Exhibit (c)(iv)

CONFIDENTIAL WORKING DRAFT—FOR DISCUSSION PURPOSES ONLY

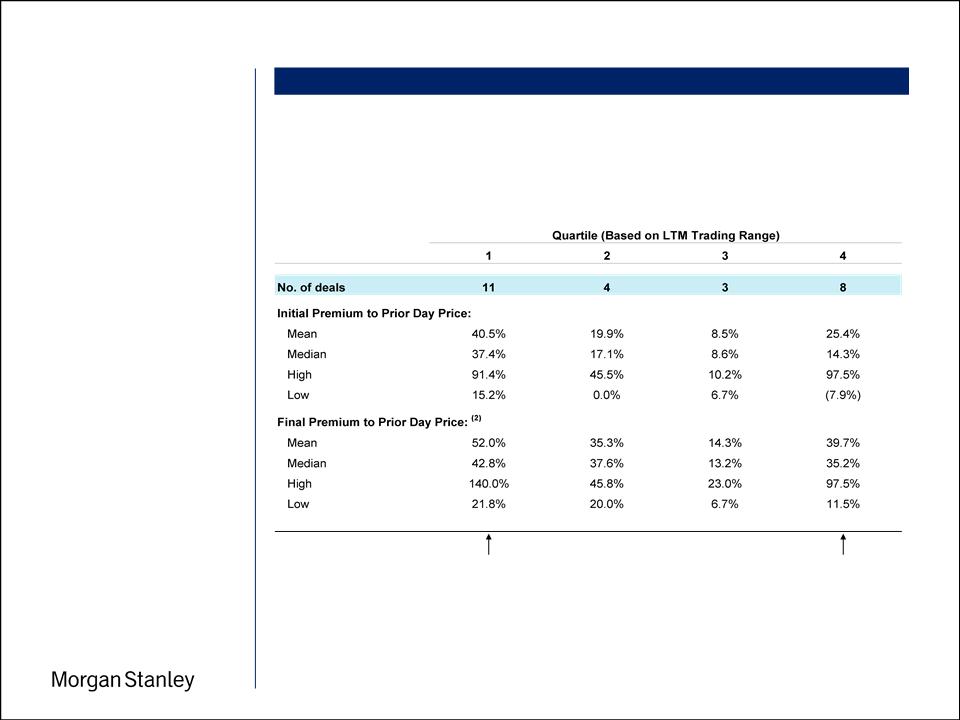

Implied Transaction Premiums vs. Stock Trading History

Project Celtic

1

• Analysis divides selected

precedents into quartiles based

on where the target’s stock was

trading relative to its 52-week

trading range, immediately prior

to announcement

precedents into quartiles based

on where the target’s stock was

trading relative to its 52-week

trading range, immediately prior

to announcement

Notes

1. Based on selected deals since 2001; all cash; US targets; minority buy-in value of $25 - $500MM; majority shareholder owned less than 90% of target

2. Final premium statistics exclude Hearst-Argyle transaction, which has not been completed

Minority Buy-in Precedents (1)

