UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

[X] Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the Fiscal Year Ended

December 31, 2008.

[ ] Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the Transition Period from _______________ to _______________.

Commission File Number 000-32409

UNITED MORTGAGE TRUST

(Exact name of registrant as specified in its charter)

MARYLAND 75-6493585

(State or other jurisdiction of (I.R.S. Employer

incorporation or organization) Identification Number)

1301 Municipal Way, Grapevine TX 76051

(Address of principal executive offices) (Zip Code)

Issuer's telephone number: (214) 237-9305

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: Shares of Beneficial interest, par value $0.01 per share

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [] No [X]

Indicate by check mark if the Registrant is not required to file reports

pursuant to Section 13 or Section 15(d) of the Act.

Yes [] No [X]

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days.

Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers in response to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K [X]

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

.

Large accelerated Filer[ ] Accelerated Filer[ ] Non-accelerated filer [ ] Smaller reporting company [ X ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes [] No [X]

State the aggregate market value of the voting and non-voting common equity held by non-affiliates of the Registrant computed with reference to the price at which the common equity as last sold, or the average of the bid and asked price of such common equity, as of the last business day of the Registrant’s most recently completed second fiscal quarter.

There is currently no established public market on which the Company’s common shares are traded. The aggregate market value of the registrant’s shares of beneficial interest held by non-affiliates of the registrant at June 30, 2008 computed by reference to the price at which the common equity was last sold was $130,948,411.

Indicate the number of shares outstanding of each of the Registrant’s classes of common stock, as of the latest practicable date.

As of March 31, 2009, 6,412,299 of the Registrant's Shares of Beneficial Interest were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The information required by Part III of this report, to the extent not set forth herein, is incorporated by reference to the Registrant’s definitive proxy statement for the 2008 annual meeting of shareholders.

| Table of Contents | |

| PART I | Page No. |

| Item 1. Business | 4 |

| Item 1A. Risk Factors | 10 |

| Item 1B. Unresolved Staff Comments | 14 |

| Item 2. Properties | 14 |

| Item 3. Legal Proceedings | 14 |

| Item 4. Submission of Matters to a Vote of Security Holders | 14 |

| | |

| PART II | | |

| Item 5. Market for Registrant’s Common Equity Related Shareholder Matters and Issuer Purchases of Equity Securities | 15 |

| Item 6. Selected Financial Data | 16 |

| Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations of the Company | 17 |

| Item 7A. Quantitative and Qualitative Disclosures About Market Risk | 35 |

| Item 8. Consolidated Financial Statements and Supplementary Data | 36 |

| Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 53 |

| Item 9A. Controls and Procedures | 53 |

| Item 9B. Other Information | 54 |

| | | |

| PART III | | |

| Item 10. Directors and Executive Officers of the Registrant | 55 |

| Item 11. Executive Compensation | 59 |

| Item 12. Security Ownership of Certain Beneficial Owners and management and Related Stockholder Matters | 60 |

| Item 13. Certain Relationships and Related Transactions | 61 |

| Item 14. Principal Accounting Fees and Services | 63 |

| Item 15. Exhibits and Financial Statement Schedules | 65 |

PART I

This Annual Report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Such statements involve known and unknown risks, uncertainties, and other factors which may cause our actual results, performance, or achievements to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements. Such factors include, but are not limited to, our ability to find suitable mortgage investments; the difficulties of the real estate industry generally in response to the “sub-prime crisis,” the “credit crisis,” the current difficulties in the housing and mortgage industries, the current economic environment and changes in economic conditions and the requirement to maintain qualification as a real estate investment trust. Although we believe that the assumptions underlying the forward-looking statements contained herein are reasonable, any of the assumptions could be inaccurate, and therefore we cannot give assurance that such statements included in this Annual Report will prove to be accurate. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation by us or by any other person that the results or conditions described in such statements or in our objectives and plans will be realized. Readers should carefully review our financial statements and the notes thereto, as well as the risk factors described in Item 1A and in our other filings with the Securities and Exchange Commission.

ITEM 1. BUSINESS.

GENERAL

United Mortgage Trust (which we refer to in this report as “we,”, “us”, “our” and the “Company”) is a Maryland real estate investment trust formed on July 12, 1996. We acquire mortgage investments from several sources, including from affiliates of our Advisor. The amount of mortgage investments acquired from such sources depends upon the mortgage investments that are available from them or from other sources at the time we have funds to invest. We believe that all mortgage investments purchased from affiliates of the Advisor are at prices no higher than those that would be paid to unaffiliated third parties for mortgages with comparable terms, rates, credit risks and seasoning.

Our principal investment objectives are to invest proceeds from our dividend reinvestment plan, financing proceeds, capital transaction proceeds and retained earnings in the following types of investments: (i) first lien secured interim mortgage loans with initial terms of 12 months or less for the acquisition and renovation of single-family homes, which we refer to as “Interim Loans”; (ii) secured, subordinate line of credit to UMTH Lending Company, L.P. for origination of Interim Loans; (iii) lines of credit and secured loans for the acquisition and development of single-family home lots, referred to as “Land Development Loans”; (iv) lines of credit and loans secured by entitled and developed single-family lots, referred to as “Finished Lot Loans”; (v) lines of credit and loans secured by completed model homes, referred to as “Model Home Loans”; (vi) loans provided to entities that have recently filed for bankruptcy protection under Chapter 11 of the US bankruptcy code, secured by a priority lien over pre-bankruptcy secured creditors, referred to as “Debtor in Possession Loans”, (vii) lines of credit and loans, with terms of 18 months or less, secured by single family lots and homes constructed thereon, referred to as “Construction Loans; and (viii) first lien secured mortgage loans with terms of 12 to 360 months for the acquisition of single-family homes, referred to as “Residential Mortgages”. We collectively refer the above listed loans as “Mortgage Investments”. Additionally, our portfolio includes obligations of affiliates of our Advisor, which we refer to as “recourse loans.”

The typical terms for residential mortgages, contracts for deed and interim loans (collectively referred to as “mortgage investments”) are 360 months, 360 months and 12 months, respectively. The line of credit we have extended to United Development Funding, L.P. (“UDF”) has a five year term. Finished lot loans and builder model home loans are expected to have terms of 12 to 48 months. The majority of interim loans are covered by recourse agreements that obligate either a third party with respect to the performance of a purchased loan, or a borrower that has made a corresponding loan to another party (the "underlying borrower"), to repay the loan if the underlying borrower defaults. Our loans to UDF are secured by the pledge of all of UDF’s land development loans and equity participations, and are subordinated to its bank lines of credit. In addition, as an enhancement, in October 2006, United Development Funding III, L.P. (“UDF III”), a newly formed public limited partnership that is affiliated with UDF and with our Advisor, entered into a limited guaranty, effective as of September 1, 2006, for our benefit (the “UDF III Guarantee”). Pursuant to the UDF III Guarantee, UDF III guaranteed the repayment of up to $30 million under the Second Amended and Restated Secured Line of Credit Promissory Note between United Mortgage Trust and UDF. The UDF III guarantee was released effective January 1, 2008.

We seek to produce net interest income from our mortgage investments while maintaining strict cost controls in order to generate net income for monthly distribution to our shareholders. We intend to continue to operate in a manner that will permit us to qualify as a Real Estate Investment Trust (“REIT”) for federal income tax purposes. As a result of that REIT status, we are permitted to deduct dividend distributions to shareholders, thereby effectively eliminating the "double taxation" that generally results when a corporation earns income (upon which the corporation is taxed) and distributes that income to shareholders in the form of dividends (upon which the shareholders are taxed).

