Trinity Industries, Inc. November 2011 Exhibit 99.1 |

2 Forward Looking Statements This presentation contains “forward looking statements” as defined by the Private Securities Litigation Reform Act of 1995 and includes statements as to expectations, beliefs and future financial performance, or assumptions underlying or concerning matters herein. These statements that are not historical facts are forward looking. Readers are directed to Trinity’s Form 10-K and other SEC filings for a description of certain of the business issues and risks, a change in any of which could cause actual results or outcomes to differ materially from those expressed in the forward looking statements. Any forward looking statement speaks only as of the date on which such statement is made. Trinity undertakes no obligation to update any forward looking statement or statements to reflect events or circumstances after the date on which such statement is made. |

3 Trinity is a Multi-Industry Company Rail Group Leading manufacturer of railcars in North America Manufacturer of railcar axles in North America Manufacturer of railcar coupling devices in North America Railcar Leasing and Management Services Group Leading provider of railcar leasing and management services Construction Products Group Leading full-line manufacturer of highway guardrail and crash cushions in the United States Leading supplier of concrete and aggregates in Texas Energy Equipment Group Leading manufacturer of structural wind towers in North America Leading producer of propane tanks, tank containers, and tank heads for pressure and non-pressure vessels in North America Inland Barge Group Leading manufacturer of inland barges in the United States Largest manufacturer of fiberglass covers for barges in the United States |

4 Trinity’s Differentiating Strategies and Tactics Trinity’s strategies and tactics are designed to improve our performance in all economic cycles During the last decade, we enhanced our multi-industry portfolio by: Strategically growing the Leasing business to provide a solid base of earnings and cash flows Increasing our manufacturing efficiency while lowering our manufacturing cost basis Focusing on selectively building our backlogs Investing in diversified businesses through organic growth Making selective acquisitions to complement our portfolio Trinity is uniquely positioned to generate significant profits during an up cycle and manage through a severe down cycle while building strength |

5 Trinity Today Leasing and Management Services Expand relationships with end-users of railcars Introduce new products into the market Provide earnings and cash flow base for Trinity Consistently grow the business Manufacturing Businesses Maintain leadership positions Utilize significant manufacturing footprint in Southern U.S. and Mexico Optimize operational flexibility Generate continuous synergies Trinity’s Multi-Industry Model |

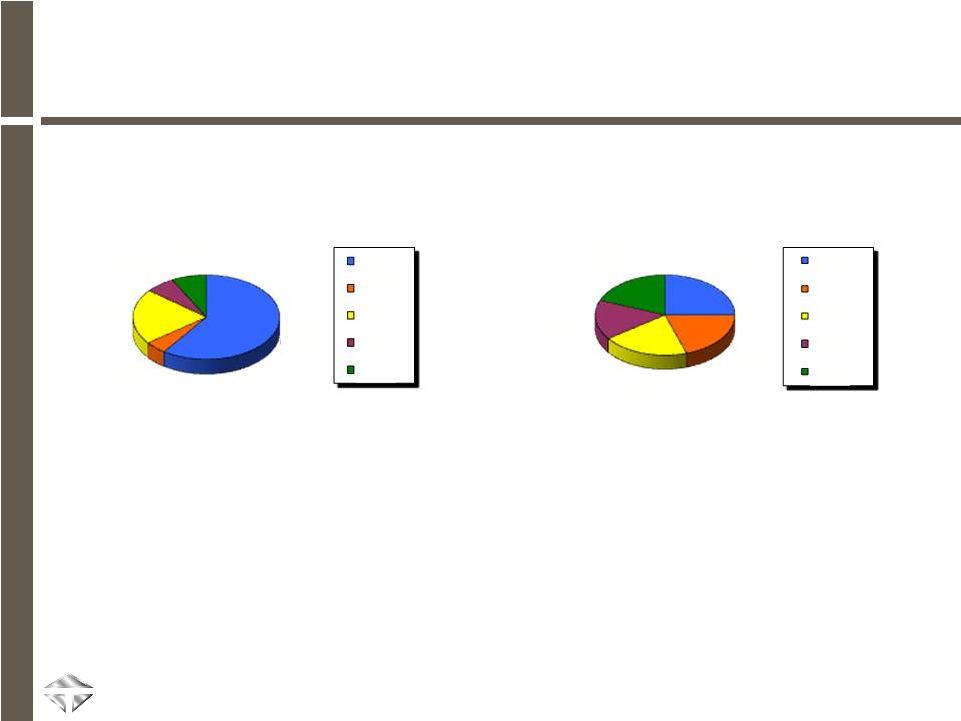

6 Trinity’s Revenues are More Diversified Than in the Past LTM 09/11 Total Consolidated Revenue was $2.8 billion Railcar Deliveries of 11,190 LTM 09/11 Total Consolidated Revenue was $2.8 billion Railcar Deliveries of 11,190 FY 2000 Total Consolidated Revenue was $2.7 billion Railcar Deliveries of 23,280 FY 2000 Total Consolidated Revenue was $2.7 billion Railcar Deliveries of 23,280 60% 5% 21% 6% 8% External Revenue Composition FY 2000 Rail Leasing CPG EEG Barge 25% 20% 20% 16% 19% External Revenue Composition LTM 09/30/11 Rail Leasing CPG EEG Barge |

