| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-226943-07 | ||

July 8, 2020

FREE WRITING PROSPECTUS

COLLATERAL TERM SHEET

BENCHMARK 2020-B18 |

Deutsche Mortgage & Asset Receiving Corporation

Depositor

| Deutsche Bank Securities | Citigroup | Goldman Sachs & Co. LLC | J.P. Morgan |

| Co-Lead Managers and Joint Bookrunners | |||

The depositor has filed a registration statement (including the prospectus) with the Securities and Exchange Commission (File No. 333-226943) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the Securities and Exchange Commission for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the Securities and Exchange Commission website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by emailing: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us. This free writing prospectus does not contain all information that is required to be included in the prospectus.

1

STATEMENT REGARDING ASSUMPTIONS AS TO SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

This material is for your information, and none of Deutsche Bank Securities Inc., J.P. Morgan Securities LLC, Citigroup Global Markets Inc., Goldman Sachs & Co. LLC or any other underwriter, (the “Underwriters”) are soliciting any action based upon it. This material is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

Neither this document nor anything contained herein shall form the basis for any contract or commitment whatsoever. The information contained herein is preliminary as of the date hereof. These materials are subject to change, completion or amendment from time to time. The information contained herein will be superseded by similar information delivered to you as part of the preliminary prospectus relating to the Benchmark 2020-B18 Mortgage Trust Commercial Mortgage Pass-Through Certificates, Series 2020-B18 (the "Offering Document"). The information contained herein supersedes any such information previously delivered and should be reviewed only in conjunction with the entire Offering Document. All of the information contained herein is subject to the same limitations and qualifications contained in the Offering Document. The information contained herein does not contain all relevant information relating to the underlying mortgage loans or mortgaged properties. Such information is described elsewhere in the Offering Document. The information contained herein will be more fully described elsewhere in the Offering Document. The information contained herein should not be viewed as projections, forecasts, predictions or opinions with respect to value. Prior to making any investment decision, prospective investors are strongly urged to read the Offering Document its entirety. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this free writing prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of the Underwriters or any of their respective affiliates makes any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities.

This document contains forward-looking statements. Those statements are subject to certain risks and uncertainties that could cause the success of collections and the actual cash flow generated to differ materially from the information set forth herein. While such information reflects projections prepared in good faith based upon methods and data that are believed to be reasonable and accurate as of the dates thereof, the depositor undertakes no obligation to revise these forward-looking statements to reflect subsequent events or circumstances. Individuals should not place undue reliance on forward-looking statements and are advised to make their own independent analysis and determination with respect to the forecasted periods, which reflect the issuer’s view only as of the date hereof.

| IMPORTANT NOTICE RELATING TO AUTOMATICALLY GENERATED EMAIL DISCLAIMERS |

Any legends, disclaimers or other notices that may appear at the bottom of the email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation being made that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

2

Various Various, Various | Loan Specific Premarketing Term Sheet Agellan Portfolio | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $172,000,000 73.1% 1.78x 9.0% |

3

Various Various, Various | Loan Specific Premarketing Term Sheet Agellan Portfolio | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $172,000,000 73.1% 1.78x 9.0% |

4

Various Various, Various | Loan Specific Premarketing Term Sheet Agellan Portfolio | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $172,000,000 73.1% 1.78x 9.0% |

5

Various Various, Various | Loan Specific Premarketing Term Sheet Agellan Portfolio | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $172,000,000 73.1% 1.78x 9.0% |

6

Various Various, Various | Loan Specific Premarketing Term Sheet Agellan Portfolio | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $172,000,000 73.1% 1.78x 9.0% |

| Mortgage Loan Information | |

| Loan Seller: | JPMCB |

| Loan Purpose: | Refinance |

| Credit Assessment | |

| (Fitch/S&P/KBRA): | [ ](sf) / [ ](sf) / [ ](sf) |

| Borrower Sponsor(1): | Elad Canada, Inc. |

| Borrowers(1): | Various |

| Original Balance(2): | $172,000,000 |

| Cut-off Date Balance(2): | $172,000,000 |

| % by Initial UPB: | [ ]% |

| Interest Rate: | 4.4000% |

| Payment Date: | 7th of each month |

| First Payment Date: | September 7, 2020 |

| Maturity Date: | August 7, 2025 |

| Amortization: | Interest Only |

| Additional Debt(2)(3) : | $231,000,000 Pari Passu Debt; $31,000,000 Mezzanine Debt |

| Call Protection(4): | L(24), D(33), O(4) |

| Lockbox / Cash Management: | Hard / In Place |

| Reserves(5) | |||

| Initial | Monthly | Cap | |

| Taxes: | $0 | Springing | NAP |

| Insurance: | $0 | Springing | NAP |

| Common Charges: | $0 | Springing | NAP |

| Required Repairs: | $2,985,266 | NAP | NAP |

| Replacement: | $0 | $101,570 | $3,656,506 |

| TI/LC: | $6,410,963 | $431,671 | $15,540,151 |

| Working Capital Reserve: | $2,000,000 | $0 | NAP |

| Gap Rent Reserve: | $172,050 | $0 | NAP |

| Property Information | ||

| Single Asset / Portfolio: | Portfolio of 46 properties | |

| Property Type: | Various | |

| Collateral: | Fee Simple | |

| Location: | Various | |

| Year Built / Renovated: | Various / Various | |

| Total Sq. Ft.(6): | 6,094,177 | |

| Property Management(7): | Various | |

| Underwritten NOI(8): | $36,198,452 | |

| Underwritten NCF(8): | $32,909,376 | |

| Appraised Value(9): | $551,000,000 | |

| Appraisal Date: | Various | |

| Historical NOI | ||

| Most Recent NOI(10): | NAV | |

| 2019 NOI: | $40,473,151 (December 31, 2019) | |

| 2018 NOI(11): | $38,961,287 (December 31, 2018) | |

| 2017 NOI(11): | $33,762,598 (December 31, 2017) | |

| Historical Occupancy | ||

| Most Recent Occupancy(12): | 90.4% (June 1, 2020) | |

| 2019 Occupancy: | 96.2% (December 31, 2019) | |

| 2018 Occupancy: | 96.1% (December 31, 2018) | |

| 2017 Occupancy: | 94.7% (December 31, 2017) | |

| Financial Information | ||||||

| Tranche | Cut-off Date Balance | Balance per Sq. Ft. Cut-off / Balloon | LTV Cut-off / Balloon | U/W DSCR NOI / NCF | U/W Debt Yield NOI / NCF | U/W Debt Yield at Balloon NOI / NCF |

| Mortgage Loan | $100,000,000 | |||||

| Pari Passu Notes | $131,000,000 | |||||

| Total Senior Notes | $231,000,000 | $38 / $38 | 41.9% / 41.9% | 3.34x / 3.04x | 15.7% / 14.2% | 15.7% / 14.2% |

| B Note | $172,000,000 | |||||

| Whole Loan | $403,000,000 | $66 / $66 | 73.1% / 73.1% | 1.96x / 1.78x | 9.0% / 8.2% | 9.0% / 8.2% |

| Mezzanine Loan | $31,000,000 | |||||

| Total Debt | $434,000,000 | $71 / $71 | 78.8% / 78.8% | 1.70x / 1.54x | 8.3% / 7.6% | 8.3% / 7.6% |

| (1) | For a description of the Borrowers (as defined below) and the Borrower Sponsor (as defined below) see “The Borrowers / Borrower Sponsor” herein. |

| (2) | Represents the principal balance of the controlling subordinate note B. The Agellan Portfolio Whole Loan (as defined below), is expected to be evidenced by eight senior pari passu notes and a controlling subordinate note B, with an aggregate outstanding principal balance as of the Cut-off Date of $403.0 million. For additional information, see “The Loan” herein. |

| (3) | See “Current Mezzanine or Subordinate Indebtedness" herein. |

| (4) | The lockout period will be at least 24 payments beginning with and including the first payment date of September 7, 2020. The Borrowers have the option to defease the full $403.0 million Agellan Portfolio Whole Loan after the earlier to occur of (i) two years after the closing date of the securitization that includes the last note to be securitized and (ii) the third anniversary of the first payment date. The actual lockout period may be longer. The interest only period and Call Protection presented in the Mortgage Loan Information above are inclusive of the additional September 2020 interest payment to be deposited by JPMCB. |

| (5) | See “Initial and Ongoing Reserves” herein. |

| (6) | Total Sq. Ft. is exclusive of 344 sq. ft. associated with remeasurements. |

| (7) | For a description of the Property Managers (as defined below) see “Property Management” below. |

| (8) | Underwritten NOI and Underwritten NCF are inclusive of contractual rent steps taken through June 1, 2021 and includes the ALDI, Inc. expansion of approximately 24,597 sq. ft. and HCSC (as defined below) relocation at the Naperville Woods Office Center property. U/W Base Rent has been further adjusted to account for a 10.0% stress to tenants who missed full or partial rent payments in April, May and/or June or have requested rent relief during the COVID-19 pandemic. The total stress to U/W Base Rent is $241,419. An additional stress loss adjustment of 10.0% was applied to total reimbursements for any tenants that missed full rent payments in April, May and/or June. The total stress to reimbursements is $85,560. All U/W Base Rent figures herein are exclusive of rent attributable to vacant space. |

| (9) | The Appraised Value is based on an aggregate “as-is” value of the Agellan Properties (as defined below) and is inclusive of excess land value that is defined in each individual Agellan Property appraisal and serves as collateral for the Agellan Portfolio Whole Loan. The excess vacant land parcels are associated with the Sarasota Distribution Hub and Supervalu properties may be released pursuant to satisfying conditions set forth in “Partial Release” below. |

| (10) | Most Recent NOI is not available as the Borrowers are only required to report financials on an annual basis. |

| (11) | The increase from 2018 NOI and 2017 NOI is due to the increase of assets in the Agellan Portfolio from 41 to 46. |

| (12) | Most Recent Occupancy is reflective of the exclusion of known vacancies and tenants that have gone dark at the Agellan Properties. Occupancy inclusive of such tenant spaces is approximately 93.4%. |

7

Various Various, Various | Loan Specific Premarketing Term Sheet Agellan Portfolio | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $172,000,000 73.1% 1.78x 9.0% |

Executive Summary.