Source Public Filings, Press Releases, FactSet

Prior to announcement,

stock price was in bottom

quartile of 52 week

trading range

stock price was in bottom

quartile of 52 week

trading range

Prior to announcement,

stock price was in top

quartile of 52 week

trading range

stock price was in top

quartile of 52 week

trading range

Summary of Implied Transaction Premiums

CONFIDENTIAL WORKING DRAFT—FOR DISCUSSION PURPOSES ONLY

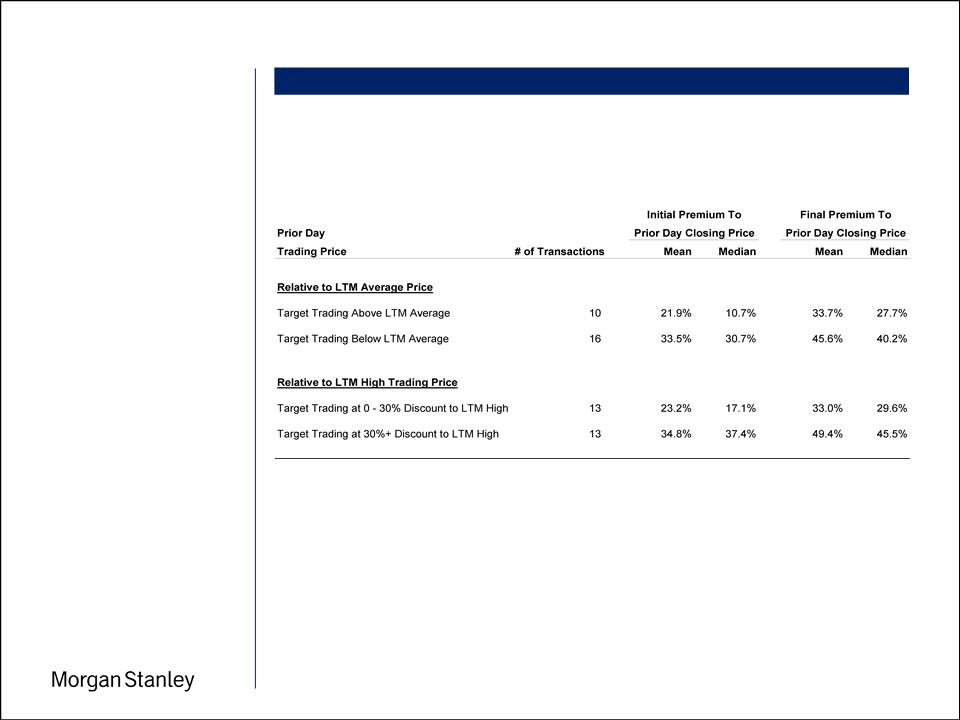

Implied Transaction Premiums vs. Stock Trading History (cont’d)

Project Celtic

2

Note

1. Based on selected deals since 2001; all cash; US targets; minority buy-in value of $25 - $500MM; majority shareholder owned less than 90% of target

Minority Buy-in Precedents (1)

Source Public Filings, Press Releases, FactSet

• Analysis evaluates premiums

paid in precedent transactions

based on where target was

trading relative to its LTM

average trading price and LTM

high trading price at the time a

transaction was announced

paid in precedent transactions

based on where target was

trading relative to its LTM

average trading price and LTM

high trading price at the time a

transaction was announced

Summary of Implied Transaction Premiums

CONFIDENTIAL WORKING DRAFT—FOR DISCUSSION PURPOSES ONLY

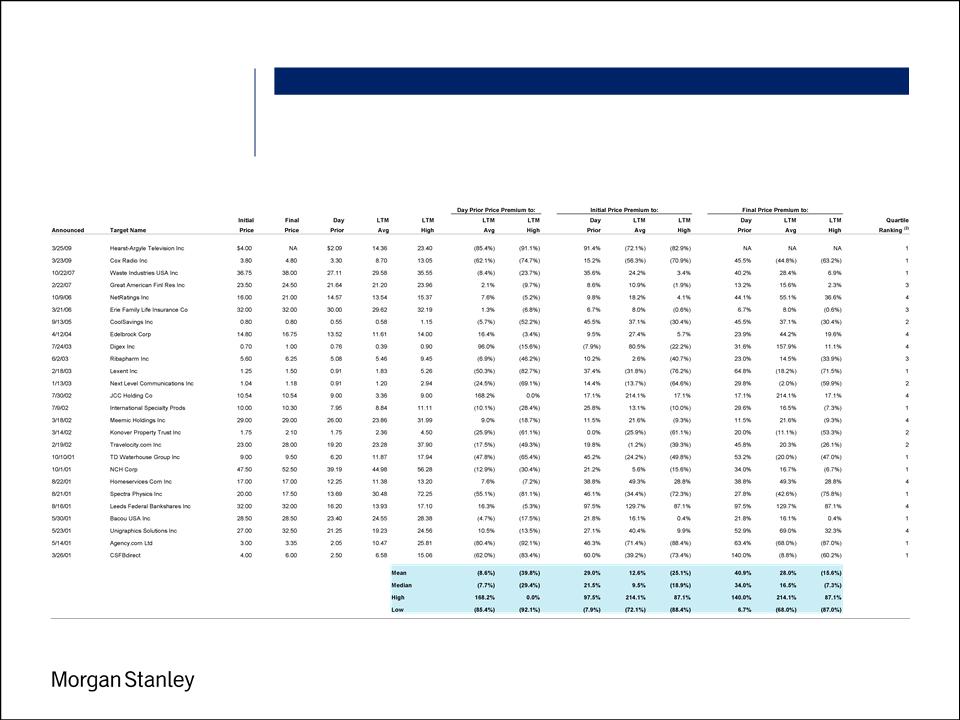

Minority Buy-in Precedents (1)

Project Celtic

3

Notes

1. Based on selected deals since 2001; all cash; US targets; minority buy-in value of $25 - $500MM; majority shareholder owned less than 90% of target

