FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Issuer

Pursuant to Rule 13a-16 or 15d-16 of

the Securities Exchange Act of 1934

Commission File Number: 001-14554

Banco Santander Chile

Santander Chile Bank

(Translation of Registrant’s Name into English)

Bandera 140

Santiago, Chile

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

| Form 20-F | x | Form 40-F | o |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

| Yes | o | No | x |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

| Yes | o | No | x |

Indicate by check mark whether by furnishing the information contained in this Form, the Registrant is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934:

| Yes | o | No | x |

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): N/A

Table of Contents

| Item | ||

| 1. | 3Q2011 Earnings Release | |

| 2. | 9M 2011 Financial Statements |

2

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| BANCO SANTANDER-CHILE | |

| By: | /s/ |

| Name: | Juan Pedro Santa María |

| Title: | General Counsel |

Date: November 4, 2011

3

BANCO SANTANDER CHILE

THIRD QUARTER 2011

EARNINGS REPORT

INDEX

| SECTION | PAGE |

| SECTION 1: SUMMARY OF RESULTS | 2 |

| SECTION 2: BALANCE SHEET ANALYSIS | 6 |

| SECTION 3: ANALYSIS OF QUARTERLY INCOME STATEMENT | 9 |

| SECTION 4: CREDIT RISK RATINGS | 16 |

| SECTION 5: SHARE PERFORMANCE | 17 |

| ANNEX 1: NEW PROVISIONING MODEL FOR RESIDENTIAL MORTGAGE LOANS | 18 |

| ANNEX 2: BALANCE SHEET | 19 |

| ANNEX 3: YEAR-TO-DATE INCOME STATEMENT | 20 |

| ANNEX 4: QUARTERLY INCOME STATEMENTS | 21 |

| ANNEX 5: QUARTERLY EVOLUTION OF MAIN RATIOS AND OTHER INFORMATION | 22 |

| CONTACT INFORMATION | Santiago, Chile |

| Robert Moreno | Tel: (562) 320-8284 |

| Manager, Investor Relations Department | Fax: (562) 671-6554 |

| Banco Santander Chile | Email: rmorenoh@santander.cl |

| Bandera 140 Piso 19 | Website: www.santander.cl |

SECTION 1: SUMMARY OF RESULTS

3Q11: preparing for a more challenging environment

In the nine-month period ended September 30, 2011 (9M11), net income attributable to shareholders1 totaled Ch$332,963 million (Ch$1.77 per share and US$3.56/ADR2) and decreased 13.1% compared to net income in the same period of 2010. Return on average equity reached 23.8% in 9M11, among the highest returns in the Chilean financial system. The efficiency ratio in 9M11 reached 38.4%.

In 3Q11, net income attributable to shareholders totaled Ch$75,153 million (Ch$0.40 per share and US$0.80/ADR). Compared to 2Q11 (from now on QoQ) net income decreased 46.9%. Compared to 3Q10 (from now on YoY) net income decreased 40.0%. Several non-recurring items and a cautious stance regarding risks affected these results.

Our outlook for Chile in 2012 continues to be positive, with GDP expected to expand 4.5% and inflation to be close to 3.0%. Nonetheless, the Bank focused its actions on 4 main points in the quarter in order to maintain sustainable levels of high profitability in 2012: (i) Liquidity, (ii) Capital, (iii) Selective loan growth and spreads, and (iv) Prudent risk policies. This process is very similar to the approach we carried out in the 2008-2009 period.

| I. | Focus on liquidity |

Core deposits grow 6.9% QoQ and 30.9% YoY

Total deposits increased 4.4% QoQ. In the quarter, the Bank continued to focus on increasing its core deposit base (non-institutional deposits). These cheaper deposits led growth and expanded 6.9% QoQ and 30.9% YoY, representing more than 70% of the Bank’s deposit base. The Bank’s loan to deposit ratio (measured as loans minus marketable securities that fund mortgage portfolio over total deposits3) improved to 94.8% as of September 2011 compared to 96.8% as of June 2011 and 100.9% in September 2010.

The Bank’s market share in total deposits has increased 36 basis points in the last 12 months to 18.7%. Throughout 2011, funding costs in the banking system have risen due to higher short-term interest rates, but the Bank’s funding costs have increased at a slower pace given the focus on core deposit growth. We currently have opened a gap of 20 basis points in average cost of funds compared to the rest of the Chilean banking system.

3 Mortgage loans in Chile are long-term fixed rate loans. Therefore, we consider it to be more conservative form a market risk and liquidity stand point to fund these loans with long-term fixed rate bonds and not short-term variable rate deposits.

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

2

Average cost of funds

Cost of funds: Interest expenses / total liabilities annualized. Competition includes all Chilean banks minus Santander. Source of data: Superintendency of Banks of Chile (SBIF)

Surplus liquidity tops US$3 billion

In the quarter, the Bank’s deposit base increased at a faster pace than its loans. This additional liquidity was temporarily invested in Chilean sovereign risk. The Bank’s surplus liquidity, defined as financial investments minus non-structural liabilities, averaged US$3.0 billion in the quarter.

| II. | Focus on core capital |

Core capital at 10.2%. ROAE in 9M11 at 23.8%

The Bank currently has one of the highest capitalization levels in the Chilean financial system. Voting common shareholders’ equity is the sole component of our Tier I capital. The Bank core capital ratio reached 10.2%, increasing 40 bp QoQ. The Bank implemented a series of measures to boost core capital ratios by optimizing risk-weighted assets. As a result, the BIS ratio reached 13.9% as of September 30, 2011 compared to 13.4% as of June 2011. ROAE in the nine-month period ended September 30, 2011 reached 23.8%.

| III. | Focus on selective loan growth and spreads |

In 3Q11, total loans increased 1.5% QoQ and 16.1% YoY. The Bank has been following a more selective approach to loan growth given the market uncertainty, while continuing to focus on retail lending activities. Higher yielding loans to individuals increased 2.1% QoQ in 3Q11. This loan growth was led by lending to middle and upper income individuals, which expanded 2.2% QoQ. Lending to Santander Banefe slowed in the quarter and grew 1.3% QoQ. Lending to SMEs led growth in retail lending and expanded 2.8% QoQ. In the middle market, loans grew 2.9% QoQ (18.1% YoY). This year the Bank is obtaining attractive returns in this segment given the positive evolution of credit risk and spreads.

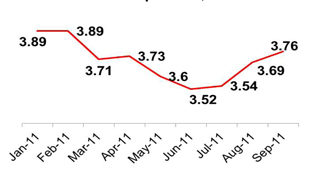

Rising spreads

The Banks net interest margin in the quarter reached 4.6% compared to 5.2% in 2Q11. The Bank’s margins in the quarter were negatively affected by lower QoQ inflation rates, as the Bank has more assets than liabilities linked to inflation. Inflation in the quarter descended from 1.44% in 2Q11 to 0.56% in 3Q11. For every 100 bp decline in inflation, net interest income falls by approximately Ch$25 billion. The increase in the Bank’s surplus liquidity has also temporarily reduced the Bank’s net interest margin.

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

3

These negative effects on margins were partially offset by rising loan spreads (excluding the impacts of mismatches in inflation indexed assets and liabilities). Loan spreads in the quarter began to rise as the Bank implemented a stricter pricing policy in light of a potential deterioration of economic conditions and a potentially higher cost of capital. This should also help to sustain or improve margins in coming quarters.

Loan spreads*, %

Spread = Loan yield minus cost of funds and excluding impacts of inflation indexed asset and liability mismatches.

| IV. | Prudent credit risk policies |

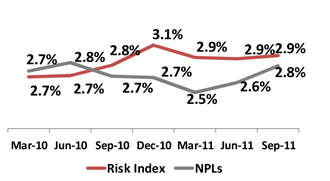

Risk index stable despite higher provisions

On a year-to date basis net provision expense has increased 7.6% compared to a 16.1% rise in loan growth. Provision for loan losses in the quarter increased 58.9% QoQ and 75.4% YoY. This rise was mainly due to one-time provisions expenses, the expansion of our lending volumes, especially consumer lending and more prudent credit risk policies implemented in light of a possible deterioration of the macro environment. This included restricting renegotiations and, therefore, increasing charge-offs. This also resulted in a temporary rise in NPLs, but did not affect the Bank’s risk index. The Risk Index, which includes non-performing loans and additional risk parameters, remained stable QoQ at 2.94%. The Bank is required to have 100% coverage at all times of its Risk Index. The NPL ratio, which includes all loans that are more than 90 days overdue, as of September 2011 reached 2.81%. The coverage ratio of total NPLs (loan loss allowances over non-performing loans) reached 104.8% as of September 2011.

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

4

Banco Santander Chile: Summary of Quarterly Results

| Quarter | Change % | |||||||||||||||||||

| 3Q11 / | 3Q11 / | |||||||||||||||||||

| (Ch$ million) | 3Q11 | 2Q11 | 3Q10 | 3Q10 | 2Q11 | |||||||||||||||

| Net interest income | 232,057 | 247,414 | 235,674 | (1.5 | )% | (6.2 | )% | |||||||||||||

| Fee income | 65,991 | 72,050 | 66,436 | (0.7 | )% | (8.4 | )% | |||||||||||||

| Core revenues | 298,048 | 319,464 | 302,110 | (1.3 | )% | (6.7 | )% | |||||||||||||

| Financial transactions, net | 23,001 | 29,076 | 21,713 | 5.9 | % | (20.9 | )% | |||||||||||||

| Provision expense | (90,372 | ) | (56,874 | ) | (51,525 | ) | 75.4 | % | 58.9 | % | ||||||||||

| Operating expenses | (128,356 | ) | (125,161 | ) | (113,570 | ) | 13.0 | % | 2.6 | % | ||||||||||

| Operating income, net of provisions and costs | 102,321 | 166,505 | 158,728 | (35.5 | )% | (38.5 | )% | |||||||||||||

| Other operating & Non-op. Income | (27,168 | ) | (24,993 | ) | (33,372 | ) | (18.6 | )% | 8.7 | % | ||||||||||

| Net income attributable to shareholders | 75,153 | 141,512 | 125,356 | (40.0 | )% | (46.9 | )% | |||||||||||||

| Net income/share (Ch$) | 0.40 | 0.75 | 0.67 | (40.0 | )% | (46.9 | )% | |||||||||||||

