Exhibit (c)(4)

Project North

CONFIDENTIAL

Presentation to the Board of Directors

April 27, 2006

PRELIMINARY | SUBJECT TO FURTHER REVIEW AND EVALUATION

THESE MATERIALS MAY NOT BE USED OR RELIED UPON FOR ANY PURPOSE OTHER THAN AS SPECIFICALLY CONTEMPLATED BY A

WRITTEN AGREEMENT WITH CREDIT SUISSE.

Table of Contents

1. Executive Summary

2. Financial Analysis

3. Buyer Analysis

Appendix

A. Preliminary Valuation

B. Recent Trading Performance

C. Industry Perspectives

CONFIDENTIAL

1

1. Executive Summary

CONFIDENTIAL

2

Executive Summary

ARM and Portfolio Management substantially unchanged

CONFIDENTIAL

CRM ramp has moderated as a result of slower customer buildouts

Highlights risk / lack of predictability in CRM

CRM remains a small contributor to the total business

What Has

Changed Since

Prior Meeting

Financial

Analysis /

Impact on

Sale Timing

Should provide potential buyers with three to four quarters of strong

performance (Q4 FY05 to Q3 FY06)

Increase confidence / visibility in Q3 and Q4 FY06

Prove that business has recovered from miss in Q3 FY05

Eliminate Q3 FY05 from the LTM period, increasing potential leverage

in an LBO

Decision regarding timing of a potential sale must balance providing

shareholders certainty of value today v. expected value in the future, taking

into account execution and market risks

“Rolling” LBO analysis suggests inflection point is Q2 / Q3 FY06

M&A, debt and equity markets are currently strong

A sale process could commence with calls to potential buyers in mid- to

late-June and conclude by early- to mid-September

Buyers could be provided preliminary Q3 FY06 results before submitting

final bids

3

CONFIDENTIAL

2. Financial Analysis

4

CONFIDENTIAL

Comparison of Management Projections

Observations

ARM: No material

change

CRM: Projections

have decreased as a

result of delays with

ramp in new

customers

PM: Q1 exceeded

prior plan; outlook for

2H FY06 appears

stable

($ in million)

Current Forecast

March Forecast

Q1:06

Q2:06

Q3:06

Q4:06

CY2006

CY2007

Q1:06

Q2:06

Q3:06

Q4:06

CY2006

CY2007

Revenue

ARM

$235.2

$234.0

$233.3

$232.5

$935.0

$985.9

$236.6

$234.0

$233.3

$232.5

$936.4

$987.3

vs. Prior

-1.5

0.0

0.0

0.0

-1.5

-1.4

(0.6%)

0.0%

0.0%

0.0%

(0.2%)

(0.1%)

CRM

59.3

62.6

71.6

81.3

274.8

325.0

59.3

67.9

77.6

84.3

289.1

348.9

vs. Prior

0.0

-5.3

-6.0

-3.0

-14.3

-23.9

0.1%

(7.8%)

(7.8%)

(3.6%)

(4.9%)

(6.8%)

Portfolio Management

50.0

47.7

46.7

45.2

189.7

189.2

48.1

47.0

45.9

44.3

185.3

189.2

vs. Prior

2.0

0.8

0.9

0.9

4.4

0.0

4.1%

1.6%

1.9%

1.9%

2.4%

0.0%

Total

(1)

312.0

311.4

321.5

330.1

1,275.0

1,374.3

311.4

315.9

326.6

332.3

1,286.2

1,399.5

vs. Prior

0.6

-4.5

-5.2

-2.2

-11.2

-25.3

0.2%

(1.4%)

(1.6%)

(0.7%)

(0.9%)

(1.8%)

EBITDA

ARM

$29.0

$26.7

$30.2

$28.9

$114.8

$135.7

$28.5

$26.7

$30.2

$28.9

$114.2

$135.9

% Margin

12.3%

11.4%

12.9%

12.4%

12.3%

13.8%

12.0%

11.4%

12.9%

12.4%

12.2%

13.8%

vs. Prior

0.5

0.0

0.0

0.0

0.5

-0.2

30 bps

0 bps

0 bps

0 bps

8 bps

0 bps

CRM

(0.5)

0.9

4.6

9.8

14.8

30.8

1.4

4.8

6.2

8.7

21.2

37.0

% Margin

(0.2%)

0.4%

2.0%

4.2%

1.6%

3.1%

0.6%

2.0%

2.7%

3.8%

2.3%

3.7%

vs. Prior

-1.9

-3.9

-1.6

1.1

-6.3

-6.2

-82 bps

-165 bps

-70 bps

47 bps

-67 bps

-63 bps

Portfolio Management

14.5

10.4

12.7

12.3

49.9

46.8

11.7

9.6

11.8

11.5

44.7

46.8

% Margin

6.2%

4.4%

5.4%

5.3%

5.3%

4.8%

5.0%

4.1%

5.1%

4.9%

4.8%

4.7%

vs. Prior

2.8

0.8

0.9

0.9

5.2

0.0

121 bps

32 bps

36 bps

37 bps

57 bps

1 bps

Total

43.0

38.0

47.5

51.0

179.5

213.3

41.6

41.1

48.2

49.1

180.1

219.8

% Margin

18.3%

16.3%

20.3%

21.9%

19.2%

21.6%

17.6%

17.6%

20.7%

21.1%

19.2%

22.3%

vs. Prior

1.3

-3.1

-0.8

2.0

-0.6

-6.4

68 bps

-133 bps

-33 bps

84 bps

-3 bps

-62 bps

(1) Net of intracompany eliminations.

5

($ in millions)

Q1:05

Q2:05

Q3:05

Q4:05

Q1:06

Q2:06

Q3:06

Q4:06

FY05

FY06

FY07

Revenue

$201.5

$195.8

$190.3

$216.8

$235.2

$234.0

$233.3

$232.5

$804.5

$935.0

$985.9

% growth (Q/Q Y/Y)

12.0%

(2.8%)

(2.8%)

13.9%

8.5%

(0.5%)

(0.3%)

(0.3%)

7.8%

16.2%

5.4%

EBITDA

$25.1

$24.8

$18.1

$22.2

$29.0

$26.7

$30.2

$28.9

$90.2

$114.8

$135.7

% margin

12.5%

12.7%

9.5%

10.2%

12.3%

11.4%

12.9%

12.4%

11.2%

12.3%

13.8%

Source: Company filings and North management.

CONFIDENTIAL

ARM Overview

Earnings miss in Q3 FY2005

ARM business was negatively impacted in Q3 FY05 by deteriorating economic conditions and

hurricanes Katrina and Rita

Strong performance expected through all of FY2006

Historically seasonal earnings with strength in Q1

Customer pricing pressure appears to have bottomed

Summary Financials

Significant ARM earnings miss, but

business rebounded in Q4

Strong performance expected to

continue through FY06

Note: Includes ARM NA and ARM International. Does not reflect intercompany eliminations.

6

CONFIDENTIAL

CRM Overview

Significant turnaround in CRM performance Q1 FY06 to Q3 FY06

Performance in 2005 negatively impacted as a result of customer losses

Investment in seat deployment for new customer ramp resulted in lower Q3 and Q4 FY05 EBITDA

Performance improvements from new customer wins demonstrated in strong Q2 to Q4 FY06 results

CRM earnings remain inherently volatile

North has 60% of FY06 revenue from top 3 customers and has suffered key customer losses in

past

Industry history of cyclical earnings and performance misses

Summary Financials

LTM 9/30/06 demonstrates turnaround and

provides confidence in Q4 FY06, but CRM

remains a difficult business model to predict

CRM is a profitable business --

decrease in profitability in Q3 FY05

reflects investment in future growth

($ in millions)

Q1:05

Q2:05

Q3:05

Q4:05

Q1:06

Q2:06

Q3:06

Q4:06

FY05

FY06

FY07

Revenue

$47.6

$43.8

$44.9

$54.1

$59.3

$62.6

$71.6

$81.3

$190.4

$274.8

$325.0

% growth (Q/Q Y/Y)

1.8%

(8.0%)

2.6%

20.4%

9.7%

5.6%

14.3%

13.6%

19.7%

44.3%

18.3%

EBITDA

$5.4

$3.0

$0.6

($0.0)

($0.5)

$0.9

$4.6

$9.8

$9.1

$14.8

$30.8

% margin

11.4%

6.9%

1.3%

(0.0%)

(0.9%)

1.5%

6.4%

12.1%

4.8%

5.4%

9.5%

Source: Company filings and North management.

