| UNITED STATES | ||

| SECURITIES AND EXCHANGE COMMISSION | ||

| Washington, D.C. 20549 | ||

| FORM N-CSR | ||

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED | ||

| MANAGEMENT INVESTMENT COMPANIES | ||

| Investment Company Act file number | 811-00816 | |

| AMERICAN CENTURY MUTUAL FUNDS, INC. | ||

| (Exact name of registrant as specified in charter) | ||

| 4500 MAIN STREET, KANSAS CITY, MISSOURI | 64111 | |

| (Address of principal executive offices) | (Zip Code) | |

| CHARLES A. ETHERINGTON | ||

| 4500 MAIN STREET, KANSAS CITY, MISSOURI 64111 | ||

| (Name and address of agent for service) | ||

| Registrant’s telephone number, including area code: | 816-531-5575 | |

| Date of fiscal year end: | 10-31 | |

| Date of reporting period: | 04-30-2010 | |

| ITEM 1. REPORTS TO STOCKHOLDERS. | |

| Semiannual Report | |

| April 30, 2010 | |

![]()

| American Century Investments® |

Balanced Fund

| Table of Contents |

| President’s Letter | 2 |

| Independent Chairman’s Letter | 3 |

| Market Perspective | 4 |

| U.S. Market Returns | 4 |

| Balanced | |

| Performance | 5 |

| Portfolio Commentary | 7 |

| Top Ten Stock Holdings | 9 |

| Top Five Stock Industries | 9 |

| Key Fixed-Income Portfolio Statistics | 9 |

| Types of Investments in Portfolio | 9 |

| Shareholder Fee Example | 10 |

| Financial Statements | |

| Schedule of Investments | 12 |

| Statement of Assets and Liabilities | 27 |

| Statement of Operations | 28 |

| Statement of Changes in Net Assets | 29 |

| Notes to Financial Statements | 30 |

| Financial Highlights | 37 |

| Other Information | |

| Board Approval of Management Agreements | 39 |

| Additional Information | 45 |

| Index Definitions | 46 |

Any opinions expressed in this report reflect those of the author as of the date of the report, and do not necessarily represent the opinions of American Century Investments or any other person in the American Century Investments organization. Any such opinions are subject to change at any time based upon market or other conditions and American Century Investments disclaims any responsibility to update such opinions. These opinions may not be relied upon as investment advice and, because investment decisions made by American Century Investments funds are based on numerous factors, may not be relied upon as an indication of trading intent on behalf of any American Century Investments fund. Security examples are used for representational purposes only and are not intended as recommendations to purchase or sell securities. Performance information for comparative indices and securities is provided to American Century Investments by third party vendors. To the best of American Century Investments’ knowledge, such information is accurate at the time of printing.

| President’s Letter |

Dear Investor:

To learn more about the capital markets, your investment, and the portfolio management strategies American Century Investments provides, we encourage you to review this shareholder report for the financial reporting period ended April 30, 2010.

On the following pages, you will find investment performance and portfolio information, presented with the expert perspective and commentary of our portfolio management team. This report remains one of our most important vehicles for conveying the information you need about your investment performance, and about the market factors and strategies that affect fund returns. For additional information on the markets, we encourage you to visit the “Insights & News” tab at our Web site, americancentury.com, for updates and further expert commentary.

The top of our Web site’s home page also provides a link to “Our Story,” which, first and foremost, outlines our commitment—since 1958—to helping clients reach their financial goals. We believe strongly that we will only be successful when our clients are successful. That’s who we are.

Another important, unique facet of our story and who we are is “Profits with a Purpose,” which describes our bond with the Stowers Institute for Medical Research (SIMR). SIMR is a world-class biomedical organization—founded by our company founder James E. Stowers, Jr. and his wife Virginia—that is dedicated to researching the causes, treatment, and prevention of gene-based diseases, including cancer. Through American Century Investments’ private ownership structure, more than 40% of our profits support SIMR.

Mr. Stowers’ example of achieving financial success and using that platform to help humanity motivates our entire American Century Investments team. His story inspires us to help each of our clients achieve success. Thank you for sharing your financial journey with us.

Sincerely,

Jonathan Thomas

President and Chief Executive Officer

American Century Investments

2

| Independent Chairman’s Letter |

Fellow Shareholders,

The principal event at a recent board meeting was the retirement of Jim Stowers, Jr. from the American Century Mutual Funds Kansas City board. This was one of those times when you felt like you were living a historical moment. Jim—who celebrated his 86th birthday in January—founded what was known as Twentieth Century Mutual Funds over 50 years ago. Through the years, his number one priority has been to “Put Investors First!” The board presented Jim with a resolution acknowledging that, by building a successful investment company, he has impacted the lives of many by helping them on the path to financial success.

We respect Jim’s decision to focus his energy on the Stowers Institute for Medical Research and American Century Companies, Inc. (ACC), the parent company of the funds’ investment advisors. The pioneering medical research that Jim and his wife Virginia have made possible through the Institute should enrich the lives of millions in the future.

Shortly after his retirement from the board, we received word that ACC’s co-chairman Richard W. Brown had succeeded Jim as trustee of a trust that holds a significant interest in ACC stock as part of Jim’s long-standing estate and business succession plan. While holding less than a majority interest, the trust is presumed to control the funds’ investment advisors under the Investment Company Act of 1940. This change triggered the need for a shareholder proxy to approve new management and subadvisory agreements for the funds. If you have not already responded, I encourage you to take the time to read the proxy materials and send your vote as soon as possible.

On behalf of the board, I want to once again thank Jim for his mutual fund board service. More than three years ago, Jim and Richard Brown installed a strong and effective leadership team at American Century Investments and I look forward to continuing to work with them on behalf of fund shareholders. And while Jim no longer sits on the fund board, the inherent optimism captured by his favorite catch phrase—“The best is yet to be”—still resonates with all of us who have the privilege of serving you. I invite you to send your comments, questions or concerns to me at dhpratt@fundboardchair.com.

3

| Market Perspective |

By Scott Wittman, Chief Investment Officer, Quantitative Equity and Asset Allocation

U.S. Stocks Continued to Advance

The U.S. stock market generated solid gains for the six months ended April 30, 2010, continuing the rally that began in early 2009. Improving economic conditions and unexpectedly strong corporate earnings were the key factors behind the market’s advance during the period.

Signs of improvement were evident across many segments of the economy during the six months—manufacturing activity picked up, consumer spending improved, and the unemployment rate began to fall after reaching a 26-year high in October 2009. Consequently, the U.S. economy generated positive growth in the second half of 2009—after more than a year of economic contraction—and this trend continued into early 2010.

In addition, corporate profits consistently exceeded expectations during the six-month period. Many companies implemented stringent cost-management programs that helped boost profit margins, allowing these businesses to generate surprisingly robust earnings growth despite stagnant revenues. Rising demand for delayed big-ticket purchases, such as cars and appliances, also contributed to stronger earnings.

The combination of better economic data and rising corporate profits helped the stock market advance steadily throughout the six-month period. Small- and mid-cap stocks generated the best results, outpacing large-cap shares (see the table below), while value-oriented issues outpaced growth across all market capitalizations.

Bonds Also Gained Ground

The U.S. bond market also advanced for the six months, though to a lesser degree than the equity market. The improving economic environment provided a lift to corporate securities, which were among the best performers in the bond market. Commercial mortgage-backed securities also generated strong returns as credit conditions in the commercial property sector improved markedly.

Residential mortgage-backed securities lagged as delinquencies and foreclosures continued to increase and the Federal Reserve ended its program of buying mortgage securities to support the housing market. Treasury bonds also underperformed as increased issuance to fund a widening fiscal deficit led to higher yields in the Treasury market. Although the improved economic environment was also a negative factor for Treasury securities, this was offset to a large degree by a lack of inflationary pressures as inflation remained at relatively low levels.

| U.S. Market Returns | ||||

| For the six months ended April 30, 2010* | ||||

| Stock Indices | Barclays Capital U.S. Bond Market Indices | |||

| Russell 1000 Index (large-cap) | 16.77% | Aggregate | 2.54% | |

| Russell Midcap Index | 24.93% | Corporate Investment-Grade | 4.83% | |

| Russell 2000 Index (small-cap) | 28.17% | Mortgage (mortgage-backed) | 2.01% | |

| Agencies | 1.54% | |||

| *Total returns for periods less than one year are not annualized. | Treasury | 0.89% | ||

4

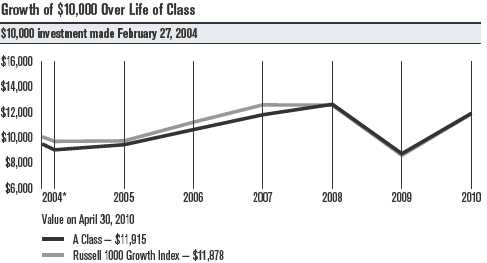

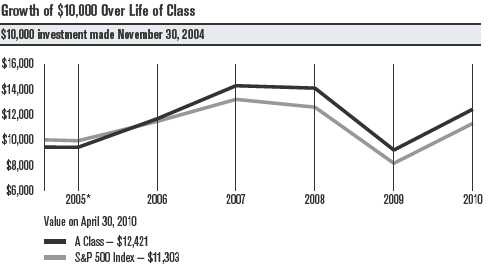

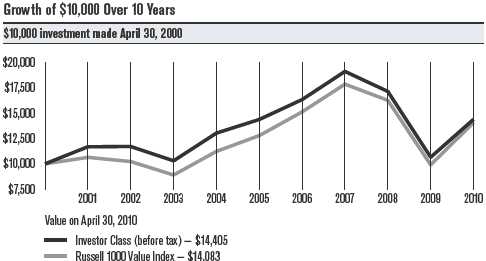

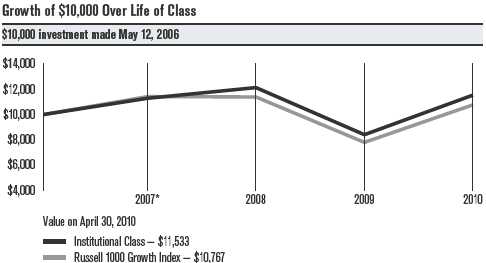

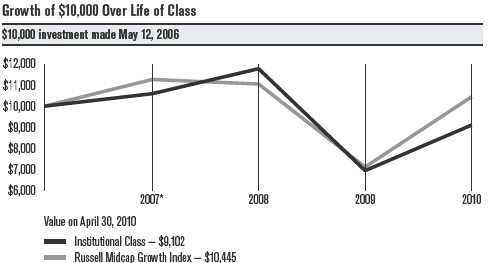

| Performance |

| Balanced | ||||||||

| Total Returns as of April 30, 2010 | ||||||||

| Average Annual Returns | ||||||||

| Ticker | Since | Inception | ||||||

| Symbol | 6 months(1) | 1 year | 5 years | 10 years | Inception | Date | ||

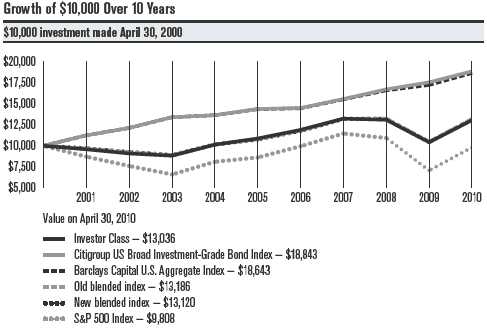

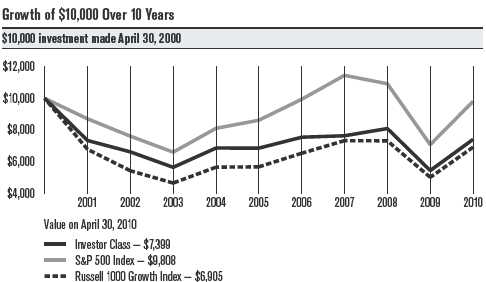

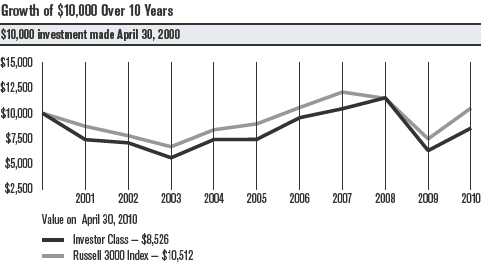

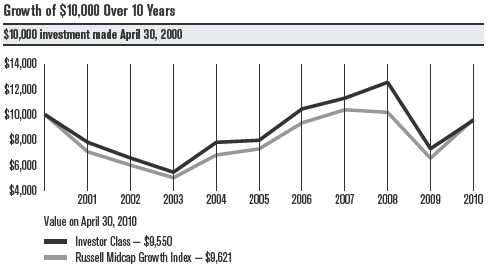

| Investor Class | TWBIX | 10.07% | 25.14% | 3.70% | 2.69% | 7.77% | 10/20/88 | |

