UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-07527 |

|

Turner Funds |

(Exact name of registrant as specified in charter) |

|

1205 Westlakes Drive, Suite 100 Berwyn, PA | | 19312 |

(Address of principal executive offices) | | (Zip code) |

|

Michael P. Malloy Drinker Biddle & Reath LLP One Logan Square, Suite 2000 Philadelphia, PA 19103 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 1-800-224-6312 | |

|

Date of fiscal year end: | September 30 | |

|

Date of reporting period: | September 30, 2014 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

Long/short equity funds

Turner Medical Sciences Long/Short Fund

Turner Spectrum Fund

Turner Titan Fund

U.S. growth equity funds

Turner Emerging Growth Fund

Turner Large Growth Fund

Turner Midcap Growth Fund

Turner Small Cap Growth Fund

Contents

| | 2 | | | Letter to shareholders | |

| | 4 | | | Total returns of the Turner Funds | |

| 6

| | | Investment review:

Turner Medical Sciences Long/Short Fund | |

| 7

| | | Investment review:

Turner Spectrum Fund | |

| 8

| | | Investment review:

Turner Titan Fund | |

| 9

| | | Investment review:

Turner Emerging Growth Fund | |

| 10

| | | Investment review:

Turner Large Growth Fund | |

| 11

| | | Investment review:

Turner Midcap Growth Fund | |

| 12

| | | Investment review:

Turner Small Cap Growth Fund | |

| | 13 | | | Schedules of investments | |

| | 32 | | | Financial statements | |

| | 46 | | | Notes to financial statements | |

| 55

| | | Report of independent registered public

accounting firm | |

| | 56 | | | Notice to shareholders | |

| | 57 | | | Disclosure of fund expenses | |

| | 59 | | | Trustees and officers of the Trust | |

Turner Funds

As of September 30, 2014, the Turner Funds offered a series of seven mutual funds to individual and institutional investors. The minimum initial investment for Institutional Class Shares in a Turner Fund is $250,000 (except for $100,000 for the Turner Medical Sciences Long/Short Fund, the Turner Spectrum Fund, and the Turner Titan Fund) for regular accounts and $100,000 for individual retirement accounts. The minimum initial investment for Investor Class Shares, Retirement Class Shares and Class C Shares is $2,500 for regular accounts and $2,000 for individual retirement accounts.

Turner Investments, L.P., based in Berwyn, Pennsylvania, serves as the investment adviser for the Turner Funds. Turner Investments, L.P., founded in 1990, manages more than $1.9 billion in stock investments as of September 30, 2014.

Shareholder services

Turner Funds shareholders receive annual and semiannual reports, quarterly account statements, and a quarterly newsletter. Shareholders who have questions about their accounts may call a toll-free telephone number, 1.800.224.6312, may visit our website, www.turnerinvestments.com, or may write to Turner Funds, P.O. Box 219805, Kansas City, Missouri 64121-9805.

TURNER FUNDS 2014 ANNUAL REPORT 1

LETTER TO SHAREHOLDERS (Unaudited)

The stock market concluded a robust 2013 with all global equity indices posting absolute gains for the fourth quarter. Highlighting the quarter was the 10.5% return of the S&P 500 Index, which vaulted that bellwether to a 30% gain for the full year, its best result since 1997. In turn, all global indices — save emerging markets — posted strong gains for the year. For all of the noise in 2013 — the U.S. government shutdown, tapering fears, the threat of military action in Syria, and Cyprus seeking a bailout — markets showed tremendous resiliency. In the face of such macroeconomic concerns investors chose to focus on the prospects of a growing global economy led by the U.S. In fact, U.S. corporate earnings rose for a fourth consecutive year to a record $109 a share for S&P 500 companies (source: S&P Capital IQ). All along the capitalization and style spectra stocks were up dramatically. Large-cap stocks reversed the dominance that small-cap stocks had displayed through the second and third quarters. The Russell 1000 Index posted a return of 10.2%, outpacing the 8.7% return of the Small-Cap Russell 2000 Index, though, for the year, small cap stocks were the clear winners with the Russell 2000 Index up over 38%. From a style perspective, performance was capitalization dependent. Broadly, the Russell 3000 Growth Index outperformed the Russell 3000 Value Index but only on the relative strength of large caps. Both the Russell Midcap Value Index and Russell 2000 Value Index outperformed their growth counterparts. For 2013, growth stocks outpaced value stocks across the market cap spectrum with the largest discrepancy coming from small cap stocks. Here, the Russell 2000 Growth Index gained 43.3% versus the Russell 2000 Value Index gain of 34.5%. All nine sectors of the Russell 3000 Index produced positive returns in the quarter. The best-performing sectors were producer durables and materials/processing while defensive sectors utilities and consumer staples lagged. For the year, the consumer discretionary (+45.9%) and health care (+41.8%) sectors led the way aided by a more confident consumer and the explosive growth in biotech stocks. Utility (+19.6%) stocks were the worst performing sector in this upward moving market as is typically the case in such an environment.

After a heady 2013, equity markets stumbled out of the gate in January and by the first trading day of February, global and US equity markets had plummeted over 5%, as measured by the MSCI World Index and Russell 3000 Index, respectively. Weaker than expected US manufacturing, disappointing data from China that adversely affected emerging markets and worries over deflation in the euro zone all combined to drive investors to safer assets. From that low, however, markets retraced their steps steadily through the rest of February and into March, as the Ukrainian crisis eased and China hinted at stimulus for its slowing economy. Ultimately, global

equity markets generally ended the quarter with positive returns. US markets fared better than non-US markets: the Russell 3000 Index posted a 1.97% return, while the MSCI World ex-USA Index eked out a 0.09% return. Along the capitalization spectrum of US stocks, mid-cap stocks posted the highest returns (Russell Midcap Index up 3.53%), followed by large caps while small caps brought up the rear with a 1.12% gain for the Russell 2000 Index. The flight to perceived safety, mentioned above, seems to have manifested itself across styles in Q1. While growth stocks jumped out well ahead of value stocks early in the quarter, a search for yield and lower volatility in the wake of the late-January swoon benefited value stocks in March, pushing them ahead of growth stocks in all capitalization ranges for the quarter. The 2.92% quarterly return of the Russell 3000 Value Index outstripped that of its growth counterpart by 185 basis points. In March alone, that gap was 343 basis points. Similar style performance patterns played out across all capitalization ranges. Within the mid-cap growth area, the healthcare sector was the strongest performer within the benchmark, while the financial sector posted negative returns.

The second quarter of 2014 began in much the same sluggish fashion as the first quarter. Equity markets continued to show weakness resulting from a 2.9% decline in first quarter GDP results in the U.S. linked to the severe winter weather, continuing weak sentiment towards Japan and escalating unrest in the Ukraine. In May, global equity markets moved higher and volatility across many asset classes declined. Investor fears eased as economic activity improved relative to the previous quarter, some geopolitical risks faded and interest rates remained low. In addition, monetary policy looked to be more accommodative, particularly in Europe with the European Central Bank lowering the main refinancing rate and announcing targeted long-term refinancing operations. With the U.S. manufacturing and labor reports indicating continued recovery and growth, U.S. markets continued the upward trend in June with all U.S. indices positive for the quarter. Along the capitalization spectrum of U.S. stocks, large cap stocks posted the highest returns (Russell 1000 Index up 5.12%) with large cap growth pushing out a few basis points ahead of value. Mid caps closely followed with a 4.97% gain for the Russell Midcap Index while small caps brought up the rear with a 2.05% gain for the Russell 2000 Index. Growth stocks reversed their downward trend at the end of April, making steady gains in May and June and the growth indices ending the quarter in positive territory. Despite these gains, investors still favored value stocks in the small cap to mid cap space as lower quality outperformed. Within mid cap growth the utilities sector was the strongest performer up over 15% with the energy

2 TURNER FUNDS 2014 ANNUAL REPORT

sector a close second up over 12%. All other sectors had modest single digit returns.

U.S. equity markets reached some new highs with the S&P 500 reaching 2000 for the first time in the third quarter of 2014. However, it was not without corrections, some of which were quite sharp. In July, equity markets declined globally due to multiple concerns: the deterioration in the Ukraine-Russia border, the escalation between Israel and Hamas, Argentina's partial bond default, and the uncertainty regarding the U.S. Fed monetary policy. While these concerns continued to depress markets in August, they were offset, at least partially, by positive news out of the U.S. Second quarter GDP was revised upward and housing and manufacturing data indicated improving conditions, which compelled markets to end on a positive note. Fear returned in September with the equity markets declining sharply as long-term interest rates in the U.S. and the U.S. dollar spiked higher, causing concerns over the impact to the European and emerging markets economies and U.S. exports. The results of these seesawing markets for the quarter were relatively flat. U.S. equity markets outperformed their international counterparts with developed markets down -5.88% and emerging markets decreasing -3.49%, as measured by MSCI EAFE and MSCI Emerging Markets, respectively. Along the capitalization spectrum of U.S. stocks, large cap stocks posted the highest returns (Russell 1000 Index up 0.65%) with large cap growth handily beating value by 1.68%. Mid caps ended the quarter in negative territory with a loss of -1.66% with small caps trailing much further behind at -7.36% for the Russell 2000 Index. Growth stocks outperformed value across all market caps. Within the Russell Midcap Growth Index, the energy sector was the weakest performer at -11% giving up all the positive territory gained in the prior quarter.

The uncertainty over the direction and velocity of long-term interest rates in the U.S. is likely to increase volatility in global equity markets over the next few months, as it impacts currency moves and inflation expectations across the globe. Following the typical seasonal correction during September and October, we expect U.S. Equities to resume their moderate appreciation into year-end. Our research has shown that during periods of improving economic activity and moderately rising interest rates, companies in the health care, technology and financial sectors with above average revenue growth and improving margins typically outperform. We believe that equities should continue to be an appealing investment and our active management strategy of focusing on companies with stronger earnings growth than peers may outperform in this lower growth environment.

Sincerely,

Bob Turner

Chairman and Chief Investment Officer

Turner Investments

Past performance is no guarantee of future results. The views expressed are those of Turner Investments as of September 30, 2014, and are not intended as a forecast or investment recommendations. The indexes mentioned are not available for investment.

