UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-07527 |

|

Turner Funds |

(Exact name of registrant as specified in charter) |

|

|

|

1205 Westlakes Drive, Suite 100

Berwyn, PA | | 19312 |

(Address of principal executive offices) | | (Zip code) |

|

Michael P. Malloy

Drinker Biddle & Reath LLP

One Logan Square, Suite 2000

Philadelphia, PA 19103 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 1-800-224-6312 | |

|

Date of fiscal year end: | September 30, 2010 | |

|

Date of reporting period: | September 30, 2010 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

Annual Report

September 30, 2010

Long/short equity fund

Turner Spectrum Fund

U.S. growth equity funds

Turner Concentrated Growth Fund

Turner Core Growth Fund

Turner Emerging Growth Fund

Turner Large Cap Growth Fund

Turner Midcap Growth Fund

Turner New Enterprise Fund

Turner Small Cap Growth Fund

Quantitative equity funds

Turner Quantitative Broad Market Equity Fund

Turner Quantitative Large Cap Value Fund

Global and international equity funds

Turner Global Opportunities Fund

Turner International Core Growth Fund

Core equity fund

Turner Small Cap Equity Fund

Contents

| | 2 | | | Letter to shareholders | |

|

| | 6 | | | Total returns of Turner Funds | |

|

| | 9 | | | Investment review:

Turner Spectrum Fund | |

|

| | 10 | | | Investment review:

Turner Concentrated Growth Fund | |

|

| | 11 | | | Investment review:

Turner Core Growth Fund | |

|

| | 12 | | | Investment review:

Turner Emerging Growth Fund | |

|

| | 13 | | | Investment review:

Turner Large Cap Growth Fund | |

|

| | 14 | | | Investment review:

Turner Midcap Growth Fund | |

|

| | 15 | | | Investment review:

Turner New Enterprise Fund | |

|

| | 16 | | | Investment review:

Turner Small Cap Growth Fund | |

|

| | 17 | | | Investment review:

Turner Quantitative Broad Market Equity Fund | |

|

| | 18 | | | Investment review:

Turner Quantitative Large Cap Value Fund | |

|

| | 19 | | | Investment review:

Turner Global Opportunities Fund | |

|

| | 20 | | | Investment review:

Turner International Core Growth Fund | |

|

| | 21 | | | Investment review:

Turner Small Cap Equity Fund | |

|

| | 22 | | | Schedules of investments | |

|

| | 54 | | | Financial statements | |

|

| | 74 | | | Notes to financial statements | |

|

| | 83 | | | Report of independent registered public accounting firm | |

|

| | 84 | | | Notice to shareholders | |

|

| | 85 | | | Trustees and officers of the Trust | |

|

| | 86 | | | Disclosure of fund expenses | |

|

Turner Funds

As of September 30, 2010, the Turner Funds offered a series of 13 mutual funds to individual and institutional investors. The minimum initial investment for Institutional Class Shares in a Turner Fund is $250,000 (except for $25,000 for the Turner Quantitative Large Cap Value Fund and $100,000 for the Turner Spectrum Fund) for regular accounts and $100,000 (with the exception of $10,000 for the Turner Quantitative Large Cap Value Fund) for individual retirement accounts. The minimum initial investment for Investor Class Shares, Retirement Class Shares, and Class C Shares of the Turner Spectrum Fund is $2,500 for regular accounts and $2,000 for individual retirement accounts.

Turner Investment Partners, Inc., based in Berwyn, Pennsylvania, serves as the investment adviser for the Funds (other than the Turner Small Cap Equity Fund). Turner Investment Management LLC, a subsidiary of Turner Investment Partners, Inc., serves as the investment adviser for the Turner Small Cap Equity Fund. Turner Investment Partners, Inc., founded in 1990, manages more than $17 billion in stock investments as of September 30, 2010.

Shareholder services

Turner Funds shareholders receive annual and semiannual reports, quarterly account statements, and a quarterly newsletter. Shareholders who have questions about their accounts may call a toll-free telephone number, 1.800.224.6312, may visit our Web site, www.turnerinvestments.com, or may write to Turner Funds, P.O. Box 219805, Kansas City, Missouri 64121-9805.

TURNER FUNDS 2010 ANNUAL REPORT 1

LETTER TO SHAREHOLDERS

To our shareholders

On balance, the stock market in the 21st century has been as underwhelming as our hometown Philadelphia Phillies in the recent National League baseball championship playoffs. In the dreary decade from 2000 to 2009 that we refer to as the Terrible 2000s, the S&P 500 Index uncharacteristically lost 0.95% annualized — an underperformance even worse than the 1930s of the Great Depression. As a result of the Terrible 2000s, the long-term average for stocks since 1926 has eroded to 9.66%, according to Ibbotson Associates. Previously the long-term average had been above 10%.

But as has often been observed, the stock market is what it is. And what the stock market is now, in our judgment, is rebounding from the Terrible 2000s. The bull market that began in March 2009 has started to push stock returns higher, to levels approximating the long-term average. Indeed, in the 12-month period ended September 30, 2010, that's the focus of this report, the S&P 500 generated a 10.16% gain.

During most of the period, macroeconomic events like central-bank actions trumped fundamentals like earnings. The market was especially roiled in the second half of the period by macroeconomic developments such as these: the sovereign-debt crisis in Europe, escalating government-budget deficits in the developed nations, China's slowing economy, the breathless reactions to the Federal Reserve's pronouncements on interest rates, and the possibility of a double-digit recession in the U.S., as reflected in persistently high unemployment, a weak housing market, lackluster consumer spending, and the bad loans still weighing heavily on banks' balance sheets.

Correlations uncommonly high

For us as investment managers, the most significant thing about a market propelled by macroeconomic forces was that stocks — whether of low or high quality, whether with weak or strong earnings — tended to move in lock step. For instance, in mid-August, the correlation of stocks in the S&P 500 Index reached 74%, compared with a correlation of just 27% between 2000 and 2006, according to Barclays Capital. Such unusually high correlations made it difficult for most investment managers to distinguish themselves by picking winning stocks. Morningstar, the mutual-fund research firm, reported in September that only about 24% of large-cap growth funds had beaten the Russell 1000 Growth Index over the past 12 months.

Our own 13 stock funds — be they large-cap, mid-cap, or small-cap funds — fared only slightly better. In the most recent 12-month period, four funds, representing about 31% of the Turner Funds lineup, beat one or more of their benchmarks. The four funds that managed to outperform were the Turner Global Opportunities Fund, the Turner International Core Growth Fund, the Turner New Enterprise Fund, and the Turner Small Cap Growth Fund. They were among the eight funds that delivered double-digit total returns.

| Total returns | | | | | |

| 12-month period ended September 30, 2010 | | | | | |

| Long/short equity fund | | | | | |

Turner Spectrum Fund,

Institutional Class (TSPEX) | | | 0.77 | % | |

| S&P 500 Index | | | 10.16 | | |

| Barclays Capital U.S. Aggregate Bond Index | | | 8.16 | | |

| Lipper Long/Short Equity Funds Classification | | | 3.55 | | |

| U.S. growth equity funds | | | | | |

| Turner Concentrated Growth Fund (TTOPX) | | | 7.94 | | |

| Russell 1000 Growth Index | | | 12.65 | | |

Turner Core Growth Fund,

Institutional Class (TTMEX) | | | 6.76 | | |

| Russell 1000 Growth Index | | | 12.65 | | |

Turner Emerging Growth Fund,

Investor Class (TMCGX) | | | 12.22 | | |

| Russell 2000 Growth Index | | | 14.79 | | |

Turner Large Cap Growth Fund,

Institutional Class (TSGEX) | | | 10.00 | | |

| Russell Top 200 Growth Index | | | 10.57 | | |

| Russell 1000 Growth Index | | | 12.65 | | |

Turner Midcap Growth Fund,

Investor Class (TMGFX) | | | 14.21 | | |

| Russell Midcap Growth Index | | | 18.27 | | |

| Turner New Enterprise Fund (TBTBX) | | | 18.25 | | |

| NASDAQ Composite Index | | | 12.77 | | |

| Turner Small Cap Growth Fund (TSCEX) | | | 15.10 | | |

| Russell 2000 Growth Index | | | 14.79 | | |

| Quantitative equity funds | | | | | |

Turner Quantitative Broad Market

Equity Fund, Institutional Class (TBMEX) | | | 8.30 | | |

| Russell 3000 Index | | | 10.96 | | |

| S&P 500 Index | | | 10.16 | | |

Turner Quantitative Large Cap

Value Fund, Institutional Class (TLVFX) | | | 7.24 | | |

| Russell 1000 Value Index | | | 8.90 | | |

| Global and international equity funds | | | | | |

Turner Global Opportunities Fund,

Institutional Class (TGLBX) | | | 15.20 | † | |

| MSCI World Growth Index | | | 9.53 | † | |

| MSCI World Index | | | 8.14 | † | |

Turner International Core Growth

Fund, Institutional Class (TICGX) | | | 15.88 | | |

| MSCI World Growth ex-U.S. Index | | | 8.69 | | |

| Core equity fund | | | | | |

Turner Small Cap Equity Fund,

Investor Class (TSEIX) | | | 12.53 | | |

| Russell 2000 Index | | | 13.35 | | |

† Returns are from the fund's inception date, May 7, 2010.

2 TURNER FUNDS 2010 ANNUAL REPORT

September 30, 2010

(Please call 1.800.224.6312 or visit our Web site at www.turnerinvestments.com for the most recent month-end performance. For more details on the performance of each fund during the 12-month period, see the Investment review beginning on page 9.)