| New blended index(2)(4) | — | 10.36% | 25.97% | 4.04% | 2.75% | 8.80%(3) | — | |

| Old blended index(2) | — | 10.19% | 25.58% | 4.14% | 2.80% | 8.84%(3) | — | |

| S&P 500 Index(5) | — | 15.66% | 38.84% | 2.63% | -0.19% | 9.36%(3) | — | |

| Barclays Capital U.S. | ||||||||

| Aggregate Index(4) | — | 2.54% | 8.30% | 5.38% | 6.43% | 7.27%(3) | — | |

| Citigroup US Broad | ||||||||

| Investment-Grade | ||||||||

| Bond Index | — | 2.14% | 7.44% | 5.57% | 6.54% | 7.34%(3) | — | |

| Institutional Class | ABINX | 10.18% | 25.48% | 3.92% | — | 2.82% | 5/1/00 | |

| (1) | Total returns for periods less than one year are not annualized. | |||||||

| (2) | See Index Definitions pages. | |||||||

| (3) | Since 10/31/88, the date nearest the Investor Class’s inception for which data are available. | |||||||

| (4) | In January 2010, the fund’s blended index changed. The old blended index was represented by 60% of the S&P 500 Index and the remaining | |||||||

| 40% was represented by the Citigroup US Broad Investment-Grade Bond Index. The new blended index is represented by 60% of the S&P 500 | ||||||||

| Index and the remaining 40% is represented by the Barclays Capital U.S. Aggregate Index. This reflects a change in the portfolio management | ||||||||

| analytics software used by American Century Investments’ fixed-income teams. The investment process is unchanged. | ||||||||

| (5) | Data provided by Lipper Inc. – A Reuters Company. © 2010 Reuters. All rights reserved. Any copying, republication or redistribution of Lipper | |||||||

| content, including by caching, framing or similar means, is expressly prohibited without the prior written consent of Lipper. Lipper shall not be | ||||||||

| liable for any errors or delays in the content, or for any actions taken in reliance thereon. | ||||||||

| The data contained herein has been obtained from company reports, financial reporting services, periodicals and other resources believed to be | ||||||||

| reliable. Although carefully verified, data on compilations is not guaranteed by Lipper and may be incomplete. No offer or solicitations to buy or | ||||||||

| sell any of the securities herein is being made by Lipper. | ||||||||

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. As interest rates rise, bond values will decline.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the indices are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the indices do not.

5

Balanced

| Total Annual Fund Operating Expenses | |

| Investor Class | Institutional Class |

| 0.91% | 0.71% |

The total annual fund operating expenses shown is as stated in the fund’s prospectus current as of the date of this report. The prospectus may vary from the expense ratio shown elsewhere in this report because it is based on a different time period, includes acquired fund fees and expenses, and, if applicable, does not include fee waivers or expense reimbursements.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. As interest rates rise, bond values will decline.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the indices are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the indices do not.

6

| Portfolio Commentary |

Balanced

Equity Portfolio Managers: Bill Martin and Tom Vaiana

Fixed-Income Portfolio Managers: Dave MacEwen, Bob Gahagan, and Brian Howell

Performance Summary

Balanced returned 10.07%* for the six months ended April 30, 2010, compared with the 10.36% return of its benchmark (a blended index consisting of 60% S&P 500 Index and 40% Barclays Capital U.S. Aggregate Index). Please note that the Barclays Capital U.S. Aggregate Index replaced the Citigroup US Broad Investment-Grade Bond Index in the benchmark. This reflects a change in the portfolio management analytics system used by American Century Investments’ fixed-income team.

The double-digit gains for the fund and its benchmark reflected the positive performance in both the stock and bond markets during the six-month period. Stocks generated the best returns, advancing steadily throughout the period as the economic and earnings environment improved. Bonds posted more modest gains as the stronger economy led to slightly higher interest rates.

The fund’s return for the period was just behind the performance of its benchmark. Both the equity and fixed-income portions of the portfolio produced returns that were roughly in line with their respective benchmarks. (It’s worth noting that the fund’s results reflected operating expenses, while the benchmark’s return did not.)

Stock Component Posted Double-Digit Return

The S&P 500 delivered a gain of more than 15% for the reporting period, and so did the stock portion of the Balanced fund. Individual stock selection is typically the main driver of performance in the stock component, and stock selection added value in seven of ten market sectors during the six-month period, led by materials and consumer staples.

The outperformance in the materials sector resulted primarily from stock choices among chemicals producers. The leading contributor was Terra Industries, which produces fertilizer and other agricultural chemicals. After competitor CF Industries Holdings gave up on its year-long effort to take over the company, Terra agreed to a buyout from a Norwegian fertilizer company. In the consumer staples sector, stock selection among beverage makers and an underweight position in food and staples retailers contributed the bulk of the outperformance. The top contributor was Coca-Cola Enterprises, the largest North American bottler of Coca-Cola products, which was acquired by Coca-Cola during the period.

Other notable positive performers included auto parts maker TRW Automotive, online movie rental firm Netflix, and medical technology company Millipore. TRW Automotive reported robust earnings during the period thanks to improving demand and a lower cost structure; Netflix rallied as subscriber growth exceeded expectations and movie streaming activity increased; and Millipore agreed to be acquired by a German pharmaceutical company.

*All fund returns referenced in this commentary are for Investor Class shares. Total returns for periods less than one year are not annualized.

7

Balanced

On the downside, stock selection in the financials sector had the biggest negative impact on relative results. Stock selection and an overweight position in capital markets firms were responsible for much of the under-performance in this sector. Several of the fund’s holdings in this segment were weighed down by uncertainty surrounding the federal government’s regulatory overhaul of the financial industry. Examples included investment bank Goldman Sachs, which also fell in response to a fraud lawsuit brought by the Securities and Exchange Commission, and asset manager BlackRock.

Bond Portion Fared Well

The fixed-income component of the portfolio kept pace with the Barclays Capital U.S. Aggregate Index for the six-month period. The portfolio is managed with a relative value focus, and our sector allocation reflected this approach. The fund held an underweight position in Treasury bonds, where yields were at historically low levels and growing budget deficits resulted in increased issuance. At the same time, we held an overweight position in high-quality corporate bonds, which were trading at attractive levels relative to Treasury securities. This positioning paid off as Treasury bonds underperformed during the period and corporate bonds were among the best performers.

The fund also benefited from its exposure to Treasury inflation-protected securities (TIPS), which outperformed for the six months. In addition, we continued to favor commercial mortgage-backed securities and mortgage-backed bonds issued by non-government agencies over agency-issued mortgage securities. Agency mortgage-backed securities offered little yield advantage over Treasury bonds, and the Federal Reserve ended its explicit support of this market segment in early 2010.

The fund’s positioning for a flatter yield curve (a narrower gap between long- and short-term interest rates) weighed on results as the spread between long- and short-term yields was little changed, remaining near historically wide levels.

A Look Ahead

The U.S. economy appears to be on the road to recovery, but headwinds and uncertainty remain. Consumers still face persistently high unemployment levels and significant debt burdens, while the stress resulting from sovereign debt issues in Europe have called into question the ability of the global economy to sustain its current pace of recovery. We will continue to focus on our disciplined investment processes for both the equity and fixed-income components of the portfolio.

8

| Balanced | ||

| Top Ten Stock Holdings as of April 30, 2010 | ||

| % of equity holdings | % of S&P 500 Index | |

| Exxon Mobil Corp. | 3.2% | 3.0% |

| Apple, Inc. | 2.4% | 2.2% |

| Johnson & Johnson | 2.2% | 1.7% |

| International Business Machines Corp. | 2.1% | 1.6% |

| JPMorgan Chase & Co. | 2.1% | 1.6% |

| Microsoft Corp. | 2.0% | 2.2% |

| Bank of America Corp. | 2.0% | 1.7% |

| Procter & Gamble Co. (The) | 1.6% | 1.7% |

| AT&T, Inc. | 1.6% | 1.4% |

| Wells Fargo & Co. | 1.5% | 1.6% |

| Top Five Stock Industries as of April 30, 2010 | ||

| % of equity holdings | % of S&P 500 Index | |

| Oil, Gas & Consumable Fuels | 8.6% | 9.4% |

| Pharmaceuticals | 5.0% | 5.8% |

| Computers & Peripherals | 4.9% | 4.4% |

| Insurance | 4.5% | 3.8% |

| Diversified Financial Services | 4.4% | 4.6% |

| Key Fixed-Income Portfolio Statistics | ||

| As of 4/30/10 | ||

| Weighted Average Life | 6.4 years | |

| Average Duration (Effective) | 4.8 years | |

| Types of Investments in Portfolio | ||

| % of fund investments | ||

| as of 4/30/10 | ||

| Common Stocks | 60.4% | |

| Mortgage-Backed Securities | 12.5% | |

| U.S. Treasury Securities | 11.4% | |

| Corporate Bonds | 10.6% | |

| U.S. Government Agency Securities and Equivalents | 3.5% | |

| Municipal Securities | 0.6% | |

| Sovereign Governments & Agencies | 0.2% | |

| Asset-Backed Securities | —(1) | |

| Temporary Cash Investments | 0.8% | |

| (1) Category is less than 0.05% of total net assets. | ||

9

| Shareholder Fee Example (Unaudited) |

Fund shareholders may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and redemption/ exchange fees; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in your fund and to compare these costs with the ongoing cost of investing in other mutual funds.

The example is based on an investment of $1,000 made at the beginning of the period and held for the entire period from November 1, 2009 to April 30, 2010.

Actual Expenses

The table provides information about actual account values and actual expenses for each class. You may use the information, together with the amount you invested, to estimate the expenses that you paid over the period. First, identify the share class you own. Then simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

If you hold Investor Class shares of any American Century Investments fund, or Institutional Class shares of the American Century Diversified Bond Fund, in an American Century Investments account (i.e., not a financial intermediary or retirement plan account), American Century Investments may charge you a $12.50 semiannual account maintenance fee if the value of those shares is less than $10,000. We will redeem shares automatically in one of your accounts to pay the $12.50 fee. In determining your total eligible investment amount, we will include your investments in all personal accounts (including American Century Investments Brokerage accounts) registered under your Social Security number. Personal accounts include individual accounts, joint accounts, UGMA/UTMA accounts, personal trusts, Coverdell Education Savings Accounts and IRAs (including traditional, Roth, Rollover, SEP-, SARSEP- and SIMPLE-IRAs), and certain other retirement accounts. If you have only business, business retirement, employer-sponsored or American Century Investments Brokerage accounts, you are currently not subject to this fee. We will not charge the fee as long as you choose to manage your accounts exclusively online. If you are subject to the Account Maintenance Fee, your account value could be reduced by the fee amount.

