Exhibit 99.2

|

Exhibit 99.2

THE TIMKEN COMPANY

2Q 2014 EARNINGS

JULY 31, 2014

|

EARNINGS CALL DETAILS

Timken 2Q 2014 Conference Call Schedule

Conference Call: Thursday – July 31, 2014

11:00 a.m. Eastern Time

Live Dial-In: 800-344-6698 or 785-830-7979

(Call in 10 minutes prior to be included.)

Conference ID: Timken Earnings Call

Replay: Replay Dial-In available through August 14, 2014:

888-203-1112 or 719-457-0820

(Replay available approx. two hours after the live call.)

Replay Passcode: 2219857

Live Webcast: www.timken.com/investors

2

|

FORWARD-LOOKING STATEMENTS SAFE HARBOR AND

NON-GAAP FINANCIAL INFORMATION

Certain statements in this presentation (including statements regarding the company’s forecasts, beliefs, estimates and expectations) that are not historical in nature are “forward-looking” statements within the meaning of the

Private Securities Litigation Reform Act of 1995. In particular, the statements related to Timken’s plans, outlook, future financial performance, targets, projected sales, cash flows, liquidity and expectations regarding the future financial performance of the company, including the information under the headings “2Q 2014 Highlights”, “DeltaX”, “Performance Improvement” and “2014 Full-Year Outlook” are forward-looking. The company cautions that actual results may differ materially from those projected or implied in forward-looking statements due to a variety of important factors, including: the company’s ability to respond to the changes in its end markets that could affect demand for the company’s products; unanticipated changes in business relationships with customers or their purchases from the company; changes in the financial health of the company’s customers, which may have an impact on the company’s revenues, earnings and impairment charges; fluctuations in raw-material and energy costs; the impact of the company’s last-in, first-out accounting; weakness in global or regional economic conditions and financial markets; changes in the expected costs associated with product warranty claims; the ability to integrate acquired companies to achieve satisfactory operating results; the impact on operations of general economic conditions; fluctuations in customer demand; the impact on the company’s pension obligations due to the changes in interest rates or investment performance, the company’s ability to complete and achieve the benefits of its announced plans, programs, initiatives and capital investments; the taxable nature of the spinoff; and the company’s ability to realize the potential benefits of the spinoff of the steel business and avoid possible indemnification liabilities under certain agreements it entered into with TimkenSteel Corporation in connection with the spinoff. Additional factors are discussed in the company’s filings with the Securities and Exchange Commission, including the company’s annual report on Form 10-K for the year ended Dec. 31, 2013, quarterly reports on Form 10-Q and current reports on Form 8-K. Except as required by the federal securities laws, the company undertakes no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise.

This presentation includes certain non-GAAP financial measures as defined by the rules and regulations of the Securities and Exchange Commission. Reconciliation of those measures to the most directly comparable GAAP equivalents are provided in the Appendix to this presentation.

3

|

AGENDA

2Q Business & Strategy Update

Rich Kyle – President & CEO

2Q Financial Review

Phil Fracassa – CFO

Q & A with Timken Management

Rich Kyle – President & CEO

Phil Fracassa – CFO

Steve Tschiegg – Director, Capital Markets & Investor Relations

4

|

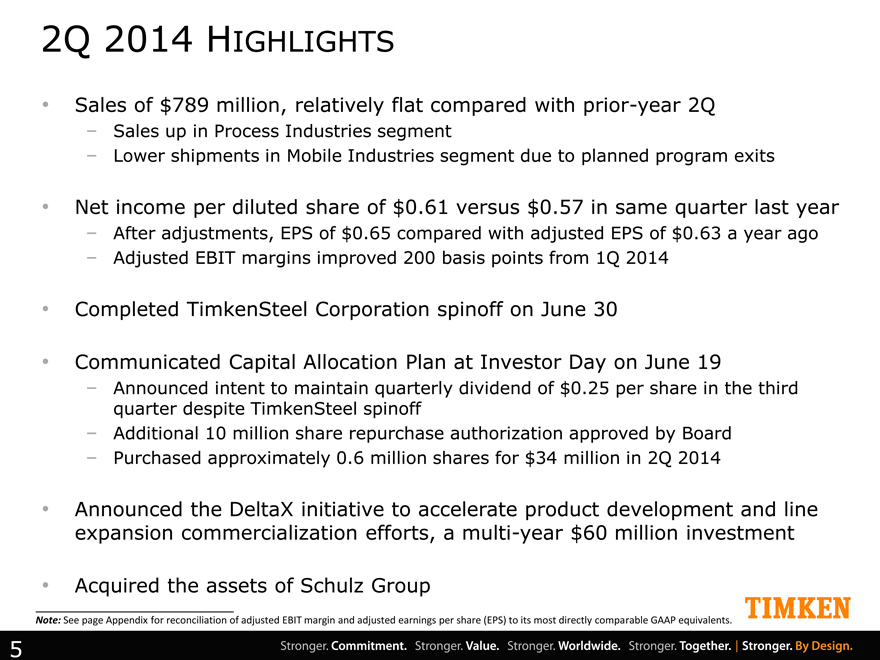

2Q 2014 HIGHLIGHTS

Sales of $789 million, relatively flat compared with prior-year 2Q

Sales up in Process Industries segment

Lower shipments in Mobile Industries segment due to planned program exits

Net income per diluted share of $0.61 versus $0.57 in same quarter last year

After adjustments, EPS of $0.65 compared with adjusted EPS of $0.63 a year ago

Adjusted EBIT margins improved 200 basis points from 1Q 2014

Completed TimkenSteel Corporation spinoff on June 30

Communicated Capital Allocation Plan at Investor Day on June 19

Announced intent to maintain quarterly dividend of $0.25 per share in the third quarter despite TimkenSteel spinoff

Additional 10 million share repurchase authorization approved by Board

Purchased approximately 0.6 million shares for $34 million in 2Q 2014

Announced the DeltaX initiative to accelerate product development and line expansion commercialization efforts, a multi-year $60 million investment

Acquired the assets of Schulz Group

Note: See page Appendix for reconciliation of adjusted EBIT margin and adjusted earnings per share (EPS) to its most directly comparable GAAP equivalents.

5

|

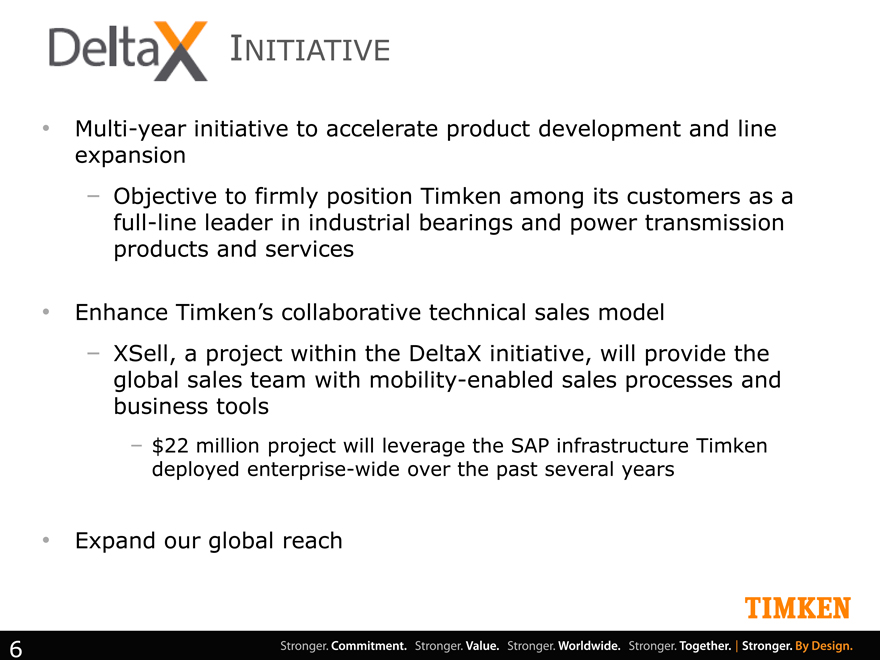

INITIATIVE

Multi-year initiative to accelerate product development and line expansion

Objective to firmly position Timken among its customers as a full-line leader in industrial bearings and power transmission products and services

Enhance Timken’s collaborative technical sales model

XSell, a project within the DeltaX initiative, will provide the global sales team with mobility-enabled sales processes and business tools

$22 million project will leverage the SAP infrastructure Timken deployed enterprise-wide over the past several years

