| | | FREE WRITING PROSPECTUS |

| | | FILED PURSUANT TO RULE 433 |

| | | REGISTRATION FILE NO.: 333-226123-06 |

| | | |

| November [5], 2019 | | JPMDB 2019-COR6 |

Free Writing Prospectus Structural and Collateral Term Sheet |

JPMDB 2019-COR6 |

This material is for your information, and none of J.P. Morgan Securities LLC (“JPMS”), Deutsche Bank Securities Inc., Jefferies LLC and Drexel Hamilton, LLC, (each individually, an “Underwriter”, and together, the ‘‘Underwriters’’) are soliciting any action based upon it. This material is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. The depositor has filed a registration statement (including a prospectus) with the SEC (SEC File No. 333-226123) for the offering to which this free writing prospectus relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter or any dealer participating in the offering will arrange to send you the prospectus if you request it by calling (800) 408-1016 or by emailing the ABS Syndicate Desk atabs_synd@jpmorgan.com. THE SECURITIES TO WHICH THIS INFORMATION RELATES WILL BE MORE FULLY DESCRIBED IN A PROSPECTUS (THE “PROSPECTUS”), WHICH IS NOT YET AVAILABLE. THE PROSPECTUS WILL CONTAIN MATERIAL INFORMATION THAT IS NOT CONTAINED IN THESE MATERIALS (INCLUDING WITHOUT LIMITATION A DETAILED DISCUSSION OF RISKS ASSOCIATED WITH AN INVESTMENT IN THE CERTIFICATES, UNDER THE HEADING“RISK FACTORS”IN THE PROSPECTUS). Neither this document nor anything contained in this document shall form the basis for any contract or commitment whatsoever. The information contained in this document is preliminary as of the date of this document, supersedes any previous such information delivered to you and will be superseded by any such information subsequently delivered prior to the time of sale. These materials are subject to change, completion or amendment from time to time. This information is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. J.P. Morgan is the marketing name for the investment banking businesses of JPMorgan Chase & Co. and its subsidiaries worldwide. Securities, syndicated loan arranging, financial advisory and other investment banking activities are performed by JPMS and its securitiesaffiliates, and lending, derivatives and other commercial banking activities are performed by JPMorgan Chase Bank, National Association and its banking affiliates. JPMS is a member of SIPC and the NYSE. THE UNDERWRITERS MAY FROM TIME TO TIME PERFORM INVESTMENT BANKING SERVICES FOR, OR SOLICIT INVESTMENT BANKING BUSINESS FROM, ANY COMPANY NAMED IN THESE MATERIALS. THE UNDERWRITERS AND/OR THEIR AFFILIATES OR RESPECTIVE EMPLOYEES MAY FROM TIME TO TIME HAVE A LONG OR SHORT POSITION IN ANY CERTIFICATE OR CONTRACT DISCUSSED IN THESE MATERIALS. |

|

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE.THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| November [4], 2019 | | JPMDB 2019-COR6 |

THE REPUBLIC OF KOREA

THE OFFERED CERTIFICATES HAVE NOT BEEN REGISTERED WITH THE FINANCIAL SERVICES COMMISSION OF THE REPUBLIC OF KOREA FOR A PUBLIC OFFERING IN THE REPUBLIC OF KOREA. THE UNDERWRITERS HAVE THEREFORE REPRESENTED AND AGREED THAT THE OFFERED CERTIFICATES HAVE NOT BEEN AND WILL NOT BE OFFERED, SOLD OR DELIVERED DIRECTLY OR INDIRECTLY, OR OFFERED, SOLD OR DELIVERED TO ANY PERSON FOR RE-OFFERING OR RESALE, DIRECTLY OR INDIRECTLY IN THE REPUBLIC OF KOREA OR TO ANY RESIDENT OF THE REPUBLIC OF KOREA EXCEPT AS OTHERWISE PERMITTED UNDER APPLICABLE LAWS AND REGULATIONS OF THE REPUBLIC OF KOREA, INCLUDING THE FINANCIAL INVESTMENT SERVICES AND CAPITAL MARKETS ACT AND THE FOREIGN EXCHANGE TRANSACTIONS LAW AND THE DECREES AND REGULATIONS THEREUNDER.

JAPAN

THE OFFERED CERTIFICATES HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDER THE FINANCIAL INSTRUMENTS AND EXCHANGE LAW OF JAPAN, AS AMENDED (THE “FIEL”), AND DISCLOSURE UNDER THE FIEL HAS NOT BEEN AND WILL NOT BE MADE WITH RESPECT TO THE OFFERED CERTIFICATES. ACCORDINGLY, EACH UNDERWRITER HAS REPRESENTED AND AGREED THAT IT HAS NOT, DIRECTLY OR INDIRECTLY, OFFERED OR SOLD AND WILL NOT, DIRECTLY OR INDIRECTLY, OFFER OR SELL ANY OFFERED CERTIFICATES IN JAPAN OR TO, OR FOR THE BENEFIT OF, ANY RESIDENT OF JAPAN (WHICH TERM AS USED IN THIS PROSPECTUS MEANS ANY PERSON RESIDENT IN JAPAN, INCLUDING ANY CORPORATION OR OTHER ENTITY ORGANIZED UNDER THE LAWS OF JAPAN) OR TO OTHERS FOR REOFFERING OR RE-SALE, DIRECTLY OR INDIRECTLY, IN JAPAN OR TO, OR FOR THE BENEFIT OF, ANY RESIDENT OF JAPAN EXCEPT PURSUANT TO AN EXEMPTION FROM THE REGISTRATION REQUIREMENTS OF, AND OTHERWISE IN COMPLIANCE WITH, THE FIEL AND OTHER RELEVANT LAWS, REGULATIONS AND MINISTERIAL GUIDELINES OF JAPAN. AS PART OF THIS OFFERING OF THE OFFERED CERTIFICATES, THE UNDERWRITERS MAY OFFER THE OFFERED CERTIFICATES IN JAPAN TO UP TO 49 OFFEREES IN ACCORDANCE WITH THE ABOVE PROVISIONS.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE.THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

| Collateral Characteristics |

| Loan Pool | |

| | Initial Pool Balance (“IPB”): | $807,180,797 |

| | Number of Mortgage Loans: | 32 |

| | Number of Mortgaged Properties: | 117 |

| | Average Cut-off Date Balance per Mortgage Loan: | $25,224,400 |

| | Weighted Average Current Mortgage Rate: | 3.94484% |

| | 10 Largest Mortgage Loans as % of IPB: | 57.5% |

| | Weighted Average Remaining Term to Maturity: | 115 months |

| | Weighted Average Seasoning: | 2 months |

| | | |

| Credit Statistics | |

| | Weighted Average UW NCF DSCR(1)(2): | 2.18x |

| | Weighted Average UW NOI Debt Yield(1): | 9.7% |

| | Weighted Average Cut-off Date Loan-to-Value Ratio (“LTV”)(1)(3): | 61.2% |

| | Weighted Average Maturity Date LTV(1)(3): | 58.2% |

| | | |

| Other Statistics | |

| | % of Mortgage Loans with Additional Debt: | 20.9% |

| | % of Mortgaged Properties with Single Tenants: | 14.6% |

| | | |

| Amortization | |

| | Weighted Average Original Amortization Term(4): | 359 months |

| | Weighted Average Remaining Amortization Term(4): | 357 months |

| | % of Mortgage Loans with Interest-Only: | 68.8% |

| | % of Mortgage Loans with Amortizing Balloon: | 21.2% |

| | % of Mortgage Loans with Partial Interest-Only followed by Amortizing Balloon: | 9.9% |

| | | |

| Lockbox / Cash Management(5) | |

| | % of Mortgage Loans with In-Place, Hard Lockboxes: | 76.0% |

| | % of Mortgage Loans with Springing Lockboxes: | 12.2% |

| | % of Mortgage Loans with In-Place, Soft Lockboxes: | 11.8% |

| | % of Mortgage Loans with In-Place Cash Management: | 10.6% |

| | % of Mortgage Loans with Springing Cash Management: | 89.4% |

| | | |

| Reserves | |

| | % of Mortgage Loans Requiring Monthly Tax Reserves: | 65.8% |

| | % of Mortgage Loans Requiring Monthly Insurance Reserves: | 34.9% |

| | % of Mortgage Loans Requiring Monthly CapEx Reserves(6): | 65.3% |

| | % of Mortgage Loans Requiring Monthly TI/LC Reserves(7): | 56.3% |

| | | |

| (1) | In the case of Loan Nos. 1, 2, 3, 4, 5, 7, 9, 11, 14, 16, 17, 18, 20 and 26, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 1, 5, 7 and 16, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or related mezzanine loan(s). |

| (2) | In the case of Loan No. 7, the UW NCF DSCR is calculated using the sum of the first 12 mortgage loan principal and interest payments after the Cut-off Date based on the assumed principal and interest payment schedule set forth in Annex H of the Preliminary Prospectus. |

| (3) | In the case of Loan Nos. 3, 17 and 20, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to“Description of the Mortgage Pool—Assessments of Property Value and Condition” and“—Appraised Value” in the Preliminary Prospectus for additional details. |

| (4) | Excludes 20 mortgage loans that are interest-only for the entire term. |

| (5) | For a more detailed description of Lockbox / Cash Management, refer to“Description of the Mortgage Pool—Certain Terms of the Mortgage Loans—Mortgaged Property Accounts” in the Preliminary Prospectus. |

| (6) | CapEx Reserves include FF&E reserves for hotel properties. |

| (7) | Calculated only with respect to the Cut-off Date Balance of mortgage loans secured or partially secured by retail, office, industrial and mixed use properties. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 3 of 95 |  |

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

| Collateral Characteristics |

Mortgage Loan Seller | Number of

Mortgage Loans | Number of

Mortgaged

Properties | Aggregate

Cut-off Date

Balance | |

| LCM | 22 | 100 | $485,460,797 | 60.1% |

| JPMCB(1) | 9 | 16 | 259,220,000 | 32.32.1.1 |

| GACC(2) | 1 | 1 | 62,500,000 | 7.7% |

| Total | 32 | 117 | $807,180,797 | 100.0% |

| (1) | In the case of Loan No. 16, the whole loan was co-originated by JPMCB, Morgan Stanley Bank, N.A., Wells Fargo Bank, National Association and Goldman Sachs Bank USA. In the case of Loan Nos. 17 and 18, the whole loan was co-originated by JPMCB and Wells Fargo Bank, National Association. |

| (2) | In the case of Loan No. 1, such mortgage loan being sold by GACC was originated by an affiliate thereof, Deutsche Bank AG, New York Branch (“DBNY”). DBNY on the origination date transferred such mortgage loan to DBR Investments Co. Limited (“DBRI”), and DBRI will transfer such mortgage loan to GACC on or prior to the closing date. The Century Plaza Towers Whole Loan, with respect to which such mortgage loan is a part of, was co-originated by DBNY, Morgan Stanley Bank, N.A. and Wells Fargo Bank, National Association. |

| Ten Largest Mortgage Loans |

| |

| No. | Loan Name | Mortgage

Loan Seller | No.

of Prop. | Cut-off

Date

Balance | % of

IPB | SF / Units/ | Property

Type | UW

NCF

DSCR(1)(2) | UW NOI

Debt

Yield(1) | Cut-off

Date

LTV(1)(3) | Maturity

Date

LTV(1)(3) |

| 1 | Century Plaza Towers | GACC | 1 | $62,500,000 | 7.7% | 2,401,641 | Office | 4.09x | 13.5% | 39.1% | 39.1% |

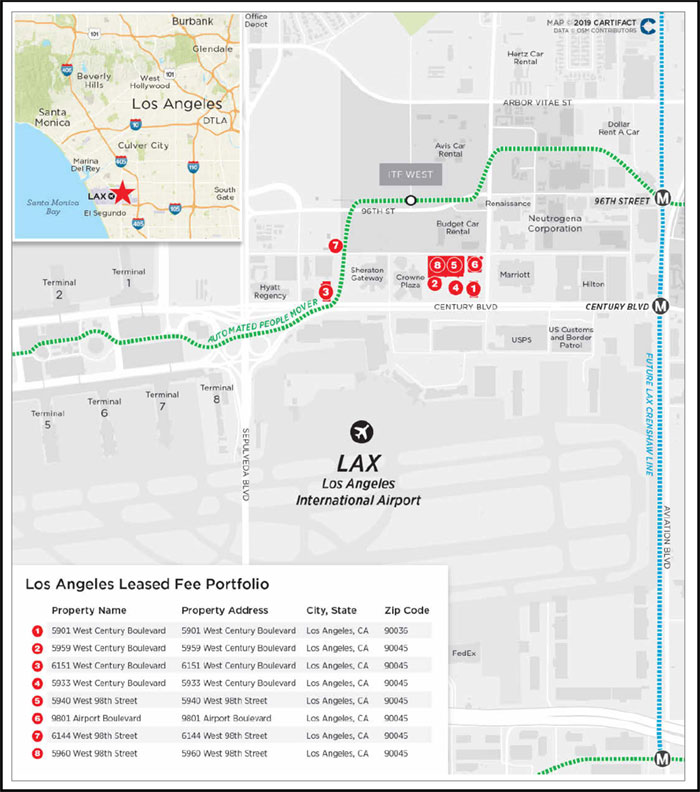

| 2 | Los Angeles Leased Fee Portfolio | LCM | 8 | $61,000,000 | 7.6% | 556,202 | Other | 1.75x | 6.2% | 63.0% | 63.0% |

| 3 | Innovation Park | JPMCB | 1 | $55,000,000 | 6.8% | 1,854,729 | Office | 2.96x | 11.6% | 68.8% | 68.8% |

