Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07739

Harding, Loevner Funds, Inc.

(Exact name of registrant as specified in charter)

400 Crossing Boulevard

Fourth Floor

Bridgewater, NJ 08807

(Address of principal executive offices) (Zip code)

Owen T. Meacham

The Northern Trust Company

50 South LaSalle Street

Chicago, IL 60603

With a copy to:

Stephen H. Bier, Esq.

Dechert LLP

1095 Avenue of the Americas

New York, NY 10036

(Name and address of agent for service)

Registrant’s telephone number, including area code: (877) 435-8105

Date of fiscal year end: 10/31

Date of reporting period: 04/30/2018

Table of Contents

Item 1. Reports to Stockholders.

Table of Contents

Table of Contents

⬛ HARDING LOEVNER FUNDS

Global equity investing for institutions is Harding Loevner’s exclusive focus. Through Harding Loevner Funds it offers distinct global strategies based on its quality-and-growth investment philosophy. It seeks to purchase shares of growing, financially strong, well-managed companies at favorable prices. Harding Loevner manages each of the Funds’ Portfolios according to a disciplined, research-based investment process. It identifies companies with sustainable competitive advantages and assesses the durability of their earnings growth by conducting in-depth fundamental research into global industries. In constructing portfolios, Harding Loevner diversifies carefully to limit risk.

⬛ RECEIVE INVESTOR MATERIALS ELECTRONICALLY

Shareholders may sign up for electronic delivery of investor materials. By doing so, you will receive the information faster and help us reduce the impact on the environment of providing these materials. To enroll in electronic delivery,

| 1. | Go to http://www.icsdelivery.com |

| 2. | Select the first letter of your brokerage firm’s name. |

| 3. | From the list that follows, select your brokerage firm. If your brokerage firm is not listed, electronic delivery may not be avail-able. Please contact your brokerage firm. |

| 4. | Complete the information requested, including the e-mail address where you would like to receive notifications for electronic documents. |

Your information will be kept confidential and will not be used for any purpose other than electronic delivery. If you change your mind, you can cancel electronic delivery at any time and revert to physical delivery of your materials. Just go to http://www.icsdelivery.com, perform the first three steps above, and follow the instructions for cancelling electronic delivery. If you have any questions, please contact your brokerage firm.

Table of Contents

Table of Contents

|

| |||

|

| |||

| ||||

International Small Companies Portfolio

| ||||

| ||||

Frontier Emerging Markets Portfolio

| ||||

|

Global Equity Research Portfolio

| |||

International Equity Research Portfolio

| ||||

Emerging Markets Research Portfolio

| ||||

Contact

Harding, Loevner Funds, Inc.

c/o Northern Trust

Attn: Funds Center C5S

801 South Canal Street

Chicago, IL 60607

Phone: (877) 435-8105 | ||

Fax: (312) 267-3657 | Must be preceded or accompanied by a current Prospectus. | |

www.hardingloevnerfunds.com | Quasar Distributors, LLC, Distributor |

Table of Contents

| DAVID LOEVNER, CFA, CIC CHAIRMAN OF THE FUNDS AND CEO OF THE ADVISER | |||||

SIMON HALLETT, CFA CO-CIO OF THE ADVISER

| ||||||

FERRILL ROLL, CFA CO-CIO OF THE ADVISER |

Investing successfully is difficult. How do you improve? The process is captured nicely in a Latin phrase: Succisa Virescit—“Having been cut down, it grows up strong again.” It speaks to the notion that you will make mistakes that set you back, but, by having the courage and humility to embrace them, you make yourself better. In investing, mistakes occur in the course of making decisions every day, whether markets are steady, booming, or collapsing. Continuous study of your own mistakes and the mistakes of others can help you continuously improve.

Ten years have passed since the peak of the global financial crisis (GFC), and last October marked the thirtieth anniversary of Black Monday. Both terrifying events interrupted long periods of market tranquility. Both unleashed emotions that affected decision-making. Both provided opportunities for investors to err and to learn. The current stretch of relatively tranquil markets means that those who started investing after 2009 may not have developed the scar tissue that comes with living through a market crash. Given the importance of these events to the investors who experienced them, we thought a reflection on mistakes and the lessons we learned—in times of crisis and quotidian times—would be a worthy subject of this letter.

An early lesson we learned was to be wary of financial “innovation.” While “proven” safe in backtesting, complex new financial strategies can reveal previously unimagined faults under the stress of reality. The sell-off in markets in 1987 was exacerbated by one such innovation, called “portfolio insurance.” Its promoters offered to indemnify institutional investors against losses from a large fall in the stock market. They avouched that institutional investors who purchased insurance could own more equities without unacceptable risk. The product became very popular. However, investors, insurers, and regulators alike failed to recognize how its popularity would undermine its effectiveness. To hedge their obligations, the insurers needed to sell stock index futures programmatically as the stock market fell. On Black Monday, with the stock market declining, they found few willing buyers for the futures contracts they attempted to sell. The futures buyers, in turn, hedged their exposure by selling equities into the falling market. The result: a vicious vortex that fed upon itself. The S&P 500 Index fell 21% that day—still the largest single-day percentage decline in its history. The Hong Kong market closed for nearly a week, then dropped more than 40% when it reopened. The insurers were unable to fulfill their promises, and investors suffered heavy losses that many could ill afford.

Twenty years later, the market repeated the lesson: when investors buy an esoteric financial product, they need to understand what they are buying, especially the fundamental sources of the underlying cash flows including those to counterparties, and to view skeptically the guarantees of others. In the lead up to the GFC, the underwriters of securitized sub-prime mortgages convinced the ratings agencies and investors in collateralized debt obligations (CDOs) that, if numerous mortgages were pooled together to diversify away such risk factors as credit worthiness and regional concentration, and their repayment cash flows assembled into a priority waterfall of “tranches,” the senior-most tranches—those engineered to have the first claim on repayments—would be insulated from defaults to be anticipated on the underlying mortgages and were therefore worthy of “AAA” credit ratings. This logic proved flawed. As the real estate bubble inflated throughout the country, large mortgages were increasingly given to borrowers lacking the wherewithal to repay them. By 2006–07, diversification turned into a mirage. Pools became dominated by low-quality mortgages whose default rates were far higher than anticipated and whose repayments in many cases were inadequate even to satisfy the senior tranches. Banks and institutional investors didn’t buy just the new products—they also bought into a false promise of security.

Extraordinary market events like Black Monday and the GFC also reminded investors never to be complacent—the unexpected can happen at any time and have a greater intensity than they could ever imagine. In such situations, companies with the strongest balance sheets are best able to withstand periods when debt and equity markets are closed for financing, and all but non-discretionary spending largely ceases. From 2002 until 2007, for example, the world had enjoyed economic growth and tranquil markets. But nothing lasts forever. Between the collapse of Bear Stearns in early 2008 and the start of the market rally in early 2009, the S&P 500 lost nearly 50% of its value. The US economy contracted at an 8% rate in the fourth quarter of 2008 and at over 5% in the first quarter of 2009.

Another lesson made clear in times of crisis is that the best values occur when others are forced to liquidate. Investors, too, must have their own strong balance sheets and be prepared (financially and psychologically) to remain calm when panic strikes to take advantage of bargains. It is emotionally difficult to buy when all about you are screaming “sell,” as we are hardwired as humans to run with the crowd. In such times investors should want to be providers of liquidity, not seekers of it.

Black Monday and the GFC afford lessons to all investors open to improvement. But crises aren’t the only powerful teachers. Mistakes that are uniquely our own can be effective tutors. In 2003–04, for example, our International Equity Portfolio dramatically underperformed its benchmark. During the dot-com bust in 2000–02, we sought shelter with a significant weight in exceptionally high-quality, stable-growth businesses—e.g. Nestlé, Heineken, Air

Table of Contents

Liquide. Coming out of the bust, such businesses were as cheap as they had ever been in our investing experience, and we added to them in 2003–04 even as the market rallied. Events would reveal that nearly all equities were cheap at that time, and anything with a cyclical or an emerging-market exposure was really cheap. And that is what we should have owned and could have owned, but did not, to our clients’ detriment.

We analyzed our relative performance to understand why it was so poor in 2003–04. Two facts emerged: we faced a style headwind—e.g., the companies with the strongest balance sheets (where we already had a large weight by 2002) significantly underperformed the most indebted businesses, and our transactions adding to secular, instead of economically sensitive, growth in the period detracted over 800 basis points in performance relative to our benchmark.