Net income/ADR (US$)1 | 0.80 | 1.66 | 1.42 | (43.5 | )% | (51.4 | )% | |||||||||||||

| Total loans | 17,680,356 | 17,422,041 | 15,232,019 | 16.1 | % | 1.5 | % | |||||||||||||

| Deposits | 13,892,003 | 13,306,475 | 11,146,945 | 24.6 | % | 4.4 | % | |||||||||||||

| Shareholders’ equity | 1,927,498 | 1,866,467 | 1,757,340 | 9.7 | % | 3.3 | % | |||||||||||||

| Net interest margin | 4.6 | % | 5.2 | % | 5.7 | % | ||||||||||||||

| Efficiency ratio | 41.3 | % | 36.5 | % | 37.2 | % | ||||||||||||||

Return on average equity2 | 15.8 | % | 30.5 | % | 29.3 | % | ||||||||||||||

NPL / Total loans3 | 2.8 | % | 2.6 | % | 2.7 | % | ||||||||||||||

| Coverage NPLs | 104.8 | % | 111.9 | % | 105.1 | % | ||||||||||||||

Risk index4 | 2.94 | % | 2.90 | % | 2.82 | % | ||||||||||||||

PDLs/ Total loans5 | 1.27 | % | 1.23 | % | 1.36 | % | ||||||||||||||

| Coverage PDLs | 232.45 | % | 235.86 | % | 206.64 | % | ||||||||||||||

| BIS ratio | 13.9 | % | 13.4 | % | 14.5 | % | ||||||||||||||

| Branches | 494 | 487 | 500 | |||||||||||||||||

| ATMs | 1,892 | 1,946 | 1,914 | |||||||||||||||||

| Employees | 11,706 | 11,516 | 11,049 | |||||||||||||||||

| 1. | The change in earnings per ADR may differ from the change in earnings per share due to the exchange rate movements. Earnings per ADR was calculated using the Observed Exchange Rate Ch$515.14 per US$ as of September 30, 2011. |

| 2. | Annualized quarterly Net income attributable to shareholders / Average equity attributable to shareholders. |

| 3. | NPLs: Non-performing loans; full balance of loans with one installment 90 days or more overdue. |

| 4. | Risk Index: Loan loss allowances / Total loans; measures the percentage of loans the banks must provision for given their internal models and the Superintendency of Banks guidelines. |

| 5. | PDLs: Past due loans; all loan installments that are more than 90 days overdue. |

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

5

SECTION 2: BALANCE SHEET ANALYSIS

LOANS

Selective loan growth led by retail lending to middle-upper income individuals

| Loans | Quarter ended, | % Change | ||||||||||||||||||

| (Ch$ million) | Sep-11 | Jun-11 | Sep-10 | Sep. 11 / 10 | Sep. 11 / Jun. 11 | |||||||||||||||

Total loans to individuals1 | 9,215,686 | 9,026,697 | 8,035,617 | 14.7 | % | 2.1 | % | |||||||||||||

| Consumer loans | 2,925,659 | 2,893,038 | 2,554,884 | 14.5 | % | 1.1 | % | |||||||||||||

| Residential mortgage loans | 5,016,419 | 4,909,630 | 4,498,799 | 11.5 | % | 2.2 | % | |||||||||||||

| SMEs | 2,524,836 | 2,455,349 | 2,301,536 | 9.7 | % | 2.8 | % | |||||||||||||

| Total retail lending | 11,740,522 | 11,482,046 | 10,337,153 | 13.6 | % | 2.3 | % | |||||||||||||

| Institutional lending | 351,686 | 372,939 | 340,274 | 3.4 | % | (5.7 | )% | |||||||||||||

| Middle-Market & Real estate | 3,731,881 | 3,625,439 | 3,160,681 | 18.1 | % | 2.9 | % | |||||||||||||

| Corporate | 1,833,084 | 1,950,992 | 1,406,210 | 30.4 | % | (6.0 | )% | |||||||||||||

Total loans 2 | 17,680,356 | 17,422,041 | 15,232,019 | 16.1 | % | 1.5 | % | |||||||||||||

1. Includes consumer loans, residential mortgage loans and other commercial loans to individuals.

2. Total loans gross of loan loss allowances. Total loans include other non-segmented loans and excludes interbank loans.

In 3Q11, total loans increased 1.5% QoQ and 16.1% YoY. The Bank has been following a more selective approach to loan growth given the market uncertainty while continuing to focus on retail lending activities.

Loans to individuals, which include consumer, mortgage and commercial loans to high-income individuals, increased of 2.1% QoQ in 3Q11. This loan growth was driven by lending to middle and upper income individuals, which expanded 2.2% QoQ. Lending to Santander Banefe increased 1.3% QoQ as the bank adopted a more selective approach to loan growth in this segment.

Breakdown loans to individuals (Ch$ million) | Sep-11 | % Change Sep. 11 / 10 | % Change Sep. 11 / Jun. 11 | |||||||||

| Middle-upper income | 8,420,540 | 14.3 | % | 2.2 | % | |||||||

| Santander Banefe | 795,146 | 18.9 | % | 1.3 | % | |||||||

| Individuals | 9,215,686 | 14.7 | % | 2.1 | % | |||||||

By product, consumer loans increased 1.1% QoQ and 14.5% YoY. In the quarter, the Bank focused on expanding its higher yielding credit card loan portfolio that increased 2.3% QoQ and 28.2% YoY. Installment loans were flat QoQ. Residential mortgage loans increased 2.2% QoQ (11.5% YoY), as long-term rates remained attractive and demand for purchasing homes continued to rise.

Lending to SMEs (defined as companies that sell less than Ch$1,200 million per year) led growth in retail lending and expanded 2.8% QoQ (9.7% YoY), reflecting the Bank’s shift in focus in the quarter given market uncertainties. This segment tends to perform better in slower economic growth periods given the high level of diversification of this portfolio.

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

6

In the middle market (comprised of companies with annual sales between Ch$1,200 million and Ch$10.000 million per year), loans grew a healthy 2.9% QoQ (18.1% YoY). This year the Bank is obtaining attractive returns in this segment given the positive evolution of credit risk and spreads.

Corporate lending (companies with sale over Ch$10,000 million per year or that are part of a large foreign or local economic group) decreased 6.0% QoQ (+30.4% YoY). This fall was mainly due to 3 corporate debt obligation that were paid in full as company’s currently have strong liquidity levels. Non-lending activities with this segment continued to grow in the quarter. (See Funding and Financial transactions, net).

FUNDING

Focus on liquidity. Core deposits grow 6.9% QoQ and 30.9% YoY

| Funding | Quarter ended, | % Change | ||||||||||||||||||

| (Ch$ million) | Sep-11 | Jun-11 | Sep-10 | Sep. 11 / 10 | Sep. 11 / Jun. 11 | |||||||||||||||

| Demand deposits | 4,496,757 | 4,450,290 | 3,991,732 | 12.7 | % | 1.0 | % | |||||||||||||

| Time deposits | 9,395,246 | 8,856,185 | 7,155,213 | 31.3 | % | 6.1 | % | |||||||||||||

| Total deposits | 13,892,003 | 13,306,475 | 11,146,945 | 24.6 | % | 4.4 | % | |||||||||||||

| Mutual funds (off-balance sheet) | 2,852,379 | 3,136,413 | 3,305,683 | (13.7 | )% | (9.1 | )% | |||||||||||||

| Total customer funds | 16,744,382 | 16,442,888 | 14,452,628 | 15.9 | % | 1.8 | % | |||||||||||||

Loans to deposits1 | 94.8 | % | 96.8 | % | 100.9 | % | ||||||||||||||

1. (Loans - marketable securities that fund mortgage portfolio) / (Time deposits + demand deposits).

Customer funds increased 1.8% in the quarter led by a 4.4% QoQ rise in total deposits. Demand deposits increased 1.0% in the same period and time deposits were up 6.1%. In the quarter, the Bank continued to focus on increasing its core deposit base. Core deposits (non-institutional deposits) increased 6.9% QoQ and 30.9% YoY. The Bank’s loan to deposit ratio (measured as loans minus marketable securities that fund mortgage portfolio over total deposits) improved to 94.8% as of September 2011 compared to 96.8% as of June 2011 and 100.9% in September 2010. The Bank’s market share in total deposits has increased 36 basis points in the last 12 months to 18.7%. Mutual funds under management decreased 9.1% QoQ. This was mainly due to weak equity markets.

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

7

SHAREHOLDERS’ EQUITY AND REGULATORY CAPITAL

Core capital at 10.2%. ROAE in 9M11 at 23.8%

| Quarter ended, | Change % | |||||||||||||||||||

(Ch$ million) | Sep-11 | Jun-11 | Sep-10 | Sep. 11 / 10 | Sep. 11 / Jun. 11 | |||||||||||||||

| 891,303 | 891,303 | 1,757,340 | (49.3 | )% | 0.0 | % | ||||||||||||||

| Reserves | 51,538 | 51,538 | 51,539 | (0.0 | )% | 0.0 | % | |||||||||||||

| Valuation adjustment | 593 | (7,831 | ) | (13,928 | ) | (104.3 | )% | (107.6 | )% | |||||||||||

| Retained Earnings: | 984,064 | 931,457 | 828,426 | 18.8 | % | 5.6 | % | |||||||||||||

| Retained earnings prior periods | 750,989 | 750,990 | 560,128 | 34.1 | % | 0.0 | % | |||||||||||||

| Income for the period | 332,963 | 257,810 | 383,283 | (13.1 | )% | 29.2 | % | |||||||||||||

| Provision for mandatory dividend | (99,889 | ) | (77,343 | ) | (114,985 | ) | (13.1 | )% | 29.2 | % | ||||||||||

| Equity attributable to shareholders | 1,927,498 | 1,866,467 | 2,623,377 | (26.5 | )% | 3.3 | % | |||||||||||||

| Non-controlling interest | 32,293 | 31,171 | 29,599 | 9.1 | % | 3.6 | % | |||||||||||||

| Total Equity | 1,959,791 | 1,897,638 | 2,652,976 | (26.1 | )% | 3.3 | % | |||||||||||||

| Quarterly ROAE | 15.8 | % | 30.5 | % | 23.0 | % | ||||||||||||||

Shareholders’ equity totaled Ch$1,927,498 million (US$4.0 billion) as of September 30, 2011. ROAE in the nine-month period ended September 30, 2011 reached 23.8%. During the quarter, the Bank implemented a series of measures to boost core capital ratios by optimizing risk-weighted assets. As a result, the BIS ratio reached 13.9% as of September 30, 2011 compared to 13.4% as of June 2011 and the Bank’s core capital ratio reached 10.2% as of September 2011 compared to 9.8% as of June 2011. Voting common shareholders’ equity is the sole component of our Tier I capital.

| Capital Adequacy | Quarter ended, | Change % | ||||||||||||||||||

(Ch$ million) | Sep-11 | Jun-11 | Sep-10 | Sep. 11 / 10 | Sep. 11 / Jun. 11 | |||||||||||||||

| Tier I (Core Capital) | 1,927,498 | 1,866,467 | 1,757,340 | 9.7 | % | 3.3 | % | |||||||||||||

| Tier II | 715,184 | 669,798 | 672,740 | 6.3 | % | 6.8 | % | |||||||||||||

| Regulatory capital | 2,642,682 | 2,536,265 | 2,430,080 | 8.7 | % | 4.2 | % | |||||||||||||

| Risk weighted assets | 18,954,146 | 18,964,803 | 16,739,710 | 13.2 | % | (0.1 | )% | |||||||||||||

| Tier I (Core capital) ratio | 10.2 | % | 9.8 | % | 10.5 | % | ||||||||||||||

| BIS ratio | 13.9 | % | 13.4 | % | 14.5 | % | ||||||||||||||

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

8

SECTION 3: ANALYSIS OF QUARTERLY INCOME STATEMENT

NET INTEREST INCOME

Net interest margins negatively affected by lower inflation in the quarter and higher levels of liquidity. Loan spreads rising.

