| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-206361-09 | ||

| March [8], 2017 | JPMDB 2017-C5 |

Free Writing Prospectus Structural and Collateral Term Sheet

| ||

JPMDB 2017-C5 | ||

| ||

This material is for your information, and none of J.P. Morgan Securities LLC (“JPMS”), Drexel Hamilton, LLC and Academy Securities, Inc., (each individually, an “Underwriter”, and together, the ‘‘Underwriters’’) are soliciting any action based upon it. This material is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

The depositor has filed a registration statement (including a prospectus) with the SEC (SEC File No. 333-206361) for the offering to which this free writing prospectus relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter or any dealer participating in the offering will arrange to send you the prospectus if you request it by calling (866) 669-7629 or by emailing the ABS Syndicate Desk atabs_synd@jpmorgan.com.

Neither this document nor anything contained in this document shall form the basis for any contract or commitment whatsoever. The information contained in this document is preliminary as of the date of this document, supersedes any previous such information delivered to you and will be superseded by any such information subsequently delivered prior to the time of sale. These materials are subject to change, completion or amendment from time to time.

This information is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change.

J.P. Morgan is the marketing name for the investment banking businesses of JPMorgan Chase & Co. and its subsidiaries worldwide. Securities, syndicated loan arranging, financial advisory and other investment banking activities are performed by JPMS and its securities affiliates, and lending, derivatives and other commercial banking activities are performed by JPMorgan Chase Bank, National Association and its banking affiliates. JPMS is a member of SIPC and the NYSE.

THE UNDERWRITERS MAY FROM TIME TO TIME PERFORM INVESTMENT BANKING SERVICES FOR, OR SOLICIT INVESTMENT BANKING BUSINESS FROM, ANY COMPANY NAMED IN THESE MATERIALS. THE UNDERWRITERS AND/OR THEIR AFFILIATES OR RESPECTIVE EMPLOYEES MAY FROM TIME TO TIME HAVE A LONG OR SHORT POSITION IN ANY CERTIFICATE OR CONTRACT DISCUSSED IN THESE MATERIALS.

| ||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 1 of 139 |

| March [8], 2017 | JPMDB 2017-C5 |

THE REPUBLIC OF KOREA

THIS PROSPECTUS IS NOT, AND UNDER NO CIRCUMSTANCES IS THIS PROSPECTUS TO BE CONSTRUED AS, A PUBLIC OFFERING OF SECURITIES IN KOREA. NEITHER THE ISSUER NOR ANY OF ITS AGENTS MAKE ANY REPRESENTATION WITH RESPECT TO THE ELIGIBILITY OF ANY RECIPIENTS OF THIS PROSPECTUS TO ACQUIRE THE OFFERED CERTIFICATES UNDER THE LAWS OF KOREA, INCLUDING, BUT WITHOUT LIMITATION, THE FOREIGN EXCHANGE TRANSACTION LAW AND REGULATIONS THEREUNDER (THE “FETL”). THE OFFERED CERTIFICATES HAVE NOT BEEN REGISTERED WITH THE FINANCIAL SERVICES COMMISSION OF KOREA FOR PUBLIC OFFERING IN KOREA, AND NONE OF THE OFFERED CERTIFICATES MAY BE OFFERED, SOLD OR DELIVERED, DIRECTLY OR INDIRECTLY, OR OFFERED OR SOLD TO ANY PERSON FOR RE-OFFERING OR RESALE, DIRECTLY OR INDIRECTLY IN KOREA OR TO ANY RESIDENT OF KOREA EXCEPT PURSUANT TO THE FINANCIAL INVESTMENT SERVICES AND CAPITAL MARKETS ACT AND THE DECREES AND REGULATIONS THEREUNDER (THE “FSCMA”), THE FETL AND ANY OTHER APPLICABLE LAWS, REGULATIONS AND MINISTERIAL GUIDELINES IN KOREA. WITHOUT PREJUDICE TO THE FOREGOING, THE NUMBER OF OFFERED CERTIFICATES OFFERED IN KOREA OR TO A RESIDENT OF KOREA SHALL BE LESS THAN FIFTY AND FOR A PERIOD OF ONE YEAR FROM THE ISSUE DATE OF THE OFFERED CERTIFICATES, NONE OF THE OFFERED CERTIFICATES MAY BE DIVIDED RESULTING IN AN INCREASED NUMBER OF OFFERED CERTIFICATES. FURTHERMORE, THE OFFERED CERTIFICATES MAY NOT BE RESOLD TO KOREAN RESIDENTS UNLESS THE PURCHASER OF THE OFFERED CERTIFICATES COMPLIES WITH ALL APPLICABLE REGULATORY REQUIREMENTS (INCLUDING, BUT NOT LIMITED TO, GOVERNMENT REPORTING APPROVAL REQUIREMENTS UNDER THE FETL AND ITS SUBORDINATE DECREES AND REGULATIONS) IN CONNECTION WITH THE PURCHASE OF THE OFFERED CERTIFICATES.

JAPAN

THE OFFERED CERTIFICATES HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDER THE FINANCIAL INSTRUMENTS AND EXCHANGE LAW OF JAPAN, AS AMENDED (THE “FIEL”), AND DISCLOSURE UNDER THE FIEL HAS NOT BEEN AND WILL NOT BE MADE WITH RESPECT TO THE OFFERED CERTIFICATES. ACCORDINGLY, EACH UNDERWRITER HAS REPRESENTED AND AGREED THAT IT HAS NOT, DIRECTLY OR INDIRECTLY, OFFERED OR SOLD AND WILL NOT, DIRECTLY OR INDIRECTLY, OFFER OR SELL ANY OFFERED CERTIFICATES IN JAPAN OR TO, OR FOR THE BENEFIT OF, ANY RESIDENT OF JAPAN (WHICH TERM AS USED IN THIS PROSPECTUS MEANS ANY PERSON RESIDENT IN JAPAN, INCLUDING ANY CORPORATION OR OTHER ENTITY ORGANIZED UNDER THE LAWS OF JAPAN) OR TO OTHERS FOR REOFFERING OR RE-SALE, DIRECTLY OR INDIRECTLY, IN JAPAN OR TO, OR FOR THE BENEFIT OF, ANY RESIDENT OF JAPAN EXCEPT PURSUANT TO AN EXEMPTION FROM THE REGISTRATION REQUIREMENTS OF, AND OTHERWISE IN COMPLIANCE WITH, THE FIEL AND OTHER RELEVANT LAWS, REGULATIONS AND MINISTERIAL GUIDELINES OF JAPAN. AS PART OF THIS OFFERING OF THE OFFERED CERTIFICATES, THE UNDERWRITERS MAY OFFER THE OFFERED CERTIFICATES IN JAPAN TO UP TO 49 OFFEREES IN ACCORDANCE WITH THE ABOVE PROVISIONS.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 2 of 139 |  |

| Structural and Collateral Term Sheet | JPMDB 2017-C5 | |

| Collateral Characteristics | ||

| Loan Pool | ||

| Initial Pool Balance (“IPB”): | $1,043,452,191 | |

| Number of Mortgage Loans: | 35 | |

| Number of Mortgaged Properties: | 50 | |

| Average Cut-off Date Balance per Mortgage Loan: | $29,812,920 | |

| Weighted Average Current Mortgage Rate: | 4.59769% | |

| 10 Largest Mortgage Loans as % of IPB: | 53.7% | |

| Weighted Average Remaining Term to Maturity(1): | 114 months | |

| Weighted Average Seasoning(1): | 3 months | |

| Credit Statistics | ||

| Weighted Average UW NCF DSCR(2)(3): | 2.03x | |

| Weighted Average UW NOI Debt Yield(2): | 11.4% | |

| Weighted Average Cut-off Date Loan-to-Value Ratio (“LTV”)(2)(4): | 58.8% | |

| Weighted Average Maturity Date LTV(2)(4): | 52.8% | |

| Other Statistics | ||

| % of Mortgage Loans with Additional Debt: | 29.6% | |

| % of Mortgaged Properties with Single Tenants: | 8.4% | |

| Amortization | ||

| Weighted Average Original Amortization Term(5): | 353 months | |

| Weighted Average Remaining Amortization Term(5): | 352 months | |

| % of Mortgage Loans with Partial Interest-Only followed by Amortizing Balloon: | 41.6% | |

| % of Mortgage Loans with Interest-Only: | 32.8% | |

| % of Mortgage Loans with Amortizing Balloon: | 25.6% | |

| Cash Management(6) | ||

| % of Mortgage Loans with In-Place, Hard Lockboxes: | 80.9% | |

| % of Mortgage Loans with Springing Lockboxes: | 17.8% | |

| % of Mortgage Loans with In-Place, Soft Lockboxes: | 1.2% | |

| % of Mortgage Loans with Springing Cash Management: | 71.4% | |

| % of Mortgage Loans with In-Place Cash Management: | 28.6% | |

| Reserves | ||

| % of Mortgage Loans Requiring Monthly Tax Reserves: | 81.0% | |

| % of Mortgage Loans Requiring Monthly Insurance Reserves: | 16.1% | |

| % of Mortgage Loans Requiring Monthly CapEx Reserves(7): | 67.3% | |

| % of Mortgage Loans Requiring Monthly TI/LC Reserves(8): | 45.8% | |

| (1) | In the case of the Loan No.18, the first payment date for the loan is May 1, 2017. On the Closing Date, JPMCB will deposit sufficient funds to pay the interest associated with the interest due for the April 2017 payment for the related loan. Information presented in this term sheet reflects the contractual loan terms. |

| (2) | In the case of Loan Nos. 1, 2, 3, 4, 5, 7, 8, 9, 10, 14, 16 and 25, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2, 4 and 9, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s). |

| (3) | In the case of Loan No. 9, the UW NCF DSCR is calculated using the sum of principal and interest payments over the first 12 months following the expiration of the interest-only period based on the assumed principal payment schedule provided on Annex G to the Preliminary Prospectus. |

| (4) | In the case of Loan Nos. 1, 5, 9, 11 and 12, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

| (5) | Excludes seven mortgage loans that are interest-only for the entire term. |

| (6) | For a more detailed description of Cash Management, refer to “Description of the Mortgage Pool—Certain Terms of the Mortgage Loans—Mortgaged Property Accounts” in the Preliminary Prospectus. |

| (7) | CapEx Reserves include FF&E reserves for hotel properties. |

| (8) | Calculated only with respect to the Cut-off Date Balance of mortgage loans secured or partially secured by office, retail, mixed use and industrial properties. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 3 of 139 | |

| Structural and Collateral Term Sheet | JPMDB 2017-C5 | |

| Collateral Characteristics | ||

Mortgage Loan Seller | Number of | Number of | Aggregate | % of |

| GACC(1)(2) | 21 | 26 | $652,817,515 | 62.6% |

| JPMCB(2) | 14 | 24 | 390,634,677 | 37.4 |

| Total: | 35 | 50 | $1,043,452,191 | 100.0% |

| (1) | With the exception of Loan No. 3, all of the loans for which GACC is the Mortgage Loan Seller, were originated by Deutsche Bank, AG, New York Branch (“DBNY”) (an affiliate of GACC). |

| (2) | In the case of Loan No. 2, the whole loan was co-originated by DBNY and Goldman Sachs Mortgage Company. In the case of Loan No. 4, the whole loan was co-originated by JPMCB, DBNY, Goldman Sachs Mortgage Company, Barclays Bank PLC and Morgan Stanley Bank, N.A. In the case of Loan No. 5, the whole loan was co-originated by DBNY, Citi Real Estate Funding Inc. and Bank of America, N.A. |

| Ten Largest Mortgage Loans | ||||||||||||

| No. | Loan Name | Mortgage Loan Seller | No. of Prop. | Cut-off Date Balance | % of IPB | SF/Units/ Rooms | Property Type | UW NCF DSCR(1)(1) | UW NOI Debt Yield(1) | Cut-off Date LTV(1)(3) | Maturity Date LTV(1)(3) | |

| 1 | 229 West 43rd Street Retail Condo | GACC | 1 | $80,000,000 | 7.7% | 248,457 | Retail | 1.75x | 7.5% | 60.6% | 60.6% | |

