Exhibit (c)(5)

Project North

CONFIDENTIAL

Materials for Discussion

March 22, 2006

PRELIMINARY | SUBJECT TO FURTHER REVIEW AND EVALUATION

THESE MATERIALS MAY NOT BE USED OR RELIED UPON FOR ANY PURPOSE OTHER THAN AS SPECIFICALLY CONTEMPLATED BY A

WRITTEN AGREEMENT WITH CREDIT SUISSE.

Table of Contents

1. Overview

2. Stand-Alone Assessment

3. Acquisition Alternatives

A. Consolidate in ARM

B. Consolidate in CRM

C. Enter BPO

4. Sale Alternative

Appendix

A. North Situation Overview

B. Comparable Company Analysis

C. Additional Materials

CONFIDENTIAL

1

1. Overview

CONFIDENTIAL

2

Executive Summary

CS appreciates the opportunity to review with North’s Board of Directors its various

strategic alternatives. The purpose of today’s meeting is to discuss the following topics:

Assess North’s stand-alone plan

Industry trends and drivers impacting North

The Street’s view of the Company and recent trading performance

Opportunities and issues surrounding North’s business segments

Assess consolidation alternatives in ARM / CRM / Portfolio Management and explore BPO

acquisitions

As a part of the review conducted, CS has:

Met with Management on multiple occasions to discuss the business and possible strategic

options

Undertaken a review of the 2006-2011 financial plan of the Company

Benchmarked North against its industry peers

Obtained perspectives on the industry and company from CS Debt and Equity Capital Markets

teams

Performed a range of financial analysis including discounted cash flow, business segment

acquisition analysis and an LBO analysis

CONFIDENTIAL

3

Overview of Strategic Alternatives

Sell the Company

CS Assessment

Stand-alone plan shows significant growth and margin expansion

Growth enhanced by additional portfolio acquisitions and CRM

Market has penalized Company for prior earnings misses

Execution risk remains a concern

Stand-Alone

Potential to provide shareholders a premium today

Strong rationale exists for both sponsors and strategic buyers to pay premium to

current market

Delivers value without execution risk

May preclude ability to fully capture upside potential of business plan

Consolidate

in ARM

Fully leverages Management expertise

Few attractive targets of size (all have operational issues)

Requires significant restructuring

Consolidation unlikely to improve pricing / margins

Consolidate

in CRM

CRM market exhibiting strong growth

Multiple acquisitions / transformational deal required to have meaningful impact on North

Higher valuations make deals less accretive

Acquisition strategy risky if market continues to value North with ARM/PM peers

Historically volatile supply and demand market

Consolidate

in Portfolio

Management

Potential for attractive returns from purchasing A/R portfolios

Complimentary service line to ARM

Competition remains high for attractive assets

Enter into

BPO

Large market opportunity

Fiercely competitive - focus of many IT companies

Lack of experience / expertise

Likely to have high value expectations

CONFIDENTIAL

4

2. Stand-Alone Assessment

CONFIDENTIAL

5

Industry Trends and Drivers Affecting North

Clients Driving Cost Savings

Nature of transaction management has

led to cost being the primary reason for

outsourcing

First party collection work has

commoditized

Trends

Observation / Expectation

Impact on North

North has faced downward pricing

pressure, but may be stabilizing

Focused on using less labor and

improving collection rates

Increasing M&A Activity,

Though Still Highly

Fragmented

~95% of market participants generate

less than $8MM annual revenue

(1)

Industry expertise, scale, opportunity to

cross-sell are competitive advantages

North is industry leader; however, few

attractive opportunities

Acquisitions unlikely to “move the

needle”

Growth in Credit Economy

Revolving consumer debt outstanding

~$800 billion as of December 2005;

growth of ~7% per year since 1994

(2)

Growth in consumer debt increases

available A/R portfolios

Increasing Competition for

Portfolios

Experience in purchasing at right price,

collecting efficiently and network to

source purchase opportunities is critical

Only handful of companies achieve

highest levels of returns and are highly

profitable

Financial services pricing becoming ultra

competitive

Disciplined bidding critical; experience

from ARM business provides

competitive advantage

Having scale permits North to bid on

larger assets where there is less

competition

Unpredictability leads to volatility in

earnings

(1) Source: Kaulkin Ginsberg, 2005.

(2) Source: Federal Reserve, 2006.

Strong Momentum in

Outsourcing

Increasing consumer, business and

government debt being outsourced to

ARM providers

Strong long-term growth expectations

CONFIDENTIAL

6

Industry Trends and Drivers Affecting North (cont’d)

Trends

Observation / Expectation

Impact on North

CRM Market is Experiencing

a Rebirth

Sykes and ICT experiencing double-digit

revenue growth

Multiples have expanded ~20% since

October

Unclear if market rewards North for

CRM potential

Two biggest peers are buying into BPO

Increasing Near-shore /

Offshore / At-home Delivery

First rush of offshore demand has been

met

Continued surge in demand being

experienced

Need significant presence offshore to

compete in long-run

Potential targets for North should

include offshore players

Domestic Outbound Capacity

Has Been Rationalized

Existing CRM vendors have added

collections or switched to inbound

capabilities

Offshore players profile increasing

Substantial rationalization already

undertaken

Domestic capacity near equilibrium

Buyers Looking for Fewer

Outsource Providers

Increasingly, service providers need to

offer a broader suite of BPO services

North’s ability to offer “bundle” of

collections and help desk services

should reduce sales cycles

Likely to require North to “acquire”

additional offerings

CONFIDENTIAL

7

8.1%

7.7%

7.7%

9.5%

10.5%

12.4%

12.7%

13.5%

14.4%

1997

1998

1999

2000

2001

2002

2003

2004

2005

55.7%

5.9%

5.1%

4.8%

2.8%

(6.5%)

27.6%

28.6%

28.4%

1997

1998

1999

2000

2001

2002

2003

2004

2005

0

100

200

300

400

500

600

700

800

900

3/18/93

6/16/96

9/16/99

12/16/02

3/17/06

S&P 500

Outsourced CRM

CONFIDENTIAL

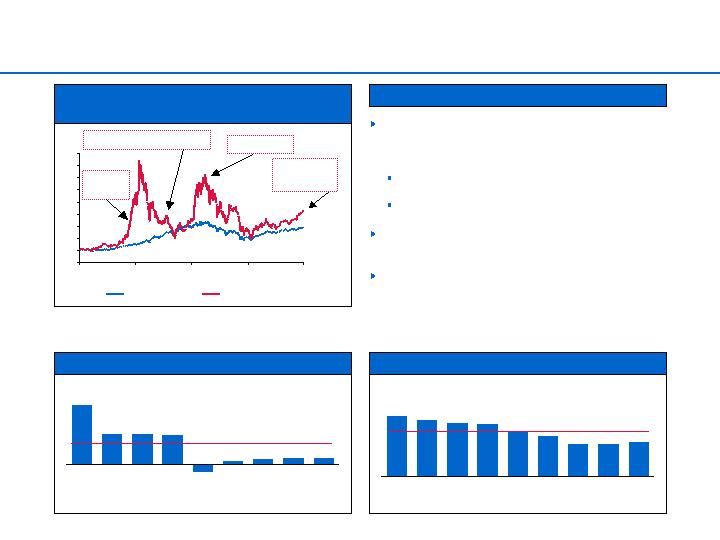

CRM Has Historically Been Very Volatile

Outsourced CRM Services v.

S&P 1993 - Current

Observations

Source: FactSet.

Note: Outsourced CRM composite includes APAC, Convergys, ICT Group, Intrum Justitia,

PeopleSupport, Sitel, SR Teleperformance, Startek, Sykes Enterprises, Teletech and

West.

CRM industry participants have learned from past

mistakes, which should partially mitigate historical

sector volatility going forward

Decreased customer / end-market concentration

Broader service offering

However, CRM growth cycles are short-lived;

momentum not sustainable over the long-term

CRM revenue growth has moderated and margins

have compressed over the last several years, but

have begun to rebound

CRM industry over-capacity

Internet bubble

Peak of

another cycle?

CRM Historical Y / Y Revenue Growth

CRM Historical EBITDA Margin

North CRM ‘05-’11 Rev

CAGR: 17.9%

North ‘07 CRM EBITDA

Margin: 10.6%

IPO market

focus

Source: Company filings. Not adjusted for acquisitions.

Note: Based on Teletech, Sykes and Sitel.

Source: Company filings. Not adjusted for acquisitions.

Note: Based on Teletech, Sykes and Sitel.

8

Review of North’s ARM Business

Street Commentary on ARM

“We think the benefits of the RMA

restructuring/integration, combined with some

return from the Department of Ed investment in

2005, and the additional emphasis on off-shore

support and technology...will probably more than

offset continued pricing pressures and increased

service demands such as security.”

“We have estimated North's sustainable organic

growth profile [with] ARM at approximately 5%"

Summary Financials of ARM Business

Wall Street Estimate:

Revenue: $818.9MM

EBITDA: $107.7MM

% margin: 13.1%

North has leading market position and is

diversified across many verticals

Scale provides a competitive advantage

Opportunity to stabilize margins as discounting

appears to have reached bottom

Top five in UK, Europe is a growth opportunity

Key Attributes

Customers use multiple vendors

Significant price competition

Investors have penalized North in the past for

disappointments in core ARM business

North strategy focused on using less labor,

price stabilization and improving collection rates

Not selected for IRS trial, but should still benefit

Considerations

($ in millions)

ARM Financial Performance

2005A

2006E

2007E

Revenue

$804.5

$936.4

$987.3

% growth

7.8%

16.4%

5.4%

Gross Profit

427.2

488.5

514.8

% margin

53.1%

52.2%

52.1%

EBITDA

90.2

114.2

135.9

% margin

11.2%

12.2%

13.8%

Note: Based on Management projections. Includes ARM international

CONFIDENTIAL

9

($ in millions)

PM Financial Performance

2005A

2006E

2007E

Revenue

$144.7

$185.3

$189.2

% growth

47.6%

28.0%

2.1%

PM Comparables

12.9%

14.6%

Gross Profit

130.9

176.1

179.5

% margin

90.5%

95.0%

94.8%

EBITDA

47.5

44.7

46.8

% margin

32.8%

24.1%

24.8%

PM Comparables

38.0%

39.3%

Note: Based on Management projections.