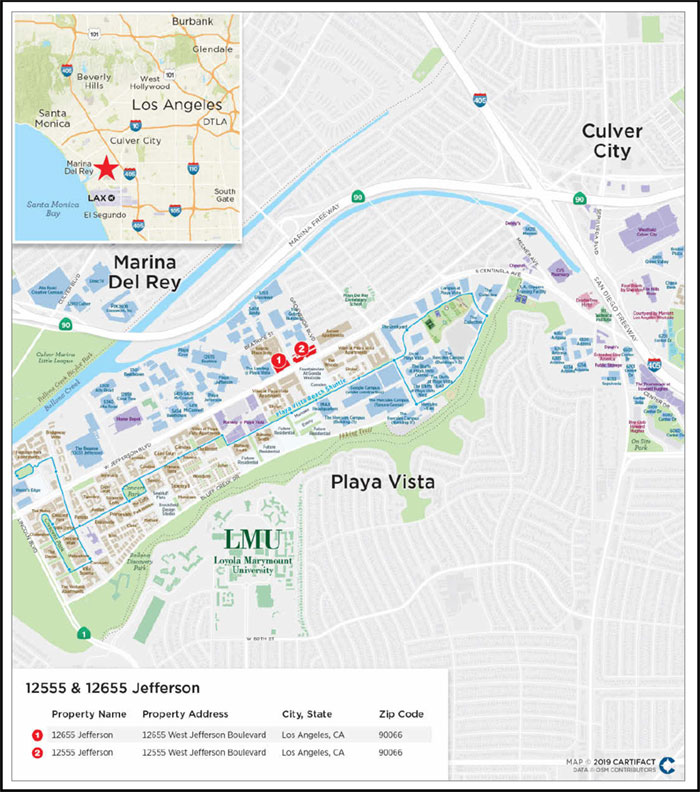

| 4 | 12555 & 12655 Jefferson | LCM | 2 | $54,000,000 | 6.7% | 193,908 | Office | 1.80x | 7.6% | 59.5% | 59.5% |

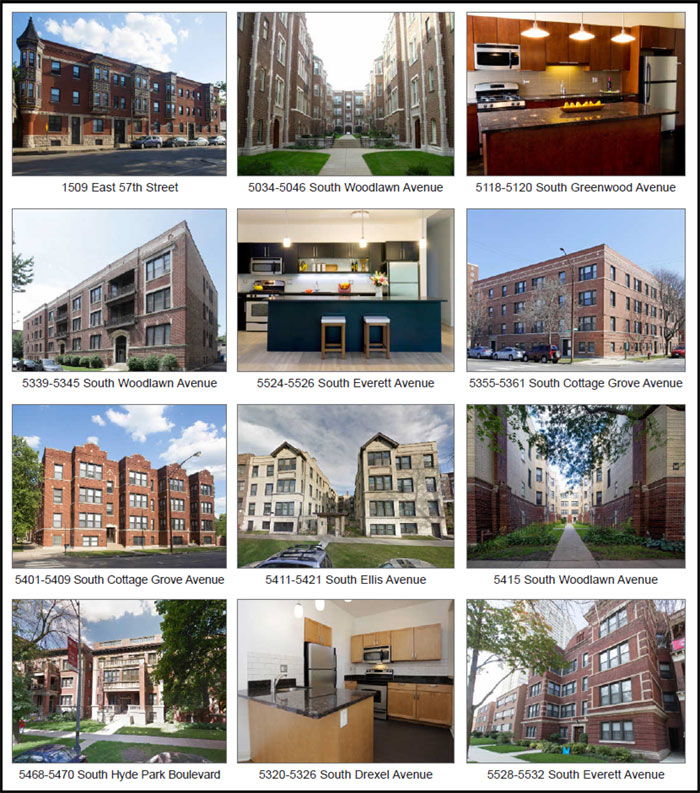

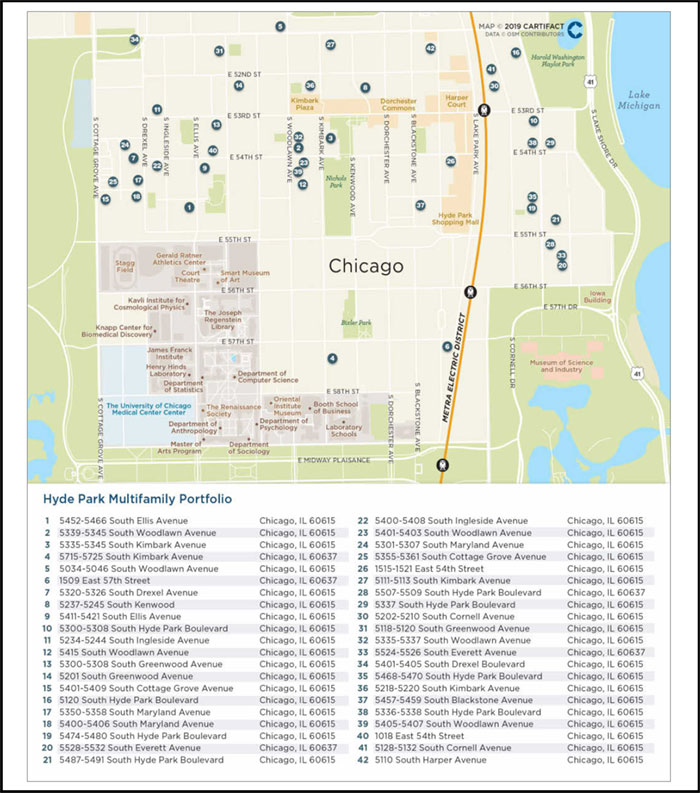

| 5 | Hyde Park Multifamily Portfolio | LCM | 42 | $46,750,000 | 5.8% | 839 | Multifamily | 1.82x | 8.7% | 60.5% | 60.5% |

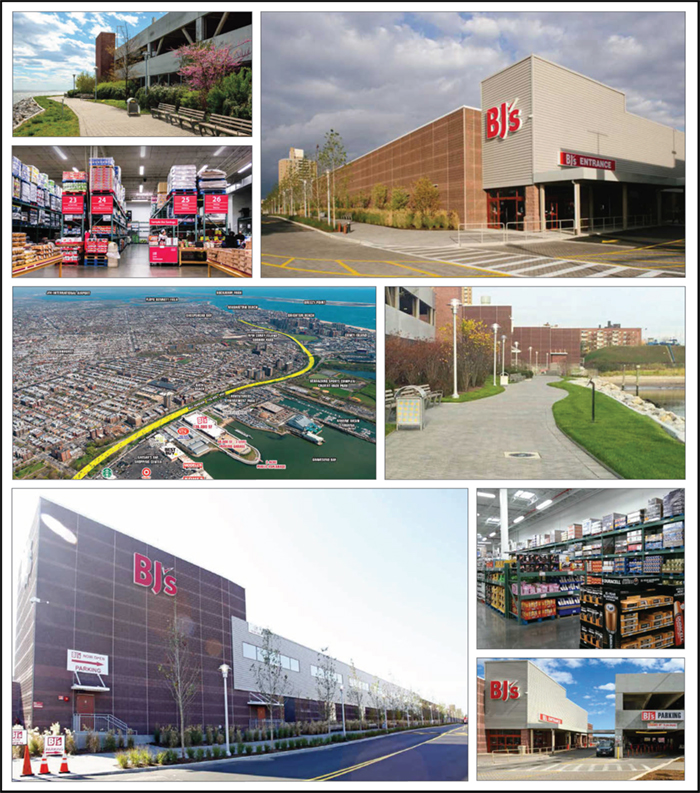

| 6 | BJ’s Wholesale Club | JPMCB | 1 | $40,150,000 | 5.0% | 135,753 | Retail | 2.58x | 9.4% | 54.3% | 54.3% |

| 7 | Hampton Roads Office Portfolio | LCM | 22 | $39,723,151 | 4.9% | 1,322,003 | Office | 1.40x | 10.8% | 71.3% | 60.3% |

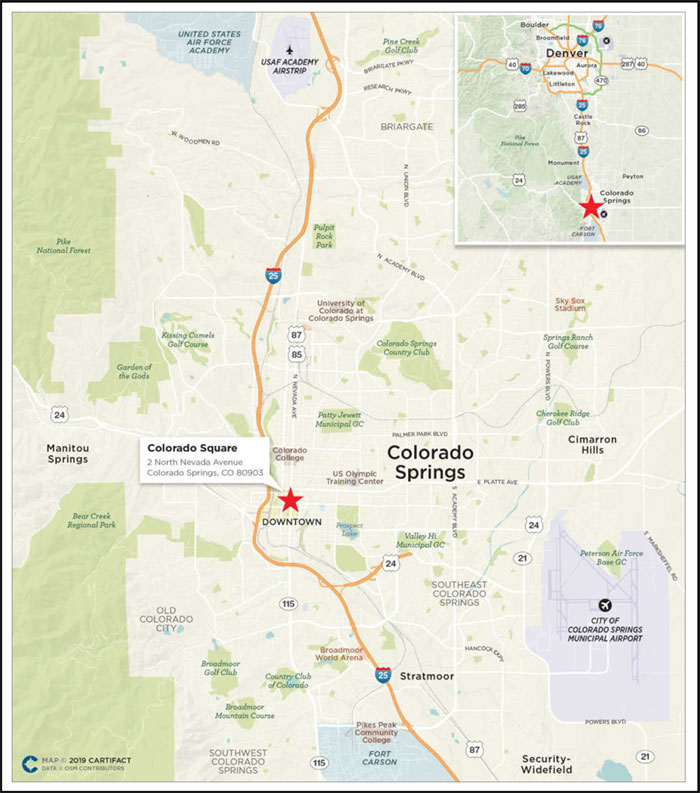

| 8 | Colorado Square | LCM | 1 | $37,050,001 | 4.6% | 245,509 | Office | 1.53x | 9.3% | 71.8% | 57.5% |

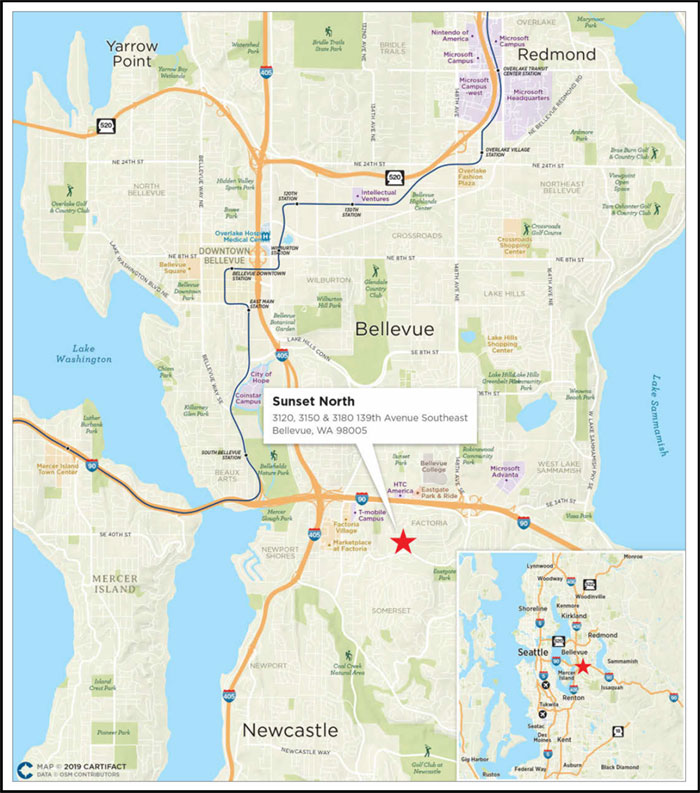

| 9 | Sunset North | JPMCB | 1 | $35,000,000 | 4.3% | 464,061 | Office | 2.63x | 9.1% | 66.1% | 66.1% |