7

CONFIDENTIAL

Portfolio Management Overview

Portfolio Management earnings highly dependent on purchases

Nature of business is that earnings depend on ability to continually replace / grow receivables

portfolios

Returns on new acquisitions lower as a result of highly competitive market

Earnings more volatile as a result of new accounting rules

Potential buyers will focus on underlying portfolio profile

Buyers will focus on capital requirements to achieve projected earnings

Summary Financials

Strongest consecutive four

quarter period in 2005 / 2006

($ in millions)

Q1:05

Q2:05

Q3:05

Q4:05

Q1:06

Q2:06

Q3:06

Q4:06

FY05

FY06

FY07

Revenue

$27.8

$33.0

$35.1

$48.8

$50.0

$47.7

$46.7

$45.2

$144.7

$189.7

$189.2

% growth (Q/Q Y/Y)

7.1%

18.8%

6.4%

38.9%

2.6%

(4.6%)

(2.1%)

(3.3%)

47.6%

31.1%

(0.2%)

EBITDA

$9.0

$10.8

$11.2

$16.5

$14.5

$10.4

$12.7

$12.3

$47.5

$49.9

$46.8

% margin

32.5%

32.6%

31.9%

33.8%

29.0%

21.8%

27.2%

27.3%

32.8%

26.3%

24.8%

Source: Company filings and North management.

8

($ in millions)

Q1:05

Q2:05

Q3:05

Q4:05

Q1:06

Q2:06

Q3:06

Q4:06

FY05

FY06

FY07

Revenue

$260.3

$252.4

$249.2

$290.3

$312.0

$311.4

$321.5

$330.1

$1,052.3

$1,275.0

$1,374.3

% growth (Q/Q Y/Y)

9.7%

(3.0%)

(1.3%)

16.5%

7.5%

(0.2%)

3.2%

2.7%

12.0%

21.2%

7.8%

EBITDA

$39.6

$38.6

$29.8

$38.7

$43.0

$38.0

$47.5

$51.0

$146.7

$179.5

$213.3

% margin

15.2%

15.3%

12.0%

13.3%

13.8%

12.2%

14.8%

15.5%

13.9%

14.1%

15.5%

EBIT

$28.8

$27.7

$18.5

$25.9

$29.8

$24.9

$34.1

$37.5

$101.0

$126.4

$165.5

% margin

11.1%

11.0%

7.4%

8.9%

9.6%

8.0%

10.6%

11.4%

9.6%

9.9%

12.0%

Net Income

$15.3

$14.1

$7.6

$7.5

$14.0

$11.0

$16.4

$18.6

$44.5

$60.1

$83.7

% margin

5.9%

5.6%

3.1%

2.6%

4.5%

3.5%

5.1%

5.6%

4.2%

4.7%

6.1%

EPS

$0.45

$0.42

$0.24

$0.23

$0.41

$0.33

$0.50

$0.56

$1.33

$1.80

2.44

$

Source: Company filings and North management.

CONFIDENTIAL

Consolidated Perspective

On an LTM basis, results improve significantly through Q3 FY2006

If management is able to execute on plan through Q2 FY2006, proves turnaround from FY2005

and gives credibility to Q3 and Q4 projections

Summary Financials

Successful sale requires providing buyers

with visibility into Q3 and Q4 FY06 during

the sale process

9

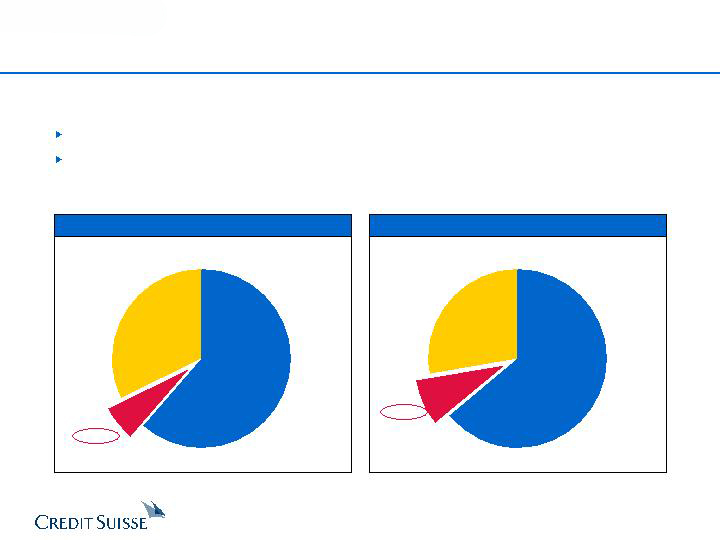

$9.1

$47.5

$90.2

ARM

61.4%

CRM

6.2%

Portfolio

Management

32.4%

CONFIDENTIAL

North Profitability by Segment

FY05 EBITDA Contribution

FY06 EBITDA Contribution

$49.9

$14.8

$114.8

ARM

64.0%

Portfolio

Management

27.8%

CRM

8.2%

($ in millions)

($ in millions)

Source: Company filings.

Source: North management.

While CRM is showing strong growth, it is not yet a significant enough contributor to overall

profitability to drive North’s current valuation

CRM represents a small part of North’s overall business profitability

Within the CRM industry, North is a smaller player and has not attracted the same trading

multiples as the CRM leaders

10

CONFIDENTIAL

3. Buyer Analysis

11

CONFIDENTIAL

Key Buyer Perspectives

North projections show a strong turnaround from FY2005 to FY2006

Buyer may need to see four quarters of demonstrated improvement (Q4 FY05 to Q3

FY06) to give credit to North’s growth plan

By end of Q3 FY06, North should be able to provide buyer with visibility and

confidence in Q4 projections; CRM backlog for Q4 FY06 will be critical

North

Projections

Financial

Sponsor

Considerations

Sponsors focus on leverage capacity and five-year IRR analysis

Bank debt markets primarily rely on LTM EBITDA to determine level of leverage

North LTM EBITDA improves significantly in Q3 FY06

“Rolling” LBO analysis suggests inflection point is Q2 / Q3 FY06

Strategic Buyer

Considerations

Strategic buyers focus on intrinsic valuation (DCF) as well as multiples-based

approach

Demonstrating turnaround with several quarters of growth provides confidence in

management plan

Will value business on its long-term growth and profitability potential

Significant improvement in

LTM EBITDA from 6/30 to

9/30 may enable sponsor to

increase leverage in an LBO

($ in millions)

LTM EBITDA as of

3/31/06

6/30/06

9/30/06

12/31/06

$150.1

$149.6

$167.2

$179.5

Source: Actuals from company filings, projections from North management.

12

North Base Case Projections

CONFIDENTIAL

Updated Preliminary LBO Assumptions

CS has performed a preliminary LBO analysis based on the following assumptions:

Total leverage 5.0x LTM EBITDA:

3.0x LTM EBITDA Term Loan A, price of L + 325 bps

2.0x LTM EBITDA Term Loan B, price of L + 725 bps

3-month LIBOR of 5.10%

CS has evaluated an LBO at 6/30/06 as well as a “rolling” LBO taking place at 9/30/06 and

12/31/06

($ in millions)

FYE December 31,

'06E - '11E

2006E

2007E

2008E

2009E

2010E

2011E

CAGR

Revenue

$1,275.0

$1,374.3

$1,463.3

$1,567.4

$1,684.9

$1,811.6

7.3%

% growth

21.2%

7.8%

6.5%

7.1%

7.5%

7.5%

Gross Profit

605.0

654.0

693.4

741.0

794.4

851.6

7.1%

% margin

47.5%

47.6%

47.4%

47.3%

47.1%

47.0%

EBITDA

179.5

213.3

235.5

252.9

271.0

292.4

10.3%

% margin

14.1%

15.5%

16.1%

16.1%

16.1%

16.1%

EBIT

126.4

165.5

190.7

208.8

229.8

253.3

14.9%

% margin

9.9%

12.0%

13.0%

13.3%

13.6%

14.0%

Source: North Management.

13

CONFIDENTIAL

Updated Preliminary LBO Analysis (cont’d)

Sponsor may

view risk in

management

plan and build

adjusted case

Illustrative LBO Sensitivity Analysis

Transaction Assumptions

Financing Assumptions

(1) Fees and expenses equal to 2% of debt offered plus $10MM.

