As filed with the Securities and Exchange Commission on May 17, 2012.

Registration No. 333-

United States

Securities and Exchange Commission

Washington, D.C. 20549

FORM F-4

REGISTRATION STATEMENT

Under

The Securities Act of 1933

Celulosa Arauco y Constitución S.A.

(Exact name of Registrant as specified in its charter)

Arauco and Constitution Pulp Inc.

(Translation of Registrant’s name into English)

| | |

| Republic of Chile | | Not Applicable |

(State or Other Jurisdiction of Incorporation or Organization) | | (I.R.S. Employer Identification No.) |

Avenida El Golf 150, 14th Floor

Santiago, Chile

+56-2-461-7200

(Address and telephone number of Registrant’s principal executive offices)

CT Corporation System

111 Eighth Avenue

New York, New York 10011

(212) 894-8940

(Name, address and telephone number of agent for service)

Copies of communications to:

David L. Williams, Esq.

Simpson Thacher & Bartlett, LLP

425 Lexington Avenue

New York, New York, 10017

(212) 455-2000

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement and the satisfaction or waiver of all other conditions to the exchange offer described in the accompanying prospectus.

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

CALCULATION OF REGISTRATION FEE

| | | | | | | | |

|

Title of each class of

Securities to be Registered | | Amount to be Registered | | Proposed Aggregate Offering Price Per Note | | Proposed Maximum

Aggregate Offering Price (1) | | Amount of

Registration Fee |

4.750% Notes due 2022 | | $500,000,000 | | 98.53% | | $500,000,000 | | $57,300 |

|

|

| (1) | The securities being registered are offered (i) in exchange for 4.750% Notes due 2022 previously sold in transactions exempt from registration under the Securities Act of 1933 and (ii) upon certain resales of the notes by broker-dealers. The registration fee has been computed based on the face value of the notes solely for the purpose of calculating the amount of the registration fee, pursuant to Rule 457 under the Securities Act of 1933. |

The Registration hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The Information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, dated May 17, 2012

Prospectus

Celulosa Arauco y Constitución S.A.

U.S.$500,000,000

Offer to Exchange All Outstanding

4.750% Notes due 2022

For an Equal Principal Amount of

4.750% Notes due 2022

Which Have Been Registered Under the Securities Act of 1933

| | |

The Exchange Offer • We will exchange all outstanding notes that are validly tendered and not validly withdrawn for an equal principal amount of exchange notes that are freely tradeable. • You may withdraw tenders of outstanding notes at any time prior to the expiration of the exchange offer. • The exchange offer expires at 5:00 PM, New York City time, on , 2012, unless extended. We do not currently intend to extend the expiration date. • The exchange of outstanding notes for exchange notes in the exchange offer will not be a taxable event for United States federal income tax or Chilean tax law purposes. • We will not receive any proceeds from the exchange offer. | | The Exchange Notes • The exchange notes are being offered in order to satisfy our obligations under the registration rights agreement entered into in connection with the placement of the outstanding notes. • The terms of the exchange notes to be issued in the exchange offer are substantially identical to the outstanding notes, except that the exchange notes will be freely tradeable. Resales of Exchange Notes • The exchange notes may be sold in the over-the-counter market, in negotiated transactions or through a combination of such methods. We do not plan to list the exchange notes on a national market. |

If you are a broker-dealer and you receive exchange notes for your own account, you must acknowledge that you will deliver a prospectus in connection with any resale of such exchange notes. By making such acknowledgment, you will not be deemed to admit that you are an underwriter under the U.S. Securities Act of 1933, as amended, or the “Securities Act.” Broker-dealers may use this prospectus in connection with any resale of exchange notes received in exchange for outstanding notes where such outstanding notes were acquired by the broker-dealer as a result of market-making activities or trading activities. We have agreed that, for a period of 180 days after the expiration of the exchange offer or until any broker-dealer has sold all registered notes held by it, we will make this prospectus available to such broker-dealer for use in connection with any such resale. A broker dealer may not participate in the exchange offer with respect to outstanding notes acquired other than as a result of market-making activities or trading activities. See “Plan of Distribution.”

If you are an affiliate of ours or are engaged in, or intend to engage in, or have an agreement or understanding to participate in, a distribution of the exchange notes, you cannot rely on the applicable interpretations of the U.S. Securities and Exchange Commission, or the “SEC,” and you must comply with the registration requirements of the Securities Act in connection with any resale transaction.

You should consider carefully therisk factors beginning on page 10 of this prospectus before participating in the exchange offer.

Neither the SEC nor any state securities commission has approved or disapproved of the exchange notes or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2012

TABLE OF CONTENTS

This prospectus does not constitute an offer to sell, or a solicitation of an offer to buy, any exchange notes offered hereby in any jurisdiction where, or to any person to whom, it is unlawful to make such offer or solicitation. The information contained in this prospectus speaks only as of the date of this prospectus unless the information specifically indicates that another date applies. No dealer, salesperson or other person has been authorized to give any information or to make any representations other than those contained or incorporated by reference in this prospectus in connection with the offer contained herein and, if given or made, such information or representations must not be relied upon as having been authorized by us. Neither the delivery of this prospectus nor any sale made hereunder shall under any circumstances create an implication that there has been no change in our affairs or that of our subsidiaries since the date hereof.

ii

WHERE YOU CAN FIND MORE INFORMATION

We are subject to the information reporting requirements of Section 13(a) of the U.S. Securities Exchange Act of 1934, as amended, or the “Exchange Act,” and file reports and other information with the SEC that apply to foreign private issuers. We file annual reports on Form 20-F which include since January 1, 2009, our consolidated financial statements prepared in accordance with the International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”) and prior to our transition to IFRS, our consolidated financial statements were prepared in accordance with generally accepted accounting principles in the United States, or U.S. GAAP. Historically, we have filed reports on Form 6-K containing our unaudited quarterly consolidated financial statements and certain other information prepared in accordance with accounting principles generally accepted in Chile, or “Chilean GAAP.” For Chilean statutory reporting purposes, effective as of January 1, 2009, we were required to prepare our annual audited consolidated financial statements and our unaudited interim consolidated financial statements in accordance with IFRS. Therefore, our financial statements as of and for the year ended December 31, 2009 were our first annual audited consolidated financial statements required to be prepared in accordance with IFRS. These reports and other information we file with the SEC can be inspected and copied at the SEC’s Public Reference Room at 100 F Street N.E., Washington, D.C. 20549. Please call 1800-SEC-0330 for further information on the operation of the Public Reference Room. Such material may also be accessed electronically at the SEC’s home page at http://www.sec.gov. As a foreign private issuer, we are exempt from certain provisions of the Exchange Act, including those prescribing the furnishing and content of proxy and information statements and certain periodic reports.