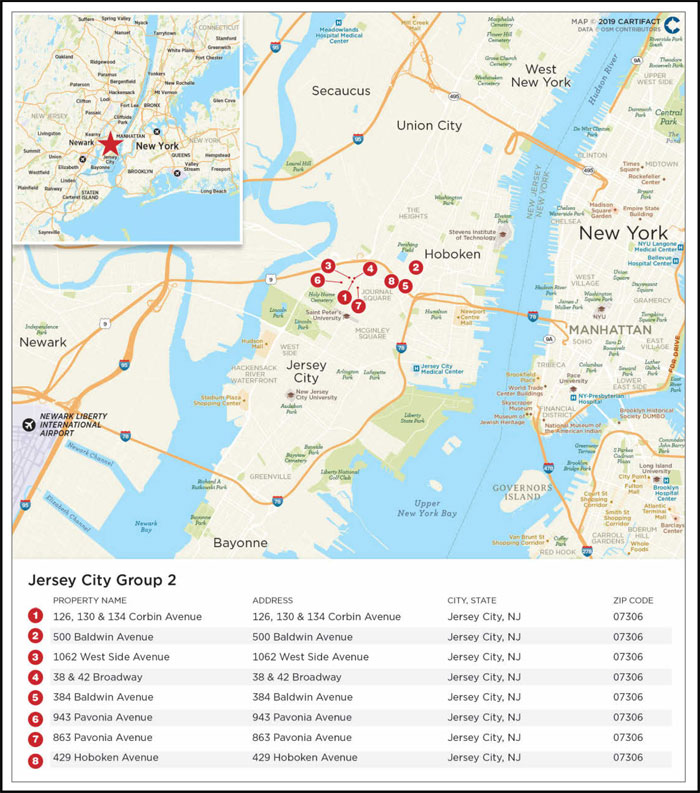

| 10 | Jersey City Group 2 | JPMCB | 8 | $32,840,000 | 4.1% | 201 | Multifamily | 1.04x | 6.6% | 78.6% | 72.0% |

| | | | | | | | | | | | |

| | Top 3 Total/Weighted Average | 10 | $178,500,000 | 22.1% | | | 2.94x | 10.4% | 56.4% | 56.4% |

| | Top 5 Total/Weighted Average | 54 | $279,250,000 | 34.6% | | | 2.53x | 9.6% | 57.7% | 57.7% |

| | Top 10 Total/Weighted Average | 87 | $464,013,153 | 57.5% | | | 2.26x | 9.4% | 61.8% | 59.3% |

| (1) | In the case of Loan Nos. 1, 2, 3, 4, 5, 7 and 9, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 1, 5 and 7, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or related mezzanine loan(s). |

| (2) | With respect to Loan No. 7, the UW NCF DSCR is calculated using the sum of the first 12 whole loan principal and interest payments after the Cut-off Date based on the assumed principal and interest payment schedule set forth in Annex H of the Preliminary Prospectus. |

| (3) | In the case of Loan No. 3, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 4 of 95 | |

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

| Collateral Characteristics |

| Pari Passu Companion Loan Summary |

| Loan No. | Mortgage Loan | Note(s) | Original Balance

($) | Cut-off Date

Balance ($) | Holder of Note | Lead

Servicer for

Whole Loan

(Y/N) |

Master

Servicer

Under Lead

Securitization | Special Servicer

Under Lead

Securitization |

| 1 | Century Plaza Towers | A-1-S1, A-1-S2, A-1-S3, A-2-S1, A-2-S2, A-2-S3, A-2-C1, A-2-C3, A-2-C4, A-3-S1, A-3-S2, A-3-S3, A-3-C1, A-3-C3 | $525,000,000 | $525,000,000 | CPTS 2019-CPT | Yes(2) | Wells | CWCapital |

| | A-1-C3, A-1-C8 | $62,500,000 | $62,500,000 | JPMDB 2019-COR6 | No | | |

| | A-1-C1, A-1-C2, A-1-C4, A-1-C5, A-1-C6, A-1-C7, | $187,500,000 | $187,500,000 | DBRI | No | | |

| | | A-2-C2, A-2-C5, A-2-C6, A-2-C7 | $62,500,000 | $62,500,000 | MSBNA | No | | |

| | | A-3-C2, A-3-C4, A-3-C5 | $62,500,000 | $62,500,000 | WFBNA | No | | |

| | | B-1, B-2, B-3(1) | $300,000,000 | $300,000,000 | CPTS 2019-CPT | No(2) | | |

| | | Total | $1,200,000,000 | $1,200,000,000 | | | | |

| 2 | Los Angeles Leased Fee Portfolio | A-1 | $61,000,000 | $61,000,000 | JPMDB 2019-COR6 | Yes | Midland | Midland |

| | A-2 | $24,000,000 | $24,000,000 | LCM | No | | |

| | | Total | $85,000,000 | $85,000,000 | | | | |

| 3 | Innovation Park | A-1 | $60,000,000 | $60,000,000 | BMARK 2019-B14 | No(3) | | |

| | A-2 | $67,250,000 | $67,250,000 | JPMCB | Yes | (3) | (3) |

| | | A-3 | $55,000,000 | $55,000,000 | JPMDB 2019-COR6 | No | | |

| | | Total | $182,250,000 | $182,250,000 | | | | |

4 | 12555 &12655 Jefferson | A-1 | $54,000,000 | $54,000,000 | JPMDB 2019-COR6 | Yes | Midland | Midland |

| | A-2 | $30,000,000 | $30,000,000 | LCM | No | | |

| | | A-3 | $27,000,000 | $27,000,000 | LCM | No | | |

| | | Total | $111,000,000 | $111,000,000 | | | | |

5 | Hyde Park Multifamily Portfolio | A-1 | $60,000,000 | $60,000,000 | JPMCC 2019-COR5 | Yes | Midland | Midland |

| | A-2 | $46,750,000 | $46,750,000 | JPMDB 2019-COR6 | No | | |

| | | Total | $106,750,000 | $106,750,000 | | | | |

7 | Hampton Roads Office Portfolio | A-1, A-5 | $50,000,000 | $49,653,939 | JPMCC 2019-COR5 | Yes | Midland | Midland |

| | A-3, A-4 | $40,000,000 | $39,723,151 | JPMDB 2019-COR6 | No | | |

| | A-2 | $33,000,000 | $32,771,600 | LCM | No | | |

| | A-6 | $10,000,000 | $9,930,788 | LCM | No | | |

| | Total | $133,000,000 | $132,079,478 | | | | |

9 | Sunset North | A-1 | $75,000,000 | $75,000,000 | BMARK 2019-B13 | Yes | Midland | CWCapital |

| | | A-2 | $20,000,000 | $20,000,000 | BMARK 2019-B14 | No | | |

| | | A-3-1 | $35,000,000 | $35,000,000 | JPMDB 2019-COR6 | No | | |

| | | A-3-2 | $20,000,000 | $20,000,000 | JPMCB | No | | |

| | | Total | $150,000,000 | $150,000,000 | | | | |

| 11 | Belvedere Place | A-1 | $32,750,000 | $32,750,000 | JPMDB 2019-COR6 | Yes | Midland | Midland |

| | A-2 | $11,250,000 | $11,250,000 | LCM | No | | |

| | | Total | $44,000,000 | $44,000,000 | | | | |

14 | Brooklyn Renaissance Plaza | A-1 | $65,000,000 | $64,503,166 | JPMCC 2019-COR5 | Yes | Midland | Midland |

| | A-2 | $25,000,000 | $24,808,910 | JPMDB 2019-COR6 | No | | |

| | | Total | $90,000,000 | $89,312,076 | | | | |

| (1) | Each note represents a subordinate companion loan. |

| (2) | In the case of Loan No. 1, the initial control note is Note B-1. During the continuance of a Century Plaza Towers Control Appraisal Period, Note A-1-S1 will be the Control Note. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans—The Century Plaza Towers Whole Loan” in the Preliminary Prospectus. |

| (3) | In the case of Loan No. 3, the whole loan is expected to be serviced under the BMARK 2019-B14 pooling and servicing agreement until such time the controlling note has been securitized, at which point such whole loan will be serviced under the pooling and servicing agreement related to such securitization. JPMCB holds the related controllingpari passucompanion loan and is entitled to exercise control rights until the securitization of such controllingpari passucompanion loan. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 5 of 95 | |

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

| Collateral Characteristics |

| Loan No. | Mortgage

Loan | Note(s) | Original

Balance ($) | Cut-off Date Balance ($) | Holder of Note | Lead

Servicer for

Whole

Loan

(Y/N) | Master

Servicer

Under

Lead

Securitization | Special

Servicer Under

Lead

Securitization |

| 16 | Grand Canal Shoppes | A-1-1, A-1-6 | $70,000,000 | $70,000,000 | MSC 2019-H7 | Yes(2) | Midland | LNR |

| | | A-1-2, A-2-1 | $100,000,000 | $100,000,000 | BANK 2019-BNK19 | No | | |

| | | A-3-1 | $50,000,000 | $50,000,000 | BMARK 2019-B12 | No | | |

| | | A-3-2 | $50,000,000 | $50,000,000 | BMARK 2019-B13 | No | | |

| | | A-4-1 | $60,000,000 | $60,000,000 | CGCMT 2019-GC41 | No | | |

| | | A-4-3 | $20,000,000 | $20,000,000 | GSMS 2019-GC42 | No | | |

| | | A-1-7, A-1-8, A-2-2-1 | $40,000,000 | $40,000,000 | BANK 2019-BNK20 | No | | |

| | | A-2-2-2 | $30,000,000 | $30,000,000 | CSAIL 2019-C17 | No | | |

| | | A-2-3, A-2-5 | $50,384,615 | $50,384,615 | UBS 2019-C17 | No | | |

| | | A-1-4 | $40,000,000 | $40,000,000 | BANK 2019-BNK21 | No | | |

| | | A-3-3-1, A-3-5 | $30,384,615 | $30,384,615 | BMARK 2019-B14 | No | | |

| | | A-1-3, A-1-5 | $53,846,154 | $53,846,154 | MSNBA | No | | |

| | | A-3-3-2 | $20,000,000 | $20,000,000 | JPMDB 2019-COR6 | No | | |

| | | A-3-4 | $25,000,000 | $25,000,000 | CCRE | No | | |

| | | A-4-2, A-4-4, A-4-5 | $95,384,615 | $95,384,615 | GSBI | No | | |

| | | A-2-4 | $25,000,000 | $25,000,000 | UBS AG | No | | |

| | | B-1(1) | $215,000,000 | $215,000,000 | CPPIB Credit Investment II Inc. | No(2) | | |

| | | Total | $975,000,000 | $975,000,000 | | | | |

17 | 600 & 620 National Avenue | A-1-1 | $38,950,000 | $38,950,000 | UBSCM 2019-C17 | Yes | Midland | CWCapital |

| | A-2-1-A | $20,000,000 | $20,000,000 | BMARK 2019-B14 | No | | |

| | | A-1-2 | $30,000,000 | $30,000,000 | WFM | No | | |

| | | A-2-2-A | $20,000,000 | $20,000,000 | JPMDB 2019-COR6 | No | | |

| | | A-2-1-B, A-2-2-B, A-2-3 | $28,950,000 | $28,950,000 | JPMCB | No | | |

| | | Total | $137,900,000 | $137,900,000 | | | | |

18 | Tysons Tower | A-1 | $50,000,000 | $50,000,000 | BANK 2019-BNK21 | Yes | Rialto | Wells |

| | A-2, A-3 | $45,000,000 | $45,000,000 | WFB | No | | |

| | A-4 | $40,000,000 | $40,000,000 | BMARK 2019-B14 | No | | |

| | | A-5 | $20,000,000 | $20,000,000 | JPMDB 2019-COR6 | No | | |

| | | A-6, A-7 | $35,000,000 | $35,000,000 | JPMCB | No | | |

| | | Total | $190,000,000 | $190,000,000 | | | | |

| 20 | Hilton Cincinnati Netherland Plaza | A-1 | $35,550,000 | $35,550,000 | BMARK 2019-B14 | Yes | Midland | Midland |

| | A-2 | $17,000,000 | $17,000,000 | JPMDB 2019-COR6 | No | | |

| | A-3 | $20,000,000 | $20,000,000 | JPMCB | No | | |

| | | Total | $72,500,000 | $72,500,000 | | | | |

| 26 | NOV Headquarters | A-1 | $20,000,000 | $20,000,000 | JPMCC 2019-COR5 | Yes | Midland | Midland |

| A-2 | $9,200,000 | $9,200,000 | JPMDB 2019-COR6 | No | | |

| | | A-3 | $10,000,000 | $10,000,000 | LCM | No | | |

| | | Total | $39,200,000 | $39,200,000 | | | | |

| (1) | Each note represents a subordinate companion loan. |

| (2) | In the case of Loan No. 16, the initial control note is Note B-1. During the continuance of a Grand Canal Shoppes Control Appraisal Period, Note A-1-1 will be the Control Note. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans—The Grand Canal Shoppes Whole Loan” in the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 6 of 95 | |

