| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| |

FORM N-CSR |

| |

CERTIFIED SHAREHOLDER REPORT OF REGISTERED |

MANAGEMENT INVESTMENT COMPANIES |

| |

| |

| |

| Investment Company Act File Number: 811-07749 |

|

| |

| T. Rowe Price Financial Services Fund, Inc. |

|

| (Exact name of registrant as specified in charter) |

| |

| 100 East Pratt Street, Baltimore, MD 21202 |

|

| (Address of principal executive offices) |

| |

| David Oestreicher |

| 100 East Pratt Street, Baltimore, MD 21202 |

|

| (Name and address of agent for service) |

| |

| |

| Registrant’s telephone number, including area code: (410) 345-2000 |

| |

| |

| Date of fiscal year end: December 31 |

| |

| |

| Date of reporting period: December 31, 2008 |

Item 1: Report to Shareholders| Financial Services Fund | December 31, 2008 |

The views and opinions in this report were current as of December 31, 2008. They are not guarantees of performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the managers reserve the right to change their views about individual stocks, sectors, and the markets at any time. As a result, the views expressed should not be relied upon as a forecast of the fund’s future investment intent. The report is certified under the Sarbanes-Oxley Act, which requires mutual funds and other public companies to affirm that, to the best of their knowledge, the information in their financial reports is fairly and accurately stated in all material respects.

REPORTS ON THE WEB

Sign up for our E-mail Program, and you can begin to receive updated fund reports and prospectuses online rather than through the mail. Log in to your account at troweprice.com for more information.

Manager’s Letter

Fellow Shareholders

We are glad that 2008 is behind us, as virtually every asset class besides U.S. Treasuries and gold lost value last year. For the second consecutive year, financials was the worst-performing sector in the S&P 500, with the S&P 500 Financials Index declining 36% in the last six months and 55% for the full year. With the U.S. economy in a deep recession and the banking system on government-assisted life support, financial services investors were taken to the precipice. Risk aversion sent yields on short-term U.S. Treasury securities temporarily into negative territory—an event we think will be looked upon and studied with great interest for generations. With the exception of a handful of individuals approaching 100 years of age, investors are operating in uncharted territory. In addition to dealing with problems that have not surfaced since the Great Depression, we are working through more events aptly described as “first,” “worst,” and “unprecedented” than there is room to write about. We think the financial services industry offers attractive return potential from current levels, but we are less sanguine about financials reverting to their long-term profitability averages and reclaiming their status as the most prominent sector in the S&P 500.

HIGHLIGHTS

• Financials was the worst-performing sector in the S&P 500, with the S&P 500 Financials Index declining 36% in the last six months and 55% in 2008.

• The Financial Services Fund outperformed its benchmarks by solid margins in both periods, but this provides little solace as losses in absolute terms were steep.

• Our outperformance can be attributed to our overweighting the property and casualty insurance sectors, a sizable cash position, our underweighting the banking sector, and the relatively good performance of our modest nonfinancial holdings.

• As of this writing, we still believe financial stocks could register significant gains in 2009, but the deterioration in the global economy has not slowed, and we may well be in for another tough year.

As always, we would like to remind our investors that the Financial Services Fund is a relatively narrow offering that is subject to a greater risk of capital losses than more diversified portfolios. We believe that only a small portion of one’s investment portfolio should be allocated to this strategy.

The Financial Services Fund lost 21.64% and 40.06% for the 6- and 12-month periods ended December 31, 2008, respectively. As shown in the Performance Comparison table on page 1, the fund outperformed its benchmarks by solid margins in both periods, but this provides little solace as losses in absolute terms were steep.

Unfortunately, we were unable to find many financial stocks that appreciated in this environment. We think financial stocks will generate excellent returns when the economy recovers, but in looking out several years, we find that many of the changes taking place, or likely to take place, across the financial services landscape are not only cyclical but also are likely to persist for decades. In essence, these will be permanent changes for most investors’ time horizons. Some of the changes we consider permanent have implications for business models, sustainable rates of growth, and long-term returns that we have not yet fully contemplated.

In the cyclical sense, we know that economies and companies grow and contract. Stock prices, new business activity, and earnings among financial companies tend to rise and fall with economic growth. We are confident that eventually (most likely in 2009 or 2010) financial companies’ share prices will move higher in anticipation of a cyclical recovery: Fee revenue based on asset levels will grow, merger and acquisition activity will increase, demand for loans and the creditworthiness of borrowers will improve, and individuals will need to save for (and spend in) retirement. Looking past the economic recovery and what we expect to be solid gains by the shares of financial services companies, we see a more muted secular outlook for financials relative to other areas of the market for several reasons.

Less Leverage, Lower Returns: Returns—especially the “peak” returns investors so often look forward to during the troughing process of an economic cycle—are likely to be significantly lower than long-term historical averages for the financial services industry. A company generates its return on equity capital via three mechanisms: profit margins, asset turnover (a company’s revenues divided by its assets), and leverage. For years, steady increases in leverage (that is, increasing the amount of assets held on the balance sheet for every dollar of equity capital) have been a primary driver of shareholder returns in the banking, brokerage, and insurance sectors. The system is currently deleveraging, and investors and regulators are unlikely to permit companies to revisit prior leverage thresholds for decades, if ever. Investment banks will no longer be levered 30 to 1, for example. Leverage was not only aggressively employed at the corporate level—it was also employed at the investor level. Collateralized loan obligations (CLOs), collateralized debt obligations (CDOs), and hedge funds used borrowed money to buy assets from banks and turn modest returns on assets into outsized returns on equity. Then the asset prices fell, and the equity was wiped out. Again, the system is deleveraging, and these entities that previously purchased loans of all types (e.g., mortgages, credit cards, auto loans, bank debt, and corporate bonds) no longer exist in many cases. Without these incremental buyers of financial assets, banks will make fewer loans but keep more of them on their balance sheets—reducing asset turnover, requiring more equity capital, and crimping returns.

Life insurance companies are unlikely to pile into structured financial instruments at the same rate they did in recent years, given that the sector’s recent forays into structured products and other less liquid investments have crippled the industry and destroyed billions of equity capital. With leverage coming down and asset turnover not likely to improve dramatically, that leaves margins.

Given all of the capacity coming out of the financial services industry, it is reasonable to expect industry-leading companies to be able to better price their products and improve profit margins. However, any improvement in profit margins is likely to be overwhelmed by the reduction in leverage employed by financial companies. So we expect financial companies—on average—to generate lower returns and thus garner lower valuation multiples than in prior economic recoveries.