| Quarter | Change % | |||||||||||||||||||

(Ch$ million) | 3Q11 | 2Q11 | 3Q10 | 3Q11 / 3Q10 | 3Q11 / 2Q11 | |||||||||||||||

| Interest income | 420,729 | 472,132 | 355,445 | 18.4 | % | (10.9 | )% | |||||||||||||

| Interest expense | (188,672 | ) | (224,718 | ) | (119,771 | ) | 57.5 | % | (16.0 | )% | ||||||||||

| Net interest income | 232,057 | 247,414 | 235,674 | (1.5 | )% | (6.2 | )% | |||||||||||||

| Average interest-earning assets | 20,068,322 | 19,099,828 | 16,463,951 | 21.9 | % | 5.1 | % | |||||||||||||

| Average loans | 17,460,992 | 17,146,712 | 14,874,816 | 17.4 | % | 1.8 | % | |||||||||||||

Interest earning asset yield1 | 8.4 | % | 9.9 | % | 8.6 | % | ||||||||||||||

Cost of funds2 | 4.1 | % | 5.2 | % | 2.8 | % | ||||||||||||||

Net interest margin (NIM)3 | 4.6 | % | 5.2 | % | 5.7 | % | ||||||||||||||

| Avg. equity + non-interest bearing demand deposits / Avg. interest earning assets | 31.3 | % | 33.6 | % | 34.7 | % | ||||||||||||||

Quarterly inflation rate5 | 0.56 | % | 1.44 | % | 0.65 | % | ||||||||||||||

| Central Bank reference rate | 5.25 | % | 5.25 | % | 2.50 | % | ||||||||||||||

| Avg. 10 year Central Bank yield (real) | 2.63 | % | 2.90 | % | 2.82 | % | ||||||||||||||

1. Interest income divided by interest earning assets.

2. Interest expense divided by interest bearing liabilities + demand deposits.

3. Net interest income divided by average interest earning assets annualized.

4. Net interest income net of provision expenses divided by interest earning assets.

5. Inflation measured as the variation of the Unidad de Fomento in the quarter.

Net interest income decreased 6.2% QoQ and 1.5% YoY. The Net interest margin (NIM) in 3Q11 reached 4.6% compared to 5.2% in 2Q11. Compared to 3Q10, the decline in net interest income and NIM was mainly due to higher short-term interest rates. The Central Bank has increased short-term interest rates by 300 basis points to 5.25% in the last twelve months. The Bank’s liabilities have a shorter duration than assets and, therefore, re-price more quickly in a rising interest rate environment. This has increased funding costs as reflected in the 57.5% YoY rise in interest expense in the quarter. Interest income on the other hand has increased 18.4% slightly above the 17.4% YoY increase in average loans. To offset this, the Bank focused on increasing core deposit base. We have currently opened a gap of 20 basis points in average cost of funds compared to the rest of the Chilean banking system.

Compared to 2Q11, the decrease in the Bank’s net interest income and NIM was mainly due to: (i) the lower QoQ inflation rates, which negatively affected margins, as the Bank has more assets than liabilities linked to inflation. Inflation in the quarter descended from 1.44% in 2Q11 to 0.56% in 3Q11. For every 100 bp decline in inflation, net interest income falls by approximately Ch$25 billion. This more than offset in the quarter rising loan spreads, which are gradually incorporating the higher interest rate environment. (ii) The increase in the Bank’s surplus liquidity has also temporarily reduced the Bank’s net interest margin. The Bank deposit base has increased 24.6% YoY and 4.4% QoQ compared to a 17.4% YoY and 1.8% QoQ increase in average loans.

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

9

This additional liquidity has been temporarily invested in sovereign Chilean risk. The Bank’s surplus liquidity, defined as financial investments minus non-structural liabilities, averaged US$3.0 billion in the quarter.

Surplus liquidity (US$ million)

Surplus liquidity: Financial investments minus non-structural liabilities

The negative effects on margins were partially offset by rising loan spreads (excluding the impacts of mismatches in inflation indexed assets and liabilities). Loan spreads in the quarter began to rise as the Bank implemented a stricter pricing policy in light of a potential deterioration of economic conditions. This should also help to sustain or improve margins in coming quarters.

Loan spreads*, %

Spread = Loan yield minus cost of funds and excluding impacts of inflation indexed asset and liability mismatches. Excludes corporate banking

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

10

PROVISION FOR LOAN LOSSES

Risk index stable despite higher provisions. Provision expense in 3Q11 affected by various one-time expenses

| Quarter | Change % | |||||||||||||||||||

| (Ch$ million) | 3Q11 | 2Q11 | 3Q10 | 3Q11 / 3Q10 | 3Q11 / 2Q11 | |||||||||||||||

| Gross provisions | (18,628 | ) | 1,040 | (9,974 | ) | 86.8 | % | (1891.2 | )% | |||||||||||

| Charge-offs | (77,466 | ) | (62,577 | ) | (49,568 | ) | 56.3 | % | 23.8 | % | ||||||||||

| Gross provisions and charge-offs | (96,094 | ) | (61,537 | ) | (59,542 | ) | 61.4 | % | 56.2 | % | ||||||||||

| Loan loss recoveries | 5,722 | 4,663 | 8,017 | (28.6 | )% | 22.7 | % | |||||||||||||

Net provisions for loan losses1 | (90,372 | ) | (56,874 | ) | (51,525 | ) | 75.4 | % | 58.9 | % | ||||||||||

Total loans2 | 17,680,355 | 17,422,041 | 15,232,019 | 16.1 | % | 1.5 | % | |||||||||||||

Loan loss allowances1 | 520,565 | 505,887 | 428,833 | 21.4 | % | 2.9 | % | |||||||||||||

Non-performing loans3 (NPLs) | 496,786 | 452,150 | 407,831 | 21.8 | % | 9.9 | % | |||||||||||||

Risk Index4 | 2.94 | % | 2.90 | % | 2.82 | % | ||||||||||||||

| NPL / Total loans | 2.81 | % | 2.60 | % | 2.68 | % | ||||||||||||||

Coverage ratio of NPLs5 | 104.8 | % | 111.9 | % | 105.1 | % | ||||||||||||||

| 1. | The Bank reclassified Ch$ 31,162 million in provision reversals for off balance sheet lines of credit recognized in 3Q10 as Other operating income to Provisions for loan losses as required by the SBIF. |

| 2. | Excludes interbank loans. |

| 3. | NPLs: Non-performing loans; full balance of loans with one installment 90 days or more overdue. |

| 4. | Risk Index: Loan loss allowances / Total loans; measures the percentage of loans the banks must provision for given their internal models and the Superintendency of Banks guidelines. |

| 5. | Loan loss allowances / NPLs. |

Provision for loan losses in the quarter increased 58.9% QoQ and 75.4% YoY. On a year-to date basis net provision expense has increased 7.6% compared to a 16.1% rise in loan growth. The QoQ increase was mainly due to:

| i. | Strengthening of the residential mortgage provisioning model. As announced in our 2Q11 earnings report, the Bank improved its provisioning model for residential mortgage lending. This change was done in line with our strategic objective of accompanying our loan growth in retail lending with a proactive stance regarding credit risk. This signified a one-time provision expense of approximately Ch$10,000 million in 3Q11. The Bank migrated to a model with more parameters to determine the risk level of a client with a mortgage loan. Previously, the main factor for determining the reserve level was non-performance. For more details on the new model, see Annex 1. |

| ii. | Higher provisions in the middle-market. In 3Q11, the bank set aside Ch$4,000 million in provisions for two deteriorated loan positions in the middle market. We do not expect further provisions for these cases in the future. |

| iii. | Provisions related to La Polar. The Bank set aside a further Ch$600 million in provisions for this loan position in 3Q11. |

| iv. | Translation loss of provisions in US$. In the quarter, the Chilean peso depreciated 9%. As some large commercial loan positions are denominated in US$ and, since the Bank must set aside minimum provisions for all large loans analyzed on an individual basis, this resulted in Ch$4,600 million in higher provision directly related to the depreciation of the exchange rate. |

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

11

Excluding these one-time items, the adjusted provision expenses increased 38.1% QoQ and 25.1% YoY in 3Q11. This rise was mainly due to one-time provisions expenses, the expansion of our lending volumes, especially consumer lending and more prudent credit risk policies implemented in light of a possible deterioration of the macro environment. This included restricting renegotiations and, therefore, increasing charge-offs. This also resulted in a temporary rise in NPLs, but did not affect the Bank’s risk index. The Risk Index, which measures the percentage of loans the banks must provision for given their internal models and the Superintendency of Banks guidelines, remained stable QoQ at 2.94%. We are required to have 100% coverage at all times of its Risk Index. The NPL ratio as of September 2011 reached 2.81%. The coverage ratio of total NPLs (loan loss allowances over non-performing loans) reached 104.8% as of September 2011.

Risk Index vs NPLs, %

NPLs: Non-performing loans; full balance of loans with one installment 90 days or more overdue.

Risk Index: Loan loss allowances / Total loans; measures the percentage of loans the banks must provision for given their internal models and the Superintendency of Banks guidelines.

NET FEE INCOME

Market conditions and the temporary slowdown in loan originations affected fee income

| Fee Income | Quarter | Change % | ||||||||||||||||||

| (Ch$ million) | 3Q11 | 2Q11 | 3Q10 | 3Q11 / 3Q10 | 3Q11 / 2Q11 | |||||||||||||||

| Collection fees | 14,684 | 16,215 | 15,324 | (4.2 | )% | (9.4 | )% | |||||||||||||

| Credit, debit & ATM card fees | 14,383 | 16,079 | 13,518 | 6.4 | % | (10.5 | )% | |||||||||||||

| Checking accounts & lines of credit | 10,020 | 10,025 | 10,604 | (5.5 | )% | (0.0 | )% | |||||||||||||

| Asset management | 8,796 | 10,179 | 10,063 | (12.6 | )% | (13.6 | )% | |||||||||||||

| Insurance brokerage | 7,955 | 9,574 | 8,683 | (8.4 | )% | (16.9 | )% | |||||||||||||

| Guarantees, pledges and other contingent operations | 6,335 | 5,697 | 5,568 | 13.8 | % | 11.2 | % | |||||||||||||

| Fees from brokerage and custody of securities | 2,469 | 2,592 | 2,399 | 2.9 | % | (4.7 | )% | |||||||||||||

| Other Fees | 1,349 | 1,689 | 277 | 388.8 | % | 43,344.9 | % | |||||||||||||

| Total fees | 65,991 | 72,050 | 66,436 | (0.7 | )% | (8.4 | )% | |||||||||||||

Net fee income was down 8.4% QoQ and 0.7% YoY in 3Q11. The main reason for this decline was the temporary slowdown in loan origination, which had a negative impact on loan related insurance premiums. At the same time, the weaker markets negatively affected our mutual fund fees and fees from securities brokerage. Credit card fees were down due to a seasonal rise in credit card expenses paid to the credit card processor. Gross fees from credit cards were up 3.0% QoQ in line with the growth of this product.

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

12

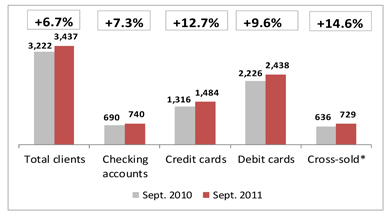

The Bank’s client base, especially cross-sold clients continues to grow at a solid pace. The amount of cross-sold clients is growing at double the pace of our total client base. Credit cards continue to be the fastest growing product, the number of which has increased 12.7% YoY.

