QuickLinks -- Click here to rapidly navigate through this document

U.S. Securities and Exchange Commission

Washington, D.C. 20549

Form 40-F/A

Amendment No. 1

o | REGISTRATION STATEMENT PURSUANT TO SECTION 12 OF THE SECURITIES EXCHANGE ACT OF 1934 | |

OR | ||

ý | ANNUAL REPORT PURSUANT TO SECTION 13(a) OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year endedDecember 31, 2012 Commission File Number1-8887

| TRANSCANADA PIPELINES LIMITED (Exact Name of Registrant as specified in its charter) |

Canada (Jurisdiction of incorporation or organization) |

4922, 4923, 4924, 5172 (Primary Standard Industrial Classification Code Number (if applicable)) |

Not Applicable (I.R.S. Employer Identification Number (if applicable)) |

TransCanada Tower, 450 - 1 Street S.W. Calgary, Alberta, Canada, T2P 5H1 (403) 920-2000 (Address and telephone number of Registrant's principal executive offices) |

TransCanada PipeLine USA Ltd., 717 Texas Street Houston, Texas, 77002-2761; (832) 320-5201 (Name, address (including zip code) and telephone number (including area code) of agent for service in the United States) |

Securities registered pursuant to section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: Debt Securities

For annual reports, indicate by check mark the information filed with this Form:

| ý Annual Information Form | o Audited annual financial statements |

Indicate the number of outstanding shares of each of the issuer's classes of capital or common stock as of the close of the period covered by the annual report.

At December 31, 2012, 4,000,000 Cumulative Redeemable First Preferred Shares Series U

and 4,000,000 Cumulative Redeemable First Preferred Shares Series Y

were issued and outstanding.

738,507,894 common shares which are all owned by TransCanada Corporation

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes o No o

The documents (or portions thereof) forming part of this Form 40-F are incorporated by reference into the following registration statements under theSecurities Act of 1933, as amended:

Form | Registration No. | |||

|---|---|---|---|---|

F-9 | 333-177789 | |||

TransCanada PipeLines Limited ("TCPL") is filing this Form 40-F/A Amendment No. 1 to its Annual Report on Form 40-F for the year ended December 31, 2012 which was filed with the Securities and Exchange Commission on February 15, 2013, to include TCPL's Annual Information Form for the year ended December 31, 2012.

Other than as expressly set forth above, this Form 40-F/A does not, and does not purport to, amend, update, or restate the information in any Item of the Form 40-F or reflect any events that have occurred after the Form 40-F was filed.

The Registrant undertakes to make available, in person or by telephone, representatives to respond to inquiries made by the Commission staff, and to furnish promptly, when requested to do so by the Commission staff, information relating to: the securities registered pursuant to Form 40-F; the securities in relation to which the obligation to file an Annual Report on Form 40-F arises; or transactions in said securities.

We disclose forward-looking information to help current and potential investors understand management's assessment of our future plans and financial outlook, and our future prospects overall.

Statements that areforward-looking are based on certain assumptions and on what we know and expect today and generally include words likeanticipate,expect,believe,may,will, should,estimate or other similar words.

Forward-looking statements in this document may include information about the following, among other things:

- •

- anticipated business prospects

- •

- our financial and operational performance, including the performance of our subsidiaries

- •

- expectations or projections about strategies and goals for growth and expansion

- •

- expected cash flows

- •

- expected costs for planned projects, including projects under construction and in development

- •

- expected schedules for planned projects (including anticipated construction and completion dates)

- •

- expected regulatory processes and outcomes

- •

- expected outcomes with respect to legal proceedings, including arbitration

- •

- expected capital expenditures and contractual obligations

- •

- expected operating and financial results

- •

- the expected impact of future commitments and contingent liabilities

- •

- expected industry, market and economic conditions.

Forward-looking statements do not guarantee future performance. Actual events and results could be significantly different because of assumptions, risks or uncertainties related to our business or events that happen after the date of this document.

2

Our forward-looking information is based on the following key assumptions, and subject to the following risks and uncertainties including the following:

Assumptions

- •

- inflation rates, commodity prices and capacity prices

- •

- timing of debt issuances and hedging

- •

- regulatory decisions and outcomes

- •

- foreign exchange rates

- •

- interest rates

- •

- tax rates

- •

- planned and unplanned outages and the use of our pipeline and energy assets

- •

- integrity and reliability of our assets

- •

- access to capital markets

- •

- anticipated construction costs, schedules and completion dates

- •

- acquisitions and divestitures.

Risks and uncertainties

- •

- our ability to successfully implement our strategic initiatives

- •

- whether our strategic initiatives will yield the expected benefits

- •

- the operating performance of our pipeline and energy assets

- •

- amount of capacity sold and rates achieved in our U.S. pipelines business

- •

- the availability and price of energy commodities

- •

- the amount of capacity payments and revenues we receive from our energy business

- •

- regulatory decisions and outcomes

- •

- outcomes of legal proceedings, including arbitration

- •

- performance of our counterparties

- •

- changes in the political environment

- •

- changes in environmental and other laws and regulations

- •

- competitive factors in the pipeline and energy sectors

- •

- construction and completion of capital projects

- •

- labour, equipment and material costs

- •

- access to capital markets

- •

- cybersecurity

- •

- interest and foreign exchange rates

- •

- weather

- •

- technological developments

- •

- economic conditions in North America as well as globally.

You can read more about these factors and others in reports we have filed with Canadian securities regulators and the U.S. Securities and Exchange Commission (SEC).

You should not put undue reliance on forward-looking information and should not use future-oriented information or financial outlooks for anything other than their intended purpose. We do not update our forward-looking statements due to new information or future events, unless we are required to by law.

3

Pursuant to the requirements of theExchange Act, the Registrant certifies that it meets all of the requirements for filing on Form 40-F/A and has duly caused this amendment to the Annual Report to be signed on its behalf by the undersigned, thereto duly authorized, in the City of Calgary, Province of Alberta, Canada.

| TRANSCANADA PIPELINES LIMITED | ||||

Per: | /s/ DONALD R. MARCHAND DONALD R. MARCHAND Executive Vice-President and Chief Financial Officer | |||

Date: February 27, 2013 | ||||

DOCUMENTS FILED AS PART OF THIS REPORT

13.1* | Management's Discussion and Analysis (included on pages 1 through 94 of the TCPL 2012 Management's Discussion and Analysis and Audited Consolidated Financial Statements). | ||

13.2* | 2012 Audited Consolidated Financial Statements (included on pages 95 through 151 of the TCPL 2012 Management's Discussion and Analysis and Audited Consolidated Financial Statements), including the auditors' report thereon and the Report of Independent Registered Public Accounting Firm on the effectiveness of TransCanada's Internal Control Over Financial Reporting as of December 31, 2012. | ||

13.3 | TCPL's Annual Information Form for the year ended December 31, 2012. | ||

* previously filed. | |||

EXHIBITS | |||

31.1 | Certification of Chief Executive Officer pursuant to Section 302 of theSarbanes-Oxley Act of 2002. | ||

31.2 | Certification of Chief Financial Officer pursuant to Section 302 of theSarbanes-Oxley Act of 2002. | ||