The overall management of our business is vested in our Board of Trustees. UMTH General Services, L.P., a Delaware limited partnership (“Advisor” or “UMTHGS”) and a subsidiary of UMT Holdings, L.P. (“UMTH”), has been retained to manage our day-to-day operations and to use its best efforts to seek out and present, whether through its own efforts or those of third parties retained by it, investment opportunities that are consistent with our investment policies and objectives and consistent with the investment programs the trustees may adopt from time to time in conformity with our Declaration of Trust. Our President, Christine “Cricket” Griffin, is a limited partner of UMTH.

In addition to this annual report, we file quarterly and special reports, proxy statements and other information with the Securities and Exchange Commission (“SEC”). All documents that we file with the SEC are available free of charge on our website, which is www.unitedmorgagetrust.com. You may also read and copy any document that we file at the public reference facilities of the SEC at 450 Fifth Street NW, Washington DC 20549. Please call the SEC at (800) SEC-0330 for further information about the public reference facilities. These documents also my be accessed through the SEC’s electronic data gathering, analysis and retrieval system (“EDGAR”) via electronic means, including the SEC’s home page on the internet (http://www.sec.gov).

Our principal executive offices are located at 1301 Municipal Way, Grapevine TX 76051, telephone (214) 237-9305 or (800) 955-7917, facsimile (214) 237-9304.

TERMINATION OF THE MERGER AGREEMENT

On June 13, 2006, the Board of Trustees voted to take no action to prevent the Agreement and Plan of Merger dated September 1, 2005 ("Merger Agreement") between the Company and UMTH pursuant to which the Company would have merged with and into UMTH ("Merger") from terminating for failure to satisfy the condition that the Merger would terminate if the Merger was not consummated by June 30, 2006. On June 13, 2006, the Company received a letter from UMTH in which UMTH also expressed the view that the Merger would terminate on June 30, 2006. On June 30, 2006 the merger terminated and as a result the Company wrote-off approximately $1,040,000 in capitalized merger costs as reflected in the statements of income. The Company did not incur any termination penalties as a result of the termination of the merger.

RESTATED INVESTMENT OBJECTIVES AND POLICIES OF UNITED MORTGAGE TRUST

February 20, 2009

PRINCIPAL INVESTMENT OBJECTIVES

Our principal investment objectives are to invest proceeds from our dividend reinvestment plan, financing proceeds, capital transaction proceeds and retained earnings in five types of investments:

Our principal investment objectives are to invest proceeds from our dividend reinvestment plan, financing proceeds, capital transaction proceeds and retained earnings in following types of investments:

(i) first lien secured interim mortgage loans with initial terms of 12 months or less for the acquisition and renovation of single-family homes, which we refer to as “Interim Loans”;

(ii) secured, subordinate line of credit to UMTH Lending Company, L.P. for origination of Interim Loans;

| | (iii) | lines of credit and secured loans for the acquisition and development of single-family home lots, referred to as “Land Development Loans”; |

| | (iv) | lines of credit and loans secured by entitled and developed single-family lots, referred to as “Finished Lot Loans”; and, |

| | (v) | lines of credit and loans secured by completed model homes, referred to as “Model Home Loans”; and, |

| | (vi) | loans provided to entities that have recently filed for bankruptcy protection under Chapter 11 of the US bankruptcy code, secured by a priority lien over pre-bankruptcy secured creditors, referred to as “Debtor in Possession Loans” and, |

| | (vii) | lines of credit and loans, with terms of 18 months or less, secured by single family lots and homes constructed thereon, referred to as “Construction Loans; and, |

| | (viii) | first lien secured mortgage loans with terms of 12 to 360 months for the acquisition of single-family homes, referred to as “Residential Mortgages” |

We collectively refer the above listed loans as “Mortgage Investments”.

In addition, we intend to generate fee income by providing credit enhancements associated with residential real estate financing transactions in the various forms as recommended from time-to-time by our Advisor and approved by our Board of Trustees, including but not limited to, guarantees, pledges of cash deposits, letters of credit and tri-party inter-creditor agreements, all of which we refer to as “Credit Enhancements”. Mortgage Investments and Credit Enhancements are expected to:

| | (1) | produce net interest income and fees; |

| | (2) | provide monthly distributions from, among other things, interest on Mortgage Investments and fees from credit enhancements; and |

| | (3) | permit reinvestment of payments of principal and proceeds of prepayments, sales and insurance net of expenses. |

There is no assurance that these objectives will be attained.

INVESTMENT POLICY

Most of our Mortgage Investments to date are geographically concentrated in the Texas market. We anticipate that the concentration will continue in the near future, but it is our intention to expand our geographic presence through the purchase of Mortgage Investments in other geographic areas of the United States. In making the decision to invest in other areas, we consider the market conditions prevailing at the time we invest.

As of December 31, 2008, our portfolio was comprised of:

| Percentage of Mortgage Portfolio: |

First lien secured interim mortgages 12 months or less and residential mortgages and contracts for deed | |

Secured, subordinate LOC to UMTH Lending Co., L.P. | |

| |

| |

| |

We no longer purchase Interim Loans that are secured by modular and manufactured homes. We increased our investment in our affiliated line of credit to UMTH Lending Co., L.P., secured by Interim Loans, by approximately $8,000,000 in the first quarter of 2009. We plan to invest in Residential Mortgages to facilitate the sale of homes securing our Interim Loans. We plan to invest in Construction Loans for the construction of new single family homes. We plan to continue to invest in Land Development Loans, Finished Lot Loans, and Model Home Loans because, 1) Land Development Loans and Finished Lot Loans have provided us with suitable collateral positions, well capitalized borrowers and attractive yields; and, 2) Model Home Loans and Construction Loans are expected to provide us with suitable collateral positions, well capitalized borrowers and attractive yields. Model Home and Construction Loans are expected to produce higher yields commensurate with Land Development Loans, Finished Lot Loans and the Subordinate Line of Credit secured by Interim Loans. As we phase out of non-affiliate Interim Loans we will increase the percentage of our portfolio invested in Land Development Loans, Finished Lot Loans, Model Home Loans, Debtor in Possession Loans, and Construction Loans, until market conditions indicate the need for an adjustment of the portfolio mix.

UNDERWRITING CRITERIA

We will not originate loans, except to facilitate the resale of a foreclosed property. Funds awaiting investment in Mortgage Investments will be invested in government securities, money market accounts or other assets that are permitted investments for REITs. See “Temporary Investments” below.

The underwriting criteria for Mortgage Investments are as follows:

| | · | Land Development Loans and Finished Lot Loans must be secured by a first lien, second lien or a pledge of partnership interest that is insured by a title company. Second liens are subject to the Loan-to-Value (“LTV”) limitations set forth below. |

| | · | Subordinate Line of Credit Secured by Interim Loans will be secured by a second lien, insured by a title company, and is subject to the Loan-to-Value limitations set forth below. |

| | · | Interim Loans purchased must be secured by a first lien that is insured by a title insurance company. |

| | · | Model Home Loans and Construction Loans will be secured by a first lien that is insured by a title insurance company. |

| | · | Residential Mortgages will be secured by a first lien that is insured by a title insurance company. |

| | · | Credit Enhancements must be secured by first or second liens or pledges of partnership interests. |

| | · | Debtor in Possession Loans will be secured by a priority lien over pre-bankruptcy secured creditors and a claim with super-priority over administrative expenses allowed by the bankruptcy court. |