7 Trinity is Well Positioned for All Economic Cycles Trinity has staying power, continually building strength during a down cycle and emerging with more opportunity for growth than when the cycle began Seasoned management team knows how to assess the market, proactively plan for cycles and address changes in economic conditions Manufacturing flexibility is a core competency, and when combined with our broad product offering allows us to pursue a wide range of orders Cost-effective manufacturing footprint in the Southern United States and Mexico is a competitive advantage for many of our product lines Shared synergies across business lines provide unique opportunities Trinity’s lease fleet of approximately 70,000 railcars (including TRIP) provides a strong strategic connection to our customers, as well as a long-term stream of profits and cash flows Strong liquidity position of approximately $810 million and solid balance sheet |

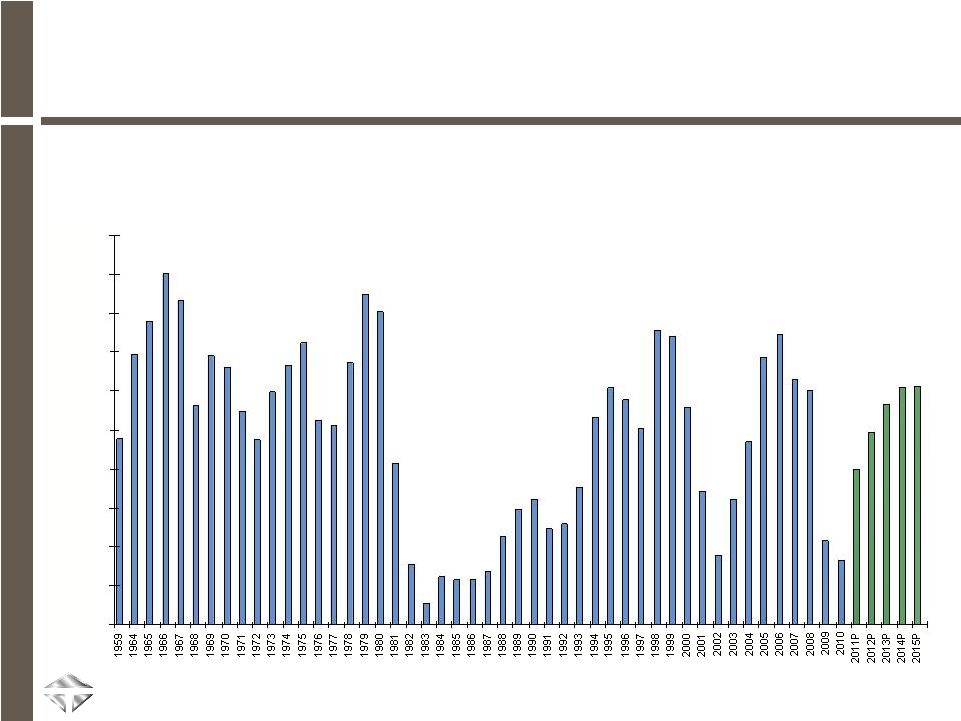

8 (1) Sources: Historical data as reported per the Railway Supply Institute. 2011-2015 projections are an average of estimates provided by Global Insight (08/11) and Economic Planning Associates, Inc. (10/11) and are provided as a point of reference. Railcar Deliveries (1959 – 2015P) Projections based on Third-Party estimates (1) Railcar Cycles Require Proactive Planning 0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000 100,000 |