TransCanada PipeLines Limited

2012 Annual information form

February 11, 2013

Table of Contents

| Presentation of information | 2 | ||

| Forward-looking information | 2 | ||

| TransCanada PipeLines Limited | 4 | ||

| Corporate structure | 4 | ||

| Intercorporate relationships | 5 | ||

| General development of the business | 5 | ||

| Developments in the Natural Gas Pipelines business | 6 | ||

| Developments in the Oil Pipelines business | 9 | ||

| Developments in the Energy business | 11 | ||

| Business of TCPL | 13 | ||

| Natural Gas Pipelines business | 14 | ||

| Oil Pipelines business | 15 | ||

| Regulation of the Natural Gas and Oil Pipelines businesses | 16 | ||

| Energy business | 17 | ||

| General | 20 | ||

| Employees | 20 | ||

| Health, safety and environmental protection and social policies | 20 | ||

| Risk factors | 21 | ||

| Dividends | 21 | ||

| Description of capital structure | 22 | ||

| Share capital | 22 | ||

| Debt | 22 | ||

| Credit ratings | 23 | ||

| DBRS | 23 | ||

| Moody's | 23 | ||

| S&P | 24 | ||

| Market for securities | 24 | ||

| Common shares | 25 | ||

| Series 1 preferred shares | 25 | ||

| Series 3 preferred shares | 26 | ||

| Series 5 preferred shares | 26 | ||

| Series U preferred shares and Series Y preferred shares | 27 | ||

| Directors and officers | 28 | ||

| Directors | 28 | ||

| Board committees | 29 | ||

| Officers | 30 | ||

| Conflicts of interest | 31 | ||

| Corporate governance | 31 | ||

| Audit committee | 31 | ||

| Relevant education and experience of members | 31 | ||

| Pre-approval policies and procedures | 32 | ||

| External auditor service fees | 32 | ||

| Loans to directors and executive officers | 33 | ||

| Securities owned by directors | 33 | ||

| Compensation of directors | 33 | ||

| Executive compensation | 34 | ||

| Legal proceedings and regulatory actions | 34 | ||

| Transfer agent and registrar | 34 | ||

| Interest of experts | 34 | ||

| Additional information | 34 | ||

| Glossary | 35 | ||

| Schedule A | |||

| Schedule B | |||

| Schedule C | |||

| Schedule D | |||

| Appendices | |||

Unless the context indicates otherwise, a reference in this Annual Information Form (AIF) toTCPL or theCompany,we,us andour includes TCPL's parent, TransCanada Corporation (TransCanada) and the subsidiaries of TCPL through which its various business operations are conducted and a reference to "TransCanada" includes TransCanada Corporation and the subsidiaries of TransCanada Corporation, including TCPL. Where TCPL is referred to with respect to actions that occurred prior to its 2003 plan of arrangement with TransCanada, which is described below under the headingTransCanada PipeLines Limited – Corporate structure, these actions were taken by TCPL or its subsidiaries. The termsubsidiary, when referred to in this AIF, with reference to TCPL means direct and indirect wholly owned subsidiaries of, and legal entities controlled by, TransCanada or TCPL, as applicable.

Unless otherwise noted, the information contained in this AIF is given at or for the year ended December 31, 2012 (Year End). Amounts are expressed in Canadian dollars unless otherwise indicated. Information in relation to metric conversion can be found at Schedule A to this AIF. TheGlossary found at the end of this AIF contains certain terms defined throughout this AIF and abbreviations and acronyms that may not otherwise be defined in this document.

Certain portions of TCPL's Management's Discussion and Analysis dated February 11, 2013 (MD&A) are incorporated by reference into this AIF as stated below. The MD&A can be found on SEDAR (www.sedar.com) under TCPL's profile.

Financial information is presented in accordance with United States generally accepted accounting principles (U.S. GAAP). Effective January 1, 2012, TransCanada adopted U.S. GAAP for reporting purposes. For more information regarding TransCanada's adoption of U.S. GAAP, refer to theOther information – Critical accounting policiesandestimatesandOther information – Accounting changessections of the MD&A.

We use certain financial measures that do not have a standardized meaning under U.S. GAAP because we believe they improve our ability to compare results between reporting periods, and enhance understanding of our operating performance. Known as non-GAAP measures, they may not be comparable to similar measures provided by other companies. Refer to theAbout our business – Non-GAAP measures section of the MD&A for more information about the non-GAAP measures we use and a reconciliation to their GAAP equivalents, which section of the MD&A is incorporated by reference herein.

Forward-looking information

This AIF, including the MD&A disclosure incorporated by reference herein, contains certain information that is forward-looking and is subject to important risks and uncertainties. We disclose forward-looking information to help current and potential investors understand management's assessment of our future plans and financial outlook, and our future prospects overall.

Statements that are forward-looking are based on certain assumptions and on what we know and expect today and generally include words like anticipate, expect, believe, may, will, should, estimate or other similar words.

Forward-looking statements contained or incorporated by reference in this AIF may include information about the following, among other things:

- •

- anticipated business prospects

- •

- our financial and operational performance, including the performance of our subsidiaries

- •

- expectations or projections about strategies and goals for growth and expansion

- •

- expected cash flows

- •

- expected costs for planned projects, including projects under construction and in development

- •

- expected schedules for planned projects (including anticipated construction and completion dates)

- •

- expected regulatory processes and outcomes

- •

- expected outcomes with respect to legal proceedings, including arbitration

- •

- expected capital expenditures and contractual obligations

- •

- expected operating and financial results

- •

- the expected impact of future commitments and contingent liabilities

- •

- expected industry, market and economic conditions.

Forward-looking statements do not guarantee future performance. Actual events and results could be significantly different because of assumptions, risks or uncertainties related to our business or events that happen after the date of this AIF and other disclosure incorporated by reference herein.

2 -- TransCanada PipeLines Limited

Our forward-looking information is based on the following key assumptions, and subject to the following risks and uncertainties:

Assumptions

- •

- inflation rates, commodity prices and capacity prices

- •

- timing of debt issuances and hedging

- •

- regulatory decisions and outcomes

- •

- foreign exchange rates

- •

- interest rates

- •

- tax rates

- •

- planned and unplanned outages and the use of our pipeline and energy assets

- •

- integrity and reliability of our assets

- •

- access to capital markets

- •

- anticipated construction costs, schedules and completion dates

- •

- acquisitions and divestitures.

Risks and uncertainties

- •

- our ability to successfully implement our strategic initiatives

- •

- whether our strategic initiatives will yield the expected benefits

- •

- the operating performance of our pipeline and energy assets

- •

- amount of capacity sold and rates achieved in our U.S. pipelines business

- •

- the availability and price of energy commodities

- •

- the amount of capacity payments and revenues we receive from our energy business

- •

- regulatory decisions and outcomes

- •

- outcomes of legal proceedings, including arbitration

- •

- performance of our counterparties

- •

- changes in the political environment

- •

- changes in environmental and other laws and regulations

- •

- competitive factors in the pipeline and energy sectors

- •

- construction and completion of capital projects

- •

- labour, equipment and material costs

- •

- access to capital markets

- •

- cybersecurity

- •

- interest and foreign exchange rates

- •

- weather

- •

- technological developments

- •

- economic conditions in North America as well as globally.

You can read more about these factors and others in reports we have filed with Canadian securities regulators and the U.S. Securities and Exchange Commission (SEC).

You should not put undue reliance on forward-looking information and should not use future-oriented information or financial outlooks for anything other than their intended purpose. We do not update our forward-looking statements due to new information or future events, unless we are required to by law.

2012 Annual information form -- 3

TransCanada PipeLines Limited

CORPORATE STRUCTURE

TCPL's head office and registered office are located at 450 - 1st Street S.W., Calgary, Alberta, T2P 5H1.

TCPL is a Canadian public company. Significant dates and events are set forth below.

| Date | Event | |

| March 21, 1951 | Incorporated by Special Act of Parliament as Trans-Canada Pipe Lines Limited. | |

| April 19, 1972 | Continued under theCanada Corporations Act by Letters Patent, which included the alteration of its capital and change of name to TransCanada PipeLines Limited. | |

| June 1, 1979 | Continued under theCanada Business Corporations Act ("CBCA"). | |

| July 2, 1998 | Certificate of Arrangement issued in connection with the Plan of Arrangement with NOVA Corporation under which the companies merged and then split off the commodity chemicals business carried on by NOVA Corporation into a separate public company. | |

| January 1, 1999 | Certificate of Amalgamation issued reflecting TCPL's vertical short form amalgamation with a wholly owned subsidiary, Alberta Natural Gas Company Ltd. | |

| January 1, 2000 | Certificate of Amalgamation issued reflecting TCPL's vertical short form amalgamation with a wholly owned subsidiary, NOVA Gas International Ltd. | |

| May 4, 2001 | Restated TransCanada PipeLines Limited Articles of Incorporation filed. | |

| June 20, 2002 | Restated TransCanada PipeLines Limited By-Laws filed. | |

| May 15, 2003 | Certificate of Arrangement issued in connection with the plan of arrangement with TransCanada. TransCanada was incorporated pursuant to the provisions of the CBCA on February 25, 2003. The arrangement was approved by TCPL common shareholders on April 25, 2003 and following court approval, Articles of Arrangement were filed making the arrangement effective May 15, 2003. The common shareholders of TCPL exchanged each of their common shares of TCPL for one common share of TransCanada. The debt securities and preferred shares of TCPL remained obligations and securities of TCPL. TCPL continues to carry on business as the principal operating subsidiary of the TransCanada group of entities. | |

4 -- TransCanada PipeLines Limited

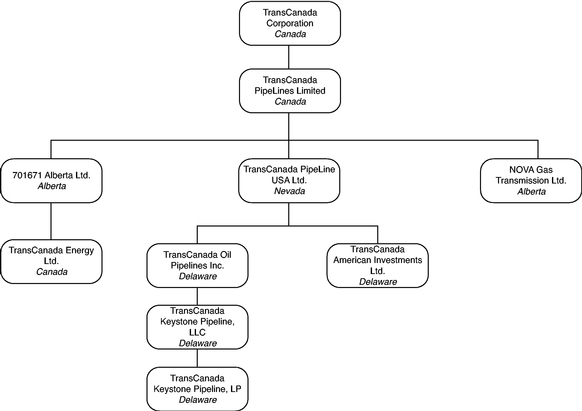

INTERCORPORATE RELATIONSHIPS

The following diagram presents the name and jurisdiction of incorporation, continuance or formation of TCPL's principal subsidiaries as at Year End. Each of the subsidiaries shown has total assets that exceeded 10 per cent of the total consolidated assets of TransCanada or revenues that exceeded 10 per cent of the total consolidated revenues of TransCanada as at Year End. TransCanada beneficially owns, controls or directs, directly or indirectly, 100 per cent of the voting shares in each of these subsidiaries, with the exception of TransCanada Keystone Pipeline, LP in which TransCanada indirectly holds 100 per cent of the partnership interests.