| | · | Our advisor, UMTH General Services, L.P. (“UMTHGS” or our “Advisor”) seeks to acquire Mortgage Investments that will provide us with a satisfactory net yield. Net yield is determined by the yield realized after payment of note servicing fees, if any, and administrative costs (ranging from 1% to 2% of our average invested assets). Rates will be either adjustable or fixed. No loans will be purchased at a premium above the outstanding principal balance. Our investment policy allows for acquisition of loans at various rates. Fees charged for Credit Enhancements will be determined by the degree of risk as determined and recommended by our Advisor. Credit Enhancement fees are expected to range between 0.5% and 3% per annum. |

| (3) | Term and Amortization. |

| | · | There is no minimum term for the loans we acquire. |

| | · | Land Development Loans, Finished Lot Loans and Model Home Loans will generally have terms from 24 to 48 months. |

| | · | Construction Loans will generally have terms of 12 to 18 months. |

| | · | Interim Loans and Subordinate Interim Loans will generally have terms of 12 months or less. |

| | · | Generally, Land Development Loans, Finished Lot Loans, Model Home Loans, Construction Loans and Interim Loans do not amortize. They are interest only loans with the principal paid in full when the loans mature. |

| | · | Residential Mortgages will generally have terms and amortizations from 180 to 360 months. |

| | · | Debtor in Possession Loans will generally have terms and amortizations from 6 to 60 months. |

| | · | Credit Enhancements will range from 12 to 48 months. |

| (4) | LTV, Investment-to-Value Ratio (“ITV”), Combined LTV Ratio (“CLTV”). |

| | · | Land Development Loans, Finished Lot Loans, Residential Mortgages and Construction Loans: Except as set forth below, loans purchased may not exceed an 85% ITV. Except as set forth below, Land Development Loans, Finished Lot Loans, Residential Mortgages and Construction Loans will not exceed 85% of the value of the collateral securing the indebtedness (the LTV of the loan). The purchase of, or investment in, subordinate liens secured loans or partnership interests securing loans will not exceed a CLTV of 85%, (subject to the exceptions listed below). CLTV shall mean the sum of all indebtedness senior to us plus the sum of our investment or loan. |

| | · | Model Home Loans: LTV may not exceed 93% each loan, will be a part of a pool of model home collateral and will also be cross-collateralized. All expenses associated with the model home are borne by the home builder. |

| | · | Subordinated Interim Loans and Interim Loans: Loans will not exceed a 75% CLTV without approval by our Board of Trustees. |

| | · | Debtor in Possession Loans will not exceed a 75% ITV. |

| | · | None of the types of loans we currently purchase, or intend to purchase, are subject to seasoning requirements. |

| (6) | Borrower, Loan and Property Information. |

| | · | Land Development Loans, Finished Lot Loans, Model Homes Loans, Construction Loans, and Credit Enhancements: Borrower, loan and property information will be in accordance with guidelines set forth by the originating entities, United Development Funding and UMTH Land Development, L. P., including economic feasibility studies, engineering due diligence reports, exit strategy analysis, and construction oversight requirements. UMTH General Services, L.P. (“UMTHGS” or our “Advisor”), our Advisor, will periodically monitor compliance and changes to underwriting guidelines. |

| | · | ·Residential Mortgages: Borrower, loan and property information will be in accordance with guidelines set forth by the originating entities, UMTH Lending Company, L. P. UMTH General Services, L.P. (“UMTHGS” or our “Advisor”), our Advisor will periodically monitor compliance and changes to underwriting guidelines. |

| | · | Interim Loans: Loans shall be underwritten in accordance with the guidelines established by the originating company, UMTH Lending Company, L.P., including borrower and property information. Our Advisor will periodically monitor compliance and changes to underwriting guidelines. |

| | · | Debtor in Possession Loans will be reviewed and underwritten on a case by case basis by our Advisor, due to their unique characteristics. Our Advisor will employ the services of outside consultants, when and if necessary, to effectively evaluate each opportunity. |

| | · | Land Development Loans, Finished Lot Loans, Construction Loans, Residential Mortgages and Model Home Loans: Appraisal must demonstrate that the LTV, ITV or CLTV is in compliance with the above referenced LTV, ITV and CLTV standards. Loans exceeding LTV, ITV and CLTV guidelines must note the criteria on which the exception was based. |

| | · | Subordinate Interim Loans and Interim Loans: Appraisal must demonstrate that the CLTV or ITV is not more than 75% (subject to the exceptions set forth in 4 above). |

| | · | Debtor in Possession loans will be underwritten on a case by case basis, given their unique characteristics and circumstances. |

| | · | The appraisals must be performed by appraisers approved by our Advisor. |

| | · | Subordinate Interim Loans, Residential Mortgages and Interim Loans: Minimum credit scores and corresponding down payment requirements will be in accordance with the guidelines set by the originating company (currently UMTH Lending Company, L.P.). UMTHGS will periodically monitor compliance and changes to underwriting guidelines. |

| | · | Land Development Loans, Finished Lot Loans, Model Home Loans, Construction Loans and Credit Enhancements: Extensions of credit to borrowers will be determined in accordance with net worth and down payment requirements prescribed by the originating companies (currently United Development Funding and UMTH Land Development, L.P.). UMTHGS as Advisor to UMT shall periodically monitor compliance and changes to underwriting guidelines. |

| | · | Loans that are secured by a residence must have an effective, prepaid hazard insurance policy with a mortgagee's endorsement for our benefit in an amount not less than the outstanding principal balance on the loan. We reserve the right to review the credit rating of the insurance issuer and, if deemed unsatisfactory, request replacement of the policy by an acceptable issuer. |

| (10) | Geographical Boundaries. |

| | · | We may purchase Mortgage Investments and provide Credit Enhancements for real estate projects in any of the 48 contiguous United States. |

| (11) | Mortgagees' Title Insurance. |

| | · | Each Mortgage Investment purchased must have a valid mortgagees' title insurance policy insuring our lien position in an amount not less than the outstanding principal balance of the loan. |

| 12) | Guarantees, Recourse Agreements, and Mortgage Insurance. |

| | · | Subordinate Interim Loans, Interim Loans and Residential Mortgages purchased shall contain personal guarantees of the borrower or principal of the borrower. |

| | · | Subordinate Interim Loans and Interim Loans shall afford full recourse to the originating company. |

| | · | ·Land Development Loans, Finished Lot Loans, Model Home Loans, Construction Loans and Credit Enhancements shall have guarantees and collateral arrangements as determined by the originating companies (United Development Funding and UMTH Land Development, L.P). Our Advisor shall review guarantees and recourse obligations. |

| | · | Debtor in Possession loans shall be secured by a priority lien over pre-bankruptcy secured creditors. |

| | · | Our Advisor shall review guarantees and recourse obligations. |

| | · | Mortgage Investments will be purchased at no minimum percentage of the principal balance, but in no event in excess of the outstanding principal balance. |

| | · | Yields on our loan portfolio and fees charged for Credit Enhancements will vary with perceived risk, interest rate, credit, LTV ratios, down payments, guarantees or recourse agreements among other factors. Our objectives will be accomplished through purchase of high rate loans, reinvestment of principal payments and other short-term investment of cash reserves and, if utilized, leverage of capital to purchase additional Mortgages Investments. |

The principal amounts of Mortgage Investments and the number of Mortgage Investments in which we invest will be affected by market availability and also depends upon the amount of capital available to us from proceeds of our dividend reinvestment plan, retained earnings, repayment of our loans and borrowings. There is no way to predict the future composition of our portfolio since it will depend in part on the loans available at the time of investment.