Review of North’s Portfolio Management Business

Street Commentary on Portfolio Management

“Q4 EBITDA was $16.5 MM, or 33.8% of revenue, due to strong

collections, lower impairment allowances and the portfolio sale

of older, nearly zero-basis accounts.”

“We have estimated North's sustainable organic growth profile

[with] Portfolio Management at low double-digit”

Summary Financials of Portfolio Management

Business

Wall Street Estimate:

Revenue: $190.7MM

EBITDA: $62.0MM

% margin: 32.5%

North is a leading portfolio purchaser -

partnership with Cargill provides significant

opportunity to grow

Ability to leverage experience and expertise

from ARM business

Growth driven by higher collection rates and

ability to rapidly re-sell difficult portfolios

Key Attributes

Wall Street applies lower multiple to portfolio

purchasers

Earnings more volatile under new accounting

methods as a result of treatment of impairments

Returns on new acquisitions lower due to highly

competitive market

Need to continually reinvest capital in new

portfolios

Considerations

Should North Divest Portfolio Management?

Unpredictable business, dependent on portfolio buys

Value investors do not like volatility

Complimentary business to ARM as identified by other

players (e.g. West)

Highest margin segment contributing ~25% of total

EBITDA in 2006

Helps North cross-sell ARM services

CONFIDENTIAL

10

($ in millions)

CRM Financial Performance

2005A

2006E

2007E

Revenue

$190.4

$289.1

$348.9

% growth

19.7%

51.8%

20.7%

CRM Comparables

9.9%

7.8%

Gross Profit

44.5

63.4

92.6

% margin

23.4%

21.9%

26.5%

EBITDA

9.1

21.2

37.0

% margin

4.8%

7.3%

10.6%

CRM Comparables

14.7%

15.2%

Note: Based on Management projections.

Review of North’s CRM Business

Street Commentary on CRM

“We have estimated North's sustainable organic growth profile

[with] CRM of 10% to 15%"

“The company is ramping up operations with a number of new

customers and should show improving revenue through 2006”

“The largest customer is now approaching annualized revenue

of $60MM and could reach $100MM.”

“Q4 EBITDA was break-even mainly due to the cost pressures

of ramping new business on an expedited schedule.”

Summary Financials of CRM Business

Wall Street Estimate:

Revenue: $242.9MM

EBITDA: $6.6MM

% margin: 2.7%

Relatively new business

Significant momentum in Q4:2005 driven by

new client wins

Long-term contracts provide revenue visibility

Opportunity to significantly grow business in

2006 and capitalize on seat deployment

Offshore facilities in Philippines, Caribbean and

Panama; near-shore in Canada

Key Attributes

Current CRM offering lacks stickiness in

economic downturn

Substantial revenue from few key clients makes

vulnerable to customer losses

Margin pressure while new customers ramp-up

Focus on near-shore labor in Canada

negatively impacted by currency movements

CRM segment still lacks scale to "move the

needle" for overall business

Considerations

CONFIDENTIAL

11

gement

Key Take Aways

Market leader

Historical pricing pressure has stabilized

Highly complementary to ARM

Attractive margins

Volatile earnings profile

New customer wins

Driving growth

Creating upside potential

North’s Business is well positioned

…However, North’s business potential has not been reflected in its past

historical financial performance

CONFIDENTIAL

ARM

Portfolio

Management

CRM

12

Overview of North Financial Plan

Growth of core ARM business in line

with overall growth in consumer debt

CRM is a key driver of growth

Ramping with key customer wins

but least profitable business

Customer concentration remains

significant risk

Projected growth faster than

peers, with higher margins than

peers

Margin expansion driven by (i)

stabilization of pricing in ARM and (ii)

scaling of CRM business following

prior investment in seat deployments

Portfolio Management remains key

contributor to EBITDA margin

However, business is very volatile

– sustainability depends on future

portfolio buys

Observations

2005 PF for acquisitions:

Rev: $1,198

NI: $ 35

Implies 06 organic revenue

growth of 7.4%

($ in millions)

Fiscal Year Ended December 31,

'05E - '11E

2005A

2006E

2007E

2008E

2009E

2010E

2011E

CAGR

Revenue:

ARM

$804.5

$936.4

$987.3

$1,039.7

$1,101.4

$1,173.6

$1,250.8

7.6%

% growth

7.8%

16.4%

5.4%

5.3%

5.9%

6.6%

6.6%

CRM

190.4

289.1

348.9

383.7

422.1

464.3

510.8

17.9%

% growth

19.7%

51.8%

20.7%

10.0%

10.0%

10.0%

10.0%

Portfolio Management

144.7

185.3

189.2

193.2

205.6

224.5

244.9

9.2%

% growth

47.6%

28.0%

2.1%

2.1%

6.4%

9.2%

9.1%

Eliminations

(87.3)

(124.6)

(125.9)

(125.5)

(131.3)

(144.1)

(158.2)

Total Revenue

$1,052.3

$1,286.2

$1,399.5

$1,491.0

$1,597.8

$1,718.4

$1,848.4

9.8%

% growth

12.0%

22.2%

8.8%

6.5%

7.2%

7.5%

7.6%

EBITDA

ARM

90.2

114.2

135.9

149.4

164.7

180.1

191.9

13.4%

% margin

11.2%

12.2%

13.8%

14.4%

15.0%

15.3%

15.3%

CRM

9.1

21.2

37.0

42.2

48.5

55.7

63.8

38.5%

% margin

4.8%

7.3%

10.6%

11.0%

11.5%

12.0%

12.5%

Portfolio Management

47.5

44.7

46.8

50.6

56.5

62.1

67.8

6.1%

% margin

32.8%

24.1%

24.8%

26.2%

27.5%

27.7%

27.7%

Total EBITDA

146.7

180.1

219.8

242.2

269.8

297.9

323.6

14.1%

% margin

13.9%

14.0%

15.7%

16.2%

16.9%

17.3%

17.5%

Net Income

44.5

60.7

86.7

102.1

118.2

135.6

149.5

22.4%

EPS

$1.33

$1.82

$2.52

$2.94

$3.36

$3.81

$4.16

20.9%

Note: ARM includes ARM International. Q2 and Q4 FY2005 reflect reclassification of gains on sales of aged portfolios into Portfolio Management revenue.

CONFIDENTIAL

13

Overview of North Financial Plan (cont’d)

($ in millions)

Quarterly FY2005A

Quarterly FY2006E

(1)

FYE December 31,

Q1:05A

Q2:05A

Q3:05A

Q4:05A

Q1:06E

Q2:06E

Q3:06E

Q4:06E

2005A

2006E

Revenue:

ARM

$201.5

$195.8

$190.3

$216.8

$236.6

$234.0

$233.3

$232.5

$804.5

$936.4

% growth

3.5%

3.9%

4.0%

20.5%

17.4%

19.5%

22.6%

7.2%

7.8%

16.4%

CRM

47.6

43.8

44.9

54.1

59.3

67.9

77.6

84.3

190.4

289.1

% growth

NM

(26.3%)

(14.9%)

15.6%

24.5%

55.1%

72.7%

55.9%

19.7%

51.8%

Portfolio Management

27.8

33.0

35.1

48.8

48.1

47.0

45.9

44.3

144.7

185.3

% growth

28.7%

36.8%

33.4%

87.9%

73.0%

42.3%

30.6%

(9.1%)

47.6%

28.0%

Eliminations

(16.6)

(20.2)

(21.2)

(29.3)

(32.6)

(33.0)

(30.1)

(28.9)

(87.3)

(124.6)

Total Revenue

$260.3

$252.4

$249.2

$290.3

$311.4

$315.9

$326.6

$332.3

$1,052.3

$1,286.2

% Y-o-Y growth

29.4%

(1.1%)

1.3%

22.4%

19.6%

25.1%

31.1%

14.4%

12.0%

22.2%

% Q-o-Q growth

9.7%

(3.0%)

(1.3%)

16.5%

7.2%

1.5%

3.4%

1.7%

EBITDA

ARM

25.1

24.8

18.1

22.2

28.5

26.7

30.2

28.9

90.2

114.2

% margin

12.5%

12.7%

9.5%

10.2%

12.0%

11.4%

12.9%

12.4%

11.2%

12.2%

CRM

5.4

3.0

0.6

(0.0)

1.4

4.8

6.2

8.7

9.1

21.2

% margin

11.4%

6.9%

1.3%

(0.0%)

2.4%

7.0%

8.0%

10.3%

4.8%

7.3%

Portfolio Management

9.0

10.8

11.2

16.5

11.7

9.6

11.8

11.5

47.5

44.7

% margin

32.5%

32.6%

31.9%

33.8%

24.4%

20.5%

25.8%

25.9%

32.8%

24.1%

Total EBITDA

39.6

38.6

29.8

38.7

41.6

41.1

48.2

49.1

146.7

180.1

% margin

15.2%

15.3%

12.0%

13.3%

13.4%

13.0%

14.8%

14.8%

13.9%

14.0%

Net Income

15.3

14.1

7.6

7.5

13.4

13.0

16.9

17.5

44.5

60.7

EPS

$0.45

$0.42

$0.24

$0.23

$0.40

$0.39

$0.51

$0.52

$1.33

$1.82

Note: ARM includes ARM International. Q2 and Q4 FY2005 reflect reclassification of gains on sales of aged portfolios into Portfolio Management revenue.

(1) Quarterly EPS estimated based on 33.4M average shares outstanding.