The above diagram does not include all of the subsidiaries of TCPL. The assets and revenues of excluded subsidiaries in the aggregate did not exceed 20 per cent of the total consolidated assets of TransCanada as at Year End or total consolidated revenues of TransCanada for the year then ended.

General development of the business

Our reportable business segments are Natural Gas Pipelines, Oil Pipelines and Energy. Natural Gas Pipelines and Oil Pipelines are principally comprised of the Company's respective natural gas and oil pipelines in Canada, the U.S. and Mexico as well as our regulated natural gas storage operations in the U.S. Energy includes the Company's power operations and the non-regulated natural gas storage business in Canada. Refer to theBusiness of TransCanada section below for further information regarding our Natural Gas Pipelines, Oil Pipelines and Energy businesses.

Summarized below are significant developments that have occurred in TransCanada's Natural Gas Pipelines, Oil Pipelines and Energy businesses, respectively, and the significant acquisitions, dispositions, events or conditions which have had an influence on that development, during the last three financial years.

2012 Annual information form -- 5

DEVELOPMENTS IN THE NATURAL GAS PIPELINES BUSINESS

| Date | Description of development | |

| Canadian Mainline | ||

| December 2010 | TransCanada filed an application with the National Energy Board (NEB) for approval of the interim 2011 tolls for the Canadian Mainline which contained certain changes to the tolling mechanism to reduce long haul tolls. The NEB decided not to approve the tolls as requested in the interim tolls application and set the then current 2010 tolls as interim tolls commencing January 1, 2011. | |

| January – February 2011 | TransCanada received approval for revised interim tolls, effective March 1, 2011 which increased interim tolls to more closely align with tolls calculated in accordance with the 2007-2011 settlement with stakeholders and more closely reflected the Canadian Mainline's costs and throughput for 2011. | |

| September 2011 | We filed a comprehensive restructuring proposal (Mainline Restructuring Proposal) with the NEB for the Canadian Mainline. The proposal is intended to enhance the competitiveness of the Canadian Mainline and transportation from the Western Canadian Sedimentary Basin (WCSB), and includes a request for 2012 and 2013 tolls that align with the proposed changes to our business structure and the terms and conditions of service on the Canadian Mainline. The NEB established interim tolls for 2012 based on the approved 2011 final tolls. | |

| November – December 2011 | TransCanada filed for and received approval to implement interim 2012 tolls on the Canadian Mainline effective January 1, 2012, at the same level as then approved 2011 final tolls. The NEB approved TransCanada's application for 2011 final tolls for the Canadian Mainline at the level of the tolls that were being charged on an interim basis. Final 2011 tolls were calculated in accordance with previously approved toll methodologies and were based on the principles contained in the 2007-2011 settlement with stakeholders, with adjustments to reduce toll impacts. Certain aspects of the 2011 revenue requirement were rolled into the Mainline Restructuring Proposal. | |

| May 2012 | We received NEB approval to build new pipeline facilities to provide Southern Ontario with additional natural gas supply from the Marcellus shale basin. | |

| May 2012 | The additional open season for firm transportation service on the Canadian Mainline, to bring additional Marcellus shale gas into Canada, closed. We were able to accommodate an additional 50 million cubic feet per day (MMcf/d) from the Niagara meter station to Kirkwall, Ontario, effective November 2012, with the potential for an additional 350 MMcf/d of incremental volume for November 2015, subject to finalizing precedent agreements with the interested parties. | |

| June 2012 | The NEB hearing on the Mainline Restructuring Proposal began and the hearing concluded in December 2012. A decision is not expected until late first quarter or early second quarter 2013. | |

| November 2012 | Natural gas supply from the Marcellus shale basin supply began moving in November 2012. | |

| Alberta System | ||

| February 2010 | TransCanada filed an application with the NEB for approval to construct and operate the Horn River pipeline. | |

| March 2010 | The North Central Corridor expansion of the Alberta System was completed. | |

| March 2010 | After a public hearing, the NEB approved TransCanada's application after a public hearing to construct and operate the Groundbirch pipeline project. | |

| June 2010 | TransCanada reached a three year settlement agreement with the Alberta System shippers and other interested parties and filed a 2010-2012 Revenue Requirement Settlement Application with the NEB. | |

| August 2010 | The NEB approved TransCanada's November 2009 application for the Alberta System's Rate Design Settlement and the commercial integration of the ATCO Pipelines system with the Alberta System. | |

| September 2010 | The NEB approved the Alberta System's 2010-2012 Revenue Requirement Settlement Application. | |

| October 2010 | The NEB approved final 2010 tolls for the Alberta System, which reflect the Alberta System 2010-2012 Revenue Requirement Settlement and Rate Design Settlement. | |

| December 2010 | The NEB approved the interim 2011 tolls for the Alberta System reflecting the 2010-2012 Revenue Requirement Settlement and continuing to transition to the toll methodology approved in the Rate Design Settlement. | |

| December 2010 | Groundbirch pipeline was completed and began transporting natural gas from the Montney shale gas formation into the Alberta System. | |

| January 2011 | TransCanada received approval from the NEB to construct the Horn River pipeline. | |

| March 2011 | TransCanada commenced construction of the $275 million Horn River pipeline. In addition, the Company executed an agreement to extend the Horn River pipeline by approximately 100 kilometers (km) (62 miles) at an estimated cost of $230 million. An application requesting approval to construct and operate this extension was filed with the NEB in October 2011. The total contracted volumes for Horn River, including the extension, are expected to be approximately 900 MMcf/d by 2020. | |

| August 2011 | The NEB approved construction of a 24 km (15 mile) extension of the Groundbirch pipeline and construction commenced. | |

6 -- TransCanada PipeLines Limited

| Date | Description of development | |

| October 2011 | Commercial integration of the Alberta System and ATCO Pipelines systems commenced. Under an agreement, the facilities of the Alberta System and ATCO Pipelines system are commercially operated as a single transmission system and transportation service is provided to customers by TransCanada pursuant to the Alberta System's tariff and suite of rates and services. The agreement further identifies distinct geographic areas within Alberta for the construction of new facilities by each of the Alberta System and ATCO Pipelines system. | |

| October 2011 | The NEB approved the construction of natural gas pipeline projects for the Alberta System with a capital cost of approximately $910 million. | |

| November – December 2011 | The regulatory decisions by which commercial integration of the Alberta System and ATCO Pipelines system was authorized are the subject of appeals to the Federal Court of Appeal. TransCanada continues to work with ATCO to gather information for the final stage of the integration which is to swap assets of equal value and will require approval by both the Alberta Utilities Commission and the NEB. | |

| May 2012 | The approximate $250 million Horn River project was completed, extending the Alberta System into the Horn River shale play in British Columbia (B.C.). | |

| June 2012 | The NEB approved the Leismer-Kettle River Crossover project, a 77 km (46 mile) pipeline to expand the Alberta System with the intent of increasing capacity to meet demand in northeastern Alberta. The expected cost of the expansion is an estimated $160 million. | |

| Third Quarter 2012 | During the first nine months of 2012, TransCanada continued to expand its Alberta System by completing and placing in-service twelve separate pipeline projects at a total cost of approximately $680 million. | |

| December 2012 | TransCanada was waiting for approval of approximately $330 million in additional projects, including the $100 million Chinchaga Expansion and the $230 million Komie North project that would extend the Alberta System further into the Horn River area. | |