A tough market to beat

Clearly, it was a tough stock market to beat. It was a market that largely neutralized our growth, core, quantitative, and alternative investment processes, which are geared to fundamentals such as earnings expectations, market-share positions, investment metrics that have proven predictive of outperformance, and balance-sheet strength. We felt a keen sense of frustration about investing in a market in which stock selection was generally of little consequence. We continued to follow the same investment processes as before. But, alas, sometimes even the best investment processes don't generate extra return across the board, and this was one of these times.

We are steadfast in our belief that if we continue to follow our proven investment processes, they will continue to yield good long-term results for our funds. Nine of our 13 funds have outperformed since their inception. We consider that a highly respectable long-term record, but that's not to say we can't do better. As perennial students of the market, we are always learning and open to promising new ideas from any source. And as investment professionals, we are self-critical and intent on improving continuously.

For instance, in our best open and self-critical manner, we recently added four new analysts to our Growth Investing Team. With their combined 65 years of investment experience, they should provide extra depth to our research of sectors, industries, and companies. Altogether, our Growth Investing Team has five teams of 25 portfolio managers/security analysts who cover industries in the five broad market sectors globally. Such a sector orientation is a distinguishing aspect of how we manage our growth funds. By enabling our analysts to conduct vigorous fundamental research in their specific industries, we think their focus, accountability for investment results, and ability to identify the best growth stocks should all improve.

Providing more flexibility

Another example: we modified our sector-neutral approach that we use in managing certain of our growth funds, refining it into what we call a sector-aware approach. We believe this will give us a bit more flexibility in portfolio management and give our growth funds a bit more potential to generate extra return.

With sector neutrality, we were compelled to keep the sector weightings of our holdings equal to the sector weightings of their target indexes. For instance, if the Russell Midcap Growth Index had a 27% weighting in the technology sector, then our Turner Midcap Growth Fund would follow suit and hold a 27% weighting in the technology sector. In contrast, our new sector-aware approach still keeps us invested in all sectors, but it enables us to overweight or underweight sectors typically by up to five percentage points, when our analysis indicates it's warranted by the fundamentals. Also, it permits us to replace a poor-performing stock in one sector with a stock that we consider to have better return potential in another sector, which we wouldn't do before.

We think these are good illustrations of how we are continually fine-tuning our investment processes in the interest of producing better results for you, our shareholders — and for us, I hasten to add, since our portfolio managers and other employees are shareholders in our funds as well.

Stocks out of favor

We believe it's rather unfortunate that more than a few mutual-fund investors outside the Turner Funds find themselves unable to reap any results in stocks at this juncture — for the simple reason that their portfolios are completely divested of stocks. Bonds, not stocks, are the investment du jour by far. According to the Investment Company Institute, since January 2009 bond funds have attracted more than $500 billion in new investment, while stock funds have suffered more than $70 billion in withdrawals. Investors' aversion to stocks is perhaps attributable to this facet of human nature: the pain of investment losses tends to be more acute than the pleasure of investment gains, and many pain-stricken investors are still wincing from the losses inflicted by stocks in the Ter rible 2000s. We believe such an aversion could prove costly because, in our estimation, the 2010s should be a decade of generally rising stock prices.

We think better days are ahead for stocks partly because the Terrible 2000s were so terrible, with stocks underperforming the long-term averages by more than 10 percentage points annualized. Like Lady Gaga's meat dress, a losing decade for stocks isn't at all commonplace. In light of a fundamental principle of economics called reversion to the mean — the tendency for investment returns to adjust, or revert, to the long-term average, given enough time — we think the probabilities are that stocks, in light of their highly unusual negative showing in the 2000s, should revert and perform at least reasonably well in the 2010s. According to Morningstar, of the 776 rolling 10-year monthly returns since 1926, only 29 of those returns were negative — less than 4% of the tota l. But subsequent 10-year returns after those negative 10-year stretches were soundly positive, averaging 9.8%.

In the near term, we think the bull market should continue to advance, especially if investors focus more on

TURNER FUNDS 2010 ANNUAL REPORT 3

LETTER TO SHAREHOLDERS (continued)

favorable earnings fundamentals and less on macroeconomic issues. For example, more than two-thirds of the S&P 500 companies' earnings have beaten Wall Street analysts' expectations for six consecutive quarters — a trend that we expect to remain intact into 2011. To cite investing guru Benjamin Graham's famous metaphor, the market is a weighing machine in the long run . . . and earnings are what ultimately register on the machine.

Also, we think stocks offer compelling valuations. Recently the earnings yield (the inverted price/earnings ratio) of the S&P 500 Index stocks exceeded the average yield of corporate bonds for the first time since the 1970s. Indeed, the earnings yield looks even more appealing in relation to the yield of the entire bond market. As of September 30, the S&P 500's earnings yield was 5.76%, more than double the 2.56% yield of the Barclays Capital U.S. Aggregate Bond Index, a common proxy for the bond market.

Emerging markets promising

We are also optimistic about the near-term return potential of the emerging stock markets, which could in particular help the performance of the Turner International Core Growth Fund and our newest fund, the Turner Global Opportunities Fund. One reason why we think the emerging stock markets represent a compelling investment opportunity is this projection by Bank of America Merrill Lynch: the governments of emerging nations may pour $6.3 trillion into expanding their nations' often-rudimentary infrastructure over the next three years. Also, we think the economies of emerging countries like China, India, Brazil, and Malaysia have the best prospects for years to come — a revved-up engine of economic growth that should help drive earnings and emerging stock markets higher.

In anticipation of generally favorable stock-market prospects worldwide, we have kept our funds positioned basically the same as when I last wrote to you in our Semiannual Report six months ago:

• Our nine U.S. and international/global growth funds hold three types of shares: classic growth stocks in industries such as biotechnology and wireless communications that we think have strong fundamentals, stocks of companies gaining market share in their businesses, and growth-cyclical stocks in industries such as chemicals that have tended to do well historically as the economic cycle progresses.

• Our core fund, the Turner Small Cap Equity Fund, follows an investment approach emphasizing companies with business momentum, cash-rich balance sheets, or undervalued assets.

• Our two quantitative funds, the Turner Quantitative Broad Market Equity Fund and the Turner Quantitative Large Cap Value Fund, are broadly diversified in stocks in each market sector that our proprietary quantitative model has identified as having the best statistical chance of outperforming the market.

• The Turner Spectrum Fund, composed of seven long/short strategies managed by us, is invested in long positions that we think have good return potential and in short positions that we think have below-average return potential.

In closing, we believe patient, long-term investing in stocks is likely to be rewarded more generously in this decade than in the Terrible 2000s. And we believe our funds are primed to share fully in those rewards, to our mutual benefit as shareholders.

Bob Turner

Chairman and Chief Investment Officer

Turner Investments

Past performance is no guarantee of future results. The views expressed are those of Turner Investments as of September 30, 2010, and are not intended as a forecast or investment recommendations. The indexes mentioned are not available for investment.

Bob Turner

4 TURNER FUNDS 2010 ANNUAL REPORT

September 30, 2010

Lipper Inc. peer group performance rankings of mutual funds with at least three years of history

Periods ending September 30, 2010

| | | One

year | | Two

years | | Three

years | | Four

years | | Five

years | | Seven

years | | Ten

years | |

| International Multi-Cap Growth Funds | |

Turner International Core Growth Fund

Institutional Class Shares | |

| Ranking versus Lipper peers | | | 32/158 | | | | 57/132 | | | | 38/108 | | | | — | | | | — | | | | — | | | | — | | |

| Percentile Ranking | | | 20 | | | | 43 | | | | 35 | | | | — | | | | — | | | | — | | | | — | | |

| Large-Cap Growth Funds | |

Turner Core Growth Fund,

Institutional Class Shares | |

| Ranking versus Lipper peers | | | 735/852 | | | | 584/792 | | | | 653/732 | | | | 567/679 | | | | 464/614 | | | | 176/513 | | | | — | | |

| Percentile ranking | | | 86 | | | | 74 | | | | 89 | | | | 84 | | | | 76 | | | | 34 | | | | — | | |

| Investor Class Shares | |

| Ranking versus Lipper peers | | | 743/852 | | | | 597/792 | | | | 660/732 | | | | 590/679 | | | | 503/614 | | | | — | | | | — | | |

| Percentile Ranking | | | 87 | | | | 75 | | | | 90 | | | | 87 | | | | 82 | | | | — | | | | — | | |

Turner Large Cap Growth Fund,

Institutional Class Shares | |

| Ranking versus Lipper peers | | | 430/852 | | | | 386/792 | | | | 691/732 | | | | 635/679 | | | | 574/614 | | | | 497/513 | | | | 323/344 | | |

| Percentile ranking | | | 50 | | | | 49 | | | | 94 | | | | 94 | | | | 93 | | | | 97 | | | | 94 | | |

| Investor Class Shares | |

| Ranking versus Lipper peers | | | 475/852 | | | | 426/792 | | | | 698/732 | | | | — | | | | — | | | | — | | | | — | | |

| Percentile ranking | | | 56 | | | | 54 | | | | 95 | | | | — | | | | — | | | | — | | | | — | | |

| Multi-Cap Core Funds | |

Turner Quantitative Large

Cap Value Fund

Institutional Class Shares | |

| Ranking versus Lipper peers | | | 691/846 | | | | 764/790 | | | | 632/736 | | | | 589/665 | | | | — | | | | — | | | | — | | |

| Percentile ranking | | | 82 | | | | 97 | | | | 86 | | | | 89 | | | | — | | | | — | | | | — | | |

| Multi-Cap Growth Funds | |

| Turner Concentrated Growth Fund | |

| Ranking versus Lipper peers | | | 364/437 | | | | 289/412 | | | | 368/375 | | | | 292/330 | | | | 256/298 | | | | 259/270 | | | | 201/203 | | |

| Percentile ranking | | | 83 | | | | 70 | | | | 98 | | | | 88 | | | | 86 | | | | 96 | | | | 99 | | |