TURNER FUNDS 2014 ANNUAL REPORT 3

Total returns of the Turner Funds

Through September 30, 2014

Current performance may be lower or higher than the performance data quoted. Please call 1.800.224.6312 or visit our Web site at www.turnerinvestments.com for the most recent month-end performance information.

The performance data quoted represents past performance and the principal value and investment return will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Past performance is no guarantee of future results. Returns shown, unless otherwise indicated, are total returns, with dividends and income reinvested. Returns spanning more than one year are annualized. Fee waivers are in effect; if they had not been in effect, performance would have been lower. The indices mentioned are unmanaged statistical composites of stock-market performance. Investing in an index is not possible.

The holdings and sector weightings of the Turner Funds are subject to change. Forward-earnings projections are not predictors of stock price or investment performance, and do not represent past performance. There is no guarantee that the forward-earnings projections will accurately predict the actual earnings experience of any of the companies involved, and there is no guarantee that owning securities of companies with relatively high price-to-earnings ratios will cause the portfolio to outperform its benchmark or index.

The Turner Funds are distributed by Foreside Fund Services, LLC, Portland, Maine. The investor should consider the investment objectives, risks, charges, and expenses carefully before investing. This and other information can be found in the prospectus. A free prospectus, which contains detailed information, including fees and expenses, and the risks associated with investing in these Funds, can be obtained by calling 1.800.224.6312. Read the prospectus carefully before investing.

Fund name/Index | | Six

months* | | Year

to

date* | | One

year | | Three

years | | Five

years | | 10

years | | (Annualized)

Since

inception | | Total

net assets

($mil) | |

Turner Medical Sciences

Long/Short Fund(1) —

Institutional Class Shares | | | 5.13 | % | | | 13.35 | % | | | 19.08 | % | | | 9.91 | % | | | n/a | | | | n/a | | | | 9.11 | % | | $ | 27.88 | | |

Investor Class Shares | | | 5.08 | | | | 13.27 | | | | 18.83 | | | | 9.68 | | | | n/a | | | | n/a | | | | 8.89 | | | | 5.97 | | |

Class C Shares | | | 4.63 | | | | 12.60 | | | | 17.93 | | | | 8.84 | | | | n/a | | | | n/a | | | | 8.09 | | | | 2.93 | | |

S&P 500 Health Care Index | | | 10.21 | | | | 16.62 | | | | 28.43 | | | | 28.84 | | | | n/a | | | | n/a | | | | 23.19 | | | | | | |

Barclays Capital U.S. Aggregate

Bond Index | | | 2.21 | | | | 4.10 | | | | 3.96 | | | | 2.43 | | | | n/a | | | | n/a | | | | 4.05 | | | | | | |

Lipper Long/Short Equity Funds

Average | | | 0.74 | | | | 1.39 | | | | 5.74 | | | | 8.18 | | | | n/a | | | | n/a | | | | 4.25 | | | | | | |

Inception date: 2/7/11 | |

Turner Spectrum Fund(1) —

Institutional Class Shares | | | 0.08 | | | | 2.22 | | | | 4.55 | | | | 2.88 | | | | 3.03 | % | | | n/a | | | | 4.30 | | | | 120.03 | | |

Investor Class Shares | | | -0.08 | | | | 1.99 | | | | 4.25 | | | | 2.61 | | | | 2.76 | | | | n/a | | | | 4.03 | | | | 15.63 | | |

Class C Shares(2) | | | -0.44 | | | | 1.34 | | | | 3.46 | | | | 1.85 | | | | 2.03 | | | | n/a | | | | 3.50 | | | | 2.92 | | |

S&P 500 Index | | | 6.42 | | | | 8.34 | | | | 19.73 | | | | 22.99 | | | | 15.70 | | | | n/a | | | | 17.94 | | | | | | |

Barclays Capital U.S. Aggregate

Bond Index | | | 2.21 | | | | 4.10 | | | | 3.96 | | | | 2.43 | | | | 4.12 | | | | n/a | | | | 4.76 | | | | | | |

Lipper Long/Short Equity Funds

Average | | | 0.74 | | | | 1.39 | | | | 5.74 | | | | 8.18 | | | | 5.44 | | | | n/a | | | | 7.46 | | | | | | |

Inception date: 5/7/09 | |

Turner Titan Fund(1) —

Institutional Class Shares | | | 2.70 | | | | 4.96 | | | | 10.00 | | | | 6.36 | | | | n/a | | | | n/a | | | | 4.53 | | | | 9.63 | | |

Investor Class Shares | | | 2.44 | | | | 4.72 | | | | 9.68 | | | | 6.05 | | | | n/a | | | | n/a | | | | 4.26 | | | | 0.55 | | |

Class C Shares | | | 2.14 | | | | 4.17 | | | | 8.90 | | | | 5.20 | | | | n/a | | | | n/a | | | | 3.45 | | | | 0.26 | | |

S&P 500 Index | | | 6.42 | | | | 8.34 | | | | 19.73 | | | | 22.99 | | | | n/a | | | | n/a | | | | 14.11 | | | | | | |

Barclays Capital U.S. Aggregate

Bond Index | | | 2.21 | | | | 4.10 | | | | 3.96 | | | | 2.43 | | | | n/a | | | | n/a | | | | 4.05 | | | | | | |

Lipper Long/Short Equity Funds

Average | | | 0.74 | | | | 1.39 | | | | 5.74 | | | | 8.18 | | | | n/a | | | | n/a | | | | 4.25 | | | | | | |

Inception date: 2/7/11 | |

4 TURNER FUNDS 2014 ANNUAL REPORT

PERFORMANCE (continued) (Unaudited)

Fund name/Index | | Six

months* | | Year

to

date* | | One

year | | Three

years | | Five

years | | 10

years | | (Annualized)

Since

inception | | Total

net assets

($mil) | |

Turner Emerging

Growth Fund(1) —

Institutional Class Shares(3) | | | -7.80 | % | | | -7.86 | % | | | -0.76 | % | | | 18.43 | % | | | 15.04 | % | | | n/a | | | | 18.97 | % | | $ | 25.91 | | |

Investor Class Shares | | | -7.91 | | | | -8.03 | | | | -1.00 | | | | 18.14 | | | | 14.76 | | | | 9.00 | % | | | 17.51 | | | | 116.86 | | |

Russell 2000® Growth Index | | | -4.51 | | | | -4.05 | | | | 3.79 | | | | 21.91 | | | | 15.51 | | | | 9.03 | | | | 5.20 | | | | | | |

Inception date: 2/27/98 | |

Turner Large Growth Fund —

Institutional Class Shares | | | 4.31 | | | | 3.74 | | | | 17.03 | | | | 18.08 | | | | 11.85 | | | | 7.16 | | | | 4.27 | | | | 17.43 | | |

Investor Class Shares(4) | | | 4.17 | | | | 3.53 | | | | 16.77 | | | | 17.80 | | | | 11.58 | | | | n/a | | | | 5.47 | | | | 20.52 | | |

Russell 1000® Growth Index | | | 6.69 | | | | 7.89 | | | | 19.15 | | | | 22.45 | | | | 16.50 | | | | 8.94 | | | | 4.93 | | | | | | |

Inception date: 2/28/01 | |

Turner Midcap Growth Fund(1) —

Institutional Class Shares(5) | | | -0.34 | | | | 4.16 | | | | 12.25 | | | | 17.64 | | | | 13.65 | | | | n/a | | | | 5.83 | | | | 46.25 | | |

Investor Class Shares | | | -0.53 | | | | 3.90 | | | | 11.88 | | | | 17.33 | | | | 13.36 | | | | 8.78 | | | | 10.54 | | | | 187.97 | | |

Retirement Class Shares(6) | | | -0.53 | | | | 3.83 | | | | 11.74 | | | | 17.12 | | | | 13.11 | | | | 8.47 | | | | 7.92 | | | | 4.67 | | |

Russell Midcap® Growth Index | | | 3.61 | | | | 5.73 | | | | 14.43 | | | | 22.74 | | | | 17.12 | | | | 10.24 | | | | 8.62 | | | | | | |

Inception date: 10/1/96 | |

Turner Small Cap Growth Fund(1) | | | -2.95 | | | | -4.69 | | | | 0.99 | | | | 20.41 | | | | 14.06 | | | | 8.58 | | | | 11.36 | | | | 130.09 | | |

Russell 2000® Growth Index | | | -4.51 | | | | -4.05 | | | | 3.79 | | | | 21.91 | | | | 15.51 | | | | 9.03 | | | | 6.92 | | | | |

Inception date: 2/7/94 | |

(1) Investing in technology and science companies and small- and mid-capitalization companies may subject the Funds to specific inherent risks, including above-average price fluctuations.

(2) Commenced operations on July 14, 2009.

(3) Commenced operations on February 1, 2009.

(4) Commenced operations on August 1, 2005.

(5) Commenced operations on June 16, 2008.

(6) Commenced operations on September 24, 2001.

* Returns of less than one year are cumulative, and not annualized.

Expense Ratio†

| | | Gross

expense

ratio | | Net

expense

ratio* | |

Turner Medical Sciences

Long/Short Fund | |

Institutional Class Shares | | | 3.01 | % | | | 1.95 | % | |

Investor Class Shares | | | 3.26 | % | | | 2.20 | % | |

Class C Shares | | | 4.01 | % | | | 2.95 | % | |

Turner Spectrum Fund | |

Institutional Class Shares | | | 2.77 | % | | | 1.95 | % | |

Investor Class Shares | | | 3.02 | % | | | 2.20 | % | |

Class C Shares | | | 3.77 | % | | | 2.95 | % | |

Turner Titan Fund | |

Institutional Class Shares | | | 2.42 | % | | | 1.95 | % | |

Investor Class Shares | | | 2.67 | % | | | 2.20 | % | |

Class C Shares | | | 3.42 | % | | | 2.95 | % | |

| | | Gross

expense

ratio | | Net

expense

ratio* | |

Turner Emerging Growth Fund | |

Institutional Class Shares | | | 1.31 | % | | | 1.15 | % | |

Investor Class Shares | | | 1.56 | % | | | 1.40 | % | |

Turner Large Growth Fund | |

Institutional Class Shares | | | 0.96 | % | | | 0.69 | % | |

Investor Class Shares | | | 1.21 | % | | | 0.94 | % | |

Turner Midcap Growth Fund | |

Institutional Class Shares | | | 1.08 | % | | | 0.93 | % | |

Investor Class Shares | | | 1.33 | % | | | 1.18 | % | |

Retirement Class Shares | | | 1.58 | % | | | 1.43 | % | |

Turner Small Cap Growth Fund | |

Investor Class Shares | | | 1.56 | % | | | 1.25 | % | |

† These expense ratios are based on the most recent prospectus and may differ from those shown in the financial highlights.