| December 2012 | The current settlements for the Alberta and Foothills systems expired. Final tolls for 2013 will be determined through either new settlements or rate cases and any orders resulting from the NEB's decision on the Mainline Restructuring Proposal. | |

| January 2013 | The NEB issued its recommendation to the Governor-in-Council that the proposed Chinchaga Expansion component of the Komie North project be approved, but denied the proposed Komie North Extension component. All applications awaiting approval as of the end of 2012 have now been addressed. | |

| 2013 | We continue to advance pipeline development projects in B.C. and Alberta to transport new natural gas supply. We have filed applications with the NEB to expand the Alberta System to accommodate requests for additional natural gas transmission service throughout the northwest and northeast portions of the WCSB. In addition, subject to regulatory approvals, we propose to extend the Alberta System in northeast B.C. to connect both to the Prince Rupert Gas Transmission Project (as described below) and to additional North Montney gas supplies. Initial capital cost estimates are approximately $1 billion to $1.5 billion, with an in-service date targeted for the end of 2015. We have incremental firm commitments to transport approximately 3.4 billion cubic feet per day (Bcf/d) from western Alberta and northeastern B.C. by 2014. | |

| Coastal GasLink | ||

| June 2012 | We were selected by Shell Canada Limited (Shell) and its partners to design, build, own and operate the proposed Coastal GasLink project, an estimated $4 billion pipeline. The liquefied natural gas (LNG) Canada project is a joint venture led by Shell, with partners Korea Gas Corporation, Mitsubishi Corporation and PetroChina Company Limited. The approximate 650 km (404 mile) pipeline is expected to have an initial capacity of more than 1.7 Bcf/d and be placed in-service toward the end of the decade, subject to a final investment decision to be made by LNG Canada subsequent to obtaining final regulatory approvals. | |

| Prince Rupert Gas Transmission Project | ||

| January 2013 | We were selected by Progress Energy Canada Ltd. (Progress) to, subject to regulatory approvals, design, build, own and operate the proposed $5 billion Prince Rupert Gas Transmission Project. This proposed pipeline will transport natural gas primarily from the North Montney gas-producing region near Fort St John, B.C., to the proposed Pacific Northwest LNG export facility near Prince Rupert, B.C. We expect to finalize definitive agreements in early 2013, leading to an in-service date in late 2018. A final investment decision to construct the project is expected to be made by Progress following final regulatory approvals. | |

| Mexican Pipelines | ||

| June 2011 | The Guadalajara pipeline was completed. TransCanada and Mexico's Comisión Federal de Electricidad (CFE) have agreed to add a US$60 million compressor station to the pipeline. | |

| February 2012 | We signed a contract with the CFE for the approximately $500 million Tamazunchale Pipeline Extension Project. The project, which is supported by a 25-year contract with CFE, is a 30 inch pipeline with a capacity of 630 MMcf/d. Engineering, procurement and construction contracts have all been signed and construction related activities have begun. We expect the pipeline to be in-service in the first quarter of 2014. | |

| November 2012 | The CFE awarded us the Topolobampo pipeline. The project, which is supported by a 25-year contract with CFE, is a 30 inch pipeline with a capacity of 670 MMcf/d. We estimate total costs to be US$1 billion, and expect it to be in-service in | |

| mid-2016. | ||

2012 Annual information form -- 7

| Date | Description of development | |

| November 2012 | The CFE awarded us the Mazatlan pipeline, from El Oro to Mazatlan, Mexico. The project, which is supported by a 25-year contract with CFE and interconnects with the Topolobampo project, is a 24 inch pipeline with a capacity of 200 MMcf/d. We estimate total costs to be US$400 million, and expect it to be in-service in 2016. | |

| Alaska Pipeline Project | ||

| April 2010 | The Alaska Pipeline open season commenced. | |

| Third Quarter 2010 | Interested shippers on the proposed Alaska Pipeline Project submitted conditional commercial bids in the open season that closed in July 2010. The Alaska Pipeline Project team continued to work with shippers to resolve conditional bids received as part of the project's open season in working toward a U.S. Federal Energy Regulatory Commission (FERC) application deadline of October 2012 for the Alberta option that would extend from Prudhoe Bay to points near Fairbanks and Delta Junction, and then to the Alaska/Canada border where the pipeline would connect with a new pipeline in Canada. | |

| March 2012 | The Alaska North Slope producers (Exxon Mobil Corporation, ConocoPhillips and British Petroleum (BP)), along with TransCanada through its participation in the Alaska Pipeline Project, announced the companies have agreed on a work plan aimed at commercializing North Slope natural gas resources through an LNG option. This would involve construction of a natural gas pipeline from the North Slope to Valdez, Alaska where the gas would be liquefied and shipped to international markets. | |

| May 2012 | We received approval from the State of Alaska to suspend and preserve our activities on the Alaska/Alberta route and focus on the LNG alternative. This allowed us to defer our obligation to file for a FERC certificate for the Alberta route beyond fall 2012, our original deadline. | |

| July 2012 | The Alaska Pipeline Project announced a non-binding public solicitation of interest in securing capacity on a potential new pipeline system to transport Alaska's North Slope gas. The solicitation of interest took place between August 2012 and September 2012. There were a number of non-binding expressions of interest from potential shippers from a broad range of industry sectors in North America and Asia. | |

| ANR Pipeline | ||

| June 2012 | The FERC issued orders approving ANR's sale of its offshore assets to a newly created wholly owned subsidiary, TC Offshore LLC, allowing TC Offshore LLC to operate these assets as a stand-alone interstate pipeline. | |

| August 2012 | The FERC approved ANR Storage Company's settlement with its shippers. | |

| November 2012 | TC Offshore LLC began commercial operations. | |

| Gas Transmission Northwest LLC (GTN) | ||

| May 2011 | TransCanada closed the sale of a 25 per cent interest in each of GTN and Bison Pipeline LLC (Bison) to TC PipeLines, LP for a total transaction value of $605 million, which included US$81 million or 25 percent of GTN's outstanding debt. | |

| November 2011 | The FERC approved a settlement agreement between GTN and its shippers for new transportation rates to be effective January 2012 through December 2015. This settlement also requires GTN to file for new rates that are to be effective January 2016. | |

| Northern Border | ||

| January 2013 | Northern Border secured a final settlement agreement with its shippers that the FERC approved in December 2012, effective January 2013. The settlement rates for long-haul transportation are approximately 11 per cent lower than 2012 rates and depreciation was lowered from 2.4 to 2.2 per cent. The settlement also includes a three-year moratorium on filing cases or challenging the settlement rates but Northern Border must initiate another rate proceeding within five years. | |

| Great Lakes | ||

| July 2010 | The FERC approved, without modification, the settlement stipulation agreement reached among Great Lakes Gas Transmission Limited Partnership, active participants and the FERC trial staff. As approved, the stipulation and agreement applies to all current and future shippers on Great Lakes. This settlement requires Great Lakes to file for new rates by November 1, 2013. | |

| Bison | ||

| December 2010 | Construction of Bison pipeline was completed. | |

| January 2011 | Bison pipeline was placed into commercial service. | |

| May 2011 | TransCanada closed the sale of a 25 per cent interest in each of GTN and Bison to TC PipeLines, LP for a total transaction value of $605 million, which included US$81 million or 25 percent of GTN's outstanding debt. | |

Further information about developments in the Natural Gas Pipelines business can be found in the MD&A in theAbout our business – A long-term strategy, Natural Gas Pipelines – Results, Natural Gas Pipelines – Outlook, Natural Gas Pipelines – Understanding the Natural Gas Pipelines business andNatural Gas Pipelines – Significant events sections, which sections of the MD&A are incorporated by reference herein.