More Saving, Less Borrowing: The “credit bubble” that went parabolic in 2001 was the beginning of the end of a two-decade secular credit expansion that began with millions of baby boomers (the 78 million Americans born between 1946 and 1964) entering the work force. Since 2001, debt has grown twice as fast as GDP. Consumers are finally retrenching, and national savings rates that bottomed in negative territory in 2006 are likely to grow meaningfully in the years to come and revisit or exceed historically normal levels of 8%. According to Merrill Lynch, household debt-to-income rose to a record 140% in 2007, while the ratio was around 70% from the mid-1960s to the mid-1980s. As recently as 2002, the ratio was 100%. Not only is debt as a percentage of income sufficiently uncomfortable to lead boomers to save more, but asset values (such as houses and retirement savings plans) have also dropped precipitously in 2008. As a result, the average baby boomer who is now over 50 years old and thinking about retirement is likely to save a greater percentage of his or her income for many years to come. This could lead to a secular decline in the demand for credit, which naturally results in fewer opportunities for most financial institutions to turn a profit.

More Regulation, Less Talent: The U.S. government is now the largest investor in financial companies in the world, and that does not bode well for the industry once it is able to finance itself. Wall Street is structurally going to become a less lucrative place to work, as the capricious rule of thumb that calls for paying out 50% of revenues as compensation likely comes to an end. Banks and insurers that now have the U.S. government as a major investor have a tough road ahead as many aspects of the business—from how capital is deployed, to “how big is too big,” to how much executives are paid, to whether or not executives use private or public aircraft—come under review by politicians with differing agendas. In addition to slower-moving companies with diminished appetites for risk and more bureaucratic decision-making structures, it strikes us that, in the years to come, the financial services industry will attract fewer of the best and brightest individuals. Areas like technology, energy, education, and health care should be able to reclaim talent that has been siphoned away by financial companies for years.

ECONOMY AND INTEREST RATES

According to the National Bureau of Economic Research, the current recession began in December 2007. Consumer spending, stock prices, and home values have declined, national unemployment increased to 7.2% by the end of 2008, and weakened financial institutions have significantly curtailed lending to preserve capital and avoid additional loan-related losses. Annualized GDP growth in the third quarter was measured at -0.5%, and fourth-quarter GDP is likely to be much worse. We anticipate that economic weakness will persist until at least the middle of 2009.

The fed funds target rate—a lending rate used by banks to meet overnight reserve requirements—was 4.25% at the end of 2007 but quickly plunged to 2.00% by the end of April 2008. In October, the Federal Reserve reduced the target rate to 1.00%; in mid-December, the Fed announced that it was reducing it to a range of 0.00% to 0.25%. In fact, the Fed is now engaged in a policy of “quantitative easing” in an attempt to provide abundant liquidity to the financial system. One manifestation of this policy is the Fed’s plan to directly purchase agency debt and mortgage-backed securities to help support the mortgage and housing markets.

IMPORTANT GUIDEPOSTS FOR FINANCIAL SERVICES INVESTORS

What is needed for financial stocks to work? Here are some of the metrics that we watch:

Housing prices need to stabilize, and supply and demand must be brought back into balance. With housing inventories exceeding 10 months of supply (six is considered healthy) and housing prices continuing to fall, this area is still working against us. Prices are down 50% in some of the worst markets and still falling. The S&P/Case-Shiller index, which tracks about 20 housing markets, is down almost 25% nationally since peaking in 2006. We think national housing prices will probably contract another 15% or so before supply and demand come back into balance. Mortgage rates are now very low (below 5% for a 20-year conforming loan), foreclosure sales are brisk (particularly in California), and annual housing starts are approaching the lowest levels in decades. Unfortunately, rising unemployment and banks’ unwillingness to lend to all but the most creditworthy customers remain significant barriers to improvement. Further, the brisk sales of foreclosure property serve to prolong the downward pressure on overall home prices. There is no shortcut to unwinding the excesses of the past, and it will likely take at least a few quarters for housing prices to bottom. Importantly, we think stocks will move in advance of housing prices and inventories completely correcting: Once the trend toward equilibrium is established, stocks should move higher. This is one reason we have more than a toe in the water as it relates to several stocks we perceive as risky. We tend to invest in advance of a bottoming of fundamentals and are often early.

Yield spreads between Treasuries and risky assets need to contract. Spreads on various asset classes—bank loans, junk bonds, investment-grade corporate bonds, municipal bonds, and asset-backed securities—widened to record levels after the Lehman Brothers bankruptcy filing in September. With the fixed-income markets shut down, the Fed stepped in and guaranteed commercial paper and debt issued by a number of financial and nonfinancial companies so that the system could function. This activity continues. Risk appetite is likely to return first to the short-term lending markets, which is why in addition to watching spreads on long-term debt carefully, we are watching the commercial paper market and measures like the “TED spread,” or the difference between the rate banks lend to one another and the rate paid by short-term government securities. This spread generally ranges between 10 and 50 basis points. This past autumn, the TED spreads widened to a nearly unfathomable 450 basis points, indicating that banks were generally unwilling to lend to one another. (One hundred basis points equal one percentage point.) Toward the end of 2008, spreads on a number of asset classes improved—in some cases a great deal. For example, as of this writing, the three-month TED spread is about 125 basis points—still far above historical norms but well below the levels seen in the autumn. The fixed-income market, which usually leads the equity market on the way down and on the way up, is still anticipating significant defaults. However, current spread levels already price in significant default activity, so it is not clear that rising defaults will lead to even wider spreads and greater risk aversion. We spend a lot of time with our colleagues in T. Rowe Price’s Fixed Income Division to gauge the prognosis for our economy, equity returns in general, and the financials sector in particular, and our conclusion is that, while conditions are much better than they were in the autumn, they remain distressed and signal that a cautious approach is warranted.

Liquidity/velocity of money. While the Fed has significantly increased the supply of money, the velocity of money—the average frequency in which a monetary unit is spent in a specific time period—remains muted. One measure of liquidity, the monetary base (Fed-provided currency and reserves), was up nearly $900 billion—or almost 79%—in 2008 as the Fed put in place various programs to buy assets and make loans available. However, this money is not being cycled through the economy. Bank lending, a good proxy for the velocity of money, is contracting and is unlikely to increase until collateral values stabilize. The most straightforward means to putting a floor on asset prices is for the government to buy assets and remove them from bank balance sheets. We hope that the Fed commits to and implements a meaningful program to achieve this outcome soon. We are watching bank lending carefully for an indication that the velocity of money (an inflationary endeavor) is accelerating in anticipation of a stabilization and eventual appreciation of asset prices.

