Investor Presentation

April 2007

Saxon

IMPORTANT INFORMATION AND IRS CIRCULAR 230 NOTICE

This material has been prepared for information purposes to support the promotion or marketing of

the transaction or matters addressed herein. This is not a research report and was not prepared by the

Morgan Stanley research department. It was prepared by Morgan Stanley sales, trading, banking or

other non-research personnel. This material was not intended or written to be used, and it cannot be

used by any taxpayer, for the purpose of avoiding penalties that may be imposed on the taxpayer

under U.S. federal tax laws. Each taxpayer should seek advice based on the taxpayer’s particular

circumstances from an independent tax advisor. Past performance is not necessarily a guide to future

performance. Please see additional important information and qualifications at the end of this

material.

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the SEC for the offering

to which this communication relates. Before you invest, you should read the prospectus in that

registration statement and other documents the depositor has filed with the SEC for more complete

information about the issuer and this offering. You may get these documents for free by visiting

EDGAR on the SEC web site at www.sec.gov. Alternatively, the depositor or any underwriter or any

dealer participating in the offering will arrange to send you the prospectus if you request it by calling

toll-free 1-866-718-1649.

Important Notice

Information presented is for the period 12/1/2006 to 2/28/2007 unless otherwise stated

FORWARD LOOKING STATEMENTS

We have included in this document, and from time to time may make in other public statements, certain statements that may

constitute forward-looking statements. These forward-looking statements are not historical facts and represent only our

beliefs regarding future events, many of which, by their nature, are inherently uncertain and beyond our control.

The nature of our business makes predicting future trends difficult. The risks and uncertainties involved in our business could

affect the matters referred to in such statements and it is possible that our actual results may differ from the anticipated results

indicated in these forward-looking statements. Important factors that could cause actual results to differ from those in the

forward-looking statements include (without limitation):

decreases in residential real estate values, which could reduce both the credit quality of our mortgage loan portfolio and the

ability of borrowers to use their home equity to obtain cash through mortgage loan refinancing, which would adversely

impact our ability to produce new mortgage loans;

changes in overall regional or local economic conditions or changes in interest rates, particularly those conditions that affect

demand for new housing, housing resales or the value of houses;

our ability to successfully implement our growth strategy throughout the various cycles experienced by our industry;

greater than expected declines in consumer demand for residential mortgage loans, particularly sub-prime, non-conforming

loans;

our ability to sustain loan production growth at historical levels;

continued availability of financing facilities and access to the securitization markets or other funding sources;

deterioration in the credit quality of our loan portfolio and the loan portfolios of others serviced by us;

challenges in successfully expanding our servicing platform and technological capabilities;

increased competitive conditions or changes in the legal and regulatory environment in our industry; and

other risks and uncertainties detailed in this document and in other filings with the Securities and Exchange Commission.

Accordingly, you are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date on

which they are made. We undertake no obligation to update publicly or revise any forward-looking statements to reflect the

impact of circumstances or events that arise after the dates they are made, whether as a result of new information, future

events or otherwise except as required by applicable law. You should, however, consult further disclosures we may make in

future filings with the Securities and Exchange Commission.

Important Notice

Information presented is for the period 12/1/2006 to 2/28/2007 unless otherwise stated

Table of Contents

Initiatives and Program Changes

Section 5

Servicing

Section 6

Production

Section 4

Growth Strategy

Section 3

Organizational Structure

Section 2

Morgan Stanley’s Acquisition of Saxon

Section 1

Morgan Stanley’s Acquisition of Saxon

Section 1

Synergies Overview

Strong

Credit

Culture

Sophisticated

Trading/Risk

Transfer

Capabilities

Risk

Management

Structuring

Expertise

Origination

Capabilities

Servicing

Capabilities

Key Success Factors

Morgan Stanley’s Strengths

Saxon’s Strengths

Saxon compliments

Morgan Stanley’s

overall mortgage

business

Morgan Stanley’s Acquisition of Saxon

Organizational Structure

Section 2

Organizational Structure

Saxon Senior Management

Saxon

Kevin Rodman (MS)

Managing Director

Co-head, US Residential Mortgage Business

20+ years exp

Chief Admin Officer

Kevin Norris

(MS)

20+ years exp

Capital Markets

Ernie Bretana, EVP

(SMI)

10+ years exp

Servicing

David Dill, President

(SMSI)

20+ years exp

Production

Wes Iseley, President

(SMI)

25+ years exp

Michael Dubeck (MS)

Managing Director

Co-head, US Residential Mortgage Business

20+ years exp

Growth Strategy

Section 3

The Next Five Years

Production objectives over the next five years:

Grow origination volumes

Offer a broader selection of residential mortgage product offerings

Reduce origination costs

Add scale in lower CTP (Cost to Produce) channels, increase loan

sizes, etc.

