UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-07527 |

|

Turner Funds |

(Exact name of registrant as specified in charter) |

|

1205 Westlakes Drive, Suite 100

Berwyn, PA | | 19312 |

(Address of principal executive offices) | | (Zip code) |

|

Michael P. Malloy

Drinker Biddle & Reath LLP

One Logan Square, Suite 2000

Philadelphia, PA 19103 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 1-800-224-6312 | |

|

Date of fiscal year end: | September 30 | |

|

Date of reporting period: | September 30, 2012 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

Long/short equity funds

Turner Market Neutral Fund

Turner Medical Sciences Long/Short Fund

Turner Spectrum Fund

Turner Titan Fund

U.S. growth equity funds

Turner All Cap Growth Fund

Turner Concentrated Growth Fund

Turner Emerging Growth Fund

Turner Large Growth Fund

Turner Midcap Growth Fund

Turner Small Cap Growth Fund

Global and international equity funds

Turner Global Opportunities Fund

Turner International Growth Fund

Contents

| | 2 | | | Letter to shareholders | |

| | 5 | | | Total returns of the Turner Funds | |

| 9

| | | Investment review:

Turner Market Neutral Fund | |

| 10

| | | Investment review:

Turner Medical Sciences Long/Short Fund | |

| 11

| | | Investment review:

Turner Spectrum Fund | |

| 12

| | | Investment review:

Turner Titan Fund | |

| 13

| | | Investment review:

Turner All Cap Growth Fund | |

| 14

| | | Investment review:

Turner Concentrated Growth Fund | |

| 15

| | | Investment review:

Turner Emerging Growth Fund | |

| 16

| | | Investment review:

Turner Large Growth Fund | |

| 17

| | | Investment review:

Turner Midcap Growth Fund | |

| 18

| | | Investment review:

Turner Small Cap Growth Fund | |

| 19

| | | Investment review:

Turner Global Opportunities Fund | |

| 20

| | | Investment review:

Turner International Growth Fund | |

| | 21 | | | Schedules of investments | |

| | 50 | | | Financial statements | |

| | 72 | | | Notes to financial statements | |

| 82

| | | Report of independent registered public

accounting firm | |

| | 83 | | | Notice to shareholders | |

| | 84 | | | Disclosure of fund expenses | |

| | 86 | | | Trustees and officers of the Trust | |

Turner Funds

As of September 30, 2012, the Turner Funds offered a series of 12 mutual funds to individual and institutional investors. The minimum initial investment for Institutional Class Shares in a Turner Fund is $250,000 (except for $100,000 for the Turner Market Neutral Fund, Turner Medical Sciences Long/Short Fund, Turner Spectrum Fund, and Turner Titan Fund) for regular accounts and $100,000 for individual retirement accounts. The minimum initial investment for Investor Class Shares, Retirement Class Shares, and Class C Shares is $2,500 for regular accounts and $2,000 for individual retirement accounts.

Turner Investments, L.P., based in Berwyn, Pennsylvania, serves as the investment adviser for the Turner Funds. Turner Investments, L.P., founded in 1990, manages more than $11.6 billion in stock investments as of September 30, 2012.

Shareholder services

Turner Funds shareholders receive annual and semiannual reports, quarterly account statements, and a quarterly newsletter. Shareholders who have questions about their accounts may call a toll-free telephone number, 1.800.224.6312, may visit our Web site, www.turnerinvestments.com, or may write to Turner Funds, P.O. Box 219805, Kansas City, Missouri 64121-9805.

TURNER FUNDS 2012 ANNUAL REPORT 1

If you've ever driven to work without recalling traveling from Point A to Point B, you can chalk it up to your basal ganglia. It's your basal ganglia that are the part of your brain responsible for procedural learning — in essence, for creating habits.

It typically takes three or four weeks of repetition to make a new habit automatic. But for stock investors, it's taken years to adjust to the stock market after the infamous financial crisis of 2008 — that is, a market ruled more by macroeconomic events like European sovereign-debt problems than by underlying company fundamentals like expanding profit margins.

Here's how the macroeconomic picture looks now. Europe is mired in a recession, but its banking and political leaders have made enough progress and enough commitments that the prospect of a debt contagion seems much less likely than before. China, the world's second-largest economy, is no longer registering blazing economic growth, but it is still growing (at a 7.7% annual rate, according to the World Bank) and thus averting the widely feared hard landing. And the United States has faced quarter after quarter of tepid (below 3%) economic growth, but at the same time no economists of any repute are forecasting even a single quarter of negative growth through 2014.

In short, after years of fretting about a dizzying array of macroeconomic issues, investors seem to have accepted that eventually, somehow, those issues will muddle through to resolution. Instead, investors now seem increasingly focused on how to cope with — and capitalize on — this new reality of slow global economic growth.

Living the new reality

In coming to terms with this new reality, long-term stock investors have notably done well; those who had the tolerance for risk to endure the few rough market patches of the last few years have generally been rewarded amply. In the 12-month period ended September 30, 2012, that's the subject of this report, the S&P 500 Index rose 30.20%. That extraordinary gain in turn helped lift the S&P 500 Index 116% from its bottom in March 2009 (and within spitting distance — within 8% — of its all-time high of 1565.15 reached in October 2007).

We believe a bull market may prevail in the 2010s. The current bull market is the eighth-strongest and ninth-longest since 1928, according to Bespoke Investment Group. We think this bull has more room to run, especially since some investors aren't convinced it's had legs to stand on. Reuters called this "the most uncelebrated bull market in history," and we agree. But we think there are a number of reasons why investors may appreciate this market more as time passes.

Green shoots in sight

First, stocks remain cheaply priced. Selling for 13 times next year's earnings, stocks are still priced below their long-term average of 16. The Federal Reserve has vowed to keep interest rates low through 2015, which has driven 10-year Treasury yields below 2%. As measly as a $1 tip on a seven-course dinner, Treasuries in particular and investment-grade bonds in general seem unlikely to even cover the rate of inflation going forward. We think stocks offer a distinctly more attractive risk/reward profile in comparison.

Then there's the reviving housing market. We believe we're seeing a true, sustainable recovery after several false starts. Demand for homes is rising along with prices, while renting is becoming prohibitively expensive and competitive for many consumers. When you factor in record-low mortgage rates, it seems like an attractive time to buy a home, which remains the essence of the American dream.

A true housing recovery could provide an additional leg up for consumer spending, which accounts for roughly 70% of U.S. gross domestic product. Rising home values enhance the so-called "wealth effect" for homeowners, based on the premise that as personal wealth increases, so, proportionately, does consumer spending and investment. Bank of America Merrill Lynch calculates that this wealth effect could raise gross domestic product each quarter in the back half of 2013 by 0.1 percentage point. As a result consumers may feel comfortable investing in stocks rather than keeping their money stashed under bedroom floorboards or — a marginally better alternative — in a five-year certificate of deposit that paid 1.38% on average nationally, as of September 30.

Up, up and away?

Third, stocks may have boosted their appeal just by continuing to rise over the past 12 months. With the exception of a brief stumble in the spring, which prompted some pundits to (incorrectly) predict a third consecutive summer slump, the market performed impressively for much of the past 12 months. All told, nine of the 12 months produced positive returns and a steady upward climb for the S&P 500 Index.

Finally, central banks around the world have been busy providing stimulus to keep the global economy chugging along. All told, more than 250 stimulus measures have been carried out in the past 12 months, according to ISI Group. We think all this activity clearly shows that governments are determined to keep the global economy's head above recessionary waters. We think such activity should soothe investors' pangs of uncertainty and in the process help keep the market investor friendly.

Even though the market has on balance been investor friendly over the past 12 months, cautionary "risk on/risk off" investing was much in evidence. Investors tended to

2 TURNER FUNDS 2012 ANNUAL REPORT

adjust their appetite for risk based on the levels of danger they perceived in the macroeconomic environment, preferring "safe" investments such as bonds when risk seemed high and flocking to "riskier" assets like stocks when conditions appeared less threatening.

Growth investing not rewarded fully

During the period, as always, the investment process used to manage our eight U.S. and global/international growth funds and our four long/short funds prized earnings, and we invested in the stocks of those companies that we believed could generate superior earnings growth. To our consternation, though, in many cases the stocks with the best earnings growth — which also tend to be more richly valued and more volatile — weren't rewarded lavishly by investors when they were in a risk-on frame of mind.

With bond yields leaving much to be desired, many investors evidently sought income from stocks with lower volatility and higher dividends — the mirror image of the growth stocks we prefer. That, alas, moderated the total returns of our funds. Ours wasn't a singular investing experience by any means; less than 40% of actively managed stock funds beat their benchmarks during the period, according to Bank of America Merrill Lynch.

Net-net, we think our family of stock funds generally performed well in absolute terms for the 12-month period. Eight of our 12 funds generated double-digit gains, but only two of them outperformed at least one of their benchmarks: the Turner International Growth Fund and the Turner Titan Fund. Our four long/short funds delivered relatively low volatility, as they are designed to do, but their short positions impaired their ability to produce positive returns in a market whose direction was decidedly up.

