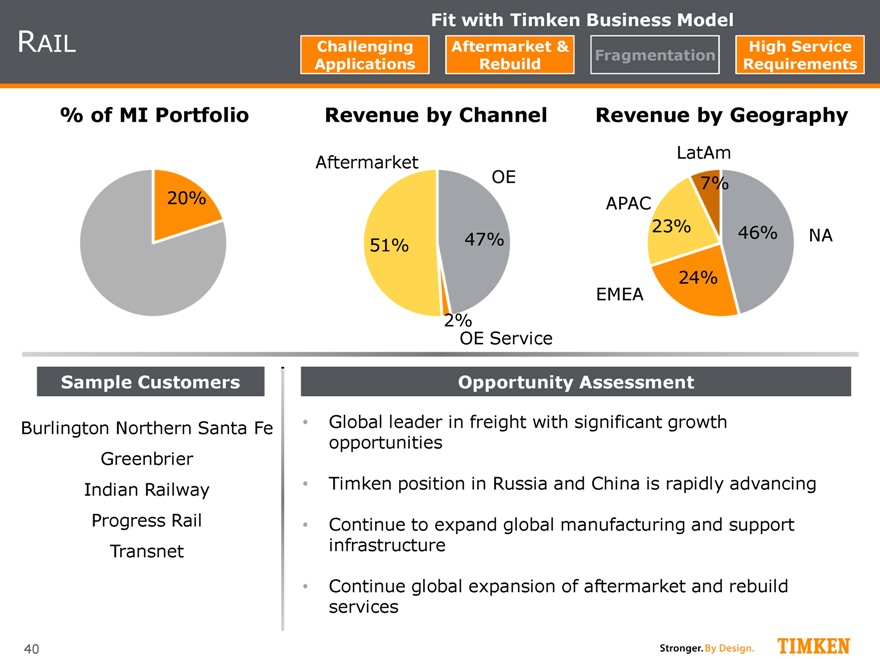

RAIL

Fit with Timken Business Model

Aftermarket & High

% of MI Portfolio

20%

Revenue by Channel

Aftermarket

OE

51% 47%

2%

OE Service

Revenue by Geography

LatAm 7% APAC

23% 46% NA

EMEA 24%

Sample Customers

Burlington Northern Santa Fe Greenbrier Indian Railway Progress Rail Transnet

Opportunity Assessment

Global leader in freight with significant growth opportunities

Timken position in Russia and China is rapidly advancing

Continue to expand global manufacturing and support infrastructure

Continue global expansion of aftermarket and rebuild services

40

|

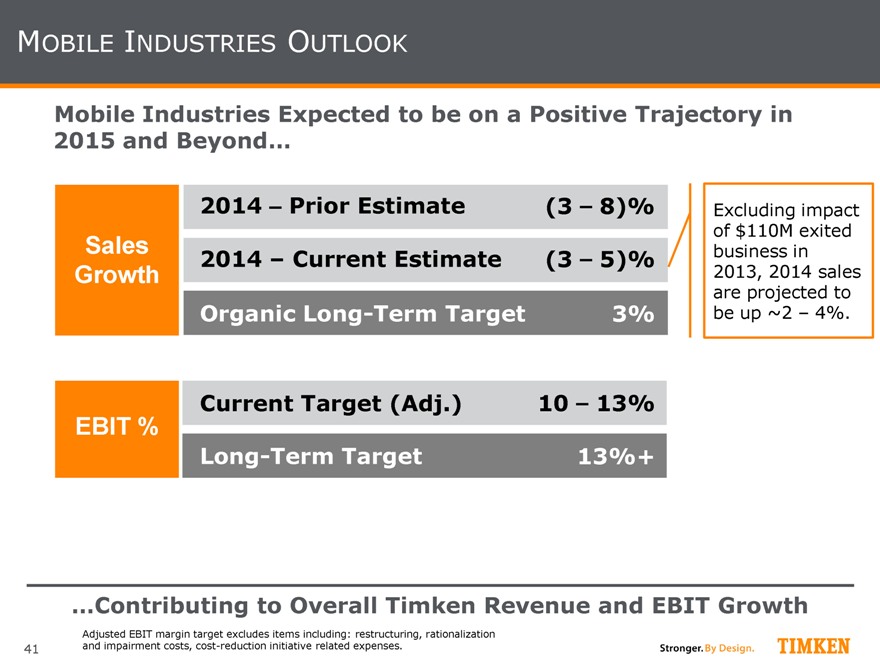

MOBILE INDUSTRIES OUTLOOK

Mobile Industries Expected to be on a Positive Trajectory in

2015 and Beyond…

2014 – Prior Estimate (3 – 8)%

Sales

2014 – Current Estimate (3 – 5)%

Growth

Organic Long-Term Target 3%

Current Target (Adj.) 10 – 13%

EBIT %

Long-Term Target 13%+

Excluding impact of $110M exited business in 2013, 2014 sales are projected to be up ~2 – 4%.

…Contributing to Overall Timken Revenue and EBIT Growth

Adjusted EBIT margin target excludes items including: restructuring, rationalization and impairment costs, cost-reduction initiative related expenses.

41

|

SUMMARY

With Structural Actions behind Us and A Stronger Base, We Are Now Focused on the Opportunities Ahead

Disciplined execution with focus on operational excellence

Pervasive innovation across the sub-segments

Continued penetration of new platforms

Gaining share when cyclical forces hit their stride

Mining and heavy truck resurgence

A major Asian expansion campaign

Mobile Industries: An Excellent Platform on Which to Build and Grow

42

|

Aerospace

Erik Paulhardt, Vice President

|

KEY MESSAGES

Aerospace is an attractive market

Timken has built strong niche positions; can compete effectively

Revenue weighted in defense, which continues to face headwinds

Focusing on margin expansion and establishing moderate growth rate

Cost and mix improvement

Timken to expand in civil fixed-wing applications with emphasis on airframe systems; longer-term opportunity expected

Focused on Margin Improvement, Longer-Term Growth

44

|

TIMKEN BUSINESS MODEL

Challenging

Applications

Aftermarket

& Rebuild

Fragmentation

High Service

Requirements

Broad array of complex flight-critical mechanical applications

Key trends driving innovation

Weight reduction/fuel efficiency and extended life

Long life of aircraft (20+ years) enables lifetime-of-revenue opportunity

Regulatory-mandated repair cycles

Fragmented low-volume components Service levels enable differentiation Countercyclical

45

|

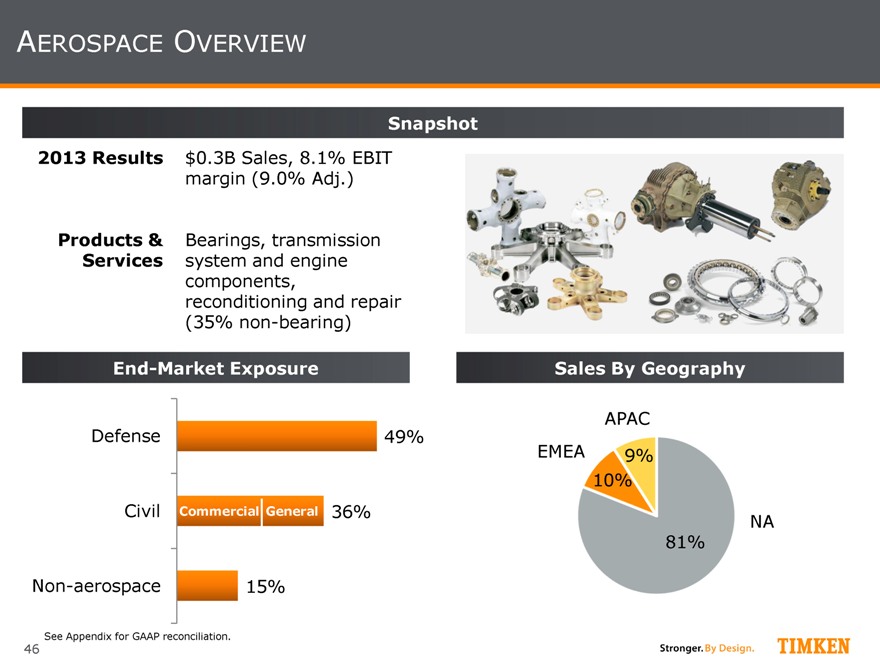

AEROSPACE OVERVIEW

Snapshot

2013 Results $0.3B Sales, 8.1% EBIT

margin (9.0% Adj.)

Products & Bearings, transmission

Services system and engine

components,

reconditioning and repair

(35% non-bearing)

End-Market Exposure

Defense 49%

Civil Commercial General 36%

Non-aerospace 15%

Sales By Geography

APAC EMEA 9% 10%

NA 81%

See Appendix for GAAP reconciliation.

46

|

MARKETS SERVED

DEFENSE

CIVIL

NON-AEROSPACE

Rotorcraft | Bearings, transmissions, drive train overhaul, replacement parts, bearing repair

Fixed Wing | Bearings, bearing repair

Spacecraft & Missile

Bearings, sub-assemblies

Ground Equipment

Bearings

Submarine | Bearings

Rotorcraft | Bearings, transmissions, drive train overhaul, engine overhaul, replacement parts, bearing repair

Fixed-Wing | Bearings, bearing repair, engine overhaul, replacement parts

Spacecraft | Bearings

Motion Control

Bearings, sub-assemblies, sensors

Machine Tool | Precision bearings, spindle repair

Medical Device & Robotics | Precision bearings

47

|

ROTORCRAFT PRESENCE

#1 Globally in Aerospace Roller Bearings and Transmission Components

Intermediate Gearbox

Engine Nose Gearbox

Fuel Pump

Engines, Generator

Tail Rotor Gearbox

Hydraulic Pump, Landing Wheels

Repair/Overhaul

Main Transmission

48

|

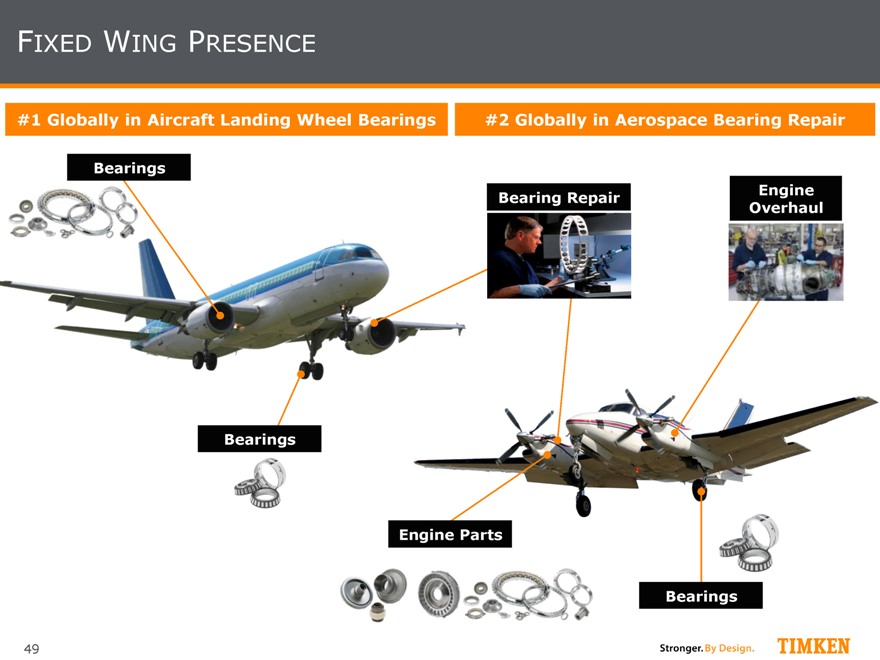

FIXED WING PRESENCE

#1 Globally in Aircraft Landing Wheel Bearings

#2 Globally in Aerospace Bearing Repair

Bearings

Bearing Repair

Engine Overhaul

Bearings

Engine Parts

Bearings

49

|

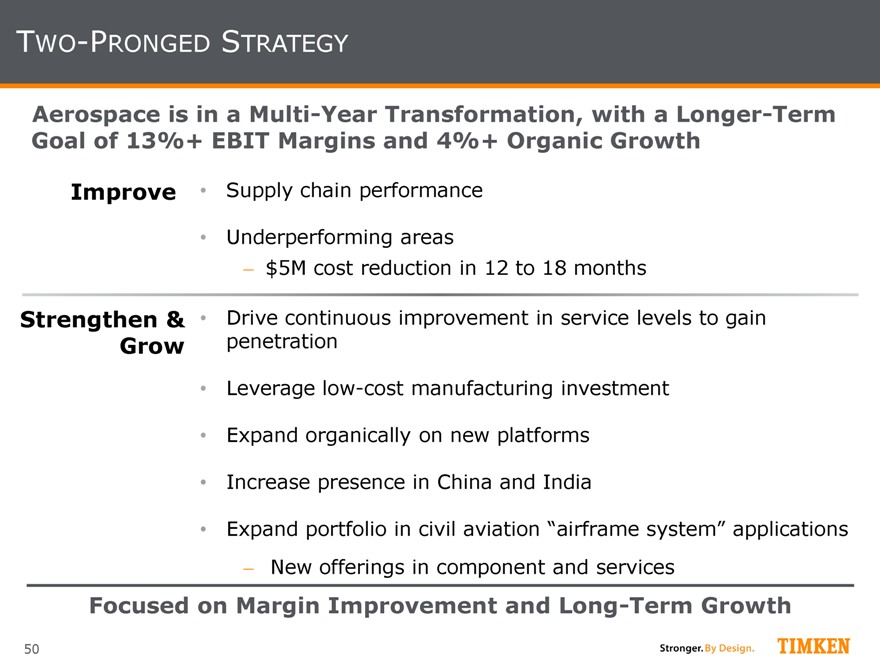

TWO-PRONGED STRATEGY

Aerospace is in a Multi-Year Transformation, with a Longer-Term Goal of 13%+ EBIT Margins and 4%+ Organic Growth

Improve • Supply chain performance

Underperforming areas

$5M cost reduction in 12 to 18 months

Strengthen & • Drive continuous improvement in service levels to gain Grow penetration

Leverage low-cost manufacturing investment

Expand organically on new platforms

Increase presence in China and India

Expand portfolio in civil aviation “airframe system” applications

New offerings in component and services

Focused on Margin Improvement and Long-Term Growth

50

|

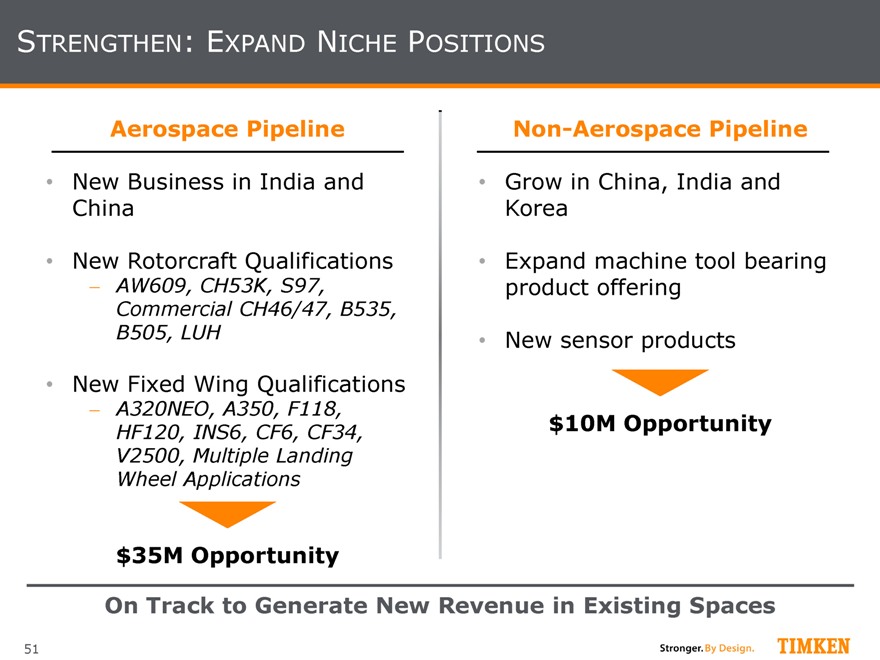

STRENGTHEN: EXPAND NICHE POSITIONS

Aerospace Pipeline

New Business in India and

China

New Rotorcraft Qualifications

AW609, CH53K, S97,

Commercial CH46/47, B535, B505, LUH

New Fixed Wing Qualifications

A320NEO, A350, F118, HF120, INS6, CF6, CF34, V2500, Multiple Landing Wheel Applications

$35M Opportunity

Non-Aerospace Pipeline

Grow in China, India and

Korea

Expand machine tool bearing product offering

New sensor products $10M Opportunity

On Track to Generate New Revenue in Existing Spaces

51

|

AEROSPACE OUTLOOK

Aerospace is Expected to Improve its Bottom Line Near-Term, while Growing the Top-Line over Time…

2014 – Prior Estimate 5 – 10%

Sales 2014 – Current Estimate 0 – 3%

Growth

Organic Long-Term Target 4%+

Current Target (Adj.) 10 – 13% (2014: 7 – 9%)

EBIT %

Long-Term Target 13%+

Focus on Performance Improvement and Margin Expansion

Adjusted EBIT margin target excludes items including: restructuring, rationalization and impairment costs, cost-reduction initiative related expenses.