Our fund remains well-diversified across over 80 issuers of securities. It is somewhat aggressively postured but with a barbell-like structure. On the relatively conservative side of the barbell, we have a 7.4% cash position, about 10% of assets in convertible securities, and large positions in a number of stocks that should be defensive in an environment of accelerating credit losses, such as tax preparer H&R Block and insurance broker AON. Also, our largest sector weighting remains the property and casualty insurance group, and these stocks have held up very well relative to most financial companies. On the aggressive side of the barbell, we hold positions in the common stocks of banks—issuers like Wells Fargo, First Horizon National, PNC Financial Services Group, and U.S. Bancorp—and capital markets companies, including Charles Schwab, asset managers Invesco and Franklin Resources, and brokerage firms Goldman Sachs and Morgan Stanley. We maintain holdings in real estate-related stocks like homebuilders Centex and Pulte and Florida developer St. Joe. (Please refer to the fund’s portfolio of investments for a complete listing of holdings and the amount each represents in the portfolio.)

PORTFOLIO REVIEW

The fund’s outperformance versus its benchmarks in the last six months can be attributed to our overweighting property and casualty insurance sectors; a sizable cash position; the relatively good performance of our modest nonfinancial holdings (which we own to help diversify the portfolio); the strong performance of our largest holding, H&R Block; and security selection within an underweight position in the common stocks of the regional banking group.

Nevertheless, absolute returns were disappointing. Our biggest detractors share a common thread, as they did in the first half of our fiscal year—significant acceleration in realized or unrealized credit losses and/or a crisis of confidence among key constituents, including counterparties and investors. Collectively, investment banks—Goldman Sachs, Morgan Stanley, and Lehman Brothers—were our biggest detractors. We lost a good deal of money when Lehman filed for bankruptcy, as our convertible bond holdings in Lehman Brothers fell to pennies on the dollar. We maintain sizable positions in Goldman and Morgan Stanley because we think their capital positions and valuations (their price/book value ratios are less than one) are attractive despite a lack of clarity about the future profitability of Wall Street firms in a world with less leverage and more regulation. Niche insurer Assurant went from being one of our best performers to one of our worst, but we remain committed to the name and added to the position recently. Our review of its balance sheet and the risk it takes in its businesses leaves us satisfied that our analysis will ultimately prove correct. We remain committed to other detractors in the period, such as MetLife and Ameriprise Financial. We think these companies have valuable franchises and will emerge from the current financial crisis intact. However, we recognize that MetLife has significant exposure to commercial real estate and that Ameriprise depends on a stable and eventually upwardly biased equity market to earn decent returns.

Once again, our largest position, H&R Block, benefitted results. We are now past the “fix it” stage with H&R Block, and the company must execute well in its core tax business in order for the stock to generate good absolute, not just relative, returns. We are optimistic that the right management team is in place and still see significant potential for gains. Stock selection in the regional banking sector helped performance, with former laggard First Horizon National recovering from distressed levels, while timely purchases and sales of Zions Bancorporation and the convertible bonds of East West Bancorp aided results. A new addition to the portfolio, gold miner Agnico-Eagle Mines, was a significant contributor in the period as investors bid up the price of gold and related companies in a flight to safety. Property and casualty stocks continue to generate good relative performance for us. In the most recent period, AON and Travelers were among the top 10 contributors in the fund.

Notable purchases in the last six months include blue chip franchises at what we think are good prices: banking giant JPMorgan Chase and capital markets stocks Goldman Sachs and Charles Schwab. The near term is challenging for these companies, but over several years, we think market share gains will allow these firms to create separation from their competitors. Other large purchases include Assurant, discussed previously, and property and casualty stocks Axis Capital Holdings and Willis Group Holdings. Axis is a Bermuda reinsurance company that should benefit from a favorable pricing cycle. Willis is a leading insurance broker that should also benefit from a favorable pricing cycle. Willis is currently out of favor as the company has done questionable acquisitions and has enough debt on its balance sheet to give investors pause. We think the strength of Willis Group’s franchise and an improving pricing environment will lead to good returns in this somewhat controversial security.

Notable sales in the second half of 2008 reflect profit taking in a few names: First Horizon National, the convertible bonds of National City (which was taken over by PNC in our reporting period), and H&R Block. Despite our favorable view on H&R Block, we tend to stop buying stocks once they reach 5% of assets and sell a portion of the position once it exceeds 6% of assets in an effort to manage risk. Other sales were at significant losses. We sold the bulk of our Bank of America common stock after the Merrill Lynch acquisition was announced and elected to move up the capital structure by buying the company’s convertible bonds. We think Bank of America has a great franchise, but we also think that they overpaid for Merrill Lynch and Countrywide last year and should be more inwardly focused at this time rather than embarking on an aggressive acquisition campaign. We also cut our losses in the common stock of Citigroup, but we maintain a position in the convertible bonds. We eliminated our nearly worthless position in Lehman Brothers and a disappointing investment in Wachovia convertible bonds as well.

OUTLOOK

We noted six months ago in our last report that our gains could be pushed out until 2009 and that our concerns over inflation in the U.S. had moderated, given the significant contraction of credit working its way through the financial system and the reduced demand that coincides with oil prices around $140 per barrel. We also commented that the rate of housing price declines and the rate of bank loan loss reserve building would likely slow meaningfully in the first half of 2009 and set the stage for financial stocks to register significant gains. As of this writing, we still believe financial stocks could register significant gains in 2009, but the deterioration in the global economy has not slowed, and we may well be in for another tough year. Inflation is no longer a near-term concern for us despite the ballooning U.S. federal budget deficit. We would welcome inflation as asset price appreciation is needed for our economy to stabilize and fighting inflation is easier than fighting deflation, which has quickly become the Fed’s main focus. We still think that the rate of housing price declines and the rate of bank loan loss reserve building will show improvement at some point in the next few quarters, but an outright recovery in housing prices and dramatic improvement in bank loan portfolios is probably a 2010 event.

We expect stocks to begin to increase in value when it becomes clear that the rate of change in these important metrics is steadily improving. We will not attempt to time the bottom of the market, and our current incrementally more aggressive positioning—holding slightly less cash and a slightly lower allocation to convertible bonds with greater allocation to the equities of some riskier financial companies relative to the prior period—is consistent with our view that nobody knows the outcome of an unprecedented event and that our shareholders’ interests are best served by our remaining humble and flexible in our approach to investing in the financial services sector.

We thank you for your confidence in T. Rowe Price, particularly during this extraordinary and challenging period.