Hypothetical Example for Comparison Purposes

The table also provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio of each class of your fund and an assumed rate of return of 5% per year before expenses, which is not the actual return of a fund’s share class. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

10

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption/exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning | Ending | Expenses Paid | ||

| Account Value | Account Value | During Period* | Annualized | |

| 11/1/09 | 4/30/10 | 11/1/09 – 4/30/10 | Expense Ratio* | |

| Actual | ||||

| Investor Class | $1,000 | $1,100.70 | $4.69 | 0.90% |

| Institutional Class | $1,000 | $1,101.80 | $3.65 | 0.70% |

| Hypothetical | ||||

| Investor Class | $1,000 | $1,020.33 | $4.51 | 0.90% |

| Institutional Class | $1,000 | $1,021.32 | $3.51 | 0.70% |

| *Expenses are equal to the class’s annualized expense ratio listed in the table above, multiplied by the average account value over the period, | ||||

| multiplied by 181, the number of days in the most recent fiscal half-year, divided by 365, to reflect the one-half year period. | ||||

11

| Schedule of Investments |

| Balanced | ||||||

| APRIL 30, 2010 (UNAUDITED) | ||||||

| Shares/ | Shares/ | |||||

| Principal | Principal | |||||

| Amount | Value | Amount | Value | |||

| Common Stocks — 60.3% | Legg Mason, Inc. | 3,715 | $ 117,728 | |||

| AEROSPACE & DEFENSE — 1.2% | Morgan Stanley | 22,897 | 691,947 | |||

| Boeing Co. (The) | 31,125 | $ 2,254,384 | 6,888,687 | |||

| L-3 Communications | CHEMICALS — 1.4% | |||||

| Holdings, Inc. | 7,333 | 686,149 | Ashland, Inc. | 10,258 | 610,966 | |

| Northrop Grumman Corp. | 10,341 | 701,430 | Cabot Corp. | 14,783 | 481,039 | |

| Raytheon Co. | 40,574 | 2,365,464 | CF Industries Holdings, Inc. | 14,534 | 1,216,060 | |

| 6,007,427 | Huntsman Corp. | 95,824 | 1,093,352 | |||

| AIR FREIGHT & LOGISTICS — 0.6% | Lubrizol Corp. | 22,087 | 1,995,339 | |||

| C.H. Robinson Worldwide, Inc. | 3,316 | 199,955 | OM Group, Inc.(1) | 21,134 | 797,808 | |

| FedEx Corp. | 8,757 | 788,218 | Valspar Corp. | 14,655 | 458,995 | |

| United Parcel Service, Inc., | W.R. Grace & Co.(1) | 6,201 | 179,147 | |||

| Class B | 28,139 | 1,945,530 | 6,832,706 | |||

| 2,933,703 | COMMERCIAL BANKS — 2.2% | |||||

| AIRLINES — 0.1% | Bank of Hawaii Corp. | 13,749 | 727,047 | |||

| Southwest Airlines Co. | 25,297 | 333,414 | BB&T Corp. | 2,615 | 86,923 | |

| AUTO COMPONENTS — 0.4% | Canadian Imperial | |||||

| Gentex Corp. | 15,439 | 331,784 | Bank of Commerce | 309 | 22,671 | |

| TRW Automotive | CapitalSource, Inc. | 25,675 | 153,280 | |||

| Holdings Corp.(1) | 46,927 | 1,511,519 | Cathay General Bancorp. | 8,728 | 107,965 | |

| 1,843,303 | Fifth Third Bancorp. | 8,853 | 131,998 | |||

| BEVERAGES — 0.4% | First Horizon National Corp.(1) | 10,514 | 148,773 | |||

| Coca-Cola Co. (The) | 7,131 | 381,152 | Huntington Bancshares, Inc. | 100,510 | 680,453 | |

| Coca-Cola Enterprises, Inc. | 67,294 | 1,866,063 | KeyCorp | 28,583 | 257,819 | |

| 2,247,215 | Marshall & Ilsley Corp. | 14,583 | 132,705 | |||

| BIOTECHNOLOGY — 1.7% | PNC Financial Services | |||||

| Amgen, Inc.(1) | 62,030 | 3,558,041 | Group, Inc. | 13,769 | 925,414 | |

| Biogen Idec, Inc.(1) | 31,815 | 1,694,149 | Regions Financial Corp. | 14,529 | 128,436 | |

| Cephalon, Inc.(1) | 20,886 | 1,340,881 | Synovus Financial Corp. | 35,322 | 106,319 | |

| Cubist Pharmaceuticals, Inc.(1) | 19,023 | 426,496 | TCF Financial Corp. | 6,423 | 119,661 | |

| Gilead Sciences, Inc.(1) | 33,187 | 1,316,528 | Toronto-Dominion Bank (The) | 12,969 | 965,672 | |

| 8,336,095 | U.S. Bancorp. | 38,987 | 1,043,682 | |||

| CAPITAL MARKETS — 1.4% | Wells Fargo & Co. | 138,885 | 4,598,482 | |||

| Apollo Investment Corp. | 9,604 | 116,785 | Wilmington Trust Corp. | 5,712 | 98,989 | |

| Bank of New York Mellon | Zions Bancorp. | 23,398 | 672,225 | |||

| Corp. (The) | 48,512 | 1,510,179 | 11,108,514 | |||

| BlackRock, Inc. | 4,271 | 785,864 | COMMERCIAL SERVICES & SUPPLIES — 0.1% | |||

| Blackstone Group LP (The) | 6,210 | 86,816 | R.R. Donnelley & Sons Co. | 17,740 | 381,233 | |

| E*TRADE Financial Corp.(1) | 52,287 | 87,842 | Waste Management, Inc. | 2,370 | 82,191 | |

| Fortress Investment | 463,424 | |||||

| Group LLC, Class A(1) | 13,418 | 63,735 | COMMUNICATIONS EQUIPMENT — 1.8% | |||

| Goldman Sachs | ADC Telecommunications, | |||||

| Group, Inc. (The) | 22,956 | 3,333,211 | Inc.(1) | 61,847 | 495,395 | |

| Investment Technology | Arris Group, Inc.(1) | 36,508 | 448,683 | |||

| Group, Inc.(1) | 5,445 | 94,580 | ||||

12

| Balanced | ||||||

| Shares/ | Shares/ | |||||

| Principal | Principal | |||||

| Amount | Value | Amount | Value | |||

| Cisco Systems, Inc.(1) | 160,522 | $ 4,321,252 | DIVERSIFIED TELECOMMUNICATION | |||

| CommScope, Inc.(1) | 12,819 | 417,643 | SERVICES — 1.3% | |||

| Harris Corp. | 5,914 | 304,453 | AT&T, Inc. | 180,438 | $ 4,702,214 | |

| Plantronics, Inc. | 12,196 | 404,907 | Verizon Communications, Inc. | 58,076 | 1,677,816 | |

| QUALCOMM, Inc. | 42,438 | 1,644,048 | 6,380,030 | |||

| Research In Motion Ltd.(1) | 6,713 | 477,899 | ELECTRIC UTILITIES — 0.5% | |||

| Tellabs, Inc. | 34,467 | 312,960 | Entergy Corp. | 4,689 | 381,169 | |

| 8,827,240 | Exelon Corp. | 16,640 | 725,337 | |||

| COMPUTERS & PERIPHERALS — 2.9% | FPL Group, Inc. | 23,239 | 1,209,590 | |||

| Apple, Inc.(1) | 27,644 | 7,218,401 | 2,316,096 | |||

| ELECTRONIC EQUIPMENT, INSTRUMENTS & | ||||||

| Diebold, Inc. | 8,768 | 274,877 | COMPONENTS — 1.1% | |||

| EMC Corp.(1) | 31,483 | 598,492 | ||||

| Anixter International, Inc.(1) | 8,244 | 431,986 | ||||

| Hewlett-Packard Co. | 29,624 | 1,539,559 | Arrow Electronics, Inc.(1) | 37,901 | 1,155,981 | |

| Lexmark International, Inc., | Avnet, Inc.(1) | 12,938 | 413,628 | |||

| Class A(1) | 15,102 | 559,529 | ||||

| Celestica, Inc.(1) | 83,759 | 820,838 | ||||

| SanDisk Corp.(1) | 31,290 | 1,248,158 | ||||

| Seagate Technology(1) | 80,613 | 1,480,861 | Molex, Inc. | 3,254 | 72,922 | |

| Tech Data Corp.(1) | 17,295 | 741,955 | ||||

| Synaptics, Inc.(1) | 9,046 | 276,989 | ||||

| Western Digital Corp.(1) | 37,076 | 1,523,453 | Tyco Electronics Ltd. | 52,724 | 1,693,495 | |

| Vishay Intertechnology, Inc.(1) | 8,829 | 91,910 | ||||

| 14,720,319 | ||||||

| CONSTRUCTION & ENGINEERING — 0.5% | 5,422,715 | |||||

| EMCOR Group, Inc.(1) | 45,994 | 1,313,589 | ENERGY EQUIPMENT & SERVICES — 0.9% | |||

| Complete Production | ||||||

| Shaw Group, Inc. (The)(1) | 19,322 | 739,646 | Services, Inc.(1) | 29,703 | 448,218 | |

| URS Corp.(1) | 6,518 | 334,699 | Helix Energy Solutions | |||

| 2,387,934 | Group, Inc.(1) | 294 | 4,286 | |||

| CONSUMER FINANCE — 0.4% | National Oilwell Varco, Inc. | 40,764 | 1,794,839 | |||

| American Express Co. | 12,802 | 590,428 | Noble Corp.(1) | 1,298 | 51,258 | |

| AmeriCredit Corp.(1) | 11,548 | 276,459 | Oil States International, Inc.(1) | 21,241 | 1,026,153 | |

| Cash America | Schlumberger Ltd. | 15,066 | 1,076,014 | |||

| International, Inc. | 24,415 | 904,820 | Transocean Ltd.(1) | 3,320 | 240,534 | |

| Discover Financial Services | 7,534 | 116,476 | 4,641,302 | |||

| 1,888,183 | FOOD & STAPLES RETAILING — 0.6% | |||||

| CONTAINERS & PACKAGING — 0.3% | Safeway, Inc. | 67,774 | 1,599,467 | |||

| Graphic Packaging | SUPERVALU, INC. | 24,347 | 362,770 | |||

| Holding Co.(1) | 105,207 | 388,214 | ||||

| Rock-Tenn Co., Class A | 17,461 | 900,987 | Wal-Mart Stores, Inc. | 19,874 | 1,066,240 | |

| Silgan Holdings, Inc. | 1,481 | 89,349 | 3,028,477 | |||

| Sonoco Products Co. | 4,717 | 156,274 | FOOD PRODUCTS — 1.5% | |||

| 1,534,824 | ConAgra Foods, Inc. | 59,989 | 1,467,931 | |||

| Corn Products | ||||||

| DIVERSIFIED CONSUMER SERVICES — 0.1% | International, Inc. | 12,718 | 457,848 | |||

| Corinthian Colleges, Inc.(1) | 23,923 | 373,677 | Del Monte Foods Co. | 85,398 | 1,275,846 | |

| DIVERSIFIED FINANCIAL SERVICES — 2.7% | Dole Food Co., Inc.(1) | 32,510 | 368,013 | |||

| Bank of America Corp. | 342,996 | 6,115,618 | Fresh Del Monte | |||

| Citigroup, Inc.(1) | 195,375 | 853,789 | Produce, Inc.(1) | 2,569 | 53,615 | |

| JPMorgan Chase & Co. | 149,303 | 6,357,322 | General Mills, Inc. | 144 | 10,250 | |

| 13,326,729 | Hershey Co. (The) | 2,799 | 131,581 | |||

13

| Balanced | ||||||

| Shares/ | Shares/ | |||||

| Principal | Principal | |||||

| Amount | Value | Amount | Value | |||

| Kraft Foods, Inc., Class A | 23,529 | $ 696,458 | HOUSEHOLD PRODUCTS — 1.3% | |||

| Lancaster Colony Corp. | 3,790 | 208,336 | Colgate-Palmolive Co. | 6,934 | $ 583,149 | |

| Mead Johnson Nutrition Co. | 5,442 | 280,862 | Kimberly-Clark Corp. | 19,403 | 1,188,628 | |

| Smithfield Foods, Inc.(1) | 22,335 | 418,558 | Procter & Gamble Co. (The) | 77,042 | 4,788,931 | |