Total returns | | | | | |

12-month period ended September 30, 2012 | | | | | |

Long/short equity funds | | | | | |

Turner Market Neutral Fund,

Investor Class (TMNFX) | | | -1.62 | % | |

S&P 500 Index | | | 30.20 | | |

Barclays Capital U.S. Aggregate Bond Index | | | 5.16 | | |

Lipper Equity Market-Neutral Funds Average | | | 2.06 | | |

Turner Medical Sciences Long/Short Fund,

Investor Class (TMSFX) | | | -1.74 | | |

S&P 500 Healthcare Index | | | 29.54 | | |

Barclays Capital U.S. Aggregate Bond Index | | | 5.16 | | |

Lipper Long/Short Equity Funds Average | | | 10.61 | | |

Turner Spectrum Fund, Institutional

Class (TSPEX) | | | -0.77 | | |

S&P 500 Index | | | 30.20 | | |

Barclays Capital U.S. Aggregate Bond Index | | | 5.16 | | |

Lipper Long/Short Equity Funds Average | | | 10.61 | | |

Turner Titan Fund, Investor Class (TTLFX) | | | 5.44 | % | |

S&P 500 Index | | | 30.20 | | |

Barclays Capital U.S. Aggregate Bond Index | | | 5.16 | | |

Lipper Long/Short Equity Funds Average | | | 10.61 | | |

U.S. growth equity funds | | | | | |

Turner All Cap Growth Fund (TBTBX) | | | 17.47 | | |

Nasdaq Composite Index | | | 29.02 | | |

Russell 3000® Growth Index | | | 29.35 | | |

Turner Concentrated Growth Fund (TTOPX) | | | 16.04 | | |

S&P 500 Index | | | 30.20 | | |

Russell 1000® Growth Index | | | 29.19 | | |

Turner Emerging Growth Fund, Investor

Class (TMCGX) | | | 25.57 | | |

Russell 2000® Growth Index | | | 31.18 | | |

Turner Large Growth Fund,

Institutional Class (TTMEX) | | | 22.48 | | |

Russell 1000® Growth Index | | | 29.19 | | |

Turner Midcap Growth Fund, Investor

Class (TMGFX) | | | 16.15 | | |

Russell Midcap® Growth Index | | | 26.69 | | |

Turner Small Cap Growth Fund (TSCEX) | | | 29.21 | | |

Russell 2000® Growth Index | | | 31.18 | | |

International and global equity funds | | | | | |

Turner Global Opportunities Fund,

Institutional Class (TGLBX) | | | 20.53 | | |

MSCI World Growth Index | | | 23.52 | | |

MSCI World Index | | | 22.32 | | |

Turner International Growth Fund,

Institutional Class (TICGX) | | | 17.92 | | |

MSCI World ex-U.S. Growth Index | | | 14.91 | | |

(Please call 1.800.224.6312 or visit our Web site at www.turnerinvestments.com for the most recent month-end performance. For more details on the performance of each fund during the 12-month period, see the Investment review beginning on page 9.)

Long term matters more

Delivering double-digit returns over 12 months, as our growth funds did in this period, certainly has its merits. But to pat ourselves on the back for such performance would be disingenuous and myopic in the extreme, since our goal is to outperform generally and since the ultimate purpose of investing is to multiply your, and our, wealth over the long term. We say "our wealth" because our employees are invested in our funds. So, although our growth funds posted strong gains in the past 12 months, our employee shareholders, like you, would have much preferred that a majority of our funds had bested the indexes.

We are far more pleased with our funds' long-term track records, which in our opinion is the true test of any

TURNER FUNDS 2012 ANNUAL REPORT 3

LETTER TO SHAREHOLDERS (continued)

investment's mettle. Since inception, seven of our eight growth funds have beaten one or more of their benchmarks. And our long/short funds have all achieved positive returns since inception, with lower volatility than that of the broad market.

While no one can always accurately predict the future, when we look forward, we believe stocks may continue rising — even if their ascent isn't quite as rapid as the number of views of a new viral video on the Internet. Even so, we think it's entirely possible that the S&P 500 Index could reach, and perhaps even surpass, its all-time high of 2007 over the next 12 months. As we see it, there's plenty to be optimistic about in 2013 and beyond. We think that stocks, after their paltry returns in the 2000s, appear to be reverting to their long-term average of 10% annualized returns in this decade.

Uncertainties remain

Don't get us wrong — there are still legitimate uncertainties out there that could thwart stocks and discourage the investors now sitting on the sidelines from getting into the market scrum. For instance, one unknown of Mount Everest stature looms in the short term: the outcome of the so-called "fiscal cliff," a combination of prospective federal tax increases and spending cuts at the end of the year. Some Wall Street analysts expect a potential drag of 1-1.5% on the economy early next year if the nation falls off the fiscal cliff. However, we don't think either political party, even in this age of fierce and dismaying partisanship, would be reckless enough to slam the brakes on the economy. Although each party's approach to solving America's fiscal problems figures to differ like the candidates' favorite red and blue ties, we think an acceptable compromise on the fiscal cliff should be reached, even though voters in the November election basically maintained the political status quo in Washington; they reelected President Obama and kept the House in Republican hands and the Senate in Democratic hands.

In the nearly four years of this economic recovery, earnings growth has been the stock market's engine. As the recovery ages, it's a stretch to expect continued blowout earnings each quarter. That's not to imply that earnings will collapse; we simply believe earnings-growth rates are likely to slow — and price/earnings multiples may rise. That could be a boon for both growth stocks and the market as a whole: investors' willingness to buy quality stocks for their sustained earnings growth could reinforce the market's upward tendencies.

In anticipation of the market's further ascent, we've positioned our U.S. and international/global growth funds to emphasize three types of stocks: classic growth stocks such as biotechnology and wireless-communications shares that we think have strong fundamentals; stocks of companies gaining market share; and growth-cyclical

stocks in industries like retailing, manufacturing, and housing that have tended to do well as the economic cycle progresses. As for our long/short funds, their long positions contain similar types of bona fide growth stocks, while their short positions consist of shares of companies that we believe have poor earnings potential.

We don't believe in timing the market; we generally remain fully invested in stocks. (That's one habit our own basal ganglia has made automatic in us.) We believe as the housing market, employment, and consumer sentiment improve in the U.S. and the global economy continues to expand, the positive catalysts will likely outweigh the negative catalysts and elevate stocks into 2013. And we pledge to continue doing our best for you and us in what we think could be a rewarding time for stocks not only in 2013 but in this decade.

Bob Turner

Chairman and Chief Investment Officer

Turner Investments

Past performance is no guarantee of future results. The views expressed are those of Turner Investments as of September 30, 2012, and are not intended as a forecast or investment recommendations. The indexes mentioned are not available for investment.

4 TURNER FUNDS 2012 ANNUAL REPORT

Total returns of the Turner Funds

Through September 30, 2012

Current performance may be lower or higher than the performance data quoted. Please call 1.800.224.6312 or visit our Web site at www.turnerinvestments.com for the most recent month-end performance information.

The performance data quoted represents past performance and the principal value and investment return will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Past performance is no guarantee of future results. Returns shown, unless otherwise indicated, are total returns, with dividends and income reinvested. Returns spanning more than one year are annualized. Fee waivers are in effect; if they had not been in effect, performance would have been lower. The indices mentioned are unmanaged statistical composites of stock-market performance. Investing in an index is not possible.

The holdings and sector weightings of the Funds are subject to change. Forward-earnings projections are not predictors of stock price or investment performance, and do not represent past performance. There is no guarantee that the forward-earnings projections will accurately predict the actual earnings experience of any of the companies involved, and there is no guarantee that owning securities of companies with relatively high price-to-earnings ratios will cause the portfolio to outperform its benchmark or index.

The Turner Funds are distributed by Foreside Fund Services, LLC, Portland, Maine. The investor should consider the investment objectives, risks, charges, and expenses carefully before investing. This and other information can be found in the prospectus. A free prospectus, which contains detailed information, including fees and expenses, and the risks associated with investing in these Funds, can be obtained by calling 1.800.224.6312. Read the prospectus carefully before investing.

Fund name/Index | | Six

months* | | Year

to

date* | | One

year | | Three

years | | Five

years | | 10

years | | (Annualized)

Since

inception | | Total

net assets

($mil) | |

Turner Market Neutral Fund —

Institutional Class Shares | | | -1.45 | % | | | -1.17 | % | | | -1.23 | % | | | n/a | | | | n/a | | | | n/a | | | | 2.41 | % | | $ | 48.05 | | |

Investor Class Shares | | | -1.65 | | | | -1.46 | | | | -1.62 | | | | n/a | | | | n/a | | | | n/a | | | | 2.11 | | | | 5.69 | | |

Class C Shares | | | -1.96 | | | | -1.96 | | | | -2.21 | | | | n/a | | | | n/a | | | | n/a | | | | 1.38 | | | | 0.09 | | |

S&P 500 Index | | | 3.43 | | | | 16.44 | | | | 30.20 | | | | n/a | | | | n/a | | | | n/a | | | | 8.23 | | | | | | |

Barclays Capital U.S. Aggregate

Bond Index | | | 3.68 | | | | 3.99 | | | | 5.16 | | | | n/a | | | | n/a | | | | n/a | | | | 7.76 | | | | | | |

Lipper Equity Market-Neutral

Funds Average | | | 0.00 | | | | 1.15 | | | | 2.06 | | | | n/a | | | | n/a | | | | n/a | | | | 1.14 | | | | | | |

Inception date: 2/7/11 | |

Turner Medical Sciences

Long/Short Fund —

Institutional Class Shares | | | -0.20 | | | | -1.64 | | | | -1.55 | | | | n/a | | | | n/a | | | | n/a | | | | 1.15 | | | | 37.12 | | |

Investor Class Shares | | | -0.29 | | | | -1.84 | | | | -1.74 | | | | n/a | | | | n/a | | | | n/a | | | | 0.97 | | | | 9.61 | | |

Class C Shares | | | -0.69 | | | | -2.33 | | | | -2.52 | | | | n/a | | | | n/a | | | | n/a | | | | 0.24 | | | | 2.89 | | |