Servicing objectives over the next five years:

Improve servicer ratings

Expand servicing platform

Build Special Servicing platform

Expand servicing product capabilities (for example: HELOCs and Option

Arms)

Invest in technology to improve efficiencies

Key benefits of vertical

integration include:

Strong origination base

Scaleable servicing

platform

Growth Strategy

Production

Section 4

Current Business Profile (as of February 28, 2007)

Saxon employs over 392

production staff, including

approximately 176 Account

Executives and

approximately 216

operations and

management staff

Originate loans in 50 states

plus Washington, DC

Top 5 states of loan

production for the period

Dec 1, 2006-Feb 28, 2007:

CA, MD, FL, NY, VA

Regional Loan production

office in CA, TX, VA &

FL (as of April 2, 2007)

Production

Tampa,

Florida (as of

April 2, 2007)

Production Volume by Channel

Production

100.00%

100%

100%

100%

100%

100%

100%

16.5%

8.2%

0.0%

0.0%

0.0%

0.0%

0.0%

Conduit

0.00%

0.5%

5.6%

5.2%

7.2%

10.2%

24.2%

Correspondent -

Bulk

22.30%

23.0%

28.0%

24.3%

24.6%

16.6%

15.2%

Correspondent -

Flow

16.40%

19.8%

21.3%

27.6%

26.8%

28.1%

19.2%

Retail

44.80%

48.6%

45.1%

42.9%

41.3%

45.1%

41.4%

Wholesale

$0.94

$3.35

$3.35

$3.49

$2.84

$2.30

$2.33

Volume ($B)

1st Qtr 2007*

2006

2005

2004

2003

2002

2001

*First Quarter 12/1/2006-2/28/2007

Production Profile (for the period Dec 1, 2006-Feb 28, 2007)

Production

Documentation Type *

Credit Score Distribution

WA Credit Score

LTV/CLTV

Production Profile Contd. (for the period Dec 1, 2006-Feb 28, 2007)

Production

Product

Top 5 States Funded Volume YTD

Purpose

53.51%

503,880,652

5.68%

53,530,544

VA

6.30%

59,341,216

NY

10.31%

97,084,231

FL

10.86%

102,244,322

MD

20.36%

191,680,339

CA

Percent

Loan Amount - Original

State

Occupancy

Initiatives and Program Changes

Section 5

Initiatives – Quality Enhancements

Completed Initiatives

Sales - implemented a new, performance based compensation plan

Pricing - tiered adjustments and layered risk adjustments

Underwriting – guideline changes including greater restrictions on first-time homebuyers

Collateral evaluation procedures incorporating History Pro risk analysis and AVM

Offsite Management Workshop focused on production center organizational structure and

work flows

Verbal verification of employment procedures

Future Initiatives

Underwriting

Underwriter training, certification program and annual assessments

Fraud training (borrower and property)

Purchase transaction fraud review and stated income reasonableness test

Property Valuation

Implementation of MARS

In-house appraisal review group with licensed appraisers

Fraud & Quality Control

Update risk analysis review

Broker Channel Management – enhancing new business partner screening and relationship

monitoring

Additional pre-funding QC requirements (risk based) and revamping of post funding QC

selections and reporting

Mavent system to automate regulatory risk management

ClosingProtectionLetter.com to verify status of title agent and wire information

Production

Highlights of Guideline Changes (effective April 11, 2007)

Guideline Changes and Loan Programs

Maximum LTV

First Time Home Buyers

Reserves/Other

Minimum Product Score

85

100

Stated

90

100

Limited

90

100

12 mo. Bank statement

95

100

Full/24 mo. Bank statement

NEW

OLD

550

500

General Minimum

575

500

50/30

Not

Offered

600

80/20

550

500

40/30

600

560

I/O Stated

580

560

I/O Full

NEW

OLD

4 (purch) /

3 (refi)

2

Min. Credit -#

Open Accts

2 months

N/A

Stated/Limited

Bal>$500k

2 months

>90 LTV

2 months

>95 LTV

Stated/Limited

W-2

2 months

>= 95 LTV

N/A

Full/12 months

NEW

OLD

If Stated

& >80

LTV, 2

months

If Stated&

> 95 LTV

2 months

Reserves

36

months

1 day to 24

months

Bk Discharge

Not

offered

100

Maximum LTV – Stated

95@

600+

100

Maximum LTV – Full

575

500

Minimum Score

NEW

OLD

Primary Product Overview (effective April 11, 2007)