Evolution of client base

NET RESULTS FROM FINANCIAL TRANSACTIONS

Positive results from client treasury services

| Results from Financial Transactions* | Quarter | Change % | ||||||||||||||||||

| (Ch$ million) | 3Q11 | 2Q11 | 3Q10 | 3Q11 / 3Q10 | 3Q11 / 2Q11 | |||||||||||||||

| Net income from financial operations | 102,133 | 2,027 | (45,068 | ) | — | % | 4,938.6 | % | ||||||||||||

| Foreign exchange profit (loss), net | (79,132 | ) | 27,049 | 66,781 | — | % | — | % | ||||||||||||

| Net results from financial transactions | 23,001 | 29,076 | 21,713 | 5.9 | % | (20.9 | )% | |||||||||||||

| * | These results mainly include the mark-to-market of the Available for sale investment portfolio, realized and unrealized gains of Financial investments held for trading, the interest revenue generated by the Held for trading portfolio, gains or losses from the sale of charged-off loans and the mark-to-market of derivatives. The results recorded as Foreign exchange profits (loss), net mainly includes the translation gains or losses of assets and a liability denominated in foreign currency. |

Net results from financial transactions, which include the sum of the net income from financial operations and net foreign exchange profits, totaled a gain of Ch$23,001 million in 3Q11, a decrease of 20.9% QoQ and an increase of 5.9% YoY. In order to comprehend more clearly these line items, we present them by business area in the table below.

| Results from Financial Transactions | Quarter | Change % | ||||||||||||||||||

| (Ch$ million) | 3Q11 | 2Q11 | 3Q10 | 3Q11 / 3Q10 | 3Q11 / 2Q11 | |||||||||||||||

Santander Global Connect1 | 16,259 | 15,045 | 11,628 | 39.8 | % | 8.1 | % | |||||||||||||

| Market-making | 4,958 | 6,012 | 8,451 | (41.3 | )% | (17.5 | )% | |||||||||||||

| Client treasury services | 21,217 | 21,058 | 20,079 | 5.7 | % | 0.8 | % | |||||||||||||

| Non-client treasury services | 1,784 | 8,018 | 1,635 | 9.2 | % | (77.7 | )% | |||||||||||||

| Net results from financial transactions | 23,001 | 29,076 | 21,713 | 5.9 | % | (20.9 | )% | |||||||||||||

| 1. | Santander Global Connect is the Bank’s commercial platform for selling treasury products to our clients. |

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

13

The quarterly results were mainly driven by Client treasury services, which totaled Ch$21,217 million in 3Q11 – more than 90% of this line item – that increased 0.8% QoQ and 5.7% YoY. The higher market volatility, especially in the foreign exchange market led to a greater number of clients to hedge exposures resulting in a high gain from Santander Global Connect.

Non-client treasury services fell in the quarter as the Bank maintained high levels of liquidity and avoided taking any major prop-trading positions or gaps, lowering trading results.

OPERATING EXPENSES AND EFFICIENCY

Operating expenses flat QoQ

| Operating Expenses | Quarter | Change % | ||||||||||||||||||

| (Ch$ million) | 3Q11 | 2Q11 | 3Q10 | 3Q11 / 3Q10 | 3Q11 / 2Q11 | |||||||||||||||

| Personnel salaries and expenses | (73,884 | ) | (70,655 | ) | (63,330 | ) | 16.7 | % | 4.6 | % | ||||||||||

| Administrative expenses | (41,041 | ) | (41,535 | ) | (37,983 | ) | 8.1 | % | (1.2 | )% | ||||||||||

| Depreciation and amortization | (13,354 | ) | (12,944 | ) | (11,294 | ) | 18.2 | % | 3.2 | % | ||||||||||

| Impairment | (77 | ) | (27 | ) | (963 | ) | (92.0 | )% | 185.2 | % | ||||||||||

| Operating expenses | (128,356 | ) | (125,161 | ) | (113,570 | ) | 13.0 | % | 2.6 | % | ||||||||||

Efficiency ratio1 | 41.3 | % | 36.5 | % | 37.2 | % | ||||||||||||||

| 1. | Operating expenses / Operating income. Operating income = Net interest income + Net fee income+ Net results from Financial transactions + Other operating income and expenses. |

Operating expenses in 3Q11 increased 2.6% QoQ and 13.0% YoY. The efficiency ratio reached 41.3% in 3Q11. The 4.6% QoQ increase in personnel expenses was mainly due to the increase in headcount and a rise in severance payments. Headcount increased 5.9% YoY and 1.6% QoQ. Of the 190 persons hired in 3Q11, 160 were collection agents. As of June 30, 2011 headcount totaled 11,706 employees.

Administrative expenses fell 1.2% QoQ as the Bank commenced to implement a stricter stance regarding costs. At the same time, the Bank continues with its projects of in investing in technology and alternative distribution channels to enhance productivity in future periods. The Bank is currently investment in a new Client Relationship Management system and other IT projects. These projects should drive stronger revenue growth while increasing productivity. The Bank also opened 7 branches in the quarter, 4 of which were Banca Prime branches for upper income individuals.

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

14

OTHER INCOME AND EXPENSES

| Quarter | Change % | |||||||||||||||||||

| (Ch$ million) | 3Q11 | 2Q11 | 3Q10 | 3Q11 / 3Q10 | 3Q11 / 2Q11 | |||||||||||||||

| Other operating income | 2,194 | 3,309 | 2,656 | (17.4 | )% | (33.7 | )% | |||||||||||||

| Other operating expenses | (12,156 | ) | (8,800 | ) | (21,333 | ) | (43.0 | )% | 38.1 | % | ||||||||||

| Other operating income, net | (9,962 | ) | (5,491 | ) | (18,677 | ) | (46.7 | )% | 81.4 | % | ||||||||||

| Income from investments in other companies | 546 | 552 | 832 | (34.4 | )% | (1.1 | )% | |||||||||||||

| Income tax expense | (16,629 | ) | (19,416 | ) | (14,109 | ) | 17.9 | % | (14.4 | )% | ||||||||||

| Income tax rate | 17.9 | % | 12.0 | % | 10.0 | % | ||||||||||||||

Other operating income, net, totaled Ch$-9,962 million in 3Q11. The lower loss compared to 3Q10 was mainly due to lower charge-off of repossessed assets. Compared to 2Q11 the higher loss from other operating income, net was mainly due to an increase in charge-off of fixed assets mainly related to vandalized ATMs.

The 14.4% QoQ decrease in income tax expense was mainly due to lower net income before taxes. In addition, in 2Q11, the Bank recognized a one-time tax benefit from real estate taxes (contribuciones) paid over assets it has leased to clients. Compared to 3Q10, the rise in the effective tax rate was due the rise of the statutory tax rate to 20% from 17% last year. In 3Q10, the Bank’s effective income tax rate also benefitted from the application of the new corporate tax rates over deferred taxes, which resulted in a higher net asset position in differed taxes and therefore a lower effective tax rate in said quarter.

In 2012, the statutory corporate tax rate should decline to 18.5% and 17% in 2013.

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

15

SECTION 4: CREDIT RISK RATINGS

International ratings

The Bank has credit ratings from three leading international agencies. In the quarter, Fitch lowered the Bank ratings from AA- to A+. Standard and Poor’s modified its outlook to negative and there was no change regarding our ratings from Moody’s. These rating changes were driven by a reduction in ratings of our controlling shareholder.

| Moody’s (Outlook stable) | Rating | |

| Foreign currency bank deposits | Aa3 | |

| Senior bonds | Aa3 | |

| Subordinated debt | A1 | |

| Bank Deposits in Local Currency | Aa3 | |

| Bank financial strength | B- | |

| Short-term deposits | P-1 |

| Standard and Poor’s (Outlook negative) | Rating | |

| Long-term Foreign Issuer Credit | A+ | |

| Long-term Local Issuer Credit | A+ | |

| Short-term Foreign Issuer Credit | A-1 | |

| Short-term Local Issuer Credit | A-1 |

| Fitch (Outlook negative) | Rating | |

| Foreign Currency Long-term Debt | A+ | |

| Local Currency Long-term Debt | A+ | |

| Foreign Currency Short-term Debt | F1 | |

| Local Currency Short-term Debt | F1 | |

| Viability rating | a+ | |

| Individual rating | B |

Local ratings:

Our local ratings, the highest in Chile, are the following:

| Local ratings | Fitch Ratings | Feller Rate | ||

| Shares | Level 2 | 1CN1 | ||

| Short-term deposits | N1+ | Level 1+ | ||

| Long-term deposits | AAA | AAA | ||

| Mortgage finance bonds | AAA | AAA | ||

| Senior bonds | AAA | AAA | ||

| Subordinated bonds | AA | AA+ | ||

| Outlook | Stable | Stable |

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

16

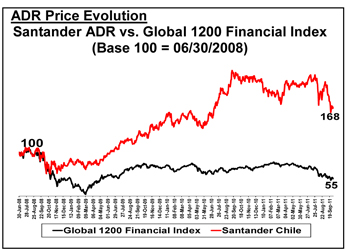

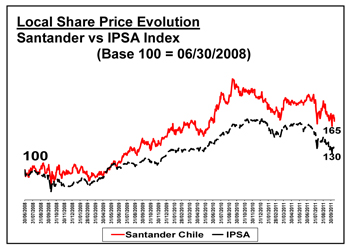

SECTION 5: SHARE PERFORMANCE

As of September 2011

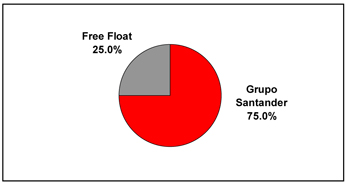

Ownership Structure:

ADR price (US$) 9M11 | ||

| 09/30/11: | 73.48 | |

| Maximum (1H11): | 96.44 | |

| Minimum (1H11): | 70.64 |

Market Capitalization: | US$13,329 million | |

| P/E 12 month trailing*: | 16.5 | |

| P/BV (06/30/11)**: | 3.66 | |

| Dividend yield***: | 3.7% |

| * | Price as of Sept. 30, 2011 / 12mth. earnings |

| ** | Price as of Sept. 30, 2011 / Book value as of 09/30/11 |

| *** | Based on closing price on record date of last dividend payment. |

| Local share price (Ch$) 9M11 | ||

| 09/30/11: | 37.46 | |

| Maximum (9M11): | 43.64 | |

| Minimum (9M11): | 35.63 | |

Dividends:

| Year paid | Ch$/share | % of previous year earnings | ||||||

| 2007: | 0.99 | 65 | % | |||||

| 2008: | 1.06 | 65 | % | |||||

| 2009: | 1.13 | 65 | % | |||||

| 2010: | 1.37 | 60 | % | |||||

| 2011: | 1.52 | 60 | % | |||||

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

17

ANNEX 1: NEW PROVISIONING MODEL FOR RESIDENTIAL MORTGAGE LOANS

Prior to June 2011, residential mortgage loans were assigned an allowance level based on credit risk profiles which were determined utilizing a statistical model that considered a borrower’s credit history, including any defaults on obligations to other creditors, as well as the overdue periods on the loans borrowed from us. Once the rating of the client was determined, the allowance for a mortgage loan was calculated using a risk category, which was directly related to days overdue. The following table sets forth the allowance to loan ratios previously used by the Bank. The ratios represent the percentage of required allowance amount to the aggregate amount of the principal and accrued but unpaid interest on the loan.

