Opportunities for Growth:

SouthStar Energy Services

Mike Braswell

President, SouthStar Energy Services

2007 Analyst Conference

March 22, 2007

New York

1

Objectives

•

Present a general overview of SouthStar’s retail natural gas business

•

Provide overview of governance and management processes, including key business risks and mitigations

•

Review factors that have contributed to the Company’s success

•

Discuss the path forward and how SouthStar is positioned to adapt to future challenges and opportunities

2

Business Summary

Financials

•

Partnership between AGL Resources and Piedmont Natural Gas

•

One of the largest deregulated retail natural gas marketing companies in the United States

•

Serve customers in seven states, specifically GA, OH, AL, TN, NC, SC and FL

•

Manage one of the largest portfolios of Southeastern pipeline and storage assets

•

Approximately 75 employees and over 200 additional FTEs supporting business through customer operations BPO

•

Revenues of approximately $1B in 2006

•

Earnings of approximately $92M* in 2006 (EBT)

•

Six-year earnings growth of 34% (EBT CAGR)

•

Strong cash-flow producing business with 100% distribution of earnings in

2004, 2005 and 2006

2004, 2005 and 2006

* Results represent 100% of SouthStar which are split 75% AGLR and 25% Piedmont.

Summary of Partnership Facts

3

Customers

Volumes

Corporate Citizenship

•

Largest marketer in GA

•

Serve 550k Georgia residential, commercial and industrial customers

•

515k residential

•

35k small C&I

•

Approx. 300 large C&I customers in the Southeast

•

Serve as supplier for Dominion East Ohio’s Standard Service Offering (SSO)

•

5 Bcf per year

•

Agreement expires August 2008

•

Approximately 70 Bcf of gas sales in 2006

•

Access to 15 Bcf of storage and 350,000 DT/day of pipeline capacity

•

7 Bcf Production area (Gulf Coast)

•

5 Bcf Market area – Georgia market

•

2 Bcf AGLC LNG

•

1 Bcf DEO SSO assigned

•

Voted one of the 75 Best Places to Work by Atlanta Magazine

•

National Points of Light Award recipient in 2005

Summary of Partnership Facts (continued)

4

AGL

Resources

Piedmont Natural

Gas Company

Georgia Natural

Gas Company

Piedmont Energy

Company

SouthStar

Energy Services

Georgia

Natural

Gas

Gas

Ohio

Natural

Gas

Gas

Florida

Natural

Gas

Gas

Piedmont

Energy

Company

Overview

•

Formed in 1998 as an LLC between AGL Resources, Piedmont and Dynegy

•

Dynegy exited in 2003

•

Current equity ownership is 70% AGL Resources and 30% Piedmont

•

Earnings sharing is 75% to AGL Resources and 25% to Piedmont except for Ohio and

Florida earnings, which are shared 70% to AGL Resources and 30% to Piedmont

Florida earnings, which are shared 70% to AGL Resources and 30% to Piedmont

•

Governance and key decision responsibilities are shared 50/50

Ownership Structure

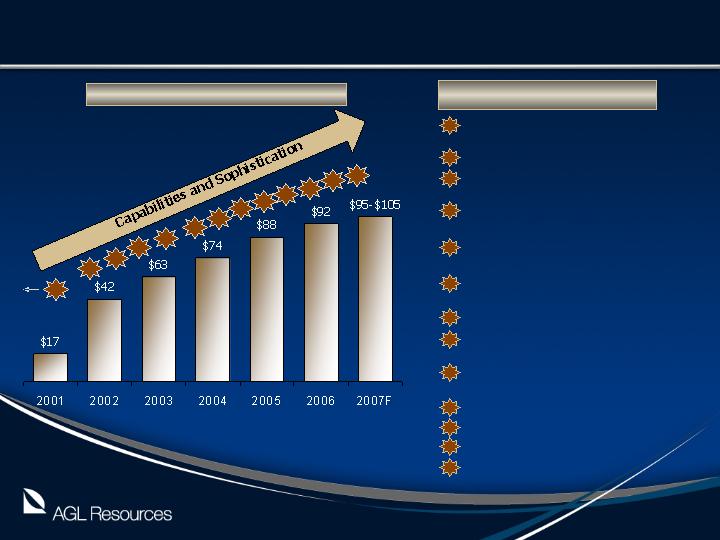

5

1

3

4

5

6

7

8

9

10

11

1998

2

13

12

* Results represent 100% of SouthStar which are spli 75% AGLR and 25% Piedmont t

34% Compounded Annual Growth

EBT* ($ millions)

