UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-07755

Nuveen Multistate Trust II

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Kevin J. McCarthy

Nuveen Investments

333 West Wacker Drive Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: February 28

Date of reporting period: August 31, 2011

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

Item 1. Reports to Stockholders.

Mutual Funds

Nuveen Municipal Bond Funds

Dependable, tax-free income because it’s not what you earn, it’s what you keep.®

Semi-Annual Report

August 31, 2011

| Share Class / Ticker Symbol | ||||||||

| Fund Name | Class A | Class B | Class C | Class I | ||||

Nuveen California High Yield Municipal Bond Fund | NCHAX | — | NCHCX | NCHRX | ||||

Nuveen California Municipal Bond Fund | NCAAX | NCBBX | NCACX | NCSPX | ||||

Nuveen California Municipal Bond Fund 2 (formerly Nuveen California Insured Municipal Bond Fund) | NCAIX | NCABX | NCAKX | NCIBX | ||||

LIFE IS COMPLEX.

Nuveen makes things e-simple.

It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready. No more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish.

Free e-Reports right to your e-mail!

www.investordelivery.com

If you receive your Nuveen Fund dividends and statements from your financial advisor or brokerage account.

OR

www.nuveen.com/accountaccess

If you receive your Nuveen Fund dividends and statements directly from Nuveen.

| Must be preceded by or accompanied by a prospectus. | NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE |

| 4 | ||||

| 5 | ||||

| 11 | ||||

| 15 | ||||

| 16 | ||||

| 17 | ||||

| 19 | ||||

| 39 | ||||

| 40 | ||||

| 41 | ||||

| 42 | ||||

| 48 | ||||

| 59 | ||||

| 66 | ||||

| 67 | ||||

Letter to Shareholders

Dear Shareholders,

The global economy continues to be weighed down by an unusual combination of pressures facing the larger developed economies. Japanese leaders continue to work through the economic aftereffects of the March 2011 earthquake and tsunami. Political leaders in Europe and the U.S. have resolved some of the near term fiscal problems, but the financial markets are not convinced that these leaders are able to address more complex longer term fiscal issues. Despite improved earnings and capital increases, the largest banks in these countries continue to be vulnerable to deteriorating mortgage portfolios and sovereign credit exposure, adding another source of uncertainty to the global financial system.

In the U.S., recent economic statistics indicate that the economic recovery may be losing momentum. Consumption, which represents about 70% of the gross domestic product, faces an array of challenges from seemingly intractable declines in housing values, increased energy costs and limited growth in the job market. The failure of Congress and the administration to agree on the debt ceiling increase on a timely basis and the deep divisions between the political parties over fashioning a balanced program to address growing fiscal imbalances that led to the recent S&P ratings downgrade add considerable uncertainty to the domestic economic picture.

On a more positive note, corporate earnings continue to hold up well and the municipal bond market is recovering from recent weakness as states and municipalities implement various programs to reduce their budgetary deficits. In addition, the Federal Reserve System has made it clear that it stands ready to take additional steps should the economic recovery falter. However, there are concerns that the Fed is approaching the limits of its resources to intervene in the economy.

These perplexing times highlight the importance of professional investment management. Your Nuveen investment team is working hard to develop an appropriate response to increased risk, and they continue to seek out opportunities created by stressful markets using proven investment disciplines designed to help your Fund achieve its investment objectives. On your behalf, we monitor their activities to assure that they maintain their investment disciplines.

As always, I encourage you to contact your financial consultant if you have any questions about your investment in a Nuveen Fund. On behalf of the other members of your Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

Robert P. Bremner

Chairman of the Board

October 21, 2011

| 4 | Nuveen Investments |

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investor Services, Inc. or Fitch, Inc. Credit ratings are subject to change. AAA, AA, A, and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Bonds backed by U.S. Government or agency securities are given an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by a national rating agency.

Portfolio managers John Miller and Scott Romans examine key investment strategies and the Funds’ performance during the six months ending August 31, 2011. John has 18 years of investment experience and has managed the Nuveen California High Yield Municipal Bond Fund since its inception in 2006. Scott has eleven years of investment experience and has managed the Nuveen California Municipal Bond Fund since 2003 and the Nuveen California Municipal Bond Fund 2 (formerly the Nuveen California Insured Municipal Bond Fund) since 2005.

How did the Funds perform during the six-month reporting period ending August 31, 2011?

The tables in the Fund Performance and Expense Ratios section of this report provide total return performance information for the six-month, one-year, five-year, ten-year and since inception periods ending August 31, 2011. Each Fund’s Class A Share total returns at net asset value (NAV) are compared with the performance of the California-specific and National Standard & Poor’s (S&P) Municipal Bond Indexes and the corresponding Lipper peer fund average. Over the six-month period, all three Funds outpaced the National S&P Index by varying degrees. Meanwhile, the Nuveen California High Yield Municipal Bond Fund also beat the S&P California Municipal Bond Index, the S&P High Yield Municipal Bond Index and its Lipper average by very wide margins. The Nuveen California Municipal Bond Fund surpassed the S&P California Municipal Bond Index and its Lipper peer group average, while the Nuveen California Municipal Bond Fund 2 trailed both of these measures.

During this reporting period, tax-exempt bonds benefited from a favorable investment environment, as this time span began just a few weeks after the municipal market bottomed after a deep downturn in late 2010 and early 2011. In addition, the Funds were helped by their emphasis on California-based securities — the state outperformed the national municipal market as a whole, thanks to an improved fiscal picture and significantly constrained supply that pushed bond prices upward. During the six months ending August 31, 2011, municipal bond issuance totaled roughly $135 billion nationwide, a 34% year-over-year decline. In comparison, new supply of California tax-exempt debt was about $19 billion during the same time span, reflecting a 37% year-over-year drop.

Nuveen California High Yield Municipal Bond Fund

As noted above, the Fund’s Class A Shares at NAV outpaced the national high-yield municipal bond market by a very wide margin. One notably helpful influence was the portfolio’s longer-than-average duration, meaning that it was more sensitive to changes in interest rates than the national index. The decline in rates fueled the tax-exempt bond market’s strong rally. As rates fall, bond prices generally rise, so the Fund’s performance

| Nuveen Investments | 5 |

was aided to a great extent by its relatively high sensitivity to interest rate movement. Similarly, as a high-yield portfolio, we were able to offer our shareholders a relatively high level of income, which can be especially valuable to investors seeking additional yield in such a low-interest-rate environment. Both of these factors contributed nicely to the Fund’s positive performance.

In addition, a number of the best-performing positions were higher-rated bonds that enjoyed healthy price growth during the period as municipal bond investors’ sentiment seemingly improved. Some of these higher-rated securities had been among the Fund’s biggest underperformers prior to the period. For example, we owned AA-rated hospital bonds issued by Sutter Health, a dominant health care provider in Northern California. These bonds had seen sizeable price depreciation during the market’s downturn in December 2010 and January 2011, but they made a nice recovery that boosted the Fund’s return. Other high-quality bonds that enjoyed similar price increases included securities issued for the Los Angeles International Airport, the University of Southern California and Bay Area Rapid Transit.

The Fund was also supported by relative price improvement among lower-rated, higher-yielding securities, including BBB-rated Children’s Hospital of Los Angeles bonds, whose financial position we believed was sound given the institution’s large endowment, fundraising capabilities and essential-service function. The portfolio also saw strong performance from bonds issued by the Drew School. Although these securities were unrated by major rating agencies, we conducted our own research and concluded the issuer was fundamentally solid and offered a very favorable risk/reward tradeoff. In fact, as market conditions improved, these bonds enjoyed very good price appreciation.

Nuveen California Municipal Bond Fund and Nuveen California Municipal Bond Fund 2

As noted, the Class A Shares at NAV of the Nuveen California Municipal Bond Fund outpaced the comparative indexes during the six-month reporting period ending August 31, 2011, while the Class A Shares at NAV of the Nuveen California Municipal Bond Fund 2 beat the national index and lagged the state index and Lipper peer group average.

The strongest positive contribution to the Funds’ results came from their interest-rate positioning. Due to the portfolios’ longer durations than the national index, the Funds’ performance was rewarded when municipal bond prices rose in response to falling interest rates. Yield curve positioning further added to results in relative terms. The California Municipal Bond Fund had less exposure to bonds with relatively short maturities, which proved helpful given the outperformance of longer-dated securities. While the Fund had good representation among longer-duration bonds, its slight underweighting in the longest bonds on the yield curve partially offset what was otherwise a very good performance story. Duration was a universally positive performance factor for the California Municipal Bond Fund 2, as the portfolio was both substantially underweighted in very-short-maturity bonds and overweighted on the long end of the yield curve.

To a lesser extent, sector positioning also proved helpful. An overweighting in the health care sector was a plus for both Funds, as California health care securities performed well

| 6 | Nuveen Investments |

compared to the rest of the tax-exempt bond market. Both Funds benefited from underweighting pre-refunded bonds, given that these very-short-duration, very-high-quality securities did not fare as well as bonds with longer maturities and lower credit ratings in an environment of decreased investor risk aversion. A modest overweighting in outperforming California tobacco-securitization bonds was helpful for the California Municipal Bond Fund’s performance, but the California Municipal Bond Fund 2 was underweighted in tobacco bonds for most of the period, which hampered this portfolio’s relative performance. On the other hand, a modest drawback for the California Municipal Bond Fund was the portfolio’s relative underweighting in local general obligation (GO) bonds. In California, local GOs are primarily school district bonds, and recently they have been zero-coupon bonds, which are very sensitive to interest-rate changes. As prices rallied during the period, this category disproportionately outperformed the municipal bond market as a whole. Being underweighted here was a disappointment for the California Municipal Bond Fund’s performance, while the California Municipal Bond Fund 2 was at an advantage by being overweighted in this category.