| Tyson Foods, Inc., Class A | 111,703 | 2,188,262 | 6,560,708 | |||

| 7,557,560 | INDEPENDENT POWER PRODUCERS & | |||||

| GAS UTILITIES — 0.1% | ENERGY TRADERS — 0.9% | |||||

| ONEOK, Inc. | 12,385 | 608,599 | Constellation Energy | |||

| Group, Inc. | 78,882 | 2,788,479 | ||||

| UGI Corp. | 4,550 | 125,079 | ||||

| Mirant Corp.(1) | 79,108 | 922,399 | ||||

| 733,678 | ||||||

| NRG Energy, Inc.(1) | 34,020 | 822,263 | ||||

| HEALTH CARE EQUIPMENT & SUPPLIES — 0.6% | ||||||

| Becton, Dickinson & Co. | 5,036 | 384,599 | 4,533,141 | |||

| C.R. Bard, Inc. | 13,014 | 1,126,101 | INDUSTRIAL CONGLOMERATES — 1.1% | |||

| Hospira, Inc.(1) | 2,355 | 126,676 | 3M Co. | 20,599 | 1,826,513 | |

| Medtronic, Inc. | 15,535 | 678,724 | Carlisle Cos., Inc. | 35,282 | 1,331,190 | |

| STERIS Corp. | 19,400 | 645,632 | General Electric Co. | 122,560 | 2,311,482 | |

| 2,961,732 | 5,469,185 | |||||

| HEALTH CARE PROVIDERS & SERVICES — 2.1% | INSURANCE — 2.7% | |||||

| Cardinal Health, Inc. | 66,152 | 2,294,813 | ACE Ltd. | 9,566 | 508,816 | |

| Centene Corp.(1) | 17,773 | 407,002 | Allied World Assurance Co. | |||

| Holdings Ltd. | 18,004 | 784,434 | ||||

| Coventry Health Care, Inc.(1) | 58,574 | 1,390,547 | Allstate Corp. (The) | 3,369 | 110,065 | |

| Humana, Inc.(1) | 48,766 | 2,229,581 | American Financial | |||

| Magellan Health | Group, Inc. | 62,236 | 1,831,605 | |||

| Services, Inc.(1) | 9,362 | 395,170 | American International | |||

| Medco Health | Group, Inc.(1) | 3,277 | 127,475 | |||

| Solutions, Inc.(1) | 18,652 | 1,098,976 | Arch Capital Group Ltd.(1) | 605 | 45,726 | |

| UnitedHealth Group, Inc. | 52,849 | 1,601,853 | Aspen Insurance | |||

| WellPoint, Inc.(1) | 22,620 | 1,216,956 | Holdings Ltd. | 12,972 | 349,985 | |

| 10,634,898 | Berkshire Hathaway, Inc., | |||||

| HOTELS, RESTAURANTS & LEISURE — 0.5% | Class B(1) | 10,472 | 806,344 | |||

| McDonald’s Corp. | 13,669 | 964,895 | Chubb Corp. (The) | 15,676 | 828,790 | |

| Panera Bread Co., Class A(1) | 15,228 | 1,186,870 | CNA Financial Corp.(1) | 12,999 | 365,532 | |

| Starbucks Corp. | 10,623 | 275,986 | Conseco, Inc.(1) | 17,731 | 104,613 | |

| 2,427,751 | Delphi Financial Group, Inc., | |||||

| HOUSEHOLD DURABLES — 0.5% | Class A | 5,580 | 153,450 | |||

| Endurance Specialty | ||||||

| American Greetings Corp., | Holdings Ltd. | 20,276 | 747,171 | |||

| Class A | 18,942 | 465,216 | ||||

| D.R. Horton, Inc. | 30,506 | 448,133 | Genworth Financial, Inc., | |||

| Class A(1) | 8,051 | 133,003 | ||||

| Harman International | Hartford Financial Services | |||||

| Industries, Inc.(1) | 12,678 | 500,527 | ||||

| Group, Inc. (The) | 2,475 | 70,711 | ||||

| NVR, Inc.(1) | 983 | 705,843 | ||||

| Horace Mann Educators Corp. | 9,669 | 166,404 | ||||

| Ryland Group, Inc. | 18,616 | 424,073 | Loews Corp. | 1,031 | 38,394 | |

| 2,543,792 | MetLife, Inc. | 2,313 | 105,427 | |||

| Old Republic | ||||||

| International Corp. | 5,627 | 84,461 | ||||

14

| Balanced | ||||||

| Shares/ | Shares/ | |||||

| Principal | Principal | |||||

| Amount | Value | Amount | Value | |||

| Principal Financial Group, Inc. | 12,347 | $ 360,779 | MEDIA — 1.4% | |||

| Protective Life Corp. | 6,690 | 161,028 | CBS Corp., Class B | 3,051 | $ 49,457 | |

| Prudential Financial, Inc. | 51,813 | 3,293,234 | Comcast Corp., Class A | 151,323 | 2,987,116 | |

| Reinsurance Group of | Gannett Co., Inc. | 7,431 | 126,476 | |||

| America, Inc. | 2,560 | 132,173 | Scholastic Corp. | 12,412 | 335,248 | |

| Transatlantic Holdings, Inc. | 2,702 | 134,370 | Time Warner, Inc. | 93,972 | 3,108,594 | |

| Travelers Cos., Inc. (The) | 40,991 | 2,079,883 | Walt Disney Co. (The) | 7,423 | 273,463 | |

| WR Berkley Corp. | 415 | 11,205 | 6,880,354 | |||

| 13,535,078 | METALS & MINING — 1.1% | |||||

| INTERNET & CATALOG RETAIL — 0.5% | Commercial Metals Co. | 24,034 | 357,626 | |||

| Amazon.com, Inc.(1) | 5,873 | 804,953 | Freeport-McMoRan | |||

| Netflix, Inc.(1) | 14,794 | 1,461,204 | Copper & Gold, Inc. | 25,347 | 1,914,459 | |

| 2,266,157 | Newmont Mining Corp. | 21,971 | 1,232,134 | |||

| INTERNET SOFTWARE & SERVICES — 1.0% | Reliance Steel & | |||||

| AOL, Inc.(1) | 25,770 | 601,987 | Aluminum Co. | 25,724 | 1,255,588 | |

| EarthLink, Inc. | 44,777 | 403,889 | Worthington Industries, Inc. | 51,508 | 822,583 | |

| Google, Inc., Class A(1) | 7,598 | 3,992,293 | 5,582,390 | |||

| 4,998,169 | MULTILINE RETAIL — 0.5% | |||||

| Big Lots, Inc.(1) | 3,406 | 130,109 | ||||

| IT SERVICES — 2.1% | ||||||

| Acxiom Corp.(1) | 8,683 | 165,671 | Dillard’s, Inc., Class A | 22,955 | 644,576 | |

| Dollar Tree, Inc.(1) | 10,769 | 653,894 | ||||

| Automatic Data | ||||||

| Processing, Inc. | 46,469 | 2,014,896 | Family Dollar Stores, Inc. | 14,337 | 567,172 | |

| Convergys Corp.(1) | 92,398 | 1,167,911 | Macy’s, Inc. | 23,294 | 540,421 | |

| International Business | 2,536,172 | |||||

| Machines Corp. | 49,400 | 6,372,600 | MULTI-INDUSTRY — 0.3% | |||

| NeuStar, Inc., Class A(1) | 8,502 | 208,044 | Financial Select Sector | |||

| Western Union Co. (The) | 34,520 | 629,990 | SPDR Fund | 81,072 | 1,309,313 | |

| Wright Express Corp.(1) | 6,394 | 217,204 | MULTI-UTILITIES — 1.0% | |||

| 10,776,316 | DTE Energy Co. | 29,431 | 1,417,691 | |||

| LEISURE EQUIPMENT & PRODUCTS — 0.2% | Integrys Energy Group, Inc. | 56,507 | 2,803,312 | |||

| Polaris Industries, Inc. | 20,534 | 1,214,997 | NiSource, Inc. | 18,943 | 308,771 | |

| LIFE SCIENCES TOOLS & SERVICES — 0.5% | Public Service Enterprise | |||||

| Group, Inc. | 13,992 | 449,563 | ||||

| Bruker Corp.(1) | 65,488 | 1,001,311 | ||||

| 4,979,337 | ||||||

| Millipore Corp.(1) | 16,206 | 1,720,267 | ||||

| OFFICE ELECTRONICS — 0.1% | ||||||

| 2,721,578 | Xerox Corp. | 41,695 | 454,475 | |||

| MACHINERY — 1.3% | OIL, GAS & CONSUMABLE FUELS — 5.2% | |||||

| Briggs & Stratton Corp. | 21,467 | 509,627 | Anadarko Petroleum Corp. | 13,908 | 864,521 | |

| Caterpillar, Inc. | 7,310 | 497,738 | Apache Corp. | 14,506 | 1,476,131 | |

| Cummins, Inc. | 16,090 | 1,162,181 | Canadian Natural | |||

| Graco, Inc. | 11,509 | 399,132 | Resources Ltd. | 21,549 | 1,657,980 | |

| Manitowoc Co., Inc. (The) | 22,979 | 321,936 | Chevron Corp. | 44,954 | 3,661,054 | |

| Mueller Industries, Inc. | 14,430 | 427,849 | Cimarex Energy Co. | 10,738 | 731,043 | |

| Oshkosh Corp.(1) | 34,429 | 1,329,648 | ConocoPhillips | 43,461 | 2,572,457 | |

| Timken Co. | 40,109 | 1,411,035 | Exxon Mobil Corp. | 142,112 | 9,642,299 | |

| WABCO Holdings, Inc.(1) | 13,987 | 464,228 | Murphy Oil Corp. | 17,447 | 1,049,437 | |

| 6,523,374 | Occidental Petroleum Corp. | 23,652 | 2,096,986 | |||

15

| Balanced | ||||||

| Shares/ | Shares/ | |||||

| Principal | Principal | |||||

| Amount | Value | Amount | Value | |||

| Peabody Energy Corp. | 20,414 | $ 953,742 | SOFTWARE — 2.5% | |||

| World Fuel Services Corp. | 48,542 | 1,380,049 | ACI Worldwide, Inc.(1) | 7,989 | $ 150,113 | |

| 26,085,699 | Cadence Design | |||||

| PAPER & FOREST PRODUCTS — 0.1% | Systems, Inc.(1) | 58,931 | 439,625 | |||

| International Paper Co. | 24,921 | 666,388 | Fair Isaac Corp. | 16,415 | 345,700 | |

| PHARMACEUTICALS — 3.0% | Intuit, Inc.(1) | 67,117 | 2,426,951 | |||

| Abbott Laboratories | 37,989 | 1,943,517 | Mentor Graphics Corp.(1) | 42,615 | 383,109 | |

| Bristol-Myers Squibb Co. | 19,691 | 497,985 | Microsoft Corp. | 201,720 | 6,160,529 | |

| Eli Lilly & Co. | 93,351 | 3,264,485 | Oracle Corp. | 59,013 | 1,524,896 | |

| Endo Pharmaceuticals | Quest Software, Inc.(1) | 9,006 | 157,875 | |||

| Holdings, Inc.(1) | 43,775 | 958,673 | Symantec Corp.(1) | 37,185 | 623,593 | |

| Forest Laboratories, Inc.(1) | 45,548 | 1,241,639 | Synopsys, Inc.(1) | 18,527 | 420,748 | |

| Johnson & Johnson | 101,341 | 6,516,226 | 12,633,139 | |||

| King Pharmaceuticals, Inc.(1) | 72,904 | 714,459 | SPECIALTY RETAIL — 1.5% | |||

| 15,136,984 | AutoZone, Inc.(1) | 1,066 | 197,221 | |||

| REAL ESTATE INVESTMENT TRUSTS (REITs) — 0.6% | Barnes & Noble, Inc. | 20,285 | 447,081 | |||

| Annaly Capital | Gap, Inc. (The) | 62,583 | 1,547,677 | |||

| Management, Inc. | 9,189 | 155,754 | ||||

| Home Depot, Inc. (The) | 2,223 | 78,361 | ||||

| CBL & Associates | ||||||

| Properties, Inc. | 8,730 | 127,458 | PetSmart, Inc. | 8,068 | 266,809 | |

| Duke Realty Corp. | 7,107 | 96,158 | Rent-A-Center, Inc.(1) | 25,049 | 646,765 | |

| Public Storage | 111 | 10,757 | Ross Stores, Inc. | 39,873 | 2,232,888 | |

| Simon Property Group, Inc. | 2,627 | 233,855 | Sherwin-Williams Co. (The) | 8,014 | 625,653 | |

| SPDR Dow Jones REIT Fund | 44,894 | 2,579,160 | Williams-Sonoma, Inc. | 57,134 | 1,645,459 | |