| ■ | The Whole Loan. JPMorgan Chase Bank is providing an aggregate $434.0 million five-year, fixed-rate, interest only whole loan and mezzanine financing secured by the fee simple interest in the Agellan Portfolio, a 46-property portfolio of industrial and office properties in the aggregate comprising 6,094,177 sq. ft. located throughout nine states The Agellan Portfolio Whole Loan, along with $31.0 million in mezzanine debt will be used to pay off existing debt of $418.6 million, fund upfront reserves for outstanding tenant improvements and leasing commissions, working capital, capital expenditures, deferred maintenance, gap rent and cover closing costs. |

| ■ | Collateral Summary. The Agellan Portfolio Whole Loan is secured by a portfolio of 46 properties that are diversified across nine states throughout 12 distinct markets. The Agellan Properties were constructed between 1967 and 2010 and are generally located in primary and secondary markets in suburban infill locations with good access to transportation. |

| - | Industrial Concentrated Portfolio: The Agellan Portfolio is comprised of 42 industrial properties (5,248,373 sq. ft.; 86.1% of NRA; 71.3% of U/W Base Rent) and four office properties (845,804 sq. ft.; 13.9% of NRA; 28.7% of U/W Base Rent). |

| o | The largest office property, Naperville Woods Office Center, is located in Naperville, Illinois and accounts for 12.8% of the Whole Loan ALA. The property is currently 95.4% occupied by 13 tenants and has a maintained an average occupancy of 93.8% since 2013. |

Property and Tenant Granularity: As of June 1, 2020, the Agellan Portfolio is approximately 93.4% leased (90.4% leased excluding dark tenants and known vacates) and consists of approximately 250 tenants across approximately 5.5 million sq. ft. of occupied space, with a weighted average lease term of 2.9 years.

| o | No individual Agellan Property accounts for more than 13.0% of Whole Loan ALA or 14.9% of NRA. |

| o | The largest tenant, Health Care Service Corp. (Moody's/Fitch/S&P: A3/A-/AA-), accounts for only 6.9% of U/W Base Rent. Health Care Service Corporation is an Independent Licensee of the Blue Cross and Blue Shield Associations and the largest customer-owned health insurer in the United States. |

| o | Four of the top ten tenants (Health Care Service Corp., General Motors LLC, Life Technologies Corporation and Allstate Insurance Co.) have investment grade credit ratings by one or more of Moody’s, Fitch or S&P and account for approximately 12.4% and 18.3% of the Agellan Portfolio’s Total NRA and U/W Base Rent, respectively. |

| - | Stable Occupancy: The Agellan Portfolio has demonstrated consistent occupancy with an average occupancy rate of approximately 93.5% since 2013. |

| - | Consistent Historic Operating Performance: The Agellan Portfolio has demonstrated consistent NOI growth year-over-year with an NOI CAGR from 2015 to 2019 for same reporting assets ranging from 2.2% to 7.0%. |

| - | Strong Leasing Momentum: Since May 2019, the Borrower Sponsor has executed 38 new, renewal and expansion leases for approximately 470,218 sq. ft. Renewal leases have had weighted average rent increases of approximately 8.7% and newly executed leases have had weighted average rent increases of 8.3%. |

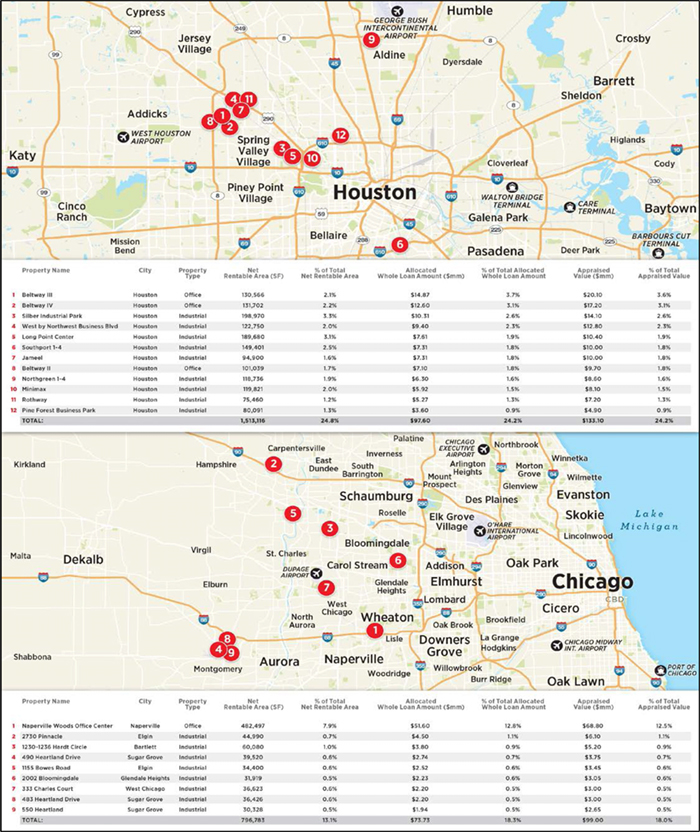

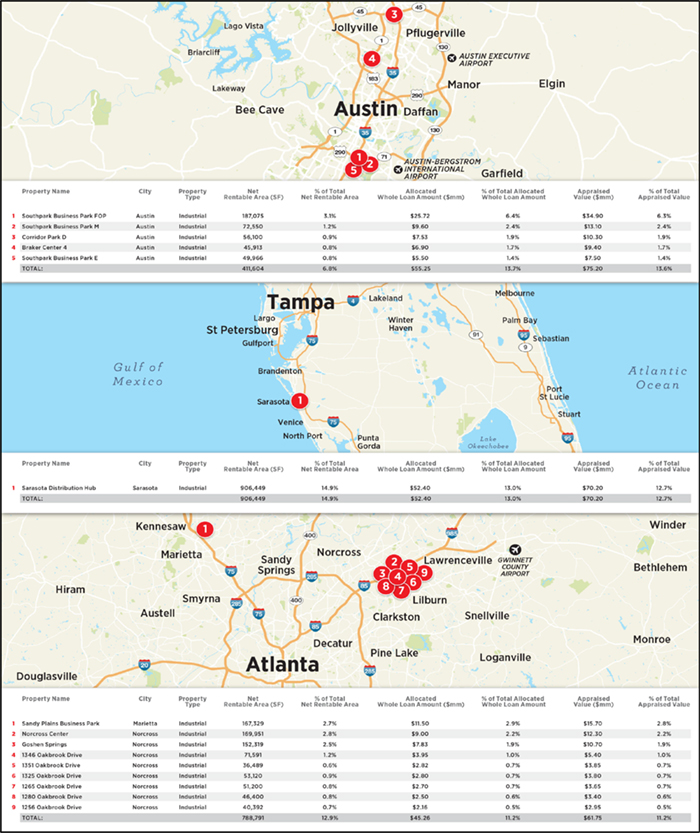

| - | Geographic Diversity Across Markets: The portfolio is diversified across 12 distinct markets. The top five markets by U/W Base Rent are Houston (23.2%), Chicago (22.9%), Austin (12.9%), Tampa (11.7%) and Atlanta (10.9%). |

| - | COVID-19 Resiliency: The Agellan Portfolio has achieved significant rent collections during the COVID-19 pandemic. Of the 250 unique tenants occupying the Agellan Portfolio, the Borrower Sponsor received approximately 97.0% rent collections for June 2020 and approximately 97.0% rent collections for both April and May 2020. The top ten tenants, representing 38.5% of NRA and 41.0% of U/W Base Rent have paid rent and have not requested rent relief. |

| - | On-going Reserves: To mitigate rollover during the term of the Agellan Portfolio Whole Loan, the Agellan Portfolio Whole Loan is structured with an on-going TI/LC collections of $0.85 per sq. ft. per year and replacements reserves of $0.33 per sq. ft. per year, both of which will be capped at 3 years of collections. The reserves equate to approximately $5.8 million in annual collections and capped at approximately $19.2 million. |

| - | Sponsor Equity: The Borrower Sponsor acquired 42 of the assets in early 2019 and four of the assets in early 2020 and has a current cost basis of approximately $507.8 million. The Borrower Sponsor’s total cash equity in the Agellan Portfolio will be approximately $185.5 million. |

8

Various Various, Various | Loan Specific Premarketing Term Sheet Agellan Portfolio | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $172,000,000 73.1% 1.78x 9.0% |

The Loan. The Agellan Portfolio mortgage loan, with an aggregate outstanding balance of $403.0 million (the “Agellan Portfolio Whole Loan”), is expected to be originated on or about July 15, 2020 (the “Origination Date”). We cannot assure you that all or any portion of the Agellan Portfolio Whole Loan will be originated. Furthermore, the terms of the final Agellan Portfolio Whole Loan documents may differ, and in some cases, materially differ, from the terms as described herein.

The Agellan Portfolio Whole Loan is expected to be a fixed rate loan secured by first mortgages encumbering the borrowers’ fee simple interests in a 46 property portfolio of industrial and office properties in the aggregate comprising of approximately 6,094,177 sq. ft. located throughout nine states (the “Agellan Portfolio” or the “Agellan Properties”). The Agellan Portfolio Whole Loan is expected to be evidenced by (i) seven senior pari passu notes with an aggregate Cut-off Date principal balance of $231.0 million (the “Agellan Portfolio Senior Notes”) and (ii) a controlling subordinate fixed rate Note B with a Cut-off Date principal balance of $172.0 million (the “Agellan Portfolio Subordinate Note”). The Agellan Portfolio Senior Notes will be senior to the Agellan Portfolio Subordinate Note. The Agellan Portfolio Subordinate Note and two of the Agellan Portfolio Senior Notes, Note A-1 and Note A-5 will be contributed to the Benchmark 2020-B18 mortgage trust, but the Agellan Portfolio Subordinate Note will not be included in the mortgage pool. Payments allocated to the Agellan Portfolio Subordinate Note will be paid to the holders of the Loan-Specific Certificates as described in “Description of the Mortgage Pool—The Whole Loans—The Serviced AB Whole Loan—The Agellan Portfolio Whole Loan” in the Preliminary Prospectus.