* Net expense ratio reflects contractual waivers of certain fees and/or expense reimbursements. Turner may discontinue this arrangement at any time after January 31, 2015.

TURNER FUNDS 2014 ANNUAL REPORT 5

INVESTMENT REVIEW (Unaudited)

Turner Medical Sciences Long/Short Fund

Fund profile

September 30, 2014

n Ticker symbol TMSFX

Investor Class Shares

n CUSIP #900297557

Investor Class Shares

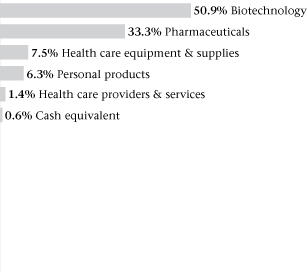

n Top five holdings1

(1) Horizon Pharma

(2) AMAG Pharmaceuticals

(3) Flamel Technologies SA ADR

(4) IGI Laboratories

(5) Chimerix

n % in five largest holdings 36.6%1,2

n Number of holdings 611

n Net assets $5.97 million, Investor Class Shares

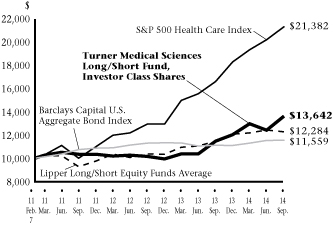

Growth of a $10,000 investment in the

Turner Medical Sciences Long/Short Fund,

Investor Class Shares:

February 7, 2011-September 30, 20143,4

Average annual total returns (Periods ended September 30, 2014)3

| | | One

year | | Three

years | | Since

inception4 | |

Turner Medical Sciences Long/Short Fund, Institutional Class Shares5 | | | 19.08 | % | | | 9.91 | % | | | 9.11 | % | |

Turner Medical Sciences Long/Short Fund, Investor Class Shares5 | | | 18.83 | % | | | 9.68 | % | | | 8.89 | % | |

Turner Medical Sciences Long/Short Fund, Class C Shares5 | | | 17.93 | % | | | 8.84 | % | | | 8.09 | % | |

S&P 500 Health Care Index6 | | | 28.43 | % | | | 28.84 | % | | | 23.19 | % | |

Barclays Capital U.S. Aggregate Bond Index7 | | | 3.96 | % | | | 2.43 | % | | | 4.05 | % | |

Lipper Long/Short Equity Funds Average8 | | | 5.74 | % | | | 8.18 | % | | | 4.25 | % | |

Sector weightings1:

Manager's discussion and analysis

The Turner Medical Sciences Long/Short Fund generated a positive absolute return for the 12-month period ended September 30, 2014. During the reporting period, the Fund outperformed the Barclays Capital U.S. Aggregate Bond Index and the Lipper Long/Short Equity Funds Average but underperformed the S&P 500 Health Care Index. The Fund invests primarily (at least 80% of its net assets) in stocks of companies engaged in the healthcare sector using a long/short growth strategy in seeking to capture alpha, reduce volatility, and preserve capital in declining markets.

During the reporting period, top contributors to performance were long and short positions in the pharmaceutical, household personal care and biotechnology industries. Over the same period, detractors to performance were long and short positions in medical specialty, biotechnology and pharmaceutical companies.

1 Cash equivalent is not being considered a holding for the top five holdings, but is counted in the number of holdings. Top five holdings are based on long positions. The fund composition is subject to change.

2 Percentages based on total investments of long positions.

3 These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. Performance of the Institutional, Investor and Class C Shares will differ due to differences in fees.

4 The inception date of the Turner Medical Sciences Long/Short Fund was February 7, 2011.

5 Fee waivers are in effect; if they had not been in effect, performance would have been lower.

6 The S&P 500 Health Care Index is an unmanaged index which includes the stocks in the health-care sector of the S&P 500 Index.

7 The Barclays Capital U.S. Aggregate Bond Index represents an unmanaged diversified portfolio of fixed income securities, including U.S. Treasuries, investment-grade corporate bonds and mortgage-backed and asset-backed securities.

8 Lipper Long/Short Equity Funds Average represents the average annualized total return for all reporting funds in the Lipper Long/Short Equity Fund category.

ADR — American Depositary Receipt

The Turner Medical Sciences Long/Short Fund is subject to the risks associated with selling securities short. A short sale involves a finite opportunity for appreciation, but a theoretically unlimited risk of loss. The fund is subject to the risks associated with health care-related companies. Many health care-related companies are smaller and less seasoned than companies in other sectors. Health care-related companies may also be strongly affected by scientific or technological developments and their products may quickly become obsolete. The fund is subject to risks due to its foreign investments. The fund is also subject to taxable income and realized capital gains. Shareholder redemptions may force the fund to sell securities at an inappropriate time, also resulting in realized gains. The fund may purchase and write options to hedge against market movements.

6 TURNER FUNDS 2014 ANNUAL REPORT

INVESTMENT REVIEW (Unaudited)

Fund profile

September 30, 2014

n Ticker symbol TSPEX

Institutional Class Shares

n CUSIP #900297664

Institutional Class Shares

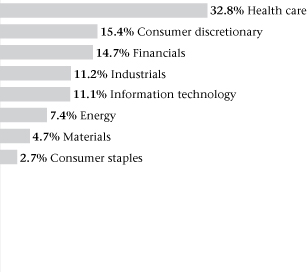

n Top five holdings1

(1) Horizon Pharma

(2) AMAG Pharmaceuticals

(3) Flamel Technologies SA ADR

(4) Atlas Mara CO-Nvest

(5) IGI Laboratories

n % in five largest holdings 10.9%1,2

n Number of holdings 2931

n Net assets $120.03 million, Institutional Class Shares

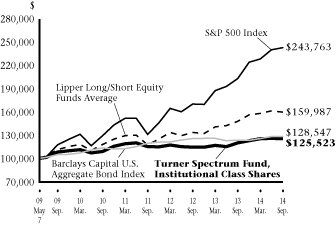

Growth of a $100,000 investment in the

Turner Spectrum Fund, Institutional Class Shares:

May 7, 2009-September 30, 20143,4

Average annual total returns (Periods ended September 30, 2014)3

| | | One

year | | Three

years | | Five

years | | Since

inception | |

Turner Spectrum Fund, Institutional Class Shares5 | | | 4.55 | % | | | 2.88 | % | | | 3.03 | % | | | 4.30 | %4 | |

Turner Spectrum Fund, Investor Class Shares5 | | | 4.25 | % | | | 2.61 | % | | | 2.76 | % | | | 4.03 | %4 | |

Turner Spectrum Fund, Class C Shares5 | | | 3.46 | % | | | 1.85 | % | | | 2.03 | % | | | 3.50 | %6 | |

S&P 500 Index7 | | | 19.73 | % | | | 22.99 | % | | | 15.70 | % | | | 17.94 | % | |

Barclays Capital U.S. Aggregate Bond Index8 | | | 3.96 | % | | | 2.43 | % | | | 4.12 | % | | | 4.76 | % | |

Lipper Long/Short Equity Funds Average9 | | | 5.74 | % | | | 8.18 | % | | | 5.44 | % | | | 7.46 | % | |

Sector weightings1:

Manager's discussion and analysis

The Turner Spectrum Fund generated a positive absolute return for the 12-month period ended September 30, 2014. During the reporting period, the Fund outperformed the Barclays Capital U.S. Aggregate Bond Index but underperformed both the S&P 500 Index and the Lipper Long/Short Equity Funds Average. The Turner Spectrum Fund is a multi-manager mutual fund that seeks long-term capital appreciation through investments in a number of long/short equity strategies offered by Turner Investments.

During the reporting period, top contributors to performance were in the energy, health care and producer durable sectors. The strongest returns came from biotechnology, oil & gas production and pharmaceutical companies. Financial, technology and consumer discretionary sectors all detracted from returns on a relative basis versus the S&P 500 benchmark.

1 Cash equivalent is not being considered a holding for the top five holdings, but is counted in the number of holdings. Top five holdings are based on long positions. The fund composition is subject to change.

2 Percentages based on total investments of long positions.

3 These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. Performance of the Institutional, Investor and Class C Shares will differ due to differences in fees.

4 The inception date of the Turner Spectrum Fund (Institutional Class Shares and Investor Class Shares) was May 7, 2009. Index returns are based on Institutional Class Shares inception date.

5 Fee waivers are in effect; if they had not been in effect, performance would have been lower.

6 The inception date of the Turner Spectrum Fund (Class C Shares) was July 14, 2009.

7 The S&P 500 Index is a widely-recognized, market value-weighted (higher market value stocks have more influence than lower market value stocks) index of 500 stocks designed to mimic the overall equity market's industry weightings.

8 The Barclays Capital U.S. Aggregate Bond Index represents an unmanaged diversified portfolio of fixed income securities, including U.S. Treasuries, investment-grade corporate bonds and mortgage-backed and asset-backed securities.

9 Lipper Long/Short Equity Funds Average represents the average annualized total return for all reporting funds in the Lipper Long/Short Equity Fund category.

ADR — American Depositary Receipt

The Turner Spectrum Fund may focus its investments from time to time on one or more economic sectors. To the extent that it does so, developments affecting companies in that sector or sectors will likely have a magnified effect on the fund's net asset value and total return. The fund is subject to the risks associated with selling securities short. A short sale involves a finite opportunity for appreciation, but a theoretically unlimited risk of loss. The fund is subject to risks due to its foreign investments. The fund is also subject to taxable income and realized capital gains. Shareholder redemptions may force the fund to sell securities at an inappropriate time, also resulting in realized gains. The fund may purchase and write options to hedge against market movements.