What strategies were used to manage the Funds during the six-month period?

Nuveen California High Yield Municipal Bond Fund

The Fund’s investment objective is to provide high current income exempt from regular federal, California state and, in some cases, California local income taxes. The Fund seeks to purchase below investment grade or medium to lower rated, high-yielding municipal bonds that offer attractive value in terms of current yields, prices, credit quality, liquidity or future prospects.

The Fund was fortunate to receive a moderate level of investment inflows during the period. This situation worked to the portfolio’s benefit because it enabled us to add new securities at a time when we saw some good investment opportunities at attractive prices in the tax-exempt municipal marketplace. With these inflows, we were able to buy bonds we believed could provide significant long-term value.

We invested a large portion of the Fund’s incoming assets into newly issued redevelopment district bonds, which raise tax-exempt money for community development projects. As we discussed in our last report to shareholders six months ago, redevelopment bonds were commonplace in California until recently, when their continued existence was put into question by an early proposal for a state budget resolution that called for their elimination. Although there was great confusion in the marketplace about the potential impact on bonds issued by these agencies, we viewed the development as a credit positive. As new issues were brought to market, we took advantage of their wider spreads and attractive structures. In all, we bought about a dozen redevelopment district bond issues for the portfolio — both new issues and from the secondary municipal bond market — and believed they provided the potential to help the Fund’s shareholders over the long term.

The rest of our new additions to the portfolio focused on “essential service” bonds, which we often favor because we believe these securities benefit from their vital nature to the communities they serve. Recent purchases included a variety of non-rated issues in health

| Nuveen Investments | 7 |

care, charter schools and community facilities districts that we believed represented good value at a reasonable amount of risk. The Fund also utilized derivatives (forward interest rate swaps) to reduce price volatility risk to movement in U.S. interest rates relative to the Fund’s benchmarks. During this period, the derivatives functioned as intended, and we continued to use these derivatives at the end of the period.

Nuveen California Municipal Bond Fund and Nuveen California Municipal Bond Fund 2

Effective as of the close of business on April 27, 2011, the Nuveen California Municipal Bond Fund 2 closed to new investors. Investors in the Fund as of that date may continue to invest in the Fund, including through the reinvestment of dividends and capital gains distributions.

In addition, effective May 31, 2011:

| • | The Fund is no longer required to invest at least 80% of its net assets in municipal securities that are covered by insurance guaranteeing the timely payment of principal and interest thereon. The Fund continues to be subject to the requirement that it invest at least 80% of its net assets in municipal bonds that pay interest that is exempt from regular federal and California personal income tax. |

| • | The Fund’s name changed from Nuveen California Insured Municipal Bond Fund. |

The Funds invest primarily in investment-grade municipal bonds in an effort to provide interest income exempt from regular federal, California state and, in some cases, California local income taxes.

New purchases for the Nuveen California Municipal Bond Fund and the Nuveen California Municipal Bond Fund 2 were relatively few during the period, reflecting both the limited supply in the municipal bond market and the low-interest-rate environment. These factors made it unattractive to try to restructure the portfolio, given that the bonds available for purchase were generally less desirable than the bonds we already owned in the portfolios. For the most part, our recent purchases were opportunistic in nature, occurring when we believed we had uncovered individual bond issues that gave the portfolio an unusual degree of value relative to the securities’ underlying risk. In the California Municipal Bond Fund, for example, we added to the portfolio’s exposure to health care and charter school bonds that we felt were favorable, as well as a non-rated charter school bond issue and a special-taxing-district bond issue we thought offered good value. Meanwhile, in the portfolio of the California Municipal Bond Fund 2, we took advantage of the Fund’s broadened ability to invest in non-insured municipal debt to add a position in California tobacco-securitization bonds that we were unable to own previously. We also bought a special-taxing district bond issue and a highly rated community college district local GO bond.

One unique opportunity that surfaced during the period was among redevelopment district bonds, in which we invested to the extent possible in both Funds. As mentioned earlier, in the Nuveen High Yield California Municipal Bond Fund, unusual circumstances led to a significant number of tax-exempt bond deals from redevelopment districts, which had previously been a popular source of issuance in California but whose future was put in doubt by a budget proposal that called for the elimination of redevelopment agencies. Because of this uncertainty, new issue supply came with wider spreads (and more

| 8 | Nuveen Investments |

attractive prices) relative to comparable AAA-rated tax-exempt bonds. Our ability to purchase these bonds was somewhat constrained by the fact that most of these deals were relatively small. Since we viewed the changes in this sector as broadly positive for redevelopment district bonds, we did find a lot of value in these types of bonds, given their high level of income, attractive structures (with ten years of call protection) and, we believe, substantial upside potential.

To fund our purchases for the California Municipal Bond Fund portfolio, we relied primarily on the proceeds of called bonds, as well as the sale of some very-short-maturity bonds that had strong demand in the marketplace and would have soon been leaving the portfolio anyway. Another approach was to realize profits on some of the bonds we bought at extremely low prices during the municipal bond market’s downturn in 2008 and 2009, as they now had achieved what we believed was their fair value and therefore had modest prospects for further appreciation.

Selling activity was somewhat more robust in the California Municipal Bond Fund 2 portfolio. In addition to utilizing the proceeds of called bonds and sales of short-maturity issues , we sold insured AA-rated and A-rated bonds whose outlook we saw as more limited than other opportunities available in the marketplace.

Risk Considerations

Mutual fund investing involves risk; principal loss is possible. Debt or fixed income securities are subject to credit risk and interest rate risk. The value of, and income generated by debt securities will decrease or increase based on changes in market interest rates. As interest rates rise, bond prices fall. Credit risk refers to an issuer’s ability to make interest and principal payments when due. Below investment grade bonds carry heightened credit risk and potential for default.

Dividend Information

All of the share classes of Nuveen California High Yield Municipal Bond Fund and Nuveen California Municipal Bond Fund 2 saw an increase in their monthly dividend in March 2011. Nuveen California Municipal Bond Fund had a dividend increase in Class B Shares in March 2011 and had an additional increase in all share classes in June 2011. There were no other dividend changes to any of the Funds’ share classes during the six-month period ending August 31, 2011.

Each Fund seeks to pay dividends at a rate that reflects the past and projected performance of the Fund. To permit a Fund to maintain a more stable monthly dividend, the Fund may pay dividends at a rate that may be more or less than the amount of net investment income actually earned by the Fund during the period. If the Fund has cumulatively earned more than it has paid in dividends, it will hold the excess in reserve as undistributed net investment income (UNII) as part of the Fund’s net asset value. Conversely, if the Fund has cumulatively paid in dividends more than it has earned, the excess will constitute a negative UNII that will likewise be reflected in the Fund’s net asset value. Each Fund will, over time, pay all its net investment income as dividends to shareholders. As of August 31, 2011, all three Funds had a positive UNII balances, based upon our best estimate, for tax purposes and a positive UNII balance for financial reporting purposes.

| Nuveen Investments | 9 |

[THIS PAGE INTENTIONALLY LEFT BLANK]

| 10 | Nuveen Investments |

Fund Performance and Expense Ratios (Unaudited)

The Fund Performance and Expense Ratios for each Fund are shown on the following three pages.

Returns quoted represent past performance, which is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Returns without sales charges would be lower if the sales charge were included. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Income is generally exempt from regular federal income taxes. Some income may be subject to state and local income taxes and to the federal alternative minimum tax. Capital gains, if any, are subject to tax.

Returns may reflect a contractual agreement between certain Funds and the investment adviser to waive certain fees and expenses; see Notes to Financial Statements, Footnote 7 — Management Fees and Other Transactions with Affiliates for more information. In addition, returns may reflect a voluntary expense limitation by the Funds’ investment adviser that may be modified or discontinued at any time without notice. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Returns reflect differences in sales charges and expenses, which are primarily differences in distribution and service fees. Fund returns assume reinvestment of dividends and capital gains.

Comparative index and Lipper return information is provided for the Funds’ Class A Shares at net asset value (NAV) only.