Previous model Residential mortgage loans | Overdue days | ||||||||||||||||||||||||||||

1-30 | 31-60 | 61-120 | 121-180 | 181-360 | 361- 720 | >720 | |||||||||||||||||||||||

| Mortgage | Profile 1 | 0.3 | % | 0.5 | % | 1.2 | % | 2.4 | % | 6.8 | % | 14.1 | % | 28.3 | % | ||||||||||||||

| Profile 2 | 1.5 | % | 1.6 | % | 2.5 | % | 4.4 | % | 6.8 | % | 14.1 | % | 28.3 | % | |||||||||||||||

As of June 2011, residential mortgage loans are assigned an allowance level based on credit risk profiles, which were determined utilizing a statistical model that considers: (i) a borrower’s credit history, (ii) if a client is a new client or an existing client, (iii) if the client is a Bank client or a Banefe client and (iv) if this client has been renegotiated in the system.

As of June 2011, the model for determining provisions for residential mortgage loans is as follows. The ratios represent the percentage of required allowance amount to the aggregate amount of the principal and accrued but unpaid interest on the loan.

New model Residential mortgage loans | Performing | Overdue days | |||||||||||||||||||

1-29 | 30-59 | 60-89 | >90 days | ||||||||||||||||||

| Mortgage (Bank client) | New client | 0.20 | % | 2.7 | % | 3.6 | % | 4.63 | % | 11.0 | % | ||||||||||

| Existing client | 0.29 | % | 1.49 | % | 2.97 | % | 3.7 | % | 11.0 | % | |||||||||||

| Renegotiated client | 1.75 | % | 1.75 | % | 1.75 | % | 1.75 | % | 11.0 | % | |||||||||||

| Mortgage (Banefe client) | New or existing client | 0.35 | % | 2.19 | % | 3.64 | % | 4.72 | % | 11.0 | % | ||||||||||

| Renegotiated client | 1.75 | % | 1.75 | % | 1.75 | % | 1.75 | % | 11.0 | % | |||||||||||

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

18

ANNEX 2: BALANCE SHEET

| Sep-11 | Sep-11 | Dec-10 | Sept. 11 / Dec. 10 | |||||||||||||

| US$ths | Ch$ million | % Chg. | ||||||||||||||

| Assets | ||||||||||||||||

| Cash and balances from Central Bank | 3,488,473 | 1,812,785 | 1,762,198 | 2.9 | % | |||||||||||

| Funds to be cleared | 1,571,444 | 816,601 | 374,368 | 118.1 | % | |||||||||||

| Financial assets held for trading | 969,524 | 503,813 | 379,670 | 32.7 | % | |||||||||||

| Investment collateral under agreements to repurchase | 23,395 | 12,157 | 170,985 | (92.9 | )% | |||||||||||

| Derivatives | 3,871,038 | 2,011,585 | 1,624,378 | 23.8 | % | |||||||||||

| Interbank loans | 169,141 | 87,894 | 69,672 | 26.2 | % | |||||||||||

| Loans, net of loan loss allowances | 33,021,822 | 17,159,790 | 15,175,975 | 13.1 | % | |||||||||||

| Available-for-sale financial assets | 4,050,118 | 2,104,644 | 1,473,980 | 42.8 | % | |||||||||||

| Held-to-maturity investments | 0 | 0 | 0 | — | % | |||||||||||

| Investments in other companies | 15,841 | 8,232 | 7,275 | 13.2 | % | |||||||||||

| Intangible assets | 148,617 | 77,229 | 77,990 | (1.0 | )% | |||||||||||

| Fixed assets | 294,652 | 153,116 | 154,985 | (1.2 | )% | |||||||||||

| Current tax assets | 53,394 | 27,746 | 12,499 | 122.0 | % | |||||||||||

| Deferred tax assets | 276,028 | 143,438 | 117,964 | 21.6 | % | |||||||||||

| Other assets | 1,354,999 | 704,125 | 640,937 | 9.9 | % | |||||||||||

| Total Assets | 49,308,486 | 25,623,155 | 22,042,876 | 16.2 | % | |||||||||||

| Liabilities and Equity | ||||||||||||||||

| Demand deposits | 8,653,434 | 4,496,757 | 4,236,434 | 6.1 | % | |||||||||||

| Funds to be cleared | 896,879 | 466,063 | 300,125 | 55.3 | % | |||||||||||

| Investments sold under agreements to repurchase | 436,915 | 227,043 | 294,725 | (23.0 | )% | |||||||||||

| Time deposits and savings accounts | 18,079,950 | 9,395,246 | 7,258,757 | 29.4 | % | |||||||||||

| Derivatives | 3,127,632 | 1,625,274 | 1,643,979 | (1.1 | )% | |||||||||||

| Deposits from credit institutions | 3,896,961 | 2,025,056 | 1,584,057 | 27.8 | % | |||||||||||

| Marketable debt securities | 8,684,511 | 4,512,906 | 4,190,888 | 7.7 | % | |||||||||||

| Other obligations | 321,357 | 166,993 | 166,289 | 0.4 | % | |||||||||||

| Current tax liabilities | 4,426 | 2,300 | 1,293 | 77.9 | % | |||||||||||

| Deferred tax liability | 22,284 | 11,580 | 5,441 | 112.8 | % | |||||||||||

| Provisions | 329,299 | 171,120 | 235,953 | (27.5 | )% | |||||||||||

| Other liabilities | 1,083,472 | 563,026 | 261,328 | 115.4 | % | |||||||||||

| Total Liabilities | 45,537,119 | 23,663,364 | 20,179,269 | 17.3 | % | |||||||||||

| Equity | ||||||||||||||||

| Capital | 1,715,199 | 891,303 | 891,303 | 0.0 | % | |||||||||||

| Reserves | 99,178 | 51,538 | 51,539 | (0.0 | )% | |||||||||||

| Unrealized gain (loss) Available-for-sale financial assets | 1,143 | 594 | (5,180 | ) | — | % | ||||||||||

| Retained Earnings: | 1,893,703 | 984,063 | 894,136 | 10.1 | % | |||||||||||

| Retained earnings previous periods | 1,445,182 | 750,989 | 560,128 | 34.1 | % | |||||||||||

| Net income | 640,745 | 332,963 | 477,155 | (30.2 | )% | |||||||||||

| Provision for mandatory dividend | (192,224 | ) | (99,889 | ) | (143,147 | ) | (30.2 | )% | ||||||||

| Total Shareholders' Equity | 3,709,224 | 1,927,498 | 1,831,798 | 5.2 | % | |||||||||||

| Minority Interest | 62,144 | 32,293 | 31,809 | 1.5 | % | |||||||||||

| Total Equity | 3,771,367 | 1,959,791 | 1,863,607 | 5.2 | % | |||||||||||

| Total Liabilities and Equity | 49,308,486 | 25,623,155 | 22,042,876 | 16.2 | % | |||||||||||

Figures in US$ have been translated at the exchange rate of Ch$519.65

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

19

ANNEX 3: YEAR-TO-DATE INCOME STATEMENTS

| YTD Income Statement Unaudited | Sep-11 | Sep-11 | Sep-10 | Sept. 11 / Sept. 10 | ||||||||||||

| US$ths. | Ch$ million | % Chg. | ||||||||||||||

| Interest income | 2,446,412 | 1,271,278 | 1,045,602 | 21.6 | % | |||||||||||

| Interest expense | (1,083,660 | ) | (563,124 | ) | (337,748 | ) | 66.7 | % | ||||||||

| Net interest income | 1,362,752 | 708,154 | 707,854 | 0.0 | % | |||||||||||

| Fee and commission income | 522,546 | 271,541 | 247,346 | 9.8 | % | |||||||||||

| Fee and commission expense | (119,525 | ) | (62,111 | ) | (53,401 | ) | 16.3 | % | ||||||||

| Net fee and commission income | 403,021 | 209,430 | 193,945 | 8.0 | % | |||||||||||

| Net income from financial operations | 295,458 | 153,535 | 51,946 | 195.6 | % | |||||||||||

| Foreign exchange profit (loss), net | (144,838 | ) | (75,265 | ) | 24,381 | — | % | |||||||||

| Total financial transactions, net | 150,621 | 78,270 | 76,327 | 2.5 | % | |||||||||||

| Other operating income | 15,497 | 8,053 | 27,554 | (70.8 | )% | |||||||||||

| Net operating profit before loan losses | 1,931,891 | 1,003,907 | 1,005,680 | (0.2 | )% | |||||||||||

| Provision for loan losses | (377,023 | ) | (195,920 | ) | (182,120 | ) | 7.6 | % | ||||||||

| Net operating profit | 1,554,868 | 807,987 | 823,560 | (1.9 | )% | |||||||||||

| Personnel salaries and expenses | (399,076 | ) | (207,380 | ) | (184,921 | ) | 12.1 | % | ||||||||

| Administrative expenses | (234,924 | ) | (122,078 | ) | (109,743 | ) | 11.2 | % | ||||||||

| Depreciation and amortization | (76,278 | ) | (39,638 | ) | (36,227 | ) | 9.4 | % | ||||||||

| Impairment | (210 | ) | (109 | ) | (4,665 | ) | (97.7 | )% | ||||||||

| Operating expenses | (710,488 | ) | (369,205 | ) | (335,556 | ) | 10.0 | % | ||||||||

| Other operating expenses | (79,994 | ) | (41,569 | ) | (45,963 | ) | (9.6 | )% | ||||||||

| Total operating expenses | (790,482 | ) | (410,774 | ) | (381,519 | ) | 7.7 | % | ||||||||

| Operating income | 764,386 | 397,213 | 442,041 | (10.1 | )% | |||||||||||

| Income from investments in other companies | 3,219 | 1,673 | 1,175 | 42.4 | % | |||||||||||

| Income before taxes | 767,605 | 398,886 | 443,216 | (10.0 | )% | |||||||||||

| Income tax expense | (120,362 | ) | (62,546 | ) | (60,032 | ) | 4.2 | % | ||||||||

| Net income from ordinary activities | 647,243 | 336,340 | 383,184 | (12.2 | )% | |||||||||||

| Net income discontinued operations | 0 | 0 | 0 | — | % | |||||||||||

| Net income attributable to: | ||||||||||||||||

| Minority interest | 6,499 | 3,377 | (99 | ) | — | % | ||||||||||

| Net income attributable to shareholders | 640,745 | 332,963 | 383,283 | (13.1 | )% | |||||||||||