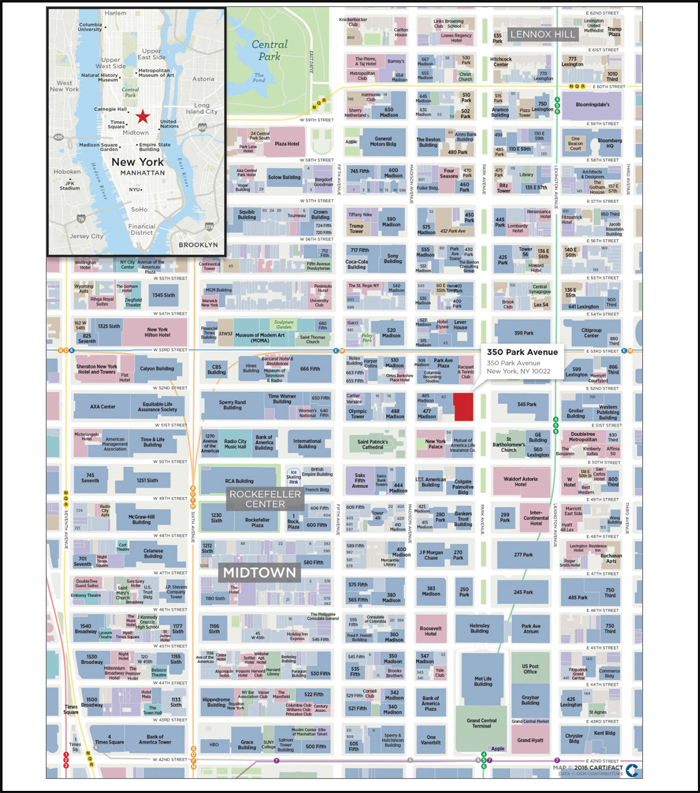

| 2 | 350 Park Avenue | GACC | 1 | $66,667,200 | 6.4% | 570,784 | Office | 2.98x | 12.0% | 41.7% | 41.7% | |

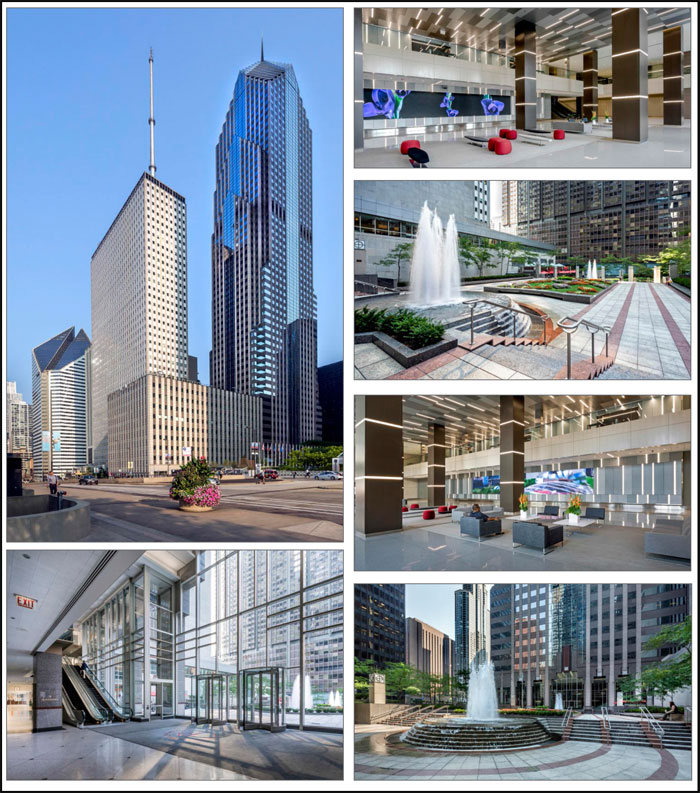

| 3 | Prudential Plaza | GACC | 1 | $65,000,000 | 6.2% | 2,269,632 | Office | 1.33x | 9.1% | 59.3% | 53.2% | |

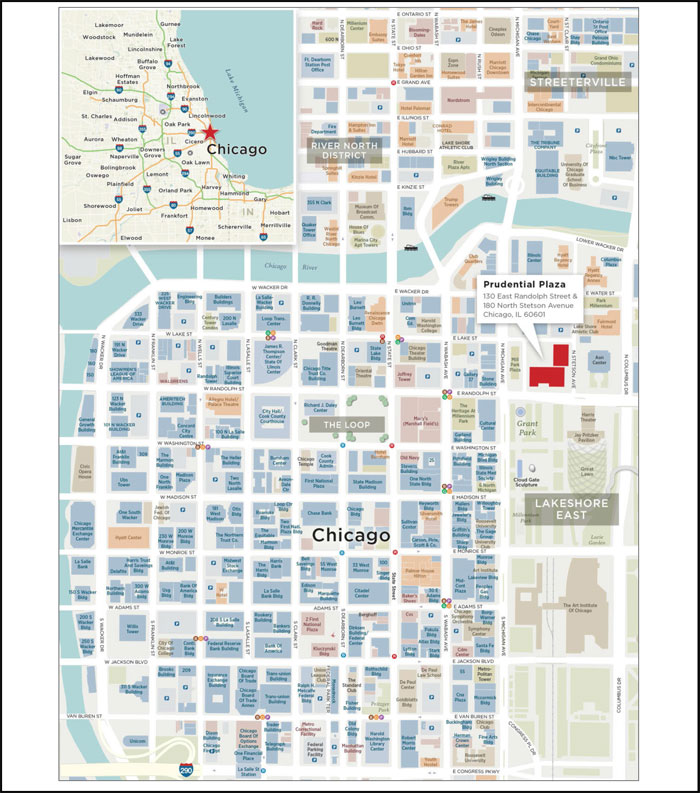

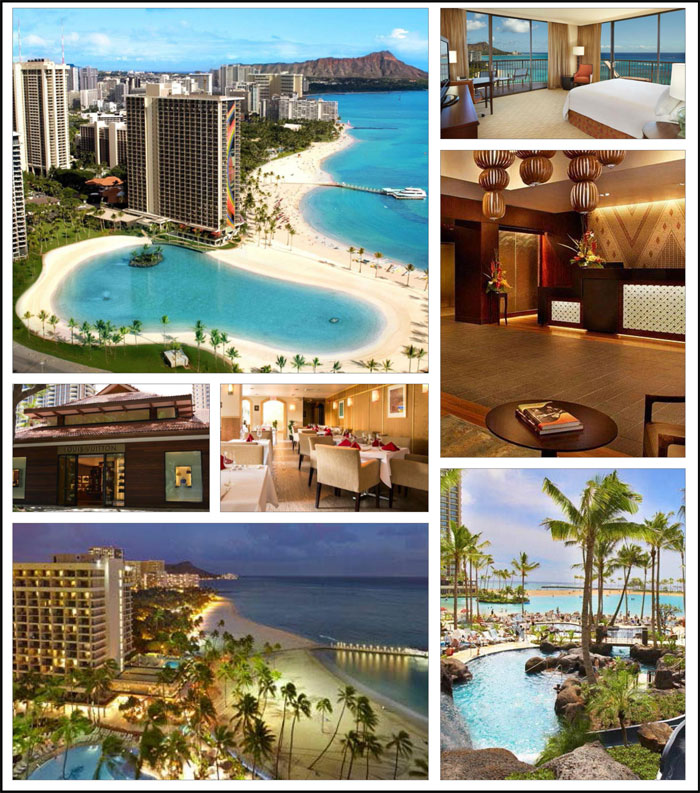

| 4 | Hilton Hawaiian Village | JPMCB | 1 | $62,250,000 | 6.0% | 2,860 | Hotel | 4.47x | 19.0% | 31.2% | 31.2% | |

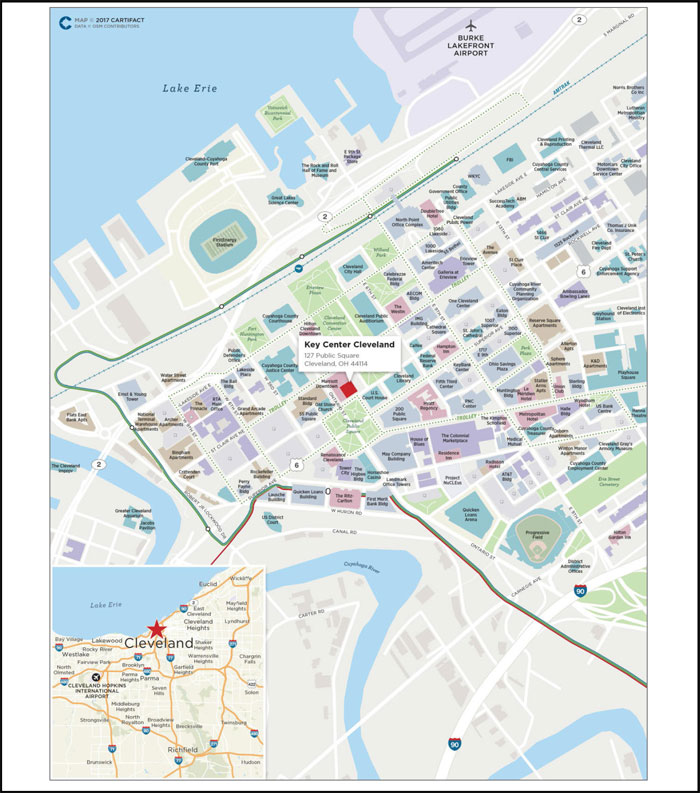

| 5 | Key Center Cleveland | GACC | 1 | $60,000,000 | 5.8% | 1,369,980 | Mixed Use | 1.59x | 12.3% | 60.8% | 49.6% | |

| 6 | Gateway I & II | GACC | 1 | $55,000,000 | 5.3% | 95,782 | Mixed Use | 1.20x | 7.7% | 71.4% | 62.8% | |

| 7 | Landmark Square | JPMCB | 1 | $49,000,000 | 4.7% | 757,917 | Mixed Use | 2.19x | 12.0% | 56.9% | 56.9% | |