Purchase Price

$28.00

Premium to Current

28.4%

Equity Purchase Price

$927.8

Plus: Revolving Debt

249.7

Plus: Non-Recourse Debt

54.1

Plus: Capital Leases

2.7

Plus: Minority Interest

39.4

Less: Existing Cash

(36.0)

Aggregate Value

$1,237.7

LTM EBITDA (6/30/06)

149.6

Implied Purchase Multiple

8.3x

Sources:

Leverage

Rate

Term Loan A

3.0x

8.35%

$448.7

Term Loan B

2.0x

12.35%

299.1

New Non-Recourse Debt

54.1

Common Equity

454.6

Total Sources

$1,256.6

Uses:

Purchase of Equity

$927.8

Refinance Revolving Debt

249.7

Refinance Non-Recourse Debt

54.1

Transaction Expenses

(1)

25.0

Total Uses

$1,256.6

Imp. AV

$1,166.3

$1,202.0

$1,237.7

$1,273.4

$1,309.1

Shr. Price

$26.00

$27.00

$28.00

$29.00

$30.00

EBITDA Purchase Price Multiple

7.8x

8.0x

8.3x

8.5x

8.8x

CY06-CY10

0.0%

34.7%

32.3%

30.1%

28.2%

26.4%

Change in

(2.5%)

30.6%

28.3%

26.2%

24.3%

22.6%

Rev. Growth v.

(5.0%)

26.4%

24.2%

22.2%

20.3%

18.6%

Mgmt. Case

(7.5%)

21.9%

19.8%

17.8%

16.1%

14.4%

14

CONFIDENTIAL

Preliminary “Rolling” LBO Analysis

Assumes sponsor applies 5% discount to Base Case revenue growth

(+$88.2)

(+$61.4)

($ in millions, except per share amounts)

LBO Date

As of 6/30/06

As of 9/30/06

As of 12/31/06

LTM EBITDA

$149.6

$167.2

$179.5

Debt Capacity (@ 5.0x Leverage)

$747.8

$836.0

$897.4

Targeted IRR

20.0%

Stock Price

$29.18

$30.83

$32.22

PV Stock Price

(1)

$29.18

$29.64

$29.77

Implied LTM EBITDA Multiple

8.6x

7.8x

7.4x

25.0%

Stock Price

$26.61

$28.53

$30.12

PV Stock Price

(1)

$26.61

$27.43

$27.83

Implied LTM EBITDA Multiple

7.9x

7.3x

6.9x

Note: Exit multiple assumed to be 8.0x LTM EBITDA. Assumes 5% discount to revenue growth v. North base case.

(1) Discounted from time of LBO to June 30, 2006 at 17% discount rate.

Q3 FY05 still in LTM period -- greater potential

a buyer will view risk in management plan and

assume lower long term growth potential

15

CONFIDENTIAL

CS Preliminary Conclusions

If North’s Board decides to proceed with a potential sale, CS believes that the

timetable should be constructed so that a buyer has full confidence in the Q3

FY 06 results

Sale process timetable should enable North to capture the value in

performance improvements

Should have four quarters (Q4 FY05 to Q3 FY06) to demonstrate the turnaround

from Q3 FY05

Provide potential buyer with confidence in Q3 and Q4 FY06, supported by

contracted revenue / backlog

Eliminate Q3 FY05 from the LTM period

Decision on process timing must take account of execution risk in the North’s

plan

ARM has stabilized but remains highly competitive and has experienced

setbacks in the past

Portfolio Management earnings dependent on ability to find attractive portfolio

purchases in the future (increasingly competitive)

CRM has significant customer concentration with contracts that are easily

terminable

M&A and LBO markets are currently strong and will be conducive to

competitive process

Record levels of leveraged loans

Strategic and financial buyers are actively acquiring companies

16

CONFIDENTIAL

2

Data room / due

diligence

Management

presentations

1

4

3

5

Data room / due

diligence

Management

presentations

7

6

9

8

11

10

12

Data room / due

diligence

14

13

16

15

18

17

19

31

28

27

30

29

21

20

23

22

24

26

25

SUNDAY

MONDAY

TUESDAY

WEDNESDAY

THURSDAY

FRIDAY

SATURDAY

2

Data room / due

diligence

Management

presentations

1

4

3

5

Data room / due

diligence

Management

presentations

7

6

9

8

11

10

12

Data room / due

diligence

14

13

16

15

18

17

19

31

28

27

30

29

21

20

23

22

24

26

25

2

Data room / due

diligence

Management

presentations

1

4

3

5

2

2

Data room / due

diligence

Management

presentations

1

Data room / due

diligence

Management

presentations

1

4

4

3

3

5

5

Data room / due

diligence

Management

presentations

7

6

9

8

11

10

12

Data room / due

diligence

Management

presentations

7

Data room / due

diligence

Management

presentations

7

6

6

9

9

8

8

11

11

10

10

12

12

Data room / due

diligence

14

13

16

15

18

17

19

Data room / due

diligence

14

Data room / due

diligence

14

13

13

16

16

15

15

18

18

17

17

19

19

31

28

27

30

29

31

31

28

28

27

27

30

30

29

29

21

20

23

22

24

26

25

21

21

20

20

23

23

22

22

24

24

26

26

25

25

Summer market slowdown

Summer market slowdown

Preliminary Process Timetable

June 2006 (Start initial work end of May)