Figures in US$ have been translated at the exchange rate of Ch$519.65

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

20

ANNEX 4: QUARTERLY INCOME STATEMENTS

| Unaudited Quarterly Income Statement | 3Q11 | 3Q11 | 2Q11 | 3Q10 | 3Q11 / 3Q10 | 3Q11 / 2Q11 | ||||||||||||||||||

| US$ths. | Ch$mn | % Chg. | ||||||||||||||||||||||

| Interest income | 809,639 | 420,729 | 472,132 | 355,445 | 18.4 | % | (10.9 | )% | ||||||||||||||||

| Interest expense | (363,075 | ) | (188,672 | ) | (224,718 | ) | (119,771 | ) | 57.5 | % | (16.0 | )% | ||||||||||||

| Net interest income | 446,564 | 232,057 | 247,414 | 235,674 | (1.5 | )% | (6.2 | )% | ||||||||||||||||

| Fee and commission income | 168,673 | 87,651 | 92,652 | 85,379 | 2.7 | % | (5.4 | )% | ||||||||||||||||

| Fee and commission expense | (41,682 | ) | (21,660 | ) | (20,602 | ) | (18,943 | ) | 14.3 | % | 5.1 | % | ||||||||||||

| Net fee and commission income | 126,991 | 65,991 | 72,050 | 66,436 | (0.7 | )% | (8.4 | )% | ||||||||||||||||

| Net income from financial operations | 196,542 | 102,133 | 2,027 | (45,068 | ) | — | % | 4938.6 | % | |||||||||||||||

| Foreign exchange profit (loss), net | (152,279 | ) | (79,132 | ) | 27,049 | 66,781 | — | % | — | % | ||||||||||||||

| Total financial transactions, net | 44,262 | 23,001 | 29,076 | 21,713 | 5.9 | % | (20.9 | )% | ||||||||||||||||

| Other operating income | 4,222 | 2,194 | 3,309 | 2,656 | (17.4 | )% | (33.7 | )% | ||||||||||||||||

| Net operating profit before loan losses | 622,040 | 323,243 | 351,849 | 326,479 | (1.0 | )% | (8.1 | )% | ||||||||||||||||

| Provision for loan losses | (173,909 | ) | (90,372 | ) | (56,874 | ) | (51,525 | ) | 75.4 | % | 58.9 | % | ||||||||||||

| Net operating profit | 448,130 | 232,871 | 294,975 | 274,954 | (15.3 | )% | (21.1 | )% | ||||||||||||||||

| Personnel salaries and expenses | (142,180 | ) | (73,884 | ) | (70,655 | ) | (63,330 | ) | 16.7 | % | 4.6 | % | ||||||||||||

| Administrative expenses | 132,041 | (41,041 | ) | (41,535 | ) | (37,983 | ) | 8.1 | % | (1.2 | )% | |||||||||||||

| Depreciation and amortization | (25,698 | ) | (13,354 | ) | (12,944 | ) | (11,294 | ) | 18.2 | % | 3.2 | % | ||||||||||||

| Impairment | (148 | ) | (77 | ) | (27 | ) | (963 | ) | (92.0 | )% | 185.2 | % | ||||||||||||

| Operating expenses | (247,005 | ) | (128,356 | ) | (125,161 | ) | (113,570 | ) | 13.0 | % | 2.6 | % | ||||||||||||

| Other operating expenses | (23,393 | ) | (12,156 | ) | (8,800 | ) | (21,333 | ) | (43.0 | )% | 38.1 | % | ||||||||||||

| Total operating expenses | (270,397 | ) | (140,512 | ) | (133,961 | ) | (134,903 | ) | 4.2 | % | 4.9 | % | ||||||||||||

| Operating income | 177,733 | 92,359 | 161,014 | 140,051 | (34.1 | )% | (42.6 | )% | ||||||||||||||||

| Income from investments in other companies | 1,051 | 546 | 552 | 832 | (34.4 | )% | (1.1 | )% | ||||||||||||||||

| Income before taxes | 178,784 | 92,905 | 161,566 | 140,883 | (34.1 | )% | (42.5 | )% | ||||||||||||||||

| Income tax expense | (32,000 | ) | (16,629 | ) | (19,416 | ) | (14,109 | ) | 17.9 | % | (14.4 | )% | ||||||||||||

| Net income from ordinary activities | 146,783 | 76,276 | 142,150 | 126,774 | (39.8 | )% | (46.3 | )% | ||||||||||||||||

| Net income discontinued operations | 0 | 0 | 0 | 0 | ||||||||||||||||||||

| Net income attributable to: | ||||||||||||||||||||||||

| Minority interest | 2,161 | 1,123 | 638 | 1,418 | -20.8 | % | 76.0 | % | ||||||||||||||||

| Net income attributable to shareholders | 144,622 | 75,153 | 141,512 | 125,356 | (40.0 | )% | (46.9 | )% | ||||||||||||||||

Figures in US$ have been translated at the exchange rate of Ch$519.65

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

21

ANNEX 5: QUARTERLY EVOLUTION OF MAIN RATIOS AND OTHER INFORMATION

| Mar-10 | Jun-10 | Sep-10 | Dec-10 | Mar-11 | Jun-11 | Sep-11 | ||||||||||||||||||||||

| (Ch$ millions) | ||||||||||||||||||||||||||||

| Loans | ||||||||||||||||||||||||||||

| Consumer loans | 2,303,983 | 2,404,128 | 2,554,884 | 2,700,791 | 2,815,118 | 2,893,038 | 2,925,659 | |||||||||||||||||||||

| Residential mortgage loans | 4,219,733 | 4,360,496 | 4,498,799 | 4,651,136 | 4,758,712 | 4,909,630 | 5,016,419 | |||||||||||||||||||||

| Commercial loans | 7,519,854 | 7,817,843 | 8,178,336 | 8,305,630 | 9,200,538 | 9,619,373 | 9,738,278 | |||||||||||||||||||||

| Total loans | 14,043,570 | 14,582,467 | 15,232,019 | 15,657,557 | 16,774,368 | 17,422,041 | 17,680,356 | |||||||||||||||||||||

| Allowance for loan losses | (375,366 | ) | (387,625 | ) | (428,833 | ) | (481,582 | ) | (489,034 | ) | (505,887 | ) | (520,565 | ) | ||||||||||||||

| Total loans, net of allowances | 13,668,204 | 14,194,842 | 14,803,186 | 15,175,975 | 16,285,334 | 16,916,154 | 17,159,791 | |||||||||||||||||||||

| Loans by segment | ||||||||||||||||||||||||||||

| Individuals | 7,411,686 | 7,715,031 | 8,035,617 | 8,407,416 | 8,652,205 | 9,026,697 | 9,215,686 | |||||||||||||||||||||

| SMEs | 2,143,885 | 2,210,170 | 2,301,536 | 2,375,192 | 2,467,951 | 2,455,349 | 2,524,836 | |||||||||||||||||||||

| Total retail lending | 9,555,571 | 9,925,201 | 10,337,153 | 10,782,608 | 11,120,156 | 11,482,046 | 11,740,522 | |||||||||||||||||||||

| Institutional lending | 313,079 | 330,980 | 340,274 | 331,153 | 352,593 | 372,939 | 351,686 | |||||||||||||||||||||

| Middle-Market & Real estate | 2,907,944 | 2,983,741 | 3,160,681 | 3,288,107 | 3,562,558 | 3,625,439 | 3,731,881 | |||||||||||||||||||||

| Corporate | 1,279,965 | 1,347,855 | 1,406,210 | 1,293,321 | 1,757,732 | 1,950,992 | 1,833,084 | |||||||||||||||||||||

| Customer funds | ||||||||||||||||||||||||||||

| Demand deposits | 3,890,230 | 4,168,884 | 3,991,732 | 4,236,434 | 4,315,563 | 4,450,290 | 4,496,757 | |||||||||||||||||||||

| Time deposits | 6,818,939 | 7,193,376 | 7,155,213 | 7,258,757 | 8,408,818 | 8,856,185 | 9,395,246 | |||||||||||||||||||||

| Total deposits | 10,709,169 | 11,362,260 | 11,146,945 | 11,495,191 | 12,724,381 | 13,306,475 | 13,892,003 | |||||||||||||||||||||

| Mutual funds (Off balance sheet) | 3,635,544 | 3,510,479 | 3,305,683 | 3,188,151 | 3,142,373 | 3,136,413 | 2,852,379 | |||||||||||||||||||||

| Total customer funds | 14,344,713 | 14,872,739 | 14,452,628 | 14,683,342 | 15,866,754 | 16,442,888 | 16,744,382 | |||||||||||||||||||||

| Loans / Deposits1 | 104.3 | % | 99.8 | % | 100.9 | % | 99.8 | % | 96.9 | % | 96.8 | % | 94.8 | % | ||||||||||||||

| Average balances | ||||||||||||||||||||||||||||

| Avg. interest earning assets | 15,776,237 | 15,816,902 | 16,463,951 | 17,176,435 | 17,866,010 | 19,099,828 | 20,068,323 | |||||||||||||||||||||

| Avg. loans | 13,879,173 | 14,291,144 | 14,874,816 | 15,470,132 | 16,150,015 | 17,146,712 | 17,460,992 | |||||||||||||||||||||

| Avg. assets | 20,746,299 | 20,742,244 | 20,915,047 | 21,841,681 | 22,679,590 | 24,435,586 | 24,961,680 | |||||||||||||||||||||

| Avg. demand deposits | 3,678,104 | 4,107,978 | 4,005,565 | 4,056,105 | 4,271,464 | 4,560,188 | 4,372,511 | |||||||||||||||||||||

| Avg equity | 1,665,977 | 1,644,453 | 1,712,967 | 1,801,866 | 1,857,339 | 1,853,926 | 1,901,447 | |||||||||||||||||||||

| Avg. free funds | 5,344,081 | 5,752,431 | 5,718,532 | 5,857,971 | 6,128,803 | 6,414,114 | 6,273,958 | |||||||||||||||||||||

| Capitalization | ||||||||||||||||||||||||||||

| Risk weighted assets | 15,513,732 | 16,210,259 | 16,739,710 | 17,245,265 | 18,013,990 | 18,964,803 | 18,954,146 | |||||||||||||||||||||

| Tier I (Shareholders' equity) | 1,683,103 | 1,665,326 | 1,757,340 | 1,831,799 | 1,905,690 | 1,866,467 | 1,927,498 | |||||||||||||||||||||

| Tier II | 599,353 | 627,608 | 672,740 | 672,099 | 642,221 | 669,798 | 715,184 | |||||||||||||||||||||

| Regulatory capital | 2,282,455 | 2,292,934 | 2,430,080 | 2,503,898 | 2,547,912 | 2,536,265 | 2,642,682 | |||||||||||||||||||||

| Tier I ratio | 10.8 | % | 10.3 | % | 10.5 | % | 10.6 | % | 10.6 | % | 9.8 | % | 10.2 | % | ||||||||||||||

| BIS ratio | 14.7 | % | 14.1 | % | 14.5 | % | 14.5 | % | 14.1 | % | 13.4 | % | 13.9 | % | ||||||||||||||

| Profitability & Efficiency | ||||||||||||||||||||||||||||

| Net interest margin | 5.8 | % | 6.1 | % | 5.7 | % | 5.4 | % | 5.1 | % | 5.2 | % | 4.6 | % | ||||||||||||||

| Efficiency ratio | 32.9 | % | 34.9 | % | 37.2 | % | 35.1 | % | 37.5 | % | 36.5 | % | 41.3 | % | ||||||||||||||

| Avg. Free funds / interest earning assets | 33.9 | % | 36.4 | % | 34.7 | % | 34.1 | % | 34.3 | % | 33.6 | % | 31.3 | % | ||||||||||||||

| Return on avg. equity | 28.6 | % | 33.8 | % | 29.3 | % | 20.8 | % | 25.0 | % | 30.5 | % | 15.8 | % | ||||||||||||||

| Return on avg. assets | 2.3 | % | 2.7 | % | 2.4 | % | 1.7 | % | 2.1 | % | 2.3 | % | 1.2 | % | ||||||||||||||