The relationship between the holders of the Agellan Portfolio Whole Loan will be governed by a co-lender agreement as described under “Description of the Mortgage Pool—The Whole Loans—The Serviced AB Whole Loan—Agellan Portfolio Whole Loan” in the Preliminary Prospectus.

| Total Debt Summary | |||||

| Note | Original Balance | Cut-off Date Balance | Note Holder | Controlling Piece | |

| Note A-1 | $75,000,000 | $75,000,000 | Benchmark 2020-B18 | No | |

| Note A-2 | 50,000,000 | 50,000,000 | JPMCB(1) | No | |

| Note A-3 | 30,000,000 | 30,000,000 | JPMCB(1) | No | |

| Note A-4 | 30,000,000 | 30,000,000 | JPMCB(1) | No | |

| Note A-5 | 25,000,000 | 25,000,000 | JPMCB(1) | No | |

| Note A-6 | 11,000,000 | 11,000,000 | JPMCB(1) | No | |

| Note A-7 | 10,000,000 | 10,000,000 | JPMCB(1) | No | |

| Total Senior Notes | $231,000,000 | $231,000,000 | |||

| Note B(2) | $172,000,000 | $172,000,000 | BMARK 2020-B18 | Yes(3) | |

| Whole Loan | $403,000,000 | $403,000,000 | |||

| Mezzanine Loan | $31,000,000 | $31,000,000 | Third Party | No | |

| Total Debt | $434,000,000 | $434,000,000 | |||

| (1) | Expected to be contributed to one or more future securitizations. |

| (2) | The Agellan Portfolio Subordinate Note will be subordinate in right of payment to the Agellan Portfolio Senior Notes. |

| (3) | The controlling Note B will be contributed to the issuing entity but will not be included in the mortgage pool. Payments allocated to the Agellan Portfolio Subordinate Note will be paid to the holders of the Loan-Specific Certificates as described in “Description of the Mortgage Pool—The Whole Loans—The Serviced AB Whole Loan—The Agellan Portfolio Whole Loan” in the Preliminary Prospectus. |

The Agellan Portfolio Whole Loan has a 61-month interest-only term. The Agellan Portfolio Senior Notes accrue interest a fixed rate of approximately 4.62820% per annum and the Agellan Portfolio Subordinate Note accrue interest at fixed rate of approximately 4.40000% per annum. The proceeds of the Agellan Portfolio Whole Loan were used to pay off existing debt encumbering 46 of the Agellan Properties of approximately $418.9 million, pay closing costs of approximately $5.7 million and fund escrows of approximately $11.6 million. As of year-end 2019, the Borrower Sponsor had a cost basis of approximately $507.8 million. The Borrower Sponsor’s total cash equity in the Agellan Portfolio will be approximately $185.5 million.

| Sources and Uses | ||||||

| Sources | Proceeds | % of Total | Uses | Proceeds | % of Total | |

| Senior Notes | $231,000,000 | 53.0% | Loan Payoff(1) | $418,924,922 | 95.7% | |

| Subordinate Note | 172,000,000 | 39.4% | TI/LC Reserve | 6,410,963 | 1.5% | |

| Mezzanine Loan | 31,000,000 | 7.1% | Required Repairs Reserve | 2,985,266 | 0.7% | |

| Sponsor Equity | 2,163,638 | 0.5% | Working Capital Reserve | 2,000,000 | 0.5% | |

| Gap Rent Reserve | 172,050 | 0.0% | ||||

| Closing Costs | 5,670,436 | 1.3% | ||||

| Total Sources | $436,163,638 | 100.0% | Total Uses | $436,163,638 | 100.0% | |

| (1) | Represents the refinance of the 42 of the Agellan Properties that were previously securitized in the MSC 2019-AGLN transaction and the balance sheet financing associated with the Sponsors’ recent acquisition of four of the Agellan Properties. |

9

Various Various, Various | Loan Specific Premarketing Term Sheet Agellan Portfolio | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $172,000,000 73.1% 1.78x 9.0% |

The Borrowers / Borrower Sponsor. The borrowers are Chicago Industrial Properties 1 LP, a Delaware limited partnership, Corridor Park LP, a Delaware limited partnership, Norcross Springs LP, a Delaware limited partnership, 6100 McIntosh LP, a Delaware limited partnership, 6100 McIntosh Vacant LP, a Delaware limited partnership, Agellan Commercial REIT U.S. L.P., a Delaware limited partnership, Continental Drive LP, a Delaware limited partnership, 9385 Washington Blvd. L.P., a Delaware limited partnership, Agellan Warrenville L.P., a Delaware limited partnership, 1300 Cox Avenue LP, a Delaware limited partnership and San Antonio Industrial One LP, a Delaware limited partnership each structured to be a bankruptcy-remote entity with two independent directors in its organizational structure (collectively, the “Borrowers”). Legal counsel to the Borrowers delivered a non-consolidation opinion in connection with the origination of the Agellan Portfolio Whole Loan. The Borrowers are indirectly owned and controlled by Elad Canada, Inc. (the “Borrower Sponsor” or “ELAD Canada”), a privately held, commercial real estate company specializing in the acquisition and development of commercial and residential properties. ELAD Canada was founded in 1997 and is based in Toronto, Canada. ELAD Canada has focused its business in central Canada, acquiring income producing properties, as well as development sites. As of 2020, ELAD Canada has 7.4 million square feet of income producing space, as well as 4.4 million square feet of construction in the pipeline and 6,000 residential units under development. Under the terms of the loan documents, Elad Genesis Limited Partnership, a subsidiary of the Borrower Sponsor, is the non-recourse carveout guarantor for the Agellan Portfolio Whole Loan and is required to maintain a minimum net worth of $100 million during the term of the loan. ELAD Canada is a part of the ELAD Group. Founded in 1992, ELAD Group is a real estate conglomerate with development projects in North America, Europe and Israel. ELAD Group has developed successful condominiums, hotels and mixed-use projects making its mark as a significant developer of ultra-luxury properties in New York City, like the Plaza Hotel. ELAD Group is focused on the acquisition, development and conversion of architecturally significant residential and commercial properties in key markets throughout North America.

The Borrower Sponsor has notified JPMCB that the controlling shareholder of the entity that owns ELAD Canada Realty Inc., has entered into a non-binding memorandum of understanding (“MOU”) to sell certain shares in Elad Canada Realty Inc., including and initial 37% of such shares to a joint venture between Plaza Partners and Argent Ventures. The non-binding MOU includes a call option in favor of the buyers and a put option in favor of the seller for the remaining 63% of ELAD Group. If the purchase of the 37% stake occurs, the buyers will take over day-to-day operations of ELAD Canada Realty Inc. In the event the transaction moves forward, the Borrower Sponsor anticipates the closing to occur in September 2020, assuming receipt of required regulatory and other approvals. Argent Ventures is a vertically-integrated, diversified real estate investment and development firm specializing in opportunistic, and value-add transactions through the United States. Founded in 1997 and headquartered in New York City, Argent Ventures pursues debt- and equity- related investments in multiple asset classes. Since its inception, Argent Ventures has purchased over $2.5 billion in real estate assets and debt instruments in major markets in the United States and Europe. Founded in 1981, Plaza Partners is a real estate developer and asset manager that focuses on rezoning and developing residential properties in strong urban locations within the greater Toronto area. Plaza Partners’ current portfolio includes approximately four million square feet of potential density. Under the terms of the loan agreement, the lender is expected to have the right to consent to the proposed sale.

10

Various Various, Various | Loan Specific Premarketing Term Sheet Agellan Portfolio | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $172,000,000 73.1% 1.78x 9.0% |

COVID-19 Update. As of June 1, 2020, the Agellan Properties have remained open; however, many office tenants have chosen to work remotely. The underwritten rent rolls as of the June 1, 2020, the Agellan Properties were approximately 93.4% occupied (inclusive of dark tenants and known vacates). For April, May and June of 2020, tenants representing approximately 97.7%, 96.7% and 97.0% of net rentable area, respectively, have paid rent in-full, with the Borrower Sponsor having collected approximately 97.8%, 97.8% and 96.6% of underwritten base rent, respectively. The top ten tenants, representing 38.6% of NRA and 41.0% of underwritten rent, had no issues with rent payment. 32 tenants representing approximately 5.5% of the underwritten base rent and 5.4% of the Agellan Properties net rentable have requested rent relief or have partial or no collections for the months of April, May and June. The five largest tenants that have put in formal requests for relief represent approximately 2.0% of NRA and approximately 1.8% of U/W Base Rent.

As of June 2020, none of the tenants have been granted a rent deferral and 25 tenants (totaling 5.4% of NRA) are in discussions with the borrowers for rent relief.

| COVID-19 Impact on Rent Collections | |||||||||||||

| No. | Property | Market | Property Type | Impacted Tenant Sq. Ft. | % of Total Sq.Ft. | Lease Expiration | U/W Potential Gross Rent | U/W Gross Rent Loss | % Unpaid April Gross Rent | % Unpaid May Gross Rent | % Unpaid June Gross Rent | Formal Relief Request (Yes/No) | |

| 26 | Rothway | Houston | Industrial | 29,230 | 0.5% | 2/28/2021 | $405,904 | $40,590 | 0.0% | 0.0% | 0.0% | Yes | |

| 38 | Cox Business Center | Cincinnati | Industrial | 27,040 | 0.4% | 4/30/2024 | $171,271 | $17,127 | 100.0% | 77.0% | 0.0% | Yes | |

| 16 | Long Point Center | Houston | Industrial | 24,482 | 0.4% | 9/30/2022 | $156,103 | $15,610 | 0.0% | 77.0% | 100.0% | Yes | |

| 14 | Norcross Center | Atlanta | Industrial | 19,848 | 0.3% | 5/31/2021 | $133,557 | $13,356 | 100.0% | 59.5% | 59.5% | Yes | |

| 13 | West by Northwest Business Blvd | Houston | Industrial | 18,790 | 0.3% | 1/31/2023 | $180,886 | $18,089 | 100.0% | 100.0% | 0.0% | No | |

| 23 | Minimax | Houston | Industrial | 17,500 | 0.3% | 11/30/2020 | $103,332 | $10,333 | 0.0% | 100.0% | 100.0% | Yes | |

| 12 | Southpark Business Park M | Austin | Industrial | 14,361 | 0.2% | 1/31/2022 | $255,120 | $25,512 | 0.0% | 0.0% | 69.0% | No | |

| 16 | Long Point Center | Houston | Industrial | 13,500 | 0.2% | 10/31/2020 | $87,699 | $8,770 | 0.0% | 0.0% | 0.0% | Yes | |

| 25 | 9385 Washington Blvd | Baltimore | Industrial | 10,800 | 0.2% | 8/31/2021 | $140,888 | $14,089 | 0.0% | 0.0% | 100.0% | No | |

| 25 | 9385 Washington Blvd | Baltimore | Industrial | 10,800 | 0.2% | 9/30/2022 | $122,654 | $12,265 | 100.0% | 88.6% | 23.8% | Yes | |

| 14 | Norcross Center | Atlanta | Industrial | 10,706 | 0.2% | 9/30/2023 | $83,966 | $8,397 | 100.0% | 100.0% | 0.0% | Yes | |

| 16 | Long Point Center | Houston | Industrial | 9,900 | 0.2% | 9/30/2022 | $79,757 | $7,976 | 0.0% | 77.0% | 100.0% | Yes | |

| 11 | Silber Industrial Park | Houston | Industrial | 9,746 | 0.2% | 6/30/2022 | $99,599 | $9,960 | 0.0% | 0.0% | 0.0% | Yes | |

| 28 | Columbus West - Interchange Rd | Columbus | Industrial | 9,500 | 0.2% | 9/30/2023 | $68,537 | $6,854 | 0.0% | 0.0% | 0.0% | Yes | |

| 12 | Southpark Business Park M | Austin | Industrial | 9,153 | 0.2% | 12/31/2020 | $182,305 | $18,231 | 100.0% | 100.0% | 100.0% | Yes | |

| 25 | 9385 Washington Blvd | Baltimore | Industrial | 9,000 | 0.1% | 4/30/2024 | $92,786 | $9,279 | 0.0% | 0.0% | 24.7% | No | |