Turner Midcap Growth Fund,

Investor Class Shares | |

| Ranking versus Lipper peers | | | 170/437 | | | | 162/412 | | | | 199/375 | | | | 124/330 | | | | 125/298 | | | | 95/270 | | | | 146/203 | | |

| Percentile ranking | | | 39 | | | | 39 | | | | 53 | | | | 38 | | | | 42 | | | | 35 | | | | 72 | | |

| Retirement Class Shares | |

| Ranking versus Lipper peers | | | 182/437 | | | | 167/412 | | | | 210/375 | | | | 144/330 | | | | 142/298 | | | | 122/270 | | | | — | | |

| Percentile ranking | | | 42 | | | | 41 | | | | 56 | | | | 44 | | | | 48 | | | | 45 | | | | — | | |

| Science and Technology Funds | |

| Turner New Enterprise Fund | |

| Ranking versus Lipper peers | | | 43/141 | | | | 62/136 | | | | 107/135 | | | | 66/128 | | | | 62/120 | | | | 39/109 | | | | 27/81 | | |

| Percentile Ranking | | | 30 | | | | 46 | | | | 79 | | | | 52 | | | | 52 | | | | 36 | | | | 33 | | |

| Small-Cap Growth Funds | |

Turner Emerging Growth Fund

Investor Class Shares | |

| Ranking versus Lipper peers | | | 369/530 | | | | 472/495 | | | | 324/467 | | | | 257/426 | | | | 232/396 | | | | 50/331 | | | | 13/223 | | |

| Percentile ranking | | | 70 | | | | 95 | | | | 69 | | | | 60 | | | | 59 | | | | 15 | | | | 6 | | |

| Turner Small Cap Growth Fund | |

| Ranking versus Lipper peers | | | 242/530 | | | | 246/495 | | | | 165/467 | | | | 115/426 | | | | 99/396 | | | | 110/331 | | | | 152/223 | | |

| Percentile ranking | | | 46 | | | | 50 | | | | 35 | | | | 27 | | | | 25 | | | | 33 | | | | 68 | | |

| Small-Cap Core Funds | |

Turner Small Cap Equity Fund

Investor Class Shares | |

| Ranking versus Lipper peers | | | 466/755 | | | | 624/717 | | | | 583/661 | | | | 528/594 | | | | 491/544 | | | | 394/434 | | | | — | | |

| Percentile ranking | | | 62 | | | | 87 | | | | 88 | | | | 89 | | | | 90 | | | | 91 | | | | — | | |

Source: Lipper Inc.

Total return is ranking criteria. Past performance is no guarantee of future results.

TURNER FUNDS 2010 ANNUAL REPORT 5

PERFORMANCE

Total returns of the Turner Funds

Through September 30, 2010

Current performance may be lower or higher than the performance data quoted. Please call 1.800.224.6312 or visit our website at www.turnerinvestments.com for the most recent month-end performance information.

The performance data quoted represents past performance and the principal value and investment return will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Past performance is no guarantee of future results. Returns shown, unless otherwise indicated, are total returns, with dividends and income reinvested. Returns spanning more than one year are annualized. Fee waivers are in effect; if they had not been in effect, performance would have been lower. The indices mentioned are unmanaged statistical composites of stock-market performance. Investing in an index is not possible.

The holdings and sector weightings of the Funds are subject to change. Forward-earnings projections are not predictors of stock price or investment performance, and do not represent past performance. There is no guarantee that the forward-earnings projections will accurately predict the actual earnings experience of any of the companies involved, and there is no guarantee that owning securities of companies with relatively high price-to-earnings ratios will cause the portfolio to outperform its benchmark or index.

The Turner Funds are distributed by Foreside Fund Services, LLC, Portland, Maine. The investor should consider the investment objectives, risks, charges, and expenses carefully before investing. This and other information can be found in the prospectus. A free prospectus, which contains detailed information, including fees and expenses, and the risks associated with investing in these Funds, can be obtained by calling 1.800.224.6312. Read the prospectus carefully before investing.

| Fund name/index | | Six

months | | Year

to

date | | One

year | | Three

years | | Five

years | | Ten

years | | (Annualized)

Since

inception | | Total

net assets

($mill) | |

Turner Spectrum Fund —

Institutional Class Shares | | | -2.17 | % | | | -0.73 | % | | | 0.77 | % | | | n/a | | | | n/a | | | | n/a | | | | 6.31 | % | | $ | 179.53 | | |

| Investor Class Shares | | | -2.27 | | | | -0.92 | | | | 0.49 | | | | n/a | | | | n/a | | | | n/a | | | | 6.03 | | | | 52.36 | | |

| Class C Shares(1) | | | -2.63 | | | | -1.38 | | | | -0.07 | | | | n/a | | | | n/a | | | | n/a | | | | 6.67 | | | | 7.17 | | |

| S&P 500 Index | | | -1.42 | | | | 3.89 | | | | 10.16 | | | | n/a | | | | n/a | | | | n/a | | | | 20.30 | | | | | | |

Barclays Capital U.S. Aggregate

Bond Index | | | 6.05 | | | | 7.94 | | | | 8.16 | | | | n/a | | | | n/a | | | | n/a | | | | 9.55 | | | | | | |

Lipper Long/Short Equity

Funds Classification | | | -1.73 | | | | 0.29 | | | | 3.55 | | | | n/a | | | | n/a | | | | n/a | | | | 12.01 | | | | | | |

| Inception date: 5/7/09 | |

Turner Concentrated

Growth Fund | | | 0.45 | | | | 2.31 | | | | 7.94 | | | | -13.07 | % | | | -1.30 | % | | | -10.18 | % | | | -0.46 | | | | 42.92 | | |

| Russell 1000 Growth Index | | | -0.27 | | | | 4.36 | | | | 12.65 | | | | -4.36 | | | | 2.06 | | | | -3.44 | | | | -1.56 | | | | | | |

| Inception date: 6/30/99 | |

Turner Core Growth Fund —

Institutional Class Shares | | | -3.39 | | | | 0.38 | | | | 6.76 | | | | -9.43 | | | | -0.30 | | | | n/a | | | | 0.77 | | | | 377.65 | | |

| Investor Class Shares(2) | | | -3.50 | | | | 0.10 | | | | 6.51 | | | | -9.67 | | | | -0.59 | | | | n/a | | | | 0.06 | | | | 163.75 | | |

| Russell 1000 Growth Index | | | -0.27 | | | | 4.36 | | | | 12.65 | | | | -4.36 | | | | 2.06 | | | | n/a | | | | 0.10 | | | | | | |

| Inception date: 2/28/01 | |

Turner Emerging Growth Fund(8) —

Institutional Class Shares(3) | | | -1.41 | | | | 8.00 | | | | 12.52 | | | | n/a | | | | n/a | | | | n/a | | | | 27.20 | | | | 276.45 | | |

| Investor Class Shares | | | -1.56 | | | | 7.79 | | | | 12.22 | | | | -7.36 | | | | 0.86 | | | | 5.43 | | | | 18.19 | | | | 176.82 | | |

| Russell 2000 Growth Index | | | 2.43 | | | | 10.23 | | | | 14.79 | | | | -3.75 | | | | 2.35 | | | | -0.13 | | | | 2.07 | | | | | | |

| Inception date: 2/27/98 | |

Turner Large Cap Growth Fund —

Institutional Class Shares | | | -1.22 | | | | 3.86 | | | | 10.00 | | | | -10.37 | | | | -1.93 | | | | -6.68 | | | | -6.66 | | | | 118.16 | | |

| Investor Class Shares(4) | | | -1.43 | | | | 3.66 | | | | 9.58 | | | | -10.66 | | | | n/a | | | | n/a | | | | -5.41 | | | | 1.36 | | |

| Russell Top 200 Growth Index | | | -1.49 | | | | 2.00 | | | | 10.57 | | | | -4.49 | | | | 1.81 | | | | -4.20 | | | | -4.51 | | | | | | |

| Russell 1000 Growth Index | | | -0.27 | | | | 4.36 | | | | 12.65 | | | | -4.36 | | | | 2.06 | | | | -3.44 | | | | -3.64 | | | | | | |

| Inception date: 6/14/00 | |

6 TURNER FUNDS 2010 ANNUAL REPORT

PERFORMANCE (continued)

| Fund name/index | | Six

months | | Year

to

date | | One

year | | Three

years | | Five

years | | Ten

years | | (Annualized)

Since

inception | | Total

net assets

($mill) | |

Turner Midcap Growth Fund(8) —

Institutional Class Shares(5) | | | -0.10 | % | | | 7.44 | % | | | 14.47 | % | | | n/a | | | | n/a | | | | n/a | | | | -6.26 | % | | $ | 164.99 | | |

| Investor Class Shares | | | -0.20 | | | | 7.25 | | | | 14.21 | | | | -5.93 | % | | | 2.41 | % | | | -3.50 | % | | | 9.81 | | | | 751.12 | | |

| Retirement Class Shares(6) | | | -0.31 | | | | 7.05 | | | | 13.93 | | | | -6.16 | | | | 2.09 | | | | n/a | | | | 5.78 | | | | 4.58 | | |

| Russell Midcap Growth Index | | | 2.95 | | | | 10.85 | | | | 18.27 | | | | -3.90 | | | | 2.86 | | | | -0.88 | | | | 6.38 | | | | | | |

| Inception date: 10/1/96 | |

| Turner New Enterprise Fund(8) | | | 2.48 | | | | 11.41 | | | | 18.25 | | | | -6.90 | | | | 3.73 | | | | -5.60 | | | | -3.37 | | | | 23.23 | | |

| NASDAQ Composite Index | | | -0.69 | | | | 5.17 | | | | 12.77 | | | | -3.27 | | | | 2.92 | | | | -3.52 | | | | -4.15 | | | | | | |