Significant EBITDA growth

in CRM as new customers

ramp during 2006

Portfolio Management

EBITDA boosted from sales

of near zero-cost portfolios

ARM negatively impacted

from impact of hurricanes

Katrina and Rita as well as

lower collection rates due to

high gas costs

CONFIDENTIAL

14

North Expects to Exceed Current Street Expectations

Management revenue estimates

exceed Street by 6% in 2006

2006 EBITDA margin in line with

Street

Management EPS estimates

exceed Street by 6% in 2006

Street does not have clear picture

of 2007 performance

EPS estimates vary

considerably (high of $2.12 v.

low of $1.70)

Analysts remain cautious about the prospect of North executing its plan in the current

market

Observations

($ in millions, except per share amounts)

Internal Mgmt.

Avg. Street

Projections

Estimates

Diff. ($)

Diff. (%)

CY2006E

Revenue

$1,286.2

$1,211.8

$74.4

6.1%

% growth

22.2%

15.2%

EBITDA

180.1

175.9

4.2

2.4%

% margin

14.0%

14.5%

Net Income

60.7

57.8

2.9

5.0%

% margin

4.7%

4.8%

EPS

$1.82

$1.71

$0.11

6.3%

Note: Average Street Estimates include Boenning & Scattergood, CIBC, First Analysis and JMP.

Street estimates are pro forma for Q1:06 expected restructuring charge.

CONFIDENTIAL

15

$0.41

$0.39

$0.47

$0.41

$0.42

$0.11

$0.45

$0.36

$0.39

$0.45

$0.24

$0.23

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

Sep-04A

Dec-04A

Mar-05A

Jun-05A

Sep-05A

Dec-05A

Estimate

Actual

$12.00

$14.00

$16.00

$18.00

$20.00

$22.00

$24.00

$26.00

$28.00

$30.00

$32.00

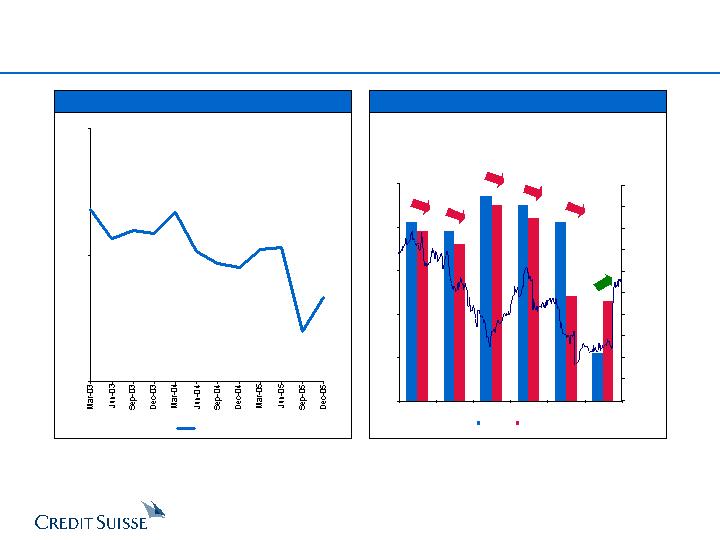

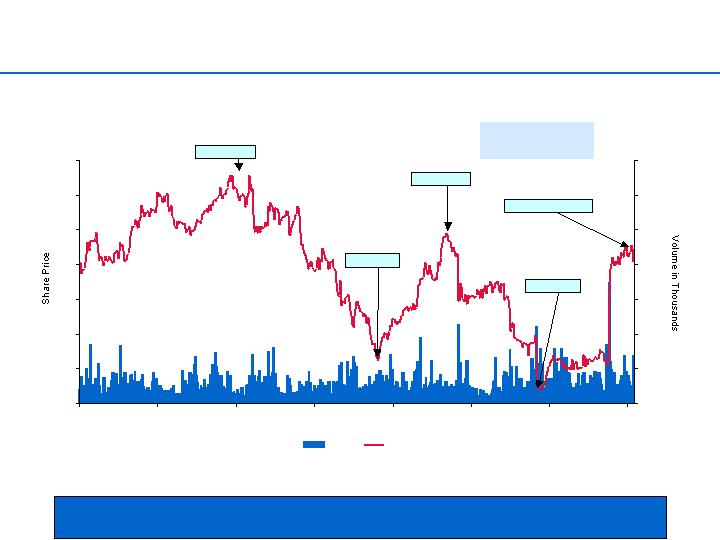

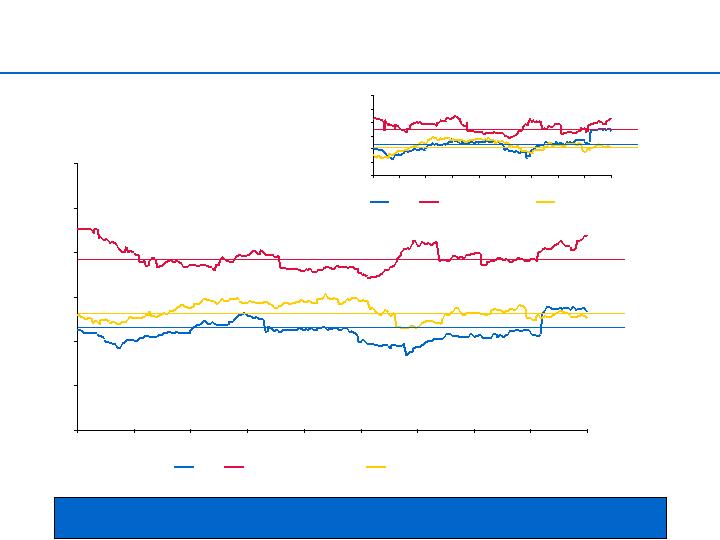

North Has Faced Challenges. . .

EBITDA Margins Have Compressed . . .

. . . With Volatile Earnings Results

10.0%

15.0%

20.0%

North

North Estimates vs. Actual Results

EPS

Stock Price

$0.02

$0.12

$0.03

$0.03

$0.17

Source: Company filings.

Source: Company filings and IBES consensus estimates.

$0.02

CONFIDENTIAL

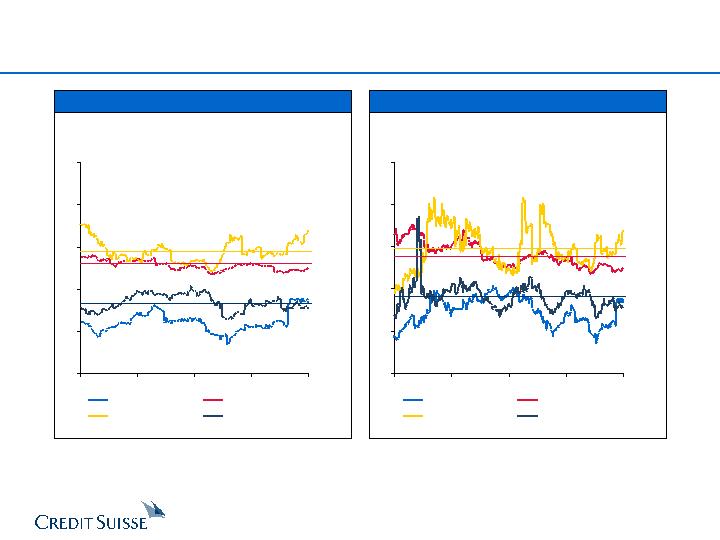

16

5x

10x

15x

20x

25x

30x

3/17/03

12/16/03

9/15/04

6/16/05

3/17/06

North

S&P 500

Outsourced CRM

Portfolio Purchasers

5x

10x

15x

20x

25x

30x

3/17/05

6/16/05

9/15/05

12/15/05

3/16/06

North

S&P 500

Outsourced CRM

Portfolio Purchasers

CRM

Average

19.4x

. . . Resulting in Lower Valuations From Investors

NTM P/E Multiple - Last Twelve Months

NTM P/E Multiple - Last 3 Years

Portfolio

Purchasers

Average

13.4x

Source: FactSet.

Note: Outsourced CRM Services composite includes APAC, Convergys, ICT Group, Intrum

Justitia, PeopleSupport, Sitel, SR Teleperformance, Startek, Sykes Enterprises,

Teletech and West.

Portfolio Purchasers composite includes Asset Acceptance, Asta Funding, Encore

Capital and Portfolio Recovery.

Source: FactSet.

Note: Outsourced CRM Services composite includes APAC, Convergys, ICT Group, Intrum

Justitia, PeopleSupport, Sitel, SR Teleperformance, Startek, Sykes Enterprises,

Teletech and West.

Portfolio Purchasers composite includes Asset Acceptance, Asta Funding, Encore

Capital and Portfolio Recovery.

S&P 500

Average

17.8x

CRM

Average

19.8x

Portfolio

Purchasers

Average

14.1x

S&P 500

Average

19.0x

North

Average

11.1x

North

Average

12.3x

CONFIDENTIAL

17

10x

15x

20x

25x

5.0%

10.0%

15.0%

20.0%

25.0%

West

Convergys

SR Tele.

Teletech

PSPT

ICT

Portfolio Recovery

Startek

North

Asset Acceptance

ASTA

Encore Capital

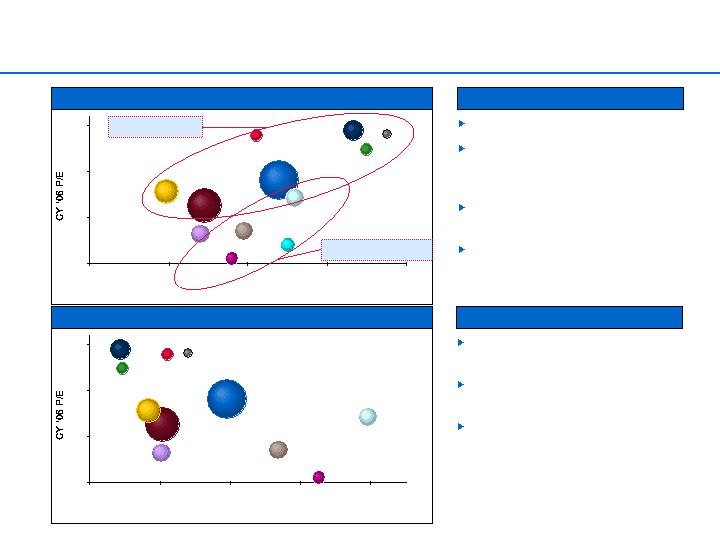

Comparable Company Benchmarking

Source: IBES consensus estimates, Wall Street research.