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

22

2| Mar-10 | Jun-10 | Sep-10 | Dec-10 | Mar-11 | Jun-11 | Sep-11 | ||||||||||||||||||||||

| Asset quality | ||||||||||||||||||||||||||||

| Non-performing loans (NPLs)2 | 385,211 | 415,556 | 407,831 | 416,739 | 413,775 | 452,150 | 496,786 | |||||||||||||||||||||

| Past due loans3 | 197,060 | 200,524 | 207,530 | 206,601 | 216,072 | 214,483 | 223,948 | |||||||||||||||||||||

| Expected loss4 | 375,366 | 387,625 | 428,833 | 481,582 | 489,034 | 505,887 | 520,565 | |||||||||||||||||||||

| NPLs / total loans | 2.74 | % | 2.85 | % | 2.68 | % | 2.66 | % | 2.47 | % | 2.60 | % | 2.81 | % | ||||||||||||||

| PDL / total loans | 1.40 | % | 1.38 | % | 1.36 | % | 1.32 | % | 1.29 | % | 1.23 | % | 1.27 | % | ||||||||||||||

| Coverage of NPLs (Loan loss allowance / NPLs) | 97.44 | % | 93.28 | % | 105.15 | % | 115.56 | % | 118.19 | % | 111.88 | % | 104.79 | % | ||||||||||||||

| Coverage of PDLs (Loan loss allowance / PDLs) | 190.5 | % | 193.3 | % | 206.6 | % | 233.1 | % | 226.3 | % | 235.9 | % | 232.4 | % | ||||||||||||||

| Expected loss (Loan loss allowances / Loans) | 2.67 | % | 2.66 | % | 2.82 | % | 3.08 | % | 2.92 | % | 2.90 | % | 2.94 | % | ||||||||||||||

| Cost of credit (prov. expense / loans) | 2.04 | % | 1.62 | % | 1.35 | % | 2.57 | % | 1.16 | % | 1.31 | % | 2.04 | % | ||||||||||||||

| Network | ||||||||||||||||||||||||||||

| Branches | 498 | 499 | 500 | 504 | 506 | 487 | 494 | |||||||||||||||||||||

| ATMs | 1,856 | 1,871 | 1,914 | 2,018 | 2,017 | 1,946 | 1,892 | |||||||||||||||||||||

| Employees | 11,155 | 11,133 | 11,049 | 11,001 | 11,115 | 11,516 | 11,706 | |||||||||||||||||||||

| Market information (period-end) | ||||||||||||||||||||||||||||

| Net income per share (Ch$) | 0.63 | 0.74 | 0.67 | 0.50 | 0.62 | 0.75 | 0.40 | |||||||||||||||||||||

| Net income per ADR (US$) | 1.25 | 1.41 | 1.42 | 1.11 | 1.33 | 1.66 | 0.80 | |||||||||||||||||||||

| Stock price | 34.4 | 35.7 | 45.1 | 42.3 | 40.1 | 42.2 | 37.5 | |||||||||||||||||||||

| ADR price | 68.2 | 67.1 | 96.6 | 93.4 | 86.8 | 93.8 | 73.5 | |||||||||||||||||||||

| Market capitalization (US$mn) | 12,373 | 12,168 | 17,512 | 16,946 | 15,734 | 17,015 | 13,327 | |||||||||||||||||||||

| Shares outstanding | 188,446.1 | 188,446.1 | 188,446.1 | 188,446.1 | 188,446.1 | 188,446.1 | 188,446.1 | |||||||||||||||||||||

| ADRs (1 ADR = 1,039 shares) | 181.4 | 181.4 | 181.4 | 181.4 | 181.4 | 181.4 | 181.4 | |||||||||||||||||||||

| Other Data | ||||||||||||||||||||||||||||

| Quarterly inflation rate5 | 0.27 | % | 0.97 | % | 0.65 | % | 0.54 | % | 0.57 | % | 1.44 | % | 0.56 | % | ||||||||||||||

| Central Bank monetary policy reference rate (nominal) | 0.50 | % | 1.00 | % | 2.50 | % | 3.25 | % | 4.00 | % | 5.25 | % | 5.25 | % | ||||||||||||||

| Avg. 10 year Central Bank yield (real) | 3.14 | % | 3.04 | % | 2.82 | % | 3.01 | % | 3.09 | % | 2.90 | % | 2.63 | % | ||||||||||||||

| Avg. 10 year Central Bank yield (nominal) | 6.41 | % | 6.42 | % | 6.07 | % | 6.12 | % | 6.67 | % | 6.31 | % | 5.64 | % | ||||||||||||||

| Observed Exchange rate (Ch$/US$) (period-end) | 526.29 | 543.09 | 485.23 | 468.37 | 482.08 | 471.13 | 515.14 | |||||||||||||||||||||

1 Ratio = Loans - marketable securities / Time deposits + demand deposits

2 Capital + future interest of all loans with one installment 90 days or more overdue.

3 Total installments plus lines of credit more than 90 days overdue

4 Based on internal credit models and SBIF guidelines. Banks must have a 100% coverage of expected loss

5 Calculated using the variation of the Unidad de Fomento (UF) in the period

Investor Relations Department

Bandera 140 19th Floor, Santiago, Chile, Tel: 562-320-8284, fax: 562-671-6554,

email: rmorenoh@santander.cl

23

C0NTENTS

| Consolidated Interim Financial Statements | |

| CONSOLIDATED INTERIM STATEMENTS OF FINANCIAL POSITION | 3 |

| CONSOLIDATED INTERIM STATEMENTS OF INCOME | 4 |

| CONSOLIDATED INTERIM STATEMENTS OF COMPREHENSIVE INCOME | 5 |

| CONSOLIDATED INTERIM STATEMENTS OF CHANGES IN EQUITY | 6 |

| CONSOLIDATED INTERIM STATEMENTS OF CASH FLOW | 7 |

| Notes to the Financial Statements | |

| NOTE 01 -SUMMARY OF SIGNIFICANT ACCOUNTING PRINCIPLES | 9 |

| NOTE 02 - ACCOUNTING CHANGES | 34 |

| NOTE 03 - SIGNIFICANT EVENTS | 37 |

| NOTE 04 - BUSINESS SEGMENTS | 39 |

| NOTE 05 - CASH AND CASH EQUIVALENTS | 45 |

| NOTE 06 - TRADING INVESTMENTS | 46 |

| NOTE 07 - DERIVATIVE FINANCIAL INSTRUMENTS AND HEDGE ACCOUNTING | 47 |

| NOTE 08 - INTERBANK LOANS | 53 |

| NOTE 09 - LOANS AND ACCOUNTS RECEIVABLE FROM CUSTOMERS | 54 |

| NOTE 10 - AVAILABLE FOR SALE INVESTMENTS | 59 |

| NOTE 11 - INTANGIBLE ASSETS | 60 |

| NOTE 12 - PROPERTY, PLANT, AND EQUIPMENT | 62 |

| NOTE 13 - CURRENT AND DEFERRED TAXES | 66 |

| NOTE 14 - OTHER ASSETS | 69 |

| NOTE 15 - TIME DEPOSITS AND OTHER TIME LIABILITIES | 70 |

| NOTE 16 - ISSUED DEBT INSTRUMENTS AND OTHER OBLIGATIONS | 71 |

| NOTE 17 - MATURITIES OF ASSETS AND LIABILITIES | 76 |

| NOTE 18 - OTHER LIABILITIES | 78 |

| NOTE 19 - CONTINGENCIES AND COMMITMENTS | 79 |

| NOTE 20 - EQUITY | 81 |

| NOTE 21 - CAPITAL REQUIREMENTS (BASEL) | 84 |

| NOTE 22 - NON CONTROLLING INTEREST | 86 |

| NOTE 23 - INTEREST INCOME AND EXPENSE | 89 |

| NOTE 24 - FEES AND COMMISSIONS | 92 |

| NOTE 25 - NET INCOME FROM FINANCIAL OPERATIONS | 93 |

| NOTE 26 - NET FOREIGN EXCHANGE PROFIT (LOSS) | 94 |

| NOTE 27 - PROVISION FOR LOAN LOSSES | 95 |

| NOTE 28 - PERSONNEL SALARIES AND EXPENSES | 97 |

| NOTE 29 - ADMINISTRATIVE EXPENSES | 98 |

| NOTE 30 - DEPRECIATION AMORTIZATION AND IMPAIRMENT | 99 |

| NOTE 31 - OTHER OPERATING INCOME AND EXPENSES | 100 |

| NOTE 32 - TRANSACTIONS WITH RELATED PARTIES | 102 |

| NOTE 33 - FAIR VALUE OF FINANCIAL ASSETS AND LIABILITIES | 107 |

| NOTE 34 - SUBSEQUENT EVENTS | 110 |

2

BANCO SANTANDER CHILE AND SUBSIDIARIES

CONSOLIDATED INTERIM STATEMENTS OF FINANCIAL POSITION

For periods ending as of

| September 30, | September 30, | December 31, | ||||||||||||||

| 2011 | 2011 | 2010 | ||||||||||||||

| NOTE | ThUS$ | MCh$ | MCh$ | |||||||||||||

| ASSETS | ||||||||||||||||

| Cash and deposits in banks | 5 | 3,488,473 | 1,812,785 | 1,762,198 | ||||||||||||

| Unsettled transactions | 5 | 1,571,444 | 816,601 | 374,368 | ||||||||||||

| Trading investments | 6 | 969,524 | 503,813 | 379,670 | ||||||||||||

| Investments under resale agreements | - | 23,395 | 12,157 | 170,985 | ||||||||||||

| Financial derivative contracts | 7 | 3,871,038 | 2,011,585 | 1,624,378 | ||||||||||||

| Interbank loans, net | 8 | 169,141 | 87,894 | 69,672 | ||||||||||||

| Loans and accounts receivable from customers, net nnrnetnet | 9 | 33,021,822 | 17,159,790 | 15,175,975 | ||||||||||||

| Available for sale investments | 10 | 4,050,118 | 2,104,644 | 1,473,980 | ||||||||||||

| Held to maturity investments | - | - | - | - | ||||||||||||

| Investments in other companies | - | 15,841 | 8,232 | 7,275 | ||||||||||||

| Intangible assets | 11 | 148,617 | 77,229 | 77,990 | ||||||||||||

| Property, plant, and equipment | 12 | 294,652 | 153,116 | 154,985 | ||||||||||||

| Current taxes | 13 | 53,394 | 27,746 | 12,499 | ||||||||||||

| Deferred tax | 13 | 276,028 | 143,438 | 117,964 | ||||||||||||

| Other assets | 14 | 1,354,999 | 704,125 | 640,937 | ||||||||||||

| TOTAL ASSETS | 49,308,486 | 25,623,155 | 22,042,876 | |||||||||||||

| LIABILITIES | ||||||||||||||||

| Deposits and other demand liabilities | 15 | 8,653,434 | 4,496,757 | 4,236,434 | ||||||||||||