| 25 | 9385 Washington Blvd | Baltimore | Industrial | 9,000 | 0.1% | 6/30/2024 | $94,934 | $9,493 | 0.0% | 0.0% | 100.0% | No | |

| 25 | 9385 Washington Blvd | Baltimore | Industrial | 8,990 | 0.1% | 12/31/2022 | $94,829 | $9,483 | 100.0% | 85.7% | 100.0% | Yes | |

| 18 | Southport 1-4 | Houston | Industrial | 8,385 | 0.1% | 5/31/2021 | $79,190 | $7,919 | 100.0% | 98.3% | 0.0% | No | |

| 18 | Southport 1-4 | Houston | Industrial | 7,937 | 0.1% | 12/31/2022 | $62,968 | $6,297 | 0.0% | 0.0% | 100.0% | Yes | |

| 9 | Sandy Plains Business Park | Atlanta | Industrial | 6,586 | 0.1% | 5/31/2021 | $73,210 | $7,321 | 100.0% | 100.0% | 100.0% | Yes | |

| 9 | Sandy Plains Business Park | Atlanta | Industrial | 6,422 | 0.1% | 8/31/2021 | $72,827 | $7,283 | 100.0% | 100.0% | 100.0% | Yes | |

| 15 | Goshen Springs | Atlanta | Industrial | 6,391 | 0.1% | 7/31/2020 | $41,231 | $4,123 | 100.0% | 100.0% | 100.0% | Yes | |

| 21 | Braker Center 4 | Austin | Industrial | 5,390 | 0.1% | 10/31/2023 | $117,169 | $11,717 | 0.0% | 0.0% | 0.0% | Yes | |

| 9 | Sandy Plains Business Park | Atlanta | Industrial | 4,550 | 0.1% | 11/30/2021 | $55,218 | $5,522 | 0.0% | 0.0% | 0.0% | Yes | |

| 22 | Northgreen 1-4 | Houston | Industrial | 3,969 | 0.1% | 12/31/2021 | $41,690 | $4,169 | 100.0% | 100.0% | 100.0% | Yes | |

| 11 | Silber Industrial Park | Houston | Industrial | 3,884 | 0.1% | 6/30/2022 | $39,693 | $3,969 | 0.0% | 0.0% | 0.0% | Yes | |

| 18 | Southport 1-4 | Houston | Industrial | 3,600 | 0.1% | 1/31/2023 | $34,889 | $3,489 | 0.0% | 0.0% | 0.0% | Yes | |

| 11 | Silber Industrial Park | Houston | Industrial | 2,950 | 0.0% | 10/31/2020 | $25,369 | $2,537 | 66.0% | 100.0% | 36.2% | No | |

| 32 | 1351 Oakbrook Drive | Atlanta | Industrial | 2,700 | 0.0% | 7/31/2021 | $25,478 | $2,548 | 100.0% | 100.0% | 100.0% | Yes | |

| 32 | 1351 Oakbrook Drive | Atlanta | Industrial | 2,300 | 0.0% | 2/28/2022 | $26,715 | $2,672 | 0.0% | 100.0% | 100.0% | Yes | |

| 22 | Northgreen 1-4 | Houston | Industrial | 1,950 | 0.0% | 6/30/2021 | $20,015 | $2,001 | 0.0% | 95.1% | 100.0% | Yes | |

| Total | 329,360 | 5.4% | $3,269,792 | $326,979 | |||||||||

11

Various Various, Various | Loan Specific Premarketing Term Sheet Agellan Portfolio | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $172,000,000 73.1% 1.78x 9.0% |

The Properties.

The Agellan Portfolio consists of the fee simple interests in a 46 property portfolio of industrial and office properties comprising approximately 6,094,177 sq. ft. in the aggregate located throughout nine states and 12 different markets. The Agellan Portfolio is comprised of 42 industrial properties (5,248,373 sq. ft.; 86.1% of NRA; 71.3% of U/W Base Rent) and four office properties (845,804 sq. ft.; 13.9% of NRA; 28.7% of U/W Base Rent). The tenancy spans a variety of industries including health care, food services, automotive parts, insurance, and technology.

As of June 1, 2020, the Agellan Portfolio is 93.4% leased (90.4% leased excluding dark tenants and known vacates) to 250 unique tenants with no single tenant accounting for more than 6.9% of U/W Base Rent. Three of the top ten tenants (Health Care Service Corp., General Motors LLC and Allstate Insurance Co.) have investment grade credit ratings by one or more of Moody’s, Fitch or S&P and account for approximately 10.7% and 15.0% of the Agellan Portfolio’s Total NRA and U/W Base Rent, respectively. The Agellan Properties have a weighted average remaining lease term of approximately 2.9 years.

| Portfolio Summary | |||||||||||||||||||

| No. | Property Name | City, State | Property Type | Net Rentable Area | Whole Loan Allocated Loan Amount | (%) Whole Loan Allocated Loan Amount | U/W Base Rent(1) | % of UW Base Rent | Appraised Value | % of Appraised Value | |||||||||

| 1 | Sarasota Distribution Hub | Sarasota, FL | Industrial | 906,449 | $52,400,000 | 13.0% | $4,804,386 | 11.7% | $70,200,000 | 12.7% | |||||||||

| 2 | Naperville Woods Office Center | Naperville, IL | Office | 482,497 | $51,600,000 | 12.8% | $7,480,569 | 18.2% | $68,800,000 | 12.5% | |||||||||

| 3 | Southpark Business Park FOP | Austin, TX | Industrial | 187,075 | $25,720,000 | 6.4% | $2,478,202 | 6.0% | $34,900,000 | 6.3% | |||||||||

| 4 | Supervalu | Fort Worth, TX | Industrial | 253,800 | $19,540,000 | 4.8% | $1,573,560 | 3.8% | $26,720,000 | 4.8% | |||||||||

| 5 | Plainfield Business Center IV | Plainfield, IN | Industrial | 434,354 | $17,630,000 | 4.4% | $1,385,853 | 3.4% | $24,100,000 | 4.4% | |||||||||

| 6 | Beltway III | Houston, TX | Office | 130,566 | $14,870,000 | 3.7% | $2,347,444 | 5.7% | $20,100,000 | 3.6% | |||||||||

| 7 | 4405 Continental Dr | Flint, MI | Industrial | 400,000 | $13,880,000 | 3.4% | $2,097,244 | 5.1% | $18,750,000 | 3.4% | |||||||||

| 8 | Beltway IV | Houston, TX | Office | 131,702 | $12,600,000 | 3.1% | $1,714,514 | 4.2% | $17,200,000 | 3.1% | |||||||||

| 9 | Sandy Plains Business Park | Marietta, GA | Industrial | 167,329 | $11,500,000 | 2.9% | $1,141,184 | 2.8% | $15,700,000 | 2.8% | |||||||||

| 10 | Silber Industrial Park | Houston, TX | Industrial | 198,970 | $10,310,000 | 2.6% | $882,818 | 2.2% | $14,100,000 | 2.6% | |||||||||

| 11 | Southpark Business Park M | Austin, TX | Industrial | 72,550 | $9,600,000 | 2.4% | $958,626 | 2.3% | $13,100,000 | 2.4% | |||||||||

| 12 | Coliseum Distribution Center #1 | San Antonio, TX | Industrial | 208,000 | $9,540,000 | 2.4% | $942,656 | 2.3% | $15,900,000 | 2.9% | |||||||||

| 13 | West by Northwest Business Blvd | Houston, TX | Industrial | 122,750 | $9,400,000 | 2.3% | $823,053 | 2.0% | $12,800,000 | 2.3% | |||||||||

| 14 | Norcross Center | Norcross, GA | Industrial | 169,951 | $9,000,000 | 2.2% | $942,051 | 2.3% | $12,300,000 | 2.2% | |||||||||

| 15 | Goshen Springs | Norcross, GA | Industrial | 152,319 | $7,830,000 | 1.9% | $718,035 | 1.8% | $10,700,000 | 1.9% | |||||||||

| 16 | Long Point Center | Houston, TX | Industrial | 189,680 | $7,610,000 | 1.9% | $741,097 | 1.8% | $10,400,000 | 1.9% | |||||||||

| 17 | Corridor Park D | Austin, TX | Industrial | 56,100 | $7,530,000 | 1.9% | $674,322 | 1.6% | $10,300,000 | 1.9% | |||||||||

| 18 | Southport 1-4 | Houston, TX | Industrial | 149,401 | $7,310,000 | 1.8% | $658,567 | 1.6% | $10,000,000 | 1.8% | |||||||||

| 19 | Jameel | Houston, TX | Industrial | 94,900 | $7,310,000 | 1.8% | $684,408 | 1.7% | $10,000,000 | 1.8% | |||||||||

| 20 | Beltway II | Houston, TX | Office | 101,039 | $7,100,000 | 1.8% | $214,432 | 0.5% | $9,700,000 | 1.8% | |||||||||

| 21 | Braker Center 4 | Austin, TX | Industrial | 45,913 | $6,900,000 | 1.7% | $579,872 | 1.4% | $9,400,000 | 1.7% | |||||||||

| 22 | Northgreen 1-4 | Houston, TX | Industrial | 118,736 | $6,300,000 | 1.6% | $474,118 | 1.2% | $8,600,000 | 1.6% | |||||||||

| 23 | Minimax | Houston, TX | Industrial | 119,821 | $5,920,000 | 1.5% | $568,098 | 1.4% | $8,100,000 | 1.5% | |||||||||

| 24 | Southpark Business Park E | Austin, TX | Industrial | 49,966 | $5,500,000 | 1.4% | $587,600 | 1.4% | $7,500,000 | 1.4% | |||||||||

| 25 | 9385 Washington Blvd | Laurel, MD | Industrial | 57,590 | $5,340,000 | 1.3% | $426,784 | 1.0% | $7,300,000 | 1.3% | |||||||||

| 26 | Rothway | Houston, TX | Industrial | 75,460 | $5,270,000 | 1.3% | $297,597 | 0.7% | $7,200,000 | 1.3% | |||||||||

| 27 | 2730 Pinnacle | Elgin, IL | Industrial | 44,990 | $4,500,000 | 1.1% | $454,404 | 1.1% | $6,100,000 | 1.1% | |||||||||

| 28 | Columbus West - Interchange Rd | Columbus, OH | Industrial | 91,200 | $4,130,000 | 1.0% | $404,218 | 1.0% | $5,650,000 | 1.0% | |||||||||

| 29 | 1346 Oakbrook Drive | Norcross, GA | Industrial | 71,591 | $3,950,000 | 1.0% | $441,662 | 1.1% | $5,400,000 | 1.0% | |||||||||

| 30 | 1230-1236 Hardt Circle | Bartlett, IL | Industrial | 60,080 | $3,800,000 | 0.9% | $287,187 | 0.7% | $5,200,000 | 0.9% | |||||||||

| 31 | Pine Forest Business Park | Houston, TX | Industrial | 80,091 | $3,600,000 | 0.9% | $106,122 | 0.3% | $4,900,000 | 0.9% | |||||||||