| Inception date: 6/30/00 | |

| Turner Small Cap Growth Fund(8) | | | 1.58 | | | | 10.19 | | | | 15.10 | | | | -4.23 | | | | 3.26 | | | | -0.73 | | | | 10.78 | | | | 274.92 | | |

| Russell 2000 Growth Index | | | 2.43 | | | | 10.23 | | | | 14.79 | | | | -3.75 | | | | 2.35 | | | | -0.13 | | | | 4.91 | | | | | | |

| Inception date: 2/7/94 | |

Turner Quantitative Broad

Market Equity Fund — | |

| Institutional Class Shares | | | -4.09 | | | | 2.18 | | | | 8.30 | | | | n/a | | | | n/a | | | | n/a | | | | -4.19 | | | | 10.95 | | |

| Investor Class Shares | | | -4.31 | | | | 2.07 | | | | 7.98 | | | | n/a | | | | n/a | | | | n/a | | | | -4.43 | | | | 0.02 | | |

| Russell 3000 Index | | | -1.10 | | | | 4.78 | | | | 10.96 | | | | n/a | | | | n/a | | | | n/a | | | | -2.35 | | | | | | |

| S&P 500 Index | | | -1.42 | | | | 3.89 | | | | 10.16 | | | | n/a | | | | n/a | | | | n/a | | | | -2.72 | | | | | | |

| Inception date: 6/30/08 | |

Turner Quantitative

Large Cap Value Fund — | |

| Institutional Class Shares | | | -3.20 | | | | 3.01 | | | | 7.24 | | | | -9.48 | | | | n/a | | | | n/a | | | | -0.24 | | | | 0.83 | | |

| Investor Class Shares(7) | | | -3.33 | | | | 2.88 | | | | 7.07 | | | | n/a | | | | n/a | | | | n/a | | | | 4.53 | | | | — | | |

| Russell 1000 Value Index | | | -2.14 | | | | 4.49 | | | | 8.90 | | | | -9.39 | | | | n/a | | | | n/a | | | | 0.30 | | | | | | |

| Inception date: 10/10/05 | |

Turner Global Opportunities Fund —

Institutional Class Shares | | | n/a | | | | n/a | | | | n/a | | | | n/a | | | | n/a | | | | n/a | | | | 15.20 | * | | | 1.15 | | |

| Investor Class Shares | | | n/a | | | | n/a | | | | n/a | | | | n/a | | | | n/a | | | | n/a | | | | 15.00 | * | | | — | | |

| MSCI World Growth Index | | | n/a | | | | n/a | | | | n/a | | | | n/a | | | | n/a | | | | n/a | | | | 9.53 | * | | | | | |

| MSCI World Index | | | n/a | | | | n/a | | | | n/a | | | | n/a | | | | n/a | | | | n/a | | | | 8.14 | * | | | | | |

| Inception date: 5/7/10 | |

Turner International Core

Growth Fund —

Institutional Class Shares | | | 4.44 | | | | 7.91 | | | | 15.88 | | | | -6.98 | | | | n/a | | | | n/a | | | | -0.47 | | | | 5.02 | | |

| Investor Class Shares(7) | | | 4.33 | | | | 7.68 | | | | 15.61 | | | | n/a | | | | n/a | | | | n/a | | | | 25.63 | | | | 0.11 | | |

| MSCI World Growth ex-U.S. Index | | | 2.25 | | | | 4.21 | | | | 8.69 | | | | -8.02 | | | | n/a | | | | n/a | | | | -2.51 | | | | | | |

| Inception date: 1/31/07 | |

Turner Small Cap Equity Fund(8) —

Institutional Class Shares(3) | | | 1.84 | | | | 5.52 | | | | 12.82 | | | | n/a | | | | n/a | | | | n/a | | | | 24.14 | | | | 0.29 | | |

| Investor Class Shares | | | 1.66 | | | | 5.34 | | | | 12.53 | | | | -8.53 | | | | -2.34 | | | | n/a | | | | 5.41 | | | | 6.16 | | |

| Russell 2000 Index | | | 0.25 | | | | 9.12 | | | | 13.35 | | | | -4.29 | | | | 1.60 | | | | n/a | | | | 5.24 | | | | | | |

| Inception date: 3/4/02 | |

(1) Commenced operations on July 14, 2009.

(2) Commenced operations on August 1, 2005.

(3) Commenced operations on February 1, 2009.

(4) Commenced operations on January 31, 2007.

(5) Commenced operations on June 16, 2008.

(6) Commenced operations on September 24, 2001.

(7) Commenced operations on October 31, 2008.

(8) Investing in technology and science companies and small- and mid-capitalization companies may subject the Funds to specific inherent risks, including above-average price fluctuations.

* Returns of less than one year are cumulative, and not annualized.

Amounts designated as "—" have been rounded to $0 ($mil).

TURNER FUNDS 2010 ANNUAL REPORT 7

Expense Ratio†

| | | Gross

expense

ratio | | Net

expense

ratio | |

| Turner Spectrum Fund | |

| Institutional Class Shares | | | 2.50 | % | | | 1.95 | % | |

| Investor Class Shares | | | 2.75 | % | | | 2.20 | % | |

| Class C Shares | | | 3.50 | % | | | 2.95 | % | |

Turner Concentrated

Growth Fund | |

| Investor Class Shares | | | 1.34 | % | | | 0.82 | % | |

| Turner Core Growth Fund | |

| Institutional Class Shares | | | 0.92 | % | | | 0.69 | % | |

| Investor Class Shares | | | 1.17 | % | | | 0.94 | % | |

| Turner Emerging Growth Fund | |

| Institutional Class Shares | | | 1.35 | % | | | 1.17 | % | |

| Investor Class Shares | | | 1.58 | % | | | 1.42 | % | |

| Turner Large Cap Growth Fund | |

| Institutional Class Shares | | | 1.21 | % | | | 0.69 | % | |

| Investor Class Shares | | | 1.47 | % | | | 0.94 | % | |

| Turner Midcap Growth Fund | |

| Institutional Class Shares | | | 1.08 | % | | | 0.93 | % | |

| Investor Class Shares | | | 1.33 | % | | | 1.18 | % | |

| Retirement Class Shares | | | 1.58 | % | | | 1.43 | % | |

| Turner New Enterprise Fund | |

| Investor Class Shares | | | 1.25 | % | | | 0.64 | % | |

| | | Gross

expense

ratio | | Net

expense

ratio | |

| Turner Small Cap Growth Fund | |

| Investor Class Shares | | | 1.58 | % | | | 1.25 | % | |

Turner Quantitative Broad

Market Equity Fund | |

| Institutional Class Shares | | | 20.30 | % | | | 0.64 | % | |

| Investor Class Shares | | | 20.60 | % | | | 0.89 | % | |

Turner Quantitative Large Cap

Value Fund | |

| Institutional Class Shares | | | 14.51 | % | | | 0.69 | % | |

| Investor Class Shares | | | 15.93 | % | | | 0.94 | % | |

Turner Global

Opportunities Fund | |

| Institutional Class Shares | | | 1.96 | % | | | 1.11 | % | |

| Investor Class Shares | | | 2.21 | % | | | 1.36 | % | |

Turner International Core

Growth Fund | |

| Institutional Class Shares | | | 5.24 | % | | | 1.10 | % | |

| Investor Class Shares | | | 5.59 | % | | | 1.35 | % | |

| Turner Small Cap Equity Fund | |

| Institutional Class Shares | | | 1.60 | % | | | 1.21 | % | |

| Investor Class Shares | | | 1.90 | % | | | 1.46 | % | |

† These expense ratios are based on the most recent prospectus and may differ from those shown in the financial highlights.

8 TURNER FUNDS 2010 ANNUAL REPORT

INVESTMENT REVIEW

Turner Spectrum Fund

Fund profile

September 30, 2010

g Ticker symbol TSPEX

Institutional Class Shares

g CUSIP #900297664

Institutional Class Shares

g Top five holdings††

(1) Hospira

(2) Pfizer

(3) Citigroup

(4) IntercontinentalExchange

(5) Universal Health Services, Cl B

g % in five largest holdings 9.1%†

g Number of holdings 340††

g Price/earnings ratio 16.7

g Weighted average market capitalization $4.74 billion

g % of holdings with positive earnings surprises 66.0%

g % of holdings with negative earnings surprises 15.1%

g Net assets $180 million, Institutional Class Shares

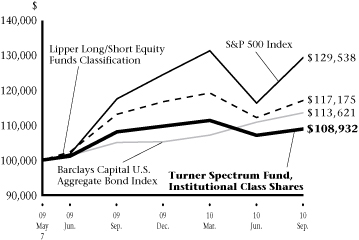

Growth of a $100,000 investment in the

Turner Spectrum Fund, Institutional Class Shares:

May 7, 2009-September 30, 2010*,**

Average annual total returns (Periods ending September 30, 2010)

| | | One

year | | Since

Inception | |

| Turner Spectrum Fund, Institutional Class Shares | | | 0.77 | % | | | 6.31 | %** | |

| Turner Spectrum Fund, Investor Class Shares | | | 0.49 | % | | | 6.03 | %** | |

| Turner Spectrum Fund, Class C Shares | | | -0.07 | % | | | 6.67 | %*** | |

| S&P 500 Index | | | 10.16 | % | | | 20.30 | %** | |

| Barclays Capital U.S. Aggregate Bond Index | | | 8.16 | % | | | 9.55 | %** | |

| Lipper Long/Short Equity Funds Classification | | | 3.55 | % | | | 12.01 | %** | |

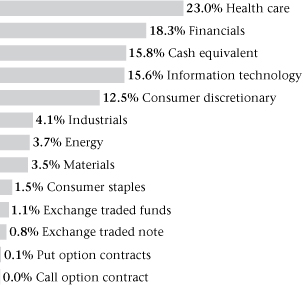

Sector weightings†:

Manager's discussion and analysis

In the 12 months ended September 30, the Turner Spectrum Fund, Institutional Class Shares (TSPEX) produced a 0.77% gain, diminished by unrewarding short positions in consumer, materials/processing, financial-services, and health-care stocks. The fund underperformed the S&P 500 Index's 10.16% gain, the Barclays Capital U.S. Aggregate Bond Index's 8.16% gain, and the Lipper Long/Short Equity Funds Classification's 3.55% gain.