We have filed with the SEC a registration statement on Form F-4 under the Securities Act with respect to the exchange notes offered hereby. This prospectus, which constitutes a part of the registration statement, does not contain all the information contained in the registration statement. We have omitted certain items from the prospectus as permitted by the rules and regulations of the SEC. For more information with respect to us and the exchange notes, refer to the registration statement, including the accompanying exhibits, financial statements, schedules and notes. You may inspect the registration statement without charge at the principal office of the SEC in Washington, D.C. and copies of all or part of it may be obtained from the SEC upon payment of the prescribed fee. Statements made in this prospectus concerning the contents of any document referred to herein are not necessarily complete. The exhibits accompanying any document referred to in this prospectus are essential for a more complete description of the matter involved.

iii

INCORPORATION OF CERTAIN DOCUMENTS BY REFERENCE

We are incorporating by reference certain information we filed with the SEC, which means that we are disclosing important information to you by referring you to those documents. The information we incorporate by reference is an important part of this prospectus, and certain information that we file later with the SEC will automatically update and supersede this information. We incorporate by reference herein the following documents:

| | • | | our annual report on Form 20-F for the year ended December 31, 2011, or the “2011 Form 20-F”, as filed with the SEC on April 30, 2012 (SEC file number 033-99720); |

In addition, all reports on Form 20-F filed by us with the SEC pursuant to Sections 13(a), 13(c), 14 or 15(d) of the Securities Exchange Act and, to the extent expressly stated therein, certain reports on Form 6-K subsequent to the date of this prospectus and prior to the termination of the offering of the exchange notes, shall also be deemed to be incorporated by reference into this prospectus from the date of filing of such documents. Any statements contained herein or in a document incorporated or deemed to be incorporated by reference herein or attached as an annex hereto shall be deemed to be modified or superseded for purposes of this prospectus, to the extent that a statement contained herein or in any other subsequently filed document and deemed to be incorporated by reference herein modifies or supersedes such statement. Any statement or document so modified or superseded shall not be deemed, except as so modified or superseded, to constitute a part of this prospectus.

We will provide without charge to you, upon your written or oral request, a copy of any or all the documents we incorporate by reference (other than exhibits, unless such exhibits are specifically incorporated by reference in such documents). Written requests for such copies should be directed to:

Celulosa Arauco y Constitución S.A.

Avenida El Golf 150, 14th Floor

Santiago, Chile

Attention: Gianfranco Truffello

Telephone requests may be directed to Mr. Gianfranco Truffello at +56-2-461-7200.

iv

ENFORCEABILITY OF CIVIL LIABILITIES

We are a corporation (sociedad anónima) organized under the laws of Chile and subject to certain rules applicable to Chilean public corporations (sociedades anónimas abiertas). Most of our directors and executive officers, and certain experts named or mentioned in this prospectus or other documents incorporated by reference herein, reside outside the United States. A substantial portion of our assets and the assets of these persons are located outside the United States. As a result, except as described below, it may not be possible for investors to effect service of process within the United States upon such persons or to enforce against them or against us in United States courts a judgment obtained in United States courts based upon the civil liability provisions of the federal securities laws of the United States. We have been advised by our Chilean counsel, Portaluppi, Guzmán y Bezanilla, that no treaty exists between the United States and Chile for the reciprocal enforcement of foreign judgments. Chilean courts, however, have enforced judgments rendered by courts in the United States by virtue of the legal principles of reciprocity and comity, subject to review in Chile of such judgment in order to determine whether certain basic principles of due process and public policy have been respected, without reviewing the merits of the subject matter of the case. Nevertheless, we have been advised by our Chilean counsel that there is doubt as to the enforceability, in original actions in Chilean courts, of liabilities predicated solely upon the federal securities laws of the United States and as to the enforceability in Chilean courts of judgments of United States courts obtained in actions based upon the civil liability provisions of the federal securities laws of the United States. In addition, it will be necessary for investors to comply with certain procedures, including payment of stamp taxes (currently assessed at a rate of 0.6% of the face value of a debt security), if applicable, in order to file a lawsuit with respect to the notes in a Chilean court.

We have appointed CT Corporation System as our authorized agent upon whom process may be served in any action arising out of or based upon the indenture or the issuance of the exchange notes. With respect to such actions, we have submitted to the jurisdiction of any federal or state court having subject matter jurisdiction in the Borough of Manhattan, the City of New York, New York. See “Description of the Exchange Notes.”

v

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This prospectus and the documents incorporated by reference contain words, such as “believe,” “intend,” “estimate,” “project,” “expect” and “anticipate” and similar expressions that identify forward-looking statements which reflect our views about future events and financial performance. Statements that are not historical facts, including statements about beliefs and expectations, are forward-looking statements. Forward-looking statements are not guarantees of future performance and involve inherent risks and uncertainties. These forward-looking statements are based on current plans, estimates and projections, and therefore you should not place undue reliance on them. Actual results could differ materially and adversely from those projected in the forward-looking statements as a result of various factors that may be beyond our control, including but not limited to:

| | • | | our ability to service our debt, fund our working capital requirements and comply with financial covenants in certain of our debt instruments; |

| | • | | our ability to fund and implement our capital expenditure programs; |

| | • | | the maintenance of relationships with customers; |

| | • | | future demand for forestry and wood products in our export markets; |

| | • | | international prices for forestry and wood products; |

| | • | | the condition of our forests; |

| | • | | possible shortages of energy, including electricity; |

| | • | | the state of the Chilean, Argentine, Brazilian, Uruguayan and world economies and manufacturing industries; |

| | • | | the relative value of the Chilean peso, Argentine peso, Brazilian real and Uruguayan peso compared to other currencies; |

| | • | | the effects of earthquakes, floods, tsunamis or other catastrophic events; |

| | • | | the effects from competition; |

| | • | | increases in interest rates; and |

| | • | | changes in our regulatory environment, including our ability to comply with new or stricter environmental regulations and to resolve environmental liabilities. |

In any event, these statements speak only as of their dates, and we do not undertake any obligation to update or revise any of them as a result of new information, future events or otherwise.

vi

PRESENTATION OF FINANCIAL DATA

For Chilean statutory reporting purposes, effective as of January 1, 2009, we were required to prepare our annual audited consolidated financial statements and our unaudited interim consolidated financial statements in accordance with IFRS. Therefore, our financial statements as of and for the year ended December 31, 2009 were our first annual audited consolidated financial statements required to be prepared in accordance with IFRS. Our consolidated financial information as of and for the year ended December 31, 2008 included in our audited consolidated financial statements was restated in accordance with IFRS. For SEC reporting purposes, we prepare our audited annual consolidated financial statements in accordance with IFRS.

IFRS differs in certain significant respects from U.S. GAAP. As a result, our financial information presented under IFRS is not directly comparable to our financial information presented under U.S. GAAP, and readers should avoid such a comparison.

References in this prospectus to “$,” “U.S.$,” “U.S. dollars” and “dollars” are to United States dollars, references to “Chilean pesos” or “Ch$” are to Chilean pesos, references to “UF” are to Unidades de Fomento, a daily indexed Chilean peso-denominated monetary unit that takes into account the effect of the Chilean inflation rate, references to “AR$” are to Argentine pesos, and references to “R$” are to Brazilian reais.

For your convenience, this prospectus contains certain translations of Chilean peso amounts into U.S. dollars at specified rates. Unless otherwise indicated, the U.S. dollar equivalent for information in Chilean pesos is based on the observed exchange rate reported by Banco Central de Chile, the Central Bank of Chile, which we refer to as the “Central Bank of Chile.” The Federal Reserve Bank of New York does not report a noon buying rate for Chilean pesos. On December 31, 2011, the observed exchange rate for Chilean pesos was Ch$521.46 to U.S.$1.00, and on May 16, 2012, the observed exchange rate was Ch$497.11 to U.S.$1.00. You should not construe these translations as representations that the Chilean peso amounts actually represent such dollar amounts or could be converted into U.S. dollars at the rates indicated or at any other rate. See “Exchange Rates.” Unless otherwise specified, references to the devaluation or the appreciation of the Chilean peso against the U.S. dollar are in nominal terms (without adjusting for inflation) based on the observed exchange rates published by the Central Bank of Chile for the relevant period.