Expand our global reach

6

|

SCHULZ GROUP ACQUISITION

Industrial Services: provides electric motor & generator repairs and motor rewinds for a broad range of commercial and industrial applications

U.S. Markets Sectors Served: nuclear, hydro and fossil, fuel power generator, water management, paper mills & general manufacturing

2013 sales of approx. $18 million

Based in New Haven, CT, with ~125 employees

Strategic Fit: advances industrial services capabilities, expanding geographic reach and servicing within the nuclear and hydro market sectors

The acquisitions of Philadelphia Gear, Wazee, Smith Services, Standard Machine, and now Schulz Group allow Timken to provide industrial services across US and Canada with a growing international presence

7

|

FINANCIAL REVIEW

|

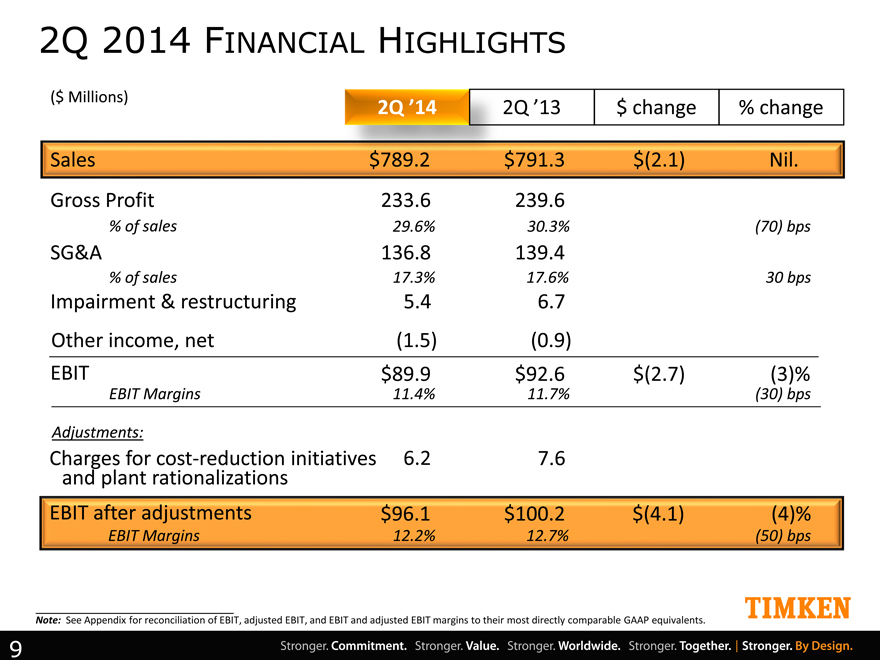

2Q 2014 FINANCIAL HIGHLIGHTS

($ Millions) 2Q ’14 2Q ’13 $ change % change

Sales $789.2 $791.3 $(2.1) Nil.

Gross Profit 233.6 239.6

% of sales 29.6% 30.3% (70) bps

SG&A 136.8 139.4

% of sales 17.3% 17.6% 30 bps

Impairment & restructuring 5.4 6.7

Other income, net (1.5) (0.9)

EBIT $89.9 $92.6 $(2.7) (3)%

EBIT Margins 11.4% 11.7% (30) bps

Adjustments:

Charges for cost-reduction initiatives 6.2 7.6

and plant rationalizations

EBIT after adjustments $ 96.1 $100.2 $(4.1) (4)%

EBIT Margins 12.2% 12.7% (50) bps

Note: See Appendix for reconciliation of EBIT, adjusted EBIT, and EBIT and adjusted EBIT margins to their most directly comparable GAAP equivalents.

9

|

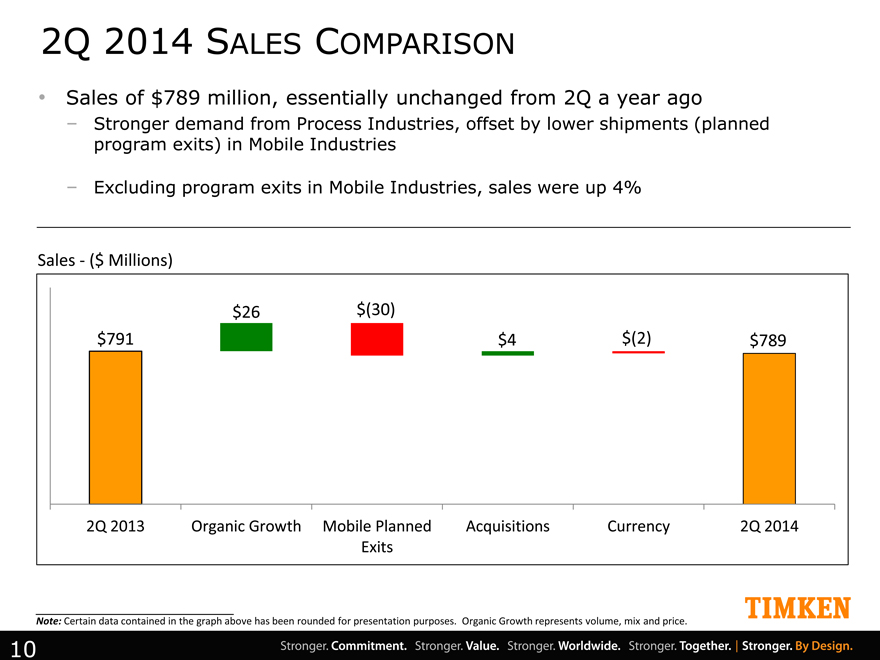

2Q 2014 SALES COMPARISON

Sales of $789 million, essentially unchanged from 2Q a year ago

Stronger demand from Process Industries, offset by lower shipments (planned program exits) in Mobile Industries

Excluding program exits in Mobile Industries, sales were up 4%

Sales - ($ Millions)

$26 $(30) $791 $4 $(2) $789

2Q 2013 Organic Growth Mobile Planned Acquisitions Currency 2Q 2014 Exits

Note: Certain data contained in the graph above has been rounded for presentation purposes. Organic Growth represents volume, mix and price.

10

|

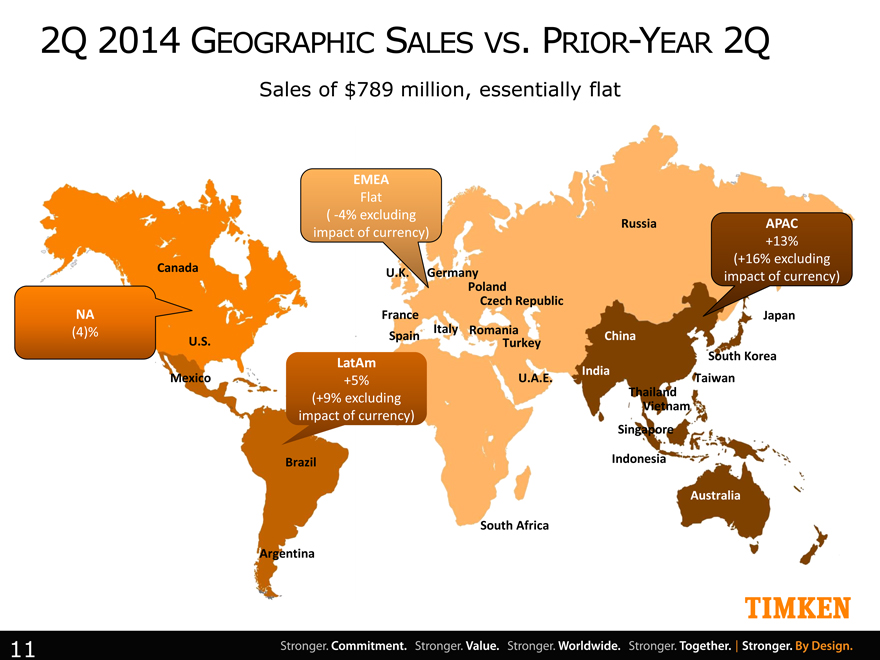

2Q 2014 GEOGRAPHIC SALES VS. PRIOR-YEAR 2Q

Sales of $789 million, essentially flat

EMEA

Flat

( -4% excluding impact of currency)

NA

(4)%

Canada

U.S.