Note: Bubble size represents relative market capitalization. APAC excluded assumed not meaningful.

CY06 P/E and LTGR

I/B/E/S LT Growth Rate

Market rewards higher growth

North trades below its CRM

peers and closer to Portfolio

Purchasers

Significant work and execution

risk to move up the P/E curve

North’s shareholder base is

primarily value-focused investors

Observations

10x

15x

20x

25x

5.0%

15.0%

25.0%

35.0%

45.0%

West

Convergys

SR Tele.

Teletech

PSPT

ICT

Portfolio Recovery

Startek

North

Asset Acceptance

Encore Capital

CY06 P/E and CY06 EBITDA Margin

CY06 EBITDA Margin

Portfolio Purchasers

CRM Comparables

Market penalizes volatility of PM

business, despite higher margins

Market rewards improved

prospects of CRM

To achieve P/E expansion, North

will need to: 1) deliver results that

consistently meet or exceed

expectations; 2) deliver

consistent growth, and; 3) drive

revenue growth and meaningful

diversification into CRM

Observations

CONFIDENTIAL

18

North’s Stock Price Has Recently Rebounded

North’s stock price has recently rebounded as a result of exceeding analysts

expectations in Q4 and providing strong guidance for 2006

March 19, 2004 to March 17, 2006

Source: FactSet.

Note: Outsourced CRM Services composite includes APAC, Convergys, ICT Group, Intrum Justitia, PeopleSupport, Sitel, SR Teleperformance, Startek, Sykes Enterprises, Teletech

and West.

Portfolio Purchasers composite includes Asset Acceptance, Asta Funding, Encore Capital and Portfolio Recovery.

$15

$17

$19

$21

$23

$25

$27

$29

3/19/04

7/1/04

10/12/04

1/24/05

5/5/05

8/16/05

11/25/05

3/10/06

0

300

600

900

1,200

1,500

1,800

2,100

Volume

North

NTM P/E: 9.2x

NTM P/E: 13.1x

NTM P/E: 8.4x

Current NTM P/E: 13.3x

NTM P/E: 15.1x

Current NTM P/E Multiples

Outsourced CRM: 21.8x

Portfolio Purchasers: 12.6x

CONFIDENTIAL

19

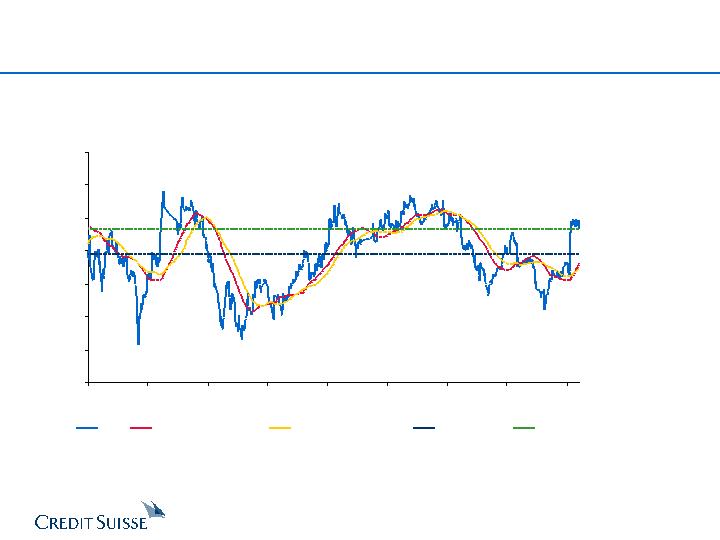

5-Year Historical NTM PE Performance

NTM Price / Earnings Multiple - March 16, 2001 to March 17, 2006

North

Current NTM P/E

13.3x

North Average

NTM P/E 11.8x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

18.0x

3/16/01

10/29/01

6/10/02

1/16/03

8/26/03

4/5/04

11/11/04

6/22/05

1/31/06

North

90-Day Rolling Average

120-Day Rolling Average

Period Average

Current

CONFIDENTIAL

20

Stand-Alone Plan:

Driving Shareholder Value Through Improved Growth

Share Price Sensitivity

Management Case

Future Stock Price - 2009EPS

Implied Stock Price -

2006EPS

Given current street outlook, North’s stock price may not reflect Management’s plan for a

number of quarters

Public market

unable to

identify

performance

improvements

from new

contract wins

($ in millions, except per share amounts)

FY05-10E Revenue CAGR

6.3%

8.3%

10.3%

12.0x

P/E

Implied FY09E Share Price

38.05

$

41.76

$ ��

45.76

$

Implied Current Share Price

(1)

21.10

23.16

25.38

Implied FY06E PEG

0.8x

0.7x

0.6x

13.0x

P/E

Implied FY09E Share Price

41.22

$

45.24

$

49.58

$

Implied Current Share Price

(1)

22.85

25.09

27.49

Implied FY06E PEG

0.9x

0.7x

0.6x

14.0x

P/E

Implied FY09E Share Price

44.39

$

48.72

$

53.39

$

Implied Current Share Price

(1)

24.61

27.02

29.60

Implied FY06E PEG

0.9x

0.8x

0.7x

Note: Assumes Net Income margin of 7.9% in 2010E based on Management projections

(1) Discounted from December 31, 2009 to March 31, 2006 assuming cost of equity of 17.0%.

Stock Price

Street

Mgmt.

FY 2006 EPS

1.71

$

1.82

$

20.55

21.84

22.26

23.66

23.98

25.48

21

Assumes $100MM buyback (4MM shares) at

10% premium to current

Buyback could be accomplished through open

market repurchase program or tender

Return Cash to Shareholders:

Preliminary Leveraged Recap Analysis

Illustrative Leveraged Recap Analysis

Observations

Strong signal to market that Company believes that shares

are undervalued

However, preliminary analysis suggests that shares may

be reasonably valued

Company should undertake buyback only when holding

excess capital vs. redeploying capital to grow existing

business

Fails to achieve a significant premium for exiting

shareholders

Repurchase program limited by liquidity issues

$100 million repurchase would represent 14% of float

($ in millions, except per share amounts)

Current Share Price

$22.64

Share Repurchase Premium

10.0%

Implied Repurchase Price

$24.90

Purchase of Shares

(1)

$100.0

Shares Repurchased

4.0

% of float

(2)

13.6%

New Debt Issued

$102.6

Pro Forma

Debt / LTM EBITDA

3.2x

PF 06E EPS

(3)

$1.88

% acr./(dil.)

3.3%

(1) Assumes fees and expense of 2.5% on new debt

(2) Based on 32.3MM shares outstanding (2.8MM held

by insiders).

(3) Assumes 7% interest on new debt.

CONFIDENTIAL

22

3. Acquisition Alternatives

A. Consolidate in ARM

CONFIDENTIAL

23

Should North Consolidate the ARM Market?

Consolidate in ARM:

Rationale / Considerations

Growth outlook for Transaction Management

continues to exceed other Finance &

Accounting BPO functions

Increased adoption rates in key verticals

Potential for significant cost and revenue

synergies

Ability to improve collection rates

May help stabilize prices

Creates opportunity to cross sell services

Continue to expand distance between next-

closest competitor

What makes it difficult

Most potential targets have inefficient operating

models

Many VC-backed with unrealistically high value

expectations

Potential strain on internal resources and

initiatives

Moves North farther away from “BPO

perception” objective

Minimal improvement to revenue visibility

Expect to continue to experience pricing

pressure

Selected Acquisition Opportunities:

CONFIDENTIAL

24

Financial Analysis of All Cash Illustrative Acquisition

Assumes an acquisition for $450MM (1.0x 06 Rev of $450MM / 12.5x 06 EBITDA of $36MM)

Incremental revenue of $450MM (2006); revenue loss of 15% in 2007 and 10% in 2008 as a result of

cannibalization

Incremental EBITDA margin of 8%, increasing to 12.5% by 2008

No synergies associated with the acquisition

Stand-Alone

Consolidate in ARM:

With Acquisition

(1) PV of Future Share price based on cost of equity of 17.0%.

An ARM acquisition at 1x revenue does not materially impact share price

10% Discount to

FY10 EPS implies:

Stand-Alone $24.74

With Acquisition $25.06

($ in millions, except per share data)

'06-'10

PF2006

PF2010

CAGR

Incremental Revenue

$450.0

$361.5

(5.3%)

Pro Forma Revenue

$1,736.2

$2,079.8

4.6%

% Growth

NM

7.1%

Incremental EBITDA

$36.0

$45.2

5.8%

% Margin

8.0%

12.5%

Synergies

$0.0

$0.0

Pro Forma EBITDA

$216.1

$343.1

12.3%

% Margin

12.4%

16.5%

Incremental A/T Int.

19.6

19.4

Pro Forma Net Income

$55.1

$137.4

25.6%

% Margin

3.2%

6.6%

Stand-Alone EPS

$1.82

$3.81

20.3%

PF EPS

(1)

$1.66

$3.86

23.6%

Accretion / (Dilution)

(9.0%)

1.4%

(1) Assumes acquisition financed through debt at a rate of 7.0%.