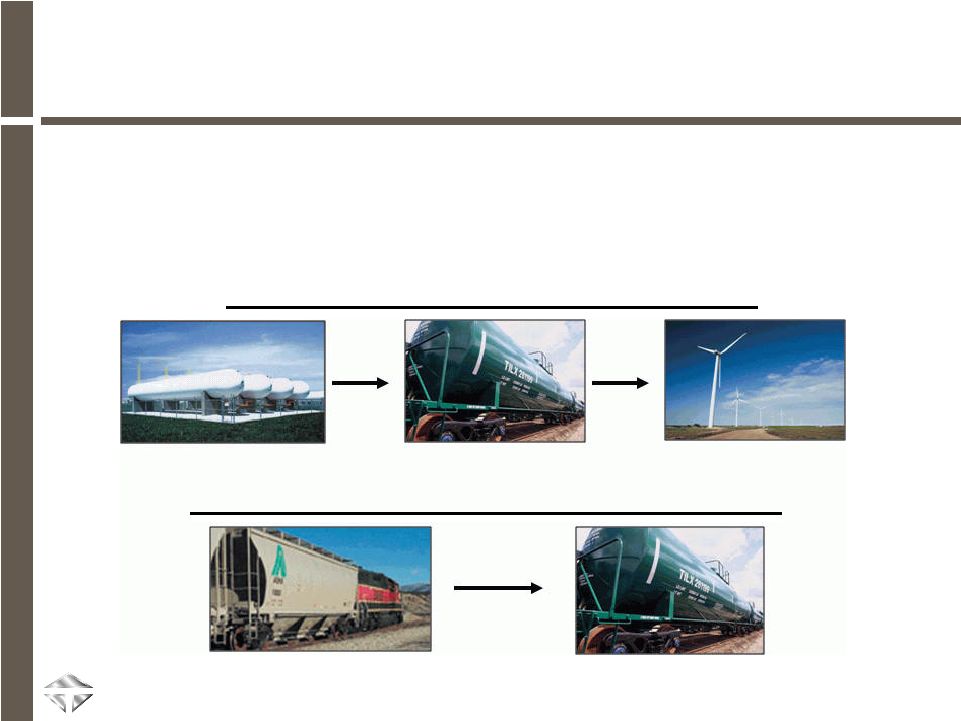

9 Trinity’s Manufacturing Flexibility is a Differentiator Trinity’s manufacturing flexibility enhances our opportunistic approach – We quickly respond to market changes and customer needs – Our resources are directed toward highest and best use Manufacturing flexibility across business lines Manufacturing flexibility across broad product lines |

10 Trinity Has an Excellent Competitive Position in Mexico More than five decades of in-country operating experience Trinity’s manufacturing capacity in Mexico continues to grow Provides benefits across multiple product lines Strong logistics network in place – approximately 990 truckloads crossing the border per month at the end of September 2011 |

11 Trinity’s Companies Have Continuous Synergistic Connections Trinity’s businesses place a high priority on collaborating with each other to continuously generate synergies that provide competitive benefits: INTERNALLY GENERATED SYNERGIES INTERNALLY GENERATED SYNERGIES Shared Best Practices in Manufacturing Technologies Internal Sourcing of Components & Sub- Assemblies Maximized Plant Efficiencies Centralized Cost Savings Optimization of Low Cost Facilities |

12 Trinity’s Railcar Leasing Company Provides Stability The growth of our railcar leasing business over the last decade has produced a consistent revenue and earnings base Trinity Industries Leasing Company (TILC), our wholly-owned leasing subsidiary, provides strategic benefits to our railcar manufacturing businesses in addition to its strong financial performance – In LTM 9/30/11, we added $215 million (net) of railcars to our TILC fleet, representing more than 5% year-over-year growth in units TILC also owns a 57% ownership interest in TRIP, a fleet of 14,600 railcars, which brings its total owned and managed fleet to approximately 70,000 railcars We have been very successful in renewing or remarketing cars in our fleet, which is reflected in our high utilization rates – TILC lease fleet utilization was 99.4% at September 30, 2011 – TRIP lease fleet utilization was 99.9% at September 30, 2011 Industry trends continue to show a large portion of new railcar orders are for leases, and we are positioned to take advantage of those orders |