| 32 | 1351 Oakbrook Drive | Norcross, GA | Industrial | 36,489 | $2,820,000 | 0.7% | $188,866 | 0.5% | $3,850,000 | 0.7% | |||||||||

| 33 | 1325 Oakbrook Drive | Norcross, GA | Industrial | 53,120 | $2,800,000 | 0.7% | $299,472 | 0.7% | $3,800,000 | 0.7% | |||||||||

| 34 | 490 Heartland Drive | Sugar Grove, IL | Industrial | 39,520 | $2,740,000 | 0.7% | $304,704 | 0.7% | $3,750,000 | 0.7% | |||||||||

| 35 | 1265 Oakbrook Drive | Norcross, GA | Industrial | 51,200 | $2,700,000 | 0.7% | $287,275 | 0.7% | $3,650,000 | 0.7% | |||||||||

| 36 | Columbus West - Business Park(2) | Columbus, OH | Industrial | 92,618 | $2,600,000 | 0.6% | $0 | 0.0% | $3,500,000 | 0.6% | |||||||||

| 37 | 1155 Bowes Road(3) | Elgin, IL | Industrial | 34,400 | $2,520,000 | 0.6% | $0 | 0.0% | $3,450,000 | 0.6% | |||||||||

| 38 | 1280 Oakbrook Drive | Norcross, GA | Industrial | 46,400 | $2,500,000 | 0.6% | $261,118 | 0.6% | $3,400,000 | 0.6% | |||||||||

| 39 | Rittiman East Industrial Park #23 & 24 | San Antonio, TX | Industrial | 50,806 | $2,320,000 | 0.6% | $308,606 | 0.8% | $3,870,000 | 0.7% | |||||||||

| 40 | 2002 Bloomingdale | Glendale Heights, IL | Industrial | 31,919 | $2,230,000 | 0.6% | $194,877 | 0.5% | $3,050,000 | 0.6% | |||||||||

| 41 | 333 Charles Court | West Chicago, IL | Industrial | 36,623 | $2,200,000 | 0.5% | $277,441 | 0.7% | $3,000,000 | 0.5% | |||||||||

| 42 | 483 Heartland Drive | Sugar Grove, IL | Industrial | 36,426 | $2,200,000 | 0.5% | $172,234 | 0.4% | $3,000,000 | 0.5% | |||||||||

| 43 | Cox Business Center | Erlanger, KY | Industrial | 52,040 | $2,180,000 | 0.5% | $247,686 | 0.6% | $3,350,000 | 0.6% | |||||||||

| 44 | 1256 Oakbrook Drive | Norcross, GA | Industrial | 40,392 | $2,160,000 | 0.5% | $191,411 | 0.5% | $2,950,000 | 0.5% | |||||||||

| 45 | 550 Heartland | Sugar Grove, IL | Industrial | 30,328 | $1,940,000 | 0.5% | $203,700 | 0.5% | $2,650,000 | 0.5% | |||||||||

| 46 | Rittiman East Industrial Park #22 | San Antonio, TX | Industrial | 37,026 | $1,600,000 | 0.4% | $184,961 | 0.5% | $2,610,000 | 0.5% | |||||||||

| Total | 6,094,177 | $403,000,000 | 100.0% | $41,013,036 | 100.0% | $551,000,000 | 100.0% | ||||||||||||

| (1) | U/W Base Rent has been further adjusted to account for a 10.0% stress to tenants who missed full or partial rent payments in April, May and/or June or have requested rent relief during the COVID-19 pandemic. The total stress to U/W Base Rent is $241,419. An additional stress loss adjustment of 10.0% was applied to reimbursements for any tenants that missed full rent payments in April, May and/or June. The total stress to reimbursements is $85,560. |

| (2) | The Columbus West – Business Park property is currently 100.0% vacant and has been underwritten as such. |

| (3) | The 1155 Bowes Road property is leased to a single tenant that is currently dark. The tenant is underwritten as vacant. |

12

Various Various, Various | Loan Specific Premarketing Term Sheet Agellan Portfolio | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $172,000,000 73.1% 1.78x 9.0% |

| Portfolio Summary (continued) | |||||||||||

| No. | Property Name | Market | Property Type | Property Sub-Type | Net Rentable Area | Property Occupancy | Year Built | Year Renovated | Ceiling Height | Percent Office | Appraisal Cap Rate(1) |

| 1 | Sarasota Distribution Hub | Tampa | Industrial | Warehouse/Distribution | 906,449 | 100.0% | 1981 | 2007 | 28' | 5.0% | 6.75% |

| 2 | Naperville Woods Office Center | Chicago | Office | Suburban | 482,497 | 95.4% | 1981, 1988 | 2007 | NAP | 100.0% | 8.25% |

| 3 | Southpark Business Park FOP | Austin | Industrial | Flex | 187,075 | 100.0% | 1982 | NAP | 16' | 96.0% | 6.25% |

| 4 | Supervalu | Dallas | Industrial | Warehouse/Distribution | 253,800 | 100.0% | 1996 | NAP | 32' | 7.0% | 6.50% |

| 5 | Plainfield Business Center IV | Indianapolis | Industrial | Warehouse/Distribution | 434,354 | 100.0% | 1999 | NAP | 30' | 3.5% | 5.75% |

| 6 | Beltway III | Houston | Office | CBD | 130,566 | 100.0% | 2005 | NAP | NAP | 100.0% | 8.00% |

| 7 | 4405 Continental Dr | Flint | Industrial | Warehouse/Distribution | 400,000 | 100.0% | 1999 | 2006 | 30' | 2.0% | 9.50% |

| 8 | Beltway IV | Houston | Office | CBD | 131,702 | 72.6% | 2006 | NAP | NAP | 100.0% | 8.50% |

| 9 | Sandy Plains Business Park | Atlanta | Industrial | Flex | 167,329 | 94.3% | 1986 | NAP | 20' | 40.0% - 95.0% | 7.00% |

| 10 | Silber Industrial Park | Houston | Industrial | Warehouse/Distribution | 198,970 | 90.4% | 1978 | NAP | 21' - 24' | 13.0% | 6.50% |

| 11 | Southpark Business Park M | Austin | Industrial | Flex | 72,550 | 100.0% | 1983 | NAP | 16' | 96.0% | 6.75% |

| 12 | Coliseum Distribution Center #1 | San Antonio | Industrial | Warehouse/Distribution | 208,000 | 100.0% | 1978 | NAP | 26.5' | 5.0% | 6.00% |

| 13 | West by Northwest Business Blvd | Houston | Industrial | Flex | 122,750 | 91.5% | 1983 | NAP | 19' | 34.0% | 7.00% |

| 14 | Norcross Center | Atlanta | Industrial | Flex | 169,951 | 100.0% | 1988 | NAP | 20' | 33.0% | 7.00% |

| 15 | Goshen Springs | Atlanta | Industrial | Flex | 152,319 | 95.3% | 1986 | NAP | 26' | 33.0% | 6.25% / 6.75% |

| 16 | Long Point Center | Houston | Industrial | Warehouse/Distribution | 189,680 | 94.3% | 1979 | NAP | 24' | 11.0% | 7.50% / 7.25% |

| 17 | Corridor Park D | Austin | Industrial | Flex | 56,100 | 100.0% | 1999 | 2016 | 24' | 100.0% | 6.50% |

| 18 | Southport 1-4 | Houston | Industrial | Flex | 149,401 | 77.7% | 1980 | NAP | 16' | 33.0% | 8.00% |

| 19 | Jameel | Houston | Industrial | Flex | 94,900 | 87.5% | 1983 | NAP | 19' | 50.0% | 6.75% |

| 20 | Beltway II | Houston | Office | CBD | 101,039 | 13.3% | 2003 | NAP | NAP | 100.0% | 9.00% |

| 21 | Braker Center 4 | Austin | Industrial | Flex | 45,913 | 90.3% | 1984 | 1999 | 16' | 95.0% | 6.50% |

| 22 | Northgreen 1-4 | Houston | Industrial | Flex | 118,736 | 61.7% | 1982 | NAP | 12’ – 18’ | 35.0% | 8.00% |

| 23 | Minimax | Houston | Industrial | Warehouse/Distribution | 119,821 | 100.0% | 1967 | NAP | 20' | 13.0% | 6.50% |

| 24 | Southpark Business Park E | Austin | Industrial | Flex | 49,966 | 100.0% | 1982 | 1992 | 16' | 100.0% | 6.75% |

| 25 | 9385 Washington Blvd | Baltimore | Industrial | Flex | 57,590 | 92.2% | 1988 | 2007 | 18' | 20.0% | 6.00% |

| 26 | Rothway | Houston | Industrial | Flex | 75,460 | 43.8% | 1983 | NAP | 14' | 90.0% | 7.00% |

| 27 | 2730 Pinnacle | Chicago | Industrial | Warehouse/Distribution | 44,990 | 100.0% | 2005 | 2007 | 20' | 45.0% | 7.50% |

| 28 | Columbus West - Interchange Rd | Columbus | Industrial | Flex | 91,200 | 89.5% | 1974 | NAP | 22' | 20.0% | 8.00% |

| 29 | 1346 Oakbrook Drive | Atlanta | Industrial | Flex | 71,591 | 100.0% | 1985 | NAP | 14' | 85.0% | 7.25% |

| 30 | 1230-1236 Hardt Circle | Chicago | Industrial | Warehouse/Distribution | 60,080 | 75.1% | 2008 | NAP | 24' | 10.0% | 6.25% |

| 31 | Pine Forest Business Park | Houston | Industrial | Warehouse/Distribution | 80,091 | 30.9% | 1980 | NAP | 20' - 22' | 14.0% | 7.00% |

| 32 | 1351 Oakbrook Drive | Atlanta | Industrial | Flex | 36,489 | 68.5% | 1985 | NAP | 12' | 72.0% | 7.00% |

| 33 | 1325 Oakbrook Drive | Atlanta | Industrial | Flex | 53,120 | 100.0% | 1986 | NAP | 20' | 21.0% | 7.00% |

| 34 | 490 Heartland Drive | Chicago | Industrial | Warehouse/Distribution | 39,520 | 100.0% | 2002 | NAP | 20' | 20.0% | 7.50% |

| 35 | 1265 Oakbrook Drive | Atlanta | Industrial | Flex | 51,200 | 100.0% | 1985 | NAP | 18' | 21.0% | 7.00% |

| 36 | Columbus West - Business Park | Columbus | Industrial | Flex | 92,618 | 0.0% | 1996 | 2005 | 25' | 20.0% | 8.00% |

| 37 | 1155 Bowes Road | Chicago | Industrial | Warehouse/Distribution | 34,400 | 0.0% | 2006 | NAP | 26' | 20.0% | 6.50% |

| 38 | 1280 Oakbrook Drive | Atlanta | Industrial | Flex | 46,400 | 100.0% | 1986 | NAP | 19' | 27.0% | 7.25% |