The fund, which consists of seven Turner long/short strategies that seek to capitalize on both rising and falling stock prices, produced its best relative returns on the long side in the financial-services and health-care sectors. Long positions in producer-durables stocks hurt performance the most. The fund was conservatively positioned, with a net long exposure generally of less than 25%. It held broadly diversified positions in large-cap, mid-cap, and small-cap stocks, most of them traded in the U.S. In general, the smaller stocks performed best.

* These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. Performance of the Institutional, Investor and Class C Shares will differ due to differences in fees.

** The inception date of the Turner Spectrum Fund (Institutional Class Shares and Investor Class Shares) was May 7, 2009. Index returns are based on Institutional Class Shares inception date.

*** The inception date of the Turner Spectrum Fund (Class C Shares) was July 14, 2009.

† Percentages based on total investments.

†† Cash equivalents are not being considered a holding for the top five holdings, but are counted in the number of holdings.

Cl — Class

TURNER FUNDS 2010 ANNUAL REPORT 9

INVESTMENT REVIEW

Turner Concentrated Growth Fund

Fund profile

September 30, 2010

g Ticker symbol TTOPX

g CUSIP #87252R862

g Top five holdings††

(1) Apple

(2) Baidu ADR

(3) QUALCOMM

(4) Halliburton

(5) Caterpillar

g % in five largest holdings 28.2%†

g Number of holdings 23††

g Price/earnings ratio 19.4

g Weighted average market capitalization $40.42 billion

g % of holdings with positive earnings surprises 95.5%

g % of holdings with negative earnings surprises 4.6%

g Net assets $43 million

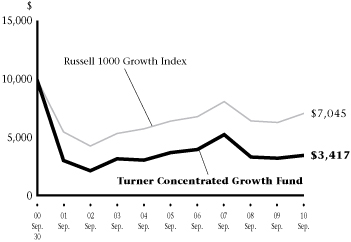

Growth of a $10,000 investment in the

Turner Concentrated Growth Fund:

September 30, 2000-September 30, 2010*

Average annual total returns (Periods ending September 30, 2010)

| | | One

year | | Three

years | | Five

years | | Ten

years | | Since

inception | |

| Turner Concentrated Growth Fund | | | 7.94 | % | | | -13.07 | % | | | -1.30 | % | | | -10.18 | % | | | -0.46 | % | |

| Russell 1000 Growth Index | | | 12.65 | % | | | -4.36 | % | | | 2.06 | % | | | -3.44 | % | | | -1.56 | % | |

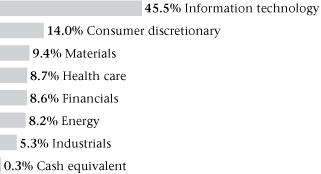

Sector weightings†:

Manager's discussion and analysis

Significant underperformance in four sectors impaired the total return of the Turner Concentrated Growth Fund (TTOPX) in the 12-month period ended September 30. As a result the fund, which contains a select few stocks that we think have the strongest expected earnings power and return potential, rose 7.94%, markedly lagging the Russell 1000 Growth Index's 12.65% gain.

Materials, financials, industrials, and health-care stocks, a 32% weighting, were the detractors from results. In those sectors, metals, mining, investment-management, insurance, semiconductor-capital-equipment, pharmaceutical, and medical-equipment shares performed poorly. Altogether, three of the fund's seven sector positions beat their corresponding index sectors. Consumer-discretionary and information-technology stocks, a 60% weighting, added the most extra return. Retailing, business-services, gaming, semiconductor, and data-networking shares were among the winning stock selections.

* These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. The inception date of the Turner Concentrated Growth Fund was June 30, 1999.

† Percentages based on total investments.

†† Cash equivalents are not being considered a holding for the top five holdings, but are counted in the number of holdings.

ADR — American Depositary Receipt

10 TURNER FUNDS 2010 ANNUAL REPORT

INVESTMENT REVIEW

Turner Core Growth Fund

Fund profile

September 30, 2010

g Ticker symbol TTMEX

Institutional Class Shares

g CUSIP #900297847

Institutional Class Shares

g Top five holdings†††

(1) Apple

(2) PepsiCo

(3) Halliburton

(4) American Express

(5) Lam Research

g % in 5 largest holdings 17.4%†

g Number of holdings 72†††

g Price/earnings ratio 18.2

g Weighted average market capitalization $44.55 billion

g % of holdings with positive earnings surprises 80.3%

g % of holdings with negative earnings surprises 16.9%

g Net assets $378 million, Institutional Class Shares

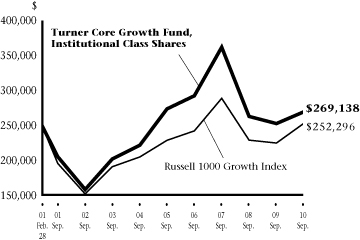

Growth of a $250,000 investment in the

Turner Core Growth Fund, Institutional Class Shares:

February 28, 2001-September 30, 2010*,**

Average annual total returns (Periods ending September 30, 2010)

| | | One

year | | Three

years | | Five

years | | Since

inception | |

| Turner Core Growth Fund, Institutional Class Shares | | | 6.76 | % | | | -9.43 | % | | | -0.30 | % | | | 0.77 | %** | |

| Turner Core Growth Fund, Investor Class Shares | | | 6.51 | % | | | -9.67 | % | | | -0.59 | % | | | 0.06 | %*** | |

| Russell 1000 Growth Index | | | 12.65 | % | | | -4.36 | % | | | 2.06 | % | | | 0.10 | %** | |

Sector weightings†:

Manager's discussion and analysis

Losses in three major sectors contributed notably to the underperformance of the Turner Core Growth Fund, Institutional Class (TTMEX) in the 12-month period ended September 30. Stocks in the energy, financials, and industrials sectors accounted for 32% of the fund's holdings, and their losses, especially in energy-services, investment-management, insurance, metals, and mining shares, hurt results in those sectors. That depressed the overall return of the fund, which was up 6.76% and trailed the Russell 1000 Growth Index's 12.65% return.

Two of the fund's 10 sector positions outperformed their corresponding index sectors; the contributors to results were the information-technology and utilities sectors, a 26% weighting. Semiconductor, data-networking, wireless-communications, and telecommunications holdings produced good relative returns.

* These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. On February 25, 2005, the Constellation TIP Core Growth Fund reorganized into the Turner Core Growth Fund. Performance of the Institutional and Investor Class Shares will differ due to differences in fees.

** The inception date of the Turner Core Growth Fund (Institutional Class Shares) was February 28, 2001. Index returns are based on Institutional Class Shares inception date.

*** The inception date of the Turner Core Growth Fund (Investor Class Shares) was August 1, 2005.

† Percentages based on total investments.

†† Cash equivalents include short-term investments held as collateral for securities lending activity. Please see Note 11 in Notes to Financial Statements for more detailed information.

††† Cash equivalents and short-term investments are not being considered a holding for the top five holdings, but are counted in the number of holdings.

TURNER FUNDS 2010 ANNUAL REPORT 11

INVESTMENT REVIEW

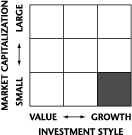

Turner Emerging Growth Fund

Fund profile

September 30, 2010

g Ticker symbol TMCGX

Investor Class Shares

g CUSIP #872524301

Investor Class Shares

g Top five holdings†††

(1) Deckers Outdoor

(2) Bucyrus International, Cl A

(3) American Physicians Capital

(4) Alexion Pharmaceuticals

(5) Orthofix International

g % in 5 largest holdings 11.3%†

g Number of holdings 113†††

g Price/earnings ratio 16.9

g Weighted average market capitalization $1.60 billion

g % of holdings with positive earnings surprises 68.8%

g % of holdings with negative earnings surprises 23.2%

g Net assets $177 million, Investor Class Shares

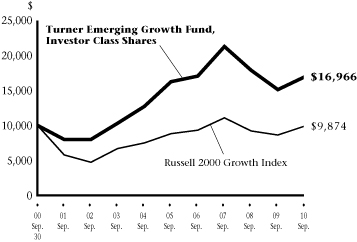

Growth of a $10,000 investment in the

Turner Emerging Growth Fund,

Investor Class Shares:

September 30, 2000-September 30, 2010*,***

Average annual total returns (Periods ending September 30, 2010)

| | | One

year | | Three

years | | Five

years | | Ten

years | | Since

inception | |

| Turner Emerging Growth Fund, Institutional Class Shares | | | 12.52 | % | | | — | | | | — | | | | — | | | | 27.20 | %** | |

| Turner Emerging Growth Fund, Investor Class Shares | | | 12.22 | % | | | -7.36 | % | | | 0.86 | % | | | 5.43 | % | | | 18.19 | %*** | |

| Russell 2000 Growth Index | | | 14.79 | % | | | -3.75 | % | | | 2.35 | % | | | -0.13 | % | | | 2.07 | %*** | |

Sector weightings†:

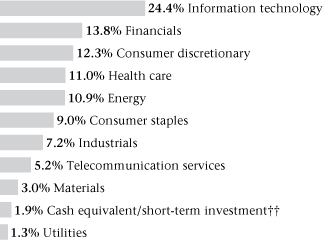

Manager's discussion and analysis

In the 12-month period ended September 30, the Turner Emerging Growth Fund, Investor Class Shares (TMCGX) gained 12.22%, underperforming the Russell 2000 Growth Index's 14.79% return. Subpar results in the information-technology sector, a 19% weighting, were the biggest drag on the fund's performance. Detractors here included semiconductor, data-networking, wireless-communications, and data-storage stocks.