The two immediate lessons we took away from this humbling experience were to place greater importance on valuation and to keep firmly in mind that what we didn’t own could hurt us (opportunity costs matter!). The scarring experience of 2003–04 taught us useful ways to navigate the extreme volatility of 2008–09. For example, our International Equity Portfolio outperformed during the terrible decline of 2008 partly due to its large overweight in the defensive Health Care sector. The Portfolio then outperformed during the sharp recovery in 2009, helped by our decision early that year to cut our Health Care weight on valuation grounds (everything was cheap) and our concerns about the impact of proposed US policy changes on the industry. We redeployed that capital into economically sensitive Industrials, Consumer Discretionary, and Information Technology companies (which were really cheap).

The experience of 2003–04 also confirmed our long-standing belief that an effective investment process requires a work environment where people feel safe in taking well-considered risks without fear of recrimination if things do not turn out as hoped. Transparency is critical for an investment team to learn and improve. During 2004, we strengthened our processes for capturing and analyzing our investment team’s actions. We also enhanced our procedures for sharing our findings internally with the stated goal of learning, not punishing. As one example, each quarter we encourage our portfolio managers to analyze their purchase and sale decisions of a year earlier and their rationales to see what they got right and wrong. Also, each year our analysts publish reviews of their biggest contributors and detractors to their individual performance in hope that patterns of behavior, both good and bad, will be recognized for the benefit of themselves and their colleagues.

Beating the market is an immensely difficult endeavor. Mistakes are inevitable. But mistakes identified, acknowledged, and dissected—whether they are made by you or others—can provide valuable insights that will help you make better decisions. Learning from your own mistakes is neither easy nor painless, and it cannot be done alone. But it will help you grow stronger. And, as we have found, learning from the mistakes of past crises and our daily work can also reduce the frequency of mistakes in the future.

Thank you for your support and your trust.

Sincerely, | ||||

|  |  | ||

| David R. Loevner, CFA, CIC | Simon Hallett, CFA | Ferrill D. Roll, CFA | ||

Opinions expressed are those of Harding Loevner and are not intended to be forecasts of future events, a guarantee of future results, nor investment advice. Please read the separate disclosure page for important information, including the risks of investing in the Portfolios. Past performance is not a guarantee of future results.

Table of Contents

PORTFOLIO MANAGEMENT TEAM

| ||

PETER BAUGHAN, CFA | SCOTT CRAWSHAW | |

| CO-LEAD PORTFOLIO MANAGER | PORTFOLIO MANAGER | |

FERRILL ROLL, CFA | CHRISTOPHER MACK, CFA | |

| CO-LEAD PORTFOLIO MANAGER | PORTFOLIO MANAGER | |

RICHARD SCHMIDT, CFA | ||

| PORTFOLIO MANAGER | ||

⬛ PERFORMANCE SUMMARY

For the Global Equity Portfolio, the Institutional Class rose 5.57%, the Institutional Class Z rose 5.61%, and the Advisor Class rose 5.46% (net of fees and expenses) in the six-month period ended April 30, 2018. The Portfolio’s benchmark, the MSCI All Country World Index, gained 3.56% (net of source taxes).

FUND FACTS at April 30, 2018

| ||||||||||||

TOTAL NET ASSETS

|

| $832.4M | ||||||||||

SALES CHARGE

|

| NONE | ||||||||||

NUMBER OF HOLDINGS

|

| 74 | ||||||||||

TURNOVER (5 YR. AVG.)

|

| 33% | ||||||||||

REDEMPTION FEE

|

| 2% FIRST 90 DAYS | ||||||||||

DIVIDEND POLICY

|

| ANNUAL | ||||||||||

| INSTITUTIONAL INVESTORS | INDIVIDUAL INVESTORS | |||||||||||

| INSTL CLASS | INSTL CLASS Z | ADVISOR CLASS | ||||||||||

TICKER

| HLMVX | HLGZX | HLMGX | |||||||||

CUSIP

| 412295602 | 412295727 | 412295206 | |||||||||

INCEPTION DATE

| 11/3/2009 | 8/1/2017 | 12/1/1996 | |||||||||

MINIMUM INVESTMENT1

| $100,000 | $10,000,000 | $5,000 | |||||||||

NET EXPENSE RATIO

| 0.93% | 0.90%2 | 1.14% | |||||||||

GROSS EXPENSE RATIO | 0.93% | 1.21% | 1.14% | |||||||||

1Lower minimums available through certain brokerage firms; 2Shown net of Harding Loevner’s contractual agreement through February 28, 2018.

⬛ MARKET REVIEW

Markets closed 2017 on an optimistic note, with stock prices rising strongly in December. Economic growth across all major regions remained positive and synchronized, while inflation was subdued. In the US, investors ignored the Federal Reserve’s signals of further interest rate increases, including a hike in mid-December. They weighed approvingly the expected future benefits of lower corporate tax rates from tax legislation, which finally passed in late December. In Europe, the European Central Bank remained accommodative on monetary policy, although it signaled a slowing pace of bond buying. China’s economy gathered momentum, shrugging off concerns over government corruption crackdowns and shaky property loans, with positive pull-through effects on its trading partners. Japanese economic growth edged higher, while inflation remained positive—a critical policy goal.

The markets’ positive trend continued into the new year, but the streak of 15 monthly gains ended in February as sanguinity gave way to worry. Although the backdrop of improving and increasingly synchronized economic growth and good corporate earnings remained in place, investors had to come to terms with some ugly prospects: higher interest rates, a trade war between the US and China, and increased regulation of technology companies.

Stock price volatility spiked at the end of January, exacerbated by the collapse of derivatives-based “inverse volatility” ETFs, contributing to an over 8% decline in equities in just 10 days. After a brief bounce in mid-February, stocks wallowed in a range through the end of April, reflecting a new set of worries about increasingly ubiquitous technology platforms. A mounting furor over

Facebook data illicitly exploited by political consultant Cambridge Analytica in favor of US President Donald Trump and Brexit, and the mowing down of a pedestrian by an Uber self-driving car in Arizona drew calls for more regulation of technology companies. The European Union continued its efforts to rein in “big tech,” announcing a tax on turnover of large digital companies and moving ahead with its General Data Protection Regulation mandate, which imposes strict requirements and stiff penalties regarding treatment of private data. The tech tumult turned farcical with Trump tweeting potshots at Amazon.com over its use of the Postal Service.

All sectors except Utilities and Consumer Staples advanced in the period. Energy was the top-performing sector, as crude oil prices reached levels in April not seen since the end of 2014. Information Technology (IT) moderately outpaced the index; its outsized January gains were nearly depleted by sharp declines late in March.

All regions except Canada advanced as well. Emerging Markets (EMs), more typically the loser from rising global risk and volatility, was the strongest-performing region. Confoundingly, EMs’ rise was supported by Brazil and Russia, two of the biggest exporters of steel and other commodities whose trade is endangered. A Brazilian court upheld the conviction of former president Luiz Inácio Lula da Silva on corruption charges, likely precluding him from running again and restoring his redistributionist policies.

The most expensive and fastest-growing quintiles of stocks gained in the period, outperforming the rest by a wide margin. Quality was not a significant return factor.

Table of Contents

PERFORMANCE (% TOTAL RETURN)

for periods ended March 31, 2018 |

for periods ended April 30, 2018

| |||||||||||||||||||||||||||

1 | 3 | 5 | 10 | SINCE INCEPTION* | 1 | 3 | 5 | 10 | SINCE INCEPTION* | |||||||||||||||||||

| YEAR | YEARS | YEARS | YEARS | Nov-09 | Aug-17 | Dec-96 | YEAR | YEARS | YEARS | YEARS | Nov-09 | Aug-17 | Dec-96 | |||||||||||||||

GLOBAL EQUITY PORTFOLIO – INST CLASS

| 23.40 | 12.13 | 12.03 | – | 11.05 | 19.07 | 11.16 | 11.56 | – | 10.85 | ||||||||||||||||||

GLOBAL EQUITY PORTFOLIO – INST CLASS Z

| – | – | – | – | 10.35 | – | – | – | – | 9.62 | ||||||||||||||||||

GLOBAL EQUITY PORTFOLIO - ADVISOR CLASS

| 23.17 | 11.85 | 11.75 | 7.56 | 7.47 | 18.84 | 10.89 | 11.28 | 7.06 | 7.40 | ||||||||||||||||||

MSCI ALL COUNTRY WORLD INDEX

| 14.85 | 8.12 | 9.20 | 5.57 | 9.46 | 6.66 | – | 14.17 | 7.43 | 8.80 | 5.10 | 9.48 | 7.68 | – | ||||||||||||||

Returns are annualized for periods greater than 1 year. *Inception of the Institutional Class, November 3, 2009. Inception of the Institutional Class Z, August 1, 2017. Inception of the Advisor Class, December 1, 1996. Index performance prior to January 1, 2001 cannot be shown since it relies on back-filled data.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Portfolio may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling (877) 435-8105 or visiting www.hardingloevnerfunds.com. Performance data shown does not reflect the 2.00% redemption fee imposed on shares held 90 days or less; otherwise, total returns would be reduced.