All references to “tons” are to metric tons (1,000 kilograms) which are equal to 2,204.6 pounds. One “hectare” equals 10,000 square meters or 2.471 acres. Percentages and certain amounts in this prospectus and the documents incorporated by reference have been rounded for ease of presentation. Any discrepancies in any table between totals and the sums of the amounts listed are due to rounding.

vii

PROSPECTUS SUMMARY

This summary highlights the information contained elsewhere or incorporated by reference in this prospectus and may not contain all of the information you need to consider. Please read the following summary, together with the information in this prospectus set forth under the heading “Risk Factors,” our audited financial statements for the year ended December 31, 2011 prepared in accordance with IFRS and our audited financial statements and accompanying notes included in our Form 20-F, as filed with the SEC on April 30, 2012 and incorporated by reference in this prospectus. “Arauco,” “we,” “us” and words of similar effect refer, depending upon the context, to Celulosa Arauco y Constitución S.A., to one or more of its consolidated subsidiaries or to all of them taken as a whole, unless the context otherwise requires. References herein to the “notes” refer collectively to the outstanding notes and the exchange notes.

About Arauco

We believe that, as of December 31, 2011, we were one of Latin America’s largest forest plantation owners, and that in the year ended December 31, 2011, we were Chile’s largest exporter of forestry and wood products in terms of sales revenue. We have industrial operations in Chile, Argentina and Brazil. As of December 31, 2011, we had approximately 1.0 million hectares of plantations in Chile, Argentina, Brazil and Uruguay. We believe that in the year ended December 31, 2011 we were one of the world’s largest producers of bleached and unbleached softwood kraft market pulp in terms of production capacity, based on information published by Resource Information Systems, Inc., an independent research company for the pulp and paper industry.

During 2011, we harvested 18.6 million cubic meters of sawlogs and pulplogs, and sold 5.8 million cubic meters of wood products, including sawn timber (green and kiln-dried lumber), remanufactured wood products and panels (plywood, medium-density fiberboard, particleboard and high-density fiberboard). In 2011, export sales constituted approximately 71.5% of our sales revenue, making us Chile’s largest exporter of forestry and wood products in terms of sales revenue. Our principal export markets during 2011 were Asia, North America and Europe.

As of December 31, 2011, our planted forests consisted of approximately 76.8% radiata, taeda and elliotti pine with the balance being primarily eucalyptus. We seek to manage our resources so the annual growth rates of our forests equal or exceed the volume harvested each year. In 2011 we planted approximately 75,750 hectares and harvested approximately 49,340 hectares in Chile, Argentina, Brazil and Uruguay. We operate our forestry business through four principal divisions: pulp, plywood and fiberboard panels, wood products and forestry products, each as described below.

Pulp. We own and operate five pulp mills in Chile and one in Argentina with an aggregate installed annual production capacity of approximately 3.2 million metric tons. During 2011, our pulp mills produced 2.4 million metric tons of bleached pulp and 0.4 million metric tons of unbleached pulp. During 2011, our pulp sales were U.S.$2,060.8 million, representing 54.7% of our consolidated revenue for such period.

Plywood and fiberboard panels. As of December 31, 2011, we owned and operated two plywood mills and one hardboard and medium-density fiberboard mill in Chile, one medium-density fiberboard mill and one particleboard mill in Argentina and one medium-density fiberboard mill and one medium-density fiberboard and particleboard mill in Brazil. In January 2012, we acquired a medium-density fiberboard and high-density fiberboard and particleboard in Moncure, North Carolina, U.S.A. The total annual production capacity of all these mills is approximately 3.5 million cubic meters of plywood and fiberboard panels. During 2011, our plywood and fiberboard panel sales were U.S.$1,273.7 million, representing 29.1% of our consolidated revenue for such period.

1

Wood products. We have eight sawmills in operation in Chile and one in Argentina with an aggregate installed annual production capacity of 2.8 million cubic meters of lumber. We also own five remanufacturing facilities in Chile and one in Argentina that reprocess sawn timber into remanufactured wood products such as moldings, jams and pre-cut pieces for doors, furniture and door and window frames. In 2011, we sold 2.5 million cubic meters of wood and remanufactured wood products. During 2011, our wood products sales were U.S.$731.6 million, representing 16.7% of our consolidated revenue for such period.

Forestry products. Our forestry products are sawlogs, pulplogs, posts and chips. During 2011, our forestry products sales to third parties were U.S.$157.5 million, representing 3.6% of our consolidated revenue for such period.

Business Strategy

Our business strategy is to maximize the value of our forest plantations by pursuing sustainable growth opportunities in our core businesses and expanding into new markets and products. We seek to implement our business strategy through the following initiatives:

| | • | | improving the growth rate and quality of our plantations through advanced forest management techniques; |

| | • | | executing a capital expenditure plan designed to reinforce our competitive advantages through economies of scale and scope, improving the efficiency and productivity of our industrial activities and optimizing the use of our forests through biomass energy generation; |

| | • | | continuing to develop our facilities, transportation, shipping, storage and product distribution network, which allows us to reach over 70 countries worldwide; and |

| | • | | expanding internationally into new regions that we believe have comparative advantages in the forestry sector. |

2

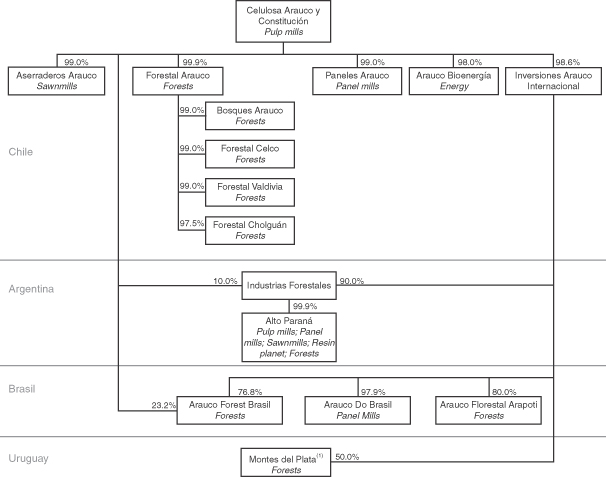

Corporate Structure

Set forth below is a diagram summarizing our corporate structure and our principal subsidiaries as of December 31, 2011:

| (1) | Montes del Plata is a collective reference to a group of companies (Stora Enso Uruguay S.A., Forestal Cono Sur S.A., Eufores S.A., Celulosa y Energía Punta Pereira S.A., Zona Franca Punta Pereira S.A., El Esparragal Asociación Agraria de Responsabilidad Limitada and Terminal Logística e Industrial M’Bopicuá S.A.) in which we have a 50% interest and through which we carry out our joint venture in Uruguay with Stora Enso Oyj. |

Our principal executive offices are located at Avenida El Golf 150, 14th Floor, Las Condes, Santiago, Chile. Our telephone number is +56-2-461-7200, and our facsimile number is +56-2-461-7541.

3

The Exchange Offer

On January 11, 2012, we completed the private offering of the outstanding notes. References to the “notes” in this prospectus are references to both the outstanding notes and the exchange notes. This prospectus is part of a registration statement covering the exchange of the outstanding notes for the exchange notes.

We entered into a registration rights agreement with the initial purchasers in the private offering in which we agreed to deliver to you this prospectus as part of the exchange offer and we agreed to use our reasonable best efforts to complete the exchange offer within 360 days after the date of original issuance of the outstanding notes. In the exchange offer, you are entitled to exchange your outstanding notes for exchange notes that are identical in all material respects to the outstanding notes except the exchange notes have been registered under the Securities Act. In addition, the exchange notes will not be entitled to registration rights and liquidated damages that are applicable to the outstanding notes under the registration rights agreement.