52

|

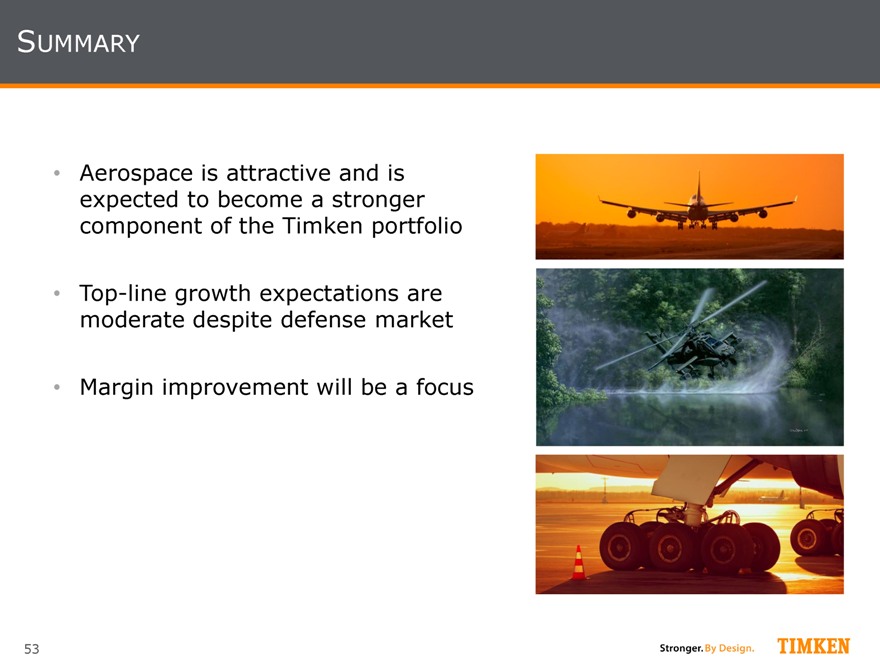

SUMMARY

Aerospace is attractive and is expected to become a stronger component of the Timken portfolio

Top-line growth expectations are moderate despite defense market

Margin improvement will be a focus

53

|

Process Industries

Chris Coughlin, Group President

|

KEY MESSAGES

Process Industries is a large, high-margin global business with a strong track record and exciting potential

The right markets: Excellent growth characteristics with vast market expansion potential; highly fragmented

The right products: Differentiated, high value-added with significant white space

The right operating model: Proven track record, defensible and leverageable with >50% recurring revenue content

The right strategy: Accelerated growth and value creation

55

|

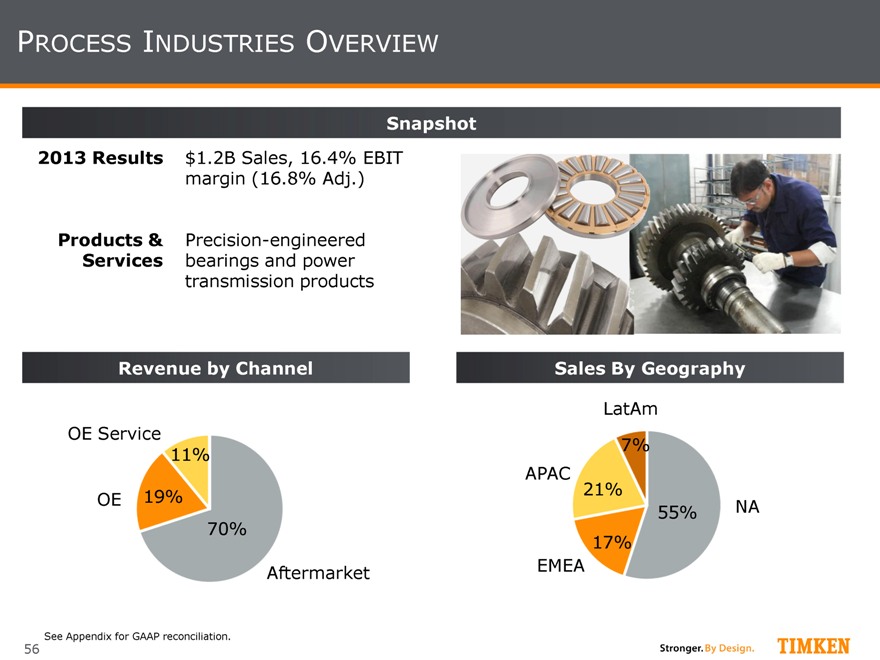

PROCESS INDUSTRIES OVERVIEW

Snapshot

2013 Results $1.2B Sales, 16.4% EBIT margin (16.8% Adj.)

Products & Precision-engineered Services bearings and power transmission products

Revenue by Channel Sales By Geography

LatAm

OE Service

11% 7%

APAC 21%

OE 19% 55% NA

70%

17%

Aftermarket EMEA

See Appendix for GAAP reconciliation.

56

|

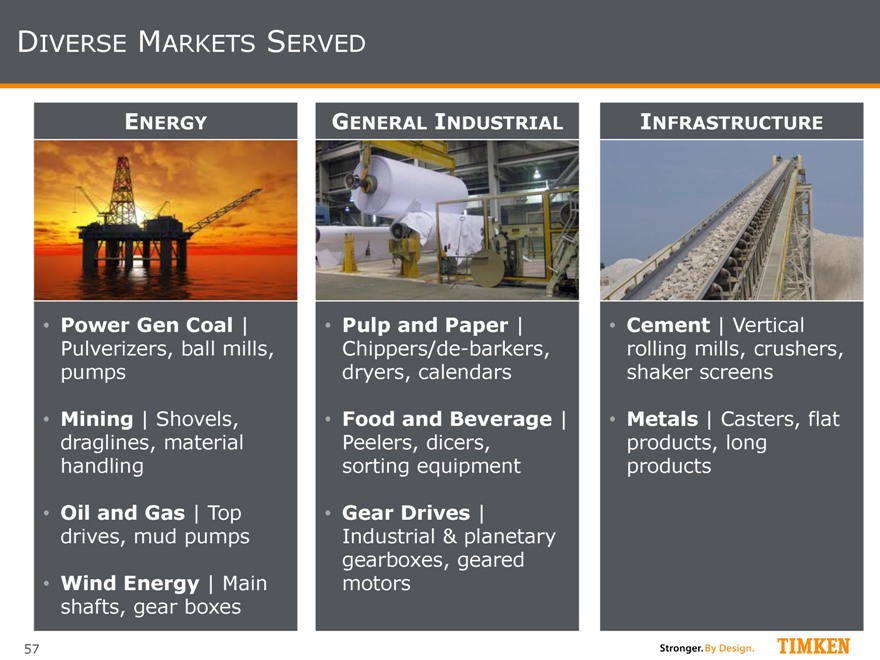

DIVERSE MARKETS SERVED

ENERGY

Power Gen Coal | Pulverizers, ball mills, pumps

Mining | Shovels, draglines, material handling

Oil and Gas | Top drives, mud pumps

Wind Energy | Main shafts, gear boxes

GENERAL INDUSTRIAL

Pulp and Paper | Chippers/de-barkers, dryers, calendars

Food and Beverage | Peelers, dicers, sorting equipment

Gear Drives |

Industrial & planetary gearboxes, geared motors

INFRASTRUCTURE

Cement | Vertical rolling mills, crushers, shaker screens

Metals | Casters, flat products, long products

57

|

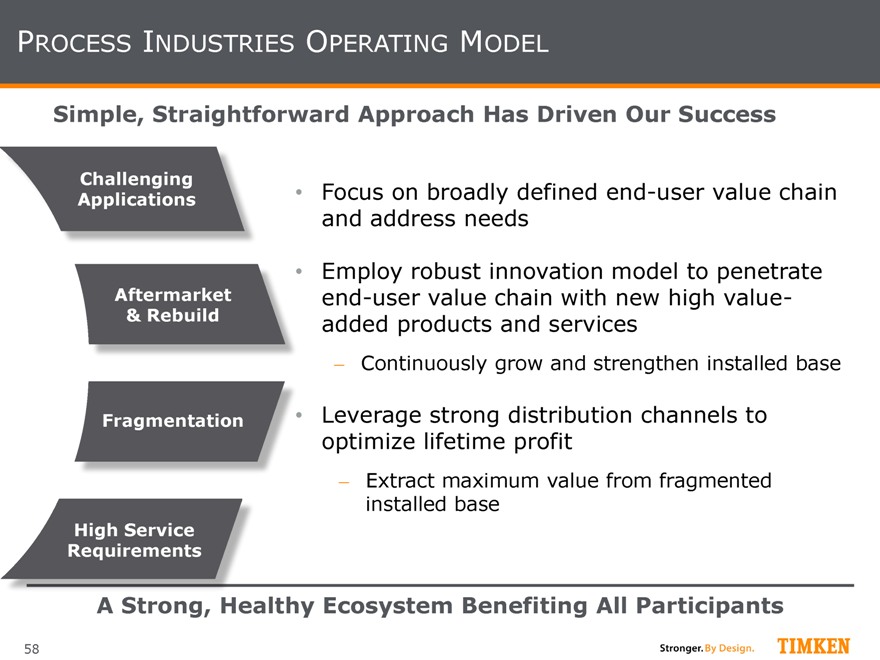

PROCESS INDUSTRIES OPERATING MODEL

Simple, Straightforward Approach Has Driven Our Success

Focus on broadly defined end-user value chain and address needs

Employ robust innovation model to penetrate end-user value chain with new high value-added products and services

Continuously grow and strengthen installed base

Leverage strong distribution channels to optimize lifetime profit

Extract maximum value from fragmented installed base

A Strong, Healthy Ecosystem Benefiting All Participants

Challenging Applications

Aftermarket

& Rebuild Fragmentation

High Service Requirements

58

|

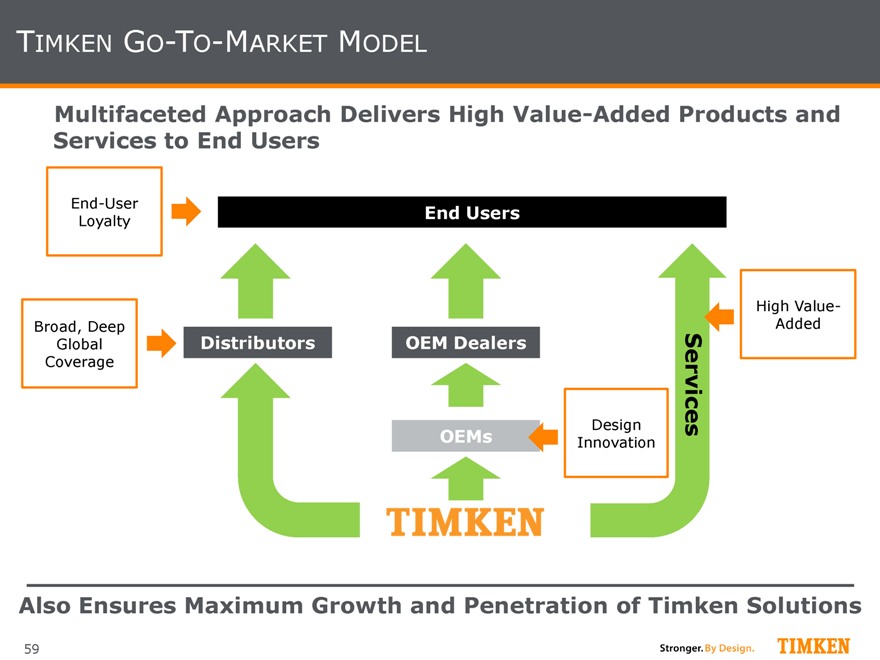

TIMKEN GO-TO-MARKET MODEL

Multifaceted Approach Delivers High Value-Added Products and Services to End Users

End-User

Loyalty End Users

High Value-

Broad, Deep Added

Global Distributors OEM Dealers

Coverage

Design Services

OEMs Innovation

Also Ensures Maximum Growth and Penetration of Timken Solutions

59

|

PRODUCT INNOVATION

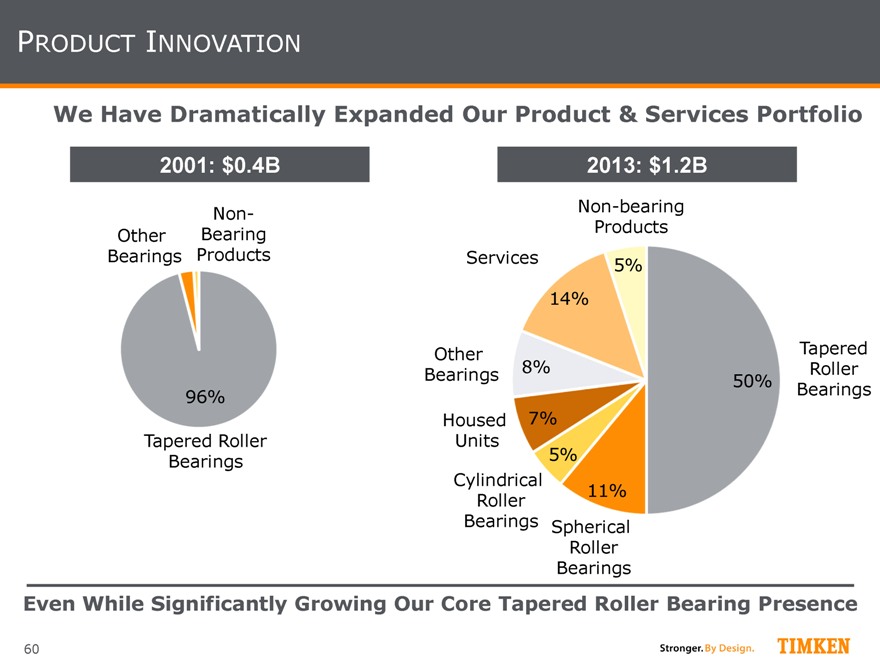

We Have Dramatically Expanded Our Product & Services Portfolio

2001: $0.4B

Non-Other Bearing Bearings Products

96%

Tapered Roller Bearings

2013: $1.2B

Non-bearing

Products

Services 5%

14%

Other Tapered

Bearings 8% 50% Roller

Bearings

Housed 7%

Units

5%

Cylindrical

Roller 11%

Bearings Spherical

Roller

Bearings

Even While Significantly Growing Our Core Tapered Roller Bearing Presence

60

|

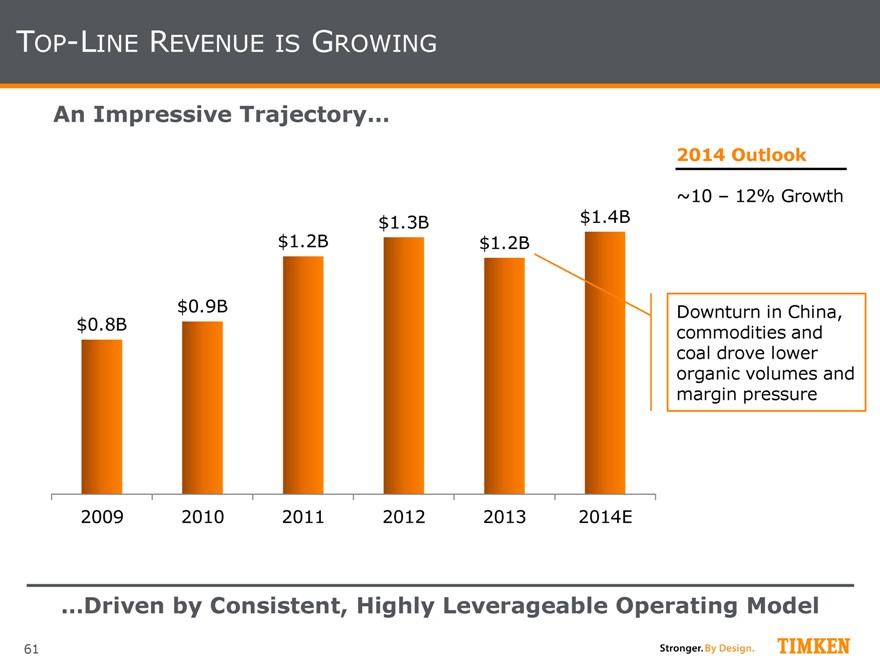

TOP-LINE REVENUE IS GROWING

An Impressive Trajectory…

2014 Outlook

~10 – 12% Growth

$1.3B $1.4B

$1.2B $1.2B

$0.9B Downturn in China,

$0.8B commodities and

coal drove lower

organic volumes and

margin pressure

2009 2010 2011 2012 2013 2014E

…Driven by Consistent, Highly Leverageable Operating Model

61

|

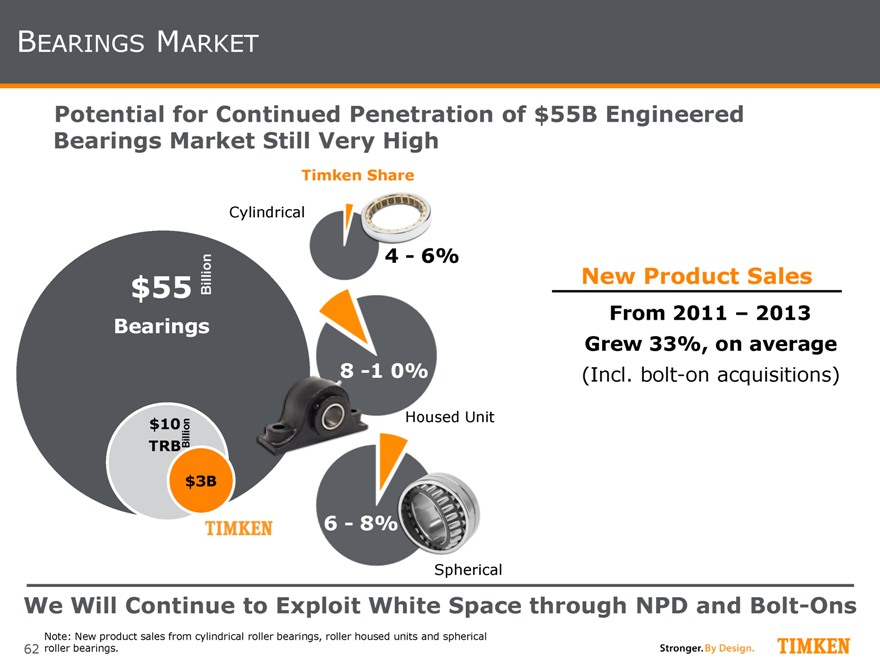

BEARINGS MARKET

Potential for Continued Penetration of $55B Engineered Bearings Market Still Very High

Timken Share

Cylindrical

4—6%

$55 Billion New Product Sales

Bearings From 2011 – 2013

Grew 33%, on average

8-1 0% (Incl. bolt-on acquisitions)

Housed Unit

TRB $10Billion

$3B

6—8%

Spherical

We Will Continue to Exploit White Space through NPD and Bolt-Ons

Note: New product sales from cylindrical roller bearings, roller housed units and spherical roller bearings.