Respectfully submitted,

Jeffrey W. Arricale

Chairman of the fund’s Investment Advisory Committee

January 23, 2009

The committee chairman has day-to-day responsibility for managing the portfolio and works with committee members in developing and executing the fund’s investment program.

RISKS OF INVESTING

The fund’s share price can fall because of weakness in the stock market, a particular industry, or specific holdings. Stock markets can decline for many reasons, including adverse political or economic developments, changes in investor psychology, or heavy institutional selling. The prospects for an industry or company may deteriorate because of a variety of factors, including disappointing earnings or changes in the competitive environment. In addition, the investment manager’s assessment of companies held in a fund may prove incorrect, resulting in losses or poor performance, even in rising markets.

Funds that invest only in specific industries will experience greater volatility than funds investing in a broad range of industries. The banking industry can be significantly affected by legislation that has reduced the separation between commercial and investment banking businesses, changed the laws governing capitalization requirements and the savings and loan industry, and increased competition. In addition, changes in general economic conditions and interest rates can significantly affect the banking industry. Financial services companies may be hurt when interest rates rise sharply, although not all companies are affected equally. The stocks may also be vulnerable to rapidly rising inflation.

GLOSSARY

Lipper indexes: Fund benchmarks that consist of a small number of the largest mutual funds in a particular category as tracked by Lipper Inc.

Morningstar Specialty Financial Average: Tracks the performance of funds that seek capital appreciation by investing primarily in equity securities of financial services companies.

Price/book value (P/BV) ratio: A ratio used to compare a stock’s market value with its book value. It is calculated by dividing the current closing price of the stock by the latest quarter’s book value.

Price/earnings (P/E) ratio: A ratio that shows the “multiple” of earnings at which a stock is selling. It is calculated by dividing a stock’s current price by its current earnings per share. For example, if a stock’s price is $60 per share and the issuing company earns $2 per share, the P/E ratio is $60/$2, or 30.

S&P 500 Stock Index: An unmanaged index that tracks the stocks of 500 primarily large-cap U.S. companies.

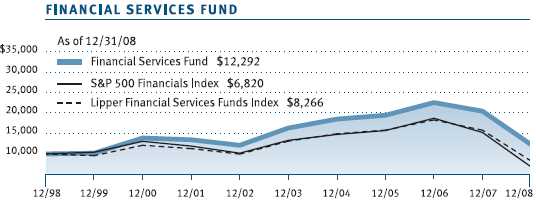

Performance and Expenses

This chart shows the value of a hypothetical $10,000 investment in the fund over the past 10 fiscal year periods or since inception (for funds lacking 10-year records). The result is compared with benchmarks, which may include a broad-based market index and a peer group average or index. Market indexes do not include expenses, which are deducted from fund returns as well as mutual fund averages and indexes.

| AVERAGE ANNUAL COMPOUND TOTAL RETURN |

This table shows how the fund would have performed each year if its actual (or cumulative) returns for the periods shown had been earned at a constant rate.

As a mutual fund shareholder, you may incur two types of costs: (1) transaction costs, such as redemption fees or sales loads, and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, and other fund expenses. The following example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the most recent six-month period and held for the entire period.

Actual Expenses

The first line of the following table (“Actual”) provides information about actual account values and expenses based on the fund’s actual returns. You may use the information in this line, together with your account balance, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The information on the second line of the table (“Hypothetical”) is based on hypothetical account values and expenses derived from the fund’s actual expense ratio and an assumed 5% per year rate of return before expenses (not the fund’s actual return). You may compare the ongoing costs of investing in the fund with other funds by contrasting this 5% hypothetical example and the 5% hypothetical examples that appear in the shareholder reports of the other funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

Note: T. Rowe Price charges an annual small-account maintenance fee of $10, generally for accounts with less than $2,000 ($500 for UGMA/UTMA). The fee is waived for any investor whose T. Rowe Price mutual fund accounts total $25,000 or more, accounts employing automatic investing, and IRAs and other retirement plan accounts that utilize a prototype plan sponsored by T. Rowe Price (although a separate custodial or administrative fee may apply to such accounts). This fee is not included in the accompanying table. If you are subject to the fee, keep it in mind when you are estimating the ongoing expenses of investing in the fund and when comparing the expenses of this fund with other funds.

You should also be aware that the expenses shown in the table highlight only your ongoing costs and do not reflect any transaction costs, such as redemption fees or sales loads. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. To the extent a fund charges transaction costs, however, the total cost of owning that fund is higher.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

The accompanying notes are an integral part of these financial statements.

| NOTES TO FINANCIAL STATEMENTS |

T. Rowe Price Financial Services Fund, Inc. (the fund), is registered under the Investment Company Act of 1940 (the 1940 Act) as a diversified, open-end management investment company. The fund commenced operations on September 30, 1996. The fund seeks long-term growth of capital and a modest level of income.

NOTE 1 - SIGNIFICANT ACCOUNTING POLICIES

Basis of Preparation The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America, which require the use of estimates made by fund management. Fund management believes that estimates and security valuations are appropriate; however, actual results may differ from those estimates, and the security valuations reflected in the financial statements may differ from the value the fund ultimately realizes upon sale of the securities.

Investment Transactions, Investment Income, and Distributions Income and expenses are recorded on the accrual basis. Premiums and discounts on debt securities are amortized for financial reporting purposes. Dividends received from mutual fund investments are reflected as dividend income; capital gain distributions are reflected as realized gain/loss. Dividend income and capital gain distributions are recorded on the ex-dividend date. Income tax-related interest and penalties, if incurred, would be recorded as income tax expense. Investment transactions are accounted for on the trade date. Realized gains and losses are reported on the identified cost basis. Distributions to shareholders are recorded on the ex-dividend date. Income distributions are declared and paid on an annual basis. Capital gain distributions, if any, are declared and paid by the fund, typically on an annual basis.

Currency Translation Assets, including investments, and liabilities denominated in foreign currencies are translated into U.S. dollar values each day at the prevailing exchange rate, using the mean of the bid and asked prices of such currencies against U.S. dollars as quoted by a major bank. Purchases and sales of securities, income, and expenses are translated into U.S. dollars at the prevailing exchange rate on the date of the transaction. The effect of changes in foreign currency exchange rates on realized and unrealized security gains and losses is reflected as a component of security gains and losses.

Rebates Subject to best execution, the fund may direct certain security trades to brokers who have agreed to rebate a portion of the related brokerage commission to the fund in cash. Commission rebates are reflected as realized gain on securities in the accompanying financial statements and totaled $26,000 for the year ended December 31, 2008.