TEMPORARY INVESTMENTS

We intend to use proceeds from our dividend reinvestment plan, retained earnings, proceeds from the repayment of our loans and bank borrowings to acquire Mortgage Investments. There can be no assurance as to when we will be able to invest the full amount of capital available to us in Mortgage Investments, although we will use our best efforts to invest or commit for investment all capital within 60 days of receipt. We will temporarily invest any excess cash balances not immediately invested in Mortgage Investments or for the other purposes described above, in certain short-term investments appropriate for a trust account or investments which yield "qualified temporary investment income" within the meaning of Section 856(c)(6)(D) of the Code or other investments which invest directly or indirectly in any of the foregoing (such as repurchase agreements collateralized by any of the foregoing types of securities) and/or such investments necessary for us to maintain our REIT qualification or in short-term highly liquid investments such as in investments with banks having assets of at least $50,000,000, savings accounts, bank money market accounts, certificates of deposit, bankers' acceptances or commercial paper rated A-1 or better by Moody's Investors Service, Inc., or securities issued, insured or guaranteed by the United States government or government agencies, or in money market funds having assets in excess of $50,000,000 which invest directly or indirectly in any of the foregoing.

OTHER POLICIES

We will not: (a) issue senior securities; (b) invest in the securities of other issuers for the purpose of exercising control; (c) invest in securities of other issuers, other than in temporary investments as described under "Investment Objectives and Policies - Temporary Investments"; (d) underwrite the securities of other issuers; or (e) offer securities in exchange for property.

We may borrow funds to make distributions to our shareholders or to acquire additional Mortgage Investments. Our ability to borrow funds is subject to certain limitations set forth in the Declaration of Trust, specifically, the Trust may not incur indebtedness in excess of 50% of the Net Asset Value of the Trust.

Other than in connection with the purchase of Mortgage Investments or issuance of Credit Enhancements, which may be deemed to be a loan from us to the borrower, we do not intend to loan funds to any person or entity. Our ability to lend funds to the Advisor, a Trustee or Affiliates thereof is subject to certain restrictions as described in "Summary of Declaration of Trust - Restrictions on Transactions with Affiliates.”

We will not sell property to our Advisor, a Trustee or Affiliates thereof at terms less favorable than could be obtained from a non-affiliated party.

Although we do not intend to invest in real property, to the extent we do, a majority of the Trustees shall determine the consideration paid for such real property, based on the fair market value of the property. If a majority of the Independent Trustees so determine, or if the real property is acquired from the Advisor, as Trustee or Affiliates thereof, a qualified independent real estate appraiser shall determine such fair market value selected by the Independent Trustees.

We will use our best efforts to conduct our operations so as not to be required to register as an investment company under the Investment Company Act of 1940 and so as not to be deemed a "dealer" in mortgages for federal income tax purposes. See "Federal Income Tax Considerations.”

We will not engage in any transaction which would result in the receipt by the Advisor or its Affiliates of any undisclosed "rebate" or "give-up" or in any reciprocal business arrangement which results in the circumvention of the restrictions contained in the Declaration of Trust and in applicable state securities laws and regulations upon dealings between us and the Advisor and its Affiliates.

The Advisor and its Affiliates, including companies, other partnerships and entities controlled or managed by such Affiliates, may engage in transactions described in our prospectus, including acting as Advisor, receiving distributions and compensation from us and others, the purchasing, warehousing, servicing and reselling of mortgage notes, property and investments and engaging in other businesses or ventures that may be in competition with us.

CHANGES IN INVESTMENT OBJECTIVES AND POLICIES

The investment restrictions contained in the Declaration of Trust may only be changed by amending the Declaration of Trust with the approval of the shareholders. However, subject to those investment restrictions, the methods for implementing our investment policies may vary as new investment techniques are developed. The Board of Trustees shall periodically, no less than annually review our investment policies and objectives and publish same in a public filing and direct mail communication to our shareholders.

COMPETITION

We believe that our principal competition in the business of acquiring and holding mortgage investments is from financial institutions such as banks, saving and loan associations, life insurance companies, institutional investors such as mutual funds and pension funds, and certain other mortgage REITs. While most of these entities have significantly greater resources than we do, we believe that we are able to compete effectively and to generate relatively attractive rates of return for shareholders due to our relatively low level of operating costs, our relationships with our sources of mortgage investments and the tax advantages of our REIT status.

EMPLOYEES

We have no employees however, our Advisor is staffed with employees who possess expertise in all areas required to fulfill its obligation as manager of our day-to-day management. Our President is a limited partner of UMTH. UMTH owns 99.9% of UMTHGS, our Advisor.

ITEM 1A. RISK FACTORS.

The following are certain risk factors that could affect our business, financial condition, operating results and cash flows. These risk factors should be considered in connection with the forward-looking statements contained in this Annual Report on Form 10-K because these risk factors could cause our actual results to differ materially from those expressed in any forward-looking statement. The risks highlighted below are not the only ones we face. If any of these events actually occur, our business, financial condition, operating results or cash flows could be negatively affected. We caution readers to keep these risk factors in mind and to refrain from attributing undue certainty to any forward-looking statements, which speak only as of the date of this report.

Our operations and results are subject to the risks associated with the real estate industry.

Our operating results and the value of our mortgage investments, and consequently the value of your shares, are subject to the risk that if our mortgage investments do not generate revenues sufficient to meet our operating expenses, including debt service and capital expenditures, our cash flow and ability to pay distributions to you will be adversely affected. The following factors, among others, may adversely affect our results:

| - | downturns in the national, regional and local economic climate; |

| - | competition from other real estate lenders; |

| - | local real estate market conditions, such as oversupply or reduction in demand for properties; |

| - | trends and developments in the homebuilding industry; |

| - | conditions in financial markets, including changes in interest rates, the availability and cost of financing, the fiscal and monetary policies of the United States government and the Board of Governors of the Federal Reserve System and international financial conditions; |

| - | increased operating costs, including, but not limited to, insurance expense, utilities, real estate taxes, state and local taxes; |

| - | civil disturbances, natural disasters, or terrorist acts or acts of war which may result in uninsured or underinsured losses; and |

| - | declines in the financial condition of our borrowers and our ability to collect on the loans we make to our borrowers. |

Recent Developments in the Residential Sub-prime Mortgage Market Could Adversely Affect Our Results.

During 2008, the mortgage lending industry continued to experience significant instability due to, among other things, defaults on sub-prime and prime loans and a resulting decline in the market value of such loans. These developments were initially referred to as the “sub-prime crisis” but it became evident in 2008 that the crisis had progressed beyond “sub-prime” mortgages as the default rate on prime mortgages also increased. The sub-prime crisis had become a credit crisis. As part of the credit crisis, lenders, investors, regulators and other third parties questioned the adequacy of lending standards and other credit requirements for several loan programs made available to borrowers in recent years. This has led generally to reduced investor demand for mortgage loans and mortgage-backed securities, tightened credit requirements, reduced liquidity and increased credit risk premiums.

The deterioration in the housing market resulting from the credit crisis may have an adverse impact on our portfolio of mortgage investments because our interim loan borrowers rely on prospective home buyers who do not satisfy all of the income ratios, credit record criteria, loan-to-value ratios, seasoning, employment history and liquidity requirements of conventional mortgage financing. These factors place the loans in the “non-conforming” category, meaning that they are not insured or guaranteed by a federally owned or guaranteed mortgage agency. Accordingly, the risk of default by the borrower in those "non-conforming loans" is higher than the risk of default in loans made to persons who qualify for conventional mortgage financing.

We believe that the impact of these factors on our operations has been significant. We have adopted active strategies to monitor and manage our credit risk and our portfolio of mortgage investments, such as reducing our investments in interim loans secured by conventionally built homes, with the objective of limiting to the extent possible adverse financial effects from the credit crisis. However, we have two loans in California, which is one of the states where the sub-prime crisis has been felt the most and conditions could change in Texas and in our other markets. Therefore, we can give no assurances that there will not be a marked increase in defaults under our interim loans accompanied by a rapid decline in real estate values that could have further material adverse effect upon our financial condition and operating results.