August 2006

July 2006

September 2006

SUNDAY

MONDAY

TUESDAY

WEDNESDAY

THURSDAY

FRIDAY

SATURDAY

2

1

3

12

11

14

13

16

15

17

Start calls to

strategic buyers

Meetings with

strategic buyers

19

18

21

20

23

22

24

26

25

28

27

30

29

7

6

9

8

10

4

5

2

3

12

11

14

13

16

15

17

Start calls to

strategic buyers

Meetings with

strategic buyers

19

18

21

20

23

22

24

26

25

28

27

30

29

7

6

9

8

10

4

5

2

3

2

2

3

3

12

11

14

13

16

15

17

12

12

11

11

14

14

13

13

16

16

15

15

17

17

Start calls to

strategic buyers

Meetings with

strategic buyers

19

18

21

20

23

22

24

Start calls to

strategic buyers

Meetings with

strategic buyers

19

Start calls to

strategic buyers

Meetings with

strategic buyers

19

18

18

21

21

20

20

23

23

22

22

24

24

26

25

28

27

30

29

26

26

25

25

28

28

27

27

30

30

29

29

7

6

9

8

10

4

5

7

7

6

6

9

9

8

8

10

10

4

4

5

5

SUNDAY

MONDAY

TUESDAY

WEDNESDAY

THURSDAY

FRIDAY

SATURDAY

1

2

Final bids

11

10

13

12

15

14

16

Announcement

18

17

20

19

22

21

23

25

24

27

26

29

28

30

7

3

6

Due diligence

5

8

9

Labor

Day

4

1

2

Final bids

11

10

13

12

15

14

16

Announcement

18

17

20

19

22

21

23

25

24

27

26

29

28

30

7

3

6

Due diligence

5

8

9

Labor

Day

4

1

2

1

1

2

2

Final bids

11

10

13

12

15

14

16

Final bids

11

Final bids

11

10

10

13

13

12

12

15

15

14

14

16

16

Announcement

18

17

20

19

22

21

23

Announcement

18

Announcement

18

17

17

20

20

19

19

22

22

21

21

23

23

25

24

27

26

29

28

30

25

25

24

24

27

27

26

26

29

29

28

28

30

30

7

3

6

Due diligence

5

8

9

Labor

Day

4

7

7

3

3

6

6

Due diligence

5

Due diligence

5

8

8

9

9

4

4

4

Final negotiations

SUNDAY

MONDAY

TUESDAY

WEDNESDAY

THURSDAY

FRIDAY

SATURDAY

9

12

11

Meetings with

financial buyers

10

13

15

14

Independence

Day

4

Meetings with

strategic buyers

3

2

Distribute

CIM

Start calls to

financial

sponsors

5

7

6

8

1

Respond to

diligence

questions

24

23

26

25

28

27

29

16

19

18

21

20

22

17

30

First round

bids

31

9

12

11

Meetings with

financial buyers

10

13

15

14

Independence

Day

4

Meetings with

strategic buyers

3

2

Distribute

CIM

Start calls to

financial

sponsors

5

7

6

8

1

Respond to

diligence

questions

24

23

26

25

28

27

29

16

19

18

21

20

22

17

30

First round

bids

31

9

12

11

Meetings with

financial buyers

10

13

15

14

Independence

Day

4

Meetings with

strategic buyers

3

2

Distribute

CIM

Start calls to

financial

sponsors

5

7

6

8

1

Respond to

diligence

questions

24

23

26

25

28

27

29

16

19

18

21

20

22

17

30

First round

bids

31

9

12

11

Meetings with

financial buyers

10

13

15

14

9

12

12

11

11

financial buyers

10

13

13

15

15

14

14

Independence

Day

4

Meetings with

strategic buyers

3

2

Distribute

CIM

Start calls to

financial

sponsors

5

7

6

8

Independence

Day

4

Independence

Day

4

Meetings with

3

Meetings with

2

Distribute

CIM

Start calls to

financial

sponsors

5

Distribute

CIM

Start calls to

financial

sponsors

5

7

7

6

6

8

8

1

1

Respond to

diligence

questions

24

23

26

25

28

27

29

Respond to

diligence

questions

24

Respond to

diligence

questions

24

23

23

26

26

25

25

28

28

27

27

29

29

16

19

18

21

20

22

17

16

16

19

19

18

18

21

21

20

20

22

22

17

17

30

First round

bids

31

30

30

First round

bids

31

First round

bids

31

17

CONFIDENTIAL

Preliminary Process Timetable (cont’d)

Closing

Anti-trust and other regulatory approvals, as necessary

Closing

Stage 1: Initial Due

Diligence / Market

Assessment

Conduct management presentations

Provide data room access / assist buyers with due diligence

Distribution of process letter and draft SPA

Provide parties preliminary Q3 results

Stage 3: Due

Diligence

CS receives initial indications and reports to Board

Selection of preferred buyer(s)

SPA negotiation with preferred buyer(s)

Board approvals

Execution of definitive agreements

Transaction announcement

Stage 4: Negotiation

/ Announcement

Stage

Description

Timing

Start end of May

3 weeks

(Weeks of Jun 19 - Jul 3)

6 Weeks

(Weeks of Jul 31 - Sep 11)

Receive final bids from potential buyers

Due diligence

Preparation of marketing materials (teaser, info memo, short-form management presentation)

Determine targeted buyers

Conduct short-form management presentation to selected group of Tier 1 strategic buyers

Determine level of Tier 1 strategic buyer interest

2 Weeks

(Weeks of Sep 11 - 18)

18

If limited Tier 1 strategic interest indicated, go broad

Contact Tier 2 strategic and all financial buyers and execute NDAs if decision to go broad

Contact financial buyers

Distribute info memo to all contacted buyers (include Q2 results)

Stage 2: Distribute

Info Memorandum

5 Weeks

(Weeks of Jul 3 - Jul 31)

Discuss with Board next steps

CONFIDENTIAL

Appendix

19

CONFIDENTIAL

A. Preliminary Valuation

20

$26.50

$25.00

$26.00

$30.00

$31.00

$29.00

$10

$20

$30

$40

Selected

Acquisitions

DCF

Leveraged

Buyout

Preliminary Valuation Summary

($ in millions, except per share amounts)

Current: $21.80

52 Week Lo: $15.28

52 Week Hi: $24.31

Note: Assumes debt of $345.8MM (includes minority interest) and cash of $36.0 million, as of 6/30/06.

Share Price

$26.00

-

$29.00

$25.00

-

$31.00

$26.50

-

$30.00

Equity Value

$856.4

-

$963.5

$820.7

-

$1,035.4

$874.3

-

$999.2

Enterprise Value

$1,166.3

-

$1,273.4

$1,130.6

-

$1,345.3

$1,184.1

-

$1,309.1

Prem. to Avg. Stock Price over Period:

30 Day Average

$22.51

15.5%

-

28.8%

11.1%

-

37.7%

17.7%

-

33.3%

60 Day Average

$21.61

20.3%

-

34.2%

15.7%

-

43.4%

22.6%

-

38.8%

90 Day Average

$20.00

30.0%

-

45.0%

25.0%

-

55.0%

32.5%

-

50.0%

120 Day Average

$19.16

35.7%

-

51.3%

30.5%

-

61.8%

38.3%

-

56.5%

Statistic

Implied Multiple

Implied Multiple

Implied Multiple

Enterprise Value / Revenue

CY2006E Revenue

$1,275

0.9x

-

1.0x

0.9x

-

1.1x

0.9x

-

1.0x

CY2007E Revenue

1,374

0.8x

-

0.9x

0.8x

-

1.0x

0.9x

-

1.0x

Enterprise Value / EBITDA

CY2006E EBITDA

$179

6.5x

-

7.1x

6.3x

-

7.5x

6.6x

-

7.3x

CY2007E EBITDA

213

5.5x

-

6.0x

5.3x

-

6.3x

5.6x

-

6.1x

Enterprise Value / Unlevered NI

CY2006E Unlevered NI

$79

14.8x

-

16.2x

14.4x

-

17.1x

15.0x

-

16.6x

CY2007E Unlevered NI

$102

11.4x

-

12.4x

11.0x

-

13.1x

11.6x

-

12.8x

21

CONFIDENTIAL

Preliminary Selected Acquisitions Analysis

($ in millions)

Date

Acquirer

Target

1/30/06

West Corp

Intrado

9/22/05

CVC International

Dun & Bradstreet - (ARM business)

9/12/05

NCO Group

Risk Management Alternatives

7/14/05

Genpact

Creditek Corp

6/30/05

Affiliated Computer Services

LiveBridge Corp

5/16/05

H-Cube LLC

Zenta Group

2/2/05

IBM Corp

Equitant

11/16/04

Mellon

SourceNet Solutions

11/8/04

Medassist

Argent

10/8/04

ICICI OneSource

Account Solutions Group

9/17/04

SLM Corp

Arrow Financial Services

7/23/04

West Corp

Worldwide Asset Management

5/25/04

Vertex

First Revenue Assurance

5/4/04

Convergys Corp

Encore Receivable Management

4/6/04

Daksh eServices

IBM Corp

3/22/04

ECE Holdings (H.I.G. Capital)

Stream International

2/2/04

Barclays Private Equity / Vision Capital

Cabot Financial (Europe)

1/15/04

CFSI

Genesis Financial Solutions

12/4/03

AllianceOne

TCH Group

11/18/03

NCO Group

RMH Teleservices

1/17/03

Affiliated Computer Services

CyberRep.com

8/1/02

Parthenon Capital

Arrow Financial Services

7/23/02

West Corp

Attention LLC

9/25/01

Solectron

Stream International

7/17/01

SNT Group NV

KPN NV - (CRM business)

7/17/01

SNT Group NV

Atos SA (CRM business)

3/13/01

Management Group / Intrum Justitia BV

Dun & Bradstreet - (ARM business)

(1) H-Cube acquired an 80% stake in Zenta Group for $80 million. GTCR Golder Rauner invested a further $20 million for a 20% stake.

(2) SLM Corp acquired a 64% stake in Arrow Financial Services and has the option to purchase the remaining interest over a three-year period.

Enterprise Value

Enterprise

as a multiple of

Target Description / Rationale

Value

Revenues

EBITDA

EBIT

Global provider of integrated data and telecommunications solutions.

$478

3.2x

13.5x

25.7x

Provides receivable management services worldwide.

NA

NA

NA

NA

Provider of debt collection and accounts receivable management services.

$119

0.5x

4.0x

NA

Supplies outsourced accounts receivable consultation and management services to accounts receivable departments of small to mid-sized

corporations.

NA

NA

NA

NA

Offers outsourced and professional services to the contact center and business process markets.

$32

NA

NA

NA

Operates as a business process outsourcing company.

$100

(1)

NA

NA

NA

Expands business consulting unit by acquiring provider of finance and accounting outsourcing services

NA

NA

NA

NA

Adds accounts payable processing capability

NA

NA

NA

NA

Acquisition of Argent HFS adds complementary business and increases geographic reach, customer services and resources

NA

NA

NA

NA

Operates as a consumer collections agency.

NA

NA

NA

NA

Engages in purchasing and servicing performing and non-performing consumer debt.