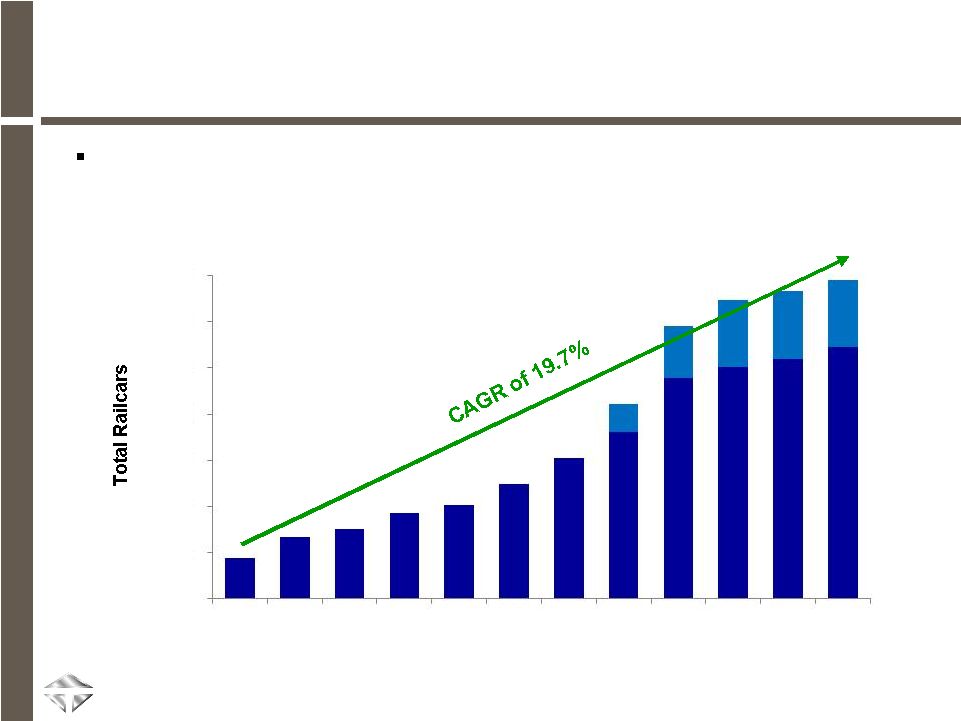

13 Trinity’s Railcar Lease Fleet has Grown Rapidly 8,700 cars 8,700 cars 69,045 cars 69,045 cars We have built a large fleet of young railcars with long-term leases – Our lease fleet provided an important base of revenues and earnings during the last downturn helping Trinity maintain profitability 3/10 3/10 10,000 20,000 30,000 40,000 50,000 60,000 70,000 3/00 12/01 12/02 12/03 12/04 12/05 12/06 12/07 12/08 12/09 12/10 9/11 TILC TRIP - |

14 Trinity’s Liquidity Position is Strong As of September 30, 2011: Unrestricted Cash and Cash Equivalents of $272.8 million Corporate Revolver availability of $342.4 million TILC Leasing Warehouse availability of $194.3 million Total available liquidity of approximately $810 million Corporate Revolver $425 million facility Matures October, 2016 No borrowings at 9/30/11 $82.6 million in Letters of Credit TILC Leasing Warehouse Facility $475 million facility Matures February, 2013 $280.7 million in borrowings at 9/30/11 |

15 Trinity’s Balance Sheet Remains Solid As of September 30, 2011: Unrestricted Cash and Cash Equivalents of $272.8 million Manufacturing/Corporate debt: – Subordinated Convertible Notes of $450 million; first call/put in 2018 Leasing debt (including TRIP): – Warehouse borrowings of $280.7 million; long-term financings of $2.3 billion including $913 million from TRIP (of which $2.2 billion in financings are non-recourse to Trinity) – Leasing assets have a net book value of $4.3 billion including TRIP – Total leasing debt to total equipment on lease of 61.5% (55.0% excluding TRIP); significant amount of unencumbered assets available for financing In July, completed the successful refinancing of TRIP’s $1.0 billion warehouse loan; refinancing executed on a non-recourse basis and included: – $857 million of medium and long term secured debt at an initial coupon of 5.4% – $175 million of three-year notes at a cash interest rate of 8% (yield step ups apply) – Trinity purchased a $112 million participation in the notes |