We may not be successful in managing credit risk, particularly as such risk is impacted by the credit crisis, which could adversely affect our results and our ability to pay distributions to our shareholders.

Despite our efforts to manage credit risk, there are many aspects of credit risk that we cannot control. In addition, the credit crisis has created new circumstances that increase the difficulty of predicting the credit risks to which we will be exposed and limiting future delinquencies, defaults, and losses. Our borrowers may default and we may experience delinquencies at a higher rate than we anticipate. Our underwriting reviews may not be effective. Our loan loss reserves may prove to be inadequate. The value of the homes collateralizing our mortgage investments may decline. We may have difficulty selling any homes that are repossessed which could delay or prevent us from recovering our investment. Changes in lending trends, consumer behavior, bankruptcy laws, tax laws, regulations impacting the mortgage industry, and other laws may exacerbate loan losses. Other changes or actions by judges or legislators regarding mortgage loans and contracts including the voiding of certain portions of these agreements may reduce our earnings, impair our ability to mitigate losses, or increase the probability and severity of losses. Our loss mitigation efforts will impact our operating costs and may not be effective in reducing our future credit losses.

Our dividend can fluctuate because it is based on earnings.

The dividend rate is fixed quarterly by our trustees, based on earnings projections. As such, the dividend rate may fluctuate up or down. Earnings are affected by various factors including use of leverage, cash on hand, current yield on investments, loan losses, general and administrative operating expenses and amount of non-income producing assets. We distributed in excess of earnings between 1999 and 2005 and in 2008. The amount of the excess constituted a return of capital.

A portion of our investments are subject to a higher risk of default than conventional mortgage loans.

Most of our mortgage investments are “non-conforming” in that they are not insured by a federally owned or guaranteed mortgage agency. Also, a portion of our loans involve, directly or indirectly, borrowers who do not satisfy all of the income ratios, credit record criteria, loan-to-value ratios, employment histories and liquidity requirements of conventional mortgage financing. Accordingly, the risk of default by the borrower in those "non-conforming loans" is higher than the risk of default in loans made to persons who qualify for conventional mortgage financing. The three year average default rate for our residential mortgages and contracts for deed was approximately 6.0% and for our interim loans was approximately 2.0%. The interim loan default rate increased in 2008 primarily due to the foreclosures of the RDC portfolio.

Fluctuations in interest rates may affect our return on investment.

Mortgage interest rates may be subject to abrupt and substantial fluctuations. Changes in interest rates may impact both demand for our real estate finance products and the rate of interest on the loans we make. If prevailing interest rates rise above the average interest rate being earned by our mortgage investments, we may be unable to quickly liquidate our existing investments in order to take advantage of higher returns available from other investments. Furthermore, interest rate fluctuations may have a particularly adverse effect on the return we realize on our mortgage investments if we use money borrowed at variable rates to fund fixed rate mortgage investments. A portion of the loans we finance for UDF are junior in the right of repayment to senior lenders, who will provide loans representing 70% to 80% of total project costs. As senior lender interest rates available to our borrowers increase, demand for our mortgage loans may decrease, and vice versa.

We have a dependence upon the UDF line of credit which also concentrates our credit risk.

Our line of credit to UDF is currently $45 million, and, if fully funded, we generate a significant amount of our total earnings through that lending arrangement. The line of credit expires December 31, 2009. The large amount that we have committed to the UDF line of credit means that we face a concentrated credit risk with UDF so that, in the event of delinquencies or defaults by UDF, a significant portion of our total portfolio of mortgage investments could be adversely affected. In addition, if we are unable to renew the line of credit when it expires or to find an alternative lending arrangement either with UDF or other borrowers that will allow us to use an equivalent amount of our lending resources and that will generate an equivalent or better return to us, our earnings will be negatively impacted which may result in an adverse impact on our ability to make distributions to our shareholders.

Our loans to UDF are junior to other lenders and expose us to the risks of the homebuilding industry.

Our loans to UDF are secured by UDF’s interest in mortgages and equity participations that it has obtained to secure its loans to real estate developers. Some of those mortgages are junior mortgages. The developers obtain the money to repay the development loans by reselling the residential home lots to home builders or individuals who build single-family residences on the lots. The developer’s ability to repay their loans is based primarily on the amount of money generated by the developer’s sale of its inventory of single-family residential lots. As a result, we are exposed to the risks of the homebuilding industry, which is undergoing a significant downturn due in large part to the credit crisis, the duration and ultimate severity of which are uncertain. Accordingly, continued or further deterioration of home building conditions or in the broader economic conditions of the homebuilding market could cause the number of homebuyers to decrease, which would increase the likelihood of defaults on the development loans and, consequently, increase the likelihood of a default on the UDF line of credit loan. If this were to occur, we may face the inability to recover the outstanding loan balance on foreclosure of collateral securing our loans because our rights to this collateral will be junior to the rights of senior lenders and because of the potentially reduced value of the underlying properties.

We purchase mortgage investments from affiliates of our Advisor, which may present a conflict of interest from our Advisor.

We acquire many of our mortgage investments from affiliates of the Advisor. Due to the affiliation between the Advisor and those entities and the fact that those entities may earn fees on the origination of mortgage investments sold to us, the Advisor has a conflict of interest in determining if mortgage investments should be purchased from affiliated or unaffiliated third parties.

We face competition for the time and services of our officers and the officers and employees of our Advisor.

We rely on our Advisor and its affiliates, including our President, who is a partner of the parent of our Advisor, for management of our operations. Because our Advisor and its affiliates engage in other business activities, conflicts of interest may arise in operating more than one entity with respect to allocating time between those entities.

We have a high geographic concentration of mortgage investments in Texas.

A large percentage of the properties securing our mortgage investments are located in Texas, with approximately 38% in the Dallas/Fort Worth area. As a result, we have a greater susceptibility to the effects of an economic downturn in that area or from slowdowns in certain business segments that represent a significant part of that area’s overall economic activity such as energy, financial services and tourism.

We face the risk of loss on non-insured, non-guaranteed mortgage loans.

We generally do not obtain credit enhancements for our mortgage investments, because the majority of those mortgage loans are "non-conforming" in that they do not meet all of the underwriting criteria required for the sale of the mortgage loan to a federally owned or guaranteed mortgage agency. Accordingly, during the time we hold mortgage investments for which third party insurance is not obtained, we are subject to the general risks of borrower defaults and bankruptcies and special hazard losses that are not covered by standard hazard insurance (such as those occurring from earthquakes or floods). In the event of a default on any mortgage investment held by us, including, without limitation, defaults resulting from declining property values and worsening economic conditions, we would bear the risk of loss of principal to the extent of any deficiency between the value of the related mortgage property and the amount owing on the mortgage loan. Defaulted mortgage loans would also cease to be eligible collateral for borrowings and would have to be held or financed by us out of other funds until those loans are ultimately liquidated, which could cause increased financing costs and reduced net income or a net loss.

Bankruptcy of borrowers may delay or prevent recovery on our loans.

The recovery of money owed to us may be delayed or impaired by the operation of the federal bankruptcy laws. Any borrower has the ability to delay a foreclosure sale for a period ranging from a few months to several months or more by filing a petition in bankruptcy, which automatically stays any actions to enforce the terms of the loan. The length of this delay and the associated costs will generally have an adverse impact on the return we realize on our investments.

We face risks under the representations, warranties and guarantees that we gave in connection with our securitization activities.