NA

(2)

NA

NA

NA

Purchaser and collector of delinquent accounts receivable portfolios from consumer credit originators.

$178

1.7x

NA

NA

Acquisition of FRA (U.S. based debt collection agency) followed Vertex’s announcement of the establishment of Vertex Outsourcing, a North

American management subsidiary; $12 million of revenue in 2003

NA

NA

NA

NA

Provides receivable management solutions.

$68

NA

NA

NA

Offers online customer relationship management services.

$155

3.0x

8.0x

NA

Provides technical support and customer service outsourcing for the high-tech industry in the U.S. and Europe.

NA

NA

NA

NA

Provides debt purchasing and credit management solutions in the U.K.

£100

NA

NA

NA

TxCollect, a subsidiary of Collins, acquired consumer debt collection debt collection facility of Genesis Financial Solutions, which will expand

TxCollect’s rapidly growing contingency business

NA

NA

NA

NA

Expand Alliance’s outsourcing capabilities and enhances its near shore international offerings

NA

NA

NA

NA

Provides CRM solutions through various cannels including voice, VoIP, email, chat and self-help.

$109

0.4x

9.9x

NM

Provider of outsourced customer service, technical support and CRM solutions.

NA

NA

NA

NA

Engages in purchasing and servicing performing and non-performing consumer debt.

$45

NA

NA

NA

Accounts receivable management company.

$40

NA

NA

NA

Provides CRM solutions through various cannels including voice, VoIP, email, chat and self-help.

$329

1.0x

7.9x

13.8x

Provides call centers, inbound services, conferencing services and consulting and CRM training.

€180

NA

NA

NA

Provides customer call centers.

€ 69

NA

NA

NA

Provider of debt collection and accounts receivable management services.

$120

0.8x

4.9x

NA

Mean

1.5x

8.0x

19.8x

Median

1.0x

7.9x

19.8x

Note: Assumes debt of $345.8MM (includes minority interest) and cash of $36.0 million, as of 6/30/06.

($ in millions, except per share amounts)

Statistic

Multiple Range

Implied Enterprise Value

Implied Equity Value

Implied Share Price

CY2005 Revenue

$1,052.3

1.0x

-

1.5x

$1,052

-

$1,578

$742

-

$1,269

$22.81

-

$37.38

CY2005 EBITDA

$146.7

7.0x

-

9.5x

$1,027

-

$1,394

$717

-

$1,084

$22.11

-

$32.34

Preliminary Valuation Reference Range

$1,250

-

$1,350

$940

-

$1,040

$28.34

-

$31.13

22

CONFIDENTIAL

Preliminary Discounted Cash Flow Analysis

DCF Assumptions

DCF Sensitivity

Discount

Terminal Multiple of 2011E EBITDA

Rate

5.5x

6.0x

6.5x

14.0%

$478

$478

$478

Present Value of Free Cash Flow

1,608

1,754

1,901

Terminal Value

835

911

987

Present Value of Terminal Value

$1,313

$1,389

$1,465

Implied Aggregate Value

1,003

1,079

1,155

Implied Equity Value

$30.10

$32.19

$34.26

Equity Value Per Share

5.4%

6.1%

6.6%

Perpetuity Growth

15.0%

$467

$467

$467

Present Value of Free Cash Flow

1,608

1,754

1,901

Terminal Value

799

872

945

Present Value of Terminal Value

$1,267

$1,339

$1,412

Implied Aggregate Value

957

1,029

1,102

Implied Equity Value

$28.81

$30.84

$32.82

Equity Value Per Share

6.3%

7.0%

7.6%

Perpetuity Growth

16.0%

$457

$457

$457

Present Value of Free Cash Flow

1,608

1,754

1,901

Terminal Value

765

835

905

Present Value of Terminal Value

$1,223

$1,292

$1,362

Implied Aggregate Value

913

982

1,052

Implied Equity Value

$27.58

$29.53

$31.46

Equity Value Per Share

7.2%

7.9%

8.5%

Perpetuity Growth

($ in millions)

FYE Dec 31,

2H:2006

2007

2008

2009

2010

1H:2011

Revenue

$652

$1,374

$1,463

$1,567

$1,685

$906

% Growth

4.5%

7.8%

6.5%

7.1%

7.5%

7.5%

Gross Profit

$309

$654

$693

$741

$794

$426

% of Revenue

47.4%

47.6%

47.4%

47.3%

47.1%

47.0%

EBIT

$72

$165

$191

$209

$230

$127

% Margin

11.0%

12.0%

13.0%

13.3%

13.6%

14.0%

After-Tax Unlev. FCF

$95.4

$135.8

$132.1

$123.7

$125.3

$65.6

23

CONFIDENTIAL

CONFIDENTIAL

Preliminary DCF Sensitivity Analysis

Sale price dependent on ability to prove margin and growth of business

DCF Sensitivity - 6.0x terminal EBITDA Multiple; 15.0% WACC

A potential acquiror’s ability to pay a substantial premium will be driven by their ability to

establish synergy opportunities

However, risk exists potential acquiror will create their own lower financial plan

Incremental Revenue Growth

(1.00%)

(0.75%)

(0.50%)

(0.25%)

0.00%

(1.00%)

$26.76

$27.15

$27.54

$27.94

$28.34

Incremental

(0.75%)

$27.36

$27.76

$28.16

$28.56

$28.97

EBIT Margin

(0.50%)

$27.96

$28.36

$28.77

$29.18

$29.59

(0.25%)

$28.56

$28.97

$29.38

$29.80

$30.22

0.00%

$29.16

$29.57

$29.99

$30.42

$30.84

24

CONFIDENTIAL

Preliminary LBO Analysis - As of 9/30/06

Sponsor may

view risk in

management

plan and build

adjusted case

Illustrative LBO Sensitivity Analysis

Transaction Assumptions

Financing Assumptions

(1) Fees and expenses equal to 2% of debt offered plus $10MM.

Sources:

Leverage

Rate

Term Loan A

3.0x

8.35%

$501.6

Term Loan B

2.0x

12.35%

334.4

New Non-Recourse Debt

47.7

Common Equity

345.2

Total Sources

$1,228.9

Uses:

Purchase of Equity

$927.8

Refinance Revolving Debt

226.6

Refinance Non-Recourse Debt

47.7

Transaction Expenses

(1)

26.7

Total Uses

$1,228.9

Purchase Price

$28.00

Premium to Current

28.4%

Equity Purchase Price

$927.8

Plus: Revolving Debt

226.6

Plus: Non-Recourse Debt

47.7

Plus: Capital Leases

1.6

Plus: Minority Interest

41.8

Less: Existing Cash

(42.1)

Aggregate Value

$1,203.4

LTM EBITDA (9/30/06)

167.2

Implied Purchase Multiple

7.2x

Imp. AV

$1,131.9

$1,167.6

$1,203.4

$1,239.1

$1,274.8

Shr. Price

$26.00

$27.00

$28.00

$29.00

$30.00

EBITDA Purchase Price Multiple

26.3%

6.8x

7.0x

7.2x

7.4x

7.6x

CY06-CY10

0.0%

42.5%

39.0%

36.0%

33.4%

31.0%

Change in

(2.5%)

37.6%

34.2%

31.3%

28.8%

26.5%

Rev. Growth v.

(5.0%)

32.3%

29.1%

26.3%

23.9%

21.7%

Mgmt. Case

(7.5%)

26.7%

23.6%

21.0%

18.6%

16.5%

25

CONFIDENTIAL

Preliminary LBO Analysis - As of 12/31/06

Illustrative LBO Sensitivity Analysis

Transaction Assumptions

Financing Assumptions

Sponsor may

view risk in

management

plan and build

adjusted case

(1) Fees and expenses equal to 2% of debt offered plus $10MM.

Imp. AV

$1,097.6

$1,133.3

$1,169.0

$1,204.7

$1,240.4

Shr. Price

$26.00

$27.00

$28.00

$29.00

$30.00

EBITDA Purchase Price Multiple

31.5%

6.1x

6.3x

6.5x

6.7x

6.9x

CY06-CY10

0.0%

52.3%

47.1%

42.9%

39.3%

36.2%

Change in

(2.5%)

46.4%

41.5%

37.4%

34.0%

31.0%

Rev. Growth v.