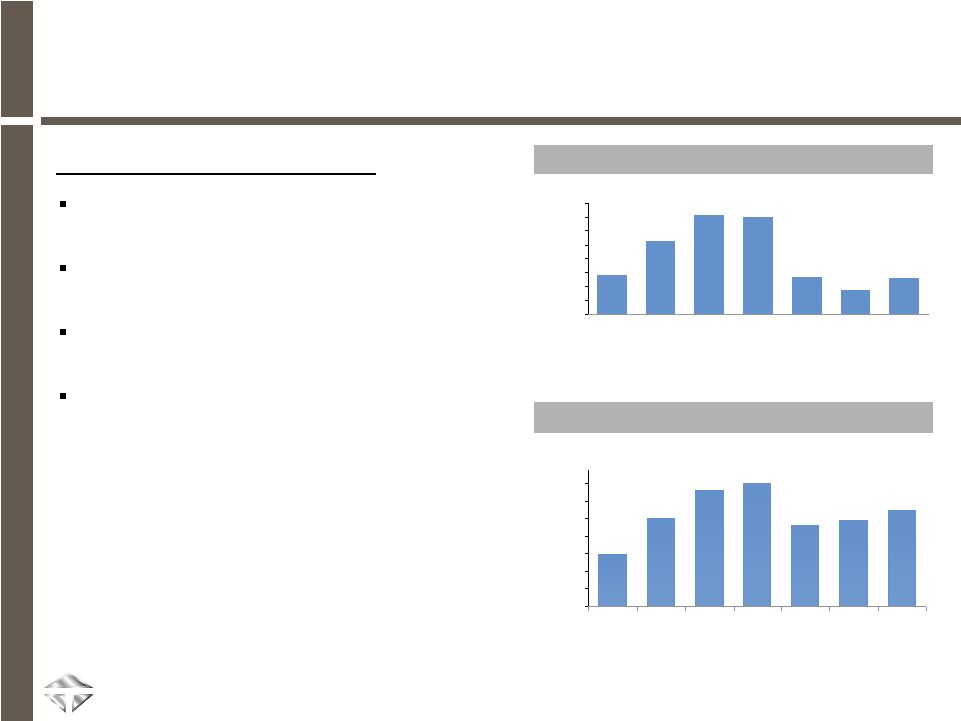

16 Trinity’s Recent Operating Results $1.42 $2.64 $3.55 $3.47 $0.85 $1.29 $1.33 $0.00 $0.50 $1.00 $1.50 $2.00 $2.50 $3.00 $3.50 $4.00 2005 2006 2007 2008 2009 2010(3) LTM 09/11 LTM as of September 30, 2011: Revenues increased 37.1% from $2.0 billion to $2.8 billion Operating profit increased by $58.6mm to $215.1mm (1) EBITDA increased 17.9% from $466.3mm to $549.8mm Earnings from continuing operations of $1.29 per diluted share ($mm) (3) (3) (3) (2) (2) Trinity’s Earnings Summary FY 2005 – LTM 9/30/11 Trinity’s EBITDA Summary FY 2005 – LTM 9/30/11 (4) $550 $295 $500 $658 $462 $704 $488 19.6% 17.9% 18.1% 17.2% 15.5% 10.9% 22.3% $0 $100 $200 $300 $400 $500 $600 $700 2005 2006 2007 2008 2009 2010 LTM 09/11 (1) Operating Profit includes Leasing External Interest Expense (2) Excludes $325mm pre-tax impact of impairment of Goodwill (3) Effective January 1, 2010, Trinity adopted a new accounting pronouncement requiring the inclusion of the financial position and results of operations of TRIP Rail Holdings and subsidiary in the consolidated financial statements of Trinity. Accordingly, the operating results of Trinity include TRIP Rail Holdings starting with the fiscal year ended December 31, 2010. Please refer to Note 1 in the Company’s Form 10-K for the fiscal year ended December 31, 2010 for further discussion. (4) See Note in Appendix pg. 24 for Reconciliation of EBITDA |

Appendix: Operating Business Summaries |

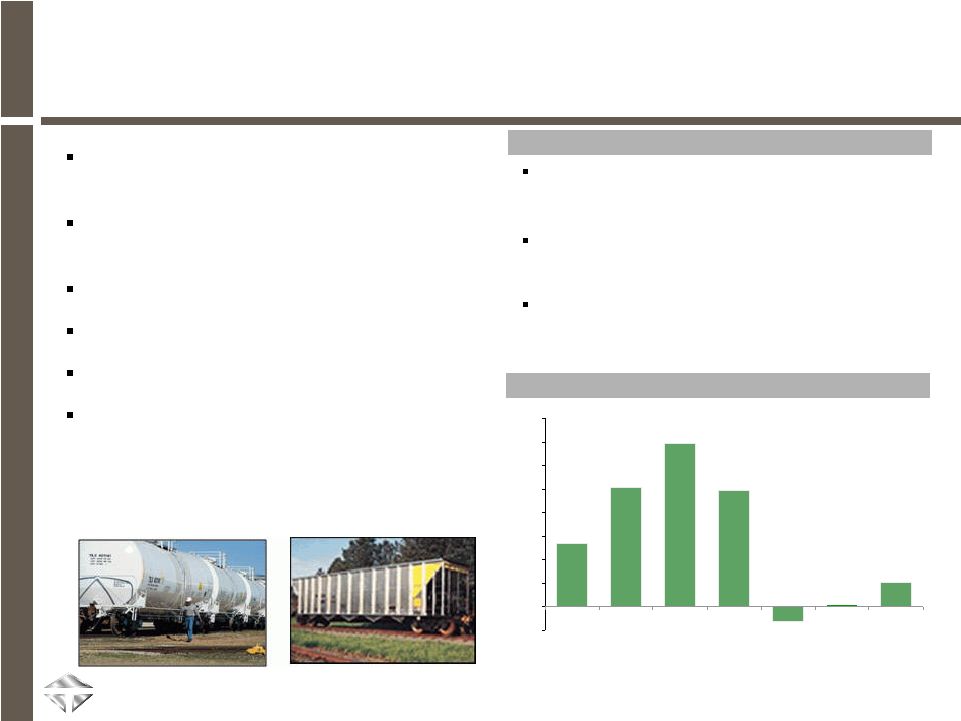

18 Trinity shipments totaled approximately 11,190 railcars representing 29% of industry shipments during LTM 9/30/11 Trinity orders totaled approximately 34,210 railcars representing 40% of the Industry total during LTM 9/30/11 Trinity’s order backlog was approximately 27,885 railcars representing 43% of industry backlog as of 9/30/11 $135.0 $253.9 $347.6 $247.7 $51.7 $1.5 ($30.9) 5.0% 0.3% 14.6% 9.7% 11.9% 7.4% -3.5% ($50) $0 $50 $100 $150 $200 $250 $300 $350 $400 2005 2006 2007 2008 2009 2010 LTM 09/11 Rail Group Leading manufacturer of railcars in North America Manufacturer of railcar axles and coupling devices in North America Focus on new and updated designs Centralized sourcing provides cost savings Streamlined manufacturing efficiencies Networking of customers between railcar sales and railcar leasing • Approximately 37% of the North American fleet is more than 25 years old (1) Before eliminations for Leasing and Intercompany Profit (2) Excludes $325mm charge for impairment of Goodwill ($mm) (2) (2) Rail Group Highlights Rail Group Historical Operating Profit/(Loss) & Margin (1) |