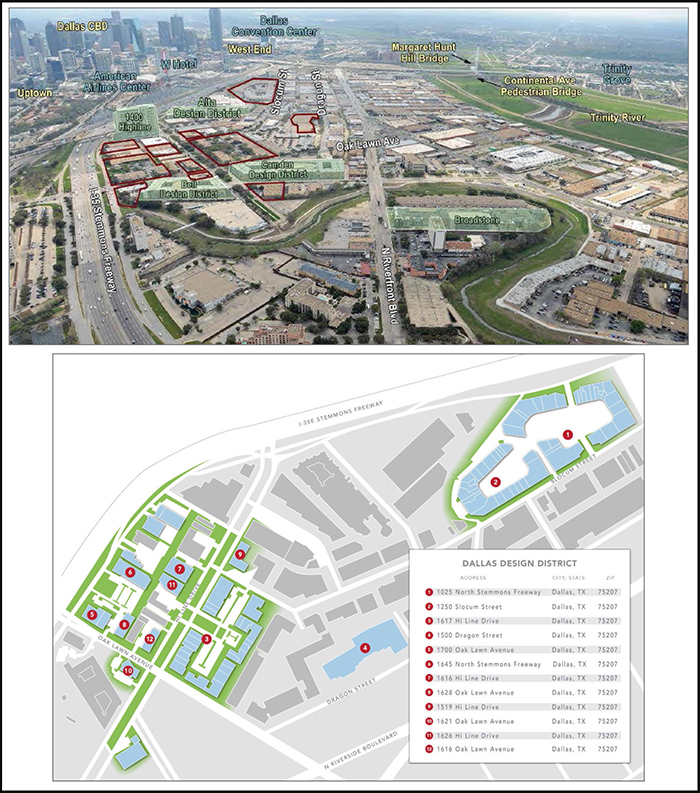

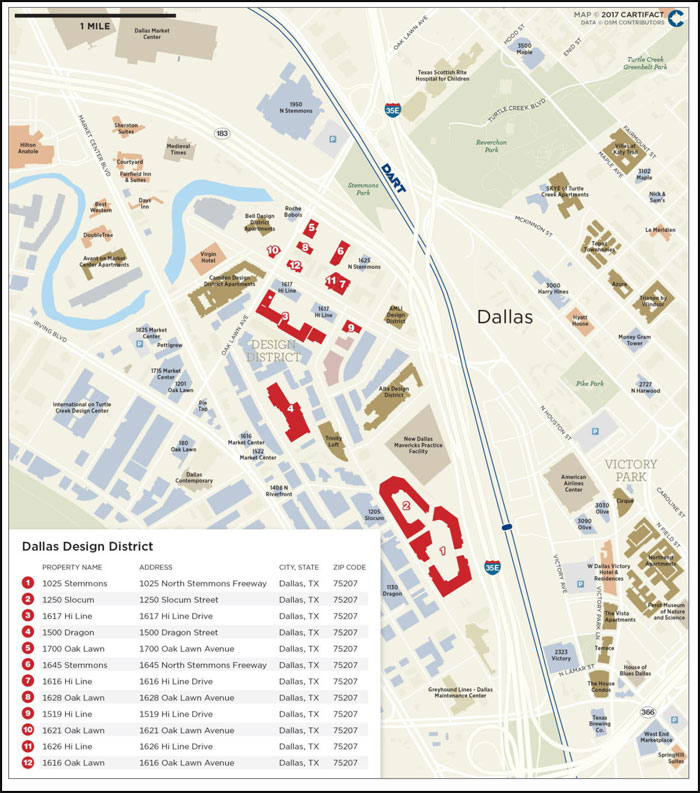

| 8 | Dallas Design District | JPMCB | 1 | $45,000,000 | 4.3% | 728,452 | Industrial | 1.28x | 9.4% | 62.1% | 55.3% | |

| 9 | Moffett Gateway | JPMCB | 1 | $40,000,000 | 3.8% | 612,691 | Office | 1.95x | 11.9% | 46.3% | 39.3% | |

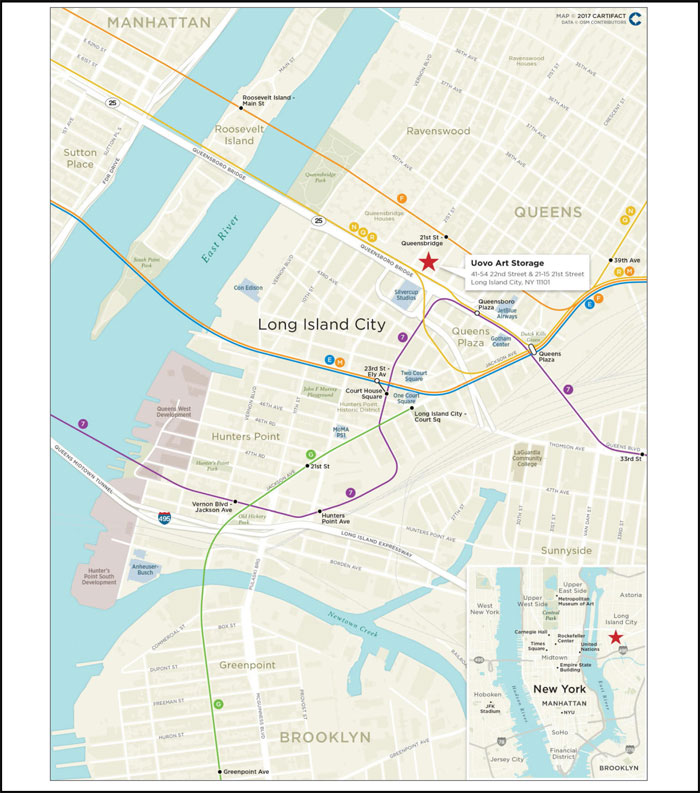

| 10 | Uovo Art Storage | GACC | 1 | $36,943,588 | 3.5% | 275,000 | Self Storage | 1.55x | 9.8% | 52.6% | 43.0% | |

| Top 3 Total/Weighted Average | 3 | $211,667,200 | 20.3% | 2.01x | 9.4% | 54.2% | 52.4% | |||||

| Top 5 Total/Weighted Average | 5 | $333,917,200 | 32.0% | 2.39x | 11.7% | 51.1% | 47.9% | |||||

| Top 10 Total/Weighted Average | 10 | $559,860,788 | 53.7% | 2.08x | 11.0% | 54.3% | 49.8% | |||||

| (1) | In the case of Loan Nos. 1, 2, 3, 4, 5, 7, 8, 9 and 10, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2, 4 and 9, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s). |

| (2) | In the case of Loan No. 9, the UW NCF DSCR is calculated using the sum of principal and interest payments over the first 12 payments following the expiration of the interest-only period based on the principal payment schedule provided in Annex G of the Preliminary Prospectus. |

| (3) | In the case of Loan Nos. 1, 5 and 9, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 4 of 139 | |

| Structural and Collateral Term Sheet | JPMDB 2017-C5 | |

| Collateral Characteristics | ||

| Pari Passu Companion Loan Summary | |||||||||

No. | Loan Name | Trust Cut- | Pari Passu | Total Mortgage | Controlling | Master | Special | Voting Rights | |

| 1 | 229 West 43rd Street Retail Condo | $80,000,000 | $205,000,000 | $285,000,000 | CD 2016-CD2 | Wells Fargo | KeyBank | CD 2016-CD2 | |

| 2 | 350 Park Avenue | $66,667,200 | $229,320,800 | $295,988,000 | VNDO 2016-350P | Midland | Aegon | VNDO 2016-350P | |

| 3 | Prudential Plaza | $65,000,000 | $350,000,000 | $415,000,000 | COMM 2015-CCRE26 | Wells Fargo | CWCapital | COMM 2015-CCRE26 | |

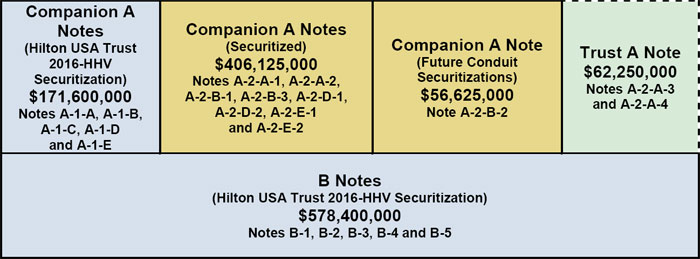

| 4 | Hilton Hawaiian Village | $62,250,000 | $634,350,000 | $696,600,000 | Hilton USA Trust 2016-HHV | Wells Fargo | Aegon | Hilton USA Trust 2016-HHV | |

| 5 | Key Center Cleveland | $60,000,000 | $160,000,000 | $220,000,000 | (2) | (2) | (2) | (2) | |

| 7 | Landmark Square | $49,000,000 | $51,000,000 | $100,000,000 | JPMCC 2017-JP5 | Midland | LNR | JPMCC 2017-JP5 | |

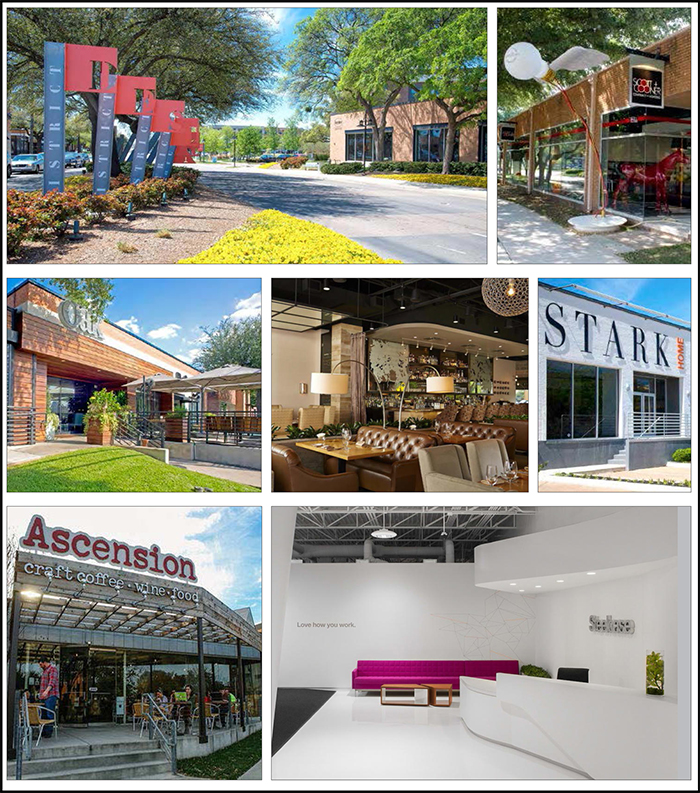

| 8 | Dallas Design District | $45,000,000 | $75,000,000 | $120,000,000 | JPMCC 2017-JP5 | Midland | LNR | JPMCC 2017-JP5 | |

| 9 | Moffett Gateway | $40,000,000 | $203,000,000 | $243,000,000 | JPMCC 2016-JP4 | Wells Fargo | LNR | JPMCC 2016-JP4 | |

| 10 | Uovo Art Storage | $36,943,588 | $49,923,767 | $86,867,355 | (2) | (2) | (2) | (2) | |

| 14 | Summit Mall | $35,000,000 | $50,000,000 | $85,000,000 | JPMCC 2016-JP4 | Wells Fargo | LNR | JPMCC 2016-JP4 | |

| 16 | Summit Place Wisconsin | $32,000,000 | $40,000,000 | $72,000,000 | CD 2017-CD3 | Midland | Midland | CD 2017-CD3 | |

| 25 | Dick’s Sporting Goods Portfolio | $12,930,513 | $17,903,787 | $30,834,300 | JPMCC 2016-JP4 | Wells Fargo | LNR | JPMCC 2016-JP4 | |

| (1) | In the case of Loan Nos. 2, 4 and 9, the Total Mortgage Loan Cut-off Date Balance excludes the related Subordinate Companion Loan(s). |

| (2) | In the case of Loan Nos. 5, and 10 the whole loans are serviced under the JPMDB 2017-C5 Pooling and Servicing Agreement until such time that the controlling pari passu companion loan has been securitized, at which point the whole loan will be serviced under the related pooling and servicing agreement. In the case of Loan No. 5, the initial controlling noteholder is CGMRC, or an affiliate, and in the case of Loan No. 10, the initial controlling noteholder is GACC, or an affiliate, in each case, as holder of the related controlling pari passu companion loan. |

| Additional Debt Summary(1) |

No. | Loan Name | Trust Cut- | Subordinate | Total Debt | Mortgage | Total | Mortgage | Total | Mortgage | Total |

| 1 | 229 West 43rd Street Retail Condo | $80,000,000 | $85,000,000 | $370,000,000 | 1.75x | 1.10x | 60.6% | 78.7% | 7.5% | 5.8% |

| 2 | 350 Park Avenue | $66,667,200 | 104,012,000 | $400,000,000 | 2.98x | 2.21x | 41.7% | 56.3% | 12.0% | 8.9% |

| 4 | Hilton Hawaiian Village | $62,250,000 | $578,400,000 | $1,275,000,000 | 4.47x | 2.44x | 31.2% | 57.2% | 19.0% | 10.4% |

| 5 | Key Center Cleveland | $60,000,000 | 42,500,000 | $262,500,000 | 1.59x | 1.17x | 60.8% | 72.5% | 12.3% | 10.3% |

| 9 | Moffett Gateway | $40,000,000 | $152,000,000 | $395,000,000 | 1.95x | 1.22x | 46.3% | 75.2% | 11.9% | 7.3% |

| (1) | In the case of Loan Nos. 1 and 5, subordinate debt represents a mezzanine loan. In the case of Loan Nos. 2 and 4, subordinate debt represents a Subordinate Companion Loan. In the case of Loan No. 9, subordinate debt represents a Subordinate Companion Loan and a mezzanine loan. |