Max 50%

Max 55% if LTV<=80, else 50%

DTI

3 months PITI if >500K,

else 2 months PITI;

sourced & seasoned 60

Days

Full/12 month: 2 months PITI if

LTV >=95; Limited/stated W2: 2

months PITI if LTV >90; sourced &

seasoned 60 days

Cash Reserves

24 months from discharge

6 months if score >=600; else varies

by LTV from discharged >2 years to

simply discharged

Bankruptcy

History – 11/13

24 months from discharge

6 months if score>=600; else varies

by LTV from discharged > 2 years

to simply discharged

Bankruptcy

History – Ch7

3 years

2 years if score >=600 and CLTV

<=90; else 3 years

Foreclosure

History

0x30

Max delinquency 1x90 in the last 12

months

Mortgage History

Middle of three

Middle of three

Credit Score –

Selection

620

550

Min Credit Score

ScorePlus2

Score Plus (Full Doc & 12 mo

Bank statements)

Guideline Changes and Loan Programs

FICO Distribution by Program

(for the period Dec 1, 2006-Feb 28, 2007)

667

611

WA

Score

0.00%

0.02%

801 -

850

0.89%

0.81%

751 -

800

10.26%

3.65%

701 -

750

60.16%

16.73%

651 -

700

28.69%

38.52%

601 -

650

0.00%

30.61%

551 -

600

0.00%

9.54%

501 -

550

0.00%

0.11%

451 -

550

Score

Plus 2

Score

Plus

Guideline Changes and Loan Programs

Servicing

Section 6

Ratings (as of March 31, 2007)

RSS2+

Residential Mortgage Special Servicer

RPS2+

Residential Mortgage Sub-prime Servicer

Fitch

Average

Residential Mortgage Special Servicer

Above Average

Residential Mortgage Sub-prime Servicer

S&P

SQ2

Special Servicer of Sub-prime Loans

SQ2+

Primary Servicer of Sub-prime Loans

Moody's

Rating

Category

Agency

Current Servicer Ratings

Key initiative is to

improve ratings from

each rating agency

Servicing

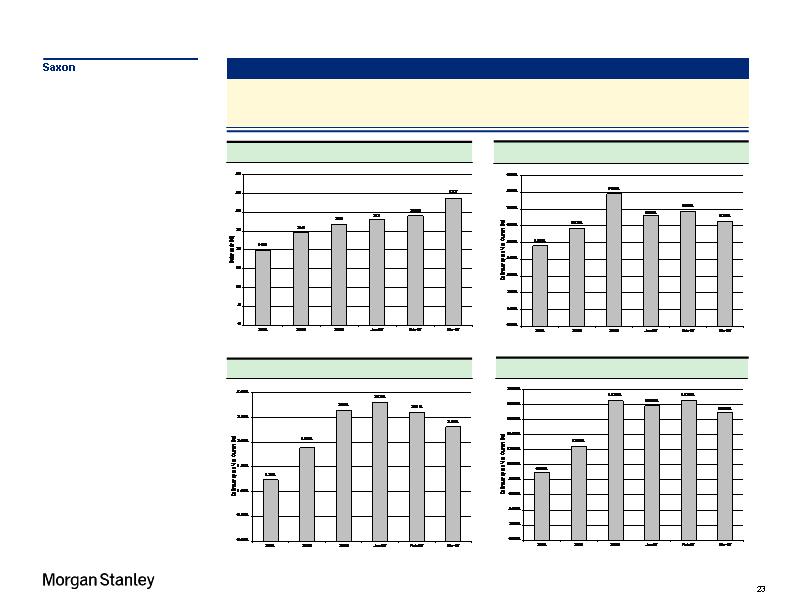

Servicing Portfolio Summary (as of March 31, 2007)

Servicing Portfolio Balance

Total Delinquency Trend

60 Day Delinquency Trend

30 Day Delinquency Trend

Servicing

Geographic Servicing Concentration (as of Dec 31, 2006)

Top 5 states equal approximately 50% of servicing portfolio

Top Five States

(Approx % of Total Portfolio)

1. California 26.35%

2. Florida 10.19%

3. New York 4.62%

4. Texas 4.53%

5. Maryland 4.01%

Servicing

Servicing Department Overview (as of Dec 31, 2006)

Customer Service/Early Collections

Loans per FTE: 1,011

Teams of 8-10 representatives, all reps handle inbound and outbound

service and collection calls (answer rate: 97.58%)

Welcome calls

ARM change/escrow change notification:

Letters: sent both 45 days prior to change and within the monthly bill

which arrives approximately 15 days prior to impacted due date

Calls: initiated 1 month prior to payment change date and within first few

days of the month of the payment change

Call center resolution desk – to handle customer escalation issues

Call center operations – statistical analysis (coverage, contacts, success) and

dialer setup/strategy

Predictive Modeling – calling campaigns using FHLMC EIS on entire 0-59

portfolio

High risk (2nd day of delinquency); low risk (17th day of delinquency)

Special collections unit for large balance, EPD or no contact loans

Early mitigation/repayment plans – 4 months or less/max 2 in 12 months

Cure Ratios

(for the period Oct 1, 2006-

Dec 31, 2006)

