Banc of America Merrill Lynch Commercial Mortgage

Filed: 9 Sep 15, 12:00am

| W. Todd Stillerman, Esq. | Henry A. LaBrun, Esq. |

| Banc of America Merrill Lynch Commercial Mortgage Inc. | Cadwalader, Wickersham & Taft LLP |

214 South Tryon Street, 18th Floor, NC1-027-20-05 | 227 West Trade Street, Suite 2400 |

Charlotte, North Carolina 28255 | Charlotte, North Carolina 28202 |

Title of Each Class of Securities to be Registered | Amount to be Registered | Proposed Maximum Offering Price Per Unit | Proposed Maximum Aggregate Offering Price | Amount of Registration Fee(1) |

| Commercial Mortgage Pass-Through Certificates | (2)(3) | (2)(3) | (2)(3) | (2)(3) |

| (1) | Calculated in accordance with Rule 457(s) of the Securities Act of 1933. |

| (2) | The registrant previously registered $38,011,194,128 of securities under a Registration Statement on Form S-3 (Registration No. 333-201743) filed on January 28, 2015, $38,011,194,128 of which remain unsold. Pursuant to Rule 415(a)(6) under the Securities Act of 1933, as amended (the "Securities Act"), the registrant is including such unsold securities and the $3,409,331.46 of registration fees previously paid in connection with such unsold securities. |

| (3) | An unspecified additional amount of securities is being registered as may from time to time be offered at unspecified prices. The registrant is deferring payment of all of the registration fees for such additional securities in accordance with Rules 456(c) and 457(s) under the Securities Act. |

| The information in this preliminary prospectus is not complete and may be changed. This preliminary prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted. |

Title of Each Class of Securities to be Registered | Amount to be Registered | Maximum Offering Price Per Unit | Maximum Aggregate Offering Price | Amount of Registration Fee(1)(2) | ||||

| $[________] | [___]% | $[________] | $[________] | |||||

| $[________] | [___]% | $[________] | $[________] | |||||

| $[________] | [___]% | $[________] | $[________] |

| (1) | Calculated in accordance with Rule 457(s) under the Securities Act of 1933, as amended. |

Class | Initial Class Certificate Balance or Notional Amount(1) | Initial Approx. Pass-Through Rate | Pass-Through Rate Description | Assumed Final Distribution Date(3) | [Offering Price] | |||||

You should carefully consider the risk factors beginning on page [__] of this prospectus. Neither the certificates nor the mortgage loans are insured or guaranteed by any governmental agency, instrumentality or private issuer or any other person or entity. The certificates will represent interests in the issuing entity only. They will not represent interests in or obligations of the sponsors, depositor, any of their affiliates or any other entity. | The United States Securities and Exchange Commission and state regulators have not approved or disapproved of the offered certificates or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense. Banc of America Merrill Lynch Commercial Mortgage Inc. will not list the offered certificates on any securities exchange or on any automated quotation system of any securities association. The issuing entity will be relying on an exclusion or exemption from the definition of "investment company" under the Investment Company Act of 1940, as amended, contained in Section 3(c)(5) of the Investment Company Act or Rule 3a-7 under the Investment Company Act, although there may be additional exclusions or exemptions available to the issuing entity. The issuing entity is being structured so as not to constitute a "covered fund" for purposes of the Volcker Rule under the Dodd-Frank Act (both as defined in this prospectus). The underwriters, Merrill Lynch, Pierce, Fenner & Smith Incorporated, [NAMES OF OTHER UNDERWRITERS], will purchase the offered certificates from Banc of America Merrill Lynch Commercial Mortgage Inc. and will offer them to the public at negotiated prices, plus, in certain cases, accrued interest, determined at the time of sale. Merrill Lynch, Pierce, Fenner & Smith Incorporated, and [NAME OF CO-LEAD MANAGING UNDERWRITER] are acting as co-lead managers and joint bookrunners in the following manner: Merrill Lynch, Pierce, Fenner & Smith Incorporated is acting as sole bookrunning manager with respect to approximately [__]% of each class of offered certificates and [______] is acting as sole bookrunning manager with respect to approximately [__]% of each class of offered certificates. [______] is acting as a co-manager and as sole bookrunning manager with respect to approximately [__]% of each class of offered certificates. |

BofA Merrill Lynch | [____] | |

| Co-Lead Manager and Joint Bookrunner | Co-Lead Manager and Joint Bookrunner |

Class | Initial Class Certificate Balance or Notional Amount(1) | Approx. Initial Credit Support(2) | Pass-Through Rate Description | Assumed Final Distribution Date(3) | Initial Approx. Pass-Through Rate | Weighted Average Life (Yrs.)(4) | Principal Window(4) | |||||||

| Offered Certificates | ||||||||||||||

[LIST SPECIFIC OFFERED CLASSES ADD APPROPRIATE FOOTNOTES DESCRIBED BELOW] | ||||||||||||||

Non-Offered Certificates [LIST SPECIFIC NON-OFFERED CLASSES ADD APPROPRIATE FOOTNOTES DESCRIBED BELOW] |

| (1) | Approximate, subject to a permitted variance of plus or minus [5]%. |

| (2) | The approximate initial credit support percentages set forth for the certificates are approximate and, for the [IDENTIFY APPLICABLE SENIOR CLASSES] certificates, are represented in the aggregate. [The [LOAN-SPECIFIC CLASS] certificates will only provide subordination with respect to losses and shortfalls on the [NAME OF LOAN] mortgage loan.] The approximate initial credit support percentages for each class of certificates presented in the table do not include the related subordinate interest of the trust subordinate companion loan. |

| (3) | The assumed final distribution dates set forth in this prospectus have been determined on the basis of the assumptions described in "Description of the Certificates—Assumed Final Distribution Date; Rated Final Distribution Date". |

| (4) | The weighted average life and period during which distributions of principal would be received as set forth in the foregoing table with respect to each class of certificates having a principal balance are based on the assumptions set forth under "Yield and Maturity Considerations—Weighted Average Life" and on the assumptions that there are no prepayments, modifications or losses in respect of the mortgage loans and that there are no extensions or forbearances of maturity dates [or anticipated repayment dates] of the mortgage loans. |

| (5) | The notional amount of the [INTEREST-ONLY CLASS] certificates will be equal to the aggregate of the certificate balances of the Class [__] and Class [__] certificates [and the Class [__] trust component]. The notional amount of the [INTEREST-ONLY CLASS] certificates will be equal to the certificate balance of the Class [__] certificates [and the Class [__] and Class [__] trust components]. The [INTEREST-ONLY CLASSES] certificates will not be entitled to distributions of principal. |

(6) | The pass-through rate for the [INTEREST-ONLY CLASS] certificates for any distribution date will equal [the excess, if any, of (a) the weighted average of the net mortgage rates on the mortgage loans (in each case adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months), over (b) the weighted average of the pass-through rates of the Class [__] and Class [__] certificates and the Class [__] trust component for that distribution date, weighted on the basis of their respective certificate balances immediately prior to that distribution date. The pass-through rate for the [INTEREST-ONLY CLASS] certificates for any distribution date will equal the excess, if any, of (a) the weighted average of the net mortgage rates on the mortgage loans (in each case adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months for the related distribution date), over (b) the weighted average of the pass-through rates of the Class [__] certificates and the Class [__] and Class [__] trust components for that distribution date, weighted on the basis of their respective certificate balances immediately prior to that distribution date. See "Description of the Certificates—Distributions—Pass-Through Rates". |

| (7) | [Note: the deal-specific class designations for the exchangeable and exchange certificates, included for illustrative purposes only, are Class [A], Class [B], Class [C] and Class [EC]. the identity and number of exchangeable classes may vary.] The Class [A], Class [B], and Class [C] certificates may be exchanged for the Class [EC] certificates, and Class [EC] certificates may be exchanged for the Class [A], Class [B], and Class [C] certificates. |

| (8) | On the closing date, the issuing entity will issue the Class [A], Class [B], and Class [C] trust components, which will have outstanding certificate balances on the closing date of $[_____], $[_____] and $[_____], respectively. The Class [A], Class [B], and Class [C] certificates and the Class [EC] certificates will, at all times, represent undivided beneficial ownership interests in a grantor trust that will hold such trust components. Each class of the Class [A], Class [B], and Class [C] certificates and the Class [EC] certificates will, at all times, represent a beneficial interest in a percentage of the outstanding certificate balance of the Class [A], Class [B], and Class [C] trust components. Following any exchange of Class [A], Class [B], and Class [C] certificates for Class [EC] certificates or any exchange of Class [EC] certificates for Class [A], Class [B], and Class [C] certificates, the percentage interest of the outstanding certificate balances of the Class [A], Class [B], and Class [C] trust components that is represented by the Class [A], Class [B], and Class [C] certificates and the Class [EC] certificates will be increased or decreased accordingly. The initial balance of each class of the Class [A], Class [B], and Class [C] certificates shown in the table above represents the maximum principal balance of such class without giving effect to any issuance of Class [EC] certificates. The initial certificate balance of the Class [EC] certificates shown in the table above is equal to the aggregate of the maximum initial certificate balance of Class [A], Class [B], and Class [C] certificates, representing the maximum certificate balance of the Class [EC] certificates that could be issued in an exchange. The principal balance of the Class [A], |