(5.0%)

40.2%

35.4%

31.5%

28.2%

25.3%

Mgmt. Case

(7.5%)

33.2%

28.7%

25.0%

21.8%

19.1%

Purchase Price

$28.00

Premium to Current

28.4%

Equity Purchase Price

$927.8

Plus: Revolving Debt

203.6

Plus: Non-Recourse Debt

41.3

Plus: Capital Leases

0.4

Plus: Minority Interest

44.1

Less: Existing Cash

(48.2)

Aggregate Value

$1,169.0

LTM EBITDA (12/31/06)

179.5

Implied Purchase Multiple

6.5x

Sources:

Leverage

Rate

Term Loan A

3.0x

8.35%

$538.5

Term Loan B

2.0x

12.35%

359.0

New Non-Recourse Debt

41.3

Common Equity

261.9

Total Sources

$1,200.6

Uses:

Purchase of Equity

$927.8

Refinance Revolving Debt

203.6

Refinance Non-Recourse Debt

41.3

Transaction Expenses

(1)

27.9

Total Uses

$1,200.6

26

CONFIDENTIAL

Weighted Average Cost of Capital Analysis

Assumptions

Cost of Equity

Tax Rate

35.00%

Cost of Equity = Risk Free Rate + Beta * Equity Risk Premium + Size Premium

Risk Free Rate (20 year)

(1)

5.11%

= 5.11% + 1.10 * 7.2% + 4.02%

Equity Risk Premium

(2)

7.20%

= 17.0%

Size Premium

4.02%

Industry Statistics

Debt /

Levering

Unlevered

Cost of

Beta

(3)

Mkt Eq.

Factor

(4)

Beta

(5)

Equity

NCOG

1.42

57.1%

1.37

1.03

12.6%

APAC

1.40

11.4%

1.07

1.31

14.5%

CVG

1.14

15.5%

1.10

1.03

12.5%

ICTG

1.09

9.5%

1.06

1.03

12.5%

737143

0.99

25.2%

1.16

0.85

11.2%

PSPT

1.03

0.0%

1.00

1.03

12.5%

SWW

1.12

44.0%

1.29

0.87

11.4%

599933

2.11

29.5%

1.19

1.77

17.8%

SRT

0.99

1.6%

1.01

0.97

12.1%

SYKE

1.11

0.0%

1.00

1.11

13.1%

TTEC

1.25

3.8%

1.02

1.22

13.9%

AACC

1.41

0.0%

1.00

1.41

15.3%

PRAA

0.99

2.1%

1.01

0.98

12.1%

ECPG

1.14

56.6%

1.37

0.83

11.1%

ASFI

1.14

18.2%

1.12

1.02

12.5%

Average

18.3%

1.10

13.0%

Plus: Size Premium

4.0%

Cost of Equity

17.0%

Cost of Capital

Pre-tax Cost of Debt

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

10.0%

10.5%

11.0%

After-tax Cost of Debt

3.9%

4.2%

4.6%

4.9%

5.2%

5.5%

5.9%

6.2%

6.5%

6.8%

7.2%

Debt/

Debt/

Average

Lev.

Levered

Cost of

Debt/

Size

Capital

Equity

Unlev. Beta

Factor

Beta

(6)

Equity

(7)

Capital

Premium

WEIGHTED AVERAGE COST OF CAPITAL

(8)

0.0%

0.0%

1.10

1.00

1.10

13.0%

0.0%

4.02%

17.0%

17.0%

17.0%

17.0%

17.0%

17.0%

17.0%

17.0%

17.0%

17.0%

17.0%

5.0%

5.3%

1.10

1.03

1.14

13.3%

5.0%

4.02%

16.6%

16.6%

16.7%

16.7%

16.7%

16.7%

16.7%

16.7%

16.8%

16.8%

16.8%

10.0%

11.1%

1.10

1.07

1.18

13.6%

10.0%

4.02%

16.2%

16.3%

16.3%

16.3%

16.4%

16.4%

16.4%

16.5%

16.5%

16.5%

16.6%

15.0%

17.6%

1.10

1.11

1.22

13.9%

15.0%

4.02%

15.8%

15.9%

15.9%

16.0%

16.0%

16.1%

16.1%

16.2%

16.2%

16.3%

16.3%

20.0%

25.0%

1.10

1.16

1.28

14.3%

20.0%

4.02%

15.4%

15.5%

15.6%

15.6%

15.7%

15.8%

15.8%

15.9%

16.0%

16.0%

16.1%

25.0%

33.3%

1.10

1.22

1.34

14.7%

25.0%

4.02%

15.0%

15.1%

15.2%

15.3%

15.4%

15.4%

15.5%

15.6%

15.7%

15.8%

15.8%

30.0%

42.9%

1.10

1.28

1.40

15.2%

30.0%

4.02%

14.6%

14.7%

14.8%

14.9%

15.0%

15.1%

15.2%

15.3%

15.4%

15.5%

15.6%

35.0%

53.8%

1.10

1.35

1.48

15.8%

35.0%

4.02%

14.2%

14.3%

14.5%

14.6%

14.7%

14.8%

14.9%

15.0%

15.1%

15.3%

15.4%

40.0%

66.7%

1.10

1.43

1.57

16.4%

40.0%

4.02%

13.8%

14.0%

14.1%

14.2%

14.4%

14.5%

14.6%

14.7%

14.9%

15.0%

15.1%

45.0%

81.8%

1.10

1.53

1.68

17.2%

45.0%

4.02%

13.4%

13.6%

13.7%

13.9%

14.0%

14.2%

14.3%

14.5%

14.6%

14.8%

14.9%

50.0%

100.0%

1.10

1.65

1.81

18.1%

50.0%

4.02%

13.0%

13.2%

13.4%

13.5%

13.7%

13.8%

14.0%

14.2%

14.3%

14.5%

14.7%

(1)

Interpolated yield on the 20-year U.S. Treasury bond (4/25/06).

(7)

Cost of Equity: Rf + B ( Rm - Rf ).

(2)

The average historic spread between the return on stocks and l-t bonds (Ibbotson Ass.)

(8)

WACC: Rd = Return on Debt Re = Return on Equity

(3)

Barra U.S. Equity Beta Book predictions

[ Rd * ( 1 - tax rate ) * ( D / (D + E) ) ] + [ Re * ( E / (D+E) ) ]

(4)

Levering Factor: 1 + [ ( 1 - tax rate ) * ( debt / equity ratio ) ]

(5)

Unlevered Beta: ( Beta / Levering Factor )

(6)

Levered Beta: ( Beta * Levering Factor )

27

CONFIDENTIAL

B. Recent Trading Performance

28

CONFIDENTIAL

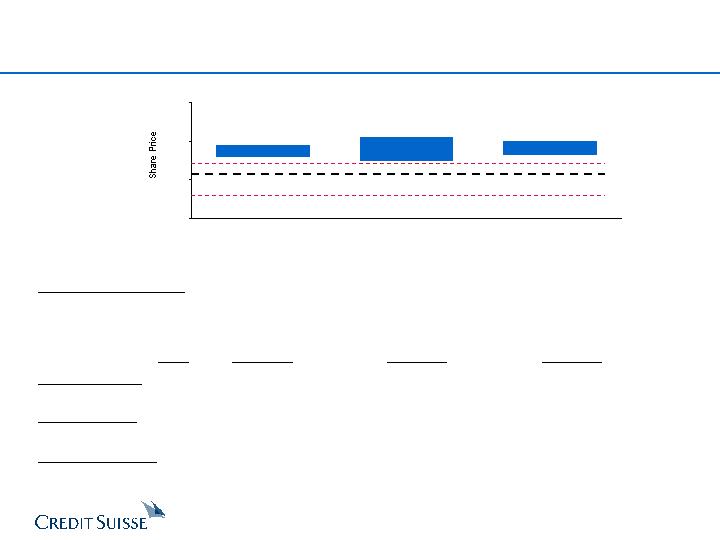

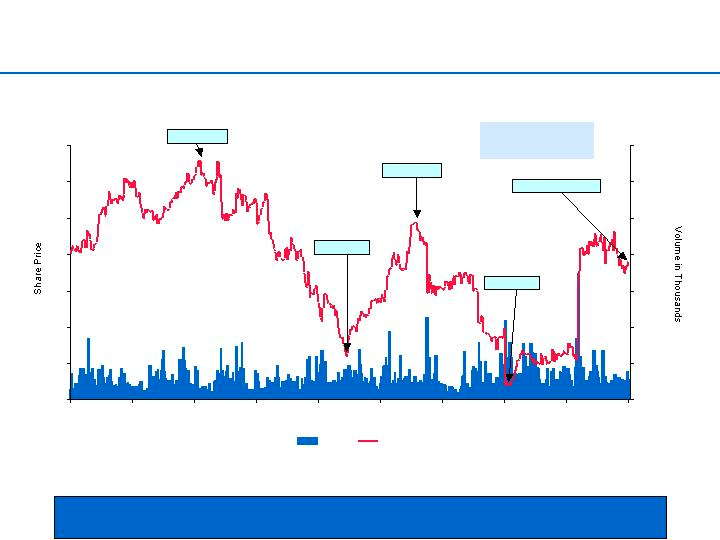

North’s Stock Price Has Recently Rebounded

North’s stock price has recently rebounded as a result of exceeding analysts

expectations in Q4 and providing strong guidance for 2006

April 20, 2004 to April 21, 2006

Source: FactSet.