Mexico

Spain

LatAm

+5%

(+9% excluding

impact of currency)

Brazil

Argentina

South Africa

U.K. Germany Poland

Czech Republic France Italy Romania Turkey

U.A.E. Russia

Japan China South Korea India Taiwan Thailand Vietnam

Singapore

Indonesia

Australia

APAC

+13% (+16% excluding impact of currency)

11

|

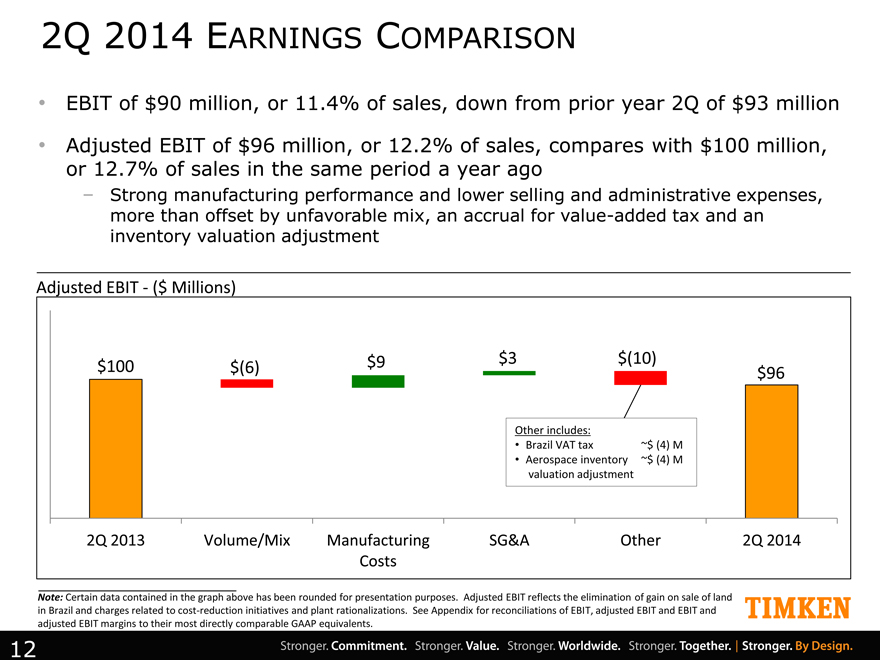

2Q 2014 EARNINGS COMPARISON

EBIT of $90 million, or 11.4% of sales, down from prior year 2Q of $93 million

Adjusted EBIT of $96 million, or 12.2% of sales, compares with $100 million, or 12.7% of sales in the same period a year ago

Strong manufacturing performance and lower selling and administrative expenses, more than offset by unfavorable mix, an accrual for value-added tax and an inventory valuation adjustment

Adjusted EBIT - ($ Millions)

$100 $(6) $9 $3 $(10) $96

Other includes:

Brazil VAT tax ~$ (4) M

Aerospace inventory ~$ (4) M

valuation adjustment

2Q 2013 Volume/Mix Manufacturing SG&A Other 2Q 2014

Costs

Note: Certain data contained in the graph above has been rounded for presentation purposes. Adjusted EBIT reflects the elimination of gain on sale of land in Brazil and charges related to cost-reduction initiatives and plant rationalizations. See Appendix for reconciliations of EBIT, adjusted EBIT and EBIT and adjusted EBIT margins to their most directly comparable GAAP equivalents.

12

|

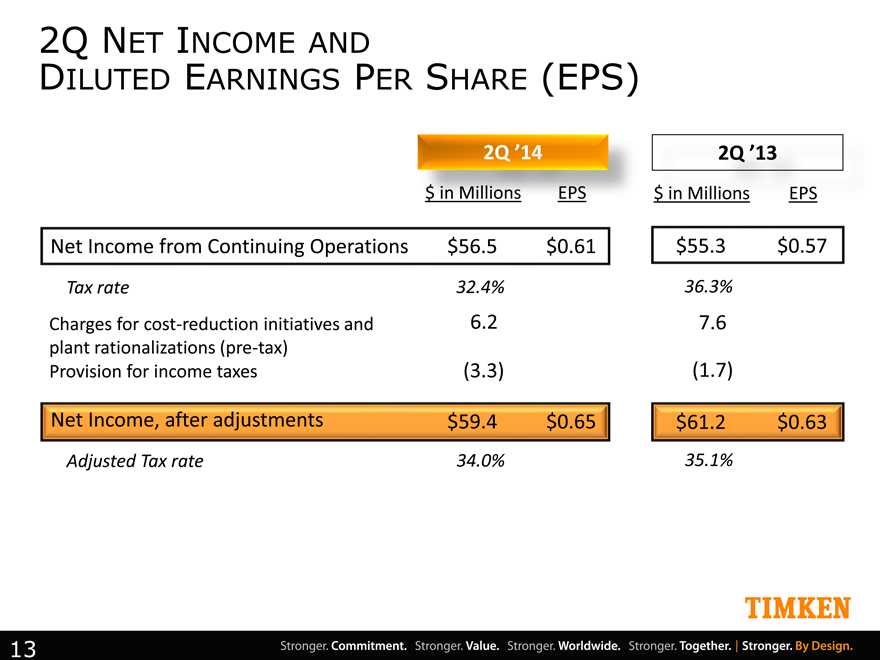

2Q NET INCOME AND

DILUTED EARNINGS PER SHARE (EPS)

2Q ’14 2Q ’13

$ in Millions EPS $ in Millions EPS

Net Income from Continuing Operations $56.5 $ 0.61

Tax rate 32.4% 36.3%

Charges for cost-reduction initiatives and 6.2 7.6

plant rationalizations (pre-tax)

Provision for income taxes (3.3) (1.7)

Net Income, after adjustments $59.4 $ 0.65 $61.2 $0.63

Adjusted Tax rate 34.0% 35.1%

13

|

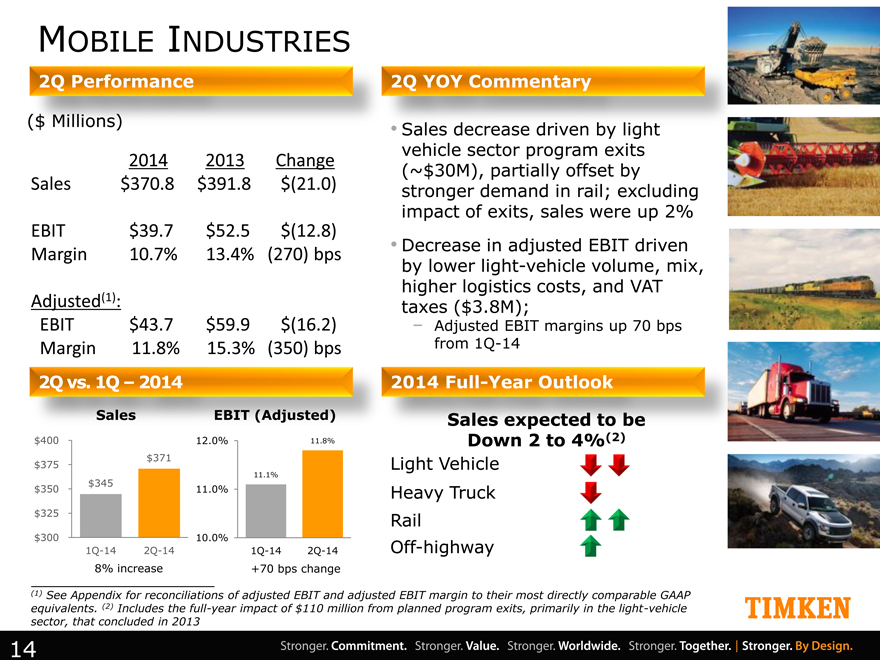

MOBILE INDUSTRIES

2014 2013 Change

Sales $370.8 $391.8 $(21.0)

EBIT $39.7 $52.5 $(12.8)

Margin 10.7% 13.4% (270) bps

Adjusted(1):

EBIT $43.7 $59.9 $(16.2)

Margin 11.8% 15.3% (350) bps

2Q vs. 1Q – 2014

Sales EBIT (Adjusted)

$400 12.0% 11.8%

$375 $ 371

11.1%

$ 345

$350 11.0%

$325

$300 10.0%

1Q-14 2Q-14 1Q-14 2Q-14

8% increase +70 bps change

2Q YOY Commentary

Sales decrease driven by light vehicle sector program exits

(~$30M), partially offset by stronger demand in rail; excluding impact of exits, sales were up 2%

Decrease in adjusted EBIT driven by lower light-vehicle volume, mix, higher logistics costs, and VAT taxes ($3.8M);