The expense ratios shown reflect the Funds’ total operating expenses (before fee waivers or expense reimbursements, if any) as shown in the Funds’ most recent prospectus. The expense ratios include management fees and other fees and expenses.

| Nuveen Investments | 11 |

Fund Performance and Expense Ratios (Unaudited) (continued)

Nuveen California High Yield Municipal Bond Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of August 31, 2011*

| Cumulative | Average Annual | |||||||||||||||

| 6-Month | 1-Year | 5-Year | Since Inception* | |||||||||||||

Class A Shares at NAV | 11.06% | 0.77% | 0.64% | 1.31% | ||||||||||||

Class A Shares at maximum Offering Price | 6.43% | -3.49% | -0.22% | 0.51% | ||||||||||||

Standard & Poor’s (S&P) California Municipal Bond Index** | 7.33% | 2.68% | 4.39% | 4.60% | ||||||||||||

Standard & Poor’s (S&P) High Yield Municipal Bond Index** | 7.15% | 3.03% | 2.24% | 2.84% | ||||||||||||

Standard & Poor’s (S&P) National Municipal Bond Index** | 6.56% | 2.62% | 4.60% | 4.93% | ||||||||||||

Lipper California Municipal Debt Classification Average** | 7.44% | 1.30% | 3.09% | 3.27% | ||||||||||||

Class C Shares | 10.79% | 0.27% | 0.11% | 0.76% | ||||||||||||

Class I Shares | 11.20% | 1.01% | 0.83% | 1.49% | ||||||||||||

Latest Calendar Quarter – Average Annual Total Returns as of September 30, 2011*

| Cumulative | Average Annual | |||||||||||||||

| 6-Month | 1-Year | 5-Year | Since Inception* | |||||||||||||

Class A Shares at NAV | 15.12% | 3.23% | 1.03% | 1.78% | ||||||||||||

Class A Shares at maximum Offering Price | 10.25% | -1.15% | 0.17% | 0.99% | ||||||||||||

Class C Shares | 14.84% | 2.71% | 0.49% | 1.23% | ||||||||||||

Class I Shares | 15.27% | 3.35% | 1.22% | 1.97% | ||||||||||||

Class A Shares have a maximum 4.20% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| Expense Ratios | ||

Class A Shares | 0.90% | |

Class C Shares | 1.45% | |

Class I Shares | 0.70% | |

| * | Six-month returns are cumulative; all other returns are annualized. Since inception returns are from 3/28/06. |

| ** | Refer to the Glossary of Terms Used in this Report for definitions. |

| 12 | Nuveen Investments |

Nuveen California Municipal Bond Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of August 31, 2011*

| Cumulative | Average Annual | |||||||||||||||

| 6-Month | 1-Year | 5-Year | 10-Year | |||||||||||||

Class A Shares at NAV | 7.82% | 2.64% | 3.68% | 4.20% | ||||||||||||

Class A Shares at maximum Offering Price | 3.34% | -1.71% | 2.79% | 3.75% | ||||||||||||

Standard & Poor’s (S&P) California Municipal Bond Index** | 7.33% | 2.68% | 4.39% | 4.81% | ||||||||||||

Standard & Poor’s (S&P) National Municipal Bond Index** | 6.56% | 2.62% | 4.60% | 4.93% | ||||||||||||

Lipper California Municipal Debt Classification Average** | 7.44% | 1.30% | 3.09% | 3.78% | ||||||||||||

Class B Shares w/o CDSC | 7.43% | 1.87% | 2.92% | 3.57% | ||||||||||||

Class B Shares w/CDSC | 2.43% | -2.05% | 2.74% | 3.57% | ||||||||||||

Class C Shares | 7.55% | 2.08% | 3.11% | 3.63% | ||||||||||||

Class I Shares | 7.93% | 2.93% | 3.90% | 4.41% | ||||||||||||

Latest Calendar Quarter – Average Annual Total Returns as of September 30, 2011*

| Cumulative | Average Annual | |||||||||||||||

| 6-Month | 1-Year | 5-Year | 10-Year | |||||||||||||

Class A Shares at NAV | 10.60% | 4.41% | 3.94% | 4.41% | ||||||||||||

Class A Shares at maximum Offering Price | 5.96% | 0.07% | 3.05% | 3.96% | ||||||||||||

Class B Shares w/o CDSC | 10.21% | 3.62% | 3.17% | 3.79% | ||||||||||||

Class B Shares w/CDSC | 5.21% | -0.36% | 3.00% | 3.79% | ||||||||||||

Class C Shares | 10.33% | 3.84% | 3.37% | 3.85% | ||||||||||||

Class I Shares | 10.60% | 4.50% | 4.14% | 4.62% | ||||||||||||

Class A Shares have a maximum 4.20% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class B Shares have a CDSC that begins at 5% for redemptions during the first year and declines periodically until after six years when the charge becomes 0%. Class B Shares automatically convert to Class A Shares eight years after purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| Expense Ratios | ||||

Class A Shares | 0.81% | |||

Class B Shares | 1.56% | |||

Class C Shares | 1.36% | |||

Class I Shares | 0.61% | |||

| * | Six-month returns are cumulative; all other returns are annualized. |

| ** | Refer to the Glossary of Terms Used in this Report for definitions. |

| Nuveen Investments | 13 |

Fund Performance and Expense Ratios (Unaudited) (continued)

Nuveen California Municipal Bond Fund 2

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of August 31, 2011*

| Cumulative | Average Annual | |||||||||||||||

| 6-Month | 1-Year | 5-Year | 10-Year | |||||||||||||

Class A Shares at NAV | 7.21% | 0.22% | 2.81% | 3.53% | ||||||||||||

Class A Shares at maximum Offering Price | 2.67% | -3.95% | 1.94% | 3.09% | ||||||||||||

Standard & Poor’s (S&P) California Municipal Bond Index** | 7.33% | 2.68% | 4.39% | 4.81% | ||||||||||||

Standard & Poor’s (S&P) National Municipal Bond Index** | 6.56% | 2.62% | 4.60% | 4.93% | ||||||||||||

Lipper California Municipal Debt Classification Average** | 7.44% | 1.30% | 3.09% | 3.78% | ||||||||||||

Class B Shares w/o CDSC | 6.91% | -0.51% | 2.05% | 2.91% | ||||||||||||

Class B Shares w/CDSC | 1.91% | -4.35% | 1.88% | 2.91% | ||||||||||||

Class C Shares | 6.95% | -0.34% | 2.23% | 2.96% | ||||||||||||

Class I Shares | 7.30% | 0.43% | 3.01% | 3.74% | ||||||||||||

Latest Calendar Quarter – Average Annual Total Returns as of September 30, 2011*

| Cumulative | Average Annual | |||||||||||||||

| 6-Month | 1-Year | 5-Year | 10-Year | |||||||||||||

Class A Shares at NAV | 10.44% | 2.05% | 3.02% | 3.75% | ||||||||||||

Class A Shares at maximum Offering Price | 5.79% | -2.21% | 2.13% | 3.31% | ||||||||||||

Class B Shares w/o CDSC | 10.00% | 1.29% | 2.26% | 3.12% | ||||||||||||

Class B Shares w/CDSC | 5.00% | -2.61% | 2.09% | 3.12% | ||||||||||||

Class C Shares | 10.07% | 1.49% | 2.45% | 3.18% | ||||||||||||

Class I Shares | 10.52% | 2.25% | 3.23% | 3.96% | ||||||||||||

Class A Shares have a maximum 4.20% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class B Shares have a CDSC that begins at 5% for redemptions during the first year and declines periodically until after six years when the charge becomes 0%. Class B Shares automatically convert to Class A Shares eight years after purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| Expense Ratios | ||||

Class A Shares | 0.83% | |||

Class B Shares | 1.58% | |||

Class C Shares | 1.38% | |||

Class I Shares | 0.63% | |||

| * | Six-month returns are cumulative; all other returns are annualized. |

| ** | Refer to the Glossary of Terms Used in this Report for definitions. |

| 14 | Nuveen Investments |

Yields (Unaudited) as of August 31, 2011

Dividend Yield is the most recent dividend per share (annualized) divided by the offering price per share.

The SEC 30-Day Yield is a standardized measure of a Fund’s yield that accounts for the future amortization of premiums or discounts of bonds held in the Fund’s portfolio. The SEC 30-Day Yield is computed under an SEC standardized formula and is based on the maximum offer price per share. Dividend Yield may differ from the SEC 30-Day Yield because the Fund may be paying out more or less than it is earning and it may not include the effect of amortization of bond premium.

The Taxable-Equivalent Yield represents the yield that must be earned on a fully taxable investment in order to equal the yield of the Fund on an after-tax basis at a specified tax rate. With respect to investments that generate qualified dividend income that is taxable at a maximum rate of 15%, the Taxable-Equivalent Yield is lower.

Nuveen California High Yield Municipal Bond Fund

| Dividend Yield | SEC 30-Day Yield | Taxable- Equivalent Yield1 | ||||||||||

Class A Shares2 | 6.25% | 6.52% | 9.98% | |||||||||

Class C Shares | 5.99% | 6.27% | 9.60% | |||||||||

Class I Shares | 6.76% | 7.01% | 10.74% | |||||||||

Nuveen California Municipal Bond Fund

| Dividend Yield | SEC 30-Day Yield | Taxable- Equivalent Yield1 | ||||||||||

Class A Shares2 | 4.50% | 4.20% | 6.43% | |||||||||

Class B Shares | 3.98% | 3.62% | 5.54% | |||||||||

Class C Shares | 4.17% | 3.86% | 5.91% | |||||||||

Class I Shares | 4.88% | 4.59% | 7.03% | |||||||||

Nuveen California Municipal Bond Fund 2

| Dividend Yield | SEC 30-Day Yield | Taxable- Equivalent Yield1 | ||||||||||

Class A Shares2 | 4.16% | 3.92% | 6.00% | |||||||||

Class B Shares | 3.61% | 3.33% | 5.10% | |||||||||

Class C Shares | 3.82% | 3.54% | 5.42% | |||||||||

Class I Shares | 4.51% | 4.29% | 6.57% | |||||||||

| 1 | The Taxable-Equivalent Yield is based on the Fund’s SEC 30-Day Yield on the indicated date and a combined federal and state income tax rate of 34.7%. |

| 2 | The SEC Yield for Class A shares quoted in the table reflects the maximum sales load. Investors paying a reduced load because of volume discounts, investors paying no load because they qualify for one of the several exclusions from the load, and existing shareholders who previously paid a load but would like to know the SEC Yield applicable to their shares on a going-forward basis, should understand that the SEC Yield effectively applicable to them would be higher than the figure quoted in the table. |

| Nuveen Investments | 15 |

Holding Summaries (Unaudited) as of August 31, 2011

This data relates to the securities held in each Fund’s portfolio of investments. It should not be construed as a measure of performance for the Fund itself.