| Unsettled transactions | 5 | 896,879 | 466,063 | 300,125 | ||||||||||||

| Investments under repurchase agreements | - | 436,915 | 227,043 | 294,725 | ||||||||||||

| Time deposits and other time liabilities | 15 | 18,079,950 | 9,395,246 | 7,258,757 | ||||||||||||

| Financial derivative contracts | 7 | 3,127,632 | 1,625,274 | 1,643,979 | ||||||||||||

| Interbank borrowings | - | 3,896,961 | 2,025,056 | 1,584,057 | ||||||||||||

| Issued debt instruments | 16 | 8,684,511 | 4,512,906 | 4,190,888 | ||||||||||||

| Other financial liabilities | 16 | 321,357 | 166,993 | 166,289 | ||||||||||||

| Current taxes | 13 | 4,426 | 2,300 | 1,293 | ||||||||||||

| Deferred tax | 13 | 22,284 | 11,580 | 5,441 | ||||||||||||

| Provisions | - | 329,299 | 171,120 | 235,953 | ||||||||||||

| Other liabilities | 18 | 1,083,472 | 563,026 | 261,328 | ||||||||||||

| TOTAL LIABILITIES | 45,537,119 | 23,663,364 | 20,179,269 | |||||||||||||

| EQUITY | ||||||||||||||||

| Attributable to Bank shareholders: | 3,709,223 | 1,927,498 | 1,831,798 | |||||||||||||

| Capital | - | 1,715,199 | 891,303 | 891,303 | ||||||||||||

| Reserves | - | 99,180 | 51,539 | 51,539 | ||||||||||||

| Valuation adjustments | 20 | 1,141 | 593 | (5,180 | ) | |||||||||||

| Retained earnings | - | 1,893,703 | 984,063 | 894,136 | ||||||||||||

| Retained earnings of prior years | - | 1,445,182 | 750.989 | 560,128 | ||||||||||||

| Income for the period | - | 640,745 | 332.963 | 477,155 | ||||||||||||

| Minus: Provision for mandatory dividends | - | (192,224 | ) | (99.889 | ) | (143,147 | ) | |||||||||

| Non-controlling interest | 22 | 62,144 | 32,293 | 31,809 | ||||||||||||

| TOTAL EQUITY | 3,771,367 | 1,959,791 | 1,863,607 | |||||||||||||

| TOTAL LIABILITIES AND EQUITY | 49,308,486 | 25,623,155 | 22,042,876 | |||||||||||||

3

BANCO SANTANDER CHILE AND SUBSIDIARIES

CONSOLIDATED INTERIM STATEMENTS OF INCOME

As of September 30, | For the quarter ended on September 30, | For the 9-month period ended on September 30 , | ||||||||||||||||||||||

| 2011 | 2011 | 2010 | 2011 | 2010 | ||||||||||||||||||||

| NOTE | ThUS$ | MCh$ | MCh$ | MCh$ | MCh$ | |||||||||||||||||||

| OPERATING INCOME | ||||||||||||||||||||||||

| Interest income | 23 | 2,446,412 | 420,729 | 355,445 | 1,271,278 | 1,045,602 | ||||||||||||||||||

| Interest expense | 23 | (1,083,660 | ) | (188,672 | ) | (119,771 | ) | (563,124 | ) | (337,748 | ) | |||||||||||||

| Net interest income | 1.362.752 | 232,057 | 235,674 | 708,154 | 707,854 | |||||||||||||||||||

| Fee and commission income | 24 | 522,546 | 87,651 | 85,379 | 271,541 | 247,346 | ||||||||||||||||||

| Fee and commission expense | 24 | (119,525 | ) | (21,660 | ) | (18,943 | ) | (62,111 | ) | (53,401 | ) | |||||||||||||

| Net fee and commission income | 403,021 | 65,991 | 66,436 | 209,430 | 193,945 | |||||||||||||||||||

| Net income from financial operations (net trading income) | 25 | 295,458 | 102,133 | (45,068 | ) | 153,535 | 51,946 | |||||||||||||||||

| Foreign exchange profit (loss), net | 26 | (144,838 | ) | (79,132 | ) | 66,781 | (75,265 | ) | 24,381 | |||||||||||||||

| Other operating income | 31 | 15,498 | 2,194 | 2,656 | 8,053 | 27,554 | ||||||||||||||||||

| Total operating income | 1,931,891 | 323,243 | 326,479 | 1,003,907 | 1,005,680 | |||||||||||||||||||

| Provisions for loan losses | 27 | (377,023 | ) | (90,372 | ) | (51,525 | ) | (195,920 | ) | (182,120 | ) | |||||||||||||

| NET OPERATING PROFIT | 1,554,868 | 232,871 | 274,954 | 807,987 | 823,560 | |||||||||||||||||||

| Personnel salaries and expenses | 28 | (399,076 | ) | (73,884 | ) | (63,330 | ) | (207,380 | ) | (184,921 | ) | |||||||||||||

| Administrative expenses | 29 | (234,924 | ) | (41,041 | ) | (37,983 | ) | (122,078 | ) | (109,743 | ) | |||||||||||||

| Depreciation and amortization | 30 | (76,278 | ) | (13,354 | ) | (11,294 | ) | (39,638 | ) | (36,227 | ) | |||||||||||||

| Impairment | 12 | (210 | ) | (77 | ) | (963 | ) | (109 | ) | (4,665 | ) | |||||||||||||

| Other operating expenses | 31 | (79,994 | ) | (12,156 | ) | (21,333 | ) | (41,569 | ) | (45,963 | ) | |||||||||||||

| Other operating expenses | (790,482 | ) | (140,512 | ) | (134,903 | ) | (410,774 | ) | (381,519 | ) | ||||||||||||||

| OPERATING INCOME | 764,386 | 92,359 | 140,051 | 397,213 | 442,041 | |||||||||||||||||||

| Income from investments in other companies | - | 3,219 | 546 | 832 | 1,673 | 1,175 | ||||||||||||||||||

| Income before tax | 767,605 | 92,905 | 140,883 | 398,886 | 443,216 | |||||||||||||||||||

| Income tax expense | 13 | (120,362 | ) | (16,629 | ) | (14,109 | ) | (62,546 | ) | (60,032 | ) | |||||||||||||

| NET INCOME FOR THE PERIOD | 647,243 | 76,276 | 126,774 | 336,340 | 383,184 | |||||||||||||||||||

| Attributable to: | ||||||||||||||||||||||||

| Bank shareholders (Equity holders of the Bank) | - | 640,745 | 75,153 | 125,356 | 332,963 | 383,283 | ||||||||||||||||||

| Non-controlling interest | 22 | 6,498 | 1,123 | 1,418 | 3,377 | (99 | ) | |||||||||||||||||

| Earnings per share attributable to Bank shareholders: | ||||||||||||||||||||||||

| (expressed in Chilean pesos) | ||||||||||||||||||||||||

| Basic earnings | - | 3.4004 | 0.399 | 0.665 | 1.767 | 1.5598 | ||||||||||||||||||

| Diluted earnings | - | 3.4004 | 0.399 | 0.665 | 1.767 | 1.5598 | ||||||||||||||||||

4

BANCO SANTANDER CHILE AND SUBSIDIARIES

CONSOLIDATED INTERIM STATEMENTS OF COMPREHENSIVE INCOME

As of September 30, | For the quarter ended on September 30, | For the 9-month period ended on September 30, | ||||||||||||||||||||||

| 2011 | 2011 | 2010 | 2011 | 2010 | ||||||||||||||||||||

| NOTE | ThUS$ | MCh$ | MCh$ | MCh$ | MCh$ | |||||||||||||||||||

| CONSOLIDATED INCOME FOR THE PERIOD | 647,243 | 76,276 | 126,774 | 336,340 | 383,184 | |||||||||||||||||||

| OTHER COMPREHENSIVE INCOME | ||||||||||||||||||||||||

| Available for sale investments | 20 | 41,347 | 22,561 | (2,924 | ) | 21,486 | 4,796 | |||||||||||||||||

| Cash flow hedge | 7 | (27,084 | ) | (12,051 | ) | 7,433 | (14,074 | ) | 10,306 | |||||||||||||||

| Other comprehensive income before income tax | 14,263 | 10,510 | 4,509 | 7,412 | 15,102 | |||||||||||||||||||

| Income tax related to other comprehensive income | 13 | (2,696 | ) | (2,058 | ) | (524 | ) | (1,401 | ) | (2,325 | ) | |||||||||||||

| Total other comprehensive income | 11,567 | 8,452 | 3,985 | 6,011 | 12,777 | |||||||||||||||||||

| CONSOLIDATED COMPREHENSIVE INCOME FOR THE PERIOD | 658,810 | 84,728 | 130,759 | 342,351 | 395,961 | |||||||||||||||||||

| Attributable to: | ||||||||||||||||||||||||

| Bank shareholders (Equity holders of the Bank) | - | 651,853 | 83,577 | 129,621 | 338,736 | 396,159 | ||||||||||||||||||

| Non-controlling interest | 22 | 6,957 | 1,151 | 1,138 | 3,615 | (198 | ) | |||||||||||||||||

5

BANCO SANTANDER CHILE AND SUBSIDIARIES

CONSOLIDATED INTERIM STATEMENTS OF CHANGES IN EQUITY

| RESERVES | VALUATION ADJUSTMENTS | RETAINED EARNINGS | ||||||||||||||||||||||||||||||||||||||||||||||

| Capital | Reserves and other retained earnings | Merger of companies under common control | Available for sale investments | Cash flow hedge | Income tax | Retained earnings of prior years | Income for the period | Provision for mandatory dividends | Total attributable to shareholders | Non- controlling interest | Total Equity | |||||||||||||||||||||||||||||||||||||

| MCh$ | MCh$ | MCh$ | MCh$ | MCh$ | MCh$ | MCh$ | MCh$ | MCh$ | MCh$ | MCh$ | MCh$ | |||||||||||||||||||||||||||||||||||||

| Balances as of December 31, 2009 | 891,303 | 53,763 | (2,224 | ) | (29,132 | ) | (3,162 | ) | 5,490 | 440,401 | 431,253 | (129,376 | ) | 1,658,316 | 29,799 | 1,688,115 | ||||||||||||||||||||||||||||||||

| Distribution of income from previous period | - | - | - | - | - | - | 431,253 | (431,253 | ) | - | - | - | - | |||||||||||||||||||||||||||||||||||

| First Enforcement of Chapter B3 | - | - | - | - | - | - | (52,662 | ) | - | - | (52,662 | ) | - | (52,662 | ) | |||||||||||||||||||||||||||||||||

| Opening balances as of January 1, 2010 | 891,303 | 53,763 | (2,224 | ) | (29,132 | ) | (3,162 | ) | 5,490 | 818,992 | - | (129,376 | ) | 1,605,654 | 29,799 | 1,635,453 | ||||||||||||||||||||||||||||||||

| Increase or decrease of capital and reserves | - | - | - | - | - | - | - | - | - | - | - | - | ||||||||||||||||||||||||||||||||||||