62

|

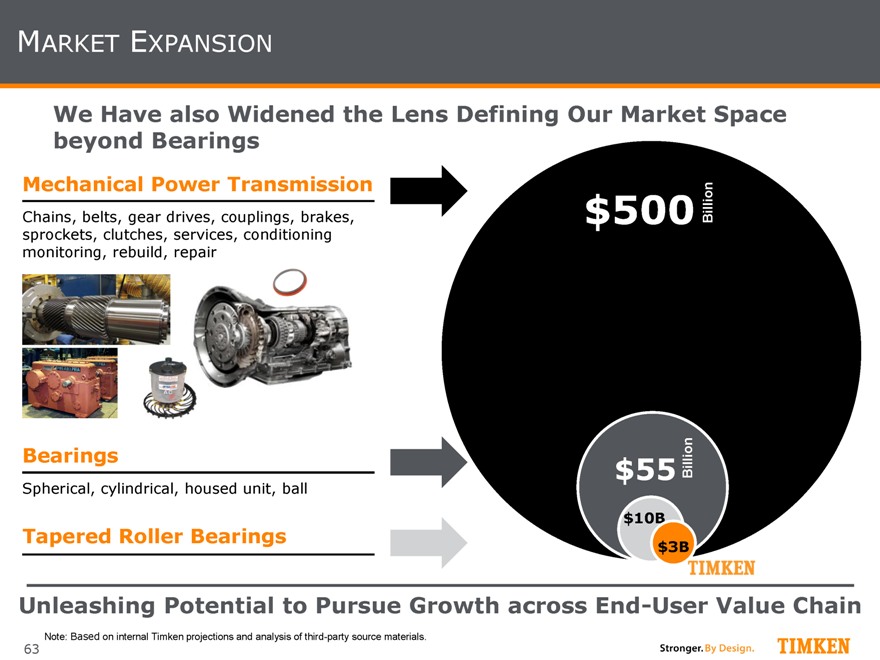

MARKET EXPANSION

We Have also Widened the Lens Defining Our Market Space beyond Bearings

Mechanical Power Transmission

Chains, belts, gear drives, couplings, brakes, sprockets, clutches, services, conditioning monitoring, rebuild, repair

Bearings

Spherical, cylindrical, housed unit, ball

Tapered Roller Bearings

Billion

$500

Billion

$55

$10B $3B

Unleashing Potential to Pursue Growth across End-User Value Chain

Note: Based on internal Timken projections and analysis of third-party source materials.

63

|

STRATEGY – A LOOK FORWARD

Strategy Leverages Process Industries’ Operating Model for

Sustained, Above-Market Growth and Strong Returns

Continue to feed the installed base

Aggressive commitment to innovation/product pipeline

Rapid development of product breadth beyond tapered roller bearings (organic and inorganic)

Leverage the large, attractive Asia opportunity

Take advantage of growing Timken presence, strong capabilities and scale

Further penetrate other growing markets outside the U.S.

Africa, LatAm and Eastern Europe/CIS

Seize robust growth opportunity in Power Systems (previously Industrial Services)

Maximize lifetime of profits

Reap benefits from strong global distribution channels

Continue to drive operational and commercial excellence

64

|

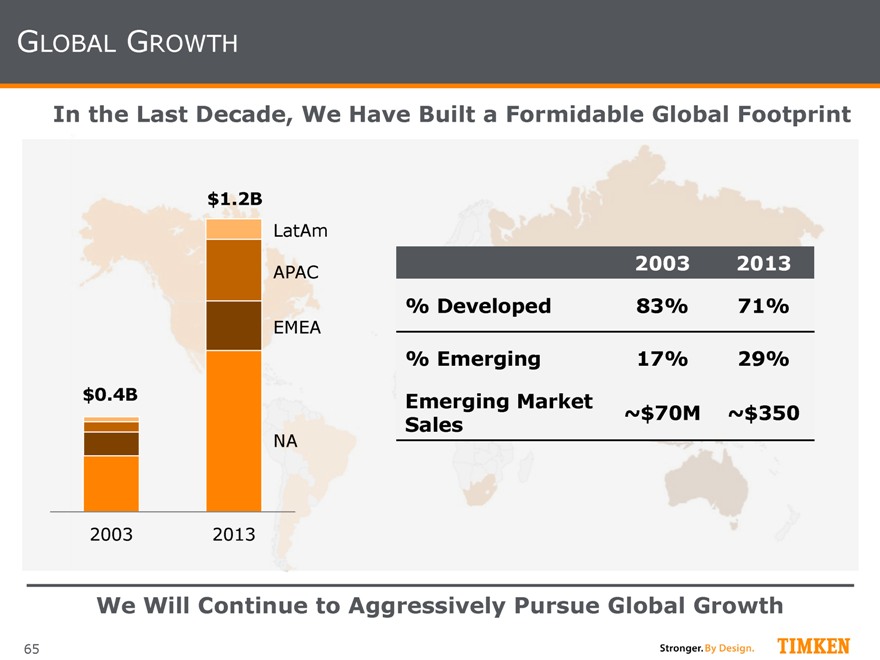

GLOBAL GROWTH

In the Last Decade, We Have Built a Formidable Global Footprint

$1.2B

LatAm

APAC 2003 2013

% Developed 83% 71%

EMEA

% Emerging 17% 29%

$0.4B Emerging Market

Sales ~$70M ~$350

NA

2003 2013

We Will Continue to Aggressively Pursue Global Growth

65

|

ASIA

Our Asia Growth Story is Early Stage

Regional Growth Drivers Are

Massive…

2015 2025

Asia to comprise

54% of world population

2.5B Asians will live in cities as urbanization continues

Implications

Infrastructure development will be massive

Huge growth in rail, steel and mining

…As Asian Continent Represents:

80% of world shipbuilding

67% of world crude steel production 47% of world global construction 42% of world electricity generation 30% of world railway industry

Timken Market Strengths Align Well with Sources of Growth

Note: Based on internal compilation of third-party source materials.

66

|

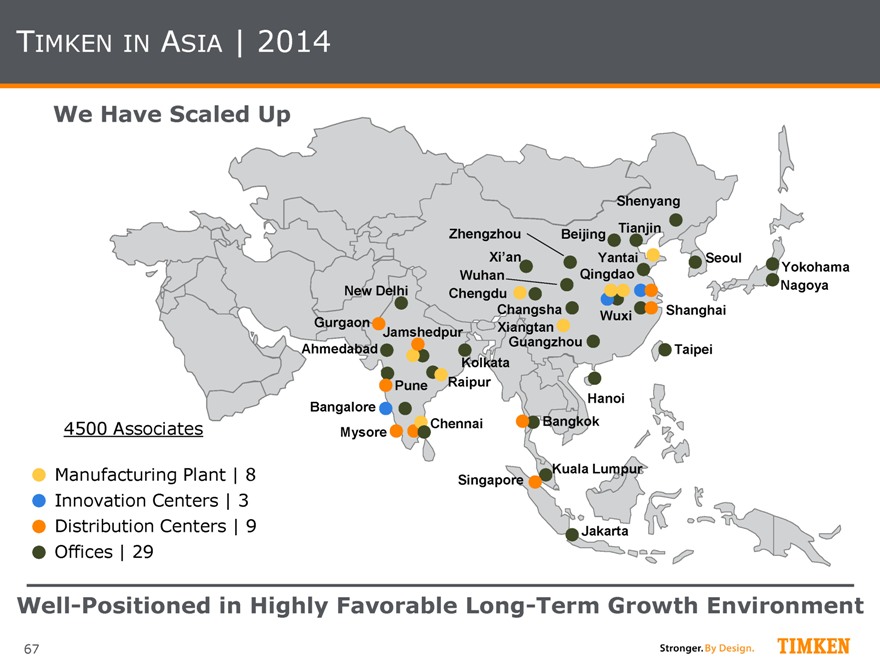

TIMKEN IN ASIA | 2014

We Have Scaled Up

Shenyang

Zhengzhou Beijing Tianjin

Xi’an Yantai Seoul

Wuhan Qingdao Yokohama

New Delhi Chengdu Nagoya

Changsha Wuxi Shanghai

Gurgaon Xiangtan

Jamshedpur

Guangzhou

Ahmedabad Taipei

Kolkata

Pune Raipur

Bangalore Hanoi

4500 Associates Mysore Chennai Bangkok

Manufacturing Plant | 8 Singapore Kuala Lumpur

Innovation Centers | 3

Distribution Centers | 9 Jakarta

Offices | 29

Well-Positioned in Highly Favorable Long-Term Growth Environment

67

|

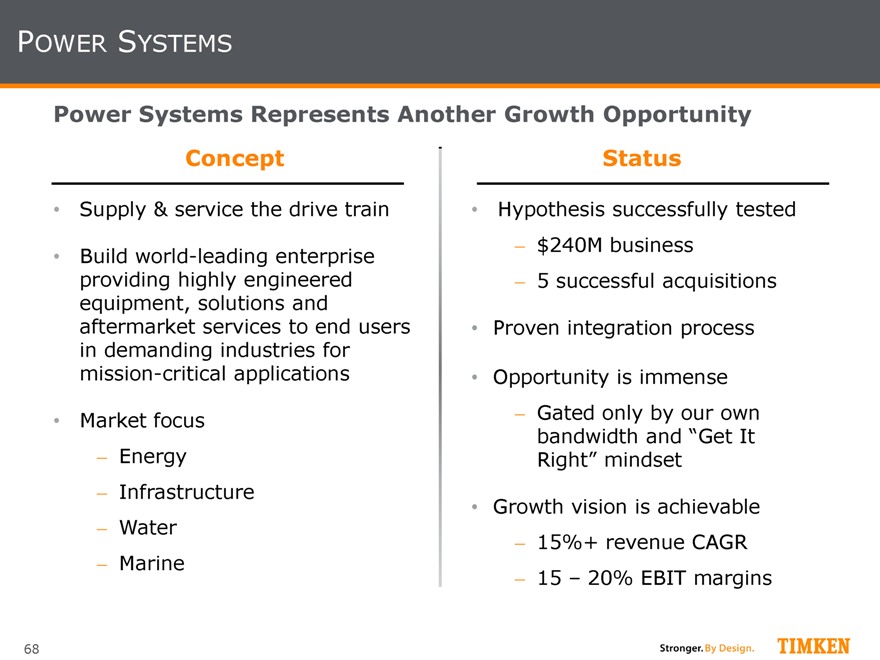

POWER SYSTEMS

Power Systems Represents Another Growth Opportunity

Concept Status

Supply & service the drive train Hypothesis successfully tested

Build world-leading enterprise $240M business

providing highly engineered 5 successful acquisitions

equipment, solutions and

aftermarket services to end users Proven integration process

in demanding industries for

mission-critical applications Opportunity is immense

Market focus Gated only by our own

bandwidth and “Get It

Energy Right” mindset

Infrastructure Growth vision is achievable

Water 15%+ revenue CAGR

Marine 15 – 20% EBIT margins

68

|

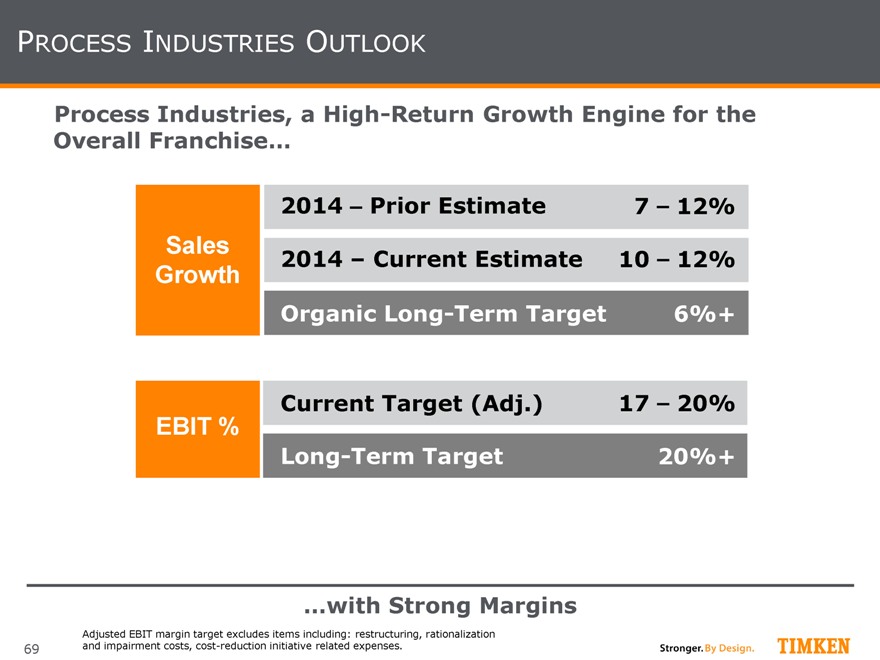

PROCESS INDUSTRIES OUTLOOK

Process Industries, a High-Return Growth Engine for the

Overall Franchise…

2014 – Prior Estimate 7 – 12%

Sales 2014 – Current Estimate 10 – 12%

Growth

Organic Long-Term Target 6%+

Current Target (Adj.) 17 – 20%

EBIT %

Long-Term Target 20%+

…with Strong Margins

Adjusted EBIT margin target excludes items including: restructuring, rationalization and impairment costs, cost-reduction initiative related expenses.

69

|

SUMMARY

Timken Process Industries is a Great Business

Operating model is proven and scalable

Excellent core growth and returns

Significant recurring revenue content

Several large, compelling opportunities ahead

Added product breadth

Asia growth

Power Systems expansion

Commitment to robust growth and profitable expansion backed up by experienced management team

70

|

Growing Through Aftermarket Services Carl Rapp, Vice President | Power Systems

|

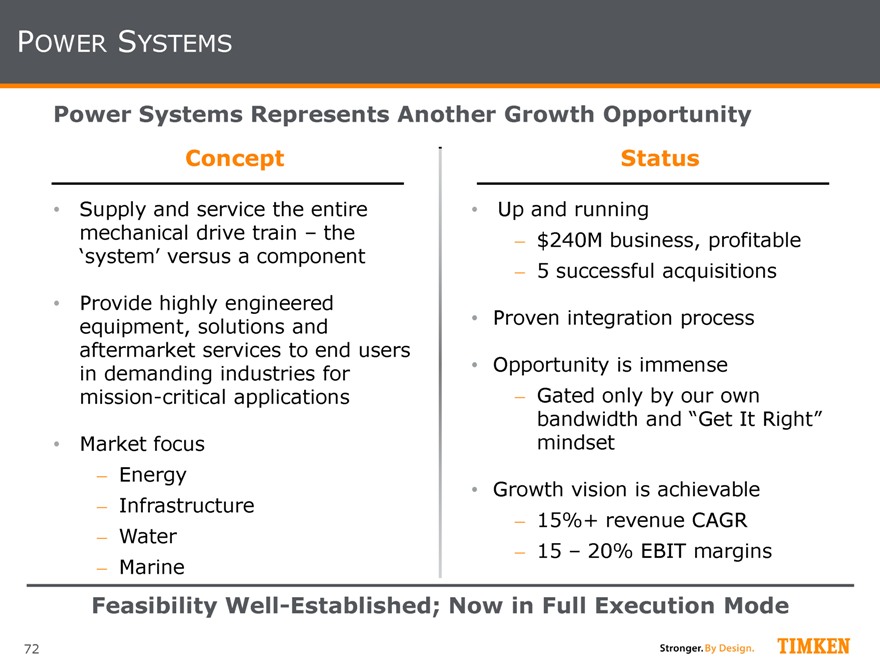

POWER SYSTEMS

Power Systems Represents Another Growth Opportunity

Concept Status

Supply and service the entire Up and running

mechanical drive train – the $240M business, profitable

‘system’ versus a component 5 successful acquisitions

Provide highly engineered

equipment, solutions and Proven integration process

aftermarket services to end users

in demanding industries for Opportunity is immense

mission-critical applications Gated only by our own

bandwidth and “Get It Right”

Market focus mindset

Energy Growth vision is achievable

Infrastructure 15%+ revenue CAGR

Water 15 – 20% EBIT margins

Marine

Feasibility Well-Established; Now in Full Execution Mode

72

|

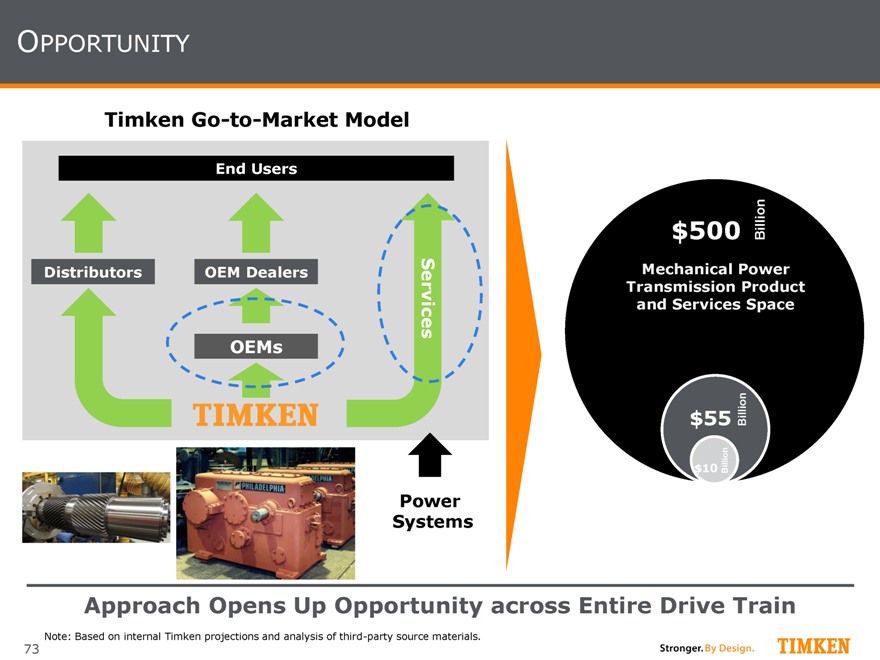

OPPORTUNITY

Timken Go-to-Market Model

End Users

Distributors OEM Dealers

Services

OEMs

Power

Systems

$500 Billion

Mechanical Power Transmission Product and Services Space

$55 Billion

$10 Billion

Approach Opens Up Opportunity across Entire Drive Train

Note: Based on internal Timken projections and analysis of third-party source materials.