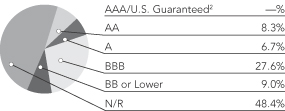

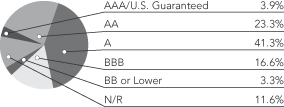

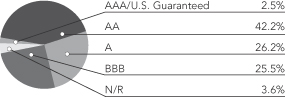

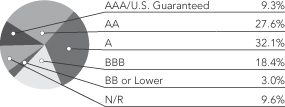

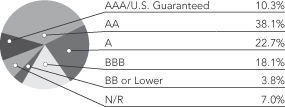

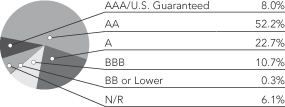

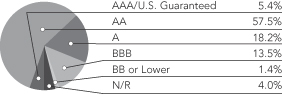

Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investor Services, Inc. or Fitch, Inc. Credit ratings are subject to change. AAA, AA, A, and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Bonds backed by U.S. Government or agency securities are given an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by a national rating agency.

Nuveen California High Yield Municipal Bond Fund

Bond Credit Quality1

Nuveen California Municipal Bond Fund

Bond Credit Quality3

Nuveen California Municipal Bond Fund 2

Bond Credit Quality3

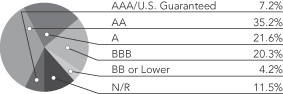

| Portfolio Composition1 | ||||

| Tax Obligation/Limited | 44.0% | |||

| Health Care | 13.3% | |||

| Education and Civic Organizations | 12.6% | |||

| Transportation | 8.9% | |||

| Long-Term Care | 4.6% | |||

| Consumer Staples | 4.5% | |||

| Other | 12.1% | |||

| Portfolio Composition3 | ||||

| Tax Obligation/Limited | 33.5% | |||

| Health Care | 20.0% | |||

| Tax Obligation/General | 13.3% | |||

| Utilities | 5.8% | |||

| Consumer Staples | 4.6% | |||

| Education and Civic Organizations | 4.5% | |||

| Water and Sewer | 4.5% | |||

| Other | 13.8% | |||

| Portfolio Composition3 | ||||

| Tax Obligation/Limited | 33.3% | |||

| Tax Obligation/General | 26.8% | |||

| Transportation | 8.6% | |||

| Health Care | 8.4% | |||

| Education and Civic Organizations | 6.3% | |||

| Utilities | 6.2% | |||

| Housing/Multifamily | 5.9% | |||

| Other | 4.5% | |||

| 1 | As a percentage of total investments (excluding investments in derivatives) as of August 31, 2011. Holdings are subject to change. |

| 2 | Rounds to less than 0.1%. |

| 3 | As a percentage of total investments as of August 31, 2011. Holdings are subject to change. |

| 16 | Nuveen Investments |

As a shareholder of one or more of the Funds, you incur two types of costs: (1) transaction costs, including up-front and back-end sales charges (loads) or redemption fees, where applicable; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees, where applicable; and other Fund expenses. The Examples below are intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The Examples below are based on an investment of $1,000 invested at the beginning of the period and held for the period.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your share class, in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance,” provides information about hypothetical account values and hypothetical expenses based on the respective Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds or share classes. In addition, if these transaction costs were included, your costs would have been higher.

Nuveen California High Yield Municipal Bond Fund

| Hypothetical Performance | ||||||||||||||||||||||||||

| Actual Performance | (5% annualized return before expenses) | |||||||||||||||||||||||||

| A Shares | C Shares | I Shares | A Shares | C Shares | I Shares | |||||||||||||||||||||

| Beginning Account Value (3/01/11) | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | ||||||||||||||

| Ending Account Value (8/31/11) | $ | 1,110.60 | $ | 1,107.90 | $ | 1,112.00 | $ | 1,020.66 | $ | 1,017.90 | $ | 1,021.67 | ||||||||||||||

| Expenses Incurred During Period | $ | 4.72 | $ | 7.63 | $ | 3.66 | $ | 4.52 | $ | 7.30 | $ | 3.51 | ||||||||||||||

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of .89%, 1.44% and .69% for Classes A, C and I, respectively, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period).

Nuveen California Municipal Bond Fund

| Hypothetical Performance | ||||||||||||||||||||||||||||||||||

| Actual Performance | (5% annualized return before expenses) | |||||||||||||||||||||||||||||||||

| A Shares | B Shares | C Shares | I Shares | A Shares | B Shares | C Shares | I Shares | |||||||||||||||||||||||||||

| Beginning Account Value (3/01/11) | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | ||||||||||||||||||

| Ending Account Value (8/31/11) | $ | 1,078.20 | $ | 1,074.30 | $ | 1,075.50 | $ | 1,079.30 | $ | 1,021.01 | $ | 1,017.24 | $ | 1,018.25 | $ | 1,022.02 | ||||||||||||||||||

| Expenses Incurred During Period | $ | 4.28 | $ | 8.19 | $ | 7.15 | $ | 3.24 | $ | 4.17 | $ | 7.96 | $ | 6.95 | $ | 3.15 | ||||||||||||||||||

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of .82%, 1.57%, 1.37% and .62% for Classes A, B, C and I, respectively, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period).

| Nuveen Investments | 17 |

Expense Examples (Unaudited) (continued)

Nuveen California Municipal Bond Fund 2

| Hypothetical Performance | ||||||||||||||||||||||||||||||||||

| Actual Performance | (5% annualized return before expenses) | |||||||||||||||||||||||||||||||||

| A Shares | B Shares | C Shares | I Shares | A Shares | B Shares | C Shares | I Shares | |||||||||||||||||||||||||||

| Beginning Account Value (3/01/11) | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | ||||||||||||||||||

| Ending Account Value (8/31/11) | $ | 1,072.10 | $ | 1,069.10 | $ | 1,069.50 | $ | 1,073.00 | $ | 1,020.91 | $ | 1,017.14 | $ | 1,018.15 | $ | 1,021.92 | ||||||||||||||||||

| Expenses Incurred During Period | $ | 4.38 | $ | 8.27 | $ | 7.23 | $ | 3.33 | $ | 4.27 | $ | 8.06 | $ | 7.05 | $ | 3.25 | ||||||||||||||||||

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of .84%, 1.59%, 1.39% and .64% for Classes A, B, C and I, respectively, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period).

| 18 | Nuveen Investments |

Portfolio of Investments (Unaudited)

Nuveen California High Yield Municipal Bond Fund

August 31, 2011

| Principal Amount (000) | Description (1) | Optional Call Provisions (2) | Ratings (3) | Value | ||||||||||||||

Consumer Discretionary – 1.9% | ||||||||||||||||||

| $ | 280 | Austin Convention Enterprises Inc., Texas, Convention Center Hotel Revenue Bonds, Third Tier Series 2001C, 9.750%, 1/01/26 | 1/12 at 100.00 | N/R | $ | 283,377 | ||||||||||||

| 1,000 | Lombard Public Facilities Corporation, Illinois, First Tier Conference Center and Hotel Revenue Bonds, Series 2005A-2, 5.500%, 1/01/36 – ACA Insured | 1/16 at 100.00 | B– | 696,190 | ||||||||||||||

| 1,000 | Louisiana Local Government Environmental Facilities and Community Development Authority, Revenue Bonds, Southgate Suites Hotel LLC Project, Series 2007A, 6.750%, 12/15/37 (5), (6) | 12/17 at 100.00 | N/R | 505,320 | ||||||||||||||

| 500 | Morongo Band of Mission Indians, California, Enterprise Revenue Bonds, Series 2008B, 6.500%, 3/01/28 | 3/18 at 100.00 | N/R | 470,415 | ||||||||||||||

| 345 | Norfolk Economic Development Authority, Virginia, Empowerment Zone Facility Revenue Bonds, BBL Old Dominion University LLC Project Revenue Bonds, Series 2006B, 5.625%, 11/01/15 (Alternative Minimum Tax) | No Opt. Call | N/R | 302,617 | ||||||||||||||

| 3,125 | Total Consumer Discretionary | 2,257,919 | ||||||||||||||||

Consumer Staples – 4.5% | ||||||||||||||||||

| 1,000 | California County Tobacco Securitization Agency, Tobacco Settlement Asset-Backed Bonds, Golden Gate Tobacco Funding Corporation, Turbo, Series 2007A, 5.000%, 6/01/47 | 6/17 at 100.00 | N/R | 599,760 | ||||||||||||||

Golden State Tobacco Securitization Corporation, California, Tobacco Settlement Asset-Backed Bonds, Series 2007A-1: | ||||||||||||||||||

| 2,750 | 5.000%, 6/01/33 | 6/17 at 100.00 | Baa3 | 1,925,165 | ||||||||||||||

| 1,000 | 5.125%, 6/01/47 | 6/17 at 100.00 | Baa3 | 645,280 | ||||||||||||||

| 1,600 | 5.750%, 6/01/47 | 6/17 at 100.00 | Baa3 | 1,133,696 | ||||||||||||||

| 1,000 | Golden State Tobacco Securitization Corporation, California, Tobacco Settlement Asset-Backed Bonds, Series 2007A-2, 0.000%, 6/01/37 | 6/22 at 100.00 | BB+ | 620,020 | ||||||||||||||