Legend

n

Outsourced asset mgt to Dynegy Marketing and Trading (DM&T)

n

Consumer Relief Act enacted

n

Executed new customer care outsourcing agreement

n

Terminated agreement with DM&T and internalized asset mgt function

n

Instituted credit criteria for new service application

n

Installed Siebel for sales force autormation

n

Re-introduced Gas Guy

n

Introduced formal processes for disaggregating natural exposures

n

Expanded financial hedging operation & talent acquisition

n

Upgraded retail billing system

n

Completed Allegro ETRM installation

n

Entered Ohio and Florida markets

n

Acquired Commerce Energy’s GA book

1

2

3

4

5

6

7

8

9

10

11

12

13

Milestones and Earnings Growth

6

Manage risks inherent to retail marketing

business

business

Build and leverage a strong portfolio of brands

Manage retail customer portfolio for

profit

profit

Create incremental value from asset management

Proactively manage

changes to

market model

changes to

market model

Brands

Retail Book

Assets

Risks

Legislative & Regulatory Process

SouthStar

Competencies

Keys To Success

7

Profitability

Drivers

Priority

Strategy Implications

Gas Margin per Customer

•

Pricing strategy and portfolio management

•

Increase revenue from asset optimization and

commodity price risk management

High

•

Continues to be the most

significant profit lever

Customer

Count/

Market Share

Market Share

•

Increase acquisition rates for prospective customers

already calling our call center

•

Target single-family customers at natural decision

point of choosing a gas provider

•

Acquire high-value switchers with special price

plans, incentives, targeted messaging and new services

•

Target larger ACN (multi-family) accounts while

shedding smaller, less profitable ACNs

Moderate

•

Remains a lever over

the long term, though

less significant on an

annual basis

less significant on an

annual basis

Operating

Expenses

•

Seek opportunities for cost savings in the customer

care BPO services

•

Continue to reduce bad debt expenses through

portfolio high-grading, automated collection calls,

prioritization of delinquency paths and use of multiple collection agencies

prioritization of delinquency paths and use of multiple collection agencies

Moderate

•

Currently not a major

lever, but requires

continued focus;

Customer care

expenses may have

higher opportunity if

these services are

off-shored

continued focus;

Customer care

expenses may have

higher opportunity if

these services are

off-shored

Retail Profitability Drivers

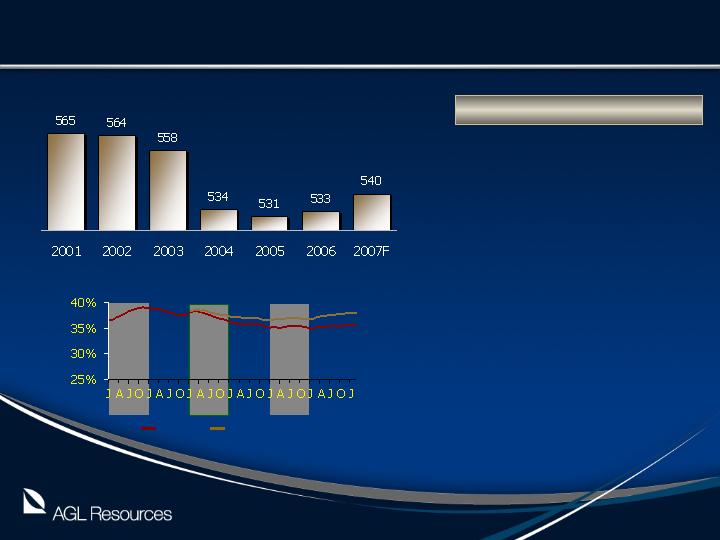

8

Average Georgia Firm Customer Count

(000's)