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

| Collateral Characteristics |

No. | Loan Name | Trust

Cut-off Date

Balance | Subordinate

Debt Cut-off

Date

Balance(1) | Total Debt

Cut-off Date

Balance | Mortgage

Loan UW

NCF

DSCR(2)(3) |

Total

Debt

UW

NCF

DSCR(3) | Mortgage Loan

Cut-off Date LTV(2) |

Total

Debt

Cut-off

Date

LTV | Mortgage

Loan UW

NOI Debt

Yield(2) | Total

Debt

UW NOI Debt

Yield |

| 1 | Century Plaza Towers | $62,500,000 | $300,000,000 | $1,200,000,000 | 4.09x | 3.07x | 39.1% | 52.1% | 13.5% | 10.1% |

| 5 | Hyde Park Multifamily Portfolio | $46,750,000 | $15,250,000 | $122,000,000 | 1.82x | 1.48x | 60.5% | 69.2% | 8.7% | 7.6% |

| 7 | Hampton Roads Office Portfolio | $39,723,151 | $19,861,576 | $151,941,054 | 1.40x | 1.16x | 71.3% | 82.0% | 10.8% | 9.4% |

| 16 | Grand Canal Shoppes | $20,000,000 | $215,000,000 | $975,000,000 | 2.46x | 1.67x | 46.3% | 59.5% | 9.6% | 7.5% |

| (1) | In the case of Loan Nos. 5 and 7, Subordinate Debt Cut-off Date Balance represents one or more mezzanine loans. In the case of Loan Nos. 1 and 16, Subordinate Debt Cut-off Date Balance represents one or more Subordinate Companion Loans. |

| (2) | In the case of Loan Nos. 1, 5, 7 and 16, the UW NCF DSCR, UW NOI Debt Yield and Cut-off Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 1, 5, 7 and 16, the UW NCF DSCR, UW NOI Debt Yield and Cut-off Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or related mezzanine loan(s). |

| (3) | With respect to Loan No. 7, the UW NCF DSCR is calculated using the sum of the first 12 mortgage loan principal and interest payments after the Cut-off Date based on the assumed principal and interest payment schedule set forth in Annex H of the Preliminary Prospectus. The Total Debt UW NCF DSCR is calculated using the sum of the first 12 total debt principal and interest payments after the Cut-off Date based on the assumed principal and interest payment schedule set forth in the related mortgage and mezzanine loan agreements. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 7 of 95 | |

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

| Collateral Characteristics |

| Mortgaged Properties by Type(1) |

| | | | | | Weighted Average |

| Property Type | Property Subtype | Number of

Properties | Cut-off Date

Principal

Balance | % of IPB | Occupancy | UW

NCF

DSCR(2)(3) | UW

NOI Debt

Yield(2) | Cut-off

Date

LTV(2)(4) | Maturity

Date

LTV(2)(4) |

| Office | Suburban | 31 | $280,753,630 | 34.8% | 95.9% | 2.22x | 10.2% | 66.2% | 62.6% |

| | CBD | 5 | 178,358,911 | 22.1 | 93.1% | 2.49x | 10.2% | 53.3% | 49.1% |

| | Medical | 4 | 9,200,000 | 1.1 | 100.0% | 1.50x | 10.0% | 58.7% | 53.9% |

| | Subtotal: | 40 | $468,312,541 | 58.0% | 94.9% | 2.31x | 10.2% | 61.2% | 57.3% |

| | | | | | | | | | |

| Multifamily | Garden | 40 | $67,106,565 | 8.3% | 94.3% | 1.44x | 7.7% | 69.4% | 66.1% |

| | Mid-Rise | 11 | 34,064,097 | 4.2 | 97.2% | 1.91x | 8.2% | 61.2% | 61.2% |

| | Subtotal: | 51 | $101,170,662 | 12.5% | 95.2% | 1.60x | 7.9% | 66.6% | 64.5% |

| | | | | | | | | | |

| Retail | Freestanding | 2 | $44,350,000 | 5.5% | 100.0% | 2.51x | 9.3% | 55.1% | 55.1% |

| | Anchored | 2 | 25,553,256 | 3.2 | 94.1% | 2.13x | 11.0% | 60.2% | 56.2% |

| | Specialty Retail | 1 | 20,000,000 | 2.5 | 94.0% | 2.46x | 9.6% | 46.3% | 46.3% |

| | Shadow Anchored | 1 | 3,395,000 | 0.4 | 92.2% | 2.52x | 11.5% | 67.9% | 67.9% |

| | Subtotal: | 6 | $93,298,256 | 11.6% | 96.8% | 2.40x | 9.9% | 55.1% | 54.0% |

| | | | | | | | | | |

| Other | Leased Fee | 8 | $61,000,000 | 7.6% | 100.0% | 1.75x | 6.2% | 63.0% | 63.0% |

| | Parking | 1 | 219,338 | 0.0 | 100.0% | 1.82x | 8.7% | 60.5% | 60.5% |

| | Subtotal: | 9 | $61,219,338 | 7.6% | 100.0% | 1.75x | 6.2% | 63.0% | 63.0% |

| | | | | | | | | | |

| Hotel | Extended Stay | 1 | $25,250,000 | 3.1% | 88.1% | 2.99x | 12.3% | 52.6% | 52.6% |

| | Full Service | 1 | 17,000,000 | 2.1 | 74.8% | 1.62x | 10.9% | 68.7% | 63.7% |

| | Subtotal: | 2 | $42,250,000 | 5.2% | 82.7% | 2.44x | 11.7% | 59.1% | 57.1% |

| | | | | | | | | | |

| Self Storage | Self Storage | 2 | $28,330,000 | 3.5% | 90.5% | 1.81x | 8.9% | 64.2% | 64.2% |

| | Subtotal: | 2 | $28,330,000 | 3.5% | 90.5% | 1.81x | 8.9% | 64.2% | 64.2% |

| | | | | | | | | | |

| Industrial | Flex | 6 | $11,060,700 | 1.4% | 100.0% | 2.49x | 16.8% | 50.8% | 41.0% |

| | Warehouse/Distribution | 1 | 1,539,300 | 0.2 | 100.0% | 1.64x | 10.6% | 66.9% | 55.1% |

| | Subtotal: | 7 | $12,600,000 | 1.6% | 100.0% | 2.39x | 16.1% | 52.8% | 42.7% |

| | Total / Weighted Average: | 117 | 807,180,797 | 100.0% | 94.8% | 2.18x | 9.7% | 61.2% | 58.2% |

| (1) | Because this table presents information relating to the mortgaged properties and not mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated loan amounts. |

| (2) | In the case of Loan Nos. 1, 2, 3, 4, 5, 7, 9, 11, 14, 16, 17, 18, 20 and 26, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 1, 5, 7 and 16, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or related mezzanine loan(s). |

| (3) | With respect to Loan No. 7, the UW NCF DSCR is calculated using the sum of the first 12 whole loan principal and interest payments after the Cut-off Date based on the assumed principal and interest payment schedule set forth in Annex H of the Preliminary Prospectus. |

| (4) | In the case of Loan Nos. 3, 17 and 20, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 8 of 95 | |

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

| Collateral Characteristics |

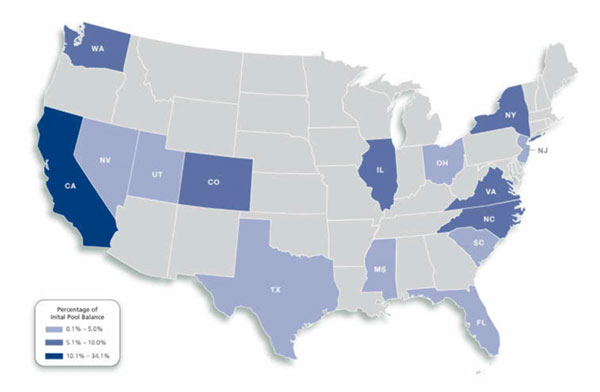

| Mortgaged Properties by Location(1) |

| |

| | | | | Weighted Average |

State | Number of

Properties | Cut-off Date

Principal

Balance | % of

IPB | Occupancy | UW

NCF DSCR(2)(3) | UW

NOI Debt

Yield(2) | Cut-off Date

LTV(2)(4) | Maturity Date LTV(2)(4) |

| California | 17 | 274,983,735 | 34.1% | 96.6% | 2.43x | 9.4% | 57.5% | 56.8% |

| Illinois | 44 | 68,550,000 | 8.5 | 95.4% | 1.86x | 8.5% | 60.9% | 60.9% |

| New York | 2 | 64,958,910 | 8.0 | 95.6% | 2.14x | 9.2% | 52.0% | 48.5% |

| North Carolina | 4 | 60,789,100 | 7.5 | 96.5% | 2.83x | 11.5% | 68.6% | 67.5% |

| Virginia | 24 | 60,258,551 | 7.5 | 93.9% | 1.96x | 10.9% | 64.9% | 57.5% |

| Colorado | 2 | 56,280,001 | 7.0 | 89.7% | 1.57x | 9.2% | 68.5% | 59.0% |

| Washington | 3 | 48,100,000 | 6.0 | 98.3% | 2.66x | 10.6% | 63.0% | 62.4% |

| New Jersey | 8 | 32,840,000 | 4.1 | 95.0% | 1.04x | 6.6% | 78.6% | 72.0% |

| Utah | 1 | 29,600,000 | 3.7 | 88.2% | 1.58x | 9.5% | 67.4% | 60.9% |

| South Carolina | 2 | 27,895,000 | 3.5 | 99.1% | 1.83x | 10.9% | 61.5% | 50.7% |

| Florida | 2 | 26,789,300 | 3.3 | 88.8% | 2.91x | 12.2% | 53.4% | 52.7% |

| Nevada | 1 | 20,000,000 | 2.5 | 94.0% | 2.46x | 9.6% | 46.3% | 46.3% |

| Texas | 5 | 18,400,000 | 2.3 | 100.0% | 1.61x | 9.1% | 63.8% | 61.4% |

| Ohio | 1 | 17,000,000 | 2.1 | 74.8% | 1.62x | 10.9% | 68.7% | 63.7% |

| Mississippi | 1 | 736,200 | 0.1 | 100.0% | 1.64x | 10.6% | 66.9% | 55.1% |

| Total / Weighted Average | 117 | $807,180,797 | 100.0% | 94.8% | 2.18x | 9.7% | 61.2% | 58.2% |

| (1) | Because this table represents information relating to the mortgaged properties and not mortgage loans, the information for the mortgage loans secured by more than one mortgaged property is based on allocated loan amounts. |

| (2) | In the case of Loan Nos. 1, 2, 3, 4, 5, 7, 9, 11, 14, 16, 17, 18, 20 and 26, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 1, 5, 7 and 16, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or related mezzanine loan(s). |

| (3) | With respect to Loan No. 7, the UW NCF DSCR is calculated using the sum of the first 12 whole loan principal and interest payments after the Cut-off Date based on the assumed principal and interest payment schedule set forth in Annex H of the Preliminary Prospectus. |

| (4) | In the case of Loan Nos. 3, 17 and 20, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 9 of 95 | |