Tobacco Securitization Authority of Southern California, Tobacco Settlement Asset-Backed Bonds, San Diego County Tobacco Asset Securitization Corporation, Senior Series 2001A: | ||||||||||||||||||

| 50 | 5.000%, 6/01/37 | 6/14 at 100.00 | BBB | 33,893 | ||||||||||||||

| 750 | 5.125%, 6/01/46 | 6/14 at 100.00 | BBB | 477,113 | ||||||||||||||

| 8,150 | Total Consumer Staples | 5,434,927 | ||||||||||||||||

Education and Civic Organizations – 12.6% | ||||||||||||||||||

| 1,065 | California Educational Facilities Authority, Revenue Bonds, Dominican University, Series 2006, 5.000%, 12/01/36 | 12/16 at 100.00 | Baa3 | 910,106 | ||||||||||||||

| 75 | California Educational Facilities Authority, Revenue Bonds, University of Redlands, Series 2005A, 5.000%, 10/01/35 | 10/15 at 100.00 | A3 | 70,500 | ||||||||||||||

| 1,250 | California Educational Facilities Authority, Revenue Bonds, University of Southern California, Tender Option Bond Trust 3144, | No Opt. Call | Aa1 | 1,535,050 | ||||||||||||||

| 100 | California Educational Facilities Authority, Revenue Bonds, University of the Pacific, Series 2006, 5.000%, 11/01/36 | 11/15 at 100.00 | A2 | 99,709 | ||||||||||||||

California Educational Facilities Authority, Revenue Bonds, Woodbury University, Series 2006: | ||||||||||||||||||

| 1,165 | 5.000%, 1/01/30 | 1/15 at 100.00 | Baa3 | 1,003,881 | ||||||||||||||

| 500 | 5.000%, 1/01/36 | 1/15 at 100.00 | Baa3 | 412,065 | ||||||||||||||

| 1,000 | California Municipal Finance Authority, Education Revenue Bonds, American Heritage Education Foundation Project, Series 2006A, 5.250%, 6/01/36 | 6/16 at 100.00 | BBB– | 811,430 | ||||||||||||||

| 1,335 | California Municipal Finance Authority, Educational Facilities Revenue Bonds, OCEAA Project, Series 2008A, 7.000%, 10/01/39 | No Opt. Call | N/R | 1,279,691 | ||||||||||||||

| 1,500 | California Municipal Finance Authority, Revenue Refunding Bonds, Biola University, Series 2008A, 5.875%, 10/01/34 | 4/18 at 100.00 | Baa1 | 1,506,810 | ||||||||||||||

| 1,000 | California Statewide Communitities Development Authority, Charter School Revenue Bonds, Rocketship 4 - Mosaic Elementary Charter School, | 12/21 at 100.00 | N/R | 1,005,200 | ||||||||||||||

| Nuveen Investments | 19 |

Portfolio of Investments (Unaudited)

Nuveen California High Yield Municipal Bond Fund (continued)

August 31, 2011

| Principal Amount (000) | Description (1) | Optional Call Provisions (2) | Ratings (3) | Value | ||||||||||||||

Education and Civic Organizations (continued) | ||||||||||||||||||

| $ | 750 | California Statewide Communitities Development Authority, School Facility Revenue Bonds, Alliance College-Ready Public Schools, Series 2011A, 7.000%, 7/01/46 | 7/21 at 100.00 | N/R | $ | 728,048 | ||||||||||||

| 815 | California Statewide Community Development Authority, Charter School Revenue Bonds, Rocklin Academy Charter, Series 2011A, 8.250%, 6/01/41 | 6/21 at 100.00 | BB+ | 820,787 | ||||||||||||||

| 500 | California Statewide Community Development Authority, Revenue Bonds, California Baptist University, Series 2007A, 5.500%, 11/01/38 | No Opt. Call | N/R | 424,245 | ||||||||||||||

| 2,135 | California Statewide Community Development Authority, Revenue Bonds, Drew School, Series 2007, 5.300%, 10/01/37 | 10/15 at 102.00 | N/R | 2,000,431 | ||||||||||||||

| 200 | California Statewide Community Development Authority, Revenue Bonds, International School of the Peninsula, Palo Alto, California, Series 2006, 5.000%, 11/01/29 | 11/16 at 100.00 | N/R | 162,214 | ||||||||||||||

| 400 | California Statewide Community Development Authority, Revenue Bonds, Montessori in Redlands School, Series 2007A, 5.125%, 12/01/36 | 12/16 at 100.00 | N/R | 294,808 | ||||||||||||||

| 100 | California Statewide Community Development Authority, Revenue Bonds, Viewpoint School, Series 2004, 5.000%, 10/01/28 – ACA Insured | 10/14 at 100.00 | BBB | 92,725 | ||||||||||||||

| 200 | Hawaii State Department of Budget and Finance, Private School Revenue Bonds, Montessori of Maui, Series 2007, 5.500%, 1/01/37 | 2/17 at 100.00 | N/R | 166,676 | ||||||||||||||

| 600 | La Vernia Education Financing Corporation, Texas, Charter School Revenue Bonds, Riverwalk Education Foundation, Series 2007A, 5.450%, 8/15/36 | 2/12 at 100.00 | N/R | 473,898 | ||||||||||||||

| 100 | Pima County Industrial Development Authority, Arizona, Choice Education and Development Charter School Revenue Bonds, Series 2006, 6.375%, 6/01/36 | 6/16 at 100.00 | N/R | 81,356 | ||||||||||||||

| 65 | Pima County Industrial Development Authority, Arizona, Educational Revenue Bonds, Paradise Education Center Charter School, Series 2006, 6.000%, 6/01/36 | 6/16 at 100.00 | BBB– | 56,375 | ||||||||||||||

| 390 | Pingree Grove Village, Illinois, Charter School Revenue Bonds, Cambridge Lakes Learning Center, Series 2007, 6.000%, 6/01/36 | 6/16 at 102.00 | N/R | 300,632 | ||||||||||||||

| 1,060 | San Diego County, California, Certificates of Participation, Burnham Institute, Series 2006, 5.000%, 9/01/34 | 9/15 at 102.00 | Baa3 | 900,618 | ||||||||||||||

| 16,305 | Total Education and Civic Organizations | 15,137,255 | ||||||||||||||||

Health Care – 13.4% | ||||||||||||||||||

| 50 | California Health Facilities Financing Authority, Health Facility Revenue Bonds, Adventist Health System/West, Series 2003A, 5.000%, 3/01/33 | 3/13 at 100.00 | A | 48,526 | ||||||||||||||

| 830 | California Health Facilities Financing Authority, Hospital Revenue Bonds, Downey Community Hospital, Series 1993, 5.750%, 5/15/15 (4) | 11/11 at 100.00 | N/R | 676,334 | ||||||||||||||

| 1,000 | California Municipal Financing Authority, Certificates of Participation, Community Hospitals of Central California, Series 2007, 5.250%, 2/01/27 | 2/17 at 100.00 | Baa2 | 941,480 | ||||||||||||||

| 1,000 | California Statewide Communities Development Authority, Revenue Bonds, ValleyCare Health System, Series 2007A, 5.125%, 7/15/31 | 7/17 at 100.00 | N/R | 858,680 | ||||||||||||||

| 495 | California Statewide Community Development Authority, Health Facility Revenue Bonds, Catholic Healthcare West, Series 2008A, 5.500%, 7/01/30 | 7/17 at 100.00 | A | 509,117 | ||||||||||||||

| 2,000 | California Statewide Community Development Authority, Revenue Bonds, Childrens Hospital of Los Angeles, Series 2007, 5.000%, 8/15/47 | 8/17 at 100.00 | BBB+ | 1,627,280 | ||||||||||||||

California Statewide Community Development Authority, Revenue Bonds, Daughters of Charity Health System, Series 2005A: | ||||||||||||||||||

| 750 | 5.250%, 7/01/30 | 7/15 at 100.00 | BBB | 636,668 | ||||||||||||||

| 515 | 5.250%, 7/01/35 | 7/15 at 100.00 | BBB | 421,929 | ||||||||||||||

| 495 | 5.000%, 7/01/39 | 7/15 at 100.00 | BBB | 382,531 | ||||||||||||||

| 715 | California Statewide Community Development Authority, Revenue Bonds, Sutter Health, Tender Option Bond Trust 3048, 18.112%, 11/15/32 (IF) | 5/18 at 100.00 | AA– | 670,155 | ||||||||||||||

California Statewide Community Development Authority, Revenue Bonds, Sutter Health, Tender Option Bond Trust 3102: | ||||||||||||||||||

| 375 | 18.317%, 11/15/46 (IF) | 11/16 at 100.00 | AA– | 353,089 | ||||||||||||||

| 1,285 | 18.322%, 11/15/48 (IF) | 5/18 at 100.00 | AA– | 1,204,405 | ||||||||||||||

| 20 | Nuveen Investments |

| Principal Amount (000) | Description (1) | Optional Call Provisions (2) | Ratings (3) | Value | ||||||||||||||