The Exchange Offer | We are offering to exchange up to U.S.$500 million aggregate principal amount of our 4.750% Notes due 2022, which we refer to in this prospectus as the “exchange notes”, for up to U.S.$500 million aggregate principal amount of our 4.750% Notes due 2022, which we refer to in this prospectus as the “outstanding notes”. The exchange offer is being made with respect to all of the outstanding notes. Outstanding notes may only be exchanged in integral multiples of U.S.$1,000. |

Resale of the Exchange Notes | Based on an interpretation of the staff of the SEC set forth in no action letters issued to unrelated third parties, we believe that exchange notes issued pursuant to the exchange offer in exchange for outstanding notes may be offered for resale, resold and otherwise transferred by you (unless you are an affiliate of ours, within the meaning of Rule 405 under the Securities Act) without compliance with the registration and prospectus delivery provisions of the Securities Act, provided that the exchange notes are acquired in the ordinary course of your business and you have not engaged in, do not intend to engage in, and have no arrangement or understanding with any person to participate in, a distribution of the exchange notes. |

| | Each participating broker-dealer that receives exchange notes for its own account pursuant to the exchange offer in exchange for outstanding notes that were acquired as a result of market-making or other trading activity must acknowledge that it will deliver a prospectus in connection with any resale of the exchange notes. |

| | Any holder of outstanding notes who: |

| | • | | is an affiliate of ours; |

| | • | | does not acquire exchange notes in the ordinary course of business; or |

| | • | | tenders in the exchange offer with the intention to participate, or for the purpose of participating, in the distribution of the exchange notes; |

4

| | cannot rely on the position of the staff of the SEC enunciated in Exxon Capital Holdings Corporation, Morgan Stanley & Co. Incorporated or similar interpretive letters and, in the absence of an exemption therefrom, must comply with the registration and prospectus delivery requirements of the Securities Act in connection with the resale of the exchange notes. See “The Exchange Offer—Resales of the Exchange Notes.” |

Expiration Date; Withdrawal of Tender | The exchange offer will expire at 5:00 PM, New York City time, on , 2012, unless we extend it. We do not currently intend to extend the expiration date. We refer to this date (as it may be extended) as the “expiration date.” Tenders of outstanding notes pursuant to the exchange offer may be withdrawn at any time prior to the expiration date. Any outstanding notes not accepted for exchange for any reason will be returned without expense to the tendering holder promptly after the expiration or termination of the exchange offer. See “The Exchange Offer––Expiration Date; Extensions; Amendments” and “The Exchange Offer––Withdrawal of Tenders.” |

Conditions to the Exchange Offer | The exchange offer is subject to customary conditions, which we may waive in our sole discretion. See “The Exchange Offer––Conditions to the Exchange Offer” for more information regarding the conditions to the exchange offer. |

Procedures for Tendering Outstanding Notes | If you wish to accept the exchange offer, you must complete, sign and date the accompanying letter of transmittal, or a facsimile of the letter of transmittal according to the instructions contained in this prospectus and the letter of transmittal. You must also mail or otherwise deliver the letter of transmittal, or a facsimile of the letter of transmittal, together with any physical certificates requesting the outstanding notes and any other required documents, to the exchange agent at the address set forth on the cover page of the letter of transmittal. If you hold outstanding notes through The Depository Trust Company, or DTC, and wish to participate in the exchange offer, you must comply with the Automated Tender Offer Program procedures of DTC, which we refer to as “ATOP,” by which you will agree to be bound by the letter of transmittal. By signing, or agreeing to be bound by the letter of transmittal, you will represent to us that, among other things: |

| | • | | any exchange notes that you receive will be acquired in the ordinary course of your business; |

| | • | | you have no arrangement or understanding with any person or entity to participate in a distribution of the exchange notes; |

| | • | | if you are a broker-dealer that will receive exchange notes for your own account in exchange for outstanding notes that were acquired as a result of market-making activities, that you will deliver a prospectus, as required by law, in connection with any resale of the exchange notes; and |

5

| | • | | you are not an affiliate, as defined in Rule 405 of the Securities Act, of ours or, if you are an affiliate of ours, you will comply with any applicable registration and prospectus delivery requirements of the Securities Act. |

| | See “The Exchange Offer––Procedures for Tendering” and “Plan of Distribution.” |

Special Procedures for Beneficial Owners | If you are a beneficial owner of outstanding notes that are registered in the name of a broker, dealer, commercial bank, trust company or other nominee, and you wish to tender the outstanding notes in the exchange offer, you should contact that registered holder promptly and instruct that registered holder to tender on your behalf. If you wish to tender on your own behalf, you must, prior to completing and executing the letter of transmittal and delivering your outstanding notes, either make appropriate arrangements to register ownership of the outstanding notes in your name or obtain a properly completed bond power from the registered holder. The transfer of registered ownership may take considerable time and may not be able to be completed prior to the expiration date. See “The Exchange Offer––Procedures for Tendering.” |

Guaranteed Delivery Procedures | If you wish to tender your outstanding notes and they are not immediately available or you cannot deliver your outstanding notes, the letter of transmittal or any other documents required by the letter of transmittal, or comply with the applicable procedures under DTC’s ATOP, prior to the expiration date, you must tender your outstanding notes according to the guaranteed delivery procedures set forth in this prospectus under “The Exchange Offer––Guaranteed Delivery Procedures.” |

Effect on Holders of Outstanding Notes | As a result of the making of, and upon acceptance for exchange of all validly tendered outstanding notes pursuant to the terms of the exchange offer, we will have fulfilled a covenant contained in the registration rights agreement and, accordingly, there will be no increase in the interest rate on the outstanding notes under the circumstances described in the registration rights agreement. If you are a holder of outstanding notes and you do not tender your outstanding notes in the exchange offer, you will continue to hold the outstanding notes, and you will be entitled to all the rights and limitations applicable to the outstanding notes in the indenture, except for any rights under the registration rights agreement that by their terms terminate upon the consummation of the exchange offer. |

| | To the extent outstanding notes are tendered and accepted in the exchange offer, the trading market for outstanding notes could be adversely affected. |

6

Consequence of Failure to Exchange | All untendered outstanding notes will continue to be subject to the restrictions on transfer provided for in the outstanding notes and in the indenture. In general, the outstanding notes may not be offered or sold, unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Other than in connection with the exchange offer, we do not currently anticipate that we will register the outstanding notes under the Securities Act. See “The Exchange Offer—Consequences of Failure to Exchange.” |

Taxation | The exchange of the outstanding notes for the exchange notes pursuant to the exchange offer will not be a taxable event for United States federal income tax or Chilean tax law purposes. See “Taxation.” |

Use of Proceeds | We will not receive any proceeds from the issuance of exchange notes pursuant to the exchange offer. |

Exchange Agent | The Bank of New York Mellon is serving as exchange agent in connection with the exchange offer. The contact information for the exchange agent is set forth in the section captioned “The Exchange Offer––Exchange Agent” of this prospectus. |

7

The Exchange Notes

Issuer | Celulosa Arauco y Constitución S.A. |

Notes Offered | U.S.$500 million in an aggregate principal amount of 4.750% Notes due 2022. |

Maturity | January 11, 2022. |

Interest Payment Dates | January 11 and July 11 of each year, commencing on July 11, 2012. |