8 -- TransCanada PipeLines Limited

DEVELOPMENTS IN THE OIL PIPELINES BUSINESS

| Date | Description of development | |

| Gulf Coast Project | ||

| February 2012 | We announced that what had previously been the Cushing to U.S. Gulf Coast portion of the Keystone XL Pipeline has its own independent value to the marketplace, and that we plan to build it as the stand-alone Gulf Coast Project, which is not part of the Keystone XL Presidential Permit process. We expect the 36-inch pipeline to have an initial capacity of up to 700,000 barrels per day (Bbl/d), and an ultimate capacity of 830,000 Bbl/d. We estimate the total cost of the project to be US$2.3 billion, and as of Year End, construction was approximately 35 per cent complete. US$300 million of the total cost is expected to be spent on the Houston Lateral pipeline, a 76 km (47 mile) pipeline that will transport crude oil to Houston refineries. | |

| August 2012 | Construction on the Gulf Coast Project commenced. We expect to place the pipeline in-service at the end of 2013. | |

| Keystone XL Pipeline | ||

| March 2010 | The NEB approved TransCanada's application to construct and operate the Canadian portion of the Keystone U.S. Gulf Coast expansion. | |

| April 2010 | The U.S. Department of State (DOS) issued a Draft Environmental Impact Statement for Keystone XL. | |

| June 2010 | Keystone XL commenced operating at a reduced maximum operating pressure as the first section began delivering oil from Hardisty, Alberta to Wood River and Patoka in Illinois (Wood River/Patoka). | |

| December 2010 | The reduced maximum operating pressure restriction on the Canadian conversion section of the Wood River/Patoka section of Keystone was removed by the NEB following the completion of in-line inspections. | |

| Fourth Quarter 2010 | Construction of the second section of Keystone extending the pipeline from Steele City, Nebraska to Cushing, Oklahoma (the Cushing Extension) was completed, and line fill commenced in late 2010. | |

| January 2011 | Required operational modifications were completed on the Canadian conversion section of Keystone. As a result, the system was capable of operating at the approved design pressure. | |

| February 2011 | The commercial in-service of the Cushing Extension was achieved, and the Company also commenced recording earnings for the Wood River/Patoka section. | |

| May 2011 | Revised tolls came into effect for the Wood River/Patoka section. | |

| Second Quarter 2011 | The U.S. Department of Transportation Pipeline and Hazardous Materials Safety Administration issued a corrective action order on Keystone as a result of two above-ground incidents at pump stations in North Dakota and Kansas. TransCanada filed a re-start plan with the U.S. Pipeline and Hazardous Material Safety Administration which was approved in June 2011. | |

| August 2011 | TransCanada received a Final Environmental Impact Statement regarding the Keystone XL U.S. Presidential Permit application. | |

| November 2011 | The DOS announced that further analysis of route options for Keystone XL would need to be investigated, with a specific focus on the Sandhills area of Nebraska. | |

| December 2011 | TransCanada announced that it received additional binding commitments in support of Keystone XL following the conclusion of the Keystone Houston Lateral open season, which commenced in August 2011. | |

| February 2012 | TransCanada sent a letter to the DOS informing the DOS that TransCanada planned to file a Presidential Permit application in near future for Keystone XL. TransCanada also informed the DOS that the Cushing to U.S. Gulf Coast portion of the Keystone XL project would be constructed as the Gulf Coast Project and not as part of the Presidential Permit process. | |

| May 2012 | TransCanada filed revised fixed tolls for the Cushing Extension section of the Keystone Pipeline System with both the NEB and the FERC. The revised tolls, which reflect the final project costs of the Keystone Pipeline System, became effective July 1, 2012. | |

| May 2012 | We filed a Presidential Permit application (cross-border permit) with the DOS for Keystone XL to transport crude oil from the U.S./Canada border in Montana to Steele City, Nebraska. We continued to work collaboratively with the Nebraska Department of Environmental Quality (NDEQ) and various other stakeholders throughout 2012 to determine an alternative route in Nebraska that would avoid the Nebraska Sandhills. We had proposed an alternative route to the NDEQ in April 2012, and then modified the route in response to comments from the NDEQ and other stakeholders. | |

| September 2012 | TransCanada submitted a Supplemental Environmental Report to the NDEQ for the proposed re-route for Keystone XL in Nebraska, and provided an environmental report to the DOS, required as part of the DOS review of our cross-border permit application. | |

| January 2013 | The NDEQ issued its final evaluation report on our proposed re-route of Keystone XL to the Governor of Nebraska. The report noted that the proposed re-route avoids the Nebraska Sandhills, and that construction and operation of Keystone XL is expected to have minimal environmental impacts in Nebraska. In January, the Governor of Nebraska approved our proposed re-route. The DOS is now completing their environmental and National Interest Determination review process and we are awaiting their decision on our cross-border permit application. We estimate the total cost of the project to be US$5.3 billion and, as of Year End, had invested US$1.8 billion. We expect the pipeline to be in-service in late 2014 or early 2015, subject to regulatory approvals. | |

2012 Annual information form -- 9

| Date | Description of development | |

| Marketlink Projects | ||

| November 2010 | The open seasons for the Bakken Marketlink and Cushing Marketlink projects, which commenced in September 2010, closed successfully. | |

| October 2012 | We have commenced construction on the Cushing Marketlink receipt facilities and expect to begin transporting crude oil supply from the Permian Basin producing region in western Texas to the U.S. Gulf Coast in late 2013 after our Gulf Coast Project is placed in-service. Our Bakken Marketlink project will transport crude oil supply from the Williston Basin producing region in North Dakota and Montana to Cushing, Oklahoma on facilities that form part of Keystone XL which remains subject to regulatory approval. | |

| Keystone Hardisty Terminal | ||

| March 2012 | We launched and concluded a binding open season to obtain commitments from interested parties for the Keystone Hardisty Terminal. | |

| May 2012 | We announced that we had secured binding long-term commitments of more than 500,000 Bbl/d for the Keystone Hardisty Terminal, and are expanding the proposed two million barrel project to a 2.6 million barrel terminal at Hardisty, Alberta, due to strong commercial support. We expect the terminal to be operational in late 2014 and cost approximately $275 million. | |

| Northern Courier Pipeline | ||

| August 2012 | We announced that we had been selected by Fort Hills Energy Limited Partnership to design, build, own and operate the proposed Northern Courier Pipeline. We estimate total capital costs to be $660 million. The pipeline system is fully subscribed under long-term contract to service the Fort Hills mine, which is jointly owned by Suncor Energy Inc, Total E&P Canada Ltd. and Teck Resources Limited. The project is conditional on the Fort Hills project receiving sanctions by the owners of the Fort Hills mine and is subject to regulatory approval. | |

| Grand Rapids Pipeline | ||

| October 2012 | We announced that we had entered into binding agreements with Phoenix Energy Holdings Limited (Phoenix) to develop the Grand Rapids Pipeline in northern Alberta. The project, which includes crude oil and diluent lines, will have the capacity to move up to 900,000 Bbl/d of crude oil and 330,000 Bbl/d of diluent. We and Phoenix will each own 50 per cent of the project and we will operate the system, which is expected to cost $3 billion. Phoenix has entered into a long-term commitment to ship crude oil and diluent on this pipeline. We expect the Grand Rapids Pipeline system, subject to regulatory approvals, to be placed in-service in multiple stages, with initial crude oil service by mid-2015 and the complete system in-service by the second half of 2017. | |

| Canadian Mainline Conversion | ||

| Third Quarter 2012 | We have determined that it is technically and economically feasible to convert a portion of the Canadian Mainline natural gas pipeline system to crude oil service. We are actively pursuing this project and have begun soliciting input from stakeholders and prospective shippers to determine market acceptance. | |

Further information about developments in the Oil Pipelines business can be found in the MD&A in theAbout our business – A long-term strategy, Oil Pipelines – Results, Oil Pipelines – Outlook, Oil Pipelines – Understanding the Oil Pipelines business andOil Pipelines – Significant events sections, which sections of the MD&A are incorporated by reference herein.