⬛ PERFORMANCE ATTRIBUTION

Our Portfolio’s good relative returns derived overwhelmingly from strong stock selection. Our stocks within Health Care delivered the most pronounced outperformance, followed by holdings in Financials, IT, and Consumer Discretionary. Health Care stocks were led by Wuxi Biologics, a new investment in December, which became the first Chinese manufacturer to receive approval for Trogarzo, an antiretroviral drug, from the US Food and Drug Administration. Japan’s Sysmex and M3, China’s Sino Biopharmaceutical, and the UK’s Shire were also strong performers in the sector. Financials got a boost from AIA Group in Hong Kong and from SVB Financial Group in the US.

From a geographic perspective, outperformance came mainly from good stocks in EMs, the US, and Japan. The two Chinese Health Care stocks along with social media platform Weibo led our EM holdings. US key contributors included SVB Financial Group, Verisk, Nike, Booking Holdings (formerly Priceline), and Mastercard. Facebook and Regeneron—high-priced, fast-growing companies—were detractors from our relative performance in the US.

Together, the outperformance in the US, EMs, and Japan more than offset poor stocks in Europe outside of the eurozone. The most significant detractor was Swedish debt collection company Intrum Justitia, which reported poor quarterly earnings. Several low-volatility stocks of high-quality, non-cyclical companies in Europe lagged the index and hurt relative performance, including Reckitt Benckiser and Nestlé.

⬛ PERSPECTIVE AND OUTLOOK

“If you buy something because it’s undervalued, then you have to think about selling it when it approaches your calculation of its intrinsic value. That’s hard. But, if you can buy a few great companies, then you can sit on your ass. That’s a good thing.”

— Charlie Munger,

Berkshire Hathaway annual meeting, 2000

Arguably the greatest contribution that Charlie Munger has made to Berkshire Hathaway’s shareholders was in convincing Warren Buffett in the 1970s that a long-duration growth business trading at an apparently premium price could still represent a good value. His reasoning was that the return on the shares would ultimately converge with the return on capital for the business as the compounding of the latter would, over a long period of time (Munger cited 40 years), come to dwarf the initial premium paid for the shares. That inevitability meant that you could buy, then sit and wait—but, presumably (and critically), only if you were assured that the company would manage to maintain its growth rate and sustain its high profitability in the process. You could tolerate occasional periods of overvaluation of that business’s shares because, given enough time, its profits would grow back into its share price.

As investors in businesses that can grow for many years with high and durable profitability, we at Harding Loevner adhere to an investment philosophy that resembles Munger’s. Through our research process, we look for companies that meet our criteria of what makes a great business. The process is focused entirely on business fundamentals: we evaluate the competitive structure of an industry, examine each participant’s competitive position, and then question whether a favorable industry structure or the particular advantages enjoyed by some participants are sustainable into the future. Upon identifying such apparently great businesses, we include them in our qualified investable universe. We estimate what their shares are worth by making financial forecasts and discounting their projected long-term cash flows to the present. While we’re not afraid to pay over the market average for shares of an excellent business, even a paragon will fail to make its way into our Portfolios if its superior long-term prospects are more than fully discounted in its current share price.

Munger’s challenge, and ours too, is in finding companies that will remain “great” for 10 years, let alone 40. Enduring jewels are more easily discovered in hindsight than in advance. The identification of such companies requires that all evidence in support of a purchase be weighed against an obvious fact—that the vast majority of businesses fail to maintain their profitability over the long term. Once an investment is made, we do much more than sit and watch the returns pour in. We set up structures

Table of Contents

to seek out evidence that the company will not stay great forever. To be able to “sit” comfortably on a holding presupposes, among other things, that the customers of that business continue to prefer its products or services. We guard against the risk of mishap through intensive monitoring of the business results of our portfolio companies, parsing financial disclosures, and checking third-party sources to gauge their progress against the mileposts that we set out in advance as supporting detail to our investment thesis. There is nothing sedentary about our ownership.

To “be right and sit tight,” to borrow a phrase from legendary Wall Street trader Jesse Livermore, is easier said than done in other ways. In addition to guarding against the deterioration of companies’ underlying businesses (the “be right” part), investors need also to guard against the human tendency to become risk averse when they are in a position of gain on their shares (the “sit tight” part); investors tend to harvest their gains too early. They process the constant bombardment of ever-shifting news as calls to action, feeding the instinct to lock in profits and avoid reversals. That flow of news can be company-specific but is often related to the general environment in which companies operate. We resist changing our views in reaction to current events. We didn’t alter the Portfolio materially in response to the Brexit referendum in 2016, nor to anticipate the “Trump bump,” or, more recently, to benefit from the US tax cuts; we also haven’t moved to a stance that bets significantly on rising interest rates. Instead, we focus on the growth prospects for each company and the specific threats that could endanger its stock’s market valuation relative to the rest of the market.

These habits of tolerating elevated valuations and resisting wholesale top-down portfolio shifts have continued to benefit the Portfolio. Despite the rising interest rate headwind and consequential impact on discount rates, growth stocks (particularly the most expensive growth stocks) outperformed this period, extending the trend from last year. Although we recognize the share prices of most rapidly growing companies are high relative to earnings and their history, we continue to take action in favor of cheaper ones only incrementally, and only against the priciest stocks in our Portfolio.

GEOGRAPHIC EXPOSURE (%) at April 30, 2018

COUNTRY/REGION

|

PORTFOLIO

|

BENCHMARK1

| ||||||

CANADA

|

| 0.0

|

|

| 3.0

|

| ||

EMERGING MARKETS

|

| 13.3

|

|

| 12.0

|

| ||

EUROPE EMU

|

| 13.3

|

|

| 11.0

|

| ||

EUROPE EX-EMU

|

| 14.8

|

|

| 10.0

|

| ||

FRONTIER MARKETS2

|

| 0.0

|

|

| —

|

| ||

JAPAN

|

| 10.8

|

|

| 8.0

|

| ||

MIDDLE EAST

|

| 0.8

|

|

| 0.1

|

| ||

PACIFIC EX-JAPAN

|

| 2.7

|

|

| 3.9

|

| ||

UNITED STATES

|

| 41.3

|

|

| 52.0

|

| ||

CASH

|

| 3.0

|

|

| —

|

| ||

1MSCI All Country World Index; 2Includes countries with less-developed markets outside the Index.

SECTOR EXPOSURE (%) at April 30, 2018

SECTOR

|

PORTFOLIO

|

BENCHMARK1

| ||||||

CONSUMER DISCRETIONARY

|

| 12.7

|

|

| 12.4

|

| ||

CONSUMER STAPLES

|

| 5.0

|

|

| 8.0

|

| ||

ENERGY

|

| 3.8

|

|

| 6.7

|

| ||

FINANCIALS

|

| 15.5

|

|

| 18.6

|

| ||

HEALTH CARE

|

| 17.6

|

|

| 10.8

|

| ||

INDUSTRIALS

|

| 14.3

|

|

| 10.7

|

| ||

INFORMATION TECHNOLOGY

|

| 19.6

|

|

| 18.6

|

| ||

MATERIALS

|

| 8.5

|

|

| 5.4

|

| ||

REAL ESTATE

|

| 0.0

|

|

| 3.0

|

| ||

TELECOM SERVICES

|

| 0.0

|

|

| 2.9

|

| ||

UTILITIES

|

| 0.0

|

|

| 2.9

|

| ||

CASH

|

| 3.0

|

|

| —

|

| ||

1MSCI All Country World Index.

Our reluctance to position the Portfolio in anticipation of political or economic developments does not mean we ignore the gathering clouds. Central banks are withdrawing monetary stimulus in reaction to signs that inflation expectations are increasing, and in the larger cause of normalizing interest rates ahead of the next recession. Rising populism, particularly in Europe, has called into question the longstanding consensus on advantages of a common currency, tax-free trade, and free movement of labor. And now the US threatens to precipitate a trade war that would have a devastating impact on globalization and potentially erase the enormous benefits that free trade has brought to nearly all parts of the world that have participated in it.