S&P 500 Healthcare Index | | | 8.01 | | | | 17.80 | | | | 29.54 | | | | n/a | | | | n/a | | | | n/a | | | | 16.89 | | | | | | |

Barclays Capital U.S. Aggregate

Bond Index | | | 3.68 | | | | 3.99 | | | | 5.16 | | | | n/a | | | | n/a | | | | n/a | | | | 7.76 | | | | | | |

Lipper Long/Short Equity Funds

Average | | | -0.03 | | | | 5.54 | | | | 10.61 | | | | n/a | | | | n/a | | | | n/a | | | | -0.69 | | | | | | |

Inception date: 2/7/11 | |

TURNER FUNDS 2012 ANNUAL REPORT 5

LETTER TO SHAREHOLDERS (continued)

Fund name/Index | | Six

months* | | Year

to

date* | | One

year | | Three

years | | Five

years | | 10

years | | (Annualized)

Since

inception | | Total

net assets

($mil) | |

Turner Spectrum Fund —

Institutional Class Shares | | | -2.51 | % | | | -0.55 | % | | | -0.77 | % | | | 1.90 | % | | | n/a | | | | n/a | | | | 4.03 | % | | $ | 832.86 | | |

Investor Class Shares | | | -2.53 | | | | -0.74 | | | | -0.95 | | | | 1.66 | | | | n/a | | | | n/a | | | | 3.79 | | | | 126.53 | | |

Class C Shares(1) | | | -2.94 | | | | -1.31 | | | | -1.71 | | | | 0.96 | | | | n/a | | | | n/a | | | | 3.40 | | | | 10.39 | | |

S&P 500 Index | | | 3.43 | | | | 16.44 | | | | 30.20 | | | | 13.20 | | | | n/a | | | | n/a | | | | 17.01 | | | | | | |

Barclays Capital U.S.

Aggregate Bond Index | | | 3.68 | | | | 3.99 | | | | 5.16 | | | | 6.19 | | | | n/a | | | | n/a | | | | 6.98 | | | | | | |

Lipper Long/Short Equity

Funds Average | | | -0.03 | | | | 5.54 | | | | 10.61 | | | | 4.73 | | | | n/a | | | | n/a | | | | 7.73 | | | | | | |

Inception date: 5/7/09 | |

Turner Titan Fund —

Institutional Class Shares | | | -1.54 | | | | 4.60 | | | | 5.75 | | | | n/a | | | | n/a | | | | n/a | | | | 2.00 | | | | 25.81 | | |

Investor Class Shares | | | -1.73 | | | | 4.40 | | | | 5.44 | | | | n/a | | | | n/a | | | | n/a | | | | 1.76 | | | | 5.04 | | |

Class C Shares | | | -2.14 | | | | 3.71 | | | | 4.53 | | | | n/a | | | | n/a | | | | n/a | | | | 0.97 | | | | 0.53 | | |

S&P 500 Index | | | 3.43 | | | | 16.44 | | | | 30.20 | | | | n/a | | | | n/a | | | | n/a | | | | 8.23 | | | | | | |

Barclays Capital U.S.

Aggregate Bond Index | | | 3.68 | | | | 3.99 | | | | 5.16 | | | | n/a | | | | n/a | | | | n/a | | | | 7.76 | | | | | | |

Lipper Long/Short Equity

Funds Average | | | -0.03 | | | | 5.54 | | | | 10.61 | | | | n/a | | | | n/a | | | | n/a | | | | -0.69 | | | | | | |

Inception date: 2/7/11 | |

Turner All Cap

Growth Fund(2) | | | -4.35 | | | | 10.55 | | | | 17.47 | | | | 14.87 | | | | 0.67 | % | | | 14.79 | % | | | -0.84 | | | | 25.84 | | |

Nasdaq Composite Index | | | 0.80 | | | | 19.62 | | | | 29.02 | | | | 13.66 | | | | 2.90 | | | | 10.27 | | | | -1.95 | | | | | | |

Russell 3000® Growth Index | | | 1.75 | | | | 16.59 | | | | 29.35 | | | | 14.69 | | | | 3.22 | | | | 8.57 | | | | -0.72 | | | | | | |

Inception date: 6/30/00 | |

Turner Concentrated

Growth Fund | | | -7.91 | | | | 11.53 | | | | 16.04 | | | | 6.65 | | | | -5.89 | | | | 6.37 | | | | 0.49 | | | | 34.93 | | |

S&P 500 Index | | | 3.43 | | | | 16.44 | | | | 30.20 | | | | 13.20 | | | | 1.05 | | | | 8.01 | | | | 2.23 | | | | | | |

Russell 1000® Growth Index | | | 1.84 | | | | 16.80 | | | | 29.19 | | | | 14.73 | | | | 3.24 | | | | 8.41 | | | | 0.88 | | | | | | |

Inception date: 6/30/99 | |

Turner Emerging Growth Fund(2) —

Institutional Class Shares(3) | | | 0.79 | | | | 11.83 | | | | 25.86 | | | | 15.15 | | | | n/a | | | | n/a | | | | 21.26 | | | | 69.39 | | |

Investor Class Shares | | | 0.65 | | | | 11.62 | | | | 25.57 | | | | 14.87 | | | | 1.43 | | | | 11.14 | | | | 17.91 | | | | 168.99 | | |

Russell 2000® Growth Index | | | 0.71 | | | | 14.08 | | | | 31.18 | | | | 14.19 | | | | 2.96 | | | | 10.55 | | | | 3.62 | | | | | | |

Inception date: 2/27/98 | |

Turner Large Growth Fund —

Institutional Class Shares | | | -2.80 | | | | 14.01 | | | | 22.48 | | | | 9.21 | | | | -1.95 | | | | 7.64 | | | | 2.38 | | | | 201.05 | | |

Investor Class Shares(4) | | | -2.90 | | | | 13.85 | | | | 22.26 | | | | 8.96 | | | | -2.19 | | | | n/a | | | | 2.79 | | | | 47.86 | | |

Russell 1000® Growth Index | | | 1.84 | | | | 16.80 | | | | 29.19 | | | | 14.73 | | | | 3.24 | | | | 8.41 | | | | 2.64 | | | | | | |

Inception date: 2/28/01 | |

Turner Midcap Growth Fund(2) —

Institutional Class Shares(5) | | | -5.42 | | | | 8.66 | | | | 16.34 | | | | 10.65 | | | | n/a | | | | n/a | | | | 0.48 | | | | 236.15 | | |

Investor Class Shares | | | -5.53 | | | | 8.52 | | | | 16.15 | | | | 10.40 | | | | -0.38 | | | | 9.78 | | | | 9.65 | | | | 404.43 | | |

Retirement Class Shares(6) | | | -5.58 | | | | 8.30 | | | | 15.83 | | | | 10.12 | | | | -0.64 | | | | 9.39 | | | | 9.37 | | | | 4.81 | | |

Russell Midcap® Growth Index | | | -0.56 | | | | 13.88 | | | | 26.69 | | | | 14.73 | | | | 2.54 | | | | 11.11 | | | | 7.19 | | | | | | |

Inception date: 10/1/96 | |

6 TURNER FUNDS 2012 ANNUAL REPORT

Fund name/Index | | Six

months* | | Year

to

date* | | One

year | | Three

years | | Five

years | | 10

years | | (Annualized)

Since

inception | | Total

net assets

($mil) | |

Turner Small Cap

Growth Fund(2) | | | -0.47 | % | | | 11.78 | % | | | 29.21 | % | | | 12.63 | % | | | 1.75 | % | | | 11.04 | % | | | 10.85 | % | | $ | 250.10 | | |

Russell 2000® Growth Index | | | 0.71 | | | | 14.08 | | | | 31.18 | | | | 14.19 | | | | 2.96 | | | | 10.55 | | | | 5.84 | | | | | | |

Inception date: 2/7/94 | |

Turner Global

Opportunities Fund —

Institutional Class Shares | | | -5.06 | | | | 11.57 | | | | 20.53 | | | | n/a | | | | n/a | | | | n/a | | | | 14.07 | | | | 1.65 | | |

Investor Class Shares | | | -5.17 | | | | 11.37 | | | | 20.27 | | | | n/a | | | | n/a | | | | n/a | | | | 13.76 | | | | 0.25 | | |

MSCI World Growth Index | | | 1.28 | | | | 14.74 | | | | 23.52 | | | | n/a | | | | n/a | | | | n/a | | | | 12.08 | | | | | | |

MSCI World Index | | | 1.65 | | | | 13.56 | | | | 22.32 | | | | n/a | | | | n/a | | | | n/a | | | | 10.63 | | | | | | |

Inception date: 5/7/10 | |

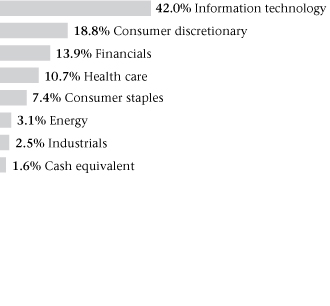

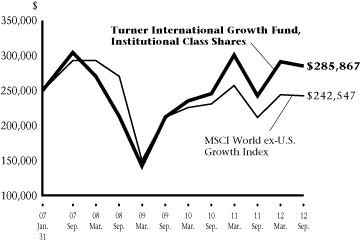

Turner International

Growth Fund —

Institutional Class Shares | | | -2.51 | | | | 9.81 | | | | 17.92 | | | | 10.48 | | | | -1.30 | | | | n/a | | | | 2.39 | | | | 23.41 | | |

Investor Class Shares(7) | | | -2.62 | | | | 9.65 | | | | 17.67 | | | | 10.18 | | | | n/a | | | | n/a | | | | 16.06 | | | | 6.17 | | |

MSCI World ex-U.S. Growth Index | | | -0.70 | | | | 10.47 | | | | 14.91 | | | | 4.62 | | | | -3.74 | | | | n/a | | | | -0.53 | | | | | | |

Inception date: 1/31/07 | |

(1) Commenced operations on July 14, 2009.