73

|

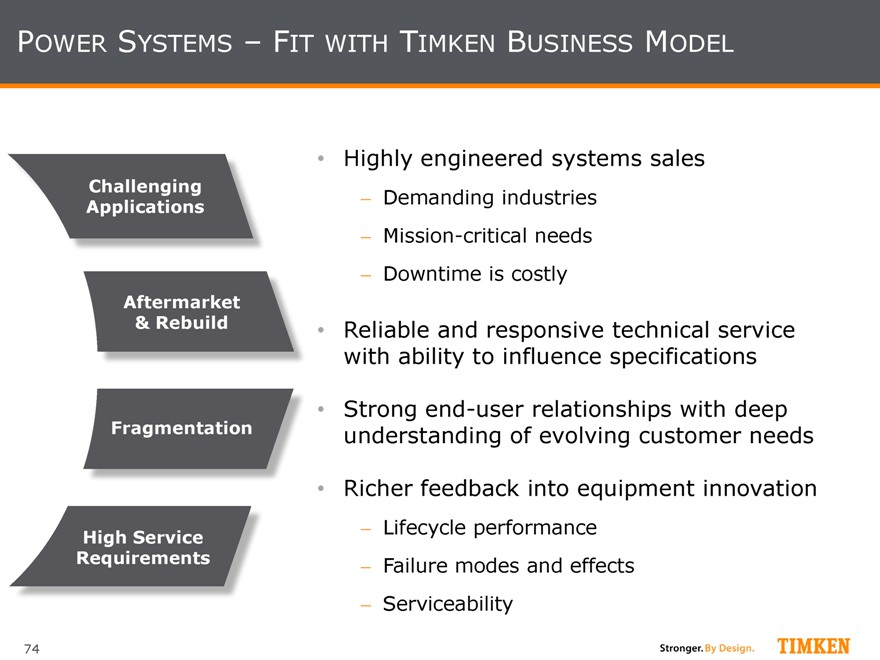

POWER SYSTEMS – FIT WITH TIMKEN BUSINESS MODEL

Challenging Applications

Aftermarket

& Rebuild Fragmentation

High Service Requirements

Highly engineered systems sales

Demanding industries

Mission-critical needs

Downtime is costly

Reliable and responsive technical service with ability to influence specifications

Strong end-user relationships with deep understanding of evolving customer needs

Richer feedback into equipment innovation

Lifecycle performance

Failure modes and effects

Serviceability

74

|

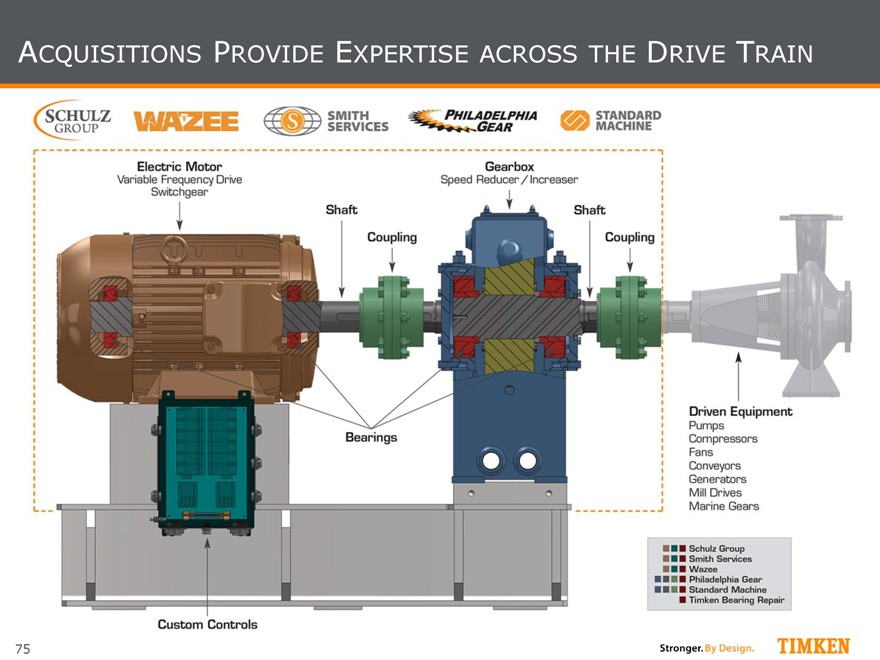

ACQUISITIONS PROVIDE EXPERTISE ACROSS THE DRIVE TRAIN

75

|

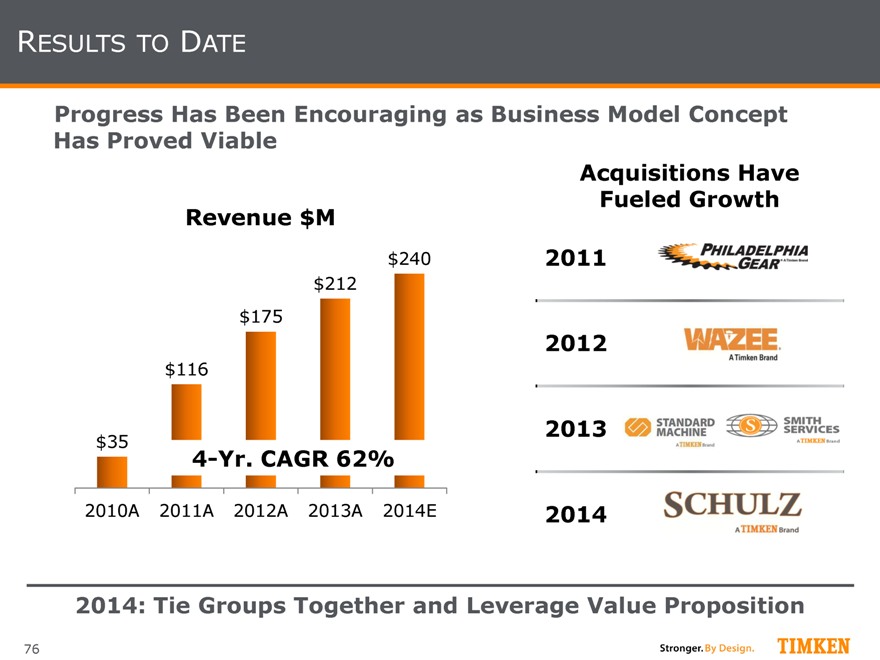

RESULTS TO DATE

Progress Has Been Encouraging as Business Model Concept Has Proved Viable

Revenue $M

$240

$212

$175

$116

$35

4-Yr. CAGR 62%

2010A 2011A 2012A 2013A 2014E

Acquisitions Have Fueled Growth

2011

2012

2013

2014

2014: Tie Groups Together and Leverage Value Proposition

76

|

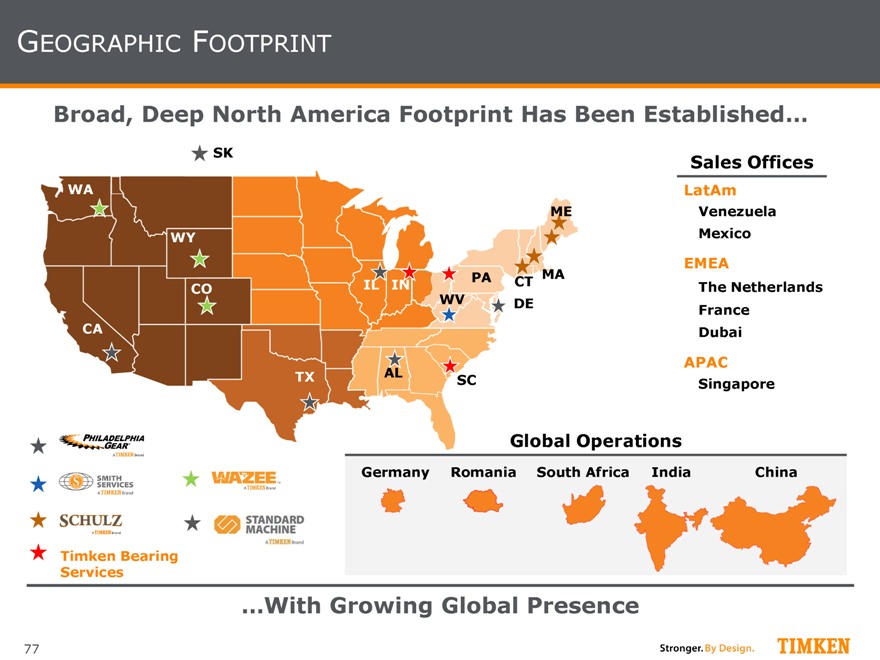

GEOGRAPHIC FOOTPRINT

Broad, Deep North America Footprint Has Been Established…

SK Sales Offices

WA LatAm

ME Venezuela

WY Mexico

EMEA

CO IL IN PA CT MA The Netherlands

WV DE France

CA Dubai

AL APAC

TX SC Singapore

Global Operations

Germany Romania South Africa India China

Timken Bearing

Services

…With Growing Global Presence

77

|

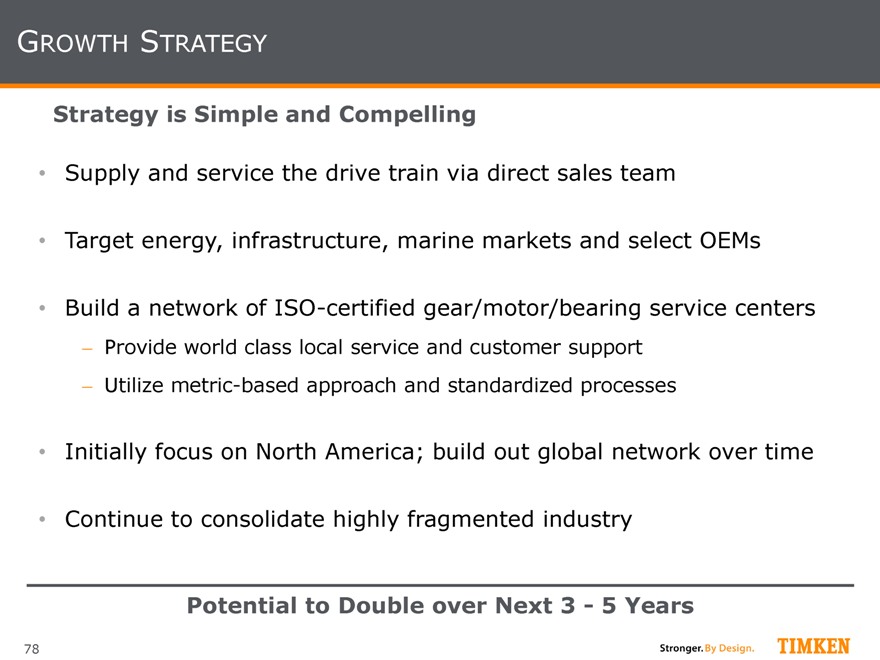

GROWTH STRATEGY

Strategy is Simple and Compelling

Supply and service the drive train via direct sales team

Target energy, infrastructure, marine markets and select OEMs

Build a network of ISO-certified gear/motor/bearing service centers

Provide world class local service and customer support

Utilize metric-based approach and standardized processes

Initially focus on North America; build out global network over time

Continue to consolidate highly fragmented industry

Potential to Double over Next 3—5 Years

78

|

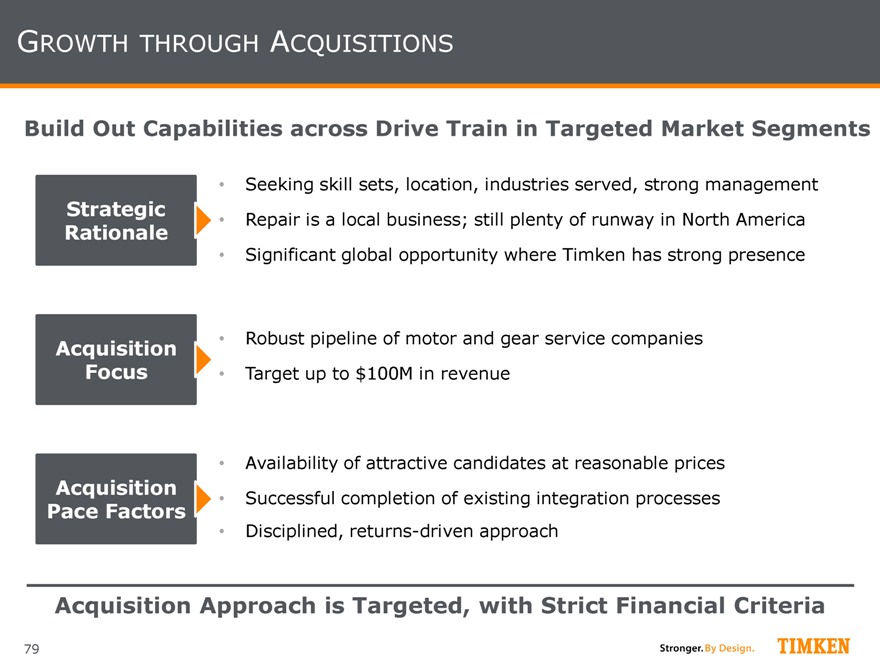

GROWTH THROUGH ACQUISITIONS

Build Out Capabilities across Drive Train in Targeted Market Segments

Seeking skill sets, location, industries served, strong management

Strategic Repair is a local business; still plenty of runway in North America

Rationale

Significant global opportunity where Timken has strong presence

Acquisition Robust pipeline of motor and gear service companies

Focus Target up to $100M in revenue

Availability of attractive candidates at reasonable prices

Acquisition Successful completion of existing integration processes

Pace Factors

Disciplined, returns-driven approach

Acquisition Approach is Targeted, with Strict Financial Criteria

79

|

SUMMARY

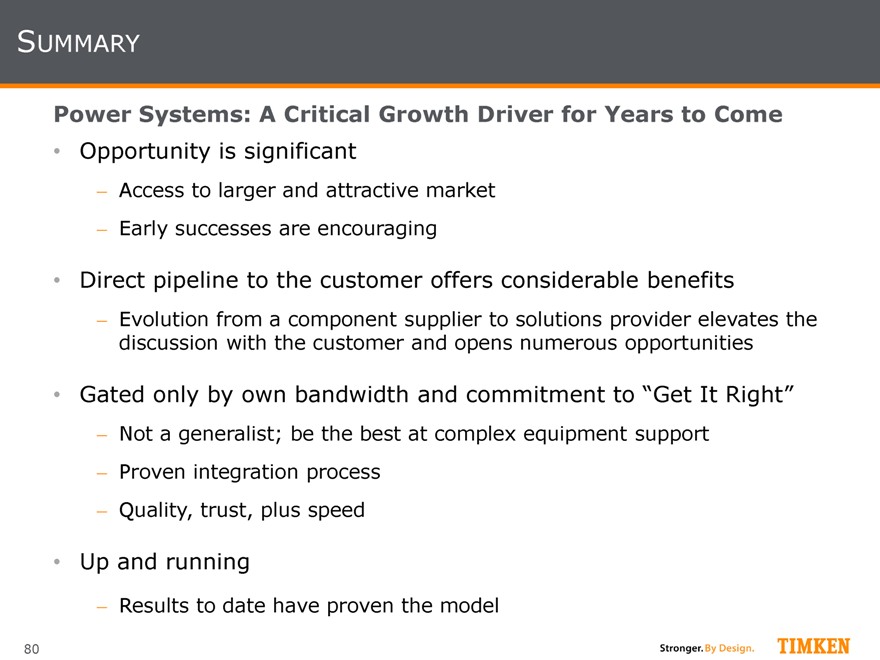

Power Systems: A Critical Growth Driver for Years to Come

Opportunity is significant

Access to larger and attractive market

Early successes are encouraging

Direct pipeline to the customer offers considerable benefits

Evolution from a component supplier to solutions provider elevates the discussion with the customer and opens numerous opportunities

Gated only by own bandwidth and commitment to “Get It Right”

Not a generalist; be the best at complex equipment support

Proven integration process

Quality, trust, plus speed

Up and running

Results to date have proven the model

80

|

Capturing Niche Opportunities

Brian Ruel, Vice President | Mobile Industries

|

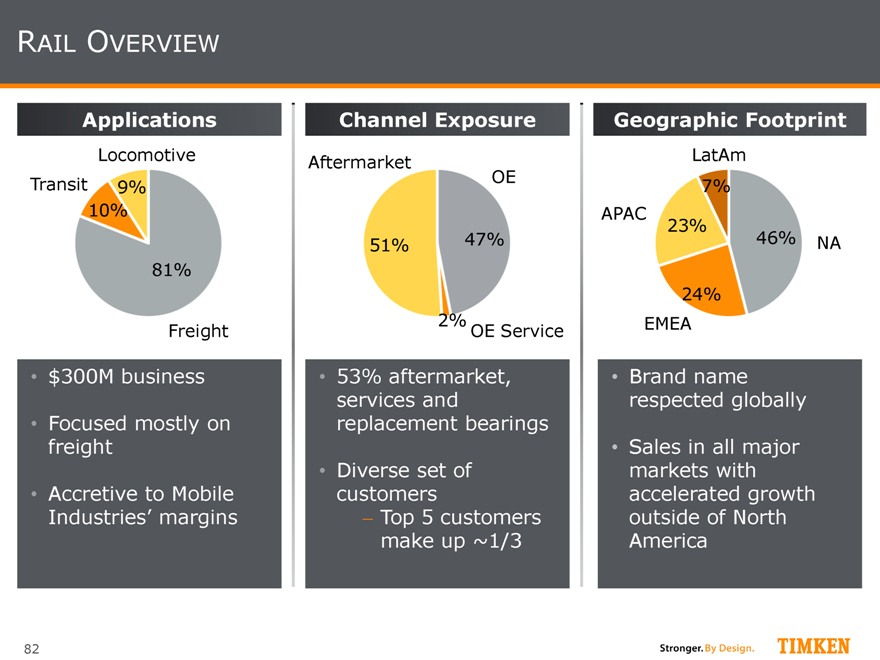

RAIL OVERVIEW

Applications

Locomotive Transit 9% 10%

81%

Freight

$300M business

Focused mostly on freight

Accretive to Mobile

Industries’ margins

Channel Exposure

Aftermarket

OE

51% 47%

2%

OE Service

53% aftermarket, services and replacement bearings

Diverse set of customers

Top 5 customers make up ~1/3

Geographic Footprint

LatAm 7% APAC

23%

46% NA

24%

EMEA

Brand name respected globally

Sales in all major markets with accelerated growth outside of North America

82

|

RAIL – STRONG SECTOR DEMAND DRIVERS

Urbanization

Infrastructure

Development Sustainability

Rail will continue to be driven by:

Demand for minerals, agricultural products, autos, general freight, etc.