The recent announcements by the Trump administration to enact tariffs on various imports—including washing machines, solar panels, aluminum, steel, and, most recently, US$50 billion of other Chinese goods—could have devastating consequences for the US and its trading partners. While the brandishing of tariffs as a bilateral negotiating tactic—or as a domestic political sop—are not unique to the Trump presidency (recall tariffs from Barack Obama on Chinese tires or George W. Bush on steel), Trump’s enthusiastic use of them seems to us unusually provocative. The absolute amount of goods subject to tariffs is small relative to GDP, but the legal justification for many of them relies on an obscure clause of trade law allowing redress on the grounds of national security. This rationale sets a dangerous precedent, as it is intended to evade any adverse ruling by objective outside bodies, such as the World Trade Organization (WTO), and undermines the entire rules-based trading system that has served the global economy so well since the Second World War.

While Trump insists that “trade wars are good,” all evidence is to the contrary. Trade wars generally create losers on all sides. As countries, one after another, retaliate with their own tariffs or restrictions, the positive effects of globalization are undone. By preventing countries from focusing their productive efforts where each has a comparative advantage, trade barriers protect inefficient industries, resulting in misallocations of capital, higher costs and inflation, and lower wealth overall. Reversing

Table of Contents

globalization also has the potential to increase interest rates, which had been until recently on a more or less steady decline since the early 1980s. When economies are interdependent, local shocks are dampened by the global economy’s equilibrating mechanism, reducing economic volatility and the real component of long-term interest rates.1

We are uneasy, but admit a range of possible outcomes, from spiraling tit-for-tat tariff actions to possibly more-measured responses, and perhaps even some positive long-term consequences, such as potential reform of the WTO. But we know from experience that we have little ability to forecast the political outcome. We have resisted the temptation to alter course, unsure even what overall course we would take if our worst fears were realized with respect to the health of the world’s trading regime. Instead we continue to focus on the business fundamentals and valuations of the most resilient companies.

⬛ PORTFOLIO HIGHLIGHTS

Sticking to our last, Portfolio transactions in the last six months reflected our bottom-up assessments of profit outlook and valuation—with a particular emphasis on the latter. Many of the Portfolio changes during the period involved selling or reducing a more expensive-looking security in exchange for a less expensive alternative. Often, this meant going against prevailing momentum to sell an outperforming stock to buy an underperforming one. As one example, we sold our position in China’s Sino Biopharmaceutical in March. The stock had doubled in prior months and become significantly overvalued in our model. We then added to our holding in the UK’s Shire, which at the time was one of our worst-performing holdings and among the least expensive-looking securities in our analyst-qualified and -rated universe of companies. This transaction promptly yielded fruit when Japan’s Takeda Pharmaceutical indicated interest in acquiring Shire in late March, giving a welcome boost to Shire’s beleaguered share price.

We sold our profitable holding in Chinese gaming and social media giant Tencent, reinvesting the proceeds into South Africa’s Naspers, whose largest asset is a 31% stake in Tencent. The value of that stake alone approximates 145% of Naspers’ market capitalization. The longstanding discount to net asset value at Naspers—around a record high today—is increasingly controversial, and pressure is building on Naspers’ management to take steps to close it.

Finally, we reduced our sizable position in Nike in March, seeing less valuation appeal after the stock’s fourth-quarter 2017 share price surge, to add to Switzerland’s Lonza Group, a global leader in outsourced manufacturing for pharmaceuticals. Though a very successful investment long term, Lonza’s share price had declined sharply during the market correction, leaving its valuation looking more attractive than at any time in recent years.

1Tao Wu, “Globalization’s Effect on Interest Rates and the Yield Curve,” Economic Letter: Insights from the Federal Reserve Bank of Dallas 1, no. 9 (September 2006).

TEN LARGEST HOLDINGS at April 30, 2018

COMPANY

| SECTOR | COUNTRY | % | |||||

PAYPAL

| INFO TECHNOLOGY

| UNITED STATES

|

| 3.2

|

| |||

SYSMEX

| HEALTH CARE

| JAPAN

|

| 2.9

|

| |||

ROPER

| INDUSTRIALS

| UNITED STATES

|

| 2.8

|

| |||

BOOKING HOLDINGS

| CONS DISCRETIONARY

| UNITED STATES

|

| 2.8

|

| |||

AIA GROUP

| FINANCIALS

| HONG KONG

|

| 2.6

|

| |||

FIRST REPUBLIC BANK

| FINANCIALS

| UNITED STATES

|

| 2.5

|

| |||

LONZA GROUP

| HEALTH CARE

| SWITZERLAND

|

| 2.5

|

| |||

VERISK

| INDUSTRIALS

| UNITED STATES

|

| 2.2

|

| |||

SYMRISE

| MATERIALS

| GERMANY

|

| 2.2

|

| |||

STANDARD CHARTERED

| FINANCIALS

| UNITED KINGDOM

|

| 2.0

|

| |||

Our Portfolio structure has evolved considerably in the last year, the most significant changes being an increase in our Health Care weight and a decrease in IT. Health Care now comprises nearly 18% of the Global Equity Portfolio. The Portfolio has the smallest overweight in IT relative the index since 2003, as the sector’s strong outperformance as of late left valuations less attractive, leading us to sell a number of IT stocks. Geographically, we significantly decreased our US holdings. At the end of April 2018, just 41% of the Portfolio was invested in US stocks, versus 46% one year ago. The capital raised from sales of US stocks was redeployed mainly in companies domiciled in Europe and EMs.

Portfolio Management Team Update

Scott Crawshaw has joined our Global Equity strategy portfolio management team as of January 2, 2018. He is responsible specifically for the World Equity strategy, which is based on our Global Equity strategy but benchmarked to the developed market MSCI World Index. In this role, Scott, in consultation with its co-lead PMs, will adapt the Global Equity strategy to the requirements of the World Equity strategy. Co-Lead PM Peter Baughan, CFA previously performed this function.

Please read the separate disclosures page for important information, including the risks of investing in the Portfolio.

Table of Contents

PORTFOLIO MANAGEMENT TEAM

| FERRILL ROLL, CFA CO-LEAD PORTFOLIO MANAGER

ALEXANDER WALSH, CFA CO-LEAD PORTFOLIO MANAGER

SCOTT CRAWSHAW PORTFOLIO MANAGER

BRYAN LLOYD, CFA PORTFOLIO MANAGER

PATRICK TODD, CFA PORTFOLIO MANAGER

ANDREW WEST, CFA PORTFOLIO MANAGER | |

⬛ PERFORMANCE SUMMARY

For the International Equity Portfolio, the Institutional Class gained 3.97%, the Institutional Class Z gained 4.00%, and the Investor Class rose 3.81% (net of fees and expenses) in the six-month period ended April 30, 2018. The Portfolio’s benchmark, the MSCI All Country World ex-US Index, gained 3.47% (net of source taxes).

⬛ MARKET REVIEW

Markets closed 2017 on an optimistic note, with stock prices rising strongly in December. Economic growth across all major regions remained positive and synchronized, while inflation was subdued. In Europe, the European Central Bank remained accommodative on monetary policy, although it signaled a slowing pace of bond buying. China’s economy gathered momentum, shrugging off concerns over government corruption crackdowns and shaky property loans, with positive pull-through effects on its trading partners. Japanese economic growth edged higher, while inflation remained positive—a critical policy goal.

The markets’ positive trend continued into the new year, but the streak of 14 monthly gains ended in February as sanguinity gave way to worry. Although the backdrop of improving and increasingly synchronized economic growth and good corporate earnings remained in place, investors had to come to terms with some ugly prospects: higher interest rates, a trade war between the US and China, and increased regulation of technology companies.