2. Ranking based on where target was trading relative to its 52-week trading range immediately prior to announcement

Selected Statistics

CONFIDENTIAL WORKING DRAFT—FOR DISCUSSION PURPOSES ONLY

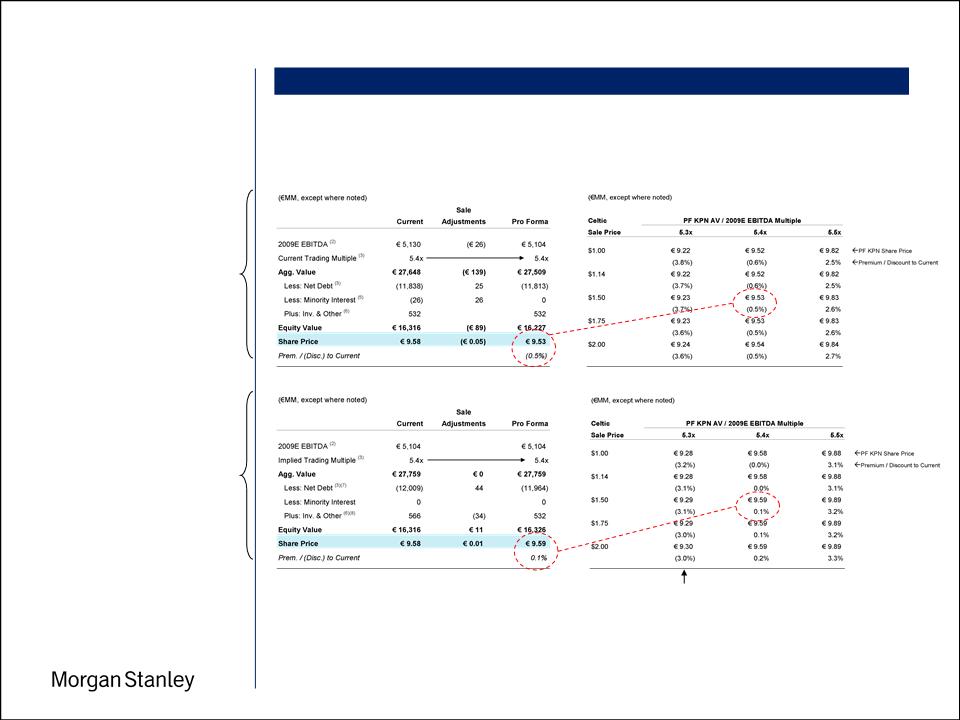

PF Share Price Sensitivity - Method B

PF Share Price Sensitivity - Method A

Pro Forma KPN Share Price - Method B

Pro Forma KPN Share Price - Method A

Source Wall Street Research, Public Filings

Hypothetical Sale of KPN’s Celtic Stake

Illustrative Pro Forma Value Impact to KPN (1)

Project Celtic

1

Notes

1. Illustrative analysis based on KPN share price of €9.58 and USD / EUR exchange rate of $1.36 as of 5/19/09

2. Current 2009E EBITDA as per Wall Street Research; Current EBITDA under Method B is reduced by Celtic’s 2009E EBITDA

3. Current AV / 2009E EBITDA multiple as of 5/19/09; balance sheet items as of 3/31/09 and also include unfunded pension liability as of 12/31/08

4. Adjustments are removal of €36MM Celtic cash and €16MM Celtic debt, with total KPN sale proceeds of €44MM assuming no tax impact

5. Represents market value of 44% minority ownership of Celtic as of 5/19/09

6. Represents KPN tax credit per Morgan Stanley Equity Research 4/20/09 and investments in associates at 3/31/09 book value (private companies)

7. Under Method B current net debt adjusted to remove €36MM of Celtic cash and €16MM of Celtic debt

8. Includes €34MM current market value of 56% KPN Celtic stake based on 5/19/09 share price of $1.14, which is removed for pro forma purposes

(4)

Current KPN Trading Multiple

Valuation Method A

• Assumes investors consolidate

Celtic and adjust for minority

interest when valuing KPN

Celtic and adjust for minority

interest when valuing KPN

– Sale adjustments include (a)

removing minority interest, (b)

deconsolidating Celtic’s net cash

position and EBITDA and (c)

including the proceeds from

selling Celtic

removing minority interest, (b)

deconsolidating Celtic’s net cash

position and EBITDA and (c)

including the proceeds from

selling Celtic

Valuation Method B

• Assumes investors treat Celtic as

an equity investment when valuing

KPN

an equity investment when valuing

KPN

– Sale adjustments include (a)

removing the value of the equity

investment and (b) adjusting net

debt to reflect the proceeds from

selling Celtic

removing the value of the equity

investment and (b) adjusting net

debt to reflect the proceeds from

selling Celtic

Constant Multiple

Constant Multiple