Opportunities for Growth:

Sequent Energy Management

Doug Schantz

President, Sequent Energy Management

2007 Analyst Conference

March 22, 2007

New York

1

Business Model – “How We Make Money”

What We Are:

•

A company with a core strength in physical logistics and optimization of transportation and storage

•

Locational spreads (transportation capacity)

•

Physical storage spreads (cash, futures, time)

•

A business that adds and creates value by understanding and meeting customers’ needs as well as by optimizing gas flows from supply basin to market center

•

Service provider (asset management, producer & peaking services)

•

Leading manager of contractual storage and transportation assets in theEastern part of the U.S.

•

An organization of 130 people supported by strong systems, processes and controls

2

Business Model – “How We Make Money”

What We Are Not:

•

Holder of large outright speculative positions

•

Modest risk limits (VaR, credit, basis)

•

Financial market-maker

3

Sequent’s business model includes a portfolio of assets and services that enable it to capture value in a variety of market

conditions.

conditions.

In any given year:

•

The proportion of segmentschanges with market conditions

•

Sequent has the ability tocapture value in a dynamic environment

For example:

•

2005 – heavy transportation activity

•

2006 – heavy storage activity

Dynamic Model

4

Egan

JISH

Moss

Bluff

Pipeline Capacity

•

Business conducted on 55 pipelines

•

Significant transport on:

TranscoTETCO GulfSouth

FGT ANR Sonat

Dominion Columbia Tennessee

El Tenn. Northwest Texas Gas

Sabine

Storage Capacity

•

More than 88 Bcf of capacity under

management

•

Includes 5 Bcf of salt-dome storage at Egan, Moss Bluff and Jefferson Island

Pipelines & Storage

5

Material Asset Management Transactions

Egan

JISH

Saltville

Pipelines

Boise, Idaho

Moss

Bluff

Material Asset Management

Transactions

Transactions

A Strategic Portfolio of Contractual Storage and Transportation Assets

6

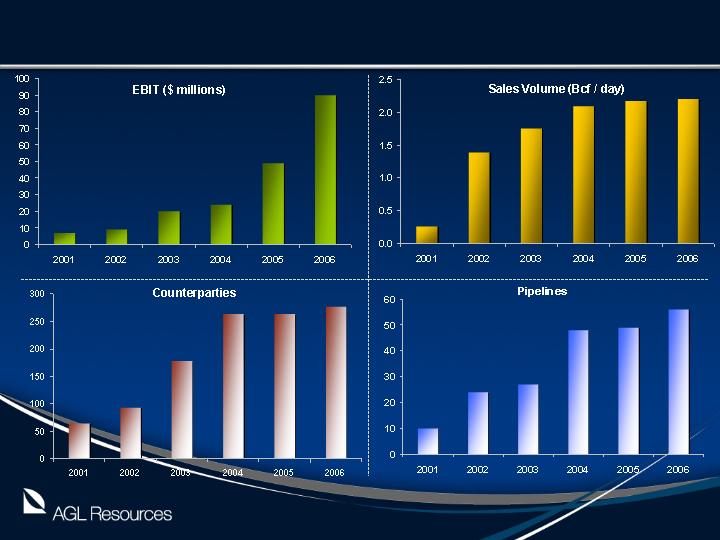

A Story of Growth

7

A Story of Growth (cont.)

8

Analysis of 2006 and Bridge to 2007

9

Weighted average portfolio credit rating of A-

As of January 31, 2007

Credit Metrics

10

Growth Initiatives

•

Move west and into Canada

•

More penetration of the power generation business

•

Contract additional salt dome storage capacity

•

Contract key West to East transportation corridors

•

Aggressively expand producer services activities

•

Set up and build commercial and industrial marketing effort

11

2007/2008

Current Footprint

4

Geographic Footprint Expansion

12

Sequent Beyond 2007

•

“Song Remains the Same” – the business model is sound

•

Growth in “baseline earnings” of about 10% / year

•

Opportunity to earn more with high volatility

•

Leverage investments in systems and processes

•

“Economies of scale” benefit in mid and back office

•

Focus on bench strength will provide headroom

•

Provide AGL Resources with substantial market intelligence

13

Questions?

14