Stock price volatility spiked at the end of January, exacerbated by the collapse of derivatives-based “inverse volatility” ETFs, contributing to a near 9% decline in equities in just 10 days. After a brief bounce in mid-February, stocks wallowed in a range through the end of April, reflecting a new set of worries about

FUND FACTS at April 30, 2018

| ||||||||||||||

TOTAL NET ASSETS

|

| $ 14,157.5M | ||||||||||||

SALES CHARGE

|

| NONE | ||||||||||||

NUMBER OF HOLDINGS

|

| 56 | ||||||||||||

TURNOVER (5 YR. AVG.)

|

| 14% | ||||||||||||

REDEMPTION FEE

|

| 2% FIRST 90 DAYS | ||||||||||||

DIVIDEND POLICY

|

| ANNUAL | ||||||||||||

INSTITUTIONAL INVESTORS

|

INDIVIDUAL INVESTORS

| |||||||||||||

|

| INSTL CLASS

|

|

| INSTL CLASS Z

|

|

| INVESTOR CLASS

|

| ||||||

TICKER

| HLMIX | HLIZX | HLMNX | |||||||||||

CUSIP

| 412295107 | 412295719 | 412295503 | |||||||||||

INCEPTION DATE

| 5/11/1994 | 7/17/2017 | 9/30/2005 | |||||||||||

MINIMUM INVESTMENT1

| $100,000 | $10,000,000 | $5,000 | |||||||||||

NET EXPENSE RATIO

| 0.82% | 0.73% | 2 | 1.14% | ||||||||||

GROSS EXPENSE RATIO

| 0.82% | 0.99% | 3 | 1.14% | ||||||||||

1Lower minimums available through certain brokerage firms; 2The Net Expense Ratio is as of April 30, 2018 as the Portfolio is operating below the contractual agreement, which is in effect until February 28, 2019; 3The Gross Expense Ratio is as of the Prospectus dated February 28, 2018.

increasingly ubiquitous technology platforms. A mounting furor over Facebook data illicitly exploited by political consultant Cambridge Analytica in favor of US President Donald Trump and Brexit, and the mowing down of a pedestrian by an Uber self-driving car in Arizona drew calls for more regulation of technology companies. The European Union continued its efforts to rein in “big tech,” announcing a tax on turnover of large digital companies and moving ahead with its General Data Protection Regulation mandate, which imposes strict requirements and stiff penalties regarding treatment of private data. The tech tumult turned farcical with Trump tweeting potshots at Amazon.com over its use of the Postal Service.

All sectors advanced in the period, led by Energy, as crude oil prices reached levels in April not seen since the end of 2014. Information Technology (IT) lagged the index, as its outsized January gains were nearly depleted by sharp declines late in March.

All regions except Canada advanced as well. Emerging Markets (EMs), more typically the loser from rising global risk and volatility, was among the strongest-performing regions. Confoundingly, EMs’ rise was supported by Brazil and Russia, two of the biggest exporters of steel and other commodities whose trade is endangered. A Brazilian court upheld the conviction of former president Luiz In-ácio Lula da Silva on corruption charges, likely precluding him from running again and restoring his redistributionist policies.

The most expensive quintile of stocks gained in the period, outperforming the rest by a wide margin. The fastest-growing quintile of stocks also rose more than the other 80% of stocks, on average. Quality was not a significant return factor.

Table of Contents

PERFORMANCE (% TOTAL RETURN)

for periods ended March 31, 2018

| for periods ending April 30, 2018 | |||||||||||||||||||||||||||

| 1 | 3 | 5 | 10 | SINCE INCEPTION* | 1 | 3 | 5 | 10 | SINCE INCEPTION* | |||||||||||||||||||

YEAR

| YEARS

| YEARS

| YEARS

|

May-94

| Jul-17

| Sep-05

| YEAR

| YEARS

| YEARS

| YEARS

| May-94

| Jul-17

| Sep-05

| |||||||||||||||

INTL EQUITY PORTFOLIO – INST CLASS | 19.20 | 8.89 | 8.34 | 5.71 | 6.58 | 16.46 | 7.67 | 7.84 | 5.22 | 6.59 | ||||||||||||||||||

INTL EQUITY PORTFOLIO – INST CLASS Z

| – | – | – | – | 9.48 | – | – | – | – | 10.24 | ||||||||||||||||||

INTL EQUITY PORTFOLIO – INVESTOR CLASS

| 18.80 | 8.51 | 7.99 | 5.38 | 6.95 | 16.07 | 7.33 | 7.50 | 4.89 | 6.96 | ||||||||||||||||||

MSCI ALL COUNTRY WORLD EX-US INDEX

| 16.53 | 6.18 | 5.88 | 2.70 | – | 7.35 | 4.97 | 15.91 | 5.01 | 5.46 | 2.26 | – | 9.06 | 5.07 | ||||||||||||||

Returns are annualized for periods greater than 1 year. *Inception of the Institutional Class, May 11, 1994. Inception of the Institutional Class Z, July 17, 2017. Inception of the Investor Class, September 30, 2005. Index performance prior to January 1, 2001 cannot be shown since it relies on back-filled data.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Portfolio may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling (877) 435-8105 or visiting www.hardingloevnerfunds.com. Performance data shown does not reflect the 2.00% redemption fee imposed on shares held 90 days or less; otherwise, total returns would be reduced.

⬛ PERFORMANCE ATTRIBUTION

The Portfolio’s positive relative performance derived primarily from good stock selection, especially in Financials and Health Care. In Financials, Hong Kong-based life insurer AIA Group added to relative returns. Brazilian lender Itaú Unibanco rallied on the Lula court ruling, while DBS Group of Singapore signaled larger distributions of capital to shareholders with a surprising regular dividend increase plus a special dividend. Health Care was led by medical information provider M3, which rose on news that the company acquired an American clinical trials firm, signaling entry into the large and profitable US market. On the other side of the ledger, crop chemicals and pharmaceuticals giant Bayer suffered on news that regulators may require the company to divest some key businesses in order to win approval for its purchase of Monsanto, reducing its ability to exploit merger synergies.

Our holdings in Pacific ex-Japan added the most to relative performance from a regional perspective, aided by DBS Group and AIA Group. Stocks in Japan also contributed, especially M3 and Sysmex, the clinical-testing equipment manufacturer. Sysmex’s management stoked optimism over the potential impact of its R&D in liquid biopsy technology. Relative performance in EMs suffered as South African media conglomerate Naspers declined. Despite the large cash proceeds from the sale of a sliver of its successful investment in Chinese internet platform Tencent, many of Naspers’ newer investments are still absorbing resources rather than generating cash flow. Samsung Electronics also underperformed due to concerns that it will earn lackluster returns from its large investment to supply the latest Apple iPhone, which has been met with slow demand.

⬛ PERSPECTIVE AND OUTLOOK

“If you buy something because it’s undervalued, then you have to think about selling it when it approaches your calculation of its intrinsic value. That’s hard. But, if you can buy a few great companies, then you can sit on your ass. That’s a good thing.”

— Charlie Munger,

Berkshire Hathaway annual meeting, 2000

Arguably the greatest contribution that Charlie Munger has made to Berkshire Hathaway’s shareholders was in convincing Warren Buffett in the 1970s that a long-duration growth business trading at an apparently premium price could still represent a good value. His reasoning was that the return on the shares would ultimately converge with the return on capital for the business as the compounding of the latter would, over a long period of time (Munger cited 40 years), come to dwarf the initial premium paid for the shares. That inevitability meant that you could buy, then sit and wait—but, presumably (and critically), only if you were assured that the company would manage to maintain its growth rate and sustain its high profitability in the process. You could tolerate occasional periods of overvaluation of that business’s shares because, given enough time, its profits would grow back into its share price.

As investors in businesses that can grow for many years with high and durable profitability, we at Harding Loevner adhere to an investment philosophy that resembles Munger’s. Through our research process we look for companies that meet our criteria of what makes a great business. The process is focused entirely on business fundamentals: we evaluate the competitive structure of an industry, examine each participant’s competitive position, and then question whether a favorable industry structure or the particular advantages enjoyed by some participants are sustainable into the future. Upon identifying such apparently great businesses, we include them in our qualified investable universe. We estimate what their shares are worth by making financial forecasts and discounting their projected long-term cash flows to the present. While we’re not afraid to pay over the market average for shares of an excellent business, even a paragon will fail to make its way into our portfolios if its superior long-term prospects are more than fully discounted in its current share price.

Munger’s challenge, and ours too, is in finding companies that will remain “great” for 10 years, let alone 40. Enduring jewels are more easily discovered in hindsight than in advance. The identification of such companies requires that all evidence in support of a purchase be weighed against an obvious fact—that the vast majority of businesses fail to maintain their profitability over the long term. Once an investment is made, we do much more than sit and watch the returns pour in. We set up structures to seek out evidence that the company will not stay great forever. To be able to

Table of Contents

“sit” comfortably on a holding presupposes, among other things, that the customers of that business continue to prefer its products or services. We guard against the risk of mishap through intensive monitoring of the business results of our portfolio companies, parsing financial disclosures, and checking third-party sources to gauge their progress against the mileposts that we set out in advance as supporting detail to our investment thesis. There is nothing sedentary about our ownership.

To “be right and sit tight,” to borrow a phrase from legendary Wall Street trader Jesse Livermore, is easier said than done in other ways. In addition to guarding against the deterioration of companies’ underlying businesses (the “be right” part), investors need also to guard against the human tendency to become risk averse when they are in a position of gain on their shares (the “sit tight” part); investors tend to harvest their gains too early. They process the constant bombardment of ever-shifting news as calls to action, feeding the instinct to lock in profits and avoid reversals. That flow of news can be company-specific but is often related to the general environment in which companies operate. We resist changing our views in reaction to current events. We didn’t alter the portfolio materially in response to the Brexit referendum in 2016, nor to anticipate the “Trump bump,” nor, more recently, to benefit from the US tax cuts; we also haven’t moved to a stance that bets significantly on rising interest rates. Instead, we focus on the growth prospects for each company and the specific threats that could endanger its stock’s market valuation relative to the rest of the market.