Adjusted EBIT margins up 70 bps from 1Q-14

2014 Full-Year Outlook

Down 2 to 4%

Light Vehicle Heavy Truck Rail Off-highway

(1) See Appendix for reconciliations of adjusted EBIT and adjusted EBIT margin to their most directly comparable GAAP equivalents. (2) Includes the full-year impact of $110 million from planned program exits, primarily in the light-vehicle sector, that concluded in 2013

2Q Performance ($ Millions) Sales expected to be Down 2 to 4%(2)

14

|

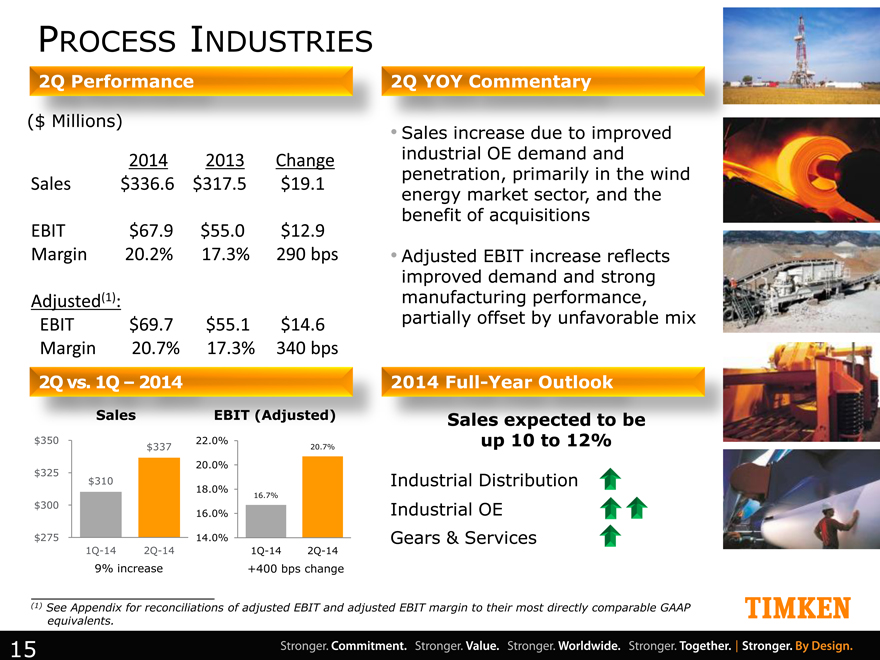

PROCESS INDUSTRIES

2Q Performance

2014 2013 Change

Sales $336.6 $317.5 $19.1

EBIT $67.9 $55.0 $12.9

Margin 20.2% 17.3% 290 bps

Adjusted(1):

EBIT $69.7 $55.1 $14.6

Margin 20.7% 17.3% 340 bps

2Q vs. 1Q – 2014

Sales EBIT (Adjusted)

$350 22.0%

$337 20.7%

20.0%

$325

$ 310

18.0% 16.7%

$300

16.0%

$275 14.0%

1Q-14 2Q-14 1Q-14 2Q-14

9% increase +400 bps change

2Q YOY Commentary

Sales increase due to improved industrial OE demand and penetration, primarily in the wind energy market sector, and the benefit of acquisitions Adjusted EBIT increase reflects improved demand and strong manufacturing performance, partially offset by unfavorable mix

2014 Full-Year Outlook

Sales expected to be up 10 to 12%

up 10 to 12%

Industrial Distribution Industrial OE

Gears & Services

See Appendix for reconciliations of adjusted EBIT and adjusted EBIT margin to their most directly comparable GAAP equivalents.

2Q Performance ($ Millions)

15

|

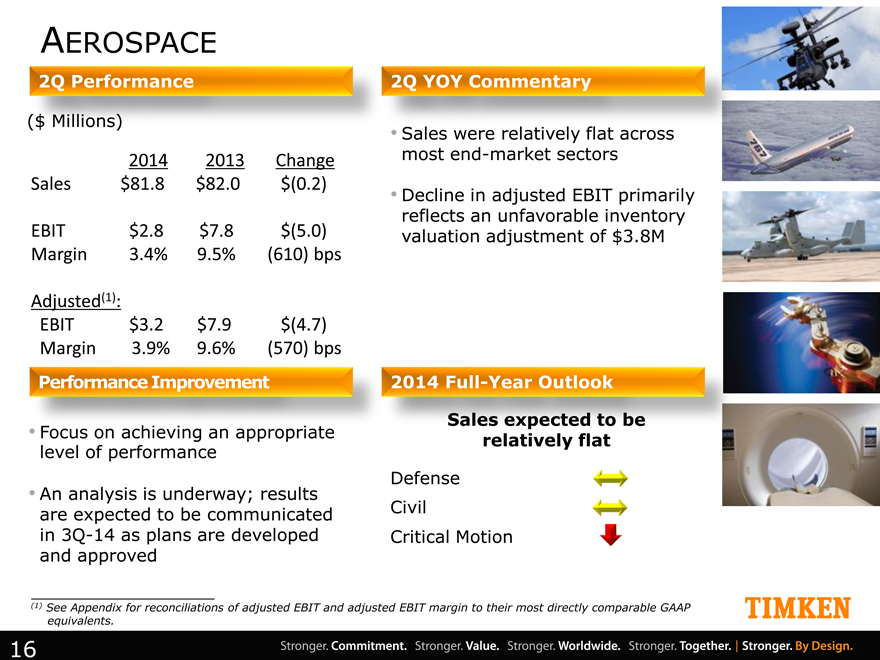

AEROSPACE

2Q Performance

2014 2013 Change

Sales $81.8 $82.0 $(0.2)

EBIT $2.8 $7.8 $(5.0)

Margin 3.4% 9.5% (610) bps

Adjusted(1):

EBIT $3.2 $7.9 $(4.7)

Margin 3.9% 9.6% (570) bps

Performance Improvement

Focus on achieving an appropriate

level of performance

An analysis is underway; results

are expected to be communicated

in 3Q-14 as plans are developed

and approved

2Q YOY Commentary

Sales were relatively flat across

most end-market sectors

Decline in adjusted EBIT primarily reflects an unfavorable inventory valuation adjustment of $3.8M

2014 Full-Year Outlook

relatively flat

Defense Civil Critical Motion

(1) See Appendix for reconciliations of adjusted EBIT and adjusted EBIT margin to their most directly comparable GAAP equivalents.

Sales expected to be relatively flat ($ Millions)

16

|

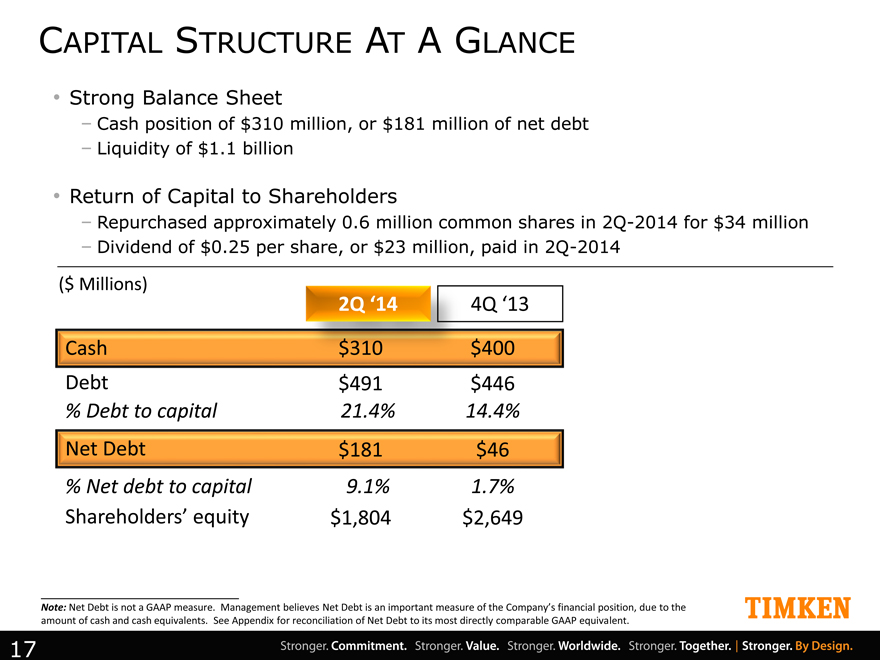

CAPITAL STRUCTURE AT A GLANCE

Strong Balance Sheet

Cash position of $310 million, or $181 million of net debt

Liquidity of $1.1 billion

Return of Capital to Shareholders

Repurchased approximately 0.6 million common shares in 2Q-2014 for $34 million

Dividend of $0.25 per share, or $23 million, paid in 2Q-2014

($ Millions)

2Q ‘14 4Q ‘13

Cash $310 $400

Debt $491 $446

% Debt to capital 21.4% 14.4%

Net Debt $181 $46

% Net debt to capital 9.1% 1.7%

Shareholders’ equity $1,804 $2,649

Note: Net Debt is not a GAAP measure. Management believes Net Debt is an important measure of the Company’s financial position, due to the amount of cash and cash equivalents. See Appendix for reconciliation of Net Debt to its most directly comparable GAAP equivalent.