| (2) | In the case of Loan Nos. 1, 2, 4, 5 and 9, Mortgage Loan UW NCF DSCR, Mortgage Loan Cut-off Date LTV and Mortgage Loan UW NOI Debt Yield calculations include any related Pari Passu Companion Loans, where applicable, but exclude the related Subordinate Companion Loan(s) or mezzanine loan(s), as applicable. |

| (3) | In the case of Loan No. 9, the Mortgage Loan UW NCF DSCR and Total Debt UW NCF DSCR are calculated using the sum of principal and interest payments over the first 12 payments following the expiration of the interest-only period based on the principal payment schedule provided in Annex G of the Preliminary Prospectus. |

| (4) | In the case of Loan Nos. 1, 5 and 9, the Mortgage Loan Cut-off Date LTV and the Total Debt Cut-off Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 5 of 139 | |

| Structural and Collateral Term Sheet | JPMDB 2017-C5 | |

| Collateral Characteristics | ||

| Mortgaged Properties by Type(1) |

| Weighted Average | |||||||||

| Property Type | Property Subtype | Number of Properties | Cut-off Date Principal Balance | % of IPB | Occupancy | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) |

| Office | Suburban | 6 | $149,225,000 | 14.3% | 98.1% | 1.72x | 11.4% | 63.6% | 56.5% |

| CBD | 2 | 131,667,200 | 12.6 | 88.2% | 2.17x | 10.6% | 50.4% | 47.4% | |

| Medical | 1 | 11,500,000 | 1.1 | 91.6% | 1.83x | 11.9% | 65.6% | 57.4% | |

| Subtotal: | 9 | $292,392,200 | 28.0% | 93.4% | 1.92x | 11.0% | 57.7% | 52.4% | |

| Hotel | Full Service | 3 | $123,627,503 | 11.8% | 85.6% | 3.43x | 16.3% | 44.9% | 41.4% |

| Limited Service | 7 | 60,872,146 | 5.8 | 71.8% | 1.92x | 13.7% | 61.8% | 51.1% | |

| Extended Stay | 3 | 16,578,635 | 1.6 | 81.4% | 2.06x | 15.1% | 57.4% | 49.6% | |

| Subtotal: | 13 | $201,078,284 | 19.3% | 81.1% | 2.86x | 15.4% | 51.0% | 45.0% | |

| Retail | Anchored | 4 | $104,628,307 | 10.0% | 99.3% | 1.75x | 8.7% | 62.5% | 60.0% |

| Regional Mall | 1 | 35,000,000 | 3.4 | 92.3% | 4.50x | 15.8% | 41.5% | 41.5% | |

| Single Tenant | 3 | 27,046,845 | 2.6 | 100.0% | 1.41x | 10.1% | 68.1% | 54.9% | |

| Shadow Anchored | 3 | 20,472,205 | 2.0 | 94.0% | 1.27x | 8.4% | 61.8% | 56.4% | |

| Freestanding | 3 | 11,571,836 | 1.1 | 100.0% | 1.37x | 9.7% | 69.6% | 57.0% | |

| Unanchored | 1 | 1,505,907 | 0.1 | 100.0% | 1.40x | 9.5% | 70.5% | 57.2% | |

| Subtotal: | 15 | $200,225,101 | 19.2% | 97.7% | 2.11x | 10.1% | 60.0% | 55.5% | |

| Mixed Use | Office/Retail | 3 | $139,445,906 | 13.4% | 91.4% | 1.66x | 10.1% | 65.6% | 59.0% |

| Office/Hotel/Parking | 1 | 60,000,000 | 5.8 | 92.9% | 1.59x | 12.3% | 60.8% | 49.6% | |

| Subtotal: | 4 | $199,445,906 | 19.1% | 91.8% | 1.64x | 10.8% | 64.1% | 56.2% | |

| Multifamily | Garden | 7 | $68,367,113 | 6.6% | 95.4% | 1.68x | 9.5% | 68.3% | 63.5% |

| Subtotal: | 7 | $68,367,113 | 6.6% | 95.4% | 1.68x | 9.5% | 68.3% | 63.5% | |

| Industrial | Flex | 1 | $45,000,000 | 4.3% | 98.7% | 1.28x | 9.4% | 62.1% | 55.3% |

| Subtotal: | 1 | $45,000,000 | 4.3% | 98.7% | 1.28x | 9.4% | 62.1% | 55.3% | |

| Self Storage | Art Storage | 1 | $36,943,588 | 3.5% | 83.9% | 1.55x | 9.8% | 52.6% | 43.0% |

| Subtotal: | 1 | $36,943,588 | 3.5% | 83.9% | 1.55x | 9.8% | 52.6% | 43.0% | |

| Total / Weighted Average: | 50 | $1,043,452,191 | 100.0% | 91.6% | 2.03x | 11.4% | 58.8% | 52.8% | |

| (1) | Because this table presents information relating to the mortgaged properties and not mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated loan amounts. |

| (2) | In the case of Loan Nos. 1, 2, 3, 4, 5, 7, 8, 9, 10, 14, 16 and 25, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2, 4 and 9, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s). |

| (3) | In the case of Loan No. 9, the UW NCF DSCR is calculated using the sum of principal and interest payments over the first 12 months following the expiration of the interest-only period based on the assumed principal payment schedule provided on Annex G to the Preliminary Prospectus. |

| (4) | In the case of Loan Nos. 1, 5, 9, 11 and 12, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 6 of 139 | |

| Structural and Collateral Term Sheet | JPMDB 2017-C5 | |

| Collateral Characteristics | ||

| Mortgaged Properties by Location(1) | ||||||||||||

Weighted Average | ||||||||||||

State | Number of Properties | Cut-off Date Principal Balance | % of | Occupancy | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) | ||||

| New York | 4 | $238,610,788 | 22.9% | 96.2% | 1.94x | 9.2% | 56.6% | 53.1% | ||||

| Ohio | 4 | 164,945,906 | 15.8 | 93.1% | 2.34x | 13.2% | 59.9% | 51.9% | ||||

| Texas | 7 | 108,578,616 | 10.4 | 96.7% | 1.53x | 9.4% | 65.6% | 60.2% | ||||

| California | 5 | 103,150,000 | 9.9 | 97.8% | 1.61x | 10.4% | 58.4% | 52.2% | ||||

| Connecticut | 2 | 84,377,503 | 8.1 | 79.8% | 1.92x | 11.3% | 62.7% | 57.7% | ||||

| Florida | 9 | 78,925,009 | 7.6 | 78.7% | 2.48x | 15.5% | 53.8% | 47.3% | ||||

| Illinois | 2 | 66,922,668 | 6.4 | 77.8% | 1.33x | 9.1% | 59.6% | 53.3% | ||||

| Hawaii | 1 | 62,250,000 | 6.0 | 94.6% | 4.47x | 19.0% | 31.2% | 31.2% | ||||

| Oregon | 4 | 40,651,146 | 3.9 | 88.6% | 1.56x | 11.1% | 67.4% | 55.5% | ||||

| Wisconsin | 1 | 32,000,000 | 3.1 | 99.1% | 1.37x | 9.7% | 72.7% | 64.2% | ||||

| Tennessee | 1 | 12,285,000 | 1.2 | 96.3% | 2.07x | 14.1% | 67.9% | 62.7% | ||||

| Washington | 1 | 11,958,011 | 1.1 | 69.8% | 1.79x | 13.4% | 64.6% | 53.6% | ||||

| Michigan | 2 | 11,163,497 | 1.1 | 96.0% | 1.67x | 12.7% | 70.2% | 57.9% | ||||

| Georgia | 1 | 9,949,173 | 1.0 | 97.0% | 1.42x | 11.2% | 69.7% | 52.3% | ||||

| New Hampshire | 3 | 7,107,803 | 0.7 | 100.0% | 1.40x | 9.5% | 70.5% | 57.2% | ||||

| Montana | 1 | 6,677,030 | 0.6 | 100.0% | 1.55x | 11.1% | 64.8% | 48.9% | ||||

| Kansas | 1 | 2,394,134 | 0.2 | 100.0% | 1.40x | 9.5% | 70.5% | 57.2% | ||||

| Indiana | 1 | 1,505,907 | 0.1 | 100.0% | 1.40x | 9.5% | 70.5% | 57.2% | ||||

| Total / Weighted Average: | 50 | $1,043,452,191 | 100.0% | 91.6% | 2.03x | 11.4% | 58.8% | 52.8% | ||||

| (1) | Because this table presents information relating to the mortgaged properties and not mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated loan amounts. |

| (2) | In the case of Loan Nos. 1, 2, 3, 4, 5, 7, 8, 9, 10, 14, 16 and 25, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2, 4 and 9, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s). |

| (3) | In the case of Loan No. 9, the UW NCF DSCR is calculated using the sum of principal and interest payments over the first 12 months following the expiration of the interest-only period based on the assumed principal payment schedule provided on Annex G to the Preliminary Prospectus. |

| (4) | In the case of Loan Nos. 1, 5, 9, 11 and 12, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 7 of 139 | |

| Structural and Collateral Term Sheet | JPMDB 2017-C5 | |

| Collateral Characteristics | ||

| Cut-off Date Principal Balance |

Weighted Average | |||||||||||

| Range of Cut-off Date Principal Balances | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI DY(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) | ||

| $4,788,497 | - | $9,999,999 | 6 | $43,848,804 | 4.2% | 5.10444% | 106 | 1.75x | 12.8% | 65.0% | 52.5% |

| $10,000,000 | - | $19,999,999 | 9 | 125,859,901 | 12.1 | 4.85807% | 114 | 1.55x | 10.7% | 67.1% | 58.9% |

| $20,000,000 | - | $24,999,999 | 1 | 23,610,000 | 2.3 | 3.82000% | 116 | 2.32x | 9.5% | 61.6% | 61.6% |

| $25,000,000 | - | $49,999,999 | 13 | 461,216,286 | 44.2 | 4.66797% | 115 | 2.01x | 11.9% | 59.8% | 53.1% |

| $50,000,000 | - | $80,000,000 | 6 | 388,917,200 | 37.3 | 4.42014% | 115 | 2.22x | 11.1% | 54.0% | 50.0% |

| Total / Weighted Average: | 35 | $1,043,452,191 | 100.0% | 4.59769% | 114 | 2.03x | 11.4% | 58.8% | 52.8% | ||

| Mortgage Interest Rates |

Weighted Average | |||||||||||

| Range of Mortgage Interest Rates | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI DY(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) | ||

| 3.31400% | - | 3.99999% | 4 | $165,277,200 | 15.8% | 3.63007% | 118 | 2.96x | 12.4% | 45.6% | 43.9% |

| 4.00000% | - | 4.49999% | 5 | 192,680,513 | 18.5 | 4.18363% | 117 | 2.85x | 13.1% | 49.6% | 48.2% |

| 4.50000% | - | 4.99999% | 15 | 453,380,717 | 43.5 | 4.79237% | 116 | 1.59x | 10.6% | 64.2% | 56.4% |

| 5.00000% | - | 5.41000% | 11 | 232,113,761 | 22.2 | 5.25011% | 107 | 1.55x | 11.2% | 65.2% | 55.9% |

| Total / Weighted Average: | 35 | $1,043,452,191 | 100.0% | 4.59769% | 114 | 2.03x | 11.4% | 58.8% | 52.8% | ||

| Original Term to Maturity in Months(1) |

Weighted Average | |||||||||

| Original Term to Maturity in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI DY(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) |

| 60 | 2 | $35,559,103 | 3.4% | 5.24751% | 59 | 1.55x | 10.9% | 67.1% | 62.6% |

| 84 | 1 | 12,285,000 | 1.2 | 5.07000% | 82 | 2.07x | 14.1% | 67.9% | 62.7% |

| 120 | 30 | 888,940,888 | 85.2 | 4.67387% | 116 | 1.98x | 11.4% | 60.2% | 53.7% |