| 3,203,142 | 7,687,914 | |||||

| ROAD & RAIL — 0.5% | TEXTILES, APPAREL & LUXURY GOODS — 0.1% | |||||

| CSX Corp. | 10,799 | 605,284 | Jones Apparel Group, Inc. | 30,077 | 654,475 | |

| Norfolk Southern Corp. | 9,916 | 588,316 | THRIFTS & MORTGAGE FINANCE(2) | |||

| Union Pacific Corp. | 16,857 | 1,275,401 | MGIC Investment Corp.(1) | 9,521 | 99,304 | |

| 2,469,001 | Ocwen Financial Corp.(1) | 8,925 | 103,084 | |||

| SEMICONDUCTORS & SEMICONDUCTOR | 202,388 | |||||

| EQUIPMENT — 2.0% | TOBACCO — 0.7% | |||||

| Advanced Micro | Altria Group, Inc. | 13,269 | 281,170 | |||

| Devices, Inc.(1) | 53,920 | 488,515 | ||||

| Philip Morris | ||||||

| Broadcom Corp., Class A | 39,046 | 1,346,696 | International, Inc. | 66,036 | 3,241,047 | |

| Integrated Device | 3,522,217 | |||||

| Technology, Inc.(1) | 62,026 | 409,992 | ||||

| TRADING COMPANIES & DISTRIBUTORS — 0.1% | ||||||

| Intel Corp. | 175,018 | 3,995,661 | WESCO International, Inc.(1) | 12,756 | 518,149 | |

| LSI Corp.(1) | 100,931 | 607,605 | ||||

| WIRELESS TELECOMMUNICATION SERVICES — 0.1% | ||||||

| Marvell Technology | Sprint Nextel Corp.(1) | 110,034 | 467,644 | |||

| Group Ltd.(1) | 9,169 | 189,340 | ||||

| Micron Technology, Inc.(1) | 51,487 | 481,403 | TOTAL COMMON STOCKS | |||

| (Cost $245,406,239) | 302,334,049 | |||||

| RF Micro Devices, Inc.(1) | 89,935 | 505,435 | ||||

| Tessera Technologies, Inc.(1) | 9,481 | 192,275 | ||||

| Texas Instruments, Inc. | 58,466 | 1,520,701 | ||||

| Xilinx, Inc. | 11,913 | 307,117 | ||||

| 10,044,740 | ||||||

16

| Balanced | ||||||

| Shares/ | Shares/ | |||||

| Principal | Principal | |||||

| Amount | Value | Amount | Value | |||

| U.S. Treasury Securities — 11.4% | BEVERAGES — 0.2% | |||||

| Anheuser-Busch InBev | ||||||

| U.S. Treasury Bonds, | Worldwide, Inc., 3.00%, | |||||

| 5.25%, 2/15/29(3) | $ 2,000,000 | $ 2,229,688 | ||||

| 10/15/12(3) | $ 300,000 | $ 308,730 | ||||

| U.S. Treasury Bonds, | Anheuser-Busch InBev | |||||

| 6.25%, 5/15/30(3) | 310,000 | 388,614 | ||||

| Worldwide, Inc., 6.875%, | ||||||

| U.S. Treasury Bonds, | 11/15/19(4) | 250,000 | 290,017 | |||

| 4.75%, 2/15/37(3) | 929,000 | 969,789 | ||||

| Anheuser-Busch InBev | ||||||

| U.S. Treasury Bonds, | Worldwide, Inc., 5.00%, | |||||

| 4.375%, 11/15/39(3) | 1,000,000 | 975,469 | 4/15/20(3)(4) | 110,000 | 111,758 | |

| U.S. Treasury Inflation | Dr Pepper Snapple Group, | |||||

| Indexed Notes, | Inc., 6.82%, 5/1/18(3) | 230,000 | 267,907 | |||

| 1.625%, 1/15/15(3) | 3,405,300 | 3,598,976 | ||||

| SABMiller plc, 6.20%, | ||||||

| U.S. Treasury Notes, | 7/1/11(3)(4) | 230,000 | 241,470 | |||

| 0.75%, 11/30/11(3) | 12,500,000 | 12,501,463 | ||||

| 1,219,882 | ||||||

| U.S. Treasury Notes, | ||||||

| 1.875%, 6/15/12(3) | 12,200,000 | 12,422,077 | BIOTECHNOLOGY(2) | |||

| U.S. Treasury Notes, | Amgen, Inc., 5.75%, | |||||

| 3/15/40(3) | 150,000 | 153,122 | ||||

| 1.375%, 9/15/12(3) | 4,200,000 | 4,222,642 | ||||

| U.S. Treasury Notes, | CAPITAL MARKETS — 0.7% | |||||

| 2.375%, 8/31/14(3) | 13,000,000 | 13,123,903 | Credit Suisse (New York), | |||

| 5.00%, 5/15/13(3) | 340,000 | 366,121 | ||||

| U.S. Treasury Notes, | ||||||

| 3.125%, 5/15/19(3) | 7,000,000 | 6,764,842 | Credit Suisse (New York), | |||

| 5.50%, 5/1/14(3) | 200,000 | 219,331 | ||||

| TOTAL U.S. TREASURY SECURITIES | ||||||

| (Cost $56,528,359) | 57,197,463 | Credit Suisse (New York), | ||||

| 5.30%, 8/13/19(3) | 230,000 | 241,050 | ||||

| Corporate Bonds — 10.5% | Credit Suisse AG, 5.40%, | |||||

| AEROSPACE & DEFENSE — 0.4% | 1/14/20(3) | 60,000 | 61,199 | |||

| Honeywell International, Inc., | Deutsche Bank AG (London), | |||||

| 5.30%, 3/15/17(3) | 262,000 | 284,088 | 4.875%, 5/20/13(3) | 330,000 | 354,515 | |

| Honeywell International, Inc., | Deutsche Bank AG (London), | |||||

| 5.30%, 3/1/18(3) | 230,000 | 249,077 | 3.875%, 8/18/14(3) | 190,000 | 196,625 | |

| L-3 Communications Corp., | Goldman Sachs Group, Inc. | |||||

| 5.875%, 1/15/15(3) | 160,000 | 163,200 | (The), 6.00%, 5/1/14(3) | 150,000 | 161,502 | |

| L-3 Communications Corp., | Goldman Sachs Group, Inc. | |||||

| 5.20%, 10/15/19(3)(4) | 130,000 | 133,749 | (The), 7.50%, 2/15/19(3) | 850,000 | 945,300 | |

| Lockheed Martin Corp., | Jefferies Group, Inc., 8.50%, | |||||

| 5.50%, 11/15/39(3) | 260,000 | 264,779 | 7/15/19(3) | 130,000 | 147,986 | |

| United Technologies Corp., | Morgan Stanley, 4.20%, | |||||

| 6.05%, 6/1/36(3) | 454,000 | 496,014 | 11/20/14(3) | 200,000 | 199,761 | |

| United Technologies Corp., | Morgan Stanley, 6.625%, | |||||

| 5.70%, 4/15/40(3) | 200,000 | 209,591 | 4/1/18(3) | 320,000 | 339,802 | |

| 1,800,498 | Morgan Stanley, 5.625%, | |||||

| AUTOMOBILES — 0.1% | 9/23/19(3) | 250,000 | 247,012 | |||

| American Honda Finance | UBS AG (Stamford Branch), | |||||

| Corp., 2.375%, 3/18/13(3)(4) | 170,000 | 170,822 | 5.875%, 12/20/17(3) | 220,000 | 233,061 | |

| Daimler Finance N.A. LLC, | 3,713,265 | |||||

| 5.875%, 3/15/11(3) | 260,000 | 269,888 | CHEMICALS — 0.1% | |||

| Nissan Motor Acceptance | CF Industries, Inc., 6.875%, | |||||

| Corp., 3.25%, 1/30/13(3)(4) | 50,000 | 51,033 | 5/1/18 | 210,000 | 219,450 | |

| 491,743 | Dow Chemical Co. (The), | |||||

| 8.55%, 5/15/19(3) | 130,000 | 159,110 | ||||

17

| Balanced | ||||||

| Shares/ | Shares/ | |||||

| Principal | Principal | |||||

| Amount | Value | Amount | Value | |||

| Rohm & Haas Co., 5.60%, | Capital One Bank USA N.A., | |||||

| 3/15/13(3) | $ 240,000 | $ 258,483 | 8.80%, 7/15/19(3) | $ 250,000 | $ 307,068 | |

| 637,043 | General Electric Capital Corp., | |||||

| COMMERCIAL BANKS — 0.4% | 3.75%, 11/14/14(3) | 200,000 | 205,234 | |||

| Barclays Bank plc, 5.00%, | General Electric Capital Corp., | |||||

| 9/22/16(3) | 200,000 | 207,499 | 4.375%, 9/21/15(3) | 200,000 | 208,903 | |

| BB&T Corp., 5.70%, | General Electric Capital Corp., | |||||

| 4/30/14(3) | 150,000 | 164,961 | 5.625%, 9/15/17(3) | 450,000 | 482,659 | |

| Fifth Third Bancorp., 6.25%, | General Electric Capital Corp., | |||||

| 5/1/13(3) | 140,000 | 151,802 | 6.00%, 8/7/19(3) | 150,000 | 162,428 | |

| National Australia Bank Ltd., | SLM Corp., 5.375%, | |||||

| 3.75%, 3/2/15(3)(4) | 100,000 | 102,240 | 1/15/13(3) | 110,000 | 110,540 | |

| PNC Bank N.A., 6.00%, | 2,023,676 | |||||

| 12/7/17(3) | 290,000 | 308,975 | CONTAINERS & PACKAGING — 0.1% | |||

| SunTrust Bank, 7.25%, | Ball Corp., 7.125%, 9/1/16(3) | 130,000 | 138,775 | |||

| 3/15/18(3) | 110,000 | 119,901 | ||||

| Ball Corp., 6.75%, 9/15/20(3) | 120,000 | 123,300 | ||||

| Wachovia Bank N.A., 4.80%, | 262,075 | |||||

| 11/1/14(3) | 373,000 | 391,685 | ||||

| Wachovia Bank N.A., 4.875%, | DIVERSIFIED FINANCIAL SERVICES — 0.7% | |||||

| 2/1/15(3) | 123,000 | 129,141 | Arch Western Finance LLC, | |||

| 6.75%, 7/1/13(3) | 100,000 | 101,250 | ||||

| Wells Fargo & Co., 3.625%, | ||||||

| 4/15/15(3) | 110,000 | 111,801 | Bank of America Corp., | |||

| 4.50%, 4/1/15(3) | 190,000 | 191,949 | ||||

| Wells Fargo & Co., 5.625%, | ||||||

| 12/11/17(3) | 50,000 | 53,928 | Bank of America Corp., | |||

| 6.50%, 8/1/16(3) | 320,000 | 345,615 | ||||

| Westpac Banking Corp., | ||||||

| 4.875%, 11/19/19(3) | 100,000 | 101,746 | Bank of America Corp., | |||

| 7.625%, 6/1/19(3) | 150,000 | 171,515 | ||||

| 1,843,679 | ||||||

| Bank of America N.A., | ||||||

| COMMERCIAL SERVICES & SUPPLIES — 0.2% | 5.30%, 3/15/17(3) | 420,000 | 416,908 | |||

| Allied Waste North America, | Citigroup, Inc., 5.50%, | |||||

| Inc., 6.375%, 4/15/11(3) | 180,000 | 188,461 | ||||

| 4/11/13(3) | 470,000 | 496,665 | ||||

| Corrections Corp. of America, | Citigroup, Inc., 6.01%, | |||||

| 6.25%, 3/15/13(3) | 250,000 | 255,000 | ||||

| 1/15/15(3) | 310,000 | 330,748 | ||||

| Republic Services, Inc., | Citigroup, Inc., 6.125%, | |||||

| 5.50%, 9/15/19(3)(4) | 250,000 | 262,940 | ||||

| 5/15/18(3) | 320,000 | 332,354 | ||||

| Republic Services, Inc., | Citigroup, Inc., 8.50%, | |||||

| 6.20%, 3/1/40(3)(4) | 140,000 | 143,832 | ||||

| 5/22/19(3) | 100,000 | 118,246 | ||||

| Waste Management, Inc., | CME Group Index Services | |||||

| 6.125%, 11/30/39(3) | 120,000 | 125,390 | ||||

| LLC, 4.40%, 3/15/18(3)(4) | 150,000 | 149,482 | ||||

| 975,623 | JPMorgan Chase & Co., | |||||

| COMMUNICATIONS EQUIPMENT(2) | 4.65%, 6/1/14(3) | 330,000 | 351,686 | |||

| Cisco Systems, Inc., 5.90%, | JPMorgan Chase & Co., | |||||

| 2/15/39(3) | 210,000 | 220,950 | 6.00%, 1/15/18(3) | 670,000 | 723,532 | |

| CONSUMER FINANCE — 0.4% | 3,729,950 | |||||

| American Express Centurion | DIVERSIFIED TELECOMMUNICATION | |||||

| Bank, 5.55%, 10/17/12(3) | 150,000 | 161,757 | SERVICES — 0.7% | |||

| American Express Centurion | Alltel Corp., 7.875%, 7/1/32(3) | 100,000 | 123,486 | |||