New Accounting Pronouncements On January 1, 2008, the fund adopted Statement of Financial Accounting Standards No. 157 (FAS 157), Fair Value Measurements. FAS 157 defines fair value, establishes the framework for measuring fair value, and expands the disclosures of fair value measurements in the financial statements. Adoption of FAS 157 did not have a material impact on the fund’s net assets or results of operations.

In March 2008, the Financial Accounting Standards Board issued Statement of Financial Accounting Standards No. 161 (FAS 161), Disclosures about Derivative Instruments and Hedging Activities, which is effective for fiscal years and interim periods beginning after November 15, 2008. FAS 161 requires enhanced disclosures about derivative and hedging activities, including how such activities are accounted for and their effect on financial position, performance and cash flows. Management is currently evaluating the impact the adoption of FAS 161 will have on the fund’s financial statements and related disclosures.

NOTE 2 - VALUATION

The fund’s investments are reported at fair value as defined under FAS 157. The fund values its investments and computes its net asset value per share at the close of the New York Stock Exchange (NYSE), normally 4 p.m. ET, each day that the NYSE is open for business.

Valuation Methods Equity securities listed or regularly traded on a securities exchange or in the over-the-counter (OTC) market are valued at the last quoted sale price or, for certain markets, the official closing price at the time the valuations are made, except for OTC Bulletin Board securities, which are valued at the mean of the latest bid and asked prices. A security that is listed or traded on more than one exchange is valued at the quotation on the exchange determined to be the primary market for such security. Listed securities not traded on a particular day are valued at the mean of the latest bid and asked prices for domestic securities and the last quoted sale price for international securities.

Debt securities are generally traded in the OTC market. Securities with remaining maturities of one year or more at the time of acquisition are valued at prices furnished by dealers who make markets in such securities or by an independent pricing service, which considers the yield or price of bonds of comparable quality, coupon, maturity, and type, as well as prices quoted by dealers who make markets in such securities. Securities with remaining maturities of less than one year at the time of acquisition generally use amortized cost in local currency to approximate fair value. However, if amortized cost is deemed not to reflect fair value or the fund holds a significant amount of such securities with remaining maturities of more than 60 days, the securities are valued at prices furnished by dealers who make markets in such securities or by an independent pricing service.

Investments in mutual funds are valued at the mutual fund’s closing net asset value per share on the day of valuation.

Other investments, including restricted securities, and those for which the above valuation procedures are inappropriate or are deemed not to reflect fair value are stated at fair value as determined in good faith by the T. Rowe Price Valuation Committee, established by the fund’s Board of Directors.

Valuation Inputs Various inputs are used to determine the value of the fund’s investments. These inputs are summarized in the three broad levels listed below:

Level 1 – quoted prices in active markets for identical securities

Level 2 – observable inputs other than Level 1 quoted prices (including, but not limited to, quoted prices for similar securities, interest rates, prepayment speeds, credit risk)

Level 3 – unobservable inputs

Observable inputs are those based on market data obtained from sources independent of the fund, and unobservable inputs reflect the fund’s own assumptions based on the best information available. The input levels are not necessarily an indication of the risk or liquidity associated with investments at that level. The following table summarizes the fund’s investments, based on the inputs used to determine their values on December 31, 2008:

NOTE 3 - INVESTMENT TRANSACTIONS

Consistent with its investment objective, the fund engages in the following practices to manage exposure to certain risks or to enhance performance. The investment objective, policies, program, and risk factors of the fund are described more fully in the fund’s prospectus and Statement of Additional Information.

Restricted Securities The fund may invest in securities that are subject to legal or contractual restrictions on resale. Prompt sale of such securities at an acceptable price may be difficult and may involve substantial delays and additional costs.

Options Call and put options give the holder the right to purchase and sell, respectively, a security at a specified price on a certain date. Risks arise from possible illiquidity of the options market and from movements in security values. Transactions in options written and related premiums received during the year ended December 31, 2008, were as follows:

Securities Lending The fund lends its securities to approved brokers to earn additional income. It receives as collateral cash and U.S. government securities valued at 102% to 105% of the value of the securities on loan. Cash collateral is invested by the fund’s lending agent(s) in accordance with investment guidelines approved by fund management. Although risk is mitigated by the collateral, the fund could experience a delay in recovering its securities and a possible loss of income or value if the borrower fails to return the securities or if collateral investments decline in value. Securities lending revenue recognized by the fund consists of earnings on invested collateral and borrowing fees, net of any rebates to the borrower and compensation to the lending agent. At December 31, 2008, there were no securities on loan.

Other Purchases and sales of portfolio securities, other than short-term securities, aggregated $461,531,000 and $385,826,000, respectively, for the year ended December 31, 2008.

NOTE 4 - FEDERAL INCOME TAXES

No provision for federal income taxes is required since the fund intends to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and distribute to shareholders all of its taxable income and gains. Distributions are determined in accordance with Federal income tax regulations, which differ from generally accepted accounting principles, and, therefore, may differ significantly in amount or character from net investment income and realized gains for financial reporting purposes. Financial reporting records are adjusted for permanent book/tax differences to reflect tax character but are not adjusted for temporary differences.

Reclassifications between income and gain relate primarily to differences between book/tax amortization policies. For the year ended December 31, 2008, the following reclassifications, which had no impact on results of operations or net assets, were recorded to reflect tax character:

Distributions during the years ended December 31, 2008 and December 31, 2007 were characterized for tax purposes as follows:

At December 31, 2008, the tax-basis cost of investments and components of net assets were as follows:

The difference between book-basis and tax-basis net unrealized appreciation (depreciation) is attributable to the deferral of losses from wash sales for tax purposes. The fund intends to retain realized gains to the extent of available capital loss carryforwards. As of December 31, 2008, all unused capital loss carryforwards expire in fiscal 2016. Pursuant to federal income tax regulations applicable to investment companies, recognition of capital losses on certain transactions is deferred until the subsequent tax year. Consequently, realized losses reflected in the accompanying financial statements include net capital losses realized between November 1 and the fund’s fiscal year-end that have not been recognized for tax purposes (Post-October loss deferrals).

NOTE 5 - RELATED PARTY TRANSACTIONS

The fund is managed by T. Rowe Price Associates, Inc. (the manager or Price Associates), a wholly owned subsidiary of T. Rowe Price Group, Inc. The investment management agreement between the fund and the manager provides for an annual investment management fee, which is computed daily and paid monthly. The fee consists of an individual fund fee, equal to 0.35% of the fund’s average daily net assets, and a group fee. The group fee rate is calculated based on the combined net assets of certain mutual funds sponsored by Price Associates (the group) applied to a graduated fee schedule, with rates ranging from 0.48% for the first $1 billion of assets to 0.285% for assets in excess of $220 billion. The fund’s group fee is determined by applying the group fee rate to the fund’s average daily net assets. At December 31, 2008, the effective annual group fee rate was 0.31%.