Comments

•

Customer retention actions focused on high-grading the customer portfolio

•

Customer segmentation analysis used to shift from broad-based to focused

marketing and advertising

marketing and advertising

•

Increased use of price plans to attract and retain high-value customers

•

Less profitable customers de-emphasized, e.g. ACNs

Market Share

2001

2002

2003

2004

2005

2006

Total

Deregulated Only

Customer Count and Market Share

9

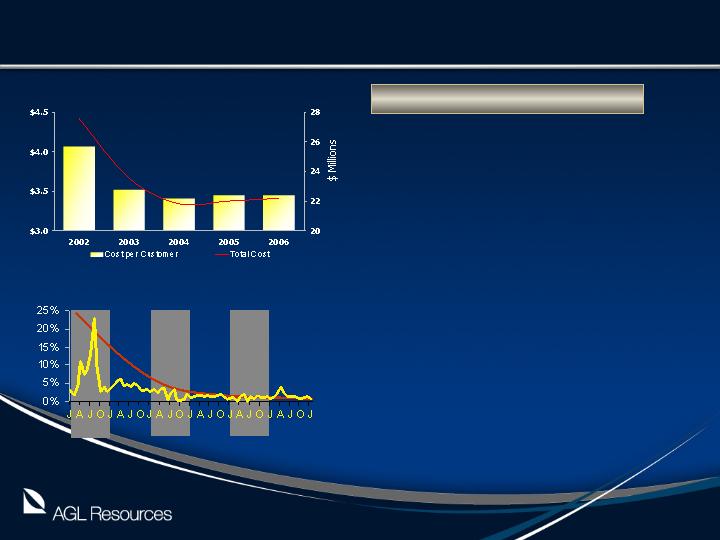

Customer Care Expense

Average Monthly Cost per Customer and Total Cost

Comments

•

Customer care is largest O&M expense

•

Outsourced to Alliance Data Systems (ADS)

•

Partnered with ADS to reduce key cost drivers

•

Call volume

•

Call minutes / duration

•

Additional benefits attained through high-grading retail book

•

High-value customers cost less to serve

•

Bad debt is second largest O&M expense

•

More difficult to manage prior to the Natural Gas Consumers Relief Act

•

Initiated a regulated provider to serve low income and credit-challenged customers

•

Portfolio high-grading and collection process improvements implemented to address bad debt

•

Actions reduced bad debt exposure and percentage has been stable for past 24 months

Bad Debt Expense

Bad Debt Expense as a Percent of Revenue

2001

2002

2003

2004

2005

2006

Key Operating Expenses

10

Profitability

Drivers

Priority

Strategy Implications

Storage

Margins

•

Use synthetic puts to lock in margins and participate

in upside potential

•

Balance economic opportunities with operational

constraints

•

High

•

Most significant

earnings lever –

dependent on spreads

dependent on spreads

Pipeline

Capacity

Optimization

Optimization

•

Leverage interruptible portfolio

•

Maintain relationships with counterparties for

secondary releases

•

Optimize daily paths to capture city-gate arbitrage

opportunities

•

Moderate

•

Less significant

earnings driver, but has

higher degree of

certainty than storage

higher degree of

certainty than storage

Portfolio

Risk

Management

Management

•

Identify and assess risks on a stand-alone basis

•

Evaluate portfolio effect of natural offsets

•

Examples of correlated positions that have natural

offsetting potential are:

•

Unhedged inventory and price lag

•

Weather, swing and physical setup

•

High

•

Significant lever to

reduce risk

management costs

using the portfolio

effect

management costs

using the portfolio

effect

Commercial Profitability Drivers

11

Natural Offsets – Storage and Lag

(Contracts)

Economic Storage Gross Margins*

($ Millions)

Pipeline Capacity Utilization

2007F

2008F

Trade Liquidity

($ Millions)

$10

$128

$173

$311

$395

$480

* Represents economic contribution of storage exclusive of accounting adjustments such as LOCOM and fixed demand charges