| Class [B], and Class [C] certificates to be issued on the closing date will be reduced, in required proportions, by an amount equal to the principal balance of the Class [EC] certificates issued on the closing date. |

| (9) | The initial subordination levels for the Class [A], Class [B] and Class [C] certificates and Class [EC] certificates are equal to the subordination level of the underlying Class [A], Class [B] and Class [C] trust component, which will have an initial outstanding balance on the closing date of $[_____]. Although the Class [EC] certificates are listed below the Class [__] and the Class [__] certificates in the chart, the Class [EC] certificates' payment entitlements and subordination priority will be a result of the payment entitlements and subordination priority at each level of the related component classes of Class [A], Class [B], and Class [C] certificates. For purposes of determining the approximate initial credit support for Class [EC] certificates, the calculation is based on the aggregate initial class certificate balance of the Class [A], Class [B], and Class [C] certificates as if they were a single class. |

| (10) | [The Class [EC] certificates will not have a pass-through rate, but will be entitled to receive the sum of the interest distributable on the percentage interests of the Class [A], Class [B], and Class [C] trust components represented by the Class [EC] certificates. The pass-through rates on the Class [A], Class [B], and Class [C] trust components will at all times be the same as the pass-through rates of the Class [A], Class [B], and Class [C] certificates.] |

| (11) | [The pass-through rate of the Class [__] certificates on each distribution date will be a per annum rate equal to the lesser of (i) the pass-through rate for such class specified in the table above and (ii) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which the related distribution date occurs. See "Description of the Certificates—Distributions—Pass-Through Rates".] |

| (12) | [The pass-through rate of the Class [__] certificates on each distribution date will be a per annum rate equal to the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which the related distribution date occurs. See "Description of the Certificates—Distributions—Pass-Through Rates".] |

| (13) | [The pass-through rate for the Class [__] certificates on each distribution date be a per annum rate equal to the weighted average of the net mortgage rates on the mortgage loans (in each case adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which the related distribution date occurs minus [__]%. See "Description of the Certificates—Distributions—Pass-Through Rates".] |

| [#] | [Insert description of pass-through rates for other offered certificates.] |

| (15) | The [LOAN-SPECIFIC CLASS] certificates will only receive distributions from, and will only incur losses with respect to, the trust subordinate companion loan related to the [______] mortgage loan. |

| (16) | For any distribution date, the pass-through rate on the [LOAN-SPECIFIC CLASS] certificates will be a fixed pass-through rate. |

| (17) | The Class R and Class [ARD] certificates are not represented in the above table. |

| SUMMARY OF CERTIFICATES | 3 |

| IMPORTANT NOTICE REGARDING THE OFFERED CERTIFICATES | 12 |

| IMPORTANT NOTICE ABOUT INFORMATION PRESENTED IN THIS PROSPECTUS | 12 |

| SUMMARY OF TERMS | 18 |

| RISK FACTORS | 47 |

| The Certificates May Not Be a Suitable Investment for You | 47 |

| Combination or "Layering" of Multiple Risks May Significantly Increase Risk of Loss | 47 |

| Risks Related to Market Conditions and Other External Factors | 47 |

| The Volatile Economy, Credit Crisis and Downturn in the Real Estate Market Have Adversely Affected and May Continue To Adversely Affect the Value of CMBS | 47 |

| Other Events May Affect the Value and Liquidity of Your Investment | 48 |

| Risks Relating to the Mortgage Loans | 48 |

| Mortgage Loans Are Non‑Recourse and Are Not Insured or Guaranteed | 48 |

| Risks of Commercial and Multifamily Lending Generally | 48 |

| Performance of the Mortgage Loans Will Be Highly Dependent on the Performance of Tenants and Tenant Leases | 50 |

| [Retail Properties Have Special Risks | 53 |

| [Office Properties Have Special Risks | 55 |

| [Multifamily Properties Have Special Risks | 56 |

| [Hotel Properties Have Special Risks | 58 |

| [Risks Relating to Affiliation with a Franchise or Hotel Management Company | 60 |

| [Self‑Storage Properties Have Special Risks | 60 |

| [Industrial Properties Have Special Risks | 61 |

| [Manufactured Housing Community Properties Have Special Risks | 62 |

| [Mixed Use Properties Have Special Risks | 63 |

| [Condominium Ownership May Limit Use and Improvements | 63 |

| Operation of a Mortgaged Property Depends on the Property Manager's Performance | 65 |

| Concentrations Based on Property Type, Geography, Related Borrowers and Other Factors May Disproportionately Increase Losses | 65 |

| Adverse Environmental Conditions at or Near Mortgaged Properties May Result in Losses | 66 |

| Risks Related to Redevelopment, Expansion and Renovation at Mortgaged Properties | 67 |

| Some Mortgaged Properties May Not Be Readily Convertible to Alternative Uses | 68 |

| Risks Related to Zoning Non‑Compliance and Use Restrictions | 70 |

| Risks Relating to Inspections of Properties | 71 |

| Risks Relating to Costs of Compliance with Applicable Laws and Regulations | 71 |

| Insurance May Not Be Available or Adequate | 71 |

| Terrorism Insurance May Not Be Available for All Mortgaged Properties | 72 |

| Risks Associated with Blanket Insurance Policies or Self‑Insurance | 73 |

| Limited Information Causes Uncertainty | 74 |

| Underwritten Net Cash Flow Could Be Based On Incorrect or Failed Assumptions | 74 |

| The Mortgage Loans Have Not Been Reviewed or Re‑Underwritten by Us | 75 |

| Static Pool Data Would Not Be Indicative of the Performance of this Pool | 76 |

| Appraisals May Not Reflect Current or Future Market Value of Each Property | 76 |

| [Seasoned Mortgage Loans Present Additional Risk of Repayment | 77 |

| The Performance of a Mortgage Loan and Its Related Mortgaged Property Depends in Part on Who Controls the Borrower and Mortgaged Property | 78 |

| The Borrower's Form of Entity May Cause Special Risks | 78 |

| A Bankruptcy Proceeding May Result in Losses and Delays in Realizing on the Mortgage Loans | 80 |

| Litigation Regarding the Mortgaged Properties or Borrowers May Impair Your Distributions | 80 |

| Other Financings or Ability to Incur Other Indebtedness Entails Risk | 81 |

| Tenancies‑in‑Common May Hinder Recovery | 83 |

| Risks Relating to Enforceability of Cross‑Collateralization | 83 |

| Risks Relating to Enforceability of Yield Maintenance Charges, Prepayment Premiums or Defeasance Provisions | 83 |

| Risks Associated with One Action Rules | 84 |

| State Law Limitations on Assignments of Leases and Rents May Entail Risks | 84 |

| Various Other Laws Could Affect the Exercise of Lender's Rights | 84 |

| [Risks of Anticipated Repayment Date Loans | 85 |

| Borrower May Be Unable To Repay Remaining Principal Balance on Maturity Date or Anticipated Repayment Date; Longer Amortization Schedules and Interest‑Only Provisions Increase Risk | 85 |

| [Risks Relating to Floating Rate Mortgage Loans] | 86 |

| Risks Related to Ground Leases and Other Leasehold Interests | 86 |

| [Leased Fee Properties Have Special Risks] | 88 |

| Increases in Real Estate Taxes May Reduce Available Funds | 88 |

| State and Local Mortgage Recording Taxes May Apply Upon a Foreclosure or Deed in Lieu of Foreclosure and Reduce Net Proceeds | 89 |

| [Risks Relating to Shari'ah Compliant Loans] | 89 |

| Risks Related to Conflicts of Interest | 89 |

| Interests and Incentives of the Originators, the Sponsors and Their Affiliates May Not Be Aligned With Your Interests | 89 |

| Interests and Incentives of the Underwriter Entities May Not Be Aligned With Your Interests | 91 |

| Potential Conflicts of Interest of the Master Servicer and the Special Servicer | 92 |

| Potential Conflicts of Interest of the Operating Advisor | 93 |

| Potential Conflicts of Interest of the Asset Representations Reviewer | 94 |

| Potential Conflicts of Interest of the Directing Certificateholder and the Companion Loan Holders | 94 |

| Potential Conflicts of Interest in the Selection of the Underlying Mortgage Loans | 95 |

| Conflicts of Interest May Occur as a Result of the Rights of the Applicable Directing Certificateholder To Terminate the Special Servicer of the Applicable Whole Loan | 96 |

| Other Potential Conflicts of Interest May Affect Your Investment | 96 |

| Other Risks Relating to the Certificates | 97 |

| The Certificates Are Limited Obligations | 97 |

| The Certificates May Have Limited Liquidity and the Market Value of the Certificates May Decline | 97 |

| Legal and Regulatory Provisions Affecting Investors Could Adversely Affect the Liquidity of the Offered Certificates | 98 |