19 Railcar Leasing and Management Services Group Leading provider of comprehensive railcar leasing and management services Single point of contact for equipment and services Strengthens relationship with end-user of railcar Marketed with railcar sales activities as TrinityRail® Strategic Position Operating Benefits Financial Results Leasing complements product offering (one-stop shopping) Provides Trinity’s rail customers option to purchase or lease Ideal method for introduction of new products Assists in balancing and extending production lines Minimizes administrative issues Strategic fleet sales take advantage of market conditions Leasing provides attractive return on investment Minimizes cyclical exposure to company Revenue and cash flow diversification for Trinity ($mm) Note: Beginning in Q1 2010, TRIP Revenues and OP were consolidated with the Leasing Group Note: Beginning in Q1 2010, TRIP Revenues and OP were consolidated with the Leasing Group $235.3 $158.9 $161.2 $106.5 $55.8 $149.0 $207.0 42.9% 41.6% 28.4% 27.4% 35.1% 25.5% 29.7% $0 $50 $100 $150 $200 $250 $300 2005 2006 2007 2008 2009 2010 LTM 09/11 Operations Car Sales Leasing Group TRIP (1) Fleet Size 54,445 14,600 Average Age (in years) 6.4 4.1 Average Remaining Lease Term 3.5 3.3 Utilization Rate 99.4% 99.9% (1) TRIP Holdings is a majority-owned subsidiary of TILC that was formed in 2007 to provide railcar leasing and management services in North America. TILC’s ownership interest in TRIP Holdings is currently 57.1%. TILC manages and services the railcars for TRIP. (1) TRIP Holdings is a majority-owned subsidiary of TILC that was formed in 2007 to provide railcar leasing and management services in North America. TILC’s ownership interest in TRIP Holdings is currently 57.1%. TILC manages and services the railcars for TRIP. Trinity Leasing’s capabilities provide the following advantages: Leasing & Mgmt Services Historical Operating Profit & Margin Fleet Statistics (as of September 30, 2011) |