We have engaged in two securitizations of our mortgage investments as a means of providing funding. In these transactions, we receive the proceeds from third party investors for securities issued from our securitization vehicles which are collateralized by transferred mortgage investments from our portfolio. As part of those securitizations we made certain representations and warranties concerning the portfolio of mortgage investments conveyed and we also guaranteed certain obligations. If, because of irregularities in the underlying loans, our representations and warranties are inaccurate, we may be obligated to repurchase the loans from the purchasing entities at principal value, which may exceed market value.

We are exposed to potential environmental liabilities.

In the event that we are forced to foreclose on a defaulted mortgage investment to recover our investment, we may be subject to environmental liabilities in connection with that real property which may cause its value to be diminished. Hazardous substances or wastes, contaminants, pollutants or sources thereof (as defined by state and federal laws and regulations) may be discovered on properties during our ownership or after a sale of that property to a third party. If those hazardous substances are discovered on a property, we may be required to remove those substances or sources and clean up the property. We could incur full recourse liability for the entire cost of any removal and clean up and the cost of such removal and clean up could exceed the value of the property or any amount that we could recover from any third party. We may also be liable to tenants and other users of neighboring properties for environmental liabilities. In addition, we may find it difficult or impossible to sell the property prior to or following any such clean up.

We face risks from borrowed money.

We are allowed to borrow an aggregate amount not to exceed 50% of our net assets to acquire mortgage investments. An effect of leveraging is to increase the risk of loss. The higher the rate of interest on the financing, the more difficult it would be for us to meet our obligations and the greater the chance of default. These borrowings may be secured by liens on our mortgage investments. Accordingly, we could lose our mortgage investments if we default on the indebtedness.

We rely on appraisals that may not be accurate or may be affected by subsequent events.

Because our investment decisions are based in major part upon the value of the real estate underlying our mortgage investments and less upon the creditworthiness of the borrowers, we rely primarily on the real property securing the mortgage investments to protect our investment. We rely on appraisals and on Broker Price Opinions ("BPO's"), both of which are paid for and most of which are provided by note sellers, to determine the fair market value of real property used to secure the mortgage investments we purchase. BPO’s are determinations of the value of a property based on a study of the comparable values of similar properties prepared by a licensed real estate broker. We cannot be sure that those appraisals or BPO's are accurate. Moreover, since an appraisal or BPO is given with respect to the value of real property at a given point in time, subsequent events could adversely affect the value of real property used to secure a loan. Such subsequent events may include changes in general or local economic conditions, neighborhood values, interest rates and new construction. Moreover, subsequent changes in applicable governmental laws and regulations may have the effect of severely limiting the permitted uses of the property, thereby drastically reducing its value. Accordingly, if an appraisal is not accurate or subsequent events adversely affect the value of the property, the mortgage investment would not be as secure as anticipated, and, in the event of foreclosure, we may not be able to recover our entire investment.

Our mortgages may be considered usurious.

Usury laws impose limits on the maximum interest that may be charged on loans and impose penalties for violations that may include restitution of the usurious interest received, damages for up to three times the amount of interest paid and rendering the loan unenforceable. Most, if not all, of the mortgage investments we purchase are subject to state usury laws and therefore we face the risk that the interest rate for our loans could be held usurious in states with restrictive usury laws.

We face the risk of an inability to maintain our qualification as a REIT.

We are organized and conduct our operations in a manner that we believe enables us to be taxed as a REIT under the Internal Revenue Code (the "Code"). To qualify as a REIT and avoid the imposition of federal income tax on any income we distribute to our shareholders, we must continually satisfy two income tests, two asset tests and one distribution test.

If, in any taxable year, we fail to distribute at least 90% of our taxable income, we will be taxed as a corporation and distributions to our shareholders will not be deductible in computing our taxable income for federal income tax purposes. Because of the possible receipt of income without corresponding cash receipts due to timing differences that may arise between the realization of taxable income and net cash flow (e.g. by reason of the original issue discount rules) or our payment of amounts that do not give rise to a current deduction (such as principal payments on indebtedness), it is possible that we may not have sufficient cash or liquid assets at a particular time to distribute 90% of our taxable income. In that event, we could declare a consent dividend or we could be required to borrow funds or liquidate a portion of our investments in order to pay our expenses, make the required distributions to shareholders, or satisfy our tax liabilities, including the possible imposition of a four percent excise tax. We may not have access to funds to the extent, and at the time, required to make such payments.

If we were taxed as a corporation, our payment of tax will substantially reduce the funds available for distribution to shareholders or for reinvestment and, to the extent that distributions had been made in anticipation of our qualification as a REIT, we might be required to borrow additional funds or to liquidate certain of our investments in order to pay the applicable tax. Moreover, should our election to be taxed as a REIT terminate or be voluntarily revoked, we may not be able to elect to be treated as a REIT for the following four-year period.

We did not have an audit committee in 2006.

During 2006 our Board of Directors did not appoint an audit committee. The Company did have an audit committee in 2008 and 2007. Typically, an audit committee is responsible for reviewing and discussing with management a company's financial controls and accounting, audit and reporting activities. A typical audit committee will also review the qualifications of the Company's independent registered public accounting firm, select the independent registered public accounting firm and recommend the ratification of the accounting firm to the board, review the scope, fees and results of any audit and review the non-audit services provided by the accounting firm. An audit committee will also be responsible for approving any transactions between the Company and its directors, officers, or significant shareholders. Failing to have a properly constituted audit committee could expose the Company to a greater risk of error or fraud in the compilation, analysis and reporting of the Company's financial results. In addition, having an audit committee is a requirement for a listing of the Company’s securities on a stock exchange.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

Not applicable.

ITEM 2. PROPERTIES.

We do not maintain any physical properties.

ITEM 3. LEGAL PROCEEDINGS.

We are unaware of any threatened or pending legal action or litigation that individually or in the aggregate could have a material effect on us.

ITEM 4. SUBMISSION OF MATTERS TO THE VOTE OF SECURITY HOLDERS.

None.

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED SHAREHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES.

SHARE REDEMPTION PLAN

There is currently no established public trading market for our shares. As an alternative means of providing limited liquidity for our shareholders, we maintain a Share Redemption Plan, (“SRP”). Under the terms of our plan that were effective during 2008, shareholders who have held the shares for at least one year are eligible to request that we repurchase their shares. In any consecutive 12 month period we may not repurchase more than 5% of the outstanding shares at the beginning of the 12 month period. The repurchase price was based on the value of our properties or a fixed pricing schedule, as determined by the trustees' business judgment based on our book value, operations to date and general market and economic conditions and may not, in any event, exceed any current public offering price. We have also purchased a limited number of shares outside of our SRP from shareholders with special hardship considerations.

Share repurchases have been at prices of $16.34 to $20.00 through our SRP. Shares repurchased for less than $20 per share were 1) shares held by shareholders for less than 12 months or 2) shares purchased outside of our Share Redemption Program.

The repurchase price of $20 was determined by our Board of Trustees based on their business judgment regarding the value of the shares with reference to our book value, our operations to date and general market and economic conditions.

The following table summarizes the share repurchases made by us in 2008:

| Total number of shares repurchased | | Total number of shares purchased as part of a publicly announced plan | Total number of shares purchased outside of plan |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

On December 31, 2008, we had 6,436,569 shares outstanding compared to 6,649,916, and 6,917,443 shares outstanding at December 31, 2007 and 2006, respectively. The decrease in shares is the net between fewer DRP shares issued and more SRP shares repurchased. The shares were held by 2,244, 2,373, and 2,760 beneficial owners in 2008, 2007 and 2006, respectively. No single shareholder owned 5% or more of our outstanding shares.