Four of the fund's 10 sector positions added value. Health-care and industrials stocks, which amounted to 32% of holdings, outperformed by the largest margin. Pharmaceutical, biotechnology, medical-device, and industrial-equipment shares were relatively strong performers.

* These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. Performance of the Institutional and Investor Class Shares will differ due to differences in fees.

** The inception date of the Turner Emerging Growth Fund (Institutional Class Shares) was February 1, 2009.

*** The inception date of the Turner Emerging Growth Fund (Investor Class Shares) was February 27, 1998. Index returns are based on Investor Class Shares inception date.

† Percentages based on total investments.

†† Cash equivalents include short-term investments held as collateral for securities lending activity. Please see Note 11 in Notes to Financial Statements for more detailed information.

††† Cash equivalents and short-term investments are not being considered a holding for the top five holdings, but are counted in the number of holdings.

Cl — Class

Amounts designated as "—" are not applicable.

12 TURNER FUNDS 2010 ANNUAL REPORT

INVESTMENT REVIEW

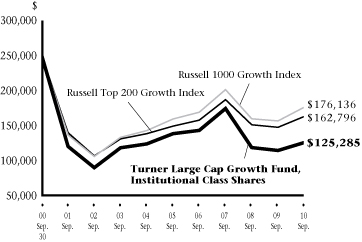

Turner Large Cap Growth Fund

Fund profile

September 30, 2010

g Ticker symbol TSGEX

Institutional Class Shares

g CUSIP #87252R839

Institutional Class Shares

g Top five holdings†††

(1) Apple

(2) PepsiCo

(3) Broadcom, Cl A

(4) Halliburton

(5) QUALCOMM

g % in 5 largest holdings 19.6%†

g Number of holdings 65†††

g Price/earnings ratio 18.1

g Weighted average market capitalization $46.32 billion

g % of holdings with positive earnings surprises 89.1%

g % of holdings with negative earnings surprises 10.9%

g Net assets $118 million, Institutional Class Shares

Growth of a $250,000 investment in the

Turner Large Cap Growth Fund,

Institutional Class Shares:

September 30, 2000-September 30, 2010*,**

Average annual total returns (Periods ending September 30, 2010)

| | | One

year | | Three

years | | Five

years | | Ten

years | | Since

inception | |

| Turner Large Cap Growth Fund, Institutional Class Shares | | | 10.00 | % | | | -10.37 | % | | | -1.93 | % | | | -6.68 | % | | | -6.66 | %** | |

| Turner Large Cap Growth Fund, Investor Class Shares | | | 9.58 | % | | | -10.66 | % | | | — | | | | — | | | | -5.41 | %*** | |

| Russell Top 200 Growth Index | | | 10.57 | % | | | -4.49 | % | | | 1.81 | % | | | -4.20 | % | | | -4.51 | %** | |

| Russell 1000 Growth Index | | | 12.65 | % | | | -4.36 | % | | | 2.06 | % | | | -3.44 | % | | | -3.64 | %** | |

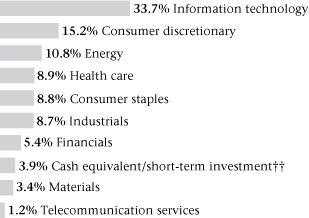

Sector weightings†:

Manager's discussion and analysis

Strong results in the consumer-discretionary and technology sectors weren't enough to offset weak relative returns in other sectors for the Turner Large Cap Growth Fund, Institutional Class (TSGEX) in the 12-month period ended September 30. Although the fund gained 10.00%, that gain slightly underperformed the Russell Top 200 Growth Index's 10.57% rise.

Consumer discretionary and information technology were the only sectors to beat the corresponding index sectors. Retailing, business-services, apparel, consumer-electronics, data-networking, wireless-communications, and semiconductor shares did especially well; together, they accounted for 49% of the fund's investments. Detracting most from performance was a loss in the industrials sector, which represented 9% of the portfolio. Relatively poor performers in those sectors included metals and mining shares.

* These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. Performance of the Institutional and Investor Class Shares will differ due to differences in fees.

** The inception date of the Turner Large Cap Growth Fund (Institutional Class Shares) was June 14, 2000. Index returns are based on Institutional Class Shares inception date.

*** The inception date of the Turner Large Cap Growth Fund (Investor Class Shares) was January 31, 2007.

† Percentages based on total investments.

†† Cash equivalents include short-term investments held as collateral for securities lending activity. Please see Note 11 in Notes to Financial Statements for more detailed information.

††† Cash equivalents and short-term investments are not being considered a holding for the top five holdings, but are counted in the number of holdings.

Cl — Class

Amounts designated as "—" are not applicable.

TURNER FUNDS 2010 ANNUAL REPORT 13

INVESTMENT REVIEW

Turner Midcap Growth Fund

Fund profile

September 30, 2010

g Ticker symbol TMGFX

Investor Class Shares

g CUSIP #900297409

Investor Class Shares

g Top five holdings†††

(1) F5 Networks

(2) Cummins

(3) Starwood Hotels & Resorts Worldwide

(4) Crown Castle International

(5) Salesforce.com

g % in 5 largest holdings 10.5%†

g Number of holdings 85†††

g Price/earnings ratio 19.0

g Weighted average market capitalization $7.50 billion

g % of holdings with positive earnings surprises 78.6%

g % of holdings with negative earnings surprises 20.2%

g Net assets $751 million, Investor Class Shares

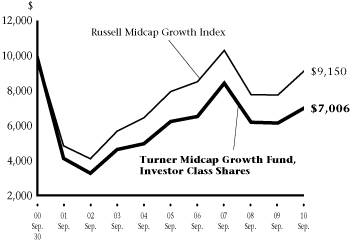

Growth of a $10,000 investment in the

Turner Midcap Growth Fund, Investor Class Shares:

September 30, 2000-September 30, 2010*,***

Average annual total returns (Periods ending September 30, 2010)

| | | One

year | | Three

years | | Five

years | | Ten

years | | Since

inception | |

| Turner Midcap Growth Fund, Institutional Class Shares | | | 14.47 | % | | | — | | | | — | | | | — | | | | -6.26 | %** | |

| Turner Midcap Growth Fund, Investor Class Shares | | | 14.21 | % | | | -5.93 | % | | | 2.41 | % | | | -3.50 | % | | | 9.81 | %*** | |

| Turner Midcap Growth Fund, Retirement Class Shares | | | 13.93 | % | | | -6.16 | % | | | 2.09 | % | | | — | | | | 5.78 | %**** | |

| Russell Midcap Growth Index | | | 18.27 | % | | | -3.90 | % | | | 2.86 | % | | | -0.88 | % | | | 6.38 | %*** | |

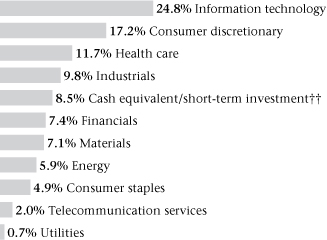

Sector weightings†:

Manager's discussion and analysis

In the 12-month period ended September 30, the Turner Midcap Growth Fund, Investor Class (TMGFX) advanced 14.21%, a result that underperformed the Russell Midcap Growth Index's 18.27% gain.

The fund's performance was most impaired by unfavorable relative returns in the health-care and industrials sectors, a 22% weighting; the fund's biotechnology, medical-equipment, and industrial-equipment stocks were key detractors. Four of the fund's 10 sector positions trumped their corresponding index sectors, with information technology, utilities, and consumer discretionary, a 43% weighting, adding the most value. Contributing the greatest degree of outperformance were semiconductor, data-networking, telecommunications, retailing, and apparel stocks.

* These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. Performance of the Institutional, Investor and Retirement Class Shares will differ due to differences in fees.

** The inception date of the Turner Midcap Growth Fund (Institutional Class Shares) was June 16, 2008.

*** The inception date of the Turner Midcap Growth Fund (Investor Class Shares) was October 1, 1996. Index returns are based on Investor Class Shares inception date.

**** The inception date of the Turner Midcap Growth Fund (Retirement Class Shares) was September 24, 2001.

† Percentages based on total investments.

†† Cash equivalents include short-term investments held as collateral for securities lending activity. Please see Note 11 in Notes to Financial Statements for more detailed information.

††† Cash equivalents and short-term investments are not being considered a holding for the top five holdings, but are counted in the number of holdings.

Amounts designated as "—" are not applicable.

14 TURNER FUNDS 2010 ANNUAL REPORT

INVESTMENT REVIEW

Turner New Enterprise Fund

Fund profile

September 30, 2010

g Ticker symbol TBTBX

g CUSIP #87252R797

g Top five holdings†††

(1) F5 Networks

(2) Apple

(3) Netlogic Microsystems

(4) Alexion Pharmaceuticals

(5) Concho Resources

g % in 5 largest holdings 22.6%†

g Number of holdings 31†††

g Price/earnings ratio 16.8

g Weighted average market capitalization $22.07 billion

g % of holdings with positive earnings surprises 93.3%

g % of holdings with negative earnings surprises 3.3%

g Net assets $23 million

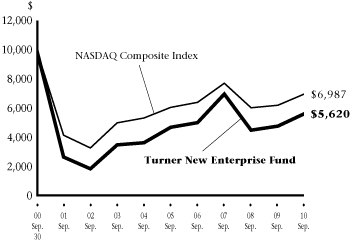

Growth of a $10,000 investment in the

Turner New Enterprise Fund:

September 30, 2000-September 30, 2010*

Average annual total returns (Periods ending September 30, 2010)

| | | One

year | | Three

years | | Five

years | | Ten

years | | Since

inception | |

| Turner New Enterprise Fund | | | 18.25 | % | | | -6.90 | % | | | 3.73 | % | | | -5.60 | % | | | -3.37 | % | |

| NASDAQ Composite Index | | | 12.77 | % | | | -3.27 | % | | | 2.92 | % | | | -3.52 | % | | | -4.15 | % | |

Sector weightings†:

Manager's discussion and analysis

Good stock selection powered the Turner New Enterprise Fund (TBTBX) to an 18.25% gain in the 12-month period ended September 30. The fund's return exceeded that of the NASDAQ Composite Index by 5.48 percentage points.