In addition, the fund has entered into service agreements with Price Associates and two wholly owned subsidiaries of Price Associates (collectively, Price). Price Associates computes the daily share price and provides certain other administrative services to the fund. T. Rowe Price Services, Inc., provides shareholder and administrative services in its capacity as the fund’s transfer and dividend disbursing agent. T. Rowe Price Retirement Plan Services, Inc., provides subaccounting and recordkeeping services for certain retirement accounts invested in the fund. For the year ended December 31, 2008, expenses incurred pursuant to these service agreements were $108,000 for Price Associates, $546,000 for T. Rowe Price Services, Inc., and $47,000 for T. Rowe Price Retirement Plan Services, Inc. The total amount payable at period-end pursuant to these service agreements is reflected as Due to Affiliates in the accompanying financial statements.

Additionally, the fund is one of several mutual funds in which certain college savings plans managed by Price Associates may invest. As approved by the fund’s Board of Directors, shareholder servicing costs associated with each college savings plan are borne by the fund in proportion to the average daily value of its shares owned by the college savings plan. For the year ended December 31, 2008, the fund was charged $47,000 for shareholder servicing costs related to the college savings plans, of which $34,000 was for services provided by Price. The amount payable at period-end pursuant to this agreement is reflected as Due to Affiliates in the accompanying financial statements. At December 31, 2008, approximately 3% of the outstanding shares of the fund were held by college savings plans.

The fund may invest in the T. Rowe Price Reserve Investment Fund and the T. Rowe Price Government Reserve Investment Fund (collectively, the T. Rowe Price Reserve Investment Funds), open-end management investment companies managed by Price Associates and considered affiliates of the fund. The T. Rowe Price Reserve Investment Funds are offered as cash management options to mutual funds, trusts, and other accounts managed by Price Associates and/or its affiliates and are not available for direct purchase by members of the public. The T. Rowe Price Reserve Investment Funds pay no investment management fees.

As of December 31, 2008, T. Rowe Price Group, Inc., and/or its wholly owned subsidiaries owned 225,117 shares of the fund, representing 1% of the fund’s net assets.

| REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM |

To the Board of Directors and Shareholders of T. Rowe Price Financial Services Fund, Inc.

In our opinion, the accompanying statement of assets and liabilities, including the schedule of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of T. Rowe Price Financial Services Fund, Inc. (the “Fund”) at December 31, 2008, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management; our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at December 31, 2008 by correspondence with the custodian and confirmation of the underlying fund by correspondence with the transfer agent, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Baltimore, Maryland

February 12, 2009

| TAX INFORMATION (UNAUDITED) FOR THE TAX YEAR ENDED 12/31/08 |

We are providing this information as required by the Internal Revenue Code. The amounts shown may differ from those elsewhere in this report because of differences between tax and financial reporting requirements.

For taxable non-corporate shareholders, $6,372,000 of the fund’s income represents qualified dividend income subject to the 15% rate category.

For corporate shareholders, $5,734,000 of the fund’s income qualifies for the dividends-received deduction.

| INFORMATION ON PROXY VOTING POLICIES, PROCEDURES, AND RECORDS |

A description of the policies and procedures used by T. Rowe Price funds and portfolios to determine how to vote proxies relating to portfolio securities is available in each fund’s Statement of Additional Information, which you may request by calling 1-800-225-5132 or by accessing the SEC’s Web site, www.sec.gov. The description of our proxy voting policies and procedures is also available on our Web site, www.troweprice.com. To access it, click on the words “Our Company” at the top of our corporate homepage. Then, when the next page appears, click on the words “Proxy Voting Policies” on the left side of the page.

Each fund’s most recent annual proxy voting record is available on our Web site and through the SEC’s Web site. To access it through our Web site, follow the directions above, then click on the words “Proxy Voting Records” on the right side of the Proxy Voting Policies page.

| HOW TO OBTAIN QUARTERLY PORTFOLIO HOLDINGS |

The fund files a complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year on Form N-Q. The fund’s Form N-Q is available electronically on the SEC’s Web site (www.sec.gov); hard copies may be reviewed and copied at the SEC’s Public Reference Room, 450 Fifth St. N.W., Washington, DC 20549. For more information on the Public Reference Room, call 1-800-SEC-0330.

| ABOUT THE FUND’S DIRECTORS AND OFFICERS |

Your fund is governed by a Board of Directors (Board) that meets regularly to review a wide variety of matters affecting the fund, including performance, investment programs, compliance matters, advisory fees and expenses, service providers, and other business affairs. The Board elects the fund’s officers, who are listed in the final table. At least 75% of Board members are independent of T. Rowe Price Associates, Inc. (T. Rowe Price), and T. Rowe Price International, Inc. (T. Rowe Price International); “inside” or “interested” directors are employees or officers of T. Rowe Price. The business address of each director and officer is 100 East Pratt Street, Baltimore, Maryland 21202. The Statement of Additional Information includes additional information about the directors and is available without charge by calling a T. Rowe Price representative at 1-800-225-5132.

| Independent Directors | |

| |

| Name | |

| (Year of Birth) | Principal Occupation(s) During Past Five Years and Directorships of |

| Year Elected* | Other Public Companies |

| | |

| Jeremiah E. Casey | Director, National Life Insurance (2001 to 2005); Director, The Rouse |

| (1940) | Company, real estate developers (1990 to 2004) |

| 2005 | |

| | |

| Anthony W. Deering | Chairman, Exeter Capital, LLC, a private investment firm (2004 to |

| (1945) | present); Director, Under Armour (8/08 to present); Director, Vornado |

| 2001 | Real Estate Investment Trust (3/04 to present); Director, Mercantile |

| | Bankshares (2002 to 2007); Member, Advisory Board, Deutsche |

| | Bank North America (2004 to present); Director, Chairman of the |

| | Board, and Chief Executive Officer, The Rouse Company, real estate |

| | developers (1997 to 2004) |

| | |

| Donald W. Dick, Jr. | Principal, EuroCapital Advisors, LLC, an acquisition and management |

| (1943) | advisory firm (10/95 to present); Chairman, The Haven Group, a cus- |

| 1996 | tom manufacturer of modular homes (1/04 to present) |

| | |

| David K. Fagin | Chairman and President, Nye Corporation (6/88 to present); Director, |