(2) Investing in technology and science companies and small- and mid-capitalization companies may subject the Funds to specific inherent risks, including above-average price fluctuations.

(3) Commenced operations on February 1, 2009.

(4) Commenced operations on August 1, 2005.

(5) Commenced operations on June 16, 2008.

(6) Commenced operations on September 24, 2001.

(7) Commenced operations on October 31, 2008.

* Returns of less than one year are cumulative, and not annualized.

TURNER FUNDS 2012 ANNUAL REPORT 7

Expense Ratio†

| | | Gross

expense

ratio | | Net

expense

ratio* | |

Turner Market Neutral Fund | |

Institutional Class Shares | | | 3.92 | % | | | 1.95 | % | |

Investor Class Shares | | | 4.18 | % | | | 2.20 | % | |

Class C Shares | | | 4.77 | % | | | 2.95 | % | |

Turner Medical Sciences

Long/Short Fund | |

Institutional Class Shares | | | 2.79 | % | | | 1.95 | % | |

Investor Class Shares | | | 2.94 | % | | | 2.20 | % | |

Class C Shares | | | 3.68 | % | | | 2.95 | % | |

Turner Spectrum Fund | |

Institutional Class Shares | | | 2.53 | % | | | 1.95 | % | |

Investor Class Shares | | | 2.75 | % | | | 2.20 | % | |

Class C Shares | | | 3.44 | % | | | 2.95 | % | |

Turner Titan Fund | |

Institutional Class Shares | | | 3.56 | % | | | 1.95 | % | |

Investor Class Shares | | | 4.68 | % | | | 2.20 | % | |

Class C Shares | | | 3.82 | % | | | 2.95 | % | |

Turner All Cap Growth Fund | |

Investor Class Shares | | | 2.12 | % | | | 1.73 | % | |

Turner Concentrated Growth Fund | |

Investor Class Shares | | | 2.08 | % | | | 1.69 | % | |

| | | Gross

expense

ratio | | Net

expense

ratio* | |

Turner Emerging Growth Fund | |

Institutional Class Shares | | | 1.29 | % | | | 1.17 | % | |

Investor Class Shares | | | 1.57 | % | | | 1.42 | % | |

Turner Large Growth Fund | |

Institutional Class Shares | | | 0.89 | % | | | 0.69 | % | |

Investor Class Shares | | | 1.13 | % | | | 0.94 | % | |

Turner Midcap Growth Fund | |

Institutional Class Shares | | | 1.05 | % | | | 0.93 | % | |

Investor Class Shares | | | 1.28 | % | | | 1.18 | % | |

Retirement Class Shares | | | 1.54 | % | | | 1.43 | % | |

Turner Small Cap Growth Fund | |

Investor Class Shares | | | 1.53 | % | | | 1.25 | % | |

Turner Global Opportunities Fund | |

Institutional Class Shares | | | 3.64 | % | | | 1.11 | % | |

Investor Class Shares | | | 3.89 | % | | | 1.36 | % | |

Turner International Growth Fund | |

Institutional Class Shares | | | 2.41 | % | | | 1.10 | % | |

Investor Class Shares | | | 2.46 | % | | | 1.35 | % | |

† These expense ratios are based on the most recent prospectus and may differ from those shown in the financial highlights.

* Net expense ratio reflects contractual waivers of certain fees and/or expense reimbursements. Turner may discontinue this arrangement at any time after January 31, 2013.

8 TURNER FUNDS 2012 ANNUAL REPORT

Turner Market Neutral Fund

Fund profile

September 30, 2012

n Ticker symbol TMNFX

Investor Class Shares

n CUSIP #900297581

Investor Class Shares

n Top five holdings1

(1) Freeport-McMoRan Copper & Gold

(2) Embraer SA SP ADR

(3) Deere

(4) SPX

(5) Invesco

n % in five largest holdings 22%2

n Number of holdings 721

n Weighted average market capitalization $40.29 billion

n Net assets $6 million, Investor Class Shares

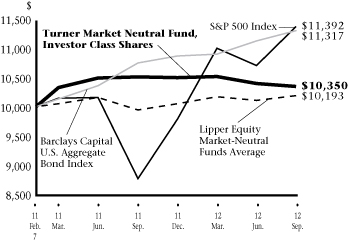

Growth of a $10,000 investment in the

Turner Market Neutral Fund, Investor Class Shares:

February 7, 2011-September 30, 20123,4

Average annual total returns (Periods ended September 30, 2012)

| | | One

year | | Since

inception4 | |

Turner Market Neutral Fund, Institutional Class Shares5 | | | -1.23 | % | | | 2.41 | % | |

Turner Market Neutral Fund, Investor Class Shares5 | | | -1.62 | % | | | 2.11 | % | |

Turner Market Neutral Fund, Class C Shares5 | | | -2.21 | % | | | 1.38 | % | |

S&P 500 Index6 | | | 30.20 | % | | | 8.23 | % | |

Barclays Capital U.S. Aggregate Bond Index7 | | | 5.16 | % | | | 7.76 | % | |

Lipper Equity Market-Neutral Funds Average8 | | | 2.06 | % | | | 1.14 | % | |

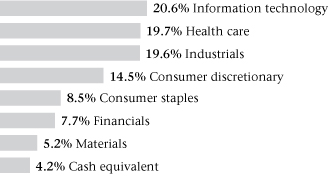

Sector weightings2:

Manager's discussion and analysis

Poor short positions hampered the Turner Market Neutral Fund, Investor Class Shares (TMNFX), which generated a loss of 1.62% in the 12-month period ended September 30. The fund's return trailed that of the S&P 500 Index by 31.82 percentage points, the Barclays Capital U.S. Aggregate Bond Index by 6.78 percentage points, and the Lipper Equity Market-Neutral Funds Average by 3.68 percentage points. The Turner Market Neutral Fund seeks capital appreciation using a long/short strategy in seeking to capture alpha, reduce volatility, and preserve capital in declining markets.

The consumer-discretionary, consumer-staples, financials, and industrials sectors added the most extra return. In those sectors, long and short positions in gaming, automotive, beverage, investment-management, regional-bank, oil-exploration, and pipeline shares generated the best performance. The materials sector was the biggest detractor from performance. In that sector, long and short positions in steel, building-products, and diversified-chemical shares produced unsatisfactory results.

1 Cash equivalent is not being considered a holding for the top five holdings, but is counted in the number of holdings. Top five holdings are based on long positions. The fund composition is subject to change.

2 Percentages based on total investments of long positions.

3 These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. Performance of the Institutional, Investor and Class C Shares will differ due to differences in fees.

4 The inception date of the Turner Market Neutral Fund was February 7, 2011.

5 Fee waivers are in effect; if they had not been in effect, performance would have been lower.

6 The S&P 500 Index is a widely-recognized, market value-weighted (higher market value stocks have more influence than lower market value stocks) index of 500 stocks designed to mimic the overall equity market's industry weightings.

7 The Barclays Capital U.S. Aggregate Bond Index (prior to November 2008, the Index was known as the "Lehman Brothers U.S. Aggregate Bond Index") represents an unmanaged diversified portfolio of fixed income securities, including U.S. Treasuries, investment-grade corporate bonds and mortgage-backed and asset-backed securities.

8 The Lipper Equity Market-Neutral Funds Average represents the average annualized total return for all reporting funds in the Lipper Equity Market-Neutral Fund category.

The Turner Market Neutral Fund is subject to the risks associated with selling securities short. A short sale involves a finite opportunity for appreciation, but a theoretically unlimited risk of loss. The Fund may focus its investments from time to time on one or more economic sectors. To the extent that it does so, developments affecting companies in that sector or sectors will likely have a magnified effect on the Fund's net asset value and total return.