| Bank, 6.00%, 9/13/17(3) | 250,000 | 270,556 | ||||

| AT&T, Inc., 6.80%, 5/15/36(3) | 350,000 | 384,083 | ||||

| American Express Co., | AT&T, Inc., 6.55%, 2/15/39(3) | 470,000 | 505,709 | |||

| 7.25%, 5/20/14(3) | 100,000 | 114,531 | ||||

18

| Balanced | ||||||

| Shares/ | Shares/ | |||||

| Principal | Principal | |||||

| Amount | Value | Amount | Value | |||

| British Telecommunications | ELECTRONIC EQUIPMENT, INSTRUMENTS & | |||||

| plc, 5.95%, 1/15/18(3) | $ 120,000 | $ 126,134 | COMPONENTS — 0.1% | |||

| Cellco Partnership/Verizon | Jabil Circuit, Inc., 7.75%, | |||||

| Wireless Capital LLC, | 7/15/16(3) | $ 250,000 | $ 266,250 | |||

| 8.50%, 11/15/18(3) | 130,000 | 164,734 | ENERGY EQUIPMENT & SERVICES — 0.1% | |||

| CenturyTel, Inc., 7.60%, | Pride International, Inc., | |||||

| 9/15/39(3) | 120,000 | 117,204 | 8.50%, 6/15/19(3) | 100,000 | 115,375 | |

| Deutsche Telekom | Weatherford International | |||||

| International Finance BV, | Ltd., 9.625%, 3/1/19(3) | 240,000 | 310,882 | |||

| 6.75%, 8/20/18(3) | 150,000 | 170,504 | ||||

| 426,257 | ||||||

| Embarq Corp., 7.08%, | ||||||

| 6/1/16(3) | 219,000 | 241,844 | FOOD & STAPLES RETAILING — 0.3% | |||

| New Communications | CVS Caremark Corp., 6.60%, | |||||

| 3/15/19(3) | 350,000 | 400,037 | ||||

| Holdings, Inc., 8.50%, | ||||||

| 4/15/20(3)(4) | 130,000 | 134,550 | Kroger Co. (The), 6.40%, | |||

| 8/15/17(3) | 200,000 | 227,669 | ||||

| Qwest Corp., 7.875%, | ||||||

| 9/1/11(3) | 120,000 | 127,950 | SYSCO Corp., 4.20%, | |||

| 2/12/13(3) | 100,000 | 106,703 | ||||

| Qwest Corp., 7.50%, | ||||||

| 10/1/14(3) | 200,000 | 219,750 | Wal-Mart Stores, Inc., | |||

| 5.875%, 4/5/27(3) | 468,000 | 508,516 | ||||

| Sprint Capital Corp., 7.625%, | ||||||

| 1/30/11(3) | 180,000 | 185,625 | Wal-Mart Stores, Inc., | |||

| 6.20%, 4/15/38(3) | 220,000 | 243,021 | ||||

| Telecom Italia Capital SA, | ||||||

| 6.175%, 6/18/14(3) | 340,000 | 365,619 | Wal-Mart Stores, Inc., | |||

| 5.625%, 4/1/40(3) | 150,000 | 153,956 | ||||

| Telefonica Emisiones SAU, | ||||||

| 5.88%, 7/15/19(3) | 220,000 | 234,298 | 1,639,902 | |||

| Verizon Communications, Inc., | FOOD PRODUCTS — 0.2% | |||||

| 6.40%, 2/15/38(3) | 70,000 | 75,227 | General Mills, Inc., 5.65%, | |||

| Windstream Corp., 7.875%, | 9/10/12(3) | 120,000 | 131,220 | |||

| 11/1/17(3) | 220,000 | 219,450 | Kellogg Co., 4.45%, | |||

| 3,396,167 | 5/30/16(3) | 200,000 | 214,829 | |||

| ELECTRIC UTILITIES — 0.3% | Kraft Foods, Inc., 6.00%, | |||||

| 2/11/13(3) | 70,000 | 77,622 | ||||

| Carolina Power & Light Co., | ||||||

| 5.15%, 4/1/15(3) | 100,000 | 110,390 | Kraft Foods, Inc., 5.375%, | |||

| 2/10/20(3) | 70,000 | 72,743 | ||||

| Cleveland Electric | ||||||

| Illuminating Co. (The), | Kraft Foods, Inc., 6.50%, | |||||

| 5.70%, 4/1/17(3) | 81,000 | 85,794 | 2/9/40(3) | 300,000 | 323,956 | |

| Duke Energy Corp., 3.95%, | Mead Johnson Nutrition Co., | |||||

| 9/15/14(3) | 130,000 | 135,204 | 3.50%, 11/1/14(3)(4) | 120,000 | 121,669 | |

| EDF SA, 4.60%, 1/27/20(3)(4) | 210,000 | 210,542 | Ralcorp Holdings, Inc., | |||

| 6.625%, 8/15/39(3)(4) | 130,000 | 130,318 | ||||

| Exelon Generation Co. LLC, | ||||||

| 5.20%, 10/1/19(3) | 150,000 | 155,227 | 1,072,357 | |||

| FirstEnergy Solutions Corp., | HEALTH CARE EQUIPMENT & SUPPLIES — 0.1% | |||||

| 6.05%, 8/15/21(3) | 300,000 | 304,475 | Baxter International, Inc., | |||

| Florida Power Corp., 6.35%, | 5.90%, 9/1/16(3) | 130,000 | 148,921 | |||

| 9/15/37(3) | 230,000 | 259,169 | Baxter International, Inc., | |||

| Southern California Edison | 5.375%, 6/1/18(3) | 220,000 | 241,243 | |||

| Co., 5.625%, 2/1/36(3) | 60,000 | 62,013 | 390,164 | |||

| 1,322,814 | ||||||

19

| Balanced | ||||||

| Shares/ | Shares/ | |||||

| Principal | Principal | |||||

| Amount | Value | Amount | Value | |||

| HEALTH CARE PROVIDERS & SERVICES — 0.2% | New York Life Global Funding, | |||||

| Express Scripts, Inc., 5.25%, | 4.65%, 5/9/13(3)(4) | $ 150,000 | $ 161,076 | |||

| 6/15/12(3) | $ 230,000 | $ 246,504 | Prudential Financial, Inc., | |||

| Express Scripts, Inc., 7.25%, | 7.375%, 6/15/19(3) | 120,000 | 141,584 | |||

| 6/15/19(3) | 360,000 | 426,351 | Prudential Financial, Inc., | |||

| Medco Health Solutions, Inc., | 5.40%, 6/13/35(3) | 270,000 | 248,611 | |||

| 7.25%, 8/15/13(3) | 270,000 | 308,881 | Travelers Cos., Inc. (The), | |||

| Quest Diagnostics, Inc., | 5.90%, 6/2/19(3) | 100,000 | 110,052 | |||

| 4.75%, 1/30/20(3) | 120,000 | 119,840 | 1,686,469 | |||

| 1,101,576 | INTERNET & CATALOG RETAIL(2) | |||||

| HOTELS, RESTAURANTS & LEISURE — 0.2% | Expedia, Inc., 7.46%, | |||||

| McDonald’s Corp., 5.35%, | 8/15/18(3) | 170,000 | 189,125 | |||

| 3/1/18(3) | 170,000 | 188,755 | LEISURE EQUIPMENT & PRODUCTS(2) | |||

| McDonald’s Corp., 6.30%, | Hasbro, Inc., 6.35%, | |||||

| 10/15/37(3) | 230,000 | 258,549 | 3/15/40(3) | 150,000 | 155,004 | |

| Yum! Brands, Inc., 5.30%, | MACHINERY(2) | |||||

| 9/15/19(3) | 310,000 | 324,057 | ||||

| Deere & Co., 5.375%, | ||||||

| 771,361 | 10/16/29(3) | 200,000 | 206,103 | |||

| HOUSEHOLD DURABLES — 0.1% | MEDIA — 1.0% | |||||

| Jarden Corp., 8.00%, 5/1/16 | 230,000 | 243,513 | CBS Corp., 8.875%, 5/15/19(3) | 120,000 | 148,852 | |

| Toll Brothers Finance Corp., | CBS Corp., 5.75%, 4/15/20(3) | 110,000 | 114,514 | |||

| 6.75%, 11/1/19(3) | 100,000 | 101,149 | ||||

| CBS Corp., 5.50%, 5/15/33(3) | 120,000 | 107,809 | ||||

| Whirlpool Corp., 8.60%, | ||||||

| 5/1/14(3) | 60,000 | 70,290 | Comcast Corp., 5.90%, | |||

| 3/15/16(3) | 189,000 | 208,167 | ||||

| 414,952 | ||||||

| Comcast Corp., 6.40%, | ||||||

| HOUSEHOLD PRODUCTS — 0.1% | 5/15/38(3) | 220,000 | 230,572 | |||

| Kimberly-Clark Corp., | Comcast Corp., 6.40%, | |||||

| 6.125%, 8/1/17(3) | 230,000 | 263,312 | ||||

| 3/1/40(3) | 80,000 | 83,473 | ||||

| INDUSTRIAL CONGLOMERATES — 0.1% | DirecTV Holdings LLC, | |||||

| General Electric Co., 5.00%, | 3.55%, 3/15/15(3)(4) | 190,000 | 189,624 | |||

| 2/1/13(3) | 158,000 | 170,726 | ||||

| DirecTV Holdings LLC/ | ||||||

| General Electric Co., 5.25%, | DirecTV Financing Co., Inc., | |||||

| 12/6/17(3) | 230,000 | 245,012 | 4.75%, 10/1/14(3) | 380,000 | 402,186 | |

| Hutchison Whampoa | DirecTV Holdings LLC/ | |||||

| International 09/16 Ltd., | DirecTV Financing Co., Inc., | |||||

| 4.625%, 9/11/15(3)(4) | 230,000 | 239,222 | 6.375%, 6/15/15(3) | 210,000 | 218,663 | |

| 654,960 | Interpublic Group of Cos., Inc. | |||||

| INSURANCE — 0.3% | (The), 10.00%, 7/15/17(3) | 300,000 | 344,625 | |||

| Allstate Corp. (The), 7.45%, | Lamar Media Corp., 9.75%, | |||||

| 5/16/19 | 150,000 | 179,312 | 4/1/14(3) | 150,000 | 167,625 | |

| American International Group, | News America, Inc., 6.90%, | |||||

| Inc., 8.25%, 8/15/18(3) | 100,000 | 106,851 | 8/15/39(3) | 190,000 | 213,083 | |

| Hartford Financial Services | Omnicom Group, Inc., 5.90%, | |||||

| Group, Inc. (The), 4.00%, | 4/15/16(3) | 290,000 | 322,309 | |||

| 3/30/15(3) | 110,000 | 109,780 | Time Warner Cable, Inc., | |||

| Lincoln National Corp., | 5.40%, 7/2/12(3) | 350,000 | 376,950 | |||

| 6.25%, 2/15/20(3) | 110,000 | 117,792 | Time Warner Cable, Inc., | |||

| MetLife Global Funding I, | 6.75%, 7/1/18(3) | 240,000 | 272,540 | |||

| 5.125%, 4/10/13(3)(4) | 200,000 | 215,331 | Time Warner, Inc., 5.50%, | |||

| MetLife, Inc., 6.75%, 6/1/16(3) | 260,000 | 296,080 | 11/15/11(3) | 195,000 | 206,865 | |