10 -- TransCanada PipeLines Limited

DEVELOPMENTS IN THE ENERGY BUSINESS

| Date | Description of development | |

| Sundance | ||

| Second Quarter 2010 | Sundance B Unit 3 experienced an unplanned outage related to mechanical failure of certain generator components and was subject to a force majeure claim by TransAlta Corporation (TransAlta). The ASTC Power Partnership, which holds the Sundance B power purchase agreement (PPA), disputed the claim under the binding dispute resolution process provided in the PPA because we did not believe TransAlta's claim met the test of force majeure. We therefore recorded equity earnings from our 50 per cent ownership interest in ASTC Power Partnership as though this event were a normal plant outage. | |

| December 2010 | Sundance A Units 1 and 2 were withdrawn from service. | |

| January 2011 | Sundance A Units 1 and 2 were subject to a force majeure claim by TransAlta. | |

| February 2011 | TransAlta informed us that it was not economic to replace or repair Units 1 and 2, and that the Sundance A PPA should be terminated. We disputed both the force majeure and the economic destruction claims under the binding dispute resolution process provided in the PPA. | |

| July 2012 | An arbitration panel decided that the Sundance A PPA should not be terminated and ordered TransAlta to rebuild Units 1 and 2. The panel also limited TransAlta's force majeure claim from November 20, 2011 until the units can reasonably be returned to service. TransAlta announced that it expects the units to be returned to service in the fall of 2013. Since we considered the outages to be an interruption of supply, we accrued $188 million in pre-tax income between December 2010 and March 2012. The outcome of the decision was that we received approximately $138 million of this amount. We recorded the $50 million difference as a charge to second quarter 2012 earnings, of which $20 million related to amounts accrued in 2011. We will not record further revenue or costs from the PPA until the units are returned to service. The net book value of the Sundance A PPA recorded in Intangibles and Other Assets remains fully recoverable. | |

| November 2012 | An arbitration decision was reached with the arbitration panel granting partial force majeure relief to TransAlta with respect to Sundance B Unit, and we reduced our equity earnings by $11 million from the ASTC Power Partnership to reflect the amount that will not be recovered as result of the decision. | |

| Napanee Generating Station | ||

| December 2012 | We signed a contract with the Ontario Power Authority (OPA), to develop, own and operate a new 900 megawatt (MW) natural gas-fired power plant at Ontario Power Generation's Lennox site in Eastern Ontario in the town of Greater Napanee. The plant will replace the facility that was planned and subsequently cancelled in the community of Oakville, Ontario and will operate under a 20-year Clean Energy Supply contract with the OPA. We were reimbursed for $250 million of costs, mainly related to natural gas turbines that were purchased for the Oakville project, which will now be used at Napanee. We plan to invest approximately $1.0 billion in the Napanee facility. | |

| Cartier Wind | ||

| November 2011 | The Montagne-Sèche project and phase one of the Gros-Morne wind farm were completed. | |

| November 2012 | We placed the second phase of the Gros-Morne wind farm project in service, completing the 590 MW, five-phase Cartier Wind Project in Québec. All of the power produced by Cartier Wind is sold to Hydro-Québec Distribution (Hydro-Québec) under 20-year PPAs. | |

| Ontario Solar | ||

| December 2011 | We agreed to buy nine Ontario solar projects (combined capacity of 86 MW) from Canadian Solar Solutions Inc. (Canadian Solar), for approximately $476 million. Under the terms of the agreement, Canadian Solar will develop and build each of the nine solar projects using photovoltaic panels. We will buy each project once construction and acceptance testing are complete and commercial operation begins. All power produced will be sold under 20-year PPAs with the OPA under the Feed-in Tariff program in Ontario. We expect to close the acquisition of the first two projects (combined capacity of 20 MW) in the first half of 2013 for a total cost of approximately $125 million. We expect to acquire the other seven projects in 2013 to late 2014, subject to regulatory approvals. | |

| Bécancour | ||

| June 2011 | Hydro-Québec notified us it would exercise its option to extend the agreement to suspend all electricity generation from Bécancour throughout 2012. Under the original agreement, Hydro-Québec has the option, to extend the suspension on an annual basis until such time as regional electricity demand levels recover. We continue to receive capacity payments under the agreement similar to those that would have been received under the normal course of operation. | |

| June 2012 | Hydro-Québec notified us that it would exercise its option to extend the agreement to suspend all electricity generation from the Bécancour power plant through 2013. Under the suspension agreement, Hydro-Québec has the option (subject to certain conditions) to extend the suspension every year until regional electricity demand levels recover. We continue to receive capacity payments while generation is suspended. | |

2012 Annual information form -- 11

| Date | Description of development | |

| Bruce | ||

| February 2011 | The Bruce Power Refurbishment Implementation Agreement (the BPRIA) was amended to extend the suspension date for Bruce A contingent support payments from December 31, 2011 to June 1, 2012. Contingent support payments received from the OPA by Bruce A are equal to the difference between the fixed prices under the BPRIA and spot market prices. As a result of the amendment, all output from Bruce A was subject to spot prices effective June 1, 2012 until the restart of both Units 1 and 2 was complete. Bruce Power and the OPA had amended certain terms and conditions of the BPRIA in July 2009, which included: amendments to the Bruce B floor price mechanism, the removal of a support payment cap for Bruce A, an amendment to the capital cost-sharing mechanism, and addition of a provision for deemed generation payments to Bruce Power at the contracted prices under circumstances where generation from Bruce A and Bruce B is reduced due to system curtailments on the Independent Electricity System Operator controlled grid in Ontario. Under the original BPRIA, which was signed in 2005, Bruce A committed to refurbish and restart the then currently idle Units 1 and 2, extend the operating life of Unit 3 and replace the steam generators on Unit 4. Fuelling of both Unit 2 and Unit 1 has now been completed and the final phases of commissioning for Unit 2 are underway. Subject to regulatory approval, Bruce Power expects to commence commercial operations of Unit 2 in first quarter 2012 and commercial operations of Unit 1 in third quarter 2012. | |

| November 2011 | Bruce Power commenced the West Shift Plus outage as part of the life extension strategy for Unit 3. | |

| March 2012 | Bruce Power received authorization from the Canadian Nuclear Safety Commission to power up the Unit 2 reactor. | |

| May 2012 | An incident occurred within the Unit 2 electrical generator on the non-nuclear side of the plant which delayed the synchronization of Unit 2 to the Ontario electrical grid. As a result, Bruce Power submitted a force majeure claim to the OPA. | |

| June 2012 | Bruce Power returned Unit 3 to service after completing the $300 million West Shift Plus life extension outage, which began in 2011. Unit 4 is expected to return to service in late first quarter 2013 after the completion of an expanded outage investment program that began in August 2012. These investments should allow Units 3 and 4 to produce low cost electricity until at least 2021. | |

| August 2012 | TransCanada confirmed that Bruce Power's force majeure claim to the OPA related to Unit 2 (Bruce A) had been accepted. The claim was the result of a May 2012 event that delayed the synchronization of this unit to the Ontario power grid. With the acceptance of the force majeure claim, Bruce Power continued to receive the contracted price for power generated from the operating units at Bruce A after July 1, 2012. | |

| October 2012 | Unit 1 and 2 were returned to service following the completion of the refurbishment. The incident in May 2012 within the Unit 2 electrical generator on the non-nuclear side of the plant had delayed returning the units to service. Bruce Power's force majeure claim to the OPA was accepted in August, and it continued to receive the contracted price for power generated during the force majeure period. | |

| November 2012 | Both Units 1 and 2 have operated at reduced output levels following their return to service, and Bruce Power took Unit 1 offline for an approximate one month maintenance outage. Bruce Power expects the availability percentages for Units 1 and 2 to increase over time, however, these units have not operated for an extended period of time and may experience slightly higher forced outage rates and reduced availability percentages in 2013. Overall plant availability for Bruce A is expected to be approximately 90 per cent in 2013. | |

| Ravenswood | ||

| Third and Fourth Quarters 2011 | Spot prices for capacity sales in the New York Zone J market were negatively impacted by the manner in which the New York Independent System Operator (NYISO) applied pricing rules for a power plant that had recently began service in this market. We jointly filed two formal complaints with the FERC challenging how the NYISO applied its buy-side mitigation rules affecting bidding criteria associated with two new power plants that began service in the New York Zone J markets during the summer of 2011. | |

| June 2012 | The FERC addressed the first complaint, indicating it would take steps to increase transparency and accountability for future mitigation exemption tests (MET) and decisions. | |

| September 2012 | The FERC granted an order on the second complaint, directing the NYISO to retest the two new power plants as well as a transmission project currently under construction using an amended set of assumptions to more accurately perform the MET calculations, in accordance with existing rules and tariff provisions. The recalculation was completed in November 2012 and it was determined that one of the plants had been granted an exemption in error. That exemption was revoked and the plant is now required to offer its capacity at a floor price which has put upward pressure on capacity auction prices since December. The order was prospective only and has no impact on capacity prices for prior periods. | |

| CrossAlta | ||

| December 2012 | We acquired the remaining 40 per cent interests in the Crossfield Gas Storage facility and CrossAlta Gas Storage & Services Ltd. marketing company from BP for approximately $220 million. We now own and operate 100 per cent of the interests of CrossAlta. The acquisition added an additional 27 billion cubic feet (Bcf) of working gas storage capacity to our existing portfolio in Alberta. | |

| Coolidge | ||

| May 2011 | Coolidge power generating station was completed and placed in-service. | |

| Kibby Wind | ||

| October 2010 | The 22 turbine, 66 MW second phase of Kibby Wind was completed and placed in-service. | |

| Halton Hills | ||

| September 2010 | The 683 MW Halton Hills power plant was completed and placed in-service. | |

12 -- TransCanada PipeLines Limited

Further information about developments in the Energy business can be found in the MD&A in theAbout our business – A long-term strategy, Energy – Results, Energy – Outlook, Energy – Understanding the Energy business andEnergy – Significant events sections, which sections of the MD&A are incorporated by reference herein.