| Nationally Recognized Statistical Rating Organizations May Assign Different Ratings to the Certificates; Ratings of the Certificates Reflect Only the Views of the Applicable Rating Agencies as of the Dates Such Ratings Were Issued; Ratings May Affect ERISA Eligibility; Ratings May Be Downgraded | 99 |

| Your Yield May Be Affected by Defaults, Prepayments and Other Factors | 101 |

| There Are Risks Relating to the Exchangeable Certificates | 105 |

| Subordination of the Subordinated Certificates and Class [EC] Certificates Will Affect the Timing of Distributions and the Application of Losses on the Subordinated Certificates and Class [EC] Certificates | 105 |

| [Pro Rata Allocation of Principal Between and Among the Subordinate Companion Loan |

| and the Related Mortgage Loan Prior to a Material Mortgage Loan Event Default. | 106 |

| Your Lack of Control Over the Issuing Entity and the Mortgage Loans Can Impact Your Investment | 106 |

| Risks Relating to Modifications of the Mortgage Loans | 110 |

| Sponsors May Not Make Required Repurchases or Substitutions of Defective Mortgage Loans or Pay Any Loss of Value Payment Sufficient to Cover All Losses on a Defective Mortgage Loan | 111 |

| Risks Relating to Interest on Advances and Special Servicing Compensation | 111 |

| Bankruptcy of a Servicer May Adversely Affect Collections on the Mortgage Loans and the Ability to Replace the Servicer | 111 |

| The Sponsors, the Depositor and the Issuing Entity Are Subject to Bankruptcy or Insolvency Laws That May Affect the Issuing Entity's Ownership of the Mortgage Loans | 112 |

| The Requirement of the Special Servicer to Obtain FIRREA‑Compliant Appraisals May Result in an Increased Cost to the Issuing Entity | 113 |

| [Risks Associated with Floating Rate Certificates] | 113 |

| Tax Matters and Changes in Tax Law May Adversely Impact the Mortgage Loans or Your Investment | 113 |

| DESCRIPTION OF THE MORTGAGE POOL | 115 |

| General | 115 |

| Certain Calculations and Definitions | 116 |

| Definitions | 116 |

| Mortgage Pool Characteristics | 126 |

| Overview | 126 |

| Property Types | 127 |

| Significant Mortgage Loans and Significant Obligors | 131 |

| Mortgage Loan Concentrations | 131 |

| Cross‑Collateralized Mortgage Loans; Multi‑Property Mortgage Loans and Related Borrower Mortgage Loans | 132 |

| Geographic Concentrations | 133 |

| Mortgaged Properties With Limited Prior Operating History | 133 |

| Tenancies‑in‑Common | 134 |

| [Condominium Interests | 134 |

| Fee & Leasehold Estates; Ground Leases | 134 |

| Environmental Considerations | 135 |

| Redevelopment, Renovation and Expansion | 136 |

| [Assessment of Property Value and Condition | 136 |

| Litigation and Other Considerations | 137 |

| Loan Purpose; Default History, Bankruptcy Issues and Other Proceedings | 137 |

| Tenant Issues | 137 |

| Tenant Concentrations | 137 |

| Lease Expirations and Terminations | 138 |

| Purchase Options and Rights of First Refusal | 140 |

| [Credit Lease Loans] | 140 |

| Affiliated Leases | 142 |

| Insurance Considerations | 142 |

| Use Restrictions | 143 |

| Appraised Value | 144 |

| Non‑Recourse Carveout Limitations | 144 |

| Real Estate and Other Tax Considerations | 144 |

| Delinquency Information | 145 |

| Certain Terms of the Mortgage Loans | 145 |

| Amortization of Principal | 145 |

| Due Dates; Mortgage Rates; Calculations of Interest | 145 |

| ARD Loan | 146 |

| Single Purpose Entity Covenants | 147 |

| Prepayment Protections and Certain Involuntary Prepayments | 147 |

| "Due‑On‑Sale" and "Due‑On‑Encumbrance" Provisions | 148 |

| Defeasance; Collateral Substitution | 149 |

| [Partial Releases] | 150 |

| Escrows | 150 |

| Mortgaged Property Accounts | 151 |

| [Delaware Statutory Trusts] | 151 |

| [Shari'ah Compliant Loan] | 151 |

| Exceptions to Underwriting Guidelines | 152 |

| Additional Indebtedness | 152 |

| General | 152 |

| Whole Loans | 152 |

| Mezzanine Indebtedness | 153 |

| Preferred Equity | 155 |

| Other Secured Indebtedness | 155 |

| Other Unsecured Indebtedness | 155 |

| The Whole Loans | 155 |

| General | 155 |

| The Serviced Pari Passu Whole Loan | 156 |

| The Serviced AB Whole Loan | 159 |

| The Non‑Serviced Whole Loan | 164 |

| Additional Information | 167 |

| TRANSACTION PARTIES | 167 |

| The Sponsors and Mortgage Loan Sellers | 167 |

| Bank of America, National Association | 167 |

| Bank of America's Commercial Mortgage Loan Underwriting Standards | 168 |

| Exceptions to Bank of America's Disclosed Underwriting Guidelines | 174 |

| Review of Bank of America Mortgage Loans | 174 |

| Repurchases and Replacements | 176 |

| Retained Interests in This Securitization | 179 |

| [NAMES OF OTHER SPONSORS] | 179 |

[The Originators] [IF THERE ARE ORIGINATORS THAT ARE NOT SPONSORS OR MORTGAGE LOAN SELLERS] | 179 |

| The Depositor | 179 |

| The Issuing Entity | 180 |

| The Trustee | 181 |

| The Certificate Administrator | 182 |

| The Master Servicer | 182 |

| The Non‑Serviced Master Servicer [DISCLOSURE TO BE ADDED IF NON‑SERVICED MASTER SERVICER SERVICES NON‑SERVICED MORTGAGE LOAN IN EXCESS OF 20% OF THE INITIAL POOL BALANCE OR IS AN AFFILIATED NON‑SERVICED MASTER SERVICER] | 183 |

| The Special Servicer | 184 |

| The Non‑Serviced Special Servicer [TO BE ADDED IF NON‑SERVICED SPECIAL SERVICER SERVICES NON‑SERVICED MORTGAGE LOAN IN EXCESS OF 20% OF THE INITIAL POOL BALANCE OR IS AN AFFILIATED NON‑SERVICED SPECIAL SERVICER] | 185 |

| [OTHER SERVICERS] | 185 |

| The Operating Advisor | 185 |

| The Asset Representations Reviewer | 186 |

| [CREDIT RISK RETENTION] | 186 |

| General | 187 |

| Determination of Amount of Required Credit Risk Retention | 190 |

| General | 190 |

| Swap Priced Principal Balance Certificates: | 190 |

| Interest-Only Certificates: | 193 |

| Yield Priced Principal Balance Certificates: | 196 |

| [Qualifying CRE Loans | 197 |

| DESCRIPTION OF THE CERTIFICATES | 197 |

| General | 197 |

| Exchanges of Exchangeable Certificates | 201 |

| Exchanges | 201 |

| Procedures | 202 |

| Distributions | 203 |

| Method, Timing and Amount | 203 |

| Available Funds | 203 |

| Priority of Distributions | 205 |

| Pass‑Through Rates | 206 |

| Interest Distribution Amount | 207 |

| Principal Distribution Amount | 208 |

| Certain Calculations with Respect to Individual Mortgage Loans | 209 |

| Excess Interest | 210 |

| Application Priority of Mortgage Loan Collections or Whole Loan Collections | 210 |

| Allocation of Yield Maintenance Charges and Prepayment Premiums | 213 |

| Assumed Final Distribution Date; Rated Final Distribution Date | 213 |

| Prepayment Interest Shortfalls | 214 |

| Subordination; Allocation of Realized Losses | 215 |

| Reports to Certificateholders; Certain Available Information | 217 |

| Certificate Administrator Reports | 217 |

| Information Available Electronically | 221 |

| Voting Rights | 225 |

| Delivery, Form, Transfer and Denomination | 225 |

| Book‑Entry Registration | 225 |

| Definitive Certificates | 228 |

| Certificateholder Communication | 228 |

| Access to Certificateholders' Names and Addresses | 228 |

| Requests to Communicate | 229 |

| List of Certificateholders | 229 |

| DESCRIPTION OF THE MORTGAGE LOAN PURCHASE AGREEMENTS | 229 |

| General | 229 |

| Dispute Resolution Provisions | 235 |

| Asset Review Obligations | 235 |

| POOLING AND SERVICING AGREEMENT | 235 |

| General | 235 |

| Assignment of the Mortgage Loans | 236 |

| Servicing Standard | 237 |

| Subservicing | 238 |

| Advances | 239 |

| P&I Advances | 239 |

| Servicing Advances | 239 |

| Recovery of Advances | 241 |

| Accounts | 242 |

| Withdrawals from the Collection Account | 245 |

| Servicing and Other Compensation and Payment of Expenses | 247 |

| General | 247 |

| Master Servicing Compensation | 251 |

| Special Servicing Compensation | 253 |

| Disclosable Special Servicer Fees | 256 |

| Certificate Administrator and Trustee Compensation | 257 |

| Operating Advisor Compensation | 257 |

| Asset Representations Reviewer Compensation | 258 |

CREFC® Intellectual Property Royalty License Fee | 258 |

| Appraisal Reduction Amounts | 258 |

| Maintenance of Insurance | 263 |

| Modifications, Waivers and Amendments | 265 |

| Enforcement of "Due‑on‑Sale" and "Due‑on‑Encumbrance" Provisions | 267 |

| Inspections; Collection of Operating Information | 268 |

| Collection of Operating Information | 268 |

| Special Servicing Transfer Event | 268 |

| Asset Status Report | 270 |

| Realization Upon Mortgage Loans | 273 |

| Sale of Defaulted Loans and REO Properties | 275 |

| The Directing Certificateholder | 278 |

| General | 278 |

| Major Decisions | 279 |

| Asset Status Report | 281 |

| Replacement of Special Servicer | 281 |

| Control Termination Event and Consultation Termination Event | 282 |

| Servicing Override | 283 |

| Rights of Holders of Companion Loans and Loan Specific Directing Certificateholder | 284 |