17

|

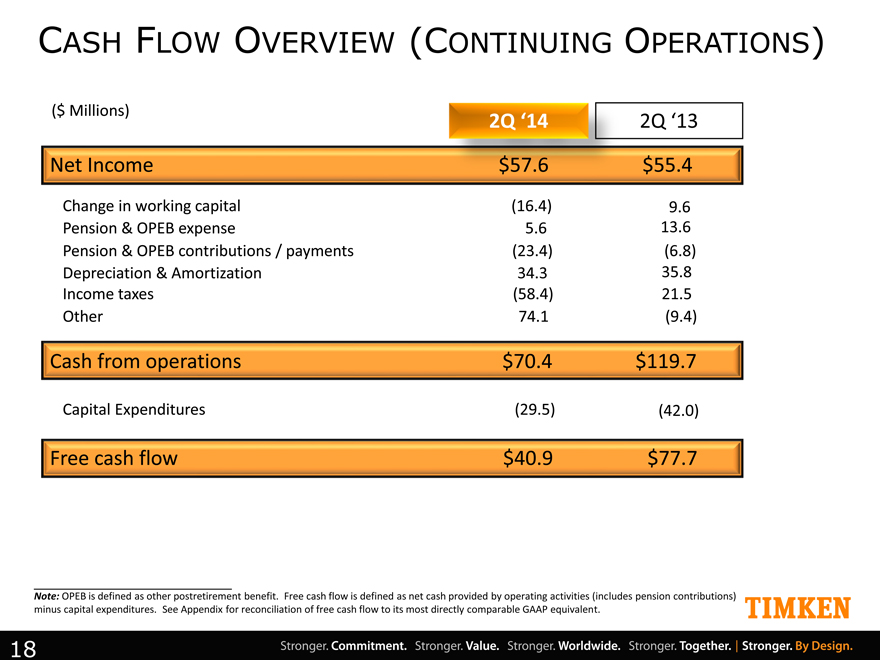

CASH FLOW OVERVIEW (CONTINUING OPERATIONS)

($ Millions) 2Q ‘14 2Q ‘13

Net Income $57.6 $55.4

Change in working capital (16.4) 9.6

Pension & OPEB expense 5.6 13.6

Pension & OPEB contributions / payments (23.4) (6.8)

Depreciation & Amortization 34.3 35.8

Income taxes (58.4) 21.5

Other 74.1 (9.4)

Cash from operations $70.4 $119.7

Capital Expenditures (29.5) (42.0)

Free cash flow $40.9 $77.7

Note: OPEB is defined as other postretirement benefit. Free cash flow is defined as net cash provided by operating activities (includes pension contributions) minus capital expenditures. See Appendix for reconciliation of free cash flow to its most directly comparable GAAP equivalent.

18

|

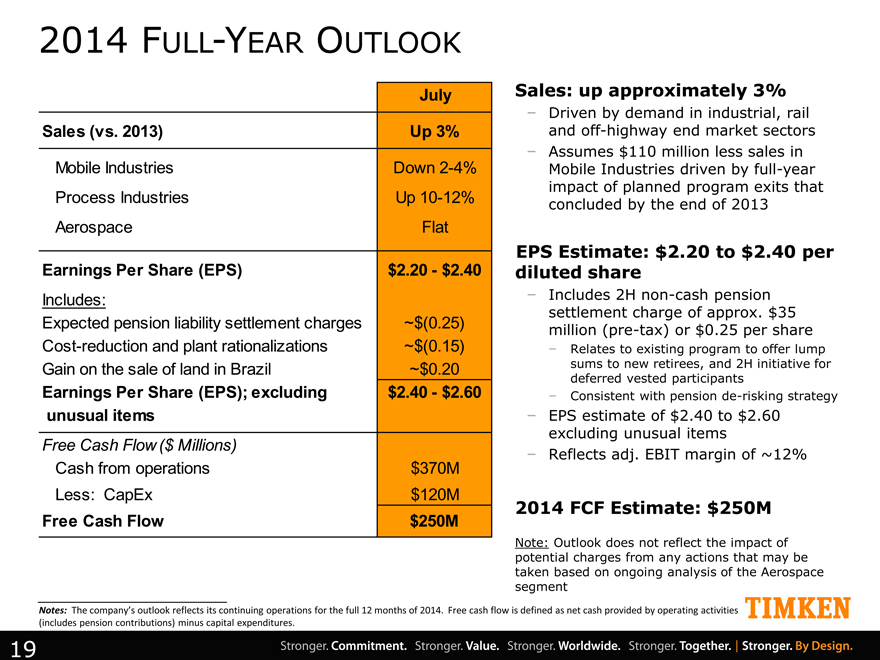

2014 FULL-YEAR OUTLOOK

July

Sales (vs. 2013) Up 3%

Mobile Industries Down 2-4%

Process Industries Up 10-12%

Aerospace Flat

Earnings Per Share (EPS) $2.20—$2.40

Includes:

Expected pension liability settlement charges ~$(0.25)

Cost-reduction and plant rationalizations ~$(0.15)

Gain on the sale of land in Brazil ~$0.20

Earnings Per Share (EPS); excluding $2.40—$2.60

unusual items

Free Cash Flow ($ Millions)

Cash from operations $370M

Less: CapEx $120M

Free Cash Flow $250M

Sales: up approximately 3%

Driven by demand in industrial, rail and off-highway end market sectors

Assumes $110 million less sales in Mobile Industries driven by full-year impact of planned program exits that concluded by the end of 2013

EPS Estimate: $2.20 to $2.40 per diluted share

Includes 2H non-cash pension settlement charge of approx. $35 million (pre-tax) or $0.25 per share

Relates to existing program to offer lump sums to new retirees, and 2H initiative for deferred vested participants

Consistent with pension de-risking strategy

EPS estimate of $2.40 to $2.60 excluding unusual items

Reflects adj. EBIT margin of ~12%

2014 FCF Estimate: $250M

Note: Outlook does not reflect the impact of potential charges from any actions that may be taken based on ongoing analysis of the Aerospace segment

Notes: The company’s outlook reflects its continuing operations for the full 12 months of 2014. Free cash flow is defined as net cash provided by operating activities (includes pension contributions) minus capital expenditures.

19

|

2Q 2014 EARNINGS

JULY 31, 2014

|

Appendix

|

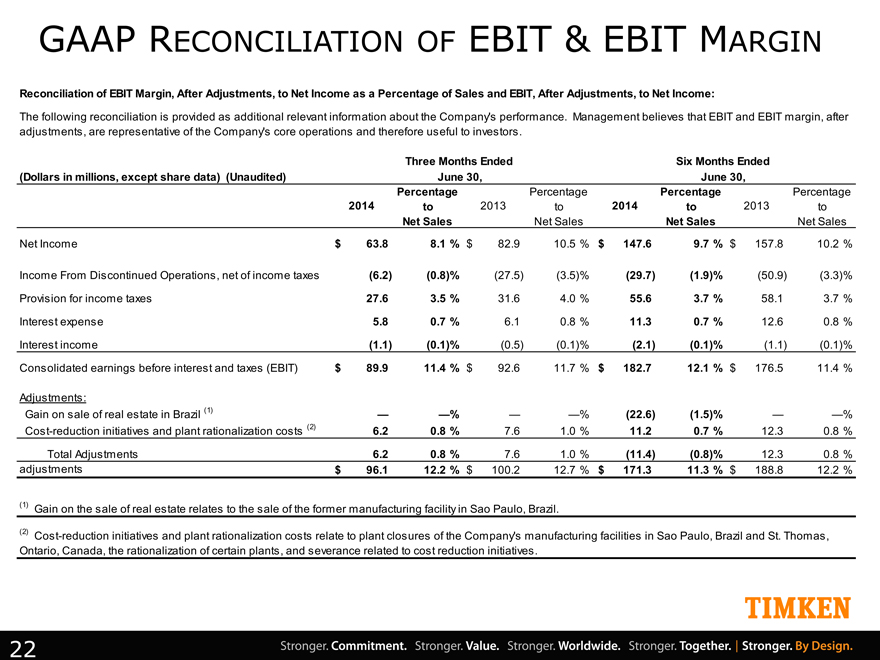

GAAP RECONCILIATION OF EBIT & EBIT MARGIN

Reconciliation of EBIT Margin, After Adjustments, to Net Income as a Percentage of Sales and EBIT, After Adjustments, to Net Income:

The following reconciliation is provided as additional relevant information about the Company’s performance. Management believes that EBIT and EBIT margin, after adjustments, are representative of the Company’s core operations and therefore useful to investors.