Business of TCPL

We are a leading North American energy infrastructure company focused on Natural Gas Pipelines, Oil Pipelines and Energy. At Year End and for the year then ended, Natural Gas Pipelines accounted for approximately 53 per cent of revenues and 47 per cent of TCPL's total assets, Oil Pipelines accounted for approximately 13 per cent of revenues and 21 per cent of TCPL's total assets and Energy accounted for approximately 34 per cent of revenues and 27 per cent of TCPL's total assets. The following table shows TCPL's revenues from operations by segment, classified geographically, for the years ended December 31, 2012 and 2011.

| Revenues from operations(millions of dollars) | 2012 | 2011 | |||

| Natural Gas Pipelines | |||||

| Canada – Domestic | $2,294 | $2,180 | |||

| Canada – Export(1) | 751 | 786 | |||

| United States | 1,112 | 1,207 | |||

| Mexico | 107 | 71 | |||

| 4,264 | 4,244 | ||||

| Oil Pipelines | |||||

| Canada – Domestic | – | – | |||

| Canada – Export(1) | 370 | 300 | |||

| United States | 669 | 527 | |||

| 1,039 | 827 | ||||

| Energy(2) | |||||

| Canada – Domestic | 1,233 | 1,749 | |||

| Canada – Export(1) | – | 1 | |||

| United States | 1,471 | 1,018 | |||

| 2,704 | 2,768 | ||||

| Total revenues(3) | $8,007 | $7,839 | |||

- (1)

- Exports include pipeline revenues attributable to deliveries to U.S. pipelines and power deliveries to U.S. markets.

- (2)

- Revenues include sales of natural gas.

- (3)

- Revenues are attributed to countries based on country of origin of product or service.

The following is a description of each of TCPL's three main areas of operations.

2012 Annual information form -- 13

NATURAL GAS PIPELINES BUSINESS

TransCanada delivers natural gas to local distribution companies, power generation facilities and other businesses across Canada, the U.S. and Mexico. Our Natural Gas Pipelines and related holdings are described below.

We are the operator of all of the following natural gas pipelines and storage assets except for Iroquois.

Length | Description | Effective ownership | ||||

| Canadian pipelines | ||||||

| Alberta System | 24,337 km (15,122 miles) | Gathers and transports natural gas within Alberta and Northeastern B.C., and connects with the Canadian Mainline, Foothills system and third-party pipelines | 100% | |||

| Canadian Mainline | 14,101 km (8,762 miles) | Transports natural gas from the Alberta/Saskatchewan border to the Québec/Vermont border, and connects with other natural gas pipelines in Canada and the U.S. | 100% | |||

| Foothills | 1,241 km (771 miles) | Transports natural gas from central Alberta to the U.S. border for export to the U.S. Midwest, Pacific northwest, California and Nevada | 100% | |||

| Trans Québec & Maritimes (TQM) | 572 km (355 miles) | Connects with Canadian Mainline near the Ontario/Québec border to transport natural gas to the Montreal to Québec City corridor, and connects with the Portland pipeline system that serves the northeast U.S. | 50% | |||

| U.S. pipelines | ||||||

| ANR Pipeline | 16,656 km (10,350 miles) | Transports natural gas from producing fields in Texas and Oklahoma, from offshore and onshore regions of the Gulf of Mexico and from the U.S. midcontinent, for delivery mainly to Wisconsin, Michigan, Illinois, Indiana and Ohio. Connects with Great Lakes | 100% | |||

| ANR Storage | 250 Bcf | Provides regulated underground natural gas storage service from facilities located in Michigan | ||||

| Bison | 487 km (303 miles) | Transports natural gas from the Powder River Basin in Wyoming to Northern Border in North Dakota. We effectively own 83.3 per cent of the system through the combination of our 75 per cent direct ownership interest and our 33.3 per cent interest in TC PipeLines, LP | 83.3% | |||

| GTN | 2,178 km (1,353 miles) | Transports natural gas from the WCSB and the Rocky Mountain region to Washington, Oregon and California. Connects with Tuscarora and Foothills. We effectively own 83.3 per cent of the system through the combination of our 75 per cent direct ownership interest and our 33.3 per cent interest in TC PipeLines, LP | 83.3% | |||

| Great Lakes | 3,404 km (2,115 miles) | Connects with ANR and the Canadian Mainline near Emerson, Manitoba, to transport natural gas to eastern Canada, and the U.S. upper Midwest. We effectively own 69.0 per cent of the system through the combination of our 53.6 per cent direct ownership interest and our 33.3 per cent interest in TC PipeLines, LP | 69% | |||

| Iroquois | 666 km (414 miles) | Connects with Canadian Mainline near Waddington, New York to deliver natural gas to customers in the U.S. northeast | 44.5% | |||

| North Baja | 138 km (86 miles) | Transports natural gas between Ehrenberg, Arizona and Ogilby, California, and connects with a third-party natural gas system on the California/Mexico border. We effectively own 33.3 per cent of the system through our 33.3 per cent interest in TC PipeLines, LP | 33.3% | |||

| Northern Border | 2,265 km (1,407 miles) | Transports natural gas through the U.S. Midwest, and connects with Foothills near Monchy, Saskatchewan. We effectively own 16.7 per cent of the system through our 33.3 per cent interest in TC PipeLines, LP | 16.7% | |||

| Portland | 474 km (295 miles) | Connects with TQM near East Hereford, Québec, to deliver natural gas to customers in the U.S. northeast | 61.7% | |||

| Tuscarora | 491 km (305 miles) | Transports natural gas from GTN at Malin, Oregon to Wadsworth, Nevada, and delivers gas in northeastern California and northwestern Nevada. We effectively own 33.3 per cent of the system through our 33.3 per cent interest in TC PipeLines, LP. | 33.3% | |||

14 -- TransCanada PipeLines Limited

Length | Description | Effective ownership | ||||

| Mexican pipelines | ||||||

| Guadalajara | 310 km (193 miles) | Transports natural gas from Manzanillo to Guadalajara in Mexico | 100% | |||

| Tamazunchale | 130 km (81 miles) | Transports natural gas from Naranjos, Veracruz in east central Mexico to Tamazunchale, San Luis Potos, Mexico | 100% | |||

| Under construction | ||||||

| Mazatlan Pipeline | 413 km (257 miles) | To deliver natural gas from El Oro to Mazatlan, Mexico. Connects to the Topolobampo Pipeline Project | 100% | |||

| Tamazunchale Pipeline Extension | 235 km (146 miles) | Extend existing terminus of the Tamazunchale Pipeline to deliver natural gas to power generating facilities in El Sauz, Queretaro, Mexico | 100% | |||

| Topolobampo Pipeline | 530 km (329 miles) | To deliver natural gas from Chihuahua to Topolobampo, Mexico | 100% | |||

| In development | ||||||

| Alaska Pipeline Project | 2,737 km (1,700 miles) | To transport natural gas from Prudhoe Bay to Alberta, or from Prudhoe Bay to LNG facilities in south-central Alaska. We have an agreement with ExxonMobil to jointly advance the projects | ||||

| Coastal GasLink | 650 km* (404 miles) | To deliver natural gas from the Montney gas-producing region near Dawson Creek, B.C. to LNG Canada's proposed LNG facility near Kitimat, B.C. | ||||

| Prince Rupert Gas Transmission Project | 750 km* (466 miles) | To deliver natural gas from North Montney gas producing region near Fort St. John, B.C. to the proposed Pacific Northwest LNG facility near Prince Rupert, B.C. | ||||

- *

- Pipe lengths are estimates as final route is still under design.

Further information about the Company's pipeline holdings, developments and opportunities and significant regulatory developments which relate to Natural Gas Pipelines can be found in the MD&A in theNatural Gas Pipelines – Results, Natural Gas Pipelines – Understanding the Natural Gas Pipelines business andNatural Gas Pipelines – Significant events sections, which sections of the MD&A are incorporated by reference herein.

OIL PIPELINES BUSINESS

TransCanada contracts and delivers North American crude oil supply to key U.S. markets. Our Oil Pipelines and related holdings are described below.