| 121 | 1 | 66,667,200 | 6.4 | 3.91513% | 118 | 2.98x | 12.0% | 41.7% | 41.7% |

| 126 | 1 | 40,000,000 | 3.8 | 3.31940% | 121 | 1.95x | 11.9% | 46.3% | 39.3% |

| Total / Weighted Average: | 35 | $1,043,452,191 | 100.0% | 4.59769% | 114 | 2.03x | 11.4% | 58.8% | 52.8% |

| Remaining Term to Maturity in Months(1) | |||||||||

| Weighted Average | |||||||||||

| Range of Remaining Term to Maturity in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI DY(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) | ||

| 57 | - | 84 | 3 | $47,844,103 | 4.6% | 5.20193% | 65 | 1.69x | 11.7% | 67.3% | 62.6% |

| 85 | - | 119 | 28 | 915,733,088 | 87.8 | 4.62189% | 116 | 2.01x | 11.2% | 59.3% | 53.2% |

| 120 | - | 121 | 4 | 79,875,000 | 7.7 | 3.95830% | 121 | 2.45x | 14.2% | 48.4% | 42.8% |

| Total / Weighted Average: | 35 | $1,043,452,191 | 100.0% | 4.59769% | 114 | 2.03x | 11.4% | 58.8% | 52.8% | ||

| (1) | In the case of the Loan No.18, the first payment date for the loan is May 1, 2017. On the Closing Date, JPMCB will deposit sufficient funds to pay the interest associated with the interest due for the April 2017 payment for the related loan. Information presented in this term sheet reflects the contractual loan terms. |

| (2) | In the case of Loan Nos. 1, 2, 3, 4, 5, 7, 8, 9, 10, 14, 16 and 25, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2, 4 and 9, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s). |

| (3) | In the case of Loan No. 9, the UW NCF DSCR is calculated using the sum of principal and interest payments over the first 12 months following the expiration of the interest-only period based on the assumed principal payment schedule provided on Annex G to the Preliminary Prospectus. |

| (4) | In the case of Loan Nos. 1, 5, 9, 11 and 12, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 8 of 139 | |

| Structural and Collateral Term Sheet | JPMDB 2017-C5 | |

| Collateral Characteristics | ||

| Original Amortization Term in Months |

| Weighted Average | |||||||||

| Original Amortization Term in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI DY(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) |

| Interest Only | 7 | $342,527,200 | 32.8% | 4.11068% | 117 | 3.00x | 12.9% | 47.8% | 47.8% |

| 300 | 4 | 85,185,306 | 8.2 | 5.26800% | 112 | 1.63x | 12.5% | 61.6% | 49.9% |

| 360 | 24 | 615,739,685 | 59.0 | 4.77586% | 113 | 1.55x | 10.5% | 64.5% | 56.0% |

| Total / Weighted Average: | 35 | $1,043,452,191 | 100.0% | 4.59769% | 114 | 2.03x | 11.4% | 58.8% | 52.8% |

| Remaining Amortization Term in Months |

| Weighted Average | |||||||||||

| Range of Remaining Amortization Term in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI DY(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) | ||

| Interest Only | 7 | $342,527,200 | 32.8% | 4.11068% | 117 | 3.00x | 12.9% | 47.8% | 47.8% | ||

| 297 | - | 356 | 5 | 98,115,819 | 9.4 | 5.15993% | 113 | 1.60x | 12.1% | 62.8% | 50.8% |

| 357 | - | 360 | 23 | 602,809,172 | 57.8 | 4.78290% | 113 | 1.55x | 10.5% | 64.4% | 56.0% |

| Total / Weighted Average: | 35 | $1,043,452,191 | 100.0% | 4.59769% | 114 | 2.03x | 11.4% | 58.8% | 52.8% | ||

| Amortization Types |

Weighted Average | |||||||||

| Amortization Types | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI DY(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) |

| IO-Balloon | 13 | $433,935,000 | 41.6% | 4.75065% | 111 | 1.50x | 10.3% | 63.8% | 56.5% |

| Interest Only | 7 | 342,527,200 | 32.8 | 4.11068% | 117 | 3.00x | 12.9% | 47.8% | 47.8% |

| Balloon | 15 | 266,989,991 | 25.6 | 4.97387% | 116 | 1.64x | 11.4% | 64.9% | 53.2% |

| Total / Weighted Average: | 35 | $1,043,452,191 | 100.0% | 4.59769% | 114 | 2.03x | 11.4% | 58.8% | 52.8% |

| Underwritten Net Cash Flow Debt Service Coverage Ratios(1)(2) |

| Weighted Average | |||||||||||

| Range of Underwritten Net Cash Flow Debt Service Coverage Ratios | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI DY(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) | ||

| 1.20x | - | 1.24x | 2 | $70,300,000 | 6.7% | 4.70306% | 119 | 1.20x | 7.8% | 68.7% | 61.3% |

| 1.25x | - | 1.49x | 11 | 274,070,184 | 26.3 | 4.92298% | 108 | 1.34x | 9.5% | 66.6% | 58.5% |

| 1.50x | - | 1.74x | 5 | 174,444,027 | 16.7 | 5.05551% | 119 | 1.59x | 11.1% | 62.8% | 51.3% |

| 1.75x | - | 1.99x | 7 | 194,198,917 | 18.6 | 4.21404% | 118 | 1.84x | 10.7% | 58.4% | 53.0% |

| 2.00x | - | 4.50x | 10 | 330,439,064 | 31.7 | 4.28924% | 114 | 3.12x | 14.5% | 48.3% | 47.0% |

| Total / Weighted Average: | 35 | $1,043,452,191 | 100.0% | 4.59769% | 114 | 2.03x | 11.4% | 58.8% | 52.8% | ||

| (1) | In the case of the Loan No.18, the first payment date for the loan is May 1, 2017. On the Closing Date, JPMCB will deposit sufficient funds to pay the interest associated with the interest due for the April 2017 payment for the related loan. Information presented in this term sheet reflects the contractual loan terms. |

| (2) | In the case of Loan Nos. 1, 2, 3, 4, 5, 7, 8, 9, 10, 14, 16 and 25, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2, 4 and 9, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s). |

| (3) | In the case of Loan No. 9, the UW NCF DSCR is calculated using the sum of principal and interest payments over the first 12 months following the expiration of the interest-only period based on the assumed principal payment schedule provided on Annex G to the Preliminary Prospectus. |

| (4) | In the case of Loan Nos. 1, 5, 9, 11 and 12, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 9 of 139 | |

| Structural and Collateral Term Sheet | JPMDB 2017-C5 | |

| Collateral Characteristics | ||

| LTV Ratios as of the Cut-off Date(2)(4) |

| Weighted Average | |||||||||||

| Range of Cut-off Date LTVs | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI DY(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) | ||

| 31.2% | - | 49.9% | 5 | $229,917,200 | 22.0% | 3.85633% | 118 | 3.50x | 15.2% | 39.7% | 38.5% |

| 50.0% | - | 59.9% | 6 | 211,668,596 | 20.3 | 4.82381% | 110 | 1.70x | 11.0% | 57.5% | 51.7% |

| 60.0% | - | 64.9% | 8 | 247,312,803 | 23.7 | 4.69912% | 118 | 1.70x | 10.1% | 61.5% | 55.7% |

| 65.0% | - | 69.9% | 8 | 154,538,463 | 14.8 | 4.78553% | 116 | 1.71x | 11.8% | 68.4% | 58.6% |

| 70.0% | - | 73.9% | 8 | 200,015,129 | 19.2 | 4.94002% | 110 | 1.35x | 9.1% | 71.4% | 62.5% |

| Total / Weighted Average: | 35 | $1,043,452,191 | 100.0% | 4.59769% | 114 | 2.03x | 11.4% | 58.8% | 52.8% | ||

| LTV Ratios as of the Maturity Date(2)(4) |

Weighted Average | |||||||||||

| Range of Maturity Date LTVs | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI DY(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) | ||

| 31.2% | - | 44.9% | 6 | $266,860,788 | 25.6% | 3.97797% | 118 | 3.23x | 14.4% | 41.5% | 39.1% |

| 45.0% | - | 49.9% | 4 | 112,102,039 | 10.7 | 5.20347% | 114 | 1.75x | 13.1% | 60.3% | 49.5% |

| 50.0% | - | 54.9% | 5 | 106,974,945 | 10.3 | 4.77637% | 108 | 1.51x | 10.6% | 61.6% | 52.9% |

| 55.0% | - | 59.9% | 10 | 243,800,803 | 23.4 | 4.97138% | 118 | 1.61x | 10.5% | 64.8% | 56.8% |

| 60.0% | - | 66.7% | 10 | 313,713,616 | 30.1 | 4.55704% | 111 | 1.61x | 9.3% | 67.4% | 62.6% |

| Total / Weighted Average: | 35 | $1,043,452,191 | 100.0% | 4.59769% | 114 | 2.03x | 11.4% | 58.8% | 52.8% | ||

| Prepayment Protection |

Weighted Average | |||||||||

| Prepayment Protection | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI DY(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) |

| Defeasance | 25 | $794,908,703 | 76.2% | 4.53229% | 116 | 1.94x | 11.1% | 59.2% | 53.2% |

| Yield Maintenance | 9 | 186,293,488 | 17.9 | 5.00978% | 107 | 1.58x | 10.3% | 66.2% | 58.4% |

| Defeasance or Yield Maintenance | 1 | 62,250,000 | 6.0 | 4.19950% | 116 | 4.47x | 19.0% | 31.2% | 31.2% |

| Total / Weighted Average: | 35 | $1,043,452,191 | 100.0% | 4.59769% | 114 | 2.03x | 11.4% | 58.8% | 52.8% |

| Loan Purpose |

Weighted Average | |||||||||

| Loan Purpose | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(2)(3) | UW NOI DY(2) | Cut-off Date LTV(2)(4) | Maturity Date LTV(2)(4) |

| Refinance | 26 | $826,789,256 | 79.2% | 4.52910% | 114 | 2.09x | 11.2% | 57.4% | 52.0% |

| Acquisition | 8 | 209,985,905 | 20.1 | 4.84984% | 116 | 1.81x | 12.2% | 64.0% | 56.3% |

| Recapitalization | 1 | 6,677,030 | 0.6 | 5.16000% | 118 | 1.55x | 11.1% | 64.8% | 48.9% |

| Total / Weighted Average: | 35 | $1,043,452,191 | 100.0% | 4.59769% | 114 | 2.03x | 11.4% | 58.8% | 52.8% |

| (1) | In the case of the Loan No.18, the first payment date for the loan is May 1, 2017. On the Closing Date, JPMCB will deposit sufficient funds to pay the interest associated with the interest due for the April 2017 payment for the related loan. Information presented in this term sheet reflects the contractual loan terms. |

| (2) | In the case of Loan Nos. 1, 2, 3, 4, 5, 7, 8, 9, 10, 14, 16 and 25, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2, 4 and 9, the UW NCF DSCR, UW NOI DY, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s). |

| (3) | In the case of Loan No. 9, the UW NCF DSCR is calculated using the sum of principal and interest payments over the first 12 months following the expiration of the interest-only period based on the assumed principal payment schedule provided on Annex G to the Preliminary Prospectus. |

| (4) | In the case of Loan Nos. 1, 5, 9, 11 and 12, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 10 of 139 | |

| Structural and Collateral Term Sheet | JPMDB 2017-C5 | |

| Collateral Characteristics | ||

| Previous Securitization History(1) |

| No. | Loan Name | Location | Property Type | Previous Securitization |

| 2 | 350 Park Avenue | New York, NY | Office | WBCMT 2007-C30 |

| 3 | Prudential Plaza | Chicago, IL | Office | JPMCC 2006-LDP7; JPMCC 2006-CB16 |