These habits of tolerating elevated valuations and resisting wholesale top-down portfolio shifts have continued to benefit the Portfolio. Despite the rising interest rate headwind and consequential impact on discount rates, growth stocks (particularly the most expensive growth stocks) outperformed this period, extending the trend from last year. Although we recognize the share prices of most rapidly growing companies are high relative to earnings and their history, we continue to take action in favor of cheaper ones only incrementally, and only against the priciest stocks in our Portfolio.

Our reluctance to position the Portfolio in anticipation of political or economic developments does not mean we ignore the gathering

GEOGRAPHIC EXPOSURE (%) at April 30, 2018

COUNTRY/REGION

|

PORTFOLIO

|

BENCHMARK1

| ||||||

CANADA

| 1.9 | 6.2 | ||||||

EMERGING MARKETS

| 19.4 | 25.1 | ||||||

EUROPE EMU

| 29.9 | 22.9 | ||||||

EUROPE EX-EMU

| 19.6 | 20.7 | ||||||

FRONTIER MARKETS2

| 0.0 | — | ||||||

JAPAN

| 14.0 | 16.7 | ||||||

MIDDLE EAST

| 2.2 | 0.3 | ||||||

PACIFIC EX-JAPAN

| 8.2 | 8.1 | ||||||

OTHER3

| 1.5 | — | ||||||

CASH

| 3.3 | — | ||||||

1MSCI All Country World ex-US Index; 2Includes countries with less-developed markets outside the Index; 3Includes companies classified in countries outside the Index.

SECTOR EXPOSURE (%) at April 30, 2018

SECTOR

| PORTFOLIO

| BENCHMARK1

| ||||||

CONSUMER DISCRETIONARY

| 6.3 | 11.4 | ||||||

CONSUMER STAPLES

| 7.1 | 9.3 | ||||||

ENERGY

| 5.7 | 7.1 | ||||||

FINANCIALS

| 19.4 | 23.0 | ||||||

HEALTH CARE

| 17.1 | 7.6 | ||||||

INDUSTRIALS

| 12.1 | 11.8 | ||||||

INFORMATION TECHNOLOGY

| 20.5 | 11.5 | ||||||

MATERIALS

| 7.7 | 8.1 | ||||||

REAL ESTATE

| 0.8 | 3.2 | ||||||

TELECOM SERVICES

| 0.0 | 4.0 | ||||||

UTILITIES

| 0.0 | 3.0 | ||||||

CASH

| 3.3 | — | ||||||

1MSCI All Country World ex-US Index.

clouds. Central banks are withdrawing monetary stimulus in reaction to signs that inflation expectations are increasing, and in the larger cause of normalizing interest rates ahead of the next recession. Rising populism, particularly in Europe, has called into question the longstanding consensus on advantages of a common currency, tax-free trade, and free movement of labor. And now the US threatens to precipitate a trade war that would have a devastating impact on globalization and potentially erase the enormous benefits that free trade has brought to nearly all parts of the world that have participated in it.

The recent announcements by the Trump administration to enact tariffs on various imports—including washing machines, solar panels, aluminum, steel, and, more recently, US$50 billion of other Chinese goods—could have devastating consequences for the US and its trading partners. While the brandishing of tariffs as a bilateral negotiating tactic—or as a domestic political sop—are not unique to the Trump presidency (recall tariffs from Barack Obama on Chinese tires or George W. Bush on steel), Trump’s enthusiastic use of them seems to us unusually provocative. The absolute amount of goods subject to tariffs is small relative to GDP, but the legal justification for many of them relies on an obscure clause of trade law allowing redress on the grounds of national security. This rationale sets a dangerous precedent, as it is intended to evade any adverse ruling by objective outside bodies, such as the World Trade Organization (WTO), and undermines the entire rules-based trading system that has served the global economy so well since the Second World War.

While Trump insists that “trade wars are good,” all evidence is to the contrary. Trade wars generally create losers on all sides. As countries, one after another, retaliate with their own tariffs or restrictions, the positive effects of globalization are undone. By preventing countries from focusing their productive efforts where each has a comparative advantage, trade barriers protect inefficient industries, resulting in misallocations of capital, higher costs and inflation, and lower wealth overall. Reversing globalization also has the potential to increase interest rates, which had been until recently on a more or less steady decline since the early 1980s. When economies are

Table of Contents

interdependent, local shocks are dampened by the global economy’s equilibrating mechanism, reducing economic volatility and the real component of long-term interest rates.

We are uneasy, but admit a range of possible outcomes, from spiraling tit-for-tat tariff actions to possibly more-measured responses, and perhaps even some positive long-term consequences, such as potential reform of the WTO. But we know from experience that we have little ability to forecast the political outcome. We have resisted the temptation to alter course, unsure even what overall course we would take if our worst fears were realized with respect to the health of the world’s trading regime. Instead we continue to focus on the business fundamentals and valuations of the most resilient companies.

⬛ PORTFOLIO HIGHLIGHTS

Two of the largest contributors to positive relative returns in the Portfolio over the trailing six months—Dassault Systèmes and M3—are prime examples of companies that Charlie Munger might like. In both cases, we’ve been right about the durable profitability and rapid growth of the businesses. And Jesse Livermore would approve our having sat tight, as we have owned their shares continuously for a long time. We believed that both companies were capable of growing rapidly for many years. But to remain invested in them, we have had to live through periods of overvaluation.

Japan’s M3 is a health care IT company, first qualified and rated by one of our analysts in January 2006. M3’s flagship service is MR-kun, an online platform for physicians that provides information specific to their individual therapeutic specialties, including all relevant research studies and clinical trial data.

M3 now has recurring interaction with more than 80% of physicians in Japan, who represent a high-value audience for pharmaceutical companies seeking to develop or market new drugs. M3 will continue to grow as it adds more online and offline services in Japan. Meanwhile the company is replicating its information ecosystem outside of its home market, with four million doctors using its platform, and where it now garners 25% of its revenues. M3 is among Japan’s fastest-growing companies, and, accordingly, its shares trade at apparent high prices. Today, M3’s market capitalization is US$13 billion, compared with just over US$1 billion when we bought it in 2008.

Dassault Systèmes is a 3D-design software company that we have owned since 2003. After starting with an aerospace-design focus, Dassault’s software is now used by over 200,000 enterprises across a dozen industries in 140 countries. Its segment of the software industry, often referred to as product lifecycle management, features above-average and durable growth, fueled by the increasing global emphasis on efficient production.

To Munger’s point about the convergence of the return on capital of a business and the return to its shareholders, we have experienced something comparable. Over our 10-year holding period, M3 has had an average annual return on capital of 26%,

TEN LARGEST HOLDINGS at April 30, 2018

COMPANY

| SECTOR

| COUNTRY

| %

| |||||

AIA GROUP

| FINANCIALS | HONG KONG | 4.4 | |||||

ALLIANZ

| FINANCIALS | GERMANY | 3.6 | |||||

SAMSUNG ELECTRONICS

| INFO TECHNOLOGY | SOUTH KOREA | 3.6 | |||||

BAYER

| HEALTH CARE | GERMANY | 3.5 | |||||

ROYAL DUTCH SHELL

| ENERGY | UNITED KINGDOM | 3.3 | |||||

DASSAULT SYSTÈMES

| INFO TECHNOLOGY | FRANCE | 3.1 | |||||

NESTLÉ

| CONS STAPLES | SWITZERLAND | 3.0 | |||||

FANUC

| INDUSTRIALS | JAPAN | 2.8 | |||||

BAIDU

| INFO TECHNOLOGY | CHINA | 2.8 | |||||

DBS GROUP

| FINANCIALS | SINGAPORE | 2.6 | |||||

within shouting distance of the 32% compound annual return of the shares in that time. Similarly, Dassault’s return on capital has averaged 14% over our 15-year holding period, close to the 16% compound annual return of its shares.

The Portfolio’s structure has changed little in the last six months, with IT and Health Care remaining our largest overweights relative the index. We added one Health Care holding to the Portfolio. Novozymes is the leading manufacturer of industrial enzymes, used in a variety of applications, including fuel, detergent, and food. Its global market share approaches 50%, and the market is expanding as manufacturers replace inorganic chemicals in household products with naturally occurring enzymes. Novozymes controls more than twice as many patents than its next-largest competitor and spends more on R&D than its three biggest rivals combined.