| (1938) | Golden Star Resources Ltd. (5/92 to present); Director, Pacific Rim |

| 1996 | Mining Corp. (2/02 to present); Director, B.C. Corporation (3/08 |

| | to present); Chairman, Canyon Resources Corp. (8/07 to 3/08); |

| | Director, Atna Resources Ltd. (3/08 to present) |

| | |

| Karen N. Horn | Director, Eli Lilly and Company (1987 to present); Director, Simon |

| (1943) | Property Group (2004 to present); Director, Federal National |

| 2003 | Mortgage Association (9/06 to present); Director, Norfolk Southern |

| | (2/08 to present); Director, Georgia Pacific (5/04 to 12/05); |

| | Managing Director and President, Global Private Client Services, |

| | Marsh Inc. (1999 to 2003) |

| Theo C. Rodgers | President, A&R Development Corporation (1977 to present) |

| (1941) | |

| 2005 | |

| | |

| John G. Schreiber | Owner/President, Centaur Capital Partners, Inc., a real estate invest- |

| (1946) | ment company (1991 to present); Partner, Blackstone Real Estate |

| 2001 | Advisors, L.P. (10/92 to present) |

| |

| *Each independent director oversees 126 T. Rowe Price portfolios (except for Mr. Fagin, who oversees 125 |

| T. Rowe Price portfolios) and serves until retirement, resignation, or election of a successor. |

| Inside Directors | |

| |

| Name | |

| (Year of Birth) | |

| Year Elected* | |

| [Number of T. Rowe Price | Principal Occupation(s) During Past Five Years and Directorships of |

| Portfolios Overseen] | Other Public Companies |

| | |

| Edward C. Bernard | Director and Vice President, T. Rowe Price; Vice Chairman of the |

| (1956) | Board, Director, and Vice President, T. Rowe Price Group, Inc.; |

| 2006 | Chairman of the Board, Director, and President, T. Rowe Price |

| [126] | Investment Services, Inc.; Chairman of the Board and Director, |

| | T. Rowe Price Global Asset Management Limited, T. Rowe Price |

| | Global Investment Services Limited, T. Rowe Price Retirement Plan |

| | Services, Inc., T. Rowe Price Savings Bank, and T. Rowe Price |

| | Services, Inc.; Director, T. Rowe Price International, Inc.; Chief |

| | Executive Officer, Chairman of the Board, Director, and President, |

| | T. Rowe Price Trust Company; Chairman of the Board, all funds |

| | |

| Brian C. Rogers, CFA, CIC | Chief Investment Officer, Director, and Vice President, T. Rowe Price; |

| (1955) | Chairman of the Board, Chief Investment Officer, Director, and Vice |

| 2006 | President, T. Rowe Price Group, Inc.; Vice President, T. Rowe Price |

| [71] | Trust Company |

| |

| *Each inside director serves until retirement, resignation, or election of a successor. |

| Officers | |

| |

| Name (Date of Birth) | |

| Title and Fund(s) Served | Principal Occupation(s) |

| | |

| Jeffrey W. Arricale, CPA (1971) | Vice President, T. Rowe Price and T. Rowe Price |

| President, Financial Services Fund | Group, Inc. |

| | |

| Anna M. Dopkin, CFA (1967) | Vice President, T. Rowe Price, T. Rowe Price |

| Vice President, Financial Services Fund | Group, Inc., and T. Rowe Price Trust Company |

| | |

| Roger L. Fiery III, CPA (1959) | Vice President, T. Rowe Price, T. Rowe Price |

| Vice President, Financial Services Fund | Group, Inc., T. Rowe Price International, Inc., |

| | and T. Rowe Price Trust Company |

| | |

| Christopher T. Fortune (1973) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Financial Services Fund | Group, Inc.; formerly intern, Hillman Capital |

| | Management (to 2005) |

| | |

| John R. Gilner (1961) | Chief Compliance Officer and Vice President, |

| Chief Compliance Officer, | T. Rowe Price; Vice President, T. Rowe Price |

| Financial Services Fund | Group, Inc., and T. Rowe Price Investment |

| | Services, Inc. |

| | |

| Gregory S. Golczewski (1966) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Financial Services Fund | Trust Company |

| | |

| Gregory K. Hinkle, CPA (1958) | Vice President, T. Rowe Price, T. Rowe Price |

| Treasurer, Financial Services Fund | Group, Inc., T. Rowe Price Investment Services, |

| | Inc., and T. Rowe Price Trust Company; formerly |

| | Partner, PricewaterhouseCoopers LLP (to 2007) |

| | |

| Steven Krichbaum (1977) | Employee, T. Rowe Price; formerly intern, |

| Vice President, Financial Services Fund | T. Rowe Price (summer 2006); student, |

| | University of Michigan (to 2007); Economist/ |

| | Statistical Analyst, Colorado Department of |

| | Labor and Employment (to 2004) |

| | |

| Patricia B. Lippert (1953) | Assistant Vice President, T. Rowe Price and |

| Secretary, Financial Services Fund | T. Rowe Price Investment Services, Inc. |

| | |

| Ian C. McDonald (1971) | Employee, T. Rowe Price; formerly insurance |

| Vice President, Financial Services Fund | correspondent and staff reporter, The Wall |

| | Street Journal |

| | |

| Michael J. McGonigle (1966) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Financial Services Fund | Group, Inc. |

| | |

| Hwee Jan Ng, CFA (1966) | Vice President, T. Rowe Price Group, Inc., and |

| Vice President, Financial Services Fund | T. Rowe Price International, Inc.; formerly Vice |

| | President of Equity Research, Merrill Lynch |

| | Investment Managers (Singapore) (to 2005) |

| David Oestreicher (1967) | Director and Vice President, T. Rowe Price |

| Vice President, Financial Services Fund | Investment Services, Inc., T. Rowe Price Trust |

| | Company, and T. Rowe Price Services, Inc.; Vice |

| | President, T. Rowe Price, T. Rowe Price Global |

| | Asset Management Limited, T. Rowe Price |

| | Global Investment Services Limited, T. Rowe |

| | Price Group, Inc., T. Rowe Price International, |

| | Inc., and T. Rowe Price Retirement Plan |

| | Services, Inc. |

| | |

| Jason B. Polun, CFA (1974) | Vice President, T. Rowe Price and T. Rowe |

| Vice President, Financial Services Fund | Price Group, Inc.; formerly Vice President, |