TURNER FUNDS 2014 ANNUAL REPORT 7

INVESTMENT REVIEW (Unaudited)

Fund profile

September 30, 2014

n Ticker symbol TTLFX

Investor Class Shares

n CUSIP #900297524

Investor Class Shares

n Top five holdings1

(1) Union Pacific

(2) Biogen Idec

(3) McKesson

(4) Facebook, Cl A

(5) Johnson & Johnson

n % in five largest holdings 17.2%1,2

n Number of holdings 1021

n Net assets $0.05 million, Investor Class Shares

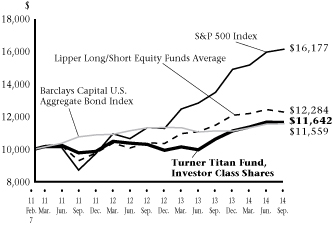

Growth of a $10,000 investment in the

Turner Titan Fund, Investor Class Shares:

February 7, 2011-September 30, 20143,4

Average annual total returns (Periods ended September 30, 2014)3

| | | One

year | | Three

years | | Since

inception4 | |

Turner Titan Fund, Institutional Class Shares5 | | | 10.00 | % | | | 6.36 | % | | | 4.53 | % | |

Turner Titan Fund, Investor Class Shares5 | | | 9.68 | % | | | 6.05 | % | | | 4.26 | % | |

Turner Titan Fund, Class C Shares5 | | | 8.90 | % | | | 5.20 | % | | | 3.45 | % | |

S&P 500 Index6 | | | 19.73 | % | | | 22.99 | % | | | 14.11 | % | |

Barclays Capital U.S. Aggregate Bond Index7 | | | 3.96 | % | | | 2.43 | % | | | 4.05 | % | |

Lipper Long/Short Equity Funds Average8 | | | 5.74 | % | | | 8.18 | % | | | 4.25 | % | |

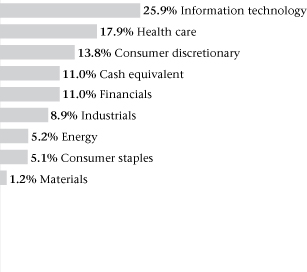

Sector weightings1:

Manager's discussion and analysis

The Turner Titan Fund generated a positive absolute return for the 12-month period ended September 30, 2014. During the reporting period, the Fund outperformed two of its performance benchmarks, the Barclays Capital U.S. Aggregate Bond Index and the Lipper Long/Short Equity Funds Average but trailed the return of the S&P 500 Index. The Turner Titan Fund invests in stocks of companies with primarily large capitalization ranges across all major industry sectors using a long/short strategy in seeking to capture alpha, reduce volatility, and preserve capital in declining markets.

During the reporting period, top contributors to performance were long and short positions in technology, energy and consumer discretionary sectors. The financial and materials sectors were relative drags on performance versus the S&P 500 benchmark for the 12-month period ended September 30, 2014.

1 Cash equivalent is not being considered a holding for the top five holdings, but is counted in the number of holdings. Top five holdings are based on long positions. The fund composition is subject to change.

2 Percentages based on total investments of long positions.

3 These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. Performance of the Institutional, Investor and Class C Shares will differ due to differences in fees.

4 The inception date of the Turner Titan Fund was February 7, 2011.

5 Fee waivers are in effect; if they had not been in effect, performance would have been lower.

6 The S&P 500 Index is a widely-recognized, market value-weighted (higher market value stocks have more influence than lower market value stocks) index of 500 stocks designed to mimic the overall equity market's industry weightings.

7 The Barclays Capital U.S. Aggregate Bond Index represents an unmanaged diversified portfolio of fixed income securities, including U.S. Treasuries, investment-grade corporate bonds and mortgage-backed and asset-backed securities.

8 Lipper Long/Short Equity Funds Average represents the average annualized total return for all reporting funds in the Lipper Long/Short Equity Fund category.

Cl — Class

The Turner Titan Fund may focus its investments from time to time on one or more economic sectors. To the extent that it does so, developments affecting companies in that sector or sectors will likely have a magnified effect on the fund's net asset value and total return. The fund is subject to the risks associated with selling securities short. A short sale involves a finite opportunity for appreciation, but a theoretically unlimited risk of loss. The fund is subject to risks due to its foreign investments. The fund is also subject to taxable income and realized capital gains. Shareholder redemptions may force the fund to sell securities at an inappropriate time, also resulting in realized gains.

8 TURNER FUNDS 2014 ANNUAL REPORT

INVESTMENT REVIEW (Unaudited)

Turner Emerging Growth Fund

Fund profile

September 30, 2014

n Ticker symbol TMCGX

Investor Class Shares

n CUSIP #872524301

Investor Class Shares

n Top five holdings1

(1) Proofpoint

(2) Ambarella

(3) Monolithic Power Systems

(4) Huron Consulting Group

(5) Electronics for Imaging

n % in five largest holdings 12.9%1,2

n Number of holdings 841

n Net assets $116.86 million, Investor Class Shares

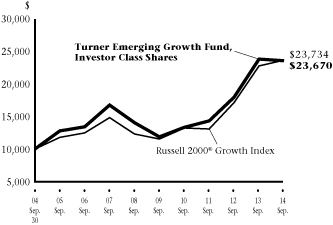

Growth of a $10,000 investment in the

Turner Emerging Growth Fund, Investor Class Shares:

September 30, 2004-September 30, 20143,4

Average annual total returns (Periods ended September 30, 2014)3

| | | One

year | | Three

years | | Five

years | | Ten

years | | Since

inception | |

Turner Emerging Growth Fund, Institutional Class Shares5 | | | -0.76 | % | | | 18.43 | % | | | 15.04 | % | | | — | | | | 18.97 | %6 | |

Turner Emerging Growth Fund, Investor Class Shares5 | | | -1.00 | % | | | 18.14 | % | | | 14.76 | % | | | 9.00 | % | | | 17.51 | %4 | |

Russell 2000® Growth Index7 | | | 3.79 | % | | | 21.91 | % | | | 15.51 | % | | | 9.03 | % | | | 5.20 | % | |

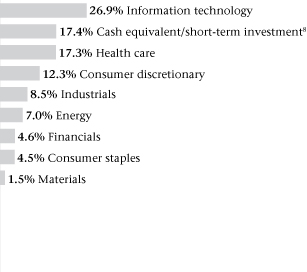

Sector weightings1:

Manager's discussion and analysis

During the 12-month period ended September 30, 2014, the Turner Emerging Growth Fund trailed the returns of the benchmark Russell 2000® Growth Index.

The two strongest returning sectors were health care and materials with those sectors outperforming their corresponding index sectors. Within those sectors, shares in the biotech, pharmaceuticals and pulp & paper industries performed the best. Consumer discretionary and consumer staple stocks detracted the most from relative returns. In those sectors, internet software, retail apparel and food distributors posted the worst returns for the year.

1 Cash equivalent and short-term investment are not being considered a holding for the top five holdings, but are counted in the number of holdings. The fund composition is subject to change.

2 Percentages based on total investments.

3 These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. Performance of the Institutional and Investor Class Shares will differ due to differences in fees.

4 The inception date of the Turner Emerging Growth Fund (Investor Class Shares) was February 27, 1998. Index returns are based on Investor Class Shares inception date.

5 Fee waivers are in effect; if they had not been in effect, performance would have been lower.

6 The inception date of the Turner Emerging Growth Fund (Institutional Class Shares) was February 1, 2009.

7 The Russell 2000® Growth Index is a widely-recognized, capitalization-weighted (companies with larger market capitalizations have more influence than those with smaller market capitalizations) index of the 2,000 smallest U.S. companies out of the 3,000 largest U.S. companies with higher growth rates and price-to-book ratios.

8 Cash equivalent includes short-term investment held as collateral for securities lending activity. Please see Note 8 in Notes to Financial Statements for more detailed information.

Amounts designated as " — " are not applicable.

The Turner Emerging Growth Fund may buy and sell securities frequently as part of its investment strategy. The smaller capitalization companies

the fund invests in may be more vulnerable to adverse business or economic events than larger, more established companies. The fund is subject to risks due to its foreign investments. The fund is also subject to taxable income and realized capital gains. Shareholder redemptions may force the fund to sell securities at an inappropriate time, also resulting in realized gains.

TURNER FUNDS 2014 ANNUAL REPORT 9

INVESTMENT REVIEW (Unaudited)

Fund profile

September 30, 2014

n Ticker symbol TTMEX

Institutional Class Shares

n CUSIP #900297847

Institutional Class Shares

n Top five holdings1

(1) Apple

(2) Google, Cl A

(3) Facebook, Cl A

(4) McKesson

(5) Comcast, Cl A

n % in five largest holdings 20.1%1,2

n Number of holdings 641

n Net assets $17.43 million, Institutional Class Shares

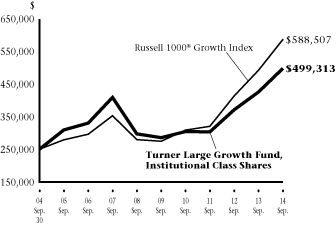

Growth of a $250,000 investment in the

Turner Large Growth Fund, Institutional Class Shares:

September 30, 2004-September 30, 20143,4

Average annual total returns (Periods ended September 30, 2014)3

| | | One

year | | Three

years | | Five

years | | Ten

years | | Since

inception | |

Turner Large Growth Fund, Institutional Class Shares5 | | | 17.03 | % | | | 18.08 | % | | | 11.85 | % | | | 7.16 | % | | | 4.27 | %4 | |

Turner Large Growth Fund, Investor Class Shares5 | | | 16.77 | % | | | 17.80 | % | | | 11.58 | % | | | — | | | | 5.47 | %6 | |

Russell 1000® Growth Index7 | | | 19.15 | % | | | 22.45 | % | | | 16.50 | % | | | 8.94 | % | | | 4.93 | %4 | |

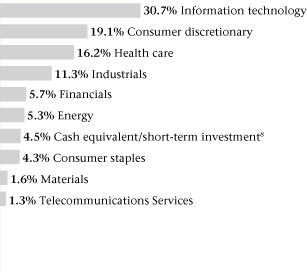

Sector weightings1:

Manager's discussion and analysis

During the 12-month period ended September 30, 2014, the Turner Large Growth Fund trailed the returns of the benchmark Russell 1000® Growth Index.

Regarding sector attribution, the consumer discretionary and producer durables contributed the most versus the corresponding index sectors. Within those sectors, internet software services, restaurants and railroads performed the best. An underweight position in the health care sector hurt relative returns versus the benchmark due to high returns in the biotech and pharmaceutical industries. The financial and consumer staple sectors also detracted from relative returns.