Commercial Operations Metric Overview

12

Exposure | Position | Natural Offset | Description | Management Tools |

Swing | Neutral | These exposures are highly correlated and are managed together. | Volumetric risk associated with selling full requirements contracts to firm customers. This exposure changes daily and is highly volatile. | GDD swaps and setup, storage |

Weather | Neutral | Volumetric risk associated with weather variations. Exposure is to warmer-than-normal winter, which results in a complete loss of expected margin. Colder-than-normal winter is beneficial, as it typically results in incremental margin. | Retail derivative products, CME weather derivatives/ physical setup | |

Storage Inventory | Long | Natural offsets. Derivatives used to manage the net position, but will disaggregate the positions when the value of one exposure outweighs the cost of managing the other. | Our largest natural long position. Increasing length throughout the summer. Managed to ensure margin capture and winter reliability. | Nymex swaps and options |

Price Effectuati on | Short | Our largest natural short position. Roughly half the firm gas we sell at our monthly price is sold in the subsequent month and is therefore exposed to the floating subsequent month’s index. | Nymex swaps and options |

Exposures in Deregulated Retail Model

13

Exposure | Position | Natural Offset | Description | Management Tools |

Fixed Price | Short | None | A natural short price position created by selling full requirements, fixed price contracts to our customers. Derivatives used to manage these positions. | Nymex swaps |

Supply Reliability | Short | None | Entire 70 Bcf portfolio must be supplied except for Force Majeure declarations. Risk of non-delivery is $30/dt plus cost of gas. | Supply diversity through multiple counterparties and geographic dispersion |

Exposures in Deregulated Retail Model

14

Identify Risks

Control Risks

•

Risks are controlled by:

•

Evaluating the entire portfolio to

determine whether natural

hedges exist

hedges exist

•

Where natural hedges do not

exist, utilize financial derivatives

to hedge residual exposures

to hedge residual exposures

•

SSE generally prefers to hedge

residual exposure with options in

order to retain upside potential

order to retain upside potential

•

Option premiums are a finite

cost versus the unknown cost /

opportunity cost of swaps in

isolation

opportunity cost of swaps in

isolation

SouthStar’s Hedging Philosophy

•

Risks inherent to retail gas

marketing business

•

Commodity price risk

(fixed price, inventory,

swing)

swing)

•

Basis risk

•

Throughput risk

•

Credit risk

•

Each category of risk is

identified and evaluated on

an isolated, independent

basis

an isolated, independent

basis

15

•

Capture spreads and manage risks

•

Manage retail customer portfolio

•

Monitor competitor activities

•

Proactively participate in regulatory and market development processes

Areas of Focus

Element

Maintain

Operational

Focus

Focus

Strengthen

Platform

•

Focus on platform elements that address:

•

Increased competition

•

Greater market sophistication

•

Improved growth opportunities

•

Examples include:

•

Banner Customer Information System upgrade

•

Siebel CRM enhancements

•

Allegro ETRM implementation

Keys To Continued Growth

16

Options

Growth Area

Strategy

Existing

Markets

Retail – GA Organic

Acquire high-value customers

New Products / Services to Leverage

Customer Base

Evaluate and introduce new products

and services

Acquire and leverage incremental assets

Target small muni’s in SE

Expanded

Markets

Emerging Retail Markets – OH and

FL (C&I)

Use multiple entry approaches to

identify and capture opportunities

-Dominions East Oio and Vectren SSO

- Retail model / market shaping

advocacy

- - Marketing partner relationships

- Inorganic opportunities

- Retail model / market shaping

advocacy

- - Marketing partner relationships

- Inorganic opportunities

Large C&I

Leverage SSE’s assets

Large C&I

Aggregate C&I books and leverage

SSE’s platform

Growth Areas Under Development

17

Conclusions

•

Strong retail organization with capabilities that span

customer and asset portfolios

•

Well defined governance, disciplined leadership and

effective risk management

•

Operated with focus on the levers that produce

financial results

•

Able to apply capabilities, infrastructure and

experiences to new opportunities

18

Questions?

19