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

| Collateral Characteristics |

| Cut-off Date Principal Balance |

| | | | | Weighted Average |

Range of Cut-off Date

Principal Balances | Number of

Loans | Cut-off Date

Principal

Balance | % of

IPB | Mortgage

Rate | Remaining

Loan Term | UW

NCF

DSCR(1)(2) | UW NOI

Debt

Yield(1) | Cut-off

Date

LTV(1)(3) | Maturity

Date

LTV(1)(3) |

| $3,395,000 | - | $9,999,999 | 9 | $65,398,256 | 8.1% | 4.28717% | 114 | 1.93x | 10.5% | 62.0% | 57.8% |

| $10,000,000 | - | $19,999,999 | 5 | 80,860,479 | 10.0 | 4.61616% | 93 | 1.84x | 10.0% | 64.7% | 62.4% |

| $20,000,000 | - | $24,999,999 | 5 | 109,308,910 | 13.5 | 3.87262% | 117 | 2.08x | 9.5% | 55.4% | 50.5% |

| $25,000,000 | - | $49,999,999 | 9 | 319,113,153 | 39.5 | 4.07770% | 117 | 1.99x | 9.5% | 65.0% | 60.7% |

| $50,000,000 | - | $62,500,000 | 4 | 232,500,000 | 28.8 | 3.46669% | 119 | 2.68x | 9.8% | 57.1% | 57.1% |

| Total / Weighted Average: | 32 | $807,180,797 | 100.0% | 3.94484% | 115 | 2.18x | 9.7% | 61.2% | 58.2% |

| | | | | Weighted Average |

Range of

Mortgage Interest Rates | Number

of Loans | Cut-off Date

Principal

Balance | % of

IPB | Mortgage

Rate | Remaining

Loan Term | UW

NCF

DSCR(1)(2) | UW NOI

Debt

Yield(1) | Cut-off

Date

LTV(1)(3) | Maturity

Date

LTV(1)(3) |

| 3.00450% | - | 3.99999% | 16 | $490,150,000 | 60.7% | 3.53174% | 119 | 2.56x | 9.8% | 58.3% | 57.8% |

| 4.00000% | - | 4.49999% | 7 | 129,434,390 | 16.0 | 4.14426% | 109 | 1.70x | 10.1% | 63.6% | 53.9% |

| 4.50000% | - | 4.99999% | 6 | 111,643,256 | 13.8 | 4.58227% | 115 | 1.53x | 8.3% | 66.2% | 62.9% |

| 5.00000% | - | 5.39000% | 3 | 75,953,151 | 9.4 | 5.33398% | 100 | 1.51x | 10.4% | 68.4% | 61.5% |

| Total / Weighted Average: | 32 | $807,180,797 | 100.0% | 3.94484% | 115 | 2.18x | 9.7% | 61.2% | 58.2% |

| | | | | | | | | | | | |

| Original Term to Maturity in Months |

| | | | | Weighted Average |

Original Term to

Maturity in Months | Number of

Loans | Cut-off Date Principal

Balance | % of

IPB | Mortgage

Rate | Remaining

Loan Term | UW

NCF

DSCR(1)(2) | UW NOI

Debt

Yield(1) | Cut-off

Date LTV(1)(3) | Maturity

Date LTV(1)(3) |

| 60 | 3 | $35,375,479 | 4.4% | 4.71509% | 59 | 1.68x | 10.7% | 70.2% | 65.0% |

| 120 | 29 | 771,805,319 | 95.6 | 3.90954% | 117 | 2.20x | 9.7% | 60.7% | 57.9% |

| Total / Weighted Average: | 32 | $807,180,797 | 100.0% | 3.94484% | 115 | 2.18x | 9.7% | 61.2% | 58.2% |

| Remaining Term to Maturity in Months |

| | | | | Weighted Average |

Range of Remaining Term

to Maturity in Months | Number of

Loans | Cut-off Date

Principal

Balance | % of

IPB | Mortgage

Rate | Remaining

Loan Term | UW

NCF

DSCR(1)(2) | UW NOI

Debt

Yield(1) | Cut-off

Date LTV(1)(3) | Maturity

Date LTV(1)(3) |

| 59 | - | 84 | 3 | $35,375,479 | 4.4% | 4.71509% | 59 | 1.68x | 10.7% | 70.2% | 65.0% |

| 85 | - | 119 | 21 | 554,415,319 | 68.7 | 4.01454% | 116 | 1.96x | 8.9% | 61.8% | 58.9% |

| 120 | 8 | 217,390,000 | 26.9 | 3.64175% | 120 | 2.82x | 11.5% | 58.0% | 55.5% |

| Total / Weighted Average: | 32 | $807,180,797 | 100.0% | 3.94484% | 115 | 2.18x | 9.7% | 61.2% | 58.2% |

| | | | | | | | | | | | |

| (1) | In the case of Loan Nos. 1, 2, 3, 4, 5, 7, 9, 11, 14, 16, 17, 18, 20 and 26, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 1, 5, 7 and 16, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or related mezzanine loan(s). |

| (2) | With respect to Loan No. 7, the UW NCF DSCR is calculated using the sum of the first 12 whole loan principal and interest payments after the Cut-off Date based on the assumed principal and interest payment schedule set forth in Annex H of the Preliminary Prospectus. |

| (3) | In the case of Loan Nos. 3, 17 and 20, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 10 of 95 | |

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

| Collateral Characteristics |

| Original Amortization Term in Months |

| | | | | Weighted Average |

Original

Amortization

Term in Months | Number

of Loans | Cut-off Date

Principal

Balance | % of

IPB | Mortgage

Rate | Remaining

Loan Term | UW

NCF

DSCR(1)(2) | UW NOI

Debt

Yield(1) | Cut-off

Date

LTV(1)(3) | Maturity

Date

LTV(1)(3) |

| Interest Only | 20 | $555,425,000 | 68.8% | 3.71279% | 117 | 2.48x | 9.6% | 58.7% | 58.7% |

| 300 | 1 | 4,000,000 | 0.5 | 3.80000% | 120 | 3.99x | 27.8% | 22.5% | 16.1% |

| 360 | 11 | 247,755,797 | 30.7 | 4.46742% | 109 | 1.47x | 9.6% | 67.2% | 57.8% |

| Total / Weighted Average: | 32 | $807,180,797 | 100.0% | 3.94484% | 115 | 2.18x | 9.7% | 61.2% | 58.2% |

| Remaining Amortization Term in Months |

| | | | | Weighted Average |

Range of Remaining

Amortization Term in Months | Number

of Loans | Cut-off Date

Principal

Balance | % of

IPB | Mortgage Rate | Remaining

Loan Term | UW

NCF

DSCR(1)(2) | UW NOI

Debt

Yield(1) | Cut-off

Date

LTV(1)(3) | Maturity

Date

LTV(1)(3) |

| Interest Only | 20 | $555,425,000 | 68.8% | 3.71279% | 117 | 2.48x | 9.6% | 58.7% | 58.7% |

| 300 | - | 359 | 6 | 130,015,797 | 16.1 | 4.54182% | 109 | 1.55x | 10.5% | 64.7% | 53.8% |

| 360 | 6 | 121,740,000 | 15.1 | 4.36602% | 111 | 1.47x | 9.3% | 68.5% | 60.8% |

| Total / Weighted Average: | 32 | $807,180,797 | 100.0% | 3.94484% | 115 | 2.18x | 9.7% | 61.2% | 58.2% |

| | | | | | | | | | | | |

| | | | | Weighted Average |

| Amortization Types | Number

of Loans | Cut-off Date

Principal

Balance | % of

IPB | Mortgage

Rate | Remaining

Loan Term | UW

NCF

DSCR(1)(2) | UW NOI

Debt

Yield(1) | Cut-off

Date

LTV(1)(3) | Maturity

Date

LTV(1)(3) |

| Interest Only | 20 | $555,425,000 | 68.8% | 3.71279% | 117 | 2.48x | 9.6% | 58.7% | 58.7% |

| Balloon | 8 | 171,515,797 | 21.2 | 4.55167% | 105 | 1.58x | 10.6% | 64.5% | 54.0% |

| IO-Balloon | 4 | 80,240,000 | 9.9 | 4.25405% | 118 | 1.36x | 8.5% | 70.9% | 64.0% |

| Total / Weighted Average: | 32 | $807,180,797 | 100.0% | 3.94484% | 115 | 2.18x | 9.7% | 61.2% | 58.2% |

| Underwritten Net Cash Flow Debt Service Coverage Ratios(1)(2) |

| | | | | Weighted Average |

Range of Underwritten Net

Cash Flow Debt Service

Coverage Ratios | Number

of Loans | Cut-off Date

Principal

Balance | % of

IPB | Mortgage

Rate | Remaining

Loan Term | UW

NCF

DSCR(1)(2) | UW NOI

Debt

Yield(1) | Cut-off

Date

LTV(1)(3) | Maturity

Date

LTV(1)(3) |

| 1.04x | - | 1.49x | 3 | $97,372,061 | 12.1% | 4.83881% | 116 | 1.29x | 8.9% | 67.9% | 58.9% |

| 1.50x | - | 1.74x | 10 | 178,813,736 | 22.2 | 4.37276% | 106 | 1.60x | 9.8% | 66.4% | 58.3% |

| 1.75x | - | 1.99x | 7 | 207,750,000 | 25.7 | 3.92996% | 117 | 1.82x | 7.5% | 62.1% | 62.1% |

| 2.00x | - | 2.24x | 1 | 9,100,000 | 1.1 | 3.90000% | 120 | 2.17x | 8.6% | 68.7% | 68.7% |

| 2.25x | - | 4.09x | 11 | 314,145,000 | 38.9 | 3.43532% | 118 | 3.03x | 11.4% | 55.3% | 55.2% |

| Total / Weighted Average: | 32 | $807,180,797 | 100.0% | 3.94484% | 115 | 2.18x | 9.7% | 61.2% | 58.2% |

| (1) | In the case of Loan Nos. 1, 2, 3, 4, 5, 7, 9, 11, 14, 16, 17, 18, 20 and 26, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 1, 5, 7 and 16, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or related mezzanine loan(s). |

| (2) | With respect to Loan No. 7, the UW NCF DSCR is calculated using the sum of the first 12 whole loan principal and interest payments after the Cut-off Date based on the assumed principal and interest payment schedule set forth in Annex H of the Preliminary Prospectus. |

| (3) | In the case of Loan Nos. 3, 17 and 20, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 11 of 95 | |

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

| Collateral Characteristics |

| LTV Ratios as of the Cut-off Date(1)(3) |

| | | | | Weighted Average |

Range of

Cut-off Date LTVs | Number

of Loans | Cut-off Date

Principal

Balance | % of

IPB | Mortgage

Rate | Remaining

Loan Term | UW

NCF

DSCR(1)(2) | UW NOI

Debt

Yield(1) | Cut-off

Date

LTV(1)(3) | Maturity

Date

LTV(1)(3) |

| 22.5% | - | 39.9% | 2 | $66,500,000 | 8.2% | 3.05235% | 120 | 4.08x | 14.4% | 38.1% | 37.7% |

| 40.0% | - | 49.9% | 2 | 44,808,910 | 5.6 | 4.10024% | 115 | 1.89x | 9.3% | 47.4% | 42.4% |

| 50.0% | - | 59.9% | 7 | 171,603,256 | 21.3 | 3.78747% | 119 | 2.29x | 9.4% | 56.1% | 55.3% |

| 60.0% | - | 69.9% | 16 | 379,675,000 | 47.0 | 3.94604% | 114 | 2.11x | 9.4% | 64.6% | 62.8% |

| 70.0% | - | 78.6% | 5 | 144,593,631 | 17.9 | 4.49078% | 111 | 1.44x | 8.9% | 73.0% | 64.2% |

| Total / Weighted Average: | 32 | $807,180,797 | 100.0% | 3.94484% | 115 | 2.18x | 9.7% | 61.2% | 58.2% |

| LTV Ratios as of the Maturity Date(1)(3) |

| | | | | Weighted Average |

Range of

Maturity Date LTVs | Number

of Loans | Cut-off Date

Principal

Balance | % of

IPB | Mortgage

Rate | Remaining

Loan Term | UW

NCF

DSCR(1)(2) | UW NOI

Debt

Yield(1) | Cut-off

Date

LTV(1)(3) | Maturity

Date

LTV(1)(3) |

| 16.1% | - | 39.9% | 3 | $91,308,910 | 11.3% | 3.41579% | 118 | 3.36x | 12.9% | 40.9% | 38.1% |

| 40.0% | - | 49.9% | 3 | 53,953,256 | 6.7 | 4.01423% | 118 | 1.97x | 10.3% | 54.7% | 47.3% |

| 50.0% | - | 54.9% | 4 | 94,600,000 | 11.7 | 3.62164% | 119 | 2.69x | 10.6% | 53.8% | 53.3% |

| 55.0% | - | 59.9% | 4 | 113,200,001 | 14.0 | 4.00018% | 118 | 1.72x | 8.4% | 63.9% | 58.4% |

| 60.0% | - | 72.0% | 18 | 454,118,630 | 56.3 | 4.09651% | 112 | 1.98x | 9.1% | 66.8% | 64.6% |

| Total / Weighted Average: | 32 | $807,180,797 | 100.0% | 3.94484% | 115 | 2.18x | 9.7% | 61.2% | 58.2% |