TURNER FUNDS 2012 ANNUAL REPORT 9

Turner Medical Sciences Long/Short Fund

Fund profile

September 30, 2012

n Ticker symbol TMSFX

Investor Class Shares

n CUSIP #900297557

Investor Class Shares

n Top five holdings1

(1) Covidien

(2) Alexion Pharmaceuticals

(3) Allergan

(4) Abbott Laboratories

(5) Cooper

n % in five largest holdings 18.6%2

n Number of holdings 681

n Weighted average market capitalization $37.92 billion

n Net assets $10 million, Investor Class Shares

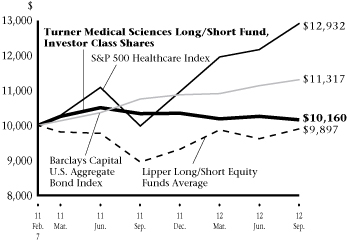

Growth of a $10,000 investment in the

Turner Medical Sciences Long/Short Fund,

Investor Class Shares:

February 7, 2011-September 30, 20123,4

Average annual total returns (Periods ended September 30, 2012)

| | | One

year | | Since

inception4 | |

Turner Medical Sciences Long/Short Fund, Institutional Class Shares5 | | | -1.55 | % | | | 1.15 | % | |

Turner Medical Sciences Long/Short Fund, Investor Class Shares5 | | | -1.74 | % | | | 0.97 | % | |

Turner Medical Sciences Long/Short Fund, Class C Shares5 | | | -2.52 | % | | | 0.24 | % | |

S&P 500 Healthcare Index6 | | | 29.54 | % | | | 16.89 | % | |

Barclays Capital U.S. Aggregate Bond Index7 | | | 5.16 | % | | | 7.76 | % | |

Lipper Long/Short Equity Funds Average8 | | | 10.61 | % | | | -0.69 | % | |

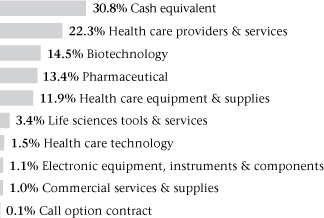

Sector weightings2:

Manager's discussion and analysis

Unrewarding short positions hurt the Turner Medical Sciences Long/Short Fund, Investor Class Shares (TMSFX), which recorded a 1.74% loss for the 12-month period ended September 30. The fund's return lagged that of the S&P 500 Healthcare Index by 31.28 percentage points, the Lipper Long/Short Equity Funds Average by 12.35 percentage points, and the Barclays Capital U.S. Aggregate Bond Index by 6.90 percentage points. The Turner Medical Sciences Long/Short Fund seeks capital appreciation by investing primarily (at least 80% of its net assets) in stocks of companies in the health-care sector; the fund uses a long/short growth strategy in seeking to capture alpha, reduce volatility, and preserve capital in declining markets.

In the fund's long and short positions, stocks in the therapeutic-pharmaceutical and biotechnology industries provided the most extra return. Detracting significantly from performance were long and short positions in the stocks of pharmaceutical, biomedical, medical-instrument, and health-care services firms. Also impeding performance was the fund's position in cash equivalents. Consistent with the fund's investment strategy and given the market's volatility during the period, the fund maintained a significant cash position during the period for defensive purposes. As a result, the fund did not participate in the market advances during the period as much as it would have if it had been more fully invested.

1 Cash equivalent is not being considered a holding for the top five holdings, but is counted in the number of holdings. Top five holdings are based on long positions. The fund composition is subject to change.

2 Percentages based on total investments of long positions.

3 These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. Performance of the Institutional, Investor and Class C Shares will differ due to differences in fees.

4 The inception date of the Turner Medical Sciences Long/Short Fund was February 7, 2011.

5 Fee waivers are in effect; if they had not been in effect, performance would have been lower.

6 The S&P 500 Healthcare Index is an unmanaged index which includes the stocks in the health-care sector of the S&P 500 Index.

7 The Barclays Capital U.S. Aggregate Bond Index (prior to November 2008, the Index was known as the "Lehman Brothers U.S. Aggregate Bond Index") represents an unmanaged diversified portfolio of fixed income securities, including U.S. Treasuries, investment-grade corporate bonds and mortgage-backed and asset-backed securities.

8 Lipper Long/Short Equity Funds Average represents the average annualized total return for all reporting funds in the Lipper Long/Short Equity Fund category.

The Turner Medical Sciences Long/Short Fund is subject to the risks associated with selling securities short. A short sale involves a finite opportunity for appreciation, but a theoretically unlimited risk of loss. The Fund is subject to the risks associated with health care-related companies. Many health care-related companies are smaller and less seasoned than companies in other sectors. Health care-related companies may also be strongly affected by scientific or technological developments and their products may quickly become obsolete. The Fund is subject to risks due to its foreign investments.

10 TURNER FUNDS 2012 ANNUAL REPORT

Fund profile

September 30, 2012

n Ticker symbol TSPEX

Institutional Class Shares

n CUSIP #900297664

Institutional Class Shares

n Top five holdings1

(1) Coca-Cola

(2) Home Depot

(3) Allergan

(4) Air Methods

(5) ProAssurance

n % in five largest holdings 6.0%2

n Number of holdings 4381

n Weighted average market capitalization $26.67 billion

n Net assets $833 million, Institutional Class Shares

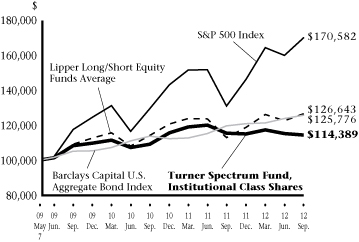

Growth of a $100,000 investment in the

Turner Spectrum Fund, Institutional Class Shares:

May 7, 2009-September 30, 20123,4

Average annual total returns (Periods ended September 30, 2012)

| | | One

year | | Three

years | | Since

inception | |

Turner Spectrum Fund, Institutional Class Shares5 | | | -0.77 | % | | | 1.90 | % | | | 4.03 | % | |

Turner Spectrum Fund, Investor Class Shares5 | | | -0.95 | % | | | 1.66 | % | | | 3.79 | % | |

Turner Spectrum Fund, Class C Shares5 | | | -1.71 | % | | | 0.96 | % | | | 3.40 | % | |

S&P 500 Index7 | | | 30.20 | % | | | 13.20 | % | | | 17.01 | %4 | |

Barclays Capital U.S. Aggregate Bond Index8 | | | 5.16 | % | | | 6.19 | % | | | 6.98 | %4 | |

Lipper Long/Short Equity Funds Average9 | | | 10.61 | % | | | 4.73 | % | | | 7.73 | %4 | |

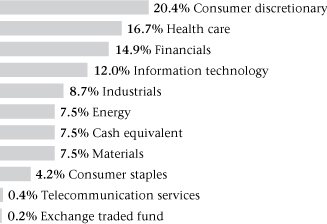

Sector weightings2:

Manager's discussion and analysis

The Turner Spectrum Fund, Institutional Class Shares (TSPEX), lost 0.77% in the 12-month period ended September 30. The fund's return trailed the S&P 500 Index by 30.97 percentage points, the Lipper Long/Short Equity Average by 11.38 percentage points, and the Barclays Capital U.S. Aggregate Bond Index by 5.93 percentage points. The Turner Spectrum Fund seeks capital appreciation through allocating its assets to various investment strategies, each managed by a separate portfolio management team at Turner.

Unproductive short positions were the main drag on the fund's results. Conversely, the consumer-staples sector added the most value. In that sector, long and short positions in cosmetics, beverage, diversified-food, and dairy shares performed best. The sector that detracted the most from results was consumer discretionary, with shares of shoe, multimedia, and home-improvement companies providing the worst returns. The fund kept a conservative net long exposure of 27%, primarily in U.S. stocks.

1 Cash equivalent is not being considered a holding for the top five holdings, but is counted in the number of holdings. Top five holdings are based on long positions. The fund composition is subject to change.

2 Percentages based on total investments of long positions.

3 These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. Performance of the Institutional, Investor and Class C Shares will differ due to differences in fees.

4 The inception date of the Turner Spectrum Fund (Institutional Class Shares and Investor Class Shares) was May 7, 2009. Index returns are based on Institutional Class Shares inception date.

5 Fee waivers are in effect; if they had not been in effect, performance would have been lower.

6 The inception date of the Turner Spectrum Fund (Class C Shares) was July 14, 2009.

7 The S&P 500 Index is a widely-recognized, market value-weighted (higher market value stocks have more influence than lower market value stocks) index of 500 stocks designed to mimic the overall equity market's industry weightings.

8 The Barclays Capital U.S. Aggregate Bond Index (prior to November 2008, the Index was known as the "Lehman Brothers U.S. Aggregate Bond Index") represents an unmanaged diversified portfolio of fixed income securities, including U.S. Treasuries, investment-grade corporate bonds and mortgage-backed and asset-backed securities.

9 Lipper Long/Short Equity Funds Average represents the average annualized total return for all reporting funds in the Lipper Long/Short Equity Fund category.

The Turner Spectrum Fund may focus its investments from time to time on one or more economic sectors. To the extent that it does so, developments affecting companies in that sector or sectors will likely have a magnified effect on the Fund's net asset value and total return. The Fund is subject to the risks associated with selling securities short. A short sale involves a finite opportunity for appreciation, but a theoretically unlimited risk of loss. The smaller capitalization companies the Fund invests in may be more vulnerable to adverse business or economic events than larger, more established companies.

TURNER FUNDS 2012 ANNUAL REPORT 11

Fund profile

September 30, 2012

n Ticker symbol TTLFX

Investor Class Shares

n CUSIP #900297524

Investor Class Shares

n Top five holdings1

(1) Concho Resources

(2) Broadcom, Cl A

(3) Coca-Cola

(4) Allergan

(5) F5 Networks

n % in five largest holdings 14.1%2

n Number of holdings 1101

n Weighted average market capitalization $27.32 billion

n Net assets $5 million, Investor Class Shares

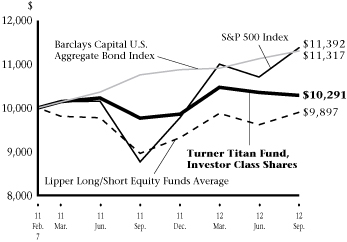

Growth of a $10,000 investment in the

Turner Titan Fund, Investor Class Shares:

February 7, 2011-September 30, 20123,4

Average annual total returns (Periods ended September 30, 2012)

| | | One

year | | Since

inception4 | |

Turner Titan Fund, Institutional Class Shares5 | | | 5.75 | % | | | 2.00 | % | |

Turner Titan Fund, Investor Class Shares5 | | | 5.44 | % | | | 1.76 | % | |

Turner Titan Fund, Class C Shares5 | | | 4.53 | % | | | 0.97 | % | |

S&P 500 Index6 | | | 30.20 | % | | | 8.23 | % | |

Barclays Capital U.S. Aggregate Bond Index7 | | | 5.16 | % | | | 7.76 | % | |

Lipper Long/Short Equity Funds Average8 | | | 10.61 | % | | | -0.69 | % | |

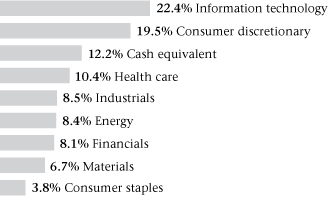

Sector weightings2:

Manager's discussion and analysis

The Turner Titan Fund, Investor Class Shares (TTLFX) gained 5.44% in the 12-month period ended September 30. The fund's return beat the Barclays Capital U.S. Aggregate Bond Index by 0.28 percentage point, but underperformed the S&P 500 Index by 24.76 percentage points and the Lipper Long/Short Equity Funds Average by 5.17 percentage points. The Turner Titan Fund seeks long-term capital appreciation by investing in stocks of companies with primarily large-capitalization ranges across all major industry sectors; the fund uses a long/short strategy in seeking to capture alpha, reduce volatility, and preserve capital in declining markets.