| 4 | Hilton Hawaiian Village | Honolulu, HI | Hotel | HILT 2013-HLT |

| 8 | Dallas Design District | Dallas, TX | Industrial | JPMCC 2015-FL7 |

| 13 | Delamar Greenwich Harbor | Greenwich, CT | Hotel | LBUBS 2007-C2 |

| 14 | Summit Mall | Fairlawn, OH | Retail | JPMCC 2007-LD12 |

| 16 | Summit Place Wisconsin | West Allis, WI | Office | BSCMS 2007-PW15 |

| 17.01 | Shopko Salem | Salem, OR | Retail | MSC 2007-IQ14 |

| 17.02 | Shopko Bend | Bend, OR | Retail | MSC 2007-IQ14 |

| 17.03 | Shopko Eugene | Eugene, OR | Retail | MSC 2007-IQ14 |

| 19 | Holiday Inn Miami Beach | Miami Beach, FL | Hotel | CGCMT 2007-C6 |

| 21 | Cupertino Civic Center | Cupertino, CA | Office | WBCMT 2007-C32 |

| 23 | Trabuco Hills | Mission Viejo, CA | Retail | MLCFC 2007-6 |

| 24.01 | Creekview Apartments | Sherman, TX | Multifamily | MLCFC 2007-6 |

| 24.02 | Country Village Apartments | Sherman, TX | Multifamily | MLCFC 2007-5 |

| 25.01 | Dick’s Keene | Keene, NH | Retail | BACM 2006-1 |

| 25.02 | Dick’s & PetSmart Concord | Concord, NH | Retail | CGCMT 2006-C5 |

| 25.03 | Dick’s Wichita | Wichita, KS | Retail | CGCMT 2006-C5 |

| 25.04 | Dick’s Bloomingdale | Bloomingdale, IL | Retail | CGCMT 2006-C5 |

| 26 | Plaza Ashland | Ashland, OR | Hotel | MSC 2007-T25 |

| 27 | Cleveland Towne Center | Cleveland, TN | Retail | WFCG 2015-BXRP |

| 28 | Courtyard Marriott Richland | Richland, WA | Hotel | BACM 2006-6 |

| 29 | Grossmont Medical Center | La Mesa, CA | Office | MSC 2004-T13; MLCFC 2007-5 |

| 33 | Shopko Billings | Billings, MT | Retail | CGCMT 2006-C4 |

| 35 | Crossroads Village Apartments | Portage, MI | Multifamily | FNA 2014-M9 |

| (1) | The table above represents the properties for which the previously existing debt was most recently securitized, based on information provided by the related borrower or obtained through searches of a third-party database. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 11 of 139 | |

| Structural and Collateral Term Sheet | JPMDB 2017-C5 |

| 229 West 43rd Street Retail Condo | |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 12 of 139 | |

| Structural and Collateral Term Sheet | JPMDB 2017-C5 |

| 229 West 43rd Street Retail Condo | |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 13 of 139 | |

| Structural and Collateral Term Sheet | JPMDB 2017-C5 |

| 229 West 43rd Street Retail Condo | |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 14 of 139 | |

| Structural and Collateral Term Sheet | JPMDB 2017-C5 |

| 229 West 43rd Street Retail Condo | |

| Mortgage Loan Information | Property Information | |||

| Mortgage Loan Seller: | GACC | Single Asset / Portfolio: | Single Asset | |

| Original Principal Balance(1): | $80,000,000 | Title: | Fee | |

| Cut-off Date Principal Balance(1): | $80,000,000 | Property Type - Subtype: | Retail – Anchored | |

| % of Pool by IPB: | 7.7% | Net Rentable Area (SF): | 248,457 | |

| Loan Purpose: | Refinance | Location: | New York, NY | |

| Borrowers: | Elmwood NYT Owner, LLC; | Year Built / Renovated: | 1913-1947 / 2009 | |

| Oakwood NYT Owner, LLC; Wallkill | Occupancy: | 100.0% | ||

| NYT Owner, LLC and Landings | Occupancy Date: | 10/1/2016 | ||

| NYT Owner, LLC | Number of Tenants: | 8 | ||

| Sponsor(2): | Jared Kushner | 2013 NOI: | $9,621,123 | |

| Interest Rate: | 4.00550% | 2014 NOI: | $11,949,215 | |

| Note Date: | 10/13/2016 | 2015 NOI(4): | N/A | |

| Maturity Date: | 11/6/2026 | T-10 Ann. NOI (as of 8/2016)(5): | $13,775,701 | |

| Interest-only Period: | 120 months | UW Economic Occupancy(6): | 100.0% | |

| Original Term: | 120 months | UW Revenues: | $25,397,158 | |

| Original Amortization: | None | UW Expenses: | $3,895,157 | |

| Amortization Type: | Interest Only | UW NOI(5): | $21,502,001 | |

| Call Protection(3): | L(28),Def(85),O(7) | UW NCF: | $20,207,655 | |

| Lockbox / Cash Management: | Hard / In-Place | Appraised Value / Per SF(7): | $470,000,000 / $1,892 | |

| Additional Debt: | Yes | Appraisal Date: | 10/1/2016 | |

| Additional Debt Balance: | $205,000,000 / $85,000,000 | |||

| Additional Debt Type: | Pari Passu / Mezzanine | |||

| Escrows and Reserves(8) | Financial Information(1) | ||||||

| Initial | Monthly | Initial Cap | Whole Loan | Total Debt | |||

| Taxes: | $651,564 | $126,690 | N/A | Cut-off Date Loan / SF: | $1,147 | $1,489 | |

| Insurance: | $18,983 | Springing | N/A | Maturity Date Loan / SF: | $1,147 | $1,489 | |

| Replacement Reserves: | $0 | $6,211 | N/A | Cut-off Date LTV(7): | 60.6% | 78.7% | |

| TI/LC: | $14,492,159 | $0 | N/A | Maturity Date LTV(7): | 60.6% | 78.7% | |

| Other: | $11,133,080 | Springing | N/A | UW NCF DSCR: | 1.75x | 1.10x | |

| UW NOI Debt Yield: | 7.5% | 5.8% | |||||

| Sources and Uses | |||||||

| Sources | Proceeds | % of Total | Uses | Proceeds | % of Total | |

| Mortgage Loan(1) | $285,000,000 | 77.0% | Payoff Existing Debt | $276,954,279 | 74.9% | |

| Mezzanine Loan | 85,000,000 | 23.0 | Return of Equity | 59,327,520 | 16.0 | |

| Upfront Reserves | 26,295,786 | 7.1 | ||||

| Closing Costs | 7,422,416 | 2.0 | ||||

| Total Sources | $370,000,000 | 100.0% | Total Uses | $370,000,000 | 100.0% |

| (1) | The 229 West 43rd Street Retail Condo loan is part of a whole loan evidenced by ninepari passu notes with an aggregate original principal balance of $285.0 million. The Whole Loan Financial Information presented in the chart above reflects the 229 West 43rd Street Retail Condo Whole Loan Cut-off Date balance of $285.0 million. The Total Debt Financial Information presented in the chart above reflects the aggregate Cut-off Date balance of the 229 West 43rd Street Retail Condo Whole Loan and the related mezzanine loan of $370.0 million. |

| (2) | See “The Loan Sponsor” herein. |

| (3) | The lockout period will be at least 28 payments beginning with and including the first payment on December 6, 2016. Defeasance of the full $285.0 million 229 West 43rd Street Retail Condo Whole Loan is permitted after the earlier to occur of (i) October 13, 2019 and (ii) the date that is two years from the closing date of the securitization that includes the note to be last securitized. The assumed lockout period is based on the expected JPMDB 2017-C5 securitization closing date in March 2017. The actual lockout period may be longer. |

| (4) | 2015 NOI is not available due to the borrower’s acquisition of the 229 West 43rd Street Retail Condo property in October 2015. |

| (5) | The increase in UW NOI from T-10 Ann. NOI is due to 121,832 square feet of recent leasing at the 229 West 43rd Street Retail Condo property (49.0% of NRA and 59.7% of U/W Base Rent). |

| (6) | UW Economic Occupancy includes four tenants (49.0% of NRA) that have signed leases but have not yet taken occupancy at the 229 West 43rd Street Retail Condo property, each of which is in a free rent period for which $11,061,751 was reserved with lender at loan origination. |

| (7) | The Appraised Value / Per SF, Cut-off Date LTV and Maturity Date LTV are calculated based on the “Hypothetical As-Is” appraised value, which applies a credit for the approximately $24.2 million of contractual free rent and TI/LC obligations for which approximately $25.6 million was ultimately reserved at loan origination. Based on the as-is appraised value of $445.0 million, the Cut-off Date LTV for the Mortgage Loan and Total Debt are 64.0% and 83.1%, respectively. |

| (8) | For a full description of Escrows and Reserves, please refer to “Escrows and Reserves” below. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 15 of 139 | |

| Structural and Collateral Term Sheet | JPMDB 2017-C5 |

| 229 West 43rd Street Retail Condo | |

The Loan. The 229 West 43rd Street Retail Condo loan is secured by a first mortgage lien on the borrowers’ fee interest in a 248,457 square foot retail condominium located in New York, New York. The whole loan has an outstanding principal balance as of the Cut-off Date of $285.0 million (the “229 West 43rd Street Retail Condo Whole Loan”) and is comprised of ninepari passu notes, each as described below. Note A-2 and Note A-3 with an aggregate balance of $80.0 million are being contributed to the JPMDB 2017-C5 Trust. Note A-1 was securitized in the CD 2016-CD2 trust and is the controlling note under the related co-lender agreement, the rights of which will be exercised by the related trustee (or, prior to the occurrence and continuance of a control termination event under the related pooling and servicing agreement, by the related directing certificateholder). However, the JPMDB 2017-C5 Trust will be entitled, under certain circumstances, to be consulted with respect to certain major decisions. The 229 West 43rd Street Retail Condo Whole Loan has a 10-year term and is interest-only for the entire term of the loan.

| Whole Loan Summary | ||||

| Note | Original Balance | Cut-off Date Balance | Note Holder | Controlling Piece |

| A-1, A-6 | 75,000,000 | 75,000,000 | CD 2016-CD2 | Yes |

| A-2, A-3 | $80,000,000 | $80,000,000 | JPMDB 2017-C5 | No |

| A-4-A | 30,000,000 | 30,000,000 | CGMRC | No |

| A-4-B, A-5, A-7, A-8 | 100,000,000 | 100,000,000 | CD 2017-CD3 | No |

| Total | $285,000,000 | $285,000,000 | ||

The Borrower. The borrowing entities for the 229 West 43rd Street Retail Condo Whole Loan are Elmwood NYT Owner, LLC, Oakwood NYT Owner, LLC, Wallkill NYT Owner, LLC and Landings NYT Owner, LLC, as tenants-in-common. Each is a Delaware limited liability company and special purpose entity structured to be bankruptcy remote, with two independent directors in its organizational structure.

The Loan Sponsor. The loan sponsor and nonrecourse carve-out guarantor is Jared Kushner. On January 3, 2017, the borrowers sent a notice to the lender stating that subject to the terms of the related 229 West 43rd Street Retail Condo Loan documents, and to the extent required, the consent of the lender, Jared Kushner intends to tender his resignation as manager of the borrowers and will be replaced in such capacity by Joshua Kushner, effective as of January 19, 2017. Following such notice, the borrower proposed that Jared Kushner be replaced by Joshua Kushner as the nonrecourse carve-out guarantor. Such notice and proposal are currently under review by the servicer and special servicer in the CD 2016-CD2 securitization under which the 229 West 43rd Street Retail Condo Whole Loan is being serviced. It is anticipated that Jared Kushner will be replaced by Joshua Kushner as the manager of the indirect owner of the borrower, and the 229 West 43rd Street Retail Condo Loan documents may be amended to provide that, among other things, both Jared Kushner and Joshua Kushner are guarantors under nonrecourse carve-out guaranties and will individually and collectively constitute key principals for purposes of such documents. However, such proposal is not final and may be subject to further change. Jared Kushner has been appointed as a senior White House advisor in the Trump administration.

According to management at Kushner Companies, Jared Kushner has tendered his resignation as CEO of Kushner Companies, a real estate organization headquartered in New York City and founded in 1964 by Charles Kushner, Jared’s father. The company’s national reach consists of more than 20,000 multifamily apartments and approximately 13.0 million square feet of office, hotel, industrial and retail space throughout the Northeast and Mid-Atlantic regions. In 2015 alone, Kushner Companies completed more than $1.5 billion of transactions. See “Description of the Mortgage Pool—Loan Purpose; Default History, Bankruptcy Issues and Other Proceedings” in the Preliminary Prospectus.