| | | | | Weighted Average |

| Prepayment Protection | Number

of Loans | Cut-off Date

Principal

Balance | % of

IPB | Mortgage

Rate | Remaining

Loan Term | UW

NCF

DSCR(1)(2) | UW NOI

Debt

Yield(1) | Cut-off

Date

LTV(1)(3) | Maturity

Date

LTV(1)(3) |

| Defeasance | 26 | $570,577,646 | 70.7% | 3.99512% | 114 | 1.91x | 9.0% | 62.9% | 59.5% |

| Yield Maintenance | 5 | 174,103,151 | 21.6 | 4.11763% | 117 | 2.38x | 10.6% | 63.4% | 60.8% |

| YM, then Defeasance or YM | 1 | 62,500,000 | 7.7 | 3.00450% | 120 | 4.09x | 13.5% | 39.1% | 39.1% |

| Total / Weighted Average: | 32 | $807,180,797 | 100.0% | 3.94484% | 115 | 2.18x | 9.7% | 61.2% | 58.2% |

| | | | | | | | | | |

| | | | | Weighted Average |

| Loan Purpose | Number

of Loans | Cut-off Date

Principal

Balance | % of

IPB | Mortgage

Rate | Remaining

Loan Term | UW

NCF

DSCR(1)(2) | UW NOI

Debt

Yield(1) | Cut-off

Date

LTV(1)(3) | Maturity

Date

LTV(1)(3) |

| Refinance | 19 | $507,482,167 | 62.9% | 3.98604% | 115 | 2.07x | 9.4% | 59.2% | 55.7% |

| Acquisition | 12 | 279,698,630 | 34.7 | 3.91406% | 114 | 2.31x | 10.1% | 65.4% | 63.3% |

| Recapitalization | 1 | 20,000,000 | 2.5 | 3.33000% | 119 | 3.07x | 11.0% | 52.1% | 52.1% |

| Total / Weighted Average: | 32 | $807,180,797 | 100.0% | 3.94484% | 115 | 2.18x | 9.7% | 61.2% | 58.2% |

| (1) | In the case of Loan Nos. 1, 2, 3, 4, 5, 7, 9, 11, 14, 16, 17, 18, 20 and 26, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 1, 5, 7 and 16, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date LTV calculations exclude the related Subordinate Companion Loan(s) and/or related mezzanine loan(s). |

| (2) | With respect to Loan No. 7, the UW NCF DSCR is calculated using the sum of the first 12 whole loan principal and interest payments after the Cut-off Date based on the assumed principal and interest payment schedule set forth in Annex H of the Preliminary Prospectus. |

| (3) | In the case of Loan Nos. 3, 17 and 20, the Cut-off Date LTV and the Maturity Date LTV are calculated by using an appraised value based on certain hypothetical assumptions. Refer to “Description of the Mortgage Pool—Assessments of Property Value and Condition” and “—Appraised Value” in the Preliminary Prospectus for additional details. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 12 of 95 | |

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

| Collateral Characteristics |

| Previous Securitization History(1) |

| No. | Property Name | Cut-off Date Principal

Balance | % of IPB | Location | Property

Type | Previous

Securitization |

| 1 | Century Plaza Towers | $62,500,000 | 7.7% | Los Angeles, CA | Office | MSC 2014-CPT |

| 10 | Jersey City Group 2 | $32,840,000 | 4.1% | Jersey City, NJ | Multifamily | TRTX 2018-FL1 |

| 12 | Union Heights | $29,600,000 | 3.7% | Sandy, UT | Office | GSMS 2012-GCJ7 |

| 31 | Opus Seaway | $4,000,000 | 0.5% | Everett, WA | Industrial | COMM 2015-PC1 |

| (1) | The table above represents the properties for which the previously existing debt was securitized, based on information provided by the related borrower or obtained through searches of a third-party database. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 13 of 95 | |

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

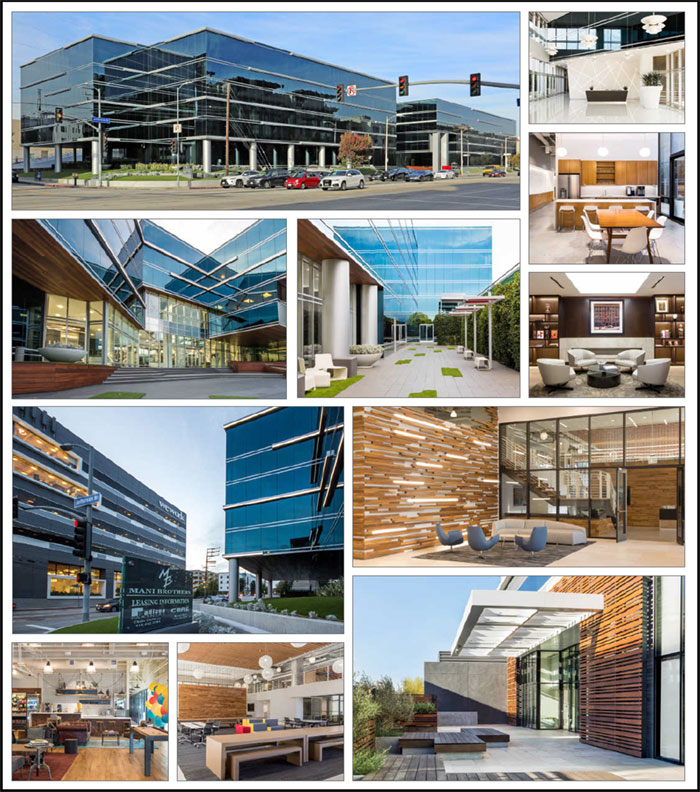

| Century Plaza Towers |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 14 of 95 | |

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

| Century Plaza Towers |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 15 of 95 | |

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

| Century Plaza Towers |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 16 of 95 | |

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

| Century Plaza Towers |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 17 of 95 | |

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

| Century Plaza Towers |

| Mortgage Loan Information | | Property Information |

| Mortgage Loan Seller: | GACC | | Single Asset / Portfolio: | Single Asset |

| Original Principal Balance(1): | $62,500,000 | | Title: | Fee |

| Cut-off Date Principal Balance(1): | $62,500,000 | | Property Type - Subtype: | Office – CBD |

| % of Pool by IPB: | 7.7% | | Net Rentable Area (SF): | 2,401,641 |

| Loan Purpose: | Refinance | | Location: | Los Angeles, CA |

| Borrower: | One Hundred Towers L.L.C. | | Year Built / Renovated: | 1975 / 2015 |

| Sponsors(2): | SPF JVP LLC; Luminance | | Occupancy: | 92.9% |

| | Acquisition Venture LLC | | Occupancy Date: | 10/1/2019 |

| Interest Rate: | 3.00450% | | Number of Tenants: | 122 |

| Note Date: | 10/21/2019 | | 2016 NOI: | $80,783,345 |

| Maturity Date: | 11/9/2029 | | 2017 NOI: | $83,200,132 |

| Interest-only Period: | 120 months | | 2018 NOI: | $89,024,555 |

| Original Term: | 120 months | | TTM NOI (as of 9/2019)(5): | $83,342,918 |

| Original Amortization: | None | | UW Economic Occupancy: | 94.8% |

| Amortization Type: | Interest Only | | UW Revenues: | $158,615,968 |

| Call Protection(3): | Grtr1%orYM(24),Def or | | UW Expenses: | $37,470,212 |

| | Grtr1%orYM(91),O(5) | | UW NOI(5): | $121,145,756 |

| Lockbox / Cash Management: | Hard / Springing | | UW NCF: | $112,250,366 |

| Additional Debt(1): | Yes | | Appraised Value / Per SF: | $2,302,000,000 / $959 |

| Additional Debt Balance(1)(4): | $837,500,000 / $300,000,000 | | Appraisal Date: | 9/24/2019 |

| Additional Debt Type(1)(4): | Pari Passu /Subordinate Debt | | | |

| | | | |

| Escrows and Reserves(6) | | Financial Information(1)(1) |

| | Initial | Monthly | Initial Cap | | | Senior | Whole Loan | |

| Taxes: | $0 | Springing | N/A | | Cut-off Date Loan / SF: | $375 | $500 | |

| Insurance: | $0 | Springing | N/A | | Maturity Date Loan / SF: | $375 | $500 | |

| Replacement Reserves: | $0 | $0 | N/A | | Cut-off Date LTV: | 39.1% | 52.1% | |

| TI/LC: | $0 | $0 | N/A | | Maturity Date LTV: | 39.1% | 52.1% | |

| Other: | $100,769,680 | $0 | N/A | | UW NCF DSCR: | 4.09x | 3.07x | |

| | | | | | UW NOI Debt Yield: | 13.5% | 10.1% | |

| | | | | | | | |

| Sources and Uses |

| Sources | Proceeds | % of Total | | Uses | Proceeds | % of Total |

| Whole Loan | $1,200,000,000 | 100.0% | | Refinance Existing Debt | $823,449,563 | 68.6% |

| | | | | Upfront Reserves | 100,769,680 | 8.4 |

| | | | | Closing Costs | 2,834,724 | 0.2 |

| | | | | Return of Equity | 272,946,032 | 22.7 |

| Total Sources | $1,200,000,000 | 100.0% | | Total Uses | $1,200,000,000 | 100.0% |

| (1) | The Century Plaza Towers Loan (as defined below) consists of the non-controlling Notes A-1-C3 and A-1-C8, which is part of the Century Plaza Towers Whole Loan (as defined below) evidenced by 29 senior pari passu notes and three subordinate notes, with an aggregate outstanding principal balance as of the Cut-off Date of $1.2 billion. For additional information, see “The Loan” herein. |

| (2) | There is no non-recourse carveout guarantor or separate environmental indemnitor with respect to the Century Plaza Towers Whole Loan. |

| (3) | The lockout period, with respect to a defeasance of the Century Plaza Towers Whole Loan, will be at least 24 payment dates beginning with and including the first payment date of December 9, 2019. Defeasance of the full $1.2 billion Century Plaza Towers Whole Loan is permitted after the date that is the earlier of (i) two years from the closing date of the securitization that includes the lastpari passu note to be securitized and (ii) three years from October 21, 2019. Prepayment in whole, but not in part, of the Century Plaza Towers Whole Loan is permitted with the payment of yield maintenance prior to July 9, 2029 at any time. |

| (4) | See “Current Mezzanine or Subordinate Indebtedness” and “Future Mezzanine or Subordinate Indebtedness Permitted” below. |

| (5) | The increase in UW Net Operating Income from TTM TO Underwritten Net Operating Income is primarily attributable to (i) $2,354,778 in straight line rent taken through the earlier of the loan term or the lease term for thirteen tenants, (ii) $3,269,254 of rent steps taken through October 2020 and (iii) new leasing that has been executed since September 2019, accounting for 20.6% of NRA and 24.6% of UW Gross Potential Rent. |

| (6) | For a full description of Escrows and Reserves, please refer to “Escrows and Reserves” below. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 18 of 95 | |

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

| Century Plaza Towers |

The Loan.The Century Plaza Towers mortgage loan (the “Century Plaza Towers Loan”) is part of a whole loan with an aggregate outstanding principal balance as of the Cut-off Date of $1.2 billion (the “Century Plaza Towers Whole Loan”), secured by the borrower’s fee interest in a 2,401,641 square foot, Class A, office property located in the Century City submarket of Los Angeles, California (the “Century Plaza Towers Property”). The Century Plaza Towers Whole Loan is comprised of (i) a senior loan, comprised of 29pari passunotes with an aggregate principal balance as of the Cut-off Date of $900.0 million (the “Century Plaza Towers Senior Notes”), two of which (Notes A-1-C3 and A-1-C8 with an outstanding principal balance as of the Cut-off Date of $62.5 million) are being contributed to the JPMDB 2019-COR6 Trust and constitute the Century Plaza Towers Loan, and the remainder of which are expected to be contributed to one or more future securitization trusts and (ii) a subordinate loan, comprised of three notes, with an outstanding principal balance as of the Cut-off Date of $300.0 million (the “Century Plaza Towers Subordinate Companion Loan”), each as described below. The relationship between the holders of the Century Plaza Towers Senior Notes and Century Plaza Towers Subordinate Companion Loan will be governed by a co-lender agreement as described under“Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans—The Century Plaza Towers Whole Loan”in the Preliminary Prospectus. The Century Plaza Towers Whole Loan was co-originated by Deutsche Bank AG acting through its New York Branch (which subsequently transferred its notes to DBR Investments Co. Limited (“DBRI”)), Wells Fargo Bank, National Association (“WFBNA”), and Morgan Stanley Bank, N.A (“MSBNA”). The Century Plaza Towers Whole Loan has a 10-year term and is interest only for the length of the loan term.

| Whole Loan Summary |

| Note | Original Balance | Cut-off Date Balance | Note Holder | Controlling Piece |

| A-1-C3, A-1-C8 | $62,500,000 | $62,500,000 | JPMDB 2019-COR6 | No |

| A-1-S1, A-1-S2, A-1-S3, A-2-S1, A-2-S2, A-2-S3, A-2-C1, A-2-C3, A-2-C4 A-3-S1,A-3-S2, A-3-S3, A-3-C1, A-3-C3 | $525,000,000 | $525,000,000 | CPTS 2019-CPT | No |

| A-1-C1, A-1-C2, A-1-C4,A-1-C5, A-1-C6, A-1-C7 | $187,500,000 | $187,500,000 | DBRI | No |

| A-2-C2, A-2-C5, A-2-C6, A-2-C7 | $62,500,000 | $62,500,000 | MSBNA | No |

| A-3-C2, A-3-C4,A-3-C5 | $62,500,000 | $62,500,000 | WFBNA | No |

| Senior Notes | $900,000,000 | $900,000,000 | | |

| B-1, B-2, B-3 | 300,000,000 | 300,000,000 | CPTS 2019-CPT | Yes |

| Total | $1,200,000,000 | $1,200,000,000 | | |

The Borrower. The borrowing entity for the Century Plaza Towers Whole Loan is One Hundred Towers L.L.C., a special purpose entity, structured to be bankruptcy remote with two independent directors in its organizational structure.