| Limitation on Liability of Directing Certificateholder | 285 |

| The Operating Advisor | 285 |

| General | 285 |

| [Duties of Operating Advisor While No Control Termination Event Has Occurred and Is Continuing | 286 |

| Duties of Operating Advisor While a Control Termination Event Has Occurred and Is Continuing | 287 |

| Recommendation of the Replacement of the Special Servicer | 288 |

| [Duties of Operating Advisor In General] | 289 |

| Additional Duties of Operating Advisor While an Operating Advisor Consultation Event Has Occurred and Is Continuing | 291 |

| Recommendation of the Replacement of the Special Servicer | 291 |

| Eligibility of Operating Advisor | 291 |

| Other Obligations of Operating Advisor | 292 |

| Delegation of Operating Advisor's Duties | 293 |

| Termination of the Operating Advisor With Cause | 293 |

| Rights Upon Operating Advisor Termination Event | 294 |

| Waiver of Operating Advisor Termination Event | 294 |

| Termination of the Operating Advisor Without Cause | 295 |

| Resignation of the Operating Advisor | 295 |

| Operating Advisor Compensation | 295 |

| The Asset Representations Reviewer | 296 |

| Asset Review | 296 |

| Eligibility of Asset Representations Reviewer | 299 |

| Other Obligations of Asset Representations Reviewer | 300 |

| Delegation of Asset Representations Reviewer's Duties | 300 |

| Asset Reviewer Termination Events | 300 |

| Rights Upon Asset Reviewer Termination Event | 301 |

| Termination of the Asset Representations Reviewer Without Cause | 301 |

| Resignation of Asset Representations Reviewer | 302 |

| Asset Representations Reviewer Compensation | 302 |

| Replacement of Special Servicer Without Cause | 302 |

| Termination of Servicer and Special Servicer for Cause | 305 |

| Servicer Termination Events | 305 |

| Rights Upon Servicer Termination Event | 306 |

| Waiver of Servicer Termination Event | 308 |

| Resignation of the Master Servicer and Special Servicer | 308 |

| Limitation on Liability; Indemnification | 308 |

| Enforcement of Mortgage Loan Seller's Obligations Under the MLPA | 311 |

| Dispute Resolution Provisions | 311 |

| Certificateholder's Rights When a Repurchase Request is Initially Delivered by a Certificateholder | 311 |

| Certificateholder's Rights When a Repurchase Request is Delivered by Another Party to the PSA | 312 |

| Resolution of a Repurchase Request | 312 |

| Mediation and Arbitration Provisions | 313 |

| Servicing of the Non‑Serviced Mortgage Loan | 314 |

| Rating Agency Confirmations | 316 |

| Evidence as to Compliance | 318 |

| Limitation on Rights of Certificateholders to Institute a Proceeding | 320 |

| Termination; Retirement of Certificates | 320 |

| Amendment | 321 |

| Resignation and Removal of the Trustee and the Certificate Administrator | 323 |

| Governing Law; Waiver of Jury Trial; and Consent to Jurisdiction | 324 |

| [DESCRIPTION OF THE DERIVATIVES INSTRUMENT] | 324 |

| [General | 324 |

| The Swap Contract | 325 |

| Significance Percentage | 326 |

| Termination Payments | 327 |

| The Swap Counterparty | 327 |

| CERTAIN LEGAL ASPECTS OF MORTGAGE LOANS | 327 |

| General | 327 |

| Types of Mortgage Instruments | 328 |

| Leases and Rents | 328 |

| Personalty | 328 |

| Foreclosure | 329 |

| General | 329 |

| Foreclosure Procedures Vary from State to State | 329 |

| Judicial Foreclosure | 329 |

| Equitable and Other Limitations on Enforceability of Certain Provisions | 329 |

| Nonjudicial Foreclosure/Power of Sale | 330 |

| Public Sale | 330 |

| Rights of Redemption | 331 |

| Anti‑Deficiency Legislation | 331 |

| Leasehold Considerations | 332 |

| Cooperative Shares | 332 |

| Bankruptcy Laws | 333 |

| Environmental Considerations | 338 |

| General | 338 |

| Superlien Laws | 338 |

| CERCLA | 338 |

| Certain Other Federal and State Laws | 339 |

| Additional Considerations | 339 |

| Due‑on‑Sale and Due‑on‑Encumbrance Provisions | 339 |

| Subordinate Financing | 340 |

| Default Interest and Limitations on Prepayments | 340 |

| Applicability of Usury Laws | 340 |

| Americans with Disabilities Act | 341 |

| Servicemembers Civil Relief Act | 341 |

| Anti‑Money Laundering, Economic Sanctions and Bribery | 341 |

| Potential Forfeiture of Assets | 342 |

| CERTAIN AFFILIATIONS, RELATIONSHIPS AND RELATED TRANSACTIONS INVOLVING TRANSACTION PARTIES | 342 |

| PENDING LEGAL PROCEEDINGS INVOLVING TRANSACTION PARTIES | 343 |

| USE OF PROCEEDS | 343 |

| YIELD AND MATURITY CONSIDERATIONS | 343 |

| Yield Considerations | 343 |

| General | 343 |

| Rate and Timing of Principal Payments | 344 |

| Losses and Shortfalls | 345 |

| Certain Relevant Factors Affecting Loan Payments and Defaults | 346 |

| Delay in Payment of Distributions | 347 |

| Yield on the Certificates with Notional Amounts | 347 |

| Weighted Average Life | 347 |

| Pre‑Tax Yield to Maturity Tables | 350 |

| MATERIAL FEDERAL INCOME TAX CONSIDERATIONS | 352 |

| General | 352 |

| Qualification as a REMIC | 353 |

| Status of Certificates | 355 |

| Taxation of Regular Interests | 355 |

| General | 355 |

| Original Issue Discount | 355 |

| [Variable Rate Regular Certificates | 358 |

| [Deferred Interest | 359 |

| Acquisition Premium | 359 |

| Market Discount | 359 |

| Premium | 360 |

| Election To Treat All Interest Under the Constant Yield Method | 361 |

| Treatment of Losses | 361 |

| Spread Maintenance Payments | 362 |

| Sale or Exchange of Regular Interests | 362 |

| Taxation of the [ARD Class] Certificates | 363 |

| Taxation of the Swap Contract | 363 |

| Taxation of Class [EC] and Exchangeable Certificates | 365 |

| [Exchangeable Certificates Representing Disproportionate Interests in Related Exchangeable Certificates. | 365 |