Three Months Ended Six Months Ended

(Dollars in millions, except share data) (Unaudited) June 30, June 30,

Percentage Percentage Percentage Percentage

2014 to 2013 to 2014 to 2013 to

Net Sales Net Sales Net Sales Net Sales

Net Income $ 63.8 8.1% $ 82.9 10.5% $ 147.6 9.7% $ 157.8 10.2%

Income From Discontinued Operations, net of income taxes(6.2)(0.8)%(27.5)(3.5)%(29.7)(1.9)%(50.9)(3.3)%

Provision for income taxes 27.6 3.5% 31.6 4.0% 55.6 3.7% 58.1 3.7%

Interest expense 5.8 0.7% 6.1 0.8% 11.3 0.7% 12.6 0.8%

Interest income(1.1)(0.1)%(0.5)(0.1)%(2.1)(0.1)%(1.1)(0.1)%

Consolidated earnings before interest and taxes (EBIT) $ 89.9 11.4% $ 92.6 11.7% $ 182.7 12.1% $ 176.5 11.4%

Adjustments:

Gain on sale of real estate in Brazil (1) — —% — —%(22.6)(1.5)% — —%

Cost-reduction initiatives and plant rationalization costs (2) 6.2 0.8% 7.6 1.0% 11.2 0.7% 12.3 0.8%

Total Adjustments 6.2 0.8% 7.6 1.0%(11.4)(0.8)% 12.3 0.8%

adjustments $ 96.1 12.2% $ 100.2 12.7% $ 171.3 11.3% $ 188.8 12.2%

(1) Gain on the sale of real estate relates to the sale of the former manufacturing facility in Sao Paulo, Brazil.

(2) Cost-reduction initiatives and plant rationalization costs relate to plant closures of the Company’s manufacturing facilities in Sao Paulo, Brazil and St. Thomas,

Ontario, Canada, the rationalization of certain plants, and severance related to cost reduction initiatives .

22

|

GAAP RECONCILIATION OF EBIT & EBIT MARGIN

Reconciliation of EBIT Margin, After Adjustments, to Net Income as a Percentage of Sales and EBIT, After Adjustments, to Net Income:

The following reconciliation is provided as additional relevant information about the Company’s performance. Management believes that EBIT and EBIT margin, after adjustments, are representative of the Company’s core operations and therefore useful to investors.

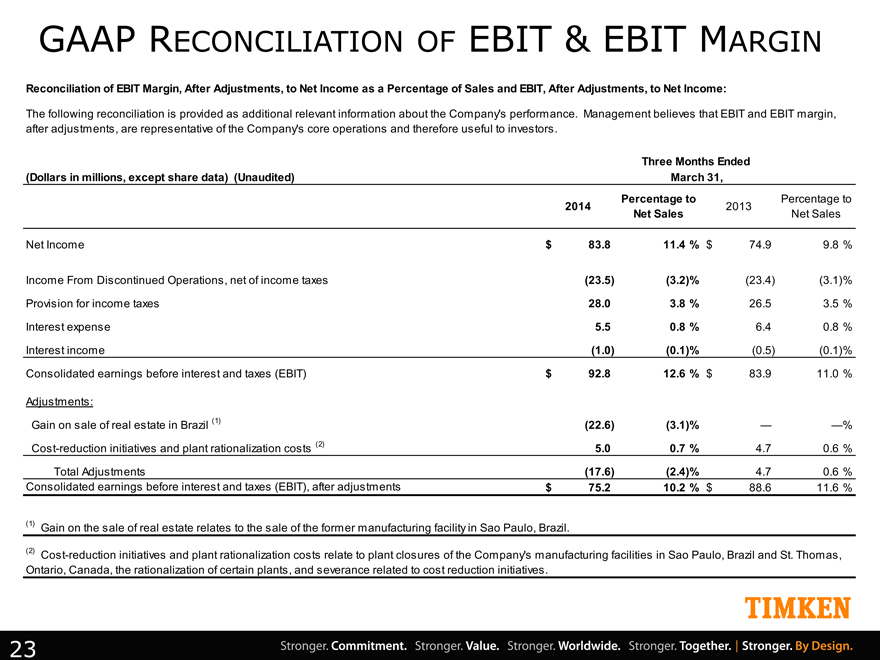

Three Months Ended

(Dollars in millions, except share data) (Unaudited) March 31,

Percentage to Percentage to

2014 2013

Net Sales Net Sales

Net Income $ 83.8 11.4% $ 74.9 9.8%

Income From Discontinued Operations, net of income taxes(23.5)(3.2)%(23.4)(3.1)%

Provision for income taxes 28.0 3.8% 26.5 3.5%

Interest expense 5.5 0.8% 6.4 0.8%

Interest income(1.0)(0.1)%(0.5)(0.1)%

Consolidated earnings before interest and taxes (EBIT) $ 92.8 12.6% $ 83.9 11.0%

Adjustments:

Gain on sale of real estate in Brazil (1)(22.6)(3.1)% — —%

Cost-reduction initiatives and plant rationalization costs (2) 5.0 0.7% 4.7 0.6%

Total Adjustments(17.6)(2.4)% 4.7 0.6%

Consolidated earnings before interest and taxes (EBIT), after adjustments $ 75.2 10.2% $ 88.6 11.6%

(1) Gain on the sale of real estate relates to the sale of the former manufacturing facility in Sao Paulo, Brazil.

(2) Cost-reduction initiatives and plant rationalization costs relate to plant closures of the Company’s manufacturing facilities in Sao Paulo, Brazil and St. Thomas,

Ontario, Canada, the rationalization of certain plants, and severance related to cost reduction initiatives .

23

|

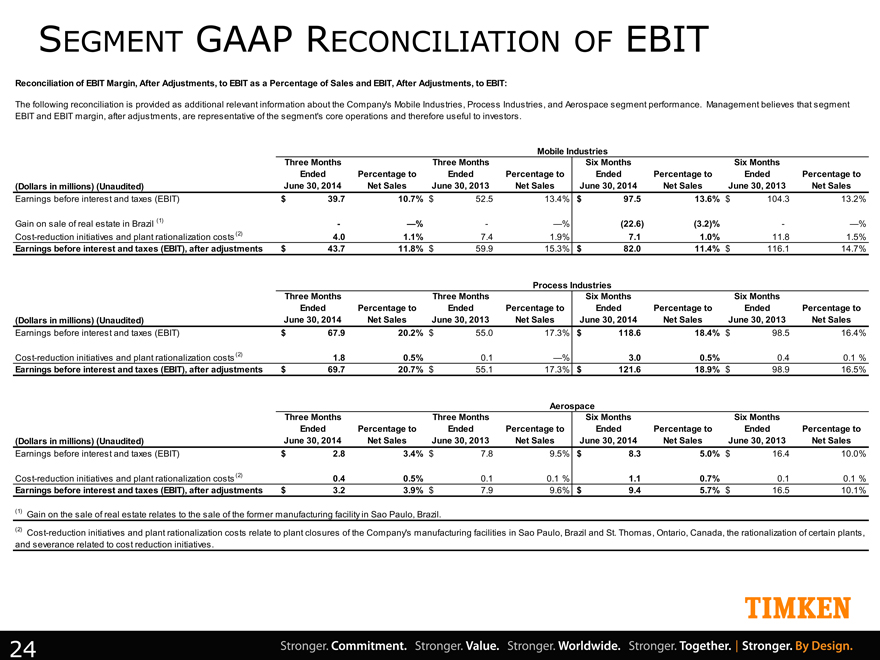

SEGMENT GAAP RECONCILIATION OF EBIT

Reconciliation of EBIT Margin, After Adjustments, to EBIT as a Percentage of Sales and EBIT, After Adjustments, to EBIT:

The following reconciliation is provided as additional relevant information about the Company’s Mobile Industries, Process Industries, and Aerospace segment performance. Management believes that segment

EBIT and EBIT margin, after adjustments, are representative of the segment’s core operations and therefore useful to investors.