Optional Redemption | We may redeem the exchange notes in whole or in part, at our option, at any time and from time to time at a redemption price equal to the greater of (i) 100% of the principal amount of the exchange notes to be redeemed and (ii) the sum of the present values of the Remaining Scheduled Payments (as defined herein) discounted to the date of redemption on a semi-annual basis (assuming a 360-day year consisting of twelve 30-day months) at the Treasury Rate (as defined herein) plus 45 basis points, together with, in each case, accrued and unpaid interest on the principal amount of the exchange notes to be redeemed to the date of redemption. |

| | In addition, we may redeem the exchange notes in whole or in part, any time and from time to time, beginning on the date that is three months prior to the scheduled maturity of the exchange notes, at our option at a redemption price equal to 100% of the principal amount of the exchange notes to be redeemed, plus accrued and unpaid interest on the principal amount of the exchange notes being redeemed to the date of redemption. See “Description of the Exchange Notes—Optional Redemption.” |

Tax Redemption | We may redeem the exchange notes in whole, but not in part, at any time at par if certain changes related to Chilean tax law occur. See “Description of the Exchange Notes—Redemption for Taxation Reasons.” |

Certain Covenants | The indenture under which the exchange notes will be issued contains certain covenants, including limitations on liens and limitations on sale and leaseback transactions. |

Ranking | The exchange notes will be unsecured obligations of Arauco and will, other than with respect to certain obligations given preferential treatment pursuant to the laws of Chile, rankpari passu in right of payment with all of our other existing and future unsecured and unsubordinated indebtedness. The exchange notes will not have the benefit of any collateral securing any of our existing and future secured indebtedness and will be effectively subordinated to all existing and future indebtedness of any of our subsidiaries to the extent of the assets of each subsidiary. |

Further Issues | We may from time to time without the consent of the holders of the notes issue further securities having the same terms and conditions as the notes so that the further issue is consolidated and forms a single series of notes with the notes offered hereby. |

8

Taxation | Under Chile’s income tax law, our payments of interest made from Chile in respect of the exchange notes to a Foreign Holder (as defined herein) will generally be subject to a Chilean withholding tax assessed at a rate of 4.0%. Subject to certain exceptions, we will pay Additional Amounts (as defined herein) as may be necessary to ensure that the net amounts received by the Foreign Holders (including Additional Amounts) after such Chilean withholding tax shall equal the amounts which would have been receivable in respect of the exchange notes in the absence of such Chilean withholding tax. See “Description of the Exchange Notes—Payment of Additional Amounts” and “Taxation.” |

Governing Law | Our contractual rights and obligations and the rights of the holders of the exchange notes arising out of, or in connection with, the indenture and the exchange notes are governed by, and will be construed in accordance with, the laws of the State of New York. |

Absence of a Public Market for the Exchange Notes | The exchange notes generally will be freely transferable but will also be new securities for which there will not initially be an established trading market. Accordingly, we cannot assure you as to the development or liquidity of any market for the exchange notes. We do not intend to apply for a listing of the exchange notes on any securities exchange or automated dealer quotation system. |

Exchange Controls in Chile | The issuance of the exchange notes does not require prior authorization by the Central Bank of Chile. Nevertheless, certain financial terms of the outstanding notes have been registered with the Central Bank of Chile after the issuance of the outstanding notes. |

Trustee | The Bank of New York Mellon is the trustee under the indenture. |

For a discussion of risks that should be considered in connection with an investment in the exchange notes, see “Risk Factors.”

9

RISK FACTORS

We are subject to various changing economic, political, social and competitive conditions, particularly in our principal markets. Any of the following risks, if they actually occur, could materially and adversely affect our business, financial condition and results of operations and, as a result, the notes. You should consider these risks, in addition to the other information presented or incorporated by reference into this prospectus, before making an investment decision in respect of the exchange notes.

Risks relating to us and the forestry industry

Fluctuations in market price for our products could adversely affect our financial condition, results of operations and cash flows.

Prices for many of the products we sell can fluctuate significantly. The price of commodities such as pulp, plywood, fiberboard and sawn timber has a high correlation with international prices. Consequently, the prices that we are able to charge for these products are highly dependent on prevailing international prices. Historically, such prices have been subject to substantial variation. For example, during the period from January 1, 2009 to December 31, 2011, the average price for Norscan bleached softwood kraft market pulp (pulp produced in Canada and Northern Europe sold to manufacturers of paper products delivered in Northern Europe, or NBSK), which is the benchmark for softwood bleached pulp, ranged from a low of U.S.$577.09 per metric ton in April 2009 to a high of U.S.$1,023.1 per metric ton in June 2011. During the last quarter of 2008 and the first quarter of 2009 there was a very rapid and significant reduction in the international prices of the products we sell and commodity prices in general as a result of the global financial crisis. In the second half of 2009, the international price of the products we sell and commodity prices in general increased up to pre-financial crisis levels and continued at high levels in 2010 and the first half of 2011. In the second half of 2011, pulp price started to decline. The continuation of severe global economic conditions may continue to exert downward pressure on commodity prices, including the international prices of the products we sell, which could result in material and adverse declines in our revenues, results of operations and financial condition. We have no control over the factors that cause prices to change which include, among others:

| | • | | worldwide demand (which may be affected by a number of factors, including economic or political conditions in Asia, Latin America, North America and Europe). |

| | • | | prevailing world prices, which historically have been subject to significant fluctuations over relatively short periods of time, depending on worldwide demand; |

| | • | | world production capacity; |

| | • | | the business strategies adopted by major integrated forestry, pulp and paper producers and other major producers; and |

| | • | | the availability of substitutes. |

In addition, the prices of many of the products we sell are correlated to some extent and historical fluctuations in the price of one product have usually been accompanied by similar fluctuations in the prices of other products. If the price of one or more of the products that we sell were to decline significantly from current levels, it could have a material adverse effect on our revenues, results of operations and financial condition.

Worldwide competition in the markets for our products could adversely affect our business, financial condition, results of operations and cash flows

We experience substantial worldwide competition in each of our geographical markets and in each of our product lines. Several of our competitors are larger than we are and have greater financial and other resources, which they could use to take steps that could materially and adversely affect our financial and competitive position. The pulp industry is sensitive to changes in industry capacity and producer inventories, as well as to cyclical changes in the world’s economies, all of which may significantly affect selling prices and, thereby, our profitability. Increased competition could materially and adversely affect our business, financial condition, results of operations and cash flows.

10

Global economic developments, and particularly economic developments in the Asian, European and U.S. economies, could have an adverse effect on the demand for our products, our financial condition, results of operations and cash flows.

The global economy, and in particular global industrial production, is the primary driver of demand for pulp, paper and wood products. Global industrial production dropped during the second half of 2008 and first half of 2009 due to the financial crisis and global economic conditions, resulting in a significant and widespread contraction in demand for pulp, paper and wood products. A continued decrease in the level of activity in either the domestic or the international markets within which we operate could adversely affect the demand and the price of our products and thus our cash flows and operational and financial results.

Due to this downturn in global industrial production, our pulp segment experienced significant price declines in the last quarter of 2008 and the first quarter of 2009 which severely affected our results. In addition, the significant downturn in the home-building industry in the United States and Europe has resulted in increased inventories of available new homes, significant declines in home prices, loss of home-equity values and loss of consumer confidence and demand. As a result of these events, our plywood and panel sales were adversely affected, continuing a downward trend both in volume and price across all markets. Our medium-density fiberboard molding sales also experienced a sharp decline in volume mainly due to the lower activity in the United States and Canadian construction markets. Our wood products segment, which is also highly dependent on the strength of the home-building industry, experienced decreases in its prices of and demand for its products.