1-29 days: 94.06%

30-59 days: 73.52%

Servicing

Servicing Department Overview Continued

(as of Dec 31, 2006)

Loss Mitigation

Cure delinquencies in the 60+ category through collection and workout options

Target staffing: 135 loans/FTE, Actual staffing: 153 loans/FTE

60 day team: high contact collections with goal of full reinstatement with use of pre-

foreclosure/short-term prepayment and plans and identifying candidates for alternative

workouts

Collection/Workout Teams (7): focus on alternatives to foreclosures (Collection,

Forbearance/repayment plans, modifications, short sales and assumptions, deeds-in-

lieu)

Loan Recovery Specialist: orphan 2nd lien monitoring, collections and charge-offs

Workout team Administration: workout team oversight, resolution approval &

execution/completion

Loan Review Team: supports DRP, BPO orders, property preservation, and insurance

claims

90+ day east/west team: primarily a post-foreclosure resolution team, manual calling,

letters skip tracing

Predictive Modeling with FHLMC/EIS – focus on higher risk delinquencies delay

foreclosure on lower risk borrowers

EIS below 200 refer at 76 days past due, EIS above 200 refer at 90 days past due

Titanium Solutions – 3 rd party face-to-face contact solution for no contact loans,

submission of financial packages (approximately 42% success rate)

Servicing

Servicing Department Overview Continued

(as of Dec 31, 2006)

REO

Assets are managed from Foreclosure Sale or Deed-in-Lieu through each

step of the disposition process: Redemption periods, evictions, available for

sale, listed, under contract, liquidation

Disposal of REO assets outsourced to three national REO asset management

companies:

First American REO

Fidelity National Asset Management

NRT Inc., a division of Coldwell Banker

Assignments based on an even distribution of loan count, UPB and

geography

Delegated authority matrix for establishing value, list price, reductions to

price and contract acceptance

Expenses carried by outsourcer until liquidation

Performance tracking via outsourcer report cards and annual audits

REO Performance (for

the period Jan 1, 2006-

Dec 31, 2006)

Turn Rate 19%

SP to FMV 96%

Days on Mkt 116

Servicing

Method of Cure Overview (as of Dec 31, 2006)

Servicing

10.77

13.47

12.14

150+ Days

Cure Rates based on UPB

120-149 Days

90-119 Days

60-89 Days

Cure Rates

19.93

25.19

26.44

30.61

39.19

44.04

49.24

54.33

58.38

2006

2005

2004

Assess customers ability and willingness to pay:

Financial packages obtained

Review of credit score, Freddie Mac Early Indicator Score (EIS) score and reason for

default

A BPO is obtained and an estimate of total recovery is determined based on historical

foreclosure and REO timelines & expenses.

Using Saxon’s Default Resolution Plan (DRP) System, a loss mitigation decision is made

to deliver the best economical outcome for the customer and investor.

If a repayment plan is used, Saxon requires that the customer be committed.

Commitment is measured by ability to contribute 30-50% of the outstanding delinquency

upfront.

A customer’s EIS score is one of the determining factors as to the amount of down

payment required coupled with customer’s recent payment history/broken plans.

Method of Cure Plan Summary

Servicing

Informal Repayment Plans

Modification

Stipulated to Modification Plan

Formal Repayment Plans

Pre-Foreclosure Referral

Verbal Agreement

General Term of Repayment: 4-7

months

Requires larger down payment (30-50%

of delinquency)

Contractually delinquent until customer

catches up on payments

Post-Foreclosure Referral

Legal Agreement

General Term of Repayment: 7-18

months or any customer having two

broken plans in the last 12 months

Contractually delinquent until borrower

catches up on payments

A modification test case which may be

used prior to an actual modification of

the borrowers loan terms

Enables Saxon to determine the

customer’s willingness to continue

payments if loan is modified

Implemented on a short term basis (3

months)

Allows cash flow without a worsening

delinquency status

A permanent change to original loan

terms – delinquency is cured upon

execution.

Do not extend maturity except where

allowed by PSA

Increases to principal balance cannot

exceed original debt

Rate reductions - generally step back up

by 25 bps every 6 months (or under

present ARM change schedule) until

reach original rate.

Reported on remittance tape

Deal Information Source

Reg AB static pool data can be found at

www.saxonmortgage.com/staticpool.

Underwriting guidelines, matrices and product profiles can

be found at www.esaxon.com/wholesale/index.jsp (under

Matrices).

Securitization program (SAST) information can be found at

www.saxonmortgage.com (click on the Securitization link).

Information available includes:

Pricing information and the prospectus for our

transactions

Remittance statements and transaction profile reports

Monthly CPR analysis and actual vs. pricing CPR

Quarterly loss reports and loss severity report

Prepayment penalty collection and roll rate

information

Corporate presentations

Servicing