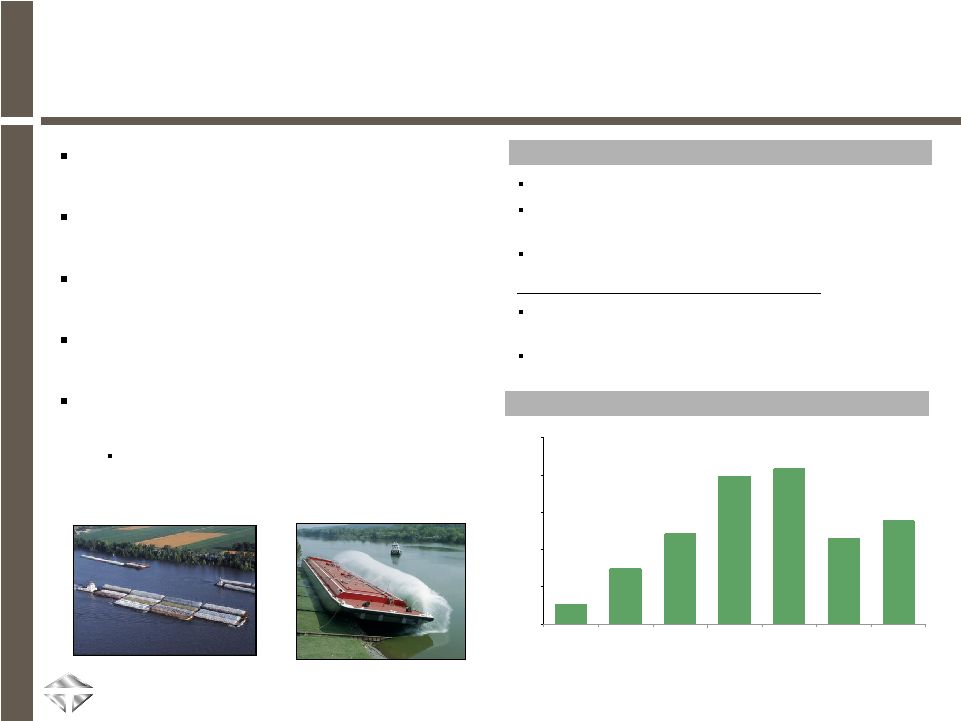

20 $15.7 $44.5 $72.6 $119.2 $125.2 $69.0 $83.6 15.9% 16.3% 23.7% 19.1% 14.7% 12.0% 6.5% $0 $30 $60 $90 $120 $150 2005 2006 2007 2008 2009 2010 LTM 09/11 Revenues up 26.4% in LTM 9/30/11 vs. LTM 9/30/10 Profitability remains high - Operating Profit margins increased from 6.5% in FY 2005 to 15.9% during LTM 9/30/11 Trinity backlog was $564mm at 9/30/11 4,120 out of 17,910 hopper barges, or approximately 23%, are 21+ years old 1,060 out of 3,010 tank barges, or approximately 35%, are 21+ years old Inland Barge Group Tank Barges Hopper Barges Transports grain & coal Transports liquids ($mm) Leading manufacturer of barges that transport goods through U.S. inland waterways Largest U.S. manufacturer of fiberglass barge covers Multiple barge manufacturing facilities on inland waterways enable rapid delivery Barge transportation has a cost advantage in high-cost fuel environments Over the past 10 years, 29% more barges were scrapped vs. built 9,674 scrapped vs. 7,495 built from 2000 - 2010 Leading manufacturer of barges that transport goods through U.S. inland waterways Largest U.S. manufacturer of fiberglass barge covers Multiple barge manufacturing facilities on inland waterways enable rapid delivery Barge transportation has a cost advantage in high-cost fuel environments Over the past 10 years, 29% more barges were scrapped vs. built 9,674 scrapped vs. 7,495 built from 2000 - 2010 (1) (1) Operating Profit includes a $5.1mm net gain as a result of flood damage to the Tennessee barge plant (1) Operating Profit includes a $5.1mm net gain as a result of flood damage to the Tennessee barge plant (2) (2) Operating Profit includes a $(2.5)mm net loss as a result of flood damage to the Tennessee and Missouri barge plants (2) Operating Profit includes a $(2.5)mm net loss as a result of flood damage to the Tennessee and Missouri barge plants Inland Barge Group Highlights Inland Barge Group Historical Operating Profit & Margin Replacement demand driver (as of 12/31/10): |

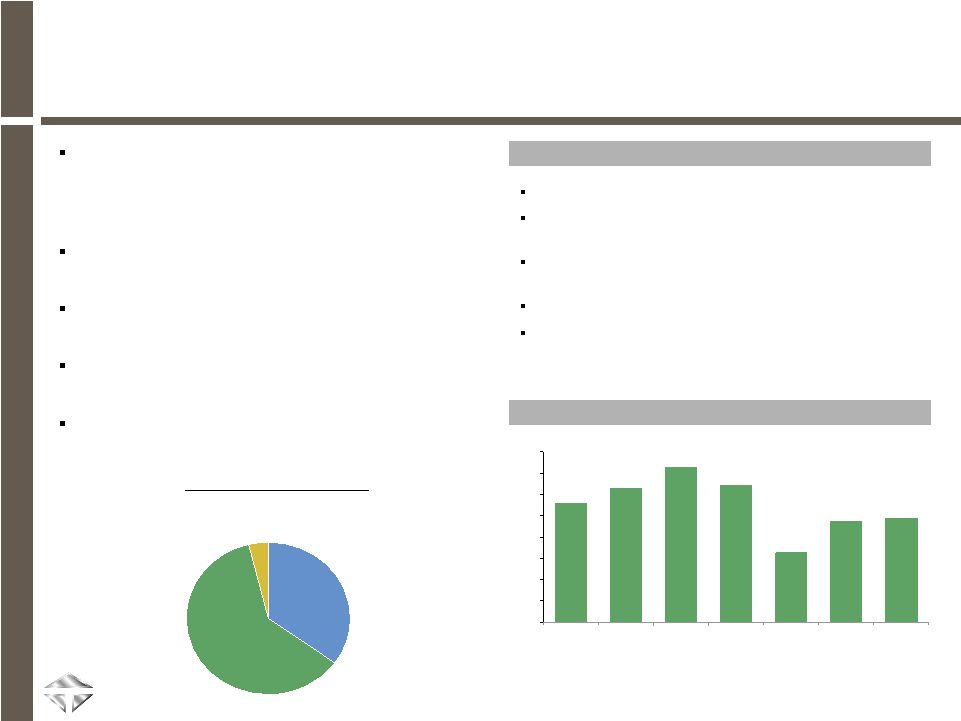

Concrete & Aggregates 35% Other 4% Highway Products 61% 21 $55.9 $62.8 $72.4 $64.2 $47.4 $48.9 $32.6 8.5% 8.2% 6.1% 8.7% 9.9% 9.0% 9.0% $0 $10 $20 $30 $40 $50 $60 $70 $80 2005 2006 2007 2008 2009 2010 LTM 09/11 Revenues increased 2.1% LTM 9/30/11 vs. LTM 9/30/10 Operating Profit increased 5.8% LTM 9/30/11 vs. LTM 9/30/10 Producer of Highway products for North America and other international markets Positioned in Texas with Concrete and Aggregates Consistent contributor to cash flow Construction Products Group Leading manufacturer of highway guardrail and crash cushions in the United States; plus a line of proprietary products including guardrail end treatments and cable barrier guardrail systems Leading Texas producer of concrete and aggregates Diversified exposure to commercial, residential, industrial, and highway markets Business has grown organically and through acquisitions Demand tied to construction projects and federal funding ($mm) Construction Products Group Highlights LTM 9/30/11 Revenue Mix Construction Products Group Historical Operating Profit & Margin |