Health Care (continued) | ||||||||||||||||||

| $ | 1,000 | California Statewide Communities Development Authority, Revenue Bonds, Saint Joseph Health System, Trust 2554, 18.324%, 7/01/47 – AGM Insured (IF) | 7/18 at 100.00 | AA+ | $ | 1,022,040 | ||||||||||||

| 1,490 | Loma Linda, California, Hospital Revenue Bonds, Loma Linda University Medical Center, Series 2008A, 8.250%, 12/01/38 | 12/17 at 100.00 | BBB | 1,642,814 | ||||||||||||||

| 1,060 | Oak Valley Hospital District, Stanislaus County, California, Revenue Bonds, Series 2010A, 7.000%, 11/01/35 | 11/20 at 100.00 | BBB– | 1,078,486 | ||||||||||||||

| 500 | Palomar Pomerado Health Care District, California, Certificates of Participation, Series 2009, 6.750%, 11/01/39 | 11/19 at 100.00 | Baa3 | 510,045 | ||||||||||||||

| 500 | Palomar Pomerado Health Care District, California, Certificates of Participation, Series 2010, 6.000%, 11/01/41 | 11/20 at 100.00 | Baa3 | 468,945 | ||||||||||||||

| 1,000 | San Buenaventura, California, Revenue Bonds, Community Memorial Health System, Series 2011, 8.000%, 12/01/26 | 12/21 at 100.00 | BB | 1,065,330 | ||||||||||||||

| 100 | Sierra Kings Health Care District, Fresno County, California, Revenue Bonds, Series 2006A, 5.750%, 12/01/36 | 12/16 at 100.00 | N/R | 59,835 | ||||||||||||||

| 2,000 | Tulare Local Health Care District, California, Revenue Bonds, Series 2007, 5.200%, 11/01/32 | 11/17 at 100.00 | N/R | 1,811,680 | ||||||||||||||

| 60 | Weatherford Hospital Authority, Oklahoma, Sales Tax Revenue Bonds, Series 2006, 6.000%, 5/01/31 | 5/16 at 103.00 | N/R | 50,061 | ||||||||||||||

| 17,220 | Total Health Care | 16,039,430 | ||||||||||||||||

Housing/Multifamily – 4.2% | ||||||||||||||||||

| 1,400 | California Municipal Finance Authority, Mobile Home Park Revenue Bonds, Caritas Projects Series 2010B, 7.250%, 8/15/45 | 8/20 at 100.00 | N/R | 1,397,298 | ||||||||||||||

| 400 | California Municipal Finance Authority, Revenue Bonds, University Students Coop Association, Series 2007, 4.750%, 4/01/27 | 4/17 at 100.00 | BBB– | 367,284 | ||||||||||||||

| 1,000 | California Statewide Community Development Authority, Lancer Educational Student Housing Revenue Bonds, California Baptist University, Series 2007, 5.625%, 6/01/33 | 6/17 at 102.00 | N/R | 858,350 | ||||||||||||||

| 375 | California Statewide Community Development Authority, Multifamily Housing Revenue Bonds, Magnolia City Lights, Series 1999X, 6.650%, 7/01/39 | 11/11 at 100.00 | N/R | 335,651 | ||||||||||||||

| 120 | Multifamily Housing Revenue Bond Pass-Through Certificates, California, Series 2001-17, Stanford Arms Seniors Apartments 01-P2, 5.750%, 11/01/34 (Mandatory put 11/01/16) (Alternative Minimum Tax) | 12/11 at 100.00 | N/R | 120,068 | ||||||||||||||

| 1,250 | Richmond, California, Joint Powers Financing Agency Multifamily Housing Revenue Bonds, Westridge Hilltop Apartments, Series 2007, 5.000%, 12/15/33 | 12/12 at 100.00 | Baa1 | 1,026,938 | ||||||||||||||

| 734 | Ventura County Area Housing Authority, California, Mira Vista Senior Apartments Project, Junior Subordinate Series 2006C, 6.500%, 12/01/39 (Mandatory put 7/01/16) (Alternative Minimum Tax) | No Opt. Call | N/R | 675,148 | ||||||||||||||

| 485 | Wilson County Health and Educational Facilities Board, Tennessee, Senior Living Revenue Bonds, Rutland Place, Series 2007A, 6.300%, 7/01/37 (4) | 7/17 at 100.00 | N/R | 293,289 | ||||||||||||||

| 5,764 | Total Housing/Multifamily | 5,074,026 | ||||||||||||||||

Housing/Single Family – 0.7% | ||||||||||||||||||

| 500 | California Housing Finance Agency, California, Home Mortgage Revenue Bonds, Series 2007E, 4.800%, 8/01/37 (Alternative Minimum Tax) | 2/17 at 100.00 | Baa1 | 426,530 | ||||||||||||||

| 600 | California Housing Finance Agency, Home Mortgage Revenue Bonds, Tender Option Bond Trust 3206, 8.115%, 2/01/24 (Alternative Minimum Tax) (IF) | 2/16 at 100.00 | BBB | 393,816 | ||||||||||||||

| 1,100 | Total Housing/Single Family | 820,346 | ||||||||||||||||

Industrials – 0.4% | ||||||||||||||||||

| 65 | California Pollution Control Financing Authority, Solid Waste Disposal Revenue Bonds, Waste Management Inc., Series 2002A, 5.000%, 1/01/22 (Alternative Minimum Tax) | 1/16 at 102.00 | BBB | 66,146 | ||||||||||||||

| Nuveen Investments | 21 |

Portfolio of Investments (Unaudited)

Nuveen California High Yield Municipal Bond Fund (continued)

August 31, 2011

| Principal Amount (000) | Description (1) | Optional Call Provisions (2) | Ratings (3) | Value | ||||||||||||||

Industrials (continued) | ||||||||||||||||||

| $ | 1,000 | California Statewide Communities Development Authority, Revenue Bonds, EnerTech Regional Biosolids Project, Series 2007A, 5.500%, 12/01/33 (Alternative Minimum Tax) (5) | No Opt. Call | CCC+ | $ | 220,340 | ||||||||||||

| 250 | Kootenai County Industrial Development Corporation, Idaho, Industrial Development Revenue Bonds, Coer d’Alene Fiber Fuels, Inc., Series 2006, 6.750%, 12/01/26 (4), (5) | 12/16 at 100.00 | N/R | 62,125 | ||||||||||||||

| 100 | Louisiana Local Government Environmental Facilities and Community Development Authority, Carter Plantation Hotel Project Revenue Bonds, Series 2006A, 6.000%, 9/01/36 (4), (5) | 9/16 at 100.00 | N/R | 18,800 | ||||||||||||||

| 750 | Western Reserve Port Authority, Ohio, Solid Waste Facility Revenue Bonds, Central Waste Inc., Series 2007A, 6.350%, 7/01/27 (Alternative Minimum Tax) (4), (5) | 7/17 at 102.00 | N/R | 135,225 | ||||||||||||||

| 2,165 | Total Industrials | 502,636 | ||||||||||||||||

Long-Term Care – 4.6% | ||||||||||||||||||

California Municipal Finance Authority, Revenue Bonds, Harbor Regional Center Project, Series 2009: | ||||||||||||||||||

| 500 | 8.000%, 11/01/29 | 11/19 at 100.00 | Baa1 | 543,580 | ||||||||||||||

| 1,040 | 8.500%, 11/01/39 | 11/19 at 100.00 | Baa1 | 1,143,095 | ||||||||||||||

| 1,500 | California Statewide Communities Development Authority, Revenue Bonds, Inland Regional Center Project, Series 2007, 5.375%, 12/01/37 | 12/17 at 100.00 | Baa1 | 1,391,625 | ||||||||||||||

| 1,000 | California Statewide Community Development Authority, Revenue Bonds, Hollenbeck Palms, Magnolia Assisted Living, Series 2007A, 4.600%, 2/01/37 – RAAI Insured (Alternative Minimum Tax) | 2/17 at 100.00 | N/R | 736,500 | ||||||||||||||

| 1,000 | Fulton County Residential Care Facilities Authority, Georgia, Revenue Bonds, Elderly Care, Lenbrook Square Project, Series 2006A, 5.125%, 7/01/37 | 7/17 at 100.00 | N/R | 678,790 | ||||||||||||||

| 50 | Louisiana Local Government Environmental Facilities and Community Development Authority, Revenue Bonds, CDF Healthcare of Louisiana LLC, Series 2006A, 7.000%, 6/01/36 | 6/16 at 101.00 | N/R | 41,452 | ||||||||||||||

| 1,000 | San Diego County, California, Certificates of Participation, San Diego-Imperial Counties Developmental Services Foundation Project, Series 2002, 5.500%, 9/01/27 | 9/12 at 100.00 | Baa1 | 984,340 | ||||||||||||||

| 6,090 | Total Long-Term Care | 5,519,382 | ||||||||||||||||

Tax Obligation/General – 2.1% | ||||||||||||||||||

| 390 | Bessemer, Alabama, General Obligation Warrants, Series 2007, 6.500%, 2/01/37 | 2/17 at 102.00 | N/R | 276,530 | ||||||||||||||

| 725 | Guam Government, General Obligation Bonds, 2009 Series A, 7.000%, 11/15/39 | No Opt. Call | B+ | 748,563 | ||||||||||||||

| 500 | Guam, General Obligation Bonds, Series 2007A, 5.250%, 11/15/37 | 11/17 at 100.00 | B+ | 427,910 | ||||||||||||||

| 250 | Palomar Pomerado Health, California, General Obligation Bonds, Tender Option Bond Trust 4683, 16.768%, 8/01/37 – NPFG Insured (IF) (7) | 8/17 at 100.00 | AA | 247,820 | ||||||||||||||

| 2,295 | William S. Hart Union High School District, Los Angeles County, California, General Obligation Bonds, Election 2001 Series 2005B, 0.000%, 9/01/27 – AGM Insured (7) | No Opt. Call | AA+ | 854,910 | ||||||||||||||

| 4,160 | Total Tax Obligation/General | 2,555,733 | ||||||||||||||||

Tax Obligation/Limited – 44.1% | ||||||||||||||||||

| 1,000 | Azusa Redevelopment Agency, California, Tax Allocation Refunding Bonds, Merged West End Development, Series 2007B, 5.300%, 8/01/36 | No Opt. Call | N/R | 762,010 | ||||||||||||||

| 740 | Azusa, California, Special Tax Bonds, Community Facilities District 2005-1 Rosedale Improvement Area 1, Series 2007, 5.000%, 9/01/27 | 9/17 at 100.00 | N/R | 615,739 | ||||||||||||||

| 1,000 | Beaumont Financing Authority, California, Local Agency Revenue Bonds, Improvement Area 8C, Series 2007E, 6.250%, 9/01/38 | No Opt. Call | N/R | 954,950 | ||||||||||||||