We sold two companies in the period. We sold Mexican media company Televisa due to rising competitive intensity. We also sold Garanti Bank, which has suffered from the stock price volatility and currency depreciation that have marked all Turkish investments. With US dollar interest rates on the rise, and Turkey’s need for capital inflows undiminished, there is little prospect for the stabilization that seemed possible just a few years ago.

Portfolio Management Team Update

Scott Crawshaw has joined our International Equity strategy portfolio management team as of January 2, 2018. He is responsible specifically for the EAFE Equity strategy, which is based on our International Equity strategy but benchmarked to the developed market MSCI EAFE Index. In this role, Scott, in consultation with its co-lead PMs, will adapt the International Equity strategy to the requirements of the EAFE Equity strategy. Co-lead PM Alexander Walsh, CFA previously performed this function.

Please read the separate disclosures page for important information, including the risks of investing in the Portfolio.

Table of Contents

PORTFOLIO MANAGEMENT TEAM

| JAFAR RIZVI, CFA CO-LEAD PORTFOLIO MANAGER

ANIX VYAS, CFA CO-LEAD PORTFOLIO MANAGER | |

⬛ PERFORMANCE SUMMARY

For the International Small Companies Portfolio, the Institutional Class gained 4.15% and the Investor Class gained 4.08% (net of fees and expenses) in the six-month period ended April 30, 2018. The Portfolio’s benchmark, the MSCI All Country World ex-US Small Cap Index, rose 5.44% (net of source taxes).

⬛ MARKET REVIEW

Stocks of international small caps rose steadily from early December through the first 25 days of 2018 on the prospects of continued economic growth and strong corporate earnings. In late January, however, employment reports stoked fears that economies were overheating and that central bankers would quicken monetary tightening. Largely absent since the Brexit vote in June 2016, market volatility returned. Between January 26 and February 9, non-US small cap stocks fell about 9% before stabilizing. Then, in March, US President Donald Trump threatened to precipitate a trade war by declaring tariffs on steel, aluminum, and other products. China and other trading partners vowed to retaliate.

Amid the tumult, non-US small caps continued to report strong revenue and earnings growth and outperformed non-US large companies by 200 basis points in the trailing six months. Smaller companies, which tend to focus more on their home markets, are relatively insulated from the effects of trade wars. One example is the Moscow Exchange, which is discussed later in this commentary.

Japan was the strongest performing “region,” rising over 7%. Europe also performed well, both within and outside of the eurozone. Emerging Market small caps were also strong, with above-index returns from Egypt, South Korea, South Africa, and Brazil. Canada and the Middle East were the only regions to decline.

All sectors rose in the six months. Health Care rose the most (14%), driven by innovations and improving prospects for growth at many small biotech and biopharmaceutical firms in both emerging and developed markets. Consumer Staples, Real Estate, and Energy were the next strongest sectors. Stocks of Industrials and Telecom Services companies lagged the index the most.

Based on our categorizations, stocks of the fastest-growing companies performed best—continuing a trend from 2017. The most expensive quintile of stocks also outperformed the rest by a wide margin. Quality was not a significant return factor in the period.

| FUND FACTS at April 30, 2018 | ||||||||

TOTAL NET ASSETS

|

| $250.1M | ||||||

SALES CHARGE

|

| NONE | ||||||

NUMBER OF HOLDINGS

|

| 96 | ||||||

TURNOVER (5 YR. AVG.)

|

| 36% | ||||||

REDEMPTION FEE

|

|

| 2% FIRST 90 DAYS

|

| ||||

DIVIDEND POLICY

|

| ANNUAL | ||||||

INSTITUTIONAL INVESTORS

| INDIVIDUAL INVESTORS

| |||||||

|

| INSTITUTIONAL CLASS

|

| INVESTOR CLASS | |||||

TICKER

| HLMRX | HLMSX | ||||||

CUSIP

| 412295875 | 412295883 | ||||||

INCEPTION DATE

| 6/30/2011 | 3/26/2007 | ||||||

MINIMUM INVESTMENT1

| $100,000 | $5,000 | ||||||

NET EXPENSE RATIO2

| 1.15% | 1.40% | ||||||

GROSS EXPENSE RATIO

| 1.41% | 1.80% | ||||||

1Lower minimums available through certain brokerage firms; 2Shown net of Harding Loevner’s contractual agreement through February 28, 2019.

⬛ PERFORMANCE ATTRIBUTION

Viewed by sector, stocks in Financials detracted from the Portfolio’s relative returns. Suruga Bank, which has over 100 branches across Japan, detracted from performance due to credit problems with the real estate company Smart Days. Smart Days leases residential property from investor-owners, then re-leases them to subtenants. Many of the owners financed their property purchases with Suruga Bank. In February, Japanese news outlets reported that due to low occupancy rates, Smart Days had been unable to continue making lease payments to many of the property owners and, as a result, the owners have stopped making payments to Suruga Bank on their loans. We are investigating whether Suraga’s arrangement with Smart Days was a one-off mistake, or if it is indicative of systematic credit-underwriting problems at the bank.

The decline was partially offset by strong stocks in Information Technology (IT) and the Portfolio’s overweight to Health Care. The bulk of our IT exposure is to software and services, which was the sector’s best-performing industry group. Infomart, a Japanese e-commerce company that services the restaurant industry, was one of the largest contributors to relative returns. In 2017, Infomart’s heavy investments in software that enables online invoicing weighed on profits. But in February, management forecast 42% growth in operating profit in 2018, suggesting that these investments are now bearing fruit as customers shift away from inefficient paper-invoicing systems in favor of Infomart’s product.

Regionally, poor stock selection in Emerging Markets detracted from relative returns. In India, Axis Bank accounts for over half of Max Financial’s life insurance distribution. This arrangement is likely in jeopardy, as Axis Bank is reportedly pursuing its own

Table of Contents

PERFORMANCE (% TOTAL RETURN)

for periods ended March 31, 2018

| for periods ended April 30, 2018

| |||||||||||||||||||||||

| 1 | 3 | 5 | 10 | SINCE INCEPTION* | 1 | 3 | 5 | 10 | SINCE INCEPTION* | |||||||||||||||

| YEAR | YEARS | YEARS | YEARS | Jun-11 | Mar-07 | YEAR | YEARS | YEARS | YEARS | Jun-11 | Mar-07 | |||||||||||||

INTL SMALL COMPANIES PORTFOLIO – INST CLASS

| 25.00 | 10.92 | 9.50 | – | 8.16 | 18.19 | 9.23 | 8.75 | – | 7.87 | ||||||||||||||

INTL SMALL COMPANIES PORTFOLIO – INVESTOR CLASS

| 24.66 | 10.63 | 9.23 | 8.09 | 7.04 | 17.98 | 8.97 | 8.50 | 7.81 | 6.87 | ||||||||||||||

MSCI ALL COUNTRY WORLD EX-US SMALL CAP INDEX | 20.60 | 10.40 | 8.57 | 5.51 | 6.49 | – | 18.44 | 8.70 | 8.24 | 5.33 | 6.59 | – | ||||||||||||

Returns are annualized for periods greater than 1 year. *Inception of the Institutional Class, June 30, 2011. Inception of the Investor Class, March 26, 2007. Index performance prior to June 1, 2007 cannot be shown since it relies on back-filled data.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Portfolio may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling (877) 435-8105 or visiting www.hardingloevnerfunds.com. Performance data shown does not reflect the 2.00% redemption fee imposed on shares held 90 days or less; otherwise, total returns would be reduced.

life insurance business. The news weighed on Max Financial’s stock price, but we continue to believe in the company’s ability to grow its other distribution channels and in the long-term growth of the Indian life insurance market overall.

The Portfolio gained from strong stock selection in Japan, our underweight to Canada, and our (off-benchmark) Frontier Market holdings, notably in Kenya. We have written about how a banking law newly enacted in Kenya that established a floor on deposit rates and capped lending rates was hurting the profitability of the entire sector. Since then, Equity Bank has sustained its profitability by increasing fee income, and by reclassifying savings accounts as current accounts to reduce the cost of funding. Equity Bank’s profits rose 14% in 2017. Further, the governor of the Central Bank of Kenya, Patrick Ngugi Njoroge, is pushing for a repeal of the 2016 interest rate regulation.

⬛ INVESTMENT PERSPECTIVES

We rely on an investment process that offers our clients a portfolio of businesses that we believe are more resilient to volatility and shocks from any number of directions. We look for competitive businesses with steady returns on capital, significant free cash flow, healthy balance sheets, and management focused on their companies’ core strengths. In particular, we look for pricing power, which we see as key to companies maintaining their margins in growth-challenged environments.