| Alternative Characterization. | 365 |

| Taxation of Exchange. | 366 |

| Taxation of the Class R Certificates | 366 |

| Taxation of REMIC Income | 366 |

| Basis and Losses | 367 |

| Treatment of Certain Items of REMIC Income and Expense | 367 |

| Original Issue Discount | 368 |

| [Deferred Interest | 368 |

| Market Discount | 368 |

| Premium | 368 |

| Limitations on Offset or Exemption of REMIC Income | 368 |

| Tax Related Restrictions on Transfer of the Class R Certificates | 369 |

| Sale or Exchange of the Class R Certificates | 372 |

| Taxes That May Be Imposed on a REMIC | 373 |

| Prohibited Transactions | 373 |

| Contributions to a REMIC After the Startup Day | 373 |

| Net Income from Foreclosure Property | 373 |

| Administrative Matters | 374 |

| Limitations on Deduction of Certain Expenses | 374 |

| Taxation of Certain Foreign Investors | 375 |

| Regular Interests | 375 |

| Class R Certificates | 375 |

| FATCA | 376 |

| Backup Withholding | 376 |

| Information Reporting | 376 |

| 3.8% Medicare Tax on "Net Investment Income" | 376 |

| Reporting Requirements | 377 |

| CERTAIN STATE AND LOCAL TAX CONSIDERATIONS | 378 |

| METHOD OF DISTRIBUTION (UNDERWRITER) | 378 |

| INCORPORATION OF CERTAIN INFORMATION BY REFERENCE | 380 |

| WHERE YOU CAN FIND MORE INFORMATION | 380 |

| FINANCIAL INFORMATION | 381 |

| CERTAIN ERISA CONSIDERATIONS | 381 |

| General | 381 |

| Plan Asset Regulations | 382 |

| Administrative Exemptions | 382 |

| Insurance Company General Accounts | 384 |

| Unrelated Business Taxable Income; Residual Certificates | 384 |

| LEGAL INVESTMENT | 385 |

| LEGAL MATTERS | 385 |

| RATINGS | 386 |

| INDEX OF DEFINED TERMS | 388 |

| ANNEX A-1 | CERTAIN CHARACTERISTICS OF THE MORTGAGE LOANS AND MORTGAGED PROPERTIES |

| ANNEX A-2 | MORTGAGE POOL INFORMATION (TABLES) |

| ANNEX A-3 | SIGNIFICANT LOAN SUMMARIES |

| ANNEX B | FORM OF REPORT TO CERTIFICATEHOLDERS |

| ANNEX C | FORM OF OPERATING ADVISOR ANNUAL REPORT |

| ANNEX D-1 | MORTGAGE LOAN REPRESENTATIONS AND WARRANTIES |

| ANNEX D-2 | EXCEPTIONS TO MORTGAGE LOAN REPRESENTATIONS AND WARRANTIES |

| ANNEX E | CLASS [A-SB] PLANNED PRINCIPAL BALANCE SCHEDULE |

| Title of Certificates | [TRUST NAME] Commercial Mortgage Pass Through Certificates, Series [___]-[___]. | ||

| Relevant Parties | |||

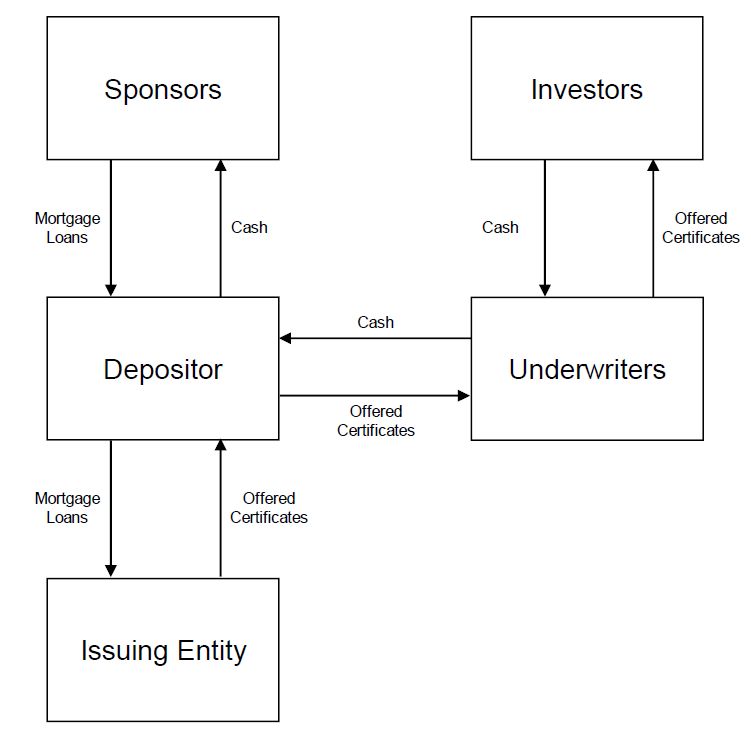

| Depositor | Banc of America Merrill Lynch Commercial Mortgage Inc., a Delaware corporation, a wholly-owned subsidiary of Bank of America, National Association, a national banking association organized under the laws of the United States of America, which is a wholly-owned subsidiary of Bank of America Corporation, a Delaware corporation. The depositor's address is One Bryant Park, New York, New York 10036, and its telephone number is (980) 388-7451. See "Transaction Parties—The Depositor". | ||

| Issuing Entity | [TRUST NAME][INSERT SERIES DESIGNATION], a New York common law trust, to be established on the closing date under the pooling and servicing agreement. For more detailed information, see "Transaction Parties—The Issuing Entity". | ||

| Sponsors | The sponsors of this transaction are: | ||

| · | Bank of America, National Association, a national banking association | ||

| · | [NAMES OF OTHER SPONSORS] | ||

[The sponsors are sometimes also referred to in this prospectus as the "mortgage loan sellers".] The sponsors originated or acquired the mortgage loans and will transfer to the depositor the mortgage loans as set forth in the following chart: | |||

| Sellers of the Mortgage Loans | |||

Seller | Number of Mortgage Loans | Aggregate Principal Balance of Mortgage Loans | Approx. % of Initial Pool Balance | |||||

| [BANK OF AMERICA, NATIONAL ASSOCIATION] | $ | % | ||||||

[LOAN SELLER] | ||||||||

[LOAN SELLER] | ||||||||

Total | $ | 100.0% |

| [INSERT APPROPRIATE FOOTNOTES] |

See "Transaction Parties—The Sponsors and Mortgage Loan Sellers". [In addition, [NAME OF LOAN SELLER] will also transfer to the depositor a subordinate companion loan relating to [NAME OF WHOLE LOAN] mortgage loan, as described below under "—The Mortgage Pool—Whole Loans".] | ||

| [Originator | ADD DISCLOSURE REGARDING AN ORIGINATOR THAT IS NOT A SPONSOR] | |

| Master Servicer | [NAME OF MASTER SERVICER] will be the master servicer and will be responsible for the master servicing and administration of the mortgage loans and the related companion loans pursuant to the pooling and servicing agreement (other than the mortgage loan and companion loan identified in the table below that is part of a whole loan and serviced under the pooling and servicing agreement indicated in the table titled "Non-Serviced Whole Loan" under "The Mortgage Pool—Whole Loans" below). The offices of the master servicer are located at [INSERT ADDRESS]. See "Transaction Parties—The Master Servicer" and "Pooling and Servicing Agreement". [OTHER SERVICERS] [TO THE EXTENT APPLICABLE, DISCLOSURE WILL BE ADDED REGARDING OTHER APPLICABLE SERVICERS] The master servicer of the non-serviced mortgage loan is set forth in the table below under the heading "Non-Serviced Whole Loan" under "The Mortgage Pool—Whole Loans". See "Transaction Parties—The Non-Serviced Master Servicer" and "Pooling and Servicing Agreement—Servicing of the Non-Serviced Mortgage Loan". | |

| Special Servicer | [NAME OF SPECIAL SERVICER] will act as special servicer with respect to the mortgage loans and the related companion loans other than with respect to the non-serviced mortgage loan set forth in the table titled "Non-Serviced Whole Loan" under "—The Mortgage Pool—Whole Loans" below. The special servicer will be primarily responsible for (i) making decisions and performing certain servicing functions with respect to such mortgage loans and related companion loans as to which a special servicing transfer event (such as a default or an imminent default) has occurred and (ii) in certain circumstances, reviewing, evaluating, processing and providing or withholding consent as to certain major decisions and other transactions relating to such mortgage loans and related companion loans for which a special servicing transfer event has not occurred, in each case pursuant to the pooling and servicing agreement for this transaction. The primary servicing office of the special servicer is located at [INSERT ADDRESS] See "Transaction Parties—The Special Servicer" and "Pooling and Servicing Agreement". The special servicer was appointed to be the special servicer by [NAME OF "B-PIECE" BUYER], which is expected to purchase the Class [__] and [__] certificates (and may purchase certain other classes of certificates) and, on the closing date, is |

expected to be the initial directing certificateholder. See "Pooling and Servicing Agreement—The Directing Certificateholder". The special servicer of the non-serviced mortgage loan is set forth in the table below titled "Non-Serviced Whole Loan" under "—The Mortgage Pool—Whole Loans". See "Transaction Parties—The Non-Serviced Special Servicer" and "Pooling and Servicing Agreement—Servicing of the Non-Serviced Mortgage Loan". | ||

| [Primary Servicer | ADD DISCLOSURE REGARDING PRIMARY SERVICER AS REQUIRED BY ITEM 1108 OF REGULATION AB IF GREATER THAN 20% OR AN AFFILIATE.] | |

| Trustee | [NAME OF TRUSTEE] will act as trustee. The corporate trust office of the trustee is located at [INSERT ADDRESS]. Following the transfer of the mortgage loans and [one] trust subordinate companion loan to the issuing entity, the trustee, on behalf of the issuing entity, will become the mortgagee of record for each mortgage loan (other than the non-serviced mortgage loan) and the related companion loans (including the trust subordinate companion loan to be held by the issuing entity). See "Transaction Parties—The Trustee" and "Pooling and Servicing Agreement". With respect to the non-serviced mortgage loan, the entity set forth in the table titled "Non-Serviced Whole Loan" under "The Mortgage Pool—Whole Loans" below, in its capacity as trustee under the pooling and servicing agreement for the indicated transaction, is the mortgagee of record for that non-serviced mortgage loan and any related companion loan. See "Pooling and Servicing Agreement—Servicing of the Non-Serviced Mortgage Loan". | |