Mobile Industries

Three Months Three Months Six Months Six Months

Ended Percentage to Ended Percentage to Ended Percentage to Ended Percentage to

(Dollars in millions) (Unaudited) June 30, 2014 Net Sales June 30, 2013 Net Sales June 30, 2014 Net Sales June 30, 2013 Net Sales

Earnings before interest and taxes (EBIT) $ 39.7 10.7% $ 52.5 13.4% $ 97.5 13.6% $ 104.3 13.2%

Gain on sale of real estate in Brazil (1)——%——%(22.6)(3.2)%——%

Cost-reduction initiatives and plant rationalization costs (2) 4.0 1.1% 7.4 1.9% 7.1 1.0% 11.8 1.5%

Earnings before interest and taxes (EBIT), after adjustments $ 43.7 11.8% $ 59.9 15.3% $ 82.0 11.4% $ 116.1 14.7%

Process Industries

Three Months Three Months Six Months Six Months

Ended Percentage to Ended Percentage to Ended Percentage to Ended Percentage to

(Dollars in millions) (Unaudited) June 30, 2014 Net Sales June 30, 2013 Net Sales June 30, 2014 Net Sales June 30, 2013 Net Sales

Earnings before interest and taxes (EBIT) $ 67.9 20.2% $ 55.0 17.3% $ 118.6 18.4% $ 98.5 16.4%

Cost-reduction initiatives and plant rationalization costs (2) 1.8 0.5% 0.1 —% 3.0 0.5% 0.4 0.1 %

Earnings before interest and taxes (EBIT), after adjustments $ 69.7 20.7% $ 55.1 17.3% $ 121.6 18.9% $ 98.9 16.5%

Aerospace

Three Months Three Months Six Months Six Months

Ended Percentage to Ended Percentage to Ended Percentage to Ended Percentage to

(Dollars in millions) (Unaudited) June 30, 2014 Net Sales June 30, 2013 Net Sales June 30, 2014 Net Sales June 30, 2013 Net Sales

Earnings before interest and taxes (EBIT) $ 2.8 3.4% $ 7.8 9.5% $ 8.3 5.0% $ 16.4 10.0%

Cost-reduction initiatives and plant rationalization costs (2) 0.4 0.5% 0.1 0.1 % 1.1 0.7% 0.1 0.1 %

Earnings before interest and taxes (EBIT), after adjustments $ 3.2 3.9% $ 7.9 9.6% $ 9.4 5.7% $ 16.5 10.1%

(1) Gain on the sale of real estate relates to the sale of the former manufacturing facility in Sao Paulo, Brazil.

(2) Cost-reduction initiatives and plant rationalization costs relate to plant closures of the Company’s manufacturing facilities in Sao Paulo, Brazil and St. Thomas, Ontario, Canada, the rationalization of certain plants,

and severance related to cost reduction initiatives.

24

|

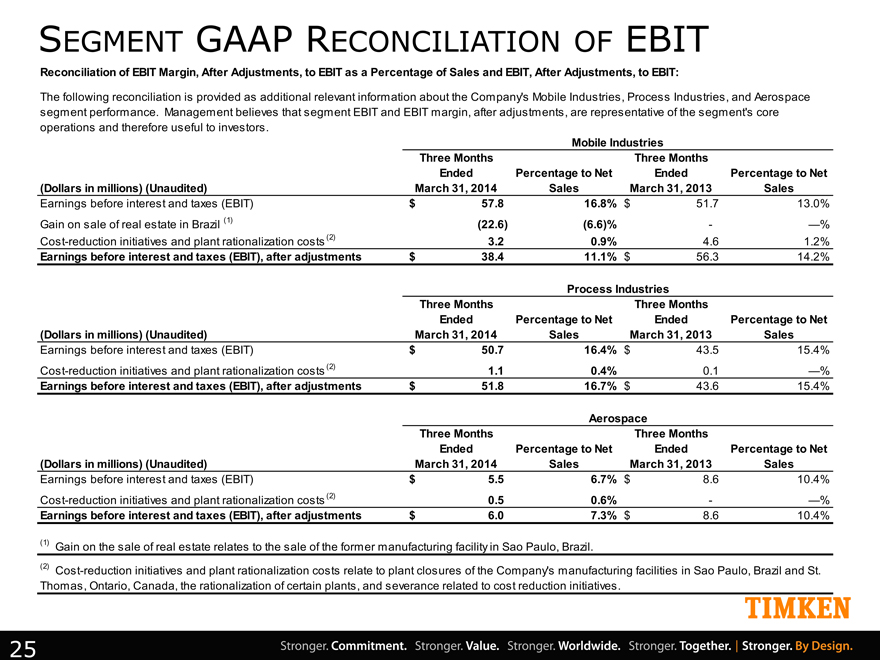

SEGMENT GAAP RECONCILIATION OF EBIT

Reconciliation of EBIT Margin, After Adjustments, to EBIT as a Percentage of Sales and EBIT, After Adjustments, to EBIT:

The following reconciliation is provided as additional relevant information about the Company’s Mobile Industries, Process Industries, and Aerospace

segment performance. Management believes that segment EBIT and EBIT margin, after adjustments, are representative of the segment’s core

operations and therefore useful to investors .

Mobile Industries

Three Months Three Months

Ended Percentage to Net Ended Percentage to Net

(Dollars in millions) (Unaudited) March 31, 2014 Sales March 31, 2013 Sales

Earnings before interest and taxes (EBIT) $ 57.8 16.8% $ 51.7 13.0%

Gain on sale of real estate in Brazil (1)(22.6)(6.6)%——%

Cost-reduction initiatives and plant rationalization costs (2) 3.2 0.9% 4.6 1.2%

Earnings before interest and taxes (EBIT), after adjustments $ 38.4 11.1% $ 56.3 14.2%

Process Industries

Three Months Three Months

Ended Percentage to Net Ended Percentage to Net

(Dollars in millions) (Unaudited) March 31, 2014 Sales March 31, 2013 Sales

Earnings before interest and taxes (EBIT) $ 50.7 16.4% $ 43.5 15.4%

Cost-reduction initiatives and plant rationalization costs (2) 1.1 0.4% 0.1 —%

Earnings before interest and taxes (EBIT), after adjustments $ 51.8 16.7% $ 43.6 15.4%

Aerospace

Three Months Three Months

Ended Percentage to Net Ended Percentage to Net

(Dollars in millions) (Unaudited) March 31, 2014 Sales March 31, 2013 Sales

Earnings before interest and taxes (EBIT) $ 5.5 6.7% $ 8.6 10.4%

Cost-reduction initiatives and plant rationalization costs (2) 0.5 0.6%——%

Earnings before interest and taxes (EBIT), after adjustments $ 6.0 7.3% $ 8.6 10.4%

(1) Gain on the sale of real estate relates to the sale of the former manufacturing facility in Sao Paulo, Brazil.

(2) Cost-reduction initiatives and plant rationalization costs relate to plant closures of the Company’s manufacturing facilities in Sao Paulo, Brazil and St.

Thomas, Ontario, Canada, the rationalization of certain plants, and severance related to cost reduction initiatives .

25

|

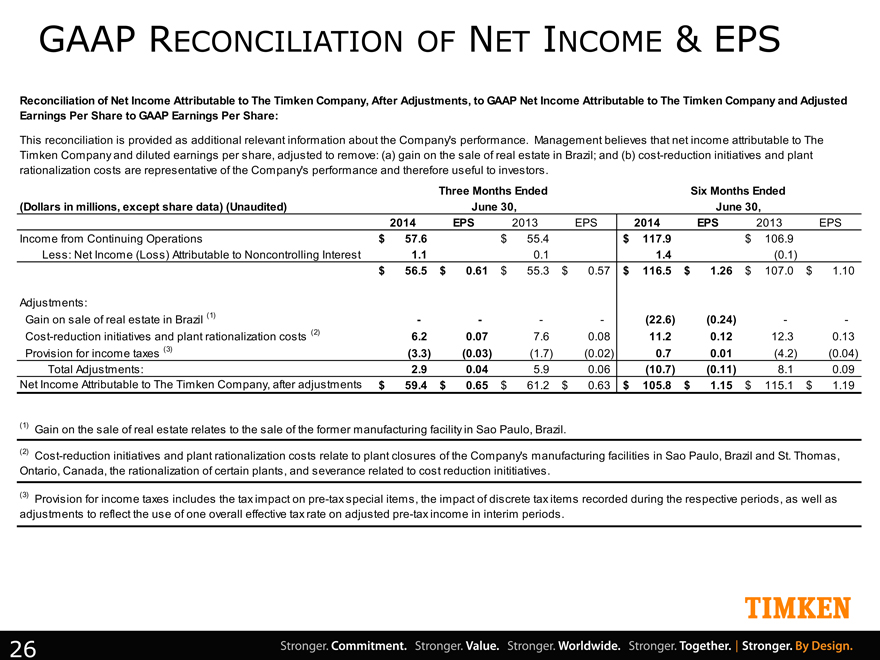

GAAP RECONCILIATION OF NET INCOME & EPS

Reconciliation of Net Income Attributable to The Timken Company, After Adjustments, to GAAP Net Income Attributable to The Timken Company and Adjusted

Earnings Per Share to GAAP Earnings Per Share:

This reconciliation is provided as additional relevant information about the Company’s performance. Management believes that net income attributable to The

Timken Company and diluted earnings per share, adjusted to remove: (a) gain on the sale of real estate in Brazil; and (b) cost-reduction initiatives and plant

rationalization costs are representative of the Company’s performance and therefore useful to investors .