In Japan, a shrinking labor market and rising labor costs are sources of mounting concern for companies large and small. We are hard pressed to think of a company more advantageously positioned than SMS, a niche health care IT firm that provides software and services for staff recruitment for hospitals and elderly care facilities. While other Japanese companies have been struggling with the country’s shrinking labor pool and rising wages, SMS has thrived. Japan’s rising number of elderly increases demand for nurses and other health care workers. The company—which earns a 20% commission on the first-year salary of recruited personnel—not only benefits from that market growth, but also from rising wages. SMS has not grown complacent; it is channeling more resources into its Kaipoke software, which provides nursing care placement services, and the platform’s expanding capabilities

are transforming neatly into pricing power and market share. Subscriber growth has been steady despite a nearly seven-fold increase in subscription fees since the software was released in 2006.

Unlike SMS, which operates in the idiosyncratic Japanese labor market, Ottawa-based Kinaxis competes in the much faster-growing global market for supply chain management software. The company is outpacing its competitors, racking up an impressive win rate over the likes of SAP, Infor, and JDA Software, primarily due to the high quality and functionality of its product. Its revenue retention exceeds 100%, with clients not only renewing subscriptions but spending more each year. Because its recurring revenues are so reliable, Kinaxis can afford to be highly selective in its sales strategy. At its recent Investor Day in Toronto, CEO John Sicard stated that management is comfortable losing low-margin deals with customers with tight budgets and limited needs to focus on comprehensive solutions for potentially larger customers. In fact, Sicard said he wants Kinaxis’s sales staff to walk away from deals rather than compromise on pricing. This strategy aims to ensure that the company’s growth does not reduce margins, and that it generates free cash for reinvestment. The company is committed to spending 18% of revenues on R&D. Spending is concentrated on its core supply chain software, introducing more advanced machine-learn-ing-based analytics tools and a cloud-based mobile app that allows managers to monitor their entire supply chain in real time.

While Kinaxis shows that a company can achieve pricing power by building a clientele selectively, the Moscow Exchange demonstrates the merits of another approach: domination of a single domestic market. The company provides clearing and custody services as well as a trading platform for financial products (equities, bonds, derivatives, foreign exchange) in Russia. The strength of the company’s competitive position is evident in its ability to coordinate price increases with system upgrades in such a way as to meet widespread approval from its client base. In the volatile Russian market, the Moscow Exchange is highly successful in providing a core financial service, demand for which would only increase if developments in the political arena lead to more sanctions or other actions that further isolate Russian firms from rival financial institutions in the West.

Table of Contents

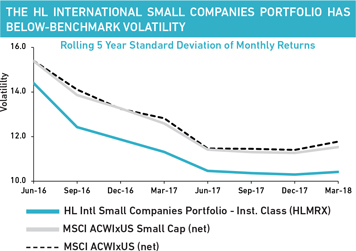

The Moscow Exchange illustrates our belief that, even in challenging environments, companies with steady fundamentals and financial strength can be resilient to a variety of shocks. Kinaxis shows how a company with a high-quality product and laser-focused management can gain market share without compromising profit margins in a highly competitive industry. SMS reminds us that, even in slowly growing economies, companies with innovative technological or service solutions for a precisely targeted market can flourish. We hold in our International Small Companies Portfolio a mix of these fundamentally strong small companies across a range of industries in developed, emerging, and frontier markets. The result of this broad diversification is a record of volatility below that of the benchmark and, in recent years, below that of international large caps as well (see chart below).

Source: eVestment alliance (eA); Harding Loevner International Small Companies Portfolio; MSCI Inc.; Data as of March 31, 2018.

GEOGRAPHIC EXPOSURE (%) at April 30, 2018

COUNTRY/REGION

|

PORTFOLIO

|

BENCHMARK1

| ||||||

CANADA

| 1.1 | 6.6 | ||||||

EMERGING MARKETS

| 16.4 | 22.2 | ||||||

EUROPE EMU

| 24.8 | 17.8 | ||||||

EUROPE EX-EMU

| 26.7 | 22.3 | ||||||

FRONTIER MARKETS2

| 7.0 | — | ||||||

JAPAN

| 13.3 | 22.2 | ||||||

MIDDLE EAST

| 1.3 | 1.0 | ||||||

PACIFIC EX-JAPAN

| 4.0 | 7.9 | ||||||

OTHER3

| 0.9 | — | ||||||

CASH

| 4.5 | — | ||||||

1MSCI All Country World ex-US Small Cap Index; 2Includes countries with less-developed markets outside the Index; 3Includes countries classified in countries outside the Index.

SECTOR EXPOSURE (%) at April 30, 2018

SECTOR

| PORTFOLIO

| BENCHMARK1

| ||||||

CONSUMER DISCRETIONARY

| 5.7 | 15.7 | ||||||

CONSUMER STAPLES

| 10.1 | 6.8 | ||||||

ENERGY

| 4.0 | 3.6 | ||||||

FINANCIALS

| 8.5 | 10.7 | ||||||

HEALTH CARE

| 14.3 | 7.6 | ||||||

INDUSTRIALS

| 21.4 | 19.0 | ||||||

INFORMATION TECHNOLOGY

| 23.4 | 11.8 | ||||||

MATERIALS

| 5.8 | 10.9 | ||||||

REAL ESTATE

| 0.0 | 10.0 | ||||||

TELECOM SERVICES

| 0.4 | 1.1 | ||||||

UTILITIES

| 1.9 | 2.8 | ||||||

CASH

| 4.5 | — | ||||||

1MSCI All Country World ex-US Small Cap Index.

⬛ PORTFOLIO HIGHLIGHTS

In the trailing six months, our complete sales included two companies for which our investment thesis had broken down. Dignity is a funeral services provider in the UK. Bereaved families are growing less accepting of high prices, in part due to the rising ease of comparing prices online. Dignity—which historically has differentiated itself by offering superior service—has responded to competitive pressures by slashing its prices. As a result, its profitability has suffered. Dignity will struggle to remain competitive, especially given its lack of a digital channel.

PAX Global makes electronic point-of-sale payment terminals in China. The market for terminals is shrinking in the country as merchants opt for online platforms such as WePay and Alipay. Our analyst’s original investment thesis anticipated that PAX would be able to move from a hardware maker to a software and services company. Despite the company’s investments in R&D, we no longer see PAX making this leap to keep up with the online payments platforms.

Other complete sales in the period included Clicks Group, GRUH Finance, Hiday Hidaka, and TPG Telecom. We also trimmed positions in several other strongly performing stocks that had become overvalued. We used the cash from these sales to establish positions in high-quality growth companies whose stocks appeared more attractively priced:

Security Bank, a commercial bank in the Philippines. We expect the bank to grow as demand for financial services accelerates in its home market. The company’s proven ability to assess credit risks places it at a strong competitive advantage in a national market that lacks a fully functioning credit bureau.

Diploma, an international group of businesses that sell technical products and services, including diagnostic equipment and supplies for hospital labs, filters and gaskets for industrial equipment, and specialty wiring used by aerospace, transportation,

Table of Contents

and defense companies. Each of Diploma’s businesses operates in lucrative niches. The company uses part of its strong cash flow to acquire more niche businesses with successful track records, expanding and diversifying Diploma’s client base.

We also purchased two South Korean companies—Hankook Tire and Coway. Other new purchases included UAE food and beverages manufacturer Agthia, Vietnamese steel producer Hoa Phat Group, and German software developer RIB Software. And we added to several existing positions because their valuations appeared attractive.

Portfolio Management Team Update

Anix Vyas, CFA was appointed co-lead portfolio manager of Harding Loevner’s International Small Companies Equity strategy, effective April 2, 2018. He joins Jafar Rizvi, CFA, who has served as a portfolio manager on the strategy since 2011. Anix joined Harding Loevner in 2013 as a research analyst and covers capital goods and materials companies—a role that he will continue as a portfolio manager.

TEN LARGEST HOLDINGS at April 30, 2018

COMPANY

| SECTOR | COUNTRY | % | |||||

REPLY | INFO TECHNOLOGY | ITALY | 2.7 | |||||

NAKANISHI | HEALTH CARE | JAPAN | 2.5 | |||||

ARIAKE | CONS STAPLES | JAPAN | 2.5 | |||||

CARL ZEISS MEDITEC | HEALTH CARE | GERMANY | 2.4 | |||||

ALTEN | INFO TECHNOLOGY | FRANCE | 2.4 | |||||

ABCAM | HEALTH CARE | UNITED KINGDOM | 2.4 | |||||