| 39 | Rittiman East Industrial Park #23 & 24 | San Antonio | Industrial | Flex | 50,806 | 90.6% | 1983 | NAP | 16’ - 18' | 19.0% | 7.50% |

| 40 | 2002 Bloomingdale | Chicago | Industrial | Warehouse/Distribution | 31,919 | 100.0% | 1998 | NAP | 23' | 15.0% | 6.00% |

| 41 | 333 Charles Court | Chicago | Industrial | Warehouse/Distribution | 36,623 | 100.0% | 2007 | NAP | 20' | 20.0% | 7.25% |

| 42 | 483 Heartland Drive | Chicago | Industrial | Warehouse/Distribution | 36,426 | 84.1% | 2010 | NAP | 24' | 10.0% | 6.50% |

| 43 | Cox Business Center | Cincinnati | Industrial | Warehouse/Distribution | 52,040 | 100.0% | 1987 | NAP | 15' - 19' | 10.0% | 7.25% |

| 44 | 1256 Oakbrook Drive | Atlanta | Industrial | Flex | 40,392 | 87.5% | 1985 | NAP | 20' | 28.0% | 7.00% |

| 45 | 550 Heartland | Chicago | Industrial | Warehouse | 30,328 | 100.0% | 2000 | 2007 | 20' | 15.0% | 6.50% |

| 46 | Rittiman East Industrial Park #22 | San Antonio | Industrial | Warehouse/Distribution | 37,026 | 83.8% | 1983 | NAP | 18' | 14.0% | 7.50% |

| (1) | Napverville Woods Office Center, Goshen Spring and Long Point Center have multiple buildings that were appraised separately. |

| Property Distribution | ||||||||||

| Property Type | Number of Properties | Total Sq. Ft. | % of Total Sq. Ft. | Allocated Whole Loan Amount | (%) Allocated Whole Loan Amount | U/W Base Rent | % of U/W Base Rent | Appraised Value | % of Appraised Value | |

| Industrial | 42 | 5,248,373 | 86.1% | $316,830,000 | 78.6% | $29,256,078 | 71.3% | $435,200,000 | 79.0% | |

| Warehouse / Distribution | 18 | 3,164,189 | 51.9% | $164,400,000 | 40.8% | $15,225,330 | 37.1% | $226,680,000 | 41.1% | |

| Flex | 23 | 2,053,856 | 33.7% | $150,490,000 | 37.3% | $13,827,048 | 33.7% | $205,870,000 | 37.4% | |

| Warehouse | 1 | 30,328 | 0.5% | $1,940,000 | 0.5% | $203,700 | 0.5% | $2,650,000 | 0.5% | |

| Office | 4 | 845,804 | 13.9% | $86,170,000 | 21.4% | $11,756,958 | 28.7% | $115,800,000 | 21.0% | |

| Suburban | 1 | 482,497 | 7.9% | $51,600,000 | 12.8% | $7,480,569 | 18.2% | $68,800,000 | 12.5% | |

| CBD | 3 | 363,307 | 6.0% | $34,570,000 | 8.6% | $4,276,389 | 10.4% | $47,000,000 | 8.5% | |

| Portfolio Total | 46 | 6,094,177 | 100.0% | $403,000,000 | 100.0% | $41,013,036 | 100.0% | $551,000,000 | 100.0% | |

Since May 2019, the Borrower Sponsor has executed 38 new, renewal and expansion leases for approximately 470,218 sq. ft. Renewal leases totaled approximately 342,447 sq. ft. and had weighted average rent increases of approximately 8.7%. Renewal and expansion leases totaled approximately 43,983 sq. ft. and had weighted average rent increases of 16.1%. New leases accounted for approximately 78,344 sq. ft. and had weighted average rent increases of 8.3%.

| Portfolio Leasing Spreads(1) | ||||||

| Lease Type | Expiring sq. ft. | Expiring Rent per sq. ft. | New sq. ft. | Rent per sq. ft. | Leasing Spread $ | Leasing Spread % |

| Renew | 342,447 | $8.58 | 342,447 | $9.32(2) | $0.75 | 8.7% |

| Renew & Expansion | 28,284 | $6.23 | 43,983 | $7.24 | $1.01 | 16.1% |

| Expansion | 11,252 | $6.00 | 5,444 | $5.84 | ($0.16)(3) | (2.7%)(3) |

| New | 109,848 | $6.71 | 78,344 | $7.27 | $0.56 | 8.3% |

| (1) | Since May 2019. |

| (2) | The leasing spread for Dish Network, Inc. is calculated based a gross renewal rent of $8.70 per sq. ft. |

| (3) | International Valve at the 483 Heartland Drive property expanded and took 5,444 sq. ft. of the 11,252 sq. ft. of vacated space. The expansion increased the tenant’s footprint to 11,032 sq. ft. and the rent for the NRA occupied prior to the expansion (5,588 sq. ft.) also increased $0.16 per sq. ft. or 2.4%. |

13

Various Various, Various | Loan Specific Premarketing Term Sheet Agellan Portfolio | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $172,000,000 73.1% 1.78x 9.0% |

| Historical and Current Portfolio Occupancy(1)(2)(3) | ||||||||||

| 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | Current(4) | Current W/ Dark Tenants(5) | Current W/ Dark Tenants and Known Vacates(6) | |

| # of Assets(7) | 21 | 21 | 28 | 31 | 40 | 42 | 42 | 46 | 46 | 46 |

| Portfolio NRA Sq. ft. (mm) | 3,224 | 3,224 | 3,689 | 4,917 | 5,631 | 5,745 | 5,745 | 6,094 | 6,094 | 6,094 |

| % Occupancy | 91.8% | 91.0% | 94.4% | 93.3% | 94.7% | 96.1% | 96.2% | 90.4% | 92.1% | 93.4% |

| (1) | Historical occupancy data for the four recent acquisitions is not available. |

| (2) | Historical occupancy for 2013 – 2019 is reflective of quarterly averages for each respective year. |

| (3) | Historical occupancy for 2013 – 2019 includes any applicable leased dark space. |

| (4) | Current occupancy is based on the underwritten rent roll dated June 1, 2020 and excludes dark, known vacate, and bankrupt tenants. |

| (5) | Current W/ Dark Tenants occupancy is inclusive of dark tenants. |

| (6) | Current W/ Dark Tenants and Known Vacates occupancy is inclusive of dark and known vacate tenants. |

| (7) | # of Assets may vary from the “Portfolio Operating History” below as certain properties have not provided occupancy history. |

| Top 10 Tenant Summary(1) | |||||||

| Tenant | Property Type | Credit Rating (Moody's/Fitch/S&P)(2) | Net Rentable Area (Sq. Ft.) | % of Net Rentable Area | U/W Base Rent PSF(3) | % of Total U/W Base Rent | Lease Expiration |

| Health Care Service Corp.(4)(5) | Office | A3/A-/AA- | 177,114 | 2.9% | $16.00 | 6.9% | 11/30/2025 |

| United Natural Foods Inc.(6) | Industrial | B2/NR/B | 463,172 | 7.6% | $5.66 | 6.4% | 7/31/2022 |

| ALDI, Inc.(4)(7) | Office | NR/NR/NR | 137,986 | 2.3% | $16.09 | 5.4% | 12/31/2028 |

| General Motors LLC(8) | Industrial | Baa3/BBB-/BBB | 400,000 | 6.6% | $5.24 | 5.1% | 8/31/2021 |

| Moran Foods LLC(9) | Industrial | B3/NR/B- | 253,800 | 4.2% | $6.20 | 3.8% | 9/30/2025 |

| Life Technologies Corporation(10) | Industrial | Baa1/NR/BBB+ | 103,645 | 1.7% | $13.00 | 3.3% | 6/30/2025 |

| Allstate Insurance Co.(11) | Office | Aa3/A+/AA- | 75,623 | 1.2% | $16.00 | 3.0% | 5/31/2024 |

| Ceva Freight LLC(12) | Industrial | B1/NR/B+ | 333,397 | 5.5% | $3.09 | 2.5% | 8/31/2022 |

| Beall's, Inc. (13) | Industrial | NR/NR/NR | 200,000 | 3.3% | $4.80 | 2.3% | 9/30/2021 |

| VTech Communications, Inc.(14) | Industrial | NR/NR/NR | 208,000 | 3.4% | $4.53 | 2.3% | 7/31/2022 |

| Total Major Tenants | 2,352,737 | 38.6% | $7.16 | 41.0% | |||

| Other Tenants | 3,156,625 | 51.8% | $7.66 | 59.0% | |||

| Total Occupied | 5,509,362 | 90.4% | $7.44 | 100.0% | |||

| Vacant | 584,815 | 9.6% | |||||

| Total / Wtd. Avg. | 6,094,177 | 100.0% | $7.44 | 100.0% | |||

| (1) | Based on the underwritten rent roll. |

| (2) | In certain instances, ratings provided are those of the parent company of the entity shown, whether or not the parent company guarantees the lease. |

| (3) | U/W Base Rent PSF is inclusive of contractual rent steps taken through June 1, 2021. |

| (4) | ALDI, Inc. reflects an expansion option for 24,597 sq. ft. that was exercised in February 2020. The expansion space is currently occupied by HCSC. HCSC will be relocated within the Naperville Wood Office Center property as part of the ALDI, Inc. expansion, which will allow HCSC to have all of its office space in one building. Additionally, HCSC’s overall footprint will increase slightly with the relocation space from 175,080 sq. ft. to 177,114 sq. ft. The expansion and relocation are estimated to occur in June/July 2021. |

| (5) | Health Care Service Corp. has one, five-year renewal option at market rent. |

| (6) | United Natural Foods, Inc. has one, five-year renewal option at market rent. |

| (7) | ALDI, Inc. has one, five-year renewal option at market rent. |

| (8) | General Motors LLC has two, five-year renewal options at the greater of market rent or 90% of the then-current base rent. |

| (9) | Moran Foods LLC has two, seven-year renewal options at $6.75 per sq. ft. and market rent, respectively. |

| (10) | Life Technologies Corporation has one, five-year renewal option beginning at $13.00 per sq. ft. |

| (11) | Allstate Insurance Co. has two, five-year renewal options upon nine months’ notice at 95% of market rent. Allstate Insurance also has a one-time termination option as of any month end between May 2022 and May 2023. |

| (12) | Ceva Freight LLC has two, five-year renewal options at market rent. |

| (13) | In May 2018 Beall’s Inc. vacated and subleased their space to United Natural Foods Inc. Beall’s Inc. has one, three-year renewal option at $5.30 per sq. ft. |

| (14) | VTech Communications, Inc. has one, five-year renewal option at market rent. |