On March 18, 2009, the Board approved certain modifications to the Company’s SRP and its Dividend Reinvestment Plan (“DRIP”), which modifications were disclosed in a Report on Form 8-K which we filed with the SEC on March 19, 2009. Pursuant to the requirements of the SRP and the DRIP, the Company sent its shareholders notice of amendment of the SRP and the DRIP, both to be effective on May 1, 2009. The modifications consist of the following:

Modifications to the Share Redemption Plan (SRP)

The redemption price shall be equal to the “Net Asset Value” (NAV) as of the end of the month prior to the month in which the redemption is made. The NAV will be established by our Board of Trustees no less frequently than each calendar quarter. For reference, at December 31, 2008 the NAV was $16.03 per share. Under the current SRP, the redemption price is $20.00 per share. The Company will waive the one-year holding period ordinarily required for eligibility for redemption and will redeem shares for hardship requests. A “hardship” redemption is (i) upon the request of the estate, heir or beneficiary of a deceased shareholder made within two years of the death of the shareholder; (ii) upon the disability of a shareholder or such shareholder’s need for long-term care, providing that the condition causing such disability or need for long term care was not pre-existing at the time the shareholder purchased the shares and that the request is made within 270 days after the onset of disability or the need for long term care; and (iii) in the discretion of the Board of Trustees, due to other involuntary exigent circumstances of the shareholder, such as bankruptcy, provided that that the request is made within 270 days after of the event giving rise to such exigent circumstances. Previously, there was no hardship exemption. Shares will be redeemed quarterly in the order that they are presented. Any shares not redeemed in any quarter will be carried forward to the subsequent quarter unless the redemption request is withdrawn by the shareholder. Previously, shares were redeemed monthly. Repurchases are subject to cash availability and Trustee discretion. Previously, the SRP provided that repurchases were subject to the availability of cash from the DRIP or the Company’s credit line.

Modifications to the Dividend Reinvestment Plan (DRIP)

Effective May 1, 2009, our DRIP share purchase price will be set at the NAV. Previously, the share purchase price was $20.00 per share.

Please refer to our Report on Form 8-K filed on March 19, 2009 for further information about the modifications to the SRP and DRIP.

DIVIDEND POLICY

Under our current dividend policy, we intend to retain up to 10% of our earnings to build share value, (“Retained Earnings”), and distribute to shareholders at least 90% of our taxable income each year (which does not ordinarily equal net income as calculated in accordance with accounting principles generally accepted in the United States) so as to comply with the REIT provisions of the Code. To the extent we have available funds, we declare regular monthly dividends (unless the trustees determine that monthly dividends are not feasible, in which case dividends would be paid quarterly). Any taxable income remaining after the distribution of the final regular monthly dividend each year, excluding our Retained Earnings, is distributed together with the first regular monthly dividend payment of the following taxable year or in a special dividend distributed prior thereto. The dividend policy is subject to revision at the discretion of the Board of Trustees. All distributions are made by us at the discretion of the Board of Trustees and depend on our taxable earnings, our Retained Earnings, our financial condition, maintenance of our REIT status and such other factors as the Board of Trustees deems relevant.

Distributions to shareholders are generally subject to taxation as ordinary income, although a portion of those distributions may be designated by us as capital gain or may constitute a tax-free return of capital. Although we do not intend to declare dividends that would result in a return of capital, we did so from 1997 through 2005 and in 2008. Any distribution to shareholders of income or capital assets from us is accompanied by a written statement disclosing the source of the funds distributed. If, at the time of distribution, this information is not available, a written explanation of the relevant circumstances accompanies the distribution and the written statement disclosing the source of the funds is distributed to the shareholders not later than 60 days after the close of the fiscal year in which the distribution was made. In addition, we annually furnish to each of our shareholders a statement setting forth distributions during the preceding year and their characterization as ordinary income, capital gains, or return of capital.

We began making distributions to our shareholders on September 29, 1997. Monthly distributions have continued each month thereafter. At year-end 2008 we had paid 136 consecutive monthly dividends. Distributions for the years ended December 31, 2008, 2007, and 2006 were made at a rate of 6.8% ($1.35), 7.4% ($1.47), and 7.0% ($1.40), respectively. The dividend portion of the distribution was 5.2% ($1.04), 7.4% ($1.47), and 7.0% ($1.40), per weighted share for 2008, 2007, and 2006, respectively. The portion of these distributions that did not represent a dividend represented a return of capital.

ITEM 6. SELECTED FINANCIAL DATA.

We present below selected financial information. We encourage you to read the financial statements and the notes accompanying the financial statements in this Annual Report. This information is not intended to be a replacement for the financial statements.

| | |

| | | | | | |

| | | | | |

Interest income from affiliate investments | | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

Weighted average shares outstanding | | | | | |

| | | | | | |

| | |

| | | | | | |

| | | | | |

| | | | | |

Investment in trusts receivable | | | | | |

Foreclosed residential mortgages and contracts for deed | | | | | |

Interim mortgages, affiliates | | | | | |

| | | | | |

Interim mortgages foreclosed | | | | | |

Allowance for loan losses | | | | | |

Line-of-credit receivable, affiliates | | | | | |

Line-of-credit receivable, non-affiliates | | | | | |

| | | | | |

Deficiency notes, affiliates | | | | | |

Recourse obligations, affiliates | | | | | |

| | | | | |

| | | | | |

| | | | | | |

| | | | | |

| | | | | |

Participation payable, affiliates | | | | | |

| | | | | |

| | | | | |

| | | | | | |

Total shareholders' equity | | | | | |

Total liabilities and shareholders' equity | | | | | |

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS OF THE COMPANY.

GENERAL

We invest (i) first lien secured interim mortgage loans with initial terms of 12 months or less for the acquisition and renovation of single-family homes, which we refer to as “Interim Loans”; (ii) secured, subordinate line of credit to UMTH Lending Company, L.P. for origination of Interim Loans; (iii) lines of credit and secured loans for the acquisition and development of single-family home lots, referred to as “Land Development Loans”; (iv) lines of credit and loans secured by entitled and developed single-family lots, referred to as “Finished Lot Loans”; (v) lines of credit and loans secured by completed model homes, referred to as “Model Home Loans”; (vi) loans provided to entities that have recently filed for bankruptcy protection under Chapter 11 of the US bankruptcy code, secured by a priority lien over pre-bankruptcy secured creditors, referred to as “Debtor in Possession Loans”, (vii) lines of credit and loans, with terms of 18 months or less, secured by single family lots and homes constructed thereon, referred to as “Construction Loans; and (viii) first lien secured mortgage loans with terms of 12 to 360 months for the acquisition of single-family homes, referred to as “Residential Mortgages”. We collectively refer the above listed loans as “Mortgage Investments”. Additionally, we our portfolio includes obligations of affiliates of our Advisor, which we refer to as “recourse loans.”

The typical terms for residential mortgages, contracts for deed and interim loans (collectively referred to as “mortgage investments”) are 360 months, 360 months and 12 months, respectively. The UDF line of credit has a five year term. Finished lot loans and builder model home loans are expected to have terms of 12 to 48 months. The majority of interim loans are covered by recourse agreements that obligate either a third party with respect to the performance of a purchased loan, or obligate a borrower that has made a corresponding loan to another party (the "underlying borrower"), to repay the loan if the underlying borrower defaults. Our loans to UDF are secured by the pledge of all of UDF’s land development loans and equity participations, and are subordinated to its bank lines of credit. In addition, as an enhancement, in October 2006, UDF III, a newly formed public limited partnership that is affiliated with UDF and with our Advisor, entered into a limited guaranty effective as of September 1, 2006, for our benefit (the “UDF III Guarantee”). Pursuant to the UDF III Guarantee, UDF III guaranteed the repayment of up to $30 million under the Second Amended and Restated Secured Line of Credit Promissory Note between United Mortgage Trust and UDF. This guarantee was released in 2008 as a result of UDF’s increased net worth.