Five of the fund's seven sector positions outperformed their corresponding index sectors. Returns in three sectors — information technology, health care, and materials, a 57% weighting — were responsible for much of the fund's performance premium. Semiconductor, data-networking, wireless-communications, biotechnology, medical-products, metals, and mining shares contributed the most. A 12% position in consumer-discretionary stocks was the main detractor, with restaurant, gaming, and apparel shares recording poor relative returns.

* These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. The inception date of the Turner New Enterprise Fund was June 30, 2000.

† Percentages based on total investments.

†† Cash equivalents include short-term investments held as collateral for securities lending activity. Please see Note 11 in Notes to Financials for more detailed information.

††† Cash equivalents and short-term investments are not being considered a holding for the top five holdings, but are counted in the number of holdings.

TURNER FUNDS 2010 ANNUAL REPORT 15

INVESTMENT REVIEW

Turner Small Cap Growth Fund

Fund profile

September 30, 2010

g Ticker symbol TSCEX

g CUSIP #900297300

g Top five holdings†††

(1) Aruba Networks

(2) Netlogic Microsystems

(3) AMERIGROUP

(4) Genesee & Wyoming, Cl A

(5) Warnaco Group

g % in 5 largest holdings 6.7%†

g Number of holdings 120†††

g Price/earnings ratio 19.0

g Weighted average market capitalization $1.63 billion

g % of holdings with positive earnings surprises 74.0%

g % of holdings with negative earnings surprises 20.2%

g Net assets $275 million

Growth of a $10,000 investment in the

Turner Small Cap Growth Fund:

September 30, 2000-September 30, 2010*

Average annual total returns (Periods ending September 30, 2010)

| | | One

year | | Three

years | | Five

years | | Ten

years | | Since

inception | |

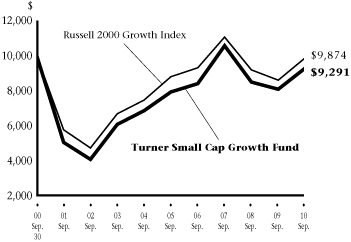

| Turner Small Cap Growth Fund | | | 15.10 | % | | | -4.23 | % | | | 3.26 | % | | | -0.73 | % | | | 10.78 | % | |

| Russell 2000 Growth Index | | | 14.79 | % | | | -3.75 | % | | | 2.35 | % | | | -0.13 | % | | | 4.91 | % | |

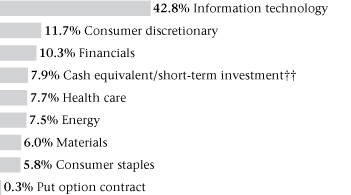

Sector weightings†:

Manager's discussion and analysis

The Turner Small Cap Growth Fund (TSCEX) produced favorable, substantial relative returns in four of the nine market sectors in which it was invested in the 12-month period ended September 30. That was enough to enable the fund to outpace its benchmark, the Russell 2000 Growth Index. The fund recorded a gain of 15.10%, a performance advantage of 0.31 percentage point over the Russell 2000 Growth Index's 14.79% return.

The fund's best relative performers were health-care, energy, and consumer-discretionary stocks, a 35% weighting. Specifically, pharmaceutical, diagnostic-test, medical-equipment, petroleum, energy-services, apparel, retailing, and business-services shares did best in those sectors. Information-technology and financials stocks, a 27% weighting, were drags on performance; semiconductor, data-networking, software, banking, insurance, and diversified-financial shares were among the laggards.

* These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. The inception date of the Turner Small Cap Growth Fund was February 7, 1994.

† Percentages based on total investments.

†† Cash equivalents include short-term investments held as collateral for securities lending activity. Please see Note 11 in Notes to Financial Statements for more detailed information.

††† Cash equivalents and short-term investments are not being considered a holding for the top five holdings, but are counted in the number of holdings.

Cl — Class

16 TURNER FUNDS 2010 ANNUAL REPORT

INVESTMENT REVIEW

Turner Quantitative Broad Market Equity Fund

Fund profile

September 30, 2010

g Ticker symbol TBMEX

Institutional Class Shares

g CUSIP #900297730

Institutional Class Shares

g Top five holdings††

(1) Apple

(2) Microsoft

(3) Wal-Mart Stores

(4) Pfizer

(5) Bristol-Myers Squibb

g % in 5 largest holdings 8.6%†

g Number of holdings 110††

g Price/earnings ratio 13.2

g Weighted average market capitalization $63.68 billion

g % of holdings with positive earnings surprises 84.4%

g % of holdings with negative earnings surprises 13.8%

g Net assets $11 million, Institutional Class Shares

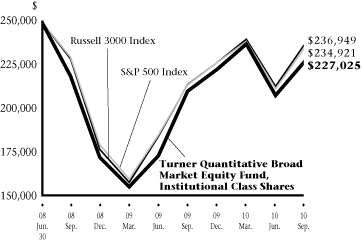

Growth of a $250,000 investment in the

Turner Quantitative Broad Market Equity Fund,

Institutional Class Shares:

June 30, 2008-September 30, 2010*

Average annual total returns (Periods ending September 30, 2010)

| | | One

year | | Since

inception | |

| Turner Quantitative Broad Market Equity Fund, Institutional Class Shares | | | 8.30 | % | | | -4.19 | % | |

| Turner Quantitative Broad Market Equity Fund, Investor Class Shares | | | 7.98 | % | | | -4.43 | % | |

| Russell 3000 Index | | | 10.96 | % | | | -2.35 | % | |

| S&P 500 Index | | | 10.16 | % | | | -2.72 | % | |

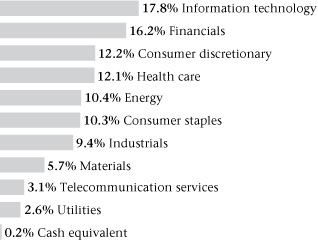

Sector weightings†:

Manager's discussion and analysis

In the 12-month period ended September 30, the Turner Quantitative Broad Market Equity Fund, Institutional Class Shares (TBMEX) rose 8.30%, a performance that fell short of the Russell 3000 Index's 10.96% gain.

The fund recorded good relative returns in three of 10 sectors, whose holdings were selected because they ranked highly in our proprietary quantitative model. Particularly rewarding relative returns were produced by the energy sector, a 10% weighting. Petroleum and energy-services shares were among the best performers in that sector. The model was less effective at selecting good stocks in the other sectors. Impairing results the most were holdings in the health-care and financials sectors, a 28% weighting. Pharmaceutical, medical-device, health-services, banking, insurance, and diversified-financial stocks were the biggest detractors.

* These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemption of fund shares. The inception date of the Turner Quantitative Broad Market Equity Fund was June 30, 2008. Performance of the Institutional and Investor Class Shares will differ due to the difference in fees.

† Percentages based on total investments.

†† Cash equivalents are not being considered a holding for the top five holdings, but are counted in the number of holdings.

TURNER FUNDS 2010 ANNUAL REPORT 17

INVESTMENT REVIEW

Turner Quantitative Large Cap Value Fund

Fund profile

September 30, 2010

g Ticker symbol TLVFX

Institutional Class Shares

g CUSIP #900297821

Institutional Class Shares

g Top five holdings††

(1) Exxon Mobil

(2) AT&T

(3) Berkshire Hathaway, Cl B

(4) JPMorgan Chase

(5) General Electric

g % in 5 largest holdings 14.5%†

g Number of holdings 91††

g Price/earnings ratio 12.9

g Weighted average market capitalization $63.49 billion

g % of holdings with positive earnings surprises 77.8%

g % of holdings with negative earnings surprises 20.0%

g Net assets $0.8 million, Institutional Class Shares

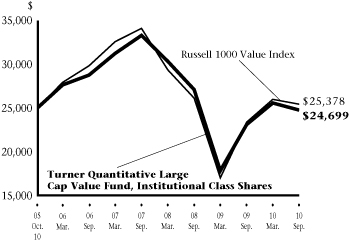

Growth of a $25,000 investment in the

Turner Quantitative Large Cap Value Fund,

Institutional Class Shares:

October 10, 2005-September 30, 2010*,**

Average annual total returns (Periods ending September 30, 2010)

| | | One

year | | Three

years | | Since

inception | |

| Turner Quantitative Large Cap Value Fund, Institutional Class Shares | | | 7.24 | % | | | -9.48 | % | | | -0.24 | %** | |

| Turner Quantitative Large Cap Value Fund, Investor Class Shares | | | 7.07 | % | | | — | | | | 4.53 | %*** | |

| Russell 1000 Value Index | | | 8.90 | % | | | -9.39 | % | | | 0.30 | %** | |

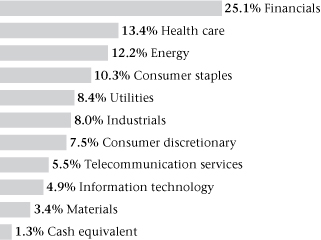

Sector weightings†:

Manager's discussion and analysis

In the 12 months ended September 30, the Turner Quantitative Large Cap Value Fund, Institutional Class Shares (TLVFX) was up 7.24%. The gain trailed that of the Russell 1000 Value Index, which rose 8.90%.