The Loan Sponsors.The loan sponsor is a joint venture between (i) the Commingled Pension Trust Fund (Strategic Property) of JPMorgan Chase Bank, N.A. (“SPF”) and (ii) a joint venture between an institutional account managed by both Hines and Hines Investment Management Holdings Limited Partnership (the “Hines JV”) (together with SPF, the “Borrower Sponsor” or “JV”).As of June 30, 2019, SPF had a net asset value of $32.7 billion and a gross asset value of $42.7 billion. Hines JV is a privately owned global real estate investment, development and management firm, founded in 1957, with a presence in 219 cities in 23 countries and $124.3 billion of assets under management—including $63.8 billion for which Hines provides fiduciary investment management services and $60.5 billion for which Hines provides third party property-level services. There is no nonrecourse carveout guarantor or separate environmental indemnitor for the Century Plaza Towers Whole Loan.

The Property. The Century Plaza Towers Property consists of two Class A, 44-story, trophy, office towers and contains 2,401,641 square feet of office space and a lower level retail concourse. In addition, the Century Plaza Towers Property has an underground garage containing a total of 6,566 parking spaces (of which 5,907 spaces are part of the collateral for the Century Plaza Towers Whole Loan). The Century Plaza Towers Property was originally developed in 1975 for Aluminum Company of America (“Alcoa”) and was designed by Minoru Yamasaki.

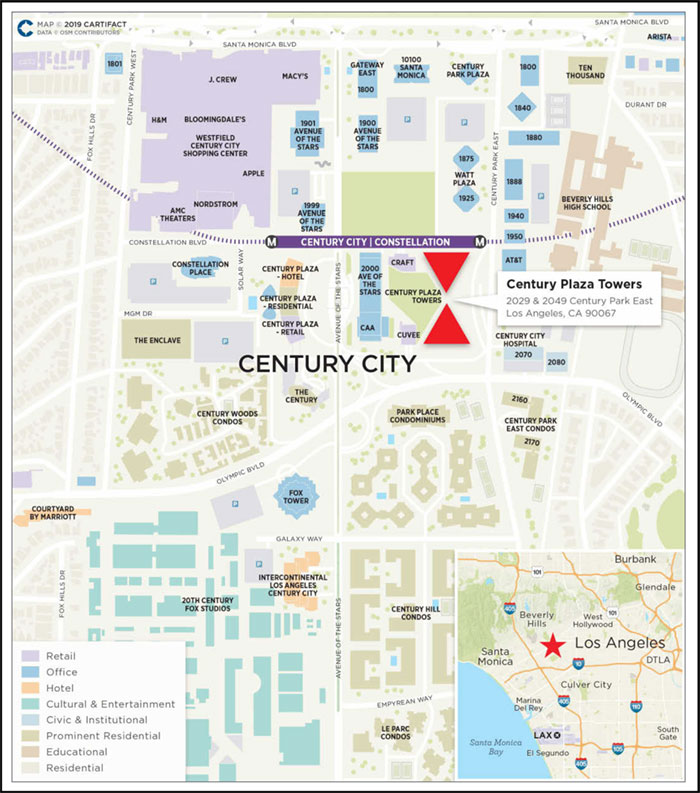

The Century Plaza Towers Property includes 26,000 square feet column-free flexible floor plates. The Century Plaza Towers Property underwent an $80.0 million renovation in 2008 and has had approximately $48.0 million of capital expenditures invested since 2014, including a multi-year program currently underway to fully renovate all restrooms, multi-tenant corridors, and elevator lobbies; nearly $28.0 million has been invested since 2015. Together with the property located at 2000 Avenue of the Stars (which is also owned by the loan sponsor), the Century Plaza Towers Property is part of Century Park, a 14-acre campus that includes a four-acre central park, restaurants, cafes, and other amenity retail.

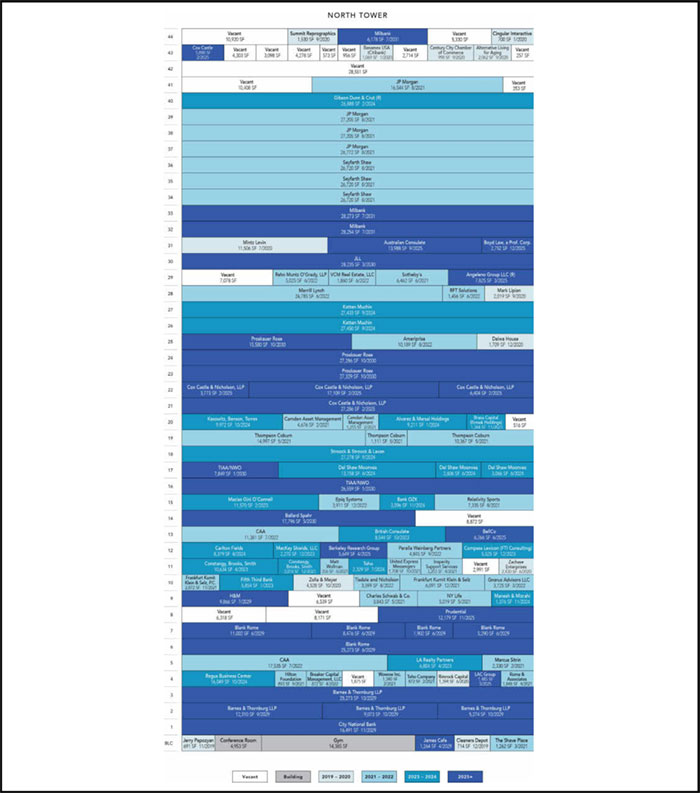

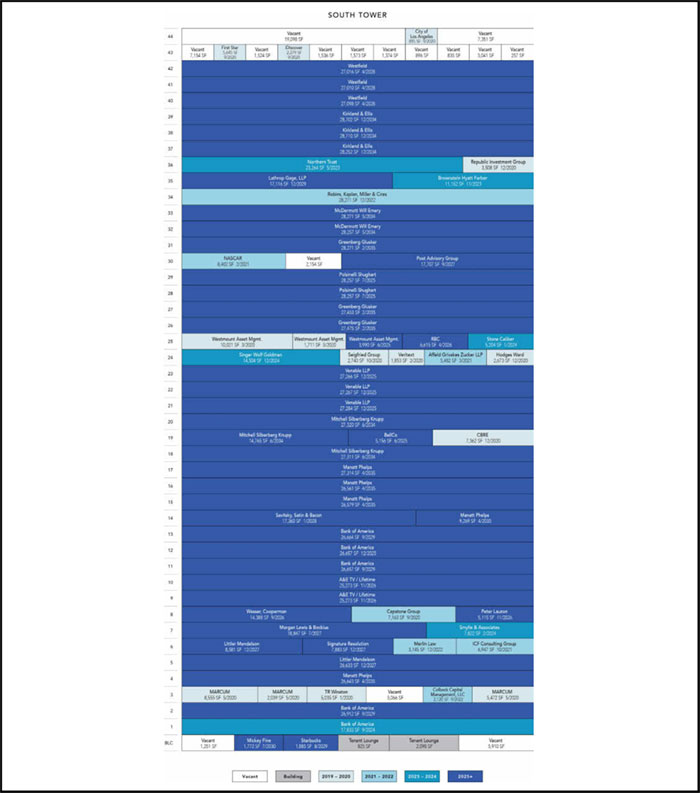

The Property is 92.9% leased as of October 1, 2019 to 122 distinct tenants across approximately 1.2 million square feet of office space in the North Tower, approximately 1.2 million square feet of office space in the South Tower and approximately 39,500 square feet of ground floor retail space. The largest tenants include Bank of America (6.2% of NRA / 6.5% of GPR / $56.98 Gross PSF / rated A2/A+/A- by Moody’s, Fitch and S&P), Manatt Phelps (4.8% of NRA / 5.5% of GPR / $62.26 Gross PSF / #105 in a magazine ranking of large law firms based on gross revenue), JPMorgan (4.1% of NRA / 4.2% of GPR / $57.00 Gross PSF / rated A2/AA-/A- by Moody’s, Fitch and S&P), Kirkland & Ellis (3.6% of NRA / 4.5% of GPR / $68.79 Gross PSF / #1 in a magazine ranking of large law firms based on gross revenue) and Greenberg Glusker (3.5% of NRA / 4.2% of GPR / $66.00 Gross PSF).

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 19 of 95 | |

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

| Century Plaza Towers |

The largest tenant, Bank of America (149,508 square feet; 6.2% of net rentable area; 6.5% of Underwritten Base Rent) is an investment and retail banking institution and financial services company based in Charlotte, North Carolina. It is the second largest banking institution in the United States by total assets. The institution’s corporate and investment banking division operates under the name Bank of America Merrill Lynch. Bank of America occupies four suites in the south tower on the 1st, 2nd, 11th and 12th floors totaling 98,059 square feet. Bank of America has signed a lease for an additional 26,664 square feet on the 13th floor of the South Tower and is expected to begin paying rent and take occupancy in January 2020. Merrill Lynch occupies one suite in the North Tower totaling 24,785 square feet. The firm pays approximately $54 to $61 of gross rent per square foot across the North and South Towers. Bank of America has been at the Century Plaza Towers Property since 1994. With respect to the additional space in the South Tower, we cannot assure you that Bank of America will begin paying rent or take occupancy as expected or at all.

The second largest tenant, Manatt Phelps (116,366 square feet; 4.8% of net rentable area; 5.5% of Underwritten Base Rent) is a Los Angeles-based law firm that has practices focused on banking, entertainment, media, technology, retail and consumer products, and real estate and energy. Founded in 1965, Manatt Phelps employs over 450 attorneys across Los Angeles, New York, Palo Alto, San Francisco, Orange County, Chicago, Washington, D.C. and Boston. The firm is ranked #105 in the 2019 Am Law rankings. Manatt Phelps has signed a lease for five suites in the South Tower on the 4th, 14th, 15th, 16th and 17th floors totaling 116,366 square feet and is expected to begin paying rent and take occupancy in stages starting in March 2020, with full occupancy of the space expected by May 2020. Manatt Phelps’s contractual rent under its lease is $62 gross rent per square foot. We cannot assure you that Manatt Phelps will begin paying rent or take occupancy as expected or at all.

The third largest tenant, JPMorgan (97,726 square feet; 4.1% of net rentable area; 4.2% of GPR) was founded in 1871, JPMorgan (NYSE: JPM) is a commercial, investment and retail banking institution founded by J.P. Morgan. Headquartered in New York City, JPMorgan is the largest bank in the United States. JPMorgan is affiliated with the borrower. JPMorgan occupies four suites in the North Tower on the 37th, 38th, 39th and 41st floors totaling 97,726 square feet and pays $57 gross rent per square foot. JPMorgan has been at the Century Plaza Towers Property since 2011.

The Century Plaza Towers Property is located in the Century City submarket of West Los Angeles, California. Situated between Beverly Hills to the east, Westwood, Brentwood, and Santa Monica to the west, and the residential neighborhoods of Bel Air, Holmby Hills, and Hollywood Hills to the north, Century City is located near the Westside’s amenities and housing communities. The Century Plaza Towers Property has access to the Santa Monica (I-10) and San Diego (I-405) Freeways and several additional major east-west thoroughfares including Santa Monica Boulevard and Olympic Boulevard.