The decrease in demand of sawn timber products due primarily to the credit crisis and continued downturn in the real estate market in the United States and decrease in demand for sawn timber products resulted in our decision to close five sawmills in 2008 and 2009. Also, the same situation of deteriorated market conditions led us to close our Bossetti Sawmill in Argentina in December 2010. Since late 2009, high levels of sovereign debt and insufficient public sector revenues have resulted in a European sovereign debt crisis. As of the date of this prospectus, credit rating agencies have downgraded the credit ratings of many of the Eurozone governments, including Greece, Spain, Italy, Portugal and France, among others. During 2011 and the first quarter of 2012, the deepening of this crisis has caused a general economic downturn in Europe, which has negatively affected the banking and credit systems, employment and production. As a result, demand and prices for pulp and wood products have declined in the European market.

Export sales of our wood products to Asia accounted for 38.6% of our sales revenue in 2011 compared to 36.3% in 2010, and 32.1% in 2009, and export sales to North America accounted for 36.7% of our sales revenue in 2011 compared to 39.7% in 2010 and 43.3% in 2009. In addition, during 2009 we exported a significant quantity of our sawn timber products, especially to Asia and the Middle East, in order to avoid additional personnel reductions in the facilities and to mitigate the impact of the global economic downturn on our sawn timber division. Our business, financial condition, results of operations and cash flows could be materially and adversely affected if the economic conditions in Asia, Europe, the United States and elsewhere abroad continue to deteriorate, and if we are unable to reallocate our sawn timber and other products to other markets on equally beneficial terms, which could require us to recognize additional impairment charges.

We depend on free international trade as well as economic and other conditions in our principal export markets.

In 2011, export sales, defined as sales out of the country where our goods were produced, accounted for approximately 71.5% of our total sales revenues. During this period, 47.0% of our export sales were to customers in Asia, 19.0% to customers in North America, 17.7% to customers in Europe, 11.8% to customers in Central and South America and 4.5% to customers in other countries. As a result, our results of operations and cash flows depend, to a significant degree, on economic, political and regulatory conditions in our principal export markets. Our ability to compete effectively in our export markets could be materially and adversely affected by a number of factors beyond our control, including deterioration in macroeconomic conditions, exchange rate volatility, government subsidies, and the imposition of increased tariffs or other trade barriers. If our ability to sell our products competitively in one or more of our principal export markets were impaired by any of these

11

developments, it might be difficult to re-allocate our products to other markets on equally favorable terms and our business, financial condition, results of operations and cash flows might be adversely affected.

We are located in a seismic area that exposes our property in Chile to the risk of earthquakes and tsunamis, and we experienced significant business disruption and losses as a result of the February 27, 2010 earthquake.

Our properties in Chile are located in a seismic area that exposes our facilities, plants, equipment and inventories to the risk of earthquakes and even subsequent tsunamis in some areas. A significant earthquake or other catastrophic event could severely affect our ability to meet our production targets, satisfy customer demand and could require us to make unplanned capital expenditures, resulting in lower sales and having a material adverse effect on our financial results.

On February 27, 2010, an earthquake measured at a magnitude of 8.8 on the Richter scale, followed by a tsunami that affected the coast, occurred in the South-Central Region of Chile, an area where we maintain a substantial portion of our industrial operations in Chile. Immediately after the earthquake, all of our production units applied their contingency plans, which involved shutting down operations and evaluating the damage caused to each facility by the earthquake. As a result of the earthquake and the subsequent tsunami, our Mutrún sawmill was destroyed. All of our operations have since reopened and are currently operating at full operational capacity, except for the Mutrún sawmill, which will not be reopened. The Mutrún sawmill represented approximately 6% of our sawn timber production capacity in Chile.

The suspension of our operations in Chile resulted in significant asset impairment charges due to earthquake-related damage to property and inventories as well as a significant decrease in our sales volumes due to plant closures which had an adverse effect on our results of operations and cash flows. Our insurance policies provide coverage for certain damages to our property, plant, equipment and inventories and for business interruption caused by such damages up to an aggregate amount of U.S.$650 million, with a deductible of U.S.$3 million for property damage and a deductible of 21 days for business interruption. On November 15, 2011, we and the insurers accepted the final report of the insurance adjusters. In accordance with such final report we are entitled to receive a total recovery of U.S.$532 million, which we have fully received as of December 31, 2011.

We cannot assure you that we will not experience other suspensions or interruptions or unexpected damage to our property as a result of other earthquakes, aftershocks, tsunamis, any related repair and maintenance or other consequences associated with such events, any of which could have a material and adverse effect on our revenue, results of operations and financial condition.

The costs to comply with, and to address liabilities arising under, environmental laws and regulations could adversely affect our business, financial condition, results of operations and cash flows.

In each country where we have operations, we are subject to a wide range of national and local environmental laws and regulations concerning, among other matters, the preparation of environmental impact assessments for our projects, the protection of the environment and human health, the generation, storage, handling and disposal of waste, the discharge of pollutants and the remediation of contamination. As a forest products manufacturer, we generate air and water emissions and solid and hazardous wastes. These emissions and waste disposals are subject to limits or controls prescribed by law or by our operating permits, and we may be required to install or upgrade our pollution control equipment in order to meet these legal requirements. We have made, and expect to continue to make, expenditures to maintain compliance with environmental laws. Failure to comply with environmental requirements may result in civil, administrative or criminal fines or sanctions, claims for environmental damages, remediation obligations, the revocation of environmental authorizations or the temporary or permanent closure of facilities. Environmental regulations in Chile and other countries in which we operate have become increasingly stringent in recent years (for example, in connection with the approval and development of new projects), and this trend is likely to continue. Future changes in environmental laws, or in the application, interpretation or enforcement of those laws, including new or stricter requirements related to harvesting activities, air and water emissions and/or climate change regulations, could result in substantially increased capital, operating or compliance costs, impose conditions that restrict or limit our

12

operations or otherwise adversely affect our business, financial condition, results of operations and cash flows. These changes could also limit the availability of our funds for other purposes, which could adversely affect our business, financial condition, results of operations and cash flows.

Since 2004, we have been subject to a number of environmental administrative and judicial proceedings in Chile, including proceedings related to the Valdivia Mill, the Arauco Mill, the Nueva Aldea Complex and the Licancel Mill. As a result of these proceedings, we have been subject to monetary fines as well as sanctions, including orders to suspend or limit our operations. Additional proceedings, enforcement actions or claims related to compliance with environmental requirements or alleged environmental damages may also be brought against us in the future. Any such proceedings or claims may have an adverse effect on our business, financial condition, results of operations and cash flows. See “Risk factors—Risks relating to us and the forestry industry—Environmental concerns led to the temporary suspension of our operations at the Valdivia Mill in 2005 and at the Licancel Mill in 2007, which adversely affected, and in the future may continue to adversely affect, our business, financial condition, results of operations and cash flows.”

Environmental concerns led to the temporary suspension of our operations at the Valdivia Mill in 2005 and at the Licancel Mill in 2007, which adversely affected, and in the future may continue to adversely affect, our business, financial condition, results of operations and cash flows.

Valdivia Mill

Our operations at the Valdivia Mill, an industrial development in the Province of Valdivia, have been subject to environmental scrutiny by Chilean environmental regulators and the Chilean public since the mill began its operations in 2004. A variety of concerns and claims have been raised regarding the mill’s potential environmental impacts in the area. Primarily, it has been alleged that the mill’s operations impacted habitat in the nearby Carlos Anwandter Nature Sanctuary and contributed to the migration and death of black-neck swans living in the area. In connection with an environmental administrative proceeding, environmental regulators required us to temporarily suspend operations at the Valdivia Mill for approximately one month in January 2005.