| | Wellington Management LLP (to 2006); student, |

| | The Wharton Business School, University of |

| | Pennsylvania (to 2004) |

| | |

| Frederick A. Rizzo (1969) | Vice President, T. Rowe Price International, |

| Vice President, Financial Services Fund | Inc.; formerly Analyst, F&C Asset Management |

| | (London) (to 2006); Senior Equity Analyst, |

| | Citigroup (London) (to 2004) |

| | |

| Federico Santilli, CFA (1974) | Vice President, T. Rowe Price Group, Inc., and |

| Vice President, Financial Services Fund | T. Rowe Price International, Inc. |

| | |

| Gabriel Solomon (1977) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Financial Services Fund | Group, Inc.; formerly student, The Wharton |

| | Business School, University of Pennsylvania |

| | (to 2004); Equity Analyst Intern, Wellington |

| | Management Company, LLP (to 2003) |

| | |

| Mitchell J.K. Todd (1974) | Vice President, T. Rowe Price International, Inc.; |

| Vice President, Financial Services Fund | formerly Senior Research Analyst, F&C Asset |

| | Management (to 2003) |

| | |

| Eric L. Veiel, CFA (1972) | Vice President, T. Rowe Price and T. Rowe Price |

| Vice President, Financial Services Fund | Group, Inc.; formerly Senior Equity Analyst, |

| | Wachovia Securities (to 2005) |

| | |

| Julie L. Waples (1970) | Vice President, T. Rowe Price |

| Vice President, Financial Services Fund | |

| | |

| Tamara P. Wiggs (1979) | Vice President, T. Rowe Price; formerly Vice |

| Vice President, Financial Services Fund | President, Institutional Equity Trading, Merrill |

| | Lynch (to 2003) |

| |

| Unless otherwise noted, officers have been employees of T. Rowe Price or T. Rowe Price International for |

| at least five years. | |

Item 2. Code of Ethics.

The registrant has adopted a code of ethics, as defined in Item 2 of Form N-CSR, applicable to its principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions. A copy of this code of ethics is filed as an exhibit to this Form N-CSR. No substantive amendments were approved or waivers were granted to this code of ethics during the period covered by this report.

Item 3. Audit Committee Financial Expert.

The registrant’s Board of Directors/Trustees has determined that Ms. Karen N. Horn qualifies as an audit committee financial expert, as defined in Item 3 of Form N-CSR. Ms. Horn is considered independent for purposes of Item 3 of Form N-CSR.

Item 4. Principal Accountant Fees and Services.

(a) – (d) Aggregate fees billed to the registrant for the last two fiscal years for professional services rendered by the registrant’s principal accountant were as follows:

Audit fees include amounts related to the audit of the registrant’s annual financial statements and services normally provided by the accountant in connection with statutory and regulatory filings. Audit-related fees include amounts reasonably related to the performance of the audit of the registrant’s financial statements and specifically include the issuance of a report on internal controls and, if applicable, agreed-upon procedures related to fund acquisitions. Tax fees include amounts related to services for tax compliance, tax planning, and tax advice. The nature of these services specifically includes the review of distribution calculations and the preparation of Federal, state, and excise tax returns. All other fees include the registrant’s pro-rata share of amounts for agreed-upon procedures in conjunction with service contract approvals by the registrant’s Board of Directors/Trustees.

(e)(1) The registrant’s audit committee has adopted a policy whereby audit and non-audit services performed by the registrant’s principal accountant for the registrant, its investment adviser, and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant require pre-approval in advance at regularly scheduled audit committee meetings. If such a service is required between regularly scheduled audit committee meetings, pre-approval may be authorized by one audit committee member with ratification at the next scheduled audit committee meeting. Waiver of pre-approval for audit or non-audit services requiring fees of a de minimis amount is not permitted.

(2) No services included in (b) – (d) above were approved pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

(f) Less than 50 percent of the hours expended on the principal accountant’s engagement to audit the registrant’s financial statements for the most recent fiscal year were attributed to work performed by persons other than the principal accountant’s full-time, permanent employees.

(g) The aggregate fees billed for the most recent fiscal year and the preceding fiscal year by the registrant’s principal accountant for non-audit services rendered to the registrant, its investment adviser, and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant were $1,922,000 and $1,486,000, respectively.

(h) All non-audit services rendered in (g) above were pre-approved by the registrant’s audit committee. Accordingly, these services were considered by the registrant’s audit committee in maintaining the principal accountant’s independence.

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Investments.

(a) Not applicable. The complete schedule of investments is included in Item 1 of this Form N-CSR.

(b) Not applicable.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable.

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

Not applicable.

Item 10. Submission of Matters to a Vote of Security Holders.

Not applicable.

Item 11. Controls and Procedures.

(a) The registrant’s principal executive officer and principal financial officer have evaluated the registrant’s disclosure controls and procedures within 90 days of this filing and have concluded that the registrant’s disclosure controls and procedures were effective, as of that date, in ensuring that information required to be disclosed by the registrant in this Form N-CSR was recorded, processed, summarized, and reported timely.

(b) The registrant’s principal executive officer and principal financial officer are aware of no change in the registrant’s internal control over financial reporting that occurred during the registrant’s second fiscal quarter covered by this report that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting.

Item 12. Exhibits.

(a)(1) The registrant’s code of ethics pursuant to Item 2 of Form N-CSR is attached.

(2) Separate certifications by the registrant's principal executive officer and principal financial officer, pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(a) under the Investment Company Act of 1940, are attached.

(3) Written solicitation to repurchase securities issued by closed-end companies: not applicable.

(b) A certification by the registrant's principal executive officer and principal financial officer, pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 and required by Rule 30a-2(b) under the Investment Company Act of 1940, is attached.

| | |

SIGNATURES |

| |

| | Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment |

| Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the |

| undersigned, thereunto duly authorized. |

| |

| T. Rowe Price Financial Services Fund, Inc. |

| |

| |

| |

| By | /s/ Edward C. Bernard |

| | Edward C. Bernard |

| | Principal Executive Officer |

| |

| Date | February 19, 2009 |

| |

| |

| |

| | Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment |

| Company Act of 1940, this report has been signed below by the following persons on behalf of |

| the registrant and in the capacities and on the dates indicated. |

| |

| |

| By | /s/ Edward C. Bernard |

| | Edward C. Bernard |

| | Principal Executive Officer |

| |

| Date | February 19, 2009 |

| |

| |

| |

| By | /s/ Gregory K. Hinkle |

| | Gregory K. Hinkle |

| | Principal Financial Officer |

| |

| Date | February 19, 2009 |