| Certificate Administrator | [NAME OF CERTIFICATE ADMINISTRATOR] will initially act as certificate administrator. The certificate administrator will also be required to act as custodian, certificate registrar and authenticating agent. The office of the certificate administrator is located at [INSERT ADDRESS]. See "Transaction Parties—The Certificate Administrator" and "Pooling and Servicing Agreement". [The custodian with respect to the non-serviced mortgage loan will be the entity set forth in the table below titled "Non-Serviced Whole Loan" under "The Mortgage Pool—Whole Loans", the custodian under the pooling and servicing agreement for the indicated transaction.] See "Pooling and Servicing Agreement—Servicing of the Non-Serviced Mortgage Loan". | |

| Operating Advisor | [NAME OF OPERATING ADVISOR] will be the operating advisor. The operating advisor will have certain review and reporting responsibilities with respect to the performance of the special servicer, and in certain circumstances may recommend to the certificateholders that the special servicer be replaced. The operating advisor will generally have no obligations or consultation rights under the pooling and servicing agreement for this transaction with respect to the non-serviced mortgage loan |

or any related REO property. See "Transaction Parties—The Operating Advisor" and "Pooling and Servicing Agreement—The Operating Advisor". | ||

| Asset Representations Reviewer | [NAME OF ASSET REPRESENTATIONS REVIEWER] will be the asset representations reviewer. The asset representations reviewer will be required to review certain delinquent mortgage loans after a specified delinquency threshold has been exceeded and the required percentage of certificateholders vote to direct a review of such delinquent mortgage loans. See "Transaction Parties—The Asset Representations Reviewer" and "Pooling and Servicing Agreement—The Asset Representations Reviewer". | |

| Directing Certificateholder | Subject to the rights of the holders of the subordinate companion loan (or directing certificateholder for the [LOAN–SPECIFIC CLASS] certificates, in the case of the trust subordinate companion loan) described under "Description of the Mortgage Pool—The Whole Loans—The Serviced AB Whole Loan", the directing certificateholder will have certain consent and consultation rights in certain circumstances with respect to the mortgage loans (other than the non-serviced mortgage loan), as further described in this prospectus. The directing certificateholder will generally be the controlling class certificateholder (or its representative) selected by more than a specified percentage of the controlling class certificateholders (by certificate balance, as certified by the certificate registrar from time to time as provided for in the pooling and servicing agreement). See "Pooling and Servicing Agreement—The Directing Certificateholder". However, in certain circumstances there may be no directing certificateholder even if there is a controlling class, and in other circumstances there will be no controlling class. The controlling class will be the most subordinate class of the Class [__], Class [__] and Class [__] certificates then-outstanding that has an aggregate certificate balance, as notionally reduced by any appraisal reductions allocable to such class, at least equal to 25% of the initial certificate balance of that class[; provided, however, that during such time as the Class [__] certificates would be the controlling class, the holders of such certificates will have the right to irrevocably waive their right to appoint a directing certificateholder or to exercise any of the rights of the controlling class certificateholder. No class of certificates, other than as described above, will be eligible to act as the controlling class or appoint a directing certificateholder. It is anticipated that an affiliate of [NAME OF "B-PIECE" BUYER] will purchase the Class [__] and Class [__] certificates (and may purchase certain other classes of certificates) and, on the closing date, is expected to be the initial directing certificateholder with respect to each mortgage loan (other than the non-serviced mortgage loan). With respect to any subordinate companion loan described under "Description of the Mortgage Pool—The Whole Loans— |

The Serviced AB Whole Loan", during such time as the holders of the subordinate companion loan (or the directing certificateholder for the [LOAN-SPECIFIC CLASS] certificates, which class represents the beneficial interest in the trust subordinate companion loan) are no longer permitted to exercise control or consultation rights under the related intercreditor agreement, the directing certificateholder will generally have the same consent and consultation rights with respect to the related AB mortgage loan as it does for the other mortgage loans in the pool. See "Description of the Mortgage Pool—The Whole Loans—The Serviced AB Whole Loan". The entity identified in the table titled "Non-Serviced Whole Loan" under "—The Mortgage Pool—Whole Loans" below is the initial directing certificateholder under the pooling and servicing agreement for the indicated transaction and will have certain consent and consultation rights with respect to the non-serviced whole loan, which are substantially similar, but not identical, to those of the directing certificateholder under the pooling and servicing agreement for this securitization, subject to similar appraisal mechanics. See "Description of the Mortgage Pool—The Whole Loans—The Non-Serviced Whole Loan" and "Pooling and Servicing Agreement—Servicing of the Non-Serviced Mortgage Loan". | ||

| Holders of the [LOAN-SPECIFIC | ||

| CLASS] Certificates | [One (1)] mortgage loan identified as "[_____]" on Annex A-1, representing approximately [__]% of the aggregate principal balance of the pool of mortgage loans as of the cut-off date, has a trust subordinate companion loan (a subordinate interest in the related whole loan), and such trust subordinate companion loan will also be held by the issuing entity. The [LOAN SPECIFIC CLASS] certificates will be backed solely by such trust subordinate companion loan, and any expenses or losses incurred in respect to the other mortgage loans will not be borne by the holders of such [LOAN SPECIFIC CLASS] certificates. The loan-specific directing certificateholder appointed by the holders of more than 50% of the certificate balance of the [LOAN SPECIFIC CLASS] certificates will be entitled to exercise certain of the rights of the holder of the trust subordinate companion loan under the related intercreditor agreement on behalf of the holders of the [LOAN SPECIFIC CLASS] certificates, as the beneficial owner of such certificates. See "Description of the Mortgage Pool—The Whole Loans—The Serviced AB Whole Loan". [IF NO TRUST SUBORDINATE COMPANION LOAN IS HELD BY THE ISSUING ENTITY, NO LOAN SPECIFIC CERTIFICATES WILL BE ISSUED.] | |

| Underwriters | Merrill Lynch, Pierce, Fenner & Smith Incorporated, [ADDITIONAL UNDERWRITERS] are the underwriters. Merrill Lynch, Pierce, Fenner & Smith Incorporated is an affiliate of Bank of America, National Association, a sponsor and mortgage loan seller, and Banc of America Merrill Lynch Large Loan Inc., the depositor. [ADDITIONAL UNDERWRITER AFFILIATION INFORMATION] The underwriters are required to purchase the certificates offered in this prospectus from the depositor (in the |

amounts to be set forth under the heading "Method of Distribution (Underwriter)" in this prospectus, subject to certain conditions. | ||

| Certain Affiliations | The originators, the sponsors, the underwriters, and parties to the pooling and servicing agreement have various roles in this transaction as well as certain relationships with parties to this transaction and certain of their affiliates. These roles and other potential relationships may give rise to conflicts of interest as further described in this prospectus under "Risk Factors—Risks Related to Conflicts of Interest". | |

| Significant Obligors | The borrowers related to the mortgage loans identified on Annex A-1 as [_____], [_____] and [_____], [are affiliated and] represent [__]% of the aggregate principal balance of the pool of mortgage loans as of the cut-off date. See "Description of the Mortgage Pool—Mortgage Pool Characteristics—Significant Mortgage Loans and Significant Obligors". [INCLUDE FOR ANY BORROWER REPRESENTING 10% OR MORE OF POOL, IF ANY.] The mortgaged properties related to the mortgage loans identified on Annex A-1 as [_____], [_____] and [_____], [are related and] represent [__]% of the aggregate principal balance of the pool of mortgage loans as of the cut-off date. See "Description of the Mortgage Pool—Mortgage Pool Characteristics—Significant Mortgage Loans and Significant Obligors". [INCLUDE FOR ANY MORTGAGED PROPERTY REPRESENTING 10% OR MORE OF POOL, IF ANY.] Certain of the lessees occupying all or a portion of the mortgaged properties related to the mortgage loans identified on Annex A-1 as [______], [_____] and [_____], [are affiliated and] represent [__]% of the [cash flow of the] initial mortgage pool. See "Description of the Mortgage Pool—Mortgage Pool Characteristics—Significant Mortgage Loans and Significant Obligors". [INCLUDE FOR ANY LESSEE ACCOUNTING FOR 10% OR MORE OF CASH FLOW, IF ANY.] [INCLUDE INFORMATION REQUIRED BY ITEM 1112(a) and (b) FOR EACH SIGNIFICANT OBLIGOR] | |

| [Swap Counterparty | [_____], a [insert entity type and jurisdiction of organization]. [_____] [is an affiliate of the depositor, and of [_____], [one of the sponsors], and [_____], one of the underwriters.] [_____], a [insert entity type and jurisdiction of organization].] [INSERT IDENTITY OF COUNTERPARTY TO ANY OTHER DERIVATIVE AGREEMENTS AS REQUIRED BY ITEM 1114 OF REGULATION AB] | |