Note: Outsourced CRM Services composite includes APAC, Convergys, ICT Group, Intrum Justitia, PeopleSupport, Sitel, SR Teleperformance, Startek, Sykes Enterprises, Teletech

$15

$17

$19

$21

$23

$25

$27

$29

4/20/04

7/12/04

9/29/04

12/17/04

3/10/05

5/31/05

8/18/05

11/7/05

1/30/06

4/20/06

0

300

600

900

1,200

1,500

1,800

2,100

Volume

North

NTM P/E: 15.1x

NTM P/E: 9.2x

NTM P/E: 13.1x

NTM P/E: 8.4x

Current NTM P/E: 12.8x

Current NTM P/E Multiples

Outsourced CRM:

Portfolio Purchasers:

12.7x

21.3x

and West.

Portfolio Purchasers composite includes Asset Acceptance, Asta Funding, Encore Capital and Portfolio Recovery.

29

CONFIDENTIAL

Trading Statistics of Comparable Companies

(USD millions, except per share amounts)

Trading Performance

FD Capitalization

Stock

Disc.

/ Prem.

Equity

Aggr.

FD Aggregate Value /

LT

CY2007

Price

to LTM

Market

Market

P/E Multiples

Revenue

EBITDA

Gr. Rate

PE /

COMPANY (FYE)

4/25/06

High

Low

Value

Value

CY06

CY07

CY06

CY07

CY06

CY07

(LTGR)

LTGR

NORTH (MANAGEMENT) (Dec.)

$21.80

(10.3%)

42.7%

$704

$1,082

12.1x

8.9x

0.8x

0.8x

6.0x

5.1x

12.0%

0.7x

NORTH (STREET) (Dec.)

$21.80

(10.3%)

42.7%

$704

$1,082

12.7x

11.5x

0.9x

0.9x

6.2x

6.0x

12.0%

1.0x

Outsourced CRM Services

WEST CORP (Dec.)

$47.07

(4.9%)

51.0%

$3,458

$3,703

20.9x

18.8x

2.2x

2.1x

8.9x

8.5x

16.6%

1.1x

CONVERGYS CORP (Dec.)

19.60

0.0%

55.8%

2,780

3,016

18.0x

16.1x

1.1x

1.0x

7.3x

6.8x

11.9%

1.4x

SR TELEPERFORMANCE (Dec.)

40.05

0.0%

43.3%

1,429

1,642

19.3x

17.1x

1.0x

0.9x

7.6x

6.9x

9.6%

1.8x

TELETECH HOLDINGS INC (Dec.)

12.70

(2.4%)

73.0%

908

910

26.5x

19.5x

0.8x

0.7x

8.4x

7.4x

23.3%

0.8x

INTRUM JUSTITIA NV (Dec.)

9.34

(5.2%)

41.2%

732

890

14.2x

13.3x

2.2x

2.1x

10.2x

9.6x

NA

NA

SYKES ENTERPRISES INC (Dec.)

16.00

(1.4%)

136.0%

648

520

27.6x

22.2x

1.0x

0.9x

10.1x

8.8x

NA

NM

ICT GROUP INC (Dec.)

27.20

(2.0%)

205.6%

369

393

24.3x

19.2x

0.9x

0.8x

9.1x

7.9x

20.0%

1.0x

STARTEK INC (Dec.)

23.02

(5.0%)

100.2%

343

303

24.5x

21.1x

1.3x

1.2x

8.0x

7.4x

15.5%

1.4x

SITEL CORP (Dec.)

4.47

0.0%

181.1%

338

449

14.9x

NA

NA

NA

5.2x

NA

NA

NM

PEOPLESUPPORT INC (Dec.)

11.25

(1.1%)

57.1%

217

175

28.1x

22.5x

2.0x

1.6x

10.4x

8.4x

23.8%

0.9x

APAC CUSTOMER SERVICES INC (Dec.)

2.12

(12.4%)

207.2%

105

116

35.3x

21.2x

0.5x

0.5x

6.2x

5.2x

15.0%

1.4x

Median

(2.0%)

73.0%

24.3x

19.3x

1.1x

1.0x

8.4x

7.7x

16.0%

1.2x

Mean

(3.1%)

104.7%

23.1x

19.1x

1.3x

1.2x

8.3x

7.7x

17.0%

1.2x

Portfolio Purchasers

PORTFOLIO RECOVRY ASSOC INC (Dec.)

$48.33

(6.4%)

39.7%

$784

$784

18.2x

14.9x

4.2x

3.5x

9.3x

7.7x

18.4%

0.8x

ASSET ACCEPTANCE CAPITL CP (Dec.)

20.41

(35.1%)

17.7%

760

710

14.1x

12.4x

2.6x

2.3x

8.1x

7.1x

14.6%

0.8x

ASTA FUNDING INC (Sep.)

34.17

(2.9%)

67.5%

504

593

12.1x

NA

6.6x

NA

NA

NA

20.0%

NM

ENCORE CAPITAL GROUP INC (Dec.)

14.43

(26.2%)

11.0%

344

526

9.2x

NA

2.4x

NA

6.4x

NA

15.1%

NM

Median

(16.3%)

28.7%

13.1x

13.6x

3.4x

2.9x

8.1x

7.4x

16.8%

0.8x

Mean

(17.7%)

34.0%

13.4x

13.6x

3.9x

2.9x

7.9x

7.4x

17.0%

0.8x

Overall Median

(2.9%)

57.1%

19.3x

19.0x

1.6x

1.1x

8.2x

7.5x

16.0%

1.0x

Overall Mean

(7.0%)

85.8%

20.5x

18.2x

2.1x

1.5x

8.2x

7.6x

17.0%

1.1x

Source: IBES consensus estimates and Wall Street Research

30

CONFIDENTIAL

Management vs. Street Projections

($ in millions, except per share amounts)

Management Forecast

Wall Street Estimates

(1)

Q1:06

Q2:06

Q3:06

Q4:06

CY2006

CY2007

Q1:06

Q2:06

Q3:06

Q4:06

CY2006

CY2007

Revenue

$312

$311

$321

$330

$1,275

$1,374

$311

$311

$308

$307

$1,237

$1,279

vs. Street

1.2

0.2

13.5

23.2

38.2

95.6

0.4%

0.1%

4.4%

7.6%

3.1%

7.5%

EBITDA

43.0

38.0

47.5

51.0

179.5

213.3

38.3

45.2

45.0

44.1

175.1

191.6

vs. Street

4.6

-7.2

2.5

6.9

4.4

21.7

12.1%

(15.9%)

5.6%

15.7%

2.5%

11.3%

EPS

$0.41

$0.33

$0.50

$0.56

$1.80

$2.44

$0.29

$0.45

$0.45

$0.46

$1.65

$1.96

vs. Street

0.12

(0.12)

0.05

0.11

0.15

0.48

42.6%

(26.2%)

10.3%

23.6%

9.4%

24.3%

(1) Based on an average of Boenning & Scattergood, CIBC, First Analysis, JMP Securities, Suntrust Robinson Humphrey and William Blair reports.

31

CONFIDENTIAL

C. Industry Perspectives

32

CONFIDENTIAL

CRM Companies Have Experienced Volatile

Earnings Results

0

100

200

300

400

500

600

700

800

900

4/23/93

7/23/96

10/24/99

1/23/03

4/25/06

S&P 500

Outsourced CRM

Outsourced CRM Services v. S&P 1993 - Current

Source: FactSet.