Three Months Ended Six Months Ended

(Dollars in millions, except share data) (Unaudited) June 30, June 30,

2014 EPS 2013 EPS 2014 EPS 2013 EPS

Income from Continuing Operations $ 57.6 $ 55.4 $ 117.9 $ 106.9

Less: Net Income (Loss) Attributable to Noncontrolling Interest 1.1 0.1 1.4(0.1)

$ 56.5 $ 0.61 $ 55.3 $ 0.57 $ 116.5 $ 1.26 $ 107.0 $ 1.10

Adjustments:

Gain on sale of real estate in Brazil (1) — —(22.6)(0.24) —

Cost-reduction initiatives and plant rationalization costs (2) 6.2 0.07 7.6 0.08 11.2 0.12 12.3 0.13

Provision for income taxes (3)(3.3)(0.03)(1.7)(0.02) 0.7 0.01(4.2)(0.04)

Total Adjustments: 2.9 0.04 5.9 0.06(10.7)(0.11) 8.1 0.09

Net Income Attributable to The Timken Company, after adjustments $ 59.4 $ 0.65 $ 61.2 $ 0.63 $ 105.8 $ 1.15 $ 115.1 $ 1.19

(1) Gain on the sale of real estate relates to the sale of the former manufacturing facility in Sao Paulo, Brazil.

(2) Cost-reduction initiatives and plant rationalization costs relate to plant closures of the Company’s manufacturing facilities in Sao Paulo, Brazil and St. Thomas,

Ontario, Canada, the rationalization of certain plants, and severance related to cost reduction inititiatives .

(3) Provision for income taxes includes the tax impact on pre-tax special items, the impact of discrete tax items recorded during the respective periods, as well as

adjustments to reflect the use of one overall effective tax rate on adjusted pre-tax income in interim periods .

26

|

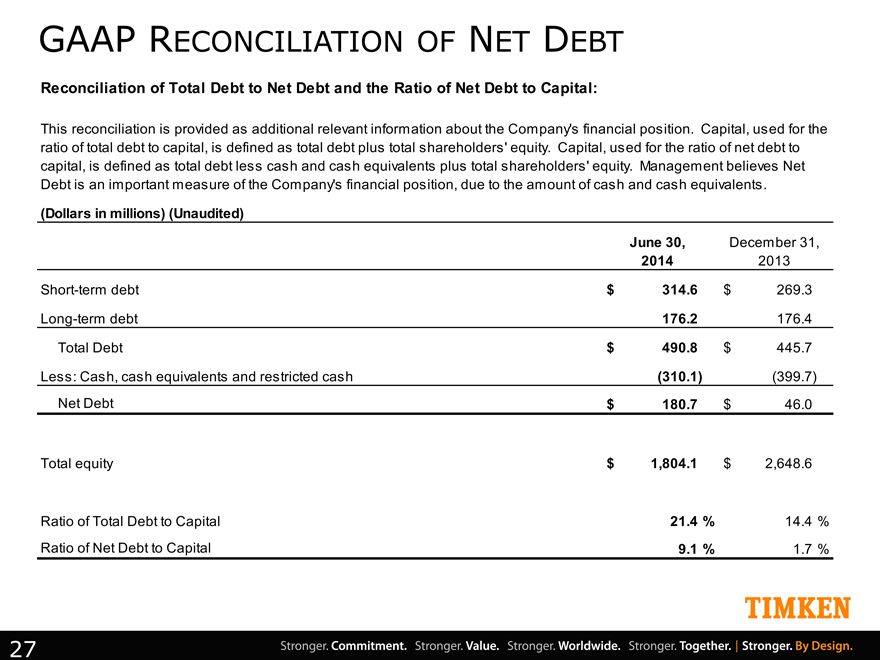

GAAP RECONCILIATION OF NET DEBT

Reconciliation of Total Debt to Net Debt and the Ratio of Net Debt to Capital:

This reconciliation is provided as additional relevant information about the Company’s financial position. Capital, used for the

ratio of total debt to capital, is defined as total debt plus total shareholders’ equity. Capital, used for the ratio of net debt to

capital, is defined as total debt less cash and cash equivalents plus total shareholders’ equity. Management believes Net

Debt is an important measure of the Company’s financial position, due to the amount of cash and cash equivalents .

(Dollars in millions) (Unaudited)

June 30, December 31,

2014 2013

Short-term debt $ 314.6 $ 269.3

Long-term debt 176.2 176.4

Total Debt $ 490.8 $ 445.7

Less: Cash, cash equivalents and restricted cash(310.1)(399.7)

Net Debt $ 180.7 $ 46.0

Total equity $ 1,804.1 $ 2,648.6

Ratio of Total Debt to Capital 21.4% 14.4%

Ratio of Net Debt to Capital 9.1% 1.7%

27

|

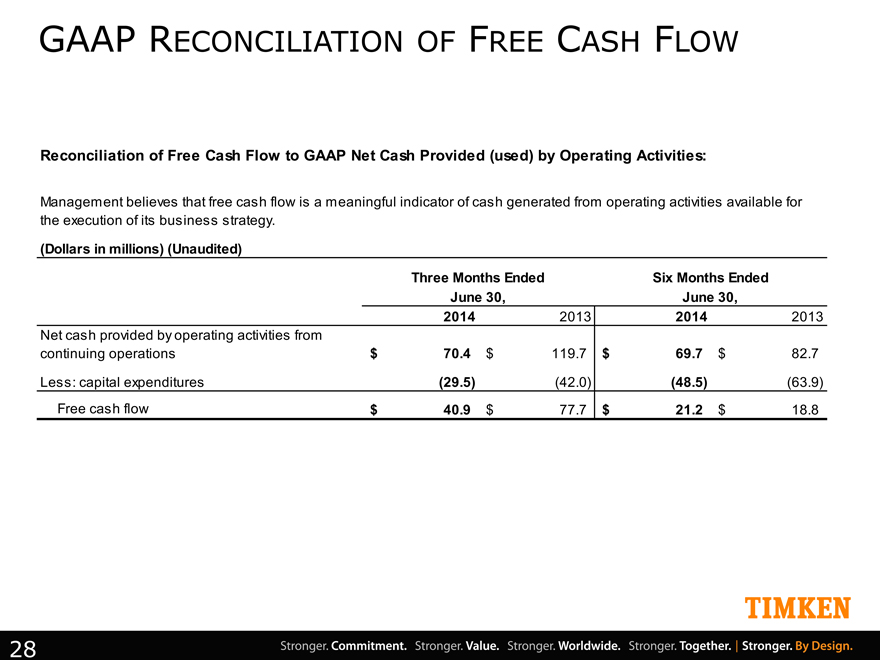

GAAP RECONCILIATION OF FREE CASH FLOW

Reconciliation of Free Cash Flow to GAAP Net Cash Provided (used) by Operating Activities:

Management believes that free cash flow is a meaningful indicator of cash generated from operating activities available for

the execution of its business strategy.

(Dollars in millions) (Unaudited)

Three Months Ended Six Months Ended

June 30, June 30,

2014 2013 2014 2013

Net cash provided by operating activities from

continuing operations $ 70.4 $ 119.7 $ 69.7 $ 82.7

Less: capital expenditures(29.5)(42.0)(48.5)(63.9)

Free cash flow $ 40.9 $ 77.7 $ 21.2 $ 18.8

28

|

TIMKEN