| Relevant Dates And Periods | ||

| Cut-off Date | [______]. | |

| Closing Date | On or about [_______]. | |

Distribution Date | The [__] business day following each determination date. The first distribution date will be in [______]. | ||

| Determination Date | The [__] day of each month or, if the [__] day is not a business day, then the business day immediately following such [__] day. | ||

| Record Date | With respect to any distribution date, [the last business day of the month preceding the month in which that distribution date occurs][INSERT OTHER RECORD DATE]. | ||

| Interest Accrual Period | Interest will accrue on the offered certificates during the [calendar month prior to the related distribution date][INSERT OTHER ACCRUAL PERIOD]. [Interest will be calculated on the offered certificates assuming each month has 30 days and each year has 360 days.] | ||

| Collection Period | For any mortgage loan or the trust subordinate companion loan to be held by the issuing entity and any distribution date, the period commencing on [the day immediately following the due date for such mortgage loan in the month preceding the month in which that distribution date occurs and ending on and including the due date for such mortgage loan in the month in which that distribution date occurs][INSERT OTHER SERIES SPECIFIC COLLECTION PERIOD]. However, in the event that the last day of a collection period (or applicable grace period) is not a business day, any periodic payments received with respect to the mortgage loans relating to that collection period on the business day immediately following that last day will be deemed to have been received during that collection period and not during any other collection period. | ||

| Assumed Final Distribution | |||

| Date; Rated Final | |||

| Distribution Date | The assumed final distribution dates set forth below for each class have been determined on the basis of the assumptions described in "Description of the Certificates—Assumed Final Distribution Date; Rated Final Distribution Date": | ||

[CLASS DESIGNATIONS] | [DATES] | ||

| The rated final distribution date will be the distribution date in [__________]. | |||

| [(1) | Although the trust subordinate companion loan is an asset of the issuing entity, amounts distributable to the trust subordinate companion loan pursuant to its related intercreditor agreement will be payable only to the [LOAN-SPECIFIC CLASS] certificates and therefore support only the [LOAN-SPECIFIC CLASS] certificates.] |

General | We are offering the following classes of commercial mortgage pass-through certificates as part of Series [____]: | ||

| · | [CLASS DESIGNATIONS] | ||

| The certificates of this Series will consist of the above classes and the following classes that are not being offered by this prospectus: [SERIES DESIGNATIONS OF NON-OFFERED CLASSES]. [The certificates, other than the [LOAN-SPECIFIC CLASS] certificates, are referred to in this prospectus as the pooled certificates.] | |||

| Certificate Balances and | |||

| Notional Amounts | Your certificates will have the approximate aggregate initial certificate balance or notional amount set forth below, subject to a variance of plus or minus 5%: | ||

[CLASS DESIGNATIONS] | [INITIAL CLASS BALANCES] | ||

| ____________________ | |||

| (1) | The initial certificate balance of each class of the Class [A], Class [B], and Class [C] certificates shown in the table above represents the maximum certificate balance of such class without giving effect to any issuance of the Class [EC] certificates. The initial certificate balance of the Class [EC] certificates shown in the table above is equal to the aggregate of the maximum initial certificate balance of the Class [A], Class [B], and Class [C] certificates, which is the maximum certificate balance of the Class [EC] certificates that could be issued in an exchange. The actual certificate balance of any class of Class [A], Class [B], and Class [C] certificates or Class [EC] certificates issued on the closing date may be less than the maximum certificate balance of that class and may be zero. The certificate balance of the Class [A], Class [B], and Class [C] certificates to be issued on the closing date will be reduced, in required proportions, by an amount equal to the certificate balance of the Class [EC] certificates issued on the closing date, if any. | ||

| (2) | Notional amount. | ||

| Pass-Through Rates | |||

| A. Offered Certificates | Your certificates will accrue interest at an annual rate called a pass-through rate. The initial approximate pass-through rate is set forth below for each class: | ||

| [CLASS DESIGNATION] | [PASS-THROUGH RATE] | ||

| ____________________ | |||

| (1) | The pass-through rate for the [INTEREST-ONLY CLASS] certificates for any distribution date will equal [the excess, if any, of (a) the weighted average of the net mortgage rates on the mortgage loans (in each case adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months), over (b) the weighted average of the pass-through rates of the Class [__] and Class [__] certificates and the Class [__] trust component for that distribution date, weighted on the basis of their respective certificate balances immediately prior to that distribution date. The pass-through rate for the [INTEREST-ONLY CLASS] certificates for any distribution date will equal the excess, if any, of (a) the weighted average of the net mortgage rates on the mortgage loans (in each case adjusted, if necessary, to accrue on the basis of a 360-day year consisting of | ||

| twelve 30-day months) for the related distribution date, over (b) the weighted average of the pass-through rates of the Class [__] certificates and the Class [__] and Class [__] trust components for that distribution date, weighted on the basis of their respective certificate balances immediately prior to that distribution date. | |||

| (2) | [The pass-through rate of the Class [__] certificates will be a per annum rate equal to the lesser of (i) the pass-through rate for such class specified in the table above and (ii) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which the related distribution date occurs.] | ||

| (3) | [The Class [EC] certificates will not have a pass-through rate, but will be entitled to receive the sum of the interest distributable on the percentage interests of the Class [A], Class [B], and Class [C] trust components represented by the Class [EC] certificates. The pass-through rates on the Class [A], Class [B], and Class [C] trust components will at all times be the same as the pass-through rates of the Class [A], Class [B], and Class [C] certificates, respectively.] | ||

| (4) | [The pass-through rate of the Class [__] certificates will be a per annum rate equal to the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which the related distribution date occurs.] | ||

| (5) | [The pass-through rate applicable to the Class [__] certificates on each distribution date will be a per annum rate equal to the weighted average of the net mortgage rates on the mortgage loans (in each case adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) for such distribution date as of their respective due dates in the month preceding the month in which the related distribution date occurs minus [__]%.]. | ||

| (6) | [Insert description of pass-through rates for other offered certificates.] |

B. Class [EC] and | ||

| Exchangeable Certificates | If you own Class [EC] certificates, you will be able to exchange them for a proportionate interest in the Class [A], Class [B] or Class [C] certificates (sometimes referred to in this prospectus as "exchangeable certificates"), and if you own exchangeable certificates you will be able to exchange them for a proportionate interest in the Class [EC] certificates. You can exchange your Class [EC] certificates or exchangeable certificates by notifying the certificate administrator. If Class [EC] certificates or exchangeable certificates are outstanding and held by certificateholders, those certificates will receive principal and interest that would otherwise have been payable on the same proportion of certificates exchanged for them if those certificates were outstanding and held by certificateholders. Any such allocation of principal and interest between Class [EC] certificates on the one hand and exchangeable certificates on the other hand will have no effect on the principal or interest entitlements of any other class of certificates. Exchanges will be subject to various conditions that we describe in this prospectus. See "Description of the Certificates—Exchanges of Exchangeable Certificates" for a description of the exchange procedures relating to the Class [EC] certificates and the exchangeable certificates. See also "Risk Factors—Other Risks Relating to the Certificates—There Are Risks Relating to the Exchangeable Certificates". | |

| C. Interest Rate Calculation | ||

| Convention | Interest on the offered certificates at their applicable pass-through rates will be calculated based on a [360-day year consisting of twelve 30-day months, or a "30/360 basis"][IDENTIFY OTHER CALCULATION CONVENTION]. For purposes of calculating the pass-through rates on the [INTEREST-ONLY CLASSES] certificates and any other class of |

certificates or trust component that has a pass-through rate limited by, equal to or based on the weighted average net mortgage interest rate (which calculation does not include any companion loan interest rate), the mortgage loan interest rates will not reflect any default interest rate, any loan term modifications agreed to by the applicable special servicer or any modifications resulting from a borrower's bankruptcy or insolvency. [For purposes of calculating the pass-through rates on the offered certificates (other than the Class [EC] certificates), the interest rate for each mortgage loan that accrues interest based on the actual number of days in each month and assuming a 360-day year, or an "actual/360 basis", will be recalculated, if necessary, so that the amount of interest that would accrue at that recalculated rate in the applicable month, calculated on a 30/360 basis, will equal the amount of interest that is required to be paid on that mortgage loan in that month, subject to certain adjustments as described in "Description of the Certificates—Distributions—Pass-Through Rates" and "—Interest Distribution Amount".] | ||

| D. Servicing and | ||

| Administration Fees | The master servicer and special servicer are entitled to a master servicing fee and a special servicing fee, respectively, from the interest payments on each mortgage loan (other than the non-serviced mortgage loan with respect to the special servicing fee only), the serviced companion loans and any related REO loans and, with respect to the special servicing fees, if the related loan interest payments (or other collections in respect of the related mortgage loan or mortgaged property) are insufficient, then from general collections on all mortgage loans. The servicing fee for each distribution date, including the master servicing fee [and the portion of the servicing fee payable to any primary servicer or subservicer], is calculated on the [outstanding][stated] principal amount of each mortgage loan (including the non-serviced mortgage loan) and the related serviced companion loans at the servicing fee rate equal to a per annum rate [ranging from [______]% to [_____]%]. The special servicing fee for each distribution date is calculated based on the outstanding principal amount of each mortgage loan (other than the non-serviced mortgage loan) and the related serviced companion loans as to which a special servicing transfer event has occurred (including any REO loans), on a loan-by-loan basis at the special servicing fee rate equal to [___]% [add caps or minimums]. The special servicer will not be entitled to a special servicing fee with respect to the non-serviced mortgage loan. Any primary servicing fees or sub-servicing fees with respect to each mortgage loan (other than the non-serviced mortgage loan) and the related serviced companion loans will be paid by the related master servicer or special servicer, respectively, out of the fees described above. |