20

| Balanced | ||||||

| Shares/ | Shares/ | |||||

| Principal | Principal | |||||

| Amount | Value | Amount | Value | |||

| Time Warner, Inc., 4.875%, | Pacific Gas & Electric Co., | |||||

| 3/15/20(3) | $ 190,000 | $ 188,653 | 5.80%, 3/1/37(3) | $ 303,000 | $ 313,392 | |

| Time Warner, Inc., 7.625%, | Pacific Gas & Electric Co., | |||||

| 4/15/31(3) | 70,000 | 81,588 | 6.35%, 2/15/38(3) | 220,000 | 244,690 | |

| Time Warner, Inc., 7.70%, | PG&E Corp., 5.75%, 4/1/14(3) | 90,000 | 99,006 | |||

| 5/1/32(3) | 200,000 | 235,425 | Sempra Energy, 8.90%, | |||

| Viacom, Inc., 6.25%, | 11/15/13(3) | 170,000 | 202,619 | |||

| 4/30/16(3) | 490,000 | 550,556 | Sempra Energy, 6.50%, | |||

| Viacom, Inc., 6.875%, | 6/1/16(3) | 100,000 | 113,852 | |||

| 4/30/36(3) | 160,000 | 175,571 | Sempra Energy, 6.00%, | |||

| Virgin Media Secured Finance | 10/15/39(3) | 80,000 | 82,220 | |||

| plc, 6.50%, 1/15/18(3)(4) | 190,000 | 191,900 | 2,540,755 | |||

| 5,031,550 | OFFICE ELECTRONICS — 0.1% | |||||

| METALS & MINING — 0.4% | Xerox Corp., 5.65%, | |||||

| AngloGold Ashanti Holdings | 5/15/13(3) | 80,000 | 85,938 | |||

| plc, 5.375%, 4/15/20(3) | 70,000 | 70,907 | Xerox Corp., 4.25%, | |||

| ArcelorMittal, 9.85%, | 2/15/15(3) | 200,000 | 204,644 | |||

| 6/1/19(3) | 240,000 | 313,046 | 290,582 | |||

| Barrick Gold Corp., 6.95%, | OIL, GAS & CONSUMABLE FUELS — 1.1% | |||||

| 4/1/19 | 170,000 | 199,510 | ||||

| Anadarko Petroleum Corp., | ||||||

| Freeport-McMoRan Copper & | 6.45%, 9/15/36(3) | 250,000 | 260,537 | |||

| Gold, Inc., 8.375%, 4/1/17(3) | 210,000 | 235,776 | ||||

| Anadarko Petroleum Corp., | ||||||

| Newmont Mining Corp., | 6.20%, 3/15/40(3) | 100,000 | 101,565 | |||

| 6.25%, 10/1/39(3) | 220,000 | 230,934 | ||||

| Cenovus Energy, Inc., 4.50%, | ||||||

| Rio Tinto Finance USA Ltd., | 9/15/14(3)(4) | 140,000 | 147,559 | |||

| 5.875%, 7/15/13(3) | 290,000 | 320,667 | ||||

| ConocoPhillips, 5.75%, | ||||||

| Teck Resources Ltd., 5.375%, | 2/1/19(3) | 240,000 | 268,169 | |||

| 10/1/15(3) | 70,000 | 74,900 | ||||

| ConocoPhillips, 6.50%, | ||||||

| Teck Resources Ltd., 10.75%, | 2/1/39(3) | 370,000 | 428,731 | |||

| 5/15/19(3) | 70,000 | 87,500 | ||||

| El Paso Corp., 7.875%, | ||||||

| Vale Overseas Ltd., 5.625%, | 6/15/12(3) | 110,000 | 117,090 | |||

| 9/15/19(3) | 90,000 | 94,876 | ||||

| Enbridge Energy Partners LP, | ||||||

| Xstrata Finance Canada Ltd., | 6.50%, 4/15/18(3) | 130,000 | 147,424 | |||

| 5.80%, 11/15/16(3)(4) | 197,000 | 211,183 | ||||

| Enbridge Energy Partners LP, | ||||||

| 1,839,299 | 5.20%, 3/15/20(3) | 100,000 | 103,457 | |||

| MULTILINE RETAIL(2) | Enterprise Products | |||||

| Macy’s Retail Holdings, Inc., | Operating LLC, 6.30%, | |||||

| 5.35%, 3/15/12(3) | 175,000 | 183,750 | 9/15/17(3) | 390,000 | 438,014 | |

| MULTI-UTILITIES — 0.5% | EOG Resources, Inc., 5.625%, | |||||

| CenterPoint Energy | 6/1/19(3) | 150,000 | 164,960 | |||

| Resources Corp., 6.125%, | Hess Corp., 6.00%, 1/15/40(3) | 110,000 | 112,216 | |||

| 11/1/17(3) | 230,000 | 249,944 | Kerr-McGee Corp., 6.95%, | |||

| CenterPoint Energy | 7/1/24(3) | 170,000 | 192,480 | |||

| Resources Corp., 6.25%, | Kinder Morgan Energy | |||||

| 2/1/37(3) | 330,000 | 334,178 | Partners LP, 6.85%, | |||

| CMS Energy Corp., 8.75%, | 2/15/20(3) | 200,000 | 230,749 | |||

| 6/15/19(3) | 180,000 | 206,917 | Kinder Morgan Energy | |||

| Dominion Resources, Inc., | Partners LP, 6.50%, 9/1/39(3) | 130,000 | 138,250 | |||

| 6.40%, 6/15/18(3) | 230,000 | 262,159 | Magellan Midstream Partners | |||

| Pacific Gas & Electric Co., | LP, 6.55%, 7/15/19(3) | 150,000 | 170,092 | |||

| 4.20%, 3/1/11(3) | 420,000 | 431,778 | ||||

21

| Balanced | ||||||

| Shares/ | Shares/ | |||||

| Principal | Principal | |||||

| Amount | Value | Amount | Value | |||

| Motiva Enterprises LLC, | REAL ESTATE INVESTMENT TRUSTS (REITs) — 0.2% | |||||

| 5.75%, 1/15/20(3)(4) | $ 160,000 | $ 171,834 | Digital Realty Trust LP, | |||

| Nexen, Inc., 5.65%, | 5.875%, 2/1/20(3)(4) | $ 150,000 | $ 150,961 | |||

| 5/15/17(3) | 150,000 | 161,546 | ProLogis, 5.625%, 11/15/16(3) | 270,000 | 267,182 | |

| Nexen, Inc., 6.40%, | ProLogis, 7.375%, 10/30/19(3) | 120,000 | 124,934 | |||

| 5/15/37(3) | 440,000 | 466,321 | ||||

| ProLogis, 6.875%, 3/15/20(3) | 150,000 | 148,781 | ||||

| Petrobras International | ||||||

| Finance Co., 5.75%, | Simon Property Group LP, | |||||

| 1/20/20(3) | 120,000 | 122,480 | 5.75%, 12/1/15(3) | 220,000 | 237,957 | |

| Petroleos Mexicanos, 6.00%, | 929,815 | |||||

| 3/5/20(3)(4) | 120,000 | 124,020 | REAL ESTATE MANAGEMENT & DEVELOPMENT(2) | |||

| Plains All American Pipeline | AMB Property LP, 6.625%, | |||||

| LP/PAA Finance Corp., | 12/1/19(3) | 160,000 | 171,256 | |||

| 8.75%, 5/1/19(3) | 190,000 | 236,625 | ||||

| ROAD & RAIL — 0.1% | ||||||

| Shell International Finance | CSX Corp., 7.375%, 2/1/19(3) | 150,000 | 179,841 | |||

| BV, 6.375%, 12/15/38(3) | 200,000 | 227,531 | ||||

| Shell International Finance | Union Pacific Corp., 5.75%, | |||||

| 11/15/17(3) | 340,000 | 370,428 | ||||

| BV, 5.50%, 3/25/40(3) | 100,000 | 101,738 | ||||

| Talisman Energy, Inc., 7.75%, | 550,269 | |||||

| 6/1/19(3) | 350,000 | 427,629 | SOFTWARE — 0.1% | |||

| Williams Partners LP, 5.25%, | Intuit, Inc., 5.75%, 3/15/17(3) | 254,000 | 273,987 | |||

| 3/15/20(3)(4) | 120,000 | 123,662 | SPECIALTY RETAIL — 0.2% | |||

| XTO Energy, Inc., 6.50%, | Home Depot, Inc. (The), | |||||

| 12/15/18(3) | 150,000 | 176,545 | 5.40%, 3/1/16(3) | 350,000 | 384,384 | |

| XTO Energy, Inc., 6.10%, | Home Depot, Inc. (The), | |||||

| 4/1/36(3) | 272,000 | 304,311 | 5.875%, 12/16/36(3) | 75,000 | 75,296 | |

| 5,665,535 | Lowe’s Cos., Inc., 4.625%, | |||||

| PAPER & FOREST PRODUCTS — 0.1% | 4/15/20(3) | 60,000 | 61,589 | |||

| International Paper Co., | Staples, Inc., 9.75%, | |||||

| 9.375%, 5/15/19(3) | 250,000 | 318,511 | 1/15/14(3) | 240,000 | 294,213 | |

| International Paper Co., | 815,482 | |||||

| 7.30%, 11/15/39(3) | 150,000 | 166,838 | TOBACCO(2) | |||

| 485,349 | Altria Group, Inc., 9.25%, | |||||

| PHARMACEUTICALS — 0.4% | 8/6/19(3) | 150,000 | 185,595 | |||

| Abbott Laboratories, 5.875%, | WIRELESS TELECOMMUNICATION SERVICES — 0.2% | |||||

| 5/15/16(3) | 100,000 | 114,394 | America Movil SAB de CV, | |||

| AstraZeneca plc, 5.40%, | 5.00%, 10/16/19(3)(4) | 200,000 | 202,177 | |||

| 9/15/12(3) | 295,000 | 323,405 | America Movil SAB de CV, | |||

| AstraZeneca plc, 5.90%, | 5.00%, 3/30/20(3)(4) | 110,000 | 111,305 | |||

| 9/15/17(3) | 200,000 | 226,835 | Rogers Cable, Inc., 6.25%, | |||

| GlaxoSmithKline Capital, Inc., | 6/15/13(3) | 180,000 | 199,826 | |||

| 4.85%, 5/15/13(3) | 180,000 | 196,064 | Rogers Communications, Inc., | |||

| Novartis Capital Corp., 4.40%, | 6.80%, 8/15/18(3) | 120,000 | 138,565 | |||

| 4/24/20(3) | 190,000 | 194,062 | SBA Telecommunications, | |||

| Pfizer, Inc., 7.20%, 3/15/39(3) | 170,000 | 211,697 | Inc., 8.25%, 8/15/19(3)(4) | 120,000 | 129,300 | |

| Watson Pharmaceuticals, | Vodafone Group plc, 5.45%, | |||||

| Inc., 5.00%, 8/15/14(3) | 410,000 | 431,467 | 6/10/19(3) | 110,000 | 115,995 | |

| Wyeth, 5.95%, 4/1/37(3) | 272,000 | 293,691 | 897,168 | |||

| 1,991,615 | TOTAL CORPORATE BONDS | |||||

| (Cost $49,711,379) | 52,880,286 | |||||

22

| Balanced | ||||||

| Shares/ | Shares/ | |||||

| Principal | Principal | |||||

| Amount | Value | Amount | Value | |||

| U.S. Government Agency | FNMA, 6.50%, 8/1/37(3) | $ 1,233,977 | $ 1,326,024 | |||

| Mortgage-Backed Securities(5) — 10.5% | FNMA, 6.50%, 6/1/47(3) | 58,302 | 62,742 | |||