The industrials and consumer-staples sectors added the most value, with long and short positions in electrical-products, diversified-foods, automotive-manufacturing, diversified-machinery, beverage, and cosmetics shares delivering the best results. The greatest detractor from performance was the consumer-discretionary sector, with shares in apparel, advertising, and social-media companies producing subpar returns.

1 Cash equivalent is not being considered a holding for the top five holdings, but is counted in the number of holdings. Top five holdings are based on long positions. The fund composition is subject to change.

2 Percentages based on total investments of long positions.

3 These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. Performance of the Institutional, Investor and Class C Shares will differ due to differences in fees.

4 The inception date of the Turner Titan Fund was February 7, 2011.

5 Fee waivers are in effect; if they had not been in effect, performance would have been lower.

6 The S&P 500 Index is a widely-recognized, market value-weighted (higher market value stocks have more influence than lower market value stocks) index of 500 stocks designed to mimic the overall equity market's industry weightings.

7 The Barclays Capital U.S. Aggregate Bond Index (prior to November 2008, the Index was known as the "Lehman Brothers U.S. Aggregate Bond Index") represents an unmanaged diversified portfolio of fixed income securities, including U.S. Treasuries, investment-grade corporate bonds and mortgage-backed and asset-backed securities.

8 Lipper Long/Short Equity Funds Average represents the average annualized total return for all reporting funds in the Lipper Long/Short Equity Fund category.

Cl — Class

The Turner Titan Fund may focus its investments from time to time on one or more economic sectors. To the extent that it does so, developments affecting companies in that sector or sectors will likely have a magnified effect on the Fund's net asset value and total return. The Fund is subject to the risks associated with selling securities short. A short sale involves a finite opportunity for appreciation, but a theoretically unlimited risk of loss. The smaller capitalization companies the Fund invests in may be more vulnerable to adverse business or economic events than larger, more established companies.

12 TURNER FUNDS 2012 ANNUAL REPORT

Turner All Cap Growth Fund

Fund profile

September 30, 2012

n Ticker symbol TBTBX

n CUSIP #87252R797

n Top five holdings1

(1) Apple

(2) NXP Semiconductors

(3) Broadcom, Cl A

(4) ASML Holding, NY Shares

(5) Cavium

n % in five largest holdings 23.6%2

n Number of holdings 381

n Price/earnings ratio 17.0

n Weighted average market capitalization $70.55 billion

n Net assets $26 million

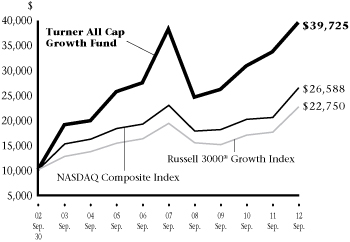

Growth of a $10,000 investment in the

Turner All Cap Growth Fund:

September 30, 2002-September 30, 20123

Average annual total returns (Periods ended September 30, 2012)

| | | One

year | | Three

years | | Five

years | | 10

years | | Since

inception | |

Turner All Cap Growth Fund4 | | | 17.47 | % | | | 14.87 | % | | | 0.67 | % | | | 14.79 | % | | | -0.84 | % | |

Nasdaq Composite Index5 | | | 29.02 | % | | | 13.66 | % | | | 2.90 | % | | | 10.27 | % | | | -1.95 | % | |

Russell 3000® Growth Index6 | | | 29.35 | % | | | 14.69 | % | | | 3.22 | % | | | 8.57 | % | | | -0.72 | % | |

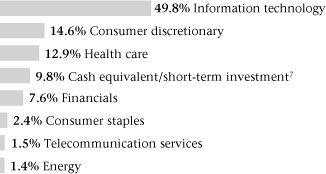

Sector weightings2:

Manager's discussion and analysis

Outperformance in drug holdings helped the Turner All Cap Growth Fund (TBTBX) to gain 17.47% in the 12-month period ended September 30. However, the fund's return lagged that of the Russell 3000® Growth Index by 11.88 percentage points and the Nasdaq Composite Index by 11.55 percentage points.

Three of the fund's seven sector positions outperformed their corresponding index sectors, with a 13% weighting in the health-care sector contributing the most return. The main detractors from performance were the consumer-discretionary, energy, and consumer-staples sectors, an 18% weighting, with shoe, apparel, social-media, coal-mining, oil-exploration, and coffee-roasting shares recording poor relative returns.

1 Cash equivalent and short-term investment are not being considered a holding for the top five holdings, but are counted in the number of holdings. The fund composition is subject to change.

2 Percentages based on total investments.

3 These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. The inception date of the Turner All Cap Growth Fund was June 30, 2000.

4 Fee waivers are in effect; if they had not been in effect, performance would have been lower.

5 The Nasdaq Composite Index includes more than 5,000 domestic and non-U.S. based common stocks listed on the Nasdaq stock market. The index is market-value weighted. This means that each company's security affects the index in proportion to its market value. The market value, the last sale price multiplied by total shares outstanding, is calculated throughout the trading day, and is related to the total value of the index. Because it is so broad-based, the Index is one of the most widely followed and quoted major market indices.

6 The Russell 3000® Growth Index measures the performance of the broad growth segment of the U.S. equity universe. It includes those Russell 3000® companies with higher price-to-book ratios and higher forecasted growth values.

7 Cash equivalent includes short-term investment held as collateral for securities lending activity. Please see Note 10 in Notes to Financial Statements for more detailed information.

Cl — Class

NY — New York

The Turner All Cap Growth Fund may buy and sell securities frequently as part of its investment strategy. The medium capitalization companies in which the Fund invests may be more vulnerable to adverse business or economic events than larger, more established companies.

TURNER FUNDS 2012 ANNUAL REPORT 13

Turner Concentrated Growth Fund

Fund profile

September 30, 2012

n Ticker symbol TTOPX

n CUSIP #87252R862

n Top five holdings1

(1) Apple

(2) Lennar, Cl A

(3) Alexion Pharmaceuticals

(4) CBRE Group

(5) Qualcomm

n % in five largest holdings 28.8%2

n Number of holdings 231

n Price/earnings ratio 15.0

n Weighted average market capitalization $111.37 billion

n Net assets $35 million

Growth of a $10,000 investment in the

Turner Concentrated Growth Fund:

September 30, 2002-September 30, 20123

Average annual total returns (Periods ended September 30, 2012)

| | | One

year | | Three

years | | Five

years | | 10

years | | Since

inception | |

Turner Concentrated Growth Fund4 | | | 16.04 | % | | | 6.65 | % | | | -5.89 | % | | | 6.37 | % | | | 0.49 | % | |

S&P 500 Index5 | | | 30.20 | % | | | 13.20 | % | | | 1.05 | % | | | 8.01 | % | | | 2.23 | % | |

Russell 1000® Growth Index6 | | | 29.19 | % | | | 14.73 | % | | | 3.24 | % | | | 8.41 | % | | | 0.88 | % | |

Sector weightings2:

Manager's discussion and analysis

Sub-par stock selection impaired the performance of the Turner Concentrated Growth Fund (TTOPX) in the 12-month period ended September 30. As a result the fund, which contains a select few stocks that we think have the strongest earnings power and return potential, gained 16.04%. The fund underperformed the S&P 500 Index by 14.16 percentage points and the Russell 1000® Growth Index by 13.15 percentage points.

One of the seven sectors in which the fund was invested beat its corresponding market sector. The health-care sector, a 9% weighting, provided the most extra return. In that sector, pharmaceutical, medical-instrument, and medical-information-system shares performed well. The worst-performing sectors were consumer discretionary and energy, a 16% weighting. Social-media, e-commerce, apparel, automotive, and oil-exploration shares underperformed the most.

On September 7, 2012, the Board of Trustees of the Turner Funds approved the reorganization of Turner Concentrated Growth Fund (the "Concentrated Growth Fund") into Turner Large Growth Fund. In anticipation of the reorganization, the Board has determined to close the Concentrated Growth Fund to new investors effective December 28, 2012.

1 Cash equivalent and short-term investment are not being considered a holding for the top five holdings, but are counted in the number of holdings. The fund composition is subject to change.

2 Percentages based on total investments.

3 These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. The inception date of the Turner Concentrated Growth Fund was June 30,1999.

4 Fee waivers are in effect; if they had not been in effect, performance would have been lower.

5 The S&P 500 Index is a widely-recognized, market value-weighted (higher market value stocks have more influence than lower market value stocks) index of 500 stocks designed to mimic the overall equity market's industry weightings.