In addition to his former role at Kushner Companies, Jared, alongside his brother, Joshua, co-founded Cadre, a company that utilizes technology to connect institutional investors with potential real estate investments. Jared Kushner has been an active investor in technology companies and has been a member on the boards of several start-ups including Urban Compass, Honest Buildings and 42 Floors.

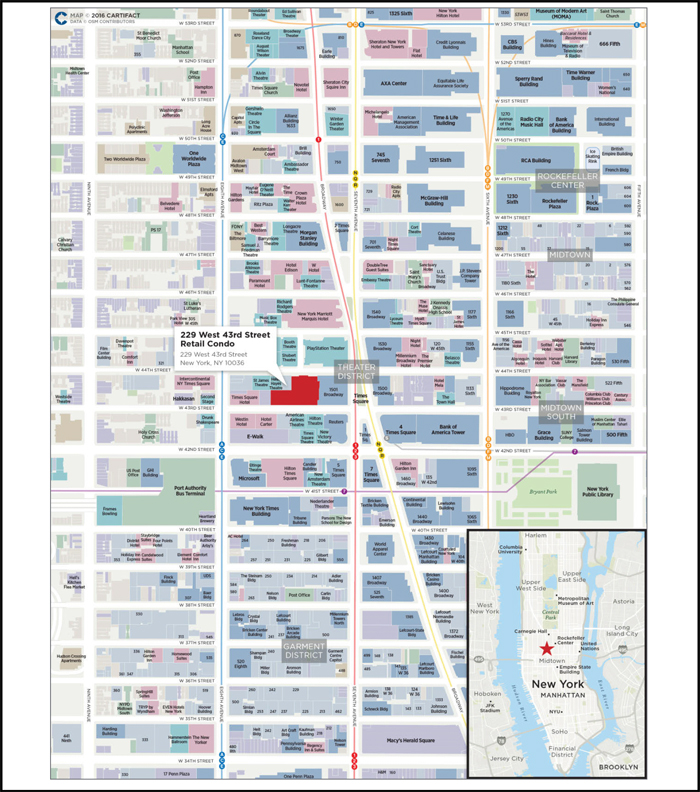

The Property. The 229 West 43rd Street Retail Condo property is a 248,457 square foot retail condominium located at 229 West 43rd Street, formerly known as The New York Times Building. The 229 West 43rd Street Retail Condo property is a landmarked building located mid-block with frontage on both 43rd and 44th streets, across from the famous Shubert Alley, a 300-foot long pedestrian alley at the heart of the New York City theater district.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 16 of 139 | |

| Structural and Collateral Term Sheet | JPMDB 2017-C5 |

| 229 West 43rd Street Retail Condo | |

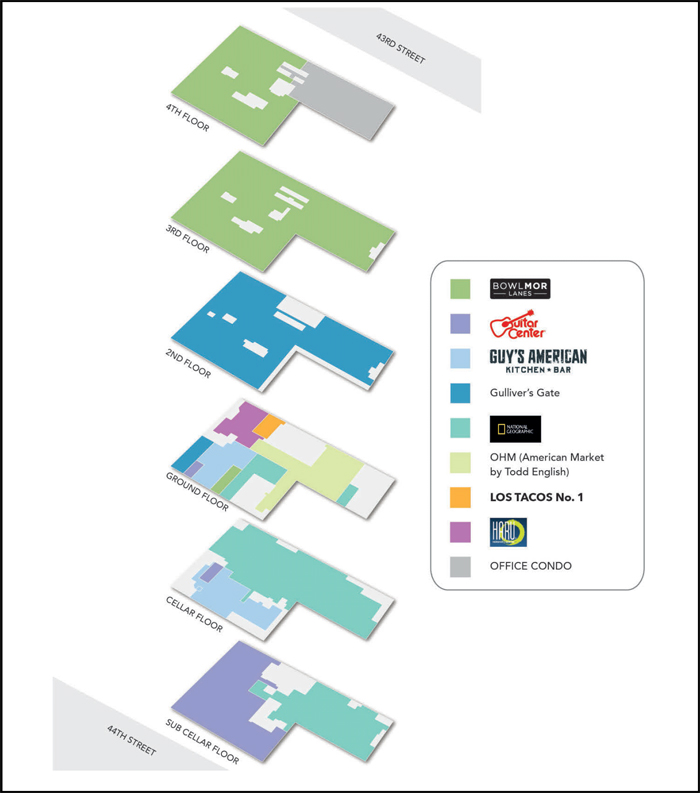

The 229 West 43rd Street Retail Condo property consists of six floors, two below-grade and four above-grade (the “Retail Condominium Unit”) that is the base of an 18-story, 729,566 square foot building that also includes an office condominium (the “Office Condominium Unit,” and together with the Retail Condominium Unit, the “229 West 43rd Street Condominium”) on floors 5 – 16. The Office Condominium Unit is not collateral for the 229 West 43rd Street Retail Condo Whole Loan. The related condominium board of directors has five board members, two of which are appointed by the borrowers. For additional information regarding the 229 West 43rd Street Condominium see “The Condominium” herein. The borrowers acquired the 229 West 43rd Street Retail Condo property in October 2015 for approximately $295.0 million ($1,187 per square foot) from Africa-Israel USA and Five Mile Capital in an off market transaction.

The 229 West 43rd Street Retail Condo property is 100.0% leased as of October 1, 2016 to 8 tenants in the retail, entertainment and restaurant sectors, all of which have lease terms that extend beyond the term of the 229 West 43rd Street Retail Condo Whole Loan. Top tenants include Bowlmor Times Square, LLC, National Geographic, Gulliver’s Gate, Guitar Center Stores, Inc. and Guy’s American Kitchen. The 229 West 43rd Street Retail Condo property’s combined weighted average lease term and remaining lease term are 18.4 and 15.7 years, respectively, and the current weighted average in-place gross rent for the 229 West 43rd Street Retail Condo property is $102.14 per square foot.

Prior to the borrowers’ acquisition in 2015, the 229 West 43rd Street Retail Condo property was 75.1% occupied. Since the acquisition, the loan sponsor fully leased up the 229 West 43rd Street Retail Condo property, signing leases for 121,832 square feet of space. New leases include National Geographic, Gulliver’s Gate, Los Tacos No.1 and OHM (American Market by Todd English). As part of its lease up efforts, the loan sponsor was able to buyout Discovery TSX’s lease and subsequently release the space to National Geographic at $101.46 per square foot. In connection with the new leases, there is approximately $16.2 million in tenant improvements, leasing commissions and landlord work, the outstanding balance of which was reserved for at loan origination. The subsequent chart details the recent leasing at the 229 West 43rd Street Retail Condo property and the borrowers’ budgeted tenant improvements, leasing commissions and landlord work associated with each lease.

| Recent Leasing | |||||||||

| Tenant | Lease Commencement | Free Rent | Rent Commencement | Tenant Possession Date | Projected | Tenant Improvements | Leasing Commissions | LL Work / Budgeted CapEx | |

| National Geographic | 10/4/2016 | 12 | 10/8/2017 | Oct-16 | Aug-17 | $4,000,000 | $2,400,000 | $0 | |

| Gulliver’s Gate | 1/4/2016 | 12 | 1/4/2017 | Jan-16 | Mar-17 | $2,500,000 | $2,571,226 | $0 | |

| OHM (American Market by Todd English) | 8/1/2016 | 15 | (1) | 11/1/2017 | Mar-17 | Apr-17 | $1,100,000 | $1,000,000 | $2,100,000 |

| Los Tacos No.1 | 12/1/2016 | 9 | 9/1/2017 | Dec-16 | Jul-17 | $0 | $164,000 | $400,000 | |

| Total | $7,600,000 | $6,135,226 | $2,500,000 | ||||||

| (1) | Includes partial free rent starting in December 2017. The free rent schedule is as follows: 100% abatement until November 2017; 50% abatement from December 2017 through July 2018; 25% abatement from August 2018 through March 2019; full rent thereafter. |

The 229 West 43rd Street Retail Condo property benefits from an existing Industrial Commercial Incentive Program (“ICIP”) tax exemption, granted to the prior owner in connection with certain capital improvements made to the 229 West 43rd Street Retail Condo property which qualified for such ICIP benefits. The ICIP program provided exemptions from real estate tax increases resulting from capital improvements installed in qualifying industrial and commercial properties. To be eligible, industrial and commercial buildings must be modernized, expanded or otherwise physically improved as required by the ICIP rules, and the benefits could last for up to 25 tax years. The 229 West 43rd Street Retail Condo property qualified for a 12 tax year exemption (total and partial exemption) period. The annual exemption totals $55,838,279; that exemption amount is multiplied by the current tax rate, to yield the annual reduction of real estate taxes. During the 2016 tax year, the dollar value of the exemption applied to taxes due totaled $5,950,127 (based on the tax rate of 10.656%) and that exemption was deducted from the $7,390,842 annual taxes before ICIP exemption (resulting in an annual $1,440,715 tax bill for the 229 West 43rd Street Retail Condo property). For the first eight tax years beginning July 1, 2009 through June 30, 2017, 100% of the $55,838,279 ICIP exemption will be applied to the tax bills. In the 2017/2018 tax year, 80% of the exemption will be applied, and the exemption will continue to decrease at a rate of 20% per year, until it is entirely phased out after the 12th exemption year, in 2020/2021. Full taxes without any exemption will be owed effective the tax year beginning July 1, 2021. Real estate taxes were underwritten to half of the payable taxes for the 2016/2017 fiscal year and half of the payable taxes for the 2017/2018 fiscal year.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 17 of 139 | |

| Structural and Collateral Term Sheet | JPMDB 2017-C5 |

| 229 West 43rd Street Retail Condo | |

The 229 West 43rd Street Retail Condo property is located in the Times Square retail submarket of New York City, which is defined as Broadway between West 42nd and West 47th Streets. The 229 West 43rd Street Retail Condo property is located across from the famous Shubert Alley and adjacent to the Times Square “bowtie”. Times Square is a highly visited tourist attraction, with an average of 350,000 people passing through the “bowtie” every day, according to the appraisal. The neighborhood is home to numerous retail and entertainment companies such as ABC/Disney, Forever21, Clear Channel Entertainment, MTV and Oakley Sunglasses as well as a number of high profile office tenants including Morgan Stanley, Thomson Reuters, the New York Times, NASDAQ, Microsoft and Ernst & Young.

The submarket also benefits from numerous transportation options. These include the Times Square subway station (the largest in New York City), MTA Buses, the Port Authority Bus Terminal and quick access to Grand Central Terminal and Penn Station. The Times Square/42nd Street/Eighth Avenue interlinked subway stations offer access to 11 different subway lines (A, C, E, N, Q, R, 1, 2, 3, 7 and Shuttle to Grand Central Terminal).

According to the appraisal, the Times Square submarket contains 169 buildings and 2,482,831 square feet of total rentable area. As of mid-year 2016, there was 258,718 square feet of directly vacant space available, which equates to a direct vacancy rate of 10.4%. Retail asking rents for grade level space in the submarket were $2,109 per square foot as of second quarter of 2016, a decrease of 8.1% over the quarter and a decrease of 15.9% year-over-year. Despite this recent decline, the Times Square submarket continued to experience the greatest long term increase in asking rents tracked by the appraisal. Five years ago, asking rents in the submarket were $691 per square foot, which equates to a 238.0% increase.