14

Various Various, Various | Loan Specific Premarketing Term Sheet Agellan Portfolio | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $172,000,000 73.1% 1.78x 9.0% |

| Lease Rollover Schedule(1)(2) | ||||||||

| Year | # of Leases Expiring | Total Expiring Sq. Ft. | % of Total Sq. Ft. Expiring | Cumulative Sq. Ft. Expiring | Cumulative % of Sq. Ft. Expiring | Annual U/W Base Rent per sq. ft.(3) | % U/W Base Rent Rolling | Cumulative % of U/W Base Rent |

| 2020 & MTM | 43 | 460,033 | 7.5% | 460,033 | 7.5% | $5.87 | 6.6% | 6.6% |

| 2021(4) | 61 | 1,264,748 | 20.8% | 1,724,781 | 28.3% | $6.24 | 19.3% | 25.8% |

| 2022(5) | 45 | 1,523,829 | 25.0% | 3,248,610 | 53.3% | $5.64 | 20.9% | 46.8% |

| 2023 | 38 | 470,932 | 7.7% | 3,719,542 | 61.0% | $8.73 | 10.0% | 56.8% |

| 2024 | 33 | 633,520 | 10.4% | 4,353,062 | 71.4% | $7.11 | 11.0% | 67.8% |

| 2025 | 18 | 786,447 | 12.9% | 5,139,509 | 84.3% | $10.09 | 19.3% | 87.1% |

| 2026 | 3 | 50,301 | 0.8% | 5,189,810 | 85.2% | $9.02 | 1.1% | 88.2% |

| 2027 | 5 | 112,643 | 1.8% | 5,302,453 | 87.0% | $15.54 | 4.3% | 92.5% |

| 2028 | 3 | 202,643 | 3.3% | 5,505,096 | 90.3% | $14.60 | 7.2% | 99.7% |

| 2029 | 0 | 0 | 0.0% | 5,505,096 | 90.3% | $0.00 | 0.0% | 99.7% |

| 2030 & Thereafter | 1 | 4,266 | 0.1% | 5,509,362 | 90.4% | $26.98 | 0.3% | 100.0% |

| Vacant | NAP | 584,815 | 9.6% | 6,094,177 | 100.0% | NAP | NAP | |

| Total / Wtd. Avg. | 250 | 6,094,177 | 100.0% | $7.44 | 100.0% | |||

| (1) | Based on the underwritten rent roll. |

| (2) | Certain tenants may have lease termination options that are exercisable prior to the stated expiration date of the subject lease or leases which are not considered in the lease rollover schedule. |

| (3) | Annual U/W Base Rent per sq. ft. is inclusive of (i) contractual rent steps taken through June 1, 2021 and includes the ALDI, Inc. expansion of approximately 24,597 sq. ft. and HCSC relocation at the Naperville Woods Office Center property. U/W Base Rent has been further adjusted to account for a 10.0% stress to tenants who missed full or partial April and/or May rent payments and/or have requested rent relief during the COVID-19 pandemic. The total stress to U/W Base Rent is $241,419. |

| (4) | General Motors, LLC leases will expire in 2021 and has two, five-year renewal options at the greater of market rent or 90% of the then-current base rent. General Motors, LLC has occupied the property since 1998. General Motors has expressed interest to renew and is expecting to receive a formal proposal with renewal terms from the Sponsor. |

| (5) | Both United Natural Foods, Inc. and Ceva Freight LLC leases will expire in 2022. United Natural Foods, Inc. has one, five-year renewal option at market rent. Ceva Freight LLC has two, five-year renewal options at market rent. United Natural Foods Inc. and Ceva Freight have both engaged the Borrower Sponsor about potentially expanding at expiration if any space were to become vacant at the respective properties. |

Ongoing Reserves.

TI/LC Reserve. The Borrowers are required to deposit into the TI/LC reserve, on a monthly basis 1/12 of $0.85 per sq. ft. of the Agellan Properties then encumbered by the lien of the Agellan Portfolio Whole Loan (approximately $431,671 as of the Origination Date), subject to a cap of the amount equal to 36 times the required monthly deposit (approximately $15.5 million as of the Origination Date).

Replacement Reserve. The Borrowers are required to deposit into the replacement reserve, on a monthly basis 1/12 of $0.20 per sq. ft. of the Agellan Properties then encumbered by the lien of the Agellan Portfolio Whole Loan (approximatelt $101,570 as of the Origination Date), subject to a cap of the amount equal to 36 times the required monthly deposit (approximately $3.7 million as of the Origination Date).

The ongoing TI/LC Reserve and Replacement Reserve are among other reserves as more fully described in the “Initial and Ongoing Reserves” section below.

Major Tenants.

The top five tenants occupying the Agellan Properties by U/W Base Rent are Health Care Service Crop. (177,114 sq. ft.; 2.9% of NRA; 6.9% of U/W Base Rent), United Natural Foods, Inc. (463,172 sq. ft.; 7.6% of NRA; 6.4% of U/W Base Rent), ALDI, Inc. (137,986 sq. ft.; 2.3% of NRA; 5.4% of U/W Base Rent), General Motors LLC (400,000 sq. ft.; 6.6% of NRA; 5.1% of U/W Base Rent) and Moran Foods LLC (253,800 sq. ft.; 4.2% of NRA; 3.8% of U/W Base Rent).

Health Care Service Corp. (177,114 sq. ft.; 2.9% of NRA; 6.9% of U/W Base Rent). Health Care Service Corp. (“HCSC”) is an independent licensee of the Blue Cross and Blue Shield Association. HCSC is the largest customer-owned health insurer in the United States and fifth largest overall. Health Care Service Corp operates through Blue Cross and Blue Shield Plans in Illinois, Montana, New Mexico, Oklahoma and Texas. HCSC affiliates and subsidiaries such as Dearborn National, Medecision and Dental Network of America offer group life, disability and dental solutions, as well as a range of other individual solutions. The company, founded in 1936, serves more than 16 million members across five states and employs more than 23,000 people in over 60 local offices. A portion of the space occupied by HCSC will be relocated within the Naperville Wood Office Center property in conjunction with the ALDI, Inc. expansion, which will allow HCSC to have all of its office space in one building. Additionally, HCSC’s overall footprint will increases slightly with the relocation space from 175,080 sq. ft. to 177,114 sq. ft. The expansion and relocation are estimated to occur in June/July 2021. Health Care Service Corp. has one, five-year renewal option at market rent.

United Natural Foods, Inc. (463,172 sq. ft.; 7.6% of NRA; 6.4% of U/W Base Rent). United Natural Foods, Inc. engages in the distribution

15

Various Various, Various | Loan Specific Premarketing Term Sheet Agellan Portfolio | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $172,000,000 73.1% 1.78x 9.0% |

of natural, organic, and specialty foods and non-food products. The company is headquartered in Providence, Rhode Island. United Natural Foods, Inc. has one, five-year renewal option at market rent.

ALDI, Inc. (137,986 sq. ft.; 2.3% of NRA; 5.4% of U/W Base Rent). ALDI, Inc. owns and operates grocery stores throughout the U.S. ALDI, Inc. offers grocery, meat, fresh produce, wine and beer, beverages, and other home products. ALDI, Inc. is located in Batavia, Illinois. ALDI, Inc. has approximately 3,000 total employees across all of its locations and generates approximately $4.32 billion in sales annually. ALDI, Inc. operated approximately 1,955 stores in across 36 states. In February 2020, ALDI, Inc. exercised an expansion option for an additional 24,597 sq. ft. ALDI, Inc. has one, five-year renewal option at market rent.

General Motors LLC (400,000 sq. ft.; 6.6% of NRA; 5.1% of U/W Base Rent). General Motors LLC is the fourth largest automaker globally and the largest in the U.S. with approximately $246.6 billion in total assets. Headquartered in Detroit, Michigan, General Motors LLC’s brands include Chevrolet, Buick, GMC and Cadillac. General Motors LLC has two, five-year renewal options at the greater of market rent or 90% of the then-current base rent.

Moran Foods LLC (253,800 sq. ft.; 4.2% of NRA; 3.8% of U/W Base Rent). Moran Foods LLC is the parent company of Save-A-Lot Holdings, LLC (“Save-A-Lot”). Save-A-Lot is an American discount grocery store chain with approximately 1,300 stores across 36 states with over $4.0 billion in annual sales. Headquartered in St. Louis, Missouri, Save-A-Lot’s stores carry most grocery products, including an assortment of fresh, canned and frozen produce as well as meat, meal products, household items and everyday groceries. Moran Foods LLC has two, seven-year renewal options at $6.75 per sq. ft. and market rent, respectively.

The Market. The Agellan Portfolio is geographically diverse with properties located across nine states which include the top five states by U/W Base Rent, Texas (46.1% of Whole Loan allocated loan amount (“Whole Loan ALA”); 43.4% of U/W Base Rent), Illinois (18.3% of Whole Loan ALA; 22.9% of U/W Base Rent), Florida (13.0% of Whole Loan ALA; 11.7% of U/W Base Rent), Georgia (11.2% of Whole Loan ALA; 10.9% of U/W Base Rent) and Michigan (3.4% of Whole Loan ALA; 5.1% of U/W Base Rent).

| Geographic Distribution | ||||||||||

| State | Number of Properties | Total Sq. Ft. | % of Total Sq. Ft. | Allocated Whole Loan Amount | (%) Allocated Whole Loan Amount | U/W Base Rent | % of U/W Base Rent | Appraised Value | % of Appraised Value | |

| Texas | 21 | 2,474,352 | 40.6% | $185,850,000 | 46.1% | $17,800,674 | 43.4% | $257,400,000 | 46.7% | |

| Illinois | 9 | 796,783 | 13.1% | 73,730,000 | 18.3% | 9,375,116 | 22.9% | 99,000,000 | 18.0% | |

| Florida | 1 | 906,449 | 14.9% | 52,400,000 | 13.0% | 4,804,386 | 11.7% | 70,200,000 | 12.7% | |

| Georgia | 9 | 788,791 | 12.9% | 45,260,000 | 11.2% | 4,471,074 | 10.9% | 61,750,000 | 11.2% | |

| Michigan | 1 | 400,000 | 6.6% | 13,880,000 | 3.4% | 2,097,244 | 5.1% | 18,750,000 | 3.4% | |

| Indiana | 1 | 434,354 | 7.1% | 17,630,000 | 4.4% | 1,385,853 | 3.4% | 24,100,000 | 4.4% | |

| Ohio | 2 | 183,818 | 3.0% | 6,730,000 | 1.7% | 404,218 | 1.0% | 9,150,000 | 1.7% | |

| Maryland | 1 | 57,590 | 0.9% | 5,340,000 | 1.3% | 426,784 | 1.0% | 7,300,000 | 1.3% | |

| Kentucky | 1 | 52,040 | 0.9% | 2,180,000 | 0.5% | 247,686 | 0.6% | 3,350,000 | 0.6% | |

| Portfolio Total | 46 | 6,094,177 | 100.0% | $403,000,000 | 100.0% | $41,013,036 | 100.0% | $551,000,000 | 100.0% | |