6 The Russell 1000® Growth Index measures the performance of the broad growth segment of the U.S. equity universe. It includes those Russell 1000® companies with higher price-to-book ratios and higher forecasted growth values.

7 Cash equivalent includes short-term investment held as collateral for securities lending activity. Please see Note 10 in Notes to Financial Statements for more detailed information.

Cl — Class

The Turner Concentrated Growth Fund is non-diversified, which means that it may invest in the securities of fewer issuers than a diversified fund. As a result, it may be more susceptible to a single adverse economic or regulatory occurrence affecting one or more of these issuers, and may experience increased volatility. The Fund may buy and sell securities frequently as part of its investment strategy.

14 TURNER FUNDS 2012 ANNUAL REPORT

Turner Emerging Growth Fund

Fund profile

September 30, 2012

n Ticker symbol TMCGX

Investor Class Shares

n CUSIP #872524301

Investor Class Shares

n Top five holdings1

(1) Catamaran

(2) Vitamin Shoppe

(3) United Natural Foods

(4) Huron Consulting Group

(5) Air Methods

n % in five largest holdings 12.0%2

n Number of holdings 921

n Price/earnings ratio 16.7

n Weighted average market capitalization $1.71 billion

n Net assets $169 million, Investor Class Shares

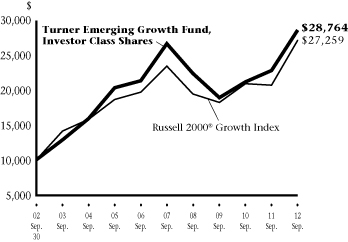

Growth of a $10,000 investment in the

Turner Emerging Growth Fund, Investor Class Shares:

September 30, 2002-September 30, 20123,4

Average annual total returns (Periods ended September 30, 2012)

| | | One

year | | Three

years | | Five

years | | 10

years | | Since

inception | |

Turner Emerging Growth Fund, Institutional Class Shares5 | | | 25.86 | % | | | 15.15 | % | | | — | | | | — | | | | 21.26 | %6 | |

Turner Emerging Growth Fund, Investor Class Shares5 | | | 25.57 | % | | | 14.87 | % | | | 1.43 | % | | | 11.14 | % | | | 17.91 | %4 | |

Russell 2000® Growth Index7 | | | 31.18 | % | | | 14.19 | % | | | 2.96 | % | | | 10.55 | % | | | 3.62 | %4 | |

Sector weightings2:

Manager's discussion and analysis

During the 12-month period ended September 30, the Turner Emerging Growth Fund, Investor Class Shares (TMCGX) gained 25.57%, underperforming the Russell 2000® Growth Index's 31.18% gain by 5.61 percentage points.

All 10 of the fund's sector positions provided positive returns, with four of the positions outperforming their corresponding index sectors. Of those sectors, information technology, an 18% weighting, furnished the greatest outperformance by far; shares in software, semiconductor, and information-services firms did best. The health-care and consumer-discretionary sectors detracted the most from results. In those sectors, which represented a 37% weighting, medical-information-systems, software, biotechnology, footwear, apparel, and hazardous-waste-disposal shares proved disappointing.

1 Cash equivalent and short-term investment are not being considered a holding for the top five holdings, but are counted in the number of holdings. The fund composition is subject to change.

2 Percentages based on total investments.

3 These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. Performance of the Institutional and Investor Class Shares will differ due to differences in fees.

4 The inception date of the Turner Emerging Growth Fund (Investor Class Shares) was February 27, 1998. Index returns are based on Investor Class Shares inception date.

5 Fee waivers are in effect; if they had not been in effect, performance would have been lower.

6 The inception date of the Turner Emerging Growth Fund (Institutional Class Shares) was February 1, 2009.

7 The Russell 2000® Growth Index is a widely-recognized, capitalization-weighted (companies with larger market capitalizations have more influence than those with smaller market capitalizations) index of the 2,000 smallest U.S. companies out of the 3,000 largest U.S. companies with higher growth rates and price-to-book ratios.

8 Cash equivalent includes short-term investment held as collateral for securities lending activity. Please see Note 10 in Notes to Financial Statements for more detailed information.

Amounts designated as "—" are not applicable.

The Turner Emerging Growth Fund is also subject to taxable income and realized capital gains. Shareholder redemptions may force the Fund to sell securities at an inappropriate time, also resulting in realized gains.

TURNER FUNDS 2012 ANNUAL REPORT 15

Fund profile

September 30, 2012

n Ticker symbol TTMEX

Institutional Class Shares

n CUSIP #900297847

Institutional Class Shares

n Top five holdings1

(1) Apple

(2) Coca-Cola

(3) Google, Cl A

(4) Qualcomm

(5) EMC

n % in five largest holdings 23.7%2

n Number of holdings 671

n Price/earnings ratio 15.0

n Weighted average market capitalization $123.78 billion

n Net assets $201 million, Institutional Class Shares

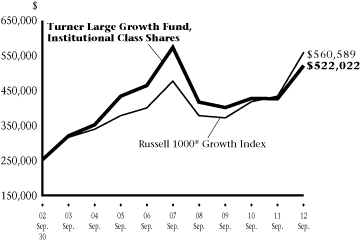

Growth of a $250,000 investment in the

Turner Large Growth Fund, Institutional Class Shares:

September 30, 2002-September 30, 20123,4

Average annual total returns (Periods ended September 30, 2012)

| | | One

year | | Three

years | | Five

years | | 10

years | | Since

inception | |

Turner Large Growth Fund, Institutional Class Shares5 | | | 22.48 | % | | | 9.21 | % | | | -1.95 | % | | | 7.64 | % | | | 2.38 | %4 | |

Turner Large Growth Fund, Investor Class Shares5 | | | 22.26 | % | | | 8.96 | % | | | -2.19 | % | | | — | | | | 2.79 | %6 | |

Russell 1000® Growth Index7 | | | 29.19 | % | | | 14.73 | % | | | 3.24 | % | | | 8.41 | % | | | 2.64 | %4 | |

Sector weightings2:

Manager's discussion and analysis

The Turner Large Growth Fund, Institutional Class Shares (TTMEX) gained 22.48% in the 12-month period ended September 30. However, the fund underperformed its benchmark, the Russell 1000® Growth Index, by 6.71 percentage points.

Four of the eight sectors the fund was invested in beat their corresponding index sectors. Industrials, information technology, and financials, a 52% weighting, provided the most extra return. In those sectors, telecommunication, computer, semiconductor, Internet-application-software, computer-services, investment-management, and transactional-software shares boosted performance. The health-care, consumer-discretionary, and materials sectors, a 29% weighting, detracted the most from performance; shares of generic-pharmaceutical, biomedical, electronic-measurement, social-media, e-commerce, automotive, apparel, gold-mining, packaging, and fertilizer companies provided unfavorable results.

1 Cash equivalent and short-term investment are not being considered a holding for the top five holdings, but are counted in the number of holdings. The fund composition is subject to change.

2 Percentages based on total investments.

3 These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. Performance of the Institutional and Investor Class Shares will differ due to differences in fees.

4 The inception date of the Turner Large Growth Fund (Institutional Class Shares) was February 28, 2001. Index returns are based on Institutional Class Shares inception date.

5 Fee waivers are in effect; if they had not been in effect, performance would have been lower.

6 The inception date of the Turner Large Growth Fund (Investor Class Shares) was August 1, 2005.

7 The Russell 1000® Growth Index measures the performance of the broad growth segment of the U.S. equity universe. It includes those Russell 1000® companies with higher price-to-book ratios and higher forecasted growth values.

8 Cash equivalent includes short-term investment held as collateral for securities lending activity. Please see Note 10 in Notes to Financial Statements for more detailed information.

Amounts designated as "—" are not applicable.

Cl — Class

The Turner Large Growth Fund may buy and sell securities frequently as part of its investment strategy. The Fund is subject to the risk that large capitalization growth stocks may underperform other segments of the equity markets as a whole.

16 TURNER FUNDS 2012 ANNUAL REPORT

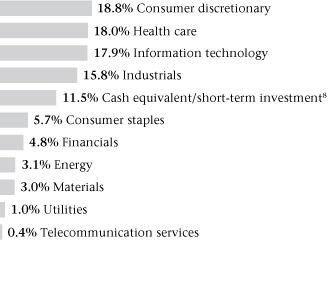

Turner Midcap Growth Fund

Fund profile

September 30, 2012

n Ticker symbol TMGFX

Investor Class Shares

n CUSIP #900297409

Investor Class Shares

n Top five holdings1

(1) Broadcom, Cl A

(2) NXP Semiconductors

(3) Citrix Systems

(4) Concho Resources

(5) F5 Networks

n % in five largest holdings 10.2%2

n Number of holdings 781

n Price/earnings ratio 19.0

n Weighted average market capitalization $9.33 billion

n Net assets $405 million, Investor Class Shares

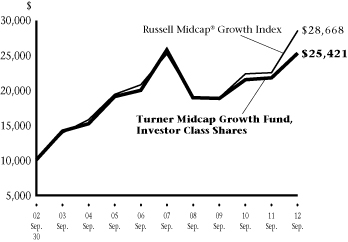

Growth of a $10,000 investment in the

Turner Midcap Growth Fund, Investor Class Shares:

September 30, 2002-September 30, 20123,4

Average annual total returns (Periods ended September 30, 2012)

| | | One

year | | Three

years | | Five

years | | 10

years | | Since

inception | |

Turner Midcap Growth Fund, Institutional Class Shares5 | | | 16.34 | % | | | 10.65 | % | | | — | | | | — | | | | 0.48 | %6 | |

Turner Midcap Growth Fund, Investor Class Shares5 | | | 16.15 | % | | | 10.40 | % | | | -0.38 | % | | | 9.78 | % | | | 9.65 | %4 | |

Turner Midcap Growth Fund, Retirement Class Shares5 | | | 15.83 | % | | | 10.12 | % | | | -0.64 | % | | | 9.39 | % | | | 9.37 | %7 | |

Russell Midcap® Growth Index8 | | | 26.69 | % | | | 14.73 | % | | | 2.54 | % | | | 11.11 | % | | | 7.19 | %4 | |

Sector weightings2:

Manager's discussion and analysis

In the 12-month period ended September 30, the Turner Midcap Growth Fund, Investor Class Shares (TMGFX) advanced 16.15%, underperforming the Russell Midcap® Growth Index by 10.54 percentage points.