2010 EPS

$3.81

12.0x P/E

Implied FY09E Share Price

$45.76

Implied Current Share Price

(1)

$25.38

Implied FY06E PEG

0.6x

13.0x P/E

Implied FY09E Share Price

$49.58

Implied Current Share Price

(1)

$27.49

Implied FY06E PEG

0.6x

14.0x P/E

Implied FY09E Share Price

$53.39

Implied Current Share Price

(1)

$29.60

Implied FY06E PEG

0.7x

$3.86

$46.36

$25.70

0.5x

$50.22

$27.84

0.6x

$54.08

$29.99

0.6x

CONFIDENTIAL

25

EBITDA Margin in 2008-10

$27.84

9.5%

11.0%

12.5%

14.0%

15.5%

12.0x

$24.45

$25.08

$25.70

$26.33

$26.95

13.0x

26.49

27.17

27.84

28.52

29.20

14.0x

28.53

29.26

29.99

30.72

31.45

Implied Share Price Sensitivity Analysis

Consolidate in ARM:

2010 P/E / EBITDA Margin Sensitivity

Purchase Price Multiple / EBITDA Margin Sensitivity

An ARM acquisition will enhance shareholder value only at the right price

Present Value of Future Stock Price

Present Value of Future Stock Price - 13x P/E

EBITDA Margin in 2008-10

$0.00

9.5%

11.0%

12.5%

14.0%

15.5%

12.0x

($3.04)

($2.41)

($1.79)

($1.16)

($0.54)

13.0x

(1.00)

(0.32)

0.35

1.03

1.71

14.0x

1.04

1.77

2.50

3.23

3.96

Purch. Price /

EBITDA Margin in 2008-10

Rev Mult.

#####

9.5%

11.0%

12.5%

14.0%

15.5%

$450

1.00x

$26.49

$27.17

$27.84

$28.52

$29.20

338

0.75x

27.47

28.15

28.83

29.51

30.18

225

0.50x

28.46

29.14

29.81

30.49

31.17

Purch. Price /

EBITDA Margin in 2008-10

Rev Mult.

$0.00

9.5%

11.0%

12.5%

14.0%

15.5%

$450

1.00x

($1.00)

($0.32)

$0.35

$1.03

$1.71

338

0.75x

(0.02)

0.66

1.34

2.02

2.69

225

0.50x

0.97

1.65

2.32

3.00

3.68

Difference v. Base Case ($27.49)

Difference v. Base Case ($27.49)

CONFIDENTIAL

26

B. Consolidate in CRM

CONFIDENTIAL

27

Should North Consolidate the CRM Market?

Consolidate in CRM:

Rationale / Considerations

Successful integration of multiple tack-ons or

transformational deal

Revenue opportunities through sale of new

services to North’s existing customers

Acquired businesses have a positive

financial impact on North’s growth profile and

profitability

Attempt to achieve P/E expansion in line

with premier CRM firms

Additional CRM services expand depth of

customer relationships and strengthen

competitive position

What makes it difficult

Multiple transactions may be required to

transform North’s business model profile

Availability of attractive targets is limited

Targets currently trade at higher valuations

than historical norms

May not be anticipated by North shareholders

Have to create, or acquire and integrate,

additional internal competencies to optimize

value of acquisitions

Require additional sales and marketing

expertise and channel strategy

Need significant offshore presence

Potential dilution in the near-term

Selected Acquisition Opportunities:

CONFIDENTIAL

28

($ in millions, except per share data)

'06-'10

PF2006

PF2010

CAGR

Incremental Revenue

$88.9

$131.9

10.4%

Pro Forma Revenue

$1,375.1

$1,850.3

7.7%

% Growth

NM

7.4%

Incremental EBITDA

$16.9

$25.9

11.3%

% Margin

19.0%

19.6%

Synergies

$0.9

$3.6

Pro Forma EBITDA

$197.9

$327.4

13.4%

% Margin

14.4%

17.7%

Incremental A/T Int.

8.8

8.7

Pro Forma Net Income

$58.3

$138.1

24.1%

% Margin

4.2%

7.5%

Stand-Alone EPS

$1.82

$3.81

20.3%

PF EPS

(1)

$1.75

$3.88

22.1%

Accretion / (Dilution)

(4.0%)

1.9%

(1) Assumes acquisition financed through debt at a rate of 7.0%.

10% Discount to

FY10 EPS implies:

Stand-Alone $24.74

With Acquisition $25.19

Financial Analysis of All Cash Acquisition - PeopleSupport

Assumes an acquisition of PeopleSupport for $192MM (30% premium over current stock price, 11.4x 2006

EBITDA of $16.9MM)

Incremental revenue of $88.9MM (Year 1), growing to $131.9MM in 2010

EBITDA margin of 19.0%, growing to 19.6%

Synergies equal to $3.6MM (5% of total costs), phased in over three years

Consolidate in CRM:

Stand-Alone

With Acquisition

(1) PV of Future Share price based on cost of equity of 17.0%.

Total CRM revenue of $586MM,

represents 32% of total.

2010 EPS

$3.81

12.0x P/E

Implied FY09E Share Price

$45.76

Implied Current Share Price

(1)

$25.38

Implied FY06E PEG

0.6x

13.0x P/E

Implied FY09E Share Price

$49.58

Implied Current Share Price

(1)

$27.49

Implied FY06E PEG

0.6x

14.0x P/E

Implied FY09E Share Price

$53.39

Implied Current Share Price

(1)

$29.60

Implied FY06E PEG

0.7x

$3.88

$46.60

$25.84

0.5x

$50.49

$27.99

0.6x

$54.37

$30.15

0.6x

Note: PeopleSupport projections based on Piper Jaffray research report, dated March 7, 2006.

CONFIDENTIAL

29

Implied Future Share Price Sensitivity Analysis

Consolidate in CRM:

Public markets may not afford North a CRM multiple without a meaningful proportion of

CRM revenue

Based on stand-alone plan, CRM represents approximately 27% of total revenue by 2010

A meaningful CRM revenue mix would require significant acquisitions

Valuations currently high

Dilutive to EPS

Significant integration risk

Achieving scale in CRM and P/E multiple expansion would require a substantial capital

investment which will also result in significant short term dilution especially given

current growth trajectory of the CRM business

($ in millions)

Targeted FY10 Rev Mix

(1)(2)

Required 2010 P/E to Achieve Premium Valuation

(3)

Target CRM

CRM Rev.

Required

FY2010

$1 Above

$5 Above

Revenue

Acquired

Acq. Cost

Acr. / (Dil.)

Base Case

Base Case

27%

$0.0

$0.0

0%

13.5x

15.4x

35%

210.9

207.5

(5%)

14.1

16.1

45%

561.7

552.5

(11%)

15.1

17.2

55%

1,068.4

1,050.8

(16%)

16.1

18.4

(1) Assumes total FY2010 revenue of $1,718MM ($464MM from CRM)

(2) Assumes 12x EBITDA purchase price (12% margin), acquired CRM revenue growth of 10% per year and net income margin of 7%

(assumes synergies).

(3) Base Case represents present value of future stock price - 2009 Management Case EPS at 13x P/E. Assumes no synergies, 7% cost of

debt, 35.6MM shares outstanding in FY2010 based on standalone plan, 17% cost of equity and 50/50 cash/stock acquisition.

Compares to current

P/E of 13.2x

CONFIDENTIAL

30

C. Enter BPO

CONFIDENTIAL

31

Should North Enter the BPO Market?

Enter into BPO:

Rationale / Considerations

Beachhead transaction required to acquire

capabilities and expertise

Revenue synergies through sale of new

services to North’s existing customers

Acquisitions would require additional

managerial focus / skill sets

Acquired businesses impact would depend

on vertical

Additional BPO services expand depth of

customer relationships and strengthen

competitive position

BPO typically “stickier” revenue

What makes it difficult

Very sought-after companies

Focus of every IT services, call center and

processing company

Acquiring BPO companies is expensive:

North less experienced with BPO business

Need significant offshore capability

Difficult to acquire when market is waiting to see

demonstrated earnings improvement

Selected Acquisition Opportunities:

Announce

Transaction Value /

Date

Acquiror

Target

LTM EBITDA

02/09/06

Solera

ADP Claims Services

10.0x

01/30/06

West

Intrado

13.2

01/09/06

Sage Group PLC

(1)

Verus Financial Management

13.5

12/27/05

Fidelity National Financial

Sedgwick CMS Holdings

12.7

09/22/05

Investcorp

CCC Information Services

12.4

09/15/05

Fidelity National Info Services

Certegy

10.5

07/05/05

Carlyle Group

SS&C Technologies

23.2

05/10/05

Metavante

MBI

8.3

04/18/05

R.R. Donnelley & Sons

The Astron Group

13.6

03/28/05

Sungard

Private Equity Consortium

10.8

Mean

12.8x

Median

12.6x

North Current

7.6x

North should be opportunistic, but not focus on BPO acquisitions

CONFIDENTIAL

32

4. Sale Alternative

CONFIDENTIAL

33

Evaluation of Sale Alternative

Stand-Alone Plan

Alternative

Present Value of Share Price

Consolidate ARM

Consolidate CRM

Future Value of Share Price

$22.50 - $27.50

$23.00 - $28.00

$23.00 - $28.00

$41.00 - $50.00

$42.00 - $51.00

$42.00 - $51.00

Analysis assumes North does not execute multiple alternatives simultaneously

Analysis is not probability adjusted for the execution risk of each alternative or for the availability

of potential targets

Sale analysis must be evaluated in the context of North’s strategic alternatives

CONFIDENTIAL

34

$26.50

$25.00

$26.00

$30.00

$31.00

$29.00

$10

$20

$30

$40

Selected

Acquisitions

DCF

Leveraged

Buyout

35

CONFIDENTIAL

17.4x

-

15.8x

17.8x

-

15.1x

16.9x

-

15.6x

$79

CY2006E Unlevered NI

Enterprise Value / Unlevered NI

7.7x

-

7.0x

7.9x

-

6.7x

7.5x

-

6.9x

$180

CY2006E EBITDA

Enterprise Value / EBITDA

1.1x

-

1.0x

1.1x

-

0.9x

1.0x

-

1.0x

$1,286

CY2006E Revenue

Enterprise Value / Revenue

Implied Multiple

Implied Multiple

Implied Multiple

Statistic

63.1%

-

44.1%

68.5%

-

35.9%

57.7%

-

41.3%

$18.39

120 Day Average

64.1%

-

45.0%

69.6%

-

36.8%

58.6%

-

42.2%

$18.28

90 Day Average

56.3%

-

38.1%

61.6%

-

30.3%

51.1%

-

35.5%

$19.19

60 Day Average

39.5%

-

23.3%

44.2%

-

16.3%

34.9%

-

20.9%

$21.50

30 Day Average

Prem. to Avg. Stock Price over Period:

$1,377.6

-

$1,252.6

$1,413.8

-

$1,199.0

$1,341.9

-

$1,234.8

Enterprise Value

$999.2

-

$874.3

$1,035.4

-

$820.7

$963.5

-

$856.4

Equity Value

$30.00

-

$26.50

$31.00

-

$25.00

$29.00

-

$26.00

Share Price

Note: Assumes debt of $402.1MM (includes minority interest and out-of-the-money convertible securities) and cash of $23.7 million, based on 12/31/05 10-K.