1 Cash equivalent and short-term investment are not being considered a holding for the top five holdings, but are counted in the number of holdings. The fund composition is subject to change.

2 Percentages based on total investments.

3 These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. Performance of the Institutional and Investor Class Shares will differ due to differences in fees.

4 The inception date of the Turner Large Growth Fund (Institutional Class Shares) was February 28, 2001. Index returns are based on Institutional Class Shares inception date.

5 Fee waivers are in effect; if they had not been in effect, performance would have been lower.

6 The inception date of the Turner Large Growth Fund (Investor Class Shares) was August 1, 2005.

7 The Russell 1000® Growth Index measures the performance of the broad growth segment of the U.S. equity universe. It includes those Russell 1000® companies with higher price-to-book ratios and higher forecasted growth values.

8 Cash equivalent includes short-term investment held as collateral for securities lending activity. Please see Note 8 in Notes to Financial Statements for more detailed information.

Amounts designated as "—" are not applicable.

Cl — Class

The Turner Large Growth Fund may buy and sell securities frequently as part of its investment strategy. The fund is subject to the risk that large capitalization growth stocks may underperform other segments of the equity markets as a whole. The fund is subject to risks due to its foreign investments. The fund is also subject to taxable income and realized capital gains. Shareholder redemptions may force the fund to sell securities at an inappropriate time, also resulting in realized gains.

10 TURNER FUNDS 2014 ANNUAL REPORT

INVESTMENT REVIEW (Unaudited)

Turner Midcap Growth Fund

Fund profile

September 30, 2014

n Ticker symbol TMGFX

Investor Class Shares

n CUSIP #900297409

Investor Class Shares

n Top five holdings1

(1) NXP Semiconductors

(2) Alexion Pharmaceuticals

(3) Cavium

(4) Avago Technologies

(5) WhiteWave Foods, Cl A

n % in five largest holdings 16.2%1,2

n Number of holdings 571

n Net assets $187.97 million, Investor Class Shares

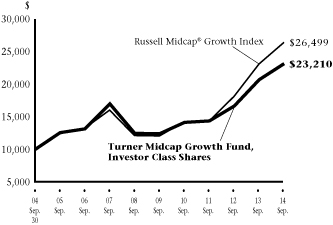

Growth of a $10,000 investment in the

Turner Midcap Growth Fund, Investor Class Shares:

September 30, 2004-September 30, 20143,4

Average annual total returns (Periods ended September 30, 2014)3

| | | One

year | | Three

years | | Five

years | | Ten

years | | Since

inception | |

Turner Midcap Growth Fund, Institutional Class Shares5 | | | 12.25 | % | | | 17.64 | % | | | 13.65 | % | | | — | | | | 5.83 | %6 | |

Turner Midcap Growth Fund, Investor Class Shares5 | | | 11.88 | % | | | 17.33 | % | | | 13.36 | % | | | 8.78 | % | | | 10.54 | %4 | |

Turner Midcap Growth Fund, Retirement Class Shares5 | | | 11.74 | % | | | 17.12 | % | | | 13.11 | % | | | 8.47 | % | | | 7.92 | %7 | |

Russell Midcap® Growth Index8 | | | 14.43 | % | | | 22.74 | % | | | 17.12 | % | | | 10.24 | % | | | 8.62 | %4 | |

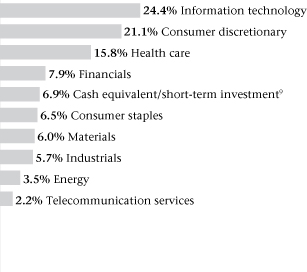

Sector weightings1:

Manager's discussion and analysis

In the 12-month period ended September 30, 2014, the Turner Midcap Growth Fund trailed the returns of the benchmark Russell Midcap® Growth Index.

The technology and consumer discretionary sectors provided the greatest contribution to the fund's performance. Semiconductor, information technology, food and beverage holdings generated the best returns within these sectors. The main detractors from performance were in the energy and utility sectors. Within these sectors, oil & gas producers and cable/satellite TV holdings were the worst performers.

1 Cash equivalent and short-term investment are not being considered a holding for the top five holdings, but are counted in the number of holdings. The fund composition is subject to change.

2 Percentages based on total investments.

3 These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. Performance of the Institutional, Investor and Retirement Class Shares will differ due to differences in fees.

4 The inception date of the Turner Midcap Growth Fund (Investor Class Shares) was October 1, 1996. Index returns are based on Investor Class Shares inception date.

5 Fee waivers are in effect; if they had not been in effect, performance would have been lower.

6 The inception date of the Turner Midcap Growth Fund (Institutional Class Shares) was June 16, 2008.

7 The inception date of the Turner Midcap Growth Fund (Retirement Class Shares) was September 24, 2001.

8 The Russell Midcap® Growth Index is a capitalization-weighted (companies with larger market capitalizations have more influence than those with smaller market capitalizations) index of the 800 smallest U.S. companies out of the 1,000 largest companies with higher growth rates and price-to-book ratios.

9 Cash equivalent includes short-term investment held as collateral for securities lending activity. Please see Note 8 in Notes to Financial Statements for more detailed information.

Amounts designated as "—" are not applicable.

Cl — Class

The Turner Midcap Growth Fund may buy and sell securities frequently as part of its investment strategy. The medium capitalization companies in which the fund invests may be more vulnerable to adverse business or economic events than larger, more established companies. The fund is subject to risks due to its foreign investments. The fund is also subject to taxable income and realized capital gains. Shareholder redemptions may force the fund to sell securities at an inappropriate time, also resulting in realized gains.

TURNER FUNDS 2014 ANNUAL REPORT 11

INVESTMENT REVIEW (Unaudited)

Turner Small Cap Growth Fund

Fund profile

September 30, 2014

n Ticker symbol TSCEX

n CUSIP #900297300

n Top five holdings1

(1) Proofpoint

(2) Cavium

(3) RF Micro Devices

(4) Team Health Holdings

(5) Penn-Virginia

n % in five largest holdings 8.8%1,2

n Number of holdings 821

n Net assets $130.09 million

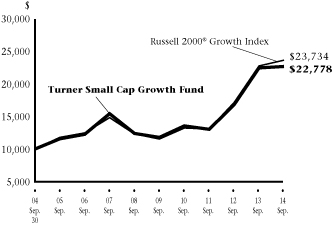

Growth of a $10,000 investment in the

Turner Small Cap Growth Fund:

September 30, 2004-September 30, 20143

Average annual total returns (Periods ended September 30, 2014)

| | | One

year | | Three

years | | Five

years | | Ten

years | | Since

inception | |

Turner Small Cap Growth Fund4 | | | 0.99 | % | | | 20.41 | % | | | 14.06 | % | | | 8.58 | % | | | 11.36 | % | |

Russell 2000® Growth Index5 | | | 3.79 | % | | | 21.91 | % | | | 15.51 | % | | | 9.03 | % | | | 6.92 | % | |

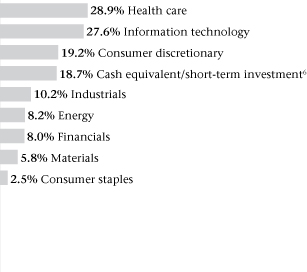

Sector weightings1:

Manager's discussion and analysis

During the 12-month period ended September 30, 2014, the Turner Small Cap Growth Fund trailed the returns of the benchmark Russell 2000® Growth Index.

The strongest returning sectors were health care, utility and producer durables with those sectors outperforming their corresponding index sectors. Within those sectors, shares in the biotech, trucking, oil & gas pipeline industries performed the best. The technology, financial and energy sectors were all drags on relative and absolute returns.

1 Cash equivalent and short-term investment are not being considered a holding for the top five holdings, but are counted in the number of holdings. The fund composition is subject to change.

2 Percentages based on total investments.

3 These figures represent past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate, so an investor's shares, when redeemed, may be worth more or less than their original cost. The performance in the above graph and table does not reflect the deduction of taxes the shareholder will pay on fund distributions or the redemptions of fund shares. The inception date of the Turner Small Cap Growth Fund was February 7, 1994.

4 Fee waivers are in effect; if they had not been in effect, performance would have been lower.

5 The Russell 2000® Growth Index is a widely-recognized, capitalization-weighted (companies with larger market capitalizations have more influence than those with smaller market capitalizations) index of the 2,000 smallest U.S. companies out of the 3,000 largest U.S. companies with higher growth rates and price-to-book ratios.

6 Cash equivalent includes short-term investment held as collateral for securities lending activity. Please see Note 8 in Notes to Financial Statements for more detailed information.

The Turner Small Cap Growth Fund may buy and sell securities frequently as part of its investment strategy. The smaller capitalization companies the fund invests in may be more vulnerable to adverse business or economic events than larger, more established companies. The fund is subject to risks due to its foreign investments. The fund is also subject to taxable income and realized capital gains. Shareholder redemptions may force the fund to sell securities at an inappropriate time, also resulting in realized gains.