In June 2005, we again suspended operations at the Valdivia Mill until certain technical and legal conditions could be clarified with the applicable regulatory authorities. We estimate this suspension resulted in a loss of sales of approximately U.S.$1 million per day and a loss of profits of approximately U.S.$250,000 per day. Pursuant to the decision of our board of directors, based on certain clarifications provided by the Environmental Regional Commission (Comisión Regional del Medio Ambiente), or COREMA, of the Tenth Region of Chile, the mill resumed operations in August 2005, after 64 days of suspended operations, at 80% of its authorized production capacity. In order to achieve the full production capacity authorized by applicable permits, the mill had to fulfill certain new requirements established by the COREMA. In January 2008, the COREMA authorized the Valdivia Mill to return to its annual authorized production capacity of 550,000 metric tons. The mill gradually increased its production over a four-month period starting in March 2008 and reached full capacity in June 2008.

In June 2007, we were required to submit to the COREMA of the Tenth Region of Chile an environmental impact study for the implementation of substantial technological improvements on the quality of effluents generated by the Valdivia Mill. In June 2008, the COREMA approved that environmental impact study subject to certain conditions that, in our opinion, adversely affected the feasibility of the project. For such reason, we filed an appeal before the Directive Council (Consejo Directivo) of the National Environmental Commission (Comisión Nacional del Medio Ambiente), or CONAMA, challenging the conditions imposed by the COREMA. This administrative appeal was partially accepted by the CONAMA, but certain of the conditions that we believe adversely affect the feasibility of the project were maintained. As a result, in September 2009 we presented another appeal in the relevant court, and as of the date of this prospectus such appeal remains pending.

Until October 2007, our Valdivia Mill was under the jurisdiction of the COREMA of the Tenth Region of Chile, but due to a change in legislation creating two new administrative regions in Chile, our Valdivia Mill became subject to the jurisdiction of the COREMA of the Fourteenth Region of Chile. In February 2009, as previously required by the COREMA of the Tenth Region of Chile, we submitted to the COREMA of the

13

Fourteenth Region of Chile an environmental impact study for the construction of a pipeline to discharge the Valdivia Mill’s wastewater in the Pacific Ocean near Punta Maiquillahue, complying with the requirement that such wastewater be discharged in a body of water other than the Cruces River, the Carlos Anwandter Nature Sanctuary or their respective sources. This environmental impact study was approved by the COREMA in February 2010 but has been partially challenged by us before the Directive Council (Consejo Directivo) of the CONAMA primarily because it included a prohibition of discharge of wastewater into the Cruces River under all circumstances, even in the case of certain emergencies. As of the date of this prospectus, the Directive Council of the CONAMA has not resolved the action presented by us.

Resolution of our disputes with the CONAMA or the pending appeals before the Chilean courts regarding the resolutions that approved the environmental impact studies of the pipeline and the effluent quality improvement projects, as well as the construction and operation of the pipeline, are each subject to many environmental, regulatory, engineering and political uncertainties. As a result, we cannot provide any assurances that the projects will be finally approved as requested or completed. If either the request for the necessary permits for the construction of the pipeline is rejected, or the installation of the pipeline is delayed for reasons attributable to us, we may face sanctions that include warnings, fines or the revocation of the Valdivia Mill’s environmental permit for operation. Alternatively, if any rejection or delays are attributable to reasons beyond our control, we believe that the environmental authorities should extend the applicable deadlines. However, we can provide no assurances that any deadline extensions would be granted, even if we comply with all the requirements that may be set forth by those authorities.

The suspension of operations at the Valdivia Mill in 2005 adversely affected our business, financial condition, results of operations and cash flows. Any future suspension of operations at the Valdivia Mill or at any other of our significant operating plants can be expected to have similar adverse effects. We offer no assurance that the Valdivia Mill, or our other mills, will be able to operate without further interruption.

Licancel Mill

Beginning in June 2007, our operations at the Licancel Mill, a pulp mill located in the Seventh Region of Chile, became subject to environmental scrutiny by Chilean environmental regulators and the public due to the death, in June 2007, of fish in the Mataquito River approximately 15 kilometers downstream of the mill. As a result, in June 2007 Chilean authorities, including certain public health authorities and theSuperintendencia de Servicios Sanitarios(Sanitary Services Superintendency), required that we suspend activities at the Licancel Mill and that we suspend any further discharges into the river. In 2007, we invested approximately U.S.$8 million in a new effluent treatment system for the Licancel Mill, and the mill resumed operations during January 2008. Nevertheless, we can offer no assurance that the Licancel Mill will be able to operate without further interruptions. Any future suspension of operations at the Licancel Mill would adversely affect our business, financial condition, results of operations and cash flows. We estimate that the suspension of operations at the Licancel Mill resulted in a total loss of profits of approximately U.S.$24 million.

We are subject to legal proceedings related to our mills, which could adversely affect our business, financial condition, results of operations and cash flows.

In April 2005, the National Defense Council (Consejo de Defensa del Estado), the Chilean national agency that institutes legal proceedings on behalf of the Chilean government, instituted a civil lawsuit seeking reparations, damages and indemnification from us for environmental harm allegedly caused by the effluent discharges from our Valdivia Mill. The National Defense Council has not quantified the damages it is seeking in connection with the Valdivia Mill lawsuit. The Valdivia Mill lawsuit remains under review by the court as of the date of this prospectus. If the result of the Valdivia Mill lawsuit is unfavorable to us, we may be required to invest a significant amount of funds or take other actions to repair any environmental harm a court determines we have caused, which could materially and adversely affect our business, financial condition, results of operations and cash flows. We cannot predict the outcome or impact of this lawsuit or when it may be resolved.

14

Since the end of 2004, we have been subject to various criminal proceedings relating to alleged violations of several environmental laws in Chile, each of which has been either terminated or abandoned by the prosecutor (decisión de no perseverar) as of the date of this prospectus. The commencement of similar criminal proceedings against Arauco at any time in the future could adversely affect some of our mills. We can neither predict the likelihood that we will face such similar proceedings in the future, nor the likely outcome or impact of any such proceedings.

We are also subject to certain other civil and administrative proceedings relating to our mills. We cannot assure you that, as a result of such proceedings, our mills will be able to operate without interruption. Any such interruption, or unexpected costs to resolve such proceedings, could have a material and adverse effect on our business, financial condition, results of operations and cash flows.

We are subject to a substantial tax claim in Argentina

On December 14, 2007,the Administración Federal de Ingresos Públicos, or AFIP, Argentina’s internal revenue service, notified our Argentine subsidiary, Alto Paraná S.A., or Alto Paraná, of a claim for unpaid taxes for fiscal years 2002, 2003 and 2004 in the aggregate amount of approximately AR$418 million (or approximately U.S.$105 million) (including principal, interest and penalties accrued through such date), arising from a dispute regarding certain income tax deductions (related to debt issued by Alto Paraná in 2001 and repaid in 2007) taken by Alto Paraná and rejected by the AFIP. On February 8, 2010, Argentina’s tax court (Tribunal Fiscal de la Nación) issued an unfavorable administrative ruling requiring that Alto Paraná pay the AFIP’s claim in full.

Alto Paraná appealed this unfavorable administrative ruling to the Court of Appeals and also filed an injunctive action requesting that the court stay Alto Paraná’s payment obligation until resolution of its pending appeal. On May 13, 2010, the Court of Appeals granted an injunction of Alto Paraná’s payment obligation in exchange for the posting of a surety bond in the amount of AR$633.6 million (or approximately U.S.$159 million). We have not established any reserve in respect of this contingency and can offer no assurance that the Court of Appeals will issue a ruling favorable to us. If the Court of Appeals upholds the decision of theTribunal Fiscal de la Nación, Alto Paraná will be required to satisfy the above-mentioned claim which would have an adverse effect on our financial condition and results of operations.