We seek to produce net interest income from our mortgage investments while maintaining strict cost controls in order to generate net income for monthly distribution to our shareholders. We intend to continue to operate in a manner that will permit us to qualify as a Real Estate Investment Trust (“REIT”) for federal income tax purposes. As a result of that REIT status, we are permitted to deduct dividend distributions to shareholders, thereby effectively eliminating the "double taxation" that generally results when a corporation earns income (upon which the corporation is taxed) and distributes that income to shareholders in the form of dividends (upon which the shareholders are taxed).

At the end of 2008, our mortgage portfolio totaled approximately $99,827,000. Approximately 29% of our income producing assets were first lien secured interim mortgages and residential mortgages and contracts for deed, approximately 18% were secured, subordinate LOC to UMTH Lending Co., L.P., approximately 47% were land development loans, approximately 3% were invested in finished lot loans and approximately 3% were invested in construction loans. As noted above, our portfolio also includes obligations of affiliates of our Advisor, which we refer to as “recourse loans” and deficiency notes.

We no longer purchase Interim Loans that are secured by modular and manufactured homes. We increased our investment in our affiliated line of credit to UMTH Lending Co., L.P., secured by Interim Loans, by approximately $8,000,000 in the first quarter of 2009. We plan to invest in Residential Mortgages to facilitate the sale of homes securing our Interim Loans. We plan to invest in Construction Loans for the construction of new single family homes. We plan to continue to invest in Land Development Loans, Finished Lot Loans, and Model Home Loans because, 1) Land Development Loans and Finished Lot Loans have provided us with suitable collateral positions, well capitalized borrowers and attractive yields; and, 2) Model Home Loans and Construction Loans are expected to provide us with suitable collateral positions, well capitalized borrowers and attractive yields. Model Home and Construction Loans are expected to produce higher yields commensurate with Land Development Loans, Finished Lot Loans and the Subordinate Line of Credit secured by Interim Loans. As we phase out of non-affiliate Interim Loans we will increase the percentage of our portfolio invested in Land Development Loans, Finished Lot Loans. Model Home Loans, Debtor in Possession Loans, and Construction Loans, until market conditions indicate the need for an adjustment of the portfolio mix.

The following table summarizes mortgage loans by type and original loan size held by United Mortgage Trust at December 31, 2008.

| | | | | | Face amount of Mortgage (1) | Carrying amount of Mortgage (2) | |

Single family residential 1st mortgages and interim loans (4): | | | | | | | | |

Original balance > $100,000 | | | | | | | | |

Original balance $50,000 - $99,999 | | | | | | | | |

Original balance $20,000 - $49,999 | | | | | | | | |

Original balance under $20,000 | | | | | | | | |

| | | | | | | | | |

First Lien secured interim mortgages | | | | | | | | |

Ready America Funding (5) | | | | | | | | |

Howe Note Consolidation (6) | | | | | | | | |

| | | | | | | | | |

Secured, subordinate LOC to UMTH Lending Co., L.P. (5), (6) | | | | | | | | |

| | | | | | | | | |

| | | | | | | | |

UDF III Economic Interest Participation | | | | | | | | |

UDF III Bear Creek Participation | | | 12/31/09 | | | | | |

| | | | | | | | | |

| | | | | | | | |

| | | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | (1) | Current book value of loans. |

| | (2) | Net of mortgage allowance for loan losses on mortgage loans of $3,827,873 at December 31, 2008. |

| | (3) | Amounts greater than thirty (30) days past due. |

| | (4) | Does not include Rental Foreclosure Properties (18). |

| | (5) | Lines of credit with Ready America Funding and UMTH Lending Co., L.P. are collateralized by 18 and 173 loans, respectively |

| | (6) | The Company has a first lien collateral position in these loans funded by the originator. The advances to the originator do not have specific maturity dates. |

Below is a reconciliation and walk forward of mortgage loans, net of allowance for loan losses for the year ended December 31, 2008.

Balance at beginning of period | | $ | 82,060,938 | |

| | | | |

| | | 60,592,738 | |

| | | - | |

| | | | | |

| | | - | |

| | | (30,004,444 | ) |

| | | (15,165,108 | ) |

Other (net change of Allowance) | | | (1,484,710 | ) |

Balance at close of period | | $ | 95,999,414 | |

MATERIAL TRENDS

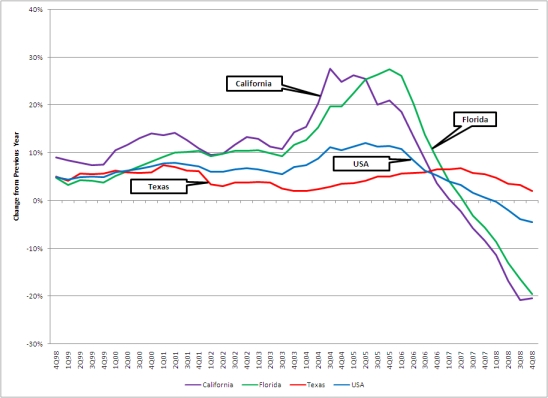

Housing Industry

The U.S. housing market has suffered declines in over the past three years, particularly in geographic areas that had experienced rapid growth, steep increases in property values and speculation. We believe that the demand for new homes continued to deteriorate progressively throughout 2008 and accelerated with the cascading events in credit and equity markets in September and October. Consumer confidence has sunk to historic lows. Market conditions remain challenging as many potential home buyers appear to have postponed the purchase of new homes until signs that the economy and employment are improving, or at least are not continuing to deteriorate. Our view is that the perspective of many potential home buyers has changed from “have home prices stabilized, and is this the right price at which to purchase a home?,” to “we will wait to purchase a home until such time as we are comfortable we are not going to lose our jobs.”

Material Trends Affecting Our Business

Nationally, the number of new single-family residential homes sold and average and median sales prices have been declining. The sales of new single-family residential homes in December 2008 were at a seasonally adjusted annual rate of 331,000 units, according to estimates released jointly by the U.S. Census Bureau and the Department of Housing and Urban Development. This is approximately 44.8% below the December 2007 estimate of 600,000. According to the same sources, the average sales price of new houses sold in 2008 was $291,800; the median sales price was $230,600. This is approximately 6.95% below the 2007 average new home sales price of $313,600. In addition, the median sales price is approximately 6.98% below the 2007 median new home sales price of $247,900. The seasonally adjusted estimate of new houses for sale at the end of December 2008 was 357,000, which represents a supply of 12.9 months at the December 2008 sales rate. We believe that this significant drop in the number of new houses for sale, year-over-year, by an estimated 137,000 units reflects the homebuilding industry’s extensive efforts to bring the new home market back to equilibrium by continuing to reduce new housing starts and selling existing new home inventory. We continue to believe that housing inventories will continue to fall until they reach between 350,000 and 375,000 units in the first half of 2009, a point we believe will mark a tightened housing market. We further believe that new home inventories are at or close to equilibrium and that what is necessary to regain prosperity in housing markets is the return of healthy levels of demand.

Also, according to the sources identified above, new single-family residential home permits and starts have declined nationally, as a result and in anticipation of a rising supply of new single-family residential homes and a declining demand for new single-family residential homes. Single-family homes authorized by building permits in December 2008 were at a seasonally adjusted annual rate of 363,000 units. This is 49.2% below the December 2007 estimate of 714,000 units. Single-family home starts for December 2008 were at a seasonally adjusted annual rate of 398,000 units. This is 48.9% below the December 2007 estimate of 779,000 units.