| FNMA, 6.50%, 8/1/47(3) | 259,501 | 279,264 | ||||

| FHLMC, 7.00%, 10/1/12(3) | $ 41,928 | $ 44,364 | ||||

| FNMA, 6.50%, 8/1/47(3) | 269,229 | 289,732 | ||||

| FHLMC, 4.50%, 1/1/19(3) | 1,395,243 | 1,472,621 | ||||

| FNMA, 6.50%, 9/1/47(3) | 171,571 | 184,637 | ||||

| FHLMC, 6.50%, 1/1/28(3) | 90,438 | 99,435 | ||||

| FNMA, 6.50%, 9/1/47(3) | 200,351 | 215,609 | ||||

| FHLMC, 5.50%, 12/1/33(3) | 769,587 | 817,814 | ||||

| FNMA, 6.50%, 9/1/47(3) | 647,306 | 696,603 | ||||

| FHLMC, 5.50%, 1/1/38(3) | 2,083,374 | 2,205,468 | ||||

| GNMA, 7.00%, 4/20/26(3) | 151,685 | 169,536 | ||||

| FHLMC, 6.00%, 8/1/38(3) | 682,897 | 731,977 | ||||

| GNMA, 7.50%, 8/15/26(3) | 80,697 | 91,083 | ||||

| FHLMC, 6.50%, 7/1/47(3) | 121,338 | 131,089 | ||||

| GNMA, 7.00%, 2/15/28(3) | 32,480 | 36,456 | ||||

| FNMA, 6.50%, 5/1/11(3) | 3,732 | 3,891 | ||||

| GNMA, 7.50%, 2/15/28(3) | 38,108 | 43,065 | ||||

| FNMA, 7.50%, 11/1/11(3) | 43,247 | 45,147 | ||||

| GNMA, 7.00%, 12/15/28(3) | 38,627 | 43,355 | ||||

| FNMA, 6.50%, 5/1/13(3) | 2,523 | 2,722 | ||||

| GNMA, 7.00%, 5/15/31(3) | 170,289 | 191,325 | ||||

| FNMA, 6.50%, 5/1/13(3) | 5,154 | 5,560 | ||||

| GNMA, 5.50%, 11/15/32(3) | 1,027,051 | 1,099,619 | ||||

| FNMA, 6.50%, 6/1/13(3) | 904 | 975 | ||||

| FNMA, 6.50%, 6/1/13(3) | 8,106 | 8,744 | TOTAL U.S. GOVERNMENT AGENCY | |||

| MORTGAGE-BACKED SECURITIES | ||||||

| FNMA, 6.50%, 6/1/13(3) | 13,194 | 14,232 | (Cost $49,446,376) | 52,579,359 | ||

| FNMA, 6.50%, 6/1/13(3) | 13,602 | 14,672 | U.S. Government Agency Securities | |||

| FNMA, 6.00%, 1/1/14(3) | 48,183 | 51,884 | and Equivalents — 3.5% | |||

| FNMA, 6.00%, 4/1/14(3) | 174,741 | 188,164 | ||||

| FIXED-RATE U.S. GOVERNMENT | ||||||

| FNMA, 4.50%, 5/1/19(3) | 1,611,239 | 1,698,330 | AGENCY SECURITIES — 2.5% | |||

| FNMA, 5.00%, 9/1/20(3) | 2,383,094 | 2,538,265 | FHLB, 1.625%, 3/20/13(3) | 1,000,000 | 1,000,717 | |

| FNMA, 6.50%, 1/1/28(3) | 26,128 | 28,514 | FHLB, 1.875%, 6/21/13 | 2,000,000 | 2,009,030 | |

| FNMA, 7.00%, 1/1/28(3) | 86,448 | 96,590 | FHLMC, 2.875%, 2/9/15(3) | 2,900,000 | 2,933,350 | |

| FNMA, 6.50%, 1/1/29(3) | 103,561 | 114,118 | FNMA, 2.75%, 3/13/14(3) | 4,000,000 | 4,088,908 | |

| FNMA, 7.50%, 7/1/29(3) | 163,283 | 184,533 | FNMA, 5.00%, 2/13/17(3) | 2,200,000 | 2,418,605 | |

| FNMA, 7.50%, 9/1/30(3) | 54,514 | 61,596 | 12,450,610 | |||

| FNMA, 6.50%, 9/1/31(3) | 84,772 | 93,413 | GOVERNMENT-BACKED CORPORATE BONDS(6) — 1.0% | |||

| FNMA, 7.00%, 9/1/31(3) | 35,031 | 39,228 | Citigroup Funding, Inc., | |||

| 1.875%, 11/15/12(3) | 1,800,000 | 1,821,726 | ||||

| FNMA, 6.50%, 1/1/32(3) | 146,986 | 161,970 | ||||

| FNMA, 7.00%, 6/1/32(3) | 375,321 | 420,385 | GMAC, Inc., 1.75%, | |||

| 10/30/12(3) | 2,000,000 | 2,018,186 | ||||

| FNMA, 6.50%, 8/1/32(3) | 154,468 | 170,214 | ||||

| State Street Bank and Trust | ||||||

| FNMA, 5.50%, 6/1/33(3) | 1,039,415 | 1,103,577 | Co., 1.85%, 3/15/11(3) | 1,000,000 | 1,011,987 | |

| FNMA, 5.50%, 7/1/33(3) | 1,300,641 | 1,380,929 | 4,851,899 | |||

| FNMA, 5.50%, 8/1/33(3) | 1,193,089 | 1,266,738 | TOTAL U.S. GOVERNMENT AGENCY | |||

| FNMA, 5.50%, 9/1/33(3) | 753,311 | 799,812 | SECURITIES AND EQUIVALENTS | |||

| (Cost $16,933,756) | 17,302,509 | |||||

| FNMA, 5.00%, 11/1/33(3) | 3,793,092 | 3,961,884 | ||||

| FNMA, 5.50%, 1/1/34(3) | 5,493,665 | 5,833,613 | Commercial Mortgage-Backed | |||

| Securities(5) — 1.2% | ||||||

| FNMA, 4.50%, 9/1/35(3) | 3,541,881 | 3,604,455 | ||||

| FNMA, 5.00%, 2/1/36(3) | 4,050,043 | 4,216,348 | Commercial Mortgage | |||

| Pass-Through Certificates, | ||||||

| FNMA, 5.50%, 4/1/36(3) | 1,687,864 | 1,784,670 | Series 2004 LB3A, Class A4 | |||

| FNMA, 5.50%, 5/1/36(3) | 3,362,250 | 3,555,089 | SEQ, VRN, 5.23%, 5/3/10(3) | 600,000 | 624,595 | |

| FNMA, 5.50%, 2/1/37(3) | 1,163,389 | 1,228,296 | ||||

| FNMA, 6.00%, 7/1/37 | 7,200,430 | 7,668,983 | ||||

23

| Balanced | ||||||

| Shares/ | Shares/ | |||||

| Principal | Principal | |||||

| Amount | Value | Amount | Value | |||

| Commercial Mortgage | Collateralized Mortgage | |||||

| Pass-Through Certificates, | ||||||

| Series 2005 F10A, Class A1, | Obligations(5) — 0.8% | |||||

| VRN, 0.35%, 5/17/10, resets | PRIVATE SPONSOR COLLATERALIZED | |||||

| monthly off the 1-month | MORTGAGE OBLIGATIONS — 0.5% | |||||

| LIBOR plus 0.10% with | Banc of America Alternative | |||||

| no caps(3)(4) | $ 46,428 | $ 45,458 | ||||

| Loan Trust, Series 2007-2, | ||||||

| Credit Suisse Mortgage | Class 2A4, 5.75%, 6/25/37(3) | $ 736,078 | $ 535,452 | |||

| Capital Certificates, Series | Countrywide Home Loan | |||||

| 2007 TF2A, Class A1, VRN, | Mortgage Pass-Through Trust, | |||||

| 0.43%, 5/17/10, resets | Series 2005-17, Class 1A11, | |||||

| monthly off the 1-month | 5.50%, 9/25/35(3) | 477,275 | 456,790 | |||

| LIBOR plus 0.18% with | ||||||

| no caps(3)(4) | 584,918 | 519,653 | Countrywide Home Loan | |||

| Mortgage Pass-Through Trust, | ||||||

| Greenwich Capital | Series 2007-16, Class A1, | |||||

| Commercial Funding Corp., | 6.50%, 10/25/37(3) | 403,011 | 349,344 | |||

| Series 2006 FL4A, Class A1, | ||||||

| VRN, 0.34%, 5/5/10, resets | Credit Suisse First Boston | |||||

| monthly off the 1-month | Mortgage Securities Corp., | |||||

| LIBOR plus 0.09% with | Series 2003 AR28, Class 2A1, | |||||

| no caps(3)(4) | 79,625 | 75,039 | VRN, 3.05%, 5/3/10(3) | 692,963 | 662,690 | |

| GS Mortgage Securities | MASTR Alternative Loans | |||||

| Corp. II, Series 2005 GG4, | Trust, Series 2003-8, | |||||

| Class A4A SEQ, 4.75%, | Class 4A1, 7.00%, 12/25/33(3) | 61,655 | 62,032 | |||

| 7/10/39(3) | 1,000,000 | 1,023,628 | Wells Fargo Mortgage- | |||

| LB-UBS Commercial | Backed Securities Trust, | |||||

| Mortgage Trust, Series | Series 2005-17, Class 1A1, | |||||

| 2004 C2, Class A4 SEQ, | 5.50%, 1/25/36 | 431,550 | 414,319 | |||

| 4.37%, 3/15/36(3) | 1,000,000 | 1,013,392 | 2,480,627 | |||

| LB-UBS Commercial | U.S. GOVERNMENT AGENCY COLLATERALIZED | |||||

| Mortgage Trust, Series | MORTGAGE OBLIGATIONS — 0.3% | |||||

| 2005 C2, Class A2 SEQ, | FHLMC, Series 77, Class H, | |||||

| 4.82%, 4/15/30(3) | 870,688 | 870,679 | 8.50%, 9/15/20(3) | 164,791 | 182,989 | |

| Merrill Lynch Floating Trust, | FHLMC, Series 2926, | |||||

| Series 2006-1, Class A1, | Class EW SEQ, 5.00%, | |||||

| VRN, 0.32%, 5/17/10, resets | 1/15/25(3) | 1,200,000 | 1,271,998 | |||

| monthly off the 1-month | ||||||

| LIBOR plus 0.07% with | 1,454,987 | |||||

| no caps(3)(4) | 536,869 | 502,219 | TOTAL COLLATERALIZED | |||

| Morgan Stanley Capital I, | MORTGAGE OBLIGATIONS | |||||

| Series 2003 T11, Class A3 | (Cost $4,026,280) | 3,935,614 | ||||

| SEQ, 4.85%, 6/13/41(3) | 405,558 | 413,500 | Municipal Securities — 0.6% | |||

| Wachovia Bank Commercial | California GO, (Building | |||||

| Mortgage Trust, Series | Bonds), 7.30%, 10/1/39(3) | 400,000 | 430,636 | |||

| 2004 C11, Class A3, 4.72%, | ||||||

| 1/15/41(3) | 300,000 | 304,199 | Illinois GO, (Taxable Pension), | |||

| 5.10%, 6/1/33(3) | 300,000 | 259,758 | ||||

| Wachovia Bank Commercial | ||||||

| Mortgage Trust, Series | Illinois GO, Series 2010-3, | |||||

| 2006 C23, Class A4, VRN, | (Building Bonds), 6.73%, | |||||

| 5.42%, 5/3/10(3) | 500,000 | 508,810 | 4/1/35 | 110,000 | 114,303 | |

| TOTAL COMMERCIAL | Missouri Highways & | |||||

| MORTGAGE-BACKED SECURITIES | Transportation Commission | |||||

| (Cost $5,986,517) | 5,901,172 | Rev., (Building Bonds), | ||||

| 5.45%, 5/1/33(3) | 130,000 | 130,424 | ||||

24

| Balanced | ||||||

| Shares/ | Shares/ | |||||

| Principal | Principal | |||||

| Amount | Value | Amount | Value | |||

| Municipal Electric Auth. | Sovereign Governments & | |||||

| of Georgia Rev., (Building | ||||||

| Bonds), 6.64%, 4/1/57(3) | $ 190,000 | $ 201,398 | Agencies — 0.2% | |||