The fund is invested in large-cap value stocks that rank highly in our proprietary quantitative model. The model had mixed success at picking outperforming stocks: four of the fund's 10 sector investments beat their corresponding index sectors. Positions in the financials and energy sectors, a 37% weighting, enhanced performance to the greatest degree; insurance, securities-exchange, investment-management, petroleum, and energy-services shares did best. Hurting results the most were positions in the health-care and consumer-discretionary sectors, which represented 21% of the portfolio; pharmaceutical, medical-equipment, health-services, apparel, restaurant, and retailing shares were significant detractors.

* These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. Performance of the Institutional and Investor Class Shares will differ due to differences in fees.

** The inception date of the Turner Quantitative Large Cap Value Fund (Institutional Class Shares) was October 10, 2005. Index returns are based on Institutional Class Shares inception date.

*** The inception date of the Turner Quantitative Large Cap Value Fund (Investor Class Shares) was October 31, 2008.

† Percentages based on total investments.

†† Cash equivalents are not being considered a holding for the top five holdings, but are counted in the number of holdings.

Cl — Class

Amounts designated as "—" are not applicable.

18 TURNER FUNDS 2010 ANNUAL REPORT

INVESTMENT REVIEW

Turner Global Opportunities Fund

Fund profile

September 30, 2010

g Ticker symbol TGLBX

Institutional Class Shares

g CUSIP #900297623

Institutional Class Shares

g Top five holdings††

(1) Apple

(2) F5 Networks

(3) Alexion Pharmaceuticals

(4) ASML Holding, NY Shares

(5) Lam Research

g % in 5 largest holdings 25.5%†

g Number of holdings 33††

g Price/earnings ratio 18.0

g Weighted average market capitalization $36.59 billion

g % of holdings with positive earnings surprises 70.9%

g % of holdings with negative earnings surprises 10.1%

g Net Assets $1 million, Institutional Class Shares

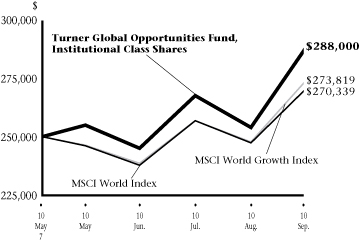

Growth of a $250,000 investment in the

Turner Global Opportunities Fund,

Institutional Class Shares:

May 7, 2010-September 30, 2010*

Cumulative total returns (Period ending September 30, 2010)

| | | Since

inception | |

| Turner Global Opportunities Fund, Institutional Class Shares | | | 15.20 | %** | |

| Turner Global Opportunities Fund, Investor Class Shares | | | 15.00 | %** | |

| MSCI World Growth Index | | | 9.53 | %** | |

| MSCI World Index | | | 8.14 | %** | |

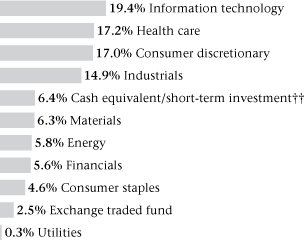

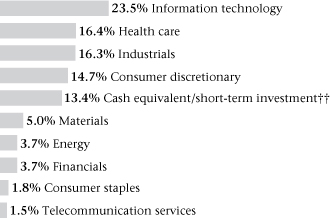

Sector weightings†:

Manager's discussion and analysis

The Turner Global Opportunities Fund, Institutional Class Shares (TGLBX) got off to a strong start in both absolute and relative terms in its first five months of operation. The fund produced a double-digit gain, 15.20%, which beat the MSCI World Growth Index's 9.53% return by 5.67 percentage points.

On balance, stock selection was superior, with five of eight sector positions outperforming their corresponding index sectors. The two sectors that produced the best results were information technology and consumer discretionary, which amounted to 43% of holdings. In those sectors, semiconductor, data-networking, wireless-communications, retailing, business-services, and apparel shares were among the outperformers. The fund's performance was hurt by unsatisfactory relative returns in the industrials, materials, and health-care sectors, with a combined weighting of 24%. Semiconductor-capital-equipment, heavy-equipment, metals, mining, and biotechnology stocks were the biggest laggards.

* These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. The inception date of the Turner Global Opportunities Fund was May 7, 2010. Performance of the Institutional and Investor Class Shares will differ due to differences in fees.

** Cumulative return, not annualized.

† Percentages based on total investments.

†† Cash equivalents are not being considered a holding for the top five holdings, but are counted in the number of holdings.

MSCI — Morgan Stanley Capital International

NY — New York

TURNER FUNDS 2010 ANNUAL REPORT 19

INVESTMENT REVIEW

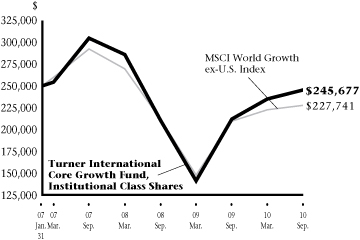

Turner International Core Growth Fund

Fund profile

September 30, 2010

g Ticker symbol TICGX

Institutional Class Shares

g CUSIP #900297771

Institutional Class Shares

g Top five holdings††

(1) Nestle

(2) Novartis

(3) Rio Tinto

(4) BHP Billiton

(5) ASML Holding

g % in 5 largest holdings 13.0%†

g Number of holdings 70††

g Price/earnings ratio 16.0

g Weighted average market capitalization $42.07 billion

g % of holdings with positive earnings surprises 43.5%

g % of holdings with negative earnings surprises 15.9%

g Net assets $5 million, Institutional Class Shares

Growth of a $250,000 investment in the

Turner International Core Growth Fund,

Institutional Class Shares:

January 31, 2007-September 30, 2010*,**

Average annual total returns (Periods ending September 30, 2010)

| | | One

year | | Three

years | | Since

inception | |

| Turner International Core Growth Fund, Institutional Class Shares | | | 15.88 | % | | | -6.98 | % | | | -0.47 | %** | |

| Turner International Core Growth Fund, Investor Class Shares | | | 15.61 | % | | | — | | | | 25.63 | %*** | |

| MSCI World Growth ex-U.S. Index | | | 8.69 | % | | | -8.02 | % | | | -2.51 | %** | |

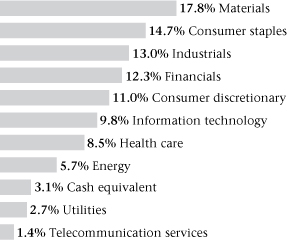

Sector weightings†:

Manager's discussion and analysis

Generally good stock selection resulted in the Turner International Core Growth Fund, Institutional Class Shares (TICGX) recording a 15.88% gain in the 12-month period ended September 30. That return was good enough to beat the MSCI World Growth ex-U.S. Index's 8.69% return by 7.19 percentage points.

Seven of 10 sector positions contributed to the fund's results. Consumer-staples and energy holdings, a 20% weighting, added the most value; in those sectors, food-processing, beverage, supermarket, petroleum, and energy-services shares performed especially well. Information-technology and industrials positions, a 23% weighting, were the two detractors from performance, with semiconductor, data-networking, and heavy-equipment stocks providing weak relative returns.

* These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. Performance of the Institutional and Investor Class Shares will differ due to differences in fees.

** The inception date of the Turner International Core Growth Fund (Institutional Class Shares) was January 31, 2007. Index returns are based on Institutional Class Shares inception date.

*** The inception date of the Turner International Core Growth Fund (Investor Class Shares) was October 31, 2008.

† Percentages based on total investments.

†† Cash equivalents are not being considered a holding for the top five holdings, but are counted in the number of holdings.

MSCI — Morgan Stanley Capital International

Amounts designated as "—" are not applicable.

20 TURNER FUNDS 2010 ANNUAL REPORT

INVESTMENT REVIEW

Turner Small Cap Equity Fund

Fund profile

September 30, 2010

g Ticker symbol TSEIX

Investor Class Shares

g CUSIP #87252R714

Investor Class Shares

g Top five holdings†††

(1) Earthlink

(2) Sally Beauty Holdings

(3) 99 Cents Only Stores

(4) Mentor Graphics

(5) Syniverse Holdings

g % in 5 largest holdings 9.3%†

g Number of holdings 86†††

g Price/earnings ratio 15.4

g Weighted average market capitalization $1.45 billion

g % of holdings with positive earnings surprises 69.4%

g % of holdings with negative earnings surprises 16.5%

g Net assets $6 million, Investor Class Shares

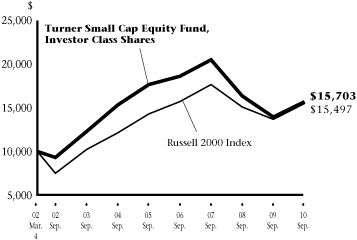

Growth of a $10,000 investment in the

Turner Small Cap Equity Fund,

Investor Class Shares:

March 4, 2002-September 30, 2010*,***

Average annual total returns (Periods ending September 30, 2010)

| | | One

year | | Three

years | | Five

years | | Since

inception | |

| Turner Small Cap Equity Fund, Institutional Class Shares | | | 12.82 | % | | | — | | | | — | | | | 24.14 | %** | |

| Turner Small Cap Equity Fund, Investor Class Shares | | | 12.53 | % | | | -8.53 | % | | | -2.34 | % | | | 5.41 | %*** | |

| Russell 2000 Index | | | 13.35 | % | | | -4.29 | % | | | 1.60 | % | | | 5.24 | %*** | |

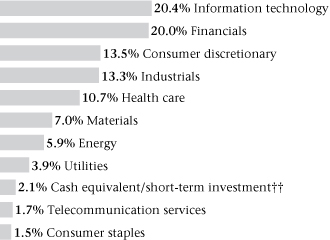

Sector weightings†:

Manager's discussion and analysis

The Turner Small Cap Equity Fund, Investor Class Shares (TSEIX) returned 12.53% in the 12-month period ended September 30. The fund's gain was less than that of the benchmark, the Russell 2000 Index, which climbed 13.35%.