12 TURNER FUNDS 2014 ANNUAL REPORT

Turner Medical Sciences Long/Short Fund

September 30, 2014

| | | Shares | | Value

(000) | |

Common stock—126.4%† | |

Biotechnology—64.7% | |

AMAG Pharmaceuticals* | | | 109,830 | | | $ | 3,506 | | |

Amarin ADR* | | | 309,470 | | | | 337 | | |

Anacor Pharmaceuticals* | | | 16,300 | | | | 399 | | |

ANI Pharmaceuticals* | | | 37,120 | | | | 1,050 | | |

Chimerix* | | | 101,780 | | | | 2,812 | | |

Concert Pharmaceuticals* | | | 85,070 | | | | 1,073 | | |

Cubist Pharmaceuticals* | | | 21,140 | | | | 1,402 | | |

Discovery Laboratories* | | | 1,425,423 | | | | 2,623 | | |

Dynavax Technologies* | | | 235,740 | | | | 337 | | |

Emergent Biosolutions* | | | 16,870 | | | | 359 | | |

Heron Therapeutics* | | | 57,740 | | | | 481 | | |

Infinity Pharmaceuticals* | | | 61,130 | | | | 820 | | |

Intercept Pharmaceuticals* | | | 8,290 | | | | 1,962 | | |

Keryx Biopharmaceuticals* | | | 25,170 | | | | 346 | | |

NPS Pharmaceuticals* | | | 63,040 | | | | 1,639 | | |

Otonomy* | | | 26,860 | | | | 645 | | |

Progenics Pharmaceuticals* | | | 89,200 | | | | 463 | | |

Prothena* | | | 58,740 | | | | 1,302 | | |

Puma Biotechnology* | | | 3,175 | | | | 757 | | |

Retrophin* | | | 165,530 | | | | 1,493 | | |

Total Biotechnology | | | | | 23,806 | | |

Health care equipment & supplies—9.5% | |

Baxter International | | | 2,240 | | | | 161 | | |

LDR Holding* | | | 63,700 | | | | 1,983 | | |

Unilife* | | | 595,810 | | | | 1,367 | | |

Total Health care equipment & supplies | | | | | 3,511 | | |

Health care providers & services—1.8% | |

Envision Healthcare Holdings* | | | 9,860 | | | | 342 | | |

Team Health Holdings* | | | 5,690 | | | | 330 | | |

Total Health care providers & services | | | | | 672 | | |

Personal products—8.0% | |

IGI Laboratories* | | | 313,842 | | | | 2,925 | | |

Total Personal products | | | | | 2,925 | | |

Pharmaceuticals—42.4% | |

Amphastar Pharmaceuticals* | | | 28,920 | | | | 337 | | |

Cardiome Pharma* | | | 65,813 | | | | 588 | | |

DepoMed* | | | 117,860 | | | | 1,790 | | |

Flamel Technologies SA ADR* | | | 221,545 | | | | 3,170 | | |

Horizon Pharma* | | | 384,060 | | | | 4,716 | | |

| | | Shares | | Value

(000) | |

Jazz Pharmaceuticals* | | | 12,860 | | | $ | 2,065 | | |

Lannett* | | | 47,680 | | | | 2,178 | | |

Ocera Therapeutics* | | | 87,590 | | | | 429 | | |

The Medicines* | | | 13,660 | | | | 305 | | |

Total Pharmaceuticals | | | | | 15,578 | | |

Total Common stock

(Cost $43,311)** | | | | | 46,492 | | |

Cash equivalent—0.8% | |

BlackRock Liquidity Funds

TempCash Portfolio,

Dollar Shares, 0.078%‡ | | | 278,466 | | | | 278 | | |

Total Cash equivalent

(Cost $278)** | | | | | 278 | | |

Total Investments—127.2%

(Cost $43,589)** | | | | | 46,770 | | |

Segregated cash with brokers—36.5% | | | | | 13,442 | | |

Securities sold short—(62.5)%

(Proceeds $(22,747))** | | | | | (22,979 | ) | |

Net Other assets (liabilities)—(1.2)% | | | | | (450 | ) | |

Net Assets—100.0% | | | | $ | 36,783 | | |

* Non-income producing security.

** This number is listed in thousands.

† More narrow industries are utilized for compliance purposes, whereas broad sectors are utilized for reporting purposes.

‡ Rate shown is the 7-day effective yield as of September 30, 2014.

ADR — American Depositary Receipt

The accompanying notes are an integral part of the financial statements.

TURNER FUNDS 2014 ANNUAL REPORT 13

Schedule of securities sold short

Turner Medical Sciences Long/Short Fund

September 30, 2014

| | | Shares | | Value

(000) | |

Common stock—62.5% | |

Biotechnology—36.6% | |

Achillion Pharmaceuticals | | | 50,940 | | | $ | 508 | | |

Acorda Therapeutics | | | 37,310 | | | | 1,264 | | |

Agios Pharmaceuticals | | | 30,450 | | | | 1,869 | | |

Amgen | | | 3,780 | | | | 531 | | |

Avalanche Biotechnologies | | | 20,190 | | | | 690 | | |

BioMarin Pharmaceuticals | | | 9,070 | | | | 654 | | |

Bluebird Bio | | | 33,770 | | | | 1,212 | | |

Isis Pharmaceuticals | | | 14,870 | | | | 577 | | |

Karyopharm Therapeutics | | | 32,097 | | | | 1,121 | | |

Ligand Pharmaceuticals, Cl B | | | 12,840 | | | | 603 | | |

Newlink Genetics | | | 54,070 | | | | 1,158 | | |

Ophthotech | | | 27,740 | | | | 1,080 | | |

Ovascience | | | 40,229 | | | | 668 | | |

Tekmira Pharmaceuticals | | | 72,310 | | | | 1,530 | | |

Total Biotechnology | | | | | 13,465 | | |

Health care equipment & supplies—10.2% | |

ABIOMED | | | 25,210 | | | | 626 | | |

Hologic | | | 15,230 | | | | 371 | | |

Hospira | | | 18,690 | | | | 972 | | |

ReWalk Robotics | | | 51,840 | | | | 1,770 | | |

Total Health care equipment & supplies | | | | | 3,739 | | |

Health care providers & services—4.7% | |

Anika Therapeutics | | | 32,480 | | | | 1,191 | | |

UnitedHealth Group, Cl B | | | 6,180 | | | | 533 | | |

Total Health care providers & services | | | | | 1,724 | | |

Life sciences tools & services—3.8% | |

Charles River Laboratories

International | | | 14,620 | | | | 873 | | |

Illumina | | | 3,270 | | | | 536 | | |

Total Life sciences tools & services | | | | | 1,409 | | |

| | | Shares | | Value

(000) | |

Pharmaceuticals—7.2% | |

ACADIA Pharmaceuticals | | | 38,290 | | | $ | 948 | | |

Nektar Therapeutics | | | 45,640 | | | | 551 | | |

Perrigo | | | 7,610 | | | | 1,143 | | |

Total Pharmaceuticals | | | | | 2,642 | | |

Total Common stock

(Proceeds $22,747)* | | | | | 22,979 | | |

Total Securities sold short—62.5%

(Proceeds $22,747)* | | | | $ | 22,979 | | |

Percentages disclosed are based on total net assets of the Fund at September 30, 2014.

* This number is listed in thousands.

Cl — Class

The accompanying notes are an integral part of the financial statements.