Prior to the economic downturn in 2007-2008, vacancy rates in the Century City submarket declined to single digits, and reached an historical low direct vacancy rate of 7.1% in 2006. As the economic downturn affected the area, vacancy rates began to increase to 14.4% in 2010. As of year-end 2017, direct vacancy in the Century City submarket declined slightly to 8.2%, representing a 3.6% decrease since 2015. As of the second quarter in 2019, the direct vacancy rate was 6.1%, 80 basis points lower than year-end 2018 (6.9%).

The appraisal identified six directly competitive office sales comparables in the Los Angeles market. Comparable buildings were built between 1925 and 2017 and range in size from 201,922 square feet to 1,006,645 square feet. The weighted average occupancy of the sales comparables was 82.8% and the weighted average sales price per square foot was approximately $830.23. Through the first half of 2019, asking rates increased slightly by 1.1% to $52.72 per square foot.

| Historical and Current Occupancy |

| 2016(1) | 2017(1) | 2018(1) | Current(2) |

| 87.0% | 84.6% | 83.5% | 92.9% |

| (1) | Historical occupancy is as of December 31. |

| (2) | Current Occupancy is as of October 1, 2019. This is inclusive of tenants that have signed a lease but are not in physical occupancy yet. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 20 of 95 | |

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

| Century Plaza Towers |

| Tenant Summary(1) |

| Tenant | Ratings

Moody’s/Fitch/S&P(2) | Net Rentable Area

(SF) | % of

Total NRA | Base Rent

PSF(3) | % of Total

Base Rent | Lease

Expiration Date |

| Bank of America(2)(3) | A2 / A+ / A- | 149,508 | | 6.2% | $56.98 | 6.5% | Various(3) |

| Manatt Phelps(4) | NR / NR / NR | 116,366 | | 4.8 | $62.26 | 5.5 | 4/30/2035 |

| JPMorgan | A2 / AA- / A- | 97,726 | | 4.1 | $57.00 | 4.2 | 8/31/2021 |

| Kirkland & Ellis(5) | NR / NR / NR | 85,664 | | 3.6 | $68.79 | 4.5 | 12/31/2034 |

| Greenberg Glusker(6 | NR / NR / NR | 83,199 | | 3.5 | $66.00 | 4.2 | 2/28/2035 |

| Venable LLP | NR / NR / NR | 81,817 | | 3.4 | $57.70 | 3.6 | 12/31/2025 |

| Westfield(7) | NR / NR / A | 81,124 | | 3.4 | $52.30 | 3.2 | 4/30/2028 |

| Seyfarth Shaw | NR / NR / NR | 80,160 | | 3.3 | $78.51 | 4.8 | 8/31/2021 |

| Proskauer Rose(8) | NR / NR / NR | 70,195 | | 2.9 | $57.26 | 3.1 | 10/31/2030 |

| Mitchell Silberberg Knupp(9) | NR / NR / NR | 69,396 | | 2.9 | $56.40 | 3.0 | 6/30/2034 |

| Ten Largest Tenants | | 915,155 | | 38.1% | $61.09 | 42.6% | |

| Remaining Tenants | | 1,315,465 | | 54.8 | $57.21 | 57.4% | |

| Vacant | | 171,021 | | 7.1 | | | |

| Total | | 2,401,641 | | 100.0% | | | |

| (1) | Based on the October 1, 2019 rent roll. |

| (2) | The square feet of Bank of America includes 124,723 square feet occupied by Bank or America on floors 1 through 14 and 24,785 square feet occupied by Merrill Lynch on floors 25 through 33. In addition, the square feet for Bank of America includes 26,664 square feet, as to which Bank of America is expected to begin paying rent and take occupancy in January 2020. |

| (3) | Bank of America has various lease expiration dates: (i) 106,890 square feet with a lease expiration date of September 30, 2029, (ii) 17,833 square feet with a lease expiration date of September 30, 2024 and (iii) 24,785 square feet related to the Merrill Lynch space, with a lease expiration date of June 30, 2022. |

| (4) | Manatt Phelps is expected to begin paying rent and take occupancy in stages in March 2020, with full occupancy of the space expected in May 2020. |

| (5) | Kirkland & Ellis is expected to begin paying rent and take occupancy in January 2020. |

| (6) | Greenberg Glusker shall have the one-time right to terminate its lease as of March 1, 2032 upon written notice on or before March 1, 2031 and the payment of a termination fee. |

| (7) | Westfield has a one-time right to terminate its lease on April 30, 2025, with 15 months’ prior notice and the payment of a termination fee of approximately $3.5 million. |

| (8) | Proskauer Rose has a one-time right to terminate its lease on October 31, 2025, upon written notice on or before October 31, 2024 and the payment of a termination fee. |

| (9) | Mitchell Silberberg Knupp has a one-time right to terminate its lease on June 30, 2029, upon written notice on or before June 30, 2028 and the payment of a termination fee. |

| Lease Rollover Schedule(1)(2) |

| Year | Number of Leases Expiring | Net Rentable Area Expiring | % of NRA Expiring | Base Rent Expiring | % of Base Rent Expiring | Cumulative Net Rentable Area Expiring | Cumulative % of NRA Expiring | Cumulative

Base Rent

Expiring | Cumulative

% of Base

Rent

Expiring |

| Vacant | NAP | 171,021 | 7.1% | NAP | NAP | 171,021 | 7.1% | NAP | NAP |

| MTM & 2019 | 2 | 1,405 | 0.1% | $45,653 | 0.0% | 172,426 | 7.2% | $45,653 | 0.0% |

| 2020 | 26 | 96,896 | 4.0% | $4,857,092 | 3.7% | 269,322 | 11.2% | $4,902,745 | 3.7% |

| 2021 | 30 | 276,557 | 11.5% | $17,553,318 | 13.4% | 545,879 | 22.7% | $22,456,063 | 17.1% |

| 2022 | 15 | 122,719 | 5.1% | $7,206,505 | 5.5% | 668,598 | 27.8% | $29,662,568 | 22.6% |

| 2023 | 14 | 89,979 | 3.7% | $5,073,213 | 3.9% | 758,577 | 31.6% | $34,735,781 | 26.5% |

| 2024 | 18 | 224,254 | 9.3% | $13,455,101 | 10.3% | 982,831 | 40.9% | $48,190,882 | 36.7% |

| 2025 | 19 | 258,081 | 10.7% | $14,826,378 | 11.3% | 1,240,912 | 51.7% | $63,017,260 | 48.0% |

| 2026 | 5 | 76,664 | 3.2% | $4,565,856 | 3.5% | 1,317,576 | 54.9% | $67,583,116 | 51.5% |

| 2027 | 5 | 79,651 | 3.3% | $4,654,199 | 3.5% | 1,397,227 | 58.2% | $72,237,315 | 55.1% |

| 2028 | 4 | 98,484 | 4.1% | $5,249,665 | 4.0% | 1,495,711 | 62.3% | $77,486,980 | 59.1% |

| 2029 | 18 | 257,405 | 10.7% | $14,489,056 | 11.0% | 1,753,116 | 73.0% | $91,976,035 | 70.1% |

| 2030 and Thereafter(3) | 27 | 648,525 | 27.0% | 39,193,695 | 29.9% | 2,401,641 | 100.0% | $131,169,730 | 100.0% |

| Total | 183 | 2,401,641 | 100.0% | $131,169,730 | 100.0% | | | | |

| (1) | Based on the underwritten rent roll dated October 1, 2019. |

| (2) | Certain tenants may have termination or contraction options (which may become exercisable prior to the originally stated expiration date of the tenant lease) that are not considered in the above Lease Rollover Schedule. |

| (3) | 2030 and Thereafter is inclusive of 22,261 square feet of amenity space. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| | 21 of 95 | |

| Structural and Collateral Term Sheet | | JPMDB 2019-COR6 |

| |

| Century Plaza Towers |

Operating History and Underwritten Net Cash Flow |

| | 2016 | 2017 | 2018 | TTM(1) | Underwritten | Per Square

Foot | %(2) |

| Rents in Place | $93,728,374 | $96,736,098 | $101,042,428 | $97,138,295 | $131,169,730 | $54.62 | 78.4% |

| Vacant Income | 0 | 0 | 0 | 0 | 14,339,776 | 5.97 | 8.6% |

| Gross Potential Rent | $93,728,374 | $96,736,098 | $101,042,428 | $97,138,295 | $145,509,506 | $60.59 | 87.0% |

| Total Reimbursements | 2,366,196 | 3,084,229 | 4,320,460 | 4,341,561 | 3,618,229 | 1.51 | 2.2% |

| Parking | 15,328,900 | 14,885,609 | 14,507,607 | 14,942,509 | 14,942,509 | 6.22 | 8.9% |

| Other Income(3) | 2,516,128 | 2,673,150 | 5,446,950 | 4,468,294 | 3,261,468 | 1.36 | 1.9% |

| Net Rental Income | $113,939,598 | $117,379,086 | $125,317,445 | $120,890,660 | $167,331,712 | $69.67 | 100.0% |

| (Vacancy/Credit Loss) | 0 | 0 | 0 | 0 | (8,715,744) | (3.63) | (5.2)% |

| Effective Gross Income | $113,939,597 | $117,379,087 | $125,317,446 | $120,890,660 | $158,615,968 | $66.04 | 94.8% |

| | | | | | | | |

| Total Expenses | $33,156,253 | $34,178,955 | $36,292,891 | $37,547,742 | $37,470,212 | $15.60 | 23.6% |

| | | | | | | | |

| Net Operating Income(4) | $80,783,345 | $83,200,132 | $89,024,555 | $83,342,918 | $121,145,756 | $50.44 | 76.4% |

| | | | | | | | |

| Total TI/LC, Capex/RR | 0 | 0 | 0 | 0 | 8,895,390 | 3.70 | 5.6% |

| Net Cash Flow | $80,783,345 | $83,200,132 | $89,024,555 | $83,342,918 | $112,250,366 | $46.74 | 70.8% |

| (1) | TTM column represents the trailing 12-month period ending on September 30, 2019. |

| (2) | % column represents percent of Net Rental Income for all revenue lines and represents percent of Effective Gross Income for the remainder of fields. |

| (3) | Other Income includes after-hours HVAC income, fitness center income, tenant services income, storage income, telecom & roof income, filming & events income, retail percentage rent income and a termination fee. |

| (4) | The main cause of the increase between TTM September 2019 Net Operating Income and Underwritten and Outstanding Net Operating Income is new leases that have been executed since September 2019, accounting for 20.6% of NRA and 24.6% of UW Gross Potential Revenue. |

Property Management. The Century Plaza Towers Property is managed byCBRE, Inc.

Escrows and Reserves.At origination, the borrower deposited (i) approximately $71,223,945 into a TI/LC reserve for outstanding landlord work and tenant allowances and (ii) $29,545,735 into a free rent reserve.

Tax Escrows– During a Trigger Period (as defined below),the borrower is required to deposit into a real estate tax reserve, on a monthly basis, 1/12 of the estimated annual real estate taxes.

Insurance Escrows –Insurance escrows are waived so long as (i) no event of default has occurred and is continuing and (ii) the Century Plaza Towers Property is covered by an acceptable blanket policy (which is currently maintained). If such condition is no longer satisfied, on each payment date, the borrowers will be required to fund an insurance reserve in an amount equal to 1/12 of the amount that the lender estimates will be necessary to pay the annual insurance premiums.

Lockbox / Cash Management. The Century Plaza Towers Whole Loan is structured with a hard lockbox and will have springing cash management during a Trigger Period. At origination, a clearing account controlled by the lender (the “Clearing Account”) was established by the borrower, into which all rents, revenues and receipts from the Century Plaza Towers Property are required to be deposited directly by the tenant (with respect to rents). If no Trigger Period (as defined below) exists, the funds in the Clearing Account are required to be swept on each business day into the borrower’s operating account and, if a Trigger Period exists, such funds are required to be swept on each business day into a cash management account controlled by the lender (the “CMA”) at a financial institution selected by the lender.

During a Trigger Period, all amounts on deposit in the CMA will be applied to the payment of all monthly amounts due under the Century Plaza Towers Whole Loan documents (including, without limitation, monthly deposits for reserves for taxes and insurance (unless an acceptable blanket policy is in place with regards to insurance), debt service and all other required reserves) and all property costs and expenses set forth in the lender-approved budget. Any funds remaining thereafter will be transferred to a cash collateral account, as additional collateral for the Century Plaza Towers Whole Loan. Under certain circumstances and for limited purposes described in the Century Plaza Towers Whole Loan documents, the borrower may request disbursements of such excess cash flow.

A “Trigger Period” will be continuing during any period when there exists (i) an uncured event of default under the Century Plaza Towers Whole Loan or under a mezzanine loan (one is incurred as described further below) or (ii) a Low Debt Yield Trigger (as defined below).