A 14% position in financials and consumer staples provided the greatest contribution to the fund's performance. Those two sectors, out of the eight the fund was invested in, beat their corresponding index sectors. Investment-management, transactional-software, commercial-bank, diversified-food, grocery-store, beverage, and vitamin shares generated the best results. The major detractors from performance were the health-care, energy, and consumer-discretionary sectors, which represented 41% of the portfolio. Subpar performers in those sectors included footwear, restaurant, apparel, coal-mining, oil-exploration, generic-pharmaceutical, medical-product, medical-instrument, and diagnostic-equipment shares.

1 Cash equivalent and short-term investment are not being considered a holding for the top five holdings, but are counted in the number of holdings. The fund composition is subject to change.

2 Percentages based on total investments.

3 These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. Performance of the Institutional, Investor and Retirement Class Shares will differ due to differences in fees.

4 The inception date of the Turner Midcap Growth Fund (Investor Class Shares) was October 1, 1996. Index returns are based on Investor Class Shares inception date.

5 Fee waivers are in effect; if they had not been in effect, performance would have been lower.

6 The inception date of the Turner Midcap Growth Fund (Institutional Class Shares) was June 16, 2008.

7 The inception date of the Turner Midcap Growth Fund (Retirement Class Shares) was September 24, 2001.

8 The Russell Midcap® Growth Index is a capitalization-weighted (companies with larger market capitalizations have more influence than those with smaller market capitalizations) index of the 800 smallest U.S. companies out of the 1,000 largest companies with higher growth rates and price-to-book ratios.

9 Cash equivalent includes short-term investment held as collateral for securities lending activity. Please see Note 10 in Notes to Financial Statements for more detailed information.

Cl — Class

Amounts designated as "—" are not applicable.

The Turner Midcap Growth Fund may buy and sell securities frequently as part of its investment strategy. The medium capitalization companies in which the Fund invests may be more vulnerable to adverse business or economic events than larger, more established companies.

TURNER FUNDS 2012 ANNUAL REPORT 17

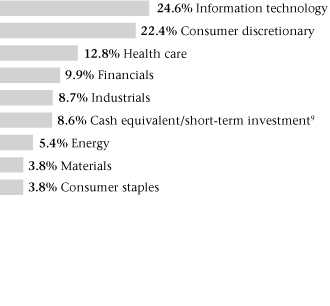

Turner Small Cap Growth Fund

Fund profile

September 30, 2012

n Ticker symbol TSCEX

n CUSIP #900297300

n Top five holdings1

(1) MAXIMUS

(2) Cubist Pharmaceuticals

(3) Boise

(4) Dril-Quip

(5) United Natural Foods

n % in five largest holdings 5.0%2

n Number of holdings 1261

n Price/earnings ratio 17.7

n Weighted average market capitalization $1.88 billion

n Net assets $250 million

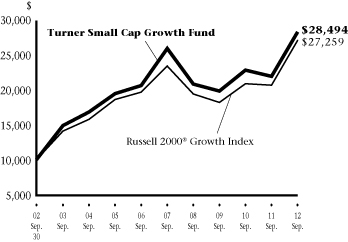

Growth of a $10,000 investment in the

Turner Small Cap Growth Fund:

September 30, 2002-September 30, 20123

Average annual total returns (Periods ended September 30, 2012)

| | | One

year | | Three

years | | Five

years | | 10

years | | Since

inception | |

Turner Small Cap Growth Fund4 | | | 29.21 | % | | | 12.63 | % | | | 1.75 | % | | | 11.04 | % | | | 10.85 | % | |

Russell 2000® Growth Index5 | | | 31.18 | % | | | 14.19 | % | | | 2.96 | % | | | 10.55 | % | | | 5.84 | % | |

Sector weightings2:

Manager's discussion and analysis

Decent stock selection in several major market sectors helped the Turner Small Cap Growth Fund (TSCEX) gain 29.21% in the 12-month period ended September 30. However, the fund lagged its benchmark, the Russell 2000® Index, by 1.97 percentage points.

Six of the fund's sector positions — consumer staples, information technology, industrials, financials, energy, and utilities, a 51% weighting — beat their index counterparts. Consumer staples contributed the most return, with shares in companies involved in diversified food and wholesale food distribution performing the best. But consumer-discretionary and materials shares, an 18% weighting, proved the biggest drag on performance. Apparel, educational-services, footwear, hazardous-waste-disposal, restaurant, filtration, gold-mining, electrical-products, and aluminum stocks recorded subpar results.

1 Cash equivalent and short-term investment are not being considered a holding for the top five holdings, but are counted in the number of holdings. The fund composition is subject to change.

2 Percentages based on total investments.

3 These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. The inception date of the Turner Small Cap Growth Fund was February 7, 1994.

4 Fee waivers are in effect; if they had not been in effect, performance would have been lower.

5 The Russell 2000® Growth Index is a widely-recognized, capitalization-weighted (companies with larger market capitalizations have more influence than those with smaller market capitalizations) index of the 2,000 smallest U.S. companies out of the 3,000 largest U.S. companies with higher growth rates and price-to-book ratios.

6 Cash equivalent includes short-term investment held as collateral for securities lending activity. Please see Note 10 in Notes to Financial Statements for more detailed information.

The Turner Small Cap Growth Fund may buy and sell securities frequently as part of its investment strategy. The smaller capitalization companies the Fund invests in may be more vulnerable to adverse business or economic events than larger, more established companies.

18 TURNER FUNDS 2012 ANNUAL REPORT

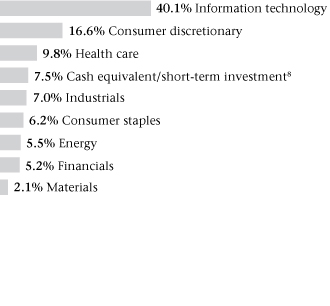

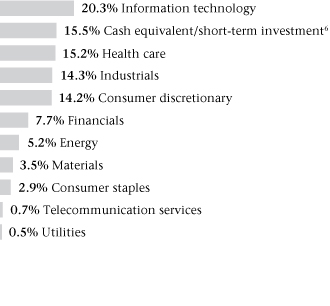

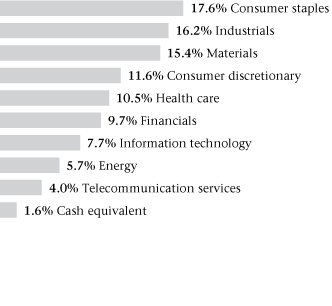

Turner Global Opportunities Fund

Fund profile

September 30, 2012

n Ticker symbol TGLBX

Institutional Class Shares

n CUSIP #900297623

Institutional Class Shares

n Top five holdings1

(1) Apple

(2) ASML Holding, NY Shares

(3) Alexion Pharmaceuticals

(4) NXP Semiconductors

(5) Broadcom, Cl A

n % in five largest holdings 29.3%2

n Number of holdings 281

n Price/earnings ratio 15.5

n Weighted average market capitalization $83.45 billion

n Net assets $2 million, Institutional Class Shares

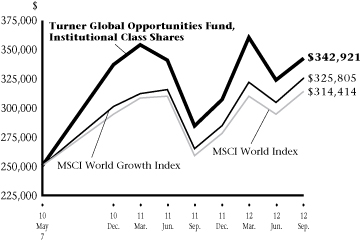

Growth of a $250,000 investment in the

Turner Global Opportunities Fund,

Institutional Class Shares:

May 7, 2010-September 30, 20123

Average annual total returns (Periods ended September 30, 2012)

| | | One

Year | | Since

inception | |

Turner Global Opportunities Fund, Institutional Class Shares4 | | | 20.53 | % | | | 14.07 | % | |

Turner Global Opportunities Fund, Investor Class Shares4 | | | 20.27 | % | | | 13.76 | % | |

MSCI World Growth Index5 | | | 23.52 | % | | | 12.08 | % | |

MSCI World Index6 | | | 22.32 | % | | | 10.63 | % | |

Sector weightings2:

Manager's discussion and analysis

An emphasis on U.S. stocks hurt the Turner Global Opportunities Fund, Institutional Class Shares (TGLBX), which gained 20.53% for the 12-month period ended September 30. The fund lagged its benchmark, the MSCI World Growth Index, by 2.99 percentage points, and the MSCI World Index by 1.79 percentage points.

A larger weighting in foreign stocks would have benefited the fund's results. Four of the fund's seven sector positions outperformed their corresponding index sectors. The best-performing sectors were industrials and health care, which amounted to 13% of holdings. In those sectors, semiconductor, diversified-machinery, biotechnology, and medical-product shares contributed the most extra return. The fund's performance was hurt the most by the energy and consumer-discretionary sectors, with a combined weighting of 22%. Oil, coal-mining, e-commerce, restaurant, and social-media stocks were the biggest laggards.