52 Week Hi: $24.31

52 Week Lo: $15.28

Current: $22.64

($ in millions, except per share amounts)

Sale Alternative:

Preliminary Valuation Summary

Sale Alternative:

Preliminary Discounted Cash Flow Analysis

DCF Assumptions

DCF Sensitivity

($ in millions)

2006E

2007E

2008E

2009E

2010E

Total Revenue

$1,286.2

$1,399.5

$1,491.0

$1,597.8

$1,718.4

% growth

22.2%

8.8%

6.5%

7.2%

7.5%

Gross Profit

603.4

661.0

701.2

749.6

804.0

% margin

46.9%

47.2%

47.0%

46.9%

46.8%

EBITDA

180.1

219.8

242.2

269.8

297.9

% margin

14.0%

15.7%

16.2%

16.9%

17.3%

EBIT

127.7

170.9

196.3

224.4

255.3

% margin

9.9%

12.2%

13.2%

14.0%

14.9%

Cash Taxes

34.0

52.1

60.9

69.5

80.1

Tax Rate

26.6%

30.5%

31.0%

31.0%

31.4%

Unlevered Free Cash Flow

137.8

135.6

124.6

131.4

138.8

Note: Unlevered free cash flow is before subtraction of minority interest (minority interest is included in debt).

Discount

Terminal EBITDA Multiple

Rate

5.5x

6.0x

6.5x

14.0%

$459.3

$459.3

$459.3

PV Free Cash Flow

924.2

1008.3

1092.3

PV Terminal Value

1383.5

1467.5

1551.5

Aggregate Value

1005.1

1089.2

1173.2

Equity Value

$30.16

$32.47

$34.77

Equity Value per Share

5.8%

6.5%

7.0%

Implied Perpertuity Growth

15.0%

$448.5

$448.5

$448.5

PV Free Cash Flow

884.7

965.2

1045.6

PV Terminal Value

1333.2

1413.6

1494.1

Aggregate Value

954.9

1035.3

1115.7

Equity Value

$28.76

$31.00

$33.20

Equity Value per Share

6.8%

7.5%

8.0%

Implied Perpertuity Growth

16.0%

$438.1

$438.1

$438.1

PV Free Cash Flow

847.3

924.3

1001.3

PV Terminal Value

1285.4

1362.4

1439.4

Aggregate Value

907.0

984.0

1061.0

Equity Value

$27.42

$29.57

$31.70

Equity Value per Share

7.8%

8.5%

9.0%

Implied Perpertuity Growth

CONFIDENTIAL

36

Sale Alternative:

Illustrative DCF Sensitivity Analysis

Sale price dependent on ability to prove margin and growth of business

DCF Sensitivity - 6.0x FY2011E EBITDA Multiple; 15.0% WACC

A potential acquiror’s ability to pay a substantial premium will be driven by their ability to

establish synergy opportunities

However, risk exists potential acquiror will create their own lower financial plan

Cost

synergy

value

CY06-CY10 Change in Rev. Growth vs. Mgmt. Case

$28.50

(2.0%)

(1.5%)

(1.0%)

(0.5%)

0.0%

CY06 - CY10

(1.0%)

$25.10

$25.92

$26.76

$27.62

$28.50

Change in

(0.5%)

$26.25

$27.10

$27.97

$28.85

$29.75

EBITDA Margin

0.0%

$27.40

$28.27

$29.17

$30.08

$31.00

vs. Mgmt. Case

0.5%

$28.55

$29.45

$30.37

$31.29

$32.22

1.0%

$29.70

$30.62

$31.55

$32.49

$33.45

CONFIDENTIAL

37

Sale Alternative:

Preliminary Leveraged Buyout Analysis

Parameter

Range

Drivers

Equity Investment Horizon

~ 5 years

Investment horizon considerations

Equity Rate of Return

20 - 25%

Market conditions

Equity Capitalization

20 - 30%

Market conditions

Rate of returns criteria

Total Leverage

(Total Debt / EBITDA)

~5.0x

Amount / level of equity

Business valuation and market conditions

Comparable companies capital structure

Senior leverage: 3x

Subordinated leverage: 2x

CONFIDENTIAL

38

Sale Alternative:

Illustrative LBO Sensitivity Analysis

A financial sponsor may view risk in the management plan and have a downside case with

conservative EBITDA / cash flow assumptions

Imp. AV

$1,234.8

$1,270.5

$1,306.2

$1,341.9

$1,377.6

Shr. Price

$26.00

$27.00

$28.00

$29.00

$30.00

EBITDA Purchase / Exit Price Multiple

8.4x

8.7x

8.9x

9.1x

9.4x

CY06-CY10

0.0%

33.5%

32.3%

31.3%

30.4%

29.6%

Change in

(2.5%)

29.0%

27.9%

27.0%

26.2%

25.4%

Rev. Growth v.

(5.0%)

24.3%

23.3%

22.5%

21.7%

21.0%

Mgmt. Case

(7.5%)

19.2%

18.4%

17.6%

17.0%

16.4%

CONFIDENTIAL

39

Sale Alternative:

LBO Leverage Analysis

LBO Leverage Analysis - Change in Timing

Debt Capacity at

5x Leverage

LBO Using LTM

6/30/06 EBITDA

LBO Using 1H:06

Run-Rate EBITDA

$755MM

$830MM

LBO Using LTM

12/31/06 EBITDA

$900MM

EBITDA

$151MM

$166MM

$180MM

$70MM difference

represents PV of

$13MM(1) in EBITDA,

or approximately 13%

of 2H:06 EBITDA

$70MM difference

represents PV $2 per

share(2)

Observations

Board needs to evaluate

potential to generate additional

value per share v. timing risks

(execution of business plan,

change in credit markets)

(1) Represents difference of $14MM in EBITDA discounted 6 months at 17%.

(2) Represents difference in debt capacity per share (based on 32MM shares) discounted 6 months at 17%.

CONFIDENTIAL

40

Strong Syndicated Loan Market

Cash Inflows vs. New Issue Volume

New Issue Volume

Commentary

($ in billions)

Source: Loan Pricing Corp.

1999

2000

2001

2002

2003

2004

2005

Leveraged

$320

$310

$218

$260

$329

$480

$501

Non-Leveraged

697

886

889

709

601

867

994

Total

$1,017

$1,196

$1,107

$969

$930

$1,348

$1,495

After a record year in overall Leveraged Loan

issuance, 2006 has continued to be strong with heavy

volume from large LBO and M&A executions

2005 Market Headlines:

Institutional volume: a record $241 billion versus

$223 billion in 2004, and new money issuance

up 20% in ‘05 to $183 billion

LBO volume: surged 36% to $65 billion as large

LBO transactions (SunGard, Hertz, Neiman

Marcus, e.g.) became more commonplace

Second lien: niche category continued to flourish

to a new high of $16 billion.

Funds flow continued to be strong in 2005, with

inflows exceeding supply by $9.5 billion.

CLO vehicles are the principle source of inflows,

and hedge funds continue to increase presence

Market pricing is issuer friendly

BB institutional loan pricing still near record lows

(L+166bps) at 170bps

B institutional loan pricing of L+257bps is only 22bps

off its record low of L+235bps set in March 2005

Sale Alternative:

Source: Standard & Poor’s PMD.

121.5

157.7

74.4

91.4

55.9

35.5

50.8

57.7

123.2

148.3

75.4

69.1

49.8

33.5

45.7

59.7

Total Flows Into Institutional Accounts

New Issue Institutional Volume

1999

2000

2001

2002

2003

2004

1H05

2005

($ in billions)

CONFIDENTIAL

41

Review of Key Considerations

Issues for consideration

Execution risk in the current management plan

Achieving long term EPS growth targets will be challenging, particularly in core ARM

business

Past performance has been volatile

Shareholders subject to share price volatility if further “misses” occur

Other strategies available to North do not significantly enhance shareholder value

Shareholders receive a premium today

M&A market is strong allowing sellers to achieve competitive pricing

Strong LBO market

May be able to attract a strategic buyer

Process launched in the short-term should capture expected near-term performance

improvements

Sale process should likely be concluded after Q2/06 with significant visibility for the Q3 and

Q4 results

Private market should give credit to performance improvements on a forward basis

Pipeline of CRM / ARM providers expected to come to market in next 12-18 months

Sale processes likely to be related to operational issues

Acquisition multiples of “broken” competitors may taint M&A market in the sector

Sale Alternative:

A market test could be conducted on an expedited time frame

CONFIDENTIAL

42

Potential Acquirors: Financial

We believe that North will be highly attractive to financial buyers

Preliminary screening criteria

Fund size – financial buyer must be large enough to make the equity investment

Fund focus – understand the business services sector

Targeted Financial Buyers

Tier 2

Advent International Corporation

Bear Stearns Merchant Banking

Cerberus Capital Management

Code Hennessey & Simmons

Francisco Partners

Leonard Green & Partners

Oak Hill Capital

Oaktree Capital Management

Parthenon Capital

Platinum Equity

Temasek

Vista Equity Partners

Warburg Pincus

Tier 1

Apax Partners Worldwide

Bain Capital

Blackstone

The Carlyle Group

Citigroup Venture Capital

General Atlantic

Golden Gate Capital

Hellman & Friedman

New Mountain Capital

One Equity

Silver Lake Partners

Thomas H. Lee

Texas Pacific Group

Sale Alternative:

CONFIDENTIAL

43

COMPANY

CS RELATIONSHIP

MARKET CAP

CY2006 P/E

Tier 1

ACS

John Rexford, Head of Corp. Development

$8,239MM

17.3x

ADP

Jan Siegmund, Head of Strategy

$27,783MM

22.6x

Convergys

Sajid Malhotra, Head of M&A

Earl Shanks, CFO

$2,513MM

16.3x

Teletech

Kennet

h Tuchman, CEO

$836MM

24.5x

Sallie Mae

Thomas Fitzpatrick, CEO

$24,138MM

19.5x

West Corp

Thomas B. Barker, CEO

Rob Johnson, M&A

$3,150MM

19.1x

Tier 2

Cargill

William W. Veazey, SVP and CFO

Private

Ceridian

Douglas Neve, CFO

$3,883MM

24.5x

H&R Bl

ock

Mark Ernst, Chairman and CEO

$6,978MM

11.2x

Potential Acquirors: Strategic

We believe that North will be highly attractive to certain strategic buyers

Rationale

Extend capabilities in F&A BPO and CRM

Establish leadership in Transaction Mgmt

Attractive top line growth

BPO / Call Center

Rationale

Extend capabilities in F&A BPO and CRM

Reduce capital intensity in current business model

More favorable industry trends than in core North

America ITO market

IT Outsourcing

COMPANY

CS RELATIONSHIP

MARKET CAP

CY2006 P/E

Tier 1

Fidelity National

Bill Foley, Chairman and CEO

Brent Bickett, Head of M&A

$6,939MM

10.5x

Hewlett Packard

Hans Lidforss, Head of M&A

$101,513MM

17.1x

IBM

Dave Johnson, EVP, Corp. Development

$133,6

26MM

14.4x

Tier 2

Bertelsmann

(Arvato)

Joachim Arenth, SVP, Corp Development

Private

Perot

Peter Altabef, President and CEO

$1,897MM

16.5x

Sale Alternative:

CONFIDENTIAL

44

Potential Acquirors: Strategic (cont’d)

Rationale

Establish F&A BPO capabilities

Potential to accelerate margin improvements

Leadership position in North American market with recognized brand

Offshore

Rationale

Extend capabilities in F&A BPO and CRM

Establish leadership in Transaction Management

Avoid upfront capital investment in CRM

Installed large customer base may allow immediate "upside" opportunities for North

Consulting / SI

COMPANY

CS RELATIONSHIP

MARKET CAP

CY2006 P/E

Tier 1

Accenture

Tim Breene, Head of M&A

$27,797MM

19.2x

EDS

Tom Haubenstricker, Co-

CFO

$15,038MM

31.3x

Tier 2

Cap Gemini

Tim Critchfield, Finance Director, North America

$6,841MM

25.0x

CGI Group

Cl

aude S

é

guin, SVP, Corp Development

$2,517MM

13.3x

COMPANY

CS RELATIONSHIP

MARKET CAP

CY2006 P/E

Tier 1

HCL Technologies

Anil Chanana, Head of M&A

Shiv Nadar, CEO

$4,388MM

17.5x

ICICI Onesource

(1)

Anada Mukerji, CEO

Rajesh Subramaqnian, Head of Corp. Dev.

$12,158MM

17.0x

Wipro Spectramind

(1)

Sudip

Nandy, Head of M&A

Suresh Senapaty, CFO

$19,106MM

35.1x

Tier 2

Intelenet

Susir Kumar, CEO

Private

Genpact

Pramod Bhasin, CEO

Private

Sale Alternative:

(1) Parent company.

CONFIDENTIAL

45

Preliminary Process Outline / Transaction Timetable

Closing

Anti-trust and other regulatory approvals, as necessary

Closing

Stage 1: Initial Due

Diligence / Market

Assessment

Conduct management presentations

Provide data room access

Distribution of process letter and draft SPA

Provide parties Q2 results

Stage 3: Due

Diligence

CS receives initial indications and reports to Board

Selection of preferred buyer(s)

SPA negotiation with preferred buyer(s)

Board approvals

Execution of definitive agreements

Transaction announcement

Stage 4: Negotiation

/ Announcement

Stage

Description

Timing

4 Weeks

(April 3 - 24)

4 weeks

(Weeks of May 1 - 22)

5 Weeks

(Weeks of June 26 - July 24)

Receive final bids from potential buyers

Due diligence

Preparation of marketing materials (teaser, info memo, short-form management presentation)

Conduct short-form management presentation to selected group of Tier 1 strategic buyers

Determine level of Tier 1 buyer interest

3 Weeks

(Weeks of July 31 - Aug 14)

46

If limited Tier 1 strategic interest indicated, go broad

Contact Tier 2 buyers and execute confidentiality agreements if decision to go broad

Distribute info memo to all contacted buyers (include Q1 results and visibility into Q2)

Stage 2: Approach

Buyers

4 Weeks

(Weeks of May 29 - Jun 19)

Discuss with Board next steps

Sale Alternative:

CONFIDENTIAL

Appendix

A. North Situation Overview

CONFIDENTIAL

47

$15

$17

$19

$21

$23

$25

$27

3/17/05

4/27/05

6/7/05

7/18/05

8/25/05

10/5/05

11/14/05

12/23/05

2/6/06

3/17/06

0

300

600

900

1,200

1,500

1,800

2,100

Volume

North

7/7/2005: Announced $119MM

acquisition of Risk Management

Alternatives, a leading provider of

debt collection and accounts

receivable management services.

North Stock Price Performance

North’s stock price has recently rebounded back to levels from early last year as a result

of improved revenue and earnings performance

March 17, 2005 to March 17, 2006

Mar-05 Earnings

Date

5/3/05

EPS

$0.45

Revenue

$260.3

Q/Q Growth

25%

Y/Y Growth

5%

Jun-05 Earnings

Date

7/29/05

EPS

$0.42

Revenue

$247.2

Q/Q Growth

(7%)

Y/Y Growth

(2%)

Sep-05 Earnings

Date

11/7/05

EPS

$0.24

Revenue

$246.3

Q/Q Growth

(43%)

Y/Y Growth

(38%)

Dec-05 Earnings

Date

2/13/06

EPS

$0.23

Revenue

$290.3

Q/Q Growth

(4%)

Y/Y Growth

(36%)

Average Statistics

Period

Price

Volume

(000s)

Current

$22.64

402.8

Last 5 Days

23.17

191.7

Last 10 Days

23.17

226.2

Last 30 Days

21.50

234.4

Last 60 Days

19.19

202.1

Last 90 Days

18.28

224.0

CONFIDENTIAL

48

60

70

80

90

100

110

120

130

140

3/17/05

4/27/05

6/7/05

7/18/05

8/26/05

10/6/05

11/16/05

12/27/05

2/6/06

3/17/06

North

NASDAQ

S&P 500

Outsourced CRM Services

Portfolio Purchasers

Indexed Stock Price Performance

Note: Outsourced CRM Services composite includes APAC, Convergys, ICT Group, Intrum Justitia, PeopleSupport, Sitel, SR Teleperformance, Startek, Sykes Enterprises, Teletech and West.

Portfolio Purchasers composite includes Asset Acceptance, Asta Funding, Encore Capital and Portfolio Recovery.

Outsourced CRM

Services

+24.6%

NASDAQ

+14.4%

Portfolio

Purchasers

+13.8%

North

+11.5%

Due to strong recent earnings report, North’s stock price performance has improved

relative to both its peers and the broader market

S&P 500

+9.8%

CONFIDENTIAL

49

Boenning & Scattergood

CIBC

Deutsche Bank

JMP Securities

SunTrust Robinson

Humphrey

Analyst

Sutherland

Thompson

Sakakeeny

Scharf

Hughes

Latest

2/15/2006

2/14/2006

2/14/2006

2/14/2006

2/14/2006

Comments

Price Target

$26.00

NA

$17.00

$25.00

$26.00

Methodology

CY06 P/E (supported by

DCF)

NA

DCF

CY07 P/E and EBITDA

CY06 P/E

Metrics

$1.72 CY06 EPS

NA

Terminal value growth

of 4%, risk premium of

6%, WACC of 12%

$1.92 CY07 EPS

$188.7M CY07

EBITDA

$1.60 CY06 EPS

Multiples Used

15x EPS

NA

NA

13x EPS; 6x EBITDA

16x EPS

Rating

Market OutPerform

Sector Performer

Hold

Market Outperform

Buy

Recent Analyst Commentary

While the Street was positive on the results for the recent quarter, analysts will likely

remain cautious for the next few quarters

Stated Valuation

Methodologies

CONFIDENTIAL

50

Our estimate is quite

conservative relative to

management’s guidance

range, which is

deliberate based on on-

going concerns about

pricing and cost

pressures in the core

ARM business.

Skepticism is likely to

linger in the shares,

given the company’s

multi- year record

earnings misses and

lower expectations.

This creates, in our

view, an excellent

buying opportunity.

Despite the lingering

hurricane-related impact

on operations in the Gulf

Coast region, and a

deterioration in the

amount of payments

received from

consumers, North

managed EPS of $0.38

(excluding ~$0.15 in

restructuring charges),

well ahead of our $0.28

est.

Given the lack of

evidence pointing to any

easing of a tough

operating environment,

we are hesitant to

herald 4Q05 as the

turning point in North’s

fortunes. However, we

applaud the impressive

4Q05 outperformance,

which certainly bodes

well for 2006.

Topline grew 23% YoY

but were almost entirely

attributed to

acquisitions. Higher fuel

costs and the overhang

from recent hurricanes

continue to weigh on

results.