Note: Outsourced CRM composite includes APAC, Convergys, ICT Group, Intrum Justitia, PeopleSupport, Sitel, SR Teleperformance, Startek, Sykes Enterprises, Teletech and West.

CRM industry over-capacity

Internet bubble

Peak of

another cycle?

8.1%

7.7%

7.7%

9.5%

10.5%

12.4%

12.7%

13.5%

14.4%

1997

1998

1999

2000

2001

2002

2003

2004

2005

33

IPO market

focus

Source: Company filings. Not adjusted for acquisitions.

Note: Based on Teletech, Sykes and Sitel.

Source: Company filings. Not adjusted for acquisitions.

Note: Based on Teletech, Sykes and Sitel.

North ‘07 CRM EBITDA

Margin: 9.5%

North CRM ‘05-’11 Rev

CAGR: 16.5%

CRM Historical EBITDA Margin

CRM Historical Y / Y Revenue Growth

55.7%

5.9%

5.1%

4.8%

2.8%

(6.5%)

27.6%

28.6%

28.4%

1997

1998

1999

2000

2001

2002

2003

2004

2005

33

30.0%

63.0%

45.0%

49.0%

33.5%

41.7%

67.4%

76.9%

78.0%

61.0%

89.3%

11.0%

12.0%

15.1%

17.3%

18.9%

24.0%

28.5%

45.0%

47.0%

54.3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Top 5 Clients

Largest Client

Largest

Client

:

CONFIDENTIAL

Customer Concentration in CRM Is A Focus

for the Investment Community

“TeleTech’s five largest clients account for

about 50% of revenue. While we believe the

company's relationship with these customers is

good, the company is obviously exposed to

some risk given its revenue concentration with

these clients.”

David J. Koning,

Robert W. Baird (11/4/05)

“While the Sprint Nextel billing contract remains

a wildcard, we note that Convergys has more or

less quantified the expected impact of the

Cingular migration. The fact that the migration

could cost Convergys more than $30 million in

operating income next year is not happy news,

but putting a number on the damage is a

healthy first step towards getting beyond this

loss and starting to focus on new opportunities.”

Shaul Eyal

CIBC (11/18/05)

“Startek’s customer base is highly

concentrated. While this is a risk, it also

provides SRT the ability to concentrate on key

customers and deliver outstanding

service…However, we are optimistic the firm

can diversify its customer base in 2005 via new

business and/or expanding into other verticals,

which could ease revenue concentration.”

Tom Carpenter,

Hilliard Lyons (April 14, 2005)

Source: SEC Public filings and Credit Suisse Investment Banking estimates

(1) WSTC top 100 clients account for 63% of revenues.

(2) Accenture and Microsoft account for 7.8% and 7.3% of revenues and

top 10 clients account for 45% of revenues.

(3) Convergys top 3 clients account for 33.5% of revenues.

(4) GM and HP both account for 12% of revenues. Top 20 clients account for 67.4%.

(5) North represents 2006 estimates for CRM business.

(6) PeopleSupport top 2 clients account for 47% of revenues.

(7) Startek top 3 customers account for 89.3% of revenues.

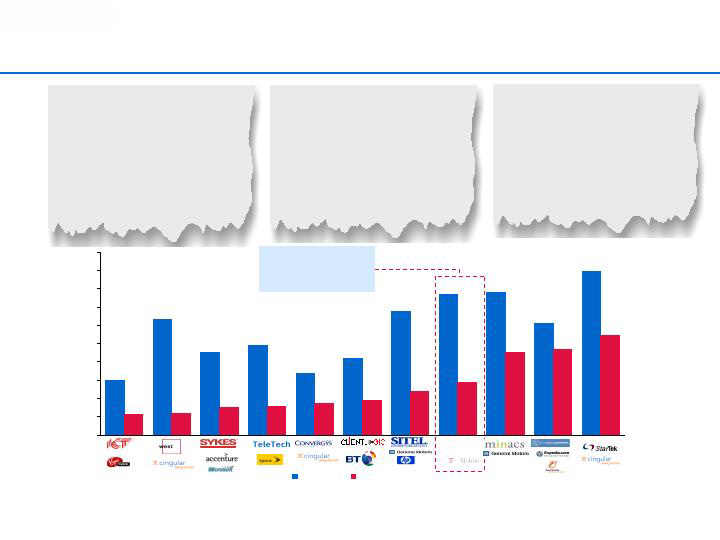

North total business:

Top 5 Clients: 37.0%

Largest Client: 10.7%

15.7%

West

Sykes

ClientLogic

Convergys

Convergys

Sitel

Minacs

Peoplsupport

(4)

(1)

(2)

(3)

(6)

(7)

North(5)

34

CONFIDENTIAL

Large Players Entering North’s Core ARM Market

In late 2004, acquired Arrow Financial Services, a purchaser of performing and non-

performing consumer debt and provider of contingency collection services, to gain

entrance to the debt recovery industry

In May 2004, acquired Encore Receivable Management for up to $68 million, to enter the

accounts receivable management business

In 2002, acquired Attention LLC for an initial payment of $35.7 million plus future

payments between $21.5 and $50 million, to capitalize on the opportunities in the

accounts receivable management arena

In late 2004, acquired Account Solutions Group, a credit card debt collection company, to

establish a footprint in the US accounts receivable industry

In March 2006, reached a five-year agreement to provide Microsoft with credit and

collection services in Europe, the Middle East and Africa

Equity Value

$3,458

CY06E Revenues

1,692.7

CY07E Revenues

1,781.6

Equity Value

$2,780

CY06E Revenues

2,701.7

CY07E Revenues

2,877.8

Equity Value

$26,076

CY06E Revenues

17,486.6

CY07E Revenues

18,906.4

Equity Value

$11,118

CY06E Revenues

2,024.4

CY07E Revenues

2,892.0

Equity Value

$22,583

CY06E Revenues

3,450.8

CY07E Revenues

4,033.8

35

CONFIDENTIAL

CS does not provide any tax advice. Any tax statement herein regarding any US federal tax is not intended or

written to be used, and cannot be used, by any taxpayer for the purpose of avoiding any penalties. Any such

statement herein was written to support the marketing or promotion of the transaction(s) or matter(s) to which the

statement relates. Each taxpayer should seek advice based on the taxpayer's particular circumstances from an

independent tax advisor.

These materials have been provided to you by Credit Suisse (“CS”) in connection with an actual or potential mandate or engagement and

may not be used or relied upon for any purpose other than as specifically contemplated by a written agreement with CS. In addition, these

materials may not be disclosed, in whole or in part, or summarized or otherwise referred to except as agreed in writing by CS. The

information used in preparing these materials was obtained from or through you or your representatives or from public sources. CS

assumes no responsibility for independent verification of such information and has relied on such information being complete and accurate

in all material respects. To the extent such information includes estimates and forecasts of future financial performance (including

estimates of potential cost savings and synergies) prepared by or reviewed or discussed with the managements of your company and/or

other potential transaction participants or obtained from public sources, we have assumed that such estimates and forecasts have been

reasonably prepared on bases reflecting the best currently available estimates and judgments of such managements (or, with respect to

estimates and forecasts obtained from public sources, represent reasonable estimates). These materials were designed for use by specific

persons familiar with the business and the affairs of your company and CS assumes no obligation to update or otherwise revise these

materials. Nothing contained herein should be construed as tax, accounting or legal advice. You (and each of your employees,

representatives or other agents) may disclose to any and all persons, without limitation of any kind, the tax treatment and tax structure of

the transactions contemplated by these materials and all materials of any kind (including opinions or other tax analyses) that are provided

to you relating to such tax treatment and structure. For this purpose, the tax treatment of a transaction is the purported or claimed U.S.

federal income tax treatment of the transaction and the tax structure of a transaction is any fact that may be relevant to understanding the

purported or claimed U.S. federal income tax treatment of the transaction.

CS has adopted policies and guidelines designed to preserve the independence of its research analysts. CS’s policies prohibit employees

from directly or indirectly offering a favorable research rating or specific price target, or offering to change a research rating or price target,

as consideration for or an inducement to obtain business or other compensation. CS’s policies prohibit research analysts from being

compensated for their involvement in investment banking transactions.

36