Demand for energy (e.g., coal, fracking sand, petroleum, etc.)

End-user efficiency needs

Increased payloads

Ample Forces to Yield GDP+ Growth

83

|

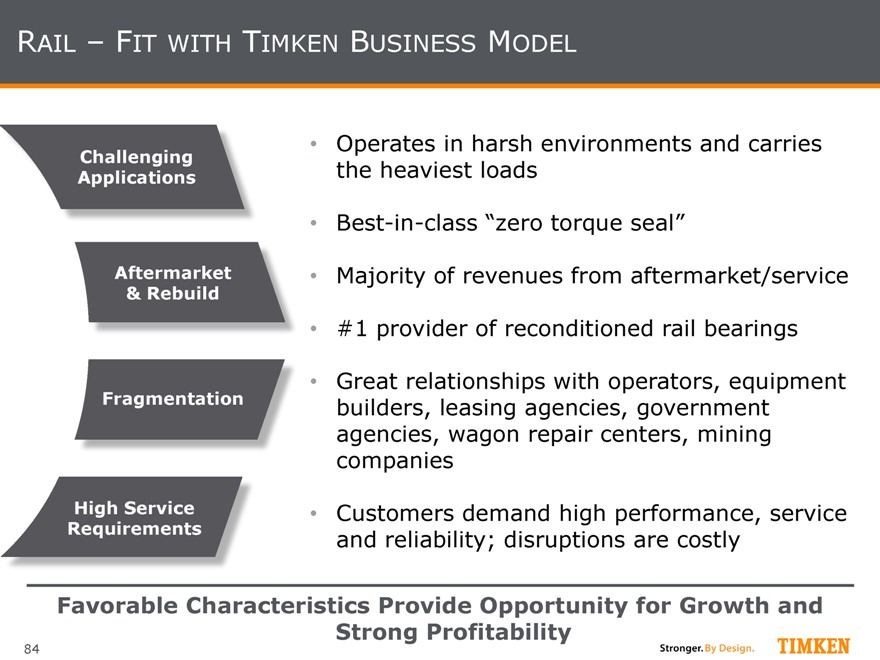

RAIL – FIT WITH TIMKEN BUSINESS MODEL

Operates in harsh environments and carries

Applications Challenging

the heaviest loads

Best-in-class “zero torque seal”

Aftermarket

Majority of revenues from aftermarket/service

& Rebuild

#1 provider of reconditioned rail bearings

Great relationships with operators, equipment

Fragmentation

builders, leasing agencies, government

agencies, wagon repair centers, mining

companies

High Service

Customers demand high performance, service

Requirements

and reliability; disruptions are costly

Favorable Characteristics Provide Opportunity for Growth and Strong Profitability

84

|

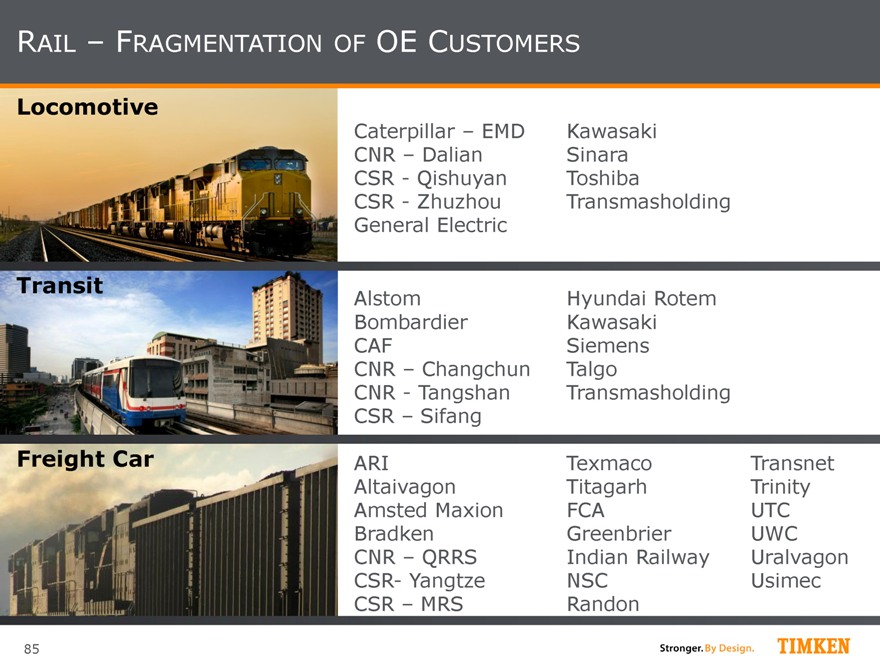

RAIL – FRAGMENTATION OF OE CUSTOMERS

Locomotive

Caterpillar – EMD Kawasaki CNR – Dalian Sinara CSR—Qishuyan Toshiba

CSR—Zhuzhou Transmasholding General Electric

Transit

Alstom Hyundai Rotem Bombardier Kawasaki CAF Siemens CNR – Changchun Talgo CNR—Tangshan Transmasholding CSR – Sifang

Freight Car ARI Texmaco Transnet Altaivagon Titagarh Trinity Amsted Maxion FCA UTC

Bradken Greenbrier UWC CNR – QRRS Indian Railway Uralvagon CSR- Yangtze NSC Usimec CSR – MRS Randon

85

|

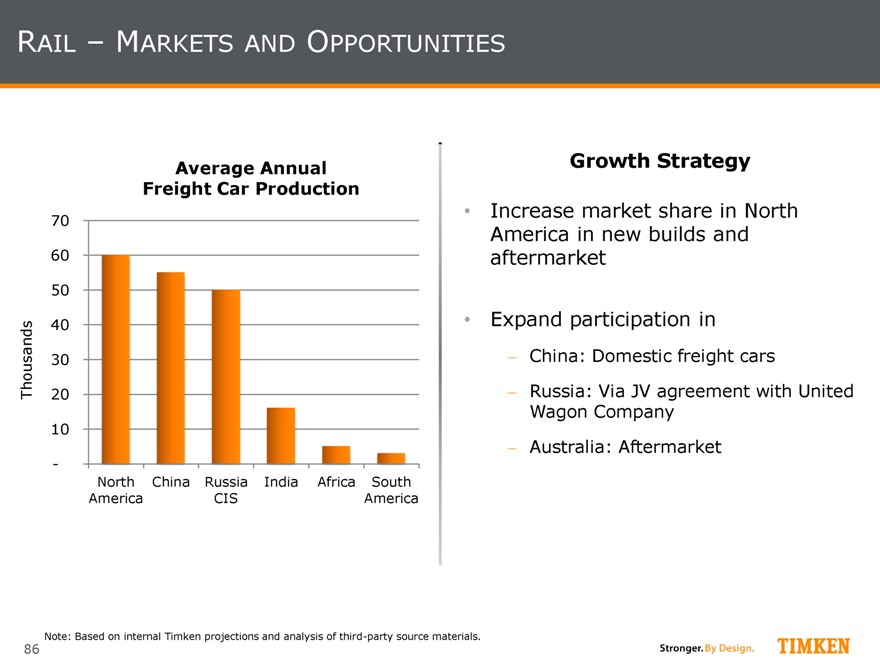

RAIL – MARKETS AND OPPORTUNITIES

Average Annual Freight Car Production

70 60 50

40 Thousands 30 20

10

-

North China Russia India Africa South

America CIS America

Growth Strategy

Increase market share in North America in new builds and aftermarket

Expand participation in

China: Domestic freight cars

Russia: Via JV agreement with United Wagon Company

Australia: Aftermarket

Note: Based on internal Timken projections and analysis of third-party source materials.

86

|

SUMMARY

Rail – A Strong and Vital Part of the Mobile Industries Portfolio

Continue to grow in concert with macro drivers

Focus on China and Russia freight car markets to drive growth

Profitable business that adds value to customers

Great fit with the Timken Business Model

Strong, deep customer relationships around the globe

87

|

Financial Review Phil Fracassa, CFO

|

DISCLAIMER

This presentation contains certain unaudited pro forma financial data derived from the historical consolidated financial statements and accounting records of the Company that have been adjusted to present the estimated impact from the removal of the TimkenSteel Corporation business from the historical financial results of the Company. This data does not necessarily reflect the financial position and results of operations that will be presented within the

Company’s consolidated financial statements subsequent to the completion of the planned spinoff of TimkenSteel Corporation. In addition, this data does not reflect what the financial position and results of operations would have been if the Company had actually operated without the TimkenSteel Corporation business during the periods shown nor are they necessarily indicative of the Company’s future results of operations or financial condition.

The assumptions and estimates used and adjustments derived from such assumptions are based on currently available information as of June 19, 2014, and management believes such assumptions and estimates are reasonable under the circumstances.

89

|

WHAT YOU’LL HEAR TODAY

TimkenSteel spinoff update

Improved outlook for 2014; increasing EPS guidance by $0.15

More efficient use of balance sheet

Intend to reach targeted leverage in 2015

Capital allocation plan; a more disciplined and robust approach

Intending to maintain $0.25 quarterly dividend despite lost earnings from spinoff

Newly authorized additional 10M share repurchase plan

New long-term targets

Note: 2014 outlook reflects The Timken Company post spinoff of the Steel business.

90

|

STEEL SPINOFF UPDATE

Spinoff of TimkenSteel Corporation Remains On Track

A leading manufacturer of SBQ steel bars and seamless mechanical tubing

Tailored products and services for most demanding applications

Form 10 effective June 10, 2014

Record Date: June 23, 2014

Name: TimkenSteel Corporation

NYSE-listed: “TMST”

When-issued trading expected June 19, 2014

Distribution targeted for June 30, 2014 (end of day)

TKR shareholders to receive

1 TMST share for every 2 TKR shares owned

91

|

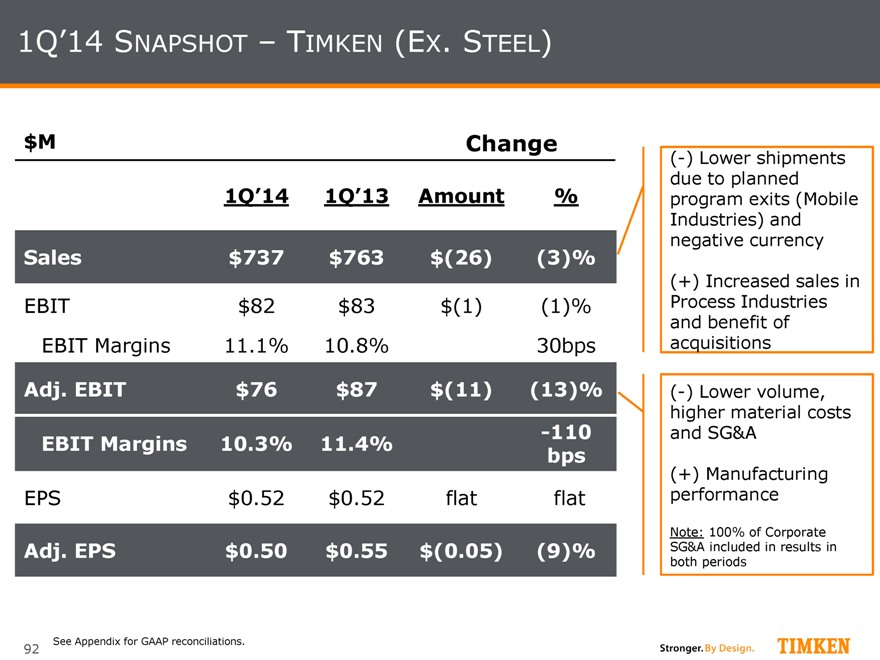

1Q’14 SNAPSHOT – TIMKEN (EX. STEEL)

$M

Change

1Q’14

1Q’13

Amount

%

Sales

$737

$763

$(26)

(3)%

EBIT

$82

$83

$(1)

(1)%

EBIT Margins

11.1%

10.8%

30bps

Adj. EBIT

$76

$87

$(11)

(13)%

-110

EBIT Margins

10.3%

11.4%

bps

EPS

$0.52

$0.52

flat

flat

Adj. EPS

$0.50

$0.55

$(0.05)

(9)%

(-) Lower shipments due to planned program exits (Mobile Industries) and negative currency

(+) Increased sales in Process Industries and benefit of acquisitions

(-) Lower volume, higher material costs and SG&A

(+) Manufacturing performance

Note: 100% of Corporate SG&A included in results in both periods

See Appendix for GAAP reconciliations.

92

|

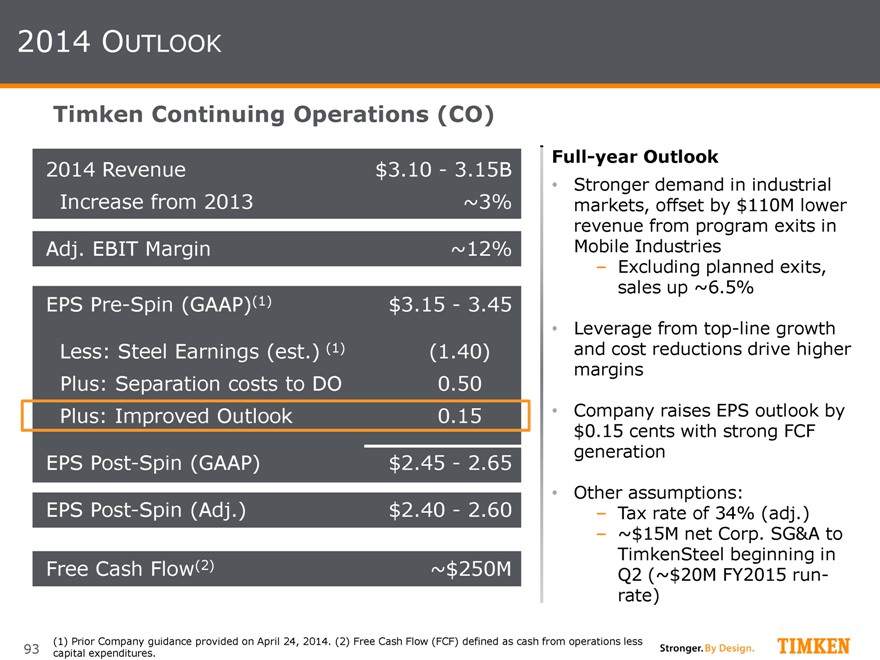

2014 OUTLOOK

Timken Continuing Operations (CO)

2014 Revenue

$3.10 -

3.15B

Increase from 2013

~3%

Adj. EBIT Margin

~12%

EPS

Pre-Spin (GAAP)(1)

$3.15

—

3.45

Less: Steel Earnings (est.) (1)

(1.40)

Plus: Separation costs to DO

0.50

Plus: Improved Outlook

0.15

EPS

Post-Spin(GAAP)

$2.45

—

2.65

EPS

Post-Spin(Adj.)

$2.40

—

2.60

Free Cash Flow(2)

~$250M

Full-year Outlook

Stronger demand in industrial markets, offset by $110M lower revenue from program exits in Mobile Industries

Excluding planned exits, sales up ~6.5%

Leverage from top-line growth and cost reductions drive higher margins

Company raises EPS outlook by

$0.15 cents with strong FCF generation

Other assumptions:

Tax rate of 34% (adj.)