14 TURNER FUNDS 2014 ANNUAL REPORT

Turner Spectrum Fund

September 30, 2014

| | | Shares | | Value

(000) | |

Common stock—96.7%† | |

Consumer discretionary—15.0% | |

Advance Auto Parts | | | 10,920 | | | $ | 1,423 | | |

American Eagle Outfitters | | | 35,550 | | | | 516 | | |

Asbury Automotive Group* | | | 7,600 | | | | 490 | | |

Best Buy | | | 21,330 | | | | 716 | | |

Big Lots^ | | | 22,830 | | | | 983 | | |

Brunswick | | | 13,180 | | | | 555 | | |

Burlington Stores*^ | | | 7,840 | | | | 313 | | |

Criteo SA ADR* | | | 11,830 | | | | 398 | | |

Deckers Outdoor*^ | | | 14,610 | | | | 1,420 | | |

Delphi Automotive | | | 4,500 | | | | 276 | | |

Expedia | | | 3,370 | | | | 295 | | |

Genesco* | | | 8,700 | | | | 650 | | |

G-III Apparel Group* | | | 7,390 | | | | 612 | | |

Home Depot | | | 15,460 | | | | 1,418 | | |

HomeAway* | | | 6,600 | | | | 234 | | |

J.C. Penney* | | | 37,540 | | | | 377 | | |

Kohl's | | | 11,220 | | | | 685 | | |

Las Vegas Sands | | | 5,690 | | | | 354 | | |

Lumber Liquidators Holdings* | | | 11,780 | | | | 676 | | |

MGM Resorts International* | | | 15,450 | | | | 352 | | |

Nike, Cl B | | | 6,590 | | | | 588 | | |

SFX Entertainment*^ | | | 22,490 | | | | 113 | | |

Shutterfly* | | | 13,460 | | | | 656 | | |

Skechers U.S.A., Cl A*^ | | | 8,150 | | | | 434 | | |

Starwood Hotels & Resorts

Worldwide^ | | | 17,040 | | | | 1,418 | | |

Tenneco* | | | 11,590 | | | | 606 | | |

Time Warner | | | 7,740 | | | | 582 | | |

Urban Outfitters*^ | | | 38,970 | | | | 1,431 | | |

VF | | | 11,950 | | | | 789 | | |

Vince Holding* | | | 10,830 | | | | 328 | | |

Zalando SE # * § | | | 1,820 | | | | 49 | | |

Zoe's Kitchen* | | | 31,910 | | | | 982 | | |

Total Consumer discretionary | | | | | 20,719 | | |

Consumer staples—2.6% | |

Mead Johnson Nutrition, Cl A^ | | | 3,980 | | | | 383 | | |

Monster Beverage* | | | 13,990 | | | | 1,283 | | |

PepsiCo^ | | | 6,200 | | | | 577 | | |

WhiteWave Foods, Cl A*^ | | | 26,140 | | | | 950 | | |

Whole Foods Market | | | 10,530 | | | | 401 | | |

Total Consumer staples | | | | | 3,594 | | |

| | | Shares | | Value

(000) | |

Energy—7.2% | |

EOG Resources^ | | | 4,160 | | | $ | 412 | | |

Green Plains Renewable Energy | | | 51,060 | | | | 1,909 | | |

Halliburton^ | | | 8,810 | | | | 568 | | |

Independence Contract

Drilling*^ | | | 160,000 | | | | 1,880 | | |

Kinder Morgan | | | 28,380 | | | | 1,088 | | |

Lehigh Gas Partners^ | | | 37,382 | | | | 1,270 | | |

Memorial Resource

Development*^ | | | 29,750 | | | | 807 | | |

Sanchez Energy Corp.* | | | 10,860 | | | | 285 | | |

Schlumberger^ | | | 7,030 | | | | 715 | | |

Vaalco Energy* | | | 63,960 | | | | 544 | | |

Whiting Petroleum* | | | 5,790 | | | | 449 | | |

Total Energy | | | | | 9,927 | | |

Financials—13.9% | |

Ameris Bancorp | | | 15,520 | | | | 341 | | |

Aon^ | | | 13,070 | | | | 1,146 | | |

Atlas Mara Co-Nvest* | | | 270,290 | | | | 2,648 | | |

Bank of the Ozarks^ | | | 18,898 | | | | 596 | | |

Bryn Mawr Bank | | | 17,181 | | | | 487 | | |

Discover Financial Services^ | | | 31,022 | | | | 1,998 | | |

East West Bancorp^ | | | 14,760 | | | | 502 | | |

Essent Group*^ | | | 61,120 | | | | 1,309 | | |

FS Investment^ | | | 75,160 | | | | 809 | | |

Goldman Sachs Group | | | 2,720 | | | | 499 | | |

Hanmi Financial^ | | | 32,540 | | | | 656 | | |

Invesco^ | | | 32,980 | | | | 1,302 | | |

Janus Capital Group | | | 23,210 | | | | 337 | | |

Kennedy-Wilson Holdings^ | | | 46,410 | | | | 1,112 | | |

MetLife^ | | | 16,160 | | | | 868 | | |

Moelis | | | 12,870 | | | | 440 | | |

Moody's^ | | | 21,390 | | | | 2,021 | | |

Morgan Stanley^ | | | 18,610 | | | | 643 | | |

Signature Bank*^ | | | 7,270 | | | | 815 | | |

Square 1 Financial, Cl A* | | | 19,870 | | | | 382 | | |

Wells Fargo | | | 7,860 | | | | 408 | | |

Total Financials | | | | | 19,319 | | |

Health care—31.8% | |

Actavis* | | | 2,950 | | | | 712 | | |

AMAG Pharmaceuticals*^ | | | 90,320 | | | | 2,883 | | |

Amarin ADR* | | | 275,550 | | | | 300 | | |

Amphastar Pharmaceuticals* | | | 24,120 | | | | 281 | | |

TURNER FUNDS 2014 ANNUAL REPORT 15

Schedule of investments

Turner Spectrum Fund

| | | Shares | | Value

(000) | |

Anacor Pharmaceuticals* | | | 14,520 | | | $ | 355 | | |

ANI Pharmaceuticals* | | | 30,670 | | | | 867 | | |

Baxter International | | | 1,960 | | | | 141 | | |

Biogen Idec*^ | | | 3,030 | | | | 1,002 | | |

Cardiome Pharma* | | | 58,600 | | | | 523 | | |

Celgene* | | | 3,120 | | | | 296 | | |

Chimerix* | | | 74,190 | | | | 2,049 | | |

Cigna | | | 3,080 | | | | 279 | | |

Concert Pharmaceuticals* | | | 70,970 | | | | 895 | | |

Cubist Pharmaceuticals*^ | | | 18,825 | | | | 1,249 | | |

DepoMed*^ | | | 102,717 | | | | 1,560 | | |

Discovery Laboratories*^ | | | 1,046,097 | | | | 1,925 | | |

Dynavax Technologies* | | | 209,900 | | | | 300 | | |

Emergent Biosolutions* | | | 15,020 | | | | 320 | | |

Envision Healthcare Holdings* | | | 8,360 | | | | 290 | | |

Flamel Technologies SA ADR*^ | | | 186,929 | | | | 2,675 | | |

Gilead Sciences* | | | 3,340 | | | | 356 | | |

Heron Therapeutics* | | | 51,410 | | | | 428 | | |

Horizon Pharma*^ | | | 318,120 | | | | 3,908 | | |

IGI Laboratories*^ | | | 279,450 | | | | 2,604 | | |

Infinity Pharmaceuticals* | | | 53,520 | | | | 718 | | |

Intercept Pharmaceuticals*^ | | | 6,870 | | | | 1,626 | | |

Jazz Pharmaceuticals*^ | | | 10,910 | | | | 1,752 | | |

Johnson & Johnson^ | | | 8,170 | | | | 871 | | |

Keryx Biopharmaceuticals* | | | 22,410 | | | | 308 | | |

Lannett*^ | | | 41,550 | | | | 1,898 | | |

LDR Holding*^ | | | 55,510 | | | | 1,728 | | |

McKesson^ | | | 4,970 | | | | 968 | | |

Merck | | | 7,390 | | | | 438 | | |

NPS Pharmaceuticals* | | | 52,660 | | | | 1,369 | | |

Ocera Therapeutics* | | | 77,990 | | | | 382 | | |

Otonomy* | | | 22,090 | | | | 530 | | |

Progenics Pharmaceuticals* | | | 79,420 | | | | 412 | | |

Prothena* | | | 52,300 | | | | 1,159 | | |

Puma Biotechnology* | | | 2,830 | | | | 675 | | |

Retrophin* | | | 138,270 | | | | 1,247 | | |

Team Health Holdings* | | | 5,070 | | | | 294 | | |

The Medicines* | | | 12,160 | | | | 271 | | |

Unilife* | | | 530,496 | | | | 1,217 | | |

Total Health care | | | | | 44,061 | | |

Industrials—10.9% | |

Aercap Holdings*^ | | | 11,050 | | | | 452 | | |

American Airlines Group | | | 31,650 | | | | 1,123 | | |

AMETEK^ | | | 7,600 | | | | 382 | | |

| | | Shares | | Value

(000) | |

C.H. Robinson Worldwide | | | 8,950 | | | $ | 594 | | |

Canadian Pacific Railway^ | | | 3,614 | | | | 750 | | |

Chicago Bridge & Iron | | | 10,950 | | | | 633 | | |

FedEx | | | 2,770 | | | | 447 | | |

Honeywell International | | | 4,590 | | | | 427 | | |

Hub Group, Cl A*^ | | | 15,790 | | | | 640 | | |

Kansas City Southern | | | 6,020 | | | | 730 | | |

Kirby* | | | 4,170 | | | | 491 | | |

Landstar System^ | | | 15,490 | | | | 1,118 | | |

Louis XIII Holdings* | | | 607,566 | | | | 306 | | |

Old Dominion Freight Line*^ | | | 10,650 | | | | 752 | | |

Precision Castparts^ | | | 5,970 | | | | 1,414 | | |

Rockwell Automation | | | 1,930 | | | | 212 | | |

Saia*^ | | | 16,345 | | | | 810 | | |

Scorpio Bulkers* | | | 41,360 | | | | 241 | | |

Spirit Airlines* | | | 2,700 | | | | 187 | | |

Swift Transportation*^ | | | 38,070 | | | | 799 | | |

Tutor Perini* | | | 12,520 | | | | 331 | | |

Union Pacific | | | 15,940 | | | | 1,728 | | |

United Rentals*^ | | | 4,950 | | | | 550 | | |

Total Industrials | | | | | 15,117 | | |

Information technology—10.8% | |

Activision Blizzard | | | 21,310 | | | | 443 | | |

Alliance Data Systems*^ | | | 2,130 | | | | 529 | | |

Apple | | | 4,290 | | | | 432 | | |

Avago Technologies | | | 4,180 | | | | 364 | | |

Digimarc^ | | | 50,000 | | | | 1,036 | | |

Envestnet* | | | 18,350 | | | | 826 | | |

F5 Networks* | | | 3,570 | | | | 424 | | |

Facebook, Cl A*^ | | | 18,910 | | | | 1,494 | | |

FireEye* | | | 27,670 | | | | 846 | | |

Google, Cl A*^ | | | 3,760 | | | | 2,211 | | |

IZEA* | | | 125,930 | | | | 47 | | |

Materialise ADR* | | | 33,970 | | | | 381 | | |

NXP Semiconductors* | | | 6,240 | | | | 427 | | |

Pandora Media* | | | 18,680 | | | | 451 | | |

Remark Media*^ | | | 140,950 | | | | 887 | | |

Salesforce.com*^ | | | 15,070 | | | | 867 | | |

SanDisk | | | 3,650 | | | | 358 | | |

Twitter* | | | 16,180 | | | | 835 | | |

Visa, Cl A | | | 5,780 | | | | 1,233 | | |

Western Digital | | | 8,980 | | | | 874 | | |

Total Information technology | | | | | 14,965 | | |

16 TURNER FUNDS 2014 ANNUAL REPORT

Schedule of investments

Turner Spectrum Fund

| | | Shares | | Value

(000) | |

Materials—4.5% | |

Compass Minerals

International^ | | | 17,770 | | | $ | 1,497 | | |

Huntsman | | | 38,380 | | | | 997 | | |

KapStone Paper & Packaging* | | | 15,990 | | | | 447 | | |

Lyondellbasell Industries, Cl A | | | 7,240 | | | | 787 | | |

Methanex | | | 11,700 | | | | 782 | | |

Packaging Corp. of America | | | 7,310 | | | | 467 | | |

PolyOne | | | 21,380 | | | | 761 | | |

Senomyx* | | | 63,100 | | | | 517 | | |

Total Materials | | | | | 6,255 | | |

Total Common stock

(Cost $125,585)** | | | | | 133,957 | | |

Warrant—0.3% | |

Financials—0.3% | |

Atlas Mara Co-Nvest* | | | 472,160 | | | | 472 | | |

Total Financials | | | | | 472 | | |

Total Warrant

(Cost $92)** | | | | | 472 | | |

Total Investments—97.0%

(Cost $125,677)** | | | | | 134,429 | | |

Segregated cash with brokers—48.5% | | | | | 67,228 | | |

Securities sold short—(53.9)%

(Proceeds $(76,749))** | | | | | (74,677 | ) | |

Net Other assets (liabilities)—8.4% | | | | | 11,598 | | |

Net Assets—100.0% | | | | $ | 138,578 | | |

# Represents a restricted security. The security has been deemed illiquid according to the policies and procedures adopted by the Board of Trustees. Trading of this security did not begin publicly until October 1, 2014. As of September 30, 2014, illiquid securities were 0.0% of the Fund's net assets.

| | | Acquisition

Date | | Acquisition

Cost** | | Share

Amount | | Fair

Value** | |

Zalando SE | | 9/30/14 | | $ | 49 | | | | 1,820 | | | $ | 49 | | |

* Non-income producing security.

** This number is listed in thousands.

^ All or a portion of the shares have been committed as collateral for open short positions.

§ Security fair valued using procedures established by the Fair Value Committee. As of September 30, 2014, the total market value of these securities was $49**, representing 0.0% of Net Assets.

† More narrow industries are utilized for compliance purposes, whereas broad sectors are utilized for reporting purposes.

ADR — American Depositary Receipt

Cl — Class

The accompanying notes are an integral part of the financial statements.