We are the operator of all of the following pipelines and properties.

| Length | Description | Ownership | ||||

| Oil pipelines | ||||||

| Keystone Pipeline System | 3,467 km (2,154 miles) | Transports crude oil from Hardisty, Alberta, to U.S. markets at Wood River and Patoka in Illinois, and to Cushing, Oklahoma | 100% | |||

| Under construction | ||||||

| Cushing Marketlink | Crude oil receipt facilities | To transport crude oil from the Permian Basin producing region in western Texas to the U.S. Gulf Coast refining market on facilities that form part of the Gulf Coast Project | 100% | |||

| Gulf Coast Project | 780 km (485 miles) | To transport crude oil from the hub at Cushing, Oklahoma to the U.S. Gulf Coast refinery market. Includes the 76 km (47 mile) Houston Lateral pipeline | 100% | |||

| Keystone Hardisty Terminal | Crude oil terminal | Crude oil terminal to be located at Hardisty, Alberta, providing Western Canadian producers with new crude oil batch accumulation tankage and pipeline infrastructure and access to the Keystone Pipeline System | 100% | |||

2012 Annual information form -- 15

| Length | Description | Ownership | ||||

| In development | ||||||

| Bakken Marketlink | Crude oil receipt facilities | To transport crude oil from the Williston Basin producing region in North Dakota and Montana to Cushing, Oklahoma on facilities that form part of Keystone XL | 100% | |||

| Canadian Mainline conversion | Conversion of a portion of the Canadian Mainline natural gas pipeline system to crude oil service, which will transport crude oil between Hardisty, Alberta and markets in eastern Canada | 100% | ||||

| Grand Rapids Pipeline | 500 km (300 miles) | To transport crude oil between the producing area northwest of Fort McMurray and the Edmonton/Heartland market region. Project is a partnership with Phoenix | 50% | |||

| Keystone XL | 1,897 km (1,179 miles) | Pipeline from Hardisty, Alberta to Steele City, Nebraska to expand capacity of the Keystone Pipeline System to 1.4 million Bbl/d. Awaiting U.S. Presidential Permit decision | 100% | |||

| Northern Courier Pipeline | 90 km (56 miles) | To transport bitumen and diluent between the Fort Hills mine site and the Voyageur Upgrader located north of Fort McMurray, Alberta | 100% | |||

Further information about the Company's pipeline holdings, developments and opportunities and significant regulatory developments which relate to Oil Pipelines can be found in the MD&A in theOil Pipelines – Results, Oil Pipelines – Understanding the Oil Pipelines business andOil Pipelines – Significant events sections, which sections of the MD&A are incorporated by reference herein.

REGULATION OF THE NATURAL GAS AND OIL PIPELINES BUSINESSES

Canada

Natural Gas Pipelines

Under the terms of theNational Energy Board Act (Canada), the Canadian Mainline, the Alberta System and other Canadian pipelines owned or operated by TransCanada (collectively, the Systems) are regulated by the NEB. The NEB sets tolls that provide TransCanada the opportunity to recover costs of transporting natural gas, including the return of capital (depreciation) and return on the average investment base for each of the Systems. In addition, new facilities on or associated with the Systems are approved by the NEB before construction begins and the NEB regulates the operations of each of the Systems. Net earnings of the Systems may be affected by changes in investment base, the allowed return on equity, and any incentive earnings.

Natural Gas Pipeline Projects

The Coastal GasLink Pipeline and the Prince Rupert Gas Transmission projects are being proposed and developed primarily under the regulatory regime administered by the B.C. Oil and Gas Commission (BCOGC) and the B.C. Environmental Assessment Office (BCEAO). The BCOGC is responsible for overseeing oil and gas operations in B.C., including exploration, development, pipeline transportation and reclamation. The BCEAO is an agency that manages the review of proposed major projects in B.C., as required by the B.C.Environmental Assessment Act. Both projects are also subject to the provisions of theCanadian Environmental Assessment Act. Pre-application activities are currently underway with the BCOGC and BCEAO as well as the Canadian Environmental Assessment Agency.

Oil Pipelines

The NEB regulates the terms and conditions of service, including rates, and the physical operation of the Canadian portion of the Keystone Pipeline System, including the Keystone Hardisty Terminal. NEB approval is also required for facility additions. The rates for transportation service on the Keystone Pipeline System are calculated in accordance with a methodology agreed to in transportation service agreements between Keystone and its shippers, and approved by the NEB.

Oil Pipeline Projects

The Northern Courier Pipeline and Grand Rapids Pipeline projects are being proposed and developed primarily under the regulatory regime administered by the Alberta Energy Resources Conservation Board (ERCB) and Alberta Environment and Sustainable Resource Development (ESRD). ERCB approval is required to construct and operate the pipelines and associated facilities. ESRD approval is required to construct and operate a tank terminal when the project involves the storage of more than 10,000 cubic meters (62,898 Bbl/d) of refined petroleum products. Pre-application activities are currently underway.

United States

Natural Gas Pipelines

TransCanada's wholly owned and partially owned U.S. pipelines are considerednatural gas companies operating under the provisions of theNatural Gas Act of 1938 and theNatural Gas Policy Act of 1978, and are subject to the jurisdiction of the FERC. The Natural Gas Act of 1938 grants the FERC authority over the construction and operation of pipelines and related facilities. The FERC also has authority to regulate rates for natural gas transportation and interstate commerce. The ANR System's natural gas storage facilities in Michigan are also regulated by FERC.

16 -- TransCanada PipeLines Limited

Oil Pipelines

The FERC also regulates the terms and conditions of service, including transportation rates, on the U.S. portion of the Keystone Pipeline System. Certain states in which Keystone Pipeline System has rights of way also regulate construction and siting of Keystone Pipeline System. The Keystone XL pipeline remains subject to the DOS decision on TransCanada's Presidential Permit application.

Mexico

Natural Gas Pipelines

TransCanada's pipelines in Mexico are regulated by the Comisión Reguladora de Energía or Energy Regulatory Commission (CRE). The CRE regulates the construction and operation of pipeline facilities including the approval of tariffs, services and related rates. However, the contracts underpinning the facilities in Mexico are long-term negotiated rate contracts and not subject to further regulatory approval.

ENERGY BUSINESS

TransCanada's Energy business includes a portfolio of power generation assets in Canada and the U.S., and unregulated natural gas storage assets in Alberta. This segment of our business includes the acquisition, development, construction, ownership and operation of electrical power generation plants, the purchase and marketing of electricity, the provision of electricity account services to energy and industrial customers, and the development, construction, ownership and operation of natural gas storage in Alberta. Our Energy assets and related holdings are described below.

We are the operator of all of our Energy assets, except for the Sheerness, Sundance A and Sundance B PPAs, Cartier Wind, Bruce A and B and Portlands Energy.

| Generating capacity (MW) | Type of fuel | Description | Location | Ownership | ||||||

| Canadian Power | ||||||||||

| 8,070 MW of power generation capacity (including facilities in development) | ||||||||||

| Western Power | ||||||||||

| 2,636 MW of power supply in Alberta and the western U.S. | ||||||||||

| Bear Creek | 80 | natural gas | Cogeneration plant | Grand Prairie, Alberta | 100% | |||||

| Cancarb | 27 | natural gas, waste heat | Facility fuelled by waste heat from an adjacent TransCanada facility that produces thermal carbon black, a by-product of natural gas | Medicine Hat, Alberta | 100% | |||||

| Carseland | 80 | natural gas | Cogeneration plant | Carseland, Alberta | 100% | |||||

| Coolidge(1) | 575 | natural gas | Simple-cycle peaking facility | Coolidge, Arizona | 100% | |||||

| Mackay River | 165 | natural gas | Cogeneration plant | Fort McMurray, Alberta | 100% | |||||

| Redwater | 40 | natural gas | Cogeneration plant | Redwater, Alberta | 100% | |||||

| Sheerness PPA | 756 | coal | PPA for entire output of facility | Hanna, Alberta | 100% | |||||

| Sundance A PPA | 560 | coal | PPA for entire output of facility | Wabamun, Alberta | 100% | |||||

| Sundance B PPA (Owned by ASTC Power Partnership(2)) | 353(3) | coal | PPA for entire output of facility | Wabamun, Alberta | 50% | |||||

| Eastern Power | ||||||||||

| 2,950 MW of power generation capacity (including facilities in development) | ||||||||||

| Bécancour | 550 | natural gas | Cogeneration plant | Trois-Rivières, Québec | 100% | |||||