We are lowering

adjusted 1Q06 and

2006 EPS from $0.42

and $1.65 to $0.37 and

$1.60. Our 1Q06 and

2006 revenue forecasts

are unchanged at

$275.0mm and $1,065.7

mm.

We believe that a

difficult sub-prime

market will continue to

limit share appreciation

and reiterate our Hold

rating.

Despite an almost 20%

rise in shares of North

today, we have

increased conviction in

the company’s

surprisingly strong 2006

guidance. The

combination of better

visibility in North

Portfolio from forward

flow deals, higher

volumes and debt sales,

the ongoing ramping of

big client wins in CRM,

and our no-growth,

cautious assumptions in

the ARM segment

combine to form

achievable estimates

with a compelling cash

flow-based valuation.

The company benefited

from acquisitions closed

in 3Q including Marlin

and RMA.

Our $26 per share price

target assumes the

current-year P/E

multiple expands to

around 16x our 2006E

EPS of $1.60. We

believe that high quality

business services

companies should trade

at P/E multiples that are

in line or slightly ahead

of their trendline growth

rates.

0.4x

0.6x

0.8x

1.0x

1.2x

1.4x

1.6x

3/17/05

4/27/05

6/7/05

7/18/05

8/26/05

10/6/05

11/16/05

12/27/05

2/6/06

3/17/06

North

Outsourced CRM Services

Portfolio Purchasers

0.0x

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

3/17/05

4/27/05

6/7/05

7/18/05

8/26/05

10/6/05

11/16/05

12/27/05

2/6/06

3/17/06

North

Outsourced CRM Services

Portfolio Purchasers

Historical NTM PE Performance

NTM Price / Earnings Multiple

CRM

Average 1.1x

North

Average 0.9x

North

Average 11.1x

CRM

Average 19.4x

NTM PEG Ratio

Portfolio

Purchasers

Average 13.4x

Portfolio Purchasers

Average 0.8x

Note: Outsourced CRM Services composite includes APAC, Convergys, ICT Group, Intrum Justitia, PeopleSupport, Sitel, SR Teleperformance, Startek, Sykes Enterprises, Teletech and West.

Portfolio Purchasers composite includes Asset Acceptance, Asta Funding, Encore Capital and Portfolio Recovery.

North has historically traded at a discount to its peers, but has recently seen its

NTM P/E improve significantly

CONFIDENTIAL

51

Appendix

B. Comparable Company Analysis

CONFIDENTIAL

52

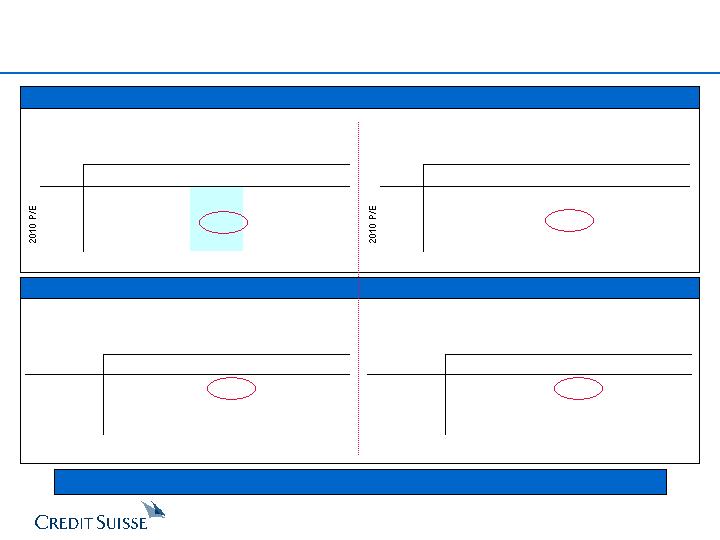

Trading Statistics of Comparable Companies

(USD millions, except per share amounts)

Trading Performance

FD Capitalization

Stock

Disc.

/ Prem.

Equity

Aggr.

FD Aggregate Value /

LT

CY2007

Price

to LTM

Market

Market

P/E Multiples

Revenue

EBITDA

Gr. Rate

PE /

COMPANY (FYE)

3/17/06

High

Low

Value

Value

CY06

CY07

CY06

CY07

CY06

CY07

(LTGR)

LTGR

NORTH (MANAGEMENT) (Dec.)

$22.64

(6.9%)

48.2%

$733

$1,112

12.4x

9.0x

0.9x

0.8x

6.2x

5.1x

12.0%

0.7x

NORTH (STREET) (Dec.)

$22.64

(6.9%)

48.2%

$733

$1,112

13.2x

11.9x

0.9x

0.9x

6.3x

6.1x

12.0%

1.0x

Outsourced CRM Services

WEST CORP (Dec.)

$43.03

(1.1%)

38.0%

$3,150

$3,395

19.1x

17.2x

2.0x

1.9x

8.2x

7.8x

17.0%

1.0x

CONVERGYS CORP (Dec.)

17.78

(0.7%)

41.3%

2,513

2,750

16.3x

14.6x

1.0x

1.0x

6.6x

6.2x

12.2%

1.2x

SR TELEPERFORMANCE (Dec.)

36.23

(1.1%)

29.7%

1,290

1,498

17.8x

15.8x

0.9x

0.9x

7.0x

6.4x

9.8%

1.6x

TELETECH HOLDINGS INC (Dec.)

11.76

(9.8%)

60.2%

836

838

24.5x

18.1x

0.7x

0.7x

7.8x

6.8x

21.7%

0.8x

INTRUM JUSTITIA NV (Dec.)

8.99

(8.8%)

35.9%

705

859

13.9x

13.0x

2.2x

2.1x

10.0x

9.4x

NA

NA

SYKES ENTERPRISES INC (Dec.)

14.34

(2.8%)

114.7%

578

451

24.7x

19.9x

0.9x

0.8x

8.8x

7.6x

NA

NM

ICT GROUP INC (Dec.)

25.10

0.0%

190.2%

339

364

22.4x

17.7x

0.8x

0.8x

8.4x

7.3x

22.5%

0.8x

STARTEK INC (Dec.)

22.52

0.0%

95.8%

335

295

24.0x

20.7x

1.3x

1.2x

7.8x

7.2x

15.5%

1.3x

SITEL CORP (Dec.)

3.99

(2.2%)

150.9%

300

412

24.9x

NA

NA

NA

5.2x

NA

NA

NM

PEOPLESUPPORT INC (Dec.)

9.66

(9.7%)

34.9%

185

143

24.2x

19.3x

1.6x

1.3x

8.5x

6.8x

23.8%

0.8x

APAC CUSTOMER SERVICES INC (Dec.)

2.31

(4.5%)

234.8%

114

125

38.5x

23.1x

0.6x

0.5x

6.7x

5.6x

15.0%

1.5x

Median

(2.2%)

60.2%

24.0x

17.9x

1.0x

0.9x

7.8x

7.0x

16.3%

1.1x

Mean

(3.7%)

93.3%

22.8x

17.9x

1.2x

1.1x

7.7x

7.1x

17.2%

1.1x

Portfolio Purchasers

PORTFOLIO RECOVRY ASSOC INC (Dec.)

$45.35

(12.2%)

40.3%

$735

$736

17.1x

14.0x

3.9x

3.3x

8.7x

7.2x

18.0%

0.8x

ASSET ACCEPTANCE CAPITAL CP (Dec.)

19.65

(37.5%)

13.3%

731

681

13.6x

11.9x

2.5x

2.2x

7.7x

6.8x

14.8%

0.8x

ASTA FUNDING INC (Sep.)

33.76

(4.1%)

74.3%

498

586

12.0x

NA

6.6x

NA

NA

NA

17.5%

NM

ENCORE CAPITAL GROUP INC (Dec.)

16.48

(15.7%)

26.8%

393

575

10.5x

NA

2.6x

NA

7.0x

NA

14.0%

NM

Median

(14.0%)

33.5%

12.8x

12.9x

3.3x

2.8x

7.7x

7.0x

16.1%

0.8x

Mean

(17.4%)

38.7%

13.3x

12.9x

3.9x

2.8x

7.8x

7.0x

16.1%

0.8x

Overall Median

(4.1%)

41.3%

19.1x

17.4x

1.4x

1.1x

7.8x

7.0x

16.3%

0.9x

Overall Mean

(7.4%)

78.7%

20.2x

17.1x

2.0x

1.4x

7.7x

7.1x

16.8%

1.1x

Source: IBES consensus estimates and Wall Street Research

CONFIDENTIAL

53

Operating Statistics of Comparable Companies

(USD millions, except per share amounts)

Y/Y Revenue Growth

Y/Y EPS Growth

Revenue

CY06/

CY07/

EBIT Margin

EBITDA Margin

Net Margin

CY06/

CY07/

COMPANY (FYE)

CY06

CY07

CY05

CY06

CY06

CY07

CY06

CY07

CY06

CY07

CY05

CY06

NORTH (MANAGEMENT) (Dec.)

$1,286.2

$1,399.5

22.2%

8.8%

10.2%

13.0%

14.0%

15.7%

4.7%

6.2%

13.8%

38.5%

NORTH (STREET) (Dec.)

$1,211.8

$1,241.8

15.2%

2.5%

NM

NM

14.5%

14.6%

4.8%

4.9%

7.0%

10.8%

Outsourced CRM Services

WEST CORP (Dec.)

$1,692.7

$1,781.6

11.1%

5.3%

17.8%

18.1%

24.5%

24.4%

9.6%

10.2%

6.6%

11.1%

CONVERGYS CORP (Dec.)

2,701.7

2,877.8

4.6%

6.5%

9.9%

10.5%

15.3%

15.5%

5.9%

6.3%

26.7%

11.9%

SR TELEPERFORMANCE (Dec.)

1,593.2

1,704.0

9.5%

7.0%

9.3%

9.6%

13.4%

13.7%

5.5%

5.8%

19.3%

13.2%

TELETECH HOLDINGS INC (Dec.)

1,146.8

1,216.0

5.5%

6.0%

5.1%