The appraisal identified the following six properties as sales comparables for the 229 West 43rd Street Retail Condo property. The adjusted comparables range from $1,574 per square foot to $2,045 per square foot with an average of approximately $1,982 per square foot.

| Summary of Comparable Sales(1) | ||||||||

| Property | NRA | Year Built | No. Stories | Sales Date | Sales Price | Price per SF | Appraisal’s Adjusted Price per SF | Occupancy |

| 229 West 43rd Street Retail Condo | 248,457(2) | 1913-1947 | 6 | NAP | $470,000,000(3) | $1,892 | NAP | 100%(2)(4) |

| 432-440 Park Avenue | 133,600 | 2016 | 6 | Jun-16 | $411,125,625 | $3,077 | $1,877 | 0% |

| The Shops at Columbus Circle | 461,080 | 2004 | 6 | Jun-15 | $1,040,000,000 | $2,256 | $2,045 | 99% |

| 150 West 34th Street | 77,760 | 1998 | 4 | Jun-15 | $355,500,000 | $4,572 | $1,951 | 100% |

| 530 Fifth Avenue | 56,039 | 1957 | 3 | Sep-14 | $295,000,000 | $5,264 | $2,034 | 47% |

| 697-699 Fifth Avenue | 24,737 | 1903 / 2000 | 3 | Jul-14 | $700,000,000 | $28,298 | $1,574 | 100% |

| 1107 Broadway | 20,609 | 1915 / 2013 | 2 | Feb-14 | $56,500,000 | $2,742 | $1,709 | 21% |

| (1) | Source: Appraisal. |

| (2) | Based on the underwritten rent roll dated October 1, 2016. |

| (3) | Represents the “Hypothetical As-Is” appraised value for the 229 West 43rd Street Retail Condo property. |

| (4) | Includes four tenants (49.0% of net rentable area) that have signed leases but have not yet taken occupancy at the 229 West 43rd Street Retail Condo property. |

The appraisal identified lease comparables ranging from $239.48 per square foot to $350.28 per square foot, on an adjusted basis, for grade space and $130.59 per square foot to $392.08 per square foot, on an adjusted basis, for multi-level space. The appraisal’s market rent conclusions for the 229 West 43rd Street Retail Condo property, broken out by floor and frontage, are summarized in the subsequent chart.

| Retail Market Rent(1) | |

| Space Type | Rent PSF |

| Grade 44th Street | $350.00 |

| Grade 43rd Street | $250.00 |

| 2nd Floor / Mezzanine | $100.00 |

| 3rd Floor | $80.00 |

| 4th Floor | $70.00 |

| Lower Level | $75.00 |

| Sub-Lower Level | $75.00 |

| (1) | Source: Appraisal. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 18 of 139 | |

| Structural and Collateral Term Sheet | JPMDB 2017-C5 |

| 229 West 43rd Street Retail Condo | |

| Historical and Current Occupancy(1) | ||

| 2014 | 2015 | Current(2) |

| 75.1% | 75.1% | 100.0% |

| (1) | Historical occupancies are as of December 31 of each respective year. |

| (2) | Current occupancy is as of October 1, 2016 and includes four tenants (49.0% of net rentable area) that signed leases but have not yet taken occupancy and opened for business at the 229 West 43rd Street Retail Condo property, each of which is in a free rent period for which $11,061,751 was reserved with lender at loan origination. |

| Tenant Summary(1) | |||||||||||

| Tenant | Ratings(2) Fitch/Moody’s/S&P | Net Rentable Area (SF) | % of Total NRA | Base Rent PSF | % of Total Base Rent | Lease Expiration Date | |||||

| Bowlmor Times Square, LLC | NA / NA / NA | 77,536 | 31.2% | $63.84 | 20.5% | 7/31/2034 | |||||

| National Geographic(2) | NA / NA / NA | 59,137 | 23.8% | $101.46 | 24.9% | 10/31/2032 | |||||

| Gulliver’s Gate(3) | NA / NA / NA | 49,000 | 19.7% | $117.35 | 23.8% | 1/31/2031 | |||||

| Guitar Center Stores, Inc. | NA / NA / NA | 28,119 | 11.3% | $61.52 | 7.2% | 1/31/2029 | |||||

| Guy’s American Kitchen | NA / NA / NA | 15,670 | 6.3% | $118.25 | 7.7% | 11/30/2032 | |||||

| OHM (American Market by Todd English)(4) | NA / NA / NA | 11,970 | 4.8% | $192.15 | 9.5% | 7/31/2031 | |||||

| Haru Broadway Corp. | NA / NA / NA | 5,300 | 2.1% | $225.00 | 4.9% | 12/31/2028 | |||||

| Los Tacos No.1(5) | NA / NA / NA | 1,725 | 0.7% | $208.70 | 1.5% | 11/30/2031 | |||||

| (1) | Based on the underwritten rent roll dated October 1, 2016. |

| (2) | National Geographic signed a 16-year lease for its space on June 14, 2016. The tenant took possession of its space in October 2016 and is expected to open for business in August 2017. The tenant is in a free rent period until October 8, 2017, and the related rent was reserved with lender at loan origination. |

| (3) | Gulliver’s Gate signed a 15-year lease for its space on November 9, 2015. The tenant took possession of its space in January 2016 and is expected to open for business in the spring of 2017. The tenant was in a free rent period until January 4, 2017, and the related rent was reserved with lender at loan origination. |

| (4) | OHM (American Market by Todd English) signed a 15-year lease for its space on August 1, 2016. The tenant is took possession of its space in March 2017 and is expected to open for business in April 2017. The tenant is in a free rent period until November 1, 2017, and the related rent was reserved with lender at loan origination. |

| (5) | Los Tacos No.1 signed a 15-year lease for its space on June 8, 2016. The tenant took possession of its space in December 2016 and is expected to open for business in July 2017. The tenant is in a free rent period until September 1, 2017, and the related rent was reserved with lender at loan origination. |

| Lease Rollover Schedule(1)(2) | ||||||||||||||

Year | Number of | Net Rentable | % of NRA | Base Rent | % of Base | Cumulative | Cumulative | Cumulative | Cumulative | |||||

| Vacant | NAP | 0 | 0.0 | % | NAP | NAP | 0 | 0.0% | NAP | NAP | ||||

| 2017 & MTM | 0 | 0 | 0.0 | $0 | 0.0 | % | 0 | 0.0% | $0 | 0.0% | ||||

| 2018 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | |||||

| 2019 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | |||||

| 2020 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | |||||

| 2021 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | |||||

| 2022 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | |||||

| 2023 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | |||||

| 2024 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | |||||

| 2025 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | |||||

| 2026 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | |||||

| 2027 | 0 | 0 | 0.0 | 0 | 0.0 | 0 | 0.0% | $0 | 0.0% | |||||

| 2028 & Beyond | 8 | 248,457 | 100.0 | 24,135,419 | 100.0 | 248,457 | 100.0% | $24,135,419 | 100.0% | |||||

| Total | 8 | 248,457 | 100.0 | % | $24,135,419 | 100.0 | % | |||||||

| (1) | Based on the underwritten rent roll. |

| (2) | Certain tenants may have contraction options that may be exercisable prior to the originally stated expiration date of the tenant lease that are not considered above. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 19 of 139 | |

| Structural and Collateral Term Sheet | JPMDB 2017-C5 |

| 229 West 43rd Street Retail Condo | |

| Operating History and Underwritten Net Cash Flow(1) | ||||||||||||

2013 | 2014 | T-10 Ann.(2) | Underwritten(3) | Per Square Foot | %(4) | |||||||

| Rents In Place | $14,741,197 | $16,019,885 | $16,863,101 | 24,135,419 | $97.14 | 95.0 | % | |||||

| Vacant Income | 0 | 0 | 0 | 0 | 0.00 | 0.0 | ||||||

| Gross Potential Rent | $14,741,197 | $16,019,885 | $16,863,101 | $24,135,419 | $97.14 | 95.0 | % | |||||

| Total Reimbursements | 2,670,754 | 2,443,708 | 782,785 | 1,261,739 | 5.08 | 5.0 | ||||||

| Net Rental Income | $17,411,951 | $18,463,593 | $17,645,886 | $25,397,158 | $102.22 | 100.0 | % | |||||

| (Vacancy & Credit Loss) | (739,044) | (1,070,219) | 0 | 0 | 0.00 | (0.0) | ||||||

| Effective Gross Income | $16,672,907 | $17,393,374 | $17,645,886 | $25,397,158 | $102.22 | 100.0 | % | |||||

| Total Expenses | $7,051,784 | $5,444,159 | $3,870,185 | $3,895,157 | $15.68 | 15.3 | % | |||||

| Net Operating Income | $9,621,123 | $11,949,215 | $13,775,701 | $21,502,001 | $86.54 | 84.7 | % | |||||

| Total TI/LC, Capex/RR | 0 | 0 | 0 | 1,294,346 | 5.21 | 5.1 | ||||||

| Net Cash Flow | $9,621,123 | $11,949,215 | $13,775,701 | $20,207,655 | $81.33 | 79.6 | % | |||||

| (1) | 2015 figures are not available due to the borrowers’ acquisition of the 229 West 43rd Street Retail Condo property in October 2015. |

| (2) | T-10 Ann. column represents the trailing 10-month period ending on August 31, 2016 annualized. |

| (3) | The increase in Underwritten Net Cash Flow is due to 121,832 square feet of recent leasing at the 229 West 43rd Street Retail Condo property (49.0% of net rentable area and 59.7% of underwritten base rent). |

| (4) | % column represents percentage of Net Rental Income for all revenue line items and represents percentage of Effective Gross Income for the remainder of the fields. |

Property Management. The 229 West 43rd Street Retail Condo property is managed by Westminster Management, LLC, an affiliate of the borrowers.

Escrows and Reserves. At loan origination, the borrowers deposited $14,492,159 into a tenant improvement and leasing commissions reserve account for tenant improvements, leasing commissions and landlord work in connection with the National Geographic, Gulliver’s Gate, OHM and Los Tacos No. 1 leases, $11,061,751 into a free rent reserve account in connection with free rent periods under the National Geographic, Gulliver’s Gate, OHM and Los Tacos No. 1 leases, $651,564 into a tax reserve account and $18,983 into an insurance reserve account, $48,329 into a bridge rent reserve account in connection with the Los Tacos No. 1 lease and $23,000 into a required repairs account, which represents 115% of the estimated costs.

Tax Escrows- On a monthly basis, the borrowers are required to deposit reserves of 1/12 of the estimated annual real estate taxes, which currently equates to $126,690.

Insurance Escrows - Provided that an acceptable blanket policy is no longer in place, on a monthly basis, the borrowers are required to escrow 1/12 of annual insurance premiums.

Replacement Reserves– On a monthly basis, the borrowers are required to escrow $6,211 (approximately $0.20 per square foot annually) into a replacement reserve. The replacement reserve is not subject to a cap.

Lockbox / Cash Management.The 229 West 43rd Street Retail Condo Whole Loan is structured with a hard lockbox and in-place cash management. The borrowers were required to send tenant direction letters to all tenants instructing them to deposit all rents and other payments into the clearing account controlled by the lender. All funds in the clearing account are required to be transferred on a daily basis into a deposit account established and maintained by the lender, and applied to all required payments and reserves as set forth in the 229 West 43rd Street Retail Condo Whole Loan documents. Provided no Trigger Period (as defined below) is continuing, excess cash in the deposit account will be disbursed to the borrowers in accordance with the 229 West 43rd Street Retail Condo Whole Loan documents.

A “Trigger Period” will commence upon the occurrence of (i) an event of default, (ii) the debt service coverage ratio, as of any calculation date, falling below 1.75x based on the 229 West 43rd Street Retail Condo Whole Loan balance or 1.10x based on the total debt (including the mezzanine loan balance), (iii) a mezzanine loan default, (iv) a Lease Sweep Period (as defined herein) or (v) receipt by the lender of a mezzanine loan trigger period commencement notice and will end upon (a) with respect to clause (i), the date on which such event of default is cured, (b) with respect to clause (ii), the debt service coverage ratio is at least 1.75x based on the whole loan balance or 1.10x based on the total debt (including the mezzanine loan balance), in each case, for two consecutive calendar quarters, (c) with respect to clause (iii), the receipt by lender of a mezzanine loan default revocation notice, (d) with respect to clause (iv), such Lease Sweep Period has ended or (e) with respect to clause (v), provided no other Trigger Period is continuing, receipt by lender of a mezzanine loan trigger period termination notice.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 20 of 139 | |

| Structural and Collateral Term Sheet | JPMDB 2017-C5 |

| 229 West 43rd Street Retail Condo | |