~$15M net Corp. SG&A to TimkenSteel beginning in Q2 (~$20M FY2015 run-rate)

(1) Prior Company guidance provided on April 24, 2014. (2) Free Cash Flow (FCF) defined as cash from operations less capital expenditures. 93

|

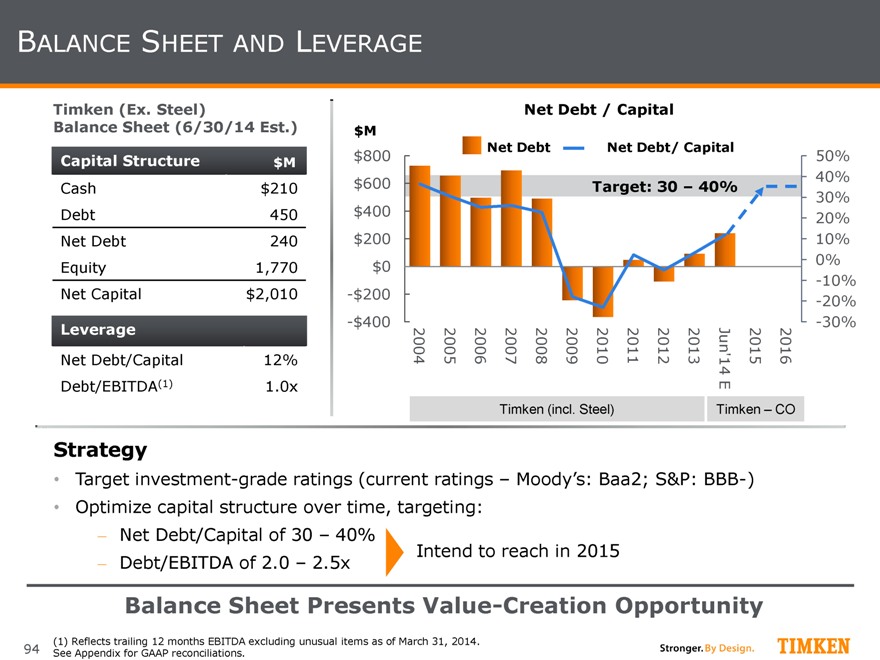

BALANCE SHEET AND LEVERAGE

Timken (Ex. Steel)

Balance Sheet (6/30/14 Est.)

Capital Structure

$M

Cash

$210

Debt

450

Net Debt

240

Equity

1,770

Net Capital

$2,010

Leverage

Net Debt/Capital

12%

Debt/EBITDA(1)

1.0x

Strategy

Target investment-grade ratings (current ratings – Moody’s: Baa2; S&P: BBB-)

Optimize capital structure over time, targeting:

Net Debt/Capital of 30 – 40%

Debt/EBITDA of 2.0 – 2.5x

Intend to reach in 2015

Balance Sheet Presents Value-Creation Opportunity

(1) Reflects trailing 12 months EBITDA excluding unusual items as of March 31, 2014. See Appendix for GAAP reconciliations.

$M $800 $600 $400 $200 $0

-$200

-$400

Timken (incl. Steel) Timken – CO

50% 40% 30% 20% 10% 0% -10% -20% -30%

Net Debt

/ Capital

Net Debt

Net Debt/ Capital

Target: 30 – 40%

2016 2015 Jun’14E 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004

94

|

95

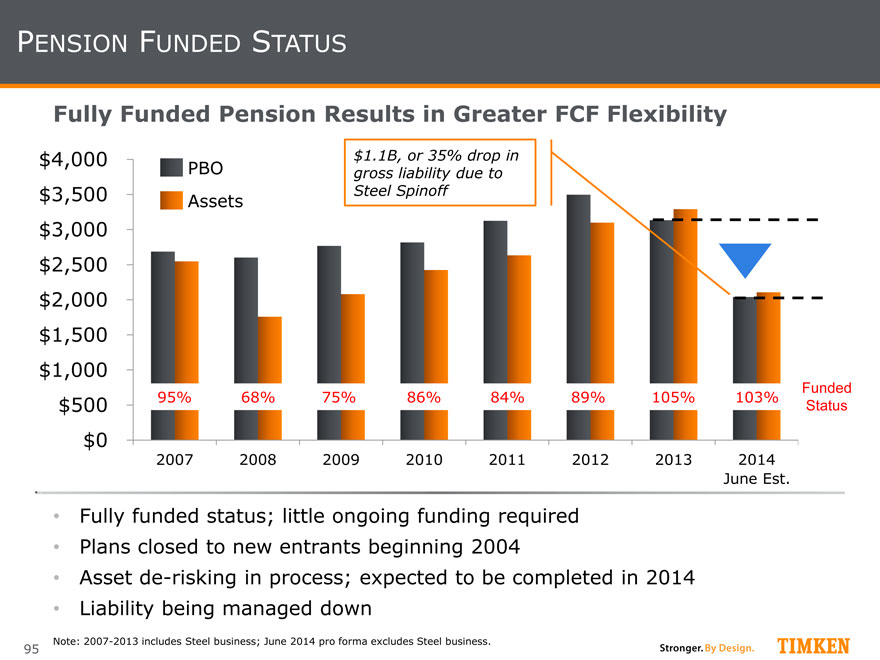

PENSION FUNDED STATUS

Fully funded status; little ongoing funding required

Plans closed to new entrants beginning 2004

Asset de-risking in process; expected to be completed in 2014

Liability being managed down

Fully Funded Pension Results in Greater FCF Flexibility

$0

$500

$1,000

$1,500

$2,000 $2,500

$3,000

$3,500

$4,000

2007

2008 2009

2010

2011

2012 2013

2014

Assets

PBO

95% 68%

75%

86%

84%

89%

105% 103%

June Est.

Funded

Status

Note: 2007-2013 includes Steel business; June 2014 pro forma excludes Steel business.

$1.1B, or 35% drop in gross liability due to Steel Spinoff

|

96

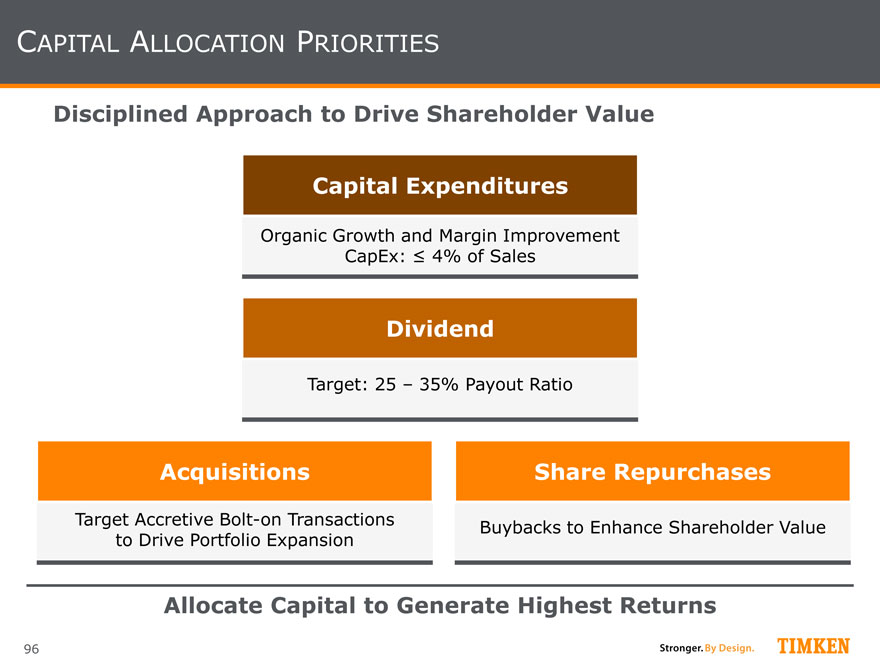

CAPITAL ALLOCATION PRIORITIES

Allocate Capital to Generate Highest Returns

Disciplined Approach to Drive Shareholder Value

Capital Expenditures

Organic Growth and Margin Improvement

CapEx: < 4% of Sales

Dividend

Target: 25 – 35% Payout Ratio

Share Repurchases

Buybacks to Enhance Shareholder Value

Acquisitions

Target Accretive Bolt-on Transactions

to Drive Portfolio Expansion

|

97

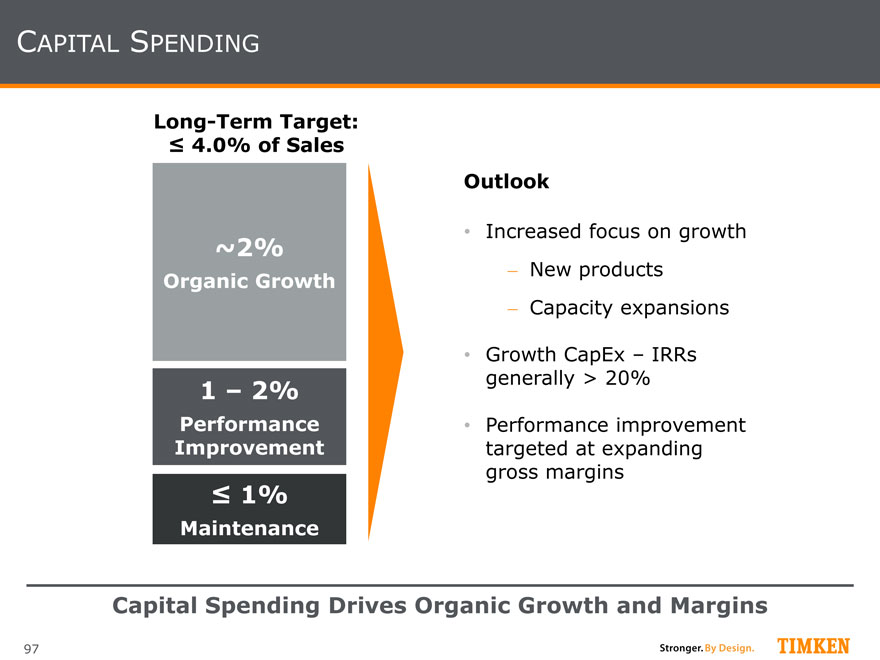

CAPITAL SPENDING

Capital Spending Drives Organic Growth and Margins

Outlook

Increased focus on growth

- New products

- Capacity expansions

Growth CapEx – IRRs generally > 20%

Performance improvement targeted at expanding gross margins

< 1%

Maintenance

1 – 2%

Performance Improvement

~2%

Organic Growth

Long-Term Target:

< 4.0% of Sales

|

98

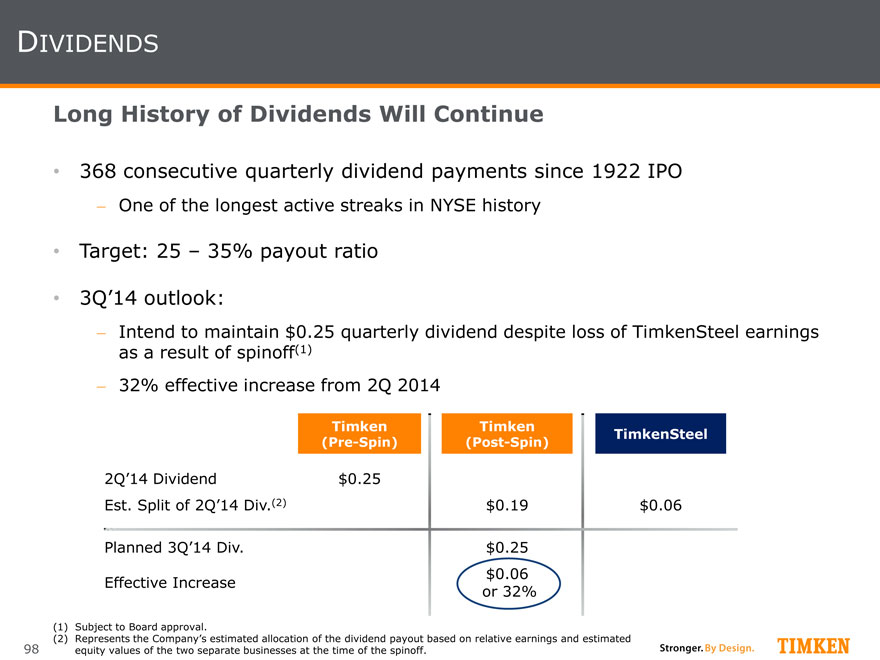

DIVIDENDS

368 consecutive quarterly dividend payments since 1922 IPO

- One of the longest active streaks in NYSE history

Target: 25 – 35% payout ratio

3Q’14 outlook:

- Intend to maintain $0.25 quarterly dividend despite loss of TimkenSteel earnings as a result of spinoff(1)

- 32% effective increase from 2Q 2014

Long History of Dividends Will Continue

Timken

(Pre-Spin)

Timken

(Post-Spin)

TimkenSteel

2Q’14 Dividend

$0.25

Est. Split of 2Q’14 Div.(2)

$0.19

$0.06

Planned 3Q’14 Div.

$0.25

Effective Increase

$0.06

or 32%

(1) Subject to Board approval.

(2) Represents the Company’s estimated allocation of the dividend payout based on relative earnings and estimated equity values of the two separate businesses at the time of the spinoff.

|

99

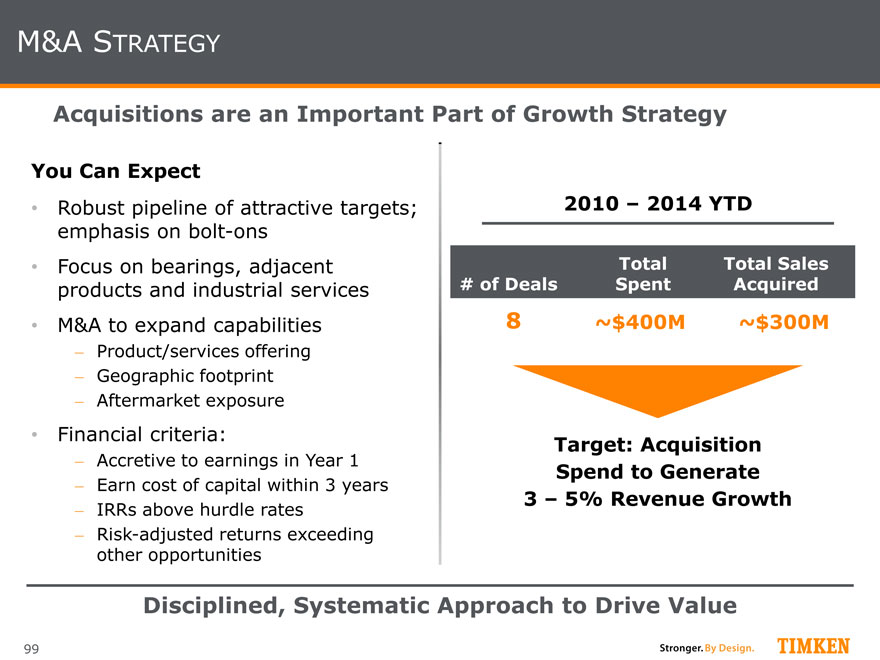

M&A STRATEGY

You Can Expect

Robust pipeline of attractive targets; emphasis on bolt-ons

Focus on bearings, adjacent products and industrial services

M&A to expand capabilities

- Product/services offering

- Geographic footprint

- Aftermarket exposure

Financial criteria:

- Accretive to earnings in Year 1

- Earn cost of capital within 3 years

- IRRs above hurdle rates

- Risk-adjusted returns exceeding other opportunities

Disciplined, Systematic Approach to Drive Value

Acquisitions are an Important Part of Growth Strategy

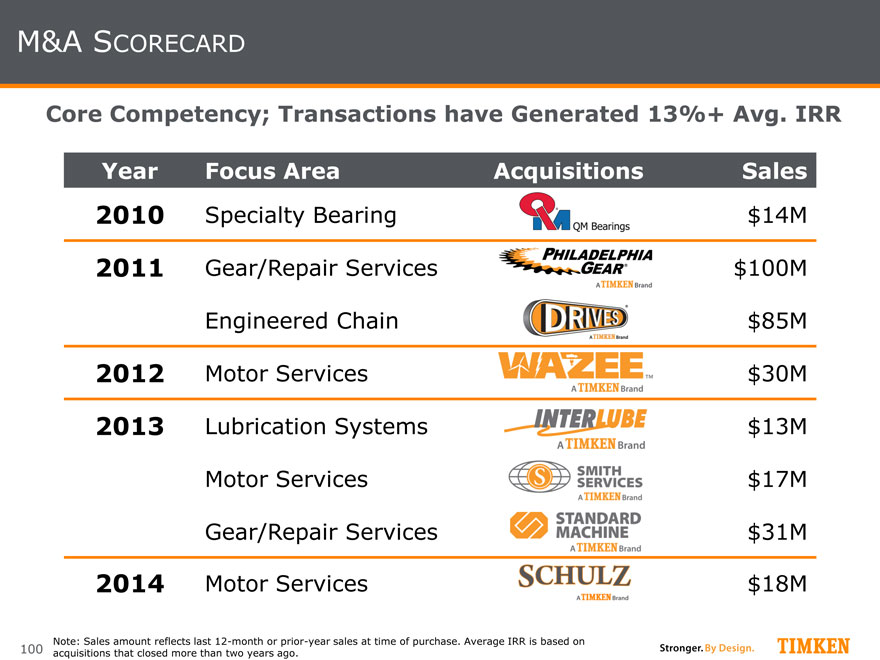

2010 – 2014 YTD

~$300M 8

Target: Acquisition

Spend to Generate

3 – 5% Revenue Growth

# of Deals Total Sales Acquired

Total

Spent

~$400M

|

100

M&A SCORECARD

Year

Focus Area

Acquisitions

Sales

2010

Specialty Bearing

$14M

2011

Gear/Repair Services

$100M

Engineered Chain

$85M

2012

Motor Services

$30M

2013

Lubrication Systems

$13M

Motor Services

$17M

Gear/Repair Services

$31M

2014

Motor Services

$18M

Note: Sales amount reflects last 12-month or prior-year sales at time of purchase. Average IRR is based on acquisitions that closed more than two years ago.