Our ability to access local and international credit or capital markets may be restricted at a time when we need financing, which could have a material adverse effect on our flexibility to react to changing economic and business conditions.

As of December 31, 2011, we had approximately U.S.$3,213.3 million of outstanding indebtedness. In light of the current economic environment, we may be unable to access, or we may be restricted in accessing, credit and capital markets to satisfy our financing needs, or we may not be able to refinance our existing indebtedness on terms that are favorable to us or at all. If we are unable to refinance our indebtedness as it becomes due, or if we refinance such indebtedness on terms that are not favorable to us, our business, results of operations and financial condition could be materially and adversely affected.

Material disruptions at any of our manufacturing, mills processing or remanufacturing facilities could negatively impact our financial results.

A material disruption at any of our manufacturing, mills processing or remanufacturing facilities could prevent us from satisfying customer demand for our products, meeting our production targets and/or require us to make unplanned capital expenditures, resulting in lower sales, which would have a negative effect on our financial results. Our Chilean facilities are located in a region known for seismic activity that exposes our facilities in Chile to the risk of earthquakes and subsequent tsunamis in some areas. In addition, our facilities (or any of our machines within an otherwise operational facility) could cease operations unexpectedly due to a number of events, including:

| | • | | unscheduled maintenance outages; |

15

| | • | | prolonged power failures; |

| | • | | fires, floods, hurricanes or other adverse weather; |

| | • | | disruptions in the transportation infrastructure, including roads, bridges, railroad tracks and tunnels; |

| | • | | a chemical spill or release; |

| | • | | the effect of a drought or reduced rainfall on its water supply; |

| | • | | terrorism or threats of terrorism; |

| | • | | domestic and international laws and regulations applicable to our Company and our business partners, including joint venture partners, around the world; and |

| | • | | other operating problems. |

Disease or fire could affect our forests and manufacturing processes and, in turn, adversely affect our business, financial condition, results of operations and cash flows.

Our operations are subject to various risks affecting our forests and manufacturing facilities, including disease and fire. Although to date certain pests and diseases afflicting radiata or taeda pine plantations in other parts of the world have not significantly affected the forestry industries in Chile, Argentina, Brazil and Uruguay, these pests or diseases do migrate and may appear in Chile, Argentina, Brazil or Uruguay in the future. Similarly, forest fires are always a risk, particularly during low rainfall conditions. We do not maintain insurance against pests, diseases or, in certain areas, fires that could affect our forests, and as a result our business, financial condition, results of operations and cash flows could be adversely affected if any of these risks were realized.

Commencing on December 31, 2011 wildfires, exacerbated by high temperatures and strong winds, broke out in the Eighth Region of Chile. As a result, the fires destroyed our Nueva Aldea plywood mill and approximately 8,200 hectares of our forest plantations. The affected forest plantations represent approximately 0.8% of our total forest plantations. Our Nueva Aldea plywood mill, which represented an investment of approximately U.S.$110 million, had an annual production capacity of 450,000 cubic meters, representing approximately 14.2% of our total panel production capacity. Although the plywood mill at Nueva Aldea and our forest plantations are insured, our insurance is subject to deductibles and caps, including a 15-day deductible relating to our business interruption insurance for the Nueva Aldea plywood mill. We believe that the interruption of our Nueva Aldea panel mill may result in a loss of profits of approximately U.S.$2.0 million during year 2012, net of the insurance coverage we may receive due to this event. We can provide no assurance that we will receive insurance proceeds to compensate us fully for the losses we have incurred.

Climate change may negatively affect our business, financial condition, results of operations and cash flows.

A growing number of scientists, environmentalists, international organizations, regulators and other commentators maintain that global climate change has contributed, and will continue to contribute, to the increasing unpredictability, frequency and severity of natural disasters (including, but not limited to, hurricanes, droughts, tornadoes, freezes, other storms and fires) in certain parts of the world. As a result, a number of legal and regulatory measures as well as social initiatives have been introduced in numerous countries in an effort to reduce carbon dioxide and other greenhouse gas emissions, which some argue to be substantial contributors to global climate change. Such reductions in greenhouse gas emissions could result in increased energy, transportation and raw material costs and may require us to make additional investments in facilities and equipment.

16

In addition, our plantations are located in regions which have ideal climatic conditions for a short growing cycle. Any climate changes that negatively affect such favorable climate conditions in central or southern Chile or in any region in which we benefit from favorable climate conditions could adversely affect the growth rate and quality of our plantations, or our production costs. Although we cannot predict the impact of changing global climate conditions, if any, nor can we predict the impact of legal, regulatory and social responses to concerns about global climate change, any such occurrences may negatively affect our business, financial condition, results of operations and cash flows.

Our operations could be adversely affected by labor disputes.

Approximately 22.7% of our employees in Chile, 49.2% of our employees in Argentina and 11.3% of our employees in Brazil were unionized at December 31, 2011. In the past, certain work slowdowns, stoppages and other labor-related disruptions have adversely affected our operations. For example, in Chile we experienced (i) a 10-day work stoppage in November 2009 at our Constitución, Arauco, Nueva Aldea, Horcones and Trupán-Cholguán complexes, (ii) a three-day work stoppage in September 2009 at our Constitución, Arauco, Nueva Aldea, Horcones, Valdivia and Trupán-Cholguán complexes and (iii) a six-day work stoppage in May 2007 at our Horcones complex (which includes the Arauco pulp mill, a panel plant and two sawmills), each of which was caused by the employees of our third party forestry contractors at each of the respective facilities. In Argentina we experienced (i) a 3-day stoppage at Alto Paraná’s chemical mill in March 2011, as a result of a strike by the chemical union and (ii) a 4-day stoppage at Alto Paraná’s pulp mill in September 2010, as a result of a strike by the pulp union, but these strikes were limited to two hours per shift and did not materially affect operations. In January 2008, Alto Paraná’s chemical mill in Argentina experienced three days of work stoppage, but these strikes were limited to two hours per shift and did not materially affect operations. In addition, in January and February 2007, we experienced (i) a 12-day stoppage at our, Zárate mill due to a dispute arising between the local chemical and timber unions with regard to the representation of their workers at the mill and (ii) a six-day suspension of operations at our Alto Paraná pulp mill as a result of a strike by a group of approximately 150 power saw operators. Our principal collective-bargaining agreements in Chile are scheduled to expire in 2015. Our collective-bargaining agreement in Argentina does not terminate, it is modified through renegotiations with our employees. We cannot assure you that a work slowdown, or a work stoppage or strike, will not occur prior to or upon the expiration of our labor agreements, and we are unable to estimate the adverse effect of any such work slowdown, stoppage or strike on our sales.

In addition, we depend to a significant extent on employees of contractors to which we outsource a wide range of services including operation of certain of our manufacturing facilities and management of certain of our plantations. As of December 31, 2011, we had contracts with approximately 1,002 contractors, who employed approximately 25,456 employees. Contractors that are not affiliated with us or with each other operate our eight sawmills and five remanufacturing facilities in Chile. Under Chilean labor legislation, we are secondarily liable for the payment of labor and the social security obligations owed to employees of our contractors. In the event that we do not exercise the rights granted to us by the labor laws regarding the supervision of our contractors in their compliance of their labor and social security obligations, then our responsibility is elevated from secondary to joint and several, thus enabling an employee of a contractor to bring a claim relating to these obligations against both the contractor and to us, as the party hiring such contractor, although the contractor would remain primarily liable for such obligations. Furthermore, as a general rule, we are also responsible for the health and safety conditions of the contractors’ workers and are obligated to ensure that the contractors comply with all obligations related to such conditions while such workers are performing activities for us within our corporate purpose.