Beaumont Financing Authority, California, Local Agency Revenue Bonds, Improvement Area 8D & 17B, Series 2009B: | ||||||||||||||||||

| 225 | 8.875%, 9/01/34 | 9/12 at 103.00 | N/R | 236,158 | ||||||||||||||

| 450 | 8.625%, 9/01/39 | 9/12 at 103.00 | N/R | 470,885 | ||||||||||||||

| 300 | Beaumont Financing Authority, California, Local Agency Revenue Bonds, Series 2006B, 5.050%, 9/01/37 | 9/12 at 101.00 | N/R | 239,745 | ||||||||||||||

| 22 | Nuveen Investments |

| Principal Amount (000) | Description (1) | Optional Call Provisions (2) | Ratings (3) | Value | ||||||||||||||

Tax Obligation/Limited (continued) | ||||||||||||||||||

| $ | 1,000 | Borrego Water District, California, Community Facilities District 2007-1 Montesoro, Special Tax Bonds, Series 2007, 5.750%, 8/01/32 (4), (5) | 8/17 at 102.00 | N/R | $ | 370,000 | ||||||||||||

| 1,000 | California Statewide Communities Development Authority, Recovery Zone Facility Bonds, SunEdison Huntington Beach Solar Projects, Series 2010, 7.500%, 1/01/31 | 1/21 at 100.00 | N/R | 1,013,350 | ||||||||||||||

| 1,415 | California Statewide Communities Development Authority, Recovery Zone Facility Bonds, SunEdison Irvine Unified School District Solar Projects, Series 2010, 7.500%, 7/01/30 | 1/20 at 100.00 | N/R | 1,432,320 | ||||||||||||||

| 250 | California Statewide Community Development Authority, Revenue Bonds, Epidaurus Project, Series 2004A, 7.750%, 3/01/34 | 3/14 at 102.00 | N/R | 251,408 | ||||||||||||||

| 800 | Chino, California, Community Facilities District 2009-1, Watson Commerce Center, Special Tax Bonds, Series 2010, 6.750%, 9/01/40 | 9/20 at 100.00 | N/R | 809,128 | ||||||||||||||

| 490 | Davis Redevelopment Agency, California, Tax Allocation Bonds, Davis Redevelopment Project, Subordinate Series 2011A, 7.000%, 12/01/36 | 12/21 at 100.00 | A+ | 530,170 | ||||||||||||||

| 100 | Eastern Municipal Water District, California, Community Facility District No 2005-38 Improvement Area A, Special Tax Bonds, Series 2006, 5.200%, 9/01/36 | 3/12 at 102.00 | N/R | 88,414 | ||||||||||||||

| 200 | El Dorado County, California, Special Tax Bonds, Blackstone Community Facilities District 2005-1, Series 2005, 5.250%, 9/01/35 | 9/14 at 102.00 | N/R | 152,052 | ||||||||||||||

| 250 | El Dorado County, California, Special Tax Bonds, Community Facilities District 2005-2, Series 2006, 5.100%, 9/01/36 | 9/14 at 102.00 | N/R | 202,308 | ||||||||||||||

Elk Grove Community Facilities District 2005-1, California, Special Tax Bonds, Series 2007: | ||||||||||||||||||

| 80 | 5.000%, 9/01/18 | 9/17 at 100.00 | N/R | 71,837 | ||||||||||||||

| 10 | 5.000%, 9/01/20 | 9/17 at 100.00 | N/R | 8,449 | ||||||||||||||

| 50 | 5.125%, 9/01/22 | No Opt. Call | N/R | 40,466 | ||||||||||||||

| 1,000 | 5.200%, 9/01/27 | 9/15 at 102.00 | N/R | 728,880 | ||||||||||||||

| 1,225 | 5.250%, 9/01/37 | 9/15 at 102.00 | N/R | 794,964 | ||||||||||||||

| 500 | Fairfield, California, Community Facilities District 2007-1 Special Tax Bonds, Fairfield Commons Project, Series 2008, 6.875%, 9/01/38 | 9/18 at 100.00 | N/R | 483,075 | ||||||||||||||

| 500 | Folsom Public Financing Authority, California, Subordinate Special Tax Revenue Bonds, Series 2007B, 5.200%, 9/01/32 | 9/17 at 100.00 | N/R | 436,955 | ||||||||||||||

| 1,000 | Fontana, California, Special Tax Bonds, Community Facilities District 31 Citrus Heights North Special Tax Bonds, Series 2006, 5.000%, 9/01/36 | 9/14 at 102.00 | N/R | 762,570 | ||||||||||||||

| 750 | Golden State Tobacco Securitization Corporation, California, Enhanced Tobacco Settlement Asset-Backed Revenue Bonds, Tender Option Bond Trust 1011, 17.391%, 6/01/45 (WI/DD, Settling 9/08/11) (IF) | 6/15 at 100.00 | A2 | 400,020 | ||||||||||||||

| 1,000 | Hawthorne, California, Special Tax Bonds, Community Facilities District 2006-1, Three Sixty Degrees @ South Bay, Series 2006, 5.000%, 9/01/36 | 9/16 at 102.00 | N/R | 687,450 | ||||||||||||||

| 1,000 | Hemet Unified School District Community Facilities District 2005-3, Riverside County, California, Special Tax Bonds, Series 2007, 5.750%, 9/01/39 | 9/12 at 101.00 | N/R | 834,720 | ||||||||||||||

| 200 | Hemet Unified School District, California, Community Facilities District 2005-1 Special Tax Bonds, Series 2006, 5.125%, 9/01/36 | 9/13 at 100.00 | N/R | 168,186 | ||||||||||||||

Hercules Redevelopment Agency, California, Tax Allocation Bonds, Merged Project Area, Series 2005: | ||||||||||||||||||

| 1,000 | 5.000%, 8/01/25 – AMBAC Insured | 8/15 at 100.00 | CCC | 676,350 | ||||||||||||||

| 500 | 4.750%, 8/01/35 – AMBAC Insured | No Opt. Call | CCC | 281,325 | ||||||||||||||

| 295 | Hesperia Unified School District, San Bernardino County, California, Community Facilities District 2006-5 Special Tax Bonds, Series 2007, 5.000%, 9/01/37 | 9/17 at 100.00 | N/R | 237,012 | ||||||||||||||

| 325 | Hesperia, California, Improvement Act of 1915, Assessment District, 91-1, Joshua West Main Street, Series 1992, 8.500%, 9/02/24 | 3/12 at 100.00 | N/R | 335,855 | ||||||||||||||

| 150 | Indio, California, Special Tax Bonds, Community Facilities District 2006-1 Sonora Wells, Series 2006, 5.050%, 9/01/26 | 9/16 at 100.00 | N/R | 129,746 | ||||||||||||||

| 120 | Irvine, California, Unified School District, Community Facilities District Special Tax Bonds, Series 2006A, 5.125%, 9/01/36 | 9/16 at 100.00 | N/R | 107,777 | ||||||||||||||

| Nuveen Investments | 23 |

Portfolio of Investments (Unaudited)

Nuveen California High Yield Municipal Bond Fund (continued)

August 31, 2011

| Principal Amount (000) | Description (1) | Optional Call Provisions (2) | Ratings (3) | Value | ||||||||||||||

Tax Obligation/Limited (continued) | ||||||||||||||||||

| $ | 1,115 | Jurupa Community Services District, California, Community Facilities District 25 Earstvale Area Special Tax Bonds, Series 2008A, 8.375%, 9/01/28 | 9/18 at 100.00 | N/R | $ | 1,230,101 | ||||||||||||

| 500 | Jurupa Community Services District, California, Special Tax Bonds, Community Facilities District 34 Eastvale Area , Series 2010A, 6.500%, 9/01/40 | 9/20 at 100.00 | N/R | 502,705 | ||||||||||||||

| 500 | Jurupa Community Services District, California, Special Tax Bonds, Community Facilities District 38 Eastvale Improvement Area 2, Series 2010A, 6.375%, 9/01/40 | 3/12 at 100.00 | N/R | 503,910 | ||||||||||||||

| 750 | Lake Elsinore Public Financing Authority, California, Local Agency Revenue Bonds, Canyon Hills Improvement Area C, Series 2010A, 6.250%, 9/01/40 | 9/12 at 103.00 | N/R | 699,848 | ||||||||||||||

| 1,000 | Lake Elsinore Public Financing Authority, California, Local Agency Revenue Bonds, Villages at Wasson Canyon, Series 2009B, 6.875%, 9/01/38 | 9/13 at 100.00 | N/R | 1,005,760 | ||||||||||||||

| 1,000 | Lake Elsinore, California, Special Tax Bonds, Community Facilities District 2005-2 Improvement Area A, Series 2005A, 5.450%, 9/01/36 | 9/12 at 102.00 | N/R | 869,550 | ||||||||||||||

| 335 | Lancaster Redevelopment Agency, California, Combined Project Areas Housing Programs, Tax Allocation Bonds, Series 2009, 6.875%, 8/01/39 | 8/19 at 100.00 | BBB+ | 339,844 | ||||||||||||||

| 1,275 | Lynwood Redevelopment Agency, California, Project A Revenue Bonds, Subordinate Lien Series 2011A, 7.250%, 9/01/38 | 9/21 at 100.00 | A– | 1,337,832 | ||||||||||||||