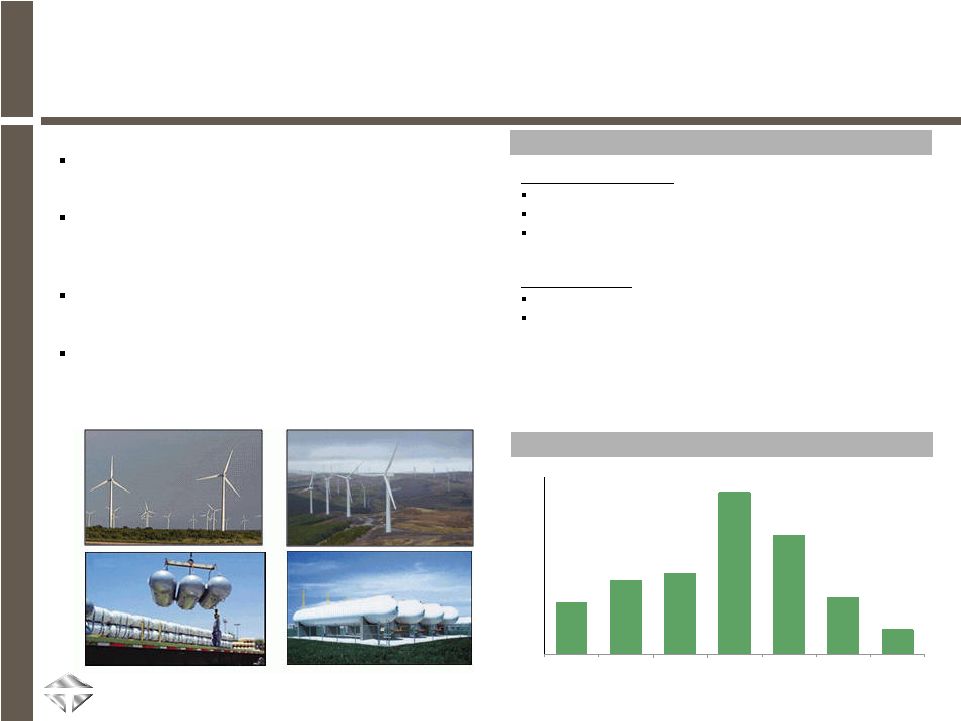

22 $31.9 $45.7 $50.1 $100.3 $35.1 $15.0 $73.8 3.3% 8.4% 14.5% 13.6% 15.9% 11.5% 13.6% $0 $10 $20 $30 $40 $50 $60 $70 $80 $90 $100 $110 2005 2006 2007 2008 2009 2010 LTM 9/11 Structural Wind Towers: Revenue of $242.4mm in LTM 9/30/11 Trinity’s backlog as of 9/30/11 was $930 million Plants are strategically located along the central corridor where the majority of wind farms are installed Tank Containers: Consistent and mature business Trinity has taken cost out of the business – Improved processes – Elimination of non-profitable products – Consolidated North American operations Energy Equipment Group Leading North American producer in structural wind tower business Leading producer of propane tanks, tank containers, and tank heads for pressure and non- pressure vessels in North America Low-cost operator with primary tank container production in Mexico facilities Synergies among products across multiple Trinity business groups ($mm) Energy Equipment Group Highlights Energy Equipment Group Historical Operating Profit |

2005 2006 2007 2008 2009 2010 LTM 9/11 Income (loss) from continuing operations $110.5 $212.6 $289.8 $282.4 ($137.5) $75.6 $107.5 Add: Interest expense 42.2 68.7 84.5 109.4 123.2 182.1 182.0 Provision/(Benefit) for income taxes 65.6 131.3 165.1 171.4 (9.4) 40.9 69.7 Depreciation & amortization expense 76.2 87.6 118.9 140.3 160.8 189.6 190.6 Goodwill impairment - - - - 325.0 - - Earnings from continuing operations before interest expense, income taxes, and depreciation and amortization expense $294.5 $500.2 $658.3 $703.5 $462.1 $488.2 $549.8 Reconciliation of EBITDA (1) Includes results of operations related to TRIP starting January 1, 2010 (1) Includes results of operations related to TRIP starting January 1, 2010 23 (1) (1) (1) (1) “EBITDA is defined as Income (loss) from continuing operations plus interest expense, income taxes, and depreciation and amortization expense including goodwill impairment charges. EBITDA is not a calculation based on generally accepted accounting principles. The amounts included in the EBITDA calculation, however, are derived from amounts included in the historical statements of operations data as adjusted for the adoption of accounting pronouncements. In addition, EBITDA should not be considered as an alternative to net income or operating income as an indicator of our operating performance, or as an alternative to operating cash flows as a measure of liquidity. We have reported EBITDA because we regularly review EBITDA as a measure of our ability to incur and service debt. In addition, we believe our debt holders utilize and analyze our EBITDA for similar purposes. We also believe EBITDA assists investors in comparing a company’s performance on a consistent basis without regard to depreciation and amortization, which can vary significantly depending upon many factors. However, the EBITDA measure presented in this press release may not always be comparable to similarly titled measures by other companies due to differences in the components of the calculation. |