|

101

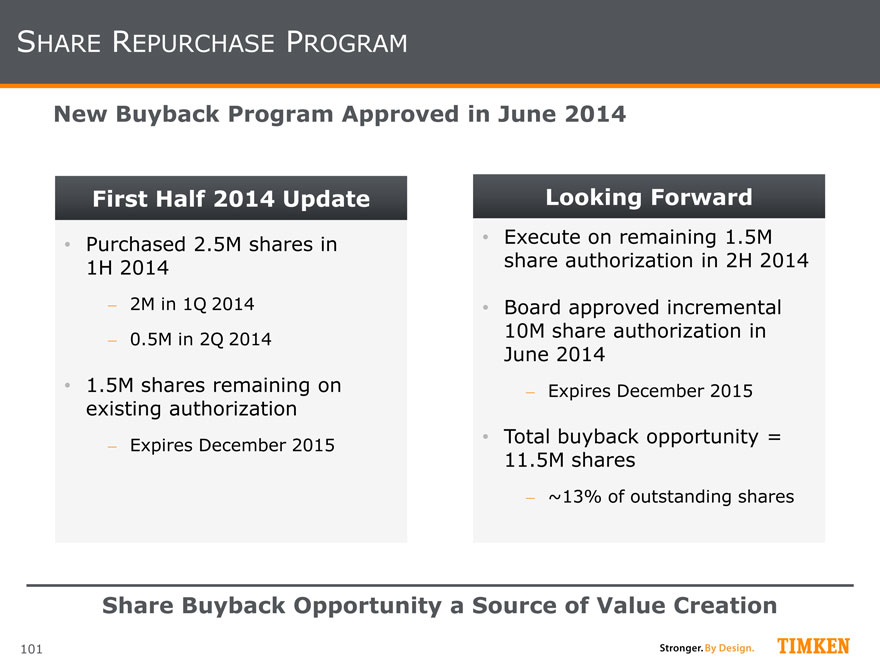

SHARE REPURCHASE PROGRAM

Share Buyback Opportunity a Source of Value Creation

New Buyback Program Approved in June 2014

Execute on remaining 1.5M share authorization in 2H 2014

Board approved incremental 10M share authorization in June 2014

- Expires December 2015

Total buyback opportunity = 11.5M shares

- ~13% of outstanding shares

Looking Forward

Purchased 2.5M shares in 1H 2014

- 2M in 1Q 2014

- 0.5M in 2Q 2014

1.5M shares remaining on existing authorization

- Expires December 2015

First Half 2014 Update

|

102

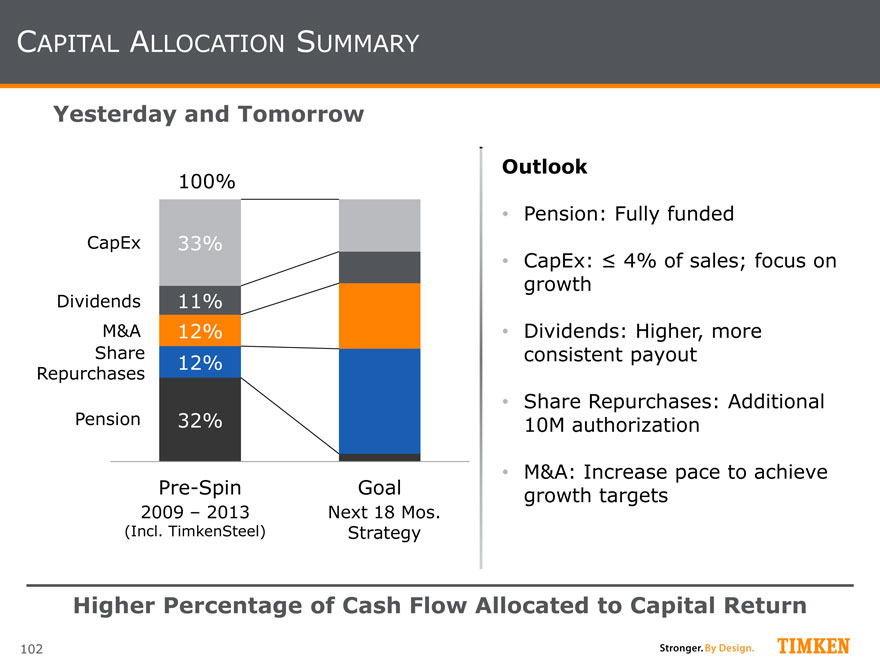

CAPITAL ALLOCATION SUMMARY

Higher Percentage of Cash Flow Allocated to Capital Return

Yesterday and Tomorrow

32% 12%

12% 11%

33%

Pre-Spin

Goal

Pension

Share Repurchases

CapEx

Dividends

M&A

100%

2009 – 2013

(Incl. TimkenSteel)

Outlook

Pension: Fully funded

CapEx: < 4% of sales; focus on growth

Dividends: Higher, more consistent payout

Share Repurchases: Additional 10M authorization

M&A: Increase pace to achieve growth targets

Next 18 Mos.

Strategy

|

103

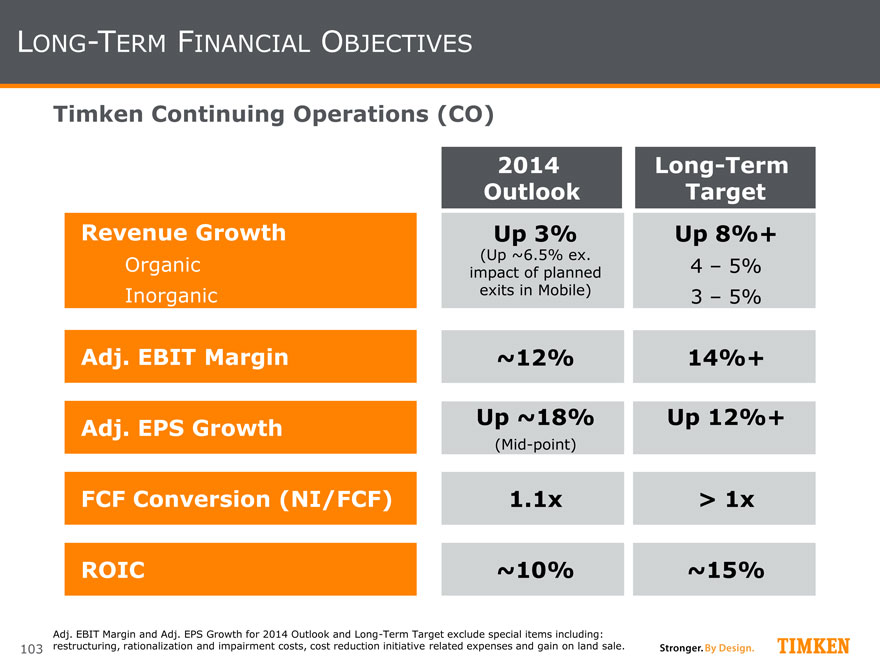

LONG-TERM FINANCIAL OBJECTIVES Timken Continuing Operations (CO)

(Up ~6.5% ex. impact of planned exits in Mobile)

(Mid-point) Adj. EBIT Margin

Revenue Growth

Organic

Inorganic

Adj. EPS Growth

FCF Conversion (NI/FCF)

ROIC Up 3%

Up 8%+

4 – 5%

3 – 5%

~12%

14%+

Up ~18%

Up 12%+

1.1x > 1x

~10%

~15%

2014

Outlook

Long-Term

Target

Adj. EBIT Margin and Adj. EPS Growth for 2014 Outlook and Long-Term Target exclude special items including: restructuring, rationalization and impairment costs, cost reduction initiative related expenses and gain on land sale.

|

104

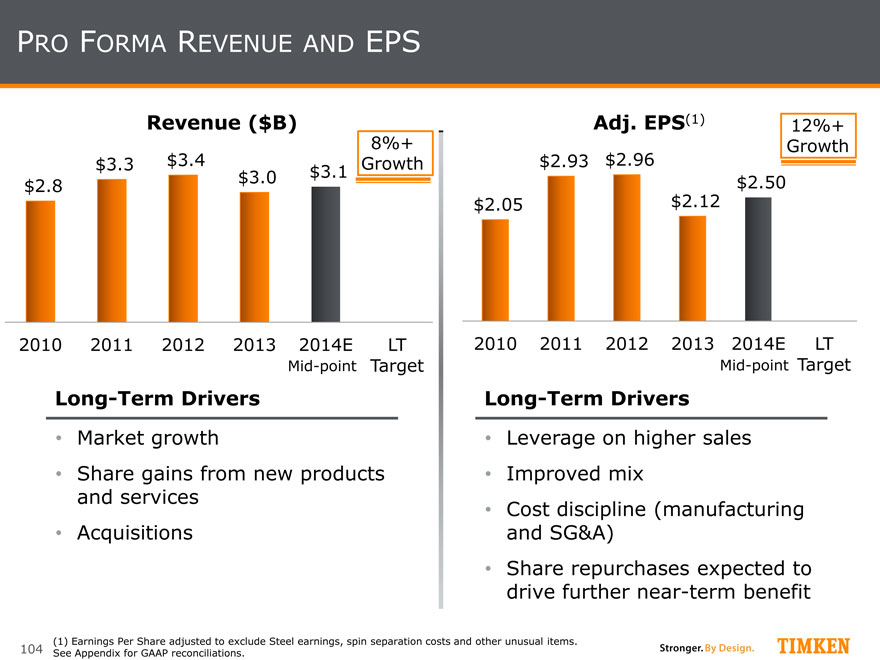

PRO FORMA REVENUE AND EPS

$2.8

$3.3

$3.4

$3.0

$3.1

2010

2011

2012 2013

2014E

LT Target

Revenue ($B)

Adj. EPS(1)

$2.05

$2.93

$2.96

$2.12

$2.50

2010

2011

2012

2013

2014E

LT Target

(1) Earnings Per Share adjusted to exclude Steel earnings, spin separation costs and other unusual items.

See Appendix for GAAP reconciliations. 8%+ Growth

12%+

Growth

Leverage on higher sales

Improved mix

Cost discipline (manufacturing and SG&A)

Share repurchases expected to drive further near-term benefit

Long-Term Drivers

Market growth

Share gains from new products and services

Acquisitions

Long-Term Drivers

Mid-point

Mid-point

|

105

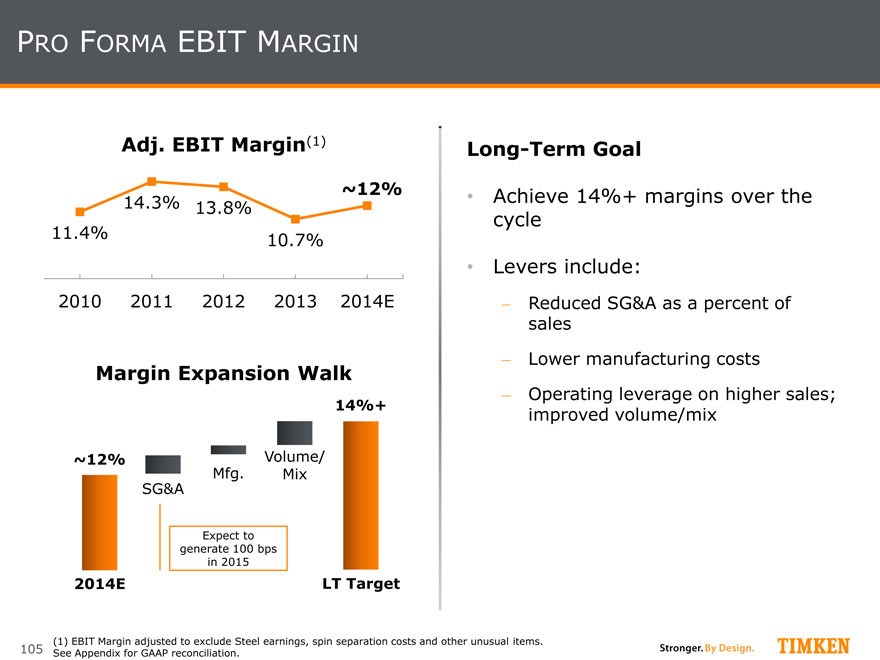

PRO FORMA EBIT MARGIN 11.4%

14.3%

13.8%

10.7%

2010

2011

2012

2013

2014E

Adj. EBIT Margin(1)

Long-Term Goal

Achieve 14%+ margins over the cycle

Levers include:

- Reduced SG&A as a percent of sales

- Lower manufacturing costs

- Operating leverage on higher sales; improved volume/mix

~12%

SG&A

2014E ~12%

LT Target

14%+

Mfg.

Volume/ Mix

Margin Expansion Walk

Expect to generate 100 bps in 2015 (1) EBIT Margin adjusted to exclude Steel earnings, spin separation costs and other unusual items. See Appendix for GAAP reconciliation.

|

106

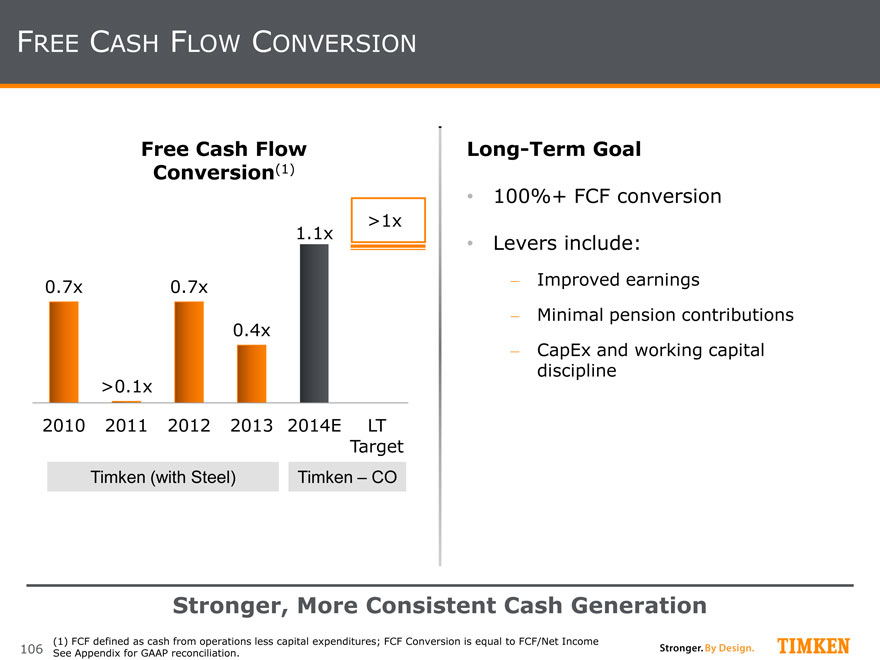

FREE CASH FLOW CONVERSION

0.7x

>0.1x

0.7x

0.4x

1.1x 2010

2011

2012

2013

2014E

LT Target

Free Cash Flow Conversion(1)

(1) FCF defined as cash from operations less capital expenditures; FCF Conversion is equal to FCF/Net Income

See Appendix for GAAP reconciliation.

Timken (with Steel)

Timken – CO

Long-Term Goal

100%+ FCF conversion

Levers include:

- Improved earnings

- Minimal pension contributions

- CapEx and working capital discipline

>1x

Stronger, More Consistent Cash Generation

|

107

KEY TAKE-AWAYS

Improved 2014 Outlook

- EPS: $2.40 - $2.60, excluding certain items(1)

A more disciplined and robust approach to capital allocation

- Intend to maintain $0.25 quarterly dividend despite lost earnings from spinoff

- 10M additional shares authorized for buyback through 2015

- Intend to reach targeted leverage in 2015

Strategy will drive strong sales and earnings growth going forward

- New long-term targets set

Well-Positioned to Deliver Top Quartile Shareholder Returns

A Compelling Investment

(1) Certain items include a gain on sale of land in Brazil and cost-reduction and plant rationalizations that net to $0.05 per share of expense.

|

Building on the Momentum

|

109

INVESTMENT SUMMARY

…Prepared to Deliver Strong Shareholder Value

Timken is a Compelling Investment…

High-Margin Business Based on Differentiated Business Model

- Fragmented, diverse end markets and customers

- Attractive mix

- Global growth opportunity

Strong Management Team Focused on Results

Improved Cash Generation

Mobile Exits Complete: Growth on the Horizon

Increased Return of Capital

|

Executive Bios

|

111

The great-grandson of The Timken Company’s original founder Henry Timken, John M. Timken, Jr., 62, was elected non-executive chairman of The Timken Company in May 2014. A private investor and successful entrepreneur, he has been a significant Timken shareholder for many years. Timken currently is co-founder and serves as a director of Amgraph Packaging, a national supplier of flexible package printing used by major food and beverage brands and private labels. His entrepreneurial activities cover a wide range of businesses and interests. Timken founded his first venture shortly after graduating from The College of Wooster, establishing Essex Racing Services. His company distributed Cosworth racing engines, Van Diemen racing cars, and provided both fabrication and performance racing engineering services. Beyond racing, his passion for business building has continued with involvement in ventures ranging from injection molding, to ophthalmic laboratories, to logistics and trucking. Timken also has owned a cable television business and established one of North America’s largest commercial mushroom farms. His ability as an investor to identify and help increase value across a range of businesses provides the Timken board with important input in evaluating and guiding the company in making important capital allocation decisions. Since joining the board in 1986, Timken has played a major role in the company’s strategic drive to add product lines that complement its bearing product portfolio, including the largest acquisition in 2003 of The Torrington Company. Originally from New London, Conn., Timken currently lives in Vermont, where he serves as a selectman for the town of Bridgewater.

JOHN M. TIMKEN JR. CHAIRMAN, BOARD OF DIRECTORS

|

112

Richard G. Kyle was named as the president and chief executive officer of The Timken Company by the board of directors in May 2014. Kyle was elected to the board of directors in 2013.

Kyle oversees all aspects of The Timken Company, which consists of the Aerospace, Process and Mobile industries segments. The company provides Timken® bearings and a broad range of other services and products—including transmissions, gearboxes, motors, lubrication systems and chain—all of which are used in diversified markets to keep the world in motion.

Kyle previously served as chief operating officer of the Bearings and Power Transmission Group, a position to which he was named in 2013. In 2012, he was named group president of Timken, responsible for the Aerospace and Steel segments as well as the engineering and technology organization.