The master servicer and special servicer are also entitled to additional fees and amounts, including income on the amounts held in certain accounts and certain permitted investments, liquidation fees and workout fees. See "Pooling and Servicing Agreement—Servicing and Other Compensation and Payment of Expenses". The certificate administrator fee for each distribution date is calculated on the outstanding principal amount of each mortgage loan (including any REO loan and non-serviced mortgage loan) and the trust subordinate companion loan at a per annum rate equal to [____]%. [The trustee fee is payable by the certificate administrator from the certificate administrator fee and is equal to [___].] The operating advisor will be entitled to a fee on each distribution date calculated on the outstanding principal amount of each mortgage loan and REO loan (including the non-serviced mortgage loan) and the trust subordinate companion loan at a per annum rate equal to [____]%. The operating advisor will also be entitled under certain circumstances to a consulting fee. The asset representations reviewer will be entitled to a fee in the amount of $[_________] per loan upon the completion of the review it conducts with respect to certain delinquent mortgage loans. [DISCLOSE ANY RETAINER FEE OR SIMILAR FEE PAID TO THE ASSET REPRESENTATIONS REVIEWER, IF APPLICABLE] Each party to the pooling and servicing agreement will also be entitled to be reimbursed by the issuing entity for costs, expenses and liabilities borne by them in certain circumstances. Fees and expenses payable by the issuing entity to any party to the pooling and servicing agreement are generally payable prior to any distributions to certificateholders. Additionally, with respect to each distribution date, an amount equal to the product of [__]% per annum multiplied by the outstanding principal amount of each mortgage loan[, the trust subordinate companion loan] and any REO loan will be payable to CRE Finance Council© as a license fee for use of their names and trademarks, including an investor reporting package. This fee will be payable prior to any distributions to certificateholders. Payment of the fees and reimbursement of the costs and expenses described above will generally have priority over the distribution of amounts payable to the certificateholders. See "Pooling and Servicing Agreement—Servicing and Other Compensation and Payment of Expenses" and "—Limitation on Liability; Indemnification". With respect to the non-serviced mortgage loan set forth in the table below, the master servicer under the related pooling and servicing agreement governing the servicing of that loan will be entitled to a master servicing fee at a rate equal to a per annum rate set forth in the table below, and the special servicer under the related pooling and servicing agreement will be entitled to a |

special servicing fee at a rate equal to the per annum rate set forth below. In addition, each party to the related pooling and servicing agreement governing the servicing of the non-serviced whole loan will be entitled to receive other fees and reimbursements with respect to the non-serviced mortgage loan in amounts, from sources, and at frequencies, that are similar, but not necessarily identical, to those described above and, in certain cases (for example, with respect to unreimbursed special servicing fees and servicing advances with respect to the non-serviced whole loan), such amounts will be reimbursable from general collections on the mortgage loans to the extent not recoverable from the non-serviced whole loan and to the extent allocable to the non-serviced mortgage loan pursuant to the related intercreditor agreement. See "Description of the Mortgage Pool—The Whole Loans—The Non-Serviced Whole Loan" and "Pooling and Servicing Agreement—Servicing of the Non-Serviced Mortgage Loan". | ||

| Non-Serviced Mortgage Loans |

Non-Serviced Loan | Master Servicer Fee | Special Servicer Fee | ||||

| A. Amount and Order of | ||

| Distributions | On each distribution date, funds available for distribution from the mortgage loans, net of (i) specified expenses of the issuing entity, including fees payable to, and costs and expenses reimbursable to, the master servicer, the special servicer, the certificate administrator, the trustee, the operating advisor, and the asset representations reviewer, (ii) any yield maintenance charges and prepayment premiums and (iii) any excess interest distributable to the Class [ARD] certificates, will be distributed in the following amounts and order of priority: First, to the [APPLICABLE SENIOR CLASSES] certificates, in respect of interest, up to an amount equal to, and pro rata in accordance with the interest entitlements for those classes; Second, to the [APPLICABLE SENIOR CLASSES] certificates, in reduction of the then-outstanding certificate balances of those classes, in the following priority (prior to the Cross-Over Date): [INSERT PRINCIPAL PAYMENT PRIORITIES FOR THE SENIOR CLASSES] However, if the certificate balances of each class of certificates, other than the [APPLICABLE SENIOR CLASSES] certificates, having an initial principal balance have been reduced to zero, funds available for distributions of principal will be distributed to the [APPLICABLE SENIOR CLASSES] certificates, pro rata, based on their respective certificate balances; Third, to the [APPLICABLE SENIOR CLASSES] certificates, up to an amount equal to, and pro rata based upon, the aggregate unreimbursed losses on the mortgage loans previously allocated |

to each such class, plus interest on that amount at the pass-through rate for such class; Fourth, to the Class [A], Class [B], and Class [C] trust components and, thus, concurrently, to the Class [A], Class [B], and Class [C] certificates and the Class [EC] certificates as follows: (a) to interest on the Class [A], Class [B], and Class [C] trust components (and, therefore, to the Class [A], Class [B], and Class [C] and Class [EC] certificates pro rata based on their respective percentage interests in the Class [A], Class [B], and Class [C] trust components) in the amount of its interest entitlement; (b) to the extent of funds allocable to principal remaining after distributions in respect of principal to each class with a higher priority (as set forth in prior enumerated clauses set forth above), to principal on the Class [A], Class [B], and Class [C] trust components (and, therefore, to the Class [A], Class [B], and Class [C] and Class [EC] certificates pro rata based on their respective percentage interests in the Class [A], Class [B], and Class [C] trust components) until its certificate balance has been reduced to zero; and (c) to reimburse the Class [A], Class [B], and Class [C] trust components (and, therefore, to the Class [A], Class [B], and Class [C] and Class [EC] certificates pro rata based on their respective percentage interests in the Class [A], Class [B], and Class [C] trust components) for any previously unreimbursed losses on the mortgage loans that were previously allocated to that trust component (and, therefore, those certificates), together with interest; Fifth, [ADD SIMILAR CLAUSES TO CLAUSE FOURTH FOR OTHER EXCHANGEABLE CLASSES] Sixth, to the Class [__] as follows: (a) to interest on the Class [__] certificates in the amount of its interest entitlement; (b) to the extent of funds allocable to principal remaining after distributions in respect of principal to each class with a higher priority (as set forth in prior enumerated clauses set forth above), to principal on the Class [__] certificates until its certificate balance has been reduced to zero; and (c) to reimburse the Class [__] certificates for any previously unreimbursed losses on the mortgage loans that were previously allocated to that class of certificates, together with interest on that amount at the pass-through rate for such class; Seventh, [ADD SIMILAR CLAUSES TO CLAUSE SIXTH FOR OTHER SUBORDINATE CLASSES THAT ARE NOT EXCHANGEABLE CLASSES]; and Eighth, to the Class R certificates, any remaining amounts. For more detailed information regarding distributions on the certificates, see "Description of the Certificates—Distributions—Priority of Distributions". | ||

| B. Interest and Principal | ||

| Entitlements | A description of the interest entitlement of each class of certificates [(other than the Class [LOAN-SPECIFIC CLASS], |

Class R and Class [ARD] certificates)] can be found in "Description of the Certificates—Distributions—Interest Distribution Amount". As described in that section, there are circumstances in which your interest entitlement for a distribution date could be less than one full month's interest at the pass-through rate on your certificate's balance or notional amount (or, in the case of the Class [EC] certificates, the related pass-through rates on the applicable percentage interest of the related certificate balances of the Class [A],Class [B] and Class [C] trust components). A description of the amount of principal required to be distributed to each class of certificates entitled to principal on a particular distribution date (other than the [LOAN-SPECIFIC CLASS] certificates) can be found in "Description of the Certificates—Distributions—Principal Distribution Amount". | ||

| C. Yield Maintenance Charges, | ||

| Prepayment Premiums | Yield maintenance charges and prepayment premiums with respect to the mortgage loans will be allocated to the certificates as described in "Description of the Certificates—Allocation of Yield Maintenance Charges and Prepayment Premiums". For an explanation of the calculation of yield maintenance charges, see "Description of the Mortgage Pool—Certain Terms of the Mortgage Loans". Yield maintenance charges received in respect of the trust subordinate companion loan will be distributed to the [LOAN-SPECIFIC CLASS] certificates pursuant to the related intercreditor agreement, and will not be allocated to the other classes of certificates. | |

| D. Subordination, Allocation of | ||