March Joint Powers Redevelopment Agency, California, March Air Force Base Redevelopment Project Series 2011A: | ||||||||||||||||||

| 300 | 7.250%, 8/01/31 | No Opt. Call | BBB+ | 320,988 | ||||||||||||||

| 1,000 | 7.500%, 8/01/41 | 8/21 at 100.00 | BBB+ | 1,069,920 | ||||||||||||||

| 130 | Merced, California, Community Facilities District 2005-1, Special Tax Bonds, Bellevue Ranch West, Series 2006, 5.300%, 9/01/36 | 9/12 at 103.00 | N/R | 79,238 | ||||||||||||||

| 65 | Moreno Valley Unified School District, Riverside County, California, Special Tax Bonds, Community Facilities District, Series 2006, 5.200%, 9/01/36 | 3/16 at 100.00 | N/R | 56,720 | ||||||||||||||

| 1,000 | Moreno Valley, California, Community Facilities District 5, Special Tax Bonds, Series 2007, 5.000%, 9/01/37 | 9/17 at 100.00 | N/R | 734,690 | ||||||||||||||

| 125 | Murrieta Valley Unified School District, Riverside County, California, Special Tax Bonds, Community Facilities District 2002-4, Series 2006B, 5.450%, 9/01/38 | 9/16 at 100.00 | N/R | 98,699 | ||||||||||||||

| 330 | Novato Redevelopment Agency, California, Tax Allocation Bonds, Hamilton Field Redevelopment Project, Series 2011, 6.750%, 9/01/40 | 9/21 at 100.00 | A– | 344,378 | ||||||||||||||

| 1,500 | Palm Desert, California, Community Facilities District 2005-1, University Park Special Tax Bonds, Series 2006, 5.500%, 9/01/36 | 9/16 at 100.00 | N/R | 1,148,385 | ||||||||||||||

| 1,600 | Palm Drive Health Care District, Sonoma County, California, Certificates of Participation, Parcel Tax Secured Financing Program, Series 2010, 7.500%, 4/01/35 | No Opt. Call | BB | 1,556,816 | ||||||||||||||

| 1,000 | Palm Drive Health Care District, Sonoma County, California, Parcel Tax Revenue Bonds, Series 2005, 5.250%, 4/01/30 | 4/13 at 102.00 | BB | 742,800 | ||||||||||||||

| 1,100 | Perris Public Finance Authority, California, Local Agency Revenue Bonds, Perris Vally Vistas IA3, Series 2008B, 6.625%, 9/01/38 | 9/16 at 100.00 | N/R | 1,105,324 | ||||||||||||||

| 495 | Perris Public Financing Authority, California, Local Agency Revenue Bonds, Series 2007D, 5.800%, 9/01/38 | 9/14 at 100.00 | N/R | 439,169 | ||||||||||||||

| 575 | Perris, California, Community Facilities District 2001-1 Improvement Area 5-A Special Tax Bonds, Series 2006, 5.000%, 9/01/37 | 9/12 at 101.00 | N/R | 450,127 | ||||||||||||||

| 500 | Rancho Cardova, California, Special Tax Bonds, Sunridge Anatolia Area Community Facilities District 2003-1, Series 2005, 5.500%, 9/01/37 | 9/13 at 102.00 | N/R | 430,965 | ||||||||||||||

| 1,000 | Rancho Cardova, California, Special Tax Bonds, Sunridge Park Area Community Facilities District 2004-1, Series, 6.125%, 9/01/37 | 9/17 at 100.00 | N/R | 935,460 | ||||||||||||||

| 500 | Redwood City, California, Special Tax Bonds, Community Facilities District 2010-1 One Marina, Series 2011, 7.500%, 9/01/31 | 9/16 at 103.00 | N/R | 521,010 | ||||||||||||||

| 2,000 | Riverside County Community Facilities District 05-8 Scott Road, California, Special Tax Bonds, Series 2008, 7.250%, 9/01/38 | 9/17 at 100.00 | N/R | 1,967,460 | ||||||||||||||

| 24 | Nuveen Investments |

| Principal Amount (000) | Description (1) | Optional Call Provisions (2) | Ratings (3) | Value | ||||||||||||||

Tax Obligation/Limited (continued) | ||||||||||||||||||

| $ | 710 | Riverside County Public Financing Authority, California, Tax Allocation Bonds, Multiple Projects, Series 2004, 5.000%, 10/01/35 – SYNCORA GTY Insured | 10/14 at 100.00 | BBB | $ | 590,230 | ||||||||||||

| 500 | Riverside County Redevelopment Agency, California, Interstate 215 Corridor Redevelopment Project Area Tax Allocation Bonds, Series 2010E, 6.500%, 10/01/40 | 10/20 at 100.00 | A– | 516,570 | ||||||||||||||

| 205 | Riverside County Redevelopment Agency, California, Tax Allocation Housing Bonds, Series 2011A, 7.125%, 10/01/42 | No Opt. Call | A– | 220,318 | ||||||||||||||

| 125 | Riverside Unified School District, California, Community Facilities District 24 Special Tax Bonds, Series 2006, 5.100%, 9/01/36 | 9/14 at 102.00 | N/R | 105,413 | ||||||||||||||

| 1,000 | Riverside, California, Improvement Bond Act of 1915, Special Assessment Bonds, Hunter Park Assessment District, Series 2006, 5.200%, 9/02/36 | 9/16 at 101.00 | N/R | 790,860 | ||||||||||||||

| 1,000 | Roseville Financing Authority, California, Special Tax Revenue Bonds, Refunding Series 2007B, 5.000%, 9/01/33 | 9/17 at 100.00 | N/R | 820,680 | ||||||||||||||

| 1,700 | Roseville, California, Special Tax Bonds, Community Facilities District 1 – Westpark, Series 2005, 5.200%, 9/01/36 | 9/15 at 100.00 | N/R | 1,423,206 | ||||||||||||||

| 125 | Roseville, California, Special Tax Bonds, Community Facilities District 1 Westpark, Series 2006, 5.250%, 9/01/37 | 9/16 at 100.00 | N/R | 104,971 | ||||||||||||||

| 1,800 | Roseville, California, Special Tax Bonds, Community Facilities District 1, Fiddyment Ranch, Series 2006, 5.125%, 9/01/26 | 9/16 at 100.00 | N/R | 1,625,832 | ||||||||||||||

| 1,510 | Sacramento City Financing Authority California, Lease Revenue Bonds, Master Lease Program Facilities Projects, Tender Option Bond Trust 4698, | No Opt. Call | Aa3 | 1,470,317 | ||||||||||||||

| 1,495 | Sacramento, California, Community Facilities District 05-1, College Square Special Tax Bonds, Series 2007, 5.900%, 9/01/37 | 9/17 at 100.00 | N/R | 1,283,517 | ||||||||||||||

| 461 | Saint Louis, Missouri, Tax Increment Financing Revenue Bonds, Grace Lofts Redevelopment Projects, Series 2007A, 6.000%, 3/27/26 | 12/11 at 100.00 | N/R | 378,343 | ||||||||||||||

| 100 | San Jacinto Unified School District, Riverside County, California, Community Facilities District 2006-1 Special Tax Bonds, Infrastructure Projects, Series 2006, 5.200%, 9/01/36 | 9/16 at 100.00 | N/R | 84,366 | ||||||||||||||

| 2,500 | Stockton, California, Special Tax Bonds, Arch Road Community Facilities District 99-02, Refunding Series 2007, 5.875%, 9/01/37 | 9/17 at 102.00 | N/R | 2,205,925 | ||||||||||||||

| 1,000 | Temecula Redevelopment Agency, California, Tax Allocation Revenue Bonds, Redevelopment Project 1, Series 2002, 5.250%, 8/01/36 – NPFG Insured | 11/11 at 100.00 | A– | 898,850 | ||||||||||||||

| 530 | Turlock Public Financing Authority, California, Tax Allocation Revenue Bonds, Series 2011, 7.250%, 9/01/29 | 3/21 at 100.00 | BBB+ | 556,701 | ||||||||||||||

| 650 | Twentynine Palms Redevelopment Agency, California, Tax Allocation Bonds, Four Corners Project Area, Series 2011A, 7.650%, 9/01/42 | 9/21 at 100.00 | BBB+ | 690,586 | ||||||||||||||

| 500 | Union City Community Redevelopment Agency, California, Tax Allocation Revenue Bonds, Redevelopment Project, Subordinate Lien Series 2011, 6.875%, 12/01/33 | 12/21 at 100.00 | A | 533,865 | ||||||||||||||

| 500 | Val Verde Unified School District Financing Authority, California, Special Tax Revenue, Junior Lien Refunding Series 2003, 6.250%, 10/01/28 | 10/13 at 102.00 | N/R | 490,210 | ||||||||||||||

| 500 | Victor Elementary School District, Los Angeles County, California, Community Facilities District 2005-1 Special Tax Bonds, Series 2007A, 5.500%, 9/01/37 | 9/15 at 102.00 | N/R | 409,745 | ||||||||||||||