The Agellan Portfolio is located across 12 U.S. markets which include the top five markets by U/W Base Rent, Houston (24.2% of Whole Loan ALA; 23.2% of U/W Base Rent), Chicago (18.3% of Whole Loan ALA; 22.9% of U/W Base Rent), Austin (13.7% of Whole Loan ALA; 12.9% of U/W Base Rent), Tampa (13.0% of Whole Loan ALA; 11.7% of U/W Base Rent) and Atlanta (11.2% of Whole Loan ALA; 10.9% of U/W Base Rent).

| Market Overview | |||||||||

| Market | Number of Properties | Total Sq. Ft. | % of Total Sq. Ft. | Allocated Whole Loan Amount | (%) Allocated Whole Loan Amount | U/W Base Rent | % of U/W Base Rent | Appraised Value | % of Appraised Value |

| Houston | 12 | 1,513,116 | 24.8% | $97,600,000 | 24.2% | $9,512,268 | 23.2% | $133,100,000 | 24.2% |

| Chicago | 9 | 796,783 | 13.1% | 73,730,000 | 18.3% | 9,375,116 | 22.9% | 99,000,000 | 18.0% |

| Austin | 5 | 411,604 | 6.8% | 55,250,000 | 13.7% | 5,278,622 | 12.9% | 75,200,000 | 13.6% |

| Tampa | 1 | 906,449 | 14.9% | 52,400,000 | 13.0% | 4,804,386 | 11.7% | 70,200,000 | 12.7% |

| Atlanta | 9 | 788,791 | 12.9% | 45,260,000 | 11.2% | 4,471,074 | 10.9% | 61,750,000 | 11.2% |

| Flint | 1 | 400,000 | 6.6% | 13,880,000 | 3.4% | 2,097,244 | 5.1% | 18,750,000 | 3.4% |

| Dallas | 1 | 253,800 | 4.2% | 19,540,000 | 4.8% | 1,573,560 | 3.8% | 26,720,000 | 4.8% |

| San Antonio | 3 | 295,832 | 4.9% | 13,460,000 | 3.3% | 1,436,224 | 3.5% | 22,380,000 | 4.1% |

| Indianapolis | 1 | 434,354 | 7.1% | 17,630,000 | 4.4% | 1,385,853 | 3.4% | 24,100,000 | 4.4% |

| Baltimore | 1 | 57,590 | 0.9% | 5,340,000 | 1.3% | 426,784 | 1.0% | 7,300,000 | 1.3% |

| Columbus | 2 | 183,818 | 3.0% | 6,730,000 | 1.7% | 404,218 | 1.0% | 9,150,000 | 1.7% |

| Cincinnati | 1 | 52,040 | 0.9% | 2,180,000 | 0.5% | 247,686 | 0.6% | 3,350,000 | 0.6% |

| Portfolio Total | 46 | 6,094,177 | 100.0% | $403,000,000 | 100.0% | $41,013,036 | 100.0% | $551,000,000 | 100.0% |

16

Various Various, Various | Loan Specific Premarketing Term Sheet Agellan Portfolio | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $172,000,000 73.1% 1.78x 9.0% |

Major Markets.

Houston. Per an industry data provider, the Houston Industrial market ended first quarter 2020 with a vacancy rate of 7.6%. The reported market vacancy rates for logistics and flex properties were 8.4% and 10.0%, respectively. The existing market inventory is made up of 74.6% logistics properties and 8.1% flex properties based on total sq. ft. Rental rates ended the first quarter at $7.42 per sq. ft. The average quoted rates for logistics and flex properties were $6.91 per sq. ft. and $10.61 per sq. ft., respectively. The 12-month net absorption ending in first quarter 2020 was 8,621,259 sq. ft. for logistics properties and -49,931 sq. ft. for flex properties.

Per an industry data provider, the Houston Office market ended first quarter 2020 with a vacancy rate of 16.8%. The reported vacancy rates for Class A and Class B buildings were 19.6% and 17.1%, respectively. The existing market inventory is comprised of 44.5% Class A, 42.8% Class B, and 12.6% Class C based on total sq. ft. The average quoted rental rate in first quarter 2020 for all classes was $28.36 per sq. ft. The average quoted rental rate for Class A and B was $34.07 per sq. ft. and $24.25 per sq. ft., respectively. The 12-month net absorption ending in first quarter 2020 for Class A & B in the market was 1,251,779 sq. ft. and -1,448,622 sq. ft., respectively.

| Historical Market Occupancy - Industrial(1) | ||||||||||||

| 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |

| 93.9% | 93.1% | 93.7% | 94.3% | 95.0% | 94.5% | 95.1% | 94.9% | 94.6% | 94.8% | 94.3% | 93.3% | |

| (1) | Source: Industry data provider. |

| Historical Market Occupancy - Office(1) | ||||||||||||

| 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |

| 88.4% | 86.7% | 86.9% | 87.2% | 88.4% | 88.6% | 89.4% | 87.1% | 85.5% | 84.0% | 83.8% | 83.4% | |

| (1) | Source: Industry data provider. |

Chicago. Per an industry data provider, the Chicago Industrial market ended first quarter 2020 with a vacancy rate of 6.2%. The reported market vacancy rates for logistics and flex properties were 7.1% and 7.6%, respectively. The existing market inventory is made up of 66.1% logistics properties and 5.8% flex properties based on total sq. ft. Rental rates ended the first quarter of 2020 at $7.36 per sq. ft. The average quoted rates for logistics and flex properties were $6.87 per sq. ft. and $12.24 per sq. ft., respectively. The 12-month net absorption ending in first quarter 2020 was 535,853 sq. ft. for flex properties and 14,631,591 sq. ft. for logistics properties.

Per an industry data provider, the Chicago Office market ended first quarter 2020 with a vacancy rate of 12.2%. The reported vacancy rates for Class A and Class B buildings were 15.2% and 11.7%, respectively. The existing market inventory is comprised of 39.0% Class A, 44.2% Class B, and 16.7% Class C based on total sq. ft. The average quoted rental rate in first quarter 2020 for all classes was $29.44 per sq. ft. The average quoted rental rate for Class A and B was $37.39 per sq. ft. and $25.20 per sq. ft., respectively. The 12-month net absorption ending in first quarter 2020 for Class A and B in the market was 3,566,358 sq. ft. and -457,122 sq. ft., respectively.

| Historical Market Occupancy - Industrial(1) | |||||||||||

| 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 |

| 89.8% | 88.1% | 88.2% | 89.1% | 90.6% | 91.3% | 92.6% | 93.2% | 93.8% | 93.7% | 94.2% | 94.1% |

| (1) | Source: Industry data provider. |

| Historical Market Occupancy - Office(1) | ||||||||||||

| 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |

| 87.4% | 85.0% | 85.2% | 85.6% | 86.1% | 86.6% | 87.3% | 88.0% | 87.7% | 88.0% | 88.4% | 87.9% | |

| (1) | Source: Industry data provider. |

Austin. The reported market vacancy rates for logistics and flex properties were 9.8% and 7.3%, respectively. The existing market inventory is made up of 60.5% logistics properties and 20.9% flex properties based on total sq. ft. Rental rates ended the first quarter at $11.30 per sq. ft. The average quoted rates for logistics and flex properties were $9.93 per sq. ft. and $14.31 per sq. ft., respectively. The 12-month net absorption ending in first quarter 2020 was 1,113,224 sq. ft. for logistics properties and 744,867 sq. ft. for flex properties. According to an industry data provider, Austin is expected to outperform the state of Texas and nation in 2020, with a high number of technology companies and housing at the forefront. Long term, Austin is viewed as a market with a well-educated labor force, high concentration of technology businesses and a relatively low cost of living compared to other high technology based industries which is anticipated to fuel a high population growth for the market.

| Historical Market Occupancy - Industrial(1) | ||||||||||||

| 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |

| 90.2% | 87.8% | 88.5% | 89.6% | 91.3% | 93.5% | 93.5% | 95.6% | 95.6% | 93.6% | 93.6% | 92.8% | |

| (1) | Source: Industry data provider. |

17

Various Various, Various | Loan Specific Premarketing Term Sheet Agellan Portfolio | Cut-off Date Balance: Cut-off Date LTV: U/W NCF DSCR: U/W NOI Debt Yield: | $172,000,000 73.1% 1.78x 9.0% |

Tampa. Per an industry data provider, the Tampa Bay Industrial market ended first quarter 2020 with a vacancy rate of 5.0%. The reported market vacancy rates for logistics properties was 5.4%. The existing market inventory is made up of 66.3% logistics properties based on total sq. ft. Rental rates ended the first quarter at $7.72 per sq. ft. The average quoted rates for logistics properties was $7.11 per sq. ft. The 12-month net absorption ending in first quarter 2020 for logistics properties was 2,025,279 sq. ft. According to an industry data provider as of year-end 2019, Tampa’s industrial sector outpaced the industrial sectors in the state of Florida in relation to demand growth at approximately 2.8 million sq. ft. of absorbed space. Tampa was the only market in the state that saw improved growth from approximately 2.7 million sq. ft. of positive net absorption year over year.

| Historical Market Occupancy - Industrial(1) | ||||||||||||

| 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |

| 92.3% | 89.4% | 89.3% | 89.8% | 90.2% | 91.6% | 92.3% | 93.8% | 95.0% | 95.1% | 95.3% | 95.1% | |

| (1) | Source: Third party data provider. |

Atlanta. Per an industry data provider, the Atlanta Industrial market ended first quarter 2020 with a vacancy rate of 6.1%. The reported market vacancy rates for logistics and flex properties were 6.7% and 5.5%, respectively. The existing market inventory is made up of 77.4% logistics properties and 9.1% flex properties based on total sq. ft. Rental rates ended the first quarter at $6.17 per sq. ft. The average quoted rates for logistics and flex properties were $5.52 per sq. ft. and $11.03 per sq. ft., respectively. The 12-month net absorption ending in first quarter 2020 was 11,337,139 sq. ft. for logistics properties and -202,543 sq. ft. for flex properties. According to an industry data provider, the Atlanta market is seen as Georgia’s main growth engine and one of the strongest economies in the nation. Job growth, in the Atlanta market outsize business services and has averaged approximately 2.0% as of year end 2019, which has been one of the best in the nation for nine consecutive years.

| Historical Market Occupancy - Industrial(1) | |||||||||||

| 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 |

| 87.5% | 86.4% | 85.6% | 86.9% | 87.5% | 88.7% | 91.5% | 93.1% | 93.0% | 94.1% | 94.6% | 94.4% |

| (1) | Source: Industry data provider. |

Environmental Matters. The Phase I environmental reports dated February 26, 2020 through March 26, 2020 recommended no further action at the Agellan Portfolio.

Cash Flow Analysis.

| Portfolio Operating History | ||||||

| 2015 | 2016 | 2017 | 2018 | 2019 | 2020 Budget | |