TURNER FUNDS 2014 ANNUAL REPORT 17

Schedule of securities sold short

Turner Spectrum Fund

September 30, 2014

| | | Shares | | Value

(000) | |

Common stock—47.9% | |

Consumer discretionary—8.9% | |

Amazon.com | | | 3,220 | | | $ | 1,038 | | |

Autoliv | | | 11,300 | | | | 1,039 | | |

AutoZone | | | 2,630 | | | | 1,341 | | |

Bed Bath & Beyond | | | 11,960 | | | | 787 | | |

CBS Outdoor Americas | | | 14,290 | | | | 428 | | |

Dillard's, Cl A | | | 6,110 | | | | 666 | | |

Discovery Communications, Cl A | | | 7,220 | | | | 273 | | |

Ford Motor | | | 14,300 | | | | 211 | | |

Fossil | | | 2,960 | | | | 278 | | |

Garmin | | | 2,820 | | | | 147 | | |

Hyatt Hotels, Cl A | | | 9,110 | | | | 551 | | |

Johnson Controls | | | 14,530 | | | | 639 | | |

L Brands | | | 5,990 | | | | 401 | | |

Nexstar Broadcasting Group | | | 3,540 | | | | 143 | | |

Nordstrom | | | 4,020 | | | | 275 | | |

ReWalk Robotics | | | 22,560 | | | | 770 | | |

Ross Stores | | | 6,390 | | | | 483 | | |

Sonic Automotive, Cl A | | | 15,000 | | | | 368 | | |

Steven Madden | | | 6,140 | | | | 198 | | |

Tiffany | | | 2,700 | | | | 260 | | |

Tumi Holdings | | | 19,000 | | | | 387 | | |

Twenty-First Century Fox | | | 6,330 | | | | 217 | | |

Ulta Salon, Cosmetics & Fragrance | | | 3,860 | | | | 456 | | |

Under Armour, Cl A | | | 2,420 | | | | 167 | | |

Wolverine World Wide | | | 15,420 | | | | 386 | | |

Yum! Brands | | | 6,860 | | | | 494 | | |

Total Consumer discretionary | | | | | 12,403 | | |

Consumer staples—2.2% | |

Campbell Soup | | | 5,140 | | | | 220 | | |

General Mills | | | 15,170 | | | | 765 | | |

Kraft Foods Group | | | 3,840 | | | | 217 | | |

McDonald's | | | 7,650 | | | | 725 | | |

Wal-Mart Stores | | | 14,100 | | | | 1,078 | | |

Total Consumer staples | | | | | 3,005 | | |

Energy—0.6% | |

Apache | | | 3,940 | | | | 369 | | |

Rosetta Resources | | | 5,020 | | | | 224 | | |

Tidewater | | | 4,420 | | | | 173 | | |

Total Energy | | | | | 766 | | |

| | | Shares | | Value

(000) | |

Financials—7.0% | |

AFLAC, Inc. | | | 11,990 | | | $ | 698 | | |

Ally Financial | | | 24,610 | | | | 569 | | |

BancorpSouth | | | 31,140 | | | | 627 | | |

Bank of America | | | 17,400 | | | | 297 | | |

Bank Pekao SA | | | 8,380 | | | | 492 | | |

CBRE Group | | | 26,180 | | | | 779 | | |

First Republic Bank | | | 9,830 | | | | 485 | | |

Franklin Resources | | | 5,450 | | | | 298 | | |

Genworth Financial, Cl A | | | 44,870 | | | | 588 | | |

Greenhill | | | 5,530 | | | | 257 | | |

IntercontinentalExchange Group | | | 5,860 | | | | 1,144 | | |

Northern Trust | | | 8,540 | | | | 581 | | |

Ocwen Financial | | | 3,530 | | | | 92 | | |

Realogy Holdings | | | 28,200 | | | | 1,049 | | |

Stifel Financial | | | 5,390 | | | | 253 | | |

Synchrony Financial | | | 30,360 | | | | 745 | | |

T. Rowe Price Group | | | 9,210 | | | | 722 | | |

Total Financials | | | | | 9,676 | | |

Health care—13.1% | |

ABIOMED | | | 22,450 | | | | 557 | | |

ACADIA Pharmaceuticals | | | 32,810 | | | | 812 | | |

Achillion Pharmaceuticals | | | 43,220 | | | | 431 | | |

Acorda Therapeutics | | | 30,910 | | | | 1,047 | | |

Agios Pharmaceuticals | | | 25,440 | | | | 1,562 | | |

Amgen | | | 3,310 | | | | 465 | | |

Anika Therapeutics | | | 28,920 | | | | 1,060 | | |

Avalanche Biotechnologies | | | 17,590 | | | | 601 | | |

BioMarin Pharmaceuticals | | | 7,900 | | | | 570 | | |

Bluebird Bio | | | 28,930 | | | | 1,038 | | |

Charles River Laboratories

International | | | 12,740 | | | | 761 | | |

Express Scripts Holding | | | 6,140 | | | | 434 | | |

Hologic | | | 13,560 | | | | 330 | | |

Hospira | | | 16,320 | | | | 849 | | |

Illumina | | | 2,910 | | | | 477 | | |

Isis Pharmaceuticals | | | 13,240 | | | | 514 | | |

Karyopharm Therapeutics | | | 28,580 | | | | 999 | | |

Ligand Pharmaceuticals, Cl B | | | 11,190 | | | | 526 | | |

Nektar Therapeutics | | | 38,680 | | | | 467 | | |

Newlink Genetics | | | 44,850 | | | | 961 | | |

Ophthotech | | | 24,700 | | | | 962 | | |

Ovascience | | | 33,177 | | | | 551 | | |

Perrigo | | | 6,780 | | | | 1,018 | | |

18 TURNER FUNDS 2014 ANNUAL REPORT

Schedule of securities sold short

Turner Spectrum Fund

| | | Shares | | Value

(000) | |

Sirona Dental Systems | | | 2,250 | | | $ | 173 | | |

Tekmira Pharmaceuticals | | | 10,000 | | | | 211 | | |

UnitedHealth Group, Cl B | | | 5,500 | | | | 474 | | |

Varian Medical Systems | | | 2,580 | | | | 207 | | |

Waters | | | 2,040 | | | | 202 | | |

Total Health care | | | | | 18,259 | | |

Industrials—9.1% | |

| 3M | | | 2,010 | | | | 285 | | |

AGCO | | | 20,770 | | | | 944 | | |

Atlas Air Worldwide Holdings | | | 15,150 | | | | 500 | | |

Boeing | | | 10,250 | | | | 1,306 | | |

Cummins | | | 2,130 | | | | 281 | | |

Deere | | | 17,920 | | | | 1,469 | | |

Dover | | | 2,640 | | | | 212 | | |

Emerson Electric | | | 14,770 | | | | 924 | | |

Expeditors International of

Washington | | | 15,690 | | | | 637 | | |

Granite Construction | | | 19,950 | | | | 635 | | |

Hunt (JB) Transportation Services | | | 6,500 | | | | 481 | | |

KBR | | | 29,030 | | | | 547 | | |

Matson | | | 22,980 | | | | 575 | | |

Team | | | 8,030 | | | | 304 | | |

Terex | | | 4,230 | | | | 134 | | |

Titan Machinery | | | 39,400 | | | | 512 | | |

United Technologies | | | 2,060 | | | | 218 | | |

Valmont Industries | | | 17,270 | | | | 2,330 | | |

Werner Enterprises | | | 15,462 | | | | 390 | | |

Total Industrials | | | | | 12,684 | | |

Information technology—4.1% | |

Accenture PLC | | | 8,260 | | | | 672 | | |

Altera | | | 6,050 | | | | 216 | | |

ARM Holdings ADR | | | 3,210 | | | | 140 | | |

Cardtronics | | | 24,210 | | | | 852 | | |

Ciena | | | 8,210 | | | | 137 | | |

Cree | | | 8,340 | | | | 342 | | |

eBay | | | 2,740 | | | | 155 | | |

Fairchild Semiconductor

International | | | 13,320 | | | | 207 | | |

LG Display ADR | | | 8,800 | | | | 139 | | |

Linear Technology | | | 6,370 | | | | 283 | | |

Oracle | | | 5,540 | | | | 212 | | |

Semtech | | | 6,340 | | | | 172 | | |

Symantec | | | 8,910 | | | | 209 | | |

| | | Shares | | Value

(000) | |

VeriSign | | | 4,890 | | | $ | 270 | | |

Western Union | | | 74,190 | | | | 1,190 | | |

Yelp | | | 6,820 | | | | 465 | | |

Total Information technology | | | | | 5,661 | | |

Materials—2.9% | |

Agrium | | | 12,840 | | | | 1,143 | | |

American Vanguard | | | 62,990 | | | | 705 | | |

Monsanto | | | 10,310 | | | | 1,160 | | |

Rock-Tenn, Cl A | | | 19,900 | | | | 947 | | |

Total Materials | | | | | 3,955 | | |

Total Common stock

(Proceeds $68,205)* | | | | | 66,409 | | |

Exchange traded funds—6.0% | |

Consumer Staples Select Sector

SPDR Fund ETF | | | 14,790 | | | | 667 | | |

iShares China Large-Capital ETF | | | 12,820 | | | | 491 | | |

iShares Russell 2000 Growth ETF | | | 11,560 | | | | 1,499 | | |

iShares Transportation Average ETF | | | 6,800 | | | | 1,026 | | |

SPDR S&P 500 ETF Trust | | | 5,350 | | | | 1,054 | | |

SPDR S&P Biotech ETF | | | 1,390 | | | | 217 | | |

SPDR S&P Retail ETF | | | 6,040 | | | | 517 | | |

Teucrium Corn Fund | | | 39,100 | | | | 891 | | |

Vanguard S&P 500 ETF | | | 7,910 | | | | 1,428 | | |

VelocityShares Daily Inverse VIX

Short-Term ETN | | | 12,500 | | | | 478 | | |

Total Exchange traded funds

(Proceeds $8,544)* | | | | | 8,268 | | |

Total Securities sold short—53.9%

(Proceeds $76,749)* | | | | $ | 74,677 | | |

Percentages disclosed are based on total net assets of the Fund at September 30, 2014.

* This number is listed in thousands.

ADR — American Depositary Receipt

Cl — Class

ETF — Exchange Traded Fund