He started his Timken career in 2006 as vice president of manufacturing, responsible for the company’s global bearings operations. He was named president of the Aerospace and Mobile Industries segments in 2008. During his tenure, he led Mobile Industries through significant changes, reshaping its product portfolio, market mix and operating capabilities, which yielded dramatic improvements in the company’s financial performance. Before joining Timken, Kyle held management positions with Cooper Industries and later was vice president of operations for a division of Hubbell, Inc.

A native of Mishawaka, Ind., Kyle received a bachelor’s degree in mechanical engineering from Purdue University and earned a master of business administration degree in management from Northwestern University’s Kellogg Graduate School of Management. He serves on the board of directors of the United Way of Greater Stark County.

RICHARD G. KYLE PRESIDENT AND CHIEF EXECUTIVE OFFICER

|

113

Philip D. Fracassa serves as chief financial officer of The Timken Company. Fracassa leads the company’s financial organization, including external reporting, treasury, tax, financial planning and analysis, internal audit, risk management and investor relations. In addition, he oversees information technology and enterprise services, and maintains leadership of the project to spin off the steel business from The Timken Company.

Fracassa previously served as senior vice president for corporate planning and development, a role to which he was named in 2012. He led the company in developing enterprise strategy, including identification and evaluation of growth opportunities.

Fracassa joined Timken in 2005, and has held several key finance positions, including senior vice president and group controller for the Bearings and Power Transmission Group, senior vice president of tax and treasury, and vice president of tax.

Prior to joining Timken, Fracassa was senior tax counsel and director of tax for Visteon Corporation. He began his career with what is now PricewaterhouseCoopers in Detroit and also served as a tax attorney with General Motors Corporation.

Fracassa is a member of Financial Executives International, the Manufacturers Alliance for Productivity and Innovation (MAPI) and the Association for Corporate Growth. He was included in Treasury & Risk magazine’s list of 40 distinguished finance executives under the age of 40 (2007) and top 100 most influential persons in finance (2009).

He is active in community affairs and currently serves as chairman of the board for the Canton Regional Chamber of Commerce.

Fracassa holds a bachelor’s degree in accounting and a juris doctor degree in law from the University of Detroit. In 2011, he completed the Advanced Management Program at INSEAD. He is a certified public accountant and licensed attorney in the state of Michigan.

PHILIP D. FRACASSA CHIEF FINANCIAL OFFICER

|

114

Christopher A. Coughlin is group president at The Timken Company.

Named to the position in 2012, he is responsible for the company’s Mobile and Process Industries segments. He also has corporate-wide responsibilities for quality assurance and advancement activities. The Mobile Industries business is focused on growing globally by serving the mining, heavy-truck, construction, agriculture, rail and light-vehicle equipment markets with a broad offering of high-performance power transmission products and related services. The Process Industries segment provides bearings and related products and services for heavy industry, power transmission, energy and global distribution market sectors.

In 2010, Coughlin became president of Process Industries and Supply Chain. He was responsible for distribution and global supply chain management for the Bearings and Power Transmission Group as well as for the company’s global purchasing organization.

In 2004, Coughlin was named to lead a multiyear initiative to streamline business processes and implement an enterprise resource planning system. He previously was based in Colmar, France, where he held a variety of management positions including vice president of industrial equipment, vice president of process industries and vice president of primary metals. Coughlin began his Timken career in 1984 in the company’s steel operations.

Coughlin serves on the board of directors of the American Bearing Manufacturers Association and the Akron Canton Regional Foodbank.

He earned a bachelor’s degree in metallurgical engineering from the University of Cincinnati and a master’s degree in business administration from Case Western Reserve University.

CHRISTOPHER A. COUGHLIN GROUP PRESIDENT

|

115

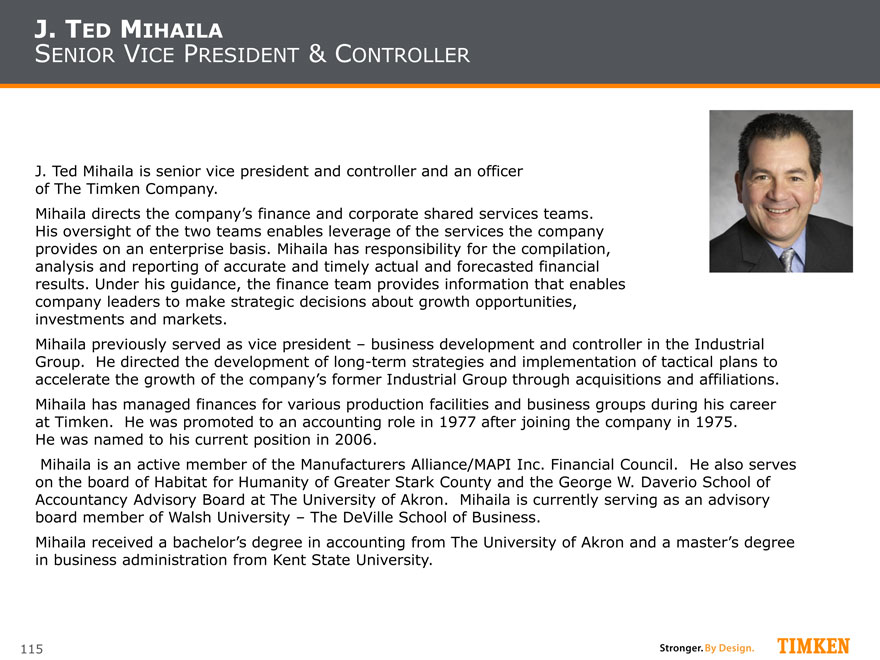

J. Ted Mihaila is senior vice president and controller and an officer of The Timken Company.

Mihaila directs the company’s finance and corporate shared services teams. His oversight of the two teams enables leverage of the services the company provides on an enterprise basis. Mihaila has responsibility for the compilation, analysis and reporting of accurate and timely actual and forecasted financial results. Under his guidance, the finance team provides information that enables company leaders to make strategic decisions about growth opportunities, investments and markets.

Mihaila previously served as vice president – business development and controller in the Industrial Group. He directed the development of long-term strategies and implementation of tactical plans to accelerate the growth of the company’s former Industrial Group through acquisitions and affiliations.

Mihaila has managed finances for various production facilities and business groups during his career at Timken. He was promoted to an accounting role in 1977 after joining the company in 1975. He was named to his current position in 2006.

Mihaila is an active member of the Manufacturers Alliance/MAPI Inc. Financial Council. He also serves on the board of Habitat for Humanity of Greater Stark County and the George W. Daverio School of Accountancy Advisory Board at The University of Akron. Mihaila is currently serving as an advisory board member of Walsh University – The DeVille School of Business.

Mihaila received a bachelor’s degree in accounting from The University of Akron and a master’s degree in business administration from Kent State University.

J. TED MIHAILA SENIOR VICE PRESIDENT & CONTROLLER

|

116

Richard M. Boyer is vice president of manufacturing for the Bearings & Power Transmission Group within The Timken Company.

Named to this position in 2012, Boyer is responsible for the operation of all global manufacturing facilities within the Mobile and Process Industries business unit. Additionally, he has oversight for the manufacturing advancement organization and the corporate purchasing function.

He joined Timken in 1984 and served nine years in the engineering and technology organizations before moving in 1993 to the Gaffney Plant in South Carolina, where he held various supervisory roles. In 1996, he was named project manager for the start-up of a new manufacturing facility in Winchester, Ky. In 2000, he was named manufacturing manager of the St. Clair Steel Plant in Eaton, Ohio. From 2001-03, he served as business development manager and then from 2003-07 he served as general manager of operations and supply chain for the precision steel components organization. In 2007, he served as manager of the Gambrinus Steel Plant in Canton, Ohio, before becoming director of manufacturing for 0-8 inch bearings in 2010.

Active in community affairs, Boyer serves on the executive board of directors for the Stark County affiliate of Junior Achievement.

Boyer holds a bachelor’s degree in mechanical engineering from The Ohio State University along with a master’s degree in mechanical engineering from The University of Akron and an executive master’s degree in business administration from Kent State University. He completed the EDGE executive development program for senior Timken leaders at the University of Virginia Darden School of Business in 2005.

RICHARD M. BOYER VICE PRESIDENT, MANUFACTURING

|

117

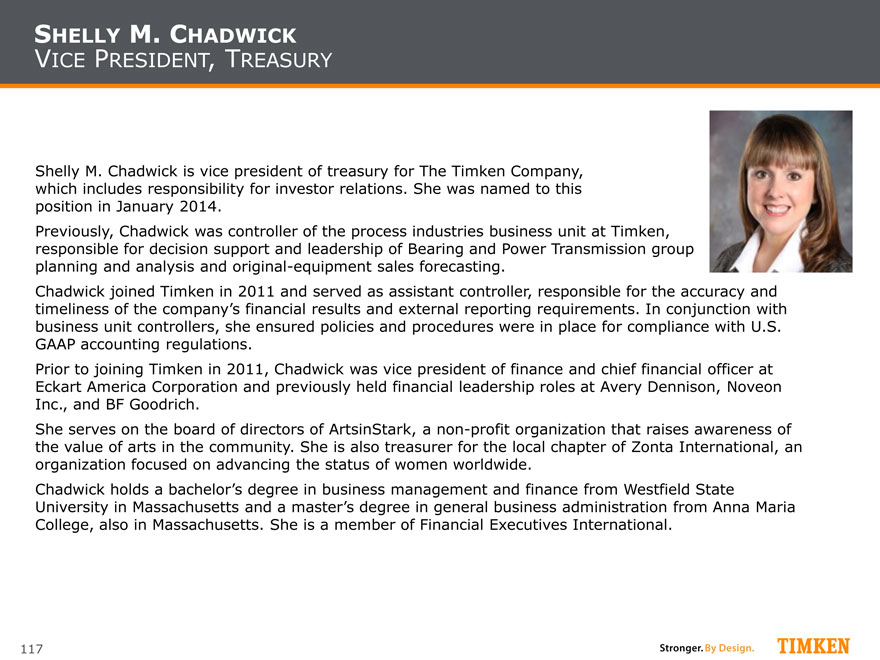

Shelly M. Chadwick is vice president of treasury for The Timken Company, which includes responsibility for investor relations. She was named to this position in January 2014.

Previously, Chadwick was controller of the process industries business unit at Timken, responsible for decision support and leadership of Bearing and Power Transmission group financial planning and analysis and original-equipment sales forecasting.

Chadwick joined Timken in 2011 and served as assistant controller, responsible for the accuracy and timeliness of the company’s financial results and external reporting requirements. In conjunction with business unit controllers, she ensured policies and procedures were in place for compliance with U.S. GAAP accounting regulations.

Prior to joining Timken in 2011, Chadwick was vice president of finance and chief financial officer at Eckart America Corporation and previously held financial leadership roles at Avery Dennison, Noveon Inc., and BF Goodrich.

She serves on the board of directors of ArtsinStark, a non-profit organization that raises awareness of the value of arts in the community. She is also treasurer for the local chapter of Zonta International, an organization focused on advancing the status of women worldwide.

Chadwick holds a bachelor’s degree in business management and finance from Westfield State University in Massachusetts and a master’s degree in general business administration from Anna Maria College, also in Massachusetts. She is a member of Financial Executives International. SHELLY M. CHADWICK VICE PRESIDENT, TREASURY

|

118

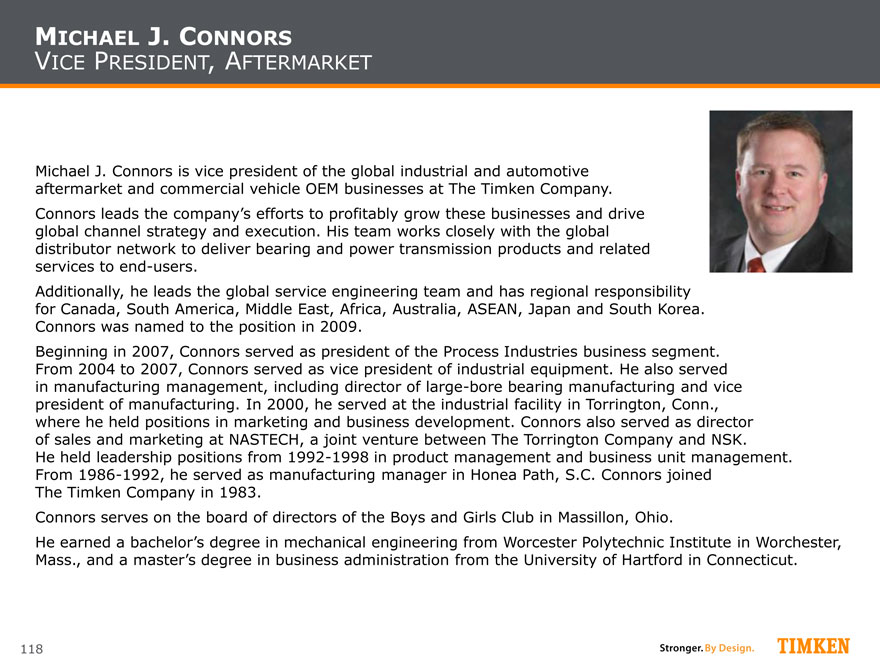

Michael J. Connors is vice president of the global industrial and automotive aftermarket and commercial vehicle OEM businesses at The Timken Company.

Connors leads the company’s efforts to profitably grow these businesses and drive global channel strategy and execution. His team works closely with the global distributor network to deliver bearing and power transmission products and related services to end-users.

Additionally, he leads the global service engineering team and has regional responsibility for Canada, South America, Middle East, Africa, Australia, ASEAN, Japan and South Korea. Connors was named to the position in 2009.

Beginning in 2007, Connors served as president of the Process Industries business segment. From 2004 to 2007, Connors served as vice president of industrial equipment. He also served in manufacturing management, including director of large-bore bearing manufacturing and vice president of manufacturing. In 2000, he served at the industrial facility in Torrington, Conn., where he held positions in marketing and business development. Connors also served as director of sales and marketing at NASTECH, a joint venture between The Torrington Company and NSK. He held leadership positions from 1992-1998 in product management and business unit management. From 1986-1992, he served as manufacturing manager in Honea Path, S.C. Connors joined The Timken Company in 1983.

Connors serves on the board of directors of the Boys and Girls Club in Massillon, Ohio.

He earned a bachelor’s degree in mechanical engineering from Worcester Polytechnic Institute in Worchester, Mass., and a master’s degree in business administration from the University of Hartford in Connecticut.

MICHAEL J. CONNORS VICE PRESIDENT, AFTERMARKET

|

119

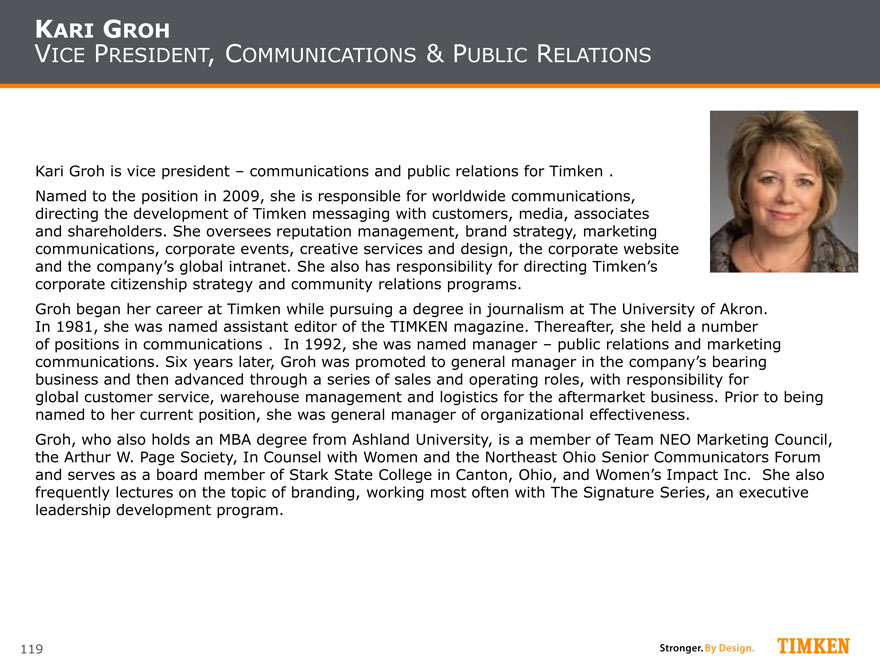

Kari Groh is vice president – communications and public relations for Timken .

Named to the position in 2009, she is responsible for worldwide communications, directing the development of Timken messaging with customers, media, associates and shareholders. She oversees reputation management, brand strategy, marketing communications, corporate events, creative services and design, the corporate website and the company’s global intranet. She also has responsibility for directing Timken’s corporate citizenship strategy and community relations programs.

Groh began her career at Timken while pursuing a degree in journalism at The University of Akron. In 1981, she was named assistant editor of the TIMKEN magazine. Thereafter, she held a number of positions in communications . In 1992, she was named manager – public relations and marketing communications. Six years later, Groh was promoted to general manager in the company’s bearing business and then advanced through a series of sales and operating roles, with responsibility for global customer service, warehouse management and logistics for the aftermarket business. Prior to being named to her current position, she was general manager of organizational effectiveness.

Groh, who also holds an MBA degree from Ashland University, is a member of Team NEO Marketing Council, the Arthur W. Page Society, In Counsel with Women and the Northeast Ohio Senior Communicators Forum and serves as a board member of Stark State College in Canton, Ohio, and Women’s Impact Inc. She also frequently lectures on the topic of branding, working most often with The Signature Series, an executive leadership development program.

KARI GROH VICE PRESIDENT, COMMUNICATIONS & PUBLIC RELATIONS

|

120